Credit cards mostly a payment method, paid off monthly. Importance for borrowing declined over the years.

By Wolf Richter for WOLF STREET.

Credit card balances include balances that accrue interest and balances that are paid in full at due date so that no interest accrues. Many Americans use credit cards purely as a payment method (and to collect the 1.5% cash-back or whatever), and not as a borrowing method. So credit card balances are much more a measure of spending, than of borrowing.

Fitch estimated that the total amount paid with credit cards in the US reached $4.6 trillion in 2021. Only a tiny amount of the spending wasn’t paid off in full and added to the interest-bearing debt.

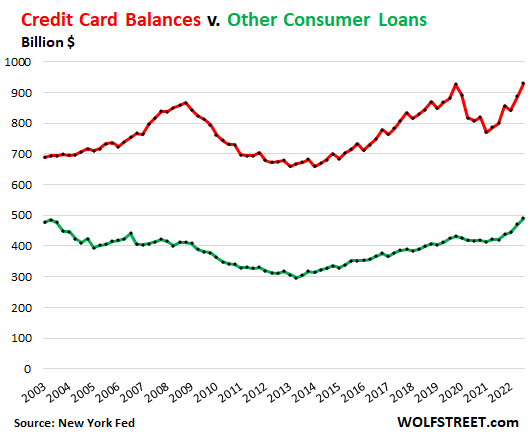

In the third quarter, credit card balances rose by $38 billion from the prior quarter, to $930 billion, according to the New York Fed’s Household Debt and Credit Report. This $930 billion includes transactions incurred roughly in September but paid off in full in October, that are not accruing interest.

Credit card spending has been boosted by the resurgence in traveling, with credit cards being used as payment method for hotels, airline tickets, rental cars, meals, etc. Surging costs further drive up the amounts that flow through credit cards. But card holders paid off in full nearly all of the new amounts that were paid for by credit card during the quarter.

Household have a lot of debt, but the problem isn’t credit cards, it’s mortgages.

In a moment, we’ll look at credit card balances as percent of total consumer debt and as percent of disposable income, and we’ll look at delinquencies and third-party collections, and we’ll see that the burden of revolving-credit is now just a small fraction of what it was in prior years and decades, and that delinquencies started to tick up, but are still below pre-pandemic lows, and that third-party collections dropped to new record lows.

During the pandemic, the plunge in bookings for airline tickets, hotels, entertainment and sports venues, restaurant meals etc., caused the use of credit cards as payment method to decline, and that’s where the big trough occurred; it shows the collapse in spending on services. This is now returning back to normal as spending on services is recovering.

And yet, credit card balances outstanding in Q3 only grew by $43 billion, which shows the universal use of credit cards as payment method, with balances paid off in full every month, and to what small extent credit cards are used as borrowing method. And that makes sense because borrowing on a credit card can be ridiculously expensive, with rates as high as 30%, but paying with a credit card can earn you a kickback.

“Other” consumer loans, such as personal loans, payday loans, and Buy-Now-Pay-Later (BNPL) loans, rose by $21 billion, to $490 billion in Q3. Most of them are interest bearing, but not all: For example, BNPL loans may be subsidized by the retailer. These loan balances are now back where they’d been in 2003, despite 19 years of population growth, income growth, and rampant inflation.

What’s amazing, actually, is how low these balances are after 20 years of population growth, income growth, and inflation:

Dwindling importance of credit card debt.

Consumers reduced their reliance on credit card debt over the years, though credit cards have largely replaced checks and cash payments as payment methods. In the year 2021, $4.6 trillion was spent on credit cards, and yet over the same period, credit card balances grew by only $40 billion.

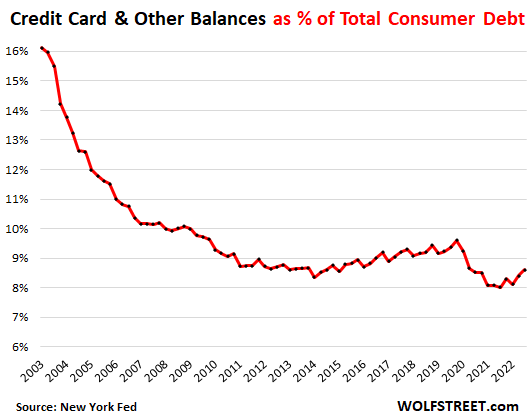

In 2003, credit card balances and other loans combined (the red and green lines in the chart above) amounted to over 16% of total consumer debt, which also includes mortgages, auto loans, and student loans. During the pandemic, this dropped to 8%. In Q3, credit card balances and other consumer debt ticked up to 8.6% of total consumer debt, roughly in the range of the pre-pandemic low in 2014.

Debt burden as percent of disposable income.

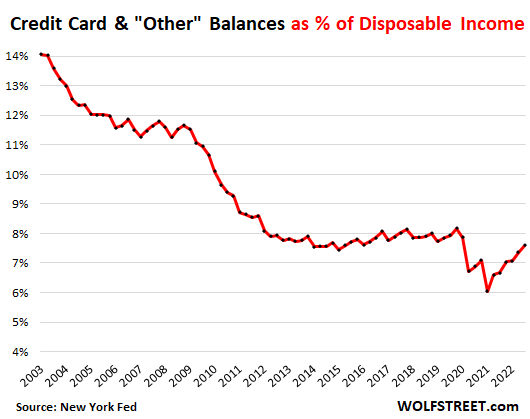

Credit card balances and “other” consumer debt combined in 2003 amounted to 14% of disposable income (income from all sources minus taxes and social insurance payments). And then over the years, it dropped steadily as the burden from credit card balances and “other” consumer loan balances declined in relationship to disposable income. In Q1 2021, it dropped to a historic low of 6%, as disposable income ballooned with stimulus money. In Q3 2022, it rose to 7.6%, roughly in the range of the pre-pandemic lows:

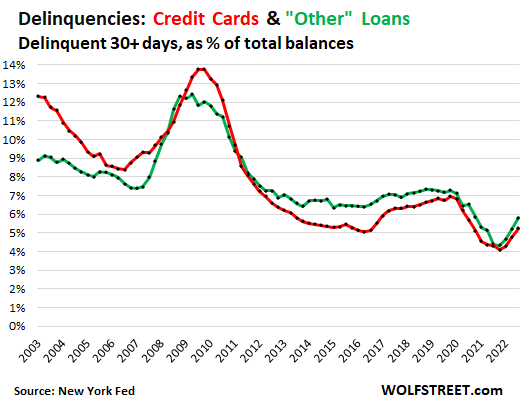

Delinquencies tick up, remain at or below pre-pandemic lows.

The stimulus monies handed directly to consumers during the pandemic – stimulus checks, PPP loans, extra unemployment benefits, and whatnot – plus the monies that consumers didn’t have to pay – mortgage forbearance, eviction bans, etc. – left consumers with some extra dough, and many of those that had fallen behind on their credit cards caught up. Others were able to enter their credit card arrearage into forbearance programs, and the delinquent balance was marked “current.”

All this has ended, and credit card balances that are transitioning into delinquency – 30 days and longer past due – ticked up all year. In Q3, they rose to 5.2% of total balances, which is in the same range as during the pre-pandemic lows in early 2016.

“Other” consumer loans, such as personal loans, that are transitioning into delinquency rose to 5.8% of total “other” balances and remain well below the pre-pandemic lows:

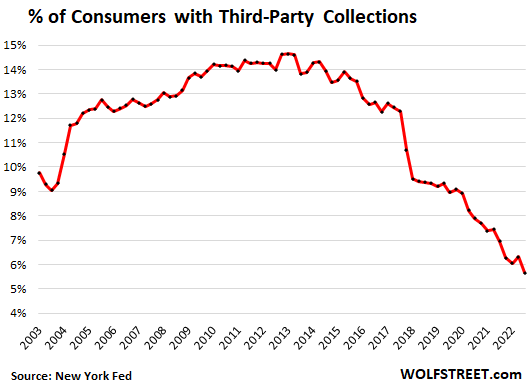

Third-party collections dropped to new historic lows.

The percentage of consumers with third-party collections fell to 5.7%, the lowest on record, and down from 14.6% of all consumers following the unemployment crisis of the Great Recession.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

When a Battleship is built, it has watertight doors, so that a single hit doesn’t sink it.

In US, we have opened all watertight doors (through bailouts and stimulus) so that no single compartment gets flooded (no bankruptcies). So now, the whole ship is taking water together (all debt is backed by shareholders and is increasing), and hence this ship will sink as a whole (We all will get poorer as inflation will exceed our raises).

I’m guessing the reason credit card balances started a long decline in 2009 is because the Fed printed money and started interest rate repression for mortgages, but credit card interest rates remained high. Would love to see a chart with the gap between cc interest rates and mortgage interest rates or other types of interest. So this is another impact of the big credit bubble. The huge gap in interest rates probably means cc debt will never again approach what it was in the past.

I think that was when people realized it was better to stay current on your credit cards and let your house go into foreclosure.

I’ve never seen published date on actual revolving credit card balances. I used to work for a major card issuer and this was tracked internally but never seen it for the industry.

An increase in this number is a lot more meaningful. if it is actually increasing.

Still, when the economy turns definitively south and the employment market gets a lot worse, no doubt in my mind that credit card balances will increase steeply.

Unsecured lending to finance necessities and tax payments will lead to big proportional write-offs in the future depression, just as it did in the GFC.

Right again AF, and can only relate an anecdote re a friend who, when faced with using CC to buy/finance ”needs” did their best to run it up to the max by taking cash from CC to make min payment,,,

Might be, these days, GUV MINT will just step in again with four or five ”bearances” to ”save us all from ourselves.”

Just like livable vehicles, a good credit account is a last ditch fall back as our wealth inequality just gets worse and worse.

Below that there are cardboard boxes and food banks.

Indubitably.

Hey folks, considering donating to Wolf.

My cheap ass just did . . . it’s likely yours can, also.

Exactly. Dream Big. Get a mug. Use your credit card.

Well ya, gotta collect those points or cash back percentages, just pay it off quickly to keep wolf’s charts looking clean.. and I guess avoiding interest payments is good too

Some of my recurring monthly expenses are billed to my checking account, others to my cash back credit card. I rarely stopped at an ATM, such as before a hurricane. After Hurricane Ian hit, one McDonald’s was accepting only cash at the drive through window.

DH: do NOT let any entity pay themselves from your ”checking account.”

Many and many have had totally unexpected monies taken that way, and some have had years of ”fighting” with the entities that took those payments in order to be made whole.

I too have accounts taken from my CC, for one reason the % I get, for the other and main reason is the promise of the CC to stop any such theft,,, and they have been very good about alerting me when my CC was used by others…

So far SO good that the current CC provider is my ”go to.”

The consumers are loaded. Absolutely no slow down in spending and people are not tightening and spending like there is no tomorrow.

Demand for all items are off the roof.

Disagree. Not in poorer cities. Also don’t believe the stats include many people in the background hurting. Watch the mattresses and couches accumulating on the sidewalks in front of low rent districts.

“mattresses and couches accumulating on the sidewalks”

The City of San Francisco offers a service: hauling off junk (mattresses, couches, etc.) once a year per address, for FREE. This is done via Recology. We use it every 5-10 years to clean out the garage. On the appointed day, you put all your junk out on the sidewalk at 5 am. And eventually the big truck shows up. A beefy guy stuffs the couch into the back of the truck via a mechanical device and the truck crunches up the couch and eats it. It’s quite a sight. And it’s a great service, and it’s free.

Which explains the periodic appearance of furniture on the sidewalk, rich or poor neighborhoods alike. Don’t you have that kind of service where you live?

No service like that anywhere in So Cal that I know of. Only the guys who pick it up and take to Mexico. This is a sign of (poorer)renters moving. When the renters collapse accelerates, then the dominoes fall across the board for R. E., then the broader economy. Just starting to see the first street deposits growing steadily.

We lived in OC. Republic (our hauler) had large item pickups which resulted in mass quantities of no longer wanted household items on the curb. They would give you a date that the truck would be making pickups.

Ditto our manse in AZ.

Here in north Texas (DFW) it’s once a month on the first Wednesday. You’ll start seeing large items appearing curb side a few days before. What’s interesting is the few times I’ve placed something large in front of my house it’s disappeared before the city truck showed up. Goodwill will also come pickup stuff depending on what you have and where you live.

Not here. We have to pay a company if we want stuff like that picked up. I have one garbage can and one recycling can, anything that doesn’t fit in those is on me.

We have “bulk pickup” once a quarter. A large truck, front loader, forklift to haul off whatever you want to put on the curb/sidewalk/alley. Free – paid for by city trash bills.

People trim trees at this time, as they will haul that way as well.

I see that stuff and I wince. I was a spartan guy whenever I was poor, and I either saved up for things that I felt were worth lugging from hovel to hovel or I restored/had restored furnishings worthy and capable of being restored or reupholstered; the things that I see on the curb — I think to myself, just one day ago and in the weeks and months prior, that living room gear sitting there was deemed good enough to be inside front & center. This whole time this person’s interior was outfitted with big trash day furnishings. It’s crazy. Oughta be a store called Future Garbage. Ugh.

Yes we have it but the “junk” goes out 3 weeks before pick up. The poor and the 2nd hand traders pick over the offerings and it is a huge industry. I have seen OLED TV’s @ 55inch with remote and a sticker saying it works and is free.. Any cast Iron off BBQ’s is boosted, as are batteries, AC units, ceiling fans, leather lounges, Fridges, working Micro waves, freezers, Light fittings, quality floor coverings ect. Flea Bay get some but mostly the poor get a recycled hand up as the professional picker is not quick enough.

We DO have that here in the saintly part of the tpa bay area Wolf, but even in our so far very stable hood, mattresses on the curb have increased and stayed there a while recently.

Easy to attribute that to the storms, Ian and Nick, but the city has picked up from the him a canes, and still has not done so for those houses becoming vacant due to moves to lower rents or whatever…

Now hearing this area becoming, quickly, one of most expensive;;; hard to believe, but, as has been said, folks coming in about 1000 ”net” per day is definitely putting major pressure on livable RE.

SoCal absolutely has this. Both Burrtec and Waste Management provide it to their customers around here. Our Inland Empire city is serviced by Burrtec and I believe they will do up to 3 visits per year per address in my neck of the woods! It’s really easy… You just call in and schedule the pick-up, leave your stuff on the curb the night before, and it’s picked up and hauled away on schedule. No fuss, no fee. Our city even runs a free used motor oil and filter pick-up program for cheapskates like me who insist on doing their own oil changes.

The bottom 50% don’t count.

No sign of recession here in the Swamp and neighboring suburbs. Traffic jams everywhere. I’m going out to my local pub tomorrow, and ordering 2 Bud lights at a time with my dinner because the bartenders are so busy. They have live music, and they are overflowing and rolling in tips from customers. It’s all cash.

There is no recession. We had a bear stock market but the economy has been fine. Low unemployment, historically low delinquencies on debt repayments, no foreclosures.

Bizarro world. Essentially the stock market was way over bought and expensive. It corrected.

We may have seen a bottom or are close to a bottom in the stock market.

I think stock market would bottom quite a bit more from here.

With fed hiking rates and doing QT, this is a paradigm shift for stocks in comparison with what we had for last 10 year or so.

Most of my friends think they can quite their job and make money in stock market to sustain.

They believe, in the long tern, one can’t lose money.

Yes. Everyone’s loaded and only feigning like they’re not out of a twisted sense of noblesse oblige.

When is the pivot coming? That’s all that matters to the ‘markets’.

The pivot to 6% LOL?

I haven’t looked at any news for awhile. Seeing equity prices, I figured the Fed already pivoted, went -75bps. Wait, you mean they haven’t????

BMO Harris bank has 4 3% CD for 2+ years. A real bank with branches. Can’t fight the Fed. This bear rally is about to run out if steam.

CNBC said credit card balances rose more than 15% from the same period in 2021, and New York Fed stated it was largest jump in 20 years. Trillions in stimulus being used to pay off CCs, but for how long does that last, the trillion dollar question.

I think this effect will drag out the mini-recession(s) and thus drags out the market corrections. We have a stimi-cycle inside of a liquidity-cycle, and I miss the easier to predict business-cycle of days long gone due to Fed QE and ZIRP manipulations.

I’ve personally use CCs with 2% cash back applied to my statement balance. Every $10k pays $200, every $100k pays $2000. CC company labels me a “Deadbeat” as I pay in full monthly. The 2% cash back used to be the best “non-taxable certificate of deposit” before the Fed increased rates recently, and thus CD rates pay much higher. In a few years, I suspect the 2% cash back will be the best “CD rate” again as the entire globe is addicted now to easy money and that will most likely be the “Easy Button” pushed again…print, print, print, something for nothing…

And instead of fiscal policy for the people, I’m guessing the Fed, once again, uses monetary policy for the elites as that didn’t seem to cause inflation like giving money directly to the bottom 99%.

People reading this forum know what who the Fed really helps, who the Fed really works for…but unfortunately, I’m guessing 90% are totally clueless of the damage the Fed does to the bottom 80% of society…thus the cycle will inevitably continue…

Hard to believe that over 50 percent of credit card users are deadbeats.

It’s as surprising to find that 37 percent of home owners have no mortgage.

By what you read in the finance news, you’d think all Americans are debt slaves.

BenX,

I removed the link of the article. The headline/URL was misleading by itself (clickbait), and it seems you didn’t read the article you linked. It defined as “deadbeats” the people that have NO (zero) credit card debts. The credit card companies use the term “deadbeats” for people who have no credit card debt. But you would have to read the first paragraph to see that.

The article you linked was based a survey of 2000 credit card holders.

Back when that article came out (2000), it impacted auto loans as solid people didn’t show high credit and often had long periods of zero debt on their cards. Our captive finance arm did some head scratching on that one.

Deadbeat. Indeed.

We haven’t “revolved” any debt on our cards – on purpose – in decades. Last time I failed to pay my Visa, the person who answered the phone said “we were waiting for your call” and credited me the interest and penalty.

I carry cash – but usually to tip off the books for exceptional service.

Thanks for pointing out my mistake. The percentage of people who have no credit card debt is about 45% – which is higher than I had expected.

I should stick to reading rather than writing.

Nah. Keep commenting. Always need new thinking here, anyway. And language is far from accurate anyway.

Ex: Katz thinks article was from 2000 and elaborated on it, I think sample size was 2000 which isn’t enough to mean anything, I figure, and CNBC agenda pretty well known to all.

Just remembered CNBC’s old line from when I was trying to learn stuff there and was for a while almost full time viewer…..’06-10 or so.

“Wealthiest Demographics on TV”

Not sure how Bloomberg let them get away with it, as that would be my guess…..B also had much better interactive charts, all now behind paywall.

My old man never used a credit card. Paid cash for everything. Had no mortgage. In Delray Beach Florida, he was called a deadbeat and could not get any credit to install his cable TV system when they sold the cable TV contract to a private contractor.

So he had to live without 72 channels of shit to choose from? Half of them in Spanish?

We are both home owners with no mortgage AND ‘deadbeats’.

We always used to pay for everything except “big ticket” items with cash. Now we ‘charge’ almost every thing. Use the cash back to pay for the cra… uh … stuff we purchase from Amazon.

We ALWAYS tip in cash however. No reason those folks actually serving us by hand should have to pay taxes – of any sort – on tips.

anecdotal observations – just got back from 3 weeks of flying all over the us – the planes are packed and I mean PACKED! airports full to the maximum- hotels maxed out especially a the higher price points – restaurants – bars – packed even on monday and tuesday nights – new vehicles fill the parking lots – talked to a friend of my brother’s that owns 3 recreational vehicle dealerships – he is sold out and said the more expensive the vehicle the faster it sells and add 5-10k in accessories – no sign or evena hint of a recession

The rich got richer.

The poor got poorer.

The former cohort underpins your observations because consumerism is publicly visible.

The latter cohort – those being crushed by inflation and inequality – are harder to observe.

Unless you are among them most all your life. But only crushed once, 80’s recession…..first time I drank alone….medicinal.

A few times a year work sends me out of town for vaca.. attendance at conventions. This is when I can live it up with paid hotel rooms and per diem meals on the card. The City I was at a couple weeks ago was packed at the hotel, packed at the nice restaurants on weekdays, even at lunch time! Oh well, that being said, time to head home for a lunchtime sandwich.

Concerts, sporting events, restaurants, and airports are packed. Most require a credit card to purchase tickets, food, and the $15 beers.

Almost full employment and wages are up. People are still able to pay off the credit cards each month. Continued Student Loan forbearance likely helps with spending but mortgage and rent forbearance are gone.

Stocks and crypto are down but most people seem to have the cash to pay their debts monthly.

Powell needs to try harder to stop people from spending and driving up inflation.

I am (presently) in The Villages in Florida due to a family emergency. You literally cannot find a parking place in the “towns” if you want to patronize an establishment therein. Drove through today to stop for a bite to eat after leaving the hospital…. Not a parking space to be found. People waiting on line to get a table. At 3 PM. On a semi-rainy day.

Whomever named Florida “The Sunshine State” should be sued back to their underwear. I haven’t seen a solid sunny day in 2 weeks.

What’s that tan, if there is no sun?

It’s rust.

That’s the thing about money supply. It just keeps circulating from hand to hand causing ever more inflation. It doesn’t disappear when you spend it, just the opposite. That’s why the Fed needs to increase the pace of QT if they are serious about their work.

Inflation is finally falling down, bond yields have fallen quite a bit and all signs show continued drop in inflation. Stocks have jumped back up and rich will now spend even more, which will cause inflation to back up again. Looks like there is too much money on the sideline to be invested or spent and every time there is any sign of economic recovery the money will pour back in. So inflation will flip flop in 5-10% band.

This implies that there will be no recession, and no asset and real estate price crash. In fact I can bet that five years later, all assets will be 2x pricier. This is what inflation does, to everything. And Fed has no balls to really fight inflation, i.e. take interest rate above inflation rate NOW (not constant jawboning and hoping that it will happen somehow).

Yes, we know you think it’s different this time.

The bond mania ended in 2020 and interest rates are ultimately destined to “blow out” past the 1981 peak.

I bet you are a perma bear who is relatively poor and have been accumulating cash to invest in the next big crash for last 20 years while your friends have got 10x returns on their investments. I wonder how you sleep being so negative.

I am always investing in real estate and my portfolio has grown to 50M over last 12 years while some of my friends with equal earning levels are still a w2 slave. You can never go wrong by buying real estate or stocks over long time and trying to time the market is fools game.

Kunal gives financial advice LOL

I despise gloating real estate speculators such as yourself. I hope you lose everything and end up living in a cardboard box.

Kunal has no shame in relishing the pain of others. Its a zero sum game Kunal, and all of your “gains” via stocks and real estate are due to the FED holding down rates for over a decade. Not because you’re smart……..

You literally did next to nothing to earn any of that

Did it ever occur to you that Kunal is just a troll — which he is — making up stuff as he goes, which he does, as we know from his prior comments.

Is there a better more rapid-acting emetic than reading “my portfolio” by some anonymous dude on the internet?

Log off already and go spend you’re millions on something cool.

Rats! I thought I could cite a commenter worth $50M here, topping ELib with his $20M and the guy who’s screen name says he’s got $15M. Pretty big deal when people with that kind of money choose to comment on WS, no?

This picture he paints of no crash and no recession but assets doubling in five years is about just as bleak a picture as any other doomsday scenario if you ask me.

If the Fed was serious about bringing inflation down they would increase bank reserve requirement above the present zero. They are a bane on humanity.

Stopped at a fine dining establishment just to have drinks at the bar before the symphony Saturday night. Couldn’t even do THAT without a reservation.

Did get drinks elsewhere, and Brahms was entertaining, but dang.

Nice.

This past weekend, here on the northern Prairie, the band on the west side of the river played played Mahler’s 3rd. It is being recorded in SACD & CD this week by BIS. Rob Suff is once again producing the recording, and it completes all ten of Mahler’s symphonies that are recorded by the band in SACD with Vanska conducting.

On the east side of the river, Joshua Bell was in town with his fiddle. His finishing piece was Bizet’s First Symphony. Mozart’s 25th Symphony & Max Bruch’s First Violin Concerto proceeded it. Mr. Bell is pretty OK on his Stradivarius.

The best part? No credit card needed was needed by me. Both concerts were simulcast live Friday & Saturday evening on Public Radio in HD FM. But no worry, Orchestra Hall in Minneapolis was packed and so was the Ordway Concert Hall in St Paul for all the concerts this weekend.

Looking at the chart, delinquencies go in multi-year trends. The trend is not good. This is a classic case when you need to look at trend and direction, not the absolute number.

Hahahaha, the trend is from stimulus-fueled-ultra-record-low delinquencies back to pre-pandemic Good Times record lows. Times are good, but the distortions of the free-money period are abating. That’s the trend.

That’s my BS (ini) take as well spending up year over year and all went towards services and other cc stuffs . Question wonder how medical spend is going as part of GDP. I personally think medical spend over time is a drag on economy. My first month on Medicare and already have spent 2k of Medicare funds on physical next a specialist appointment in Jan and March for another 6k. My family uses medical much more often with Medicare. Higher spend more services.

“Disease” seems to be the major industry where I live. Many hospitals, clinics, physicians’ offices etc. lining the major streets. A real growth business.

The American economy needs the sick. It’s your patriotic duty to become ill. Dying for your country has taken on a whole new meaning, (cough).

It’s not health care… it’s sick care. There’s no financial incentive for those folks to “cure” you of anything. Imagine if the American Cancer Society found a cure for cancer. What would happen to their donations? Ditto the cancer centers?

Bs: If you’re spending that much while on Medicare, something is wrong. Get a Plan G supplement. Not cheap, but far less expensive than $8K in two months.

Spent a lot of time in a hospital (as a visitor) the past several weeks. The volunteers are generating funds to support the hospital through fundraisers. Makes you wonder why – with the absurd charges incurred – that they can’t at least break even.

When checking the Medicare statements, the amount charged is a totally different animal than what Medicare pays, which is why many doctors do not accept Medicare patients.

The older we get the more we spend on medical care. Just goes with the territory.

Purchases with CC will dwindle in Canada because the gov is now allowing the retailer to add a surcharge of what they are paying to CC companies.

That’s been at thing in the U.S. for a long time. Gas stations are notorious for “Cash” prices vs. “Credit” prices. There’s also credit card “surcharges” added to invoices or restaurant checks. Most people don’t notice. Our local pizza dive does it. Few catch it.

Be that as it may, the word “notorious” seems to assume that something bad exists in that. Please explain why anyone should give a shit whether or not you’ve got a piece of plastic in your pocket, and borrowed plastic at that since you aren’t the thieving fat cat actually issuing the card? Personally, I’d be happy to give my business to someone whose sign reads, “In God We Trust. All others must pay cash.” At the least, I’d actually know who’s robbing me face to face.

I love the Jean Shepherd reference!

“Gas stations are notorious for “Cash” prices vs. “Credit” prices.” — It depends on the spread as to which is a better deal! Gas at $5.00/gal. cash vs. $5.10/gal cc – If the cc company gives a 4% rebate, the “actual” price is $4.90/gal using the card! ($5.10 x 4%=.204 $5.10 – .20 = $4.90) Yeah, gotta wait for it, inflation, etc.

If I could put the bills into the pump, I would, but I’m not paying inside waiting in line behind the lotto, cig and funion buyers.

Meh, unless retailers go the extra mile to highlight the extra fee I think most people won’t even notice. My telecom did just that so I went with a cheaper method for my last bill but given how much less convenient that was and the fact that the fee would simply be offset with my cash back I’ll pay by CC next time. So, I’d say slightly less transactions rather than dwindle.

Wolf,

I hear what you are saying re CC balances long term but…

I look at the upward angle of the line for the last 6 months or so and it looks pretty steep.

What happened?

The end of the Pandemic subsidies and unZIRPing.

The Pandemic subsidies (and plain ole economic fear) drove the balances down from March 2020 to March 2022 (roughly) – but that is a past era.

Again, I look at the sharp upward angle of the last 6 months or so.

It is possible that post-pandemic subsidies, people are going to be forced to lean heavily on their CC again.

The upward angle is the trend from stimulus-fueled-ultra-record-low delinquencies back to pre-pandemic Good Times record lows. Times are good, but the distortions of the free-money period are abating. That’s the trend.

At the risk of being deleted, I’ll say this:

Credit cards are the ultimate scam, in my opinion. The “agreements’ aka contracts/promissory notes are fraudulent, in my opinion. Spend some time in Article 3 of the UCC and learning about the debt-backe monetary system. We may not end up sharing opinions, but the wizardry behind all of this is truly impressive, as diabolical is it is – yes, in my opinion.

Very happy to see credit card debt on the, overall, decline – despite the recent uptick. Hopefully, just a blip, and the over trendline continues downward.

Even though some of this debt was probably restructured into a home loan, I can only hope that those folks don’t fall back into, or worse – are forced – back into the same situation.

I’ll leave it at that. Queue the last scene of Fight Club, please.

Credit cards a tool to be used. Some get the % back, extended warranties, rental coverage, etc.

For some it is a better option in an emergency that borrowing from Fat Tony.

Crow bars, baseball bats, and ice picks are tools too, and also handy in an emergency. Fat Tony ain’t the one telling you to spend your way into a hole to begin with. Those people behind the cards are no less sleazy, they just like to nickle and dime everybody up front with a smile and a welcome mat that reads “Thanks. Come Again, real soon suckers!”.

Tony called and wants to know who’s you calling fat.

Also I agree, how am I supposed to pay for all the extra channels to supplement my “free” antenna tv.

Also I use my scheels gift cards to by ammo after they pile up on the dresser.

Well, there is a solution to your problem, a return to late 70’s or even earlier credit standards which is where the US is ultimately heading though I presume anyone reading my post thinks this is impossible.

If (more like when) this happens, the majority of the population wouldn’t have a credit card, they would have to live within their means, and their living standards would decline or plummet.

That’s what you are implicitly hoping for, and you will eventually get your wish.

Curious, might it be possible that they’d all have plastic spendo-badges and still be living under lower standards? The only difference being that somebody else would be deciding all your limited choices for you.

Wolf: interesting article. Do you have any idea why the numbers of consumers with third party debt collection dropped so much in 2018-2019? I know from my own experience at work that some hospital chains basically wrote off a lot of their debt portfolio due to bad press, but I can’t imagine that covers all of it.

Consumers are in the best shape ever. They’re still flush with cash, and pay is up, and their assets are still up (though they have come down some). People need to forget about this nonsense that today’s consumers are “tapped out.” That’s just BS. They’re spending huge amounts of money. In terms of healthcare, a record number of Americans are now insured: the national “uninsured rate” dropped to 8%, lowest ever — which means that hospitals have much less of a problem getting paid.

“Do you remember, your President Nixon? Oooh

Do you remember, the bills you have to pay?”

-Bowie

When will this trend reverse? When do you think they will tap out? I understand they have all this cash because of excess savings etc .. But this will come to an end at some point?

Great questions. I’ve been waiting for it, and I’ve been looking for it, but I’m not yet seeing it.

This whole contorted economy fills me with amazement every day.

Well what the inverted yield curve represents then?

“Word”, but what say ye about the fact that almost half of Americans cannot afford a $500 emergency payment without worry?

That’s total BS. And it keeps getting regurgitated because people read nothing but idiotic clickbait headlines. They never read beyond it, and they certainly never read the original survey report from the Fed.

The question is whether they have a savings account with x$ in it. And nowadays people don’t have cash in the bank anymore. They have ample room on their credit cards, they have 401ks, IRAs, stock portfolios, cars and houses that are paid off, but they don’t keep cash in a savings account because it pays no interest and because all expenses run through their credit cards, not their bank accounts. The Fed, which comes up with these figures actually spells this out better. But you don’t get it from reading the idiotic clickbait headline at a clickbait website, such as the one you linked.

Thank you Wolf Richter, I will have to check the info on that!

You don’t think about the debts you owe, but don’t show up on the personal balance sheet.

Debts as a percentage of disposable household income is and always has been a misleading statistic because the small proportion at the top of the income distribution and don’t normally have a lot of debt.

Credit card debt in and of itself isn’t going to create a financial crisis. Concurrently though, this ratio would look a lot worse if limited to those who are revolving.

This is a common misconception. It’s the young dentist that has $100k on his credit card. A poor schmuck cannot even get a credit card that has a $5K credit limit. And that dentist likely pays 7% APR on his $100k, and the poor schmuck pays 30% on his $1,000. That’s how credit works.

Poor or lower-income people don’t have much debt because lenders won’t give them a lot of credit.

It’s not hard to get a credit card, unless the person has a low FICO score. My mother is in a nursing home, has no income except SS, and still gets credit card offers offering her credit lines above her SS income.

Lower income people with bad credit scores can’t get a credit card.

Essentially everyone else who can fog a mirror can get one. Credit standards are not strict. I got my first VISA card in 1985 at age 20 when credit standards were a lot stricter. It had a low limit but didn’t take me long to get a much bigger one.

You are probably right that a low percentage of borrowers account for an above average of revolving balances, but what’s also a misconception is that credit card issuers actually know the financial position of their borrowers.

They do not, and I worked for one though it was years ago. They know borrower debts from the CBR and have some idea of expenses from the CBR and the company’s history with the borrower. They have no clue what kind of assets the customer has and have little if any indication of their income.

I got my first one around the same time, Augustus- was turned by by Visa and Mastercard because I had no credit history at all. Only Amex was willing to give me one, and with it, I built up a history that allowed me to get the others about a year later.

All of these poor or lower income people don’t have much debt because the US Govt gave them PPP loans.

Rep. Matt Gaetz (R-Florida) with a $476,000 loan

Rep. Greg Pence (R-Indiana) for $79,441

Rep. Vern Buchanan (R-Florida) for $2.8 million

Rep. Kevin Hern (R-Oklahoma) for $1.07 million

Rep. Roger Williams (R-Texas) for $1.43 million

Rep. Brett Guthrie (R-Kentucky) for $4.3 million

Rep. Ralph Norman (R-South Carolina) for $306,520

Rep. Mike Kelly (R-Pennsylvania) for $974,100

Rep. Vicki Hartzler (R-Missouri) for $451,200

Only neediest and the Greediest Get Feed

Rep. Markwayne Mullin (R-Oklahoma) for $988,700

Rep. Carol Miller (R-West Virginia) for $3.1 million

Why did you leave out all the Democrats who received PPP loans?

People expect more from GOPers.

Wolf, you mentioned that only a tiny amount of the spending wasn’t paid off in full and added to the interest-bearing debt but I didn’t see where this percentage was delineated.

Those who paid off their balance every month were always referred to as “deadbeats” by the credit card industry. There used to be stats on this if I remember correctly.

Side note: I’m very curious if there is a statistic about average job applicants per job opening or posting. Given the concerted effort to exclude discouraged workers from BLS tabulations, I wonder if a survey of the number of applicants per opening might show a deeper picture.

1) Visa is down since July 2021, down below Oct 2020 low. MC is

down since Nov 2021, under 2018 high.

2) Every month, on a certain day, online banking take care of our debt.

Consumers piled so much debt, c/c debt pale in comparison to all other

debt.

3) Creepto sucked hundreds of billions from US consumers. Creepto

market cap fell by over $2T. Most creepto investors are Z gen and millennial. Their confidence in the system is shaken.

4) Retailers are loaded with merchandise to sell. Retailers and department store c/c charge 30%/y. That’s how they make money.

5) Online co don’t have salesmen that know how to pull c/c out of customers pockets.

They use data to get us, but data is no match to human touch.

6) US gov debt ceiling might rise in Dec. The Fed will stick to it’s negative rates policies. TY might dive. Inflation might flare in 2023/2024.

This article plus the very good retail numbers this morning are extremely bullish even with the higher rates. If anything it shows that the economy is doing just fine with “normalized” interest rates and high inflation. I’m not even sure there’s anything the fed needs to fix anymore. The fed will raise some more but not enough to push down actual prices and kill employment. Sure poor people are having a tougher time of it but tell me when that wasn’t the case.

I understand this point made by Wolf, “And that dentist likely pays 7% APR on his $100k, and the poor schmuck pays 30% on his $1,000. That’s how credit works.”

But I have to wonder if the transition sometime in the 80’s or 90’s from normal interest rates on CC to the ultra high rates now, have killed the golden goose for CC issuers. Particularly after many people got hurt during the GFC. If they charged somewhere around prime+few % instead of 19%, probably more consumers would run balances month to month on their CCs. The issuers have made it so prohibitive to do that. Article in today’s WSJ noted the rise of HELOC borrowing and one reason cited was the favorable interest rates compared to CCs.

I came across the HELOC stat from WSJ too, it said about a 40% increase in applications over last year. Not sure what the significance of that is given the strange times we are in. Anecdotally though I feel you could be right, my sis for instance doesn’t own a home so no HELOC, but she’s in debt since the 3rd yr of Uni when my parents savings for that purpose ran out, that was like 8yrs ago, and she pays off her CC in full all the time.. using her Bank LOC because the % is about 1/3 her CC would charge. She also pays some of it using bank of MomDadBigBro but that is another story.

Here are the HELOC balances. They finally stopped dropping, that’s what happened:

Is it it possible that a lot of these cc balances that are paid in full and counted in the statistics are being paid by their credit line at much cheaper rates?

IMO the consumer is on shaky ground. With credit card balances at all time highs, and delinquency trending up sharply, the indication is that people are struggling with inflation.

The fact that they are up to their eyeballs in debt other than credit cards, is not a positive indicator either, especially when the value of what they owe that money on is diminishing daily. The trick of draining the strategic reserve to bring down oil and the inflation it impacts is now over and every indication is that oil is on its way back up and taking inflation with it. Energy is the key to inflation, and so long as governmental policy is to wage war against energy both domestically and internationally, the inflation will continue to outpace wages as it has done for 19 straight months.