Blame whatever. Just don’t blame money-printing and interest-rate repression.

By Wolf Richter for WOLF STREET.

“To front-load the path to higher interest rates,” the Bank of Canada today jacked up its main rate by a 100 basis points to 2.5%, the fourth rate hike in a row, and the biggest rate hike since 1998, which made the BoC the first of the G-7 central banks to raise by 100 basis points in this cycle.

“An increase of this magnitude at one meeting is very unusual,” said BoC Governor Tiff Macklem in the opening statement. “It reflects very unusual economic circumstances: inflation is nearly 8% – a level not seen in nearly 40 years.”

CPI inflation in May had spiked by 7.7% from a year ago, and the June CPI hasn’t come out yet, but we know from the 9.1% June fiasco in the US, where services inflation is now spiking, that in Canada, June CPI readings are going to be ugly too.

And now there’s talk that the Fed too will raise by 100 basis points at its meeting at the end of July to grapple with this ugly metastasizing inflation in the US by “front-loading” the rate hikes.

Atlanta Fed President Raphael Bostic – who caused a rally in the stock market a while back when he said that a “pause” might “make sense” in September – was asked today if the ugly June CPI print would cause the FOMC to consider a 100-basis-point hike at the July meeting. And he said, “everything is in play.”

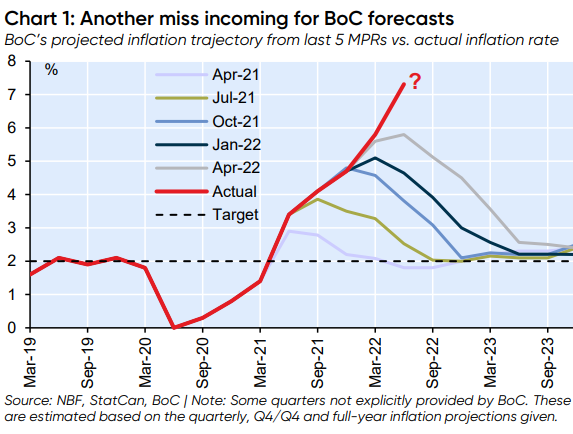

BoC ‘s inflation expectations not worth the paper they’re written on.

“Inflation in Canada is higher and more persistent than the Bank expected in its April Monetary Policy Report (MPR), and will likely remain around 8% in the next few months,” the BoC said in the statement.

That “expected” inflation in the April Monetary Policy Report is the light blue line in the chart below. It was only two months before the actual May CPI data was released, and the BoC was totally off. And the prior projections were hilarious, a form of central-bank humor. The exasperated economists at the National Bank of Canada produced the chart:

The Bank of Canada – like the Fed, like the ECB, like all of them – blamed the laundry list of global factors for this raging inflation. But it didn’t even mention the reckless money-printing binge, years of interest rate repression, and government stimulus.

Just don’t blame money-printing and interest-rate repression.

No way, that this reckless money-printing binge, interest-rate repression, and government stimulus might have had anything to do with this raging inflation, no way Jose. But the lockdown in Shanghai and the grain exports from the Ukraine did.

Then, in a bit of veiled navel-gazing, the BoC added that “domestic price pressures from excess demand are becoming more prominent.” Still not admitting anything, but at least looking in the right direction.

“More consumers and businesses are expecting inflation to be higher for longer, raising the risk that elevated inflation becomes entrenched in price- and wage-setting. If that occurs, the economic cost of restoring price stability will be higher,” it said.

Which already occurred months ago. And the cost of restoring price stability will be higher.

Macklem then addressed Canadians directly.

“I want to explain to Canadians why we’ve made this decision,” he said in the opening statement.

Canadians have mortgages that are variable or that are fixed for only a set number of years, such as five years. Those rate hikes are going to be reflected when current mortgages reset, and Canadians are on the hook already, and they’re staring at that monster rate-hike, and the Canadian housing market has already U-turned.

So Macklem tried to explain this rate hike:

First, inflation is too high, and more people are getting more worried that high inflation is here to stay. We cannot let that happen. Restoring price stability—low, stable and predictable inflation—is paramount.

Second, the Canadian economy is overheated. There are shortages of workers and of many goods and services. Demand needs to slow so supply can catch up and price pressures ease.

And third, our goal is to get inflation back to its 2% target with a soft landing for the economy. To accomplish that, we are increasing our policy interest rate quickly to prevent high inflation from becoming entrenched. If it does, it will be more painful for the economy—and for Canadians—to get inflation back down.

Things are not normal right now. After 30 years of low, stable inflation, many Canadians are experiencing the pain of high inflation—and the uncertainty that comes with it—for the first time.

When inflation is this high, it erodes the purchasing power of every Canadian.

The soft landing…

Getting inflation back to 3% by the end of 2023 and back to 2% by the end of 2024, that’s “the soft landing we are projecting,” he said.

“Interest rate increases can cool demand and inflation without choking off growth or causing a surge in unemployment. Some sectors will be more affected by interest rate increases than others, but the very tight labor market means there is room to reduce the number of job vacancies without having a big impact on overall employment,” he said.

“But the path to this soft landing has narrowed because elevated inflation is proving more persistent. And this requires stronger action now so consumers and businesses can be confident that inflation will return to its 2% target,” he said.

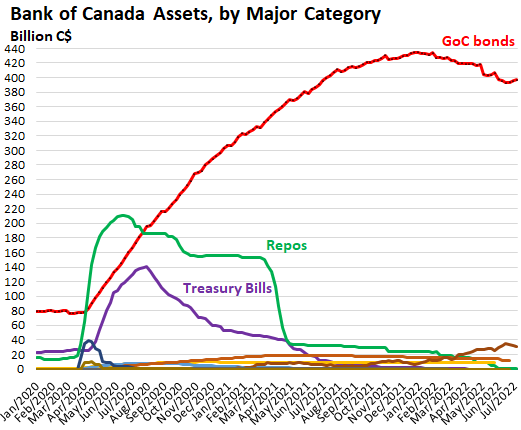

Quantitative tightening purrs along on autopilot.

QT was kicked off in April and will continue on autopilot. Maturing Government of Canada bonds will roll off the balance sheet without replacement. Its holdings of GoC bonds have already declined by over 8%. Repos and Canada Treasury Bills have been reduced to essentially zero. And its overall holdings have declined by 21% since the peak in March 2021:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The landing is never soft from more than 10 feet.

If the central banks really want to restore a normal economy they should be hiking by 1700 basis points, not 100.

Don’t give them any ideas :-]

No danger in giving them any ideas. They never take ideas from outside the clan.

The central banks could «print» a lot of money in a short time, can they not «burn» that money equally fast or faster? Skip interest rate hikes, just remove a lot of money outright.

They could dump all their ill acquired securities on the market at any time. That will probably also kill the markets for a while. Not a bad outcome.

Amen, even with 100 basis points, Papa Powell will still be wayyyyy behind the curve..

If he is truly seriously about bringing down demand and inflation asap, the fact that Wallstreet can telegraph and assume your next move means you already failed miserably. If he can find his big boys panties, next hike do at least 200 to 300 basis points, I can almost guaranteed you he’ll get at least some disinflation which let him have some wiggle room to proclaim inflation is peaking..

We seem to live in the age of narrative. Maybe this is just the way it is in a western democracy. There were a lot of narrative stocks, with no fundamentals to sustain them in a recession.

Central banking has relied more and more on narratives, but anyone looking closely can see the central bank’s forecasting narratives have been horribly wrong.

With a leveraged up system, the central banks have to keep control of the narrative. They have to say “whatever it takes” or “it’s going to be a soft landing” because to be less than optimistic is going to immediately cause individual “market participants” to become risk off all at once.

Rhetoric is more important than action and policy.

It’s unfortunate. Action was needed in ’21 but now it’s too little too late.

Yes. However, big boy pants are hard to come by in that group. As Wolf noted, the blame buck NEVER stops there. Outside factors upon which the board has no control are always cited.

Kind of a funny game to observe – they blame anything and everything except what is really to blame. So I don’t see anything above a 100bps increase at the next meeting.

Would a larger increase be the right thing to do under the circumstances? Yes. Does the current board have the intestinal fortitude to do it? Doubtful. Very doubtful.

The mantra of the CBs is incrementalism at least when hiking rates.

Arithmetic progression seems like the most orderly way to reach the target rate and Fed seems to be following that so far. First 3 meetings with hikes:

25bp

50bp

75bp

Next one is now 100bp in two weeks.

Three more this year so 125bp, 150bp, 175bp

Nice round total of 7% by year end and 9% to begin 2023.

Hitting for the cycle!

What about just greatly accelerating QT?

I wonder about this also. There are obviously buyers out there for the debt as evidenced by the current yield curve. Why not sell to them?

You mean have the Fed sell bonds and stop buying bonds? LOL!

Cytotoxic,

Yes, you’re onto something.

IF the Fed WERE serious about quashing inflation, they would simply let all maturing securities roll off each month without replacement. If that proves ineffective, then simply start selling outright.

Of course they’re NOT serious about inflation which is why we’re here in the first place.

Inflation is now ingrained. The PPI report today (+11.3%) tells us that CPI is nowhere near peaking yet.

Yet delusional Wall St pundits still publishing nonsense about rate cuts in 2023. Not sure if they think they’re being funny or not.

Double digit CPI not far off.

HR01,

The Fed is *getting* serious. They are cranking and J-Pow is not interested in being another Arthur Burns. The Fed is just finding out what it means to be serious, and I think that has a lot of people at that juncture just before you have to throw out long-held comforting but false notions about how things work. The pundits you mention are in for a hell of a learning experience. Vibe checks inbound.

Normally one would expect an increase in unemployment as interest is raised. The higher the raise, the more unemployment. According to the Canadian Central bank the ‘tight’ labor market will prevent some of what one would expect to be a ‘normal’ reaction to interest rate hikes. I’m a tad skeptical, to say the least. But if so, that’s a ‘first’ for me.

I really dont understand why everyone focuses on rate hikes on the short end of the spectrum, why dont the central banks actually start dumping long term bonds to the market and force the prices much higher?

Look at that chart. They have barely sold any of the bonds back to the market. Just dump the stuff on the market day after day and allow interest rates to soar and just keep dumping. That will kill inflation and return things to a bit of normalcy.

All this talk about tightening is a joke. They still have a ton of bonds sitting on their balance sheets.

After todays US CPI report anything less than 100bp would be fully expected and align with previous Mission statements. Can’t hurt your billionaire friends too badly.

Phx has 4x over the avg. listed houses on market right now. There will be some deals 2H around here. Patience pays off once again.

Unless those billionaires have sold their economic stake through this miracle called Total Return Swaps.

Musk already sold 8.5 billion dollars of stock. Unlike last time when he almost went bankrupt, he is going to be fine this time around.

What in the hell is a “Total Return Swap”?

Soros was right.

“They will invent this shit (my word) faster than (was speaking to a Congressional dog and pony show because he got rich on shorting the GFC) you can understand or make laws regulating it.”

Back in ’06-10 when I was trying to learn finance, mostly from CNBC and Wikipedia, it was Bloomberg, I think, that had CDS rate tables for sovereign bonds, but never could find corp bonds (too many kinds?).

Everything informative is behind a paywall now, which is why I glance thru Yahoo and Yahoo Finance, and then come here. In fact, Yahoo used a WS article which is how I got here….way before mug days.

Don’t forget the impacts we are seeing now are in some important ways directly related to the huge income inequality now present in western, debt centric economies. Legislatures need to restore progressive tax rates and to close the corrupt tax codes that have been wedged into the system. All this has done is create ‘bubble’ prices in assets that predictably go ‘pop.’

The public needs to prosecute the Fed for fraud.

Wake me up once the housing market has crashed for real. I have my eye on the Singapore real estate market, because that thing is still hot. The Singaporean Central Bank did an out of cycle hike yesterday, but rates are still low IMO.

I think my RE agents is telling me this is just a gully and sellers are motivated. Price will remain high forever in SoCal..

It’s also possible that this is the same agent that was in The Big Short

An increase to 8% unemployment will be required. The mindset here is best described as totally disconnected from reality.

9% is average lol at charts

What do you think is going to cause 8% unemployment? It was 3.6% last month.

Well, there certainly are some things that will remain high forever in SoCal. Just keep drinking that kool aid.

Are you ready to compete with those fleeing Hong Kong for assets in Singapore?

Singapore is not making it easy for those Hong Kong escapees. Also many more foreigners left Singapore because they were laid off.

What’s unexpected is that most of the demand for housing came from the locals. They are in for a rude shock though if the Singapore Central Bank were to get aggressive. I am currently short the Singapore dollars because I think the Government can not afford to hurt the local population in the end.

Anyone else thinks gold will get to around $1300?

I hope it does so I can buy as much as possible! It’s in a bit of a funk right now because interest rates are rising and gold pays no yield. In the long run though I like metals as a hedge/insurance policy.

Food commodities are probably a way better bet ,

Especially if they are stored in your basement and attic, and wherever.

:)

Nah, either .22 bricks or become a Mormon. They insist on 2 years supply and are known for taking care of each other….watch your daughters, though, as a loved one or an asset, your choice.

Yes and probably lower than that.

No, but it will probably go up by the fall. It often does, and it is due.

My bet is 1500. I am ready to buy a ton of coins at that price.

What do you spend your coins on?

What I love is the mantra the preceding years have been those of “low, stable inflation” It’s so great, that trick of repeating something again and again. It’s like white noise and seeps into the subconscious like the fog in Cuckoo’s Nest.

Of course the simple fact is, and this was before the covid monetary eruption, the dollar is worth a tenth of when I was a kid.

Then there’s the popular lie it’s mainly asset prices that have increased the last 20, 30 years. Although when you think about it…..a candy bar is an asset, and so is a car, and a sheet of plywood, so maybe they have a point on that one.

“…a sheet of plywood…”

I’m doing a bit of remodeling on the house and I was at Home Depot to buy some OSB (similar to plywood). The guy in front of me was loading up 10 sheets, I only needed four. I helped him, he helped me. I asked him what he was doing with the OSB and he said “nothing, just storing it up.” He said it was less than half the peak price and he knew he’d need it in the future and was afraid that it would go ballistic again in price in the meantime.

Not in a deflationary environment,food storage a better bet

I actually think that the computer industry has proven that a deflationary environment forces companies to innovate and optimize their efficiency. It proves more value to customers and forces companies to compete or die.

One of the most important changes we need to make is to stop companies from merging together, thereby eliminating competition. The more companies, the better economy. Only rarely should companies be allowed to merge.

We have the ability to provide a decent lifestyle for everyone who works in our country, but we simply dont do it, because it would reduce the profits to the billionaires.

That is classic inflation-driven behaviour; precisely the kind of “inflation expectations” that keep central bankers up at night.

Go to kit or interviews watch Alfonso Peccatiello ,one of best interviews in my life

Kitco

I love your comment about the value of the U.S. dollar compared to when you were a kid. I placed a 1 ounce Canadian Gold Maple Leaf coin at the bottom my 29 year-old daughter’s stocking last Christmas. She and her husband were totally clueless as to what it was worth. She looked at the $50 nominal value printed on the coin and said “Thank you, how generous of you”. I gently suggested that she not spend it for $50 if she visits Canada. The next day, my son-in-law texted me “Holy crap, that coin is worth almost $2,000!” I told him that when I was in college, that same coin was only worth about $100.

Jokester Mark Dice did a street interview event in which he offered the passing public a choice between a large bar of silver or a chocolate bar, for free. Everyone who accepted the gift took the chocolate bar.

Also to love is how inflation numbers are such a surprise to the Bank of Canada (and any other central bank), after about a 100% federal ‘budget’ deficit in fiscal 2020/21. Federal debt has risen from $600B to $1.4T in a few years.

A one-percent rise should be considered a panic response at this stage of the game, with the blame naturally attributed to consumers buying too much (‘demand forces’). Of course they’re just buying the same or less at inflated prices.

Here’s what I don’t understand and worries me a little: as they do small interest rate increases month after month, won’t inflation naturally reset after 1 year because then it won’t be comparing the “normal” times but will be comparing the red hot inflation of this year. Put another way, people can’t afford the services now but in a year, the prices could still be up 10% compared to 2021 but only 2% compared to 2022 and they will say it is back to normal. Yet we will still be stuck paying the much higher prices. We should be comparing prices to some target (2% year over year starting in 2020) instead of just year over year.

Over Time you shall Learn that nothing go’s in a straight line like I did right here . So all you really need to master is a general synopsis “correctly”

and then you will end up at that Place >You shall then have Future Vision

but what are you going to do with it is the question ?

Good point.

I am thinking the economists at the Fed believe prices may at least hold steady (due to major drop in energy prices) while income rises.

I have noticed apartments now offering a free month of rent if a lease is signed for at least 13 months. They are keeping the same lease price, but offer incentives like free month of rent.

I’m seeing stuff like this where I’m at, as well.

Because a renters collapse /exodus is commencing. Unwillingly but unavoidably.

The one time incentive is a scam to keep the advertised rents high, otherwise the market value of the property goes down, the property is underwater, the lender will have to act, and eventually might end with the ‘owner’ going bankrupt. Like most other business in this country, it’s a financial engineering scam.

Josh

“, won’t inflation naturally reset after 1 year because then it won’t be comparing the “normal” times but will be comparing the red hot inflation of this year.”

Exactly.

The YOY readings will probably come down…but the spiked prices will be baked in. The Fed never talks of roll backs in these prices, only small increments stacked upon these elevated prices. That bothers me. I fear it is a revelation of their acceptance, even promotion of inflation.

It will be heralded as a great victory, but the citizen consumer will not be left in a good place.

The Fed has no business promoting ANY inflation…even 2%

If that happens, the Fed will have totally failed to achieve their explicitly stated objective of average 2% inflation over the business cycle. The Fed should be targeting a few years of deflation now to achieve their published goals.

The fediots recently used time averaging to justify their decision to allow inflation to exceed 2% by stating that it used to be so low that the average was still OK. Remember that? I wish we could insist that the same treatment is required going forward. If we required the time average to be 2%, we would have to have rates well below 2% for quite some time, and this would erase much of the damage that is currently happening. Pipe dream.

If they don’t offset the 10% inflation in the future, does this mean the Fed was not revealing its true intentions all along?

If they say they want 2% inflation over time, they have to run inflation below 2% for a long time to offset it. If they don’t, then the stated policy was never in line with their true intentions.

That would be a very non-transparent way to run policy. No wonder there is no trust in government or society anymore.

Legislators stand by and watch, like purchased lawn statues, or old horses staring blankly in the field.

What about retired people,we have nowhere to run .Fixed income everything rising in price ,as usual destroy the elderly ,that built this country.This will not end well

Well, we could help them out, but they would never except welfare.

Flea, no one cares about what the elderly did yesterday or during their lifetime of building the nation or whatever.

You should focus on learning to live on less. That may be a title for a new book, Learn to Live on Less…the three LLL’s.

Very appropriate for today’s times.

Boomers still have their houses, time to sell!!

When the shite hits the fan (large spiking volatility of volatility), everything goes down lower than it was several years ago, that is my bet.

Hyperinflation is a better bet on food energy,

Yes. It’s important to understand that the Fed’s official policy goal is average 2% annual inflation over the business cycle i.e. from the end of one recession to the end of the next, inflation should average 2% per year.

Two years have passed since the end of the last recession and inflation totaled 15% over that time so assuming the next recession ends about 2 years from now, the Fed is now targeting -7% inflation over the next 2 years to achieve their target i.e. the current Fed goal is 3.5% deflation for this year and next.

They are currently 12.6% over target so extremely aggressive tightening is needed – say 7% FFR and $250bn a month of QT.

Dazed and Confused.

I assume that was tongue in cheek.

Powell still says the Fed’s goal is 2%. So, these prices with 2% more next year is defined as a Fed victory. That is ridiculous.

I agree, if the Fed has a target rate (debatable), going forward the goal should be NEGATIVE….but nothing from Powell on that…..hopefully some questions in that regard.

2 years also coninsides with China 2025 plan

Saw this after writing my reply above. Yes, we can dream.

No Inflation never ever has and never ever will stop inflation, never anywhere ever. It just accelerates when uncontrolled as people loose faith in the value of money and demand ever increasing amounts of money in return for anything and you guessed it that is inflation!

The cure for high prices is high prices.

Maybe not. The cure for high prices will be higher wages, and the cure for higher wages will be higher prices, and so on.

There is evidence we are in a wage price spiral.

Apparently not

and the EU and RCB rate is still stuck at minus forever…not sure how they get away with that……

Oh and the UK economy grew 0.5% in May, much to the annoyance of all the people who were selling the idea that the UK for some reason is in the worst position than anywhere in Europe.. It is bad(too much money printing through the China virus) but they have obviously never been to Southern Europe.

The ECB rate will be positive after the September meeting and will shoot higher from there.

US Inflation is 9.1% and fed rate is 1.75%,actual rate =1.75%-9.1%=-7.35%. Does that mean big institutions still make a killing until actual rate is positive?

EU is way worse in the same calculation.

Doesn’t seem like it. Look at the big bank earnings which just came out. And look how the bank stocks performed over the past few months. JPM is down 35% from the peak last October.

I think banks’ shares dropping are due to reserve, which is due to projected over-leveraged business failure.

Is it true that the negative real interest caused debt extension (rotation) and borrowing more debt in the last 2 decades? If, that’s a big if, businesses can continue borrowing new debt (maybe prime+2%?) cheaper than inflation, what are the factors to prevent them from making money from this spread? Lack of means to preserve the value?

I always heard there is large money on the sideline due to larger printing press in last 2 decades. Do you think this will buffer any downside risk? Thanks

“much to the annoyance of all the people who were selling the idea that the UK for some reason is in the worst position than anywhere in Europe”

That’s mostly Brits themselves in our experience, they’re growing more and more furious about the crushing inflation rippling through Britain and there’s a down-pour of negativity throughout the country based on our recent conversations with our teams out there. And for now at least, the inflation on the GBP is worse than most other places in Europe, in fact the UK’s inflation is close to ours in the USA, one of the few countries to rival the ridiculous collapse in buying power of the US dollar. (Much of the economic growth the UK is registering is from the effects of ongoing stimulus, one of the main contributors to the inflation to begin with.) Ironically though, based on what one clever econ-background specialist in our team brought up last week, Britain may actually be better placed to disinflate than a lot of other countries due to Brexit. Not because of goods and services imports (which are getting more expensive), but simply because millions and millions (and soon the overwhelming majority) of EU citizens who came to England, Scotland and Wales while the UK was within the EU are being forced to leave, or leaving on their own.

The essence of the hard Brexit path that Britain chose to go down was a complete separation from the Continent, but just to put an exclamation point on it, the UK has basically been going out of its way to make things incredibly miserable for the dwindling number of EU citizens still living in Britain, and make it ridiculous hard, expensive and frustrating for them to stay there. An absolute nightmare of red tape based on what our associates there are telling us, and massive bureaucratic cold shoulder and even outright hostility everywhere they turn. And then with the COVID pandemic issues on top, millions more EU citizens are headed out the door, in fact even more and more younger Britons themselves are leaving too (especially the Europhiles and a lot of “Remain” voters who want to ex. attend European universities). This is leading to a drop in the population of England especially and easing pressure on housing, food and other resources. This may wind up doing more than anything to ease Britain’s inflation levels.

It is truly interesting to see how having some clueless person from a meaningless, failed institution like a “central bank” or some “whistleblower” utter some unintelligible nonsense that can mean just about anything and the opposite moves markets these days. All that with interest rates across the board having completely decoupled from some central planner’s wet dream and things blowing up all around them.

But people need some stooge to project their hopes in. And the illusion that “someone is in control”. Must be that guy behind the curtain.

Plus ca change, plus c’est la mème chose. On connait le chanson.

It just takes a while for markets to read my articles, which are too long for algos and only work when read by a human. Now these humans finally read my articles and markets are tanking…

A “Fed official” just came out and said something was on or off a table, time or ventilating device.

Markets are surging.

The chances of a “soft landing” for the Canadian economy approximate to zero.

Interesting to see from Germany how this will develop as the ECB has probably no chance at all for a similar hike given the local financial needs of our Southern neighbors. Will become quite shake in the FX-markets.

And FYI – Singapore also just moved its rates upwards this morning.

What’s kind of scary is that the Bank of Canada has been ahead of the curve compared to the Fed and they’re still dealing with out of control inflation. Assuming our economies are similar (a big if), that means that, even when the Fed reduces their assets by 8% (which it won’t hit for another >6 months or so), it still will not have cooled inflation.

Plus, Canada having largely adjustable rate mortgages means the interest rates will be transmitted into the economy (and asset markets) much more rapidly than in the US where lots of people will simply hold on to their 15 and 30-year fixed rates.

In both ways, Canada’s tightening started earlier and is currently significantly further along than the U.S. If they still haven’t gotten inflation under control, that probably means that, under the current Fed plans, we won’t see inflation under control for perhaps another year or longer!

Inflation won’t come under control in US or Canada until the housing bubbles have deflated significantly – say 25% or more.

The CBs can hurry this along by raising rates much faster and doing much faster QT.

Agree. And the housing bubbles won’t fully correct until the renters collapse from layoffs.

Russia and China don’t have inflation ,how can this be

Flea,

“How can this be?”

This can be because maybe you’re uninformed?

Inflation in Russia is a RED HOT 15.9%.

Inflation in China is a milder 2.5%.

I love your fact checking of these type of comments!

“Inflation in China is a milder 2.5%”

Right.

And you believe what the Chinese say?

They have a major economic problem there: their property development industry (construction), a huge contributor to the economy in all kinds of ways, has been in a slow-motion collapse. And they have all kinds of other issues in China, and excess demand is NOT their problem. Demand for all kinds of things plunged. That tends to push down inflation.

I agree that the BoC has been far more aggressive towards inflation and QT than the Fed has been. The problem is that they sit next to an economic Colossus called America… and even have a Free Trade agreement with said Colossus. It is hard for Bank of Canada’s QT to work when the Americans are still pouring gas on the fire.

And you are absolutely right about the rest of it as well. QT in America won’t really begin to take hold until this fall. Which means that inflation will be with us well into the next year or two in the U.S.

I am not sure any of us really understand how most people and most companies are dependent on cheap credit for their well being. How many homes and cars are going to be built with a 4% increase in loan rates? How many governments can handle a 4% increase in debt servicing cost.

Central banks are so far behind the curve. My base case is a severe recession with a lot of casualties like 2009 as consumers, businesses and governments are all addicted to cheap debt.

My understanding of the 1970’s are that houses were built and cars manufactured despite high interest rates. I may be wrong though.

Those years also didn’t have the magnitudes of debt that we have now that will be defaulting shortly.

How does that effect a house being built?

Inflation is emotive and understandably so. It’s real and debilitating. Consequently, high inflation draws a crowd and the crowd anticipates higher interest rates linked to mortgages and credit cards. The debt servicing charges; now another form of inflation.

Observers should rather look to the outstanding stock of debt relative to the stock of real assets and the effect of QT.

Fictionally speaking, crypto investors would dream of paying higher interest rates and prices generally if they could only have the liquidity back. As holders of an artificial asset, they were predictably the first domino.

QE stopped working. It reached its limits. In any event, it was never anything other than a Buy Now Pay Later deferral scheme. QT means Pay Now Buy Later. It really is that simple.

“An increase of this magnitude at one meeting is very unusual,”

Not as unusual as counterfeiting your currency for 30 years straight.

“No longer relevant, Powell, 68, told Republican U.S. Senator John Kennedy, 69, about the once-important measures of cash and easily spent assets that was a central focus for the Fed in the past

“When you and I studied economics a million years ago M2 and monetary aggregates seemed to have a relationship to economic growth,” Powell said, referring to one main measure of the money in public hands. “Right now … M2 … does not really have important implications. It is something we have to unlearn I guess.”

Powell said that in February 2021…..right before the inflation kicked in.

Powell also said that “We Now Understand How Little We Understand About Inflation”

So as they think they should “unlearn” the importance of M2, they admit they dont understand inflation. Perhaps they should check all their assumptions.

This seems like a “earn while you learn (or unlearn) Federal Reserve”.

I, too, remember his “unlearn” comment. He’s certainly unlearned a lot. We need to unlearn that. We’re gonna let it run hot. It’s just transitory. Amazing.

I think Hussman said it right in his latest market report. The Fed’s monetary policies have been child-like in derivation.

Not so. Counterfeiting your currency for 30 years is actually normal.

Irrresponsible, yes. Destructive, yes. But normal.

Greed is normal. But that doesn’t mean it should be pursued. Too much money almost inevitably distorts one’s thinking and behavior in ways that are deeply negative, avaricious and wasteful. There is a great deal to be said about the traditional values of restraint, discipline, humility, charity, frugality, thrift, and a lot of other words that make the addicts of pleonexia stick their fingers in their ears and say ‘Nah nah nah nah! I can’t HEAR you!’

“Of the fate of Ungoliant, no tale tells. Yet some have said that she ended long ago, when in her uttermost famine she devoured herself at last.”

40 years….Reagan started deficit spending….but I’m sure it was a typo.

“Ungoliant”?

Similar to that bird who climbs to extreme heights, then uses gravity to descend in ever tightening spirals till it flies up it’s own ass and disappears? Forgot it’s name.

‘gold pays no yield”

Versus the “yield” of the fiat dollar , at minus 18% …….

Not many people would want to hold gold and silver if governments and central banks didn’t have a long history of screwing over their citizens with paper. Gold and silver certainly aren’t perfect assets, but history says you are not a fool if you keep some squirreled away.

Bing Bing Bing… we have a winner!

Gold is transportable.

Gold spends well in most societies.

Gold holds value.

I am no “gold bug” but even I can recognize those facts. For people looking for an alternative to their own nation’s currency (or a hedge against what their Central Banks might do to it in the future) holding smallish positions in Gold is not a bad strategy.

Large Gold miners NEM and AEM pay good yields

Jim roger said he would buy gold at 1100$ ,he’s smarter than me ,which would be about a 50% haircut

In 2021 the budget deficit was $2,772B or 12.1% of GDP. Why is anyone surprised that inflation is 9.1%?

One way to lower inflation is to stop the spending or raise taxes. That is not the way to win elections.

Danlxyz: Raising taxes is a fiscal tool of Congress, among many other fiscal tools. Congress is paid to be AWOL by their billionaire donors. Manipulating interest rates (The one pony Fed tool) is a lousy tool. Too blunt and very imprecise. It creates ‘boom and bust’ cycles that benefit the billionaires, who can make money going down as well as going up. It’s a ‘fixed’ system.

And a pretty slick one, too. You have to admire how all the bases are well covered, whether you have been BSd into liking it or not.

Unilateral Class Warfare, perfected? Time will tell.

When the Fed’s done, I think we’ll be looking at 10%+ interest rates.

Yes – rate hiking cycles don’t end until FFR exceeds inflation.

Maybe 5-7% by year end.

The one thing that might keep FFR in single digits is the possibility of accelerating QT – maybe 7% FFR + $250bn per month of QT will be enough to tame the inflation monster.

They had 2% inflation with ZIRP. Some of the inflation is due to the war, labor shortages, COVID shutdowns in China, zero carbon mandates etc. I do not see interest rate hikes as curing structural defects. Perhaps rate hikes will reduce hoarding of empty homes.

JPM is down on higher loan reserves.

In order to close Nov 6/9 2020 open gap JPM have to drop < 103.

Currently at 7AM : 107.50.

Higher reserves, no buyback, reducing risk is good.

WTIC approached dma200. In order to close Feb 25/28 gap oil

have to drop to 90-91. it might osc on dma200 for a while, before

testing June highs.

Hey, there you are.

What’s with this S&P bouncing along down +/- 1000 points from the top? People just making decisions based on nice round numbers?

GMC offering 0 percent interest on some new vehicles last night June 13 on TV commercial. Claims to have new inventory of vehicles arriving every week.

The rural town dealers have no inventory when I drive by them. Ageism and lack of employment on the 55+ workforce is also a drag on economy and may have a negative impact on inflation.

But not healthy for economy as they become unproductive and not a contributor to GDP.

I have noticed a few local auto dealers seem to be getting a little added to their inventories.

I get your point that in general as you get older you become a drag on the economy but in my industry the average age is probably in the early 70s. These guys have grown up working very hard even from a young age. Working a 18 or 20 hr day doesn’t scare them. Case in point Im going commercial halibut fishing with my father. Just the two of us. He is 71. We will be putting in 100 to 120 hrs a week. Usually we have an extra person or two but we cant find anyone even though we pay far more than minium wage. I usually try and get college kids for 3 or 4 years. Usually pay 20k to 25k for the summer. All expenses are paid for as well. Maybe about 60 to 90 days of work and then they are done. Anyways no young guys want to come out. Anyways lots of old guys still contributing to the economy and lots that dont cost the taxpayer really anything as they are pretty self sufficient and surprisingly healthy. My grandfather didnt take anything from Canada’s social welfare system but he gave back much. Made it to 91 and worked till he was 77. Most these guys are working because they want to not because they have to. Its a way of life.

Growing real GDP means accelerating the Earth’s plunder and harder exploitation of labor (which are the only sources of profits). Both will have to come down as well as population to reach an equilibrium to the level of the 1800s. Regression by one means or another.

The king of not supported by science lockdowns which spawned the CARES money spewing, amongst other ills, still sits on his throne.

Wolf wrote:

“Canadians have mortgages that are variable or that are fixed for only a set number of years, such as five years. Those rate hikes are going to be reflected when current mortgages reset, and Canadians are on the hook already, and they’re staring at that monster rate-hike, and the Canadian housing market has already U-turned.”

This should make it easier for the Bank of Canada to quickly deflate their housing bubble and get shelter inflation back under control. This also applies to Australia, New Zealand and UK. More aggressive action will be needed by the Fed to deflate the US housing bubble including much more aggressive QT.

The housing bubble has just moved to places like Quebec, Montreal and Halifax even with rising mortgage rates. 100,000 people left the workforce in the last jobs report. Residential rents are so high people have stopped coming to Canada. There’s huge upward pressure on wages especially low paying jobs. People are leaving Canada in droves due to the sky high cost of living.

And what is sort or of funny or ironic is central America illegal immigrants head to California for the high cost of housing while I read San Diego or SoCal residents are moving to Mexico for lower costs housing.

Why did they let it get out of control in the first place if they want it under control? Makes zero sense.

They are raising rates because the Fed are raising. They have to or CAD slides, further exacerbating inflation.

BoC would let housing double again if they didn’t have a joke of a currency that is bobbing about on the waves of USD.

Well politicians never let a good crisis go to waste. I wonder if it’s them creating the problem so they can ‘create’ the solution to show the masses ‘see we fixed it! Vote for us in November! ‘ and like most sheep they will blindly do so.

Does this mean that the War on Savers will finally end? Asking for a friend.

My guess is that the “war on savers” will grind on until the dollar is finally wiped out and a new monetary paradigm is in place.

History is a guide and the picture is not pretty.

B

Continue raising rates and pop the worldwide everything bubble or return to the War on Savers. Which do you think they’ll chose? It’s obvious to me.

No. Financial repression in real terms is worse now than it was before. The war on savers is now killing more savers than it did before. Subtract the inflation rate from your savings account interest rate and compare that to what it was before inflation took off.

No. At 9% CPI inflation, your bank would have to offer you 10% on your savings account. Not happening. “High-yield” savings today pay about 1% to 1.5%. Inflation is a war on all assets.

“Restoring price stability—low, stable and predictable inflation”

Talking out of both sides of his mouth.

Central Bankers need to look at a dictionary

Stable: Fixed, unchanging, constant

The mandate is NOT stable inflation….it is stable PRICES.

Inflation is theft, and thus those who promote it are thieves. (even 2%)

Yep

Totally, YEP!

In June BoC made this comment, with speculation of a 50 basis point increase after the last two increases early 2021. Now, wonder how dire this is going to be for those 5 year resets, with a 100 bp increase just announced. Who can afford a 45% increases in ONE major budget item with everything else already up 25% to 30%?

“OTTAWA, June 9 (Reuters) – Some Canadians who took out mortgages in 2020-21 could see their monthly payments jump by as much as 45% in 2025-26, given rising rates, according to a Bank of Canada scenario released on Thursday.”

US Wholesale inflation 11%. When that percolates to the retail market, in coming weeks and months, inflation will continue to crush what little is left of the middle class.

They say wages are up in the 5% range, but not for those steadily working. They don’t get a monthly raise, and the annual raises are not that great. So, in the real world the earners are massively losing out.

Wait till the 2022 food crop fall harvest comes in with its massive input costs. 2022 may turn out looking like mild inflation by comparison.

“US Wholesale inflation 11%.”

Just trying to understand; but is Canada importing some inflation from the US as the US is its biggest export customer — 75%+ of all exports?

What’s happened is people have stopped coming to Canada because jobs here don’t cover the cost of rent. People are leaving the workforce in droves so now there’s no workers to fill jobs. There’s huge upward pressure on the minimum wage.

Housing has gone up 50% in 5 years in Canada.

Imagine working and trying to save for that.

Now wages are up and the BoC are looking to cut workers off at the legs.

Housing in two thirds of Canada has doubled in price in the last 6 years. Wages in Canada have only gone up 14 percent in the last 7 years since 2015.

Sure, either way Canada is going down very hard *if* the Fed hold rates high enough for long enough.

At some point BoC won’t follow the Fed and CAD will slide, once it gets too hot.

Hoo boy. What a mess.

We in the Household of the Unamused organize our finances in such a way as to Hope for the Best, but to Prepare for the Worst, using the boom times to prepare for the debacle. To us it doesn’t matter whether CBs get their act together or not. Humanity is already seriously blowing it in a other ways unrelated to finance and that isn’t going to change.

We have no illusions about human nature and its deeply negative tendencies towards tribalism, short-term thinking, and wishful thinking. There are lots of lists:

– We view minorities and the vulnerable as less than human.

– We experience Schadenfreude by the age of four.

– We believe in karma, that the downtrodden of the world deserve their fate.

– We are blinkered and dogmatic.

– A lot of people would rather electrocute themselves than think. No, really.

– We are vain and overconfident.

– We are moral hypocrites.

– We are all potential trolls.

– We favour ineffective leaders with psychopathic traits.

– We are attracted ‘that way’ to people with dark personality traits.

People don’t like to be reminded, but to control these tendencies and redirect them constructively one must first admit to them.

E.O. Wilson said, “The real problem of humanity is the following: we have paleolithic emotions, medieval institutions, and god-like technology.”

Neil deGrasse Tyson has noted that humans possess one characteristic it shares with no other animal, the neurotic need to feel ‘special’. That ‘need’ has been systematically exploited by ambitious politicians and marketing guys to the detriment of billions for a hundred years, for profit and for power, and it’s getting worse.

The evidence supports my prediction that the CBs will not be getting inflation under control, or prevent recession, or prevent the collapse of civilization or reverse the Anthropocene Extinction. If they could have done these things they already would have, but instead they have operated to help cause them. See above.

It may be helpful to remember that CBs do not work for you or for the general population. They operate for the benefit of the Financial Industrial Complex. Whatever they do for the great mass of people who are not wealthy financiers isn’t entirely incidental. It’s to keep them from coming after the rich with pitchforks and torches, for as long as possible, and that is also to their benefit.

I love your moniker “The Household of the Unamused”! Your comments are spot on. Regarding monetary debasement, never in the history of human civilization has a fiat currency regime survived. Inevitably, the currency is debased by excessive money printing in a desperate attempt to fill all of the vacant promises by politicians. As you stated, honesty is in very short supply these days, along with logical thinking. The two go hand-in-hand.

Even with all of the Fed’s backing and undivided attention, the Financial Industrial Complex seems to be hurting. Banks are down 40% or so since Nov 21.

There are some additional surprises percolating. Surprise. more than 50% of the Sri Lankan debt is owned by Western financial institutions. As always, there is leverage involved. Will be interesting to see how they are getting bailed out. And you know, Sri Lanka is not a one off situation.

Because I mostly agree with unamused, I have given up on abiogenesis studies (I’ll settle for the RNA world and let it go at that, e.g., “doped water” happened somehow) and decided to pursue just pursue multi cell evolution…in the interest of time, obviously…which has led me inexorably to Glycomics, as yet unexplained states of water, and of course, giving the electron it’s proper place in all our “theories”.

If only the Greeks had become totally fascinated by how amber rubbed with fur picks up things….instead of points and lines and over reliance on words…..they had already written off that blood thirsty ME diety as BS, and listened to an oracle who just babbled about all kinds of deitys, and left one to figure out what they wanted it to mean, anyway. And they celebrated their bodies.

I’m lucky I have lived close to the bottom all my life, at least for a European land stealer/enslaver/indigenous killer, anyway.

Make that, the electron, whatever it is.

The greek word for amber is elektron.

The credibility of all media is at all time lows.

The credibility of government is at all time lows

To think that the predictions and statements of the Federal Reserve are any different is an act of self deception.

The inflation genie is out of the bottle. To assume that rates in 2% zone will have any significant effect in reducing inflation is unrealistic .

The astounding part is that people keep buying.

They will keep buying so long as their RE values are high. Over 60% of families own their homes, and the Fed gifted these families price appreciation that ranged from $200k to $2M over the past five years.

That perceived wealth will be spent, as long as it exists.

The credibility of advertising is at all time highs…..it goes with education being at all time lows.

I learn more from ads than I do content, and that includes nearly all talking heads and their sponsored content.

“No way, that this reckless money-printing binge, interest-rate repression, and government stimulus might have had anything to do with this raging inflation, no way Jose. But the lockdown in Shanghai and the grain exports from the Ukraine did.”

Actually they all contribute to inflation to varying degrees. It may be helpful to come up with a list of causes and assign values to them according to their relative contribution.

Then make a list of policies and actions that will get inflation under control.

Then try to get them enacted.

Repeat the process for your Top Ten List of Things That Are Going Wrong and you are likely to come to the same conclusion that I did, and that you need to figure out how to get safely out of ranger, keeping in mind that Mars and a time machine really aren’t viable options. And that sooner would be better than later.

What percent of mortgages have an adjustable rate? What happens when people can’t afford the higher mortgage payments? More demand for rentals? More price pressure on home sales?

Scott,

In Canada:

About 37% of all new mortgages in April were “variable” rate. They became very popular this year when interest rates started rising.

This variable rate fluctuates with the “prime rate” that lenders usually adjust based on the Bank of Canada’s overnight rate.

Then there are the so-called “fixed” rate mortgage, where the rate is fixed for only set number of nears, typically two to five years. After the term, the rate is adjusted to the new rate in effect at the time.

The US-style government guaranteed 30-year fixed rate that doesn’t change at all over those 30 years is not a standard mortgage in Canada. I’m not sure if you can even get one.

You cannot get a 30year fixed rate in Canada. I believe the max I’ve seen is 10 years.

No, I think it depends upon who your lender is. There is no term limit for private mortgages. It is the regulated banks that limit the term of a closed mortgage to no more than 5 years. (Such banks can offer, say a 10-year term, but regulations allows the customer to opt to convert from closed to open after 5 years.)

So many took out a variable rate mortgage because that was the only way they could obtain a mortgage at the then lower rate.

Bingo.

And when amortized at the 30yr max, there’s no room left to maneuver to keep payments low as variable rates start to eclipse fixed rates.

Nearly ZERO in the US in 2022.

Adjustable rate applications in the US are currently around 10% of total mortgage applications, according to the Mortgage Bankers Association.

Point of information:

I’ve lost track. Specifically who pays Central Bank interest, and for what?

It makes sense that the Central Bank rate would underpin the consumer rates that I see — I’d like to puzzle out how.

Short-term government securities pay roughly that interest. Some CDs do. The yields of some other investments are closely tracking the central bank rate. The repo market trades with yields in the central-bank range. And that’s a huge market. If you can borrow in the repo market, you’re paying central bank interest.

I expect the rising dollar will totally crush the global economy. Commodities have much further to fall, as China will continue to falter (China is world’s biggest commodity consumer). China’s economy is a wreck and their only solution is to print more money. Expect defaults in debts all over the world (interesting article here).

And yet America is the last becon of hope in the coming storm. How long will that last?

I expect it to do the opposite. The US be able to import more goods as the dollar raises in value and export countries will be able to sell more goods to the US.

Weak local currencies are very good for exporting countries.

The US Dollar is now at 108.56 on the DXY today and is SOARING IN VALUE and will soon be well over 110.

Wolf, I am reading reports of auto repo’s increasing. Any thoughts?

Yes, from record historic all-time lows during the stimulus era when people used their stimmies and auto-loan forbearance to get caught up. I’ve covered this phenomenon extensively. They’re still way below pre-pandemic normal.

I cover the quarterly delinquency data on auto loans. The Q2 delinquencies, when the data comes out in a little while, will show an uptick but will still be below normal. Same with foreclosures.

The internet is a strange place, full of BS-ing YouToubers that try to get clicks.

Morgan Stanley :

The first close < May 12 low was June 13. June 16 was the trigger.

Today low was < the trigger, a lower low. It's not bs. It's a hammer at the bottom.

It might be a buying opportunity when the news are worst.

I found this a fascinating, fact-based (including statements from the Fed in the past) take on The Fed :

Jeff Snider: Recession Will Worsen The Bear Market & The Fed Is Powerless To Stop It – Wealthion – 14 Jul 2022

Looks like the crazies in MSM land is out in full force already playing preemptive defense for the FED. Saw this on Marketwatch….geez, why not suggest open back up the QE tap all over again..wtf

“Opinion: A Recession can be avoided if americans accept 4% inflation”

that is insanity

4% compounded over ten years is almost a 50% drop in Purch Power

4% inflation means 4% or more short rates….or did this person think holders of dollars must be punished?

So many fully long equities and spewing this nonsense

The pressure on the Fed to pivot when the inflation rate goes down will be gigantic. This will be a huge test for them. I expect them to fail the test, pivoting prematurely, and thus causing a resurgence in inflation.

By the time the inflation rate goes down assets will be a smoking crater any way.

Job done for inflation.

And a population shock and awed out of the ‘BTFD’ mantra.

That’s the whole point.

People front-running stimulus, the very stimulus that causes this issue of asset price and then cpi inflation.

Until people are weary, the inflation won’t drop.

And weariness will arrive with a bang, not ‘softly’, just like we’ve never had soft cycle ends before.

The big question is, will confidence return quickly enough at the other side?

Or will people fear BTFD if they think inflation may return and their assets are cratered further as stimulus upon which the economy is seemingly dependent, returns?

Will confidence be too battered just like 2008/9, despite the record bailouts?

That’s the $64 trillion dollar question right there. Will people default back to BTFD everything will go back up mentality? My cynical side is pointing to a yes. Simple conditioning from the last 2 decades, in fact for some young bucks, this is their entire mentality since existence so the gravitational force of don’t miss out on the wave up is strong out there.

One of the largest components of all goods and services is energy. Wolf has written about the NG price and the age of low LG price we have experienced for decades.

Except for the bounce in price in 2001-2008 we had flat to decreasing NG price since the 1980s when NG was deregulated. Then the shale industry kicked off and the rush for new acreage and drilling spurred a PE and public rush to capture the resource.

Many companies went bankrupt the PE firms continued their hype and marketing to fund the industry. My point is we had below market oil and NG domestically that helped fuel the economic expansion during the interest rate suppression from 2008 until 2021.

The reset may be much more difficult to sustain as a permanent ESG push has hit the world.

Nothing moves in straight line and these events will take years to emerge and filter through the world economies. At the same time over time the human race will continue to produce and live.

Most NG is still burned off at the well head.

It’s less than 2%. Look it up.

Still, any is bad. It’s good to deplore wastefulness, but there are plenty of more promising targets, for example, it’s estimated that about 40% of the food produced in the US is wasted, which means the NG used up to produce it is also wasted, as is every other input.

There are many examples. Unfortunately, the way economic statistics are engineered, waste is profitable, so the incentive to waste is built in.

One might wonder how the human species has survived this long, but then, bacteria have survived for hundred of millions of years with no brains at all.

Harold,

“Most NG is still burned off at the well head.”

Hahaha, where do people come up with this stuff??

In the US, 1.0% of the natural gas produced is vented and flared (burned at the wellhead). This amounted to 420 billion cubic feet in 2020, according to the EIA, compared to 40,614 billion cubic feet of natural gas produced in 2020.

That said, there shouldn’t be any NG flared. NG is a valuable product and it should be sold and used. The problem is that at some oil wells, there is no infrastructure in place to process the gases (not just natural gas) and take them away by pipeline.

“Just don’t blame money-printing and interest-rate repression.”

This reminds of a guy I used to work with. He was in his late 60s and was a hard core chain smoker. At the office he would go into these 2 minute long terrible coughing episodes. Some got so bad that I would be just about ready to call for the paramedics when the coughing episode would stop. Then the old guy would claim that it was his allergies that made him cough. He would never admit that it had anything to do with smoking!

Lol!!

Gas prices are falling and oil is low 90s.

Food is going to keep going up as late summer is when the “new crop”, (I.e. new fertilizer and fuel price based crops) start coming in.

Still not seeing 1% in July though; there is an election coming in November.

Hi Wolf,

Could you comment on international inflation more generally? Is there a mechanism by which US inflation is/was “exported” to the rest of the world, or is it solely the result of policies conducted inside the individual currency areas?

Thanks!

Great question. Wolf touches on it here but I too would like to see a more complete discussion of the worldwide inflation picture. Particularly now that the whole planet seems to have NOW figured out that inflation is not “Transitory”… “this time” really isn’t different from all the rest of the times.

Kevin,

Do you think that the US “exported” inflation to Europe, the biggest most reckless money-printers and the most rabid interest-rate repressors of all? That’s funny. They created their own inflation.

BTW, the US imports a heck of a lot more than it exports, so if anything, it would be importing inflation from other countries.

But the simple fact is that all these governments printed huge amounts of money, repressed interest rates, and doused consumers with free money. So what do you expect? It’s going to be the same everywhere. Central bankers will learn a lesson – and unlearn many other lessons – that will make their ears ring.

Hi Wolf,

Kind of funny, “and the most rabbit interest rate-repressors of all”.

Great article by the way.

So much fraud out of the Fed and even Wall St. and Washington. Inflation is just wealth transfer to the top. If the taxpayer ever understood it, and collaborated, they might collectively refuse to pay taxes or even rent like the Chinese started. Lying cheatin thievin scammers. Everyone, everywhere, especially the banksters

LOL smoking and cough

ESG investment and inflation

Money printing and rent forgiveness and inflation

No energy investors and inflation

No chips and inflation

China shutdown and inflation

Interest rate suppression and inflation

None are the reason!

Russia find someone to blame!

When is the Fed going to learn that credibility is EVERYTHING for a Central Bank? Stop talking about how your goals are to return to 2% inflation AND have a “soft landing.” 2% inflation was an outgrowth of a Great Recession… which is NOT the situation we currently find ourselves in. The current economy is flush with cash and thus overheated.

If the Fed truly wants a soft landing then the real inflation target for them is going to have to be 3 to 4%. Which is OK… for the 40 years since Volcker worked his magic that is where inflation sat. If the Fed wants 2% inflation then they are going to have to bring on a powerful recession.

Like so any things in life… solutions are not about choices but about trade-offs. The Fed needs to decide where the sweet spot is for the trade-off between inflation rates and recession. They can’t have the BEST of BOTH worlds.

I love the look on people’s faces who are under 40 when I suggest that 3% 10 yr yield is low and that 5% to 6% is closer to historic norm . This lack of understanding amongst a significant portion of the population is most concerning IMO .

The Fed will do what it always does when it looses control…move the goal post and change the make up of the CPI .

There are also a surprising number of the over 40, 50 and 60 who seem to lost all long term memory.

Stupid economic policy has stupid consequences. Unfortunately, it is not the people responsible for the policy decisions that suffer the consequences.

The people are about to learn the reason why you should never let government run amok.

Are some people planning to attack the Democracy Store again and demand to speak to the store manager?

Today was an interesting trading day as the wall street spin machine trotted out Fed’s Waller to tell the markets that a 100 bp hike was likely off the table. The fact the markets reversed on that news and semis rose tells me this is a thinly traded market with modest inflows (is everyone on vacation?). The fact semis rose in a slowing economy tells me that the inflows were retail money. (Big gap on the charts above most semi stocks shows massive profit potential to the retail mind.)

The markets seem to be in paralysis just waiting for the data to come in bad enough to justify a Fed pause.

We’ll see if upcoming earning allows the markets to keep treading water. The markets should be falling, yet they keep waiting on the Fed to turn dovish. Any day now….

.

.

.

Maybe we should redesign the economy so that it automatically generates demand reducing forces as it overheats — instead of waiting for the gauges to get pegged and the gaskets to start blowing?

.

.

.

The magnitude of a 1% increase in the funds rate on a system used to operating at a funds rate of zero or below. Unless one compares that statistic with percentage change in the current rate which in this case is nearly a 50% change in the existing rate. Variable rate debt that was a no brainer at zero pct interest begins to be a serious drag on cash flow at 3 to 12 pct commercial rates. Still a bargain compared to the coming reconciliation between price and value that may eventually occur. It may take awhile.

How is there a market when the Fed suppresses interest rates to zero ? Even now, the invisible hand of Fed cash rescuing the market from it’s opening swoon the last few days feels organic. My point is that what is happening in the markets is choreographed and individual investors should stand aside because they are whom are on the dinner menu.

In my experience, the outcome has never been clearly predicted by the facts, as currently measured. So no one can accurately predict how the current malaise will resolve itself. Unless they are lucky to have guessed correctly.

There is a mathematical calculation in Finance that describes the logarithmic effect of the value of a fixed income security at various interest rates. It’s called convexity. As the current interest rate rises, the value of an issued security falls.

The QE experiment seems to have a clear positive hypothesis: that asset price inflation causes a general price inflation.

Bubbles are not benign. They are an economic disequilibrium that only makes sense from the point of view of the winners.

I am trying to understand buying durable goods in this world of still low interest rates and high inflation. So say I am buying a car. If I pay cash I have a car that is worth what it is worth and the cash is gone. Say the interest on a loan is 3.1% and inflation is 9.1%. Doesn’t it make sense to finance it and pay the loan payments over time as long as inflation is greater than the 3.1% interest I am paying?

Inflation is only helpful if your income rises faster than inflation. If it doesn’t, you’re screwed, and inflation just saps your spending power and makes servicing debts harder.

One thing that escapes my understanding is why the Fed has the burning desire to strive for a rate of 2% inflation; given that ‘inflation’ is a process rant decreases the value of the USD.

Wolf ?

The funny thing is that 2% used to be the upper limit of tolerated inflation until about 2011 (?), when the Fed changed it to a “target” of 2%. Then in 2019 or 2020, it changed the “target” to “symmetrical target” allowing for overshoots to make up for undershoots, which is in part why the Fed was so late in its reaction to this bout of inflation. I wouldn’t be surprised if this inflation fiasco leads to a re-think in a few years (2025?) with a return to the “2% is the upper limit” concept.

Wolf,

Given low interest in last a few years, why don’t people use fixed? Because of expectation of long lasting low interest rate or higher house price?

I don’t know the distribution of 3y and 5y arm, the reset time seems still a few years in the future. It seems it will bolt down to the will power of FED during recession. And we know their will is fragile. Given labor shortage and growing population and appreciated-a-lot shadow inventory, the market seems unlikely to repeat 2008. Maybe RE market will not drop much and most ppl will be ok.

1. In Canada, there are not government-guaranteed 30-year fixed rate mortgages in Canada. That’s a US creature coming out of the Great Depression.

2. Variable rate mortgages had lower rates than 2 year fixed or 5 year fixed, and given the sky-high prices, people went for the lower rates at the time, and now they’re facing reality. That is typical human behavior. That’s why you have housing bubbles and housing busts.

Have you written anything about ARM/fixed % in total loan, ARM period/reset date break-down in US? In US, it’s foolish not to lock in ultra-low interest rate during the last 2 years, so the reset date could be 2-4 years away. With massive appreciation over the last 2 years, I would think ppl can easily unload the house and won’t lose much. Do you think so?

Assuming the recession usually lasts 6 months and RE is in slow motion in nature, it’s hard to see FED will maintain the high rate in 2-4 years. So maybe this time is different from 2008.

In terms of the US: ARMs have a bad reputation because many of them blew up before the housing bust when rates rose. But ARMs can be a good deal and are a legitimate choice. What they do, and what people need to realize, is that they add a lot of risk to the ownership experience. So you need to be able financially to deal with the consequences. If you’re getting an ARM because that’s the only way you can afford the payment, then you’re walking a tightrope, and you have a good chance of falling off. But if you’re getting an ARM and have enough assets and income to deal with the issues when rates rise, an ARM can save you money. Obviously, practically no one takes out an ARM when you get a 30-year fixed at 3%. But when the 30-year fixed is 7% an ARM could be a good choice for people with lots of financial wriggle room.

I see a replay of 1980 when interest rate were as high as20% and unemployment was 10%.

They created a monster with their run hot policies and it will take a very hard landing to snuff out this inflation

With the current supply chain issue, the debt load and the tracking record of both parties, there is zero chance.