“Not enough” v. “Too much”: If not enough, it “will require much higher interest rates and potentially a severe recession to control inflation. No one wants that.”

By Wolf Richter for WOLF STREET.

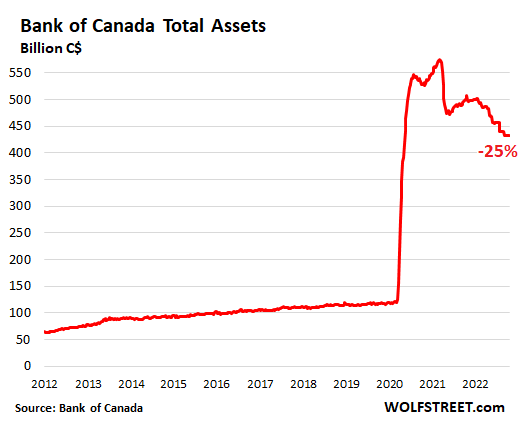

The Bank of Canada hiked the target for its overnight rate for the sixth time in a row, today by 50 basis points, to 3.75%, the highest since 2008, following the 75-basis-point hike in September and the 100-basis-point hike in July. Since it started the rate-hike cycle in March, the BOC has jacked up its rate by 350 basis points. Quantitative tightening, which already reduced the BOC’s balance sheet by 25%, will continue on autopilot.

And “the policy interest rate will need to rise further,” the BOC said in the statement.

“How much further will depend on how monetary policy is working to slow demand, how supply challenges are resolving and how inflation and inflation expectations are responding to this tightening cycle,” BOC governor Tiff Macklem said in his opening statement at the press conference.

While overall CPI inflation has declined from 8.1% earlier this year to 6.9%, largely due to the drop in gasoline prices, as the BOC pointed out in the statement, core inflation measures “are not yet showing meaningful evidence that underlying price pressures are easing.”

“Inflation in Canada is broad-based, reflecting large increases in both goods and services prices,” Macklem said at the press conference.

Given this inflation scenario, and “ongoing demand pressures in the economy,” the BOC “expects that future rate increases will be influenced by our assessments of how tighter monetary policy is working to slow demand, how supply challenges are resolving, and how inflation and inflation expectations are responding.”

“We are resolute in our commitment to restore price stability for Canadians and will continue to take action as required to achieve the 2% inflation target,” the BOC said.

Quantitative tightening continues.

“Quantitative tightening is complementing increases in the policy rate,” the BOC said. Since peak-balance-sheet in March 2021, the BOC’s total assets have dropped 25%:

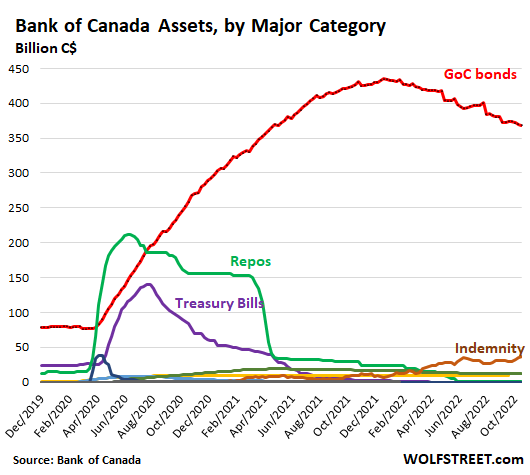

The BOC has shed its repos (green in the chart below) and short-term Canada Treasury bills (purple) starting in mid-2020. It never bought many of the other assets on its QE list to begin with. And it started shedding Government of Canada bonds in February 2022 (red line). What is rising on its balance sheet is the amount that the government has agreed to pay the BOC to cover any losses on its bond holdings under the indemnity agreement they entered into in March 2020 (“Indemnity” in this chart):

Macklem’s five reasons for the 50-basis-point rate hike:

1. “Inflation in Canada remains high and broad-based.” Though it has “come down in recent months, but we have yet to see a generalized decline in price pressures.”

2. “The economy is still in excess demand—it’s overheated. Households and businesses want to buy more goods and services than the economy can produce, and this is driving prices higher.”

3. “Higher interest rates are beginning to weigh on growth. This is increasingly evident in interest-rate-sensitive parts of the economy, like housing [in fact, home prices are plunging at the fastest pace on record] and spending on big-ticket items. But the effects of higher rates will take time to spread through the economy.”

4. “There are no easy outs to restoring price stability. We need the economy to slow down to rebalance demand and supply and relieve price pressures. We expect growth will stall in the next few quarters—in other words, growth will be close to zero. But once we get through this slowdown, growth will pick up, our economy will grow solidly, and the benefits of low and predictable inflation will be restored.”

5. “Finally, we are trying to balance the risks of under- and over-tightening.”

“Not enough” v. “Too much.”

“If we don’t do enough, Canadians will continue to endure the hardship of high inflation. And they will come to expect persistently high inflation, which will require much higher interest rates and potentially a severe recession to control inflation. Nobody wants that,” Macklem said.

“If we do too much, we could slow the economy more than needed. And we know that has harmful consequences for people’s ability to service their debts, for their jobs and for their businesses,” he said.

“This tightening phase will draw to a close. We are getting closer, but we are not there yet,” he said.

Higher rates have caused fireworks already.

“Higher policy interest rates are beginning to slow demand. Higher mortgage rates have contributed to a sharp slowing in housing activity from unsustainable levels, and consumer and business spending on goods is moderating. This has led to declines in house prices [well, the sharpest declines on record] and is exerting downward pressure on goods prices,” Macklem said.

“Moving forward, we expect the effects of higher interest rates to continue to work through the economy, moderating household spending and business investment,” and GDP growth will “stall through the end of this year and the first half of 2023 before picking up in the second half,” he said.

BOC “mindful” these rates whack households, but OK.

Canadian households rank among the most over-indebted in the world, largely due to housing loans. And housing prices are now plunging at the fastest rate on record. Since most mortgages in Canada are either variable-rate or fixed-rate for shorter terms, such as fixed rates for two years or five years, households see rate increases impacting their existing mortgage payments.

And the BOC said it is “mindful” of this – but is brushing off the home price plunges “from unsustainable levels” and remains “focused on our mandate” which requires the BOC to bring inflation down with “higher interest rates”:

“We are mindful that adjusting to higher interest rates is difficult for many Canadians. Many households have significant debt loads, and higher interest rates add to their burden. We don’t want this transition to be more difficult than it has to be. But we remain focused on our mandate. Higher interest rates in the short term will bring inflation down in the long term. And getting through this difficult phase will get us back to price stability with sustained growth.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

“Higher interest rates in the short term will bring inflation down in the long term.”

One hears increasing cries for a very short term.

See how much they like a little Weimar then.

Maybe some old fashioned stagflation too.

The 1% elite are not affected by inflation. Also they have figured out that the other 99% are too divided on “feelings” based issues and so can be easily suppressed by the 2 party system where both parties exclusively serve the 1% elite.

So, we can see the slow QT and negative real rates (4% interest – 8% inflation = -4%) that is unable to control inflation. They only wat to control hyperinflation as that will break the current system and hurt the 1%.

The fix: Start voting for Libertarians and Independents. This is the only way to make the other 2 parties realize that they are accountable to 99%.

I’m with you on voting for libertarians, and other free-market leaning politicians, but your comment is off-base:

1) Canada is not a two-party system.

2) It’s not true that the 1% are unaffected by inflation. The irony of the current situation is that the wealth gap between the rich and poor has shrunk dramatically over the last 10 months; entry level jobs are actually paying more than they were a year ago while investment accounts have lost substantial value – something like the average .1% richest families have lost $12m dollars this year.

“Not enough” v. “Too much”

Should that be “vs.” or does “v.” mean something else.

As in court cases.

“Brown v. Board of Education”

Citizens v. Govt has morphed into Govt v. Central Banking over the last few decades…

Our Fed Overlords rule the Universe at this moment…”Long Live the Fed”???

Per Bloomberg today:

Markets didn’t oust Truss, the Bank of England did — through poor financial regulation and highly subjective crisis management.

Why not continuing the 0.75 increase trend if “the policy interest rate will need to rise further,” ? To easy the tightening and encourage spending before Santa is gone for the year perhaps? I’ve heard that the shipment and sales data from Asia to Europa and North America so far are down dramatically compare to previous Christmas seasons.

“the shipment and sales data from Asia to Europa and North America so far are down dramatically..”

That’s the goal of the rate hikes, to lower demand, and those rate hikes are working already in lowering demand, as you said yourself. The hope is that lower demand will eventually reduce inflation — that’s a hope, not a certainty (see stagflation).

They don’t want to crash demand to zero and bring everything to a halt and turn off the lights. They just want to lower demand some, so that price pressures are easing.

No one today knows how this will work out due to the “long and variable” lags between monetary policy changes and inflation changes.

The BOC and the Fed will both pause when rates are somewhere between 4% and 5%, and see what happens. With the lag being usually 12-18 months, they might have to pause for a year or longer after they get to 4%-5%, to see how inflation reacts to their policies.

The real interesting question to me is whether these central banks will EVER be able to sell off all the bonds they purchased in the COVID response. If not, then is it economically sound policy to keep these bonds on the books at the central banks? Doesnt keeping these bonds at the central banks just give cover to politicians to continue to overspend?

Isnt this really the core of the economic question? Central banks, by purchasing government debt and taking off the market are distorting the normal market dynamics that tell government how much they can deficit spend, without financial markets reacting negatively.

I just think that our forward policy objective should be to sell off ALL or most of these assets and allow the markets to send proper signals to each government about whether the fiscal policies make sense.

Maybe politicians need to be held accountable for the real policies that have wrecked our country and caused the most massive wealth inequality in history.

– Lower tax rates for billionaires than middle class

– Easy money for real estate that jacks up the prices

– Shipping most manufacturing jobs off to China and others

– Allowing China to close markets to our high tech companies, while giving full access to our markets (mostly)

– Too much government spending for payments to individuals instead of spending on infrastructure

– Creeping inefficiencies in our inept federal agencies

Have you seen a single reform or law that actually addressed the core policies that have caused this massive wealth inequality in a compelling manner?

You mean reverse it? Why would those who have been fighting since the 50’s-60’s to get back to the Gilded Age ever allow that to happen? They are winning their now almost completely unilateral multi-faceted class warfare battle quite handily as it is.

And yet you still choose to babble about “inept government”, as if you would like to help them “clear out all the dead weight” and improve things in a “compelling way”

It is just about bathtub sized now, almost ready for the final drowning, as they say.

Sounds like you want a savior…again…and you might get one and maybe then you will wake up….but too late.

NBay,

The central, taxing, money printing G expends trillions every single yr – if that is your idea of a bathtub, you must be Mr. Creosote from Monty Python (“Wafer Thin”).

I do agree that the economic pathologies have infected every corner of the society at this point and they need drastic reform too – but the G has spent 80+ years making itself the central actor and culprit.

If not for 20 yrs of Fed ZIRP “fixes” we would have had at least 2 fewer asset implosions and 1+ inflationary explosions.

And we have not even reached the nightmare of unfunded entitlements yet.

In a democracy the “central” government SHOULD be the “central actor”. Or would you leave it to unregulated corporations, which do best under a fascist government, as they are fascist organizations themselves? Bigger than many Nation States.

Unfunded obligations are just the results of extreme wealth inequality…the lack of progressive taxation…future generations would prefer a simple bean counting problem to a trashed planet problem, I am certain.

You want to help them or not? If so, then downsize your own life, instead of whining about your “hard earned money”. Vote for a Comprehensive Green New Industry on a WW2 scale…Now! Of course “Central Actor” led! And get rid of crap like Citizens United and “Corporate Personhood” and let the same Existing laws that apply to the little guy apply to their members and shareholders. Or keep your happy little head buried in the sand and count all your beans.

And the FED is NOT the central government. Sheesh, haven’t you got that here yet? It’s more like a banking lobby than anything.

I don’t even know why I even bother to argue with government (and by default democracy) haters. I have a Biologist world view, and while we are a rather unique species, we sure aren’t anything “special” or even the present evolutionary winners….not even close. But we could use what got us this far (against some real big odds) a whole lot better.

If I don’t wake up tomorrow, fine. It will save me the trouble of doing it myself when my quality of life degenerates further. The stats say I go downhill pretty fast in the next 5-10 years, and I’ll be damned if I go out in a care home, home care, or a hospital.

“They don’t want to crash demand to zero and bring everything to a halt and turn off the lights. They just want to lower demand some, so that price pressures are easing.”

A measly 25 basis points wouldn’t do that, Wolf. Between 50 and 75 is hardly like raising 500 basis points to start taking a hatchet to the legs of speculators and cutting them off at the knees, like I’d want to see.

It’s clear these banks are talking a bunch of sh!t while doing as little as possible. Let’s be real – if they were more concerned about “doing too little” than they were about “doing too much,” they wouldn’t be choosing the smaller hikes. These guys are kicking and screaming while doing rate hikes at all. They’re pissed that their looting had to come to an end.

If they were so concerned about inflation and “doing too little,” they wouldn’t have ignored it for 18 months. The fact of the matter is that they want to go right back to low rates and speculative manias as soon as possible, they just won’t admit it. All of the distortions of the past 25 years were their wet dreams come true.

DC, you are spot-on. Indeed, they do want to go right back to low rates as soon as they can get away with it. They’re not even particularly shy about admitting it. Not long ago on 6/15/2022, Powell said, “We need to get back to a place where supply and demand are back together. And where inflation is down low again and mortgage rates are low again.”

I know that I’ve already posted that quote here a couple times, but only because it opens such a clear window into the mind of our top central banker. Central banks see rate hikes and QT as something they begrudgingly must perform as a means to an end. The end goal is to “get back” to the good ol’ days of low rates when they were making money out of thin air, back when more than one Fed governor was caught front-running their own policy decisions. Martha Stewart went to white-collar jail for an incomparably small infraction, yet a couple of poisonous Fed officials barely got a slap on the wrist and walked away cash-in-hand after committing perhaps the highest possible order of rotten insider trading. They have not suddenly transformed into white knights, ready to valiantly fight the good fight in the name of financially responsible citizens. These people are not to be trusted. The minute that it best suits their interests, rates will drop and QT will end.

“they do want to go right back to low rates as soon as they can get away with it”

They sure do, and large part of population wants this too, and wants it badly, but IMHO none of this matters anymore. Reality has asserted itself over the grand financial Matrix that we all had been living in during the last decade. Inflation, supply chain disruptions, wars (in plurals – current one in Ukraine, and coming ones in Taiwan etc.), energy crisis, geopolitical struggles between American empire and its challengers, social unrest in EU an US, all these factors will make it impossible to go back to “good old days”.

Look at the markets, look at home prices. The whole construct is already wobbling. I know you want the whole thing to just collapse in one fell swoop, but that’s not what most people want.

Agreed, they should have started hiking rates in early 2021. And they should have never cut rates this low in the first place, and they should have never ever done QE, but that’s where we are now.

Wolf, may I ask, if you haven’t covered it already on your site. Let say next spring the rate is up to 4.5% and the FED give the signal that they will pause the hike for a year or half. Would they also pause QT the same time? What do you expect to happen to the market overall?

If the economy slowly decays while the market bounce for several months before FED makes another move, I feel everyone would jump in and buy the “dip”. Thanks.

QT will run on autopilot independent of rates until they have run down their balance sheet enough. They want to get rid of all their MBS, no matter what. That’s the plan.

They may eventually cut rates, if inflation has come down enough, while still maintaining QT. QT will be with us for several years until the balance sheet is run down enough.

What if the only thing driving the Canuck economy was real estate, and the increase in rates destroys housing? Then MAYBE the government might be forced to look at how inefficient the country is and how it serves government and NOT the common people.

Housing prices and wealth effect by newly minted millionaire house owners, and a firm belief that the pension system is rock solid, not at all invested in stock market casino. After all, it’s run by the government.

As long as everybody is saying what they want to hear, all will be great.

Paraphrasing an old New Yorker cartoon, we’ll just dance and sing ’til we’re not hungry anymore!

Natural Resource industries make up nearly double the RE market is in Canada; agriculture is also big. When energy prices are high; the good times roll.

The interest rate hike nudged the Loonie a little higher; so there’s that.

I share Nouriel Roubini’s opinion as shared on Bloomberg Surveillance this morning. On this blogging site he’s probably and abrasively referred to as a “tightening denier”

Are the tightening deniers still out there, after all this tightening? By now, no one looks more ridiculous than the tightening deniers that started fanning out in October 2021 — including here in the comments — and that said that none of the tightening that has actually happened in those 12 months could ever happen because yada-yada-yada. I’m still laughing about this stuff I read here.

The FED created the tightening deniers and pivot people. It’s the “unintended consequences” portion of their mind-blowing recklessness as they ignored their stable prices mandate and started doing the exact opposite. The FED has lost all credibility, and short of some sort of overhaul of the entire regime they will never gain it back.

They’ve got a real problem on their hands in that nobody believes they are actually dead serious about inflation, which is why you see all the BTFD people hanging out, buying every f***ing dip. And this goes back almost 10 years. When you engage in QE infinity for over 10 years when it was supposed to only be a one year emergency, you reap the whirlwind. There’s no “soft landing” this baby. The wings came off at 35,000 feet and the airliner is pointed straight down.

No QT denying for myself, so let’s be uber clear. There’s no shortage of homes. Rather, there’s an absolute total shortage of affordable homes. Prices nationally have to drop at least 20% for there to be some semblance of affordability. 30% over the next two years would be better.

The Fed needs to drink it’s own price stability Kool-Aid going forward, and they MUST get out of the business of suppressing long-term rates with QE They have no business buying anything beyond 7-year notes, EVER! Otherwise, we’ll see the same crazy home price escalation again & again.

And most importantly, the government needs to get out of the business of rent & mortgage relief. Those programs had just as much to do with soaring rent & home prices as anything.

Canadians are slowly acquiring some much needed cynicism regarding government (and health authorities), not to mention the holy cow of that Liberal mouthpiece, the CBC.

Don’t see any of that cynicism in Ontario, they’re simply brainwashed progressives who can’t understand the ottawa elites are manipulating them. The province has been destroyed.

Could someone answer this:

Why do central banks raise rates by 0.75% (for example) for three consecutive months? Why not do a 2.25% rate hike? That is, what is the purpose of spreading the hikes out over three months, why not just all at once?

Because of the central banking mantra that you can only CUT by full percentage, but only HIKE by a quarter, and even that by trembling hands.

That and not to spook the casino too much.

/sarc what else

You forgot “unscheduled emergency meetings are only for rate cuts, not rate hikes. Rate hikes can only take place during scheduled meetings, because crushing inflation is not an emergency, but falling stock prices are.”

Exactly. July, august and then October, they could have easily done an emergency rate hike during these months, while inflation is inflicting massive pain on average people. But we all know that the fed’s job is to not surprise the market. They are corrupt to the core.

It is called BS for the population. They could do 2.25% at ounce and let it settle for 4.5 months. Just like taxes taken off your paycheck, a little at a time they think you will notice less the full impact of paying through your nose.

Markets need time to adjust. There is already a huge amount of turmoil in the markets. Markets can deal with just about anything, but they need time to adjust gradually: lower prices, but not all at once in one day. If it’s all at once, the whole system can come to a halt. People are being silly about this. Some commenters here just want central banks to jack up rates to where in the ensuing chaos, no one can borrow anymore, and the whole economy shuts down and the lights go out. That’s easy for anonymous commenters to wish for, but it’s hard to live through, and would be complete nonsense.

I know you mean well Wolf but central banks really help the bankers, real estate industry too much for too long. My son, my daughter in law tried to buy a house in the GTA, southern Ontario and in 2020, there were 0.99% variable mortgage specials everywhere. Yes, this is not a typo, less than 1% a year mortgage rate.

They had a decent $200,000 down payment and the rest was supposed to be a $550,000 mortgage. This is almost 27% down so they were taking more risk with their own money than all others trying to buy the house. You know what happened because these ridiculous low, less than 1% mortgage rates, there were so many bidders that they wanted $900,000 not $750,000 for that house. A 20% increase in a few minutes.

They could not buy the house so those that were borrowing to the moon and irresponsible that do not save their money and do not risk the most with their money got the house. Believe me, these lowest mortgage rates do much more damage than years of normal interest rates were have almost now. If those that bought the house can not afford 5%+ mortgage rates in Canada now with higher mortgage payments of $20,000 annually or more a year I do not have much sympathy because they knew that 1% mortgage rates were impossible to be there for years, decades. They played with the house’s money and now have to pay up with dire consequences.

This is not like it never happened before, remember with Greenspan and adjustable rate mortgages, lower to lower mortgage rates and the millions that got foreclosed on in the US, 2008 financial, housing meltdown. There was plenty of warning for this happening before from 2008 and after so it is happening again, people should know this stuff by now.

That’s why people like me are not in charge of things, Wolf, because I’d do something very, very mean, nasty and financially painful to the speculators and pigmen among us. I figure since they decided it was such a good idea to really shaft the working class and the poor to benefit themselves, I’d like to shaft them even worse. Two eyes for an eye sort of thing. :)

But really, I’m in favor of ripping the whole bandaid off quickly. I figure as soon as the entire thing can collapse, we can get to building something more sustainable and equitable. The system we have right now, which they’re desperately trying to save, needs to be scrapped altogether. It’s all based upon high asset prices. We need to value labor once again, not all this “passive income” bullsh!t where fat cats don’t lift a finger and buy bigger and bigger yachts while impoverishing the masses.

I’m just sad and angry that it ever came to this – interest rates never should have gone this low, nor QE for so long.

We too have had a good downpayment for a decade, but were unwilling to carry a $500k mortgage back then, let alone the current $1.2M mortgage on the same house.

Of course if we had realized that the Canadian government would see dropping house prices as an existential threat and support them to the ends of the earth to never drop much, well we could have jumped in with both feet like all other speculators.

But instead we plan to buy and pay off a house, so no way would we pay 10-12x annual earnings for a basic house in the Vancouver suburbs. That’s simply ludicrous.

But now, with house prices finally coming down a bit, we’re 55 and our kids are already teens. And, I can only assume that the second that inflation in Canada appears to have rolled over, the BoC will halt QT and start lowering interest rates again to reinflate the “critically important ” housing market.

So, sadly I’m now making plans to leave Canada as soon as the kids graduate, and take them with me. Some other, smarter, more reasonable country can have their skills and youth, and the rest of my working years.

There are huge consequences of easy money policies, something the idiots who run Canada are just starting to get hints of, but will paper over for longer yet.

Depth Charge for FED chairman please asap

A huge hike would duplicate March 2020, when, due to the pandemic, markets just did a huge panicked rug-pull on all assets.

Another analogy I think would be “shock and awe” in out Gulf War 2, which just shattered everything in that society and left it all utterly broken. Years of dysfunction followed, to this very day.

Or look at Liz Truss’s shock and awe moves, which brought panic, unstable core markets in the UK, and ridicule at best. Rarely do you get things fixed by huge blunt force. They don’t just fall into a neat hoped-for pattern.

You have everything bass-ackwards. They broke shit with the rate cuts and the money-printing. They broke the entire economy through artificially hyperinflating asset prices and the cost of living. A crushing rug pull on all asset prices is a healing of sorts.

They have control of the money, and can do whatever they want.

Buy Gold and Silver and opt out of their game

There is nothing per se bad about incrementalism…it allows the Fed to gradually test the violence of mkt reactions before proceeding.

The problem is that the Fed has spent 20 years cultivating the risk of horrific inflation by destroying interest rates – all so that a pathologically dysfunctional DC would not have to deal with America’s fundamental economic decline and its causes (most basically, that China has been thoroughly kicking our ass in productive efficiency).

Not joking.

The 0.5% rate hike vs the 0.75% “expected” rate hike was touted as a central bank “pivot” and one of the reason for a sharp swing of stocks to the upside…and the FED will see this a good reason to also “pivot.”

With stocks down sharply now, it didn’t take markets long to figure out that this pivot BS being spread by pivot morons was just pivot BS and that the BOC did what it needed to do, which has been the plan, which is to bring interest rates to 4%-5% and then pause.

Hoping someone can explain why pivot BS exists. Is it wishful thinking? An attempt to sway attitudes/perceptions? There seems to be so much psychology to all of this…

This is largely driven by hedge fund managers and bond fund managers to drive markets their way. It was the same with the tightening deniers. Many of these people have a huge following in the social media and they get on CNBC and Bloomberg TV to spread their stuff in order to move markets their way. CNBC and Bloomberg love to have these people on their show because they draw an audience. And then it gets picked up from there by ZH and the blogosphere, and Mish, and all the others, and it gets spread from, a lot of times by unwitting people who don’t know that they’re being played by hedge fund managers and bond fund managers.

Along Wolf’s lines, there are also a lot of excessively leveraged longs in the market (that’s how they made any money over 20 years of ZIRP) now looking to dump their deteriorating positions on any bag holders they can CNBC bamboozle into believing that the Fed is going back to pouring crack in the punchbowl.

The fact that the Fed *has been pouring crack into the punchbowl for 20 years* doesn’t help.

It is hard to express just how hiddenly awful the underlying economy has really been for a long time and how horrible things might get now that the Fed (finally) has to take the drugs away to keep from killing the patient (who may have actually died years ago).

One thing that puzzles me is the assertion that stocks are down sharply. SPX today is where it was in Feb 2021. Sure, a substantial drop from the max (Dec 2021), but the run up from Feb 21 to Dec 21 was crazy.

Does the assertion imply that there isn’t much downside from here? I mean, why not have SPX go back to where it was in 2018 or 2015? I’m not an expert, just a humble reader of this blog and a couple of others, but I find it curious when I see financial experts describing this “correction” from pure madness as a sharp downturn or even as a bear market. BTW, I think the same applies to the housing market.

Perhaps you’d like to comment on this, here or in a future article. I’d love to hear your opinion.

Thank you for all effort you put into this.

S&P 500: -0.74% today, -20.5% from high

Nasdaq: -2.0% today, – 32% from high.

Qualifies as “substantial” in my book.

During the dotcom bust, the Nasdaq plunged 78%. That’s my model, given the many parallels we have.

Wolf,

Which crowds do you think is more delusional, the tightening deniers or the Pivot pushers? Raising the interest rate does affect assets prices but how is the consumer prices doing? I do see that used car prices are down 10% YOY but still high based on 2019 prices. Is it possible that assets prices (stocks, bonds, real estate) crashed but consumer prices (rent, food, energy, healthcare, etc.) stay stubbornly high for the next few years???

Thanks,

qt

“Which crowds do you think is more delusional, the tightening deniers or the Pivot pushers?”

From what I can tell, it’s the same crowd. First they were tightening deniers, and when that started looking ridiculous, they became pivot mongers.

Speaking of stocks down, has META earned its date-with-destiny on your imploded stocks list?

Yes…

https://wolfstreet.com/2022/10/26/meta-makes-huge-mess-afterhours-enters-my-imploded-stocks-after-tech-social-media-stocks-already-made-mess-during-the-day/

Now, that is what I call a sharp downturn… Wolf, thank you for your earlier answer.

This “pause” thingy…..sounds an awful lot like “doing too little instead of too much” if you ask me. With CPI over 8%, why would any central bank pause with their funds rate at roughly HALF of CPI?

I am guessing that central banks are of the opinion that below-inflation interest rate will be sufficient to slow down spending, due to abnormally high debt levels. If one pays 40% of income for the mortgage, and rise of mortgage rate from 2.5% to 6% will increase this share from 40% to 70%, then any further increases in interest rates may actually be counter-productive (will bankrupt the mortgage holder). Or something like this…

The BOC is under a lot of political pressure to not raise rates as the housing market is falling due to mortgage rates. Canada is economically overly dependent on construction and the housing sector so if a decline turns into a crash, we are going to have a very nasty recession up here.

Wait a minute… It raised by 50 basis points. Until the last couple of mega rate hikes, 50 basis point hikes were the steepest in 22 years.

I understand that most of Canadians have adjustable mortgages. If the central banks raise interest rates further, what will happen when the rates reset?

The you know what will hit the fan, obviously

Canada can just move their citizens from real housing into the Metaverse as I hear “Horizon World” in the MetaVerse is much warmer and cheaper than real life in Canada. Better move fast a there are 200,000 folks there at the moment hiding from reality inside the infinite Meta…Jeremy Powel likely one of them…HA

Oh wait breaking news AF, Meta down 20% today (15% AHs), which makes 70% from peak so maybe don’t move to the Meta yet as the Meta looks slated to hit Wisdom Seekers 80% CARNAGE list soon…

We seem to be following China ,huge correction in tech,now housing down 50% . Bye ,Bye middle class all planned why do you think we have G-7 ,G20 meetings it’s all PLANNED . FOOLs

Didn’t you know? Everyone wants to buy US Treasuries! /sarc

Hope springs eternal! Central bankers are hoping that inflation pressures will fall away and they will have a nice soft landing.

I think the central bankers are now more afraid of inflation than anything and will continue on their course as long as it takes, but they are hoping to see some changes after their current actions.

Housing is a major piece of the inflation puzzle. Let home prices fall far enough and we will have major financial problems that will help to bring down demand.

We’re in a huge deflating environment,the world produces to much to fast wait a year it will be worse .Food scarcity is a major obstacle for world peace

The media is making it sound like now is the best time to invest in Toronto real estate.

Article says that Bank of Canada intends to keep its rate at 4% for at least a year. If this is indeed what is coming, the impact on Toronto housing market should be be a major one. Hopefully this will give you the opportunity to buy in at more reasonable price level.

I’m betting Canada’s long-term interest rate cycle bottomed about the same time as the US, in 2020.

This means rates are destined to “blow out” later.

Of course it is Just ask Jimmy Cramer He knows best lol Remember him pushing Bear Stearns just before their collapse ? I sure do

Why are they acting like households getting put in a tight financial spot is an unfortunate side effect of raising rates? It’s the goal.

The way they are planning to stop inflation is to make people broke enough through QT and higher rates that there is serious friction to raising prices…because people can’t afford to purchase at the higher price.

They have to say this because they need to show they’re aware of these issues and that they feel their pain.

Many households are feeling a much greater pain from inflation. And that’s the main problem.

They don’t mind creating the bubble but they don’t want to be blamed for a crash. They are trying to orchestrate a “soft landing”. I still get the feeling they really screwed up.

I think the higher savings rates and next years SS raise has covered my inflation bite so far, but I’m retired. Higher rates will only be better.

The Cola increase in SS in no way covers actual inflation That is fiction pure and simple

No thought of what we can do to increase supply? Kill demand is the only way?

Central banks and governments overstimulated demand with their ridiculous free-money policies. Now inflation is in services, and in many services there is no shortage of supply, and yet prices in services are spiking — nothing to do with China or gasoline or whatever. It’s that the inflationary mindset has kicked in, and people and businesses are just paying whatever. And it’s that inflationary mindset that needs to be crushed so the consumers and businesses REFUSE to pay higher prices because they cannot pay them. And then inflation might wither.

Let’s not neglect to mention the disincentives to work created by all the stimulus, Ppp, tax credits, etc. Tight labor market drives inflation and smaller labor force produces less, which drives inflation….

Originally called supply chain issues in the vernacular

Yes, Rico, I am retired too so now here in Canada I am finally getting some financial payback for saving all these years. I was just getting max 2.3% to 2.5% in the fixed bank deposits. The higher interest rates of 4.85% to as high as 5.20% means we will be $200,000 more ahead after taxes over the next 7 years.

How can the Fed be forecasting 3% GDP increase tomorrow? Seems to be no indication of that anywhere…

The Fed doesn’t forecast 3% GDP. Neither for this year nor for any future years.

In its latest projection, the Fed forecasts 0.2% GDP growth by end of 2022; 1.2% GDP growth by end of 2023, 1.7% in 2024, and 1.8% in 2025.

That 2% inflation goal by the CB’s may prove to be a wet dream. They might want to yell victory at 4% inflation and a 5.5% Funds Rate. External realities beyond their governments control that they themselves have engineered may prove to be the proverbial rock they lifted only to drop it on their feet.

I second your suggestion that 4% inflation will be the “new normal” for observable future.

How is that “stable prices?” It’s not.

What I meant to say is that Federal Reserve will discover that costs of bringing inflation down to their current 2% target is too painful in many way, and will opt to abandon their price stability mandate (“temporarily”) by elevating inflation target range from 2% to 4%.

Combined with a major bear market, it’s high enough to put most retirees in the poor house, especially when so many are retiring young when their savings needs to last several decades.

Regretfully that seems to be our future – the poor house. All signs point to this IMHO.

And the terrible thing is, this is actually an optimistic look at our future (pessimistic involves nukes, dictatorship, better not think about this..)

If CBs declares 4% inflation as normal rather than 2%, then their credibility would take a big hit.

So far, they have been screaming that 2% is their goal.

Then the 10-year yield would be 7% and mortgages 8.5%. Fine with me. But people forget that. With inflation come higher interest rates.

Right said.

Thank you

As wolf said, rates would be higher too.

But there is also another reason why they have been targeting 2% and not 4%. Since inflation is self-enforcing, it is more difficult to anchor 4% than it is to anchor 2%.

Better yet would be 0% inflation, but among central banks there is an (unfounded) fear for DEflation, which is why they try to anchor expectations at a low, but above zero rate.

I agree. 3 to 5% inflation was the norm following the end of the Volcker/Reagan inflation battle for about a decade. You really didn’t see inflation drop down to 2% until we started offshoring manufacturing to China in a big way in the mid to late 90s. But that is coming to a screeching halt right now.

The BOC managed its balance sheet comparatively well prior to the pandemic. It set the bar quite high for money printing. This will really matter in the future when we compare asset price declines relative to QE levels by country.

Importantly, Repos were decisively pulled at the end of the winter 2021 and during the commencement of the vaccine rollout. Total assets also dropped at the right time.

The only retrospective error that I can identify is BOC not reducing its holdings of GoC bonds sooner. Ironically, the protections afforded by the Indemnity provisions might have been the cause of delay.

That said, I can’t quantify the scale of the fiscal ramifications of the government covering BOC’s losses. It is inferred that the guarantees remain promissory and pending, rather than realized cash assets on the balance sheet. Superficially, this looks like an extra form of tightening on top of QT and rate hikes.

The worry over inflation and housing prices declining is overstated and amplified by the news & media. The story is not so clear cut. If you look at the underling factors in Canada such as:

1) Not sufficient existing inventory.

2) Not sufficient new homes. Not enough new homes are built to satisfy the population growth. Even if we overbuild homes for a few years we still would not catch up.

3) Mortgage rates will not remain high forever. Once they start going down there is a lot of demand waiting to enter the market.

4) Even now with all the doom’s day scenarios many experts predict, the real estate prices in metropolitan cities like Toronto have not declined much. In Toronto neighbourhoods prices are holding . In fact certain segments such as townhouses have increased in price, while condos have also done well.

Most of the price drops are in suburbs and areas where the covid crisis made people bid up prices. In those areas I agree we’ll see 20-30% drops.

Yes, the plunge in prices and the collapse in sales volume is just our imagination: In the Greater Toronto Area, home prices plunged 3.0% in September from August. Over the four months, the index has plunged by 11.1%:

Are you land lord holding homes in Toronto neighborhood or a realtor ?

Just asking.

People are usually blinded by their own tinted glasses.

A realtor or landlord is the last person to admin there is a home price crash coming.

I am curious as to how the Canadians are viewing this politically. In America the Biden Administration is getting eaten alive over inflation. I am not sure if that is fair but it is what it is. I don’t follow Canadian politics enough to know if the same is true for Justin Trudeau.