But there won’t be an adjustment for the Fed-favored “core PCE” price index that will come out before the next Fed meeting.

By Wolf Richter for WOLF STREET.

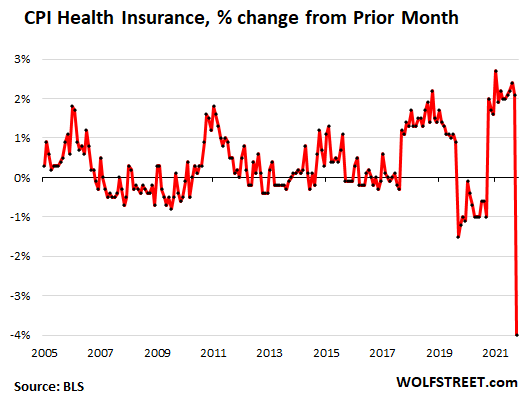

Let’s just start with inflation in services today because nearly two-thirds of consumer spending ends up in services, so this is the biggie. And some extra-special stuff happened in the CPI for services in October. What would come today was discussed over the past weeks in the Wall Street Journal and elsewhere, and it wasn’t a surprise: a massive mega-adjustment by the Bureau of Labor Statistics in the CPI for health insurance. And today it came.

Everyone knows that the costs of health insurance didn’t plunge in October from September. But because of the periodic adjustment, the CPI for health insurance plunged 4.0% in October from September, a 6.1 percentage-point swing from September (+2.1%), according to data from the Bureau of Labor Statistics today. This was by far the biggest month-to-month plunge in the BLS data going back to 2005, and far outstripped the adjustments in prior periods:

The CPI for health insurance accounts for 0.9% in overall CPI and for 1.1% in the Core CPI. And the plunge today pushed down the overall index, and even more the core CPI and the services CPI.

Inflation in health insurance is difficult to figure because numerous factors change, not just the premium but also co-pays, deductibles, out-of-pocket maximums, what is covered and what isn’t covered, etc., and there are all kinds of insurance plans out there.

So the BLS uses a different method to estimate price changes, the “retained earnings method,” which the BLS explains here, and once a year or so, it has to adjust the index as more data become available.

Normally the annual adjustment isn’t such a huge deal, but this time, the adjustment was gigantic.

The adjustment will carry forward for the next 12 months, meaning that health insurance CPI will be negative on a month-to-month basis for the next 12 months to work down the overstatement for the past 12 months.

Year-over-year, the health insurance CPI was still up 20.6%, but the year-over-year increases will be slashed for the next 11 months. It was also negative from month-to-month from August 2020 through August 2021.

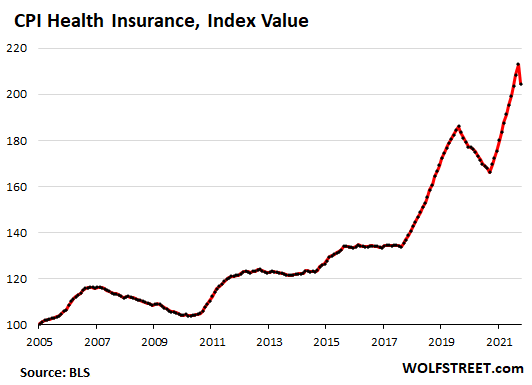

This chart shows the index value, which will continue to drop for another 11 months, until the next adjustment:

But no adjustment for the Fed’s favored “core PCE” index.

The Fed uses the “core PCE” price index as yardstick for its 2% inflation target. This “core PCE” price index uses a different and broader methodology, and it’s put together by a different government agency (the Bureau of Economic Analysis), and it figures health insurance inflation differently, and there will not be an adjustment.

It’s the lowest lowball index that the government produces, and we may pooh-pooh it, but it’s the most important inflation index for the Fed, and this “core PCE” price index won’t be adjusted in October. It will be released on December 1, just ahead of the Fed’s next meeting.

Services Inflation.

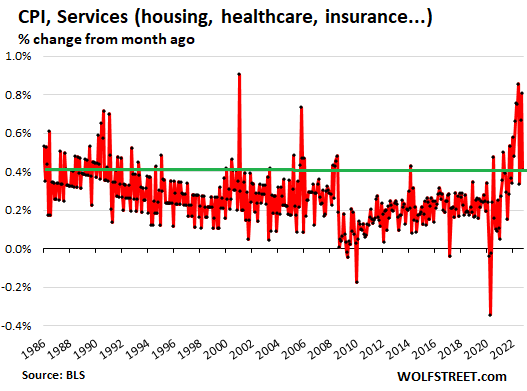

The CPI for services jumped by 0.4% in October from September, less steep than the 0.8% spike in the prior month, thanks to the massive adjustment to health insurance CPI.

In this chart of month-to-month changes of the CPI for services, note the large ups and downs from month to month, which is why you cannot conclude anything by just looking at one month:

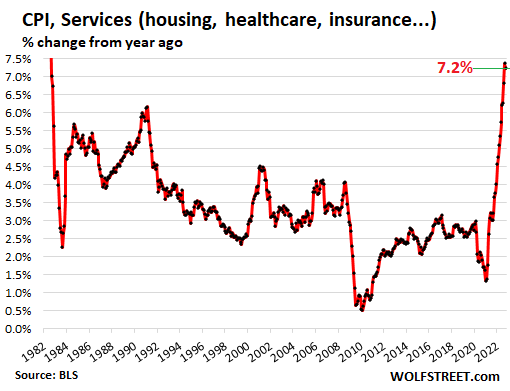

On a year-over-year basis, the services CPI jumped by 7.24%, just a tiny bit less than in September (+7.38%). Both are the worst since August 1982.

Without the health insurance adjustment, the year-over-year spike in October would have set a new four-decade record.

Services CPI by category.

The table shows the major services CPI categories in order of the month-to-month change, from the biggest increase (hotels & motels) to the biggest decline (health insurance). More on the housing CPIs Rent and Owner’s Equivalent of rent in a moment:

| Hotels & motels | 5.6% | 6.4% |

| Postage & delivery services | 3.6% | 4.2% |

| Motor vehicle insurance | 1.7% | 12.9% |

| Admission to movies, concerts, sports events | 0.8% | -1.9% |

| Rent of primary residence | 0.7% | 7.5% |

| Motor vehicle maintenance & repair | 0.7% | 10.3% |

| Video and audio services, cable | 0.7% | 3.2% |

| Owner’s equivalent of rent | 0.6% | 6.9% |

| Other personal services (dry-cleaning, haircuts, legal services…) | 0.4% | 5.8% |

| Pet services, including veterinary | 0.2% | 10.7% |

| Water, sewer, trash collection services | 0.0% | 4.8% |

| Telephone services | -0.1% | -0.6% |

| Car and truck rental | -0.5% | -3.5% |

| Medical care services | -0.6% | 5.4% |

| Airline fares | -1.1% | 42.9% |

| Health insurance | -4.0% | 20.6% |

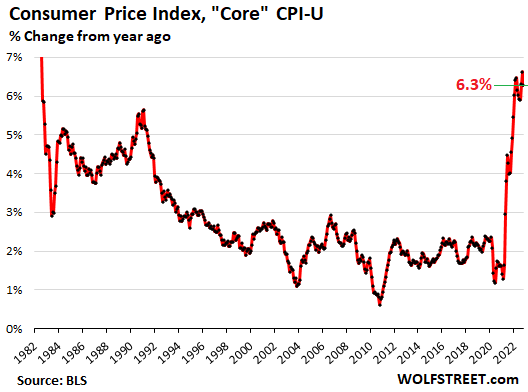

“Core CPI”

The core CPI, which excludes the volatile food and energy products, rose 0.3% in October from September, less bad than the 0.6% spike in the prior month, thanks in part to the massive insurance adjustment.

Year-over-year, core CPI jumped 6.3%, along with several other months this year, the worst since 1982.

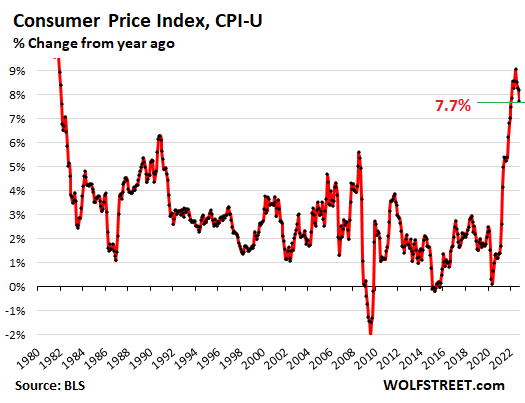

Overall CPI.

The all-items CPI rose 0.4% in October from September, same as in the prior month, and by 7.7% year-over-year, a deceleration from October.

Food inflation.

The CPI for “food at home” – food bought at stores and markets – jumped by 0.6% in October from September. Prices in some categories that had spiked wildly are now dipping on a month-to-month basis, such as beef. But others, such as eggs, are re-spiking. The game of inflation Whac-A-Mole

Year-over-year, the CPI for food at home jumped by 10.9%, less terrible than the 13% jump in September.

| Food inflation | MoM | YoY |

| Eggs | 10.1% | 43.0% |

| Fats and oils | 2.1% | 23.4% |

| Baby food | 1.8% | 10.9% |

| Coffee | 1.2% | 14.8% |

| Cereals and cereal products | 0.8% | 15.9% |

| Juices and nonalcoholic drinks | 0.5% | 12.7% |

| Alcoholic beverages at home | 0.5% | 3.8% |

| Overall food at home | 0.4% | 12.4% |

| Fish and seafood | 0.0% | 7.4% |

| Beef and veal | -0.1% | -3.6% |

| Dairy and related products | -0.1% | 15.5% |

| Fresh vegetables | -0.5% | 8.3% |

| Pork | -0.6% | 4.0% |

| Poultry | -1.1% | 14.9% |

| Fresh fruits | -2.4% | 6.6% |

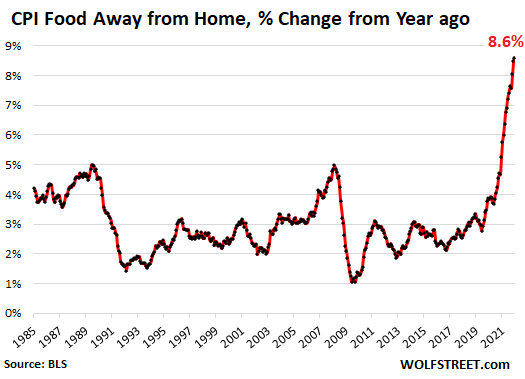

The CPI for “Food away from home”– restaurants, vending machines, cafeterias, sandwich shops, etc. – spiked by 0.9% in October from September, and by 8.6% year-over-year, the worst since 1981.

Energy takes off again.

After the decline in September, the CPI for energy products and services rose 1.8% in October from September, on rising gasoline prices and spiking heating oil prices. Year-over-year, the energy CPI jumped 17.6%:

| Energy | MoM | YoY |

| Overall Energy CPI | 1.8% | 17.6% |

| Gasoline | 4.0% | 17.5% |

| Utility natural gas to home | -4.6% | 20.0% |

| Electricity service | 0.1% | 14.1% |

| Heating oil, propane, kerosene, firewood | 10.5% | 44.2% |

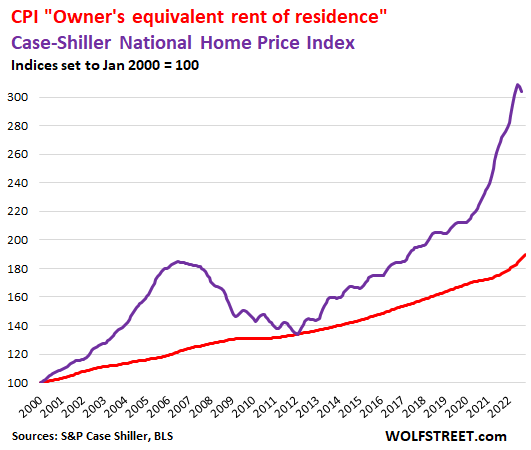

Housing costs spike.

The CPI for “rent of shelter,” which accounts for 32.3% of total CPI, tracks housing costs as a service, not as an investment asset. Its major components:

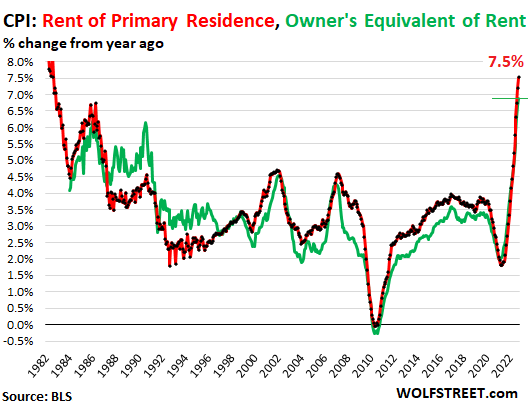

“Rent of primary residence” (accounts for 7.4% of total CPI) jumped by 0.7% in October from September. Year-over-year, it jumped by 7.5%, the highest since 1982 (red in the chart below). It tracks actual rents paid by a large panel of tenants, including in rent-controlled apartments.

Other rent indices, including Zillow’s rent index, are based on “asking rents,” which are the advertised rents that landlords want to charge future tenants.

“Owner’s equivalent rent of residences” (accounts for 24.0% of total CPI) jumped by 0.6% for the month and by 6.9% year-over-year (green line). It tracks the costs of homeownership as a service, based on what a large panel of homeowners report their home would rent for.

Home prices have started falling month-to-month, according to the most recent Case-Shiller Home Price Index (purple line in the chart below), which whittled down the year-over-year gain to 13.0% (read… The Most Splendid Housing Bubbles in America: Biggest Price Drops since Housing Bust 1. Record Plunge in Seattle (-3.9%), Near-Record in San Francisco (-4.3%) & Denver. Drops Spread Across the US).

The red line represents “owner’s equivalent rent of residence.” So, given how this worked out last time, this is going to be interesting to watch unfold.

Durable goods CPI.

The CPI for durable goods fell for the second month in a row, finally, after the spikes last year and earlier this year. Year-over-year, it was still up 4.8%, down from the 18% range earlier this year.

| Durable goods | MoM | YoY |

| Used vehicles | -2.4% | 2.0% |

| Information technology (computers, smartphones, etc.) | -1.0% | -10.8% |

| Household furnishings (furniture, appliances, floor coverings, tools) | -0.8% | 7.6% |

| New vehicles | 0.4% | 8.4% |

| Sporting goods (bicycles, equipment, etc.) | 1.6% | 3.0% |

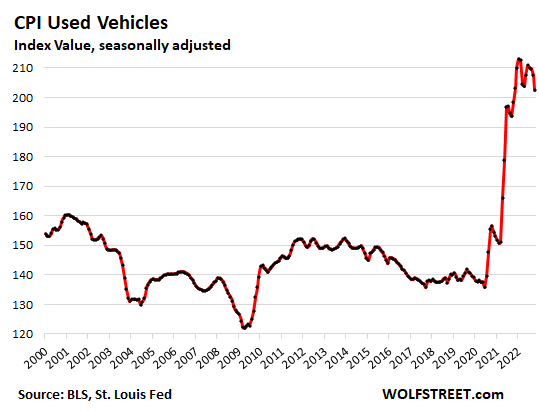

Used vehicle retail prices aren’t “plunging” or whatever.

Used vehicle retail prices barely ticked down from the ridiculous high level they’d spiked to in December 2021, and have remained largely stuck in the stratosphere, though wholesale prices are plunging:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Wolf,

You made reference to it but I didn’t see a specific number – do you know what the total YoY CPI % would have been without the health insurance adjustment?

Per Bloomberg:

Jonathan Levin Now, they want to celebrate a report in which medical-care services — the broader category including health insurance — single-handedly swung the month-on-month change in the index by 0.11 percentage point, moving from a seven-basis-point pressure point to four-basis-point drag.

This is how WallStreet read it. The inflation went down => Prices decreased! => Deflation Starts => Instant Fed Pivot => Massive Rally => Screw Short Seller Andy.

Couldn’t have said it better myself! There is no way in heck that Powell has the courage to not pivot. The entire economy is full of corruption. It has a very thin veneer of reality. The rest pure cat piss!

This Stupidity of wallstreet of dreaming of a Fed Pivot is what is causing the mainstreet to stop functioning.

Most people are working less because of one of the 2 reasons:

1. Either they have lost faith in value of labor as they realize that Fed prints trillions as they earn pennies and so inflation makes them poorer.

2. Or they are hoping for a recession where free stimulus checks and forbearance will start rolling again.

God bless America!

According to my calculations: If health insurance CPI had increased in October at the same rate as in September, YOY services CPI would have risen to 7.4%, eking past the prior month and setting new 4-decade high.

In terms of core CPI, it would have increased to 6.4%.

The soft landing that isn’t.

You can still pull out a ‘chute and make do. Just don’t look down.

You don’t hit the ground quickly, contrary to ALL your previous life experiences. Took me a while to overcome that….like Wolf’s cold water panic. And yes, you better look down when low.

Nothing goes to heck in a straight line in the air except when below 1000 ft at terminal.

Wolf,

so if you were single-handedly in charge at the Fed. What would you decide to do now?

We see right through your name “Andy”, or should I say J-Pow. I bet he lurks in these boards.

Keep going like they’re doing. Raise to about 5% or maybe a little higher and wait and see for a year. If after a year core PCE is still above 5%, go raise some more and wait. Keep QT on track, and sell MBS to get to the cap every month. This is going to take a while, and the current pace is pushing it already, as you can tell from all the volatility. Markets and the economy need time to adjust.

Wolf, and in answer to the very good question from andy:

Nah, IF and only IF FRB actually wants to ”show” that they, and their very clear owners, the folks who ”own” the banks and banksters WANT to at least try to ameliorate the damages “THEY” have done to WE the PEONs,,, in this case WE who have been ”willing, able, and ready” to DEFEND those owners,,,

“THEY” in this case the FRB and their owners need now to make US,,, those who have fought their battles on land, sea, air, and now ”space” at least ”good enough” to be able to retire in at least enough ”beneficence” to be able to live out our lives without being subjected to ”soup kitchens” for our food,,, etc., etc…

LOVE the WOLFSTERs very WONDERFUL WORK…

THE only one, so far, to which I am sending as much $$$ as I can because of honesty and thoroughness of work…

AND, BTW, reading on here, Wolf’s and commentary has probably ”saved us many thousands, SO FAR.”

Givem’ what Volker gaveem’

“The adjustment will carry forward for the next 12 months, meaning that health insurance CPI will be negative on a month-to-month basis for the next 12 months . . .”

I realize this is based on the BLS making a carry forward adjustment based on recent data, but everything I’ve read suggests that most types of insurance are set to spike next year, including healthcare. If the BLS is pushing the HC inflation down due to the 2022 adjust for the next 12 months while the real data for that period shows rising HC costs that could turn out to be a significant inflationary divergence this time next year.

Last, we’ve had 5 consecutive months of slowing housing and for the CS index to show the most recent data as “only” a 13% YoY gain is just absolutely mind boggling. One really has to wonder if these perpetual gains are ever going to turn into negative YoY losses.

JayW,

Yes, health insurance is going up.

What the BLS in effect said is that it overestimated the last 12 months. And it probably did: CPI health insurance was up 25% yoy in September, and that seemed way too high to me. Though some people might have gotten those kinds of increases, my wife didn’t, not anywhere near, and lots of other people didn’t because she’s covered by a HUGE organization. My health insurance actually dipped a tad. So that 25% yoy spike on average for all Americans, well, that seemed like way too high. So now it’s time to correct for that – that’s all this is.

I guess Medicare is going to stay same, $170?….and my Blue Cross Low Plan supplement never tells me till open season is well over.

Medicare Part B dips to $164.90 for 2023.

Wolf-

IMHO, the lack of health insurance inflation was a mirage: health insurance companies spent much less money in 2019/2020/2021 because the pandemic meant tons of elective and routine care was never done. And the government covered a lot of the Covid care expenses.

Obamacare regulations mean that when health care outlays go down, health insurance companies *must* lower their premiums (they are allowed a maximum of 30% of each dollar “overhead” that they can keep i.e. not disbursed to healthcare providers)

This will reverse in a big way in 2022 and beyond. Now that covid care is no longer throttling hospitals, all that deferred care will need to be addressed. And as anyone in healthcare will tell you, deferred care ends up being far more expensive (e.g. catching a tumor 1 year earlier is often far cheaper to treat, not to mention much better outcomes).

This increase in disease burden and delayed care will, IMHO, cause health expenditures to increase far faster than historical trends (at least for a few years), which will lead to higher than expected insurance costs.

Stocks rally, mortgage rates crater, even worthless crypto gets a huge bump right in the middle of yet another major exchange implosion. Mortgage brokers’ phones ringing off the hooks today, if online anecdotes are to be believed.

Don’t worry, though: we’ll have a whopping 50 basis point rate hike next month to calm these animal spirits down.

This ridiculous stock rally shows how desperate investors are getting to pump-and-dump before it’s too late to convince everyone of ghost pivots.

Stop shorting because this is how they take your money.

When I see the market react like that, I imagine Powell tearing out his hair wondering just how hawkish he will have to sound at the December meeting to stamp out this sort of nonsense.

Here’s what he looked like today, according to sources familiar with the matter:

The post-CPI jump today was obviously, clearly, algo-driven. Then other big money had to dance while the algo band was playing. Happiness for the pivoteers will be fleeting.

Powell lost trust of 99%. Now even wallstreet can defy him.

Now mortgage rates are crashing. Powell has lost control. FIRE JEROME POWELL.

Yeah but I would counter that by saying action speaks louder than words..if he doesn’t want this type of hopium action in the market, perhaps raising a full % point last time might have sent a stronger signal. He has to realize that his jawboning the other way is simply not as effective as when he was jawboning on the QE side.

Regardless of the wisdom or foolishness of a 100 bp rise in December, I think everyone has to admit at this point that the tough act at the press conferences is losing its effectiveness.

“the tough act at the press conferences is losing its effectiveness.”

Gee you mean a Fed guy with 85 million of personal wealth, with his lips moving in front of a microphone , is not to be believed ?

They believed him earlier this month, and they believed him after Jackson Hole.

I just have a hard time imagining the markets buying it again without action–specifically, a higher than expected rate rise.

Even knowing with high confidence what was coming, I froze and slid my mouse off the SP E-mini buy button once I seen the futures jump 2.5% in a few seconds due to 23,000 instantly filled contracts…HA

Completely Insane Day with only $123 million in margin to move the SP500 literally billions in a few short seconds after CPI release (23,000 contracts x roughly $6000 margin per contract)…

Yesterday I posted (yet still shocked/froze when CPI data released):

But beware Thursday early morning CPI data release, which is just another excuse for possible extreme volatility (profiteering) over macro inconsequential economic data flows…

Well… at least he has a full head of hair! That’s more than I can say.

Wolfstreet Meme :)

I don’t think he is tearing his hair out, but let’s suppose he is. The solution is simple- do a 1% or 1.5% hike at the next meeting, and forcast another 1% or 1.5% hike at the one following that. You get nonsense like today because we are convinced 0.75% raises are something dramatic. If the Fed retreats to .5% at the next meeting, we may get the S&P 500 at 5000 within a week following.

Powell is a complete failure. He should be fired. The anemic QT pace is a big part of the problem. Look how Canada has been rapidly reducing their balance sheet. Powell is like Chicken Little, but he talks a big game. Volcker my asz. He’s pathetic. There is so much money sloshing around out there that it’s sickening. Today was the epitome of the grotesque speculative frenzy this madman has created.

I don’t think the Fed is concerned with stock market reactions. To do so only distracts them for their core mission. And as you report periodically, a fairly high FFR for the next 18 months is going to push margin debt lower, making it less likely of this triggering a big sell off. They are, of course, concerned about bond market liquidity which puts the QT runoff squarely in focus in the first six months of 2023. That’s where the real hazard awaits.

IMO, it’s really starting to look like services will remain mostly unaffected by a terminal FFR of 4.75%’ish. As such, the economy may only shed significant jobs in first mover industries like mortgage originators, on-line auto sales / lending, & technology companies that hired too many employees. The broader economy may well skirt meaningful layoffs, IMO.

IMO, the final outcome is mostly dependent on IF the Fed is forced into pivoted sooner rather than later with regards to QT. And last, I think the Fed must do everything it can to keep the 30YFRM above 5%. If it dips below 5%, I see housing stabilizing without any significant price reduction nationally, meaning the egregious housing affordability problem remains on the backside.

The Fed will not achieve housing price stability without a significant decline in home prices. What the desired final % is only the Fed knows. To me, it’s a least 20% with a minimum 5% 30YFRM on the backside.

This entire mess is about home & bond prices. The stock market doesn’t really matter.

Absent the logical continued market downtrend that portends badly for pensions and middle class 401k’s etc… JPow gets the perfect cover to raise rates with abandon.

I agree staying the course on rates. Keep raising. Would not like to see MBS selling at a loss. Let that be.

Pundits talking Santa Clause RALLY into year end. BOOM TIMES!!

Harter Verbrecher!!!!!!!!!!!!!!!!!!!!!!!!!!!

Seems like if you are a peon like me and don’t know how this is going to play out that the best risk adjusted play is to keep most funds at the short end of the Treasury curve so you are liquid and so Fed policy can’t strike you with a fatal blow with high inflation or severe recession.

Only way you miss out is on a soft landing, but chances of that are slim.

“we’ll have a whopping 50 basis point rate hike next month to calm these animal spirits down.”

Funny how the mainstream media will (incorrectly) call this “unprecedented” over and over, while NIRP has never been mentioned.

Gold prices up as well. Gross margins for gold miners back above 30%. Barrick is my only stock, but I lightened up yesterday as I think it’s still a bear market rally.

Pea Sea

“a whopping 50 basis point rate hike next month to calm these animal spirits down”

I doubt that.

The expected Santa rally will keep the indexes keep going up. Algoes and Money mangers (MFunds,Pensions) will jump into year end rally. The siren song from Wall St will make sure of it.

Why is Wolf the only analyst willing to identify and highlight important issues like the medical services adjustment that skewed the CPI comparison?

Most Wall Street analysts are lazy and know nothing. Listen to them, if you want to lose money. Even when they aren’t lying, they are cherry picking data.

Most financial reporters are young and clueless (waiting to be replaced by AI software). The media outlets got rid of their old fossils that knew this kind of stuff and that could have coached the young ones.

Good analysts and good reports know. But I guess they didn’t want to be party poopers.

ZH had an article yesterday, reprinting stuff from Goldman that outlined what would happen today. The Wall Street Journal ran an article two weeks ago, citing some experts that discussed some details. I saw other stuff in prior weeks.

But today, no one wanted to spoil the party.

Wolf here in Nebraska eggs are up 100%+, coffe up 3.99 to 5.99 both on sale .But maybe we’re just not average

At my Ralph’s supermarket (Laguna Hills CA), sliced Turkey (Boar’s Head of course) has risen from $6.99 lb to $13.99 lb.

Boar’s Head Roast Beef, sliced, has risen from $8.99 lb to $17.99 lb.

@gary,

If people stop paying those prices, prices will stop going up.

So when we see these type of inflation numbers for food, cars, services. Why will housing drop and food prices will not? I just had my truck transmission flued changed and it was $289. 5 years ago it was $199.

I get that housing is overvalued because of the 3% interest rates allowed people to take out a bigger mortgage than otherwise. Cheap Wall Street money, plus the WFH, and of course FOMO.

But it appears inflation will stick around. Maybe it has peaked but it will not go fast.

I do think some of the bubble prices in housing will drop. But how far will they drop if we still have high inflation over the next 5 years. Most people on this board say housing it will crash yet in my neck of the woods, I am seeing price reductions but only a 5% drop in price at the most. Things that go into maintaining or building a house are much more expense than 4 years ago.

Bank of America thinks inflation will stick at 5% for the next 5 years. Lets be conservative and say 4%.

To build a $400k house in 5 years at 4% inflation will mean that it will cost $486k to build the exact same house.

I am thinking out loud but how can we have goods, services, and salary inflation yet no house inflation.

“But today, no one wanted to spoil the party.”

Just really, really disingenuous and gross. The DOW is essentially all the way back to the peak in August after the pivot rally of the summer. That quickly. All-time highs are not far off. ALL THE SPECULATORS expect 50 basis points next meeting, then a FED pause, then it’s blastoff to the moon for asset prices.

I think you’re underestimating the effects these rate increases will have. There are so many companies out there that are dependent on cheap financing, not only for operations, but for buybacks, and the increased cost is going to wreak havoc on their income statements.

I work at the outskirts of the capital markets. I can tell you affirmatively that while capital is still available for good companies, it’s available at much higher prices, and it’s not available at all for zombies.

These things take time.

Because Wolf is not beholden to Wall Street to maintain the PIVOT narrative

Jim Cramer was on CNBC this morning and he must have suddenly found Jesus. He actually said to “SELL INTO THIS RALLY”!

I couldn’t believe it!

Harry Houndstooth would also like to document his advice to sell this classic sharp euphoric bear market rally.

Buy STRY and SQQQ at 46.

Correction

SRTY and SQQQ

Oh, BTW, if they get closer to 40, especially in the premarket, back up the truck.

Be fearful when others are bold.

Be bold when others are fearful.

Cramer might have seen that financial conditions eased by 50 basis points Thursday, the third largest decline on record, per Nick T – WSJ:

Goldman Sachs reports that its intra-day estimate of U.S. financial conditions from its financial-conditions index eased by over 50 basis points today following the rally triggered by the October CPI print. That is the third-largest single day decline on record.

haha that took us by surprise too, even Cramer was catching on to the total lunacy and manipulations when it became clear that the algos had gone into total meltdown mode, the gyrations esp in the NASDAQ yesterday were equivalent of a gigantic computer glitch in the software carried out on the scale of a national market. (And from what’s basically a CPI data artifact like Wolf is saying) Anyone still holding or buying into this overinflated equities stupidity after the weekend is a fool and begging to be a bagholder. The equity markets have been utterly ruined as a source of price discovery and valuation by all this central bank manipulation and algo-driven investing, but yesterday showed just how broken and dangerous it’s becoming. The most worthless companies, some teetering on bankruptcy were the ones that often gained the most on Thursday, not to mention crypto and NFT’s including the coins that even the crypto-bros mock. Complete, utter disconnection from reality, and with the NASDAQ swings someone could post up an openly fraudulent company losing billions of dollars and it’s value would moon. The Fed has to get even more aggressive in throttling this or the dollar will soon become a worthless token, and even Cramer is realizing this.

Miller

“the dollar will soon become a worthless token”

Dollar is definitely losing purchasing power but never become token in the near future. Read what’s necessary (a long list) to become global/commercial trade currency’

TINA!

Good point.

Is health really just 0.9%? I would have thought more like 10%!

A lot of consumers are not paying for health insurance; or are paying only a small part of it. Their employers and the government are paying the rest.

In terms of the weights, this is the “consumer” price index, so the basket of goods and services that consumers are actually paying for directly.

Medical costs are 8.5% of CPI-U. “Health” insurance is separate, it’s what the insurance companies make after paying medical costs, and is 0.8%. So the total cost of medical care and insurance seems to be 9.3%.

Health insurance weight in overall CPI = 0.918%. It’s included in “Medical Care Services,” which weighs 6.89%.

Insurance is just not a big part of what most Americans pay for healthcare. That includes all the people on Medicare that pay $170 a month. It’s all the other stuff that adds up, from deductibles and co-pays to stuff that isn’t covered.

Medical care services (weighs 6.89%) is composed of:

— Professional services: weighs 3.46% which includes physicians (weighs 1.8%), Dental services (0.91%), Eyeglasses and eye care (0.36%), other medical professionals (0.38%)

— Hospital and related services: weighs 2.51% (Hospital, Inpatient, Outpatient hospital services)

— Nursing homes and adult day services: 0.21%

— Care of invalids and elderly at home 0.16%

— Health insurance: 0.918%

https://www.bls.gov/news.release/cpi.t02.htm

We can frame USA health care costs in terms oF $/person/yr and $/family/yr.

Family of four guesstimate:

+ $48k/yr health care

+ $20k/yr k-12 and college, 2 students

Operating and financial solutions are needed for health care.

That’s an entirely different issue than inflation, and the portion that consumers pay.

We have never paid the amounts anywhere near that you mention. Not even close. I have no idea what kind of platinum-plated gold plans you have in mind.

Get a high-deductible plan with an HSA (big tax deduction), where the tax savings will pay of part of the plan costs. Bush-era stuff, works really well, if you know what you’re doing.

My employer plays out ~$12K-$15K for family coverage for a decent (but definitely not gold plated) plan. We pay around 10%, but it depends on the plan.

The top plan with the best benefits is quite expensive to the employee, but since we don’t use the services unless we have to, we’re on the high deductible HSA plan, which is way cheaper — I like putting money away into the HSA every month, and have enough socked away already to cover the deductibles if needed.

After last year massive increases in deductibles and many other shenanigans, like tier 1 , tier 2, co-insurance, maximum out of pocket increases, selective coverage of brand medications, limited access to hospitals I got this year 12% increase in my plan. They do not pay for anything since I rarely go to the doctor. When I need them, I pay out of pocket since my deductible is just outrages. It is like catastrophic hospital coverage. I am self employed and I buy my own health insurance. I live in NJ and it is supposed to be a good state where almost everyone is insured. Before “Obama” care I paid way less for the same plan.

LL, i had the same type of health insurance, bought an individual policy as a consultant a few years ago. Let me share from my experiences which make me such a cantankerous old goat.

The US annual health insurance contract is actuarially jiggered to increase more as you age up to Medicare (65). From 55 to 64 the policy crept up by 10 to 20% per year despite my deductible and catastrophic-level coverage. Every year a ridiculously ludicrous increase for an ever more tilted playing field. Location can influence premium.

By the time I hit 64, for the cheapest PPO policy with hIghest copay, the monthly premium was equal to leasing two Mercedes or Lexus luxe chariots.

IMHO, at 64 You pay $1k/mo more than younger insureds for the same level of health care treatment. Healthy folks like me who don’t meet annual deductible due to fewer services really get screwed.

Although insurance covered 97% of charges related to my quintuple bypass at age 60.

I would be living in a tent today without carrying health insurance back then, probably.

It might not be quite as bad as you describe in the individual market today since the ACA subsidy cliff was fixed… through 2025. After that, who knows?

Obamacare certainly didn’t help but tbh the health insurance premiums and deductibles calculations was a mess even before ACA, and were going up for all kinds of reasons. It’s kind of like the equity markets these days, no longer a free market at all but some kind of Frankenstein mess of monopolies and oligopolies, with both government interference and coercion and crony capitalism from the most corrupt companies, a mix of the very worst parts of socialism and rentier dysfunctional capitalism. Healthcare costs in the US are an out of control train without brakes picking up speed and heading straight for a cliff, it’s going to take major surgery to reign them in any significant way

Christmas came early for the pivot crowds today…WS was jizzing all over themselves today…Beyond Meat up 20% and earnings were crappy…you really can’t make this crap up

The horses and cattle eat better food than Beyond Meat. Its mostly soy bean meal. Nothing on Alex Vieira’s youtube channel about Beyond Meat he’s usually the main shareholder with his AI buy signals.

I tried beyond meat. It tasted good and gave me severe indigestion. Never again.

Don’t forget sodium. Lot’s of sodium. You can hide a lot of nastiness with salt.

I use to eat at a Chinese Resturant back in NZ and I would be thirsty for days afterwards

MSG. Post Chinese food I sometimes got really wild dreams. Glutamic acid. And in jail they sometimes had spaghetti with “sauce”, but no Parmesan cheese….just a huge can of pure MSG and the career types really piled it on. Worse food than the Army, which I didn’t think was possible.

Always welcomed PB&J either place.

PB by law has to be 90% peanuts…hard fought battle.

But beware Peanut “Spreads”!!!! Like lo-fat what appears to be PB. Can be anything.

PB still the main part of my diet, but no jelly, and good double fiber bread. Some moo and that is IT!. Plus a multi vit and 1000mg C.

I’ve been “beyond meat” personally for over 30 years, and didn’t eat much before. Mother even told me in grammar school I was going to turn into a peanut.

So far so good….well over 75….no meds except tramadol for W-2 back. I live cheap.

It’s interesting to look at the consumer price index itself, not the annual percentage change or the monthly percentage change, but the underlying index. You can see it at FRED. It is very difficult to see any recent progress in the inflation fight in recent months. The line has a straight upward slope spanning multiple recent months. Moreover, it follows a multimonth period during the summer when the line had very low slope. Looking at this data it appears that inflation is well entrenched and worse than it was recently.

… “Without the health insurance adjustment, the year-over-year spike in October would have set a new four-decade record.”

Hopefully this mean the Canadian CPI will come in hot as there’s health insurance component.

Hopefully this mean the Canadian CPI will come in hot as there’s NO health insurance component.

Rewritten

Here you go:

Thanks Wolf. Blowing up the right end shows what I was trying to explain. Derivatives in noisy data are dangerous, even when low-pass filtering is done (and I’m not sure it’s ever used in economics, though they do perform some averaging). Derivatives at the end of a record are always nasty. This is why it can be helpful to look at undifferentiated data. I see strong inflation in this data, perhaps lower than a year ago, but much higher than this past summer, and no evidence of a recent decline.

Thank you for your contribution to sanity. President Biden’s remarks today about inflation are in stark contrast to a sub 4% 10 year yield with an artificially suppressed CPI of 7.7%. Those souls who have consistently and methodically perused this website have the confidence to sell into this explosive bear market rally for their betterment.

Up to now, anyone selling into this bear market rally is likely regretting it.

There were three market moving events in recent trading days. The market was disproportionately knocked back by the first two and rose disproportionately yesterday. The S&P 500 reached 3900 prior to being buffeted by these scheduled events.

The scale of the impulse pushing down bond yields in response to a modest attenuation in inflation was noteworthy.

If downward moves in bond yields outrun downward adjustments to the rate of inflation, the Fed might regret climbing down from 0.75% increases. What will be the yield on the 10-year at 7% Overall CPI inflation.

Is good news going to be bad news for the Fed.

Stories move markets more than fundamentals, and Thursday was a really good story of theoretical “peaks”…

That said, I’m guessing the Fed won’t like the fundamental fact that financial conditions are easing at record pace due to falling dollar, falling yields, and skyrocketing risk assets…so the Fed may need to create a new story to replace the current story in the next few weeks…especially if the SP500 blows past the 200 SMA and reaches the 13 week highs and takes yields and the dollar further down in the process.

The entire financial construct is trapped in a perpetual feedback loop, and any earnings collapse and/or the resulting depth of the current/existing recession will further complicate the Feds job of creating future financial stability…

Good Luck Fed…pick our story wisely…

Maybe it made Wall Street and the folks in BLS feel better, but I sincerely doubt health insurance has slowed down based upon my admittedly anecdotal experience.

My number is closer to 16% per year which is unsustainable over the long term. And I know at least the copay for MRIs didn’t change from year to year. :)

My guess is there are many people seeing unwelcome surprises in their benefit selections at work where they will be expected to contribute more to their 2023 health insurance.

“health insurance CPI will be negative on a month-to-month basis for the next 12 months to work down the overstatement for the past 12 months.” and “the CPI for health insurance plunged 4.0% in October from September”. So 12 months at -4% equals a total of -48% for the year. And if health insurance rose 24.6% over the past 12 months (20.6 + 4.0) that would mean it should have decreased 23.4% over the past 12 months instead of increasing 24.6. It doesn’t make sense to me. Maybe I’m missing something?

“So 12 months at -4% equals a total of -48% for the year.”

That’s now how it’s going to work. It’s going to whittle down part of the year-over-year increase of the past 12 months.

Look at the second chart for the period August 2020 to August 2021. It will look similar. The big month-to-month adjustment was for October, and future month-to-month adjustments are going to be smaller.

Thanks.

So the inflation numbers for health insurance can still increase each month net of the monthly downward adjustment, correct?

No, the health insurance CPI will decline every month for 11 months, but not by today’s huge amount.

My Medicare Supplemental insurance has been increasing by 20% each year for the past 4 years. This September, another 20%.

Reiterating the obvious, inflation is not going to come down quickly until the interest rate is above the inflation rate. Powell is HOPING inflation will be drawn down by a higher interest rate. That will probably work over time, but since inflation is 7.7% and the interest rate is 4.25%, the gap is larger than optimal. It will take (guessing) 24 to 36 months, for inflation to be tamed with Powell’s approach.

Going back to Sept, Powell stated unequivocally the increases were going to be on the order of 0.75% (Nov. – done), 0.5% (Dec.) and 0.25 (or .5% in Jan. -depending on progress.)

Whether jiggering the statistics counts as progress… well, you decide.

Unless something is done to increase productivity increasing interest rates at these puny amounts will do nothing to tame inflation. A lot of businesses especially services like Comcast, Verizon, AT &T are monopolies and they will just pass on the increased cost of doing business to the consumer. I use all three. They keep raising their rates, and I keep paying it. They suck but I have no alternative. The result will be more inflation created by the higher interest rates.

Where’s musk when u need him hahahahaha

Try Google Fi.

Including taxes/fees, I average $75/mo total for 3 mobile phones. Service is as good as any.

I also have Comcast, but I don’t have to pay Verizon/ATT prices for cell service.

Same problem for me Swamp, and exactly same bunch. All low plans, but still they keep creeping up. Pay way more for them than I do food, which, simple as it is, I’m totally fine with. I eat once a day, so no “what sounds good” problem at all.

FOOD sounds good.

JPow said the Dec and Jan increases were up in the air, he originally said Dec would be 0.5 but that’s why his tone got so much more hawkish at the last FOMC mtg, he said Dec absolutely could go up to 0.75 and be higher than expected after that. The calculation of the rates relative to inflation is complicated by the role of QT and the reverse repo’s along with the rates, but still he now has every reason to push the rates even higher. The Fed very much kept that option open at the last mtg

Re ” inflation is not going to come down quickly until the interest rate is above the inflation rate.”

That used to be true, back when money supply was tightly tied to the interest rate. Until very recently, tightening rates also tightened up the money supply. The rates get more media hype, so now everyone thinks it’s the rates that matter, but that could be very very wrong.

Today, rates and QE/QT are independent knobs. It may take more than just rates to rein in the inflation.

Well, my health insurance quadrupled so I don’t know if those numbers are right. Making me wonder if it is time to sell everything and move out of the country. Getting close to retirement and was not expecting a new mortgage payment at these costs.

There has never been a better time to move to Latin America or a cheap European country like Portugal. Your quality of life will be so much better.

There was a better time for me 2015 and my quality of life is tremendously improved Im in SW Turkey no mortgages , very inexpensive healthcare and no property taxes Now if they could only get the inflation under control

BTW, inflation is closer to 10% if you back in the jiggered statistic for insurance (and yes, my insurance rose by about that too….)

I knew they’d dream up some voodoo magic right before Black Friday sales and the Christmas reason. There would have been yearend profit taking by the shorts on stocks and yearend profit taking on the dollar by the shorts. I figure the stock market should drop about 12 percent in the month of January 2023 to make up for some of this. I’ll be in heavy short at the very end of this year.

Nov 10, 2022.

Today’s moves are a thundering endorsement by Mr. Market of both stocks and bonds anticipating the return of the Fed Put.

Mr. Market believes that the Fed will return to a 0% Fed Funds Rate and expansion of its balance sheet as the economy slows, unemployment grows, credit declines, Treasury liquidity continues to tighten, and Fiscal spending rages on in 2023 (even with inflation somewhere above the 2% target).

Is Mr. Market correct?

Impossible so say.

Time will tell.

Then the dollar is destroyed. That’s not what the Fed wants.

A 6% rally off of manipulated data (as Wolf Richter has documented) is clearly a classic bear market rally giving us the opportunity to profit quickly, efficiently and safely.

Don’t get greedy.

Great article and comments. Erased my confusion and FOMO in seconds. Heaps of useful context to make sense of a blizzard of weirdness.

My Dental insurance did not go up very much at all. They have been good a keeping premiums reasonable. I’ve been getting back way more than my premiums. I’ve had them since 2011 and they were part of the Federal Employees Network of insurance providers.

1) The markets popped up, so did TY, demand for 10Y note is rising.

NDX banged a cloud. AMZN in the morning was up 15.5%. AMZN might be doing an new Anti BB.

2) Next year, y/y, the CPI, the core CPI, rent, rent equivalent… might be

negative.

3) Next year, y/y, the CPI might still be above fedrate.

4) Next year y/y US gov debt might be 20% higher.

5) Next year, y/y, the Dow might be negative. Today the weekly Dow hit Aug 15 close. It’s down only 9% from Jan peak. That’s not good enough for The Fed.

We’re already seeing the wage-price spiral so fairy tales likely won’t occur. No more “and they lived happily ever after”.

I do not think inflation will come down quickly even if interest rates are above inflation. The reason is that interest rate increases reduce spending in the interest rate sensitive areas: housing and autos. Downturns in these cause layoffs and orders cut to many suppliers who in turn reduce production and lay off workers. Then the big demand thing that drives GDP, namely consumer spending goes down and we get a recession.

With a huge shortage of workers in construction trades, any laid off workers by builders will get hired elsewhere. Auto demand will also be slow to go down given we have underproduced millions of autos due to parts shortages the last few years. So little rise in unemployment means consumer spending keeps growing and inflation continues.

Also, when the dollar exchange rate eventually starts falling, that raises the price of imports which in turn lets domestic industries raise prices.

We are in for a repeat of the 1970s.

“We are in for a repeat of the 1970s.”

No, we aren’t.

Your comments didn’t fully consider financial conditions. Rising rates will impact housing and autos first but tightening financial conditions will do a lot more than that.

If the mania is over, then stock prices will actually tank “soon” and it’s only a matter of time before C-Suites issue pink slips in mass and the fake wealth effect reverses with the top 5% who account for most “growth” cut spending noticeably. That will solve the labor shortage, in spades. This isn’t directly connected to monetary policy or inflation either. It’s psychological.

Currently, I’m on the fence on whether the stock mania is actually over (it should be) but the bond mania ended in 2020.

Without low rates and ultra-loose credit conditions, the economy sinks.

There may still be an inflation problem anyway, but it’s not going to be with a labor shortage and unlike the 70’s living standards are going down too.

Demographics is also irrelevant to the labor shortage because it isn’t the actual cause, it’s a secondary factor. No one ever retires because they reach a certain age, only because either they have the resources or someone else provides it. The reversal of the wealth effect will force potentially millions back into the labor market, assuming they can even find a job.

No comparison to the 70s We didnt have 31 Trillion in debt back then and China and Russia were still basketcases economically BRICS werent a thing and Saudi Arabia was still basically a US protectorate Things are going to heck faster than I expected

What about the CPI-W, which is the inflation measure for 65 million Americans? Why is that not listed and discussed?

What about the huge increase in social security stating this January?

Swimmer,

Because it’s irrelevant for our purposes here. It’s used for SS COLA, but that is determined in Q3, which is finished, and I covered the COLA and CPI-W a month ago. The only time we care about CPI-W is in July, August, and September because the average of those months determine next year’s COLA

https://wolfstreet.com/2022/10/13/social-security-cola-for-2023-biggest-since-1981-might-finally-outpace-inflation-in-2023-unless-inflation-dishes-up-more-surprises/

Dollar down, equities up, shorts on fire. But if your home currency is sterling or Aussie dollars, say, then the price of US equities in the home currency doesn’t change that much (after things settle down). However, it’s my guess that US equities will keep going up – at least until the 1st Dec PCE numbers. (Thanks for the CPI/PCE info., Wolf.)

Wolf,

Is the Dec. 1st release a typo? BLS shows release on the 13th?

Not a typo. You’re looking at CPI released by the BLS. I was talking about “core PCE,” which is released by the BEA (Bureau of Economic Analysis) on Dec 1.

Thanks!

Wolf, in the eighth paragraph, you talk about YoY twice in a row – is that second one supposed to be MoM? If not, could you explain what you mean by ‘slashed for 11 months’?

Also, first table lacks column headings, I presume they’re the same as the other tables…

The paragraph is correct as is. It’s a complex issue. And I tried to be clear. You might have to read it one more time to see it.

At least part of the market seems to think that when inflation stops going up, the problem has gone away. Wrong; if inflation stays where it is, we just have entrenched, self-reinforcing inflation, at 7%. That’s not what Powell and the Fed are supposed to be aiming at, and are not what they are saying they are aiming at. What they say they are aiming at is price stability, which they interpret, very debatably, as 2% inflation. Now whether they will actually take the actions required to shove inflation back down to 2% remains to be seen. Some would think that will require a long recession, and for decades the Fed has been chickening out, and dropping rates, at the first signs of recession. That’s what the other part of the market is focusing on. But both parts are screaming buy buy buy.

1) NQ is back in May 12/17 trading range. NQ entered the cloud (9,26,52), above Oct 25 high.

2) Creepto is dying, but DX is crying, down under Sept 7/13 trading range, a spring.

3) The German 1y is 2.25, the 10y is 2.046 and the 30y is 1.99. Gravity

is pulling them together. US long duration down and the German UP. Distortions in the German yield curve shield the bad economy in Germany.

4) The Dow is only 9% from the peak, JP will not retreat. Madam ECB will

follow his footsteps. The front end of the German yield curve will popup and the long duration further down.

5) Black Friday is two weeks from today.

1) EUR/USD is 1.021 > Sept 12 high. The Euro is booming.

2) Many currencies are circling DXY like a moon. They can go up and down, but rising with the dollar since 2008 nadir.

3) The real estate markets in many countries, including in China, is falling y/y, but in dollar terms, when the dollar reached 115, they are still stable, or falling less. Rent/Prices suck all over the world.

4) USD/CNY was down from 8.3 in the early 2000’s to 6.01 in Jan 2014.

In 2014 the Fed started raising rates. USD/CNY is making higher highs and higher lows, well below 8.3. USD/CNY is testing Sept 2019 highs @7.3, but Nov 2022 isn’t over.

Interesting. It’s good to get some realistic details about the inflation data.

In Germany we had 10.4% inflation YOY in October after 10.0% in September. They said the biggest increase since about 70 years. They say we should be below 10% in March with the help of Government price cuts for energy.

This huge bounce in the SP500 yesterday was amazing but exactly what to expect from time to time in a bear market.

“They say we should be below 10% in March with the help of Government price cuts for energy.”

Another gimmick.

It should be self-evident that this is only a temporary measure and is ultimately unsustainable, as eventually the “printing” (from deficit spending) will lead to more inflation.

Hiding the costs by sticking a portion of them on someone else’s ledger doesn’t make them go away.

But it does discourage additional production.

If there isn’t a rapid return to normality, this approach just makes everyone poorer…. Soviet Style.

More inflation for sure. We add to debt during normal times and we add to debt during an emergency like we have one today.

At least the debt levels in Germany are relatively low if you look at the EU.

Great work. But if you look back, the CPI is up 9x since 1967.

This is absolute joke. Powell is crying out saying that he will hike interest rates, but market pundits are grabbing on any small bits and working against him. It’s like almost a week after the fed hike the market tanks, after that it keeps going up for the next 11 weeks.

If FED has to send a message, the 75 and 100 basis point hike won’t work. But then will the economy be able to take anything higher than that?

“If FED has to send a message, the 75 and 100 basis point hike won’t work. But then will the economy be able to take anything higher than that?”

There is a difference between rising rates and tightness of credit conditions. That’s what most people (not necessarily you) don’t understand. Rising rates are only half of the equation.

As long as someone will continue to lend to these (sub)basement quality borrowers (which is most people and companies in the US), monetary policy will not be completely “effective”.

This is psychological, not a mechanical outcome from pulling “levers” from monetary policy or anything else.

I work for a small/mid size manufacturing company in KY.

This open enrollment period, HDHP family plan went from $19,707/year to $22,977/year, 16%+ increase.

My employer covers more than 90% of the cost for HDHP plan.

In fairness, premium didn’t increase the past two years, so I guess this could be a catch-up increase.

It’s still a significant YoY increase nonetheless considering my pay hasn’t been increasing in proportion to inflation.

My real earnings continue to erode.

The annual cost of housing for most households in KY has to be less than $23K, probably noticeably less. This is for everything, including utilities.

The cost of living in Kentucky is 11.4% below the national average. And, we have pretty horses and fast women.

If you think about many of the drivers of inflation – stimulus checks, student loan payment pause, tidal wave of cash out refinances, lowered monthly payments resulting from mortgage refinancing, perceived wealth increase from surging home prices, lowered commuting costs via a surge in WFH, etc, etc, some of these drivers have faded or will fade while others will remain sticky. This perfect storm of demand side drivers clashed with supply chain chaos to get us where we are today. Higher borrowing costs and increased unemployment (huge X factor) should work concurrently with some of these fading background demand drivers to significantly cool inflation. Will we collapse back to the fed target of 2%? Unlikely. But I’m not sure the fed will have to raise rates much beyond 5% before we see inflation correct in meaningful fashion.

Agree, Josh. There’s no magic lack of effect if rates are lower than current inflation. They are two related but separate things.

I got this e-mail from Home Depot. I need to replace my 35 year old electric stove. I’m going to take the free money and buy a new one that looks exactly like the one I have.

“No Interest if Paid in Full Within 12 months† on purchases of $299‡ or more. Interest will be charged to your account from the purchase date if the purchase balance (including premiums for optional credit insurance) is not paid in full within 12 months. Valid now through 11/19/22.”

I’m guessing they bank on lots of buyers to forget or blow off paying it off before the year is up. And then…bam…what, 21%

And retro for the prior year of unpaid interest as well…

JP : the long duration indicate future inflation. Inflation will be lower…

Wrong : the long duration is pulled lower by the German yield curve,

dragged lower.

40% of the CPI is shelter. And shelter is a lagging indicator.

Read the article – the section titled, “Housing costs spike”; it tells you where you’re wrong

1. The housing-related components of shelter — “rent of primary residence” weighs 7.35%, and “owner’s equivalent of rent” = 24.0% — for combined weight of 31.3%, not 40%. This was spelled out in the article.

2. It’s NOT lagging any more than other CPI categories, for the reasons spelled out in the article.

“Rent of primary residence,” as I said in the article, “tracks actual rents paid by a large panel of tenants, including in rent-controlled apartments.” It shows how their actual rents changed over time (the same people get asked over and over again over a span of years).

But Zillow’s and others rent figures are “asking rent” — advertised rents of vacant units. Hardly anyone actually pays asking rents. It’s what landlords want for their vacant units. Asking rents are the landlords’ wish list, not reality for the tens of millions of tenants.

The actual rent increases that existing tenants get are an entirely different thing, and they get them after the lease runs out, not during the lease, and the CPI picks those up. Asking rents doesn’t track that at all. So if you want to know what people are actually paying, and how much more they’re paying FOR THE SAME UNIT, you cannot look at asking rents.

“Owner’s equivalent rent of residences” (24.0% of total CPI) tracks the costs of homeownership as a service, based on what a large panel of homeowners report their home would rent for. This is not lagging at all. It’s a direct pricing survey of homeowners.

OER

“homeowners report their home would rent for..”

without furnishing+ or utilities!

Does this reflect reality?

With the dollar tanking can we expect inflation to get a little fuel if this persists, especially with energy costs. I guess this the end of the dollar’s run up.

Sure looks that way unless the FED surprises with a bigger rate hike in December Glad Im diversified

Wolf . Great article…primary residence” weighs 7.35%, and “owner’s equivalent of rent” = 24.0% . Why the large percentage for owners equivalent rent relative to primary residence particularly when home ownership is about 65% ?

I’d guess that your average homeowner lives in a larger, nicer, more expensive home than your average renter.

I don’t know about anyone else, but I just did my wife’s health insurance for the year, and it went up substantially, not down….

It looks like the DOW will now be going to all-time highs. Jerome Powell has failed in his job, which is not just a stable prices mandate, but to read the tea leaves and take away the punch bowl just as the party is getting started. He has concocted a relentless, maniacal speculative mania, and now lost all control of it.

The latest moonshot on the indices, and the associated narrative which has now made its way across the world that the inflation fight is over and the FED’s job is essentially complete, has dropped another zephyr of rocket fuel onto a raging speculative inferno, only made possible by the more than $4 trillion that is still sloshing around in newly printed Powellbucks.

The fact that a mere .2 drop in CPI could result in such a vicious price move to the upside in all risk assets is indicative of the grossly excessive amount of liquidity sloshing around in the system. The speculators are playing Powell like a fiddle. They know him better than he knows himself. He talks big, pretends to channel Paul Volcker, but Powell is at best another Arthur Burns.

The market knows Powell will bring his little pea shooter out in the next meeting, and fire off a 50 basis point rate hike, and another 25 basis point hike the following meeting. Because Powell already told them as much. And that’s all priced in and now the market has decided that Powell’s job is done and it’s back to the races because none of that money has been sucked out of the system. Powell made sure of that.

Don’t panic, Depth Charge :-]

Sometimes I just really wish there was a “like” function.

I don’t understand why Feds and their apologists ANALyst are so naive about the myth of Employment Strength?!

If my business can borrow at 6% rate to expand my production and sell with 9% inflated price, I WILL BORROW AND EXPAND!

Until the Fed Funds rate is above 8% and above, the “conundrum” of STRONG Employment would stay.

Or Fed could quickly cut their balance sheet by $200 Billion per month, the same speed as they expanded over last 2 years.

Wolf,

I always enjoy reading your articles, and over the years it has become my go-to place for economics/financial sense, helping clear out all the noise and smoke there is in the media. For this article, The second I saw the market going up like crazy, I told myself “I can’t wait to see what the real story is at WolfStreet”.

I apologize this comment is off topic but, I’m still relative young so I hope Wolf street will still be around for another 40 yrs. Are you mentoring anyone or planning to do a transfer-of-knowledge with someone so this site can keep going for years on end?

Thanks.

I’ll stick around for a good while longer, that’s the plan LOL

I’m just a young whippersnapper.

Are we still short? Or solvent?

Maybe the phrase don’t fight the fed should be changed to don’t fight the market sentiment.

Sure. 2022 has been good for the short. Bear-market rallies are part of the deal, and they keep you focused.

Today the technology to do it is there, so why not switch from a checks and balance accounting system for banks to an individual serial number (identity) on all money on the books like it is done with notes? The central bank could then take full control over monetary inflation by controlling the issuing of new serial numbers (identities) on money.

They could even implement interest rate control as part of the design, in a way that the central bank did set interest rate on individual electronic “dollars”.

With full control over monetary inflation, the central bank would have more power on consumer price index and asset inflation too.

As long as the narrative spin of ‘peak inflation’ and possible pause or pivot any time early ’23, the power of perception will carry the indexes to keep recovering. There will be definitely Santa/year end rally next month unless CPI goes above 8.0% and 75 basis rise in rates.

I reduced all my shorts but kept key ETFs earning div, energy, food, grains and fertilizers.

The power of perception is hard to discount until rate is increased to 5% and above. Some of the FOMC members also talking dovish. Irrationality is winning just like, for the past 13 yrs.

Its all a charade or ruse because of Black Friday sales and the holiday season just get heavy short at the very end of this year. The markets will get trounced this January with double digit losses for the month.

The effect of the adjustment is barely noticeable and wouldn’t affect market sentiment.

Reported CPI:

Index = 298.012, YoY = 7.7%, MoM = 0.4%

if CPI Health Insurance would be 0% MoM instead of -4%

Index = 298.090, YoY = 7.8% MoM = 0.4%

if CPI Health Insurance would be 2% MoM instead of -4%

Index = 298.130, YoY = 7.8% MoM = 0.4%

Source data:

CPI Health Insurance:

Relative Importance = 0.918%

2022-09 = 213.036

2022-10 = 204.489, MoM = -4.01199797217%

2022-10 (for CPI HI MoM=0%) = 213.036

2022-10 (for CPI HI MoM=2%) = 217.29672

CPI:

2021-10 = 276.589

2022-09 = 296.808

2022-10 = 298.012

2022-10 (for CPI HI MoM=0%) = 298.09046146

2022-10 (for CPI HI MoM=2%) = 298.12957487

Here’s a comment on youtube almost identical to mine under this video

A Market Melt-Up Or Meltdown? The Answer Will Shock You

da no

1 day ago

The markets are rallying by manipulation of those pulling strings because Black Friday shopping and the coming Christmas season is counting on consumers feeling good, wealthier and generous. Create the theatrics of positive vibes and then come January CRASH!

Almost verbatim to my comment here. 36 thumbs up on the comment

No conspiracy theory left behind :-]

These people crack me up.

I noticed an increasing amount of items on the shelves of my local grocery chain store are not market with the price or if they are marked the price is wrong, and always on the low side. I complained a week or so ago with the management and they said they were short on employees to update the posted prices and would try to do a better job and correct the problem. A week later I went into the same store and nothing was corrected. They are also having massive supply chain problems. Many basic essential items like clean water and half & half and other dairy products are completely out of stock, while junk & frozen food is stocked to the hills.

The published 7% or 8% rate of “inflation” is silliness.

Inflation for everyday items required, or desired for living, is at least twice the silly published rates. Food, gas, you name it, all up double digits. The quality and even quantities are down too. How are those measured?

Small example in lawn equipment.

Bought a Zero Turn April 2021 for $4,299 at Home Depot. The exact same model with cheaper engine, cheaper transmissions (the costliest parts) is now listed at $5,299 at the same local big box retailer.

That is a 23% increase YOY for less quality machine, under the same model designation.

If the Fed uses their inflation numbers to guide actions, no wonder they appear to be a year behind and lost most of the time.

My AAA insurance used to be annually $1600, they added $800 additional charge for this year, thats 50%, the chart shows much less, I looked for better quotes and didn’t get any better prices

Wolf – One of the more confounding questions that I have not been able to wrap my mind around is a framework for how global/national/state economies will be able to meet entitlement programs with aging populations (U.S, Europe, Japan, etc.)?

The two options are print/borrow more money or benefit cuts, then what?

Being in my mid 40s, moderate amount of professional success and financially disciplined (savings, no debt) I am concerned about future generations (my children) and their ability to even have a moderate amount of success or what will be required to just claw to our current standard of living given my experience operating within a global firm and level of effort, sacrifice required to just obtain that.

I look at my father and his generations (in his 70s) and come to the conclusion his generation grew up in an era akin to China’s renaissance and growth trajectory where conditions were favorable: playing field was local v global, where the ability if you were enterprising, worked hard, disciplined you could obtain generational wealth or wider windows for success, have multiple homes – primary and second home. etc.

I foresee my generation and children’s generation shoring up excesses either via higher taxes, narrower windows for success collectively, and lower standard of “material” living but a return to stronger family units and communities, at least that’s my hope, versus mass consumerism brought on and encourage via Fed debt punch bowl.

Thank you for all you do on this site as it is my go to. Look forward to your feedback.

Your mistake is to call them “entitlement programs.” The expression is part of the propaganda. They’re pension funds and healthcare insurance that is paid for by the people that participate in it — LIKE ALL PENSION FUNDS AND HEALTHCARE INSURANCE. The Social Security system has amassed a $2.7 trillion pile of funds.

READ THIS:

https://wolfstreet.com/2022/11/08/status-of-the-social-security-trust-fund-income-and-outgo-fiscal-2022/

Sure, but that only means that the Social Security system has $2.7 trillion to pay out. It doesn’t mean that that $2.7 trillion will be able to buy what people expect it to buy. I think when people like Tim Holcer say “afford the entitlement programs,” they mean “afford them such that they can provide the same benefits and standard of living as they have in the past.” It’s the part that is in question.

Nah. Look at the g*d**n article I linked. Don’t people EVER even try to understand the facts????

Social Security has income and outgo. The Fund only needs to make up for the shortfalls, if there are any shortfalls, and over the past 35 years, there were only three years with shortfalls. The rest of the time was surplus, which accumulates in the Trust Fund:

Wolf, with all due respect, I did read the article, and I understand how Social Security works.

My point is that Social Security’s ability to provide a certain standard of living to retirees is dependent on the productive capacity of the United States. If the dollar loses its reserve currency status and the standard of living drops for everyone, recipients of Social Security won’t go unaffected simply because of the trust fund or any other factor.

So, when people say “Will Social Security be around,” they mean will there been enough excess production that retirees can be taken care of. As Augustus Frost often says, the only way people can retire is if someone else is paying for them. There’s a lot of truth to that.

Didn’t mean to offend re: “entitlement programs”, I too have contributed $250k+ to date in SS with employer contributions and frankly don’t expect to see a dime in my planning.

While I agree we should honor arrangements, would prefer a dose of reality and shared sacrifice to get everything on a sustainable path (e.g get tax incentives for continuing to fund SS or reduce 6.2% rate and cap and allow us to pivot our money to 401k IRAs etc with clear understanding our generation will see reduction to our expected SS commensurate with that.

At a local level, seeing public pensions $300k annually for lifetime payout of ~ $7M with 5% lifetime funding of $350k for jobs with little to no career risk and market risk effectively an annuity for life with COLA, it’s so far from reality of global/national/local marketplace and private employees experience, why should they be on the hook for arrangements like this made and effected by politicians dislodged from taxpayers?

Thanks for the link will take a look, appreciate it.

Why doesn’t the BLS ( Bureau of Lying Statistics) also incorporate the cost of healthcare from Medicare and Medicaid?

There isn’t a retained earnings but the federal and state government costs can be derived by examining outlays and adjust per population adjustments, increased enrollees, etc.

So what Im reading here is that we should expect a hot CPI in December and likely a more hawkish JPow because he is pissed the market raged after this CPI which came in low, due to once a year skewed health insurance CPI numbers??

The key data for the Fed will the next core PCE reading, on Dec 1.

But they already said a gazillion times: they’re not going to react to just one inflation report. Year-over-year and month-to-month inflation numbers jump up and down erratically — just have a look at the long-term charts — and you cannot conclude anything from just once reading.

The last three years of health insurance corrections look like an unstable system. They increase sequentially, like a control system out of control.

There’s something they got very wrong during the pandemic . . . maybe a complicated system that worked well during normal times but tweaked and tweaked and burdened with new coefficients and inputs until it was extremely unwieldly in the event of disruption.

Interesting article, thank you.

“Keep it simple stupid.” is an engineering cliche. But it has it’s moments. Typically engineers will have several models.

Often there is a simple, untuned model, which is nonlinear (like reality) but has few inputs because it’s difficult to solve nonlinear system equations. That is what you turn to in the event of a “large signal” disruption (like the pandemic).

In normal times, a linearized model with more inputs is used.

The BLS won’t have needed the nonlinear model for their health insurance modelling since, what, the 1920’s? Bet they don’t have one!

(My word choice may not be perfect for the BLS case, but someone who does modeling there will know of which I speak.)