Financial Conditions loosen further: credit markets blow off the Fed to make sure “higher for longer” gets entrenched? That would be funny.

By Wolf Richter for WOLF STREET.

One of the big surprises this year is that the Fed’s 5.5% policy rates and $1.1 trillion in QT have neither meaningfully tightened financial conditions nor slowed the economy.

The Fed has been “tightening” since early 2022 in order to “tighten” the financial conditions, and these tighter financial conditions are then supposed to make it harder and more expensive to borrow which is supposed to slow economic growth and remove the fuel that drives inflation. “Financial conditions,” which are tracked by various indices, got a little less loose, and then they re-loosened all over again. It’s almost funny.

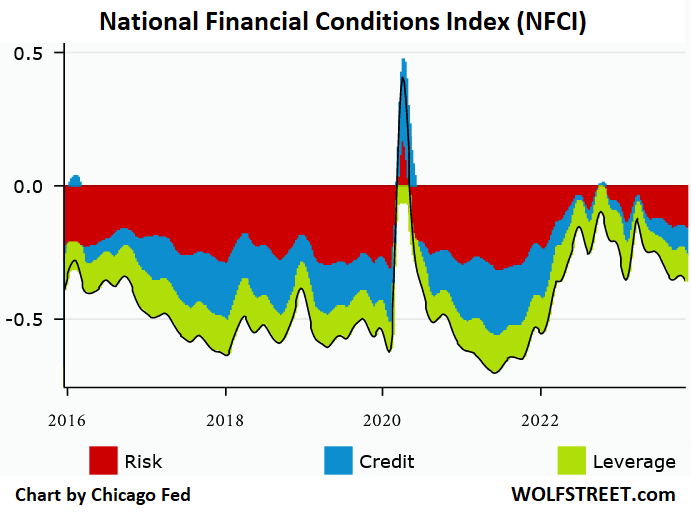

The Chicago Fed’s National Financial Conditions Index (NFCI) loosened further, dipping to -0.36 in the latest reporting week, the loosest since May 2022, when the Fed just started its tightening cycle. The index is constructed to have an average value of zero going back to 1971. Negative values show that financial conditions are looser than average, and they have been loosening since April 2023, after a brief tightening episode during the bank panic (chart via Chicago Fed):

You can see in the chart above how financial conditions tightened in March 2020, but not for long – by May 2020, as the Fed was dousing the land with trillions in QE, they were already loose again.

So, despite the rate hikes and QT by the Fed, financial conditions are as loose as they were when the Fed had just started tightening in May 2022, and they are far looser than the long-term average, though they have become somewhat less loosey-goosey than during the free-money era starting in mid-2020 through early 2022.

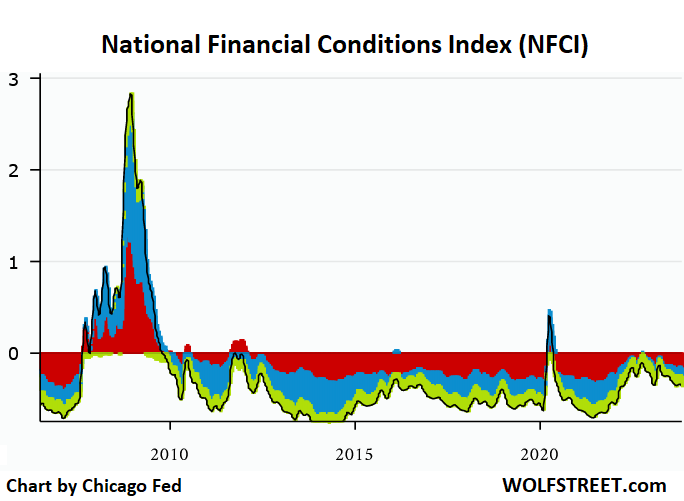

The long-term chart below of the NFCI shows what happens when financial conditions tighten so much that they strangle the economy, as they did during the Financial Crisis. The March-2020 spike barely registers in comparison.

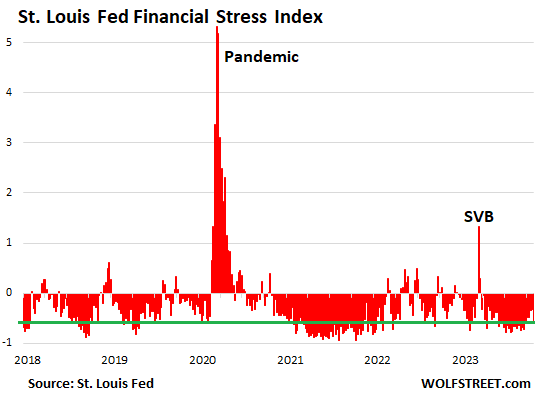

The St. Louis Fed’s Financial Stress Index takes a similar approach and measures financial stress in the credit markets. The zero line denotes average financial stress. Negative values denote less than average financial stress. In the current week, it dropped to -0.56. The green line shows this current value across time and denotes that credit markets are still in la-la-land.

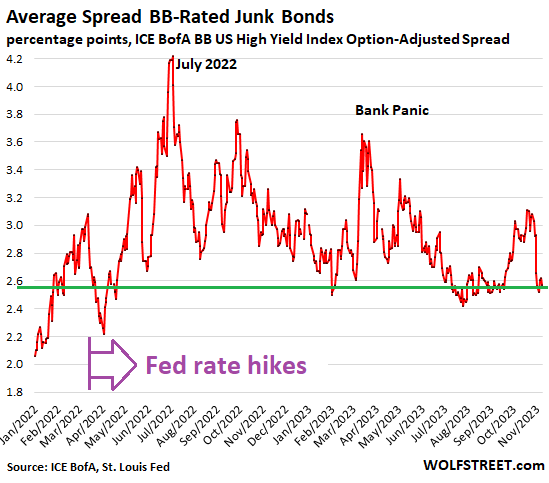

The BB-rated junk-bond spreads are another measure of financial conditions. Corporate bond yields should rise or fall with Treasury yields. But a wider spread between those corporate bond yields and Treasury yields indicates tighter financial conditions; a narrower spread indicates looser financial conditions.

The average spread of BB-rated bonds, the less risky end of high-yield (my cheat sheet for corporate bond rating scales) narrowed further yesterday to 2.57 percentage points. So this is going in the wrong direction, in terms of what the Fed wants to accomplish.

Sure, some sectors are stressed and financial conditions tightened in those sectors, such as the office sector of commercial real estate, but the troubles in the office sector have structural causes, including working from home and the corporate realization that they don’t need all this vacant office space that they have been hogging for years, and will never grow into.

And home sales have plunged because potential sellers don’t want to give up the 40% to 60% price spike they got over the period of pandemic QE; and buyers just laugh at those prices and go blow their down-payment on all kinds of stuff and services, including travels and cars – new vehicle sales surged 20% year-over-year in Q3 – contributing to consumer spending.

And subprime lending has tightened all around. In terms of auto sales, selling and lending to subprime-rated customers is focused on older used vehicles, often by specialized dealers and lenders — often owned by PE firms — some of which have now collapsed. Securitizing subprime auto loans has become difficult as investors are now taking losses. And the subprime segment, a small portion of the auto business, has tightened up, but with essentially no impact for new vehicle sales, where subprime loans are just a tiny portion.

And sure, the major stock indices are down from their highs a couple of years ago. Sharply higher yields (lower bond prices) have put pressure on bank balance sheets, and a few, run by goofballs that failed to manage this properly, have collapsed.

But consumers are working in record numbers and are making record amounts of money, after receiving the biggest pay increases in 40 years that in 2023 are finally outrunning inflation, and they’re spending huge amounts of money and are still able to save some. We’ve been lovingly and facetiously calling them our Drunken Sailors here since at least March.

And companies, flush with cash from selling a tsunami of bonds at low rates during the Fed’s 0% era, are investing, including in a huge construction boom of factories. And they’ve raised their prices, because, you know, this is inflation, and they got away with it.

And the true Drunken Sailors, the folks in Congress, are throwing trillions of dollars a year in still easily borrowed money at the economy to fuel growth and inflation.

So the Fed’s policy rates that went from 0.25% to 5.5%, and its $1.1 trillion in QT so far have failed to broadly tighten financial conditions and slow down this train.

Could it be... that so much central bank liquidity was created during and before the pandemic that financial conditions cannot meaningfully tighten, despite the Fed’s tightening, until this liquidity gets burned up?

The Fed alone, not counting other central banks, created $4.8 trillion within two years of giga-money-printing, as Musk would say; it has now removed $1.1 trillion of it via QT.

Could it be, with so much liquidity still out there, that it might take a lot more and a lot longer to tighten financial conditions enough to where they have even a chance of removing the fuel from inflation?

And that’s kind of funny because if financial conditions don’t tighten enough to slow the economy and remove inflationary fuel, and if it then turns out that this dip in year-over-year inflation rates was just a “head fake,” to then resurge again, as Powell said he suspects it might, the Fed will go at it with more rate hikes. Powell made that clear. With credit markets still blowing off the Fed, are they trying to make sure that “higher for longer” gets entrenched? That would be funny.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

wage are increases ARE inflation; they are the cost of labor.

Unless the wage increases are matched by productivity increases.

They’re not, unless you think the same workers are 20-30% more productive than prior to 2021. I see no evidence of it in my industry.

the workers however do get to pay more income taxes

remember ‘inflation’ is made up word

meaning = devaluation of fiat $dollar

or THEFT BY GOVT

If we’re hung up on nomenclature call it reparations for 40+ years of uncompensated productivity gains – or maybe wage deflation (less triggering to the triggerable). But we can all do this math at home. Just get some FRED data, start the clock in Jan 1980 and you’ll see:

GDP (adjusted for population) +568%

Hourly earnings +342%

CPI +294%

If you believe in math then we (the haves) owe the working man a ~50% pay hike, from the current $29/hr to $44, just to keep pace with how much more we’re getting from him every hour.

And in case anyone thinks I’m cherry picking dates start the clock at Jan 2020:

Population adj GDP +27%

Hourly earnings +22%

CPI +19%

More confirmation that being poor is expensive

So white Bob

You would increase prices and leave wages alone?

Letting the workers fend off hire prices with no cover?

sufferinsucatash, I don’t think that’s what white bob meant. What he meant is that if the average worker’s wages go up by 20%, but prices stay the same, assuming that the wage rate is set by the market, then that means that the average worker is 20% more productive. This has happened throughout history through technology.

If a worker’s wages go up by 20%, but prices go up by 20%, that’s just inflation.

That’s what we’re seeing now.

Labor productivity (output per hour) for non farm labor is just shy of its 2020 peak in q3. It is continuing to rise, but no, it’s not 30% more than prior to 2021. I do find it interesting that productivity has started climbing since people are returning to the office. Lends credence to actually being in the office.

This is to Wolf. OF COURSE IT DOES!

Not trying to be mean, but are you just now figuring this out or is this just the first time you’re rhetorically posing the question?

You don’t create $9T without that having vast consequences for inflation. As I’ve said many times, I want to see the RRPO facility to go away at least in terms of the monies being parked overnight. I certainly don’t understand the full inner workings of how the Fed maintains liquidity, but it’s very obvious that their move away from reserves has created even greater problems.

Furthermore, the Fed should be statutorily barred from purchasing treasuries 7 years or longer. Mucking with the longer-end of the curve is downright criminal. Consequently, this means the Fed shouldn’t be allowed to purchase MBS.

Rates associated with MBS should be market rates, and the consequences of their failure should be held by the MBS market. When the next recession hits, Congress is going to trot out rent & mortgage relief again and this is criminal.

The Fed & Congress are stuck in this perpetual game of picking winners & losers which is just wrong. WRONG! WRONG! WRONG!

Ha ha ha..productivity increases, that’s a good one.

“Be more productive”

“Oh cool then I can afford a house!

“Well no…”

“Oh well at least afford to start a family!”

“Also no… we will import the new workers for the next round…”

“Oh… well then at least pay down these loan?”

“Also no, listen I’m doing you a favor here. I created this job!”

“What’s this all for though?”

The stone will produce water soon enough.

That’s good.

Good article that articulates, without bias, the measurements that are continuously made on the economic patient that we are all concerned about, whether we admit it or not. One thing that stood out was the sentence:

“Corporate bond yields should rise or fall with Treasury yields.”

IMO, one of the indicators of a synthetic economy, which we are living in, when the first derivative of the price of corporate bonds as a function of the T yields, the margin above the T yield.

Or it is a monetary thing. Increase the amount of money tenfold, increase all wages and prices by addeing a zero and there is inflation, but everything is much the same.

Well, less those that had money in the bank have just one tenth left. Those who lent money is no better of, the money they get back is worth just one tenth.

You put your finger on it…inflation is *all* about the printing entity’s (G) appropriation of the historically accumulated savings of the saving entities (private sector).

The G does not earn or save…but it can print.

The public earns/saves…but it isn’t allowed to print.

That is the absolute crux of the power relationship in the economic realm.

At any time, the G has empowered itself to dilute away (and appropriate unto itself) the value of accumulated human savings.

It takes a village…but only a tiny sliver control it.

The problem is that the rate of earnings and savings has a massive spread, hence wealth inequality. Too many people at the bottom with no pre-pandemic earnings or savings delta, this charade becomes completely unsustainable.

Bay Area person, the charade becomes unsustainable because all government “help” comes at the expense of other people. Basically, the Fed has decided that holders of dollars, both foreign and domestic, should pay for the entire pandemic “response.”

Asset holders came out whole, as the prices of their assets rose to meet the new dollar amount in circulation, and the Fed has no intention of pulling even a majority of that new money out.

Well, I think it is significantly simpler than all that.

It is the real world data point that the libertarian low tax policy sold to America beginning with the improbable election of the ultra right wing, the John Birch Society like candidate,Wrongald Rayguns, is more destructive than was warned about.

Dang,

But the Keynesian pitch is that government spending (even at the cost of 50 years of paradoxical deficits or money printing) will lead to macro-economic growth, allowing for “self- financing” by the G.

But $32T+ in debt argues that that Keynesian utopia is an illusion.

I’ll buy that there has been some level of under-taxation at the highest levels…but uncontrolled, unfunded G spending has contributed far, far more to the problem – and things are so fiscally horrible now that my guess is that outright 100% wealth confiscation of billionaires/millionaires (with *huge* consequences) would *still* be inadequate to balance the G’s books.

(One note – estimates of cumulative US private “wealth” can be pretty misleading…based on eminently volatile asset “valuations” that can change pretty damn quick – all the more so if dramatic changes/confiscations take place. Increased taxation at the margin is one thing, but dramatic policy changes have dramatic consequences too. As with *any* balance sheet/bankruptcy, America’s “asset values” are pretty theoretical, its “liability values” much more concrete.)

So, I assume you can hardly wait til the government is “drowned in a bathtub” too, and replaced with a “well run and businesslike” police state wherein YOU are one of the protected?

Get ready to be surprised…..unpleasantly……the “sliver” doesn’t need or want you at all.

Me either…..just to be cordial per the rules.

Oh yeah, that completely ridiculous guess of yours is evidence of an ignorant debating style similar to, “Like you have never seen before”.

Intended it to be the “accent” on your garbled comment?

Please tell my large private sector employer to add a zero. So far they have used inflation to cut salaries.

Pension are inflation, fake wallstreet evaluations (see overblown ‘tech’ companies like WeTwerk) are inflation, fake housing appraisal are inflation, non producing gov cogs are inflation, sports ball is inflation….anyone working to actually produce something of value could be getting 10x and it would still be deflationary because many, most, 75% percent or more produce nothing. Or collect the 10x difference between wages and inflated quasi gov business, clown bucks. The grandparents robbed the kids and there kids and then they have the audacity to spill this nonsense slave-justification propaganda on behave of the American-conglomerate-nanny state-corporation

Having large deficits doesn’t help the fed does it?

Running persistently large deficits ultimately injects liquidity doesn’t it?

Some percentage of these massive deficits does work its way to main Street after all.

Actually, the massive deficits are made possible by the savings which cannot be invested productively in the home market as long as the dog eat dog practice of offshoring is encouraged by our dear Government.

Could it be, with so much liquidity still out there, that it might take a lot more and a lot longer to tighten financial conditions enough to where they have even a chance of removing the fuel from inflation?

So much liquidity – yep you are absolutely correct. First, the Federal Reserve during the QE timetable provided ($7 trillion) free money which caused artificially low interest rates to create a magnificent asset bubble. Our sailors are drunk. Then Covid Hit. To help our drunken sailors, government must provide unprecedented stimulus to help both business and individuals to the tune of roughly $9.6 trillion (6 major tax acts starting in 2019 – 2022). So, $17 trillion dollars pumped into the enconomy and the Federal Reserve has been only able to reduced it by 1.1 Trillion. So much Liquidity. And

Currency debasement causes hyperinflation which….starts as inflation. Moody realizes this and just rated USA negative. This can’t be fixed.

It didn’t “rate” the US negative. It still “rates” the US triple A. It changed its outlook on its rating to “negative,” all that means is that it might downgrade the credit rating in the future.

Moody’s chickened out. It should have downgraded the US, but left it at triple-A and instead said that it might downgrade the US in the future. It was just chickenshit. Buffett owns Moody’s. That’s why.

So where does this leave the everyday consumer who has debt because of high interest rates on credit cards, why is there no help for the everyday poor consumer who has to pay high prices with the same money and can’t get a loan because interest is to high.

They shouldn’t spend money they don’t have, Jackie.

No one owes anyone cheap money.

We’re in this mess because of cheap money.

As a wage earner, my savings shouldn’t cost banks 0.1% to lend to other people.

Finally savers are getting 1% or so real interest which should be the norm.

The US economy is the cleanest dirty shirt, the AAA rating is the best guess that the borrower will pay you back.

At this juncture, the US is the AAA lender and the idea that hucksters like the bond rating agencies, paid for their opinion, spew anything but bullshit, is preposterous.

It takes a long time for higher interest rates to filter thru. As ultra low interest bonds mature, they have to be replaced by ones with higher rates. Companies that are barely profitable now may not make it with vastly higher interest expenses. Or at least their earnings will be reduced.

As wolf pointed out, congress is still blowing bubbles faster than the fed is doing QT. What I haven’t seen him mention is other central banks (hello japan) are still keeping rates near zero. It’s a global economy and big corps can borrow there too.

Japan is the big exception, last NIRP country out there. But it’s taking baby steps to move away from it. I post articles on Japan from time to time. Not a lot of people read them, so I don’t do it often.

Wolf – I’m hoping you’ll do anther Japan article soon.

Specifically curious to hear your thoughts on the BOJ’s recent YCC adjustment. Seems like they’re flirting with the idea of letting rates rise.

I recall reading that the BOJ owns half of the entire JGB market. Not sure how alarming that is but I imagine its somewhat responsible for the weak Yen. USD:JPY has been >150 lately.

Well, Wolf’s article is about how the obese Fed balance sheet is nullifying the normally expected economic response.

Reading between the lines, the markets are in danger of imploding without the monetary stimulus of the QE philosophy, a financial crisis averted by a financial solution.

As a small business owner I can tell you that all the government programs during the pandemic – county grants, PPP, ERC – were not enough to offset losses – rent, taxes, utilities, insurance, licensing . I am sick of hearing how businesses “made a killing” on government “stimulus”. I lost about $100K and had to get an SBA loan. And I know others who had to also. And that loan will not be “forgiven” like student loans.

It was the biggest transfer of capital from small business to big business in history.

BTW, Wolf. I found a good new lease and did not sign any personal guarantee. Only 3 months security deposit. This landlord knew I had walked away from other deals and needed a good tenant as he had to evict the previous one for non-payment. No one always holds all the cards.

I agree with you the shut downs that occurred and continued put large numbers of businesses out of business many forever. I thought horrible then and still do today and a fund to help you is worthwhile in my opinion . Fraudsters should pay back triple.

Joe2, no offense, you’re using n=1. For every one of you, I know (first hand) of others with small businesses who did make a killing…. received millions. They bought ski boats and in some cases, jets. Maybe we’re just differing on the definition of “small”.

I view PPP and all the other stimulus as the biggest ripoff ever.

Agreed. Congress was either stupid or evil to dole out money to businesses that didn’t suffer a revenue loss.

Don’t forget the employee retention credit that was halted by the IRS for fraud and reached $30 Billion in August

I agree. The entitled that have taken control of the world that others forged, masters of the harvest.

So true. Same to me. The SBA, sends the payment due notice on a timely basis every month. Now, not only has RTW been slow (in the business district of Boston) but I have loan payments on lower sales.

Exactly, all that money has to come out of the system to restore the stolen purchasing power

Atlanta Fed has a Taylor rule calculator. The jaws between the EFFR and the rule based estimates are closing in Q4. We will find out how ‘resilient’ the economy is soon enough. My guess is a couple of quarters until cuts cause “they don’t want to interfere with election”. So we’ll get more inflation *and* unemployment in 2024.

Also behold the huge gap that opened in 2021, when they should have raised. They knew exactly what they needed to do, chose to ignore their duties, and will pay no price for it. Our institutions reek of late USSR stench, and the corporate media is their Pravda.

It’s been obvious for months now that whatever the Fed has been doing hasn’t been enough. That’s why so many people are frustrated with their puny .25 increases.

It’s not but the problem for them is what happens when it finally is.

If it’s like reeling in a long (perfect) elastic then the tension felt by the other end increases slowly but proportionally.

If it’s like reeling in a long slack rope then the other end feels nothing until all slack is removed at which point the other end feels a jerk proportional the the speed of tightening at that moment. If you’re tightening too fast when the slack runs out, the results can be disastrous. And we have no measure of how much slack remains.

Wolf’s analysis seems to indicate that reality is closer to the latter than the former.

Bullwhip effect.

Crack the whip!

I’ve been saying this for two years. QT should have proceeded with the same force and pace as the QE. If you don’t take it out quickly, it gets embedded and increases asset prices and debt levels, and increases financial instability. It’s the extreme level of asset prices, stocks and residential RE, that is causing the excessive inflation and spending, relative to savings and historical trends.

They need to ramp up the QT and sell the MBS before too many more people buy overpriced homes with overpriced mortgages.

We are three years into this thing, with CPI 20% higher, asset prices 200-300% higher, and the Big Seven priced to walk on water, and the Fed is still putting more cards on the house that it built by not withdrawing sufficient liquidity.

However, if the goal of asymmetrical QE/QT was to permanently ramp up consumer and asset price levels by 20-30% in five years, what the Fed did makes total sense.

Given the Fed isn’t talking about achieving its 2% average inflation promise during the 2020s decade, we know the motivation, which may stem from intentional misdirection or kick-the-can spinelessness.

To assess true motivations, you have to look at results.

Bobber,

I couldn’t agree with you more.

“I’ve been saying this for two years. QT should have proceeded with the same force and pace as the QE.”

No. I hate QE and think QT should be more rapid. HOWEVER, what you’re suggesting makes little sense. QE was lightning fast in response to an acute crisis. Drastic environment, drastic solution. To have ripped QT down at that pace, when no acute crisis was evident, would have been reckless in the opposite direction. It would have caused another crisis itself. What we have been facing is a more chronic and slow moving problem, in no way justifying a giant rushed contraction of the Fed’s balance sheet.

I can see it now, plenty of readers here crowing about the crisis of inflation since 2022. I get it. But sorry, 15% CPI cumulative is nothing compared to the -25% GDP (or whatever it was) of 2020.

There is an asymmetry in crises, and thus an asymmetry in Fed response.

2020 did not have -25% GDP. Where did you get that nonsense from?

Einhal, not nonsense — Q2 2020 was -30%. It’s on Statista. Acutely acute, I’d say, warranting more drastic action than today’s or 2022’s inflationary environment. Yes, Q3 snapped back by nearly that, which argues drastic action either worked or was no longer needed. But that’s another issue.

I’m merely explaining why Fed action need not be symmetrical.

Gattopardo, that was not 30%. That was 30% “annualized,” meaning it assumed that the 7.5% or whatever it was would continue each month. It didn’t.

Thank you, Einhal, for remembering the good old times:

No, GDP Didn’t Plunge “32.9%” in Q2, it Plunged a Still Terrible 9.5%: Time to Kill “Annual Rates”

Einhal, I know. I apologize for not saying annualized, as I thought that was clear (enough). My underlying point is the same — that was a nutball, acute and scary (though self-inflicted) crisis. It makes perfect sense for the Fed to have reacted quickly and powerfully, and to react much more slowly on the backside.

The rate increases do little to reduce inflation. The increased interest expense to the borrower is offset by the increase interest income to the lender. It slows down economic activity a little. QE/QT is where it’s at, but the Fed is afraid of pulling liquidity out so fast that they cause a depression.

FED broke price stability by printing extravagant amount of money during the pandemic.

In early 2020, the FED balance was around ~4.3T. This was already elevated when compared to late 2019 (~3.8T). In just two years between March 2020 and March 2022, it printed another ~4.6T, raising the balance sheet to ~8.9T. In other words, in just two years, the balance sheet was more than doubled.

FED said they are starting so called “QT” in June 2022. In almost 18 months, they only shed about ~1.1T and reduced the balance sheet to ~7.8T, which is still gigantic (more than twice of 2019).

This gigantic balance sheet and the market’s expectations that FED will stop QT soon (probably in 2024), is constantly fueling asset prices, inflation and reducing the value of dollar against real assets (but not against other currencies because nearly all CBs went nuts and they all printed recklessly).

Just like target rates, FED must have “target balance sheet” and it must be close to the prepandemic levels, which were already inflated. The only way to go is to sell mortgage BS.

I think the Wall Street expectation is that FED will stop bond roll off very soon and balance sheet will never ever go under 7T. That expectation must be decisively broken by declaring a solid target balance sheet and starting to sell mortgage BS, even though it may be at the minuscule levels (like 10B each month).

According to Chris Whalen, the Fed’s own formula will NEVER reduce it’s bal sheet below $6 Tril link>

A little late to the party?

According to Wolf Richter over a year ago (Sep 2022), the Fed can reduce its balance sheet at the most to $5.2 trillion over the next few years. It cannot go any lower:

https://wolfstreet.com/2022/09/05/by-how-much-can-the-fed-cut-its-assets-with-qt-feds-liabilities-set-a-floor/

According to Chris Whalen bank analyst Fed’s own formula will NEVER take bal sheet below $6 Tril. “Inflation, Politics & Fed Chairman” good read too.

GN – If you’re suggesting we accept the insights of a (*cough*) bank analyst over that of Mr Richter, I’ll pick myself up from the floor after I piss my pants in laughter.

As for the 1 minute response (4:14 after 4:13) …. RTGDA

One good thing that’s happening is that wages are increasing which is not inflationary, given the deficit between the increases in profits and the increase in productivity over the years since the early seventies and the increase in pay.

Wouldn’t it be wonderful if that was what “our” Fed was trying to do, instead what they probably are doing.

I hope it is a head fake so we get more rate hikes and faster QT. Drop the cutesy “bank term funding program”. Sink or swim. No more bailouts.

Easy to say now, but if it causes a depression with 25% unemployment, who gets the blame?

It can’t because soon retirees will outnumber workers. The retirees are all getting wealthy with higher interest rates and spending big time. In the future higher interest rates will produce more inflation instead of less as retirees outnumber workers.

“The retirees are all getting wealthy with higher interest rates and…”

LOL, no one “gets wealthy” from 5% interest payments when inflation is 5%. Or even when inflation is 2%. But retirees might make some cash flow that they can plow back into the economy, which is good for the economy, and the younger workers in it.

Wish you were correct…but alas….

As a retiree, my costs are rising much faster than investing in short term bills and manipulated stock market pricing can compensate for. The basics should be obvious but are easily lost in the averages over the last 2-3 years: HOA fees, insurance fees, gasoline, service fees (“sure we can sked an a/c check for next Wed, but we charge $150 just for the drive to your place”), medicare deduction increases (from soc sec), auto maintenance fees, red meat per lb costs, and on and on….all working to reduce standard-of-living. Buttttt……..PCUs are certainly faster and large screen smart TVs cheaper – can never own enough of those!

Yup…Wolf is correct about the huge excess liquidity being a key driver…as is seriously deranged political autocrats creating current and future debt obligations beyond imagination.

I do not have a crystal ball…but it is unsustainable. It is impacting a very large number of people at the middle and lower rungs, it will create (my guess) difficult budget decisions for most retirees within the next 3-5 years. Just the imbalance in wealth distribution keeps getting worse from an already de-stabilizing social coherence pov.

Excuse….CPUs. Didn’t sleep well last night….

That is the fearful scenario that more often than not ,suggests itself. A sudden repricing of the value of overpriced assets, the bubbles, collapsing, housing selling price falling 45 pct, stock prices by an astounding 60+pct.

Well, it certainly has happened several times in my lifetime. Hardly, as if, it were a tragic, unheard of event. What makes it really scary is that is the logical conclusion.

I am totally WITH you, BB, but am not exactly holding my breath on that. Our whole financial system has now morphed into a series of convoluted bailouts for all institutions (including homeowners, screw the renters and the poor), that I’m afraid we’ll always be stuck with in some form or another. I don’t think there’s any hope for the poor or the younger generations going forward. Sad state of affairs.

“screw the renters”

Are you insane? You must not have paid attention for the last, oh,….forever years. Especially in CA. The “system” protects renters at the expense of landlords and neighbors to an extreme.

Maybe so, but a different problem on a different level is a young generation taking their paycheck and handing all directly to landlords. No personal capital is formed. I look at my college students knowing many are in the serf stratum. At some point that brings political heat (or in some place in history, worse). It’s a good time to be born in a family with assets!

Yes, in some places, the system protects the renters. But there are plenty of booms who bought rental houses for $100k in the 80s, and now rent them out for $10,000 a month, all while screaming about how brilliant they are.

Einhal, you must think this home inflation is new. In the late ’70s, my dad, a very hardworking professional, bought a $125k house, and barely could afford it. Neighbors who had bought 30 – 40 years before him had paid $10k – $20k+/-. His house is now worth about 10x. The rate of appreciation is approx the same over those periods.

I try to avoid age/generational warfare, so I won’t comment on your ‘boom’ line.

phleep, I’m not convinced the economic environment is really all *that* different than decades past. Most of us were in the serf stratum when in college (10, 20, 30, 40 years ago) and for a decade after (or longer), breaking out only with hard work (genuine hard work, not the 40 hr/wk imagined “hard” work) and/or some luck. And it has ALWAYS been a good time to be born in a family with assets!

“CAN” BUT WILL NOT. It’s still $8 Tril .

Assets are dropping at a pretty good clip, and you’re behind the curve, already down to $7.86 trillion. Going to be $7.7x trillion on the Dec 7 balance sheet. They’re already down $1.1 trillion, despite the bank panic depositor bailout. The Fed has already shed 27.5% of the $3.27 trillion in Treasury securities it had piled on during pandemic-QE.

Good analysis Wolf, but that chart from the Chicago Fed grossly underrepresents the financial pain/dislocation associated with the onset of the pandemic. Many astute observers of both 2008/2009 and 2020 found moments of the later substantially worse than 2008/2009.

That was before the Fed came in and made financial markets ‘comfortably numb’ 🎼💰💰🥴

All the financial conditions indices picked up the stress during March 2020. I don’t know what your problem is.

There was huge turmoil in the Treasury market! It went completely haywire. That’s what they’re referring to. Hedge funds were starting to blow up because their basis trade backfired and all kinds of stuff related to Treasuries was happening, including Treasury money market funds threatening to cause grey hairs. But that’s not really “financial conditions” in the credit markets. The Treasury market is supposed to be safe and smooth, not chaos, since there is no credit risk.

AIG and Lehman blowing up and along with the mortgage crisis attempting to take down the entire global financial system was a MUCH bigger event for financial conditions than March 2020. At the time, businesses weren’t even sure their payroll account would still be functional on payday. Those were the times!

Easy Wolf… I just meant that visually the St. Louis Fed chart shows a 5X ‘financial stress’ event whereas the Chicago Fed barely shows a historical blip.

March 16, 2020 Dow decline of -12.9% was truly historic (-37% from Feb. 12-Mar 23). And the bond market was a mess too as you just pointed out. Briefly negative oil futures yet the Chicago Fed chart makes that period look like ‘a molehill’. 😏

I believe the issue is that hiking interest rates doesn’t do anything to solve what is primarily a supply side collapse. Those raises affect demand, not supply, problems. Congress needs to pass progressive tax rates. That helps to fight inflation caused by demand. l

Inflation has been in services for over a year, and there were never any supply problems in services. Services are over 60% of consumer spending. But not all services have consistent price increases, as I pointed out.

Durable goods prices have fallen for over a year. Durable goods CPI is negative. Used vehicle prices have come down a bunch. Prices of electronics have come down a bunch, etc. The supply problem was in durable goods, and those issues got resolved a while ago.

Yes, higher taxes would take some demand off the table. But less deficit spending would also take some demand off the table.

You got it backwards as usual. Tax rates didn’t decrease after 2021. Government deficit spending increased. That is pushing inflation.

I remember those days after Lehman and Lehman crushed my income, employment, moved cities , and several hundred thousand of Lehman bonds poof. Other banks bailed out but not Lehman ?! I was left holding the bag of worthless bonds . Not to mention I was in the oil business and our revenue disappeared. 140 dollar oil to something south of 40 dollar oil. I don’t want a repeat of that one . Slow and steady QT .

Problem is we don’t know slow and steady in this country. I’ll be surprised if the Fed sticks with it long enough to finish the job. Hopefully, I will be pleasantly surprised.

Fed – when the ‘thought processes’ of digital tools start to dominate the thought processes of their digital ‘masters’?…

may we all find a better day.

…(damn, this went WAY off-piste!), should have read “…analog ‘masters’…”.

Apologies.

may we all find a better day.

Banks are upside down, Wolf. The private surplus is enormous, particularly at the top. This is the golden age of private credit. Junk spreads don’t matter because borrowers prefer private credit for lower origination fees, even with rates on loans as much as 6% higher (fees were/are predatory.) Leveraging your receivables is a hell of a lot easier than jumping through bank hoops for lines of credit and loans. Alot of profitable small businesses are getting screwed by banks without the liquidity to lend to them. Yield seekers with big money are getting 10-12% yields on no-brainer underwriting for private credit BDC’s and the financialization of leasebacks goes even further. There is no income tax until capital is returned.

Tens of thousands of small businesses were started with pandemic stimulus. Those businesses could very well be profitable. But the banks are looking for unreasonable conditions to lend to them.

The only thing that is being slowed by the Fed are the extreme fringes of Private Equity, Venture Capital, and housing and even then, the builders and flippers take bridge loans from Private credit and then buy back points on their sales.

On the other end, giant conglomerates that should have anti-trust suits against them probably 6 years ago at this point but prop up the entire American pension/401K system have gigantic stashes of cash. And in-flows to the SPX continue because, well, where else is there to go? The “Mag 7” carry the entire SPX.

Really weird times. I don’t see how it ends until something breaks and the system seems to be self-sufficient and robust because it has so much to fall back on.

The Fed is irrelevant now. At least until they are ordered to do QE & YCC and monetize the government debt again, which will much exacerbate inflation.

We are in fiscal dominance regime, which is more like war time finance and economy.

Most debtors are insulated from interest rates because after 10 years of ZIRP the effective interest rates of individuals and corporations are much lower. Of course the hyper financialized economy cannot run on higher interest rates, so eventually it will reset.

In the meantime the holders of old debts are underwater- banks and the Fed.

You cannot deflate a debt bubble, it will eventually implode. Reset is coming. Paper assets will become cheap compared to real assets.

They should have taken or take all the money out of the worker’s vacation pay for the next 20 years to pay back all the money they should never have gotten during this Covid scam. For the next twenty years your vacation will be spent working for no pay.

You love hating workers, don’t you?

They’ve been screwed by employers for decades where wage increases lagged behind productivity gains.

Rabid capitalists love hating workers.

Powell: Biggest mistake Fed could make would be to fail to get inflation under control

It seems he already has…

Seems to me that if inflation isn’t cut back, then these rate hikes will only add to the inflationary pulse.

The good news is that the rate of inflation has diminished. That’s not to say that it can’t worsen. But economic cycles aren’t stationary; they rise and fall.

He has a tough battle when the Government is issuing $2 trillion in debt this year.

Looking forward

Though the feds may have declared a temporary truce on their monetary inflation, they’ve increased inflation pressures on the fiscal front. So while the quantity of lendable money is restrained, the world’s biggest borrower – the US government – spends more money than ever.

A two-trillion-dollar deficit must be financed, there is also the old debt that must be refinanced. There is $7.6 trillion in Treasury debt that will mature in the next 12 months.

That will bring the total funding requirement to nearly $10 trillion. Whatever else might happen as a result, interest rates will probably go up.

I read 34 of 46 states reported year-over-year declines in tax revenue, inflation adjusted, over the last fourteen months. Draining the liquidity swamp seems to be taking longer than expected.

The Game of Fed is perhaps half way completed, but don’t tell Wall Street, as I need the SP500 to get to 4900 first…HA

Wall Street is the problem.

Government deficits of $1.7 trillion per year isn’t the problem? Government bailing out Wal Street isn’t the problem?

White:

Of course government is also the problem, but Wallstreet is very much the cause. I was responding to a post that was mentioning stocks. Geez!

White

Meant to say a big part of the cause. Of course there are many factors, wall street being majorly complicit.

Fed Up, you’re trying to find a villain and found “Wall St.” Evil incarnate.

It’s a casino. Is the casino the villain, or the patrons, or the casino owner, or the state government, or the public who want gambling casinos?

Origin of stock market?? Amsterdam, during the tulip mania, 1600s. Dutch East India Company was the first company that traded shares (and gave dividends).

Why is it that every belief system has to have an evil force to keep it in business? Answer: you can’t have a good guy without a bad one.

How – Mr. Youngman today might say to today’s audiences: “…now, casinos-take my money, please!…”.

may we all find a better day.

The Fed is playing with” inflationary-psychological-wildfire”, as the US consumers’ long-term (5-10 year) inflation expectations increased to the highest since 2011 according to Bloomberg, rising from 3.0% to 3.2% (large relative increase).

The trend is not the Fed’s friend, in regards to inflation, the stock market melt-up, and the idiotic idea to tie rate expectations to an indicator as volatile as the “financial conditions” indexes. Come on Jay, just make it Tesla’s stock value and lets get immediately to the end game..>LOL!

Fed seems concerned as “Fed Whisper/Mouthpiece” Nick Timiraos posted the U-Mich survey this past week, stating the year-ahead inflation expectations up at 4.4%, with September reading at 3.2% and October at 4.2%.

The Game of Fed has begun and 2024 is coming…

OK, where is your proof that the ” inflationary-psychological-wildfire” will be unleashed on Tom, Dick, and Harry ?

With the ill-advised monetary actions taken by the Fed in the last 50 years, and the consequential fall in purchasing power of the dollar, how can it be that we are not questioning the Fed’s mission, scope and modus operandi?

It defies all logic and common sense. Commanding the economy to create jobs via monetary manipulations is no more effective than were wage and price controls in the 1960’s.

Haven’t we learned anything over the last 110 years?

I would like to point out that, in fact, stable NGPD growth _is_ effective in maximizing employment and economic growth.

(Where wage and price controls are not)

Acknowledged that CBs have made huge errors that seemed obvious to some of us at the time, and are blindingly obvious in hindsight.

NGDPLT-

I hate to reveal my non-academic background, but what in the world is “NGPD.”

In an attempt to educate myself, I searched NGPD, and got Newman Grove Police Department, and Next Generation Prenatal Diagnosis, but neither seems appropriate (the latter was listed under the heading of “midwifery.”)

If what you are referring to is some sort of attempt at economic stabilization policy, I’d love to see evidence for your statement — evidence of a society where the policy worked over a series of cycles, with no nasty side effects, and still exists. Kindly direct me.

Thanks.

National gross domestic product?

Given the context, I’d guess it’s nominal gross domestic product. I’m guessing that because the name is “NGDP”LT, so I’m thinking NGPD in the comment is a typo.

Sorry – I totally typo’d – nominal GDP, as another commenter deduced.

Australia, for example, was largely able to avoid the GFC (Global Financial Crisis).

I didn’t mean to imply that central banks had a great track record – on the contrary, I think there is a good case to be made that the Fed cause both the GFC and the Great Depression.

But unlike with price controls – bad in theory and in practice – monetary policy can stabilize the economy, in both theory and (only spottily so far) in practice.

Like the difference between shamanism and 18th century medical – both can kill you instead of helping, but one of them actually could work with improvements.

Level-targeting would help a lot – a promise to “make up” in both nominal shortfalls or excesses (because, say, high spending today means hard times tomorrow, so people and businesses cut back to prepare, and do a lot of the stabilization work).

Not sure I’m allowed to link elsewhere but I’d highly recommend Scott Sumner’s blog or books (but the books might be dense if you’re completely new to macro).

NGDPLT-

I’d be interested in hearing a summary of Austalia’s experience with NGDP targeting, especially:

– When did it begin?

– How has it fared at controlling inflation?

– Has the $AU fared well?

– How has systemic debt trended? (Gov’t, financial, corporate, and household)

Also how does NGDPLT avoid this problem that you identified earlier:

“Acknowledged that CBs have made huge errors that seemed obvious to some of us at the time, and are blindingly obvious in hindsight.”

Thank you in advance.

Thanks Rojo and Vecchio-

I think I found it: Nominal Gross Domestic Product – Level Targeting. Scott Sumner and David Beckfield, among others.

NGDPLT-

I would still be very interested in evidence of how this targeting has worked in action and over time. It looks scientific and mathematical, and would be really interesting if the realities live up to the elegance of the theory…

(Sorry if this dragged site of subject, Wolf!)

No central bank has NGDP level targeting as their policy target (yet?). It was only in 2012 that the Fed adopted a formal 2% inflation target, so… yeah, things move slowly.

I will note that people who used NGDP growth as a framework for evaluating the stance of monetary policy were much more likely than average to correctly expect that:

– the post-GFC monetary stimulus (say 2010-2016) wouldn’t cause inflation

– the 2013 budget cuts would not hurt the economy

– the 2021 period looked poised to blow up inflation

– we currently have 6-8% annual NGDP growth, so inflation is going to be way above target until that comes down (lmao when people say monetary policy is “tight.”)

Which is to say – empirically, using NGDP is a superior mental model and probably 95% of professional and academics are fundamentally confused on how macro works.

Separately, level-targeting brings inherent stability (like a super-effective version of forward guidance).

Sorry if this is too much, or too little, or the wrong kind of, information. I hope it points you in some directions you find interesting.

(I deleted a lot already… but there is a whole other rabbit hole about “what alternative could there possibly be to monetary policy”)

NGDPLT-

1. Not sure how these two statements you made above jibe:

“I would like to point out that, in fact, stable NGPD growth _is_ effective in maximizing employment and economic growth,” and

“No central bank has NGDP level targeting as their policy target (yet?).”

2. I don’t see your second paragraph as rigorous proof that NGDP is a superior mental model, and to the exclusion of all other mental models (though I’m guessing that you sincerely believe that it is). I do agree that 95% or maybe more (mostly Keynesians IMHO) are confused. The confussion lies less with how to successfully administer the economy than with the belief that monetary and fiscal stimulus can be used to SUSTAINABLY alter the economy without eventually paying an ever-rising price. “Deficits without tears,” as Jacques Reuff entertainingly referred to them.

3. Does “super-effective guidance” bring inherent stability? I’d love to see some empirical evidence showing that!

4. Does your last paragraph, mentioning the “rabbit hole,” include a new gold standard? If not, does it include some other automatic limitations placed on central banks to keep it from mushrooming as ours has these past 20? If yes to either, I’m all ears.

Respectfully.

BPOT

Big pile of twenties

My favorite ! Now off to farmers market LOL

For point 1 – if a central bank “successfully” balances inflation and employment, that virtually requires a stable path of NGDP. NGDP doesn’t have to be the policy target to be useful in evaluating whether or not a CB is screwing up.

I don’t really want to invest more in this, I’ll just say that “Commanding the economy to create jobs via monetary manipulations is no more effective than were wage and price controls in the 1960’s.” was a very strong claim and highly unusual claim. So I’d assumed there was a lot of research into it and tossed out an additional avenue of investigation – feel free to explore further, or not. :)

PS: It’s certainly a rare pleasure to have a corner of the Internet with productive discussion with curious people.

I appreciate the line of conversation too, NGDPLT.

For any nerdy or curious commenter who wants to read some up-to-date thinking on the endgame of fiscal/monetary control of economy, google “calomiris + fiscal dominance”

Calomiris is Henry Kaufman Professor of Financial Institutions Emeritus at Columbia Business School,. The article is published on St. Louis Fed site.

Stable GDP growth that relies on increasing the debt-to-GDP ratio is anything but “stable”. It’s elementary.

A system with a constant growth ratio do grow exponetially. No system with exponetial growt is stable.

Basic math and control engieneering.

…old bumpersticker from the (formerly) redwood timbering area I live in:

“Earth First! (we’ll log the rest of the planets later…)”.

may we all find a better day.

It helps if you start with the assumption they will do exactly the wrong thing at exactly the wrong time. They will not disappoint. It is self-evident tautology. Good question though.

The US is the best bet for business currently available.

Logic and common sense thought the Civil War was a good idea.

Speeding up QT could be the answer. 90 billion a month clearly is not enough. But the Fed doesn’t want to shock the bloated market.

You mean the ‘bloated BOND market’? Remebemr, those are their REAL customers!

Law of unintended consequences.

“The Fed alone, not counting other central banks, created $4.8 trillion within two years of giga-money-printing, as Musk would say; it has now removed $1.1 trillion of it via QT.

Could it be, with so much liquidity still out there, that it might take a lot more and a lot longer to tighten financial conditions enough to where they have even a chance of removing the fuel from inflation?”

This is like over-stretching a rubber band, then trying to somehow force it to become taut again. Sure, there are ways to do it, but in all honesty the most important financial condition that will repair this mess — ceteris paribus — is TIME.

I resisted using this comparison. Same with the ‘doorknob’ or the ‘tragedy of the commons / community pool’ examples.

Greg should use his little pea brain to come up with non sexist remarks.

Until those dollars get destroyed by defaults or otherwise why shouldn’t they just keep circulating? With higher rates comes higher velocity.

Per John Hussman the only way dollars get destroyed it to go back to the Fed to be retired.

“Every dollar of liquidity created by the Fed must be held by some investor until the Fed retires it by shrinking its balance sheet. That liquidity can be held in only three forms: currency in your wallet, bank reserves that you hold indirectly as a bank deposit, or funds on “reverse repo” with the Fed that you hold indirectly as a money market fund deposit. It can’t turn into anything else.”

This may be true but I would think my Lehman bonds that were defaulted on were retired. That “money” was burned because I did not get any of the bond value . If the Fed were to hold any corporate bonds if those default that balance sheet value is destroyed. The government bonds are different since the government issues unlimited new bonds for the cash and as Wolf says always can raise rates to find buyers

What is a check?

It’s the thing when you are losing at chess.

Your six.

andy,

Hussman seems a little confused here. I mean VERY confused.

His line…

“That liquidity can be held in only three forms: currency in your wallet, bank reserves that you hold indirectly as a bank deposit, or funds on “reverse repo” with…”

…is BS.

There are $3.3 trillion in reserves parked at the Fed, but there are $17.3 trillion in deposits at commercial banks, plus lots more deposits at credit unions and thrifts.

So there’s $14 trillion ($17.3 minus $3.3) in cash from deposits at commercial banks that they did not lend to the Fed (reserves).

Guess what commercial banks did with that $14 trillion in cash from those deposits? Buy Treasury securities that are now under water (see SVB), lend to consumers, companies, and even governments, engage in trading of securities, buy derivatives, etc. Banks send only a small portion of their cash from their deposits to the Fed (for liquidity purposes primarily and now also to earn 5.4%). The much larger portion, they use in running their basic banking business (lending).

Wolf, that is why I start with “per Hussman…”. I know you’d correct any misunderstandings. Thank you for that.

He is pretty good though. Check out one of his monthly comments sometime (he repeats 90% from month to month). He is not great on market timing, not even close. Sorry for double post.

Yes, he’s very good on a lot of things.

The only way to reduce the volume of bank deposits is for the saver-holder to use his funds for the payment of a bank loan, interest on a bank loan for the payment of a banks service, or for the purchase from their banks of any type of commercial bank security obligation, e.g., bank stocks, debentures, etc.

Also per Hussman- The long history of business cycles illustrates that rising inflation precedes recessions. And it’s the FED, in responding to one crisis the Fed has created another crisis, which is a process of booming the booms and slumping the slumps.

BTW Does anyone follow the Output Gap analysis?

The difference between actual output and potential output is called the output gap, which is expressed as a percentage of potential output. The short-run fluctuations of actual output around potential output determine the business cycle —economic expansions and contractions, or recessions.

Here is the NowCast Atlanta Fed OUTPUT GAP-

Output Gap 2023Q4: 2.9% (nowcast

Somewhere there is a chart that tracks the output gap with inflation, they seem to correlate.

Then there is the money not created by the FED. An example is the money generated by interest. The math of interest is that accrued interest are money generated.

Historical side node, that is the reason all gold standard and gold money system have to fail if interest are allowed. And maybe the reason why the Bible probit lending with interest. Someone did know their math.

Pow Pow is the greatest pilot of all time. We are going in for super comfy plush ultra soft landing or maybe the plane will just keep flying…no landing and no fuel needed…

Thumbs up Pow Pow

I took all my stimulus money as twenties and put it in the safe. This week I took out the last of the twenties and will spend it over the next couple of weeks. I can’t be the only one.

Yes paid property taxes for 2 years ++ with stimulus.

I always have big pile 40k to 50k of twenties. BPOT

“Make Cash Great Again”. MCGA as per CAF Solari.

Now in Hawaii 2 months for scuba, farmer markets and relaxation.

My observation folks are spending to enjoy life NOW !

My opinion at 70 the government and all institutions have broke our country since 1960. I do not waste time on the false narrative. I just enjoy the fruits of our labors. Spending millions in retirement is a joy.

I paid my Federal taxes with the last California stimulus check. Thanks, California!

Liquidity is only part of the reason I believe. How much international money was poured into US equity from abroad YTD because of the AI hype? In my capacity working in Private Banking HK, I have seen so much more buy orders into US tech from Asian investors. Maybe it’s also good to investigate international money flows apart from focusing solely on Fed liquidity movement.

Where does international money come from?

Pile of US dollars in foreign banks.

Plus dollars borrowed by foreign entities, through foreign banks in the US, through US banks in other countries, through foreign banks in foreign countries with a relationship bank in the US, through USD bond offerings by foreign companies and governments. Look at the stock offerings and ADRs by foreign companies in the US (Arm was the big one recently) that all raise USD.

More like ‘what gets bigger the more you take away from it?’

Going to be interesting how this aligns with the massive interest on debt that continues to grow. Theoretically they could cap yields on bonds but that would just lead to greater inflation and likely have a lot of other negative effects. With Hollywood and auto makers back to work things actually pick up in the economy rather than slow down.

Capping yields would lead to unsold inventory.

Yup. Last thing the Treasury needs is an auction failure.

Howdy Folks. Our Govern ment would never try and paper over its problems. Everybody trusts that the Govern ment knows what it is doing.

There are many who don’t believe that government deficits of $1.7 trillion per year is a problem. They believe the real problem is that workers and retirees aren’t paying enough taxes to fund all of the wars and government grift.

Wait, how are those different? If workers and retirees were paying enough taxes to fund all of our spending, then the government wouldn’t be running $1.7 trillion deficits.

“how are those different?”

That’s like saying “I don’t need to cut back on $8 lattes every day, you just need to give me a 30% raise”

Its a spending problem, not a revenue problem. Gov’t needs to tighten its belt and learn to live within its means; sadly this won’t happen until the bond market revolts.

I’m a partner is a small commercial real estate mortgage brokerage, and all of the regionals that we deal with in California have significantly tightened their lending criteria starting back in Q1 of this year. It’s getting more and more difficult to get anything done. Sooner or later this will further impact the CRE market, which eventually should have an impact on the overall economy. We subscribe to a commercial real estate service that tracks NODs and defaults, the numbers are moving up steadily month over month, but they still have a long way to go before an earthquake hits.

CRE is cooked.

You can stick a fork in it! We are in the process of switching our business model to buying distressed properties for a series of LPs. The number of SoCal NODs and foreclosures are still low but they have started to accelerate over the past 6 weeks or so. Best guess, the bargain hunting will begin in earnest Q2 next year.

I had a zoom call with a big CRE firm about placing one of my alpha properties for sale in a pre-covid top 10 US city. Mostly I wanted to see what they are thinking and what they are seeing. The take aways from them. They did a full package analysis:

1. Comps do not matter. Comps do not matter. Comps do not matter. No recent data to reflect current reality.

2. Developers are in charge, so you have to give them 2-3 years of holding time. Developers can only develop what they can borrow. So best use of the land does not matter.

3. Banks are not lending.

4. As a landowner, if you need to sell, you will take a huge haircut, like shave your head bald. My property was valued at 1/3, no really 1/3 of the recent comp value. So, if it was $15 dollars, now they are saying $5 dollars. This is truly a Class A property which I got unsolicited offers all the time, but I am getting really, really good rents. No FOMO or regrets, but mostly a kick in the teeth of what is going on.

I am talking to another big CRE firm to confirm this. I didn’t know the previous guys, so maybe they are snakey fuks, but my gut tells me no.

With longer and probably higher, things are not looking good for CRE. Maybe, I will pick up some bargains, but I am keeping my powder dry.

Good luck all.

I have regular discussions with CRE credit managers and portfolio managers, and the picture is not pretty. Most all of the banks and private money CRE lenders that we work with have cut max loan size in half, dropped LTVs from 65% to 50%, bumped DSCRs to 1.50+ and are more focused than ever on income, security & PGs in addition to the subject. They are now turning down deals that would have been an easy yes last year.

@CRE DUDE. If you’re in the right commercial building at the right location you’ll be doing just fine.

Selling? It all depends on cap rate. Here where I live most commercial for sale are listed at average 5% cap rate.

Retails strips are all the rage. I just tested on Loop Net a potential lease and was swamped with requests.

Only 5% cap rate when risk free for 5-20 years is the same? I would be looking for 7-8%.

It’s tough today to get a mortgage for a property with a cap rate of 5%, because the mortgage rate is going to be 7.5%, and you will not even be able to make the interest payments, and when you explain this to the lender, they will tell you to go into detox. You’d have to put a massive amount of cash down to persuade the lender to give it a shot.

That’s the rub, figuring out cap rate with longer and maybe higher rates with wonky comps and inflation. Meth smoking pro forma are LOL to read. It’s all about cash flow and good tenants. The dirt of this particular property is worth way, way more than some cap rate due to location, zoning, permitted use, special incentives, and no mortgage. But now, that is on hold until the bad air is cleared out. I’m good for 5+ years with good rents and tenants.

These CRE dorks are seeing if I am willing to blink first and went lowball with me with comps do not matter bs. Persona non grata. I see lots of hungry brokers, architects, and loan officers, oh my, in the near future. Take care.

I took all my stimulus money and traded them for gold coins

Or could it be…real rates are really still negative. The cost of goods & services are actually rising faster than the government says they are and its still profitable to purchase now because prices are increasing more than current interest rates.

in October, we got the cheapest direct flights from San Francisco to Europe that I found in the 18 years I lived here. Airline tickets are a service in CPI. There is big deflation in airline tickets.

The email service I use for this site just lowered its monthly fees — not by much though, LOL.

I changed broadband suppliers again and cut my costs from $70 a month to $25 a month. That’s a service in CPI.

My healthcare expenses plunged when I came on Medicare. It saves me hundreds of dollars a month if I don’t need medical services (just in premiums), and a lot more if I do use medical services.

People don’t ever look at the stuff that gets cheaper, and then their perception gets skewed.

Wolf.. to your point of reduced cost/pricing. The one thing that has to be pointed out is that you have to look for the decreased pricing – it won’t come to you. I did the same thing as you a while ago with our broadband. Moved from cable ($119 a month plus plus plus) to 5G at $25 a month with no degradation in service. There are multiple examples of that in our life…. we don’t just keep paying bills and kvetch because the rates have risen… we look for alternatives and often can find them. Heck, I just went to the grocery store and saved 51% on what I bought simply by using their dopey app.

Yes, that’s the only way to keep inflation down: consumers and businesses have to fight price increases — if they have to by taking their business somewhere else.

FWIW, my husband works at UCSF and nearly all of the health insurance plans option’s monthly premiums are going up enormously. In our case, our monthly premium is going up 79% if we opt to stick with Kaiser HMO, but some PPO options are going up by over 100%. It’s so much, that we are likely going to switch to the catastrophic plan with the higher deductible (3k each or 6k for both of us) as it has a $0 monthly premium, but makes more sense than paying 5k a year in monthly premiums whether or not you are actually sick and need to use services. The increases in monthly premiums are staggered based on how much you earn at UCSF so they are less if you earn less, and they are also much more if you cover your spouse and/or children vs only yourself (the employee). I had also read that UCSF added $93 million to fund their insurance program for their employees for 2024, but even that wasn’t enough. Sigh.

tangojennifer,

High-deductible plans can be a good deal if you’re not chronically ill and if you have a good amount of taxable income because you can set up a Health Savings Account (HSA).

An HSA is like an IRA, where contributions are tax deductible and earnings are non-taxable. They’re better than IRAs in that when you take money out for medical expenses, it’s not taxed either (but some states, such as CA, don’t allow you to deduct the contributions from your state taxes).

We’ve had those since 2006, ever since Bush came up with them, and now we have big balances in them that we use to cover future medical expenses as we get older, and they’re invested and earn income tax-free.

The tax benefits every year paid for about 1/3 of our premiums (which were low because we had big deductibles with $4,500 max out of pockets per year. But after our second year, we had more than that in our HSAs, so if we had had a big-ticket repair, the HSA would have funded the max out of pocket.

If you have chronic illnesses and don’t have enough taxable income, HSAs with high deductible plans may not be a great idea. This is a very personal decision, but do check them out.

Chemo is $15,000 per week for months.

Letro,

With a high-deductible plan, you have a maximum out of pocket per year, after which 100% is covered. Our max-out-of-pocket was $4,500 the last year I was still on it. So the most medical expenses you’re going to have per year is your max-out-of-pocket. Once you hit that, you do 10 years’ worth of elective stuff because now everything is free. But then add up all the premiums you save in 12 months with a high-deductible plan, and then add up the tax benefits from the HSA, and you will get a feel for it.

Mine in NC actually went down a tiny $ amount. Self pay because my employers is such bad insurance.

It’s still a lot but I was happy it stayed basically static.

I would also like to mention the living amenities retired people can choose to make.

For ex I’m on high income but I’ve chose to sell the McMansion home and settled down into a nice manufacturer home on a small lot-thus, cutting my fixed cost by 50%.

Well, my boss would not like that. I could totally swing it, but the boss would fire me. She needs coffee and books meetups and get togethers with her friends and family. I usually hide out in my study or go for a long walk.

Yeah, there are many other ways to lose 50%, my friend.

Twenty years ago, my cousin bought a double wide mobile home. I had never been in one before and was stunned by how nice the interior was, both in floor plan and upgrades. The cabinetry was stunning throughout. The price was somewhere between a third and a half of stickbuilt, if I remember correctly.

I mentioned my Costco prices in a comment a few months back how the only big change I noticed was their boneless skinless chicken breasts (6 packed in pairs) went up from $2.99/lb to $3.49/lb earlier this year. First price increase I’ve seen in well over 5 years. Today, the same Costco now has it back down to $2.99/lb…0% inflation in 5+ years easily if not 10 (I’ve been buying them that long regularly). Also saw reg gasoline was $2.95/gal and 93 was $3.25/gal so figured I’d top off since no line that moment I came in (was packed when I left).

And ditto the airfares. I mentioned a few months ago I got MCO (Orlando) to NRT (Tokyo) for $1051 and go back home recently. YUL (Montreal) connection was eerily empty and our gate was only one with a departure over a 4 hour span I wait for at least a dozen around. I was literally only person walking through the connections customs section of airport (thousand of square feet of empty lines with no one person visible til I got to sublevel stairs to scan my connecting ticket). No idea what that was about…flight was full at least.

Cool info.

I love to see real prices. I think maybe everyone put all their trips and purchases onto credit cards that they are now having to pay off. So they will pull back awhile. Then go at it like starving woodchucks who Chuck a lot of wood.

Z33,

In terms of the airports, my experience was different. The two I saw — San Francisco and Frankfurt — were packed with huge lines. Frankfurt’s departure hall was total mayhem. Both flights were overbooked with people on standby, some of whom were called up and could get on. They know how to fill those planes: cut the prices for the crappiest seats.

Is the $25/month that Verizon wireless thing they’ve been advertising? I got a flyer in the mail the other day. If that is it, how do you like it? How reliable is it?

No, it’s not Verizon. But the Verizon people actually “physically” knocked on my door selling 5G after they installed the antennas in my street, and we got tons of their fliers in the mail.

We now have three competitors selling Gigabit broadband in my street: Sonic fiber, Comcast coax, and Verizon 5G.

In addition, I have regular 4G on my cellphone, which runs at about 17 Mbts, which is more than enough for what I do; when my primary broadband fails, I set up a hotspot as backup (I have backups for everything since I live on the internet). That’s why I would not use 5G alone because I always need a backup. I could use 4G alone too, it’s good enough and reliable enough, but I need a backup.

The thing for me is if there is a broader blackout, both fiber and coax go down. And then I switch to my cellphone hotspot because the wireless system runs on its own power supply, including batteries. So even in a blackout, you can still use your cellphone — and therefore the hotspot (until I run out of battery power at home).

Thank you for the detailed explanation, that makes sense. Our cable provider charges like $100/month now, so I was looking to try the $25 Verizon deal to see if it’s any good.

We have the Verizon 5G. Works seamlessly vs. the cable provider that was unreliable and nearly 5x’s as expensive. Yes, there’s the risk of an outage…. but I can stick the “brick” in the car and drive to another area and use it there. Can’t do that with hardwire. The only flaw in my grand plan is that both my mobile phone and broadband are on the same carrier.

Nothing’s perfect.

I’m looking at 5G jet box hotspot from Verizon. The reviews are pretty horrible. Might want to check them out.

you must have a very patient life partner. mine wouldn’t stand for all those changes (banking,services etc)

I’m in the East Bay (north). What decent broadband supplier is only $25 a month? Thanks in advance. I use Comcast at $50 month to get 300 Mbps.

Yes, wait till you get the offer in the mail. Or google: cheapest broadband rates in city-name

If there is no competition on your street, if Comcast is it, that’s what you’ll pay.

Yes there’s too much capital out there. The supply side is limited, whether it’s new cars or houses or to some extent chips. AI is keeping demand of chips high and these are not cheap. Yes, some cars can be had for below MSRP, but it’s not a given. Consumer chip parts are rarely discounted as they used to be.

In the good times, if you either cross shopped or waited for some shopping season: you could have the deal you wanted. People wouldn’t pay sticker for even a custom ordered car. Now from Porsche to Toyota, things are nuts across the spectrum of prices.

My anecdotal go to has been seeing the trends on slickdeals dot net. There was a time when popular electronics were regularly go on sale. That’s not the case, though things have dramatically changes from last year. It is possible that the quality of slickdeals has gone down. But real life consumer experience matches the same.

The bottom line is, people are maximally employed and the real assets they park most of their wealth in are still left untouched. Some meme stocks exploding here and there doesn’t change anything. And QT has slowed the rate of change, but we are not on course.

Why do people keep claiming that there’s a shortage of housing? Were a bunch of homes destroyed over the past 3 years? Has there been a huge population increase over the past 3 years?

Census Bureau shows an increase of 2.7M from 2020 to 2023. From the data I see, an average of over 1 million new housing units have been completed each year since 2020. So that’s 2.7 million additional population and over 3 million new housing units during the same period. How is there a shortage?

It’s actually 1.41 million new housing units per year from 2018-2022. There was an increase in 2023.

So over 3 years, the population increased by 2.7M while over 4 million new housing units were completed. There’s an excess of 1.3M housing units over the past 3 years. Explain again how there’s a shortage of housing instead of constantly parroting what the RE industry keeps telling you.

There is absolutely no shortage of housing per se.

The distortion we see in housing market is not because of supply and demand but because if FeD doings.

That is what is odd. Supposedly the census included all people which would include undocumented immigrants. There has been 7 million new migrants over the past 3 years. 2.7 appears to be way off.

They require housing.

Yes, there has been housing units added but many are multi family rentals. Plus many new homes are built for rentals. This leads to a shortage of single family affordable homes. If you’re looking for a $700k or more house, there is Plenty of inventory out there.

Plus the myth that undocumented immigrants don’t buy houses is a myth. Maybe not right away but sometime in a couple of years. I have a rental house in a low income neighborhood. I see it all the time. They are the majority of the buyers in this neighborhood over the past 5 years.

I now of a guy and his business model is selling homes to undocumented immigrants.

Because for 10 years starting in 2008, not enough homes were built to cover demand once the panic ended.

At one point the new homes market was 4 million short. Its slowly coming back, but now the shortage is on the existing home side.

The millieniels and gen Z soon are all coming into their own. So yep each year there will be lots more buyers.

If they can afford at these prices and rates 😀

Wolf wrote:

“Could it be… that so much central bank liquidity was created during and before the pandemic that financial conditions cannot meaningfully tighten, despite the Fed’s tightening, until this liquidity gets burned up?”

My short answer is: I don’t think it works that way. The liquidity certainly lubricated financial conditions, but it was neither necessary nor sufficient to cause the asset bubble that we’re observing. The key to the inflation of the asset bubble (and the commensurate feeling of wealth that leads to consumption) is the underlying *belief* that investing in those assets is better than holding cash.

As the Fed tightens, people at the margin between having some surplus funds to invest and having to draw down on their investments, switch from one to the other. This effectively drops these people out of the investment cycle. When their investments run down completely they become impoverished. However, those who are able to retain some liquidity continue to buy and sell assets at ever increasing prices. I have an agent-based computer model that demonstrates exactly this. As the money supply tightens, asset prices take a dip, but then as liquidity is transferred from those who have to divest to those who are still able to invest, asset prices take off again.

The key to it all is the *belief* that holding the assets with inflating prices is better than holding cash. The vicious cycle will continue until that belief is given a reality check.