Oh dearie, the Fed is going to meet in late July, and it’s going to talk about services inflation.

By Wolf Richter for WOLF STREET.

Services are now starting to power this inflation. And services are where people spend the biggest part of their budget. It’s where inflation is now getting entrenched, independent of commodity prices, and where it’s very tough to bring inflation under control. The declining commodities prices may help contain food prices and gasoline prices, but not services.

Inflation in June was also driven by food and gasoline where it’s staring consumers in the face on a daily basis, though some of the price pressures are now abating. And prices of durable goods, such as cars and electronics, are rising at a less ugly pace.

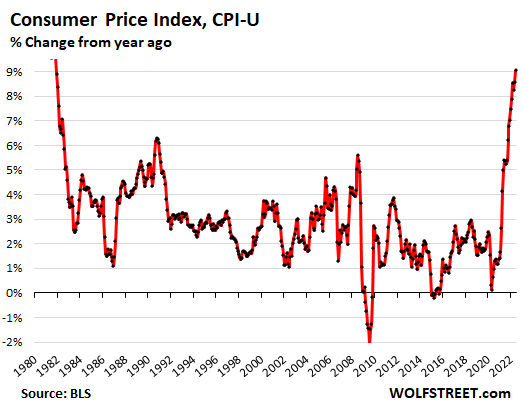

The headline Consumer Price Index (CPI-U), released today by the Bureau of Labor Statistics, spiked by 1.3% in June from May, and by 9.1% year-over-year, the worst since 1981:

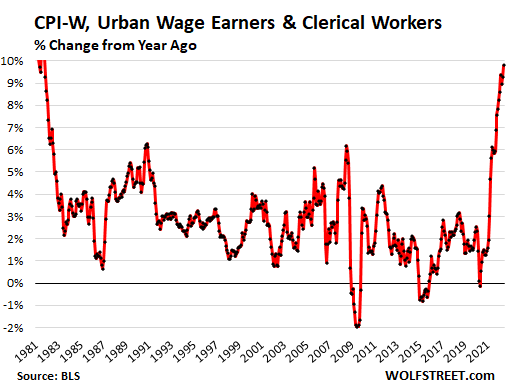

The Consumer Price Index for “all urban wage earners & clerical workers” (CPI-W), whose third-quarter average is used to adjust the COLAs for Social Security next year, spiked by 9.8% in June:

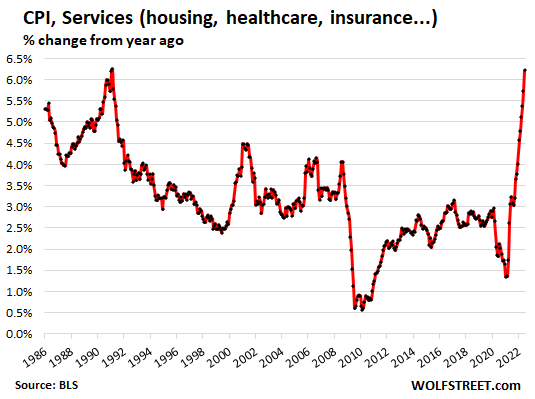

Services Inflation gets ugly and is hard to control.

Inflation in services is not related to commodities. And the recent declines in commodities that will eventually show up as lower inflation in gasoline and some food items has no impact on services.

The CPI for services spiked by 1.0% in June from May, and by 6.2% from a year ago, the worst since 1991. And this isn’t going to turn around anytime soon, and this is why the Fed is going to dish out some salty rate hikes to get this under control:

Services include housing costs, which we’ll get to in a moment, and other key items, most prominently these (year-to-year % change):

- Housing: +5.7%;

- Hotels & motels: +11.5%

- Health insurance: +17.3%

- Medical care services: +4.8%

- Airline fares, summer special: +34.1%

- Delivery services: +14.4%

- Other personal services: +6.7% (personal care: +6.3%; laundry and dry-cleaning services: +10.2%, haircuts: 6.3%)

- Video and audio services: +4.9%

- Pet services, including veterinary: +7.9%

Some services prices declined, year-over-year:

- Telephone services: -0.1%

- Car and truck rental: -7.7%

- Admission to sporting events: -6.1%

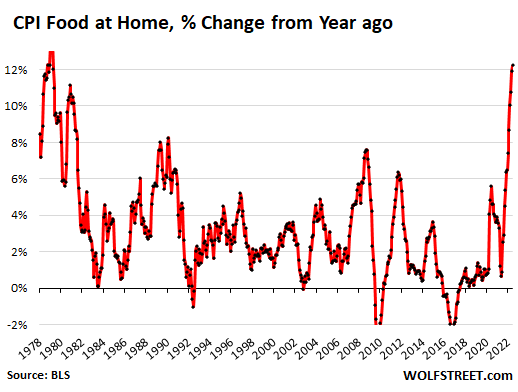

Food, oh dearie…

For people in the lower part of the income spectrum spend most of their money on necessities, and a relatively big portion of their income goes to food, and they’re getting crushed by this food inflation.

The CPI for “food at home” – food bought in stores and at markets – spiked by 1.0% in June from May, and by 12.2% year-over-year, the ugliest spike since 1979:

In some categories, the price spikes earlier this year are running into resistance, and prices dipped on a month-to-month basis, such as beef and pork. But prices in other categories are now going haywire, such as cereals, poultry and eggs, as inflation jumps from product category to product category.

Major food-at-home categories, and % change from a year ago:

- Cereals and cereal products: +15.1%

- Beef and veal: +4.1%

- Pork: +9.0%

- Poultry: +17.3%

- Fish and seafood: +11.0%

- Eggs: +33.1%

- Dairy and related products: +13.5%

- Fresh fruits: +7.3%

- Fresh vegetables: +6.5%

- Juices and nonalcoholic drinks: +11.6%

- Coffee: 15.8%

- Fats and oils: 19.5%

- Baby food: 14.0%

“Food away from home” CPI – such as food from restaurants, vending machines, cafeterias, and sandwich shops – jumped by 0.9% In June from May, and by 7.7% year-over-year, the most since November 1981.

Energy…

The Energy CPI spiked by 7.5% in June from May and by 41.6% from a year ago. This was driven by:

- Gasoline: +11.2% for the month, +59.9% year-over-year.

- Utility natural gas to the home: +8.2% for the month, +38.4% year-over-year.

- Electricity service: +1.7% for the month, +13.7% year-over-year.

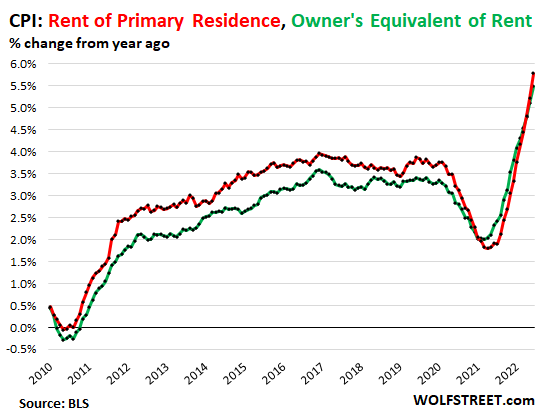

Housing costs – they’re spiking with a lag.

The CPI for “rent of shelter” accounts for 31.9% of total CPI and is the largest component. It attempts to measure housing costs as a service (not as an asset to be purchased). It comes in two components:

“Rent of primary residence” (accounts for 7.2% of total CPI) jumped by 0.8% in June from May, and by 5.8% year-over-year (red in the chart below). It tracks what a large panel of tenants reported about their actual rent payments over time, including in rent-controlled apartments.

“Owner’s equivalent rent of residences” (accounts for 23.7% of total CPI) jumped by 0.7% for the month and by 5.5% year-over-year (green line). It tracks the costs of homeownership as a service, based on what a large panel of homeowners report their home would rent for.

Both measures, though spiking, are still below the overall CPI and therefor are still holding down CPI, but they’re holding it down less each month, and in a few months, they will become the primary driver of CPI inflation:

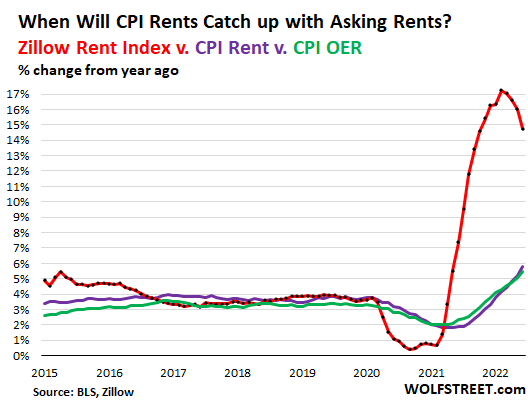

CPI for housing costs, Asking Rents, and Home Prices.

The CPI for housing costs consists of two above rent measures: the first tracks rents as experienced by tenants that have been renting these homes for a while; the second tracks what homeowner think their own homes would rent for.

“Asking rents” track advertised rents of apartments and houses listed for rent. They’re a measure of rents that landlords are trying to get on their vacant units. They do not reflect actual rents paid by tenants. But they show where landlords think the current market is.

The Zillow Rent Index reflects asking rents. It jumped by 0.8% in June from May, to a record of $2,007, but that jump was smaller than the prior spikes. On a year-over-year basis, it spiked by 14.8%, which is a huge and gigantic spike, but it was smaller than the prior spikes.

But it takes a while for asking rents to become actual rents that tenants have to start paying when their lease expires and that they are then reporting as part of the CPI panel.

The “rent of primary residence” (purple) and the “owner’s equivalent rent” (green) are slowly catching up with the Zillow Rent Index (red), and they will continue to rise well into 2023 even if asking rents tracked by Zillow rise less (my discussion of this phenomenon):

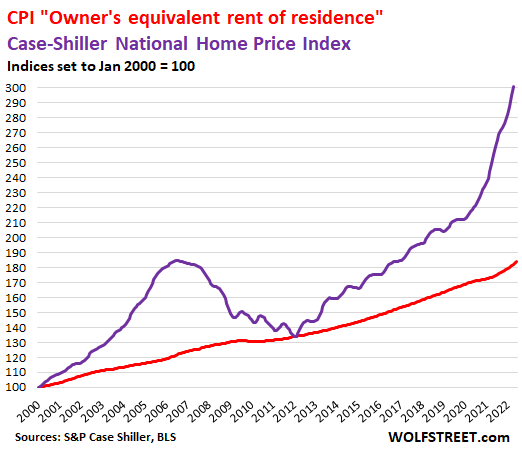

Home prices spiked by 20.4% year-over-year, according to the latest Case-Shiller Home Price Index (purple line below). I have been documenting this raging mania with my series, The Most Splendid Housing Bubbles in America.

But the CPI attempts to measure the cost of the service that a home provides – shelter – via its “owner’s equivalent or rent” (red). Both indices here are set to 100 for January 2000:

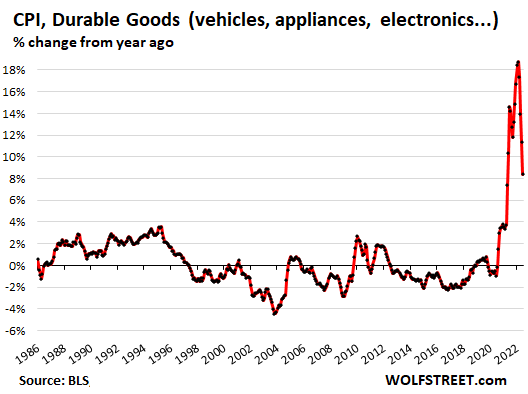

Durable goods CPI.

New vehicles, used vehicles, consumer electronics, furniture, appliances, etc. Month-to-month, CPI for durable goods rose 0.7% in June, after having ticked up just 0.1% in May and April, and having dipped in March.

Year-over-year, durable goods still spiked by 8.4%, but this was way down from the 18.7% spike in February:

Some major categories of durable goods:

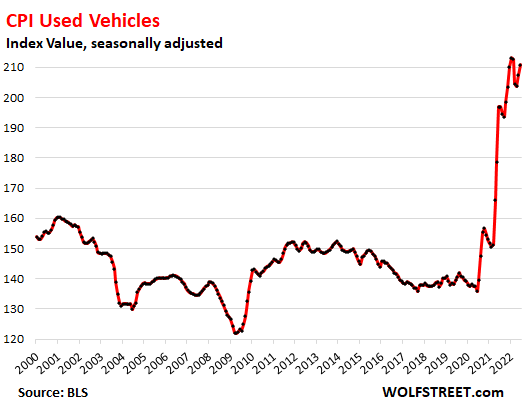

Used vehicles CPI: +1.6% in June from May, +7.1% compared to the sky-high spike a year ago exceeding 40% at one point. In February, March, and April, prices had dropped. But in May and June, prices jumped again.

This chart shows the index value (not the year-over-year % change of the index value):

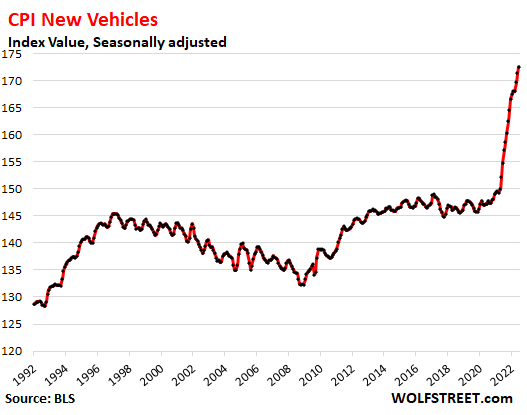

The new vehicle CPI: + 0.7% in June from May, +11.4% year-over-year. The last few months have seen the worst price spikes in the data going back to the 1950s, amid still widespread new-vehicle shortages and “above-sticker” prices. Much higher interest rates would help bring demand down, which would relieve some of the price pressures.

This chart shows the index value (not the year-over-year % change of the index value):

Information technology (computers, software, accessories, smartphones, etc.): +0.3% in June from May, -6.7% year-over-year. These types of products have gotten immeasurably more powerful over the years. Today’s smartphone runs circles around super computers in 1980 that cost millions of dollars back then. So the amount of money that you pay for what you get – which is what inflation measures – tends to fall year after year.

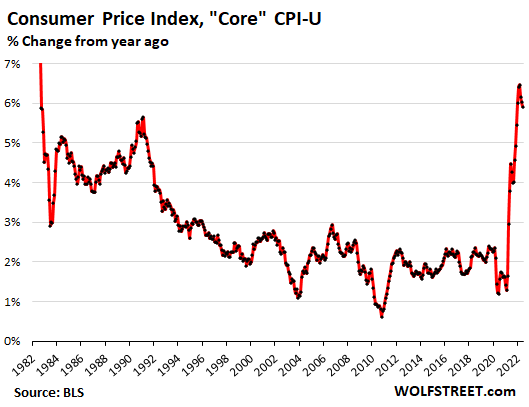

“Core” CPI.

The “core” CPI, which excludes the volatile commodities-dependent food and energy components, tracks inflation in the broader economy. It jumped by 0.7% in May from June, the biggest jump since February – accelerating again, now driven by services!

Year-over-year, it rose 5.9% from the red-hot levels a year ago. The sharper month-to-month increases and the spike in services will start to push the core CPI higher later this year.

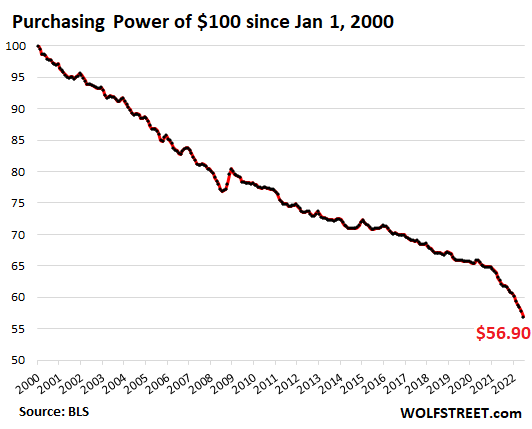

Purchasing Power of the dollar goes WHOOSH.

The CPI tracks the loss of the purchasing power of the consumer’s dollar and the purchasing power of labor. In June, the purchasing power of $100 in January 2000 dropped to $56.90 in June 2022. No wonder Americans are in a rotten mood:

And here is Fed Chair Jerome Powell contemplating the next rate hikes, as captured by cartoonist Marco Ricolli for WOLF STREET:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Appreciate the sector breakdown! Fortunately, this is old news. /s

Ya, the CPI is clearly a lagging indicator now. I’m witnessing price drops everywhere, but not in everything. I paid $3.93 for gas yesterday, down from $4.59 and housing prices are dropping like a rock in our area. Bulk shipping rates are dropping as are most commodities including semiconductors. Coffee is still expensive, but that could be from other reasons like drought in SA, or whatever. Services I’m not so sure about. We don’t really eat out that often, and when we do it simple stuff like burgers. I don’t think we’ve had any rate hikes in our health insurance, but car insurance definitely went down. I’m thinking it’ll take a little more time for commodity price drops to bleed into everything else. Services will be the last to fall, but that should start fairly soon as competition for customers, who will be enjoying services less frequently, kicks in.

Djreef,

Hahaha, Publius was being sacrastic about a Biden comment — concerning gasoline. I think you missed the sarc tag.

You’re right about gasoline inflation backing off and food inflation may have topped out too, it seems. Durable goods inflation is already heading lower, as I pointed out with a chart.

But you’re dreaming about services. They’re just now heating up — and that’s 60% of where consumers spend their money.

I had to read what Djreef wrote twice. Caught the sarcasm from Publius. Other than saving a few cents on gasoline I am not seeing many price drops in goods or in services.

Well, I take that back. I am seeing real estate price reductions more frequently now. But that depends on the perspective of the time frame to determine if it really is a price drop.

If this is the case, then the drop in demand in the services sector over the coming months may ruin quite a few businesses. I suspect if recession comes that a decline in services will be the triggering event.

You say food, I cannot walk out of a Safeway or a Sprouts without hitting $100. Pre pandemic, $100 was a very rare occurrence.

Hopefully the drop in commodities will help with services as commodities are part of the cost of service providers?

I read airline fares are up 34% for June YOY.

Auto Body repair work is up 14%

Other auto services are up 9 to 10% (I just had an air compressor replace in my truck and it ran $1100. Ouch)

Medical insurance is up 17%.

Discretionary things like travel will have to take a hit eventually? I do not people who are taking a vacation this summer even though they should not but it has been over 3 years because of Covid.

I haven’t purchased any gas for a couple of weeks, but noticed that the local tourist trap station near me has reduced its price for 87 octane from $6.19 to $5.99 per gallon. I think I paid $5.80 when that station was charging $6.40 per gallon.

House prices here have increased by 50 percent since Election Day 2020. I’ve noticed a few price cuts recently, but not big enough to get me to buy.

Here in the Phoenix suburbs I saw my house bought for $400K in Dec 2019 go to $650K at the beginning of this year. Now similar houses are being listed at 600K, with reductions of 1k here and there. It was still too expensive when I bought it, but I had to get out of CA. Was paying 3.5k / month for a 900 sq ft apartment, which was starting to turn into a ghetto.

Ground report from San Diego about home prices: Real estate is still very hot. No drop in price. Which area are you in where home prices are dropping ?

Also, I don’t see consumer reigning their expense yet.

Tons of price drops in the Bay Area and lots of houses staying on the market for weeks. Still at levels above Jan 2021 but the Zestimate graphs are starting to drop down dramatically after the dramatic spike of the last 18 months.

Ground report from San Diego. Everyone I talk to is Fed up with housing and wants to leave.

Central Ohio is not seeing house prices drop, yet. However, inventory is finally starting to build.

Houston/San Antonio/Austin triangle. Current listings (about 1 in 4) are being reduced anywhere from $5,000-$35,000 depending on starting price according to Redfin/HAR/Zillow.

jon, a thoughtful fellow who has tracked San Diego residential real estate for over 15 years — Rich Toscano at ‘Professor Piggington’ — shows that prices are moving down, now:

https://www.piggington.com/june_2022_housing_data_interest_rates_starting_bite#comment-299369

In San Diego, YOY, pending sales are down, inventory is up, and price cuts are up.

In San Diego, MOM, prices for homes and condos are both down, as are prices/sq. ft.

In a few months, we will see prices falling not only MOM but YOY.

I have seen this movie before, and its start has been long overdue. My sense is that the move down will be sharper and deeper than the mid ’00s downturn of ~40% in median home price.

Bend,OR. Inventory spiking, prices beginning to fall. Yay!

Even though gas is indeed going down, like Wolf is saying costs are still way up for services which is where most US spending is. And inflation is especially difficult for American individuals and families with rising rents–that’s where the real economic damage is being done. Plus food prices are indeed up. On our trips out to some states and regions esp in southern California, the Pac NW, New York, New Jersey (except for Newark) and New England, prices are in general higher, but it’s the sharp increases in rent and food that are hitting Americans especially hard and esp in those states. The food pantries and homeless shelters are filling up, and shoplifting and other petty crime is way up. Even though we also have a lot of stupid inflation in Texas and Arizona too, it’s still comparatively affordable here esp in the rent costs compared to those states and regions at least from what we’ve seen. Even Florida with its own rental crisis in cities like Tampa and Orlando, hasn’t gotten as bad as NY or southern Cal. (People are still moving down from NY to Fla, and a lot to Texas and the Midwest now too).

The Fed really has no option but to go full Paul Volcker now, and if anything, even a 1 percent or 125 basis points interest rate hike late in July might be undershooting the aggressive action they need. It would make sense to schedule an emergency meeting before the main scheduled FOMC meeting in late July to do an additional rate hike then and more aggressive quantitative tightening, perhaps just as a signal about how serious they are in breaking this inflation in its tracks. The QT if anything may be even more important than the rate hikes as a way of shutting down the asset bubbles that are one of the primary causes of the general inflation, esp the housing bubble that’s the main cause of these out of control rents. That’s the one tiny advantage the Fed may have here compared to Volcker, who didn’t have that kind of QT at his disposal.

It should have gone full “Paul Volcker” last year, at least based on the food prices that I have been paying the last four years. Remember, if you multiply the rate of actual inflation, less whatever they pay depositors, times the fifteen trillion to twenty trillion that banks hold in deposits, CDs, etc., you can compute the over trillion dollars a year in their profits from the actual, negative interest rates they pay depositors, which motivated the banksters to discourage the “Fed” from raising interest rates.

Very well-said. Exactly the same question that puzzled me. With a 9.1 CPI, why are they not doing an emergency rate hike right now? Why wait for another two weeks to do a 0.75? This is absolutely ridiculous. They only care about the crooked stock market. It is criminal. Shorting the market is the only just and right thing to do. Good will triumph over evil in the end.

Inflation may be old news, but it’s a derivative and so its impact keeps increasing even if it goes down a little bit. Let the mainstream media assume that people a foolish enough to think that any small decrease in inflation will decrease the prices across the basket of goods.

The fed planned that they would couple tiny rate hikes (Real inflation rate = 1.6% – 9.1% = -7.5%) with tiny QT (still hard to see on chart!) to control huge inflation.

Today we got the result of that plan!

Inflation also is monetary thing. Price indexes may or may not have a strong coupling to inflation. For a long time the cuopling between inflation and CPI have been weak. Now we either see all pent up inflation hitting the CPI, or if the coupling still is weak, something else is going on.

They love their inflation-caused, effectively negative (negative 6%-7%) interest rates on the depositors funds that they hold: $15 to $20 TRILLION. I am already asking for more for my work. I am sure that labor/wage inflation has taken and will continue to take off, because more and more Americans will find their current wages insufficient to keep the same standard of living.

The banksters’ CCP buddies may unknowingly be coming to Americans’ rescue with a reduction in the demand for commodities that may reduce inflation. LOL.

Yes, and the charts above are all laughably and ludicrously outdated and of no relevance whatsoever on 07/13/2002.

Just gross. Rent cpi a long way to catch up

Minutes

Agreed. Hard to believe anyone is buying any type of residential RENTAL real estate anymore – margins are G O N E !! Real estate moves slowly and those who bought rental stuff in 2020-2022 will have to raise rents significantly to cover costs (increased: prop taxes, insurance, utilities, maintenance labor). The old mom / pops grinders who kept what they have should finally get a bit of a windfall since their acquisition costs were less. Their margins will likely increase a little bit as the rents rise in 2023+

Let’s remember that you can raise the price/rent to whatever. If there are no takers to your price hikes, you either eat the loss or lower your price.

Renting must be local.

Over the last 1-2 years, rent has skyrocketed here. People are moving to Kansas due to high rents.

I don’t see that yet in Wolf’s “Owners equivalent rent of residence” excellent chart above.

What does the chart measure? Are rent increases really flat on average in the US?

Sorry, Wolf may have answered my question above.

From Wolf’s explanation, the Zillow rent index likely reflects reality. Zillow uses real data for asking rents which likely more closely reflect current rents.

The CPI Owners Equivalent of Rent is more vague.

“Qwners’ equivalent rent is obtained through surveys asking homeowners the following question: “If someone were to rent your home today, how much do you think it would rent for monthly, unfurnished and without utilities?”

This assumes the current owner is aware of the current rental value of their primary home. Also, If I was asked that question, and I was not intending to rent my primary home, I would tend to be on the low side since I don’t want the tax collectors to rank my property on the high end of the property values.

Over time, both Zillow and OER should converge.

I made fun of that OER a while back, and wolf smacked me down about it. Apparently, there’s more sense to it than it seems like.

Hey Bob. I am curious. What area are people moving from to go to Kansas or was that sarcasm?

I thought everyone was moving to Texas and Florida and North Carolina. ;)

Yeah it’s the rent where the inflation is most brutal right now, it’s also bad in food but rent has been surging so ridiculously in a lot of markets that it’s squeezing people’s ability to buy food too. Especially out in at least southern California right now, and New York, New Jersey (outside of Newark) and just about anywhere in the Pac NW or New England (Seattle is out of control). Everytime we travel there for business or to visit family, seems like the food pantries are overflowing, people literally can’t feed their families right now with inflation like this.

Those are also the places where the housing bubble has been the most sustained and crazy, so little surprise that the buyers at the top of the housing bubble (or corporate rental purchasers looking to get rich as slumlords) are pushing rent through the roof. I truly can’t understand how even upper middle-class professionals can afford to live there anymore. We’re also getting stupid real estate bubbles and rent issues down here in Texas and Arizona, but rent here is chump change compared to what people in those states are having to come up with every month. Even in Florida with its infamous rent mark-ups in ex. Tampa, it’s still more affordable overall, which is saying something given the fact that the home price bubble has been ridiculous there too. It’s the monthly rent where Americans in general really feel this inflation, and paying the price of the folly of QE and other recent Fed policy.

We all saw this coming, but the speed of it is still shocking. Toonces could’ve done a better job than these folks. You youngsters will have to search that one.

Ha!

Driving off a cliff?

I got the Toonces reference (coz I’m old). As of April 5, the Fed was still unsure whether we were in a housing bubble: “warns the Federal Reserve Bank of Dallas, is that the property market is showing ‘signs of a brewing U.S. housing bubble.’ Housing prices had already gone up 20% in 1 year and 38% in 2 years per Case Shiller. At least Toonces knew when he’d driven off the cliff.

I am amazed that Steve Hanke was able to accurately predict inflation % and persistence and the Fed got it so wrong. I just can’t believe the Fed 400 PhDs can’t better predict inflation than a lone economics professor.

I wonder if Fed is working with Yellen to soft default a portion of the debt away as paying a real interest rate on debt would be too much for good ol uncle Sam.

I grew up with a tabby cat we named after Toonces, thanks for the trip down memory lane!

According to the National Association of Realtors, the June 2022 median home active listing price was up 16.9% compared to last year.

This is from their June 2022 Monthly Housing Market Trends Report.

Inflation is out of control.

I was just reading a local news article here in Maricopa County. In April and May 2022 the average amount of homes listed for sale in the Phoenix Metro Area, was between 3500-4500. In June there were 17,000 active listed homes for sale. The value of my home has dropped 100K over the past 30 days. I am predicting this will be worse than 2008 bubble.

Wow!!!

100K in 30 days, what percentage drop is that?

I haven’t been monitoring home prices in Ventura County, but I don’t think they are anything near what you are seeing in Maricopa County.

12 %. We bought our house for 320k in 2012. Zillow had it valued at 859k last month, and 759k a couple of days ago.

Everything is local and based on supply. There are some areas where prices have not dropped that much, others that are coming back down a bit more. But supply needs to rise even more before prices really fall. Another 1% higher and prices will start to really drop, Let’s see what prices look like in a year from now.

What with deflating the amount of money to 2008 level?

Should that not make the price indexes go down too?

The last chart says it all for me (Purchasing Power of $100 since 1/1/2000).

That is why, other than in 2008, in the event of a market dislocation -aka a “crash” – the central banks will not be able to bail anybody out by printing money. Because it’s simply worthless because of their own policies. They could print quadrillions, it wouldn’t make a difference.

Banking stocks are looking ugly across the board. They are all insolvent anyway, but with their stocks heading south, a banking crisis is pretty much inevitable. And that will be it.

Agree, that really sums it up.

Now even official CPI is nearing 10% (real is probably 20%) and still practically no dent on stocks. Even the bond yields are not rising. This is because insiders know that this is all orchestrated. This inflation is orderly, well planned and synthetic and Fed and UG Govt. are the root cause. This was needed to reduce the debt burden and then only way out of the debt crisis and Covid gave them a good cover and now War.

Remember when USA defaulted last, when it moved away from the gold standard. US Govt basically said one fine day they will not honor what each USD stood for anymore. This was the biggest inflation event in the recent history. Everyone thought stock market will crash next day but it exploded instead. This is called planned inflation. As money is worth less, everything goes up in nominal terms, including all assets. This is terrible for creditors (bag holders) and payday for debtors. Since US and West are the biggest debt nations, this is not surprising. It will only accelerate.

So what can ordinary citizens do. Hold on to your assets and get as much USD denominated fixed interest debt as you can get hold of. It will pay off in the long run.

Re “Even the bond yields are not rising. This is because insiders know that this is all orchestrated.”

Strongly disagree. Longer-term bond yield aren’t rising because there’s still too much money in the economy, and the insiders are in denial and have no idea about the beast they have awoken. So they think inflation is just oil prices, or that the Fed’s rates have control over it, or whatever, but they think inflation will stop fast and roll over and die so longer-term bonds at 3% are reasonable deals. They don’t see how the economy actually works, it’s not in their day-to-day experience, and they don’t remember the ’70s (when, BTW, longer-term bonds paid a lot more…).

Wolf’s depiction has been spot on for over a year. Inflation acts like economic cancer – it starts in one area, metastasizes, spreads to other areas, becomes entrenched and becomes really, really difficult to control. It’s not a one-hit wonder, or a one-year event. It’s a process, an ordeal, a major long-term challenge… fixing it requires not lower rates, but an economic overhaul to restore productivity and balance between supply and demand.

Agree that bond yields probably aren’t rising more than they are because there’s still too much fiat floating around. Seems like QT should be larger.

i read this earlier today, it was written by a wise man back in 2012:

“The law of supply and demand, in fact, is one manifestation of a basic principle of systems theory, a principle pervasive and inescapable enough that it’s not unreasonable to call it a law. The law of equilibrium, as we might as well call it, states that any attempt to change the state of a whole system will set in motion countervailing processes that tend to restore the system to its original state. Those processes will not necessarily succeed; they may fail, and they may also trigger changes of their own that push the system in unpredictable directions; still, such processes always emerge, and if you ignore them, it’s a fairly safe bet that they’re going to blindside you.”

our complex system (global economy) is getting pushed and pulled in many directions. mostly out of desperation. and i’m pretty sure many, if not all, policy makers are going to be blindsided by the consequences of their previous, desperate actions.

There is no “master plan” and no one or no group is anywhere near as intelligent or has the foresight you claim.

I agree, AF.

Kunal wrote:

” Hold on to your assets and get as much USD denominated fixed interest debt as you can get hold of.”

This could backfire badly in a stagflation scenario. Your income will deflate if you lose your job. Even if you don’t asset values might deflate if many others are losing their jobs and have to liquidate because they are unable to service their debts.

Stagflation = consumer price inflation + asset price deflation

Told my wife recently. We need extreme stagflation ASAP. It’s going to suck for everyone else, but with our cash and need of a home now, personally we can benefit greatly.

I don’t think you understand how stagflation works.

Prices continue to raise under stagflation.

Could it be inflation is paying to bring down budget deficit.as reported by uncle decreased1.7 trillion .AMAZING

Debt to GDP is actually lower today then it was pre-pandemic due to growth in Nominal GDP (mostly inflation and higher tax receipts due to capital gains in 2021).

Government Debt to GDP in the United States averaged 64.54 percent of GDP from 1940 until 2021, reaching an all time high of 137.20 percent of GDP in 2021 and a record low of 31.80 percent of GDP in 1981. 12/2019 at 107%, so no

You’re right. But it is lower than the peak of 137. It’s 124 today.

Seems the stock markets likes hot inflation. Unless Powell does 1% or higher, it looks like the markets may grind higher on all summer. My guess is that there’s substantial foreign inflows here to take advantage of the strong dollar. It just tells me there is way too much money in this world.

First they sell off on rate hike fears then when the fears are confirmed they say – let’s buy anyway!

Uber Driver

“…Unless Powell does 1% or higher, it looks like the markets may grind higher on all summer…” ???

Fed has been rate raising (slightly) for 4 months and the DJIA and S&P are down 16% and 21% (respectively) YTD ???

Why would markets “grind higher” with ANY level of future rate hike ??

yeah that didn’t make sense to me either. The Fed if anything is getting even more aggressive with rate hikes and QT now, and the market in general is pushing yields higher. That’s going to absolutely crush the housing bubble and equities bubble in particular.

Stock indicies tend to follow m3 money supply. Despite the bleak prospects for the markets substantial inflows continue. I assume much of that is foreign money but many naive US investors look at a gap in a stock’s price and see that as a profit opportunity. Again, there is too much money out there.

If money flows into the markets -stocks will rise, regardless of fundamentals. Hasn’t that been the case for the last several years?

i think looking into money flows into 401k accounts during the lockdowns and ensuing layoffs might get interesting. when you’re laid off you aren’t contributing anymore. i always assumed the markets expected that reliable income stream.

sort of how bmw is offering an $18 a month subscription to the heated seats in a car. a car you have purchased, mind you. trying to get in on the subscription model that’s all the rage these days.

when times get tough, people cancel their subscriptions. they don’t contribute to their 401ks either.

some of their “models” might, yet again, not exactly comport with reality. they’re not paying attention to the big picture, just trying to make it to next week.

This inflation is getting ridiculous. I don’t know how families with non MBA skills can make it.

Seeing lots of paper money with economic messages written on them like “Inflation killing U.S.- Gold instead of In God in we trust- **** Biden!”

Looking at the positive side, people must be learning how to cook at home, garden, fix things. ?

JT-your first sentence a national question not seriously addressed by any party (or the general population) since the Eisenhower administration.

belief in an infinite cheap and permanent prosperity-the driving wheel of folly and history…

may we all find a better day.

I could go into my woods for pine bark and wild berries to eat but I’m too old to fight sasquatch for them.

Squatches are cool. They will not hurt you. Those Jack Links beef jerky commercials are dramatized – real Squatches are curious but kind. :-)

They also sing with remarkable castrato voices and make wicker furniture.

Just the way I planned it! Muhahahahahahaha!!!

The dollar’s purchasing power has swooned. Yet the USD has been soaring vs. other currencies (DXY up to 108). So the purchasing powers of those other currencies (especially the Euro) have swooned even more.

Purchasing power of the USD is what the USD buys in the US.

Exchange rates of the USD against other currencies are negotiated in the biggest market in the world, and traders do what they do.

Those two don’t go in lockstep. They’re subject to different dynamics.

True, but when it comes to, for example, commodities priced in dollars on the international markets, they have to be getting even more expensive for people in other countries.

From Monday, 11 July Farm Net News out of Grand Forks:

“Since the interest rate hike by the Fed in mid-June, spring wheat futures have dropped 27%. Canola declined 22 percent; corn is off 19% and soybeans down by more than 13 percent.”

One other note from my weekly farm news email:

‘Machinery Pete’ Greg Peterson says supply chain issues and the lack of new machinery continues to keep used equipment prices moving higher. “I’ve never seen (it) like in the 32 and-a-half years I’ve been tracking auction prices. It went higher all of 2021 and now, in 2022, It’s like a rocket ship.”

Due to the shortage of parts, Peterson is seeing used equipment being used as a hedge. “It’s coming off last fall when the parts and availability issues were problematic. Even if you wanted to get that new tractor, planter or combine, you couldn’t gets your hands on it. That spooked people. We’re seeing people buying that nice 300 horsepower tractor just to have it.”

And despite a very wet and late spring, things in the Red River Valley of the north are holding some hope. If the weather is fairly normal for the next few months, and there’s no early, hard frost at the end of summer, harvest time, although late, might be better than expected a month ago.

The best prices for 2022 crops may have been in early June, but it’s hard to sell futures when the planting is not done.

The Russians will not allow Ukraine to export its grain. They were a top five wheat and corn exporter. Ukrainian ports are blocked by mines. There are sanctions on Belarus preventing the export potash fertilizer. Natural gas is feedstock for nitrogen fertilizer production. High natural gas/LNG prices caused the closure of some European nitrogen fertilizer plants. Food prices may fluctuate.

It doesn’t work that way, we’ve had this discussion a lot before but the DXY is confusing and can often be misleading as far as the dollar’s true strength, the DXY and Forex markets after all have a limited basket and inputs, and are basically moneymaking opportunities that investors will stretch and tweak all over if they can make extra dough from their trades. And the carry trade (big in the DXY) can be especially distorting. In other words, the FX markets don’t really tell us much about a currency’s true strength of value, and they sort of represent a case of over-thinking what’s going on. Not to mention the USD is falling against many currencies, but again the gyrations of the Forex markets don’t really give us an accurate picture.

A currency’s only real-world value is in purchasing real goods and services that have actual intrinsic value, as one of my econ professors emphasized over and over again (and wrote a lot of exam questions on that basis). Therefore that currency’s purchase power, and the inverse of that purchase power (aka inflation), is the most accurate measure of that currency’s value–it only matters in what it can buy you. And the US dollar is clearly getting weaker and more worthless every month as inflation gets higher and higher. Some other developed countries (ex. the UK) are having similar inflation (and the housing bubbles in Canada, Australia and NZ are even worse than the USA’s), but currencies in many other countries are experiencing more moderate inflation than the US dollar, even if interest rates are lower, so the value of those currencies is dropping less, whatever the numbers on the DXY or what the Forex traders are paying in a transaction set. It’s inflation, and the composition of currency baskets (where the USD is also falling across much of the world) which show that the US dollar is indeed losing its luster as a reserve currency. It’s why the Fed is reacting so aggressively now to fight inflation, as it must.

@Miller – that may be so, but our economy is actually still faring better than many other parts of the world. Over the last 5 years, the S&P 500 is up 54%, while the Chinese, UK and German stock markets are all down over that period. The charts are looking very ugly all over, but our markets have actually fared just about the best of anywhere lately.

@Marc D. Jul 13, 2022 at 8:55 pm

Stock market indices like the S&P500 are not representative of how well an economy is faring. This has been demonstrated time and time again.

Stocks were doing very well in Weimar Germany while at the same time, ordinary people were hurrying with a wheelbarrow full of money to buy a loaf of bread, before the price would rise to two wheelbarrows. The same phenomenon could be seen in Zimbabwe, I still have a framed 100 trillion Z$ banknote somewhere.

Stock market indices have little to do to with economic well-being as perceived by real people.

Yesterday Biden’s press secretary was saying inflation numbers are “already out of date” since gas prices have come down. I wonder if Wolf can forward this article to her so she understands services inflation.

They’re already handing it around amongst the aides there :-]

I think the real reason the press secretary said this was to forestall a panic reaction in the markets today.

COLA baked in at 9% per CPI-W index values…

That’s 1% per month over 3rd quarter index average from last year…

With 3 months to go…

I’m betting around 11-ish unless something drastic happens ( or somebody starts lying)…

COWG

A person turning 62 in 2023 should start taking early SS bennies ASAP – right ? Likely to see 5-7% increase in monthly bennies for 2023 and another 5-7% increase in the couple years that follow ??

Although, waiting until 67 to get the max will have those prior COLAs baked in as well, so the monthly benny will prolly be 20-25% higher than it is today anyway ??

I’m getting close to 62 – so any advice from those of you in the Soc Sec pool is appreciated.

Bear,

I’m the lower earning spouse so I am cashing out early and saving most of the money. We will need all the SS income so hubby will wait for full retirement at 67 and I will get bumped up to half of his benefit. That puts us at the max for us and I will still have 5 years of my lower benefit at my disposal.

Pet,

My brother got in on the program you are talking about I think, but I believe it has ended. He was born in 1952 and me 1956.

There have been at least two and maybe three program cuts that affected me and not him due to when we were born. That’s ok. Probably going to be more for benefit cuts depending on age.

Take it early, while it’s still on offer..the eligibility rules can always be adjusted further out and while you’re waiting the 5 years to reach maximum (devalued) payments, you’re getting 60 monthly payments of dollars with some residual value.

I agree

While in a different situation, I did look at the difference paid to me between 62 and 67, and figured I didn’t come out ahead until 6 or 7 years after 67… so I took it early and didn’t about it anymore….

Been a while, so I might not be totally memory intact… not an unusual situation these days…

This has been our thinking too, and our relatives. While there may be some advantages to waiting past 62, the whole US financial system seems so fragile right now, who knows what politicians might do to eligibility, or if they’ll move the goalposts claiming a financial crisis. Might as well take it now and get plugged in while you can.

Depends entirely on the individual situation Bpup.

For some folks who have little savings or net worth but a good income, it might work out best to wait to initiate SS payments, even waiting longer than ”full benefit” time.

For others, ASAP might be best, but keep in mind that for most folks the monthly SS is NOT going to be anywhere near their earnings potential at a full time job or gig, and there are tax differences too…

For me, right when I hit 65, my full SS age, the industry I had been in for decades collapsed, with reported 15% UN-employment, but almost all of the guys I knew who wanted to work, weren’t, so seemed 85%.

When I went back to full time W-2 work six years later for a while, my monthly SS jumped up a bit; didn’t do that after going back to part time ”consulting” on a 1099 basis, (my long time preference.)

There may be a free ”calculator” on the web these days to help figure out your best policy; or, find a math teach/nerd to help with the calcs.

Beardawg For what it’s worth I retired in 2000, taking SS at 62 some years later. Prior to retiring I had built a spreadsheet calculating my retirement from work along with SS. The SS side indicated I would break even and begin losing at 81, which is 3 years away. Family history was also in the calculation and looks like I have lasted longer than expected. I’m not complaining about living longer.

That’s the typical number I see calculated as well. Saw a mathematician calculate it differently because he calculated odds of not drawing anything due to death while waiting to hit full SS age and he came out that break even number was around 90.

I was making good salary between age 65 and 70, had no debt obligations. Since savings interest rates available were ridiculously low, delaying Soc Sec was a no-brainer for me. At that time, your monthly Soc Sec payments went up about 3% a year for each year you delay.

I could have made some solid jack in the stock market with Soc Sec payments during those years, because it turned out to be in a gargantuan bubble.

But no regrets – my payments are about 20% more than they would have been if I started at age 65. And I’ve always played the long game in terms of frugal, health-promoting, and financial longevity lifestyle. Plus I’m not sure how tax would have been factored in with my working income.

My brother and sister both took Soc Sec at earliest opportunity. Brother for economic reasons, and sister for pessimistic longevity and bird-in-hand reasons.

So reflective self-knowledge, and serious factual research, are the way to go.

Calculate (add up) the current payments you’d receive at age 62 through 65, 66 or 67, whichever age you’d choose for a future retirement date. Then compare the breakeven point in the future using today’s SS payment at age 65, 66 or 67. Also, there’s an “opportunity cost” in that you might use the earlier money to make investments and, hopefully, benefit from its early access rather than later. And factor in the income you won’t be earning if employed until those later dates. Getting payments early may be breakeven at age 74 or so. Consider too your health, your current personal income needs, family longevity, etc.

Bear,

It’s a complicated problem and more complicated if you are married. It’s affected by the peculiar tax rules on SS and it’s probably good to try to find some software program to put in all the inputs about your financial life and let it spit out an answer. At least you would know you gave it your best shot on getting an answer or playing around with what ifs.

I used to use a free retirement planning software on line, but last time I tried to access it, it wasn’t available. The programs have the tax code imbedded and can spit out a lot of data on minimizing taxes and making you feel comfortable about sustainable spending.

The right way to do it I believe is to recalculate your financial future every year, because world changes all the time. Who would have plugged in 9.1% inflation three years ago?

Cowg,

Miraculously, even if the cpi-w goes to 20% over the third quarter, the increase to SS will be in the single digits and wiped out by the medicare premium. Why do you expect it to be otherwise? Have you learned nothing from reading this site?

“ Have you learned nothing from reading this site?“

Yes, I have….

Mostly that Maff is hard…

Medicare, I don’t know about… you’re probably right… find some flimsy excuse ( Doctor’s wives require premium fuel) to snatch some back… so we’ll have to wait and see…

The COLA right now is 9% based on the,

by law, comparison of the CPI-W index values per month with todays index values compared to last years 3q average…

Wolf states all the time about seeing very few deflationary numbers and if you look at the index numbers, you’ll see that in only a very few months has it ever decreased from the preceding month…

With inflation running at one percent per month on the index, even a slightly lower percentage change in the index number will still get to 10-11%…

Even if the next three months numbers ( 3q this year) were flat compared to this month ( no inflation), you’ve still got 9% on the table…

For less than that would require

a ”deflationary” index value, which would have to be lower than this months index reading….

And that ain’t happening…

You forgetting it’s election year Pet?

With all the polls showing POTUS going lower, raising the SS COLA — and bragging on doing so of course — might be one of the few supports the incumbent majority party can claim.

Other times I would heartily agree with your comment, though IMO ”juicing the numbers” is a feature of ALL USA GUVMONEY information and depends hugely on the party in charge and their cronies in the bureaucracies.

VV,

FYI, my millennial and his peers are eagerly awaiting that student loan bailout they were promised. If SS gets an increase that is anywhere near the actual inflation number and the millennials get screwed on the SL bailout…expect them to stay home in droves. That’s what I hear.

I did warn my son to keep paying it down, and mostly he has, but he still expects that “they” are not stupid enough to screw their base. I think they are that stupid.

Petunia,

My guess is that Biden is encountering legal trouble with his student loan thingy. He should. It would effectively be a new tax since the taxpayer would have to pay for it, and he is not authorized to institute a new tax.

Raising the SS COLA? Really? A 5% raise, in a 15% real inflation environment is a huge cut in my mind…..

I don’t know how you can say that. The last Medicare increase for me was $13! Meanwhile my Social Security monthly payment increased by $101. So no, it wasn’t eaten up by Medicare increases.

Medicare went from $148 to $170, a $22 increase, and the deductible went up too. So it wasn’t $13.

I thought my Medicare premium was $157 a month but I guess it wasn’t. Nevertheless even if it went up by $22 that’s still far less than the $101 my monthly payment went up. So no it didn’t ALL get eaten up by Medicare increases.

My Medicare has not gone up at all since I signed up for it.

Was free of current fee, and still is, though quite certain I paid ”tons” into it every pay check or tax return since it was started in 1965.

Maybe y’all talking about something else?

Drugs money, doctor money, something(s) like that?

Those, of course are NOT free and never have been, not to mention all the ”non-medicare covered” stuff.

My wife’s SS increase monthly from 2021 to 2022 was $80. Her Her part B monthly premium increase was 21.60, her deductible increased 3.00 per month, her part D premium actually went down a few shekels. Net net, of around $55 so was not eaten up by Medicare increases. Reason I used her example was she is a bit under the national average monthly SS income. So she took home about 2/3 of the COLA increase. If COLA, which is projected around 9% increase (or more) this year and numbers on Medicare increases are proportionally the same, she would get $86 increase net a month. That won’t even cover monthly grocery/utility cost increases. Inflation is a leaving tire tracks on our back. Ugh!

What effect do big issues (hundreds of billions of dollar’s worth) of IMF Special Drawing Rights (SDRs) have on inflation in the USA? While the Fed is trying to lower inflation, are these “end runs” around those efforts?

Wolf, CPI basis and timeline is used to adjust federal tax brackets?

I’m not sure if they use CPI-U or some other measure (such as CPI-W, GDP deflator, PCE price index…) to adjust the tax bracket and other indexed levels in the tax code.

The IRS uses the average change in CPI-U for the 12 month period of September through August of the year preceding the relevant tax year. After the August CPI is released in September 2022 the IRS will be able to calculate the new brackets and other indexed adjustments for 2023. Usually the IRS releases the inflation adjustments in November.

1) BCD, Bloomberg commodity ETF, is sharply down since June 8.

2) WTIC might osc under 110, before rising to test Mar 7-9 highs.

3) The Fed treat the symptoms, but not the real causes.

4) SPX might rise, before a sudden avalanche.

5) Rent is baked in, but “events” in Europe aren’t.

6) Rolling blackouts might help to fill NG tank, before winter arrive.

We knew this day would come. Bernank…it’s contained.

Soon the average American will be forced to car pool to work, or even more humiliating, take some form of public transportation. Multi-generational housing also coming our way, or hook up utilities for the brother-in-law’s RV in your back yard. My city of 50k in flyover has already relaxed zoning to allow apartments and guest houses in back yards with separate utilities if preferred. Food trucks and recreational cannabis are now also allowed. I can see where this is going. Welcome to the party, pal!

I had already reduced the money I spent eating out, and today I cancelled a music subscription and reduced an art related subscription.

I suspect I will be reducing expenses to only housing and food in the coming months.

I ride the bus, but because of staffing shortages they are running reduced schedules. It may be a fluke, but a couple times this week there was a lot more people on the bus than I usually see, on a couple routes.

Thankfully I don’t own a vehicle, though I do miss it. A bus pass is dirt cheap in comparison to cost of ownership.

The nearby used car places appears to have even less vehicles to sell than a few days ago.

Help wanted signs everywhere.

Luxembourg has ” free bus service ” the government pays for it.

of course its the size of Road island

Fast Forward USA

Woof’s chart > Airline fares, summer special: +34.1%… Not Free

…

Luxembourg’s healthcare system is mainly publicly financed through social health insurance. All employees contribute on average 5.44 percent of gross income / 5.4 percent of $60,000 = (EU ) 3240 that’s $ 3251.11 US

A few rich people own a Lot in Luxembourg’ can’t help wonder why

Luxembourg is a money hideout. I remember around ’06-7 or so, when I first decided to learn a stock from a bond and other things financial, (after a bank guy sorta insulted me for being happy with 5% yearly on my savings) plus bought my very first personal computer, Germany offered a $1M reward for a banker there to get a list of Germans hiding money. Think he delivered about 900 names, a warrant for his arrest is probably still outstanding in Lux, and he moved to Germany.

Why there isn’t more of that action going on is VERY suspicious, indeed.

But but, but…

Speaker of the House Nancy Pelosi responded to another report of decades-high inflation by saying she believes that price increases are “peaking.”

“I think we’re peaking. I think we’re going to be going down from here,”

“I think we’re peaking. I think we’re going to be going down from here,”

I’m glad she has inflation under control now that Joe is out of town…/s

Both political parties in the US are full of idiots, dumb policies from both (and pressure on the Fed) led to this inflationary mess in the USA, and it’s a pipe dream to think that either has policies designed to help working Americans vs their rich donors, leave alone thought through those policies to make them effective. We’re on our own to make it through this.

#1, our political corporations are NOT dumb, WE ARE, nor are their corp/oligarch donors. A good general rule of thumb is Fossil Fuel and Chemical corps/oligarchs own the GOP Corp, while Medical Industrial Insurance Complex and Bank corps/oligarchs own the DEM Corp. And of course the Military Industrial Complex protects all corps/oligarchs, so they get theirs from both “sides”, which makes Tech corps/oligarchs a toss-up depending on their specialty.

Yeah, there are many many many more side games going on, plus the distraction “issues” used to divide the peasants.

But you are right, none of them give a rusty about “main street”…..anywhere.

But they all agree we should keep up this excess consumption game, and of course that the free market will pick the winners, along with our main diety.

I’m a Socialist like IKE was, but unlikely we will ever see his tax schedules again, or his world class public schools, or infrastructure spending, or unions (who used to donate to the DEMs before Ronnie ended that stuff along with anti-trust).

Unilateral class warfare is the game, the “sides”? Meh…….grow up.

It’s like unamused said…..fixing it would be like changing oil at 60mph…..good luck!

And try not to be nasty to people unless you think you really need their money.

Look up slums and check out the worlds 20 biggest….good pictures.

Skeletor always comes through with great wisdom. “Peaking” okay Nancy, whatever.

I hope rural areas relax some of the codes on tiny homes, rvs and park model homes. There need to be more housing choices for people with only a $1000 or $1500 income each month. That means people need to live in something that costs less than $100,000 and no traditional home can be built for that anymore.

There is enough manufacturing capacity to build alternate homes, but not enough areas zoned to receive them. It’s not an ideal situation, but it is better than people living in cars and tents.

Seems that professional & institutional stock holders are sick of the real economy and decided thah they are going to pump the stock regardless of what happens to the rest of us and regardless of coming earning revisions.

Housing prices (but not rent) are cooling off a little bit here in Boston suburbs and I see price reductions of around %10 but from ridiculously inflated asking prices, need to be reduced by %20 and still would be over priced.

Meanwhile my Marcus account still pays only 1.2% while 4 week bills pay over 1.5% and fed fund is 1.6% and heading up.

Stocks down a good amount. I’d say they might be prematurely testing a bottom rather than pumping.

I don’t think we’ve seen real capitulation yet in the markets, except maybe crypto (although in a rational world that would have hit penny stock territory by now). Plenty of room to go down in the US markets when looking at P/E and CAPE.

Stocks are very expensive even if you don’t consider the coming earnings revision, why? because rates are suppose to go up and QT just started add to that threat of a recession…. But if you listen to insiders on TV, you would see how majority of them claim that stocks are cheap(pumping) … Cramer claimed today is/was the bottom!

Cramer also pumped Garrick gold stock @20$ now in 17.50$ range ,he’s a idiot u don’t buy gold in a rising interest rate environment

P/e went from around 37 to 19. Median is 14. So very expensive not that accurate. 37 was very expensive. 19 is just pricey.

Still room to go down though. Often for big declines the pe will go below median.

I don’t believe one should assume earnings revision. Anything is possible.

Yeah the Boston housing bubble is nuts, that’s one of the places where we saw a big increase in homelessness and general economic misery with rents going up to the moon. It’s probably one of those markets that could see price drops of 50 percent or even more like 60 to 80 percent to reach a realistic value. By definition if prices of esp an essential good rise way beyond American incomes, then it’s a bubble by any definition. And those prices must fall hard.

Most TV experts have been saying inflation has peaked for last 4 months and proven wrong every time yet keep claiming its peaked again every month. I think we are staying in a permanent hight inflation situation, maybe 8 or 7% by end of the summer and end up with 6 or 5% if we are lucky by the year’s end.

They’re right you know. Inflation has been peaking every month. And it shows every sign of continuing to peak every month for the foreseeable future.

I should have mentioned that they add its turning down ward after their peak claim…. I though it’s implied in my post.

Una just having fun G, as he frequently does.

Which will create a Sri Lanka scenerio

What does the US have in common with Sri Lanka? The US has food and fuel security and doesn’t borrow in foreign currencies.

So the Fed raises interest rates and inflation goes UP.

Betcha they didn’t see that coming.

‘the Fed is going to meet in late July, and it’s going to talk about services inflation.’

Also about the best country to defect to. Just in case.

To be fair, inflation is bound to rise, what with looming shortages (some of them contrived, some of them due to the planet running out of resources, others due to the usual crappy mismanagement), the entrenched corporate religion of profits over people (and everything else, including their own existence), and the general cultivated atmosphere of philarguria, pleonexia, and chrematiske.

If you’re going to plant potatoes to survive on, and to make vodka as a coping mechanism, you’ll do well to select one of the heat-resistant varieties.

The word ‘philarguria’ is from 1 Timothy 6:10, meaning ‘the love of money’, as in ‘the love of money is the root of all evil’. Probably most of the branches too.

Very fashionable these days.

Maybe peniaphobia is the cause of their philarguria?…

Canada’s housing bubble has been inflating since 2012-ish. I bought a detached bungalow in Toronto in 2008 (at the height of our housing slowdown as buyers digested the US collapse). Now, in 2022, in my neighbourhood comparables now in the $1.3-$1.4M range. I sold in February for $1.7M.

Bog standard suburban SFH’s elsewhere in S. Ontario jumped by 40-50% since 2020.

For a decade housing price increases in BC and S. Ontario has been nuts. Indebtedness among Canadians is at an all time high. Prices are completely detached from fundamentals. The use of Home Equity Lines of Credit to purchase rental housing, pre-con condos, or simply to speculate in a variety of markets, was rampant. Mortgage fraud in certain new Canadian-dominated communities (*cough* Brampton *cough*) is openly advertised in the RE industry. Foreign money laundering in housing is also commonplace.

The Bank of Canada has been front running the Fed since this tightening cycle began, and just raised it’s benchmark rate by 100bps today bringing it to 2.5% (the market gave the probability of a 100bps increase at 48%). The BoC’s monetary policy statement was also decidedly hawkish.

The American housing bubble now, or in 07’-08’ ain’t got nothing on our insanity.

I am fully stocked on popcorn. Next rate announcement in September.

Canadians are *insane* when it comes to housing.

They have no anchor by which to judge prices.

> oh that house is “worth” $2mm because the house next to it is

Median wage means nothing.

They all trust their banking system.

They think BoC sets rates, not the Fed.

They are naive.

Agreed. It was hard to believe that anywhere could be worse than the US housing bubble and dumb Fed policy with loose QE, but Canada and Australia seem to be even worse. As you say, home prices completely disconnected to incomes. That’s basically what happens in a third world country or developing country, whatever the claims otherwise. A lot of corruption and mismanagement, and from our more-and-more frustrated Canadian colleagues, a lot of anger at the way Canadian real estate had basically become a home for massive money laundering for rich corporations, billionaires and foreign capital investors. It’s like the government forgot its main responsibility is to the Canadian people, not to the rich plutocrats. (And by that I mean all parties, just like the Democrats and Republicans in the USA, Canadian parties are just two sides of the same useless coin)

The funniest thing about Canada is that it’s the worst place to do it.

Small currency where you can’t set rates independent of the Fed and therefore can’t control it? Check.

Small population and fairly average cities that can’t attract the ultra rich? Check.

Vast landmass that dwarfs small population? Check.

Canadian Establishment: I’ve got an idea, let’s run a land pyramid scheme!

This year I watched the pre election debate. Wow. That is one low, low standard of politicians you have. Every single person on that stage would sink without a trace in most European countries, intellect wise.

I think you just have a really low IQ establishment who tried to run a land pyramid scheme in a huge, huge country. Not smart.

Oh, we’re going to plumb further depths where Canadian political leadership is concerned, georgist. The Conservative Party of Canada is almost sure to elect Pierre Poilievre as its leader in September. Among other “real men of genius” ideas he has espoused is the use of cryptocurrency to avoid the effects of inflation …

Greed is NOT good ?? ;-)

Not if you don’t get any. Or, more to the point, me.

I want either less corruption or more opportunity to participate in it.

Is there a collectables market for Wolfstreet beer mugs? If I have Sotheby’s put one up for auction I’d like to give them an asking price.

We were asking $500 for a pair a while ago una, with the cash to be sent to support Wolfstreet.

Didn’t see any offers/bids.

I would like to make a market starting at $250 but I can’t get my hands on any.

They’re just priceless :-]

unamused: “I want either less corruption or more opportunity to participate in it. ”

—

Methinks that is not how corruption(avarice) works. Wouldn’t selfless sharing ruing that particular vice?

Unrelated story:

So I stopped by the Capital Building and asked security where the Investment Club was meeting and he called his sup and handed me the phone. The guy almost whispered who do you know? I said plainly I read the Wolf Street blog and message board. Sometimes. There was pause followed by a longer pause which made me uncomfortable and so I just hung up and left. I figured that with all those members of congress there probably wasn’t any more seats available and I didn’t want to press and embarrass the guy.

I’ll try the Federal Reserve next week. I mean they must have room for one more, right?

I wonder if Wolf , being the reigning king of statistics , would consider

calculating for us the inflation we are experiencing in terms of the Volcker CPI calculations ?

Why tie ourselves to a fraudulent calculation designed to deceive us ?

We should be able to view the current level of inflation with some degree

of honesty. Without hedonic insults. ( per Volcker stats, we’re probably over 15%).

Mark,

I’ll just say this: you cannot compare a smartphone of today to the telephone in 1980. When you’re buying a smartphone today, you’re buying more than a super-computer in 1980. You’re paying $400 for something that didn’t even exist in 1980, and the closest thing to it that did exist cost $40 million. Hedonic quality adjustments are used to deal with these technical improvements of everyday stuff. People who ignore this are pulling a bag over their heads.

And don’t forget about life-saving vaccines for $40 or anti-virals for $500 as opposed to $50K hospital bills and/or death …..

Except that nobody does big data analysis on a smartphone, much less supercomputer applications. You can’t even do video processing on a smartphone. If I need a supercomputer I’ll uncrate the Cray in the dungeon and brush up on my Fortran.

My Western Electric Trimline works just fine. No annoying texts and it doesn’t spy on me (illegal in all civilized countries but Big Business SOP in the US).

I also don’t need a weapons-grade SUV with high-end entertainment center standard to schlep children to their soccer losses three counties away.

In fact, the world is full of things I do not want, do not need, and have no intention of wasting my shekels on.

Immunity to diseases spread by corporate marketing weasels requires no booster shots.

I get your point and a lot of the improvements don’t seem to add much value, but, for the Cray data crunching just keep this in mind:

The Cray 1 could at its peak achieve 160 MFLOPS at its peak, using all its hardware

The iPhone 12, can deliver 11 TFLOPS (11,000 MFLOPS, just using is ML cores, not including that it has many more cores for other tasks including 6 CPU cores and 4 GPU cores, which can be used to perform many more tasks.

So the improvements in computer tech are actually mind blowing.

‘So the improvements in computer tech are actually mind blowing.’

So it’s smarter than you. Should I be impressed? Keep an eye on it in case it decides to get a new model after figuring out you’re obsolete. In the meantime you might want to cancel your credit cards.

My brokerage app on my phone allows me to do big data analysis along with reading Wolfstreet!

Fair point, but hedonic adjustments don’t help for cars. Who cares if the $40k car I buy today has a lot more gadgets than the $20k car of yesteryear? I can’t buy a “basic” car equivalent to the one from the past, so if I want a car at all, I HAVE to buy all of those improvements, which I might not need nor want.

Einhal,

I certainly would never ever want to drive the deathtraps I drove in 1980 – not even my gorgeous turbo-charged modified 280Z. I love the new vehicles, the stuff we take for granted now, such as the backup camera that keeps you from running over your dog (my friend did that 20 years ago, horrible!), the safety features, the comfort, the quiet, the handling, the fuel economy, a million things. The improvements since 1980 are just about immeasurable.

That said, I prefer to walk, and so we moved to San Francisco. Walking is the best solution of all, because I’m easily good for 8 miles out and back, which takes me just about anywhere I need to go, it’s beautiful and healthy, and the weather is nearly always good for walking. We now only have one car (for my wife to drive to work), which cuts all car-related costs in half.

Wolf, with safety features, I agree with you 100%. I wrote to my Congressmen many years ago to say that backup cameras should have been required, as it would lower the prices, much like airbags. But I’m talking about heated seats, luxury sound systems, seats moving on the motors, and things like that. I don’t want those things, but I usually find that I can’t get the safety features outside of “packages” that include some crap too.

But in any case, it’s unfair for the government to say that because cars are safer now, the prices have really dropped (if that’s what hedonics do, I can’t say I’m an expert on it). People still have to buy what’s available on the market.

“But I’m talking about heated seats, luxury sound systems, seats moving on the motors, and things like that.”

OK, now you’re arguing with the wife, who’s the boss in here. She loves those heated seats, uses the seat motors all the time because she takes power naps at lunch and adjusts the seat to do that, and she loves the sound system, and the stuff in the dashboard that I never use. Those automakers got their customers hooked!

More seriously: you are putting your finger on a different issue: a lot of things have gone upscale and people can’t afford them anymore, but the lower-cost alternatives have disappeared — or in cars, the lower-cost alternatives are these upscale cars when they’re a few years old. There is an academic distinction between “costs of living” and “inflation.” What you’re correctly lambasting is that the cost of living has shot up. And I totally agree with you.

@Wolf,

Of course you are 100% correct in describing all the good features of modern cars. On the rational level, no discussion.

However, I *hate* modern cars with a vengeance. It’s an emotion thing. When I drive, I want to feel connected to the machine, not isolated from it by layer upon layer of software, chips, controllers, aides, features and G knows what.

And don’t get me started on the repair costs of modern vehicles. Yes they are reliable and normally do require much less maintenance than old cars. But if you are unlucky enough that your car develops some electronic gremlin that no mechanic can solve except by trying to replace every electronic component in some trial-and-error process, get ready for some serious bills. And if it ever ends up getting damaged, the horrors will start for real. Replacing bumpers full of sensors, repairing bodywork made of exotic ultra-thin steel, replacing headlights and grilles full of cameras, exchanging parts that all have their own obscure chips in them, getting wiring looms back in order, it’s almost impossible to get right and will cost a fortune. Insurance companies already grok this and adjust their premiums accordingly.

So, I am trying to make my 2000 Land Cruiser last forever, and drive my 1965 Mustang whenever possible. And if you no longer drive that 280Z and it’s in your way, I’ll be glad to take it off your hands :-)

Jos Oskam,

Sorry about the 280Z. It’s gone. Sold it over 20 years ago. I spent a gazillion hours modifying the engine (turbo), the suspension, and the body (G-nose, flares, whale tale, side vents behind the front wheels, extra set of hood vents…) I loved that car, but it was time to move on, get married to the boss, and drive reasonable vehicles where you could put a suitcase in the trunk.

Wowsers Wolf. This must be the nicest 280Z I have ever seen. I’m getting more and more impressed by the breadth of your skills :-)

I think I read somewhere that Larry Summers and some of his students had done the opposite calculation i.e. estimated peak 70s inflation using today’s CPI formula – the main difference being the replacement of house prices with OER in the early 80s. IIRC, they said peak 70s inflation was about 9% using today’s CPI but they felt that Volker style 20% FFR would not be needed because of QT which can be significantly accelerated and because the “neutral” FFR is lower than in the 70s.

The CPI-W may go north of 10% in the 3rd quarter? I don’t know what the largest increase in Social Security benefits has ever been but can this country afford 10% in one year?

Brant Lee :Defense will proabaly get an increase of 20% in its next appropriation over the last. Does the DOD or the MIC ask Congress if the Empire can afford it? F$&k no. I Hope we get the 10%. You can give me yours if you feel guilty. I damn sure do not. Did you see the BLS $56.90 handle on the loss of buying power of a $100 since 2000 chart in the article? The way I look at it at this stage our Empire and its Fiat Dollar is that there is still $56.90 left out of the $100. I want every f$&King penny I can get before we hit $0. The sound money ship sailed a long time ago.

DD,

I Friend & Like you on WS.

So true. No, I’m not griping about a 10% raise.

But the Social Security fund is a good example of how this runaway inflation is going to destroy it in just a few years, not decades. What you say is right, the government allowing the Fed (Bankers) to change and control policy for the benefit of a few (while no one was paying attention) brings us to this point. Bankers have no mercy.

Wolf makes a good case that services will take over as the driver of inflation in the near term, undermining the case some in Wall Street are pushing of the inflation turning a corner, so Fed may back off soon narrative. Housing and food really aren’t discretionary. I do expect people to start cutting more discretionary service spending (restaurants and amusement), if they haven’t already. But that’s rather marginal.

I’ve read some media stories on rents and repos that give me some doubt, but nothing I’d say is reliable enough to cite to and it read more anecdotal. I got no crystal ball, that’s for sure.

Since food inflation might be driven by UKR war, and if Wolf is right that high rents are inevitable, I don’t see a way Fed can navigate without raising rates and QT to force a recession and/or popping the housing bubble. Hands seem tied with what happened to housing prices. Time will tell.

Yes – JPow has started talking about a housing “reset”.

If he persists with this term over time I would assume he is telegraphing a massive acceleration of QT specifically targeting MBS to drive mortgage rates up to 7-9% and gently deflate the housing bubble.

Mortgage rates at 7-95% would deflate the housing bubble all right, but it sure wouldn’t be “gentle.”

I liked his use of the word “reset” for housing, but he followed that by suggesting that mortgage rates would be low again (or something like that). It concerns me that he said that part. I wonder if he still thinks this is all tansitory (whatever that means).

So long as J-Pow isn’t referring to a “Great Reset” I’m okay with it.

Nate,

My son’s friend was offered a job in Austin, TX and looked at rents. An average house near the job was $5900 a month. My son asked me how much his friend would need to make to afford the rent. I told him landlords typically want 3X the rent as gross income, but in Florida I had been asked for 5X for an apartment.

We rounded up for simplicity $6K x 12 = $72K for rent after taxes. If you keep rent at 33% of expenses which is what is recommended. His friend would need to make $218K per year to work and rent in Austin. Highly unlikely.

Yeah Austin’s gotten bad but I didn’t know that it was that ridiculous. Another example of how the Everything Bubble has made the Asset Class go completely bonkers with their price-setting, detached from reality. Prices have to be in line with incomes. When they get that high (even worse in California, New York and New England from what we’ve seen), esp in a housing bubble like this, prices need to fall hard.

Unlikely far damn shore Pet, but possible.

Friends of the spouse went directly from college to work in tech in CA for $150K — in 1981!!!

Another, younger, friend who does some ”high end remodeling” work in Tahoe and Kauai tells me some electricians in those places are getting $150 per hour these days, and charge ”portal to portal.” Some folks are getting that along with temporary housing and transportation to the area if reports are true…

IOW, with our entertainers of all stripes, political, sporties, actual performing artists, frequently getting millions or dozens of millions of USD per year these days, $218K just ain’t what it used to be!!!

$218K a year? Pssss….that’s my annual Grey Poupon budget.

I’m waiting for the pain. Hoping to see some blood in ’23 but conceding it may not be until ’24. Patience.

May 1980 i moved into a one bedroom by the pool on North Lamar near Research Blvd. $225/mo. Summer ’81 a private room with all meals at Deutsches Haus co-op a block from UT Austin was $265/mo. And Hippie hollow and mount bonnell and Hamilton’s pool were uncrowded and safe. And the homeless were called “musicians”, and you tipped the bass player for your pizza. Those were the days.

1) Inflation shortening of the thrust :

2) In May 31 2020 inflation dropped to a higher low at 0.10%.

3) From the next low in Nov 30 2020 it increase 4.20% from 1.20%

5.40% in June 30 2021, breaching 2.90% the previous high in June 30 2018 high. 4.20% was the biggest jump.

6) From the next low it was up 3.20% from 5.30% in Aug 31 2021 to

8.50% in Mar 31 2022.

7) Since the last low in Apr 30 2022 inflation is up from 8.30% to today

high.

8) We don’t know how far it will go, but today rise is a thud.

9) Inflation is losing momentum.

Yes, the acceleration of inflation is decreasing.

The question is: Will it keep accelerating into outer space, go into a stable orbit, or plummet to the ground with a recession.

Stay tuned for next quarter.

Rate hikes are working, but due to mass, lag effects prevent immediate results.

Unlike a satellite launch where results are known in minutes, the controlling the economy is more difficult than trying to turn the Titanic with tiny propellers.