Big drops in San Diego, Los Angeles, Dallas, Portland, Phoenix, Boston. Prices going down faster than they’d spiked? No way. Oops.

By Wolf Richter for WOLF STREET.

This is the first month in this cycle that the S&P CoreLogic Case-Shiller Home Price Index, which lags reality on the ground by 4-6 months, is showing house price declines in all the metros in the index.

In Seattle, the month-to-month plunge was the steepest on record (-3.8%). In San Francisco, the month-to-month plunge (-4.3%) was the third-steepest on record, outdone only by the two worst months during Housing Bust 1 in 2008. In San Diego (-2.8%), Los Angeles (-2.3%), Phoenix (-2.1%), and other metros, the plunges were the worst since Housing Bust 1. And the declines are spreading across the country to other metros, including Dallas, Boston, Washington D.C., and Las Vegas.

These are serious declines for the Case-Shiller Home Price Index, where each month is a rolling three-month average which irons out the month-to-month variability.

Today’s release of the index was for “August,” which consists of the three-month average of closed home sales that were entered into public records in June, July, and August. Due to the delay between when a deal is made and when the “closed sale” is entered into public records, the time span for “August” roughly covers deals made in May through June. During that time, the average 30-year fixed mortgage rate reached the 6% range. Today, we’re at 7%, and mortgage bankers are frazzled.

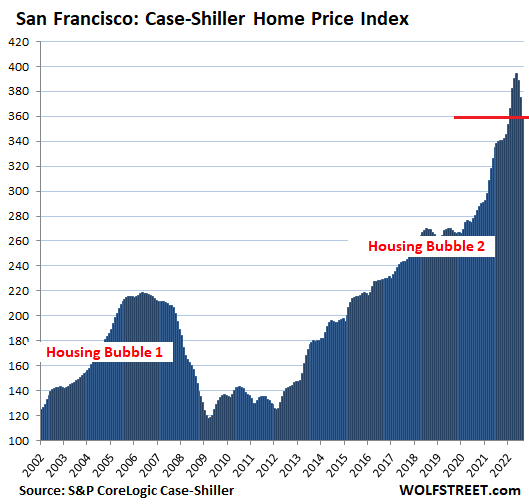

In the San Francisco Bay Area, house prices plunged 4.3% in “August” (three month moving average of June, July, and August) from July, the third-steepest plunge on record, outdone only by the two slightly steeper plunges during the depth of Housing Bust 1 in 2008. The plunge in August was an acceleration of the drops in July (-3.5%) and June (-1.3%).

The index has dropped 8.9% from the peak. Over those three months, the index plunged faster (-35 points) than prices had spiked during the last three months of the spike (+27 points). House prices going down faster than they’d spiked? No way, impossible. Oops.

This turn of events slashed the year-over-year gain to +5.6%, from +24% earlier this year, unwinding so far just the final stages of the ridiculous spike over the past two years. The index is now at the lowest level since January.

The Case Shiller Index for “San Francisco” covers five-counties of the nine-county San Francisco Bay Area: San Francisco, part of Silicon Valley, part of the East Bay, and part of the North Bay.

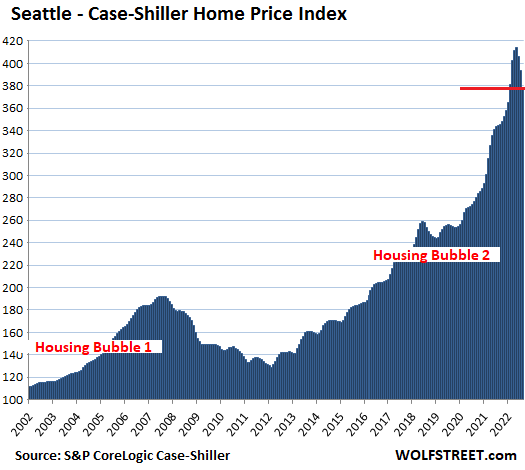

In the Seattle metro, house prices plunged 3.9% in August, the biggest month-to-month plunge on record, on top of the 3.1% plunge in July, and the 1.9% drop in June. The index has dropped 8.6% from the peak.

During the last three months of the spike, the index soared 33 points; over the first three months of the decline, the index plunged 36 points, like San Francisco unwinding faster than it had spiked. The index is now at the lowest level since January. The year-over-year gain shrank to +9.9% from +27% earlier this year.

The Case-Shiller Index uses the “sales pairs” method, comparing sales in the current month to when the same houses sold previously. The price changes within each sales pair are integrated into the index for the metro, and adjustments are made for home improvements and other factors (methodology). By tracking the change in dollars needed to buy the same house over time, the index is a measure of house price inflation.

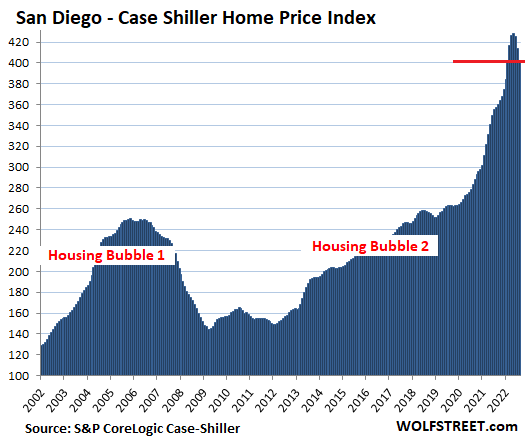

In the San Diego metro, house prices fell 2.8% in August, the biggest month-to-month drop since Housing Bust 1, after the 2.5% drop in July, and the 0.7% drop in June, to the lowest level since January.

The index is down 5.9% from the peak and unwound with symmetrical speed the last three months of the spike. This slashed the year-over-year gain to 12.7%, from 29% earlier this year.

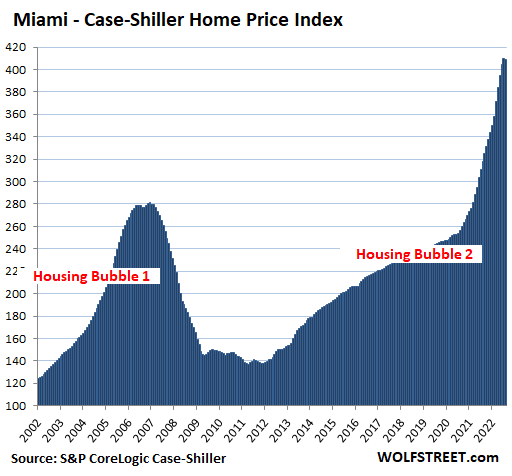

The current index value of 403 for San Diego means that home prices shot up by 303% since January 2000, when the index was set at 100. Based on the increase since 2000, San Diego used to be the #1 Most Splendid Housing Bubble in America, but has now fallen below Miami (+309%) and Los Angeles (+305%).

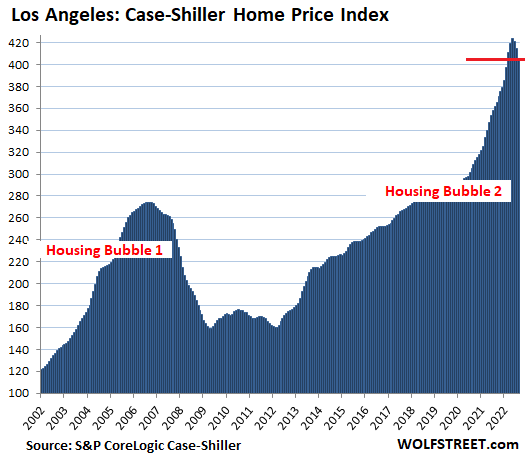

In the Los Angeles metro, house prices fell 2.3% in August from July, the steepest drop since Housing Bust 1, after having dropped 1.6% in July, and 0.4% in June. This slashed the year-over-year price gain to +12.1%, from +23% a few months ago. The index is down 4.3% from the peak.

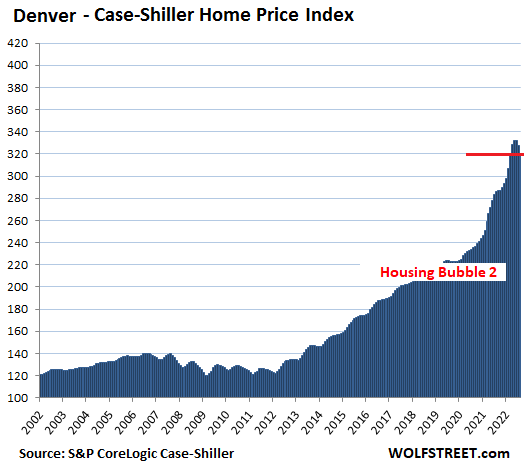

In the Denver metro, house prices dropped 2.3% in August from July – the second steepest drop on record after January 2009 – following the 1.4% drop in July, and the 0.1% dip in June.

The index has dropped 3.7% from the peak, cutting the year-over-year gain in half, to 12.0%.

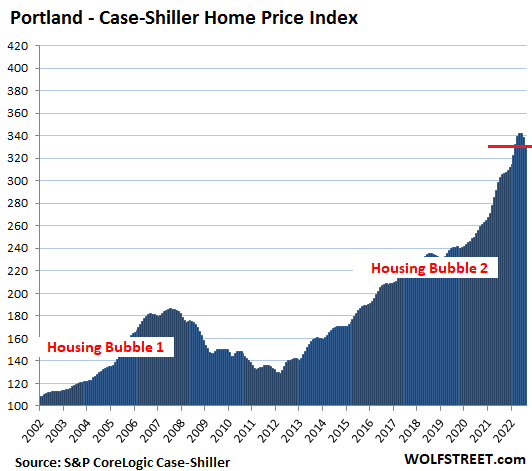

In the Portland metro, house prices dropped 1.9% in August, after the 1.1% drop in July, and the 0.1% dip in June, following a ridiculous spike.

The index has dropped 3.1% from the peak, cutting the year-over-year gain to +8.6%, from +19% earlier this year.

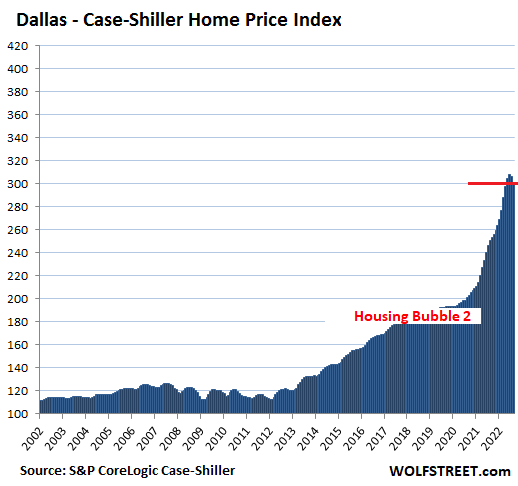

In the Dallas metro:

- Month over month: -1.9%, after the -0.4% dip in July.

- Year over year: +20.2%, down from +30% earlier this year.

- From the peak: -2.3%.

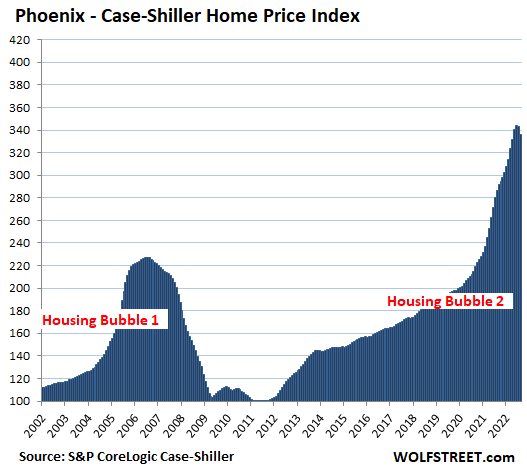

In the Phoenix metro:

- Month over month: -2.1% after -0.2% in July.

- Year over year: +17.1%, down from +32% earlier this year.

- From the peak: -2.3%.

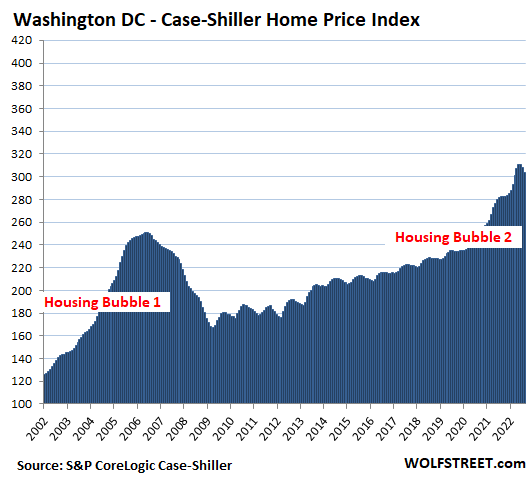

In the Washington D.C. metro:

- Month over month: -15%, after the 0.7% dip in July.

- Year over year: +7.4%, down from +13% earlier this year.

- From the peak: -2.2%.

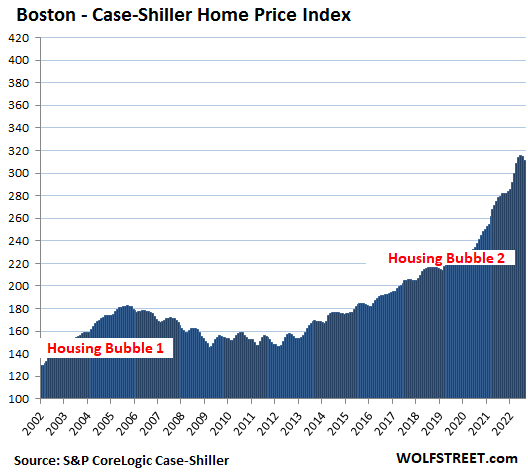

In the Boston metro:

- Month over month: -1.2% after -0.3% in July.

- Year over year: 11.4% from +15% earlier this year.

- From the peak: -1.5%.

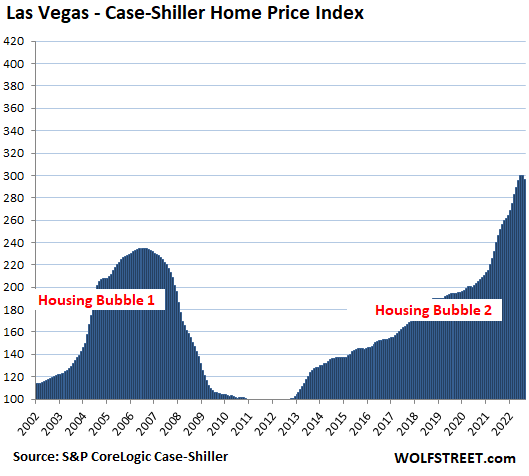

Las Vegas metro:

- Month over month: -1.3% from the record in July.

- Year over year: +17.5%, down from +28% earlier this year.

- From the peak: -1.3%.

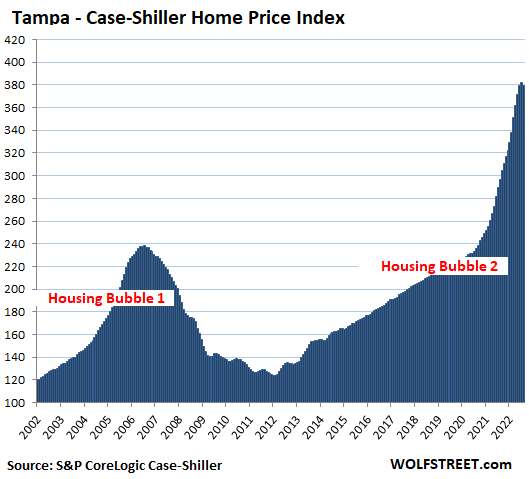

Tampa metro:

- Month over month: -0.5% from record in July

- Year over year: +28.0%, down from +36% earlier this year

- From peak: -0.5%

Miami metro:

- Month over month: -0.1% from record in July.

- Year over year: +28.6%, down from +34% earlier this year.

- From peak: -0.1%.

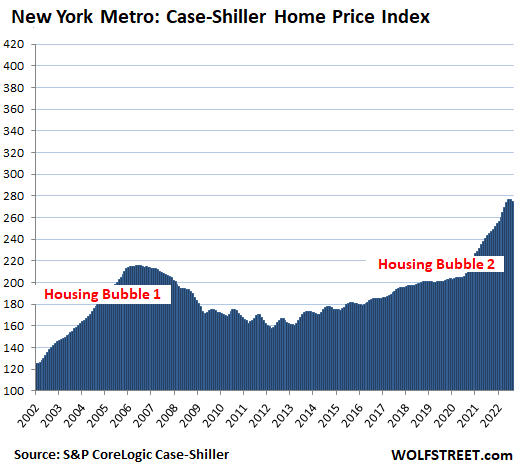

In the New York metro:

- Month over month: -0.5% from record in July

- Year over year: +12.3%, down from +15% earlier this year

- From peak: -0.5%

The New York metro has experienced 175% house price inflation since January 2000, based on the Case-Shiller Index value of 275. The remaining cities in the 20-City Case-Shiller Index (Chicago, Charlotte, Minneapolis, Atlanta, Detroit, and Cleveland) have experienced less house price inflation and don’t qualify for this illustrious list of the most splendid housing bubbles. But all of them booked month-to-month declines in August.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

It is interesting to see that the multi decade erosion in NYC economic strength is reflected in the fact that it has had some of the more muted reactions to the rigged-interest-rate “booms” of the last 20 years.

Even PCP-laced crack won’t get a dying horse moving very much…

Interesting extrapolation, cas127. Your take on NYC’s fading economic strength, vis-a-vis house price run-ups, would seem to lead to the conclusion that SF, LA and San Diego are among the strongest economies in the country which comports well with the article I read this AM indicating that CA is about to displace Germany as the 4th largest economy in the world. All of a piece, I guess.

The most important thing to note is that “The rate of drop is atleast exceeding the rate of rise, just like a mirror image!”. So many real estate “experts” were predicting a slow correction over 5 years citing 2007.

These experts were most probably on payroll of Real Estate industry. It’s important to figure out a conflict of interest.

If they thought 2007 was a slow correction over 5 years, they didn’t have skin in the game at the time, and they haven’t bothered to study any of the charts like Wolf’s that people have made since 2007 either.

spoke with my realtor yesterday

he took listing over weekend(Tucson)

and had 7 showings on monday

asked if he discounted – not really

inventory?? still low

closings? 50% all cash

Crazy to think only Japan and China have a bigger economy than California.

Agreed, Harrold. Especially when you consider that Germany has twice the population of CA. (Per capita: $85K for CA and $48K for Germany).

Really? I haven’t dug into it, but I suspect a lot of what gets counted as “California’s economy” is really made elsewhere. For example, are all of Apple’s sales counted as part of CA’s economy?

TonyT,

That’s NOT AT ALL HOW GDP is counted. No one counts Apple’s sales as GDP, anywhere.

State GDP formula for California is the same as national GDP formula.

In the GDP formula, no one cares about corporate revenues – never ever. They’re not counted.

GDP counts spending and investment minus imports plus exports. How much did Apple invest in California by building an add-on shack to its Spaceship, and how much did Apple consume in California, such as utility bills paid in California, food bought in California for the employees, gasoline bought in California for its corporate fleet, lease and maintenance spending for its office buildings in California, etc. Plus all the products and services any entity exported from California minus all the products and services any entity imported into California, including whatever Apple did.

The formula for GDP for any state or country:

GDP = consumer spending plus business consumption (both together are “private consumption”) plus government consumption (not for salaries but for paperclips, vehicles, lease payments, etc.) plus gross investments by all entities (for buildings, machinery, infrastructure, etc.) plus exports minus imports.

Thanks Wolf. Not sure GDP is the best overall metric for the health of an economy.

Agreed. But that’s what we got.

I am going to take the wild guess that if true, this reflects the methodology of measuring GDP, not a reflection of real production much less relative living standards.

True. Living standards in California are superior to China.

Got to sell it for double to mean anything.

Let me know when you sell it for double. Sorry bud you missed this one!

Fun part about having your house double is the house you want to buy has also doubled…

Win lose sort of situation

I bought in 2011, bank repo. Under $50K and only a bit of fix up / paint needed. It hit $295K at the peak.

But I’m not moving, so what it would sell for means nothing in real dollars.

Aaand a nice fat increase in the taxes i have to pay to live on my land in my house… argh.

Calling this an epic bubble might be stretching it? Interest rates go up, cash prices come down, simple economics. There will be an equilibrium. I don’t feel like this is ’07. This is a supply/demand distortion that needs to be corrected. Sure, maybe a nice big drop, but not a recessionary force.

Everything might be a lie. Supposedly the main job of the Fed is stable prices. See any stability in price of a house?

All of these spikes look like fast money to me. It’s a price vs value proposition ultimately.

Actual value of houses (ie utility) of houses didn’t change all that much since 2020 but the speculators and real estate floggers appear to have gotten ahold of the pricing mechanism.

That fast run up will work against them for now. Back to the trend I suppose.

Or as noted below maybe it is the big wad of free money they just printed blasting into housing? If there’s nowhere for that to go now it might mitigate the price drop at this point too. Watch gov’t bond prices maybe as a relief valve for all that moolah.

@Natron,

Here’s the calculus — the Fed doubled the price of stock in about a years time, while simultaneously reducing interst rates to zero. So anyone with $1 million in stock at the beginning now has $2 million at the peak, for $1 million in instant “free” money. So obviously, price is meaningless at that point. Overbid a house by $300K? Big deal! You still have a free $700K left over. So of course there was a stampede to buy, paying hundreds of thousands over asking to get the house you want. Then, this herded the lower end buyers into a stampede, and so now we have raging inflation that won’t abate/correct until a massive fall in the stock market and millions of job losses.

Finally, what does this absolutely moronic decision say about the “leadership” running the governments and central banks of the world?

If you have multiple buyers outbidding each other and willing to pay way over asking price – it is an epic bubble indeed.

Mike,

Your comment reflects a common misconception about the definition of a bubble. The bubble is the run up, the drop is a bust. It was the 0% interest that created the bubble, not the interest rate hikes we need now to combat inflation. It’s yet to see if the rate increases will deflate the bubble into a full on crash, or if the correction this time around will come via years of inflation with stagnant home prices.

The question is if this is (a) a “rhyming” repeat of 2008 and prices really crater, or whether, (b) the Fed freaks out and pivots, lowering interest rates and thus re-inflating. For me, the prices are simply too high to match wages without overburdening the average person at 50% of their income spent on housing.

Don’t forget the Fed freaked out and pivoted in 2008, and prices still went down a lot.

in 2008 you had FREE loans to masses

NINJA anyone?? no income, no assets

no problem – here’s $400k home with $0 down

—

around 50% of ALL home sales since 2020 are all CASH

I bought 3 homes this year all cash(1031)

and 1 duplex last year all cash

simple numbers for all you fiat worriers

in 1972 my home was built – cost $6,000

today $600,000

is there MORE VALUE today?? NO

so it only took more WORTH LESS fiat $dollars to buy same VALUE

“around 50% of ALL home sales since 2020 are all CASH”

That’s not consistent with any of the data I’ve seen or has been reported here on Wolf Street. From different sources (NAR, RedFin, Zillow) all cash sales have been around 30% give or take a few percentage points in recent years. Even at the low point for all cash sales in 2005-2008, they still represented over 20% (21-27% according to redFin) of all sales.

And how much of that “all cash” was really all cash?

How much investor “all cash” is actually backed by loans?

How much individual “all cash” offers are just a front by a company such as FlyHomes?

There’s a third option too. Despite much higher interest rates, the national median house price nearly tripled in the 70’s, and doubled again in the 80’s. But it dropped about 8% during the S&L crisis then went entirely flat for the first half of the 90’s. The median price only increased by about 33% from 1990 to 2000.

House prices don’t have to crash catastrophically, nor do they have to continue increasing. Prices could cool a bit where more affordable markets drop less and bubbly markets drop more, then the national median price could just go flat for much of the 2020’s while incomes catch up a bit. Time will tell.

Was the national medium house price already in bubble territory in the 1970’s? I don’t think so. Were mortgage rates at 3% then? Nope, they were > 7%.

There are other reasons for increasing house prices in areas like CA, including building restrictions. So it’s very likely that there were a lot of unique, non-repeatable circumstances.

Also, the US housing market is still very regional. For example, I don’t think the S&L crisis had much effect on CA, and I doubt the defense industry cutbacks in 1990’s or the dot-com bust of the early 2000’s had much effect on TX.

Essentially my thoughts.

The end of the bond mania in 2020 means rates are going to “blow out” later.

The stock mania may or may not be over, but if it isn’t, no reason to believe it has more than one up leg on a partial retracement of interest rates.

The job market is dependent upon a fake economy. That isn’t sustainable either.

Tony, how would we know that we’re in a bubble?

The fed funds rate was as low as 1% and spent most of the 60’s between 3-5%, so mortgage rates weren’t very high leading up to the inflationary 70’s. Median price in 1980 was 2.7 times what it was in 1970. That probably felt like an unsustainable jump to a lot of people at the time (a bubble). By 1990 it doubled again to 5.2 times the 1970 median. That probably felt like another big jump to a lot of people (a bubble). By comparison, the current median of $440k is *only* 2.3 times what it was 20 years ago in 2002 at $189k.

My point is that it is very difficult to identify a bubble until after it pops. Are we in a bubble, or did the dollar simply loose a bunch of value because we pulled trillions of them out of thin air in the last couple years?

I agree that real estate is local, but most commenters on here are talking about the broader U.S. housing market, so I chose to look at the national median price. Many commenters on here also seem to ignore the shear volume of money printing we just experienced. Our money supply (M2) grew ~40% from $15.4T in 2020 to $21.8T at the 2022 peak. Median house price went from $322k to $440k, just shy of 40%. Coincidence? Probably not.

This is in reply to Not Sure below.

I really liked his post, shared it actually.

But then I thought some numbers seemed high maybe.

I can’t vouch for the accuracy of the numbers at Dont Quit Your Day Job website, but he has nationwide median prices for 1953 to the present listed on a month by month basis.

Based on his numbers the 1970 to 1980 increase was a factor of 2.29. Not Sure reports 2.7.

And from 1970 to 1990 the factor is 4.04. Not Sure reported 5.2.

Lower factors make Not Sure’s argument a bit less persuasive.

The author of this website somewhere explains his methodology for the numbers published.

I’m not that housing savvy, anyone know why these discrepancies might exist ?

Randy, my figures are from the St. Louis Federal Reserve Bank’s FRED data tool. Specifically the (MSPUS) dataset for median sales price of houses derived from HUD and Census bureau data stretching back to 1963. These are nominal values for all sales (new and existing) listed quarterly and not seasonally adjusted. Your source’s numbers are still easily close enough to reinforce the point that house prices have multiplied a lot less over the most recent 20 years than they did between 1970 and 1990. Another 20 years from now, we’ll be able to look back and say with confidence whether the 2020’s were another housing bubble or simply another inflationary period. Here in the now, it’s hard to say for sure.

I am responding to Not Sure’s post on 10/26 9 am.

Thank you for the excellent response.

I have summarized the content of your 2 posts as well as mine and sent it to the folks running the Dont Quit Your Day Job website. I said that I was not suggesting their data is wrong but given the non trivial differences in the two factors (2.7 vs. 2.29; 5.2 vs. 4.04)…

could they explain why these discrepancies exist ?

I included links to your posts (Thanks Wolf, smart move).

I hope they get back to me.

If they do I will let Wolf know what they have to say.

A couple weeks ago I briefly read their methodology for creating their median home price data. I didn’t follow it too well, but I believe they draw from 2 or 3 datasets in generating the house price data. Don’t recall if the St. Louis Fed Reserve data which is your source is one of their sources.

Randy

One last comment regarding “Not Sure’s ” post regarding historical housing prices. Wolf suggested I post this:

Hi Wolf,

Here’s a link to their (dqydj.com) website dataset.

Scroll down and they mention the 3 datasets they draw from to generate their historical home prices. It does NOT look like the St. Louis Federal Reserve dataset is one of them. This is what “Not Sure” used and presumably is one of the more standard sources. It could be they went this route to avoid costly subscription fees I’m not sure.

I hope they get back to me.

They have a contact us form, that is what I used.

https://dqydj.com/historical-home-prices/

They state they use these 3 sources for historical home prices:

– NAR median sales price

– Shiller NSA home sales index

– FHFA home sales index

Please see their site for details.

Randy

House prices can only flatten out if people can generally afford the payments. In many markets the new interest rates make payments at

“flat” pricing totally unaffordable.

I think there’s a common conception that home prices could just plateau, but that can only happen if the payments are affordable. With a looming recession and payments jumping 40% in such a short time, there are much higher probabilities we see prices dropping fairly rapidly, possibly faster than they went up – as this article is illustrating.

There’s also the psychology factor.

When prices are going UP, people are OK with >45% DTI’s, over bidding, and other risky behaviors.

When prices are going down, well, then a lot of people will decide to wait.

If prices having been going down, many will be skeptical about levelling off; even if prices do level off (maybe temporarily), most will have much less risk tolerance than when prices are shooting up.

Note Sure – Well Put.

just finished a 90 min beach sandbag workout … i’ve got the covid vaccines/boosters. haven’t croaked yet but i’ll let you know if i do.

If Housing Bubble 2 crashes in about the same way as Housing Bubble 1, the bottom for prices is 1-5 years from now.

The wide range depends on the local market (jobs & housing supply). It also depends on whether one is looking for the lowest price, the lowest price after inflation, or the lowest monthly payment.

If the Fed is forced to sustain the high interest rates this time (whereas before they were cutting rates), it could go a little faster. But psychologically I think it will take buyers and sellers at least a year to adapt, regardless of rates.

There is always a light bulb moment where sellers go from “sticky” price cuts and a “not giving it away” mentality to a race to under cut the competition and sell quickly before the market tanks even lower.

And then comes the “how much do I need to bring to the table” to closing moment and a decision on jingle mail.

In markets dropping this fast the only way to sell for sure is an auction.

The vast majority of home owners won’t hit the jingle mail boundary until prices drop by around 40%. Expect a long wait for that, *if* it ever happens.

To clarify, there are 140 million homes out there. Let’s say that after extreme losses, six million of these homes become jingle mail. The vast majority of homeowners will be intact.

The other consideration is that jingle mail is less likely today thand during the GFC, because those who refinanced at zero percent today are likely paying (much) less per month to live in their current home than they could find by renting or buying another home. This “sticky” situation didn’t exist during the GFC.

Wisdom Seeker

“…..If Housing Bubble 2 crashes in about the same way as Housing Bubble 1, the bottom for prices is 1-5 years from now….”

I would agree this is going to be drawn out compared to 2008-2012 for the reasons you cite. Doing the comparison, we are in early 2008 now. As you suggest, we will likely see annual drops and a leveling off in 2025-2026. It will likely look like a natural projection from where we were headed in 2020 before Covid. We are still 13% higher YOY across the board…….looooooong way to go.

No one knows how this would play out but keeping in mind the proliferation of social media, I guess the drops would be faster the way hikes were faster ( 50% plus in my place in last 2 year ).

It is easier for news to spread like fire now a days.

Let’s see.

jon

I would agree there may be some rapid declines in pricing initially (2022 / 2023), but when you are still 13% (on average) higher in Oct 2022 vs Oct 2021, it will take massive drops in pricing over an extended period to even be termed a “correction.”

The last one took five years. You guys have got to get off the instant-gratification bandwagon. Real estate doesn’t correct like cryptos overnight. It takes years. But this is a VERY FAST start compared to Housing Bust 1.

Prices are set at the margin on the way down, same as on the way up. The “blow-off” top poses no obstacle to a crash. To the contrary, it makes it more likely.

Best argument I can think of for a slower decline is future mortgage forbearance and foreclosure moratorium.

Otherwise, the decline should happen much faster.

QE stoked asset prices. QT will implode asset prices. One wonders how many people owned multiple homes for speculation?

All will be fine.

Everyone put down 20%

Plenty of savings in the bank.

With a job that easily covers the mortgage.

Rock steady mortgage standards.

No government guarantees, banks eat their bad loans so they are super careful.

The 90s called, they want to keep their affordable housing.

Amen Brother. I was one of those. We said to heck with a big wedding reception to get to a 20% downpayment and avoid PMI. Today, my circle of friends and neighbors just kept borrowing up to max home equity. They have big trucks and in-ground pools (in PA, pools are good for 2 months of the year). They keep checking their credit scores to see if more money can be borrowed. I haven’t looked at my credit score in ?? years. I have no debt either. Not because I hit the lottery but because we are prudent. We should go back to the responsible 90s and our elected officials should set the example. I am afraid that too many people don’t understand fiscal responsibility.

I thought we were the looney ones. We took our home savings and paid off 147k in student loan debt (wife’s a pharmacist) instead of buying a home and I felt pretty miffed missing the boat on 2% rates. But I see everyone with a new car, massive upgrades to their homes or the endless Disney vacations from every mother at my child’s school.

It definitely makes us feel like we are doing something wrong. About 2/3s of the way to the 20% down payment saved up again (plus closing costs), inflation is not helping that at all.

I get paid very well for my line of work, wife is part time due to the daughter but she pulls in a nice income still. Our cars are paid off and are 10+ years old at this point and chugging along fine.

I tell ya the whole keeping up with the Joneses is more apparent now than ever, maybe living in NY doesn’t help either.

Outward appearances of wealth are a poor reflection of what is going on behind the scenes. Leverage allows for a bigger lifestyle, but leverage is risk when things go wrong.

I went to no debt living about 20 years ago and within a couple of years was able to stop working. I am much happier than when I was knocking myself out 60 hours per week in corporate life, but modest lifestyles aren’t for the undisciplined.

Very true OS:

NO DEBT and modest life style means ”savings in the bank” every month in spite of ”income” low enough to pay no federal income taxes since retired in mid 2019.

But, as you say, takes a bit of self discipline that appears to be lacking these days as always, or at least since WW2 in USA.

Many, maybe most folks do not seem to comprehend the vast difference between NEED and WANT,,, certainly not being taught in the schools where the latest FAD become SO important.

NY, particularly downstate, is seemingly culturally devoid of normal thinking. I know of many over-leveraged, debt-to-eyeballs types desperate to keep up with the many others in the area who truly are wealthy.

New wealth folks in huge houses using lawn furniture in the rooms guests don’t see, not using coupons at the grocery store because of optics, heavy substance abuse and deep tax debt, all to keep up with the neighbors. The Old Money always seem to be the nicest and most down to earth folks, not flashy. But the New Moneys can be vipers, not all of course.

For some reason though, it persists over the decades and generations. The ones who fail do so incredibly quietly.

Slightly unrelated but still curious how Student Loan repayment will factor into the housing market (not downstate NY’s of course). If prices are plummeting already, will Jan 1st throw cold water on buyer’s plans? My broker said the bank will factor 5-10% of income for loans in the DTI until repayment resumes and hard #’s are available, but previously they left it at 0 and other banks may too.

All great points by you guys. I took have noticed that when I deal with old money clients (I still do side work repairing luxury cars from time to time) and they are some of the nicest people I’ve ever met. They don’t haggle me on a price, half of them have invited me to their summer parties or to a BBQ or three, and keep in touch from time to time.

Most (but not all) of the new money people have been downright rude, obnoxious and quite selfish. Always nagging me on prices, quoting others, and usually never hear from them until they try to price out some work (albeit cheaply in their eyes)

Ahhhh,

You forget that job losses also play a HUGE part in foreclosure crisis. I’m watching as the construction industry is collapsing and all the jobs that go with it: architects, material suppliers, etc.

Many of the people who ended up in foreclosure during the Great Financial Crime Spree were innocent victims by job losses.

But people have to at least consider the possibility of job loss when making major buying decisions.

Historically at least, there was a major choice between taking on a $150k home mortgage or a $450k one…the latter created major financial risk/stress for little more reason than to keep up with the (hidden addict/abuser) Joneses.

It was an exercise in ego that led to financial ruin.

Today (the era of Societal Joneses Psychosis, as fed by the Fed) it is marginally harder – since a deluded society builds a much higher percentage of $450k houses.

But avoiding a large degree of financial risk is still possible – rent instead of buy, move instead of accepting financially insane housing prices.

Leverage works both ways.

What’s a decent “used to be middle class” house in SF now…a million bucks?

Now, imagine losing close to $100,000 over the summer…ooofff. You are way underwater now. Hope you don’t have to move in the next few years.

Now imagine all the flippers getting wrecked. The alligator will eat them alive.

“The index has dropped 8.9% from the peak.”

Thank goodness that the Fed/DC used money printing/manipulated interest rates for 2 decades to “save” the economy…

Turning the housing market into a casino (and, after all, how many people really use housing…) to “optimize GDP growth” is really one of the genius moves in human history.

LOL

Even the people who don’t intend to move will be impacted at least psychologically if their home drops $100k. No one likes to feel like they’re stuck where they’re at or that their home is no longer worth what they paid.

I just got full asking price in SF, closed today, listed in June

Inner Sunset area. Nice young couple.

Full price, eh? No price reductions in 4 months? Just sat there since June? Interesting.

Longer escrow, more tedious than interesting.

Cd,

He means “interesting” as in, “you are full of shit”.

It’s always the younger people who seem to take it on the chin the hardest. Lack of experience and wisdom imho. Should be underwater in less than a year

I still have friends owning 3 or 4 properties in San Diego and they think prices won’t go down.

In fact one of them is buying another property for 1.4 million dollar.

Things are crazy.

We all see what we want to see.

There the ones that can take it on chin, over 30 yrs they will be Head no matter

@Steve: I think the young people buying homes for Airbnb are in for a wakeup call. They have been getting their advice from gurus on tiktok.

@Jon: San Diego is implementing new rules limiting vacation rentals to a limited number of permits being given out selectively. If interest rates don’t lower house prices, these new restrictions will. It may even cause a sell off as people discover they can no longer rent their houses nightly.

From June to today, mortgage rates went from 5% to 7%.

But you got full price from a young couple?

Yea, Young people are making a lot of money I know I work with a bunch of them, I work in a credit industry, Still busy, just went to a fintech conference, Amazing things coming In the financial world. If you’ve been around the block or were actually on calculated risk in 2005 you already know that this is not 2008-9

I bought a lot of paper at these rates in the nineties And the incomes were a lot lower to go along with a lower price hous

Cd,

So you work in a “credit industry”…maybe mortgages?

Did you work for Countrywide, etc about 20 yrs ago?

They were “doing incredible things” in finance too.

(Actually, when I saw this line, I laughed my ass off…it is like been told to go into “plastics” after exiting a showing of “The Graduate”).

Let me guess, you work for Trolling Credit Originators…

Young & hyper-credulous = synonyms.

Look at Wolf’s chart above. The only people who would be underwater from a $100K loss in SF bought in the last year. That’s a tiny fraction of homeowners.

I read a lot of the comments along with the articles. Wolf lays it out like a champ.

I’m not one of the financial ‘learned’ but it seems to me that the price was never really paid in the GFC and everyone and their brother was bailed out.

I think there’s a reset coming all the way back to 2010 -2012 pricing. Can anyone really state (other than free FED money) what is better since then? Maybe even more.

They talk about the quality of the borrower as better. Ummm, yeah okay whatever. Those same great borrowers have $60k trucks they pay $700 a month on. Meanwhile, if they have a 401k it’s lost 1/3 value.

Still lots of money sloshing but all it takes is one stumble and this bucket is getting poured out.

“$60k trucks they pay $700 a month on.”

Making hugely overpriced “sales” via ZIRP-addled, doomed loans (in turn sold off to intentionally yield starved savers) bears the same relation to a healthy economy as an animated corpse bears to a living human being.

DC has engineered two decades of a zombie economy, the Walking Dead of responsible governance.

Democracy is messy. Don’t worry, you won’t have to put up with it much longer. You’ll probably get another figurehead Savior pretty soon, (much better the Reagan, but similar agenda) unfortunately. Hope you are well connected, and NOT in DC…..like I am. You will still need the people I know, and they also know it.

Borrower quality is still in the basement, maybe just not in the sub-basement.

Yes, aggregate consumer credit indicators look good now, thanks to a waterfall of “free” stimulus money and an artificial labor market from a fake economy.

Lending 80% (where it even happens) on a bubble priced house isn’t conservative lending.

The idea that mortgage standards are “tight” is a farce.

Even aside from rising mortgage rates and now falling prices, 2022 is purportedly the worst year in over a century for the 60/40 “balanced” portfolio. Or so, I read. Hard to believe it’s worse than 1931 but there you have it.

Hammered portfolios are also going to reduce housing demand, if not now then later.

For Washington DC, there is a decimal missing in the month over month number.

Double digit percentage gains for the year is pretty damn good, but the light at the end of the gravy train tunnel is now heavily obscured. Housing Bust #1 occurred in rapid fashion. This Bust will be even faster & steeper as evidenced by what is happening now.

We sold in Commiefornia a year ago. You can never market time the real estate market but having experienced enormous pain as a homeowner in 08/09, we saw the writing on the wall. And we wanted to sell while there were still buyers looking to buy at astronomical prices. Now we’re living in a small farming community of 3,000 people & preparing for the Great Reset soon upon us all. It’s a matter of how best to survive and prosper in the coming dark winter.

Must now be in some place warm. Texas?

Warm is not the word for Texas. Insufferably brutally hot. It’s almost November and the AC is still on! Soon there won’t be a month it’s not on.

A bit off topic but believe many will find this of interest.

I lived near Dallas for 11 years. Agree, quite hot there.

This year was quite brutal for Dallas and Austin, much hotter than usual.

Accu Weather website let’s you see temperatures for any month, any decent sized city, last 2 years.

Another unusually hot summer where I live in Spokane Valley, WA as well. Per numbers I got from Accu Weather the average July high was 90°, the average August high was 92.3°. Also per the Accu Weather numbers we had 9 days with highs 100 or more. Last year 10 days.

Total of 44 days 90 or above (including 100 days). Fifty last year.

We are only supposed to average 20 to 25.

These numbers do not agree with the official reading numbers which come from the airport 6 or 7 miles outside Spokane at about 2400 ft elevation.

Official readings are cooler. I prefer Accu Weather numbers, they come from Spokane or Felts Field I believe.

Spokane is at 1850 ft. elevation, hence warmer than the airport readings at higher altitude.

Dallas might well have had close to 50

days 100 and above, also considerably more than their average. It was around 35 days end of July I believe.

Thing is Spokane is 2.6° latitude north of Minneapolis… about 180 miles.

And yet we are getting these really hot summers now.

Two or three years ago, a small town maybe 100 miles to the NE of Vancouver, BC broke the all time Canadian record high temperature of 120 or 121° F (it was just under 50° C).

Yes ! British Columbia.

Its October 26 and we may have gotten a little snow tonight already… will melt quickly if we did. But it cools down quickly September to November here in Spokane. Not a native Washingtonian, resident 26 years.

> Commiefornia

Good luck, and I mean it.

I don’t know how old you are, but I’ll tell you what. My SoCal home is 1/2 mile from a literal medical city, that is my health care provider. Costs me all of $170/month and everything else is lavishly subsidized. Pharmacy 1/2 block away.

My energy bill is now circa $25/month, winter or summer. How best to survive is about adding one more blanket, done.

I lived in the country (yeah, rural SoCal, it did exist) as a kid and loved it. Key words “as a kid.” Everything has its risk profile. I guess Kim could drop a missile on us.

“Lavishly subsidized”

Government “worker”/public sector union member retired at 52?

Also, for yucks, what is,

1) the top marginal income tax rate in CA?

2) the median marginal tax rate in CA

3) the median mtg pmt/2 bedroom rent in Med City Suburb

Subsidies don’t get pooped out by the magical glitter dusted unicorn fairy…not even in CA.

The money/resources come from *somewhere* and it ain’t all from Fed defrauded savers in other states…

Thanks for the laugh, D.

I’ll stay where “the grapes grow”, as I told my logger friends from HS when I was out of work (80s recession was very hard on me) 40 years ago, when they said I could make really good money fixing all the equipment used on Vancouver Is. and other places in that area. (they knew how good I was at learning, and fixing or building anything)

They said, “fine, just keep sending them up in little bottles then”.

I could see prices rapidly contracting over the next 12-18 months, erasing 15%-20% of their previous gains, but then continue to slide more slowly over the following months to finally bottom out sometime in the next three or four years.

I’m thinking along similar lines:

— Rapid decline to pre-pandemic levels (~2019)

— Slow down (given amount of $$$ sloshing around)

— Slow decline / stay pretty flat despite consumer price inflation.

Even with a serious Fed, I’m guessing we’ll have significant inflation for at least 3-4 more years.

That would be the way if everything goes per plan. I just keep thinking about the amount of bad collateral it creates. People did cash out refinances and HELOC at record high prices. They owe full amount on those houses. They tapped all of their equity. What happens when they are 30% down, and people owe a lot more than what the house is worth.

Everyone says no subprime so all is good. But in my view, it would be naive to think that all of that bad collateral is just going to sit there harmlessly.

When to many owe to much, the bank have a problem. Or maybe rather the holders of MBS as the loan originator have sold the debt.

Banks get bailed out. Individuals do not.

Some banks offering high interest rates have a bunch of junk debt like subprime car loans. But they are FDIC insured. I can’t figure it out, or maybe, I don’t want to figure it out. Where are the auditors with green eyeshades warning these lenders about their shaky balance sheets? then I remember the S&L debacle. I’m not sure about the ability and willingness of home buyers to keep paying. Bank of America’s CEO said this week (I paraphrase) it’s all cool.

Subprime auto loans, and even prime auto loans, are offloaded into asset backed securities (ABS) and sold to investors. The bank is just the originator and servicer and got paid fees to do it.

Phleep,

As Wolf laid out, just think of today’s “bankers” as middle man bookies, backed by the G-built “secondary loan mkt” (only for homes…but homes are the overwhelming source of debt).

There are gamed “standards” that are supposed to apply to conforming loans sold into the G guaranteed secondary market, but the G systemically loosens them causing a doomed build up of price inflation/correlated risk.

Built today (along with ZIRP) to be a habitual bubble machine.

Better look at Chinese economy,we see to be following them albeit in a slower car .

Chinese are much, much better off.

They may have a lot of debt (US has more and effectively zero foreign reserves compared to China’s 3 trillion) but they have a brand new, world scale industrial base and the US has the rotting corpse of Pittsburgh, Detroit, etc).

You’ll have to hold Yuan to buy new products from China in the future.

Your progressively diluted USD will only be good for buying decaying real estate in a former “superpower”

I’m still baffled by how the S&P likes to sit 1000 points below the all time high. People liking round numbers doesn’t cut it as an explanation.

So, I propose that any future study of Economics be divided into three sub-disciplines, based on what Bush2 said at a fund raiser for his brother.

“You have the haves, the have-nots, and the really haves” It got a good laugh, too…..must have been mostly the latter there.

Its all going to go the way of the tech stocks in San fran. A friend bought a 3 bed for 3.5 MM and closed in May, poor sucker

I wonder what that home will be worth in a year. 2.5 million?

1.2

I wouldn’t be surprised!

your dreaming. We closed today, full asking price in one of best neighborhoods in SF…RE is local, hard to find any homes in our area up for sale, very gentrified and best walking score you can get….nice young couple.

cd,

Someone tells me they got “full asking price,” I get the willies. Asking price is whatever you want it to be. It doesn’t matter what it is. You should have said that you closed at “$1 million over asking.” Lots of stories out there about that. Asking = $500,000 to start a bidding war, then sell at $1 million “over asking” for $1.5 million, after having bought it a year ago for $1.8 million, and having lost $300,000 on the sale, but it was $1 million over asking.

No one here should even mention “asking” because it is invariably designed to deceive.

*Another* “nice young couple” from cd (he of Troll Real Estate).

Were they a “nice young couple” of Swedish Bikini Supermodels?

“Dear Penthouse/NAR Journal,

You won’t believe this, but as I was eagerly eying the MLS…”

He who panics first, panics best!

“Try. Fail. Try again. Fail better.”

– Samuel Beckett

These 3 and 4% fall in price is noise compared to almost 2x increase. If you dissect further into data you will realize that the price of good homes in good neighborhoods have barely budged. In fact in Bay Area, good homes in tier 1 cities are still rising. Its the bad apples which are falling back to the ground as expected. With rising costs: construction, permit, labor, fee, material, insurance, rent, land, fuel, energy, electricity, etc. there is literally ZERO rationale behind a housing crash. If anything they will keep rising with inflation which shows little signs of fall.

Inflation seems like a vicious beast which Fed is trying to tame and hold in a box with laughable hikes but the moment Fed will blink, it will come back roaring. Inflation mindset has set in deeply and only a depression will stop it in its tracks and Fed has no balls to do that. Keep in mind that interest rates are still deeply negative.

Our jokester is back :-]

SocalJim has risen from the dead just in time for Halloween.

This has to be a troll post, because nobody could be stupid enough to believe this sort of nonsense.

I believe every word this is the most reliable comment board in history. I study it daily for wisdom, including archive pages.

Are you related to Abby Normal?

If the Fed choice poison will be recession as they have been saying.

In absence of Lawrence Yun visiting this site and posting a comment..Kunal you complete me :)

Kunal wrote:

“These 3 and 4% fall in price is noise compared to almost 2x increase.”

That’s just basic innumeracy.

These monthly drops are HUGE.

The SF drop of 4.3% is fully 41% annualized.

Yes we shouldn’t extrapolate from one month’s data but the pace of price declines is accelerating and likely to continue to do so that almost 2x gain could easily be gone within a year.

If you find the M2 and M3 graphs at the St Louis FED site you will observe a small reduction in both. That is a measurable deflation.

Next construction cost, permit, labor, fee, material, insurance, rent, land, fuel, energy, electricity, etc. do not necessesarrilly matter in the pricing of existing houses. Purchasing power on the other hand do matter.

Also of course, a 100% increase in a house price only needs a 50% decrease to get back to same starting point:

$100k house goes up 100% to $200k; same house at $200k has a 50% decrease and so is back to $100k.

And even worse if you levered up with part of that $100k equity increase!

Also, I suspect that many ‘all cash’ buyers are no such thing: with negative real rates and newly non-zero returns on CDs etc, it makes no sense to lock up a bunch of cash in fully-paid-for new real estate purchases in a declining market.

The asking prices have risen slightly here in the past 2 weeks, but the selling price has fallen.

This is just getting started on the West Coast.

Microsoft, Amazon, Google, Facebook, etc. only recently announced hiring freezes and/or initial layoffs in Seattle. New building construction has been put on hold. This drop-off in Big Tech hiring activity hasn’t even impacted the market yet, even though buyer interest has already declined significantly. Buyer interest has a LOT further to fall.

Also, one must factor in the mortgage rate increase to 7%, which happened recently, as well as this first break down in Case/Shiller trend.

Potential sellers have nothing but bad news to look forward to. Fed pivot is a pipe dream until RE fall 20%, and even then, it won’t be enough to stop the trend. A flood of inventory is about to hit the market next Spring.

The negative feedback cycle has started.

Few blockbusters coming out of Hollywood, too. I’m curious what the CA economy is levitating on.

Black Panther returns next month

What the blockbuster movies contribute to the Hollywood economy is a mere peanut when compared to the RE industry.

Alas, in formerly more affordable cities near big, expensive cities, the party continues — although not as furiously.

In the biggest city in the littlest state, I’m seeing prices holding steady, and even a few 1-3 percent over asking bids on the most desirable homes. The true dogs are sitting and having to cut by $10-20,000. But anything affordable ($200-350,000) is still going for asking, even if that asking price is $50,000 more than it was last year. The buyers, I suspect, are all WFH/hybrid folks from the more expensive metro up north. Local wages do not support these prices.

So I fear this type of city will only see price declines once layoffs happen, if they ever do happen. Anything short of that, I’m afraid a new normal has been set. Which is a shame, considering the housing prices in this city completely deflated after the housing bust of 2008, and it was truly affordable for average joes. Only now are some of the people who bought at the 2006/7 top able to offload their properties — thanks to the WFH/hybrid folks.

Just wait for few months/ a quarter or two. Reversion to mean is coming and would be painful.

we are in the very early stage at this time.

WFH = E2F (Easier to Fire), or so goes the current mass media wisdom, lol.

Hal? You still around?

I live between the two metros. The number of Bostonians/inner ‘burbanites coming into our market has skewed things for many years to come. We don’t earn anywhere near what they seem to make up there. Our residents are moving to Pawtucket or Fall River, and even there the costs of just surviving have grown to a crazy level.

And this is a 3 month lagging data. The situation on the ground right now is a lot different (worse). Keep in mind that June, July and August still had low (near 5%) rates and several buyers in the Seattle area were buying, thinking rates had hot a bottom. BTFD is the way of living, right?

Rates were 6% in September and 7% in October. That deceleration is only accelerating and will show up in Jan/Feb 2023 reports.

Correct, my county had a LOT of sales in august due to the lower rates I’m guessing. Since that time almost nothing has moved.

Due to social media, this bubble rose more quickly than the last one and is popping more quickly than the last one – at least so far. Those who followed the market very closely in the last bubble and called the top know many markets topped YEARS before recognition nationwide and in the stock market. We’ve managed to cover that ground in 8-10 months in this bubble. Shorting a lot of the housing related sectors has worked pretty well.

Also, hard to think a recovery is anywhere close with commercial RE sucking wind. We need business to drive the economy and right now it seems that at least some significant portion of businesses are the cartoon coyote that has gone off the cliff but refuses to look down (and do significant layoffs).

Great article as always Wolf. I love the primer of Shiller methodology also. It just means that the pain and hurt from the interest rate hikes are just slowly starting to show up. I will be waiting patiently in my rental for the ‘impossible’, which should be occurring next summer!

There wasn’t any short term rentals in the first housing bubble, and you’d have to think that more than a few AirBnB’ers are headed for the exits, and unlike a conventional home owner, it’s pre-staged and ready for sale!

I’ve never used an STR, never would, but have looked at Airbnb’s website out of morbid curiosity. I laugh out loud at the prices. They are delusional. Every time I have plugged in dates, they are all available. Methinks most are languishing with no “customers.” When I want a hotel, I go to a hotel, not some speculator’s overpriced pressboard sh!tbox.

I never stayed in ABnB as I prefer hotel and related services.

I don’t travel in group, so a hotel room is usually sufficient for me.

ABnB nay show $100/day but they also add on lot of $$ for cleaning fees.

Wolf Oct fest.

Wolf ,

Can you please explain state GDP? If a semiconductor company headquartered in California, sells chips that were designed in Texas, manufactured and tested overseas, and sold by a salesperson working from a North Carolina office, does all of the sale accrue to California’s GDP?

State GDP formula is the same as national GDP formula.

In the GDP formula, no one cares about corporate sales – never ever. They’re not counted.

GDP counts spending and investment minus imports plus exports. How much did TI invest in California by building a new chip plant in Silicon Valley, and how much did TI consume in California, such as utility bills paid in California, food bought in California for the employees, gasoline bought in California for its corporate fleet, maintenance of its buildings in California, etc.

The formula for GDP for any state or country:

GDP = consumer spending plus business consumption (both together are “private consumption”) plus government consumption (not for salaries but for paperclips, vehicles, lease payments, etc.) plus gross investments by all entities (for buildings, machinery, infrastructure, etc.) plus exports minus imports.

Amazing and yes the AirBNB has contributed to the bubble and the most reckless Fed ever to bubble number 2 with checks and zero percent interest and two home purchases etc etc the list goes on with how and why the housing leverage is so large . REIT are leveraged then the CEF market in REIT has leverage on top of leverage.

I think the amounts are mind boggling .

In 1977, the FED’s mandate, “specified by Congress, explicitly stated the Fed’s goals should be “maximum employment, stable prices, and moderate long-term interest rates.””

Look at these charts. Where in the f**k was the FED? Asleep at the switch? No, ACTIVELY BLOWING THE BUBBLES. How in the world, and why in the world, did the FED pivot from a “stable prices mandate” to a “stable prices destroyer?” WHERE IS THE OVERSIGHT?

Ladies and gentlemen, what we have is completely corrupt to the core political system where the FED, in cahoots with corrupt, wealthy politicians,” looted the country. Jerome Powell, Ben Bernanke, Janet Yellen and Alan Greenspan should be arrested!

Arrest not enough.

Completely agree. Worst bunch of academic junkheads ever.

Hey, all the crooks made so much money in the Great Financial Crime Spree, why not do it again?

Kept their bonuses, kept the govt dole, kept the houses…

What more can you ask for but a do-over?

We currently have some sort of insane stock market melt-up going on – the DOW is up over 3,000 in less than a month. This is bad omen for interest rates and housing, because there ain’t no “FED pivot” coming anytime soon.

Waaaaayyyy too much liquidity sloshing around out there, looking for a place to get yield. Uh-oh, big ol’ rate hikes and mortgage rate increases coming right up, further destroying house prices. This is going to be the ugliest price crash in the history of housing.

haha everytime I see these melt up like today or this past week, I just picture in my head the market is taunting Powell and making him look even more like a little B**tch as if they know they got Powell figured all out.

Papa Powell might still get the last laugh though…this is the benefit afforded to someone that’s both the arsonist and the firefighter. These melt up actually is helping him even though WS and bond market think they got it all figured out…

If the FED actually came out and said they were going to pivot, I have no doubt the DOW would blast off to new all-time highs, and probably in a few short months. The amount of money sloshing around has been underestimated by even the FED. It’s a ridiculous speculative mania we have going on right now. Powell’s “soft landing” BS is a fantasy. The markets are roaring.

Agree with you. If the Fed wants to show that they are not slave to the market, they would reduce 200 billions of bonds a month instead of 95 billion. The fact is they are with the wall street, not the common people.

Wall street interprets moving from a 0.75% rate increase to a 0.5% rate increase as capitulation by the Fed, same as a pivot. I’m waiting for SPX to break the 3400 threshold, possibly causing wallstreet to change its tune.

Look at a 1-year chart: Lower highs, lower lows. On trend.

Tomorrow is going to be interesting. Much of big tech is down 4-7% afterhours today on earnings from GOOG, MSFT, TXN, etc.

I think it is kind of normal if we are in bear market to have strong rallies, but the bigger trend is probably down.

I have a few value stocks that I buy if they fall to what I see as a long term fair value, but if they rip 7% – 10% higher in a couple of weeks I sell. Still allocated to less than 10% stocks as they are relative too pricey for me on fundamentals.

I work for a division of company that is closely tied to the housing market. New construction and existing homes. I’ve been with this company now for over 11 years. Last year at this time the manufacturing floor was the busiest I have ever seen it. I just now walked across the manufacturing floor to get a package from Receiving. This is the slowest I have ever seen the manufacturing floor. My boss gave her notice last week.

I think this will turn out to be an inflection point…a point in time when everything changes….

As I have said before I watch a guy that builds tiny homes and offers lot rentals. House prices $20K – $100K. Lot rentals $200 – $300. Business is hot. Not many people are trying to provide housing for low income retirees.

He also offers total off grid if that is what you want. That is a hot business too.

totally cool innovation IMHO OS.

Please provide web link, and spell it out in case Wolf deletes it.

Thanks.

Incredible Tiny Homes out of TN.. Puts up a video nearly everyday. Basic to beautiful small homes.

OS: I’m seeing this as a example of a major underlying trend.

That “trend” is toward autarky (self-sufficiency), local production and consumption, reduction of overhead, elimination of recurring payments (rents). Getting off the high-earn/higher-spend rat-wheel.

Off-grid = get rid of payments to others. Water, energy, food made in-house. If you pay cash for a “tiny home”, then no mortgage.

That’s a big chunk of a household’s monthly non-discretionary expense eliminated. Water and power are automatic; food requires extra labor; it’s not free, but it may well be both “less” and “better”.

One meter (recurring payment to others) at a time, you staunch the blood-flow.

If you’re a young person, looking at the prices/long-term debt you face to become a “professional”, you might decide to become a generalist instead, and provide for yourself.

It’s now an option. “Autarky” may become a word known to many.

Technology has gotten a lot better about off grid as well.

Hi Wolf,

Some guy I read said, “Nothing goes to heck in a straight line” or words to that effect. I think that we’re seeing that across most markets globally.

A few random RE related thoughts from my perch in a NorCal resort town (where I live full-time):

1) Earlier today I received my monthly Redfin Estimate; from June to October the estimate is down 8+%. Both the June estimate and the current estimate are (IMHO) absurd, but probably directionally correct.

2) There are a huge number of empty/vacation as well as Vacation Rental houses in my area (all potential shadow inventory); of the 14 surrounding properties there are three with full-time residents, four empty/vacation (used maybe 2 weeks a year) and seven Vacation Rentals.

3) Real estate is a slow transaction process that most people engage in only a few times in a lifetime. So prices are absolutely in a downtrend overall and will continue that way for the foreseeable future. I have no idea how long the downtrend will continue, but a return to pre-pandemic prices (so about 30% down from peak) is a lock and prices will probably go lower, primarily due to interest rates.

4) The move in interest rates will lock buyers out of the market: the mortgage cost per 100K at 3% was $337/month; at 7.5 it’s $559. That’s $222 per month; on a typical $400k mortgage that’s an extra $888 a month or $10k + per year. For most buyers, the price is almost irrelevant; it’s the cost per month.

5) The fact that interest rates are below the inflation rate is a distraction; in the 1970’s and early 1980’s wages lagged but were not far below inflation. Chairman Powell wants to CRUSH labor and the idea that a person making $80k / yr facing 8% inflation will be making $100k three years from now is absurd. Sure, they’ll get some wage increase, but my guess is that it will be (at best) half of the published CPI. Borrowing money in an inflationary environment makes sense if your income increases at a rate equal to or greater than inflation. It’s possible that the experience of “inflating away debt” at the individual level was a one-time anomaly of 50 years ago.

6) Finally, a well priced home in good condition will sell (there are always buyers) but as most properties are both overpriced and in need of substantial repair, expect there to be a lot of properties sitting for extended periods. Expect lots of hoopla over the “bidding war” or the “on the market for 8 hours” exception.

Thanks for the awesome summary.

Ed: why do you say Chairman Powell wants to crush labor?

Hi Tom,

A great question. I think that Chairman Powell is stuck in a difficult position – I think that the fundamental cause of current US inflation is supply based (see Wolf’s ongoing discussion of automobiles as an example of supply chain based shortages driving price increases) and that increasing interest rates will not have ANY impact on supply chains. And Chairman Powell is smart enough to know that there’s nothing that he can do about supply chain issues (fundamentally, the Fed controls monetary policy to some degree, but has no direct influence on fiscal policy).

I do think that Chairman Powell is really concerned about inflation taking hold in wages and is willing to enable a deep recession to prevent what used to be called “wage-push” inflation. Higher rates cause a recession, increasing unemployment, and limited wage increases. I’m old enough to remember the late 1970’s and early 1980’s – labor was able to force wages to track inflation for many years (for example, union contracts with Cost of Living Adjustments). The back to back recessions (basically running 1980 to 1984) ended those.

Perhaps “CRUSH” was too strong but I think that using a recession to limit wage inflation is the new FED policy.

Hope this makes sense.

The Fed wants to reduce this “temporary” inflation by any means so this enormous mass of monetary value in stocks and real estate will have to drastically reduce, in the real estate portfolio it will have to reduce by at least 50% it could be quick or slower according to the economic situation but I believe that this is the goal of the Fed.

It should be noted that we would be on the high values of the immo bubble of 2008 but inflation has passed in the meantime.

General inflation is caused by government policy. It can not be accurately modeled. If it gets out of control it can destroy nearly everything. Fed has got to slay it.

Bernanke getting the economic prize now is like a team getting the trophy at half time. They should have waited til the plane safely landed from his experimental policies.

I RTGDFA and just have to ask Where’s Kunal? I am sure these charts don’t apply to his reality/market…

He’s busy at the bar with SoCalJim.

I’m delighted to report that he made a very Kunal contribution to this thread :)

Our prices are dropping and we can’t make it to the World Series, all in the same week. This sucks.

Wonder how all this is going to work out in Hawaii.

The state government has passed some really restrictive laws limiting the rental of condos that has reduced the legal supply by a huge amount.

These laws want to remove the ability of condo owners, except for a small number of units, to rent out for no less than 90 days.

Most people had been able to rent out for a period of 30 days or more and as a result a lawsuit had been filed as a result. The lawsuit is still pending.

Hawaii used to draw a huge number of people renting these condos for a period of around 30 days and now will either have to compete for the available properties or reduce their time in Hawaii and pay for hotels at higher prices.

And the market is already reflecting the loss of these rentals even before the lawsuit has been decided.

In August 2022 visitor numbers are at about 90% of the total compared to August 2019, but that number really hides a mixed result. There has been a huge increase in people coming from mainland USA and a huge drop in Japanese tourist numbers.

There were 28,384 visitors from Japan in August 2022 compared to 160,728 visitors (-82.3%) in August 2019. Visitors from Japan spent $53 million in August 2022 compared to $236.9 million (-77.6%) in August 2019. Daily spending by Japanese visitors in August 2022 ($227 per person) was flat compared to August 2019 ($228 per person, -0.7%).

There have been a large number of comments on various Japanese blogs about the change in Hawaii compared to prior the pandemic with many Japanese saying that they no longer feel safe in Waikiki and the atmosphere of the destination has changed for the worse.

In July Hawaii hotel occupancy was at 81.5% only 3.8% lower than before the pandemic in July 2019.

BUT, statewide hotel room rate in July 2022 was at $413.57 per night, representing 36.1 percent increase from July 2019.

The average room rates increased more than 50 percent on all neighbor island hotels while O’ahu hotels increased 17.9 percent. Reflecting the higher room rate, the state accommodation tax revenue increased 39.3 percent between the two periods.

Data is from the State of Hawaii Department of Business, Economic Development, and Tourism

Depends on which area of Hawaii. Big Island NW corner, likely unaffected. Areas with high density rental condos, like chunks of Maui, maybe a hard hit.

One thing’s for sure — Hawaii was relatively sane, price-wise, going into C/19. Most of Hawaii has been a historically slow moving market, and that all ended with Covid. Apparently a whole lot of people decided the islands are great for WFH/WFA, and in additional to that, people who are super rich and don’t need to work suddenly got an interest to to own there. The difference pre/post C/19 is shocking.

Well I know that the price of houses and condos took off there despite the lock downs and ridiculous rules put in place.

The cost of living there is ridiculous and the cost of holding a condo has gone through the roof.

Monthly maintenance fees are sky high and boggle the mind.

Taxes on short term rentals are out of this world.

Property tax on these type properties is $13.90 per thousand dollars. Then you have to pay GET, TAT, and OTAT.

GET is 4.5% on all rental income.

TAT is also paid in addition to GET if you rent for less than 180 days and that is 10.25%.

And if you are on Oahu starting backing in December 2021 you get hit with OTAT as well on rentals of less than 180 days. This one is 3%.

So all that adds up to 17.75% added to the rent!!!

PS: that amount has to charged on the cleaning fees too. I heard a while back some smart a%%%% were charging huge cleaning fees which were exempt from the tax and low rent to get around the tax.

So the government “fixed” the problem by applying the tax to the cleaning fees.

I’m wondering whether the Fed might announce they’re going to slow rate hikes, but simultaneously increase the speed of the balance sheet reduction.

Anyone else consider that possibility?

Prices at this time show June-July-August closed sales, with some of them with rates locked in at 4%-5% in April or May.

What will happen once those sales reflect 7% rates, prices going to decline big time

In my subdivision (affluent north Dallas suburbs), houses are now sitting for weeks and not selling even after multiple substantial price cuts.

The zestimates here are now down 15% from the peak in July. A mere 5% drop over the next year will put them back on the trend line they were on pre-pandemic. But average drop is now 5% a month and accelerating so it now seems likely that prices will dip below pre-pandemic levels early next year.

Case-Shiller with its 3 month lag seems to be just registering the very beginnings of this in the latest release.

Don’t want to nitpick but the Dallas figures don’t look quite right:

Month over month: -2.3%, after the -0.4% dip in July.

From the peak: -2.3%.

Shouldn’t that be:

From the peak: -2.7%?

Thanks. The “from peak -2.3%” is correct. The month over month was a slip-up. The correct mom: +1.9%

I haven’t read anywhere here that the RE market has more weaker hands than in the past. Forget the debt, interest rates, payments etc.

1. 25% of RE is held by institutions/investors, i.e. BlackRock.

2. 33% of RE is owned by someone or some group that holds multiple properties.

In other words, 30% or so of RE is not held by stronger hands who need RE for a roof over their head, but instead use it to generate cash flow or capital gain. What happens when the.return is not there or the renters can no longer pay the rent or the government puts on price controls? I would think weaker hands will be quick to exits

“25% of RE is held by institutions/investors, i.e. BlackRock.”

That sounds rather high. I believe 25% is recent purchases in last few yrs, not ALL purchases/owned.

1) You must mean “Blackstone” not “Blackrock”.

2) Funds/institutional hands are MUCH STRONGER than residential hands. First, most funds have LTV considerably lower than the usual 80-90% that home buyers typically go for. More like 60%, 70% toward the high end. Some funds are <50%. And they borrow at WAY better rates than you and I do, because they have deep banking relationships, more collateral, and super-sized borrowings that bankers love love love. Smart managers locked up ridiculously low rates awhile back for 10 years. And then the investors in those funds, they hate recognizing losses. Much more likely they ride out the downturns than Joe Sixpack with hardly any equity who can jingle mail and go rent down the street.

If you're thinking this amplifies downside, doubtful.

What is more interesting is the calculation these folks will make when comparing rental income vs the yield from the 2 or 10 year.

So far rental prices has been rising FAST but will alot of multi-family apartment currently in construction, supply might be coming online to crush those rental prices.

Sell high and put some money in the 2 year might be the smart play.

Keep your hands, arms, feet and legs inside the dive roller coaster at all times. Hang on tight.

There is no stopping it.

Australia A spate of construction companies have collapsed this year with more than a dozen failing caused by a perfect storm of supply chain disruptions, skilled labour shortages, skyrocketing costs of materials and logistics, and extreme weather events.

The central bank has stopped in the last meeting with the interest increase, now at 2.6%.

I find it hard to believe RE will correct by some of the figures mentioned in this blog post (30%-50%). If that’s the case, what little equity many millenials have begun to generate will be wiped out in short order. Hosed by student loans, then hosed again by a sham housing market. If we do indeed see a severe housing recession, I’d expect a collapse of household formation and birth rates in the coming years. RIP starbucks latte generation.

You must be extremely young. During the last housing bust, many markets dropped over 60%, and that bubble was nowhere near the size of this one. Furthermore, rates never hit where they’re going this time. 80% off seems likely in some places. Think Boise, Bend, Reno, Spokane, etc.

Correct again IMO DC!

Areas of FL likely to be in that class w the western cities you cite.

Last time saw many older places down 75% from 2006 highs, and tons of new construction just stop no matter at what point of the process SO similar to 1929 crash.

Folks with tons of hopium still, especially the youngsters with the double $200K income.

The very long term trend growth has to be limited by growth in household income. Can’t have house price grow 2X – 4X income forever. Correction comes when rates go up instead of down.

There is a theory going around that Powell got bad data from Fed phd system and blew inflation call and now he is using more real time data from outside the Fed.

I agree with you, though 80% seems like a lot to me even in the worst bubble markets. I also think if inflation is sustained that will mitigate some of the nominal price declines. If the Fed keeps raising though and actually brings inflation down close to its target with high rates and QT, maybe some places experience declines worse than Phoenix and Vegas did after HB1.

Didn’t realize that millennials were “hosed” by student loans. I thought that that’s what taxpayers were for. Taxpayers are a larger group that incorporates some millennials, to be sure. They are for hosing as overseas is for war, a matter of convenience to politicians. Reduce your consumption to the irreducible minimum and starve the tax farmers out. The demonstrated competence of government is major infrastructure and the guns to protect it. All else is lagniappe and we shouldn’t have to pay for it.

Wolf, could higher interest rates also have some effect on inflation in the positive? I understand their is a negative effect for private credit as companies and households either don’t take on new debt or use revenue to pay old debt which would have been costly to refinance. But doesn’t seem like .gov has got the message yet.

As the US gov bonds rate rise, the pay out on the increases as well. If the US gov uses deficit spending to pay off those debt payments, aren’t they just printing more money to pay off the debt? At some point, something needs to give, either government spend within their means or we just continue this cycle of ever increasing monetary supply.

I have seen arguments like this about the inflationary effect of increases in the interest rate channel. Much depends upon the “propensity to spend” of interest payment recipients (generally lower the richer they are) as well as the competing disinflationary effect that interest rates have on the demand side.

There are also inflationary forces on the supply side that don’t respond to interest rates terribly directly — for instance, what difference do they make to the price setters in OPEC+? And fossil fuel prices influence a lot of other prices. And then there is war — historically a reliable source of inflation not terribly susceptible to control via monetary policy in any way.

None of this is as simple as some would have you believe.

Jpjpjp,

I don’t think I fully understand what you’re trying to say. In general, inflation makes it easier for the government to service its debts because tax revenues increase with pay increases over time and GDP increases with or above the rate of inflation, and so the debt burden declines. The other side of that equation is that investors in those securities are getting crushed by the loss of purchasing power of those securities and don’t get compensated for it by high enough yields.

What you will see happening is that the government debt-to-GDP ratio will decline during this inflationary period.

The government doesn’t print money; the Fed would do that. But the Fed is now doing the opposite: QT.

If all the young people decide to live with their parents, going forward, because they can’t afford to buy or rent, then very bad news for the housing market.

The Fed created too much (stock market) wealth too rapidly, making people think they were playing monopoly in real life. Same for congress and the executive branch, who made some of the dumbest decisions in US history in a knee jerk reaction to a mild pandemic.

Hello Wolf and Helpers,

In the Treasury Direct, when I submit to buy the Bills of various maturity duration, do I just enter the amount I am committed to buy regardless of the final auction rate?

Is there a conditional buy offer with the minimal limit of interest rate, which my buy order would not fulfilled if the rate is not met?

I took a quick look yesterday, could not figure the proper process. Now today seems like the Treasury Direct site is not accessible.

Thank You

You submit your bid, and then you get whatever yield is established at the auction. After your purchase settles, you can check the security you purchased and see what yield it has.

You’re going to get some (minor) surprises because yields are very volatile these days.

I don’t know of any way of submitting a conditional bid.

The charts look like a classic blow-off top