QT’s impact on the Fed’s liabilities, and the massive movements between them.

By Wolf Richter for WOLF STREET.

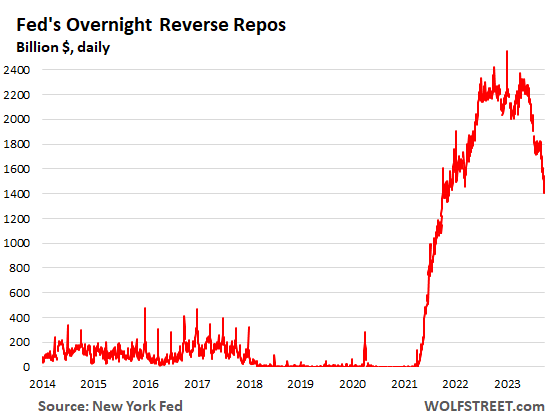

The daily measure of Overnight Reverse Repurchase agreements (ON RRPs) at the Fed have plunged to $1.40 trillion as of Friday. This is down by 45%, or by $1.152 trillion, from the one-day-wonder peak on December 31, 2022.

Under these RRPs, the Fed takes in cash and hands out collateral (Treasury securities). RRPs are a liability for the Fed because they’re cash that the Fed owes its counterparties. The counterparties are mostly US money market funds, but also banks, and government-sponsored enterprises (Federal Home Loan Banks, Fannie Mae, Freddie Mac, etc.). These counterparties use ON RRPs to park their extra cash risk-free at the Fed, and earn interest. As of the rate hike in July, the Fed pays them 5.3% in interest.

This 5.3% is less than what the Fed pays banks on their reserve balances (5.4%), so banks don’t use RRPs much. For money market funds (MMFs), ON RRPs are a good risk-free deal, but they pay a little less interest than Treasury bills (around 5.5%). And MMFs have been yanking their cash out of these RRPs, to load up on T-bills.

Which Money Market Funds?

The Fed started paying interest on RRPs in the spring of 2021, minuscule rates of interest at the time, at first 0.05% APR and then 0.1% APR because policy rates were near 0%. It did so because there was so much liquidity in the financial system as a result of the then still ongoing QE, chasing after everything, that T-bill yields dipped into the negative.

Treasury money market funds that primarily invest in T-bills were threatened by these negative yields; they could cause the MMFs to “break the buck” where the Net Asset Value of the fund drops below $1, which could trigger a run on the fund, forced selling by the fund, the collapse of a fund, contagion from there, etc., etc., you know the financial panic routine. The Fed’s solution was to pay a little interest on RRPs, and MMFs flocked to them, and with each rate hike starting in March 2022, the Fed paid more on RRPs.

In addition, MMFs switched some of their cash that they need for liquidity reasons from their bank accounts to RRPs, since banks paid 0% interest, and even now are stingy with the interest they pay. This shift from banks to RRPs via the MMFs caused the banks’ reserve balances to fall starting when QE ended. More in a moment.

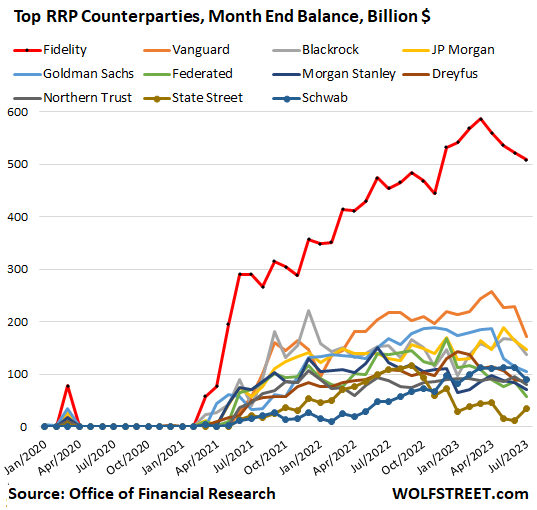

The government’s Office of Financial Research publishes RRP balances by money-market funds on a monthly basis, unfortunately with a big delay. The most recent release was for July 31, by which time MMF participation in RRPs had dropped to $1.75 trillion.

The biggest providers of money market funds lead the list: About 29% of these RRPs were with Fidelity’s funds ($508 billion); 10% were with Vanguard’s funds ($172 billion); 8.4% were with JP Morgan’s funds ($148 billion); and 7.9% were with Blackrock’s funds ($138 billion):

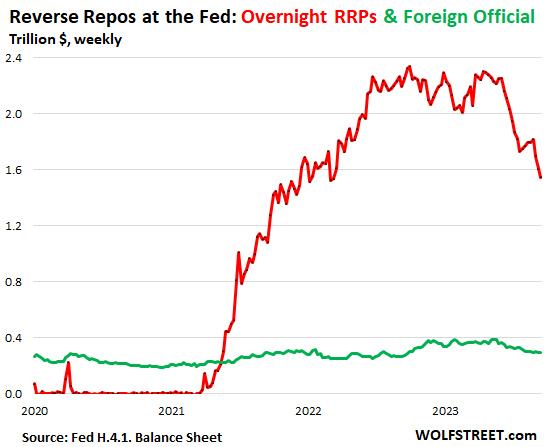

Foreign official RRPs and ON RRPs.

The Fed also offers RRPs to “foreign official” accounts, where other central banks can park their dollar cash.

The weekly balance sheet of the Fed – the latest was released Thursday afternoon – shows only balances as of Wednesday every week, not daily balances. So these are balances through Wednesday, which have not yet captured the las two days of the plunge in RRPs.

Foreign official RRPs dropped to $289 billion, down by $94 billion, or by 25%, from the peak in January 2023 (green line).

The chart also shows the ON RRPs (red line) as of Thursday’s balance sheet ($1.546 trillion). Since then, ON RRPs have plunged by another $145 billion, which is reflected in the daily chart above.

Both combined – ON RRPs and foreign official RRPs – have plunged by $803 billion, or by 33%, from the weekly Wednesday peak last September:

Rising/falling reserves & RRPs don’t negate effects of QE/QT. They’re part of those effects.

The fact that liabilities (mainly reserves and RRPs) rose during QE in equal measure with assets did not negate the effects of QE. And the fact that liabilities have fallen during QT in equal measure with assets does not negate the effects of QT. That’s just how a balance sheet works – it always stays in “balance.”

Massive shifts among the liabilities on the Fed’s balance sheet.

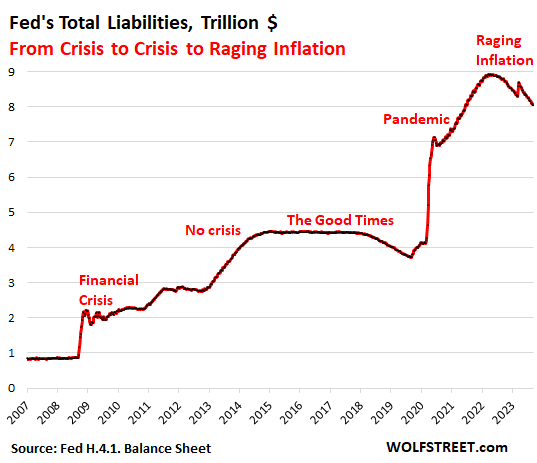

Every balance sheet has assets, liabilities, and capital, where: Assets = liabilities + capital. The Fed’s capital is limited by Congress, and it changes only in small ways. But its assets and liabilities change massively.

On the asset side of the balance sheet, QT is proceeding at a record pace; the Fed has shed $867 billion in assets since the peak, now down to $8.099 trillion.

On the liabilities-and-capital side, the Fed has shed $868 billion in liabilities since the peak in April, now down to $8.056 trillion; and it increased its capital by $1 billion to $43 billion.

But there have also been massive shifts between liabilities, with some rising and others falling that we’ll get to in a moment.

The four major liabilities:

- RRPs (discussed above)

- Reserves

- Currency in circulation (paper dollars)

- Treasury General Account (TGA), the government checking account.

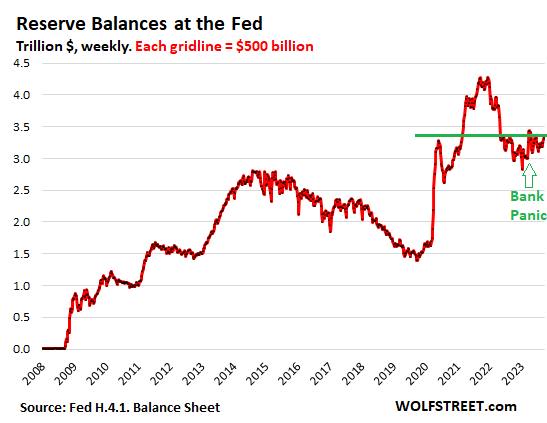

Reserves: $3.33 trillion, -$940 billion since Dec 2021 peak. But +$337 billion since the March bank panic.

Reserves are cash that banks put on deposit at the Fed, and are a form of instant liquidity in the banking system. Reserves are a liability on the Fed’s balance sheet because the Fed borrowed this cash from the banks. Since the rate hike in July, the Fed pays banks 5.4% in interest on their reserve balances.

Banks, on their own balance sheets, don’t call them “reserves,” but “interest-earning cash,” or similar. They’re assets for the banks. They use their reserve accounts at the Fed to transfer cash between banks, to do business with the Fed, to have liquid cash available when needed, and to earn 5.4% interest.

Reserves have risen since the bank panic in March, after falling sharply for the prior 15 months.

QT is draining liquidity from the financial system, and reserves are one place where the drainage showed up. But the March bank panic – Silvergate Capital, Silicon Valley Bank, Signature Bank, and First Republic toppled – caused banks to increase their liquidity, and they put some of this cash on deposit at the Fed as reserves.

QE ended in March 2022. QT started in July 2022. Note the sharp drop in reserves from December 2021 until the March 2023 bank panic, and then cash started flowing back into reserves:

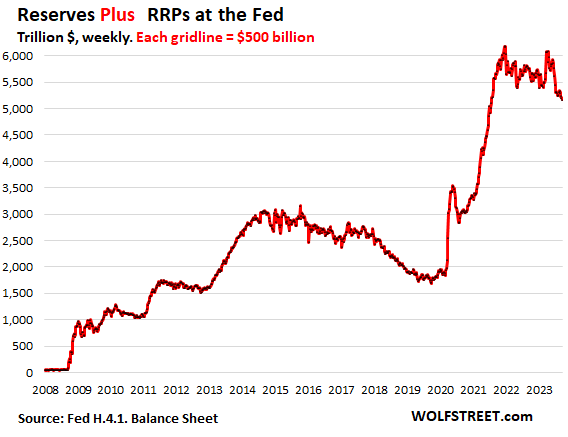

Reserves plus RRPs: $5.17 trillion; -$1.01 trillion from Dec 2021 peak.

Since there are big shifts of cash between reserves and RRPs via the MMFs, it makes conceptual sense to look at them together to see the combined amount of liquidity that is getting drained out of the financial system via QT.

The pandemic-era QE had inflated the combined total of Reserves plus RRPs by $4.2 trillion, to $6.18 trillion in December 2021.

Since that peak, the combined balance of RRPs and reserves has dropped by $1.01 trillion, or by 16%, to $5.17 trillion

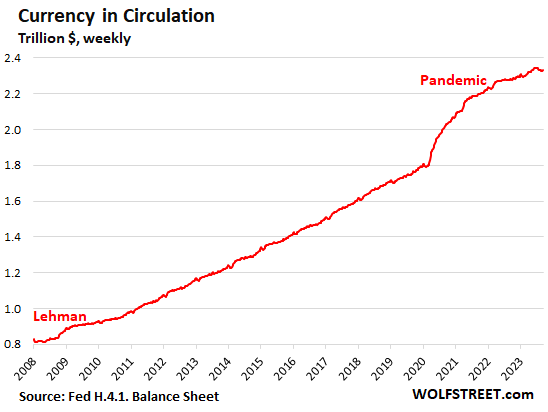

Currency in circulation dipped to $2.33 trillion.

Currency in circulation reflects the paper dollars in wallets, under mattresses, and in safes in the US and globally. Various studies show that the majority is overseas.

The amount of currency in circulation is demand-based through the US banking system. If customers demand paper dollars, the banking system must have enough on hand. Foreign banks have relationships with US banks to get dollars for their customers.

These “Federal Reserve Notes,” as they’re called, are a liability for the Fed. Banks get those paper dollars from the Fed in exchange for collateral, such as Treasury securities, which are assets on the Fed’s balance sheet.

That’s one reason why the Fed’s assets increase when there is no QE and no QT: demand for currency must be met by banks, and in return banks must post collateral at the Fed for those amounts, which are assets for the Fed, and its assets rise in part with the rise of currency in circulation.

Before QE, currency in circulation was the primary driver of the increase in assets on the Fed’s balance sheet through the collateral (Treasury securities, etc.) that banks have to post to get these paper dollars.

Currency as payment methods for legitimate purchases is increasingly being replaced by electronic payment systems (credit cards, debit cards, ACH, Zelle, PayPal, etc.). But demand for currency was huge during the pandemic. When there is fear of a crisis, demand for paper dollars surges: before Y2K, after the Lehman bankruptcy, and massively starting in early 2020.

Demand for currency in circulation has now stabilized, as some people return their paper dollars to the bank to then earn 5% interest on their electronic dollars.

Since the peak in early June, currency in circulation has dipped by $14 billion, to $2.33 trillion.

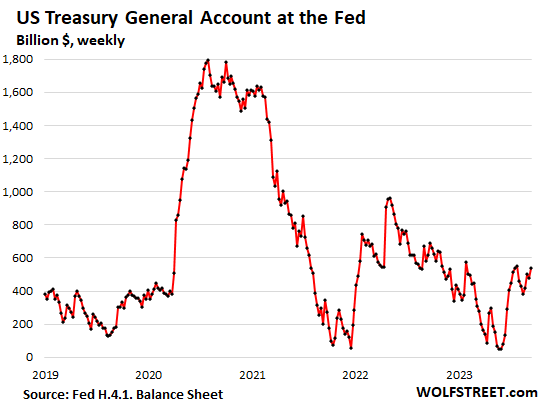

Treasury General Account (TGA): $537 billion.

The Treasury Department is unleashing a tsunami of new Treasury notes and bonds to fund the government deficits and to raise the balance of the TGA account, the Treasury Department’s checking account a the Fed.

The amount in the TGA account is a liability for the Fed – money that the Fed owes the government.

The Treasury Department said that it wants to end Q3 with $750 billion in the TGA. September 15 was the day estimated taxes were due, and so over the next two weeks, those tax receipts will show up in the TGA and push up the balance. As of the Fed’s balance sheet on Thursday, the amount in the TGA was $537 billion.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

From Wolf post:

“The Fed’s capital is limited by Congress, and it changes only in small ways. But its assets and liabilities change massively.”

I understand that Fed assets have mushroomed since approximately the GFC, as shown in you Total Liability chart (and recognizing the speck-sized contribution of capital in the Assets = Liabilities + Capital equation).

Fed assets as a percent of GDP ranged around 5% for decades prior to 2000, but is closer to 20% now.

– What is a “reasonable” goal for Fed Assets as Percent of GDP? -How long should it take to get there?

-What has changed in the financial world that justifies a substantial increase in the footprint of the Fed?

Thanks

As soon as Bernanke mentioned the benefit of a “wealth effect”, somebody should have escorted him off the stage.

It’s all built on a continuation of artificil stimulus. Any fool can see it ends with hyperinflation or a reverse wealth effect, with a lot of arbitrary, counterproductive, and destabilizing societal transfers along the way.

It’s a massive Ponzi, really.

Absolutely. He should have been flogged in the public square. Instead the POS gets the Nobel Prize.

Same way that 44 got the Nobel Peace Prize and had the committee admit that it was a political statement.

Nobel is a joke at this point.

Even though most politicians, economists, and mainstream pundits won’t admit it, central banks exist to help governments finance themselves by stealthily transferring wealth away from the average person’s savings.

It’s the hidden, but real, reason why central banks exist.

It’s Congress’s job to control growth and wealth allocation through taxes, if and when it chooses. These are the elected officials. The Fed illegitimately assumed control over economic policy and has become an interventionist organization doing the bidding of speculators and asset holders.

Hence, smart guys like Wolf have to spend time trying to analyze their crazy unfounded policies and next moves. The Fed’s balance sheet wouldn’t even be the topic of discussion in a productive sustainable monetary environment.

Then Congress should take up their responsibilities again. They can any time they are willing.

Yes, the “King” Bernanke named popped into my mind too. Paulson

and Bush should’ve been escorted off the stage along with him. I feared Bush would leave us with such a legacy and didn’t vote for him. My

impession was Bernanke was seeking to make a name for himself with his “new economics” at the Ivy Leagues. He had yet to learn there’s nothing new under the sun and everything’s old again, including retirees.

The Bond Market Has Never Sounded Recession Alarms for This Long

10-year yield has been below 3-month rate for 212 trading days

‘Ignore the signal at your own risk,’ Duke’s Harvey says

https://www.bloomberg.com/news/articles/2023-09-14/the-bond-market-has-never-sounded-recession-alarms-for-this-long

Wolf,

I am going to greatly enjoy watching you eat crow…. You deserve to choke on the bones for being such an utter asshole by denigrating anyone who has the audacity to post facts that run counter to your opinions.

Bloomberg’s bond market recession calls have been dead wrong for 18 months. You can see the reporter’s frustration with the stubborn refusal of the economy to follow the inverted yield curve into a recession. Look at the last part of the title: “The Bond Market Has Never Sounded Recession Alarms for This Long.” And “The 10-year yield has been below 3-month rate for 212 trading days,” and there is STILL NO RECESSION. You see how frustrated these recession mongers are getting?

People have been saying the same stuff for a year-and-a-half: In the spring of 2022, they said, recession in H2 2022 because the US economy cannot handle 1% rates. Ok, fine, no recession, but it will come in H1 2023 because no way in hell that the US economy can handle 5% policy rates. Ok, that was a dud, but then a recession in H2 2023, because you know… So H2 2023 is nearly drawing to a close and there is still no recession in sight; Q3 looks hot. Jury still out on Q4. So now most recession mongers buried their H2 2023 recession bet as well, and put out a new recession bet for 2024… It never ends.

All along I’ve been on recession watch. I looked at the economic data, and not at the BS floating around out there, and all along there was no sign of a recession, and there is still no sign of a recession — and I said so.

I also said a gazillion times that there will be a recession someday, because eventually there ALWAYS is a recession, and Wolf Street has been on recession watch ever since March 2022, when the Fed started hiking rates, and we’re still on recession watch here, and when the actual economic data starts pointing in direction of a recession, you’ll see articles about it here, and I’ll put it into the headlines, and I’ll make hay with it because recession articles get a lot of clicks.

But for now, economic growth has further accelerated, and the economic data does not point at a recession, and we’ll just have to be patient and watch the data, and not get hysterical.

The yield curve is NOT economic data. It’s a result of the Fed in the bond market. This has been the case since 2008 (QE). The inverted yield curve is a result of the Fed pushing up the front end of the curve (to 5.5%), while the long-term bond market is following, but lags behind, in part pushed down by the still ginormous weight of the Fed’s bond holdings. That’s not a secret.

Wolf is too classy to respond to your fucking bullshit, but I’m not. Hey, If you don’t like this website, go away and never come back!

KML,

And you will choke on a cock and die. But no one will know or care.

Ken

Surely you are not claiming that the current bond market, after 15 years of Fed suppression, which continues, is suddenly an accurate indicator of anything other than the suppression of the interest rates by the Fed’s engorged balance sheet.

It is unclear which bones Wolf deserves too choke on that you are praying for as opposed to his posting of the facts. You remind me of my friend Chris who passed away as a result of untreated syphilis.

Wolf, and is the recession on the threshold in Europe? What do you think?

Why are you on this website, if that is how you feel?

KML – …remember that you are always free to start YOUR OWN blog, complete with its own rewards (and Scyllas &Charibdys’). As ‘Scoop’ Nisker (newscaster on the long-ago-and-lamented Bay Area KSAN radio station) always said at the end of his signoff: “…if you don’t like the news, go out and make some of your own…”.

may we all find a better day.

Perhaps. One has too remember that the mark (the American Taxpayer) was unaware that the banking industry fraud was so immense that had the capacity too crash the financial and asset markets. We were being told by the Fed and the Treasury that scummy people had taken out loans they couldn’t afford and were now refusing to pay the kindly bankers.

Well, in the fullness of sunlight, we are beginning to realize how badly we have been had. While continuing too be had, choosing yesterday’s transgression to complain about rather than today’s.

The Fed is still screwing everyone whose income and wealth is less than the top 5% of citizens.

The Fed balance sheet is a disgrace no matter how much lipstick one put’s on that pig. Money has been manufactured, distributed, and circulates among the worthy.

Meanwhile, the unworthy struggle which is concrete evidence that they are unworthy. So what if they actually fought, in battle, America’s enemies. That was before.

dang, dang! I do admire your elegant turns of phrase…(particularly like ‘…yesterday’s transgressions’…, illuminating how we so often prefer to argue over how the hole in the hull got there instead of staunching the flow and mending the breach…).

may we all find a better day.

I am not defending Bernake because he was a eff-up, but you are wrong saying this ends with hyperinflation.

4-6% inflation is not hyperinflation. Not even close.

John H.

Fed’s assets (nominal) to GDP (nominal) are now around 31%. This chart shows you how much further the assets might drop, in terms of GDP. I think 15% might be possible over the years.

Nothing justifies the proportional increase in the footprint of the Fed. As a result, we now have the worst inflation in 40 years, and it’s going to be tough to get rid of

As always, a very good analysis of how the Federal Reserve and the banking system works.

Maybe I should say that it’s not working very well for us since we now have excessive inflation, unless that’s how our Government wants it to work.

That’s a scary thought for citizens of the land of the free.

The government dedicated too concentrating the wealth of the nation to an aristocratic elite that is unsympathetic to the plight of the every day people.

We really should do something about that.

However, I will point out that the Fed, which is the banks whore, is out of reach of the average conscript. And it isn’t even an agency of the government.

Not too mention the so called Supreme Court of the United States. A partisan elite without shame.

Thank you for using “Federal Reserve” lingo…the use of “Fed” of “the Fed” automatically mis-translates to the federal government and I go into confusion.

From my historical understanding, I am well aware of Woodrow Wilson’s terminal syphilis and how Warburg et al and rigging the 1912 election* got Congress to pass FedRes legislation and Wilson signed it. The current state of accumulated

economic insanity is the direct result.

Here is a clue to the financial/economic craziness.

The historical source is traced to this fact:

Before there was money, there was credit/creditors and debt/debtors.

Arguably, a corollary might be that “creditors”

described the class that figured-out how to game any system of governing. To wit, the FedRes.

*re: 1912 election. Teddy Roosevelt, a former Repub. Pres., decided to run against incumbent Repub. Taft for Pres. and split the Repub. voters so that Dem. Wilson easily won…and would push to create the FedRes.

Thanks for the clarification Wolf.

I’m thinking that downward blip in the chart above, followed by the Pandemic/Raging Inflation spike are the epitome of your slogan that nothing goes to heck in a straight line.

The Chinese curse “may you live in interesting times” comes to mind…

We had worse inflation in 2000 to 2008, it was just that people who write about inflation own at least one house and so we’re perfectly happy to accept that the main expense for most people was not necessary to fully include into inflation statistics. Now that inflation has Fed through into things they buy the noise has begun.

Where do you dream up this garbage? Math is math. Go ahead and diss the methodology (I do), but everything in your post is just…silly.

This is exactly right, people who own houses are cheering when their house prices were going up, but now that insurance, taxes, food and other items are going up now they’re unhappy.

All the equity that they’re cashing out from their house was actually transferred from savers.

> math is math

they include imputed rent but not the actual price.

right now Canadians are finding out that we *did* have house price inflation, it was just the calculation said there was none *if interest rates stay at record lows forever*.

Turns out they didn’t, now people are paying the real price of that housing.

You need to take a look at the M1SL long term chart money supply. It EXPLODED 1quarter of 2020 by a factor of 5Xs and peaked May, 2022. Today it has dropped a whopping 10-12%. Note : The Real Estate market peaked June, 2020 and today Nationwide is down 16%. What the Hell is going to happen when this supply reverts to the long term trend line ( MILES BELOW )???

M1 and M2 primarily measure bank deposit liabilities and Fed-held assets, denominated in dollars, which are not US currency.

Here’s a fun little fact, it is against the law (12 USC 411) for the Federal Reserve to use US legal tender currency in any of its market operations.

Exercise: Pull up the Fed’s M1 chart and add a line ‘currency in circulation’, add M2 also. The ‘currency in circulation line’ represents the true and official US legal tender money supply, everything above that line is Fed and bank-induced credit inflation, not US money.

The reason a recession has not hit yet is because households and corporations are sitting on mountains of low interest debt taken out during ZIRP. However, their counterparts, the banks and non-banks, and the Fed, are sitting on underwater assets. A massive refinancing wall is going to hit, and then the assets are going to reprice lower. Either crisis, and more monetization, or a long deflationary drag, with high interest rates! Grab your popcorn, this is just now getting started!

Unemployment is still at record lows.

Unemployment rate is 3.8%. It was as low as 3.5% right before the pandemic started. Healthy unemployment rate is between 4% and 6%.

I am not sure how high it may go for the next recession, but we have a way to go for unemployment to get to that point.

I suspect when it reaches around 5.25% then we may be near the middle of the next recession.

If I remember correctly, the high point of unemployment in Weimar Germany was 4%. But after 1924 it went down.

Re: Weimar – “superhero” films were all the rage then too; Caligari, Golem, Nosferatu, Schatten, Phantom, Metropolis. The guiding theme being some all powerful strongman pulling the strings while the powerless simply obeyed. (not an original thought – See Kracauer’s “From Caligari to Hitler” for more).

Ironic how all that worked out for them, but somewhat concerning to the current state of both domestic cinema and politics…

“The reason a recession has not hit yet is because households and corporations are sitting on mountains of low interest debt taken out during ZIRP.”

Something like that. The economy is structured in such a way that total debt must continue to increase, and that’s without having any handle on that black hole called the derivatives market. The FIC will simply continue to kick the can down the road until they run out of road. There’s no interest in actually fixing the problem.

Worse, and beside your point, most of that debt is unproductive and merely finances the increasing overexploitation and depletion of our primary asset, the productive capacity of the natural world. Very little is invested to preserve it, much less enhance it. That depletion is treated as an economic externality and is largely ignored by decision-makers, so reversing the relevant path dependencies is just happy talk and won’t happen, but it no longer matters. The timelines have been very well-established for a long time. Iacta alea est. It’s too late.

Sorry.

Unamused: Yes, I had a long-time chum who was excited about “fixing” the planet in our school days, and spent his life as a marine biologist. By the end of his time he was saying the same thing as you, that human life was hoplessly destructive at best and that the planet couldn’t begin to heal until the last one of us was gone. Then he left, gifting his home and land to an adjacent nature preserve by the sea.

I came up with a video game about Saving the World but nobody wants to market it. You can imagine why.

-sigh-

Mental illness is a terrible thing.

“business is business! And business must grow regardless of crummies in tummies, you know.”

Mr. Lorax

Canada is hitting this now as many are on variable rates or renewing fixed 5 year rates.

It’s going to be epic.

Canadians think BoC can do yield curve control, I’m doubtful, CAD is tiny they can’t dictate like boj.

Not directed at u but the mention about households sitting on covid or low interest zirp debt, Perhaps I am uninformed but how could this be the case. are you referring to covid small biz loans, there wasn’t any wide reaching liquidity program for households. I hear this reference all the time and have no clue what is being referenced.

Please educate me

Alternatively,

The reason that a recession hasn’t hit is because there is an enormous reservoir of subsidized low interest rate cash available too purchase whatever like share buybacks, the ultimate evidence of loose goose stimulative monetary policy.

If the Fed were serious they would extinguish their excess cash balance sheet immediately. But no. That would crash the bubbles that they created,

Somewhere along the line, the Ivy League government decided that the population needs to suffer so that the rich and the speculators don’t lose their bets. No matter what.

And the population, competing with Walmart’s Chinese hoard, were in no shape to compete with a monopolist labor provider like the Chinese Communist Party.

The reason there isn’t a recession is that people are seeing crazy wage increases and have lots of personal wealth (even if it might be in inflated assets)

It is that simple.

I’ve given up expecting a recession while the US Federal government is running such large deficits.

Amen. The Fed’s bumbling attempt to pretend to try to tame inflation is becoming almost a satire, as is our economy, with hilarious moments: A rating agency just now downgraded a certain country’s imploded, property sector. No doubt, it is considering lowering its rating on Enron too. LOL

Wolf, a question.

Understood that in RRP “, the Fed takes in cash and hands out collateral (Treasury securities)” and pays 5.3%.

Who is getting the interest on the Treasuries? Doesnt the Fed get the interest on the Treasuries involved in the RRP. So the Fed paying 5.3% out is offset by what they are receiving in Treasury interest payments?

Thanks

So less RRPs, but the counter parties are out buying TBills ….

so either way they end up possessing Treasuries, right?

So the Fed reduces their involvement, but the money is still “soaked up” by govt debt, yes?

With bank-held savings being transferred through the MMMFs, and O/N RRPs being exited, liquidity is increased. That’s why Atlanta’s GDPNow is @4.9%

Both sentences are nonsense.

Like I said in 2007, I don’t need a disclaimer.

1. I explained in the article why the first sentence is nonsense.

2. The second sentence is nonsense because an increase in liquidity goes directly to the financial markets (higher asset prices), and does not feed into the factors that feed into GDP: it does not increase consumer spending; it does not increase business consumption and investment; it does not increase government consumption and investment; it does not increase exports; and it does not impact inventories. GDPNow reflects data inputs from those factors. The GDPNow is hot because consumers and businesses and governments are all spending and investing more, and exports are up too.

The sharp drawdown of the RRP can go a long way in explaining how the re-fill of the TGA has played out relatively uneventfully. At this rate, it can continue to sop up T-bill issuance for years.

In the big picture view, the giant pile of money left over from the pandemic helps explain why the Fed’s sharp interest rate increases don’t seem to have affected the economy to as negative a degree as some were expecting.

An interesting question is how will T-bonds behave as the Treasury begins issuing a flood of those (and while the Fed is simultaneously conducting QE). Given the duration mismatch, the RRP isn’t likely to be a source of funding for those longer-dated securities.

Wolf:

The Fed at one time only purchased Treasury securities, correct?

The Fed at one time, did not by long duration, correct?

The Fed has bought a lot of duration now, and has Hugh unrealized losses on its portfolio just like banks, correct?

The Fed buys duration to implement policy like operation Twist?

The Fed bought long term MBS for the purpose of lowering long term interest rates, correct?

If the Fed stuck to lender of last resort and did not buy long term debt and MBS, then other market participants like banks and life insurance companies would have bought such securities instead of Fed?

What is the net effect of Fed buy non treasury securities and also buying duration?

When the Fed buys securities, the net effect is asset price inflation almost immediately. And eventually consumer price inflation, as we now see.

That used to really bother me, but I take a pill for that now.

unamused,

Nice to see you back. I miss the days when you would embellish your comments with lyrics. I hope it’s not the pills.

One pill makes you larger. My pill makes me small. And you shouldn’t encourage me, Root Farmer.

Draftsman, draftsman,

What do you draw?

Dog days. Draggy days.

Days of straw.

In case you’re interested in emigrating from the US to, say, Canada, despite the sky-high real estate prices, it can cost upwards of a million US a head. New Zealand, two million. Government policy is to discourage emigration from the US. We checked. A high-paying professional skill is generally required unless you have very substantial investment income.

Then we will see stagflation where the real GDP stagnates and inflation still is raging. The only difference is this time many other nations are lining up to permanently fill the vacuum created the US Federal Reserve’s monetary policy.

Yield curve is still inverted…but it is steepening now.

We’ve had some nasty events when the curve reversed up into positive (1990, 2001, 2008, 2020)

There was always some “trouble” 6mos-1yr in advance the Fed had to deal with, and then declare everything fine. After which, kaboom.

CRE seems to qualify today.

You said the curve is a result of the Fed in the bond market. Perhaps the curve is showing that.

By the time recession data is conclusive, it may be too late for the stock market.

On the other hand, big bull markets began after the curve flattened against Fed panic rate cuts, then resumed steeeping long term.

Eric,

You need to take 2020 off your list. That wasn’t a business cycle recession, which is what the yield curve is supposed to predict. That was a pandemic and lockdown that had nothing to do with the business cycle.

Yes, and when they sell securities it’s the opposite effect. So, with ongoing QT who’s going to step in and buy US Treasuries and at what price? TBD. If the Federal Reserve really wanted to slow things down it could sell securities.

1) In Jan 2008 Fed Asses were 895B. Fed Debts were 857B. After the raids

in Jan 2015 Fed Assets were 4,507B and Fed Debts were 4,450B. The Fed used its Assets to finance the gov, suppress interest rates and mortgage rates. The Fed became more powerful than ever before.

2) In Aug 2019 Fed Assets were 3,773B. Fed Debts were 3,734B.

In Feb 2021 Fed Assets were 7,500B. Fed Debts were 7,461B. The money was legally borrowed by the Fed from the banks for an IOU. The gov

borrowed from the Fed for an IOU, but the gov spent it. The money is gone.

3) In Aug 2008 total commercial bank deposits were 6,800B. In Oct

2008 it popped up by 800B to save the banks. In 2020 it leaped vertically.

Commercial banks were flooded with money when our econ was comatose until “we know what we don’t”.

4) In Aug 2021 cash deposits exploded to 17.4T. Cash deposits rose

from 6.8T in Aug 2008 to 17.4T in Aug 2021, up 10.6T in 3Y. Consumers and companies had an extra 10.6T in the banks. The banks had 10.6T extra cash to invest. Total ==> 21.2T in cash. 10.6T in new money was created. No printing. Part of it financed the gov, the rest for speculations.

5) In….

#1 and # 2 are nonsense. What does it say in the article about a balance sheet, any balance sheet, including the Fed’s? That it MUST and WILL ALWAYS balance.

Quoted from the article:

“Every balance sheet has assets, liabilities, and capital, where: Assets = liabilities + capital. The Fed’s capital is limited by Congress, and it changes only in small ways. But its assets and liabilities change massively.

“On the asset side of the balance sheet, QT is proceeding at a record pace; the Fed has shed $867 billion in assets since the peak, now down to $8.099 trillion.

“On the liabilities-and-capital side, the Fed has shed $868 billion in liabilities since the peak in April, now down to $8.056 trillion; and it increased its capital by $1 billion to $43 billion.“

Oct fest started.

Basically the M1 money supply exploded and at its peak was up nearly $20TT in 10 years and is now down slightly. But how much have total assets increased during the last decade?? $50TT $100TT?? maybe more?

“Banks, on their own balance sheets, don’t call them “reserves,” but “interest-earning cash,” or similar. They’re assets for the banks.”

Would these reserves not be liabilities to the banks? Or is this cash their own money rather than customer deposits?

“Would these reserves not be liabilities to the banks?”

No. Cash and cash-equivalent on any balance sheet is the top asset, it doesn’t matter where that cash comes from. Bank cash on deposit at the Fed (“reserves”) is pure cash for banks that now earns 5.4%.

Keep in mind, always: one entity’s financial asset is another entity’s debt. So bank cash on deposit at the Fed is an asset for the banks and a liability (debt) for the Fed.

The banks have a liability called “deposits” on their balance sheet. This is the amount they owe their depositors. So when you put $100 in the bank, the bank credits your deposit account with $100 (increases the amount it owes you); and it debits its asset account “cash” with $100 (increases its cash balance by $100). The bank can then do whatever with this cash, including putting it on deposit at the Fed.

If the bank puts this $100 on deposit at the Fed, it credits its asset account “cash” with $100 (lowers its balance) and debits its asset account “interest earning cash” with $100 (increases its balance). So overall, the bank’s assets don’t change when it puts $100 on deposit at the Fed, but the $100 shifts from one asset account to another asset account.

A basic accounting course (where you learn about debits and credits) at your junior college is the best investment ever. I encourage everyone to do that.

Isn’t the Fed paying of “Interest-On-Reserves” (IOR) both a fairly recent development, and a spirited debate?

Allowing IOR was unthinkable for many decades of the existence of the Fed because it encourages/subsidizes commercial banking by enhancing profits and stimulating more (or more aggressive) lending.

In the old days (pre 2008), banks earned the same amount on reserves held at the Fed as they earned on their vault cash… ZERO. That seems the superior systemic rule, because banks are thereby encouraged to avoid foolhardy expansion.

Again, did something in the financial system change during the Great Recession that made paying IOR by the Fed to it’s depositors a good and permanent practice?

1. “Isn’t the Fed paying of “Interest-On-Reserves” (IOR) both a fairly recent development…?”

Since Oct 2008, authorized by Congress by the Emergency Economic Stabilization Act of 2008. Essentially with the start of QE 15 years ago, not so recent, I’d say.

2. “…and a spirited debate”

Yes.

3. IOR was an attempt to solve the problem of banks not knowing what to do with their cash. In the early days during near-0% policy, IOR was a minuscule rate that didn’t add up to much. It only becomes a big issue when policy rates rise.

4. “…did something in the financial system change during the Great Recession that made paying IOR…”

Yes, QE arrived and created massive amounts of excess liquidity.

Texas RenFest is the largest renaissance festival in the country, visited

by 500,000 people who mock dons and kings. Wine and beer tasting,

beer mugs for donations

Micheal Engel- I was going to Magnolia, TX, for the falconry before Renaissance festivals were mainstream. Quite a few now. Tuxedo/Sterling Forest in New York has had a good faire for decades, and the Hood Faire alongside the river Dart near Totnes on the Devon/Cornwall border in 1979 is a cherished memory.

Congress spends money that they don’t have.

The Fed prints that money through monetization aka buying treasuries and printing currency. The public decides how much currency they want and in what denominations.

Hyperinflation is in the cards. We just don’t know when they will be dealt.

Cheers,

No. That is not how it works at all, except in your delusions.

I find it hilarious how many people keep wishing for hyperinflation despite a complete and utter lack of any evidence supporting it.

I never actually believed people were into being spanked and whipped, but some of the comments in this blog have provided good insight.

Good article.

2021- The year of the Milton Friedman. He’s watching over us and saying “Now look at that mighty inflation you have here!”

Personally, Milton Friedman was a raving lunatic that envisioned two macroeconomic relationships that seem to be valid amongst his thousands of crackpot conjectures. Not what I would call a trend.

He was right about inflation though. How low interest rates can worsen inflation.

The low interest rates to take on loans, and the excess stimulus for both businesses (PPP loans), and individuals (pandemic benefits) caused prices to go up for Pokemon cards. People were getting more from pandemic benefits than working or unemployment, and a few went FOMO on the stonk markets.

dang

“Personally, Milton Friedman was a raving lunatic”

care to REALLY explain?

Go and watch Dr. Friedman dismantle Phil Donahue’s positions (probably yours as well) on youtube

He is dead right when he connects money supply to inflation…..and Powell’s dismissal of the M2 explosion is an example of people ignoring Friedman’s observations.

Curious how certain figures are attacked post mortem. He defended himself and his theories very well when alive.

No, Friedman was only good at math. Friedman was “one dimensionally” confused.

What is there to dispute? An increase in money supply is inflation, which will hit the CPI sooner or later, and there is no doubt about that.

The Fed obviously does not understand this because its monetary policy is soooo contradictory. On the one hand, Bernanke said QE creates a wealth effect that increases asset prices and stimulates demand (i.e., creates inflation). Then the Yellen/Powell Fed denied that QE is the cause of asset bubbles and wealth concentration.

The public deserves cautious, consistent, thoughtful monetary policy, not excessive fiddling and wanton experimentation.

Howdy Folks. Just imagine if you could control that kind of $$$. Oh, well, just an old fool not as smart as these folks…..

Wolf….thanks for connecting the financial/balance sheet dots.

In the larger scheme of things (i.e., quick synopsis):

– Fed Reserve foray into MMT was/is a disaster

– Fed gov’t deficit spending is/has been out of control

– Consumers flush with cash/credit are spending irrationally

The time to pay the piper is coming sooner than some expect. We don’t know when….but it’s coming.

It is already here. Inflation.

It sucks and is will have some serious consequences, but some people want it to be apocalyptic. They don’t realize things can be bad without being catastrophic.

The Fed used the COVID shutdown and in conjunction with Federal Government to pump the economy full of cash at the individual spending level. Much different than QE in past. This was intentional and somewhat of an experiment as even the Fed knows that none of this is science.

Businesses across the board took advantage of supply side issues coming out of COVID to jack prices (and margins). I also believe there was prompting from the Fed behind the scenes but no one will ever be able to prove that.

The inflationery impulse was created. Since then the Fed has done a fairly good job of letting it run it’s course (wage increases, more but lower price increases) via interest rates.

All of you that rail against the Fed for being out of control, make no mistake, they wanted every bit of the inflation we’ve had to date. There main job now is to assist with tamping it out gradually which will happen between increased rates and the demand destruction created from higher prices. It takes some time.

But a lot of little people (bottom 90% now) are getting crushed to varying degrees by all of this inflation. Too bad, that is the price we all know we have to pay for endless deficits and huge debt. It’s the tax that comes due.

Now here’s the real thing to be concerned about. There is a distinct possibility that Russia may move towards a gold backing of it’s currency in 2024. If that occurs and is not subverted by the US or others, all of these discussions will be trivial.

The Fed did indeed pump money….

and in the process they rewarded a certain group at the expense of another.

As Hayek said, when central planners plan, they decide to assist one group at the expense of another.

Asset holders and leveragers won (MBS purchases)….. earners and savers lost. Now the rash of strikes begins….and will spiral the inflation.

The bottom 90% are most certainly not getting crushed by inflation. Wage increases are outpacing inflation.

Also, no true economy will ever go back to a gold backed currency. There is literally no reason to unless they want to destroy their own economy. It is just silliness and ignorance from those who do not understand modern economics.

The Fed balance sheet is a disgraceful example of what’s wrong with American capitalism. You have captured, what would be an absurd observation in a previous epoch:

“It did so because there was so much liquidity in the financial system as a result of the then still ongoing QE, chasing after everything, that T-bill yields dipped into the negative.”

Well, here we all are in the armchair quarterback situation. The situation we are in is also absurd and yet we seem as clueless as too the absurdity as we were when we chose to normalize the extreme absurdity, captured by Wolf, above.

Demand without income only works for so long. Not a concern for the rapacious aristocracy that established themselves as the deserving because of their work ethic.

Unlike, as Mittens Romney let slip his true belief that those whose father wasn’t a US Senator, are scum.

Harvest ends and planting begins, eventually.

dang

“here we all are in the armchair quarterback situation.”

Nope.

This site and many others were screaming at the Fed when they flooded the system. The predictions of what we now suffer were dead on.

One time when I was driving from Chicago to Las Vegas with a friend, we totally got a late start due to me. I had a brain fart and misunderstood when we were leaving. For the whole 27 hour trip, I kept hearing how if we had just left one hour earlier things would have been better. Literally the whole trip.

At some point we need to let go of the past and what coulda, shoulda happened and actually deal with what was.

QE was phenomenally stupid by the FED, especially to the degree it was used. Dumb. No argument. Here is the thing, even the FED recognizes it wasn’t worth it.

When do we stop lamenting about how dumb it was and move on and figure out what is best going forward given the past is the past and unchangable?

Thank you for sharing your knowledge and wit! %^)

Does anyone else come here when the 11 tv streaming apps you pay for run dry?

$9.99 and you’d think there would be something, I mean Anything!

Nah, they may give you 1 show every Friday. If you behave.

Every major sporting event of the television era is available for free on youtube. I’m not a boxing fan, but Hearns/Hagler is the most entertaining 11 minutes I’ve ever experienced. Watching the Rumble in the Jungle with full knowledge that Ali prevails allowed me to truly appreciate the science of the sport.

Not into pugilism, check out the 1971 world series and realize what was taken from the sport when Clemente died a few months later. Bonus – Stargell was one hell of a left fielder.

Not a sports fan – “All in the Family” reruns are as relevant today as they were 50 years ago. Just swap in the name Trump every time someone says Nixon.

Americans needs new content as much as they need new cars…

Wolf-

Love the data and explanations in your articles, but I’m somewhat confused as to your conclusions.

The data you report and interpret points to malpractice by the Federal Reserve (and perhaps some other agencies?) in its attempts to predict the economic future, and apply broad policies that lead to price distortions and unintended consequences.

Given our current predicament (inflation, off-the-charts debt, and a brittle banking system) how is it that you sometimes seem to defend the fractional reserve/lender-of-last-resort banking system? Or am I getting that wrong?

115 years ago a movement to reform the banking system arose and led to a National Monetary Commission that completely redesigned banking in a new direction.

Even a return to that Federal Reserve System as originally envisioned would be a significant improvement over the existing bloated Leviathan that currently seems to do more harm than good.

Isn’t the failure you referred to above (“… QE arrived and created massive amounts of excess liquidity.”) reason enough for a grassroots movement to slim down the footprint of the Fed and reform fractional reserve banking to a reasonably benign proportion of the US economy.

I don’t mean to impose my opinions on your excellent website and commenters, but it seems like central bank reform is supported by much of what you very ably report, as well as by many of your readers.

The feds original purpose was to act as a clearing house and lender of last resort to its member banks. That should still be its purpose. All the financial engineering and congressional mandates are a dereliction of duty on the part of an evermore incompetent congress.

With every “emergency” the central bankers accrue more power….twist, bend and expand their “mission”.

They have no business in the long end of the market, and didnt for decades. The “dual mandate” deals with real time issues (employment and prices).

Then suddenly $5 Trillion in purchases of long maturities…inverting the yield curve, and intentionally forcing investors to take more risk.

A jump the shark watershed mistake, IMO.

AND…. the Fed purchased BBB rated bonds and vocalized a desire for authority to buy stocks.

This is crazy dumb illegal monetary intervention. Congress should be clamping down.

1. The Fed should never engage in QE, period. We now see how that ends: massive inflation.

2. It only bought small amounts and then made money selling those bonds and bond ETFs during the corporate bond bubble in the fall of 2021 that it had triggered with its hype-and-hoopla announcements.

https://wolfstreet.com/2021/11/19/after-fueling-corporate-bond-junk-bond-rally-to-lowest-yields-ever-fed-ends-bailout-spv-with-513-million-profit-sends-90-to-us-treasury/

“ The Fed should never engage in QE, period. We now see how that ends: massive inflation. “

Bless you Mr. Richter! 15% Fed footprint (still too high IMO, but a start) and never use QE to address future economic slowdowns/credit contractions/systemic meltdowns.

The sad reality is that humans will forget these lessons — individuals unaware, and government apparatchiks willfully.

Like Kipling’s Gods of the Copybook Headings they will “… come wabbling back to the fire” for another burning.

Wolf, Is the Fed balance sheet a consolidated balance sheet of the 12 regional federal reserve banks?

Yes.

Wolf, Thank you for your quick reply! Keep up the good work!

5) In Sept 2023 commercial bank deposits were 17.3T, up 10.5T from

6.8T in Aug 2008, slightly beyond peak.

6) Inflation speed was high. It leaped from 0.1% in May 2020 to 9.1% in

June 2022 and plunged to 3.0% in June 2023. Despite the volatility bank deposits stayed almost the same. They tripled in thirteen years from

6.8T to 17.3T ==> the banks are strong. They lend, though less, at the second highest spread.

Wolf, what does the Fed losses as a result of holding lower earning securities in a higher rate env mean?

https://www.msn.com/en-us/money/markets/fed-losses-breach-100-billion-as-interest-costs-rise/ar-AA1gM016

You mentioned the fed lets some of the MBS wind down to term, but is the fed selling off any MBS during QE? Wouldn’t that result in a loss?

If there’s a hundred billion dollar loss this year, how does that “deferred asset” work on the balance sheet…just a carry-over for next year and no profit check written to the Fed?

The article claims the loss could reach 200 Billion by 2025, but if rate policy is higher for longer under QT , how does the Fed reconcile sustained losses? By playing perpetual motion machine and financing the losses it owes?

Detailed article coming in a few hours.

As far as I know, low interest rate environments always ends up with an inflation episode. Going back for centuries. Reading a book on interest and speculative episodes low rates create. Some promises made to get more suckers were: animate the Dead Sea; ‘For importing large number of Jack Asses from Spain’; For a Wheel of Perpetual Motion; and, most famously, ‘For an undertaking which shall in due time be revealed.’ Old version of the modern SPAC.

Wolf,

As you, and others, point out. The QT has a long, long way to go AND the currency in circulation remains elevated (thanks to the drunken sailors in DC).

I was wondering if you had any good metrics on the flow of dollars outside the U.S. coming home? One would thin, this could be a substantial complication for the fed moving forward.

Thanks,

WB

Wolf, technical question for you (or anyone). The H.4.1. report shows the Reverse Repo Agreement balance at $1.835T as of 9/13.

How does this reconcile to the NY Fed’s balance of $1.452T? What other reverse repos are there to make up the ~$400B difference?

Thanks,

recant question, i misread your graph above wiht the foregin offical/international line…thought it was included in the $1546.

Yes, correct!