Buyers’ strike is in effect. Used vehicle retail sales drop, dealers sing the blues but don’t want to cut prices from their ridiculous levels.

By Wolf Richter for WOLF STREET.

The thing about used-vehicle prices is that wholesale prices at auction have plunged all year, and dropped again in October, and this is where dealers buy a big portion of their inventory.

But retail prices of used vehicles haven’t dropped, even as retail sales declined amid a buyers’ strike following the ridiculous price spikes in 2021 and 2020. And there is pressure on dealers to cut prices, and dealers are bitching about this environment and dropping sales. But they’re still furiously trying to hold up these ridiculous retail prices for as long as they can.

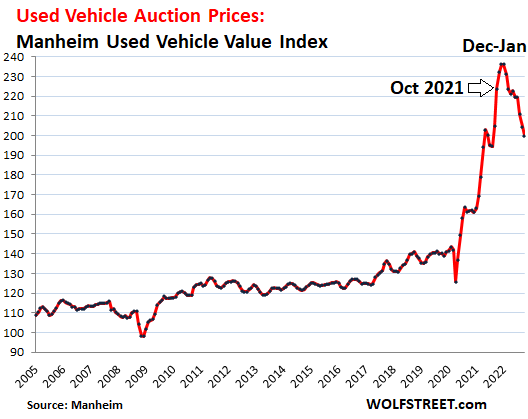

Used vehicle wholesale prices dropped by 2.2% in October from September, by 16% from the peak in December and January, and by 10.6% year-over-year, the first year-over-year decline since May 2020, according to data from Manheim, the largest auto auction house in the US and a unit of Cox Automotive. Compared to October 2020, despite the recent drop, the index is still up by 24%, which shows how ridiculous the price spike has been.

Wholesale prices reflect input costs for dealers. The cost of newly purchased inventory has been dropping all year. And generally, businesses don’t complain when their input prices drop.

But whatever vehicles they had sitting on the lot for a while were purchased at the higher prices effective at the time, and that’s a problem for dealers.

And since these input costs are dropping for all dealers, price competition will eventually have an effect on retail prices that dealers charge, but dealers are furiously trying to hold the line.

In 2020 and 2021, dealers had been starry-eyed over the buyers’ sudden willingness to pay whatever, even paying more for a used vehicle than an equivalent new vehicle would have cost, if there had been any. This special effect of paying-whatever was in part due to the torrent of free money that was raining down on everything and everybody since the spring of 2020.

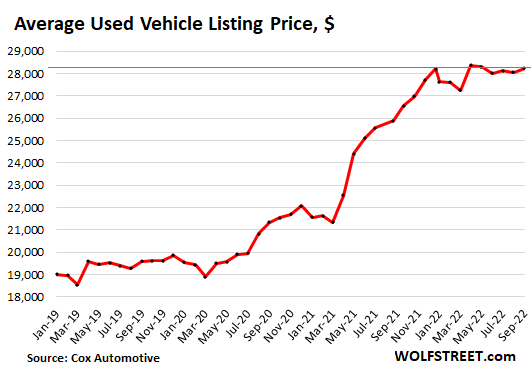

The “average listing price” at dealers hasn’t budged this year. At $28,237 in September, it was roughly unchanged from December, according to Cox Automotive (it will release the October data in a few days). This reflects the average price at which dealers advertise their retail units.

Over the 17-month period from August 2020 through December 2021, the average listing price jumped by a ridiculous 41%, as dealers were foaming at the mouth over the buyers’ sudden willingness to pay whatever, and they were bidding up prices at auctions to ridiculous levels, knowing that they still make historic gross profits by selling those vehicles at even higher prices to retail customers suddenly willing to pay whatever.

This mania peaked in December and January. But listing prices just haven’t come down since then:

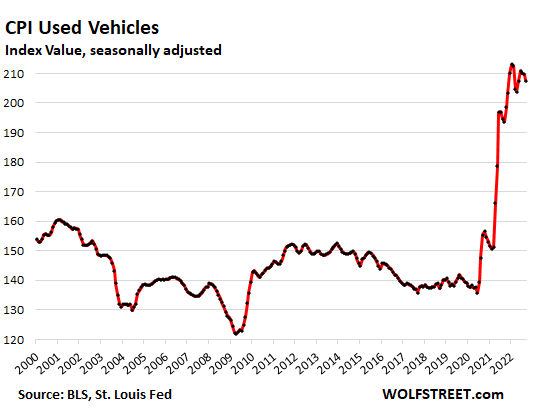

The Consumer Price Index for used vehicles hasn’t dropped either, but has been wobbling along in the ridiculous zone since February. In September, it was still up by 7.2% year-over-year, and by 34% from September 2020, that’s how ridiculous the whole spike was.

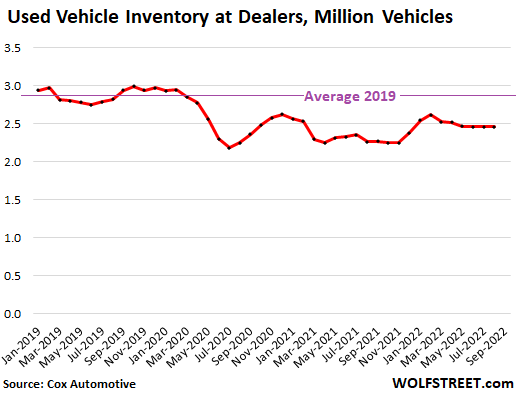

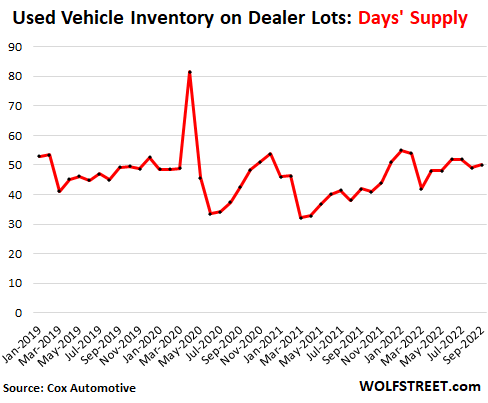

But there has never been a shortage of used vehicles to justify the ridiculous price spike. In February 2020 before the distortions of the pandemic, there were 2.95 million used vehicles in inventory at dealers. In the early months of the pandemic, inventory dropped, but never into the “shortage” range, and it then largely recovered. So far this year, inventory has been in the 2.46 million range, according to data from Cox Automotive:

Vehicles are discretionary purchases: Most people can easily drive what they already have for another year or three. But buyers were suddenly willing to pay whatever – which is when the inflationary mindset kicked off. The entire industry picked up the ball and ran with it, and they ran as fast and as far as they could. The run ended at the end of last year in the ridiculous zone.

Demand at these prices has fallen for two reasons: One, the prices are just ridiculous and no one should buy a used vehicle at those prices; and two, interest rates to finance used vehicle purchases have jumped, making those ridiculous prices even more expensive. Just say no?

A sharp drop in retail prices to less ridiculous levels would boost demand. But falling retail prices is the last thing dealers would want. But it sure would perk up sales.

Supply is back to normal and ticked up to 50 days in September, which is where it had been before the pandemic, given the decline in sales this year:

Used vehicle dealers are singing the blues.

CarMax, the largest used-vehicle dealer in the US, said in its last earnings report that in the quarter through August 31, comparable-store used vehicle retail sales, in terms of the number of units sold, fell by 8.3% from a year ago; and total unit retail sales fell by 6.4%.

Despite the decline in sales, CarMax reported that the average retail selling price rose by 9.6% to $28,657 per vehicle sold.

The gross profit her retail unit rose to $2,282 per vehicle, “an increase of $97 per unit despite steep market depreciation,” as it said in its earnings report.

This higher gross profit reflects whatever dynamics in selling prices and the dropping costs of the vehicles it purchased in the wholesale market. Its net income fell by 56% to $126 million.

That was through August, and the retail pricing situation has remained tough, and shares of CarMax have plunged by 59% from peak-mania-November 2021.

But the folks at CarMax are the adults in the room; they’ve been through a turning market many times before. And they still made money.

That cannot be said for Carvana, the largest pure-online used vehicle dealer. Similar to CarMax, it reported an 8% drop in the number of used vehicles it sold retail, but its gross profit per unit plunged by 25%, its expenses jumped, and its net loss skyrocketed to $508 million. Its shares plunged by 39% on Friday, following its catastrophic earnings report, and today are down another 15.8% today, closing at $7.39, having collapsed by 98% from the peak in August 2021.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

“Used vehicle retail sales drop, dealers sing the blues but don’t want to cut prices from their ridiculous levels.”

Go ahead and cling to those dreamy prices, greedheads, and I’ll continue to drive what I have. In fact, I think a couple more years of watching you guys wither and die on the vine sounds delightful.

well said

might buy ‘used'(not really) toyota tacoma 2022

has total 167 miles on it

— estate sale

looking for that 30-40% off lot discount

of course I also use the 1 payment plan

I’ll second that ,always have tried to screw over consumers

It’s greed, and they paid too much and don’t want to take a loss. Also their expenses have increased. Half the dealers will go bust, again. Especially the pandemic no look models like Carvana and Vroom, the wework and zoom of cars. And how many other pandemic business models still think they will make it? Add them all to the implosion list. Cause it was not really a pandemic business model, it was a fool with free money model. The pet rock could have made a comeback.

It did. In digital form. I present NFTs, the pet rock of the zoomer generation.

Where’s all that free market competition the media tells me will happen to invisible hand lower prices?

Seems like we’ve got none of that free market in 2022 USA. Looks to me like a handful of rich guys telling us to pay an arm and a leg or go pound sand.

My take also, A.

And we are in good company, like Abe Lincoln, who tried to warn us.

Now, who is to blame? Well ultimately it is ourselves, but you can now select the media that will blame the guilty of your choice, saving you the need to question your own intelligence, or do anything but badmouth the guilty.

Part of the our Full Service Economy. Enjoy.

NBay-very, very well-said…

May we all find a better day.

Thanks. Just trying to do best effort “recon in the smoke”, like you said…..and do…..situational awareness IS intelligence, for any life form.

Sounds like the same story in real estate. The hopium is still strong. Waiting for the dam to break for the deluge. Unless of course the fed pivots :-P

The last Fed pivot was more hawkish. The next Fed Pivot is going to be even more hawkish.

https://wolfstreet.com/2022/11/02/fed-hikes-75-bpts-to-3-75-4-0-pivots-even-more-hawkish-very-premature-to-be-thinking-about-or-talking-about-pausing-markets-tank/

Wolf,

The Fed is becoming more hawkish – but much of the rest of the world believes that US State Department ambitions (read: ensuring a united coalition against Russia) will ensure that the Fed is not acting in a vacuum. Galloping appreciation of the US Dollar undermines those by exporting our would-be inflation to other countries.

As it stands, the Fed’s statement still allows for slowing the pace of the rate increases.

And there’s always the specter of a major crack-up in the credit markets happening (think: September 2019) which forces a major policy adjustment.

Yes, the Fed will slow the pace of rate hikes, and it will pause, obviously because the sky is not the limit, but that pause will take place at much higher rates and previously thought. The Fed is already at 4% top range. The pivot mongering started at 1%.

As yet, there are no significant signs of the housing market weakening in Greater Boston. We’ve seen a drop of a couple percentage points in prices, but that’s the usual seasonal dip.

Some of the relative strength is probably down to a substantial influx of European buyers that began entering the market in mid-June. Realtors would gladly sacrifice their first born for these buyers as they have proven to be *highly* motivated.

Nonsense. The market here has markedly weakened. We sold a house in June (closed in July). ~$1.3M, no inspections deal, in an expensive inner I-95 suburb. Only because we lucked out with a buyer that had mortgage locked at 4.5%.

It would have been $1.1M sale now at best, judging by comparable sales closing now.

BoA has started a no downpayment, no closing costs, no pmi, no min credit score to minorities. Sounds a lot like the crazy loans from the early 2000’s the targeted subprime borrowers.

I’ve also read where builders have started to sell equity in homes. So, if you want to buy a $600K home, but you can only afford a $400K mortgage, then you become an investor as opposed to the outright owner.

Also, the lower teaser loans are starting to come back as well.

With the insane levels of price increases, housing has officially moved beyond what we saw 20 years ago. Builders, real estate agents, home sellers are all going to fight tooth & nail to prop up housing. From what I can tell, the craziness has decreased but that’s not translating into much in price drops. Houses are simply sitting on the market longer without significant cuts in prices, oftentimes.

Every market is different. All I know is that here in Woodstock GA a recession is absolutely nowhere in sight.

Where is the point that selling a vehicle in parts is more profitable then selling the vehicle?

Commenters here have shown examples of ridiculous wait time on new parts for newer cars.

That’s always been the case. Its why chop-shops exist.

Sams-have tearfully dismantled many restorable classic motos over the years in the cause of profit in the restoration of others (…a different market to much of the automotive one, admittedly…).

(…it does give one pause to consider human nature and its organ-donor market, however…).

May we all find a better day.

Wolf describes CARMAX as the adults in the room. I’ve dealt with them twice in the last few years and would describe them as highly professional and good to do business with. If you have a car you want to sell, I recommend you go see them. Mind you they will buy your car for wholesale and sell it for retail, but that’s how they stay in business.

I’ve sold two cars to Carmax over the years – very happy with the process and prices actually not bad at all. And not having to do the process myself very worthwhile.

I bought the KIA soul in Sept of 20 and sold in June 21 due to moving abroad. Bought for $10300 sold for $12250 at a dealership. CARMAX was giving me $9000. This not the first time they were trying to flees me with a price.

you don’t make money selling used cars. You make it by buying.

A dealership makes money from the loan, volume and can give a discount/ or overpay for a trade-in.

Wolf, you have a typo: The gross profit her retail unit rose by 7.9%

Amazing how market forces regress to their traditional trends.

Who would have thought that the most fungible commodity, an irrationally priced, depreciating, wasting asset – a used car – would some day drop in market value.

I am shocked to observe that economic forces work as predictably as they do!

Economic forces only work effectively for things that people don’t actually need for which demand is not elastic. Housing, food and healthcare keep getting more expensive

There wasn’t just rampant speculation the stock market, crypto and housing, it made its way into cars, boats, RVs, etc. All of a sudden you had a bunch of Johnny-come-latelys buying brand new luxury vehicles and trying to flip them for $50k-$100k over sticker.

Craigslist was loaded with “brand new” vehicles which were technically not brand new because they were purchased by a speculator through a dealership, who was trying to then find a sucker to cash out with.

Now we are at a very interesting period where rates are shooting the moon so buyers can afford less, all the free money is essentially gone, and urgency is waning. Once new vehicle inventories start building in earnest, you may really see some financial pain as the car industry experiences a very rude awakening.

Don’t forget luxury watches even. Buy a Submariner for retail, flip it immediately for 4-5k more on the secondary market.

The part that I never got about “retail arbitrage”…don’t the buyers have access to Google?

I mean, if I am about to shell out money, I take 5 seconds and Google “inexpensive X” so I have *some* sense of reasonable prices.

How can Johnny Rando *pay* retail and then flip it for 20% *more* – are those second buyers in a sensory deprivation tank?

I understand buying from manufacturers/wholesalers and then flipping…in exchange for a large minimum order size, the retailers get a discount and a promise (ahem) of no consumer direct sales from the manufacturer/wholesaler.

So that discount is the retailers’ margin.

But if a retailer pays retail…there is no margin.

@Cas127

It’s not only simple retail arbitrage. Oftentimes there is a time aspect involved. Certain watches (or other articles) are not immediately available, you have to order and wait for them. Some Rolex models are examples of this.

Now suppose you feel super rich because your crypto’s are doing so well, and all of a sudden you decide you want to wear a Rolex Submariner to this great party tonight, so you don’t mind overpaying to get it NOW.

This is why scalpers, hustlers, speculators and whatnot exist. And they move from field to field, be it high-end graphics cards for gaming PCś, certain brands and types of watches, theater or concert tickets, new or used cars or whatever. Nine out of ten times money is made here from buyers who just want something NOW.

There is a good article on this on ablogtowatch.com, search there for “scalpers” who are ruining the watch purchasing experience for consumers. It’s really an eye-opener for people who are not heavily into watches.

The pain might take a different form than you realize.

Right now the industry is stuffing its scarece microchips in enormous SUVs – which cost an increasingly-large amount of mone to fuel-up. Of course, such vehicles are much more profitable for the manufacturers.

But they may not be what the public actually wants to buy.

Wolf should take a deeper dive into those used vehicle inventory stats. Because if the Greater Boston market is any indication – used cars and SUVs are hard to come by while larger SUVs are just piling up unsold.

The above should have read:

“smaller used cars and SUVs are hard to come by…”

Everything is stagnating at the tipping point. On another subject, I looked at an area today to try and see which houses probably sold for cash in the past week. Only 3 out of 16 houses sold in the past week had normal pending times. The rest went through pending quickly in 2 days to 2 weeks- which means they were either sold cash or the parties had phenomenally good connections as the county is taking a minimum of 4 to 6 weeks to get it done. It looks like some investor(s) unloaded a bunch of properties to another investor to me. Most properties looked empty when sold. Chips on the gambling table.

To me, the amazing story is the amount of supply being held off mkt (homes for sale inventory is still just about 60% of 2019 levels…if it were me, unZIRP means you can be on the train…or under it…but a ton of senior boomer homeowners seem to be loitering around the train station parking lot).

I’ve been looking at “for sale” inventories by metro and the only metros with inventories higher than 2019 are the hottest mkts that CA refugees fled to (presumably speculators noticed the trend early, amped it, and are now dumping).

I don’t know the big picture or big data on this, but I’d personally rather go down with the ship in my own home versus in a retirement/senior/assisted/medical setting, which contain all of the attendant racketeering to squeeze out every last cent.

Fair enough and I tend to agree, but 60% of 2019 levels (mere 3 yrs ago) is a huge change.

I assume it is Covid related – fear of potential infection being brought into house, etc.

But how long will that fear last? It works in opposition to the strong historical desire to get the heck out of the frozen North and live (some…any?) sunset years somewhere warm.

And now there is the unZIRP countdown timer…wait too long and you’ll have at home cryo-preservation because Minneapolis/Chicago/Boston/etc prices have fallen too low to migrate South…

Not necessarily S1:

FIL died at 93.5 years after 5 years in what we old timers call a nursing home because he was too heavy, even after losing about 50#s, for his children to take care of at home after the last stroke. It WAS formerly a church sponsored facility, but just sold to a PE firm, so possibly big changes coming.

FIL had large shared room full of light, BIG guys to help, and many hands to feed him up to his last day.

Although he couldn’t talk for years, he always had a smile when his children showed up, and they worked shifts for him to see one of them almost every day…

Similarly many decades ago for my grand mother who had arthritis SO badly she had to be fed her last 5 or 6 years.

They definitely NOT all bad, though clear enough all too many are not desirable, at all.

Cas, the extra inventory will come from investors and second and third home owners. Hopefully when someone dies or has to have assisted living their relatives will be able to live there. If not, yes, many assisted living facilities will take the amount of equity in the home- one way or another.

Large corporations and foreign buyers have been buying up a huge percentage of homes. Sometimes with a front person or couple who pretend to be the occupant.

There are no stats on how much of the housing inventory is owned by them. But- it may be a lot. If 15 – 20% pr year of inventory is bought by them, how much of that is accumulative? How much is left empty? How much is traded in bulk to other large investors to pay loans rather than going to the MLS? If even 10% of the inventory is owned by large interests that is a LOT. I personally think that is a low estimate after a decade of this.

These ridiculous price spikes were only possible because of the subprime lending credit bubble, where banks allowed loan-to-value ratios up to 170%. Who the hell decided that was a good idea? I hate government, but there needs to be strict lending standards, because we’ve found that banks sure don’t have them.

Well, the big dogs are trading their inventory.. I would think prices will start to go down more quickly when their done.

“they’re”

Perhaps Ally will be shut down for good, they started the subprime back again in 2012 when eyes were elsewhere…the former GMAC ABS disposal company was free to destroy courtesy of banker fluffer party in that era

Always thought that “Ally” really should be called “Iago”

Well, I’m pretty sure there were some regulations put in place to require debt packaging securitizers to retain some skin in the game (ie, not sell off 100% of loan default risk) but court rulings blocked the regs.

But self-preservation shouldn’t require regulation – I don’t get the suicidal impulse of professional securitization buyers who don’t contractually require skin in the game (or go on a buyer’s strike).

I suspect it is ZIRP shell-shock…when your alternative is a 1% return, a 5% trollop with likely chlamydia (sp?) gets roped in to the realm of possibilities.

(3 mixed metaphors…one sentence…a record).

We don’t need government to regulate if lenders actually had to hold the loans on their own books. But since they don’t, they have no real incentive to do proper credit underwriting.

And risk your own capital ,hahahaha

Wrong… they Do have incentive to properly underwrite… secondary market doesn’t want junk either…

And if secondary market is stupid enough to buy junk, we’ll then that’s their problem,,,,

Tell me that you’ve never worked in the capital markets without telling me that. LOL

Top Gun,

Plenty of bad actor banks from Bust 1.0 were never really held to account by loss of reputation/burned customer base.

Goldman may be called a vampire squid…but it is as busy as ever, out there vampiring and squiding.

It is a fair question to ask just why people with money are willing to repeatedly play frog to many banks’ scorpion – how many stings before buyers wake up and say “oh, you are a bad little pony and I’m not going to bet on you any more…”

(More mixed metaphors…frogs and ponies…)

To a certain extent, it must be industry concentration/stagnation…to dump Goldman, you have to have an alternative…

But it isn’t like money managers are in short supply…

There’s a funny little “ad valorem” tax that drops in the first quarter of ’23. Bet those dealers are not going to walk away from any qualified buyer in the last two weeks of December. All they have to do is walk away on the first pass. Holding commodities during periods of dropping inflation is a nervy game, few can handle it.

Ad valorem taxes aren’t nationwide. One of the few states I know that does that is WA.

I bought a used car yesterday – only a couple of years old, very low miles, most the dealers were advertising the same model with three times the miles for 10 to 15% more than I paid for it. It looks to me like the dealer is trying to reduce the high cost inventory ahead of the the other guys. With that said, there is still very low inventory of new cars on their lots.

Musical chairs? (…in ‘forward’ or ‘reverse’?)…

May we all find a better day.

This is not entirely on topic, although it affects prices at dealers somewhat. If you trade in a car (at least in all of the states I’ve lived in), the amount of the trade in offsets sales tax on your new tax. So if you live in a state with 8% sales tax, you have to get significantly more than 8% more in a private sale for it to be worth it versus just taking the trade in offer.

This means that dealers have somewhat of an advantage from the beginning.

Bought a new rig (2021) in the fall of 2020. It was amazing. Got an f350 for a pittance more of the f250 I was looking to buy. I couldn’t get it at the dealer. They kept trying to get me into fancy stuff with bunches of bells and whistles. I finally built it on Ford’s website and took the paper in to the dealer. It was not a comfortable deal. Took 2.5 months and it arrived.

Not sure that can be done in a few months anymore. And the dealerships hate it when you do that. But if you have time, screw them and their searches. You can get exactly what you want.

And then it comes in and they hold you hostage because they have your deposit in hand when they start to play games with the price, loan rates, etc. These guys are fraudsters, for the most part. Sure, there are some decent dealerships, but they are by far the minority.

That’s exactly what happened. It took over four hours to take possession with me refusing every upsell. Then they said I couldn’t leave until FordConnect was configured and it would affect my warranty. But It wouldn’t work. Finally I said I was leaving. I still don’t have that dang thing connected, Why? We have no cell connection. The service guys are great. The sales folk, not so much. And we have a long history there.

Yes, we have all had that experience, but many dealers are getting much better due to the online competition. The online prices leave little room to haggle, you can see the difference when you look at the pricing they have on the car sticker vs the advertised price. I was in an out of the dealer in an hour.

When I bought my first Nissan Sentra from a big dealership here in Northern VA, I had a young salesman who seemed pretty nice. We negotiated a trade in on my lemon 1978 Mustang, and I only had to put up $6K. We shook hands on the deal. Then he started getting into, undercoating, etc and all the extra’s that I didn’t want. Apparently, the handshake didn’t mean much. Then he said he had to get approval from “The Big Guy” to close the deal. I began to walk out. He grabbed me in the parking lot as I was getting into my car to leave, and we finally closed the deal.

The ability to walk away is the biggest leverage a customer has. When you put down a deposit and order one and wait, you lose all of your leverage. I like to buy an existing vehicle on the lot. That way I not only have my leverage, but I can actually inspect it and drive it and make sure it’s ok and exactly what I want. When something comes from the factory with your name on it, you’re married to it no matter what.

Did exactly this walked out,got home called closed the deal at my price.Asked manager about some oil changes stated u get nothing.Car came without a owners manual called said they had to order one ,never heard from them .Went in to dealerships talked to. Salesman very rude ,so told him I would contact VW directly,manager heard this I walked out with a Manuel,needless to say will never go back

I got the last laugh. That car (1978, Ford Mustang), I dumped on them looked great, but it was a piece of s$it. Needed at least $5,000 worth of repairs and was essentially totaled out after 40K miles. You couldn’t even drive it up a hill with more than 2 passengers in it. Couldn’t tune it up. How could Ford manufacture such a piece of s$it. I guess most of the cars from that period (Mid 70s) were just that, Crap. Wolf mentioned that in one of his articles. I believe he owned one himself. I couldn’t sell it to a private owner without them coming back at me under the lemon law, so I unloaded on this corrupt dealership in N VA. It was the last American car I ever bought. Bought Japanese cars for the last 35 years.

Isn’t it cheaper to steal a used car…..?

Personally, I plan on hijacking a succession of those Nuro autonomous delivery vehicles (no steering wheel might be an issue, though).

Slightly more seriously, I do wonder about about stagecoach robberies of smallish autonomous delivery vehicles (well, *grocery* robberies).

I suppose the vehicles can be programmed to loudly shriek “stranger danger!!” If molested, or “Witness the violence inherent in the system!!”

Good point.

I have often wondered how an autonomous semi convoy would fend off Toretto and company out in the desert.

The scooter rental people learned the hard way that people don’t always behave well and it can be a big risk to your business model.

Small repairs or big car repairs, I don’t care…

Still waiting to replace my alternator, starter and brakes on my 2004 Cavalier. These parts will all eventually, fail.

If, I walk into any car dealership, new or used, when it is all said and done… With all the ridiculous fees and etc that they add on, I could easily repair my car and have no new monthly car payment.

No, Thank You!

Cuba been doing it for 60 years,great innovation when there are no viable alternatives

You made a great point, “Vehicles are discretionary purchases: Most people can easily drive what they already have for another year or three.” One question, are motorcycles and/or bicycles part of this vehicle price data or just automobiles? Thanks!

It’s true — even the nastiest repair is still going to be cheaper than buying new.

And if you happen to be discerning enough to captain something like an Aries K convertible or Fox body Mustang, then you get to feel good keeping it on the road a bit longer.

OR… a 2006 Toyota Solara (Camry chassis) 6 valve convertible (only 94,000 miles!) This one is good for another 5-10 years riding the beach towns in Northern Baja :-)

Speaking of bicycles, demand for new bikes shot up 80% during the pandemic and there were major shortages, year-long waiting times for special orders, etc. My local bike shop which normally has dozens of bikes hanging up around the store, sold off every last one.

Now the industry is in a slump, new pedal-bike demand has dropped below 2019 levels, though electric bikes are still doing well. There are more bikes out there now needing maintenance so hopefully the local shops will still do OK.

Happy (excited) to hear this. Been waiting for a deal to update my full-squish. Wife gave me the thumbs up a year ago but I decided to be patient. One of several reasonably large purchases we have on the down-economy, to-buy list.

People will soon be entirely opting out of expensive cars and realize they can save $20k to $30k just purchasing an ebike. Use it for most trips, and when a car might be needed for weather or long trip, just Uber or rent a car. No insurance is needed, no license, and no gas. A ‘fill up’ is 8 cents which will get you 50 miles.

The new Bianchi E-Omnia electric bike retails for $5,100 at my local bike shop. They have lights, fenders, a rear rack, good range, are quick and have a “Bosch mid-drive system.”

A friend just bought a Bianchi Specialissima with a SRAM eTap 12 groupset & HED Vanquish carbon-fibre wheels for around $15k at the shop. A fantastic machine; fast, nimble and very comfortable for long rides.

Two years ago, my Bianchi Oltre XR4, also with SRAM eTap 12 & HED Vanquish wheels was $12.4k. Up until recently, they were not available, and yeah, they cost around $15k now that they are.

For those prices, you might as well spend a tad bit more and get a much more capable electric motorcycle.

“For those prices, you might as well spend a tad bit more and get a much more capable electric motorcycle.”

Price does not equal value. There is no value for most people at those prices, except rich people who have more money than sense. For that much, you could buy a gorgeous brand new motorcycle with exceptional performance. The only justifications for that Made In China overpriced e-bike garbage are deep pockets and enlarged egos.

I just inquired at my shop regarding the Bianchi E-Omnia and where it was built. Like today’s cars, it’s a United Nations of sources. The frame is made in Taiwan, and the bike is finished in Taiwan. The battery is made in Japan. The drive assist is German and made by Mahle. But yes, the hubs are indeed Chinese.

My Bianchi road bike has the carbon-fibre frame initially laid up in Vietnam, and the frame, stem and bars combo is finished in Italy. The SRAM company is based in Chicago, and the parts are made in Taiwan. HED Wheels are designed and made in Roseville, Minnesota.

Only highway-legal automobiles.

I still get a good and sad laugh when I see 2000 Acura Integra Type R asking for $100k or close to it and then some joe blow with a not so special Civil Si asking for $50k..

Some of these sellers are so out of their mind it ain’t never coming back…

This Entire Used Car / Used House Thing is simply a Can of worms created By the Fed and all who work with them, Noted Politician’s, Presidents, Real Estate company’s / Developers Etc .

Still Love Capitalism ?

What I hate to say would be the ” Expected Reversal ” back to Inflation > what > 2025 ? 2027 ? 2030 ?

To See :

Charts Forecasts expected dates going forward back to the Same Old Same Old Pump and Dump of the economy

Buying Low again Pump it up Basically with a lot of Hot air until the next bail out occurs . The evolved Players praying on Victims / Bag Holders

Known as Citizens perhaps a Term that has passed evolution now near ending …… Sigh …… Migrants the new Citizens ….. Sigh …..

I was considering gotta new daily driver as my 05’ Outback blew a head gasket. I have a little mechanical ability but nowhere near that level.

I had been looking for a while, not liking prices at all. So, I found an auto repair site online with a 2.5-hour step by step video on how to take the whole engine apart and do the job. Figured why not… car was done and wasn’t worth a $3000 repair bill.

Bought the parts and some additional tools for about $350 and pulled it in the garage. 3-weeks after starting, watching that video about 47 times, and intermittently working on it, finished the job. 500+ miles later, it’s still running like a champ.

Like Wolf said, most people can keep driving what they have.

Good for you. That’s awesome.

Nice work. Subarus are infamous for head gasket issues.

Congratulations! That is a daunting task to learn by video. Furthest I’ve gotten is cleaning out my throttle.

Really inspirational post

This is a great story.

Thank you for sharing.

Shouldn’t the evaporated ‘wealth’ in the stock market and cryptos and cars trigger decreased demand enough to satisfy the FED that inflation is coming down and allow them to stop raising rates.

The FED is tasked with keeping the economy running smoothly and them don’t seem to know how to do it. So what is the point?

Stocks are still up 18% since January 2020, housing is up way more than that, wage gains aren’t far behind inflation, and unemployment is well under 4%.

We are a long way from pain for most people, if you ask me.

Unfortunately, the Fed seems like it wants to see unemployment tick up. They may have to raise rates a lot to see inflation fall much, especially if inflation is being driven by profits more than labor costs, which seems a possibility.

In other words, if labor isn’t driving inflation it may take more job losses than expected to cause a change in pricing.

(Not my original idea, tho I couldn’t tell you where I read it)

Total announced tech layoffs in 2022? 52000

That’s something. But the country just added 261000 jobs this last month. The lost tech jobs pay better but they’re still small job losses at companies that have been hiring madly the last two years.

(Don’t get me wrong. I think the Fed *intends* to kill the goose.)

“Total announced tech layoffs in 2022? 52000”

Announced by US companies, of their global workforce. Not all those layoffs are in the US.

Fed is going to raise rates minimum to 6%. Mortgage rates will go higher than 10%. Think about that environment in 2023, and what happens to home buying. That trickles down to fewer cars purchased, less durable goods like furniture purchased, and so on. There’s still a LoT of boomers to go, who have yet to retire, yet to downsize, and they are probably going to get stuck in their homes for many years to come,or have to be willing to take a far lower price. Home prices will be sticky though, and it will be a long time before buyers will feel like they are getting a deal.

I don’t think the Fed will get much above 4.5%

a) Geopolitical allies are getting angry over the USD’s strength – which is undermining action against Russia.

b) Sooner or later the Credit Markes will impode as the Fed simultaneously tries to reduce its balance sheet and raise rates. They will have to cease one or both shortly.

Financial engineering may have gotten us into this mess – but it can’t get us out of it.

One of the newest hopium things I’ve read lately is citing used car prices coming down as a reason that Thursdays CPI will come in lower then expectations😂….. Time will tell.

Cleveland Fed says it’ll come in hotter then expectations and this time the market doesn’t have a nice moving average to bounce off of so 😳 LFG

The dealers can hold out the buyers all can’t walk to work. I can’t believe anyone would finance a car? If all the sellers collude the buyers are doomed and will be forced to pay top price.

What part of “discretionary purchase” did you miss, Junior?

The dealers can not hold out. Their monthly expenses are very high. The weak will close one by one when buyers say no to high prices. When and if layoffs come, the correction will fully come, like in the last recession.

There has been a big adjustment to the way insurance is calculated, which they do periodically, and this will likely impact CPI (lower it). We’ll see. A bunch of other stuff jumped.

At the Battle of Gettysburg General Winfield Hancock and staff watched General Dan Sickles ill-advised forward deployment of the southern end of the Union line. Hancock commented to his justifiably upset staff, “Wait a moment. You will soon see them come tumbling back.” I believe he’d say the same thing about used car prices

Just looking for a silver lining on these used car prices.

I agreed a year or two ago that we will get a family mini van once prices “return to sanity”. Younger me swore he would never own one. Sedan, truck, SUV, or even short bus, sure, but never mini van.

For now I still have a good excuse in high prices. “The prices are too high” works a lot better than “It just feels too dorky”.

Yeah yeah…I’m sure after a week of owning one, I will be telling everyone I know about the unbelievable practicality, and questioning how I ever did without… much like my wonderful bidet toilet seat.

Ford F150’s are selling like hotcakes in China…

Germany, Japan, Korea,,etc, all have large export economies.

Who are they selling their stuff too?

In the USA, we finance everyone for everything and the world booms!

This is likely coming to an end.

As things unravel, there is much more pain ahead for all involved, IMO.

Maybe free oil changes for life will change the buyers’ mind. They have to hold the line on prices somehow.

They need to build more expensive new cars to boost used car prices.

Is it only I that find it interesting that used vehicle inventory, both number of vehicles and days of supply have not shifted much even if sales of new vehicles are down in the same time frame?

Should not lower supply of new vehicles show up on more than the price of used vehicles? I would expect to see signs of less transactions as people do not trade for a factory new car.

Again, I love reading these Wolfstreet articles. However, I feel compelled to fill in some of the gaps for the ludicrous used car prices. During 2020 and 2021 car manufacturers experienced supply-chain issues and chip shortages, which dealt a 1-2 blow to new car sales. Many auto consumers turned to the used car market to satiate their desire for a new(er) set of wheels with all that stimulus money. This was classic supply and demand, which ran up the price of new cars, both at the wholesale and retail level. However, thanks to the Fed, who took away the punchbowl of financing cars in the low single digits over 5, 6 or even 7 years, the demand started to fall. Used car dealers who overpaid at auction 6 months ago when the market was still hot and have that inventory are stuck. Buyers are no longer willing to fork over 30k for a used car at 7 or 8 percent interest. Of course, new cars, which I think are now averaging 45K, are an even tougher pill to swallow. If we have a recession in 2023, the car market for both used and new will probably collapse and Carvana may be one of it’s biggest casualties. Let’s see what happens in the new year. Cheers.

A question then, do the supply chain delays come to the manufacturers rescue? In other words, are parts that delayed that the manufacturers can ramp down production, or rather not get production up again without getting exessive part inventpories/have to pay subcontractors?

To be honest I don’t understand why people buy shiny new 45k dollar cars only to lose value immediately. In 2020 I got a 2 year old car under 9k miles for $35k which would have cost $60k brand new. I know this didn’t work for last 2 years and doesn’t work for everyone but some people just don’t think.

Doing the math I have found the economy in buying brand new cars and keep them for 10 at least years one of the better options economicaly. At least with the cost of ownership here.

Buying new the car loses most values the first years, but keeping the car I know the maintenance history and maintenance cost do not get high the first ten years.

With an older second hand car the maintenance cost may be higher than the value loss on a newer car.