Looks like households have lots of fuel left to throw on inflation, if they’re in the mood.

By Wolf Richter for WOLF STREET.

What is the burden on households from servicing their debts and other financial obligations, in terms of their disposable income? That’s perhaps the most important debt measure, and the question we’re going to grapple with in a moment.

The pandemic-era policies left households flush with money, allowed them to catch up with past-dues, and allowed them to move delinquent debt into forbearance. They had free money by not having to make payments on mortgages, student loans, and rent. Then there were the PPP loans, over $800 billion of them. Delinquency rates, foreclosure rates, third-party collections, and bankruptcies all dropped to record lows. As a result, credit scores improved across the board. This was topped off by the blistering asset price inflation in stocks, bonds, real estate, cryptos, etc. But all of this is now getting more or less rapidly unwound.

Auto loan delinquencies in Q3 rose for the third quarter in a row, but are still lower than any time before the pandemic. Consumer bankruptcies remain near record lows in Q3; foreclosures, after ticking up for two quarters, fell again in Q3; and the number of consumers with third-party collections fell to a record low in Q3 (I discussed this in detail here).

Credit cards are being used as a universal payment method, and credit card “debt” includes balances that get paid off every month and never accrue interest. So credit card balances are more of a measure of transactions than of debt. And despite the surge in spending on travels this year, nearly all of which is purchased via credit cards, balances only went back to where they’d been three years ago (which I discussed in detail here).

So how much of a burden is this debt for households?

First a caveat. We’ll get into ratios in a moment. These are estimates by the Federal Reserve based on all kinds of aggregate data. The absolute ratios are not important, and whether or not they’re “realistic” or whatever for a particular household is not important either.

What is important is how the ratios move over time, whether they rise or fall, and where the breaking points were at which households started to buckle under their debts – for example during the employment crisis and mortgage crisis that accompanied the Financial Crisis.

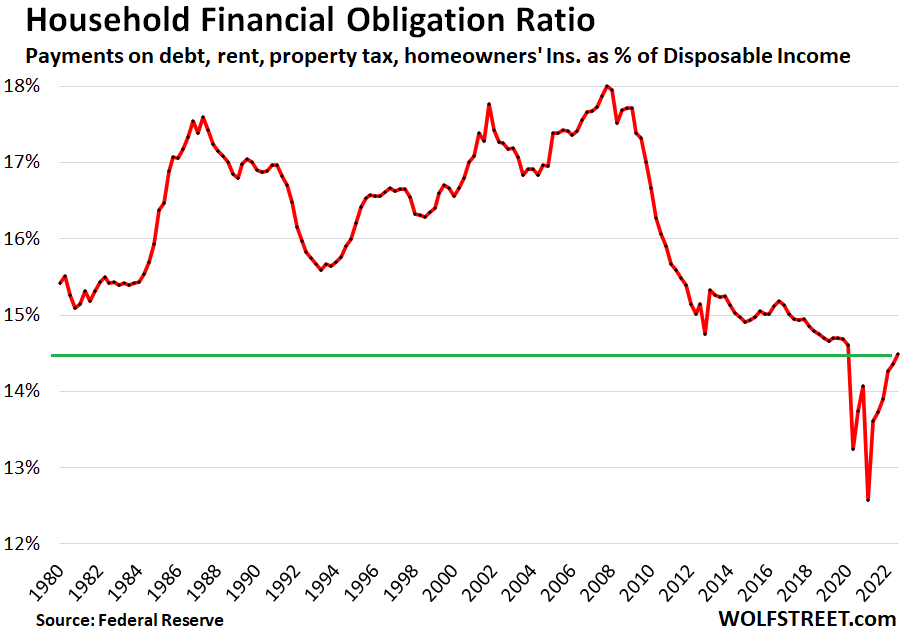

The household Financial Obligation Ratio (FOR) tracks total financial obligations as a percent of disposable income. These financial obligations are the broadest measure of burden and include not only payments on mortgages, credit cards, auto loans and leases, etc., but also rent payments, homeowners’ insurance, and property tax payments.

For revolving debt, such as credit cards, the Fed uses an estimate of the required minimum payments, rather than total balances because borrowers are only obligated to make that minimum payment.

The ratio of these financial obligations ticked up to 14.5% of disposable income in Q3, according to the Federal Reserve’s data released today. Disposable income is income from all sources minus payroll deductions.

During peak stimulus in Q1 2021, the Financial Obligation Ratio dropped to a record low of 12.6%. On the eve of the Financial Crisis, in Q3 2007, it hit 18%. Today’s reading, while up from the pandemic lows, is still below any pre-pandemic lows.

In other words, households are far less burdened by financial obligations, in terms of their income, than at any time going back to 1980, and are therefore less likely to get into the kind of trouble they got into during the Financial Crisis, as long as jobs are holding up.

Jobs... If there is an unemployment crisis, as there was during the Financial Crisis, the disposable income of millions of people plunges to the level of unemployment benefits, and the burden of debt payments becomes insurmountable for many households. But this is still the weirdest job market ever, and a very hot job market, with surging pay, where laid-off workers are still quickly absorbed by other employers. And so far, so good.

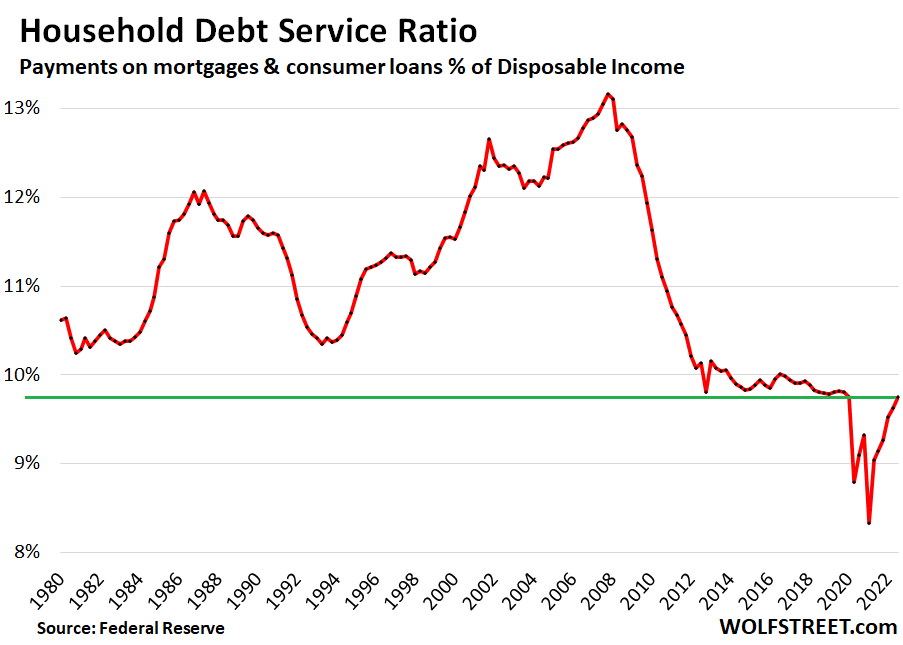

The household Debt Service Ratio (DSR) is narrower than the FOR and only tracks payments on mortgages and consumer loans (payments on auto loans and minimum required payments on revolving credit, such as credit cards and personal loans) as a percent of disposable income.

In Q3, the DSR ticked up to 9.8%, matching the previous record lows in 2019. On the eve of the Financial Crisis, in Q3 2007 through Q1 2008, the ratio had exceeded 13%:

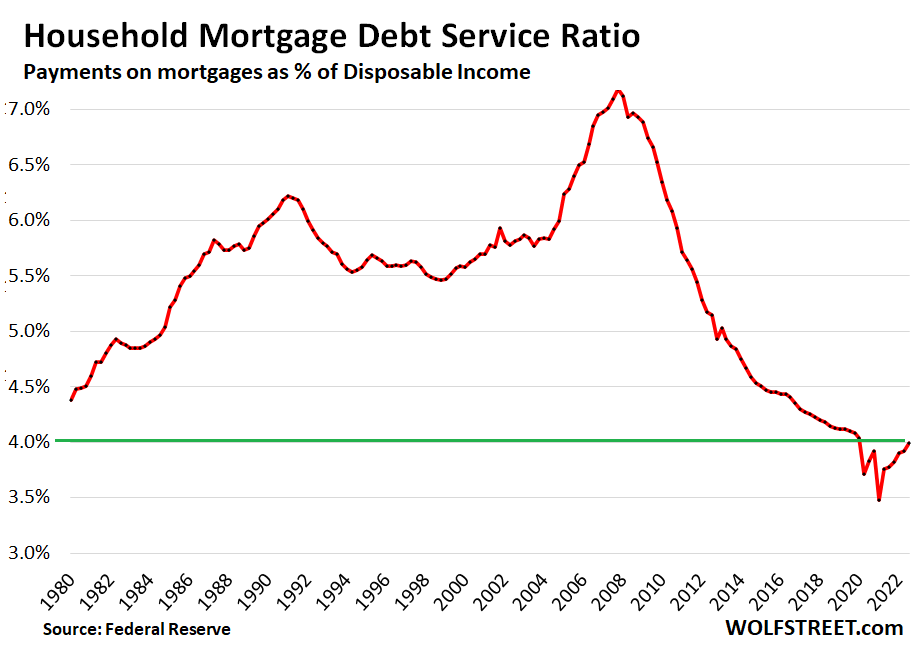

The Mortgage Debt Service Ratio tracks mortgage payments as percent of disposable income. Roughly one-third of homeowners don’t have a mortgage. Another big bunch of homeowners bought their home many years ago at much lower prices and have relatively low mortgage payments. That has always been the case.

What we have had in recent years is a huge spike in home prices, and so a big increase in the size of new mortgages, and now the spike in mortgage interest rates. People who recently bought their home and financed it carry a much higher burden than those who’d bought it a long time ago.

But wait… In mid-2020, the mortgage forbearance programs started, when participating households suddenly had no mortgage payments until they exited the program. And this sudden disappearance of mortgage payments due to forbearance caused the mortgage DSR to plunge from already record lows in 2019. And now, homeowners have mostly exited those programs, and the mortgage DSR is getting back to normal.

The mortgage DSR rose to 4.0% of disposable income, which is still lower than any time before the pandemic:

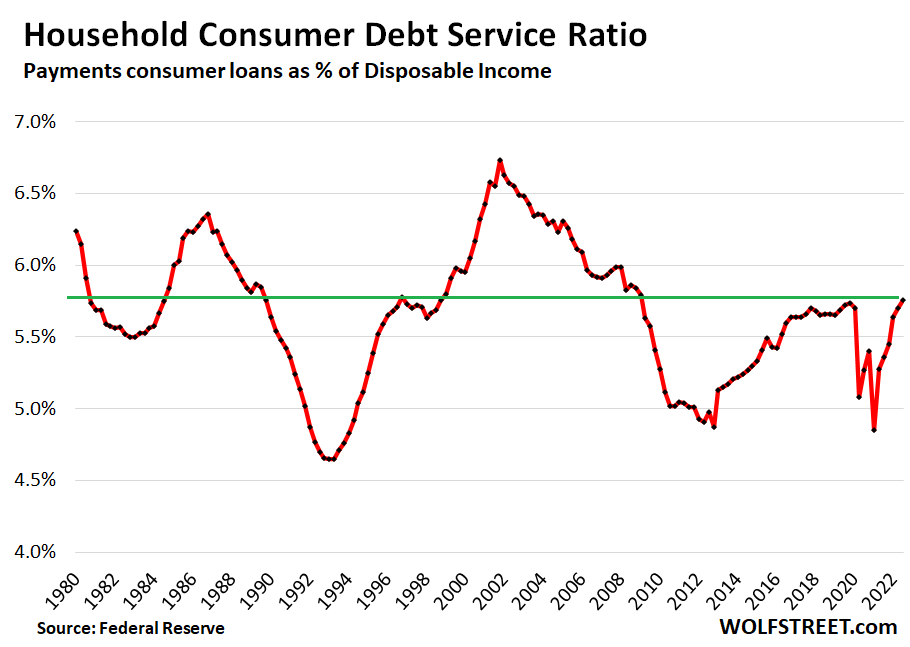

The Consumer Debt Service Ratio tracks the minimum required payments of revolving credit, such as credit cards and personal loans, along with the non-revolving forms of consumer credit, such as auto loans.

The ratio rose to 5.8%, just a hair above where it had been in 2019, and somewhere in the middle of the historic range, amid ballooning auto loan balances due to massive price increases of new and used vehicles. In addition to that spike in prices in 2020 and 2021, there are the higher interest rates that have phased in this year.

So what we’re seeing here is that the overall Financial Obligations Ratio and the Debt Service Ratio are normalizing at historically low levels, despite some pressures from vehicle loans, following the craziest period ever.

In other words, households have lots of room left, along with rapidly growing incomes, that allow them to carry higher debt loads if they so choose. They’re far from being “tapped out,” but instead have lots of fuel left to throw on inflation, if they’re in the mood.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Encouraging news but with all the manipulation (economic and psychological) I am not willing to take this as predictive. People act and react largely as they’re instructed to do. Let’s do this again in 3-6 months and see what changes.

I’m going to do this quarterly from now on so that we’ll see where this is going.

My bet is that the change will be brought by layoffs only. These will be forced by investors as revenues and profits will drop significantly. Why I believe this will happen is because of quality of our business leaders, who are still expanding in face of inevitable slowdown, believing in a Fed Pivot fantasy.

These corporations are ill-prepared to take on the economic challenges, so end result will be very painful. E.g. Auto companies expanding their sales and monitoring departments while cutting back on manufacturing as unit sales decrease while price per unit inflates significantly.

Typo: Sales and monitoring departments => sales and marketing departments

VP of “Sales and monitoring”? Epic!!

Look for the pink slips to start flying during or after the next big down leg in stocks. The decline hasn’t bene large enough for the average in aggregate.

It’s been covered on this site but limited so far.

Unemployment is still very low 3.7% and corporations have record profits.

Layoffs won’t be happening like in 2008.

Apple, that’s what they said in 2007, and it was true then as well. But we still got a crash in 2008.

Apple, they also have record debt. Debt that will have to be refinanced at much higher rates.

“Sales and Virtue Signaling” departments. In my 70 years, never before have I seen such a departure from manufacturing and selling a great core product as in auto industry. Not just them however.

How do corporate boards justify multi millions on this non core stuff while their products become mere commodities, almost indistinguishable from each other absent their name plates.

Are we now seeing the results of business academia’s woke products in the board rooms? More capital allocated to “messages” than products? Who can out woke the other guys is a road to bankruptcy and oblivion.

Even their ads barely show the vehicles they produce. Instead we have “stories” and smiling faces relaxing in some “sanctuary” with heated and massaging seats while it parks itself. Portrayals of narcissistic people hiding from the real world.

Guess its back to my corner now.

HaHa- “woke” vehicle ads. Even the mighty Ram ad agency switched from “guts and glory” to people who look out the Ram window and “notice the leaves are turning color”.

Cracks my ass up.

If that’s all “woke” means, then it’s hardly an insult as used on Fox, just means realizing people are different…..big deal.

Guess I’m woke, so am I on the road to oblivion? Should I demand more guts and glory to save the world, GB?

“These are estimates by the Federal Reserve based on all kinds of aggregate data.”

You mean the same people who said inflation was transitory?

Didn’t the BLS just come out and revise down 1M jobs?

Let’s not be surprised these ratios “suddenly” tick up to concerning levels if & when we get to 270K initial jobless claims next year.

“Didn’t the BLS just come out and revise down 1M jobs?”

No it didn’t. The Philadelphia Fed came out with a new algo that tries to predict quarterly the future adjustment that the BLS does annually. That algo has never been tested by reality. They just started doing it this year. Wouldn’t surprise me if their algo is screwed up. But it sure got a lot press on ZH and other pivot mongers.

The private sector ADP employment report has been strong ALL YEAR. Every other employment or unemployment report has been strong all year. You people are going nuts on me over this ZH nonsense. I’m so unbelievably tired of people dragging this BS into here. If you step into some BS out there, don’t wipe your boots off on my rug.

The only way to win is to not play the game.

Give it some time when money gets tight the debt load increases and anyone who has been riding on bold tires will be on the side of the road SOL.

…Damon-brand crypto-coin wheels ‘n tires???…

may we all find a better day.

As many of us predicted…

The Show begins…

Great article as it beings in the Greater Toronto Area – one of the biggest FOMO lov’in areas in the World…

(Go Long Popcorn and Butter)

Watch.. everyone will start squeeeeeling for “Bailouts” and lots and lots of crying scenes on the media…

This is a great website to watch from as well…

Read this carefully and look at the numbers…

Some Financial Institution actually lent these wankers money…

“The only way to win…”: Which raises the serious question, What if you had simply played the GSR fluctuations over time with the goal of increasing total ounces regardless of prices in short spans? That is, staying only in cash/gold/silver positions and moving at the right point in trends. Does Wolf have any thoughts on this beyond what he has already written? (Waiting to get hit over the head with the barrage.😹)

‘regardless of prices’, ‘moving at the right point in trends’.

Quite the plan. No thanks!

Yes, if the GSR dropped rapidly you might dump a silver position, ignoring the increasing price, in order to trade for more ounces of gold. The people who buy into increasing prices become the bagholders, not you. You might have periods of holding in cash before buying the other metal position, but you are looking for a reversal trend in the ratio. There are cost considerations, but that’s the trading game. If you had been dumping gold a while back and moving into silver, you’d now be dumping silver as the GSR dropped back toward 76 (now below that). The point being, to gain more ounces because the price eventually rises long term and is not the concern in the immediate. You just can’t panick over prices in the short term. Again, the costs of movement are your primary problem…and I’m not talking about pretty coins or Silver Surfer comic books.

Wolf…

Have you shown a chart of the wealth locked up in those who are on the property ladder at one level or another?

Think of the Spectrum…

One person bought their first home 25 years ago, and added over the years.. lets say they own a spread of properties.. 10 or more..

Purchased in the intervening years..

The next might be someone who has owned and upgraded the size of the Family home over 20 years…

Lets move to the other end…

This person suffered demented FOMO and purchased at very very high leverage..

Their First home… right at the peak…

Then you have the Renter Class…

Each of these large groups of people, are living in entirely different

Economic worlds…

Some of these groups are sitting on a lot of Wealth and Credit..

They are very insulated from any downturn…

Folks have been doing some form of this for a long time: building wealth. Or not.

But yeah, the slope from the bottom has got a lot steeper. The Fed enabled a wonderful ride on credit for those who had a foothold and the focus to do it. That may be transitory. It was after the Gilded Age and Depression (keynotes were major wars). Fashions change.

The Matthew effect, some call it: to those who have, more will be added. And vice versa. This is maybe the most fundamental argument in politics. Errors and all, Karl Marx was all about that.

Boomer alert. Not all generations had your advantages.

To quote SNL, “I got 5 houses? Good for me!”

come on

I like making my 15% + 2 points on flipper loans

Have you seen a drop in demand for your loans?

Let me guess, you’re one of the “soon to be sunk” Private Money Lenders who’s still lending on flips at 90% of purchase and 100% of repairs? Lol. I’m watching these types of guys getting ready to eat some serious shit, some already are. Can’t wait until they all sink, and sink hard. Everyone is a genius when the market is going up!

I liked your running a construction business stories better.

Wolf just delivered a load of Christmas coal to the FED pivot crowd.

New sales pitch: QT ending soon because of low bank reserves (or some such). Fed is forced to pivot.

And everyone is running around with their hair on fire claiming the economy is in free fall because of the fed. What a joke!

Yes, it’s funny how wishful thinking on Wall Street is now twisted into wishing for an economic catastrophe.

Exactly. Everyone is talking their book. I’m noticing how gold/silver bugs are upset because their “hedge against inflation” will be hurt if the fed crushes inflation and continues QT.

How do you reconcile this with the potential of a housing crash? Looks like we have reached a permanently high plateau here , for those hoping to buy 50% lower.

Yeah, that’s the thing with Wall Street: they want the economy to tank so that the Fed will cut rates and start QE or whatever, to push up asset prices. But right now the Fed is doing the opposite and asset prices are tanking.

“Looks like we have reached a permanently high plateau here”

Ha I was just going to reference the famous Irving Fisher and his

“permanently high plateau” place in history.

(Right next to Jerome ” transitory” Powell ? )

Even Morningstar is on the pivot bandwagon now (2023).

“Initially, we expect the Fed will end its quantitative tightening policy of letting maturing bonds roll off its balance sheet. Then in the second half of the year, it will begin to cut the federal-funds rate.”

The Google says combined debt of USA (gov + corp + consumer) is 7.7 × GDP. That’s pretty darn high. Powell is going to find out exactly what real rate will roll the economy over.

I think this suggests a motive to allow relatively higher inflation (than 2%): look, everybody has a job, and (if the Fed only bends a bit, which is a push of a button) debt service is cheaper. I mean, Powell bent on “transitory,” so why couldn’t he flex (revise views, whatever label is attached) the other direction “a bit”? Suddenly he’s a credible Winston Churchill? Where is that pain threshold that shifts the policy, in truth? I think that’s what stock investors who are long are thinking.

OS:

So 7.7x23T is about 177 TRILLION in debt according to that estimate.

That IS a lot of debt, far damn shore, but even so a more or less ”known un known” eh,,,

How some ever,,, IMHO what WE the PEEDONs have to consider more carefully is the approximately $600 TRILLION to over $1,000,000,000,000.00 of paper AKA ”derivatives” out there somewhere, according to estimates I have read recently.

And it appears these paper products CAN be called and CAN cause various and sundry ”real” assets to crash???

Anyone knowing any more information about this??

We saw a little bit of that play out in Great Britain with derivatives leveraging up interest income til it went bad. I think the safest assets are those in your possession cash, gold and silver. Next is probably t-bills.

The further you get from there the more risk you take. Once you get outside the banking system to Wall Street loan products you better be the type that reads the prospectus through three times to try to find the landmines.

I was taught to own stocks and loan money to the government (not business) but not for more than 5 year duration to make sure you get paid back and in something worth having.

Not too sure what to make of this, sounds like a lot of resilience in the system good for company earnings et al, but not what the Fed would want to see. makes it a longer and harder job for them, probably means the US economy can take a bit more hammer. As Wellington said at Waterloo “this is will take careful timing”.

First thought is, this is not the worst of all worlds. I think the pre-2008 consumer (and economy) had a much more delusional, euphoric, financially weak underpinning. That has been tamped down some by the Fed over a well-orchestrated year (IMO). We didn’t just blissfully sail off the 2008 cliff. There’s always a black swan possible, but the thing is, by nature that is wildly unpredictable, i.e., invisible. Until it’s not. I still have a slice of portfolio for that.

@ phleep –

“I think the pre-2008 consumer (and economy) had a much more delusional, euphoric, financially weak underpinning.”

———————————————-

Why? Do you have any numbers to support this?

Reading the WSJ daily I haven’t seen any talk of companies hiring left and right lately. It is talk of layoffs left and right instead. Rather than the unemployment rate (that doesn’t count those unemployed and not looking for a job) I would rather see the percentage of the workforce employed for a more realistic view of employment in the US of A.

The problem is the workforce, and everyone knows it’s the problem. Several million people have refused to rejoin it. There are a bunch of fairly well-documented reasons for that, the biggest being “excess retirements,” meaning a lot more people retired than would normally have been the case. This also involves rampant ageism that seems to be worse than before.

Labor shortages are still all over the news: NPR just had a big thing about hotel staff shortages. The other day, there was a big thing about teacher shortages. Healthcare workers have gone on strike to protest staff shortages… this stuff is ALL OVER the news. If you didn’t see it, it’s because you don’t want to see it.

The shortages have caused businesses to further innovate to deal with it. Like McDonald’s the customer places his own order and prepares his own beverage. The have automated beverage machine for drive thru. Once the job gets automated, that job is gone forever.

In theory price should close the gap between labor supply and demand, but things are always a little messy in our American style economic system. People have a voice in politics to push back on pure market forces. Every year is an adventure.

McDonalds has invented the automat.

Labor shortages are a short term anomaly. There are simply not very many people who are truly financially independent enough to stop working permanently even among the retired. Especially in a high inflation environment. About 22% of people over 65 are still working despite being eligible for Social Security.

Even of those who do manage to remain retired, most burn through most or all of their wealth before they pass away. That is the way the system is designed.

I wonder how it all fits together geographically. There seems to have been a huge exodus of working people where I live and in all of coastal California. Even police and doctors are very difficult to attract, let alone gas station attendants etc – many shortages.

The main reason given by people wanting to work here and the people who would hire them is the cost of living, particularly housing. People who want to move here to work can not afford to. The calls out to hire people in one resort town in particular are increasingly desperate.

So, the people who have moved from here must have moved *somewhere*. So it stands to reason there must be places where the labor pool is bigger than the jobs offered? Unless a large percentage of those people are now homeless and not as able to look for much work- not many people want to hire the homeless..

cut welfare and you will get more job applicants

That doesn’t really square with the data. Prime age participation is near highs in the low 80’s which looking back further is well above anything prior to the 1980’s.

Wolf cites “excess retirements” and I’d further argue that retirements at any rate will be problematic as the prime age population currently sits at a low of 48% and is trending down.

In practical terms, their is no one left to hire, without structural changes to education/training/retirement to start bringing more people outside of the prime age into the workforce.

Walmart, Kroger, and the liquor distributor parking lots all packed to capacity yesterday. Self check out lines stretched to back of store. 4 man crew of young entrepreneurs out in neighborhood at noon today -18 degrees offering snow shoveling services for $40 per home. Wolf article makes perfect sense. Denver giving out $1,000 month to homeless and we have about 1500 new migrant arrivals. “People have habits, people have plans that they don’t change. “

Almost as though there were a major holiday coming up in the next few days.

Can everyday prices really go down? In my area during and after the GFC I was looking for a huge reduction in things like building products, home improvements, paver driveways, construction labor. What I found was things slowed down to a point many contractors and other businesses closed. For a while the remaining businesses were charging MORE to make up for the loss in volume. I tried to negotiate lower bids but they were not having any of that. As the crash slowed and was on the way to recovery pricing just seamed to stay at about what it was pre crash, no big decline? Is it wise to expect labor and materials to drop significantly with this coming crash or will the consumer be still healthy enough to afford the new pricing thus establishing the new normal. I must be crazy to think we will ever have any meaningful deflation in everyday stuff, only assets like stocks and real-estate taking the hit?

Can you expand on this “coming crash” you’re talking about?

We look like we have entered the anticipated housing correction-crash. It could be better or worse than 2008. Some say the homeowner is in a much better position than in 08 but any market that is over heated will correct to some degree.

“Crash” and “correct to some degree” are very different categories. I think equating them loses any meaning. Markets constantly “correct to some degree,” as does seismic activity or any variable. Crash means disaster with overwhelming side affects severely disruptive in in impact, scale and scope.

Many of us are biased to over-predict crashes or moves. The world has a weird way of smoothing most things.

In order for real deflation to occur, there must be more goods and services being produced than money. In a real crash, which is not what is happening now, you have massive money destruction due to loan defaults, bankruptcies, and asset devaluation.

The amount of money being destroyed offsets the amount of money the government is dumping into the economy. Money, as it used to be phrased in the Great Depression is hard to come by.

It is simply supply and demand. It is hard to imagine we will ever see deflation on that scale again, but it is possible. Many people were wiped out in the Great Depression because their banks were not insured, and they simply lost all the money in their accounts.

While banks are now backed by Federal insurance, that insurance does not prevent a bail in, should the government declare an emergency and decide it needs the assets of its citizens to bail itself out. That is what happened when it confiscated gold in the 30’s and there is no reason it could not happen again. That would take much of the money supply off the books, and increase the value of the dollar significantly. Be careful what you wish for…

Perhaps true…but don’t forget that today’s workers seem to be well armed, unlike in the 1930s…confiscation might not be the best of choices

Jdog…ever heard of antiques? The guv only went after monetarily used gold. You could keep your 14k cigarette case as long as they didn’t catch you trading for dental services. There are silver antiques much older than the Fed…the guv ain’t ordering you to turn them in for meltdown next week. You people need to qualify what form of metals you claim they have taken (actually it was purchased in an open window redemption). If you just want to scare people talk about whiskey, gunpowder, and tobacco…we’ve got plenty of intervention activity there.

@ Jdog

@Wolf

neither loan defaults nor bankruptcies destroy money.

Debt forgiveness, such as in bankruptcy court or restructuring, destroys assets (my debt is your asset)! If it’s your asset that gets destroyed, it’s your money that gets destroyed. Happens all the time.

Will this poor fellow EVER get his badly needed all paver driveway, or will he have to settle for asphalt, or even (god forbid), blue shale?

Time will tell.

Cool, looks like these numbers give Papa Powell all the ammos he need to keep hiking and may I suggest hike bigger and faster? Obviously American consumers still have plenty of money left, that QT mop isn’t soaking up all the loose money that well…time for the FED to upgrade it to the Shamwow instead if he wants to get to 2% target sometime this decade…

I wonder if this includes installment payments for purchases. For example, my Amazon card keeps offering to let me make six payments for purchases, instead of paying now. Other such debts are reportedly not listed in usual credit card debt measures.

Of course, Americans are not yet starving. However, remember that we can expect inflation to go on for years: it is too lucrative to the banksters and financiers (and their fellows and cronies, the other wealthiest 1%), because it reduces the real value of their customers-depositors’ bank deposits, wages of their employees, bondholders’ outstanding bonds held, etc., as the dollar’s value is reduced via inflation–WORLDWIDE.

Remember that: inflation is a benefit for the ultrarich WORLDWIDE to the extent they use the US dollar because through it their liabilities/expenses are reduced while they can pass on any real price increases actually suffered by their companies, gigantic farms in third-world countries, mines, banks, etc., to their consumers.

Your Amazon card debt is included in the green line, and it’s included in “consumer credit” numbers above.

> my Amazon card keeps offering to let me make six payments

Seems like regular business and sales, AMZ is just trying to siphon off some of those extra consumer cash reserves to themselves by luring in the (still solvent) buyer. They book the receivables and all looks good.

What Amazon is doing is “Buy Now Pay Later” (BNPL), which is a form of installment credit that has gotten hot with retailers recently. It’s everywhere, and it’s included in all the revolving credit data.

If he keeps turning the screws he is going to get the job done. It all works with a delay. The swindlers are starting to go belly up. Next in line will be those using margin.

He probably could stop at 4% and wait a couple of years and it might be enough as the rates bite, but he knows he can’t risk inflation getting out of control and have a good legacy.

If he wanted to be a tough guy, he should call a special meeting next week and raise rates another 3/4% to punch Congress in the nose about spending. In the big scheme of things waiting til next meeting will not matter much. He will just have to keep going a little longer than planned.

I suspect a lot of pain to new and old homeowners will be property tax hikes. Granted, its not a one size fits all, I highly doubt any local state government will skip out on their “fair” share of housing bubble.

In Chicago alone, people are dumbfounded, when they learn about their new reassessed taxes going anywhere 30%-50% higher.

Old homeowners get screwed, because they get reassessed based on comparable properties that are overpriced, new owners seem like they don’t care about property taxes. I remember stopping by townhome hosting open house earlier this year. Despite property taxes being $10,000 – it sold within a day…

“Old homeowners get screwed, because they get reassessed based on comparable properties that are overpriced”

Not in California.

Gotta love Prop 13..NIBYism at its best

What, we don’t want this place turned into Vegas-Macao in a day by some hot and horny developers, their political handmaidens and come-lately so-and-sos too dumb to have got here until such a late date? That’s a crime? California was a gem, of the world, of the universe, and still has a few shreds of that left, which these idiots want to erase. Go ruin someplace else in the name of your phony “progress.” And yeah, it’s progressives all over this scam. Just keep importing people with no end. Is that wise?

NOT in the flower state either HM!

Same guy got a cap on prop taxes though both legislatures or something, and for the same reason.

Folks kept losing their homes when next door McMansion increased their taxes, sometime to crazy levels doubling in a year, etc…

Friend had to go back to work years ago when his went from $3K to $12K in three years — at age 75…

Not exactly fair dinkum, eh???

My whole family would be out in the street if that madness had been allowed to continue, to subsidize (1) the rich consuming vast resources and (2) unwashed masses demanding handouts (and fronting subsidized offspring into the mess). So we would join the latter.

And yeah, I lived at my parents’ house through much of college, I wasn’t whining for my own house until I earned it, or demonizing anyone about it.

I don’t think they “don’t care about property taxes” so much as the $10,000 property tax bill is not real to them until they actually have to write that check the first time.

It’s a phenomenon that applies to all of us from time to time. We know something exists, but we don’t internalize it until we are directly confronted by it in a very personal way.

The data segmented by wealth distribution, income distribution, or a combination of both would be a lot more revealing.

(Yes, you’ve told me more affluent people have the bigger debts. I know that but the .01%, .1% and 1% who account for a disproportionate percent of total income usually have assets far above their debts. Remove them from the calculation and I’m confident the numbers increase considerably. Same idea for lower or slightly lower percentiles in the distribution.

As an example, years ago, I read that Larry Ellison of ORCL had a $2B personal loan, probably secured by his company stock. Since the article didn’t explain, I infer he did this to avoid paying capital gains taxes while potentially finding a way to write off the relatively modest interest expense for him given his net worth.)

THIS IS ABOUT WEALTH DISTRIBUTION.

Income distribution is an entirely different data set that is not compatible.

ONE TOPIC AT A TIME.

Assets and debts are detailed for the 0.1%, the next 40%, and the bottom 50%. All you have to do is read the article.

I know you said not to worry about the actual percentage, but what about what they are measuring? I must say that as someone with no debt, my rent “debt, rent, mortgage, property tax, homeowner’s insurance” is a very, very small portion of my monthly budget.

However, my childcare costs have gone up 15% since last year and every daycare has a waiting list. Right now we pay 2.5x more for our childcare, than for ALL household services and costs, including the HFOR. We have two under 5’s.

So sure, we have plenty of money leftover each month according to this metric, but only if we ignore the real world. I appreciate the point the article is making, and agree that we’re going to be fine so long as we all stay employed, but there isn’t much fat to trim in our budget and I don’t think we are too unusual in the crowd that has kids.

How everyone is going to stay employed is certainly something to ponder . With all the Cash still sloshing around and the Perhaps Mass layoffs coming ( possibly ) or Lesser but continued Layoffs both having similar effects . The fight is a many edged sword with the Inflation world on one side and the Pre Inflation world on the other, humm before and after.

Without the present induced economy just think we would not Have Hi Home Prices and Rental Costs or the Inflation like it is effecting everything . Many are Happy like Powell and Trump who In Cut Rates basically to make $$$ ( Not ours )

The Leftovers now are at hand 5% CD’s are available and Hi mortgage Rates as example, soon turning to to be Loss of Equity . Whats the light at the end of the Tunnel ? cheap foreclosed properties , New Government work programs ?

The layoffs are coming, i would argue that most large companies these days are like twitter before elon musk took the axe to many of those “jobs”. Virtual jobs for a virtual economy.

Elmo fired his CEO, CFO, CLO and thousands of programmers.

Inflation in services will not decline in meaningful way due to a shortage of workers and workers attempting to keep up an ongoing inflation. It will take a very high unemployment rate to bring wage inflation down. I just do not see that given the shortage of workers for most jobs.

100% agree in healthcare the shortages are incredible throughout the spectrum of medical assistants all the way up to surgeons. Everyone of them that has been around and made it through Covid stress either 1) jumped jobs for big pay increase 2) retired due to burnout and some level of financial stability due to asset appreciation ( Jan 22 timepoint). 3) quietly quit demanding salary increase from current employer of no less than 15-20%. Healthcare system’s fighting hard to keep and get employees. Private practices pretty much dead.

hmmmm you’d think if you had a life threatening pandemic that wasn’t as bad as advertised we’d have a glut of nurses and MDs now. Instead we have the opposite, almost like everything about 2020, along with the solutions to it (printing money at a scale that even shames 2008) was all about the finance system………..

At what point do you stop believing the “news” and start to trust your own eyes?

I mean it was so bad here we are two years later and people still don’t have to make any payments on their student loans. ;)

Betcha that helps with “services inflation”! At what point will the responsible people of this society say enough is enough? Has anyone else noticed that we must save the “worst” of us while punishing what used to be considered the “best” of us?

It’s strange out there as far as what people can and can’t afford. How stable is their job? Do they have a family to cover? Do they have a chronic health need? A family that can gamble and skip health insurance costs for a year or more has much higher spending power than one that can’t. Our health insurance costs for 2023 just came in at work. Employer covers half but $590 for one person per month and $1,972 for a family per month. A person who is Medicare age with a paid off house or a mortgage from a decade+ ago has more spending power. Someone in their 40’s with asthma or dependent on insulin who bought a house in the last 5 years could have a very rough time. Who can spend in the face of this inflation seems dependent on what sort of economic pocket they occupy. Some folks are doing ok and some are in a pretty bleak position. The part that is hard is it seems more dependent on age, health, gov’t subsidy or timing of asset purchases which are factors that are often only partially under any individual’s control. There seems to be too much manipulation of the knobs and levers of the overall economy to have any sort of level playing field and the rules keep getting changed. It seems like there is an effect like a rolling blackout except it is a rolling economic blackout that hits certain groups at different times and does serious damage to their wealth and prospects. The government subsidies act as aid or relief to these groups after they are hit but the entire thing seems pretty unstable as well as unsustainable.

A “person who is of Medicare age” pays close to the $590 per month for Medicare, a viable Medicare supplement, and their part D premium – just like you. Ask me how I know. Your employer provided insurance covers things Medicare does not. Most of our generic pharma is cheaper outside the Part D coverage (we have two different policies and the results are similar). Your drug coverage keeps paying. We have a “donut hole” where reimbursements drop. No dental. No vision. Transitioning to Medicare was an eye opener.

Virtually every generation has had the same challenges you outline..

Presently, geezers like us don’t need much. No need for more furniture, the latest fashion, and the like. Don’t need a Rolex, a Peloton, an E-Tron or Hellcat. As such, we aren’t feeding services inflation nor asset inflation as cheap money doesn’t influence our behavior. The demographic most loudly complaining about the issue are the primary drivers of the problem.

The rules are similar, contrary to popular belief. George Carlin pointed it out in his “it’s a big club and you ain’t in it” schtick decades ago. I’ve lived through a variety of economic and social gyrations. Probably the biggest change is there seems to be more pervasive grift, far less civility, and more propaganda passing for *news*.

We’ve gotten screwed on our income for 14 years because we’re primarily savers. How much did it cost us? Easily 6 figures. Waah! Waah! Boo hoo! No one threw a pity-party for us. The rules changed? Adapt. Life ain’t fair.

The truth is that most people have an out-go problem, not an in-come problem as many have eyes (or egos) bigger than their wallet.

There are big diffs within Medicare, I think depending on the market you are in. My Medicare Advantage has dental, vision, ears, covers all my meds, for $170/month all in. Covered all my medical issues to the last dime, so far. Only applies within this network, which is physically close, but I’m not traveling much.

There is a literal medical city of this provider half a mile away. But this is in the city.

Try lining up a heart transplant with your MA insurance.

Or even selecting your own specialists. Good luck!

Anthony A.,

A heart transplant when you’re of Medicare age??? Good lordie. You’re just enriching the PE-firm that owns the hospital with taxpayer money while you’re being tortured to death.

At least Kaiser isn’t a PE firm (I’m guessing that’s who the provider here is)

The way I look at it, there comes a point when your body tells you it’s time to go. And you go peacefully, instead of allowing it to be abused to transfer taxpayer money to PE firms.

I think you chose the worst possible example LOL

I think there might be a better example that might have made your point, possibly.

“The way I look at it, there comes a point when your body tells you it’s time to go.”

But is the body always the most honest, unbiased messenger?

I used to think the human brain was the most marvelous organ in the entire anatomy, until I realized which organ was telling me that.

LOL, yes, there’s that

Yeah, the example was extreme, but it jumped into my pea-sized brain and I was trigger-happy.

Wolf, my brother-in-law received a heart transplant under his Medicare and supplemental insurance at age 74 here in Houston at the Memorial Herman facility in downtown Houston. He is 83 now and doing quite well. Not everyone at that age will qualify, though as it depends on your health history.

Health history meaning no history of other issues like cancer, diabetes, etc, etc. His heart was failing and his wait time was only a few weeks. He got lucky.

A friend of my father’s received a heart transplant in his early-mid 60s. He died a couple of years ago, 20+ years after his transplant. I don’t recall the exact years now, but I do remember that he was going strong up until close to the end, and that he had his new heart for at least a decade when my father told me about the transplant. I would never have known otherwise.

As you say, it all depends on the individual. Some 80 year olds are running marathons; some 60 year olds are in nursing homes and will never leave under their own power.

1) If household debt service is so low why people are so depressed.

2) If income is much higher than debt service retained earnings should be in the trillions.

3) People are depressed because their financial superstars – AAPL, AMZN,

MSFT, GOOGL – are injured, down 38% since Nov 2021, hugging the lows for eight months, since May. The bond market massacre is shocking and now real estate failed to perform.

4) People are depressed, but VIX don’t care.

5) For some people marriage and employment are form of slavery. Offer them whatever, they don’t care. They are out of work since LBJ.

1), 3) Depressed: my guess is, folks are addicted to cheap gratifications that are detached from nature, poor substitutes for the world’s real innate healthy beauty, and instead just digitally goosing their spent dopamine glands.

2) Maybe low labor participation makes average retained earnings lower?

4) VIX is interesting. The ride to the bottom has been relatively smooth. My VIX-sensitive investments paid well in mid-year, but have sucked lately. Too much benign news is in the mix. This seems according to Fed’s hopes.

5) Real freedom, non-slavery, is a bracing tonic, but has its price. The grass is greener across the fence. I accept that steep price, and rejoice in it, but many folks I know are temperamentally much more like dogs: group, herd or pack animals. That takes a huge investment in schmoozing and forebearing.

5A)

The window from my cell faces north. Two fat robins hop upon patches of newly-seeded grass along the sidewalk to my living unit. The birds are oblivious they set up shop in a prison. They are free to fly over the fence.

Like breathing, the need for freedom is innate; our bodies are made to move, our minds are programmed to learn, and our hearts are constantly contracting and expanding. Freedom is expansion and joy.

My freedom lives beyond walls, beyond flag, beyond expectation. I’ve learned real freedom is in the mind and heart. It is there I focus my attention.

-Elizabeth Hawes

@ Michael Engel –

“1) If household debt service is so low why people are so depressed.

2) If income is much higher than debt service retained earnings should be in the trillions.”

———————————————-

coherent points

Sorry Sir,

why would we?

What is the burden on households from servicing their debts and other financial obligations, in terms of their disposable income?

I grapple this from being amused by the simplicity yet also sorrow.

I don’t want to toot the pike kids horns but it’s been a long time a coming.

-shandy

Gold & silver might be the winning asset for the next decade. Real Assets will outperform Financial Assets. The debt ceiling is up by $1.7T, up 5.6%, mostly for defense. New $10,000 stimulus checks are coming to the gold diggers.

Hey Wolf,

Love your content and am thankful for it.

$1.8 Trillion omnibus passed tonight.

I may not know enough about inflation. But do you think Powell grunts when things like that are passed, and in turn factors it in with the rate setting …?

I feel like congress has made themselves immune to inflation and it’s kind of scary.

In the UK at least the pound reacted to unfunded debt. But the US just keeps the faucet open.

Thoughts I’m just very confused?

You’re not confused at all :-]

The problem is that there is always someone willing to outbid any fiscally conservative Congress person for the seat at the next election by promising more goodies paid for with deficit spending.

So even any principled people in Congress who start out with the intent on getting our fiscal house in order eventually turn to other things when they realize that they’re fighting a losing battle.

If you accepted “donations” to first get elected, then you were never principled to begin with. It costs nothing to talk to people about their future and freedoms. Of course you might have to find a tree stump that ain’t owned by some private entity or controlled by a government agency that thinks they know better than you the meaning of “free speech”…a hell of a lot of that nowdays.

1) Oil is old. Use it as long as it last. The glut is gone, only shortages.

2) Europe imported more LNG than ever. China replaced coal with US LNG. India was first to import LNG from US. India signed a new $2.5B LNG import from US.

3) Japan demand for LNG will grow by 50% in the next decade.

4) Norway became a wholesaler for US LNG.

5) Demand for US weapons and energy is growing. King dollar rule.

6) China have 14 land border neighbors. They flare a regional war with each of them, one at a time, risk free, to cover their own domestic problems.

7) China must have an enemy. Without one they die. They like it so much they asked for more : Japan, Taiwan, S. Korea, South China Sea, their pearl necklace, the Silk Road and Gwadar Baluchistan. The people of Baluchistan ordered 500 Chinese in Gwadar to leave at once, this weekend. That’s first.

8) The Eagle hunt a Rabbit down below.

-Japan is restarting its nuclear reactors.

-Germany abandoned plans to close coal mines. They have been demolishing villages and moving windmills to get to the coal seams.

-Global coal consumption is forecast to increase by 1.2% in 2022.

-World oil production is near 100 million barrels per day.

-They may not complain about global warming when it is near record cold. They will wait until hurricane season.

-There was a 5.4 magnitude earthquake in Midland, TX the other day. The epicenter was in the world’s second largest oil field.

This is the clearest explanation of “pay whatever” mentality and entrenched inflationary expectations on the web. I hope the Fed is reading, so they stop quaking in their boots, and actually address inflation.

No doubt folks are in great shape financially. The one fly in the ointment is the slope of the line from the pandemic bottom in the various charts. If that trend continues, eventually there will be problems, albeit that could take a while. Still, the ubiquitous steepness of the slope across the various indicators is concerning. The question is – is it simply just a mirror image recovery of the pandemic drop or a trend that will continue into the future at the same rate now that most indicators have recovered to their pre-pandemic levels.

Completely agree. The optimistic view is that the current situation is good, the pessimistic view is that the current trend is bad. So the question is, when and where do the worsening trends stabilize or improve?

1) The 100Y inflation downtrend line : May 1920 to Mar 1947 and to

Mar 1980 highs. June 2022 might be an aberration. Inflation might return to it’s historical boundaries : zero to 7%.

2) We are deeply divided nation. NYC became the most expensive city

in the world to live in for the first time. Tel Aviv, last year sleaze meter winner, dropped to #2.

3) Houston is far below. Our open borders flooded Texas and Arizona. Only

eight thousands illegal immigrants arrived in NYC. The flood of unskilled labor from all over the world stayed in the South. Business with access to a large supply of cheap labor can produce more, while cutting prices.

4) US south have ample energy, the North is deprived. US national interest is to provide energy to the suffering people in Europe, Asia and China.

5) The south became our industrial hub. Automation is a good thing. With

fewer people businesses can produce more. With automation we can

rejuvenate old industries that died fifty years ago, to replace China and Vietnam.

6) Industrial workers higher real wages can support the service sector.

7) A crime wave render NYC transportation system useless. Dead end job laborers cannot afford to drive and park in the city to avoid the clogged subway arteries. NYC might drop from #1 back to 1975/78.

The elephant in the room is demographics and imigration.

Imigration is getting harder and harder but the demand of cheap labour for services remains. There is no lever the Fed can pull to change the underlaying reality.

With the new geopolotical tensions and many companies trying to move manufacturing back to the US as well as federal subsidies to manufacture cars, batteries, chips and so on in the US the labour demand can’t be filled domestically.

Higher pay will just move people but especially in services vacancies will remain. People will get improved conditions and I’m glad but there needs to be a bit more strategic planning.

I just want to point out that immigration for “cheap labor” is ultimately a terrible deal for Americans.

Suppose a migrant enters the United States and is willing to work for $10/hour instead of $20/hour. Over a year, that’s a $20,000 “savings” in labor costs.

But that same migrant will likely have several kids, all of whom will need education in public schools, and possibly expensive ESL services. In many cities, public school kids cost $20,000 or more per year.

That same migrant (and family) will also likely get “free” health care from clinics and emergency rooms. Some of it will be reimbursed by Medicaid (that is, by U.S. taxpayers) and some will not.

And this isn’t even including the cost of crime by migrants, WIC, food stamps (which citizen children are entitled to even if the parent is not) and so forth.

So people shouldn’t delude themselves into thinking that “cheap” labor is a good deal for us. It’s not. It’s a good deal for the employers only, and they shove all of the costs onto society as a whole.

Point 1: Last line is somewhat correct when you consider that shoving the costs of transportation (via the auto) onto the backs of workers played out fine for employers in the last hundred years. (Ignoring the fact that that too has created a societal costs spillover.) And that’s a big part of why we never built any high speed monorail networks instead if a handfull of exspensive frickin’ tubes under the ground…the future sewer systems of America!

Point 2: You totally are ignoring the runaway costs that are incurred by rampant land speculative practices which make it impossible for that Citizen/Resident worker to compete in the wage market. Any way you work this out, the winnings are going to the moneymen behind the land schemes…that’s your real problem and immigration of legals or illegals is only secondary to that at best.

It’s too bad the last Prez couldn’t make that point with some subtlety. But that aint his strong point. It all got muddled and murky with other impinging weirdness.

I worry now that there could be a bigger level of immigration surge, in coming conditions. Whatever we feel about immigration, I think stronger border infrastructure is a priority.

Even at $20/hr still the same issues. Your comment points out that immigration reform is also tied to other reforms. Healthcare reform, welfare reform, and education reform. Possibly birthright citizenship re-examination.

Agree 100% , and it is worse in Canada as the likes of low paying employers like Starbucks repatriate earnings back to the USA . Income taxes on $15/ hr wage barely cover the per capita cost of health care in this country .

In addition I would love to know what we do in 20 years when AI eliminates these jobs.

Thanks Einhal for your post.

I may have missed this but I am wondering if there is chart showing when debt will have to be rolled over. i.e. by duration 3 months, 5-years, 10-year, 30-years

With about $93T of outstanding debt amongst Government, Business and Personal it could get dicey with increasing debt service costs.

I just met someone this week who put 5% down on multiple Condos in Northwest major metropolitan market with mortgage 3%, he would buy one and rent it out after a year in order to purchase his next condo wash and repeat, recently put down 25% on a house in SoCal with mortgage at 3% and was boasting of the low mortgage and how he managed to buy before the mortgage went up, renting out other rooms in his house to pay for the home and build “cash flow”. I was shocked he had such little equity in his homes but he works for top 3 big tech company so he figures he can build wealth and tells me homes move up and down in price so if you’re going to live somewhere long term then you just don’t need to sell if market is down… but what if you go underwater on everything and lose your job? He doesn’t fear this…

Tell me this is somehow different than the scene in the big short movie with the stripper… Cause I thought he was joking at first but he flat out wasn’t. I mean strippers make good money too but in a downturn… So as to people saying what bubble its different this time? Dear God, maybe he’s an anomaly and one case, but I was thinking the whole time this can’t be real… I mean that stripper in big short was supposed to be a caricature wasn’t it?

If the rates hadn’t increased, I would be tempted to do as he did at this point. No wonder there is real estate inflation… Now, I’m hoping for mass layoffs and feel a little bad about that because people will lose their jobs but I also have to look out for me, and can’t help but feel Fed Reserve is encouraging risky behavior STILL…

If employment stays this low, there won’t be an issue but if there is unemployment, I think the real estate bubble might crash harder than people think although the foreclosures will take time. I mean the guy has less than 20% equity on all of his homes and condos… Fixed rate though so without unemployment, he wins I guess… Fed Reserve still failing to curb this behavior…

He’s not high earning tech aka not a software engineer. He’s a middle level salary worker. Fed Reserve needs to go up 100 bps a few months in a row and just kill this kind of risk taking behavior but instead we have mass inflation eating into my savings instead.

And here I’m sitting on all cash/treasuries/cds/high yield savings in maximum defensive position with limited exposure to stock market and real estate (renting) to wait for 2023 layoffs and recession to reprice a bit… 2022 having proven everyone on Wolf street right in regards to the market … Fed Reserve is thieving from everyone with sense and giving money to people with no sense. Once everyone holding out surrenders and commits to live YOLO for today, then the market crashes and people lose their livelihoods. They are thieves, thieves. Banks sitting on homes without foreclosing as to keep their values high because it backs a massive number of loans… Bailouts. 1.7 trillion dollar spending bills where nobody knows whats in them… I missed the low interest money making train that I should have been on… and the only way to catch up to the risk taking guy now is to work harder. God i hate the fed…

I owned condos out in Edmonton, Alberta with no mortgages and still ran negative cash flows yearly with no special assessments. It’s possible to lose big.

“And here I’m sitting on all cash/treasuries/cds/high yield savings in maximum defensive position”.

Sorry, but your position is not defensive. It is speculative. You should always maintain at least a 20% portfolio allocation to stocks, gold, RE, etc. to protect your portfolio against inflationary spikes. Betting your entire wad on deflation is highly speculative, and such speculation can cost you a lot of money. We’ll be witnessing 20% inflation in three years. People that bought long-term bonds in 2021 are down 30-40%. When non-elected central bank leaders with questionable motives, outdated models, and a low political pain thresholds run monetary policy, you simply cannot expect inflation to be under control on a consistent basis.

Don’t believe me? Read Benjamin Graham.

Alternatively, just live your life; love your dog and don’t kick your wife.

All systems fail, eventually.

Great advice, thanks for posting.

He didn’t say the duration of those treasuries.

Equities clearly aren’t protecting anyone from anything this year, and it seems unlikely to change in the first half of ’23 as well.

In order to bring down inflation people should have to pay back all their stimulus money with interest on top of it. To this day I still can’t believe people got free money. Under a worldwide dictatorship no one would have received anything. The whole idea is let the people starve or starve and freeze to death because they didn’t prepare for an emergency like Covid-19.

Hungry people with access to guns?

What could go wrong??

the nerve of those not well-born to be unprepared

The most horrific effects of COVID-19 will be the economic pain caused by pandemic stimulus withdrawal.

As with anything, trying to group the entire population into a single group and make assumptions about the economy based on that is problematic.

With 40%+ of credit cards carrying a balance, and 15% being more than $5000, credit card transactions do indicate that at least the lower tiers of wealth are using high interest cards as a major source of financing. No one pays interest in the high teens unless they have to.

Credit is never a problem in high employment environments, it is only when the employment market begins to tighten that you begin to see the repercussions. The construction industry is the canary in the coal mine when it comes to employment, and with home-builders struggling to offload inventory, they will be very reluctant to start new projects. That means come spring time, when many of the construction workers who collect unemployment during winter will return, they find few to no projects hiring. That will force them to seek employment in other areas, increasing competition for jobs elsewhere. This slowdown will also effect all the people in construction support industries from truck drivers, to equipment operators, to factory workers who make everything from paint to door knobs to kitchen appliances. The effects of a housing slump are huge, and will be felt by the entire economy in 2023. Credit statistics will look much different then.

From Wolf’s article: “The pandemic-era policies left households flush with money, allowed them to catch up with past-dues, and allowed them to move delinquent debt into forbearance.”

Man, having paid taxes for 45 years and now retired, I don’t get it. I must have missed the boat on a lot of this free cash deal. The couple of payments the Gov sent, but not requested, are LONG GONE. And since then, inflation is eating up the retirement income too.

Who still has any of the Gov payments left for covering expenses?

Those who never needed it to begin with simply deposited it and it is counted as not spent, and potentially available to be spent. Personally, I believe if it is not spent by now, it is not going to be, at least not on goods or services.

One thing to ponder in this strong consumer construct, is the amount of disposable income being utilized in terms of speculative endeavors. The last 20 years have been virtually low interest easy money, with huge asset gains made in super low inflation environment. That era will be somewhat tested in 2023 as super strong consumers face challenges they’ve never experienced. As stocks tumble slowly downward and the house ATM stops spitting out profit, the growth engine is going to impact savings rates, consumption and speculation. Disposable income is going to become far more scarce sooner than people realize.

What the past 20 years have been if borrowing from the future to pay for unearned standards of living. The folly was never thinking the bill would come due….

@ Wolf –

Being in California, it is hard to relate to these type of articles, where an 18% Total Financial Obligations to Disposable income ratio is considered high. Most Californians would be living easy with that kind of ratio.

Rent alone approaches 50% for many Los Angeles residents.

Articles like this are not stories about the plight of one downtrodden household. There are lots of Californians who are IMMENSELY RICH. They’re part of the totals too. There are lots of Californians who are very well off. They have no debts, they have lots of income and lots of assets… Median household income in San Francisco is $126K. That’s the median — meaning half of SF households make over $126k!

The 1% by wealth of US households comprise 3.3 million households!

The 10%, who are still very rich, comprise 33 million households.

The next 40% have an average household wealth of $768,000.

Lots of Americans are very well off. People forget that. It’s the bottom 50% that is not well off.

https://wolfstreet.com/2022/12/21/fed-tightening-reduces-horrendous-wealth-disparity-that-qe-and-interest-rate-repression-have-wrought-fed-data/

Corporate Debt is resetting 2023-2025 to the tune of $1T per year. Debt service x2, x3 up.