Stunning numbers out today. Investors will buy the securities, plus those the Fed steps away from. But… Crystal ball sees rising longer-term yields.

By Wolf Richter for WOLF STREET.

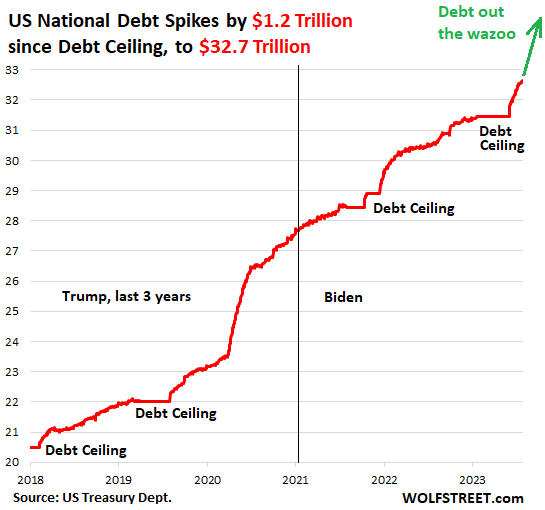

To set the scene for what’s to come in a moment: The total US national debt spiked by $1.19 trillion since the debt ceiling was lifted, to $32.66 trillion.

And to set the scene further: This $32.66 trillion of debt is composed of two groups of Treasury securities:

- $6.9 trillion of nonmarketable (not traded in the market) Treasury securities that have been bought by US government pension funds, the Social Security Trust Fund, etc.;

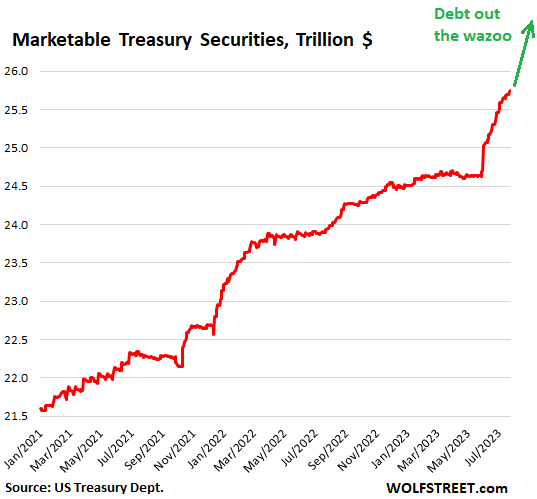

- $25.7 trillion in marketable securities (Treasury securities held and traded by the global public, from regular folks to central banks, including the Fed).

Marketable securities outstanding have spiked by $1.05 trillion since the debt ceiling was lifted on June 2, a huge amount of issuance in two months.

And in a moment, we’ll get into how much more will be issued for the remainder of the year: Another $1.5 trillion (as indicated by the green line and technical term for this phenomenon), according to the jacked-up projections released today by the Treasury Department:

Today’s debt-issuance shocker for the 2nd half.

The Treasury Department today jacked up its borrowing plans to deal with the lower-than-previously-expected revenues and the higher-than-previously-expected outlays, as the deficit keeps careening out of all control.

For the current quarter: $1.01 trillion in additional debt. This July through September quarter has only two months left, Treasury jacked up its borrowing plans by $274 billion, to total borrowing in the quarter of $1.01 trillion, up from the $733 billion it had imagined in May, according to its announcement today.

In other words, the government will issue over $1 trillion in marketable securities this quarter that the market has to buy this quarter, in addition to refinancing maturing securities.

Last time the government issued securities at this pace and faster was in 2020, but back then, the Fed was buying Treasuries hand over fist, including $3 trillion in March through May 2020. Now the Fed is shedding Treasuries at a pace of about $60 billion a month.

Markets not only have to digest the new issuance but also pick up the $60 billion a month that the Fed is walking away from.

The Treasury Department cited three main reasons for this $274 billion increase to this monster $1.01 trillion in new issuance this quarter:

- It raised by $50 billion the balance it wants to have in its checking account, the Treasury General Account (TGA), by the end of September, to $650 billion, from $600 billion as planned in May.

- It started out the quarter with $148 billion less in the TGA than projected in May. So it was behind before the quarter even started.

- It now projects “lower receipts and higher outlays” than imagined in May, requiring an additional $83 billion new debt to cover this additional deficit.

For the next quarter: $852 billion in new borrowing. In the October through December quarter, Treasury expects to borrow an additional $852 billion, to end with a cash balance in its TGA of $750 billion.

The way things are going, with these big upward revisions of borrowing estimates, along with the less than projected receipts and more than expected outlays, we can expect an upward revision of this $852 billion by the next update.

Total new borrowing in the second half: $1.85 trillion. In July – the first month of the second half – the government already borrowed nearly $300 billion. So for the five months from now through the end of December, the government projects to issue $1.56 trillion in new debt. Some of it to refill the TGA to $750 billion (from $550 billion now), and the rest of it cover the budget deficit.

Bon appétit, investors!

This is a huge amount of supply of Treasury securities coming to the market, on top of the $60 billion a month in maturing securities that the Fed is walking away from, and as they’re refinanced, the market has to pick them up too.

Yield solves all demand problems. That’s what yield is for, and it’s a good thing, we know that. You can sell even the riskiest junk bonds if the yield is high enough. So there will be buyers, but the yields will have to be high enough to attract them.

So far, the government has only increased its issuance of Treasury bills (securities of one year or less) and Cash Management Bills – a veritable flood of CMBs.

CMBs are the most flexible securities for the government. They are sold at auctions on short notice and outside the normal auction schedule. Their balance is not included in the above charted $32.66 trillion in national debt. CMBs can have peculiar terms, from one day on up to several months. For example, on July 27, Treasury announced that it will offer $50 billion in 42-day CMBs at an auction on August 1.

Even though CMBs are not included in the balance of the US national debt, they will still have to be absorbed by investors and are part of what investors have to buy.

The longer-term securities are coming. On Wednesday, Treasury is expected to announce a substantial increase in the issuance of longer-term securities – Treasury notes of 2 to 10 years and bonds of 20 and 30 years – most likely through increases of the sizes of its regular auctions.

This increased supply of longer-term securities will have to attract enough buyers with a yield that is high enough. Currently, Treasury bills are paying somewhere near 5.5%. But the 10-year yield is only around 4%. So this will be interesting.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

“For the next quarter: $852 trillion new borrowing.”

It’s a typo. Should be $852 Billion. But you know what’s sad? $852 trillion doesn’t sound THAT far away from reality. I bet my son will see that headline someday and it won’t be a typo. Heck, I’m only 39 years old, so maybe I’ll even see it in my lifetime!

Oh, good point. What comes after Trillion?

GOLD

Quadrillion?

One Quadrllion dollars. Probably can buy Alaska with that much money.

Only need 7.2 mil fo Alaska.

Trillion, Quadrillion and then Quintillion. In a pure fiat monetary regime, the sky’s the limit. The miracle of the loaves and fishes is nothing compared to the miracle of modern central banking.

The money is NOT coming from any of the central banks.

Next, confuse The Muppets with grade school scientific notation.

Pure yang transforms to pure yin

Quadrillion.

Perfidy, penury, fear and loathing….

The word “Trillion” was rare in Washington before 2008. Now it is the small integer game……3.1 , 4.2, ….the little decimals that are actually hundreds of millions.

The national debt was circa $9 Trillion in 2008, and GWB signed his last budget with a Trillion dollar deficit from the Democrat House.

But lost on all parties is the enormity of these numbers…

One billion seconds is 32 years.

One trillion seconds is 320 CENTURIES!

Think one billion seconds is 32 ,000 years.

I will need to googol these large numbers.

Starting in late 2020, the not “Federal” Reserve, banker cartel printed more and more dollars than were ever created in one decade or more. As long as the banks kept such funds, e.g. , at their “Fed,” inflation was not much. It has grown since.

Possibly, recession may tame inflation, which reportedly mitigated as to some goods already. However, with no tax increases on the owners of most, US capital (and thereby income) possible politically due to corruption (see “The Quiet Coup”), the ultra rich, how will the real, US federal government meet its obligations and defense needs given a certain, oncoming threat as higher interest rates on rolled over treasuries, issued to pay-replace low interest, coming due treasuries, squeeze its finances?

Wolf,

Do you think that Bill Gross is on target with his prediction of 10 year around 4.75% by year end? He had 70% confidence rating on this, but he has been pretty good so far this cycle.

Sounds reasonable. 5% sounds reasonable too. But at 5%, there will be stampede of buyers. For yields to rise further, that stampede will have to be satisfied first. If we get big whack-a-mole inflation numbers later this year, the stampede at 5% will be much smaller, and it might go over 5%.

Wolf,

During Debt out the Wazoo 1.0 (March – May 2020) yields fell. Why did they fall then but are expected to rise now?

Because the Fed was monetizing all of the debt that was issued back then, and then some, so there was no increase in the debt that had to be absorbed by the market.

(Note, the Fed didn’t directly buy from the Gov’t, they bought from dealers)

Johnny5/Wolf,

At some point higher rates will break the economy and the markets. Does the FED step in again if Debt out the Wazoo 2.0 forces the ten year to 5% and beyond? If not at 5%, when?

The higher rates haven’t broken anything yet (except for a few badly managed banks).

The big thing that has broken is “price stability.” That’s a huge thing, the HUGEST thing the Fed is in charge of, and it has broken into a million shards. So it will take a while to glue it back together with higher rates. The task of gluing it back together is made more difficult because the government keeps breaking them all over again with its reckless and very stimulative deficit spending.

Breakouts above 4% have been few and far between during this tightening cycle. But another is happening as I type this message.

Personally, I’d watch what Japan does. If it looks like they need to sell US Treasuries to fund a doubling of their defense spending – that could have a pretty big impact right away on US Treasury markets. Admittedly, I do not know how Japan’s 1.1T (or so) of US Treasury holdings are distributed across the yield curve.

Thanks BA,,, WE, in this case the family WE will try to pay more, repeat MORE attention to the situation in Japan as another ”leading indicator” for WE, in this case WE the usually uniformed except for Wolfstreet.com so called retail investors…

To be able to invest our hard earned by actually producing something USDs.

And will only add that sooner or later, the entire edifice built up on and depending on tons of so called derivatives will hit the bricks,,, and to be sure I do NOT mean the so called BRICs…

This is just absolutely disgusting. I don’t know how else to put it.

Forget about daytime drama shows and horror movies, just visit this site for gut-wrenching end-of-the-future reality.

As I am paying +25% of my salary to this GOV, I am feeling my gut is being ripped apart. Almost zero responsibility these days – our people in CONgress just don’t get it.

Your paying way more than that lol. You forget about all the other taxes depending on where you live like 5 taxes on a gallon of gas, 6 taxes on liquor, 6 on cigarettes, real estate, licenses, tags, Sales tax and those sales taxes are taxing taxes, hidden taxes on sugar the list goes on and on! Most people don’t have a clue about all the taxes they actually pay.

Corruption

And these corrupt-to-the-core Congresscritter maniacs continue to spend and pump inflation to the hilt. Like Wolf says, governments will always choose to inflate away debts. So, look forward to more massive inflation, and poverty….

We have 2 options to preserve the nation in the grand scheme of things:

1) We can find some blend of lower spending and increased tax revenue to run a balanced or even positive budget.

2) We can inflate the currency to “pay” our debt.

And let’s face it, option 2 isn’t sustainable forever, so option 1 is ultimately the only viable path. But it’s looking like there’s a 0% chance that voters and politicians will ever choose the viable path. So Depth Charge, you are 100% correct. The path ahead is one of inflation and an ever-decreasing standard of living for most Americans in the long run.

The baby boomer generation holds 90T in private wealth. Wealth that is a direct result of the result of a 30T+ government deficit. The 30T in overspending has to go somewhere, it’s been divvied up into the private wealth of the American people. It’s time to begin paying back what has been borrowed. Upon death, baby boomer estates should be taxed at a flat 30%, with no exceptions.

Maybe you should be blaming those greedy teachers and firefighters – the ones who can’t afford to live where they work.

Jeff Bezos, Elon Musk, Michael Bloomberg, and Carl Icahn, in recent years, have paid zero in federal income tax. Maybe you should talk to them. They’re set to become trillionaires.

Money flows uphill, Mr. B, and it’s flowing uphill faster all the time.

Depth Charge,

Uncle Sam’s monkey on the back just gets bigger and bigger. The question is, when it will it break Uncle Sam’s spine, the almighty dollar?

As Wolf says, “Yield solves all demand problems.” But this yield also has to be paid to feed the monkey.

As of May 2023, the CBO say that fiscal year 2023’s revenue will be $4.815T. We are two months away from fiscal year 2024, and the CBO predicts that in ’24, revenue will be $4.848T.

But a 5% cost to carry $33T = $1.65T (Yes, some of the cost to carry is held now @ longer term & lower interest rates than 5%. But in general terms, this works.) So, we are close to having the cost to carry equal to one-third of annual revenue. That might be one-half in the not too distant future.

You’re damn right, “This is just absolutely disgusting.” Nope, there is no other way to put it, without using some appropriate eff-bombs anyway.

Not once did I hear of the cost of servicing the increasing debt in the debt “ceiling” deliberations.

The politicians are oblivious to the realities.

I just hope the Fed doesnt step in to curb the free market reaction to this increasing debt.

And what of the forgotten bank portfolios loaded up with long term debt? More problems with the higher rates.

And the unrealized losses at the Fed…..

I will point to the forgotten 3rd mandate of the Federal Reserve….one of the mandates that allows their existence and is agreement and instruction to allow their special powers..

“Promote moderate long term rates”…..and what the Fed did beginning in 2009 was POUND long rates to all time LOWS….immoderately low. “Moderate” means not extreme….either way. But there was not a word of objection.

We need a positive yield curve, IMO. The BOJ is wobbling.

‘what the Fed did beginning in 2009 was POUND long rates to all time LOWS….immoderately low. “Moderate” means not extreme….either way. But there was not a word of objection.’

Not from the Financial Industrial Complex. Those rates saved their collective -bleeps!- and and enabled them to resume profiteering. But Our Illustrious Blogger here posted plenty of objections.

The debacle of 2007-2008 never really ended. It just got papered over with debt, but the problem with kicking the can down the road this way is that eventually you run out road.

Many Wallstreet funds believe that long-term treasuries will go down as we are headed into a recession. This happens in all recessions. They are all recommending bond-funds that have loaded up on treasuries of mixed duration as sure fire way to get a 20% upside within the next year.

Interesting to see how the issuance of new debt and no takers resulting in higher yields coincides with the recession message

Long-term yields went down for 40 years, interrupted by brief increases. But that ended in Aug 2020, when the 10-year yield bottomed out at 0.5%. So nothing in those 40 years can be used as a model.

Before 1982, long-term yields went up for 20 years, with only brief dips late in the recession (1970) or two years after the recession (1976), and only just a tad, before surging again.

For a model, you need to look back in time when we had this kind of inflation burst on the scene, and that period was the 1960s and 1970s.

Deficit financing of the Vietnam War, the entry of women into the workforce in huge numbers, and the coming of age of the Boomers triggered the inflation of the Seventies and early Eighties. A multi-trillion dollar injection of monetized fiat into Main Street and the de facto adoption of MMT by both parties during Covid triggered the inflation of the present. The difference is the puny accumulated federal debt back then and the immense debt we have now. Have no fear-the USS Titanic is unsinkable!

Keep in mind, the Fed has already “hidden” circa $5 Trillion in long term debt from the market by absorbing into the balance sheet…..beginning in 2009.

That is unprecedented in the history of the Fed.

Now, with QT assumably to continue …. what then of the new supply finding a home? Which of course is why there never should be stimulus when it is not absolutely necessary.

If this isn’t inflationary, I don’t know what is. Higher for longer.

Yes, that’s one of the big problems with this scenario.

And oil prices are now heading higher, which won’t help either.

I’ve been saying for almost a year now. When everyone is convinced we’re not going to have a recession, that’s when we’ll have one. We’re getting closer.

In the huge US oil and gas sector (largest in the world), higher oil prices are a godsend. They create investment and jobs, and they stimulate manufacturing of equipment and vehicles, they stimulate construction, etc. Don’t count on higher oil prices causing a recession. They didn’t last year either. And they didn’t in 2011-2014 when WTI was $100-$120.

The end game is currency devaluation and inflation.

People ( working class ) not sitting on assets would be punished.

But will asset appreciation out run the short term interest rates going forward?

As I keep saying…

If you reckon the value of your house in terms of dollars – the value of your house will never go down again

If you reckon the value of your house in terms of short-term needs like a gallon of Milk or gasoline, or a pound of chicken etc. – it may never go up again.

Therein lies the reason why the poor get crushed and the rich are fine with inflation. You can spread your payment on a house (asset) over time and if inflation is hot, you get to pay the loan back with increasingly worthless dollars, so it becomes a smaller debt burden over time. Today’s $2k/mo mortgage payment might feel like a burden now, but it could feel pretty light after 10-15 years of cpi and wage inflation when a crummy studio apartment is renting for $4k/mo in less valuable dollars.

But milk is not durable, so you have to buy it with today’s money. Worse yet, food price increases tend to lead wage increases, so the paycheck-to-paycheck crowd is paying today’s increased milk price with last year’s decreased dollar value, making the real burden even greater. Rich folks have assets while poor folks have to burn all of their money on consumables. The poor folks certainly don’t own the Fed, so it should be pretty clear why the rich are being favored.

What kind of assets?

But… but…all the MSM business news said today there will BE NO RECESSION.

With this kind of deficit spending — a huge stimulus! — how can you even have a recession?

But you can have inflation!

Wolf most of stimulus is being put into economy by employee retention act ,pretty sneaky

So would this time be ” different” with QT?

Mosler has been banging on about the fiscal stimulus (particularly via the interest income channel) for at least a year now — maybe others will start to catch on?

MMT sucks.

Yes I wonder what kind of unspoken arrangement goes on between the Treasury and the Federal Reserve. Do they never talk to each other so they don’t have to admit that one is creating inflationary conditions while the other is trying to do the opposite?

I’m not sure who, but I do recall that someone said ‘debts don’t matter’. We’ll, we’re about to find out but it’ll probably take awhile…

IIRC it was Dick Cheney, in the early Reagan days, who said “deficits don’t matter”. He was correct back then, because Reagan inherited a debt to GDP ratio of about 36% from Jimmy Carter. Fast forward to today, with a debt to GDP ratio of about 112%, and deficits really do matter, especially when they’re huge and piled on top of trillions in Covid spending.

No wolf said that in his previous post, declaring Debt doesn’t matter because the debt-to-GDP ratio is not increasing. I still remember it lol. Looks like he changed stands afterwards.

DebtsDoesntMatter,

Your brain has deteriorated too much. Booze? Or maybe you never had a brain. Could be. Happens. Here is what I said, my entire comment on July 26:

“Once a quarter, I do an article on how much tax revenues the governments gets and how much interest it pays, and what percentage of tax revenues goes to interest. This chart was the latest. Bloggers that just talk about the spiking interest without talking about the surging tax revenues are morons:

https://wolfstreet.com/2023/05/29/update-on-the-us-governments-holy-moly-debt-interest-expense-and-tax-receipts-and-how-they-stack-up-against-gdp/

During the high inflation days, the 10 year got to around 15.5% and SP500 got to PE of 6.9 (earnings yield of 14.5%). Thus the saying interest rates are like gravity. Buffet closed his hedge fund and owned no stocks at one time.

To appraise the effect of the Federal budget deficit on interest rates, it is necessary to compare the deficit, not to a debt to N-gDp-ratio (a contrived figure), but to the volume of current net private savings made available to the credit markets.

Unprecedented large deficits “absorb” a disproportionately large share of N-gDp (as gov’t spending is a component / factor of N-gDp).

Based on that chart, we’ve gone from a burden under 20% to darn near 35% in just half a year. This recent period is represented by the steepest ascent on the whole graph. From the lowest point since at least the 70s quickly reaching the highest it’s been in a quarter century!

With continued incremental hikes and huge debt issuance as far as the eye can see, we’ll be at 50% pretty darn quickly, perhaps in a year or two even if the slope flattens out a bit due to rate hike pauses or reaching a terminal peak in 2024. So when does this start becoming a problem big enough to kick the Fed back into Japanification mode? At some point debt buyers will refuse to buy at a still historically low 4% yield and they will only be willing to buy at yields too high for the Gov to sustainably support. I suspect this burden will be the beast that gov must again start feeding with printed money at some point. “Higher for longer” sounds dandy. But how much longer until 50% and then 75% or more of the government’s revenue is eaten up by debt maintenance alone? Not that long at the current rate of increase. And we sure as heck won’t cut spending or increase real tax revenue, so we’re going to have to print it.

old school said: “Buffet closed his hedge fund and owned no stocks at one time.”

——————————————-

Don’t spread errant history. Footnote that Buffet owned no stocks other than when was a kid.

The last time the Federal debt to GDP ratio was this high, the top marginal income tax bracket was north of 90%. Congress is captured by the plutocracy at this point, so massive inflation will be the endgame this time, country be damned.

‘Reagan inherited a debt to GDP ratio of about 36% from Jimmy Carter.’

Reagan’s tax cuts for the rich caused an explosion in federal debt so huge they were soon followed with the biggest tax increases in US history. Naturally Carter gets blamed for Reagan’s policies, just as Obama gets blamed for the policies of Bush II.

According to Investopedia, US federal debt increased 160% under Reagan, but less than 30% under Carter. Clinton nearly balanced the budget, thanks to tax increases under Bush I, but tax cuts for the rich under Bush II and more tax cuts for the rich since then now makes that impossible.

The numbers don’t lie. Without the Bush and Trump tax cuts for billionaire and corporate profiteers, debt as a percentage of the economy would be declining permanently. Tax Cuts Are Primarily Responsible for the Increasing Debt Ratio. You can google it.

There are all kinds of lag times between when a policy is implemented and when its effects are truly known. Sometimes years, and often a decade or more. Truth is the President at any given time doesn’t affect nearly as much as they’re given credit for, or are beaten up for. They’re most fervently blamed for problems that were almost always at least to some extent inherited. Obama inherited a massive economic disaster that came about during the Dubya admin. That admin had no shortage of faults, but at least some major components of W. Bush’s disaster were also influenced by the policies of past admins as well. The budget was balanced during the Clinton years by a Repub congress (let’s not forget). Big Repub tax cuts have a played a huge role in our deficits, but lets not ignore the multi decadal non-stop explosion of Gov spending we’ve witnessed. 2 decades of mid-east wars with largely bipartisan support weren’t cheap either.

This is such a huge 2-headed beast that we would need to raise taxes AND cut spending (both significantly) to ever hope to see a balanced budget again. Alas, neither side of the isle seems particularly interested in doing so. We already know where this is going… We’ll just print the money.

Occam. You are half right. The actual quote: “(President) Reagan (r) proved deficits don’t matter.”

Dick Cheney (r).

Cheney was VP at the time (2003) to President Baby Bush (another r). And he was justifying another round of tax cuts. This fits with a rich tradition of conservative tax-cutters abandoning deficit hawkery when they want to hand money to favored groups.

Just my 2¢ to set the record straight.

And “Reagan’s” deficits were the result of a compromise with Democrat Tip O’Neill: each got the spending he wanted, at the expense of bloated deficits. But we can pretend that Congress has no say in the budget.

LOL. There is a second part to this sentence: Debt doesn’t matter – until it does.

Howdy Folks and YEA HAW. Don t lock in on 10 or 20 yr T Bills. We is just gettin started. Long way to go and only a few months have passed……

Minor nomenclature fix:

1-year T-bills (everything of 1 year or shorter is a “bill”)

10-year T-notes (2-10 years are “notes”)

20 year T-bonds (20-year and 30-year are “bonds”)

Don’t ask me who came up with this, but that’s what it is.

It’s not clear how inflation gets better from here. At any given time, there is a finite amount of stuff available for purchase. So every unit of purchasing power spent by the government has to come from somewhere else. If it’s not taken in direct taxes, it is taken by indirect means. Either the cost of money goes up or its purchasing power goes down, or both. It’s not manna from heaven.

Whether you’re trying to buy a home or groceries, the uphill battle gets steeper.

Quantitative Easing (QE): Around May 2023, the Federal Reserve sent out the news that in 2024 they will start buying back long term treasuries, for “Liquidity” purposes. Financial reporting is that they are hard to sell. This sounds like either QE or the so called “Twist;” both designed for interest rates to avoid market price discovery; i.e., down. interest rates. Seems like that balance sheet graph is going to stop going down.

BS. Bloggers out there who say this is QE are ignorant morons. Don’t go to their sites and don’t read their braindead shit. They’re lying to you.

QE is done by the Fed with newly created money.

The Fed is NOT the Treasury Department.

The Treasury Department cannot print money and cannot do QE.

The Treasury Department is planning to exchange old securities for new securities. This has to do with the fact that if you have a 10-year note that was issued three years ago, it’s hard to sell, and if you do sell it, you will get a lower price due to the liquidity issues. I learned my lesson with that. So now I hold Treasuries to maturity because when I sold them in the past, I got screwed because there were few buyers for older Treasury securities (lack of “liquidity”). This happens to everyone. It’s a well-known issue in the Treasury market. By exchanging some of the older bonds with new bonds, which are easy to trade, the liquidity in the market increases.

They are liquid if you are willing to take the duration related loss in a rising rate environment-just ask SVB. Or is it that no one wants a seven year instrument even if there is a duration-related capital gain?

Nope, that loss of market value when yields rise is a different issue, it’s where market value is BELOW FACE VALUE.

The liquidity issue is where you end up selling bonds below calculated MARKET VALUE (at a higher than market yield), in a market with few transactions.

Each bond issue is unique. There is no bond issue like it. Different maturity dates, different coupons. With corporates, it gets even more complicated: different covenants, different assets securing them or nothing securing them, etc.

The liquidity issue is that older bonds don’t sell readily. Older corporate bonds may have no trades for years.

But the Treasury market is supposed to be the most liquid bond market in the world — it underpins a lot of financial stuff.

So to get someone interested in buying $1 billion in older bonds, you end up lowering the price below calculated MARKET VALUE — selling them at a higher yield than calculated MARKET YIELD in a very thin or no market to this particular bond.

So if you’re trying to sell $1 billion of an older Treasury issue, you can, but at a big discount from calculated MARKET PRICE — in other words at a higher yield (lower price) than market yield. That’s the issue here. It’s a well-known issue in the world of bonds.

Considering Wolf’s comment below….

Should one chasing UST yield focus on purchase of older bonds with the intent to hold to maturity?

For example, assuming FED raises interest rates to 6%, is it sensible to buy a 10 year note if one can get > 6% to maturity?

INDY

Cash for bondkers.

“You can sell even the riskiest junk bonds if the yield is high enough. So there will be buyers, but the yields will have to be high enough to attract them”. Wolf

NOT IF THERE’S ZERO CHANCE OF PAYBACK.

As Confucious once said “that which is unsustainable, cannot be sustained”.

No more recession is possible!!!! Deficit drives spending, which drives inflation, which drives more deficit!!!

My logic is unassailable, and the stock market is going Dow 900K!!!!

Lewis Clark Credit Union is offering an 11-month certificate special paying 7.23% APY. It also has a 19-month certificate special paying 6.43% APY. Great time to a resident in the state of Washington or Idaho. All the 2 comma wealth hoarders can sleep easy knowing their money is working overtime compounding interest. Americans will be upgrading to first class tickets, dining at the finest 5 star restaurants, and continue shopping for luxury items attainable by the few. More work visas will be needed to cover the workers needed for service and hospitality industry. Here in Colorado migrant workers come every year to keep the ski resorts staffed and running efficiently. We entering somewhat of a Golden Age of elite spending, our Federal Government debt should be required reading for all 6th graders.

That’s good rate. My credit union is doing 5.25% 18 month CD. I believe Vanguard fed m/m is at 5.19% today and rising. Should peak in a few weeks at about 5.26%. If Fed Funds stay where they are the compounded return should be close to 5.5%. That’s about 1% more than our local regulated utility.

Wolf – the St Louis Fed chart shows interest cost as pct of tax rev for mid 80’s at over 50%. Seemed hard to believe it was ever that high so out of curiosity I poked around and found that other sites didn’t match. Not sure why.

Once a quarter, I do an article on how much tax revenues the governments gets and how much interest it pays, and what percentage of tax revenues goes to interest. This chart was the latest.

https://wolfstreet.com/2023/05/29/update-on-the-us-governments-holy-moly-debt-interest-expense-and-tax-receipts-and-how-they-stack-up-against-gdp/

To calculate this, you have to take actual interest expense (not adjusted for inflation, not annual rate) and divide it by actual tax receipts (not adjusted for inflation, not annual rate). If you use seasonally adjusted annual rates and inflation-adjusted data, the results go all over the place.

Thanks Wolf for taking the time to clarify this.

Clown show, top to bottom.

Why should I even contribute to this bs soceity.

The system is stealing all my stuff. I’m not going to play this game anymore

There are trillions upon trillions of dollars held outside of the US. No one seems to be thinking about what happens when those holders decide enough is enough.

What happens?

“What happens”

Yields will rise high enough to where I will finally want to buy some of the 10-year, 20-year, and 30-year Treasuries. I’m looking forward to it, as are a gazillion other investors. Not sure if we get there, and where “there” is, but I know what to do if we ever get there (back up the truck and load up).

Given the utter lack of spending discipline in Congress, the promises made by politicians, and the expectations of the public, long term federal instruments might need some implicit YCC expectations via the Fed. Otherwise, the risk of capital losses in an inflationary environment is too great. The US got its spending habit under control in the nineties and early 2000s; the GFC blew up that restraint and Covid incinerated the fragments. The US government and its people are also much different in attitudes now than 25-30 years ago. Things will get better on inflation in the short run but medium and long term it looks bad. Duration of two years or less might be a good place to hide.

@ Wolf –

Have you considered Occam’s point as you look forward to “backing up the truck”?

If Occam is just close to correct, long term Treasury’s become a loser.

That’s what makes a market.

What I said is that yields would have to be high enough, and that they’re not nearly high enough now.

If it happens, it could be a pain-trade: with high yields and high inflation and everyone despairing that inflation will never come back down, et. etc. like in 1981. People who back then bought 30-year bonds with a 15% coupon made out like bandits for 30 years (unless they bought callable bonds that then got called, and many did). That was the pain trade. It wasn’t obvious at all. People lost sleep over it.

Debt doesn’t matter as long as others willing to play the game. BOJ has shown what the FED can do when it needed to. The FED can always step in to stabilize the market when the YIELD SPIKE. So, will you play another game that currently promoted like the GOLD base currency? Will other players started to use own currencies for bilateral trade? These will crucial to bring the END to this notorious ballooning debt.

“So there will be buyers, but the yields will have to be high enough to attract them.” – but the question is how much yield is too high for the creditor or for the economy?

Emil

“the question is how much yield is too high for the creditor or for the economy?

15.5% yield for 10 y bond in the very 80s but the inflation was close to 20% (until Volcker tamed it)

Are we going to have similar scenario? I don’t know.

This is important information. Thanks again Wolf!

We are getting closer to the end of this cycle. Whether it be a recession or a soft landing, this indicates we are close. Banks continue to tighten. Oil has had a big rally and Dr. Copper is in an up trend but down big today. China is reluctant to boost. So, I continue to watch.

Incidentally, one of my oil company dividend plays declared a special dividend which in addition to it’s quarterly dividend is about 4-1/2 percent this quarter! I like my natural resource dividend plays!

If it begins to look like a probably recession I will dump half of them and short zomby companys that need low interest rates. But not yet. It’s time to watch and be flexible.

I agree, and precisely why I have been in and out of four week T-bills, picking up close to 5.5% interest while these opportunities materialize.

What do you think of ICL? International fertilizer company that has taken a beating but still paying over 10% dividend with a low P/E and solid income. What am I missing. If inflation is really going run wild, I don’t see how quality stocks don’t go up (along with bread etc.)

WB,

I don’t know about ICL. I am too lazy and or dumb to do fundamental analysis. Neither Schwab nor Morningstar rates it.

I did see this for July 10th:

S&P Reaffirms ICL’s BBB- Rating with a Stable Outlook

The Company hereby reports that S&P has reaffirmed its Long-term Issuer Default Rating at BBB- with a Stable Outlook. In addition, S&P reaffirmed the Israeli local rating at ilAA stable outlook.

—–

S&P says: 3 year cumulative default rate for BBB is 0.91% which seems ok for that dividend. But sadly I am older and I no longer swing for the fences.

That is the sort of company I like though. I like companies that produce things necessary to human life. I don’t understand Tech Growth even though I know it is powerful.

Like this next tech wave, AI, is going to wack the stuffings out of the ‘mind workers’, ie… doctors, lawyers, writers, teachers … I guess it is only fair since laborers and assembly line workers have been getting wacked for 50 years.

Wacking on ‘mind workers’ though may produce some dandy push back! It never gets simpler…

WB

Quality stocks (Value stocks?) also get trounced once the stampede begins for any valid or no valid reasons. Gone thru more than 1 bear mkt since ’82.

One has to stick them more than the assumed ‘recovery’ time and that is the hard part. I do like that stock and on watch list

Yeah everything gets thrown out in a recession sell off but we aren’t there.

GDP and employment are fine and inflation is down by half though the next half is looking together. World manufacturing is slow but not off the cliff or even near the edge.

The world is trying to reorganize, the markets are trying to climb the wall of worry. This is the time to be flexible.

TC and WB

The total Global debt to GDP is over 350%, unlike any time before. The current wealth is built on thin ice of ‘debt on debt’ with no underlying productive economy.

QEs have inflated the assets. Stocks by any means are in over valuation zone.

I am fairly deep in retirement and can not afford to be NOT conservative. I won’t bet another bull or extension of this after 14 yrs with S&P gain of nearly 400%.

Reversion to the mean is a part of all mkt cycles in the 200 yrs of US mkt history. It can be delayed but cannot be banned.

To each his/her own.

All the best for you.

It is possible to overcome a large national debt load with persistent high inflation. Which at this point, seems like the only option given the size of the national debt. But the problem is that congress is creating new debt so fast that there is no acceptable level of inflation that can keep up with it. I am not sure where that leaves us. A single massive blast of Hyperinflation? Total economic and political collapse with a restart at the end? Am I missing a choice here?

Thats right, we could knuckle down, drop federal spending to a pittance, and all agree to pay high taxes for decades to clear out the debt through toil, sweat and frugality. Nevermind!

No, it is certainly not possible at all to do that.

I think the real plan is to inflate at 3-6% per year, in a controlled manner, which means pretending there is a 2% inflation target. Realistically, they can hoodwink the population for a while longer, before more drastic measures are required such as additional money printing and debt monetization.

My bet is they keep heading down the debt monetization path until they absolutely cannot. Unfortunately, today’s leaders don’t have the stomach or fortitude to handle a significant market correction or moderate recession. The past 30 years shows us the Fed favors cry babies over prudent decision-makers.

The previous (high) pivot point was when inflation was nearly 20% and the 10 y bond was 15.5%. in early 80s under Mr. Volcker.

No one knows what’s ahead. Amount of private and public (including Global total debt) are a lot worse now, then and even since 2008.

But again, one should remember this is the same gang who brought us TWO boom-bust cycles in this century! 3rd time is charm, right?

No Country in human history has prospered by spending debt on debt in the long term. Will that be different this time?

Stay Tuned!

Okay, that’s US federal debt. The Government Accountability Office states that “The federal government faces an unsustainable long-term fiscal future.”

Now add in corporate debt, as reported in previous articles here. Wowsers. And next add in household debt. MarketWatch reports that U.S. consumer debt is now above levels hit during the 2008 financial crisis, and that’s without a recession. More wowsers.

Still, it’s all good, sort of, so long as the economy can continue to levitate on increasing rates of debt. The bad news is that it can’t continue to levitate without increasing rates of debt, debt can’t continue to increase faster than gdp indefinitely, and gdp can’t continue to increase by plundering the planet unsustainably.

The worse news is that Anthropogenic financial, economic, social, political, technological, and ecological Catastrophic Risks are all increasing. They’re probably worse than reported because these risks are routinely low-balled so as to avoid accusations of excessive pessimism, for example, climate change projections.

Hedge the projections here and there and add them up, accounting for certain synergies and mitigations, and civilization collapses around 2040, but probably sooner. It’s why the billionaire class is grabbing as much as they can as fast as they can. They know what’s coming.

The billionaire class isn’t magically smarter or more knowing of the future. The statement “they know it’s coming” is unfounded and just uses tribal psychology.

Billionaires buy up stuff because they have the money to do it.

Two of my brother-in-laws are billionaires (VC guys, undergrad Stanford, Harvard MBA). They are intelligent and know how to deploy capital, but very privileged. They have no “income” in the traditional sense. They have numerous investments that involve controlling shares of productive business ventures. So long as money moves through those businesses, they keep taking their pound of flesh. Having said that, they also seriously believe that the world would be better off run by benevolent dictators. They also suffer from serious cognitive dissonance. They really think capitalism made them so wealthy all the while turning away every time I mention “mortgage backed securities”… Arrogant pricks, Carlin was right about the “club”.

WB

“Having said that, they also seriously believe that the world would be better off run by benevolent dictators.” — I laughed when I read this.

Just where do you find ‘benevolent dictators’? Do they have a special line at the employment office for them?

The way I read it: “benevolent dictators that are benevolent to billionaires.”

@ WB –

Sounds insufferable having arrogant billionaire brother in laws.

1. If capitalism didn’t make them wealthy, what did?

2. Did they make their money via mortgage backed securities? Do they tuen away because they recognize mortgage backed securities were a con job backed by the FED/Government?

‘Anthropogenic’, ooh! Nice!

Bonds getting rushed like Soylent Green.

Only $60B not refinanced.

TLT should be <90 but its just under 100 today as 10yr finds a 4 handle. Rabid buying.

Profligate spending policy means those monies borrowed in August will be injected into our economy by early next year.

No landing.

Living in a no state tax of FL, I look to short term CDs as well as T-bills. I noticed for the first time that the short term CDs are not at the their usual 1/4 to 1/2 percent higher than the T-bills.

So I am back to buying just T-bills.

Wolf, is this a short term anomaly? If not, should we be worried for the banking industry as more people will be withdrawing their funds for higher interest T-bills?

Banks respond to supply and demand, driven by their need for cash. They’ll try to sell brokered CDs at the lowest rate possible, but it’s competitive, and a if bank out-offers others by 0.1%, so 5.1% when others are offering 5.0%, than that bank will sell all its CDs while the other banks wait for this supply to be eaten up. The market for brokered CDs is very dynamic. As is the market for Treasury bills. On a day-to-day basis, they don’t always move in the same direction.

I am wondering the same thing. This is exactly what I have been doing.

Wolf, we would appreciate your insight. Could this be a new era where banks become “just banks” (actual intermediaries and good stewards of savings and capital…)

Your parenthesis would be wishful thinking,. Ever since there were banks, banks collapsed. That’s why they’re so heavily regulated. It’s fundamentally an unstable system (borrow short, lend long). But it functions normally well in what it does (payments, intermediation, etc.) and fills an important role in the economy. Higher rates however might clean up the sector a little, and that would be helpful.

Sounds like there is clearly a demand for such good stewards. Crypto does not fix this, but will the new Basel III “rules”? I think that is what the IMF is hoping.

Yes, there is lots of need for “good stewards.” Better regulation would help. Separating commercial banks from investment banks and hedge funds would help (like Glass-Stegall did), etc. But share prices, share buybacks, bonuses, stock-based compensation, etc. are far more important in running a bank, it seems.

Gabriel,

It’s definitely an interesting time to shop for CDs.

It’s pretty easy to get 5.5% for 12 months right now, but I’d rather take 4.5% for 18 months.

I think we’re going back to ZIRP within 12-18 months (if not sooner) and when we do – we’ll be there until the End Times.

If that happens, your dollars will be worthless anyhow, so no use worrying about it.

3.27 trillion by 150 million workers is 218K per worker.

A good question instead of whats going to happen in the future is how exactly the US has managed to get to this point succesfully at all, and the reason must be that major holders of treasuries -cannot- sell for some reason, so minus these holdings the market is relatively small.

The central banks can’t sell their dollar reserves, and China/Japan/Korea can’t sell without revaluing to the detriment of their export markets. So this is a standoff in a way.

Yes, definitely. It’s ALL just a fiat game. NO WAY those export markets want to hold the reserve currency, why don’t people understand that?

LOL. They want to hold it just fine. Lots of countries have INCREASED their holdings of Treasuries:

https://wolfstreet.com/2023/07/19/time-to-look-at-foreign-demand-for-the-incredibly-ballooning-us-national-debt/

Chill Wolf. You abruptness and emphasis is not necessary. That should read export markets do not want to BE (not hold) the reserve currency!

OK, “not want to be” is different than “not want to hold”

Looking at Chart #2 of that link which shows the “% of US Treasury Securities Held by Foreign Holders is clearly decreasing. Yes, SOME countries are increasing their holdings, BUT are they merely vassal states? The UK is gonna save us? LOL indeed!

It’s a GOOD THING for the US that the US has been, in relative terms, relying less on foreign holders to finance it debts. That’s what that chart shows. As I said just above that chart: “In other words, the US debt financing has become less dependent on foreign holders.”

In absolute terms (dollar amounts), foreign holdings are near record highs.

Yes, but if this is down to anything more than implied US security guarantees, the Britons’ desperation to vicariously hold on to its empire via its American progeny, and India’s continued distrust of China (Quad) – then I am a two-headed unicorn. Whatever the reasons – treasuries remain in demand for now.

The Brazil graph is pretty telling – I’d say they are all-in on the multipolar BRICs narrative now. Not a bullish development for the dollar long-term

Maybe Brazil used their dollar holdings by selling them to defend their own currency?

Yes, a standoff like one of the early scenes in blazing saddles. Seriously though, why don’t people understand why those export markets do not want to have the reserve currency? In the meantime, the interest and short duration of the four week T-bills is looking more attractive while waiting for other opportunities.

Specifically for Japan, imo, in the future, the BoJ will have to set rates to deal with domestic wage inflation, as all the yen gone abroad has come back through buying Japanese exports (vendor financing) while at the same time that Japanese repatriation of assets causes yen appreciation externally.

So BoJ appears stuck. Yen strengthening/exports reduced competitiveness/ domestic inflation prevents easing.

Except !

The one way out would be to sell US treasuries externally for oil/commodities for domestic sale which would suppress (at least of stated figures) the domestic inflation.

They aren’t doing this yet because they don’t have domestic inflation yet. I think eventually yen weakness will turn to strength very quickly. Or maybe this is happening already, copper having quadrupled in dollars since 2003. Anywy my point is the only way to rid oneself of US treasuries is by purchasing commodities unless you want to finish your own export markets.

LordSunbeamTheThird,

I think you’re overstating the importance of having a weaker currency against the dollar.

The US no longer has the productive capacity to compete with Asian countries in many industrial sectors. They are at no real danger of losing market share to the USA. And it’s consumers – however drunk those sailors be – can’t really be relied up to spend much more than they are already.

Vying for LNG contracts in the region is rapidly reaching “Hunger Games”-like mania – better I think for those countries to have strong currencies.

Correct. Energy markets have been global for a long time, and the dollar is being increasingly bypassed. My only disagreement may be in our capacity to refine petroleum, but if that goes the way of manufacturing (as you point out), then we will see some serious increases in our dollar-based cost of living.

It’s actually $21,800 per worker, not $218,000.

Whoops…I now see the typo in the post I replied to. They meant $32.7T and not $3.27T. Divided by 150 million works. Yes $218k per worker for total debt.

I want to do my part…do you think they will accept a check? A post-dated one until after I win the Lottery….

The ONLY thing I would consider buying from the government/treasury these days would be 4 week T-bills. Close to 5.5% heading to 6.0% soon. Not keeping up with inflation, but better than parked in a savings account, and the short duration is great while waiting for other opportunities to present themselves. Mostly in the energy and commodities sector. So long as there are 8 billion or so mouths to feed, these things will be in demand…

Tend to disagree. If you can get 5.5% for a 12 month CD – I’d take it. I would not put all my money there – but that seems good.

I’d give pretty good odds that we are back to ZIRP within 12 months and remain there indefinitely.

Energy and commodities *seem* like safe sectors in inflationary times – but not always. For example, inflation can cause dysfunction that prevents producers from bringing product to market.

I am hedging with PGNAX among other things.

Looking at offerings via my broker, 6-month bills have the highest yield right now. Just bought some maturing 1/24/2024 @ 5.42%.

Why in the heck are you going through a broker and not treasury direct?

Yes, anything less that a year duration has a decent yield. I simply want to remain nimble, and for now the yield on the 4 week T-bill is increasing, I also believe the limits (for tax reasons) on the shorter duration are larger. At least that is how I read the law.

Not MM, but Treasury direct required me to get a bank medallion stamp to open account since my address on file did not match my actual address. After trying 6 banks, some I am a customer at and some not, and none willing to stamp the paperwork, I gave up. Beyond frustrating.

I have my ibonds at t direct (only option) but the hassle of funneling cash through a bank is a hassle.

Vanguard, fidelity and the other big guys offer Treasuries without fees, so super easy to move money in and out of equities, money market, bonds.

Vanguard federal money market (their sweep account) is offering a tad over 5% today – I’m struggling on just keeping money there or getting bit more with a t bond. I do think inflation is not stamped out and more rates increases coming, so maybe I let it sit there and lock in a long bond when the time is right. I’m part of the stampede at 5% long.

MW: 2- through 30-year Treasury yields jump after U.S. data batch, including job openings; 2-year rate rises bit above 4.9%, 10-year yield climbs to 4.04%

Who wants to follow a martyr?

This entire narrative is easily reduced to the cost of debt.

The Fed liberty street blog has an interesting post from 2017, bragging about the low cost of debt as a share of GDP.

That chart changed drastically since then. I’d post a link, but realize that’s contentious and even more so if you look at it in relation to inverted term curve dynamics.. The cost of financing for the Fed and Treasury is a bit like SVB with its maturity mismatching.

The cost of U.S. debt worries me.

Solving it is going to require both sides of the isle to agree to things they both think stink!

Where are Ronald and Tip when you need them?

As Wolf mentioned more than once, as long there enough REVENUE to cover the servicing that DEBT (ratio), this can go on, a lot longer.

Oh yeah! Sad…we aren’t more rational…

Where exactly is this $1 trillion going? Is this plugging a hole for some economic loss, or is this needed to pay higher rates on treasuries, and if not – if it’s supposed to grow GDP, then where exactly has it been spent in our economy?

“The American Republic will endure until the day Congress discovers that it can bribe the public with the public’s money.”

― Alexis de Tocqueville

Wolf,

Have you been tracking the 25 year Treasury zero coupon ETF (ZROZ)?

This is a PIMCO ETF and Bill Gross was talking about monitoring it closely. He said he always looks at this to get a sense of what long term treasuries are actually doing.

Since there is no coupon, and you can only get capital gains, it is the least subject to manipulation by outside entities. It is also less subject to options shenanigans.

It has been trending down for quite a while, and recently took another hit.

Do you have thoughts on whether this is a market indicator of the Treasury issuances later this year?

Or potential stress on liquidity for pre-existing bond issuances?

I imagine zero coupon long bonds will continue to trend down as rates trend up.

Definitely.

But they are likely a better forward indicator of where the market is going, without all of the options nonsense and external manipulation.

The point is getting a clear signal of what is actually happening and to strip out a lot of the noise.

Really hoping to get Wolf’s take on this…

Why it (ZROZ) is called Treasury ‘coupon’, since you later state there is NO coupon? Am I missing something?

I saved ZROZ into my bond watchlists. Wish I had known about it in January of 22. Thanks!

We know what Treasury issuance will be. They just announced it. They might still increase the amount in their update in three months. The market reacts to these announcements (today, for example). And then the market reacts to the reality of the issuance when it actually has to be absorbed. For me to be drawn into buying a 10-year T-note, yields will have to be a lot higher. So if a lot of supply comes on the market, demand dries up quickly at current yields, and to pull in more demand, yields must rise to where the demand is… so that’s the market.

ETFs reflect that. TLT (20-year+) was down 1.6% today. ZROZ (25-year) was down 2.5% today. But they track different kinds of bonds. Not a huge difference.

ZROZ would have been a primary short for me in Jan 22.

DM: These ten states are where homes are taking the longest to sell – as soaring mortgage rates pour cold water on the market

Hawaii is the state where it takes the longest time to sell your home, it has been revealed, with properties spending an average of 65 days on the market.

When rates were sinking to Titanic level…..let’s borrow short term with a duration of zip.

When rates are roaring higher……let’s borrow long term.

and these government folks have phd’s.

A side note…..Wolf ought to patent the phrase….debt out the wazoo…… hover between total disgust and panic…..with some laughter every time he posts it.

It’s just a matter of time before there is not enough interest on the bid and the long rates explode……just hope it’s after I’m dust.

A long time ago, a stock advisor of mine stated….if there is a difference of opinion between the stock market and the bond market….always go with what the bond market thinks……it’s where the heavy money is. Wonder if that still holds.

fred flintstone

Credit mkt (bond) is the foundation upon which Equity (stock) mkt is built. A shaky credit mkt is a harbinger of potential problems in the equity mkt

US GDP is growing only 2% per year in real terms (optimistically). Deficits are currently running $2T a year, or around 8% of GDP.

Doesn’t this mean we need 6% inflation every year, just to maintain a stable economy and debt/GDP ratio?

If we need 6% inflation to avoid making the debt problem worse, why is the inflation target only 2%? Perhaps 6% is the real inflation target that nobody likes to talk about.

Glad I’m not holding any treasury notes or bonds.

MW: 30-year Treasury yield ends at almost nine-month high

Look for 10 year Treasury yields to go to 5% and mortgage rates to 8%. Inflation is re-accelerating. There is nothing the Fed can do at this point. The Federal government is spending like drunken sailors on useless Wars and domestic Green Energy boondoggles. I just got my homeowners insurance declaration for the next year. It’s up 20%. Wolf needs to update his services inflation data and graphs to reflect reality, not fake government published data. Also, may I add, gas prices are up 20% here in the last month alone. ENJOY

This was a HECK of a day in the markets!

Long bonds wacked. Dollar continues upward. Hard commodities (metals and minerals) wacked! The Dow up again. Oil recovered to finish only about 0.3% down.

Tell me what the theme behind all of that is?

I guessed and bought a small basket of energy dividend payers that pay soon. I may look very smart, smart, dumb, or very dumb tomorrow but I bet the volitility will continue.

Well, you can’t get to HECK in a straight line, so critical thinking is usually the smart thing to do. May the volatility be with you.

posts like this always bring out the ‘end of the US as we know it’ comments. oh it’s just such a scary future. oh my. (sic) just don’t make investment decisions based on that nonsense. but if you insist, go ahead and be a sheep … the wolves will appreciate it.

What does it all mean? Cash is king. It is good to be King.

“Stunning numbers out today”

Where do you see stunning numbers? There’s nothing stunning about it. When it’s a debt based monetary system, the debt will continue to expand and increase.

On a side note, I’ve been following some of the above comments on CD options. Ive never invested in one, but a local guy told me I should move my savings from a bank and get 5 or so percent on a 6 month CD I believe. Of course the money remains tied up for that period further delaying goals. I’ve never owned a brokerage account or bought a T bill direct? Like to find some further help in what would be a wise choice or steps to consider.

I’m on an aggressive (aggressive considering my financial condition and circumstances) plan and am on track to keep saving up through first of 2024.