Good Lordy.

By Wolf Richter for WOLF STREET.

The US Treasury Department today released data to what extent it will boost the issuance of Treasury notes (maturities of 2 years to 10 years) and Treasury bonds (20 years and 30 years), and it starts in August. This oncoming flood of supply at these coupon auctions is a doozie.

So far, Treasury has funded the huge gigantic deficits and the refilling of its checking account, the Treasury General Account, by selling at auction a torrent of Treasury bills (1 year or less) and Cash Management Bills (short-term bills with maturities ranging from a few days to months). But now comes the supply of longer-term notes and bonds.

It starts in August, when Treasury will sell $270 billion in notes and bonds, up by $24 billion from July ($246 billion). The Treasury Department said in its Quarterly Refunding Statement today:

“Treasury plans to increase auctions sizes by slightly larger amounts in certain tenors in order to maintain the structural balance of supply and demand across tenors. Treasury will evaluate whether similar relative adjustments are appropriate when determining auction size changes in future quarters.”

Next week, Treasury will increase the auction size of notes and bonds by $13 billion from July, to $103 billion:

- 3-year notes: $42 billion, +$2 billion from July

- 10-year notes: $38 billion, +$6 billion from July

- $30-year bonds: $23 billion, +$5 billion from July.

The $103 billion in issuance next week will replace $84 billion in notes and bonds that mature on August 15. The additional $19 billion in issuance will be needed to fund the new deficits; it’s that additional $19 billion that will increase the total debt.

Later in August, Treasury will sell $167 billion in notes and bonds, up by $11 billion from July

- 2-year notes: $45 billion, +$3 billion from July

- 5-year notes: $46 billion, +$3 billion from July

- 7-year notes: $36 billion, +$1 billion from July

- 20-year bonds: $16 billion, +$4 billion from July

- FRN (Floating Rate Notes): $24 billion, unchanged

“Treasury plans to increase auctions sizes by slightly larger amounts in certain tenors in order to maintain the structural balance of supply and demand across tenors. Treasury will evaluate whether similar relative adjustments are appropriate when determining auction size changes in future quarters,” the Treasury Department said in the announcement.

In September, Treasury will increase its issuance of notes and bonds also by $24 billion from July, to $270 billion.

In October, Treasury will increase its issuance of notes and bonds by $35 billion to $281 billion.

The issuance of TIPS (Treasury Inflation-Protected Securities) will be increased starting in October with the 5-year TIPS new issue auction. It will be boosted by $1 billion to $22 billion.

Over the next 12-month, Good Lordy.

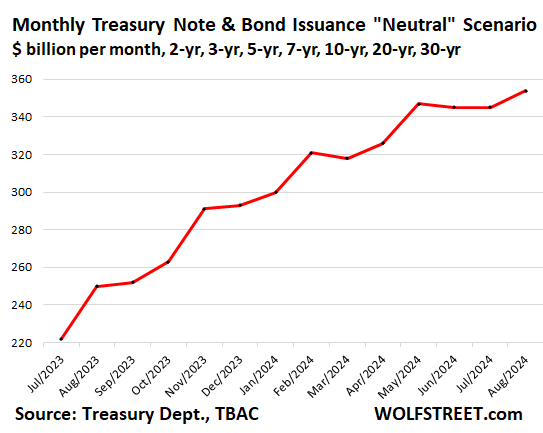

Treasury should jack up its monthly issuance of the seven main notes and bonds (not including TIPS and FRNs) by nearly 60% over the next year, to $354 billion in August 2024, from what it issued in July 2023 ($222 billion), according to “Neutral Issuance” scenario in the presentation by the Treasury Borrowing Advisory Committee (TBAC).

These quarterly projections could be subject to hefty increases over the next quarters, as we have seen today. The chart shows the projected monthly combined issuance of 2-year notes, 3-year notes, 5-year notes, 7-year notes, 10-year notes, 20-year bonds, and 30-year bonds:

This is a tsunami of notes and bonds that is going to flood the market. And it is occurring while the Fed, under its QT program, is letting about $60 billion a month in maturing Treasury securities roll off the balance sheet without replacement.

With the Fed reducing its holdings, that tsunami of notes and bonds being issued will have to find buyers, and those buyers will have to be enticed by yields.

Yield solves all demand problems. If the yield is high enough, just about anything will sell. So it’s not that Treasury won’t be able to sell those notes and bonds, but at what yields it will have to sell them, and yield investors are already licking their chops.

The scenario is further clouded by inflation, which, once it breaks out to this extent, has a nasty tendency to serve up bad surprises, and bond investors hate inflation and want to be paid for it. Compared to the tsunami of issuance coming our way in this inflationary environment – partly fueled by this huge deficit spending from the government – the Fitch downgrade of the US credit rating to AA+ from AAA is just decoration.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Sounds like one might want to get ahead of all that selling. Hmmm.

All the professionals buying longer dated treasuries at 1% LOWER yields than on risk free T-Bills are gambler morons….

Long dated bonds should have a HIGHER yield

= 10 year bond should be at over 6% now….

Instead its slightly over 4%

= potential for huge losses in bonds

= losses in long duration assets, such as stocks

= Huge sell signal for stock investors

You sound like someone who began trading when fundamentals actually mattered. Well, sort of mattered, fundamentals may have died with JFK, some may argue even sooner… (1913), but I digress. We make our choices and make a living where we can. Yes, big sell signal, but then go to what exactly? Personally I am thinking about more real estate (rentals) in stable societies.

AGREE, like totally dude or dudette RE: 1913 and ’63, to the enduring and continuing shame of any and all or almost all paid political puppets since those two dates.

Surely, at least some of those puppets know what is going on??? OR NOT, eh

As to the RE in ”stable societies”,,, when you have a moment — a second might do,,, please let us know where such a thing exists today when every turn of the knob reveals another society that is NOT stable.

Thank you,

Doesn’t matter what the yield is if you don’t expect to pay it back.

Ask Bernie Madeoff-with-the-loot.

maybe and maybe not. the key to smart investing here is to find the top for long term rates, because if you buy a long term bond at a 5% yield, lock it in for 10 or 20 years and then rates fall back down, you are a smart investor. but if long term rates go to 6% and you lock it in for 20 years and then rates fall again, you are a genius.

but that is a big IF. i do think that yields will spike higher and this will cause a financial crisis. if the US cant borrow money cheaply/recklessly anymore EVERYTHING changes fast.

i have been invested in TMV, a fund that is inversely correlated to long term interest rates. wish i had bought more, i was waiting for the break-out to fail and come back down to an uptrend line before I bought more, but oh well, that is life.

my playbook is:

– long term rates continue to spike as demand falters and supply is outrageously high

– dollar moves higher as rates go up, but then at some point there is a disconnect between the two and the dollar starts to fall (trade against the dollar)

– high p/e stocks that ran up the beginning of this year start to collapse, and really collapse over the next year. the AI bubble (outside of NVDA will collapse, difficult to say about NVDA because they are actually delivering results for now)

– real estate is on a 5 year decline, and prices finally start to drop by q4 of this year in a sustainable way. next spring there is a minimal bounce. the real price drops will be in 2024 and 2025. 50% downside in some locations.

– tough to say if bitcoin or gold will benefit from the collapse of the dollar and the BRIC countries moving away from dollar trade.

That would be true if we had free markets. In reality the driving forces are the Central Bank and Government gorillas. Everything else is a play on liquidity and stimulus. Markets have been stealth nationalized and everyone is pretending it’s the new normal.

When the Treasury curve inverts, it is usually a sign that a recession is on its way.

Very few of these professionals are buying long-term bonds for the long haul. Their plan is to buy long bonds, wait for the recession, sell at a higher price when the Fed announces the next monetary stimulus and rate repression cycle. If economy tanks, you get 4% plus capital gain. If the economy rises, you still get 4%, so you can’t lose much to inflation if you don’t own the bond for long.

If you are following that plan, however, it might be better to wait and see if long bond rates break out. You could get more gain by waiting a bit.

Of course, you’d never want to hold a long bond for more than a year or so. We’re looking at consistently high inflation in the future, and current long bond rates don’t come close to compensating for that. See Ackman’s comments today, indicating long bonds should now be 5% or 6%.

With deficits projected to be 6-8% of GDP as far as the eye can see, and real GDP growth of 2% or less, the government needs 4-6% inflation simply to maintain a stable debt-to-GDP ratio.

Anybody buying a long bond paying less than 6% is going to regret it.

Agreed… and the inevitable recession has not even started, which will crush govt revenues.

WSJ article today:

“America’s Fiscal Time Bomb Ticks Even Louder”

“Fitch’s downgrade of the U.S. debt rating only caused a flutter in markets, but fiscal strains will soon get harder to ignore”

It’s definitely a ticking time bomb that’s for sure.

it’s like the scene from Oppenheimer when the countdown hits the two-minute mark from detonation.

FRED is now reporting that the annualized interest expense as of Q2 was $970B. The next 4 or so quarterly updates are going to be spectacular!

What we need to look at is tax revenues to pay for that interest expense. Tax revenues have also shot up. We don’t yet have the metric for Q2 tax revenues that pays for interest expense (government receipts from all sources minus social insurance receipts, and a few other items). This metric will be released on Aug 30 with the 2nd estimate for Q2 GDP. I’ll post my updated chart of interest expense as percent of tax revenues then. It will look ugly, but not as ugly as interest expense in a vacuum, which is what you’re referring to.

If I read the monthly Treasury Statement correctly, tax revenues are declining compared to 2022. For the period ending June 23 total receipts were 3.4 trillion as compared to 3.8 trillion in the comparable period 2022.

pigeon,

Capital gains taxes, after spiking in prior years, plunged because 2022 was a shitty year for stocks and bonds and cryptos, and that played into tax payments in 2023. Capital gains taxes are very volatile, with huge ups and downs.

And that’s why you see in my chart of “interest expense as % of tax revenues” a spike to over 30%. But it was over 50% in the 1980s.

Bobber,

There are really smart people with Phds in economics which make the case that bond yields will be lower in the future. The logic is government debt is past the point of being productive, so the real economy will have less real income to service the debt. If Fed isn’t going monetize the government’s debt and the Fed is going to hit its 2% inflation target then real long term growth will be less than 1.5% and nominal growth will be less than 3.5% and the US will be only able to afford a nominal rate below 3.5%.

I don’t know if the theory is right. It probably depends on who the Fed chairman is. I would just say that higher sustained rates aren’t a slam dunk.

Well presented, Old School.

I guess that your analysis argues against keeping all of one’s safe money in shorter bills, and FOR using a short to medium length ladder to preserve today’s rates. This worked well several times during the 90’s to preserve some portfolio income when rate declined.

Professionals are paid to think ahead and prepare for various scenarios. Of course, preparing for different scenarios by being on the right side of the market guarantees that the portfolio will always have some money on the WRONG side of the market. That’s the unspoken peril of diversification…

“If Fed isn’t going monetize the government’s debt”

LOL! That train left the station a long time ago!

To be determined. Legally at least I think Powell has to try to run off the monetization that was done during the Pandemic. He will have a tough decisions in the future.

PHDs brought us to this situation.

As Yellen deflected …”The theories we chose to follow were wrong.”

Notice they themselves (PHDs) werent wrong for choosing, it was the theories.

That doesnt fly in the real world, just government.

There are smart people with PhDs that say that long-term bond yields will be higher in the future, and that the bond bull-marked died in Aug 2020, and that we’re headed into a long uptrend in bond yields, similar to the 1960s-1982.

Absolutely so. I really don’t know if anyone can say with certainty. I just wanted to voice that there are two intelligent opinions on the subject, and that someone can buy 10 year at these rates and not be a complete moron.

I agree real growth will be around 1.5%. That part is fairly straight forward. The problem with these institutional economists is they assume the US will not monetize debts, even though they’ve done it for 15 years. The Fed’s balance sheet trend is clearly increasing, despite recent small contractions. They need to wake up.

The leaders have been inflating for decades (either assets or CPI) to avoid recession. It’s a dependency. Why do institutional economists fail to see and consider that obvious trend?

Are you talking to me?

–Warren Buffet, who says this is a good time to buy T bonds.

“There are some things people shouldn’t worry about. This is one.”

Great observation

If you issue long term treasuries at higher interest rates, you are locking in having to pay higher interest rates for years, whereas if you expected rates to decrease later, then it would be smarter to just issue shorter term treasuries at those high interest rates, so you could then roll them over (pay them later when interest rates go down through funds obtained by issuing treasuries at lower interest rates then) at lower interest rates later. This indicates that the powers that be must either be desperate or expect inflation to continue despite indicators of a possible recession or at least, a taming of inflation

Remember what I said about higher interest rates, and how long they will continue, and how higher rates lower asset prices? This is going to be tight interest rate policy for 10 years, and longer it takes to raise taxes, pay debt, and enforce the tax laws, the longer it will take higher rates, period.

Nothing has changed, nor will it change until gridlock is smashed, taxes go up, and reality finally hits America.

Anybody dragging the corpse of the Trumplican party out for real governance is part of the problem and not part of the solution. That self serving tax cut was insane. Kudlow comes straight to mind.

Higher taxes, lower asset prices, and some fiscal sanity.

I am amazed how far from common sense most of the really partisan people have gotten, and how crazy international leaders have gotten.

In some ways, the delusions of politics have infested economics, and until everyone finally gets some common sense it has become pointless.

TANSTAFL applies.

And those who got the pandemic low rates will be happy to pay in deflated dollars, as usual, in America.

You forgot to add that the government could cut spending.

Hahahahahaha

For 2022, per CBO, we spent $6300B but took in only $4900B

Cut spending?

Fine, we need to trim $1400B or 22% across the board.

Which sacred cow would you like led to the slaughter yard?

Mandatory spending $4100B

– Social Security $1200B

– Medicare $747B

– Medicaid $592B

– Income security $581B

– Student loan $482B

– ‘other’ $520B

Discretionary spending $1700B

– Defense $751B

– non-defense $910B

Net interest $475B

You can take SS off that list. SS has its own revenues (from contributions), and ran a huge surplus since 1990 ($2.7 trillion in total). It has run only small deficits over the past couple of years:

https://wolfstreet.com/2022/11/08/status-of-the-social-security-trust-fund-income-and-outgo-fiscal-2022/

I certainly do not wish to see SS cut, reduced, or mucked about with. For many it is all they have, often through no fault of their own.

My point is that everyone has their own cow, it’s always the other guy’s herd that needs to be culled.

If spending cannot be realistically reigned in then increasing revenue — through restoration of taxation is the only solution.

Tailored tax cuts, loan forgiveness, additional entitlements, etc, may serve noble purposes but, unless they are properly funded in a sustainable fashion, it’s just “bread-and-circuses”.

Oh I think a defense budget of about $75 Billion would be just fine for starters.

Out of NATO

Out of Asia

Out of Africa

Out of South America

I laughed at the idea of the government cutting spending. It’s nice when all you have to do is spend other people’s money without being responsible or reasonable. That goes for both sides of the aisle.

SS is NOT an entitlement Bunter, my employees and I have been paying for that our entire working lives. If you are going to cut that, then we all want our money back! It amazes me how many talking heads parrot this propaganda. SS also has it’s own revenue stream.

WB,

Thank you for reminding people. I too get really tired of having to read this propaganda over and over again.

Re: mandatory spending –none of them to the slaughter yard!

Why? Propose reining in any of them and the party out-of-power will air ads showing the party-in-power running grandma, in her wheelchair, off a cliff.

Suddenly, the proposal vanishes. Or vanishes to be replaced by an even bigger entitlement!

Wolf and WB,

Social security is by definition an “entitlement”: the fact of having a right to something. The paying of FICA taxes is actually what makes social security an entitlement. That’s not propaganda.

It’s a government social insurance program that is far broader than simply retirement checks. In this regard, every statement I’ve received about future benefits admonishes that Congress can change the program at any time. The funding mechanism for social security doesn’t change this fact.

Bunter,

Thank you. Very useful summary.

The US Government has played out its string and sooner or later (sooner) there will have to be spending cuts or relentless inflation (if the Fed starts monetizing the debt again).

Summaries like your own are useful because they broadly pinpoint where the savings essentially *have to* come from.

education and healthcare – two of the biggest scam industries that are propped up by bad government policies.

should a college education really cost 90K a year (including housing/food)? where does that money go?

and why is the government funding these ridiculous tuitions with government backed loans?

and why are we funding programs with limited job prospects that are not crucial to our global competitiveness? like gender studies?

the original student loan programs were only for technical degrees in engineering and science and it was done to help US competitiveness.

the education industry is one of the biggest lobbyist industries in the US.

how about we actually fix the primary school system so that every kid who graduates can read and write and perform complex math.

Cut spending is not in their vocab.

Your post was great except for the Trumplican party nonsense. Do you think the Dems are going to impose any sense of fiscal sanity? this is the party that advocated people being paid $600/week to sit at home for years. They advocated for “forgiving” student loans. Heck, they gave $7,500 for funeral expenses to the families of anyone who died from CV-19.

For sure. Why waste all that money bailing out the common herd when it can be put towards corporate welfare and tax cuts for the rich?

But not to worry Einhal. It’ll get spent, and money flows uphill. It’ll just show up in the profit statements a little later, rather than sooner. In the meantime the money is helping somebody besides you.

An argument could be made that non of that money bailed out the “common herd”. It just cemented inflation that is now hurting them. I’d also state that most beneficiaries of recent “bail outs” were on the wealthier side of the spectrum regardless of how it was spun.

Anyway, I may be mistaken, but you seem to be stating that government waste is a requirement and you rather it go to “the common man” than corporations. How about it go to neither and not point partisan fingers to parties that do the Alex act same thing.

“I may be mistaken, but you seem to be stating that government waste is a requirement”

If you want campaign contributions from corporations it is.

As for the rest, well, we’re all Keynesians now, aren’t we? Just kidding.

Keynes balanced the equation by saying deficits should be paid back when the economy recovers. Fine, go ahead and laugh. Now stop laughing. It’s not funny.

Sarc. Right?

LOL. So true, yet some fat cats didn’t like your comment. Tax the god damn rich who can afford it. They’ve been getting tax cuts they didn’t deserve for years. They wanna spend all that money for the military that pays 10 grand for a special nut which probably cost 10 bucks to make but you wanna spend money to take care of fellow citizens? Hell no! says the republicans. And these people claim they are Christians.

Both parties are correlated with almost and equal distribution of defense increases and decreases from their initial starting to party tenure end (as defined by president).

If you look at an actual data, the differences are that big. Just go by what they say (the sales line) who’d think the parties are miles apart.

I have never understood why it is “greed” to want to keep the money you have earned but not greed to want to take somebody else’s money.

Thomas Sowell

Top 10% of wage earners pay the vast amount of the taxes in this country and the bottom 50% pay almost nothing.

Look around you- one out of two Americans have almost no participation in taxes.

Of course those who pay the most in taxes should be the ones benefiting from tax cuts.

To you the words ” tax cuts” are evil. You forgot tax cuts actually means keep more of your own money; keep more of the money you earned.

CalCon – if only those on the right side of income disparity would frontline man the divisions in proportion to protecting their wealth when the time comes (…and it always comes…).

Using your example, one might see that it’s getting harder to convince folks of the benefits of an ‘ownership society’…

may we all find a better day.

may we all find a better day.

“Top 10% of wage earners pay the vast amount of the taxes in this country and the bottom 50% pay almost nothing.”

I think you’re confusing the top 10% with the remaining 40% you left out, who are probably the real tax donkeys in this country. Keep what you earn? Sure, I can get behind that, but I have some reservations about what the top 10% really “earned.”

Tax cuts expire in 3 years anyway. Taxes will probably have to be higher and benefits will have to be cut. Problem with high taxes is they cause avoidance and there are 70,000 plus pages of tax code for tax attorneys to exploit.

It’s only the tax cuts for individuals that expire. The huge corporate tax cut, which cut the corporate tax rate from 35% to 21%, will not expire. Labor gets the shaft, again.

Government usually gets two cuts on public corporations. $1.00 taxed at 21% leaves you $0.79. But if you are share holder you probably are going to be taxed again whether in an IRA or as capital gains. For many that is going to be in the 20% range so really the stock holder gets about $0.63 of company earnings or pays 37% tax. Add state tax on corporation and on individual and in my state you would be down to stock holder keeping $0.57. Now if I want to go spend it there is a 7% sales tax so now the stock holder in my state is down to $0.53 or 47% tax rate. I missed a few additional taxes, but my finger was getting tired. So whether labor or capital owner government usually gets a big cut.

And if they have to lower the price to increase the yield to get the required buyers… Then in the end, they have to sell even more of them, right? Even more debt for the same number of dollars in the TGA?

With notes and bonds, that’s not quite how it works. For example, in July, Treasury sold 10-year notes, face value $1,000. The announcement days before the auction set the coupon interest at 3-3/8% (3.375%), which was roughly the 10-year market yield on that day. So the buyer will get interest payments of 3.375% a year ($33.75 per $1,000). So at the auction, bidders know that this 10-year note pays a coupon interest of 3.375% of face value per year for 10 years. But at the day of the auction, the 10-year market yield had already moved higher, and bidders bid below face value (at a discount, 96.08% of face value), in effect $960.80 per $1,000 face value note, to get roughly that day’s market yield with a coupon interest of 3.375%. So the “high yield” at the auction was 3.857%.

If market yields had been lower than the coupon interest, bidders would have bid the price up above face value (paid a premium).

The amounts of the discounts/premiums are small. In this example, $4 per $1,000 note. And over time, they sort of balance each other out and don’t impact issuance in a measurable way.

We called this OID when I worked in the debt markets. Is that terminology used for government tbills too?

Who will be the first one to the exit?

With new issuance & Fed roll-off, will a foreign Central Bank blink? No more mark-to-par, no more hold to maturity, just pennies on the dollar cash in hand NOW.

Wolf, could this tsunami actually be an avalanche or treasury bill/note selling?

If investors want to get out and start selling, then yields will finally rise to pull in new buyers. Looking forward to it.

hello wolf as you said “it’s that additional $19 billion that will increase the total debt.”

So in your estimate how much of the new debt will be issued in the the treasury notes and bonds by next August? Also the old debt rolls over at higher rate right?

I am asking this because @ $20B a month, it will be only $100B or so out of $1.5T planned for the remaining year. That means majority will be bills?

Being that mortgage rates are closely tied to the 10year, with this flood of notes that need to be chased with attractive return rates, what does this mean for the mortgage market? Seems mortgages would need to be increased yet again nevermind the higher rates now with low inventory of properties. Would this lead to a further slowdown of housing loans?

10 year US Treasuries are indeed what mortgage interests rates are keyed off plus about 3% and the question as to how high mortgage rates will be going from their present around 7% is just how high the yields of the 10 year US Treasuries will soar this year. That has nothing to do with the Federal Reserve and what it does or doesn’t do. It depends on the US Treasury markets where yields continue to soar.

Wolf has shown that housing shortage is a myth. But the key is Airbnb and other vacation rentals–I believe that’s where the crash will happen when they can’t rent them out at a profit and need to sell fast. More and more owners are talking about it.

All it takes is a few fire sales to bring entire neighborhoods down just like in 2010.

Calculated risk.posted an article this week.. rents have started to fall YoY. So here we go, if you can’t raise rents how ya gonna pay these mortgages?

That’s not true. May be some measure of “asking rents” fell year-over-year — though not the Zillow ZORi index — but it would be falling from the “asking-rent” bubble a year ago that never made it into actual rents.

CPI tracks actual rents, what current residents are actually paying. And “asking rents” are irrelevant. Asking rents are advertised rents, what landlords hope to get for their vacant units.

Here is the Zillow asking rent index in dollars (red, right scale), and you can see how this asking rent bubble in 2021 and into 2022 never made it into actual rents (green, left scale). And even asking rents, after the dip last year, started to rise again this year. Actual rents in June were up 8% year-over-year:

Wolf,

That CPI (ahem) vs ZORI (ahem ahem) chart is worth a future post of its own (“Duel of the Dubious Methodologies”).

I have no problem believing that reported asking rents were somewhat in excess of actual rents…but there are multiple rental surveys that show data well in excess of CPI reporting.

And I’m not sure why landlords would all-of-a-sudden start inflating asking rents far above achieved rents…and then keep doing it (unsuccessfully) for months and months and months on end.

I’m sure that rent promotion givebacks and attempted valuation gaming play a small role, but we’re talking about an asking-to-achieved rent gap that has supposedly gone up 5x.

In light of that, I have no problem believing that CPI is underreporting too.

” ..is worth a future post of its own (“Duel of the Dubious Methodologies”).”

Not dubious but different — the difference between advertised rents on vacant units and rents that tenants are actually paying over time in the SAME units. People have to understand the difference. The article you want me to write, I already wrote:

https://wolfstreet.com/2023/05/22/rent-inflation-re-accelerates-to-red-hot-all-three-now-agree-zillow-asking-rents-what-big-landlords-said-and-actual-rents-tracked-by-cpi/

It’s very common to call something “dubious” because you don’t understand it.

Yep. The airlines talking about declining demand is probably not a good sign for AirBNBs.

Kurtismayfield, that’s also a bad sign given that many municipalities have increased property taxes in recent years. You know that they’ll never cut them if rents drop. They’ll find new ways to spend the money.

Here in Florida, property taxes are based on property sales. They have a code for every neighborhood, and within neighborhoods they compare houses with similar square footage. Prices in most areas are still on an uptick, but going down in other areas.

We have a strange double-whammy: the market is frozen as lots of people don’t want to sell into higher interest rates, while most conservatives in the Northeast are selling their expensive homes and buying them at top dollar here. Florida Man, who never made much money schlepping ice cream at Disney World, now can’t afford to live here. We have the worst house price to income ratio in the country.

Kent, I’m in Palm Beach County, and while there certainly was a huge tsunami of “remote workers” moving to Florida and driving prices up with the profits from their NY/NJ houses, I’m not seeing much of that anymore. I think most people are expected to be in the office at least on a hybrid schedule, so those people need to be able to find jobs in Florida, and there just aren’t enough of them.

The volume of sales has slowed dramatically, and I’ve seen quite a few reductions. But the affordability for the average person is still terrible, as you’ve mentioned.

Yup. Anyone with a house to sell ought to be rushing for the exit right about … NOW.

Honestly i just don’t see it. Can the current trend reverse and go back into decline for a while? Obviously yes. But anyone hoping for another 50 or even 30% drop in prices like last time isn’t looking at the bigger picture. People from all over the world want to live in America and that’ll never change. And 40% of sales are all cash.

This part is true Kern: ”People from all over the world want to live in America ( FL especially from what we are seeing these days,,, and that’ll never change. ”

Last house my parents purchased in FL was from a retired Col. of the British Army who could not stand the weather in England after decades in India.

Unfortunately, FL real estate has waxed and waned, sometimes well over 50% on the downside for eva, or at least since European folks started ”legally” buying and selling it.

Old timers in the 1940s-’50s used to talk about properties changing hands multiple times PER DAY in the 1920s,,, until the crash that wiped out many totally, others just at the 90% range of losses.

Of course it’s different this time,,, it’s always different is SOME ways while always the same in other ways.

It will lead to higher mortgage rates and fewer sales (fewer loans). Marginally qualified buyers who keep waiting for lower rates are getting priced out of the market.

On the seller side, higher mortgage rates will increase the difference between their existing low mortgage rates and higher mortgage rates movers will have to pay on their new home purchase.

As a result, sellers will hold tight and postpone any move for absolutely as long as they possibly can. This will keep inventories low and push sales volume lower… sales volume, not sales prices… not yet.

Until something forces a lot of folks to all try to sell at once and overload inventory, prices aren’t going to crash or even decline meaningfully.

It’s definitely getting to the point where buying a home requires one to roll a bunch of equity from a departing residence sale, or being in a situation where someone can get sizeable gift funds from friends and/or family to help with the purchase. Not a great set of cards to play for first-time homebuyers or those who don’t come from backgrounds where they know someone who has plenty of liquid cash to gift. I don’t see this changing given the current environment.

Prices in the most overheated markets have already declined meaningfully.

Disagree. As Wolf pointed out a few days ago, those sellers who are postponing a move also aren’t out looking to buy. So it’s a net zero effect on inventory.

Must be feeding time.

Do folks realize that the US Treasury issues around $15+ trillion a year in US Treasuries now that it has to sell in order to pay off maturing treasuries across all durations as well as increasing the net new debt of $1.5 trillion to $2+ trillion a year now?

Former vice president Dick Cheney once said, Ronald Reagan proved that in politics, “deficits don’t matter.”

“The US government has a technology, called a printing press, that allows it to produce as many dollars as it wishes at essentially no cost.”

– Ben Bernanke

It is starting to matter–a lot. You can’t print your way to prosperity and export your inflation forever. Print all you want, but many nations are starting not to take those dollars for their raw materials and products.

It is all up to Powell now either to cave in and destroy what is left of the dollar, or do the right thing and let the markets fall where the may.

Cheney was MMT before MMT was cool?

Bernanke won the Nobel…..and we are still dealing with the stage he set with his QE. Can they retract the award?

Cheney…… sure, feed the monster I am riding. No surprise. Politician and neo con. Does Liz hold the same view?

Who has stopped trading in dollars?

Brazil, Russia, Iran, and many Asian countries including India.

Asian Central Banks To Adopt Iran’s SWIFT Alternative As De-Dollarization Accelerates

In the latest shot fired in the growing rebellion against US dollar dominance, the nine-nation Asian Clearing Union (ACU) has agreed to use Iran’s financial messaging system as an alternative to the dollar-denominated SWIFT system that has long served as the globe’s financial nervous system.

Time to go long Iranian bonds, stocks and currency? I’m hesitant a bit, but maybe that’ll turn around and I’ll miss the boat.

THE BOND VIGILANTES ARE COMING BACK!!!

Just don’t go too big too soon…

Remember, there are a lot of very dumb fixed income investors who need to get flushed out of the market (Exhibit A– Silicon Valley Bank– still waiting for the rest of the alphabet).

The bond vigilantes are already in the market. This time they are fighting the Fed by bidding longer dated bonds higher in price and lower in yield, hence the inversion in the yield curve. Funny how the corporate media doesn’t make any noise when bond vigilantes fight the Fed to keep rates lower versus when they fight the Fed to move rates higher.

“If I leave here tomorrow, would you still remember me”. The great reset has begun to take shape could this really be the end of QE for decades. You get a home, they get a home, we all get a home saga is over. Theres no where to go but up, for sure the USA debt bill will keep running deficits, Wall St. Says the credit downgrade does not matter, but tune changes when the average Joe walks into a bank for a loan. The rabbit finally got the gun, USA will have to atone for reckless spending. How did we ever get so over leveraged?

Simply by wanting to and living far beyond our collective means.

Everybody wants and accepts services, nobody wants or accepts the supporting revenues (taxes). Path of least resistance for government in a democracy is: print. It goes back to unrealistic expectations in the voting masses (and organized lobbying and resistance by the rich, to keep their piles).

Corruption, period.

Question: “How did we ever get so over leveraged?” Answer: By handing out windfalls to the Oligarchs and using debt, instead of equity or cash ,to pay for deficit spending.

Here comes “crowding out” (competition for available savings)

If it is like the tech bubble or the housing bubble, its going to be great until its not. Wonder how many levered companies are doing shady stuff on their balance sheet that higher rates will eventually be found out. Remember WorldCom, Enron, Bear Sterns, Washington Mutual, GE, Cisco?

Any guesses on whether a federal budget or continuing resolution will be passed by the House this fall?

There will be no single ‘omnibus’ appropriations bill but rather around 13 separate budget appropriation bills as a result of the House’s Republican decision to do it that way, so the Senate will a vastly more complex issue with 13 separate bills. As to a CR that is not at all likely this year as that would not in anyway address the 13 separate appropriations bills that are the key holdup to doing the budget by October 1, 2023.

Always and aways at the last second. The one fairly recent time that it wasn’t passed the party that appeared obstinate got roasted.

Most people pay no attention to treasuries or debt to GDP. They do know if their SS check doesn’t show up or if the favorite federal campground is closed. Then people look for somebody to blame.

Debt bill will be passed after great shouting and screaming.

The political moral is ‘dont get in the way of the circus’.

“Appeared obstinate” is based on the way it is presented by the media.

There are whispers that a shutdown is a very real possibility this fiscal new year, although not up for discussion publicly, so who knows. Although with the current political situation and coming circus, it would be likely, IMHO.

Am I correct in thinking that this is essentially how the Quantitative Easing of yesterday becomes the Monetary Inflation of today?

No. This is unrelated to QE and monetary inflation. The Fed is in charge of QE and monetary inflation.

This article was about the government, not the Fed, about the government’s issuance of notes and bonds to fund its deficit spending.

If there hadn’t been QE over the last decade then the government couldn’t have spent so much which drove up the budgetary baseline. QE not only raises the debt today, it makes it so any future fiscal sanity requires painful cuts from government cheese that people and agencies have gotten used to.

Wolf- “ This article was about the government, not the Fed…”

It’s so hard to tell where “government” ends, and the “Fed” begins.

The Fed is an organ of the banking system AND an appendage of the state.

It’s also owned by the big U.S. banks and never forget that.

The Fed is a hybrid organization.

The Federal Reserve Board of Governors is a government agency, and all its employees are federal government employees with a government salary and a government pension, including the seven members of the Board, including Powell. These seven members of the Board of Governors are appointed by the President and confirmed by the Senate. The Board of Governors has lots of employees, and they’re all employees of the Federal Government. They’re headquartered in the Eccles Federal Reserve Board Building, the main office of the Board of Governors of the Federal Reserve System. This is a federally owned building on 20th St. and Constitution Avenue in Washington, DC.

The 12 regional Federal Reserve Banks are private organizations that are owned by the largest financial institutions in their districts. They include the New York Fed, the San Francisco Fed, the Dallas Fed, etc. All their employees are private-sector employees.

The FOMC – the policy-setting committee – consists of the 7 members of the Board of Governors who are federal employees and have permanent votes on the FOMC. The New York Fed governor also has a permanent vote. The other 11 regional FRBs rotate into and out of 5 voting slots annually.

The FOMC is designed to give the 7 government employees a voting majority over the 6 presidents of the regional FRBs.

Sounds to me like the Fed is a government institution that is partly owned by the banks, ostensibly designed to help the banks when they get out over their skis as they seek private profit, and to socially fund their efforts via bailouts, subsidy, interest rate short-circuitry, and other taxpayer-funded “solutions.”

Sort of a command economy wolf in free-market sheep’s clothing, if you’ll pardon the personal allusion.

I wish the Fed (and the rest of us) well in it’s current gambit to un-paint itself out of a tight corner, but I seriously question whether it’s long-term quest to achieve economic stability is remotely achievable.

Mr. Wolf, can’t the Federal Reserve buy up all the treasuries with interest crushing demand? Then people are looking at the balance sheet; however, the Federal Reserve has an IOU account at the Treasury with only chump change of a few tens of billions of dollars of Federal Reserve IOUs. Seems that the Federal Reserve could pump up that account into the positive for a trillion or two dollars without anyone noticing.

Sure, the Fed could buy every single Treasury security that isn’t nailed down. That would be like the biggest QE ever. It would totally blow up the dollar through massive inflation in weeks. Inflation is the problem we already have. So the Fed is doing the opposite of what you suggest in order to get inflation back down.

If another banking panic starts the Fed will do whatever it takes to stop it, including further inflating its balance sheet. A disorderly increase in rates could trigger another panic similar to SVB and I think Fed intervention in the market to cap rates would then be inevitable.

You’re spreading BS because it fits your agenda?

“…including further inflating its balance sheet.”

This is the kind of repeated BS that put you on my troll list. The balance sheet is down by $722 billion from the peak and is at the lowest level since Aug 2021. Tomorrow afternoon, we’ll get the July 31 roll-off. And it’ll be down further — deflating further, not “inflating further.” Update coming tomorrow evening.

Hi. The question I was pondering over was – “Will the Fed be forced to buy the bonds and lend support in this plan?”

The largest buyer and holder of US Govt securities, Japan having its own problems of inflation/ managing 10-yr yield and JPY may not be that keen to participate. China probably not that keen due to geopolitical reasons. Will other international buyers and domestic institutions have enough muscle to see this through or Fed will have to step in? Do you see that as a high probability scenario?

Would be great if you share your views.

Thanks.

The Fed won’t be “forced” to do anything.

The Fed WANTS higher long-term yields, and it has been frustrated that longer-term yields have remained below its policy rates, and that financial conditions haven’t really tightened outside the banking sector. Remember, the Fed is in a rate-hike cycle to fight inflation. Short-term rates don’t really impact the economy much; long-term rates do. But markets have fought the Fed and kept longer-term yields too low.

On the positive side, high borrowing costs might finally encourage Congress to take these deficits seriously. ZIRP has turned Congressional brains to mush. Higher yields might cure that.

This deficit-spending is adding fuel to the inflation fire. So inflation won’t be going away anytime soon, and long-term yields need to stay higher.

Once you have binged on debt, like the US has, and inflation breaks out, there are really not any good options. All options are more or less lousy.

Will our governmental institutions do the right thing, when push comes to shove? That is the question.

If the Fed continues to tighten until inflation is 2%, it will undoubtedly throw the economy into a recession, and that recession could be a big one. A recession at this point in the debt cycle would be like a tire losing grip when the semi truck is doing 70 mph on an icy road. It potentially triggers a nasty chain reaction.

What will be the response to a recession? Will the government and Fed try to artificially stimulate again, or will they raise taxes, cut spending, allow bankruptcies and debt write-offs, etc?

Based on governmental behavior the past 30 years, we have to expect an outcome commensurate with procrastination, spinelessness, and favoritism of capital over labor. The wealth of the top 10% is on the line, and they control the government.

The Empire gotta sell its debt. Congress gotta keep getting its grift and Buyers like me with dripping long term yield starved chops are packed up and on top of the hill howling at the moon waiting for the feast. The return to the 0% dream of the pivot bobble heads on cable and click bait video might want to set this cycle out. They can watch all of the re-runs of I Love Lucy and Wagon Train and all of the rest of the prime time 30 minute time killers of the past. They gonna have a lot of time on hand.

US and Canadian bond yields have increased quite a bit this week.

Meanwhile, across several grocery stores in the Greater Toronto Area, prices continue to rise like there’s no tomorrow.

Simpletons are cheering on when corrupt regimes indicate that they want to “balance the markets” with US$100-$200 oil, and that the current US$80 is not enough for the OPEC alliance to profit.

Core Inflation is not going to go back down to 2% in the short term. High food prices and gas prices appear here to stay.

About 50 percent of the Federal debt is under 2 years.

Combine this factor with the constant roll-over of debt and it becomes obvious that the burden of higher interest rates will be compounded.

The burden becomes a function of the major portion of the debt, not just the current deficits. The burden, in fact, becomes exponential. In other words, if the trend is not stopped, the debt inevitably has to be repudiated.

Interest expense as a percent of tax revenues is the metric to look at since tax revenues pay for interest. Tax revenues have shot up too. This is through Q1. I will update this chart when Q2 tax revenues minus SS receipts are available:

So to break inflation, interest rates have to rise, and tax revenues have to rise, and interest costs have to rise. We can see it in your chart in no uncertain terms, with those peaks in the 1980s. Anybody ready for 15% interest rates?

And every single business that has levered up has to either earn out and pay off the soon to be uncomfortable debts and much larger debt service for every bit of finance. Look at the balance sheets and the debt of every single company using US debt. Anyone who has to roll over debt continuously will be raising prices to get the funds to either service or payoff.

So financially driven inflation has yet to really arrive.

Start your predictions for the survivors. I would note that Wall Street is still insane and begging for the pandemic to return. Sorry Charlie.

My business is built on bricks and cash. While my competitors bought themselves fancy cars, homes, boats, vacations, and expanded via “leverage”, I saved, invested, and lived way, way below my means, like driving a 17 years old used car and living in the same starter home of 20+ years. I have absolutely no debt in anything, but piles of cash, assets, and cashflow.

Funny thing is that I was preparing for this time for last 15 years as being the last man standing. Now, I am charging much less than my competitors where they can not even come close because I can. They are complaining bitterly to my suppliers. Good times.

cam: to answer your question, ” Anybody ready for 15% interest rates?”

YES indeed,,, some of us old farthers, or something spelled approximately that way, ARE ready.

IF you would care to read more than headlines on Wolfstreet.com, you might imagine that there are quite a lot of folks of all ages ”ready” to invest in USD ”Treasuries” when they, T-bills, Notes, and, yes, even Bonds get back to where they, in this case the entire Treasury they, SHOULD have been, for eva…

Thanks for asking

“Anybody ready for 15% interest rates?”

Yes please!!

Here’s something I was wondering Wolf. Feel free to ignore, but I figure you might be one of the few people around who is able to answer this question.

I saw a chart showing that the proportion of Americans with variable rate mortgages is at an all time low and it made me think. Is is possible that, due to flooding the economy with cash post-Covid, due to everyone refinancing into low rate 30 mortgages not too long ago, due to demographics and all of the boomers sitting on a pile of investments to get them through retirement, due to much of the lending now coming from non-bank lenders, is it possible that the increased money to consumers from higher rates on their savings is more than offsetting the higher rates those people with variable rate debt need to pay. And that any reduction in new private lending due to the higher rates is offset by the massive federal deficit/borrowing spree?

I wouldn’t even know where to start to assess the balance on the scales between higher interest receipts vs outlays from consumers as rates go up.

I still feel like we haven’t seen the necessary lag time yet to assess if rate increases will slow the economy as they have done in the past, but as the months go by, and I question my own assumptions, I wonder if something *is* different this time, and what is different is the impact of rate increases on consumers due to all the factors I listed above.

I know some people have said that rate increases cause inflation, but I always considered that a quack theory (eg see Erdogan in Turkey and the mess they have made of the economy), but it could be that they are just a very weak lever this time around, especially in the US due to lack of variable rate lending, and long terms for mortgages – if that is true, and the gov. is not smart enough to pivot from monetary to fiscal measures to slow the economy, then rates might end up going very high for a very long time. Long rates going up, as the post above seems to suggest, will just bring more revenue into consumers hands and may not slow down government spending, at least not for a while.

I guess time will tell.

If your hypothesis is correct I suspect the Fed will stop hiking, maybe at a per cent or two above where we are…realizing it’s not bringing inflation down, although curbing it some. Not sure how this could be done, but a combination of asset price softening and tax increases to balance the budget may be needed to get our financial house in order.

“I question my own assumptions”

Start there, and then proceed:

“all of the boomers sitting on a pile of investments to get them through retirement”

All? Several percent maybe. Better off than their kids will be, though.

“Long rates going up, as the post above seems to suggest, will just bring more revenue into consumers hands”

Higher interest rates don’t benefit consumers. They benefit whoever is charging them higher interest rates.

“Feel free to ignore”

I did try to, but sometimes I’m fascinated by word salads.

> “Higher interest rates don’t benefit consumers. They benefit whoever is charging them higher interest rates.”

That is, the subset of consumers who live as if they can always float along carrying significant debt at (presumed) low rates. I have never lived like that. Consumers who consume within their means, tend also to be savers, and indeed, for them (me), “Long rates going up, as the post above seems to suggest, will just bring more revenue into consumers hands.” Living beyond my means has always, for me, been a choice, I choose not to take. That takes advance planning and long-term discipline though. Grasshoppers can dance in the sunshine and expect cheap credit into the indefinite future.

“Higher interest rates don’t benefit consumers. They benefit whoever is charging them higher interest rates.”

Seems like you should have ignored it, since you missed the point. Higher rates on govt bonds, benefit people who invest their savings in govt bonds. So as the rates go up, people get paid more for their savings. How much does that offset the higher rates that people (govt in this case) need to pay when they borrow – that is the question.

I think your analysis puts way too much emphasis on mortgages. There is a huge portion of the economy having nothing to do with housing. There are a lot of companies that have to borrow to pay their operating expenses (zombie companies). The effects of higher rates hasn’t really shown themselves yet, as many companies still are burning through the cash they borrowed when rates were low.

There is a “lag effect.” That isn’t just a media talking point. Bed Bath and Beyond, Party City, etc. are just the tips of the iceberg.

Check out The Chicago Fed’s National Financial Conditions Index (NFCI). Financial conditions are now as loose as they were in April 2022 ! That’s why no recession, no market correction or crashes. Whatever the Fed is doing, it’s not working as they’re claiming. Maybe by design. Maybe they’re hoping to prop it up until after the election.

The Treasury is issuing short term debt, probably expecting the Fed will have to monetize the long dated Ts in the next crisis. Good luck waiting for those to roll off the balance sheet in 30 years!

According to Biden it’s all Trump’s fault….the downgrade and all that.

This continuing issuance and huge increase in interest payments will make Japan look like a piker in a few years time.

Place your bets on who is in the worst economic situation and it sure isn’t Japan.

People also forget that Japan still has a cohesive culture. That’s worth a lot. It’s not all just about GDP and debt.

Okay, so longer term interest rates are headed up, maybe by a lot. Assets (stocks, bonds, real estate) are going to lose value and maybe even get crushed. So… do I ride the yield wave up and continue to buy Treasury bills and bonds? That’s pretty much what I have been doing since June 2022, and I have enjoyed the result. I am now enjoying a “risk-free” 5.3% yield that is free of state income tax. Riding the yield wave up to even higher rates sounds great and long overdue. BUT, BUT, BUT… I’ve got a little voice whispering in my ear, “Beware: how can buying the debt securities of the U.S. government be your best investment option?”

Lots of smart, battle hardened contributors on this chain. I would love to hear your thoughts. Disagree or agree with me, but keep it positive. I’m trying to invest, not argue about politics. Thanks.

Howdy DT. Its your money and you earned it? Do what you think is best, trust someone else, give it to me…..

The big driver of very long term returns (30 year plus time horizon) has been the % of your portfolio in stocks. Knowing where rates are going to be in a year can’t be done. Buffet doesn’t hold anything in long term treasuries, and is a big believer that when there is a problem you better not get caught without a lot of cash or cash equivalents.

One of the best investment books I read said for average investors the sweet spot in the treasury market is around 5 years. It is far enough out on the curve to give you some yield, but not so far out as to drastic price swings.

I am not sure what Buffet is saying today, but a decade ago his estate for his wife was to be 10% cash / 90% SP500.

The credit market is telling investors to buy short duration and high credit( shorter term Treasuries) .

The stock market is telling investors to be long both those largest stocks with the highest P/Es and the those stocks with very little chance of generating FCF .

The answer is entirely political, because nothing is more political than money.

Anyway, in the current state of degeneracy which prevails in our country, you trust them to safe keep your interests? By all means, give them more of your assets to keep…safe, they would never gate them, tax them away, reallocate them, debank you, would they?

“…nothing is more political than money…”

and” follow the money”

Buying overpriced shares of stonks in public companies is still ultimately “investing” in the U.S. If you’re convinced that the degeneracy will ultimately destroy treasury bills, stocks aren’t safe either.

You’d have to buy non-U.S. dollar denominated assets.

Right now the level of “investment” in non financial assets is astronomical. Everybody buying overpriced houses, 100K+ watches and trucks, 10K+ designer items, the restaurants are busy, all those spenders are choosing not to buy financial assets with their dollars. All those dollars are being allocated away from paper assets, this trend is global, because everybody understands, nobody is safe.

I had a front row seat to the rise of financial assets in my lifetime and I can see the train coming at the end of the tunnel. Even the investor class is buying status. I think Musk is a smart guy, but $44B for a company that can broadcast a message to a chat board anybody can easily connect to, is nuts. Any programmer can write this in a month( goofing off most of the time, I know this for a fact). The status of the brand was worth more than the dollars.

Any suggestions to exactly what that would be E???

Seems to this old boy that anything and everything else is actually more risky at this time ???

Too old to build or rehab real estate any more, otherwise would be looking carefully at some of the dirt and construction already selling wwwaaaayyyy below what it was a year or two ago.

““Beware: how can buying the debt securities of the U.S. government be your best investment option?””

I have this voice in my head too – despite the fact that 75% of my portfolio is in Tbills right now.

My logic is: the only risk to Treasuries is a USG default or dollar collapse. Both of those are extreme scenarios and I suspect we’ll all be focused on other things rather than the values of our portfolios.

Wolf, thanks for the chart on issuance under neutral scenario, which I’m trying to interpret. The chart shows Aug at what looks like $250. But in your text you stated $270 ($103 + $167). Is there an error in the chart, or did I miss something in the text?

Yes, Aug, Sep, and Oct issuance spelled out in the article is what Treasury has already decided it will do, and what it is implementing.

The chart is based on one of the options, presented by TBAC, of what Treasury should consider doing. TBAC recommends. Treasury decides. The different scenarios outlined by TBAC (I picked the “Neutral” scenario) go into details about tenors (for example, shifting more to 7-year notes and 20-year notes in one scenario), which I didn’t get into.

Why are they referring to folks who sing in a particular key or something???

Just asking ,,, he heh heh

90% of the comments are Greek to me and don’t help me in my investment decisions. Only what Buffett says makes sense: the market is the only place to be long term and short term is not the place to be. So do what the very rich do: protect your capital and invest in the best of the US economy.

Buffett holds tends of billions of dollars of Treasury bills, making 5.5% and laughing all the way to the bank.

Buffett’s proclamation were made at a time when the U.S. had a very different economy and political climate than it does today.

QT hasn’t “bit” yet. If you look at the amount of bonds/bills owned by the Fed maturing in any given month, its far beyond the 60 billion tightening. More like 100-300 billion. That difference is rolled into whatever the treasury is selling that day/week/month. So the SOMA remains a buyer in size at treasury auctions. This will last through 2024 and only by about 2025 will the Fed start to really be absent from any auctions.

That’s when treasury auctions get a little wobbly, IMO.

“More like 100-300 billion.”

In terms of notes and bonds, that’s not correct.

Since QT started, the amount that matures every month has run from about $40 billion a month to about $110 billion a month. The Fed lets $60 billion roll off, and replaces the rest. In a month when $110 billion mature, the Fed lets $60 billion roll off and replaces $50 billion. In a month when $40 billion mature, it lets them all roll off and then also lets $20 billion in Treasury bills roll off to meet the $60 billion cap.

What is constantly being replaced are the Fed’s short-term Treasury bills (1 month to 1 year). The Fed still has about $260 billion in bills, and since they’re short-term, they mature all the time, and the Fed replaces them, unless the roll-off of notes and bonds is less than $60 billion, in which case it makes up the difference in bills.

“The Fed still has about $260 billion in bills, and since they’re short-term, they mature all the time, and the Fed replaces them”.

“100-300” was my range.

I downloaded the CSV file posted by the NYFed listing all the holdings by CUSIP. Some manipulations to tease out the maturity month year and then some calculations to factor in the roll off and you can see the exact progression of QT and the mountain of bills that will be rolled forward like a bulldozer pushing dirt, for awhile to come.

Wolf- I was just doing the work that you said you didn’t want to do.

Thanks!

Could you copy and paste the same comment also under the Fed-balance-sheet article under my comment about this topic:

https://wolfstreet.com/2023/08/03/fed-balance-sheet-qt-update-91-billion-in-july-759-billion-from-peak-biggest-drop-ever-to-8-2-trillion-lowest-since-july-2021/#comment-534165

And with the bond “route” what of bank bond portfolios?

All depositors covered again, Janet?

Don’t ask for whom the bell tolls. It tolls for thee.

The government will payoff the debt by using the money of the people that bought (assumed) the debt thinking it was a loan.

Nope. They will default. They are issuing so much of this crap, the planet could not consume it. They are going after the ‘Re-work” plan. Delusional belief in a Bretton Woods II. …part of “The Reset.” The not so great one.

The market is telling investors to buy short term and high quality assets-Treasury bills under a year.

Other assets such as long duration bonds are in a bear market ,while stocks and real estate are on the brink of a crash

“while stocks and real estate are on the brink of a crash”

“Waiting for Godot”

What I find confusing and confounding is people chasing yield now, with some, wanting to lock in current yields on 5 year treasuries, but willing to pay somewhat excessive costs for term premium.

As yields on 5yr have gone higher, its price has moved much higher, and we’re at an expensive range to be paying for future value.

It’s weird, but perhaps Wolf can explain why this time is different?

Wolf, any thoughts on how this reconciles with QT and bank deposits?

When the Treasury dept refilled the TGA account after the debt ceiling issue was “resolved”, it did so by primarily issuing bills. Since money markets are permitted to invest in bills, the growth in the TGA account was offset by a $0.5T decline in the ONRRP and did not materially impact bank reserves.

However, if the next wave is skewed towards notes and bonds, the ONRRP can not absorb this since money market funds are only permitted to invest in bills. Bank reserves will have to re-continue its role absorbing the brunt of QT. This means continued pressure on bank deposits and cost of funds from my perspective.

Wolf,

Can you please explain why this week’s 28-day, 56-day and 119-day Treasury Bill auction prices are EXACTLY the same as last week’s auction prices — to the sixth decimal place ?

I realize that such happens, but Treasury auctioned $70, $60 and $46 billion respectively — and the auction price is exactly the same as the prior week’s to the sixth decimal place ?

How & why does that happen?

I don’t compare prices that closely, and I don’t know if they did or if this is just another thing the internet made up, and it doesn’t matter. Apple’s shares too sell occasionally for exactly the same price down to the penny as a week earlier. I’ve got other things to worry about.

There is another way to look at buying long dated bonds. We’re undergoing the steepest and fastest unbroken ascent on Wolf’s wonderful chart showing gov interest expenditures as a percentage of tax receipts. In a year’s time, we will likely be shooting past a point where the gov is collecting tax money and spending half of it on interest payments on our debt. Keep in mind it was under 20 percent just a year ago.

So here are some points to consider:

1) We can’t sustain a 15% increase each year of tax receipts on interest payments.

2) Congress will continue to avoid spending cuts and/or tax hikes to address the situation.

3) The Fed could eventually be forced to become the buyer of choice again to avoid runaway interest expenditures as bond buyers demand a much higher yields on this tsunami of newly issued debt.

It’s a betting man’s game that has already blown up a couple of badly managed banks. But if you believe the points above are true, then buying long dated bonds could make sense. If the Fed is eventually forced to buy, then you would be in a great position to sell bonds at a higher price than you paid.

Yes, but if the Fed isn’t forced to buy, you’re locked into an overpriced asset with duration risk.

The people who bought 10 year treasuries at 0.54% or whatever it was in 8/2020 thought they’d be able to flip for a profit too. How wrong they were…

Einhal: Agreed, playing chicken with the Fed is a dangerous game. I personally don’t have the guts to do it, but I can see how somebody else might. Certainly buying in now at 4% yield is not quite as risky as when it was sub-1%, because the downside scenario (being forced to hold) may not be as disastrous.

Regular Joes buying long dated bonds are making a bet. And it’s actually a rational bet. As companies, regular folks, and the gov start feeling the crushing pain of higher debt servicing costs, and as bond buying dries up at lower yields with a flood of new notes and bonds rolling in, the Fed could be forced to relapse in their debt monetization addiction. And if something big blows up under these historically normal servicing costs in the next few years (I’m looking at you, commercial debt and RE), the Fed will “do whatever it takes,” including dropping the FFR and reinstating shock-and-awe QE.

I’m not saying it’s a surefire bet by any stretch, but it’s not an insane bet.

It’s nice to see the 10 year rate move 2% higher today. Maybe the markets are finally trying to price in heightened inflation expectations that are consistent with continued $2T deficits.

Money must be earned in sustainable economy. You can’t print it up and drop it from helicopters, like Bernanke says.

You must mean 0.2% – although I personally would welcome a 6+% 10-year.

The 10 year yield is over 2% higher than yesterday. Increased from 4.08% yesterday to around 4.2% today, threatening to break out.

Long bonds, and long bond funds like TLT, have lost 5% market value in three days.

Tech stocks are weak. Lots of speculative stocks dropping 20-40% on earnings announcements. Things are moving this week. Even Nvidia took a 5% hit yesterday.

Oh I see what you mean.

I agree with all that – and personally am short TLT.

From above, “The Fed wants higher long term yields…”. I agree for now. But the question is: Will the Fed pivot to QE if, or when, the higher rates cause an economic crisis? (Similar to how the Fed pivoted for the SVB banking crisis and earlier for the Covid epidemic). The higher rates go the more likely it is that an economic crisis will occur.

The Fed will eventually “pivot” to ending rate hikes. And if all goes well and core PCE durably goes down, it might “pivot” to cutting rates a little but not below core PCE. And if the US economy goes into a recession, it might cut a little more and still be at 3% or whatever.

The Fed may never do QE (bond purchases) the way it had done before. They all now see what long-term damage that has done to the economy that will haunt the economy for many years, including years of battling inflation at every twist and turn.

The Fed has already gone back to the old model before the financial crisis: rate hikes or rate cuts, and brief liquidity injections to solve problems instead of QE (long-term bond purchases).

I am not sure why anybody would buy T-notes or T-bonds (these are Treasuries over one year), unless they are legally obligated to. It is pretty clear to me T-bills (3 to 6 months) are going to 6%. Buy at auction, hold to maturity. Ladder while riding the wave. When the wave starts to crash, move to CDs.

Wolf and the Gang,

I had an interesting discussion with Lance Roberts about long duration treasuries.

I mentioned that Ray Dalio had concerns about buying long duration treasuries at present rates (Dalio’s argument is that we would be looking at stagflation with a flat yield curve, meaning longer tenor treasuries should rise to around 5-6% in the next 6 to 18 months, assuming nothing weird happens).

Lance Roberts said flatly that Dalio was wrong, which really surprised me.

Underlying his premise is that the United States is on the same path as Japan, meaning endless QE, interest rate repression, etc.

This premise appears to be widely held in the bond bull community, and almost has a character as a religious article of faith.

My personal opinion is that Japan and the United States have very different inflationary and spending dynamics (the US has a big army, different political constituencies endlessly pushing tax cuts and debt relief, shameless election vote buying, etc.), and that these political and social dynamics make the inflation outcomes very different.

The bond bulls seem to think that ZIRP is going to return and that everyone should load up, and that they are evangelizing this, and it is built on what I believe to be a faulty analogy to Japan’s economic path.

What do people think about this?

Am I off base? Is Lance off base?

I would like to get a poll going… not on what you believe, but on how you are allocating capital…

I tend to think Dalit I

Has always been the shaper of the two, but things seem very out of whack after the GFC and especially after pandemic.

It looks to me like people are paying high prices for various treasuries, making them very hard to measure in terms of future cash flow, more so with lingering sticky inflation.

My gut feeling is, people are making the same duration mistake banks made over the last several years, in misinterpreting future inflation dynamics, including, higher for longer terminal rate.

The thing I’m scratching my head over is, rising yields and prices of treasury stuff and the disconnect between the inverse relationship with equities…

Full disclosure: I have no idea about what’s happening.

Just a sudden hunch, but maybe the reason people are paying the higher term premiums, is directly related to sticky inflation, hence that’s a real-time barometer for inflation.

Makes sense that premium would be higher with inflation and lower during ZIRP. The higher treasury prices and increased premium decrease the yield…

I don’t know if Lance is right or not but like many people he has been conditioned with easy monetary policy of last 15 years or so where FED did nothing but kept on going with QE. People believe that if deep recession comes or if something bad happens ( e.g. big market drop ) FED is gonna come in with their QE.

On top of this, someone has to fun the Govt deficit and it’d be FED at some point in time.

It basically means long tern bonds yield has to go down, meaning bond value would go up.

I believe the long term bond bulls are correct and Ray Dalio is wrong. I would be loading up to the hilt on long term bonds around the end of this year.

Bond Vigilante Wannabe,

Lance Roberts is flat wrong. The 40-year bond bull market died in Aug 2020 when the 10-year yield was 0.5%. Now it’s 4.2% and heading higher. Everything has changed. Now we have the kind of inflation that we haven’t had for 40 years. Roberts hasn’t figured that out yet.

Wolf,

I agree, and I think that the underlying premise of Lance (and by extension all bond bulls) is false for 2 reasons:

1) It assumes that the Fed CAN actually control inflation without causing long term interest rates to rise substantially (the 70s proved that this isn’t always possible).

2) It assumes that the US will follow in the footsteps of the last 30 years of Japanese monetary policy history, even though the two countries have radically different economic structures and dynamics.

I believe that the current standoff is going to get resolved, and that putting these 2 false premises front and center and demolishing them will help save naive people a lot of money.

My feeling is also that the stock market is no longer a predictor of anything due to passive flows, and instead simply reacts to the bond market.

And the bond market is dominated by people who hold a return to ZIRP as an article of religious faith.

The day of reckoning is likely to be biblical.

Bond bulls are like RE bulls. They don’t want to believe their assets will depreciate.

‘This tsunami of notes and bonds … is occurring while the Fed, under its QT program, is letting about $60 billion a month in maturing Treasury securities roll off the balance sheet without replacement.’ — Wolf Richter

It is widely believed that the Treasury market is barely affected by mundane supply and demand issues. A bid will always be there, it’s complacently assumed.

But sometime soon, the poorly understood consequences of QT are going to bite both the bond and stock markets hard … just as the Fed’s poor understanding of the effect of doubling reserve requirements in 1937 kicked the economy back into Depression by 1938.

“Nobody knows nuthin'” — it’s true on Wall Street, and axiomatically true for the cane-tapping blind governors of the Federal Reserve. Accidents lie dead ahead.

I am looking forward to Jackson Hole, the last week of August! I sure hope Powell gives a speech. I remember his 9 minute 2022 bomb.

Copper and oil are saying party-on today.

Interest rate sensitive GROWTH is not so happy.