Powell said many times consumers can take tightening because loan distress is at historic lows. What consumers cannot take for long is raging inflation.

By Wolf Richter for WOLF STREET.

We’ll start with consumer bankruptcies because that’s where credit troubles, if they cannot be resolved, often end up. Then we’ll look at foreclosures, third-party collections, and delinquencies. What emerges is the picture of a consumer, still flush with pandemic money and rising incomes.

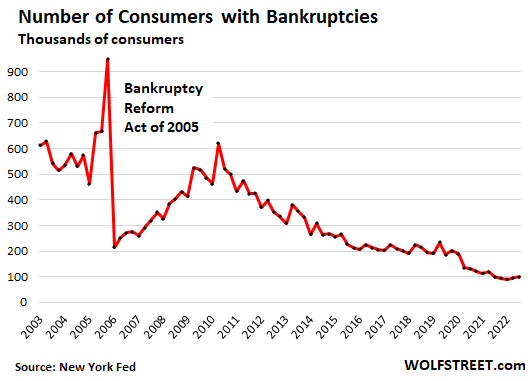

Consumer bankruptcies had plunged when the free money arrived, including the PPP loans, along with the various forbearance programs and the eviction bans. And the number of consumers with bankruptcies continued to drop to historic lows and have been hobbling along those historic lows for the last year-and-a-half.

In the third quarter, the number of consumers with bankruptcies inched up a tad from the second quarter, to 99,000, but was still below a year ago, according to data from the New York Fed’s Household Debt and Credit Report, and half of the already low levels of the Good Times (around 200,000):

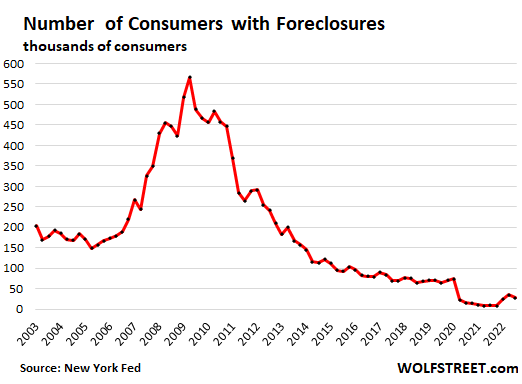

Foreclosures dipped in the third quarter and have been at ultra-historic lows since the mortgage forbearance programs, where delinquent mortgages were put on ice, and no longer counted as delinquent. Most of the borrowers have now exited the forbearance programs, either by having the mortgage modified in some way, or by having sold the home and paid off the mortgage, which was easily possible amid the pandemic spike of home prices. The free pandemic money also helped.

Foreclosures, after ticking up for two quarters, ticked down again in Q3 to just 28,500 mortgages with foreclosures, thereby nixing the beginnings of a trend that had been forming. During the Good Times before the pandemic, there were about 70,000 mortgages with foreclosures, more than double the current number:

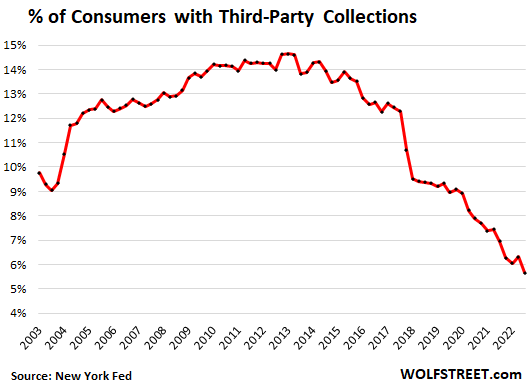

The portion of Consumers with third-party collections dropped to a new historic low in Q3, to just 5.7%, after a slight uptick in Q2. Third-party collections are registered on a consumer’s credit report when a lender sold a seriously delinquent account for cents on the dollar to a collection agency which will then hound the defaulter for some amount larger than what it had paid for:

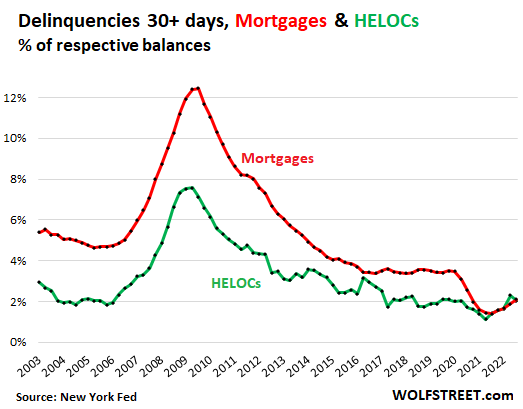

Mortgage and HELOC delinquencies remained near historic lows. The 30-day-plus delinquency rate of mortgages ticked up to 2.1% (red line in the chart below), which was still far lower than before the pandemic. During the Good Times before Housing Bust 1, in 2005, the delinquency rate was 4.7%. During the Good Times before the pandemic, the delinquency rate was around 3.5%.

The 30-day-plus delinquency rate of HELOCs ticked down to 2.0%. This is right in line with the Good Times:

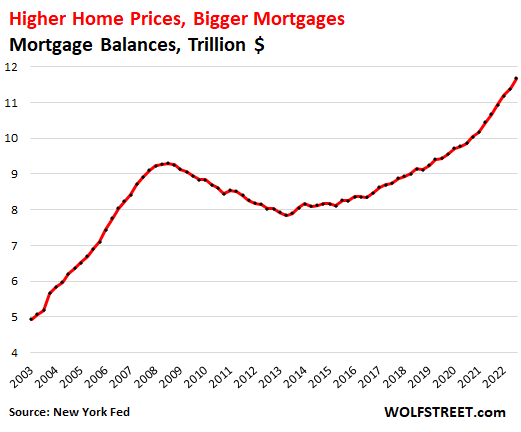

Mortgage balances have exploded because of the exploding home prices in recent years, even has home sales have plunged in 2022. In Q3, they reached $11.67 trillion:

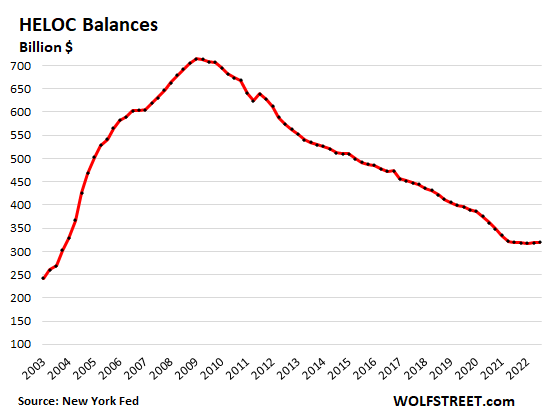

But HELOC balances had been declining ever since HELOCs blew up during Housing Bust 1, and over the last year-and-a-half have crept along very low levels and haven’t come off those levels yet.

I expect that HELOC balances will gradually rise going forward because pulling cash out of home equity via a cash-out refi is very expensive now as the whole mortgage would come with current mortgage rates, not just the extra cash-out portion.

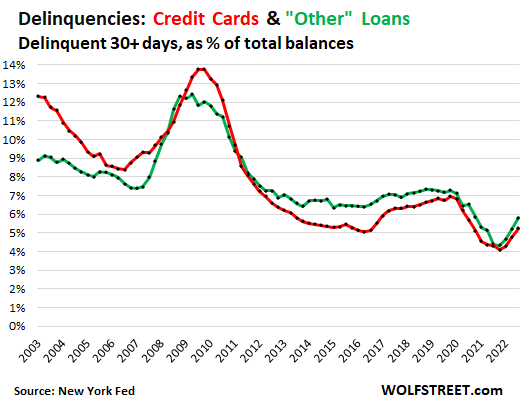

Credit cards and personal loans: I discussed credit card balances and delinquencies in much detail here. The 30-day-plus credit-card delinquency rate in Q3 rose to the pre-pandemic low of 5.2% of total balances (red line). The delinquency rate of “other” consumer loans, such as personal loans, rose to 5.8% and remains well below the pre-pandemic lows (green line):

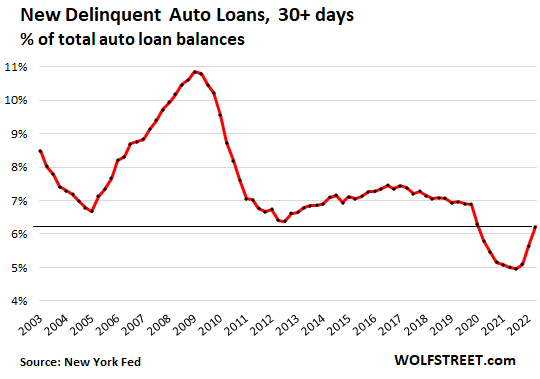

Auto loans: I discussed prime and subprime auto loans & delinquencies in detail here. The 30-day-plus delinquency rate rose to 6.2%, still below the record lows before the pandemic.

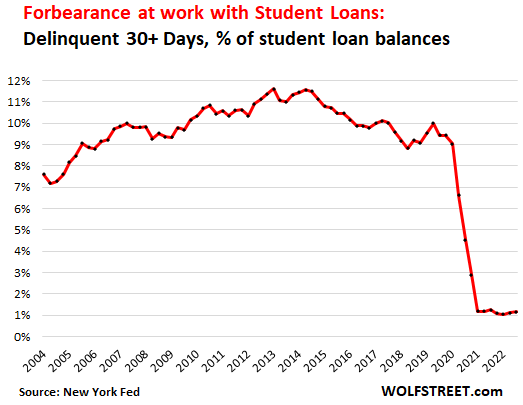

Student loan delinquencies are no longer delinquencies, and student loans are practically no longer loans, as far as federal student loans are concerned, because no one is making payments on them, and everything is still on hold, and balances don’t accrue interest, which has just been extended further into mid-2023, and partial loan forgiveness has been promised but turns out to be hard to deliver as a battle in the courts has ensued.

The only student loans that are delinquent are those held by private lenders, and the overall delinquency rate – kind of an absurd notion with student “loans” these days – has plunged:

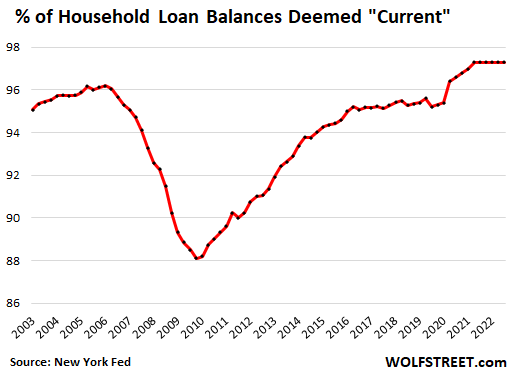

To portion of household loan balances deemed “current” (not delinquent) reached a record high in Q2 2021 of 97.3% of total household loan balances, and has remained at this record high ever since, including in Q3 2022.

These are the total loan balances from all types of loans – mortgages, auto loans, student loans, credit card balances, and other consumer loans – that are “current,” as a percent of total loan balances outstanding:

The Fed has already said that the consumer can take further tightening because consumer balance sheets are in great shape – Powell mentions this at every press conference – and loan distress is minimal and below historic lows. What consumers cannot take for long is raging inflation.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

“The portion of Consumers with third-party collections dropped to a new historic low in Q3, to just 5.7%, after a slight uptick in Q2.”

It would be ironic if collection agencies were to go out of business due to a lack of available third-party collection opportunities.

I did a brief internet search, but could find no information. Perhaps they’re weathering the downturn just fine, at least to date.

Looking at these wonderful graphs, I must take back everything I have ever said about the government. How can anyone question our beloved government officials when they achieve such outstanding economic benefits to everyone???? Comrades, this is a wonderful economy.

Or, maybe this is the mirage in the desert, and it will evaporate just as quickly.

It is interesting how different the housing market is than the last bubble.

There is a heck of alot of equity that needs to be lost before true clearing can happen, when delinquencies are high and stress returns and foreclosures swamp the market. This is truly a buyer strike, not seller-driven.

Given that the Fed still has a massive balance sheet, can we really expect anything different?

It makes sense that the market has really not tanked when it sees these economic statistics. It all looks rosy from here and we imagine a soft landing, where the reality of economics doesnt rear its ugly head.

Yes, it’s simple individual entities (customers or businesses) are not going bankrupt because through QE, stimulus checks, forbearance and bailouts we have merged the balance sheets for everyone and this BS carries a lot of debt owned by taxpayers!

It’s vary much like watertight compartments on a battleship. If a section takes a hit, only it gets flooded (bankrupt). To prevent this, we opened all watertight doors. Now, while no single section is flooding (bankrupt), the whole ship is taking in water and sinking (continuously increasing debt). So US taxpayers as a whole (not the oligarches) will go bankrupt together.

The biggest problem with Fed is that it measures economy health by consumption of goods and services and not by their production. The latter is where the problem is concentrated, so inflation can keep rising despite all this lip-service QT with real negative interest rates.

Biggest problem with the fed is that it exist.

Fix it for us.

Peace out brother

Rant on ! Ignoring the elephant in the room:

The amount of money we’re talking about is a 3rd order rounding error when compared to the total budget of the pentagon and the MIC. I disagree with your parochial view.

Household loan balances deemed “current” (not delinquent) reached a record high in Q2 2021 of 97.3% of total household loan balances, and has remained at this record high ever since, including in Q3 2022.

—

Without raging inflation how will household loan balance deemed “current” ever go down?

And without household loan balance deemed “current” going down, how will inflation go down, and labor market will tighten?

Mortgage balance is $11.7tn and not $16.7tn perhaps? Description and picture don’t match.

“11.67” the first one was missing and decimal migrated south, Chaos everywhere LOL

Thanks

With student loan forgiveness, what’s the point of showing that data? I know; it’s a data point ; )

I like how cars & credit card delinquencies are seeing steepening slope of the tangent to the curve. Nice!

Looking forward to the February 2023 update. Maybe with a little luck we’ll see foreclosures up around 70K with slope that looks like the current car situation.

“The Fed has already said that the consumer can take further tightening because consumer balance sheets are in great shape – Powell mentions this at every press conference – and loan distress is minimal and below historic lows. What consumers cannot take for long is raging inflation.”

Honestly amazing anyone can walk away from this saying inflation is the boogieman, when the Fed’s quite clearly saying they will keep choking off liquidity as long as consumer account balances can handle to be depleted.

Is inflation bad because it eats into savings? Or is the Fed bad because they don’t want people to save money? Which boogieman are we supposed to be scared of now?

Or is this a tale of two cities, inflation is bad for some people, while more expensive access to loans is bad for some other people? I propose it’d be prescient to figure out who fits into which group, rather than pretend we’re all part of the same class.

Inflation is bad because it destroys the currency, and when inflation gets out of hand, as it has now, it also destroys the functioning of the economy over the longer term. ALL ASSETS LOSE PURCHASING POWER due to inflation at the same rate of inflation: crypto, real estate, stocks, bonds, gold… nothing escapes inflation. The only hope you have is that asset prices will rise faster than inflation, and that yields will outpace inflation, and that incomes rise faster than inflation, but none of them are the case now. So everyone gets whacked, some more than others.

So if you think your debt burden will become lighter due to inflation driving up your income, well the underlying asset will lose purchasing power. There is no escape from inflation.

Remember assets only lose value when they are used to purchase something with an inflated price. The well worn advice to consumers here is postpone purchases. If you can gain a higher rate of return for say five years, and inflation is less than the cumulative interest you earned, you come out ahead. Meanwhile if your wages rise your debt payments are less burdensome. Fixed income earn Colas, but paycheck to paycheck are losers. Inflation and high unemployment which the Fed seems to want are anthema. My view the Feds rate hike were a red herring, to satisfy the public, and set up a booster rocket for wall street traders when they pivot. Sure they can put some deflationary spin on things, but that is playing with fire.

The thing needed to thwart hyperinflation in Weimar Germany was other peoples money, French francs, British pounds, American $, etc.

The problem now is there is inflation everywhere, it isn’t localized.

Sorry that you keep on this broken narrative. I like inflation just like this financial news tabloid.

It don’t hurt us any, probably it won’t.

The suffering of hard working, wage saving loyal investors will be monumental.

It’s not right what’s coming down the pike but it’s in the cards.

We’ve been robbed and we allowed it. I know that I just woke up in a land that my fathers once owned.

What about you?

I had to read Wolf’s statement a few times, before I ended up agreeing with him. The thing that tripped me up at first was about inflation hitting all assets at the same rate (the inflation rate).

From a different perspective which assets you hold during inflation is very important. In 70’s inflation, t-bills allowed you to maintain your purchasing power during the inflationary cycle while stocks and bonds got smoked. If Powell does what he says and goes to a restrictive policy, t-bills might keep up with inflation if you look at it over the total time period that inflation runs hot. My guess is t-bills will average just below inflation because US has too much debt to pay a positive interest rate over a sustained period.

But the US government is bankrupt

A government that issues its own currency can NEVER go “bankrupt.” It can always print more through its central bank – In the US, through the Fed. The Federal Reserve Board of Governors, of which Powell is the chair, is a federal agency.

What a government and its central bank CAN do and ARE doing is destroying the currency through inflation.

It’s worse than that. Money has to be stable for economic exchange ie the economy to work. Further, for investment to work, money must be stable. If the value of the unit of account is falling, investment will not make sense except in ‘sure’ things like real estate and oil and the like. We saw this in the 2000s. Investment is the source of all wealth.

“So if you think your debt burden will become lighter due to inflation driving up your income, well the underlying asset will lose purchasing power. There is no escape from inflation.”

For most people, that asset is their home. Perhaps the underlying problem is thinking of a home as a financial asset (piggy bank) in the first place. If instead we think of homes as shelter, then they are immune to inflation. Say I am in home X and want to move to equivalent home Y. The value of X & Y will go up and down, but so long as I can move from X to Y, what do I care? I am in a home. And for many, Y can be a lot more modest than X, if necessary, to cover the shelter requirement, if debt is owed on X. In other words, escape inflation by downsizing (or sharing a home…it would be interesting to see metrics on how much wasted housing space there is in the U.S.).

This would seem to be a problem with taking on debt in the first place for shelter. Historically, has this always been the case? When did humans decide to borrow money from the tribe to build out their caves and mud huts? And the tribe issued more pretty shells to pay for the shelter improvements?

I own my home and the property it is on free and clear. Except for one little detail that must be accounted for: In 2022, every 175 minutes and 13.89 seconds that elapses requires $1.00 be paid to Hennepin County Treasury in order to keep my title and deed free and clear.

The appraised value or market value of my home matters absolutely zero to me; except for the above mentioned single detail.

Prairie,

We are never completely free from the need to keep the money flowing. At best you can shop around to try to live in a location that the services the county provides matches how you want to live.

In my state that ranges from about 0.6% to close to 2%. Last I checked the county tax breakdown was about 1/3 to social services, 1/3 to education and 1/3 other.

Old School,

I hear you. I am at very close to 1%, and all things considered, it is a pretty good deal. As I am about to go out for my daily lunchtime ride, when I return home, I’ll look around and feel blessed to have my modest old Sears Craftsman kit bungalow.

To Stymie’s point, my home is shelter — and where I spend most of my time. “I love this place.”

This thread speaks to my ongoing focus on the difference between price and value which constantly get conflated to meaning the same thing.

I’d argue the value of a home/shelter is basically constant (given maintenance) whereas the price is what’s concerning if inflation erodes incomes enough to prevent acquistion.

my only employee is from Poland. He was 9 years old when the Soviet union collapsed.

He said that inflation went up 400 percent overnight when that happened

His parents had built a house and had taken a loan out to build it and when that inflation hit they were able to pay the loan off for what was essentially beer money. He said it was comical what they did to the money

Seems to me kind of like the same thing is happening here just in slow motion

The longer i live the more i think the only way out of the debt for the government is inflation

The reason powell is hiking now doesn’t really seem to be about taming inflation but crushing the offshore dollar or euro dollar market and by extension old European banking cartels

EB,

I agree hyper inflation will help you pay off your housing debt. But taxes will keep rising to pay those inflated public salaries and pensions. Your income needs to keep up with the local taxes or you will be homeless and broke too.

During Weimar salaries were increased and paid daily. Don’t think the public sector won’t take it all, they are well on their way already.

Last paragraph is Luongo’s theory.

“That the necessary reforms could not be achieved without hardship and sacrifice had been made clear to the public. What they, the public, had not been told, and were now finding out, was that the victims of the recovery would be hardly less unfairly selected than those of the inflation.”

From “When Money Dies”, page 152

Translation: The poor, the lower middle classes, who got screwed the most by the inflation will be the 1st to get screwed royally by the measures taken to end the inflation.

@ Wolf –

Thought provoking, but I suspect you are wrong.

You can now buy an income producing building for less dollars than you could a year ago.

The dollar’s purchasing power, in terms of buying income producing buildings has risen.

When discussing inflation on asset prices, don’t forget any underlying liabilities against those assets.

A consumer doesn’t benefit from inflation because it increases his house value. He benefits because inflation erodes away the underlying principal balance held against that house: his mortgage.

A fixed-rate mortgage is the main hedge fund consumers have against a depreciating dollar.

Inflation benefits borrowers and punishes lenders. This is the reverse of the way an economy operating on honest money would work. Inflation rewards the debt-hungry spendthrift and punishes the forward-looking saver.

But at least you can protect yourself by acquiring a mortgage and participating in the game by by paying off your loan in depreciating dollars.

Correct –

The right move for anticipated inflation is to purchase an income producing asset and fund it with a non-recourse loan, best at 100% of acquisition costs.

Many have gotten rich this way. Undeservedly so, at a cost to society at large, but that’s the game. Reward the biggest hedged “risk-takers”, at the cost of inflation and prudent savers.

Do you think perhaps Romney, Powell, Private Equity and Rich Kid insiders benefitted from this play?

…well, it seems when the only apparent choices/results are ‘bad’ and ‘less bad’ for long enough, that ‘less bad’ can become equated with ‘good’ in the reasoning of many…

may we all find a better day.

It balances out for me. My dollars lose purchasing power, and my property taxes inch up, but my fixed rate loan cheapens my mortgage payments. It seems reasonable to me that some of the ridiculous market value increase in my house tapers off.

Younger folks will find housing as we oldsters sell down and die away. The opportunities will not remain static, as they have not during my life. The point is to be ready when they arrive.

Pancho

You can play that game. I’ll sit it out THANK YOU!

“Everything, everywhere, all at once. “

For T yields to outpace inflation, JPowell will have to put on his big boy pants. Hopefully, this will happen, so he gets the FFR up to at least 5% before pausing and doesn’t let all the pivot chatter keep him from delivering on his T & MBS runoff schedule.

Wolf Ritcher,

I do live in Argentina all my life. We don’t have inflation, we ARE in In-Flames-Nation.

Actual REAL inflation here is around 90% YOY in US currency. If you want to learn how to handle the ship in a “Perfect Storm” come to my country. People became experts to economic shifts.

Cheap credit usually leads to mal-investment.

I’d don’t believe there was ever an instance where it did not. I don’t have access to the data though.

I believe there are moments when loosening credit or money averts a catastrophe. We can’t prove the counter-factual: run the world down a different path like a physics experiment, and get the “data” such an alternative would show. It is the fog of war. I believe 2008’s crash might have devolved into Great Depression 2 and World War 3. But, like using certain drugs, folks don’t stop when things level off. They keep taking the sugar rush until things screw up again.

The Fed will beat the shit out of the markets to re-assert it’s mandate and regain it’s credibility.

The markets needed to have some air let out. Not that the Fed was so wise as the bubble was blowing up. But I can’t imagine that departure from fundamentals should be supported more.

Great comment. Instigates my propensity to respond with my own opinion to a couple of points in the general disagreement I have to the gist of what you said.

You expressed uncertainty, which is also known as the ” kiss of death” to career hopefuls.

Inflation is not a joke. We, as a world, have a serious breakdown of what is the value of a currency.

Or is it a joke ?

I’d say that it is a great time to be an American! That is if you can avoid being shot at while enjoying yourself in a public place!

I could only dream of this job market while I was coming up and access to credit these days…if used to get ahead in life…is terrific.

How much did you pay for college and your first house?

Job market may be good, but what you can buy with that jobs is less than you could decades ago.

I had this exact argument at Thanksgiving. I’m really tired of people saying “Young people today need to stop complaining about 7% interest rates on mortgages. We paid 14% for our first house in 1983!”

Yeah, well, that first house was only $80k, 3 times your income. Houses are now 10-15 times income in many places.

100% valid and hence the reason we have made a society (in gen Z and below) that does want to work especially the lower income half. Why toil for the big company if there are not ascertainable rewards. Average wage to housing and vehicle price is out of wack.

Einhal,

Sometimes the only way to win is not to play. Dropping out is becoming the way to go.

…as all grope in the smoke surrounding the ever-moving target of price discovery…

may we all find a better day.

Inflation equals a lower standard of living

for the working class. Running faster just to fall further behind.

what happened in 2017-2018 that caused third-party collections to fall? was this a regulation that changed the collections game?

gametv

During this period Democrat Senator Dick Durban authored and passed a bill requiring the credit card companies to print a section on their bill giving true information as to what it cost to pay just the minimum. Surprisingly people began to pay most or all the invoice. This was such a good piece of legislation I wrote and complimented him.

After reading this article, it seems as though the United States is in great shape and everything is hunky dory. There will be no landing anytime soon.

It’s 1:00 a.m. in America. Better top up that punchbowl, the night is young! Hangovers can be put off forever with fresh shots of booze (NOT).

I always thought it hilarious imagining Old Greenspan at a frat party pouring Everclear and Mad Dog 20-20 into a punchbowl. Mix and shake with some other funny business, then a generation later out pops Sam Bankrupt Fraud.

…makes me envision a bargain-basement booze offering with ‘Old Greenspan’ labelling…

may we all find a better day.

Yeah, a real cheap looking label (like Night Train’s), with big letters saying, “alcohol 20% by volume, serve very cold”

“A permanently high plateau”

Haha, Irving Fisher.

All of these numbers indicate the ferocious velocity of the current inflation and are ominous for Mr. Powell.

He’ll most probably have to take unemployment to 8-10% to make any major dent to this inflation.

He may have to go higher than Mr. Volker with FFR..

JPow can’t go higher than Volcker, that was $29T of national debt ago.

If the FFR gets to 6%, I’ll eat my Golden State Warriors hat.

Would 6% hurt the common people? It adds to savings accounts FINALLY. For a while, most people have already bought a home or taken out equity loans at low rates. Most people can’t borrow at less than 6% already, it’s more like an average of 10%.

The ones crying for pivot are the stock market, corporations, and banks. How can they borrow to buy back stocks at these rates? How can you tighten your corporate monopolies at 6%? How can billionaires borrow against their stocks at these rates and be comfortable?

It’s a darn shame.

The tighter credit conditions that are in store will ultimately kneecap the economy. It’s only a matter of time now that the credit cycle has turned until rates “blow out”.

Most people don’t have enough savings to meaningfully benefit from higher rates.

They don’t have problems paying their debts now, but their employers’ finances are starting to suck wind and the pink slips are just getting started.

If he does go as high as Volker or 1/2 as high as Volker, you might need to eat your hat to keep from starving. A good hat should last a couple of meals. Obey The Pug

That is a ridiculous assertion. Unemployment may rise. If you had been paying attention to the likelihood of unemployment exceeding 4.5% before the Fed halts the increase in interest rates that they are systematically increasing in an effort to subdue inflation.

These numbers point out why monetary policy will not work well to slow the economy down. Consumer Spending is 70% or more of GDP. High interest rates are not likely to impact Consumer Spending very much because of their financial condition. So yes GDP growth will slow (a soft landing) but there will be only a slight slowing of inflation. Expect it to stay high, at lease 4 to 5% per year. It will then get worse if the Fed starts lowering interest rates. Its 1970s stagflation all over again.

Pedal to the metal, demand more more more wages, benefits, forebearances, let’s outrun inflation!

It’s the corporate sector that’s the canary in the coal mine this time, not households. This and unknown supposed “black swans” outside the US which will catch Main Street and Wallstreet off guard, again.

Belief in a “soft landing” is a delusion, a belief in something for nothing.

The idea that a mediocre pre-pandemic economy miraculously turned robust or healthy after shutting down the economy while making up the difference through “printing” and deficit spending is ridiculous.

So the lower 90% learned some prudence but the corporations thought they could continue their gluttonous behavior forever believing the 0% loans would never stop?

Yes, exactly. There are many, many companies that don’t have a viable business model in today’s economy, meaning that they have been financing their operations with debt, that they have continued to roll over for many years.

Zombie companies financing with, say, 2 year bonds is fine as long as you can keep refinancing them at their maturity with new debt at the same low rates.

Well, guess what? Those days are over. When those 4% bonds mature, they’ll have to be refinanced with bonds at 10%. Many won’t be able to afford the debt service.

That’s the reason that the rate hikes have not had immediate effect. There are many bonds out there, both government and corporate, that have not yet matured and still bear the low rates from the 2009-2021 era.

Once zombie companies start collapsing, resulting in not only laying off all of their employees but also a drastic reduction in demand across the economy (after all, even zombie retailers still buy goods and services from the more stable companies), we’ll start to see a reduction in inflation.

That said, this means there won’t be a “soft landing.” The idea that they could ever get inflation under control without pain was always a fantasy. From the beginning of QE, the day was also going to come where our policy makers were going to have to pick between out of control inflation and a painful recession. That day is here. There is no avoiding it.

Just now I was reading an article on Daily Upside claiming many large European businesses are looking to relocate manufacturing facilities to the US due to inflation and war eroding competitiveness, on top of that the “Inflation Reduction Act” seems to be offering incentives to qualifying plants which are up to 6x higher than the best European nations can offer. Meanwhile, here on Wolf’s page the data seems to indicate still a rather robust labor market and very low unemployment despite some layoffs in big tech and many people not counted in unemployment stats (re) entering the workforce. I realize the layoffs are probably ly just starting, but so far no large u employment claims and potentially more job openings on the horizon if this mass EU business migration materializes.

I’m not smart enough to make proper heads and tails out of this but I get the feeling the US FED is attempting to sail upwind with their hikes while the situation globally responds to that attempt with more investment into the US. That is my perception right now anyway.

Maybe I should reconsider relocating to the US afterall, I don’t see a way in which Canada also becomes a winner in this game, hopefully I’m completely wrong on that.

The talking heads used the term “soft landing” to avoid causing panic. If JP said “It’s all going to sh1t in a handbasket! Run for your economic lives!” what might you think would happen?

IIRC, the term “landing” is airline lingo for a controlled crash.

“High interest rates are not likely to impact Consumer Spending very much because of their financial condition. ”

That doesn’t…compute. Look up ‘wealth effect’. Also, just wait for Italy and Japan to capsize. Those fireworks will put a damper on velocity of money.

There will be few bankruptcies initially etc. because inflation is pushing up wages while the existing debts are for a fixed amount. In such an environment spending now is wise if you can get cheap debt.

At first, like the insanity of low interest rates, inflation is an elixir for a debt-burdened society, even if one is falling behind income., the old debts are “shrinking.” Fixed rate debt is wonderful if inflation increases.

However, as you correctly point out, when it takes off business planning and investment become very difficult. Is profit profit when you have to replenish your inputs with new higher cost inputs etc.?

Crushing inflation will be really difficult because we are also destroying the controllers of inflation the “China Price” and loose capital that was allowing shale oil to be pumped at a loss is disappearing and capital-burning firms such as Uber etc. will have to raise prices as interest rates increase. Finally, of course, there is cheap Russian and Ukrainian commodities being taken off the market.

What a wicked Zugzwang. Situation would be difficult to manage if we had really great leaders. With what we have wow!

Stopping inflation in this situation will make the crises of the 1970s and response in early 1980s seem tame.

I look at these charts, and while the current levels are low, the delinquency charts show large increasing slope that has just begun in the last several months. Looks ominous to me.

Great to see positive financial wellness post pandemic. Americans get what they want when they want it. Exhaustion of overindulgence the last 2 years from homes, cars, electronics, and remodeling. Peloton rage/home gyms etc. Traveling on the road from Denver to Natchez this Turkey Day Marriot Hotel parking lot is full, southern hospitality and free flows of greetings. Refreshing to see no one panhandling/homeless.

We see what we want to see.

Hotels are full.

AirBnB’s are reported to be hurting.

Is this a sign? Consumer bad experience with unregulated “hotels” that can’t afford a decent extremely high cost cleaning staff may be taking a toll.

That is my humble opinion.

Airports are full. Good thing you drove. Gas prices are down.

$3.85 / gallon, tax included of course, at the Family Express Convenience Store Gas Station off I-65 on U.S. 231 Indiana.

Gas up if going into Illinois.

Doo, Doo, doo lookin’ out my back door.

Low unemployment seems to play a role. The numbers look good. The last time it was lower was back in 1968. It seems to proceed every recession and a spike in unemployment going back to the 1950’s.

ROFL no offense I saw that statistic.

It ain’t what it seems son, yet I do enjoy the humor.

Delinquencies, foreclosures, etc still at or near rock bottom. Meanwhile, Thanksgiving online sales hit 5.29 billion, a new record and a 2.9% increase YoY. This goes to show the consumer remains resilient in the face of rampant inflation. It also would appear Powell has plenty of room to work with when it comes to raising rates to tamp down inflation.

One has to wonder how much of a role the perma-ban on student loan payments is playing in goosing consumer strength. Or maybe the leftover stash of cash-out refi money?

2.9% rise with 10%+ inflation is a decline of 7%.

Well. no. Because goods inflation has come down — and people buy goods for Christmas gifts. What is spiking is services inflation.

In a way services are just as hard hit.

Take the car towing industry and the nurses positions then the real estate hawker and broker then even lawyers.

Don’t believe go check the court rooms.

Service industries are way bad shape.

We are encouraged to step in our grand parent’s foot steps. Learning to do everything, fixing cars doing plumbing and other house repairs your self except that today its is way more complicated to fix a car.

My mazda 3 2019 car was. In dealership. The dealer had to connect the car to laptop and an engineer from Japan was checking to to figure out that the thermostat was bad.!

So we have to step up our knowledge to be self sufficient as much as we can

My goodness. On my 73 Mopar my 17 year old self could change out a thermostat with screwdriver.

Shiloh – raising the question (ic or ev): “…at what point does the tool of engine management become more important than the affordability of the transportation mission?…”.

may we all find a better day.

Exactly thank you

“This goes to show the consumer remains resilient in the face of rampant inflation.”

Whatever happened to referencing Americans in print as just people? Citizens, even? I hear it/read it constantly: Consumers…taxpayers…we seem to regard human beings as little more than agents of commerce; walking gas bags doping on unbridled materialism, dining-out and vacationing in a bid to keep our fragile, pretend economy aloft. Yick.

“I am not a number, I am a free man!”

To corporations, that’s what you are.

Their favorite term is Bodies.

Human capital, or headcount like cattle.

The TSA regard you as self-loading cargo…

(Spellcheck prefers self-loathing)

I regard the TSA as perverted parasites.

I second this 100%. It’s a masturbatory shell game for men who will never quiet measure up in other ways and we’re all sort of coerced into playing along.

We as “consumers” need to take our dignity back. That useless word is little more than a smug pejorative for sad, depraved suits filled with hot air to patronize us with.

It’s high time for the Cleansing of The Temple – expel all of the merchants and money changers who are so bold as to try and keep the human condition confined within their vice grip.

Reject all markets and consumerism to the best of your abilities. Tell the financier perverts just what they can do with their interest-accruing loans.

There is no reasoning, no middle ground with parasitic misanthropes. No parley, only powder kegs now.

bulfinch,

This debate goes back to the Middle Ages and beyond. Christian thinkers argued for a “fair price” that made sense for all stakeholders. This is in the 1300s. Capitalism fought to disaggregate these things into components/commodities/numbers/value streams. With the Enlightenment, it was decided the clunky old religion part (and its emotional-humane components embedded in human relations) could go out with the baggage too. Congratulations to all those modern advanced people who have been stripped of so many tools and means along the way, to make the world safe for stripped, platonic markets as determinants of everything! Every innovation means something has to die.

The perma-ban on student loans shows that government assistance in all areas will keep flowing as needed.

Or someone will sue the government to continue payments as needed as in this case.

As a holder of college debt I think I am in the majority who’s loans are held by private finance and these debt traders are unaffected by fed forbearance or amnesty. Further, they enjoy variable rates of interest.

I do not think loan forgiveness will be but the smallest of marginal effects on consumption. Albeit, the right moral and economic move.

Why is it the right moral and economic move, pray tell?

Why should people who borrowed money to go to school have their debts transferred to taxpayers and/or savers?

Same reason that 11.5 million PPP loans were forgiven.

Einhal exactly Its the absolute worst message to be sending Things are fugazzi enough now

Credit Card debt at all time high. ( I understand at this stage it is solely used for convenience of purchases, cash-back point etc). It means to me, that people are confident about paying it off on time.

Personal Savings Rate – at 3% or so.

It seems scary, because it looks like majority of Americans live paycheck to paycheck, yet the financial “morale” stays high. Based on current FED increases unemployment rate doesn’t get affected significantly.

Therefore as long as Labor Market Stays strong, where employees dictate terms, this merry go round can go on uninterrupted?

“The majority of Americans have been living paycheck to paycheck” for the last 20 years. Not picking on you but that saying has been around as long as I can remember.

When we will have a recession…some people who are living paycheck t paycheck will get unemployment. Default on their car loan or credit card paymetns….then start anew. Wash, rinse, repeat.

It seems like the FED has been doing a real good job at avoiding recessions or making them less than 2 quarters so after people default….they will have a new car loan and some new credit cards.

Print prosperity has been the mantra since 2009. No wonder we have millions of people migrating across our borders to the good life in the U.S. Most people do not realize how good it is to be living in the U.S.

50 years imho

Yes, for now. We’ve basically taken full advantage of being the reserve currency. As I’ve pointed out before, however, we’re not going to get a warning when the game starts to fall apart. It’ll just happen. Right now, the dollar is strong against foreign currencies because people believe Powell will continue the war on inflation. If he pivots, watch the dollar tank.

Thats my opinion as well and Im worried as Im holding substantial cash in USD

The ultra-low 3% savings rate may be alarming but actually makes sense given that Americans are still churning through the gigantic pile of excess savings left over from the pandemic.

Estimates vary as to when this pile of cash will be exhausted. Experts interviewed for a recent WSJ article on this topic provided a range of between 2H2023 and 2H2024. That’s a long ways off!

One thing for sure is that there’s plenty of kindling to ensure elevated inflation for a while, even as the economy weakens.

Although inflation has come down recently, that was expected thanks to favorable YoY comparisons. Now comes the harder part of reducing more pernicious and persistent inflation fueled by the aforementioned pile of cash and the still ultra-tight labor market.

How do you un-print 8 trillion dollars?

the conmen and their beneficiaries have absconded with the purchasing power of your dollars ……………..

The Nov 2022 fed minutes were a boon for the markets – as intended. For those that forget and think current inflation and unemployment will lead the fed to soften less than 75 bp dec 2022- ha (imho). I think we need rates 12-18% to curb the current inflation (monetary)crisis we are in.

Inflation emerged as an economic and political challenge in the United States during the 1970s. The monetary policies of the Federal Reserve board, led by Volcker, were widely credited with curbing the rate of inflation and expectations that inflation would continue. US inflation, which peaked at 14.8 percent in March 1980, fell below 3 percent by 1983.[21][22] The Federal Reserve board led by Volcker raised the federal funds rate, which had averaged 11.2% in 1979, to a peak of 20% in June 1981. The prime rate rose to 21.5% in 1981 as well, which helped lead to the 1980–1982 recession,[23] in which the national unemployment rate rose to over 10%.

There’s some controversy over this raised by John Tamny, who claims that the real credit should go to Reagan for essentially putting the USD back on gold by de facto. The US Treasury has a dollar policy, and it matters. There’s evidence it matters a lot more than the fed for where the USD sits. And from the beginning of Reagan’s term to the beginning of W’s, there was as 20 year period where the price of gold in USD was stable/declining. That is, in essence, a gold standard. China had a similar period of de facto gold standard for the Yuan after the 2015 mini-deval disaster.

I for one, think Tamny is wrong to dismiss Volker’s contribution, and believe he potentiated Reagan’s dollar policy shift ie without the prior stringency it would have meant little or nothing.

@ Cytotoxic – ” John Tamny, who claims that the real credit should go to Reagan for essentially putting the USD back on gold by de facto. ”

—————————————–

Who is John Tammy? This sounds like complete BS.

He’s a Forbes commenter I don’t even like very much, but you should read some of his stuff. He made a semi-compelling case that the fed matters less than people think. I think events have gone against that narrative but I also think he’s right about USD policy being an important thing.

George Schultz, well before he went ga-ga on Holmes.

…reinforcing the verity of Barnum’s Dictum existing in ALL classes…

may we all find a better day.

Did you actually read the Nov 2022 fed minutes? I did. They were not intended as a boon for the markets, nor were they materially different from anything the Fed has been saying for 5-6 months at this point.

The “markets” hear what they want to hear.

“…and disregard the rest”

We certainly need higher interest rates not a redefining of the inflation rate to make it look a lot lower than it actually is.

For people in the US, it’s about what lifestyle level can be maintained. Most people are far from grubbing out a living like in the depression. People are still not wanting to work and don’t have to for whatever reason in the lower-paying jobs market.

I think stimulus checks will be handed out again when the economy will call for it. Unemployment will be fully funded for however long it takes to keep the votes coming in. The US can print even with 10% inflation for a long time. Because we are the reserve currency and the politicians know it and take full advantage.

No you can’t. Things are changing you can’t just print the money. Inflation isn’t just bad economics it’s political poison. Besides, the USG is divided right now.

USG not divided about blowing money. It’s pedal to the metal. Print baby.

Yes it is, in effect. Team Red doesn’t actually care about fiscal sanity but they will spike spending by Team Blue out of spite.

Elites and their lackeys in government aren’t going to trash the USD for “bread and circus”. It’s not 2009 or even 2020.

Watch what happens to the DXY. There is some latitude at 105. The danger zone is when it gets into the 70’s or low 80’s.

Britain passed a faux “austerity” budget recently and more is in store where that came from too.

There is nothing magical about being (global) reserve currency. The Empire must be maintained at all costs and that’s not possible with open ended “bread and circus”.

What is this so called “Pandemic Money?

Did some of us miss something here?

As usual they did not send me any. Stimi checks were sent to most so they could spend it on worthless stuff. Most PPP loans were forgiven. So it was essentially free money to those that received it. Or it could be considered compensation for a government mandated vacation.

I also got zilch.

Before I moved from the western Chicago burbs I never saw as many home improvement projects and new luxury suvs in the 20 years I was there, as I did in 2020-2021, including leading up to the 2008 GFC. All of those with ‘housewife hobby’ businesses hit the jackpot with the PPP.

“What is this so called Pandemic Money?”

Money that was given to just about every business with one or more employees.

You can see here:

https://projects.propublica.org/coronavirus/bailouts/

The search query is pretty weak. In order to look up a company you seem to need the exact name as on the application. But if you type in your city state and zip you can scroll through.

I looked up a few people that I know got the loans, and the information seems to be accurate. Also, most of these companies got 2 “loans”. If you see 1 company loan, keep scrolling and you will see a second for the same company (or you can highlight the company name and paste it into the search). Most likely you will find you local plumber, electrician etc. on the list.

The people I know that got the “loans” businesses were thriving during this period.

Of course this is just the ppp. There was also all the stimi checks and extended unemployment and fed matching etc.

It all makes me sicker than covid.

Great resource. Thank you for sharing this. I checked few business and sounds about accurate. makes me sick, but at the same time it sheds important light on major cheating done by the government. It seems to me that “covid” was just an excuse for an another bailout. This time around, the government also sprinkled money on people a little bit so that they don’t revolt, but the larger context was the excuse for bailouts and money printing, all in the name of “COVID”.

The problem was not requiring proof of loss of revenue.

If they had made that one simple change, 95% of the problems would have not existed.

After 14 years total mortgage balances are up by $2T from $9.5T

to $11.5T. In real terms they might be lower.

In the last 4 dots : auto loans, c/c loans and other loans delinquencies are rising sharply. It might get worse after Xmas.

Americans always insist on a nice Christmas. Debt be damned, we will have a giant pile of pricey gifts under the tree and the traditional mega-feast.

Then the bills will come due.

1) A software engineer making 200,000/y might be equivalent to 6-7 MCD workers annual income. It’s all about weight.

2) Layoffs are not equal. Each 100K units of high tech layoffs might be equivalent to half a million in the service sector.

3) Mortgages delinquencies are not equal either. MCD workers usually rent, software engineers buy expensive homes. Their mortgages might exceed a $1M. Once they are out they cannot pay. There will be no buyers. What matter is the accumulated total dollar value of delinquencies not their numbers. Same with auto loans.

4) Gen Z wealthy parents are piling student loans debt to secure high standard of living for their children. Two/ three children in college can wipe them out. Gen Z kids will be chronically unemployed if the layoffs start.

5) Today, on Black Friday malls are packed, mostly by young people, but the number of malls are down. Old boomers avoid the mall crowds.

1. Dyslexia for cure found.

2. A missing service sector worker/MCD employee will be missed more than a WFH employee…

3. I agree with you on this one. Obviously, a regular full time working family cannot afford a home either.

4. I rather disagree. Gen Z parents (may be late boomers or Gen X?) sending gen Z to college is equivalent of 1900’s parents sending children to farms. They intentionally send kids to farms as sharecroppers.

5. Again, more boomers with tee’s + flannels shirts + jeans walking with their children and grand kids. Also strollers.

6. Please get out of the van and buy a coffee in the gas station.

4) purely anecdotal, but did not witness from my Archie Bunker chair within earshot of the dining room table any discernible difference between online Ivy League zoom course and same from local community college in Spring 2020.

I was waiting for months for a real electrician to replace a breaker box at that time, however.

The FED needs to focus on servicing our current debt…not increasing it! Our debt based economy is a failed Keynesian experiment…it is unsustainable in will be the ruin of Planet Earth and all of its inhabitants.

Unsustainable growth will be our demise. It’s time for austerity. Let’s raise the Fed Funds rate back to 18%…let’s rip off this band aid now before the U.S. end up like Zimbabwe.

That’s honestly unfair to old Keynes. He was serious about paying back in good times the debts racked up in bad times. He was a snake oil conjurer who came to hate those who peddled his snake oil.

“Of everyone in the room, I was the only non-Keynesian”

“Oh my followers? They’re all idiots”

I paraphrase lightly at most.

To your point, Keynes was not a “Keynesian” — the latter having bastardized his work almost out of all recognition courtesy of the neoclassical synthesis. Those who adhere most closely to Keynes’ work are the post-Keynesians.

Services inflation inflates faster each month. Just this week witnessed a plumber clearing a home sewer line 1 hr, a water well service and a culligan guy diagnosed an issue with water softener

1 hr snake run $500 (rotor rooter)

1 hr water wells service $550

30 min cullugan guy 600

1750 in one week ! One pressure guage for parts all labor

You need to quit your job and do it yourself. It is effectively tax free income. All the goofy ways people try to avoid taxes are beaten by doing it yourself.

I thought I was the only one doing that lol

BS

Spent a hard scrabble life scraping a living so would suggest the 1.6 gal toilet was the cause of the blockage. Reinstall old taller water reservoir add 2 or 3 bricks to reduce volume and flush with increased pressure. Everything new and fashionable isn’t always useful. It will take several years to use up the $500 in water. Can’t speculate on the other two costs although I could have changed the pressure gauge.

When you add Bricks to a Toilet you Reduce the Volume of water >

Then your back to the same amount of Volume .

Good Toilets flush Good bad ones don’t

IE: your Old Taller Toilet becomes a 1.6 Toilet with bricks added or the like Etc

for increased pressure you need a pressure-assisted toilet and with that you also need good water pressure rather then a Gravity fed water system with low pressure most often

You discounted the increased height giving more initial pressure on the liquid down flow. Did this for many years before constructing a new house. Same process occurs with a larger diameter pipe for water supply. Both bath showers work well at the same time with the increased volume and same pressure.

Haha. I remember a classic rant from Peter Schiff several years ago about the Government messing with the toilets.

“I expect that HELOC balances will gradually rise going forward because pulling cash out of home equity via a cash-out refi is very expensive now as the whole mortgage would come with current mortgage rates, not just the extra cash-out portion.”

——

Sorry, but I don’t quite follow? Wouldn’t the factors WR mentioned here cause HELOC financing to fall, not rise?

I could understand why HELOC balances may rise as credit cards and other means of borrowing becomes more expensive, or as government deficit spending crowds out private borrowing.

As an aside, I do love markets and economics, yet all these years of MMT, ZIRP, and titanic government debt have just perverted in every respect how we even think about it. Makes my head hurt.

Ah. I get it now. Easier and cheaper to do a HELOC loan to raise cash rather than a complete re-fi at higher rates.

Apologies.

“No wonder we have millions of people migrating across our borders to the good life in the U.S.“

Oh sure — blinded by sun on our streets of gold.

“Most people do not realize how good it is to be living in the U.S.“

Let me guess; it’s been good for you. Congratulations.

Hi Wolf any chance of an article and predictions of the UK gilts market? I know not the US but on this article we are the canary in the mine simply because we are further along the path. The 10 year yield is a tad over 3% and my personal opinion is that it will keep rising, the central bank says it will peak at 4%. If it doesn’t peak at 4% the UK will have to go to the IMF.

Our government debt servicing costs are now above the Japanese as a percentage of GDP ( a fact in itself which is incredible). The currency has collapsed. Inflation is now over 10% and the housing ponzi scheme looks like its rollilng over. Taxes are being increased and government services are being cut. Immigration is being forced through to stop wage inflation becoming obvious. There are strikes breaking out across different sectors.

This is all due to misguided cheap money policy of the central bank since 1997 which has enabled blatant corruption in the public sector to remain hidden. I think the US gets to this point as well. However, the US has huge untapped natural resources.

If you are interested in economics and like fireworks look at the UK or Italy.

I covered the gilt turmoil when the pension funds started to implode. With yields where they are now, I’m not worried about demand for gilts… With 11% inflation guilt yields should be in the double digits across the board. The fact that they’re not shows that consensual hallucination still rages, creating excess demand for financial assets — as you said because of the cheap money policy. That cheap money policy finally ended in massive inflation. So now, yields must rise, or inflation will totally blow out. That’s the choice. And yields haven’t been rising enough.

“With 11% inflation guilt yields should be in the double digits across the board. The fact that they’re not shows that consensual hallucination still rages”

——————————————–

consensual hallucination or central bank manipulation and money creation?

Wolf, demand for financial assets will fall when enough money is destroyed by the Fed- because that has been the fuel for four decades since inflation was finally under control.

Now we get the flip side of the coin, asset demand will fall as will prices during an inflation- which is not how most of the players think it will go.

Just look at the folks calling for a pivot- change, etc.

The new way is a very old way- which of course has been long forgotten.

Unaffordable housing due to “shortage”- which really means overpriced for the actual earnings of the proles.

This adjustment means much higher wages, or much lower asset prices- just in time for the boomer downsizing.

It is a long way until 1982 from 1970.

Much of the supposed labor shortage will be eliminated from tighter credit conditions, noticeably tighter.

There isn’t going to be much higher wages across the labor force. A substantial number of jobs will be outsourced or eliminated, many by automation. Potentially more office jobs this time around than other types.

Still waiting for an automated electrician or plumber.

Why would the UK “have to go to the IMF?” Gilts are debts denominated in pounds, a currency unavailable at the IMF which operates in US dollars.

Are you claiming that the UK has sufficient dollar denominated debt to require IMF assistance? If so, I think you are misinformed.

Opening the border to increase immigration to solve the labor shortage will ultimate make most British poorer while increased congestion will decrease quality of life.

1) Gen Z and millennial are under pressure. Delinquencies are rising. To save money young couples will move with mommy.

2) She will cook, take care of the kids, while the couple work and save money.

3) Demand for rental units will be fall.

4) If mom and dad sell the house for $10K, before they expire, Case Shiller will flip from positively bias to negative bias. Our mass flourishing will hit a wall.

5) People will say : NO. Our discipline and frugality will hurt China.

China mercantilism policies of max export/ min import will get a deadly

blow.

Buy a 1920s Berwyn Illinois bungalow and turn it into an illicit 2-3 flat. That’s what they did in the 1930s.

I see reports of layoffs and business firings to trim the dead wood. Does anyone know of the government doing this? Not since air traffic controller’s can I recall it happening.

I know people with management positions in gov’t. They are having a hard time recruiting good people because of housing costs and lower than private salaries.

A lot of government agencies need to be abolished. This won’t solve the entire problem but will for much or most of it.

Absent that, I’ll volunteer to restructure these organizations if given sufficient latitude. I guarantee you the staffing shortage will diminish substantially by the time I’m finished. Example is taking a hatchet to administrative positions which didn’t exist decades ago.

I remember that imbecile Rick Perry in 2011 debates not remembering the 4 cabinet departments he would eliminate. Ron Paul, standing next to him, answered for him.

Augustus Frost

David Stockman once said “Cutting government Agencies across the board won’t cut it”

You need to “zero them out altogether, otherwise they will grow back the same or bigger than before”

Never has a truer word been said.

Shiloh1

SO WHAT if Pick Perry couldn’t remember one of the cabinet departments he would eliminate. You sound like those losers in the main stream media making fun of people who they don’t like.

Pay peanuts, get monkeys.

Those who want to destroy government like this.

Step 1: Ensure government can’t hire well-qualified people.

Step 2: Attack government for poor performance.

It’s simply bizarre how many ignorant assertions get made about the size and/or efficacy of government without any evidence. At some point it becomes indistinguishable from religious dogma.

Most government jobs pay far more than the private sector when you consider defined benefit COLA pensions, retirement at 55, free or very low cost health insurance for life, and so on.

Yes, it’s true that if you have the ability to make $500k at McKinsey, you won’t make more in the government.

But the random accounts payable employee working at a company making $80k can do better in government.

And don’t get me started on teacher/police/fire salaries in many places.

The dysfunction of government has nothing to do with the quality of people it can hire (they pay them plenty) but its illegitimate scope and bad reward structure ie businesses that do badly go out of business, schools and such that do badly get more money.

Cyto – not enough ‘done badly’ businesses have gone out of same. The whole idea of ‘done badly’ is now a null term given the incessant gaming of capitalism via financial ‘engineering’ and modern high-speed communications as to who or what ‘does badly’ (is it financial? morally hazardous? Both? Neither? Done TO or FROM?).

Meanwhile, the proportion of the high-consuming ‘left behind’ planetary population continues to grow beyond a reasonably sustainable replacement rate. ‘Living standards’ going forward will be fraught, species adaptability as demonstrated over this ol’ space rock’s long (in human reckoning) history will be key. Hollowing-out, propping up or backstopping a faltering system while continuing to defer maintenance won’t work indefinitely.

Of course, we are not particularly long-lived, or these days, memoried…

may we all find a better day.

Due to hundreds of unfilled jobs, Florida no longer requires five years of college for entry level teaching positions. Boomers took early retirements during the COVID first wave creating job vacancies.

Household Debt Service Payments as a Percent of Disposable Personal Income (FRED) is rising.

In Florida, Police Officers don’t even need a high school diploma. High school dropouts are welcome with open arms.

Flashman

Most of the deadwood in the government agency (DOD), I worked for was with the contractors who literally took over the place. They hired 20 contractors to do the work I was doing, and they screwed it all up to boot. When I left, I could not name a single project in the IT Department that was outsouced to them that they didn’t destroy. Same happened with some of my co-workers.

1) SF vacancies are rising. When leases expire, the high tech co call the movers.

Landlords, hit with higher interest rates, cannot cover their debt.

2) Consumers mass flourishing never stopped. Politicians and our society

benefit from infinity spending. After Xmas the bills are coming. cC/C loans can range between 15% and 35%. The poor and the upper middle class are loaded with them.

3) Delinquencies are rising. Bankers have two options :

– the recycle bin, write off assets, send to collection agencies.

– settle : stretch the balance to 5y-8y, make the monthly payments affordable and cut interest rates to zero, in order to keep them running. Losing profit, keep the cash flow, is better than assets write offs.

4) The zombie consumers, – small mfg, landlord… – don’t go bk due to higher interest rates. That’s what the charts above say. The bankers keep them alive and kicking. Their books are not impaired. People pay on due day.

1) I loved that late 70s show Too Close For Comfort set in San Francisco. Ted Knight was the dad and cartoonist, who rented one apartment to his 2 daughters and the other to this comic Monroe character.

All the damage done by Alan Greenspan and Ben Bernanke needs to be reversed. The world needs permanent higher interest rates.

Cue Jeremy Siegal for another CNBC appearance Monday morning to tell us the Fed must PIVOT!!

I’d rather them cue Let’s Do Time Warp Today- “it’s just a jump to the left!…and a step to the right!”

That’s my idea of a pivot!

Low-middle income earners are the ones seeing all the wage growth in last 2.5 years. Higher incomes seem to be stagnating. Less then 3 years a go entry level jobs were paying $8, now it’s $15-20 minimum to get anyone to show up.

This makes me think that the housing market does not all have to come down. The market is divided into lots of price categories. Entry level housing/starter homes all the way up to luxury. I’m still bullish on starter homes, especially the ones that can still be bought under replacement value.

Lower wage earners cannot afford most homes, even “entry level” in a noticeable percentage of markets.

Where I live in metro ATL they would be better off renting than buying into another housing bubble anyway. Or, even if there was no housing bubble, many of the areas where they can buy aren’t worth living in anyway, a noticeable number. The places are dumps.

The entire area I live in 5 percent of wage earners can afford most homes. 95 percent can’t.

What about buy now, pay later? Do consumers put the next new big purchase there instead of on the CC? Is that in this data (3rd party collections?) is it sizable? What if the bubble pops on one of those companies?

They have put a big dent in credit card balances….60 days no interest, 6 month installment instead of revolving loans…..they are going to keep eating credit card companies up and thus why big banks are now taking them down market cap wise to get in on the cheap

The savings chart from another article seems to imply that savings are being consumed and credit card debt increasing. Except for those who use CCs in lieu of checks as I do, that implies that as savings dry up, credit cards take their place for expenses.

Maybe I am just not getting all this but the more worrisome item would seem to be the tanking savings rate.

The saving rate = total income minus total consumption, at the seasonally adjusted annual rate. That’s the number everyone throws around. But consumption doesn’t include buying stocks, putting money down on a house, buying cryptos, putting money into a 401k, et. This is one of the most misleading stats out there if cited like this.

Good to know, thank you! It seems that every stat released these days has major flaws or “seasonal adjustments, or is poorly defined.

Some of it is seasonal with Black Friday sales and buying gifts for the Christmas holiday season.

Taiwan pm, our good friend, out !

Why does there seem to be no discussion, outside wolf’s update, of Powell selling off MBS into the market. Gee, just like selling a home, now would seem the opportune time to aggressively sell MBS to minimize loss to the fed and see how interest rates & inflation can be affected. The absence is telling.

Hi, I’m Matt Damen for crypto MBS, what say you Larry David “,pretty pretty good”. You just have to want to create the market.

Thank you for introducing me too the dark measures of the tragedy of credit. The dilemma is which set of data one chooses. From the curmudgeon to the spend thrift, all take measure of the economic winds.

I have an idea that the data you have presented is a portrait of a loan industry that has been funded by the Federal Reserve Bank of the United States of America. Overextended, but thankfully, still in the range of being able to pay the onerous cost living this new “Gilded Age” has engineered.

I overheard someone that was claiming that the entire credit card business is a loan sharking cartel, sanctioned by the various greased hands in the government.

I agree with you:

“What consumers cannot take for long is raging inflation.”

Inflation is cancer for an economic organism.

You have forced me to think up my own projections of what is likely to happen in the various bubble markets going forward:

Stocks – from my conservative POV, return of capital is more important than return on capital

Bonds – the longer the snake, the harder it bites. Holders of 30 yr treasuries have lost up to 35% after 15 years of dwindling income in their conservative account.

My wayward view is that the asset prices will decline long before the personal compensation and benefits of the 380 million people that constitute this great nation, increase to the level of family level wages.

I am destined to be wrong in a left handed way which sometimes I entertain the idea that that may be the way it really works.

What consumers cannot take for long is the Fed funds rate being below the inflation rate. This is what eats away at banks accounts.

There is no way around that without large scale debt default. Insufficient real production to pay positive rate, especially after taxes. “Real” rate in taxable accounts is even worse, but I never see this reported or discussed.

Will Tesla go bankrupt following law suits from purchasers who paid for unsafe car?

American electric carmaker Tesla is recalling 67,698 vehicles in China due to software issues, Chinese state media said on Friday.

According to China’s State Administration for Market Regulation, the recall includes Tesla’s Model S and Model X vehicles produced between Sept. 25, 2013 and Nov. 21, 2020, reported Xinhua News Agency.

China’s top market watchdog said the vehicles’ battery management mistakenly issue warnings, such as “maintenance required” and “safe parking” on their screen, which may cause cutting off power and lead to unintended collisions in some cases.

The electric car manufacturer will provide free software updates on the recalled vehicles.

I can’t comment on China’s lemon law, but in the U.S. the manufacturer has three attempts to repair the car before lemon law kicks in. If this isn’t a chronic issue (comes back again and again, despite repair efforts) and they offer to repair it, then there is no basis for a lawsuit until the three strikes occur for the same defect.

Each defect is a separate event, so if the malfunctions differ, the clock starts over.

“Buy backs” are not that common (usually one-offs) and when a class action is successful, the remedy is often a certificate for $X off their next vehicle. The lawyers are the only winners.

As I learned with Fords 6.0

That truck sure loved riding on a flatbed.

Wisoot,

A Tesla bankruptcy due to recalls? LOL

Ford just recalled 634,000 vehicles because of “engine fire” risks. Of them, 520,000 vehicles in the US and 114,000 in other countries.

All automakers issue recalls ALL THE TIME. No automakers ever goes “bankrupt” over recalls.

It’s a lot cheaper issuing a recall that is handled via an over-the-air software update (Tesla) than issuing a recall that requires dealers to replace engine components in 634,000 vehicles (Ford).

The Fed protect the banks. The Fed will never be NPL. The Fed will raise

rates, paying the primary banks $2T RRP at 5% an annual rate = $100B/y.

Experts are in full agreement that free money is the best kind.

To paraphrase P.J. O’Rourke:

“If you think money is expensive now, wait until you see what it costs when it’s free.”

Everyone who gets free money loves free money. It’s like manna from heaven.

The consequences of free money are another issue for others to deal with. And inflation is one of them, and now we suddenly have lots of it.

The interesting thing is that essentially no Americans have ever been privy to exorbitant inflation of the kind we’re experiencing now. we’re all learning on the job.

“What consumers cannot take for long is raging inflation.”

Hourly earnings fell 3% for workers in the United States from September 2021 to September 2022, according to a release by the Bureau of Labor Statistics (BLS).

No they did not. Average hourly earnings of all private-sector employees JUMPED 5.0% in Sep 2022 from Sep 2021. Average hourly earnings of production and nonsupervisory employees jumped 5.8% in September 2022 from Sep 2021.

But those year-over-year increases weren’t as high as those in the spring when they year-over-year increases were in the 5.5% and 6.5% range respectively. Those are the largest increases in decades.

They are only taking themselves down at this point-which is a real shame. They’ve done so much good as the world’s factory. I hope and believe they will come to their senses and leave COVID0 behind.

Question

What will the average person notice in their daily lives if we have a nationwide rail strike? It’s been a long time since we’ve had one, and I can’t remember what happened as a result.

Here are some points of impact, and there are many others.

The biggest consumer goods category transported by rail are new vehicles on their way from the factory or port of entry (including from Mexico) to the various distribution points around the country where vehicles are loaded on car carriers and delivered to dealers. So more vehicle supply issues if the strike lasts long enough.

Container shipments (intermodal) would shift from rail to truck, and that’s going to bring up costs of transportation further because more demand for trucking services increases freight rates. In addition, trucking may not be able to handle the extra demand, so more delays.

Then longer term, commodities will be disrupted (coal, wheat, chemicals used for production of goods, fertilizers, etc.). Many of them cannot be shipped by truck, and there may not be an alternative to rail. This will cause all kinds of problems for consumers further down the road if a strike lasts a long time.

A rail strike of a few days may not be noticed by consumers (though companies are going to cuss a lot), but a long rail strike would be noticed.

To add, I heard the average track maintenance worker makes $130,000/year currently. They want a 25% wage increase to $160,000/year, and 25 days of paid sick leave. The unions want it all or they are going on strike right before Christmas.

25% over 5 years, I think. So less than 5% a year.

Seems a bit stretch on your number. I have brother in law who left as engineer because at one stop in Wyoming a coal mine caught wind of his maintenance and welding skills and offered him much more and it wasn’t near the 130K, still great for that state though..

With household balance sheets still holding strong, which segments of the population are actually feeling a legitimate pinch due to QT or inflation right now?

I promise I don’t own a chain of pawn shops or payday loan centers, just trying to figure out if & when there will be actual pressure, and who will feel/is feeling it first.

And when folks do actually start to feel the pain, do the politicians start to subsidize/postpone rents & mortgage payments until we cross the choppy waters?

NPR breathlessly reports trumpet Black Friday sales “raked in a record $9.12B … despite inflation”. Despite inflation?? With 8% inflation they’re really down 5+% from last year in terms of how much people actually felt able to buy. But we’ll call it “a record,” right?

Nope, 8% inflation is NOT because of prices of goods. It’s because of prices of SERVICES, which are 2/3 of what consumers spend their money on. Prices of durable goods have actually come down. Prices of nondurable goods are mixed, with gasoline down some, and food still rising but more slowly. The big driver of inflation is SERVICES, and retailers don’t sell services, they sell goods. So you cannot apply 8% overall CPI inflation to the prices of the goods sold on Black Friday.

Read this about how inflation is now driven by services, and how goods are coming down, including consumer electronics:

https://wolfstreet.com/2022/11/10/services-inflation-spiked-to-second-highest-in-4-decades-would-have-hit-new-high-if-not-slowed-by-biggest-ever-adjustment-of-health-insurance-cpi/

I stand corrected on the point of how much people are getting for their money.

I would still note, however, that as the services inflation is driven by wage increases, which in percentage terms have, I believe, been significantly greater than the approximately 2% reported rise in Black Friday spending, NPR’s breathless “raked in a record $9.12B … despite inflation” is misleading. This appears to me as rather a sign that people are not spending on goods in proportion to their raises.

Was at the Mall this weekend and there were so many people.

The parking was pretty much full.

Our family are tapped out with spending. We can’t afford to spend

much more with everything going up and up. Where are the people

getting the money? Black Friday is not really that much discount from

normal. Just crazy. So much money around. We are spending and

consuming as if the world is infinite.

Thanks for the data to remind us all that there’s still way too much purchasing power for us to be in a death spiral. As you mentioned, the PPP bailout funds to many business owners that thrived during the pandemic or simply didn’t need it, eg Tom Brady. Then the record number of cash out refinances in 2021, only topped by 2007. And then the rapid fire on HELOCs this year. Tons and tons of purchasing power. I don’t believe Powell will be able to stem inflation with all of the money he created still sloshing around out there. Great article, thanks.

Looks like the Fed can do another 75 in December, no problem.

Am I the Only One??

Some 40 or so years ago, I was thinking it was time to build a house. Got a good buy on a lot from a friend who was going on vacation and needed some money, The lot was the last in a good subdivision and hadn’t sold because it was on a steep hill. So found a very good architect. Designed the house so I could add – didn’t have to use all my money initially. And borrowed some from my mother and with that and savings, came out debt free (except for mother). Lived there happily with no mortgage for 40+ years. Never once thought about what the house was worth; I just enjoyed living there. When the time came to move, I didn’t need the money and so gave it to Habitat. This not only let me have 5 years of very big tax deductions but I got to move out on my own time schedule and Habitat cleaned up and sold the house. No prospective buyers tromping thru, no big consults and redos with RE people, no having to keep clean all the time. So I recommend a house as something to love and inhabit happily and give with gratitude; not as a worrisome investment.

Late comment. Kind of off topic but…

There were some entries about a third thru the comments section about stuff being cheaper relative to income long ago, say 1970s.