Total liabilities dropped by $344 billion since QT began. Big shifts between liabilities: reserves already plunged by $1.12 trillion.

By Wolf Richter for WOLF STREET.

We generally discuss the Fed’s assets on its balance sheet: Treasury securities, MBS, repos, etc. But today, we’re going to look at the four major liabilities on the Fed’s balance sheet. On every balance sheet, total assets = total liabilities + capital (the Fed’s capital is limited by Congress, currently $42 billion).

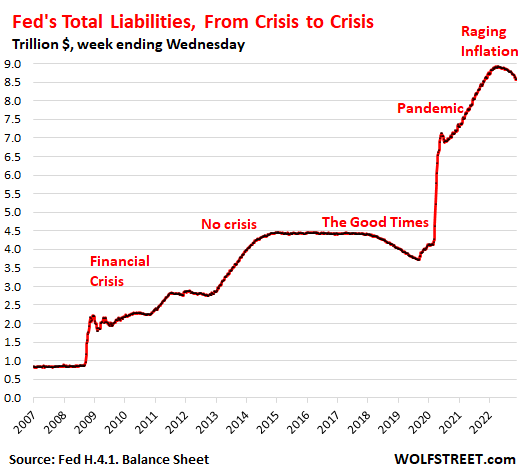

Total liabilities dropped to $8.58 trillion, according to the Fed’s weekly balance sheet released a day later than normal, on Friday, due to Thanksgiving. This was down by $344 billion from the peak on April 13, 2022, and the lowest since November 3, 2021. Total liabilities mirror the Fed’s total assets (minus $42 billion in capital).

But there are big shifts in the composition of those liabilities, which is what we’re going to look at in a moment, involving banks, Treasury money market funds, the amazingly record-popular US paper dollars, and the government’s checking account:

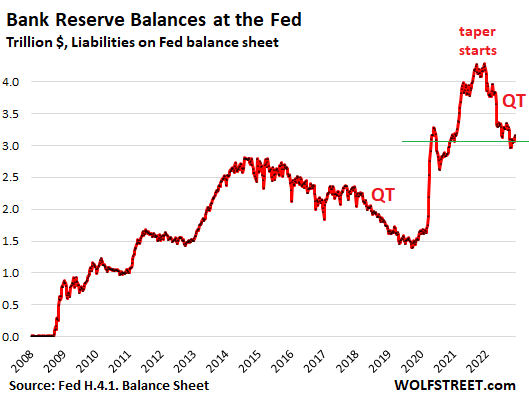

Reserves plunged by $1.12 trillion since December 2021.

Reserve balances – cash that banks put on deposit at the Fed to earn interest, similar to a big savings account – plunged by $1.12 trillion from the peak in December 2021. Late 2021 was when the Fed began “tapering” its QE asset purchases, and QE ended in March 2022.

Banks use their reserve accounts at the Fed to transfer money between banks and to do business with the Fed, such as selling securities to the Fed under QE. Reserves are a liability on the Fed’s balance sheet; they’re money that the Fed owes the banks.

Reserves are the most liquid, risk-free interest-paying asset banks can invest in, and they also figure into the banks’ regulatory capital.

The Fed, as of the last FOMC meeting, pays the banks 3.9% interest on reserves. Alternatively, banks can invest their excess cash by buying Treasury securities, and they’re doing that. The one-month Treasury yield is currently 4.16%, but these securities are less liquid than reserves; they have to be sold in order to be turned into cash, while reserve accounts are like a savings account that banks can just draw on.

The banks, on their own balance sheets, don’t call these reserves “reserves.” That’s a Fed term. Banks carry them as assets and call them “interest-earning deposits,” “interest-earning cash” or similar.

Reserves are a manifestation of liquidity in the banking system that is not chasing after other assets.

QT is draining liquidity from the financial system, and one of the places where the liquidity drain shows up is in reserves.

But the $1.12-trillion plunge in reserves is far larger than the $344 billion decline in the Fed’s overall assets and liabilities under QT. This means that banks are now chasing after other options that are paying higher yields than reserves, and these options include Treasury securities.

Reserves, bank deposits, and competition for cash (which is no longer trash).

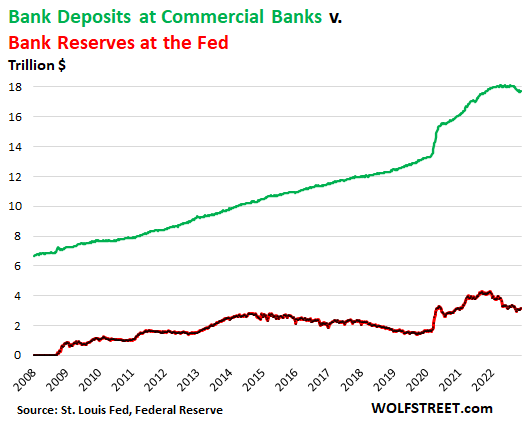

This bank-cash put on deposit at the Fed represents only a small portion of the cash that the banks received from their customers’ deposits. [For banks, a customer deposit is two things on its books: the amount owed the customer (a liability); and the amount in cash received from the customer (an asset). To earn income with this cash, a bank buys securities, or puts the cash on deposit at the Fed, or makes loans, etc. It also has to keep some on hand to process transactions, meet withdrawals, etc.]

Total deposits (the liability) at all US commercial banks dropped by $433 billion from the peak in April 2021, to $17.7 trillion. In other words, customers lent banks $17.7 trillion in cash, via savings products and transaction accounts, such as individual and business checking accounts, corporate payroll accounts, and corporate accounts that suddenly and briefly swell with cash when major transactions take place, such as the purchase of a company involving billions of dollars in cash.

But customers are now finding better use for some of their cash than depositing it at the bank and earning nearly no yield, while for example shorter-term Treasury securities now pay over 4%, and so they’ve pulled $433 billion in cash out of banks since April.

Banks have begun to fight back to stop this cash drain, and they now offer CDs – usually brokered CDs that you can buy only through your broker, not a the bank itself – of 4% and more. Some savings accounts are now at 3% or higher – a sign that there is now finally some competition for cash as the era of free money has ended and cash is suddenly no longer trash but in demand.

This chart shows total deposits at all commercial banks (green) and the portion of the cash from those deposits that banks put on deposit at the Fed, which the Fed calls “reserves” (red):

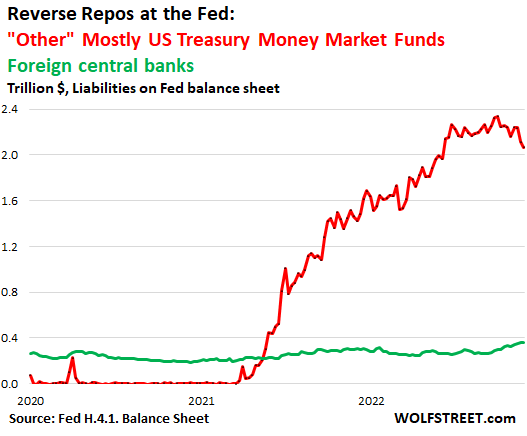

Overnight Reverse Repurchase agreements.

The Fed currently pays 3.8% on what it calls overnight “reverse repurchase agreements” (RRPs). Under these RRPs, the Fed takes in cash and hands out collateral (Treasury securities). RRPs are a liability for the Fed because it’s cash the Fed owes its counterparties.

The Fed offers RRPs to two groups: foreign official accounts, where other central banks park their dollar cash; and “other” accounts, mostly US Treasury Money Market funds. The total balance of both combined dropped by $208 billion from the peak in April, to $2.43 trillion.

But wait…

Foreign official RRPs shot up by between $60 billion and $80 billion from the range early this year, to $361 billion, which was, along with the prior week, the highest ever.

“Other” overnight RRPs dropped by $269 billion from the peak in September, to $2.03 trillion, the lowest since June. This means that Treasury money market funds have less need to park excess cash at the Fed:

Starting in the spring 2021, Treasury money market funds got flooded with cash. They normally buy Treasury securities with short maturities, but demand was so high that short-term yields dropped briefly below 0% in early 2021, which could have caused money market funds to “break the buck,” where a unit’s value drops below $1, which could trigger a run on the fund, and contagion could spread from there, which is why the Fed started offering RRPs, and then started paying interest on them.

And earlier this year, when the Fed started raising rates, but banks still paid near 0% on deposits, Treasury money market funds started to shift their short-term cash on hand from their bank accounts to RRPs, because the Fed pays higher interest than the banks.

So…

- Reserves, as we’ve seen above, peaked in December 2021.

- “Other” RRPs seem to have peaked in September 2022.

- RRPs with central banks, though relatively small, have surged to a record.

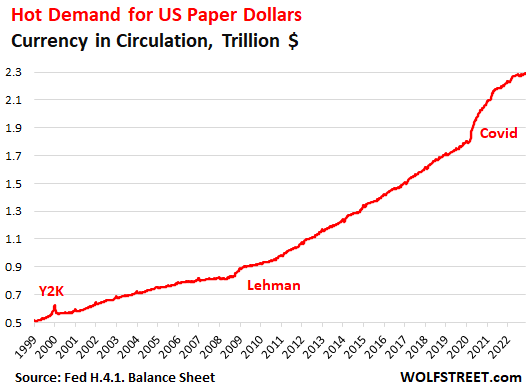

The beloved Paper Dollars.

Currency in circulation – the paper dollars in wallets and under mattresses – is demand-based through the US banking system. If customers demand paper dollars at the ATM or at the counter, the bank must have enough on hand. Foreign banks have relationships with US banks to get dollars for their customers.

Banks get those paper dollars from the Fed in exchange for collateral, such as Treasury securities, which are assets for the Fed.

Officially called “Federal Reserve Notes,” they’re a liability for the Fed, essentially money it borrows from the holders.

Before QE, currency in circulation was the primary driver of the increase in assets on the Fed’s balance sheet through the collateral that banks have to post to get FRNs.

And demand has been huge – but not for payment purposes, for which demand is declining. Paper dollars are stashed around the world for legal and illegal purposes, and when there is fear of a crisis, demand surges.

Currency in circulation spiked throughout the pandemic and now reached a new record of $2.29 trillion, up by $501 billion from pre-pandemic February 2020:

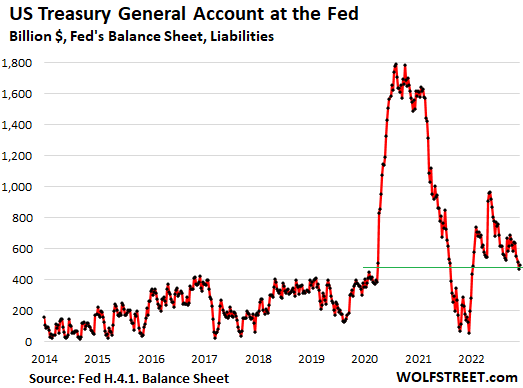

The Treasury General Account.

The government’s checking account is at the Federal Reserve Bank of New York. The amount that the government has in the Treasury General Account (TGA) is money the Fed owes the government, and is a liability for the Fed.

The balance has been swinging majestically, from lows during debt-ceiling fights when the government nearly runs out of cash, to the high in July 2020, after the government raised gigantic amounts of cash through gigantic debt issuance to pay for the stimulus programs.

Inflation also has an impact over the years: it drives up outlays, and the larger outflows require larger balances to avoid running out of cash on particular days.

The TGA balance ticked up a tad to $493 billion, from the prior week, which at $472 billion, had been the lowest since January 2022. Account balances are now in the process of normalizing after the craziness starting in the spring of 2020:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Appears it may be time to begin laddering CDs for the run up.

Once the lockdown in China ends oil and gasoline prices will shoot back up pushing inflation back up. The shorts will run for the hills. This will push interest rates higher as gasoline is a major component in the CPI.

Fed is busy protecting its Precious (financial economy and asset bubbles) as the real economy (production, not consumption) has been dying!

I would consider this QT real that can control inflation when:

1. Real interest rates are positive.

2. Fed starts selling treasuries and MBS outright at same rates at which ot bought them!

The lockdown in China may end in revolution or an even tighter lockdown.

As Mel Brooks said – “the peasants are revolting”

Nov 28 (Reuters) – The Federal Reserve needs to raise interest rates quite a bit further and then hold them there throughout next year and into 2024 to gain control of inflation and bring it back down toward the U.S. central bank’s 2% goal, St. Louis Fed President James Bullard said on Monday.

“We’ve got a ways to go to get restrictive,” Bullard said in an interview with MarketWatch, as he restated his conviction that the Fed’s target policy rate needs to rise to at least a range between 5.00% and 5.25% from the current level of 3.75%-4.00% to be “sufficiently restrictive” to reduce inflation.

Once at a high enough level, rates would then “have to stay there all during 2023 and into 2024” given the historical behavior of inflation, Bullard said.

https://www.reuters.com/markets/us/fed-has-a-ways-go-interest-rate-hikes-bullard-says-2022-11-28/

“This means that banks are now chasing after other options that are paying higher yields than reserves, and these options include Treasury securities.”

Deposits at commercial banks have fallen by $400 billion, I’m guessing because customers are finding better returns elsewhere?

Yes, as I explained in detail in the article.

If Banks were really buying the treasuries that central banks and foreign pension funds are dumping, why is Yellen complaining about liquidity in the Treasury market?

Why are central banks around the world hoarding gold?

1. Gold is always being “hoarded.” That’s what it’s for. What else are you going to do with it??? Industrial use is small. Gold is not a consumption item.

2. Treasury yields are still very low, 10-year yield under 4%, with 7-8% inflation, which means there is HUGE demand for Treasuries, and everyone is buying them.

3. What Yellen is talking about is the since-forever-well-known difficulty of trading long-term Treasuries that were issued years ago. That has always been the case. If you ever tried to sell a 30-year Treasury that has 15 years left, you’ll know. Your broker will drum up a bid, but the price will be below what the market index says. Only newly issued Treasuries trade easily. Bonds don’t trade like stocks. That’s just how it is.

Many bonds don’t ever trade, as investors buy them at auction and hold them to maturity, collect coupon interest along the way, and get face value when they mature. That’s how I do it. The bonds I buy never ever trade. Insurers, pension funds, etc. do the same thing.

There are now efforts underway to rethink how bonds are being traded, and they include centralized clearing for Treasuries, which would be a good thing, and should have been done years ago. What Yellen is talking about is an idea that has also been kicked around for a long time, but is difficult to implement, which is why it hasn’t been done yet. There are other efforts under way to bring the Treasury market into the 21st century, so to speak.

Applause for Operation Un-Twist if thats what she’s hinting is necessary to break the log jam.

Get Creative!!

Hi Wolf, I have a dumb question. When companies, investment firms and banks hold treasuries, corporate bonds, etc. Are they required to mark to market the bond value vs the face value? Any other words, do they take the loss on income statement to reflect the balance sheet writedown?

Trying to understand the reporting requirements for price to earnings impact. Do earnings reflect the impact of higher interest rates on bond and a lower value on the bond?

I’m going to address bank accounting. I’m not 100% sure if it’s the same for non-bank entities. A bank has two ways to account for securities: those that it holds for sale and that it might sell some day; and those that it will not sell but will hold till maturity.

Securities that it holds for sale must be marked to market on the financial statement. So if these bond prices fall, the bank will reduce the value of those securities on its balance sheet, and it will make a loss entry on its income statement.

Securities not held for sale are not marked to market. The bank just waits until the bonds mature, collects interest along the way, and then gets face value in cash when the bond matures.

Since the Fed doesn’t hold its Treasury securities for sale, it doesn’t mark them to market. It collects interest along the way and collects face value when they mature.

By “Centralized Clearing” I assume you mean letting the Treasury operate it’s own Treasury Bond exchange, as opposed to the CBOE, and others.

It’s the public’s debt, why should the public rake in the profits from running a place to trade it?

I can just see that Bond trader at CBOE who worked for CNBC throwing another shit fit (which was given credit for starting that “tea party” idiocy) about creeping socialism….when just the opposite is now going on, as the corporations and PE are now truly “enthroned” as Lincoln feared. The simple proof is ridiculously insane wealth inequality. Most other human phenomena follow a bell shaped curve, why not wealth?

Anyway, they have plenty of other things to “trade” (gamble with) and profit from the hefty and likely unfair transaction fees.

meant “why shouldn’t”…..

And as I’ve mention before, there are a lot of kids running around with various financial, admin, and legal degrees to fill positions.

And contrary to the opinion of many deceived souls here, they don’t become instantly ( or slowly) incompetent and lazy when they enter Gov’t service.

I worked half over my life in private industry, and the last 17 years at the Post Office. People are different the the same way everywhere, which most of these one-trick, one-career ponys here will never get…..talk about living barren, limited stimulus, lives.

Never had a chance to go do much Recon, as 91B20 would say, and therefore lack good SITUATIONAL AWARENESS…..aka, intelligence.

The responses to your article show that understanding QT in terms of fed assets and liabilities is not easy for non- accountants.

QE during covid created cash by printing money (for gov spending) whilst giving the fed a load of securities at the same time (to balance the money printed, as though the fed had purchased those securities). Prior to that (2008) money was printed to recapitalize banks in exchange for bonds and mbs.

To EFFECTIVELY reverse QE one has to exchange the securities held by the fed for cash AND retire that cash. The cash needs to be destroyed -taken out of circulation. Anything else, like allowing the bonds to run-off at their natural expiry, will not reduce the total amount of currency (expanded by QE).

To combat inflation the total amount of currency will have to be reduced. Increasing interest rates just encourages less cash to be spent. Using that tool on its own may not be effective in reducing the amount of cash that is chasing assets. It certainly will not compensate me for the loss in value of my savings when the extra cash was printed during QE.

What I would like to know is whether the total USD currency on the planet has been reduced by QT, and by how much.

This discussion of QT destroying money doesn’t go into an article on the Fed’s liabilities, but in the articles on the Fed’s assets.

I spell this out in every article on the FED’s ASSETS, and all my regular readers know this. The Fed doesn’t have a cash account. Every time a security matures and the Fed gets paid cash for it, and every time the Fed receives the cash from the pass-through principal payments from MBS securities, the Fed destroys this cash. But this discussion goes into the articles on the Fed’s assets.

Here is the last one on the Fed’s assets (QT). Go down to the section with the heading, “QT is the opposite of QE”

https://wolfstreet.com/2022/11/03/feds-balance-sheet-drops-by-289-billion-from-peak-november-update-on-quantitative-tightening/

“….not easy for non-accountants….”

That’s a HUGE understatement. While I LOVE learning, I kept a free tutorial on Double Entry Accounting on my cluttered desk top and tried to start learning it several times before I realized I was never going to study it and deleted it to make space for other interests.

But the way things are presented here, I have a good picture of how the FED works, the flow of assets vs paper fiat currency, although it’s in my own mental shorthand and I could never explain it to anyone, and have to have it constantly refreshed, anyway. Who’s point of view is hugely important in all accounting and financial stuff, and is often taken as a given by those who understand it better.

How does one know that, when a gov bond on the fed balance sheet expires, the fed receives cash for the bond and then retires that cash?

Presumably the cash it receives is either derived from tax the gov collects, or cash from newly issued gov bonds. Is there a separate published record of cash that the fed destroys, or are the public just expected to believe that it has been destroyed because the balance sheet has been reduced? Thanks for your help.

The website is very educational for retail investors trying to understand gov financing.

All transactions involving Treasury securities (coupon interest, payoffs) are official government records and market records. Each Treasury security is tracked by its CUSIP number.

In terms of the Fed’s balance sheet, you can get the detail by CUSIP number, amounts, and maturity dates here (click on the type of security you want to look at, such as “T-bills”):

https://www.newyorkfed.org/markets/soma-holdings

One paragraph down. First time I haven’t read the whole article before commenting, so of course I got bit. :-)

Domestic demand for treasuries is different from foreign demand. The latter allows the US to print dollars, but EXPORT the attendant inflation.

Now that foreign central banks are dumping US treasuries and hoarding gold, I wonder whether Powell can tame inflation with only interest rate hikes. Only actual mop-up of excess liquidity, through asset sales(and retiring the dollars earned), will tame inflation.

Linkz said: “The latter allows the US to print dollars, but EXPORT the attendant inflation.”

—————————————————-

This is stated all the time, but I must question it.

1. The US does not need foreign demand for dollars in order to print dollars.

2. How would foreign demand for treasuries export inflation?

Whatever taming inflation means. It has already happened and has been baked in the cake. That’s what creating Trillions of dollars does.

So the bottomline is that, despite the Fed’s QT, the actual amount of money in useful circulation has *increased* in the past few months. Because money parked in Bank reserves and in reverse repos are basically stealth QT, and when those unwind, that’s money taken out of the Fed and placed back into circulation.

This why I believe that we won’t really see the effects of tightening until the Fed mops up perhaps $2tril: $1tril to eliminate excess bank reserves, and $1tril to at least make a dent in the reverse repo market. And we may not see real effects until the entire reverse repo market (except for central banks) is unwound, which would imply a minimum of $3tril in QT.

While I think the Fed is on the right track, I think their moves are increasingly unbalanced: they’ve been very aggressive about raising the FFR, but not nearly aggressive enough with QT. As a result, interest rates have risen but the net effective money supply has actually expanded. Which has led to effects like a flat and sometimes inverted yield curve.

The other factor to consider is that the Federal deficit is declining rapidly. This means a lower supply of new treasuries, which also boosts prices and lowers yields. While there’s plenty of private debt that buyers could buy, a trillion dollar decrease in government issued debt is nothing to sneeze at and also counteracts the effects of QT.

What the Fed should do is accelerate QT, perhaps with a one-time drawdown of $500bil and an increase in the monthly limit, and rely less on further interest rate hikes. Interest rates alone won’t solve inflation or asset bubbles as long as the money supply remains loose as cash from excessive reserves and RRPs compensate for whatever the Fed sheds.

Lune,

“So the bottomline is that, despite the Fed’s QT, the actual amount of money in useful circulation has *increased* in the past few months.”

You COMPLETELY misread this and turned it into the opposite. Give it another shot. Including the first paragraph, which is very important (on a balance sheet, assets = liabilities + capital).

Which means, when assets go down, liabilities MUST go down by the same amount.

QT removes liquidity — and that’s WHY liabilities (RRPs, reserves) go down... it’s a sign of reduced liquidity (effect of QT).

As QT progresses and liquidity vanishes, RRPs and reserves will go down further as a result, and by a lot. RRPs and reserves are signs of excess liquidity. The declines in RRPs and reserves shows you how QT is working; they show some of the effects of QT.

Wolf, I could be wrong but I think Lune may have been referring to this paragraph: “But the $1.12-trillion plunge in reserves is far larger than the $344 billion decline in the Fed’s overall assets and liabilities under QT. This means that banks are now chasing after other options that are paying higher yields than reserves, and these options include Treasury securities.” Couldn’t you think of that extra $776B plunge in reserves as being put back in circulation therefore being a one-time QE-like injection in the economy? Or is that not the right way to think about it? If that entire $776B went to buying treasuries it might be neutral but some of that cash could have gone to house purchases or other investments no?

SWE Josh,

This is all twisted.

QT is removing liquidity — and you can see that liquidity-drain in the decline in reserves and RRPs. And they will continue to decline as QT progresses.

People have got to get a grip on this.

SWE Josh-

That’s exactly what I was getting at.

Wolf, I’m sorry if I’m misunderstanding this. Here’s a simplified model of what (I think) is happening, and please tell me if/where I’m wrong:

Pre-2007 (i.e. before the Fed did QE/QT/etc): the government would issue say $1tril in treasury bonds. These would be bought by private players, giving the govt. money to spend. This was basically balanced, because the private players would have to sell assets like stocks, other bonds, houses, or maybe not buy goods and services, in order to buy the treasury bonds. But this extraction of money from the real economy would be balanced out by the govt taking the $1 tril in cash and spending it on medicare / SS / defense / govt. employees / etc. basically recirculating the money back into the private economy. So it’s a wash in terms of money supply.

Now we get to the Fed engaging in QE. The govt sells $3T in treasuries. But instead of the private market buying it, the Fed buys it. Now, the private market doesn’t have to sell their assets, curtail their spending, etc. *and* the government will now be buying $3T of goods, services, and assets, thus goosing the private economy. That’s why demand explodes, assets rocket higher, etc. The money the govt is spending into the economy is not balanced by money being taken out of the economy (by either taxes or borrowing). Instead, the Fed is “giving” the govt “free money” and holding the treasuries on its balance sheet.

Now for QT, the process reverses: in order to redeem the $3T that the Fed has on its balance sheet, the government issues $3T in new treasuries, which are purchased by the private market. But that new cash doesn’t go to buying stuff from the private economy; it goes to paying back the Fed, which promptly zeros out the cash. Thus, the private economy sells assets, curtails spending, etc. to purchase $3T in treasuries, but that money doesn’t get recirculated into the economy, causing demand to fall, assets to fall, etc.

I think so far, you would agree with this picture? So here is where the confusion comes from. The govt issues $3T in treasuries, which the Fed promptly buys. This is nominally $3T in QE. The govt releases this money into the economy. $1T of it ends up with banks. Normally banks would use that $1T in assets to lend out $10T in loans to companies, mortgages, car loans, etc. But here, the banks take that $1T and park it with the Fed, as excessive reserves. They don’t make loans, or buy assets in the real economy. And here’s my point: because of this, while the Fed has bought $3T in treasuries, because $1T is parked back with the Fed rather than underwriting new loans, the Fed’s *effective* QE is only $2T worth.

Now, when it’s time to reverse effect, let’s say the Fed lets $1T runoff its balance sheet. So the govt issues $1T in new debt, and uses the cash to pay back the Fed. That’s $1T in QT, leaving $2T of QE still in circulation. But… the banks withdraw the $1T in excess cash and start making loans with it, and buying assets. So the $1T that the govt drained by issuing new bonds, is offset by the $1T in excess reserves that the banks are now putting in play. So the *effective* QT remains $2T.

That’s why I’m saying that while you’re right about the headline, nominal amount of treasuries the Fed is rolling off its balance sheet, in terms of the actual effects the QE/QT had on the real economy, you have to subtract out the excess reserves and reverse repos.

What does this mean in the real world, outside of my thought experiment? I agree that the nominal amount of QE is $9T and this is being reduced. But my point is that all the asset bubbles and demand blowouts we are seeing, is the result of much less *effective* QE than we thought. The Fed may have bought $9T of treasuries, but if banks’ excess reserves are $4T and reverse repos are $2.4T, then we got the S&P hitting 4K with only $2.6T of “effective” QE. We can only wonder where we would be if the full force of the $9T was unleashed! :-)

And now that the Fed is reversing, it has withdrawn $300bil, for a nominal QE of $8.56. But if bank excess reserves are down to $3T, then the “effective” QE (i.e. cash in circulation powering the real economy) is $8.6 – $3 – $2.4 = $3.2T of “effective” QE.

That’s why I’m saying the effective amount of money sloshing around the economy, powering demand and asset bubbles, has actually increased. I’d love to learn where my mistake in this line of reasoning is.

Lune,

You didn’t quit while you were ahead?

They say the hardest thing about art (which definitely includes writing) is knowing when to stop;)……

Don’t get me wrong, FWIW, I think you are one of the better commenters here.

NBay- I know I’m risking getting a beat down by Wolf or someone else who knows this stuff better than me. but I figure it’s worth it if I learn where I’m making a mistake :)

Lune,

Good luck, I know I don’t have the desire to “master” it, and don’t think that is possible, anyway. But if you learn the present lingo-in-use (or logic-in-use, every endeavor or disciple has it’s own) and some major interactions, that’s a big help.

Again good luck, to me, words are notoriously inaccurate. And Aristotle sure didn’t do us any favors. Check out Science and Sanity by Korzybski…very tough read but most all the linguists/semantics guys like it….or did in the 70’s.

Can’t imagine the work that goes into these updates. Bravo and kudos.

Wolf, Why were the reserves zero, or near zero, before 2009?

Before 2020, there were “required reserves” that were non-zero but small; and there were “excess reserves.” Excess reserves were zero before 2009. In 2020, the Fed lifted the reserve requirement, and from that point on, there were no more required reserves, and all reserves are now just “reserves.”

Also because the banks didn’t get interest paid on their excess reserves before 2009. No point in sticking a reserve where it wouldn’t generate yield.

The interest on excess reserves (IOER) and now ongoing interest on reserves is (from one perspective) a huge subsidy of the banks by the taxpayers. And getting huge-er as rates go up.

That’s right. Seems corrupt to me.

Wolf,

Thank you kind sir! So 300 something billion QT. I think of the leverage in the markets you have written about. I read 3 trillion in wealth vanished.

Yes, $300+ billion in QT already did that! Now think what $600 billion in QT will do! And what $1.2 trillion in QT will do!! And what $2.4 trillion in QT will do. Coming to a portfolio near you. We’re just seeing the beginning.

I have a feeling there are going to be millions of shrill screams for mercy by the time $2.4 trillion in QT is ever reached.

Long before then. Mizuho’s U.S. chief economist already issued a shrill scream for mercy today, LOL, these friggin crybabies on Wall Street. And QT barely started.

What will this do to several M I have in my stocks, farms, bonds, and cash? I think I am too dumb to understand Fed Finance. Is there a book on this stuff?

Not enough to undo the 8 trillion added over the past 3 years. Still theft of purchasing power from previously saved dollars.

NOT $8 trillion. But $4.6 trillion over the past 3 years.

The Fed has already undone $344 billion since QT started, as of last week.

@ Wolf –

I am unclear on the number. I have read that the “covid response” resulted in 8 trillion new dollars being introduced into the system.

Roughly 4 trillion via the FED buying treasuries and mortgage backed securities,

and another 4 trillion via stimulus – direct payments to citizens and a huge number of forgiven PPP “loans” administered through the banks.

I am unclear how a bank makes a loan and then forgives it as directed by the government. Do they create the money from nothing, then suspend the collection, just letting the money stay in the system?

“…and another 4 trillion via stimulus”

This was not “new dollars” but borrowed money, me handing my cash to the US Treasury department in exchange for a minimally interest-paying Treasury security.

In March-June 2020, the Fed printed about $3 trillion and the government issued about $3 trillion in new debt. So that’s where the cash came from to buy the $3 trillion in new Treasury securities.

PPP Loans: the banks made the loans, which were guaranteed by the government. When the loans were “forgiven,” the government in effect paid off the loan to the bank, so the bank got its money back and got paid interest, the borrower was free to go, and the taxpayer paid for it.

For the government, the PPP loans were an expenditure — not a loan (asset) where it would expect to earn interest and then get its money back.

Some of the PPP loans were bought by the Fed as part of its SPVs. The Fed never said which bank it bought those loans from, but I believe it was mostly from Wells Fargo.

The Fed had punished Wells Fargo in prior years for its misdeeds, and part of the punishment was a cap on Wells Fargo’s banking assets (loans). In other words, Wells Fargo was not allowed to grow its loan business. When the PPP loans came out, Wells Fargo couldn’t participate because of this cap. This was a HUGE problem in California, where WF dominates with small businesses. And CA politicians complained about it and businesses wailed because everyone was getting the PPP loans from their banks except WF customers.

So then the Fed started buying the PPP loans that WF extended to its clients, and the system then ran smoothly.

@ Wolf-

Much appreciation. It is very generous of you to share your research, knowledge and insights. Your capacity for finance is impressive.

Why does 300bln of QT result is banks reducing their holding of cash by 1.12 trillion at the fed? You seem to be suggesting cause and effect. Why should QT cause that? They dont seem to be directly connected. One could argue that QT would make holding cash more appealing because QT increases the value of cash (QE decreases it)

As I said in the article, banks are putting their cash where they can earn more, including in Treasury securities, lending to the repo market, etc., with an eye on their regulatory capital formula. QT and rate hikes are making other assets produce higher yields. Deposits have fallen too, for similar reasons, as I pointed out.

“…the Fed’s capital is limited by Congress, currently $42 billion.”

“Total liabilities dropped to $8.58 trillion, according to the Fed’s weekly balance sheet released…”

How can the Fed possibly be solvent? I hope someone can explain this beyond the usual explanations that “the dollar is the reserve currency” and/or “the Fed can create money indefinitely” and pay itself.

I believe it’s the latter condition you mention — that the Fed (and its agents) is the sole entity (by US law) which creates $USD — which makes a solvency constraint for itself in $USD a logical impossibility.

John Apostolatos,

The Fed can create money whenever it wants to, however much it wants to. “Solvency” doesn’t apply to a central bank that can create money. It will never run out of money.

Wolf, a question regarding this.

Central Banks can create money, that’ is true and the way they do this is expanding their balance sheet, they acquire an asset and add in the liability column. Commercial banks, as we know this, do the same when they “create” money (loans) and at some point they will be capital constrained, they cannot expand their balance sheet ad infinitum.

Central banks obviously are not commercial banks however they must have some official formal capital rules in place (otherwise why having official capital accounted at all??) even if they can disobey them when needed.

When the Fed balance sheet exploded after the 2008 crisis did they receive an injection of capital from Congress or they simply operated outside of whatever capital ratio they had on paper??

Thanks!

The only real constraint central banks have is fear of the destruction of the currency (inflation). The government can put constraints on the central bank, but those constraints get moved out of the way, no problem, as we have seen. But inflation is something no one can just move out of the way.

I think that the real limit on banks “creating” more money with loans is credit quality. If a bank could find an endless amount of borrowers that were guaranteed to pay back the loan, they would only be constrained by the amount of capital they could access. But in the real world the more they try to loan out, the weaker the credit quality of the marginal borrower.

Expansion of the monetary base by banks is therefore a much more market-driven approach, as it is dependent upon the strength of the economy to provide a return on the invested capital that gets borrowed, so the loan plus interest actually gets paid back.

The $500 billion increase in currency since ’21 is interesting to me because the Fed cannot control how much currency the public demands. Atms are very profitable to their owners.

Several Sevice people prefer cash payments and some restaurants are offering cash discounts.

Holding currency make sense to me.

PS. “cash has no enemies”

> Several Sevice [sic] people prefer cash payments and some restaurants are offering cash discounts.

Brings to mind why crypto may have a terminal value above zero: it is useful for tax evasion. The discount could be bigger than the card usage fee, if the tax evasion benefit exceeds the card fee. There are incentives for the *informal* economy to grow.

I am currently getting a quick lesson in why “Cash is King” and Millennials are drawn to cryptocurrencies. Earlier this month a customer of mine took shipment of three pallets of product… they arrived… they were inspected… and THEN he sent the payment through my regular payment provider (Paypal). This was the sixth large transaction we have conducted this year.

Only this time Paypal decided to hold onto the money for 23 days so that they could “verify” that the shipment had arrived. 11 days ago I sent them the tracking number of the shipment… and ten days ago the purchaser responded to them that he has already received the shipment.

They are still holding the money. Instead of being a quasi-bank Paypal is now a quasi-bank ROBBER.

The bottom line is that our institutions simply don’t work as they are supposed to. It is hard to fault people for trying to find workarounds.

Get your customers (if they’re with a US bank) to use Zelle. No fees, the transfer is instant (you’ll get email confirmation within seconds), it’s easy to use, and it doesn’t involve a third party, such as PayPal. It goes from their bank account to your bank account. Zelle is owned by a group of banks, and most banks and credit unions participate. I’ve been using it since 2014. Works like a charm. That’s how banks are trying to protect their turf from other payments services, such as PayPal.

Thanks Wolf. I have never had this big of a payment held up by Paypal before so I was really caught off-guard. Plus the fact that this guy has sent thousands to me in previous transactions (with neither one of us complaining to Paypal) should have made the algorithm just push the payment through. It has definitely put me in a temporary cash flow bind.

PayPal refuses to process some donation from overseas, based on credit cards that were issued by banks that PayPal finds objectionable. HSBC in Hong Kong is on that list. A bank in Japan. A bank in Australia…. I called PayPal about that, and he said it was due “credit card spam.” BS? Who knows. Relying on PayPal is kind of a gamble, it seems. Plus, it’s expensive.

Paypal has gone full evil with the implementation of their new ToS. As a result, I canceled my own account and would recommend other paypal clients to read the new ToS and cancel their accounts as well.

They are riding the float for whatever bogus reasons they feel like inventing. Now that the float has some kick in it, this isn’t surprising at all.

Zelle is great but depending on the bank I believe they set limits on transaction amount.

My understanding is because these transactions do actually take forever to settle and they don’t want to front too much money.

Why are they so slow is a great question?! I’d say cuz they can be and banks don’t care about you

In my account, they settle very quickly.

The reason why they limit the amount early on when you use it, until you establish a history, is to avoid fraudulent transfers and people getting scammed for big amounts because the transfer is immediate, final, and cannot be reversed, or stopped (no stop payment, etc.). This is very different from checks or credit cards. It’s more like paying with cash.

Time to short paypal? Haven’t looked at their chart yet. Making their customers angry can’t be a good thing.

I think this may also be why tipping “suggestions” are so aggressive on all the tablet-based payment systems at every damn type of store imaginable now. Whereas before it was a jar full of cash that never got reported/taxed, now almost all transactions/tips are automatically reported/taxed. To stay even, that $1 that used to go into the jar at the coffee place needs to be $1.50.

If I understand it correctly, when the Fed was first chartered, they were to be the lender of last resort to banks. They were forbidden from buying US debt.

After politicians got us into WWI the charter was changed to allow the Fed to monetize the cost of the war, with the stipulation that Congress would have to take a vote on the maximum amount that could be borrowed. When you hear about the debt ceiling vote in a few weeks, you will know why it is done the way we do it.

The requirement to have a vote to increase the borrowing authority of the US government is one of the few limitations on their ability to spend. It is kind of a stupid fight every year or two, but in one way it shows how dependent we are on government debt expansion. Would economy collapse if debt limit was fixed at $31 T.

Seems the current system is overly complicated and designed to hide the cost of government spending and we would have to end up in a place where Fed has to “fix” interest rates so government can service the debt.

Right now we are having a slow work off of government debt with real wages and real earned treasury interest trending negative. Next few years looks a little scary.

Good to know, I never actually got a full history of the Fed in econ classes, recall learning something about how the Fed had much more limited duties at the start and they were prohibited from making debt purchases. Unsurprising that a war was used as the excuse to change it, never let a crisis go to waste as they say

The (unavoidable) 20th century wars required huge adaptations in large scale finance. (You can trace roots back to the Civil War as it all ramped up.) The world saw it coming. Britain fell out of the race and *we* stepped up. It’s not like the USA didn’t get vast benefits alongside these costs: *we* became the apex of the world order. Millions had amazing standards of living here. As Jeffersonian scattered farmers, we would’ve been roadkill.

The US did not have to get involved in WWI.

Yes it did. Our Military Industrial Complex was woefully behind the other major players. And that is NOT sarc.

I think something is missing from your history lesson here. Before the “innovation” allowing the Fed to purchase US federal debt during WWI, every appropriations bill in the house had to be accompanied by one itemizing the relevant taxes (and the form they would take: stamp duties, excise taxes, income taxes, wealth and/or inheritance taxes, etc). In a war, especially one featuring lend-lease, you can probably see how this could become cumbersome to the point of irritation.

That may be true about appropriations for WWI, but the Lend-Lease Act was for WWII.

Yes, thank you. I was trying to infer that subsequent circumstances tended to cement the change — it’s highly unlikely that they are ever going back to the old system because it was clumsy and unnecessarily rigid.

So the dollar is a dog and the US has a crazy amount of debt. Economically the US is still the cleanest shirt in the world wide dirty laundry bin (I know, that analogy has been used a lot). Everything is fine, until it isn’t. When this game ends it will be ugly.

Agreed but hard to be even really sure of cleanest shirt assumption, the predictions were for the EU to be in sharp recession in 2022 while the US would be soaring, instead it was the US that had two quarters of contraction in Q1 and Q2 while EU even with all the issues to the east has held steady. (France was esp resilient, Germany defied expectations) Which sort of goes against the cleanest dirty shirt theory, but saying that, with inflation still this high it’s a mess everywhere. (A bit lower in the US now but the price increases now are on top of the heavy price rises that started a year ago) Hard to go out on the town when every shirt in the closet is too dirty to leave the house with

> When this game ends it will be ugly.

So ends every game, at some terminal point. That does not make all games worthless or bad. The key to success is figuring out the timing: the “when” and the “how,” and formulating a bet that pays off on it. “This game will end” is a truism, of course it will. All do. Thriving is riding the wave smartly before it closes out.

Its enlightening to see the liabilities side explained. As Wolf has posted months ago QT cannot reduce the asset side to levels below liabilities.

Now that liabilities have accelerated in decline nearly 3:1 to assets, perhaps the Fed can get creative in reducing assets further.

I dont support a fire sale of MBS even though I object to their presence in principle.

Awesome education Wolf on how the Fed/Banks operate, thanks for putting that together!

I can’t help But wonder if this may be the start of what happened before when Banks began offering Larger and Larger Interest rates to draw People in.

Then several Banks failed and the bailout’s began , I remember getting close to 6 % on CD’s and certainly liked that .

Lets see if in time we get Bailouts again.

Bask Bank one of the leaders in High Rates is now at 3.60 % Savings Rate, so after the Dec Rate Raise may go to 4% before long . Their no Fee accounts and wire transfers are a Big draw but I would not exceed the FDIC Limits however as your funds may end up sucking wind big time

This Blog subject is great and very important thank you

> Bask Bank

I don’t know about this bank one way or another, but despite that FDIC label, I will tend to loses a few basis points to get a big name that I speculate would have trustworthy cyber-security (with a bigger stake in a long term reputation).

“I remember getting close to 6 % on CD’s and certainly liked that .”

I remember getting 12% CDs from Columbia Savings and Loan in 1982 or thereabouts. That was a fun time, until it wasn’t.

6% CDs may be a few months away….

I am definitely in the camp of cash is not trash. The retail stock gambler is in the camp of FOMO on the Christmas Rally 2022 and the Fed Pivot which must be close because the 10yr and 1yr treasury are big time inverted. The Fed must pivot because it is being ordered by the inversion police to do so. Bond barkers are gonna ride the 20 year treasury equity TLT and double their money after the Fed Pivot. Inflation is completely ignored in their calculus. The Fed policy of a Fed Fund Rate greater than inflation is a bed time fable. The only Fed policy that can happen is QE forever. There is a possibility that at some point in the future my cash might end up actually creating real economic activity that benefits me and the average person on the street. Real economic activity? Is that possible? The FOMO cult will produce nothing. They need to be liquidated in the Great American Liquidation Sale. I hope Jerome de-burrs them with a dull and rusty reamer. Does he have the stones to do it?

The FED’s Williams is offgassing through his pie hole again, talking about inflation of 5% to end 2022, and 3% in 2023. I guess he had a liquid Thanksgiving dinner – and breakfast.

It’s amazing how these FED bankers can predict the future with such detail. With that talent, maybe they should run for office and replace the brain dead crew in 2024.

Why would anybody trust the FED? They couldn’t even forecast inflation, then when it started raging they called it “transitory.” But all of a sudden this clown can magically predict future inflation rates? This stuff would be comical if it weren’t so disgustingly filthy.

Truflation has dropped to 6.36%, so I’d say he has some points to be made. We’re definitely down from 12% this summer. Mostly due to the cost of fuel.

Down $344 billion from the peak is nothing; there is still $2.43 billion is RRPs that, the way I read it, is still potentially surplus liquidity. This is going to take a long time.

This is going to keep on for years. Smooth and steady. Month after month. As asset prices unwind. You don’t want to do all this at once. Give it some time. The pace of the sell-off is already bad enough as it is. There is no reason to speed it up.

“Soft landing” = death by a thousand paper cuts. They should have allowed the entire market to clear in 2008. Price discovery is what free market capitalism is all about, and we could have built a healthy country from there. Instead, these guys have destroyed everything with their “command and control” tactics. They love the power. They’re drunk on it.

Fascinating.

fascinating to look at the liabilities part of the equation. seems to me that a good portion of the bond buying is being countered by the reverse repos. i have read another article that said the runoff of assets would stop by middle of next year since they can only shrink liabilities a certain amount.

it would seem to me that the Fed interjecting itself into the banking system is another way of transferring risk from financial players to the taxpayer and that it all just causes more risk-taking.

THE OTHER WAY AROUND: QT CAUSES RRPs and reserves to drop. That’s where the liquidity drain manifests itself.

Question: How long can the Fed continue to tighten and pay higher and higher rates of interest on Excess Reserves before they become technically insolvent?

I believe that a good portion of the “Assets” on their Balance Sheet carry very low coupon rates (dating from the “ZIRP” era) and the older, higher-yielding assets are the ones now rolling off the books.

Is the mechanism by which customers can remove cash from the banking system entirely dependent on QT because when you buy a treasury you give money to the government which then pays off a maturing treasury at the Fed, which destroys the money? Because if there was no QT, then purchasing a treasury gives the government money which is spends into the general population i.e its found its way back into the banking system.

In which case these customer actions are ultimately caused by the Fed base rate and QT which also causes higher rates on treasuries i.e. cash is being removed from the system by the inducement of the Fed through QT and higher base rates.

What I mean is that its impossible to remove cash from the banking system unless you take out paper dollars.

My point is the competition is not between banks (apart from their usual interbank borrowing to make things balance) but between the force of the Fed trying to destroy cash and the forces of the banks trying to stop the money from being destroyed (because they can earn interest at the Fed). In this case both the banks(collectively) and fed are trying to outbid each other on yields.

“….it’s impossible to remove cash from the banking system unless you take out paper dollars.”

That means the GFC left some REALLY stuffed mattresses somewhere.

Chasing all those down would make a great reality show….move over Treasure of Oak Island, that is chicken feed hardly worth people wondering about.

Now, where might one find a rumpled map to get the show going?

I know the Fed is tightening, but NFCI is trending looser. Is that the Markets fighting the Fed?

I would assume the ANFCI is the adjustment to the Fed moves in this statement: “the adjustments for prevailing macroeconomic conditions contributed 0.02 to the index in the latest week.”

Being positive is I assume the adjustment for the Fed ‘tightening’?

From the Latest NFCI Release:

Index Suggests Financial Conditions Continued to Loosen in Week Ending November 18

The NFCI moved down to –0.26 in the week ending November 18. Risk indicators contributed –0.04, credit indicators contributed –0.11, and leverage indicators contributed –0.10 to the index in the latest week.

The ANFCI was unchanged in the latest week at –0.10. Risk indicators contributed 0.03, credit indicators contributed –0.07, leverage indicators contributed –0.08, and the adjustments for prevailing macroeconomic conditions contributed 0.02 to the index in the latest week.

The Fed has a fight on its hands, fighting inflation with all us boomers gladly spending our hard saved money, before it becomes worthless.

sarcasm or no sarcasm? Guess.

Of course it’s not sarcasm. That is what the FED is facing from every age group. The FED has punished saving. That is why restaurants are full and people travel, paying big bucks for accommodations.

How can bank reserves fall if banks purchase treasury securities? Who do they buy it from and what do they pay it with?

Shouldn’t purchase of treasury security just change reserve balances within banks keeping total the same?

Shouldn’t bank reserves only decrease ONLY IF the Fed sells securities?

Read the article (RTGDFA as I used to say). What are reserves? You clearly have no idea what reserves are. Read the definition in the article and don’t post garbage here.

I guess I annoyed you. Which wasn’t my intention. I am trying to learn from you.

Would highly appreciate if you could point to your blog about reserves. Not sure if I understood what RTGDFA means.

Many thanks and I love your blog. I have gained a lot from your work.

1. RTGDFA = Read The G*d D**n F***ing Article

2. From the article above (relevant sections highlighted to make it easier for you to read since you refused to read the SAME section in the article):

Reserve balances – cash that banks put on deposit at the Fed to earn interest, similar to a big savings account – plunged by $1.12 trillion from the peak in December 2021. Late 2021 was when the Fed began “tapering” its QE asset purchases, and QE ended in March 2022.

Banks use their reserve accounts at the Fed to transfer money between banks and to do business with the Fed, such as selling securities to the Fed under QE. Reserves are a liability on the Fed’s balance sheet; they’re money that the Fed owes the banks.

Reserves are the most liquid, risk-free interest-paying asset banks can invest in, and they also figure into the banks’ regulatory capital.

The Fed, as of the last FOMC meeting, pays the banks 3.9% interest on reserves. Alternatively, banks can invest their excess cash by buying Treasury securities, and they’re doing that. The one-month Treasury yield is currently 4.16%, but these securities are less liquid than reserves; they have to be sold in order to be turned into cash, while reserve accounts are like a savings account that banks can just draw on.

The banks, on their own balance sheets, don’t call these reserves “reserves.” That’s a Fed term. Banks carry them as assets and call them “interest-earning deposits,” “interest-earning cash” or similar.

Reserves are a manifestation of liquidity in the banking system that is not chasing after other assets.

QT is draining liquidity from the financial system, and one of the places where the liquidity drain shows up is in reserves.

But the $1.12-trillion plunge in reserves is far larger than the $344 billion decline in the Fed’s overall assets and liabilities under QT. This means that banks are now chasing after other options that are paying higher yields than reserves, and these options include Treasury securities.

Reserves, bank deposits, and competition for cash (which is no longer trash).

This bank-cash put on deposit at the Fed represents only a small portion of the cash that the banks received from their customers’ deposits. [For banks, a customer deposit is two things on its books: the amount owed the customer (a liability); and the amount in cash received from the customer (an asset). To earn income with this cash, a bank buys securities, or puts the cash on deposit at the Fed, or makes loans, etc. It also has to keep some on hand to process transactions, meet withdrawals, etc.]

Total deposits (the liability) at all US commercial banks dropped by $433 billion from the peak in April 2021, to $17.7 trillion. In other words, customers lent banks $17.7 trillion in cash, via savings products and transaction accounts, such as individual and business checking accounts, corporate payroll accounts, and corporate accounts that suddenly and briefly swell with cash when major transactions take place, such as the purchase of a company involving billions of dollars in cash.

But customers are now finding better use for some of their cash than depositing it at the bank and earning nearly no yield, while for example shorter-term Treasury securities now pay over 4%, and so they’ve pulled $433 billion in cash out of banks since April.

Banks have begun to fight back to stop this cash drain, and they now offer CDs – usually brokered CDs that you can buy only through your broker, not a the bank itself – of 4% and more. Some savings accounts are now at 3% or higher – a sign that there is now finally some competition for cash as the era of free money has ended and cash is suddenly no longer trash but in demand.

This chart shows total deposits at all commercial banks (green) and the portion of the cash from those deposits that banks put on deposit at the Fed, which the Fed calls “reserves” (red):

I just saw an article that Mizuho’s chief economist says that QT is a huge mistake. Of course, he would say that. QT is essentially the taxpayer propping up the value of every investor bubble. And Mizuho doesnt want markets to actually operate normally.

The guy isnt stupid, he is simply talking his book and cares only about his fat paycheck. All these financial players are nothing but leeches on the real productive economy.

I am late to the party. Fantastic article. I am looking forward to an article where you discuss what banks do with Treasuries. As I understand it, banks and the global financial markets treat U.S. government debt as the best form of collatoral out there. So they would naturally lend treasuries out and create all sorts of derivatives built on them to squeeze out more overall yield.

Also, the most compelling explanation I’ve heard for mass foreign dumping of US government debt is the rising dollar. These foreign entities, including foreign central banks, needed US cash for all sorts of reasons. The most urgent reason being to make interest payments on their own USD denominated debt. Foreign private buying of US government debt increased over the same period.