It shed 24% of the Treasury securities it had added during pandemic QE, footprint in ballooning Treasury market shrinks.

By Wolf Richter for WOLF STREET.

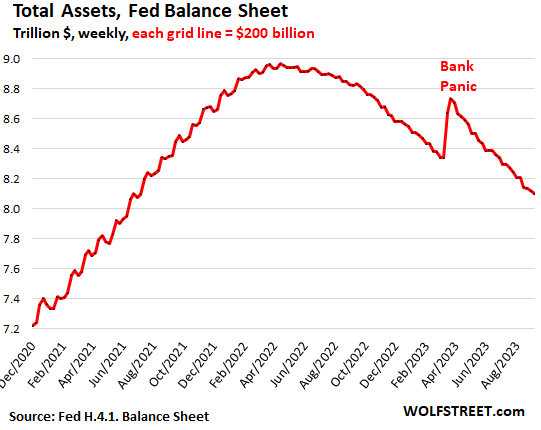

The Fed’s Quantitative Tightening (QT) and the liquidity unwind from the bank bailouts in March continued: Total assets dropped by $105 billion in August, and by $864 billion since peak-QE in April 2022, to $8.10 trillion, the lowest since July 2021, according to the Fed’s weekly balance sheet today.

At this pace, the Fed’s total assets will fall below $8 trillion in October.

Since the bank panic in March, the Fed has reduced its assets by $632 billion, as QT continued unperturbed on the same track as before the panic, and as the bank liquidity support measures got unwound.

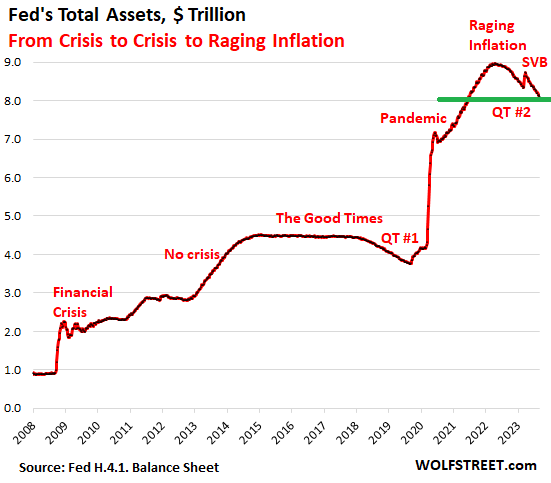

From crisis to crisis to raging inflation: Note the cute little QT #1 between November 2017 and August 2019, when total assets dropped by $688 billion. QT #2, which started ramping up in the summer of 2022, has already reached $864 billion, but the Fed’s pile has gotten a lot bigger and there’s a lot more to take off the pile.

And now inflation is way above the Fed’s target, while during QT #1, inflation was at or below the Fed’s target:

QT continues relentlessly.

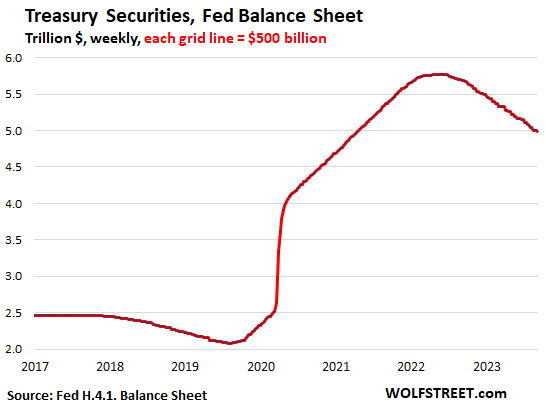

Treasury securities: -$59.5 billion in August, -$783 billion from peak in June 2022, to $4.99 trillion, the lowest since April 2021.

The Fed has shed 24% of the Treasury securities it bought during pandemic QE ($3.27 trillion).

Treasury notes and bonds “roll off” the balance sheet mid-month or at the end of the month when they mature and the Fed gets paid face value for them. The roll-off is capped at $60 billion per month, and about that much has been rolling off, minus the inflation protection the Fed earns on Treasury Inflation Protected Securities (TIPS) which is added to the principal of the TIPS.

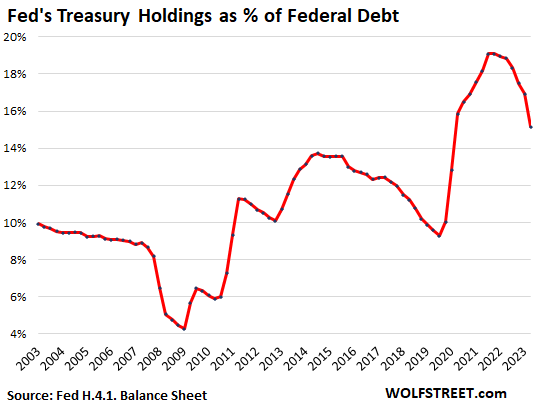

The Fed’s weight in the Treasury market dropped as its holdings of Treasury securities dropped to $4.99 trillion while the government’s debt ballooned to $32.9 trillion amid the tsunami of new issuance of Treasury securities to fund its deficit spending. This reduced the Fed’s holdings to 15.2% of total Treasury securities outstanding.

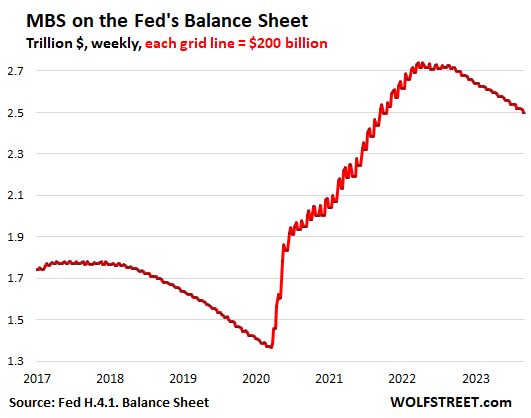

Mortgage-Backed Securities: -$19 billion in August, -$241 billion from the peak, to $2.50 trillion, the lowest since October 2021.

The Fed only holds government-backed “Agency MBS,” where taxpayers carry the credit risk. MBS come off the balance sheet primarily via pass-through principal payments that holders receive when mortgages are paid off (mortgaged homes are sold, mortgages are refinanced) and when mortgage payments are made.

The surge in mortgage rates has caused passthrough principal payments to slow to a trickle as fewer mortgages are getting paid off because home sales have plunged and refis have collapsed. So the MBS run-off has been between $15 billion and $21 billion a month, well below the $35-billion cap.

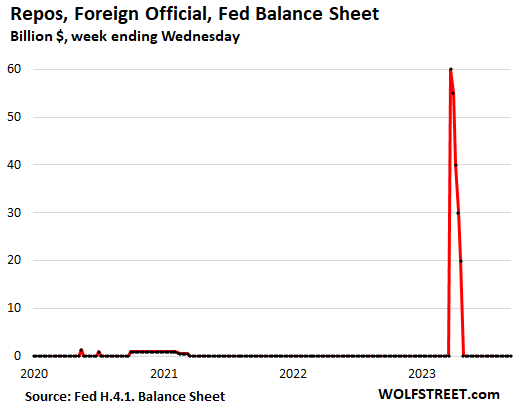

The bank-panic liquidity measures.

Repos with “foreign official” counterparties: $0, paid off in April. The Swiss National Bank likely used them to fund the dollar-liquidity support for the take-under of Credit Suisse by UBS.

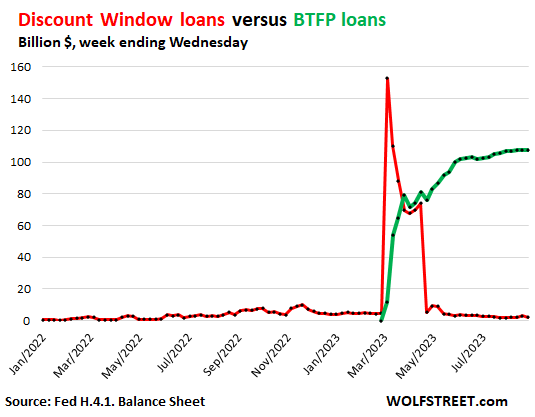

Discount Window: roughly unchanged in August, at $2.0 billion, compared to $153 billion in March (red line in the chart below).

Discount Window lending to banks has been around for a long time. This is not free money, it’s expensive money: since the last rate hike, the Fed charges banks 5.50%. In addition, banks have to post collateral under strict limits and at “fair market value.” So banks pay off these Discount Window loans as soon as they can.

Bank Term Funding Program (BTFP): +$2.2 billion in August, to $108 billion (green line).

A creature of the March bank panic, this facility is less punitive than the Discount Window. Banks can borrow for up to one year, at a fixed rate, pegged to the one-year overnight index swap rate plus 10 basis points. And the collateral can be valued at purchase price rather than at the lower market price.

This $108 billion borrowed by banks from the Fed is tiny compared to the $22.8 trillion in commercial bank assets held by the 4,100 commercial banks in the US.

Loans at the Discount Window in red, loans at the BTFP in green. Clearly, some loans were shifted from the punitive terms of the Discount Window to the less punitive terms of the BTFP.

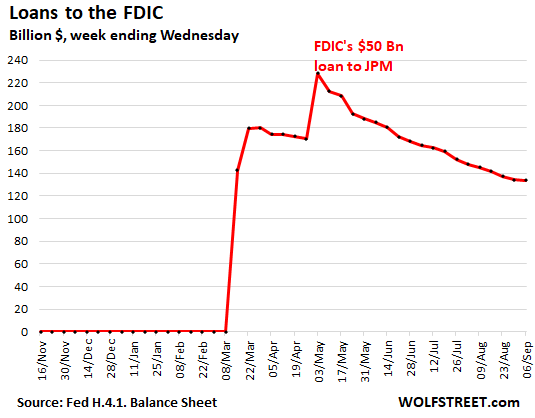

Loans to FDIC: -$14 billion in August, to $134 billion.

The FDIC has been selling the assets that it took on with the takedowns of Silicon Valley Bank, Signature Bank, and First Republic. It has started selling its MBS holdings to the market at a fairly steady clip. Two days ago, it announced that it would start selling a $33 billion CRE loan portfolio that it took on from Signature Bank. Nearly half of those CRE loans are backed by multifamily rent-stabilized or rent-controlled properties in New York. As the FDIC sends the asset-sales proceeds to the Fed, the loan balance declines.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The time to sell mbs was 20-22, they missed their window although arguably window is still open as it won’t have any effect on availability of mortgages until rates drop to 6.5 anyway, so sell sell Jerry

They own $2.5 Trillion of mortgage backed securities paying like 3%. Now rates are 7.5%. What would they get by selling … 70 cents on the dollar?

I’m paying off mortgage

origination was 8% in 1994

FHA ARM so come jan I’ll be over 4% – not going to happen

of course the balance is like under $5k

taking extra $1k month out of income

I don’t have anything to pay off. I have zero debt, and pay no interest to anybody.

Finally….. From snail’s pace to turtle pace. May be they will advance to sloath face next year (if they don’t stop). QE was at the Ferrari speed however. Buying 1.3T mortgage BS when housing market was on fire was the most stupid monetary policy ever.

Fed must start selling mortgage BS yesterday. And it will be very easy indeed. Because mortgage originations are crazy low, there is quite a large share of mortgage BS buyers. But it will hurt the pockets of the rich, so they wont do that.

Mortgage originations are low but so are mortgage retirements. So it is not clear that there is an unsated demand for MBS.

Even though most politicians, economists, and mainstream pundits won’t admit it, central banks exist to help governments finance themselves by stealthily transferring wealth away from the average person’s savings.

It’s the hidden, but real, reason why central banks exist.

Kramartini,

There will be demand at the right price, price discovery is important and it’s sad the fed is the asset inflation department instead of making sound economic decisions. In 2 years it’ll be too late & actually damaging to sell mbs, time is still now.

Couldn’t of said it better. QE on top of ZIRP to that extreme was a dumb policy in general, especially since there was already massive covid stimulus in the form of almost $11 trillion in fiscal pandemic stimulus, way more than any other country and way more than needed. Hence the US national debt at a far higher level than most other countries now (certainly far, far higher than any other country that has a credit rating one notch below AAA). But QE to that level with mass MBS purchases was criminally stupid. Now the US economy has practically become dependent on the heroin fix of ongoing mass deficit spending just to juice consumption, and keeping asset bubbles inflated.

JPow and the Fed at least saw the light on the dangers to the survival of the US economy and US dollar from ZIRP and inflation with the interest rate rises. But they’ve been way behind the curve in shedding those MBS’s, even the Bank of Canada has been more aggressive with QT, despite Canada having an even worse housing bubble and basically building its own economy on it now. They really need to step up on QT and more actively shed the MBS’s to even begin to partially undo that disastrous mistake.

It was not a dumb policy, it was intended to do so. And I guess everyone know what was the agenda.

They should never have bought a single MBS.

That’s the problem.

georgist, that’s absolutely the case. Buying mortgage BS was the biggest mistake FED made during the pandemic. They were buying mortgage BS when an average house was getting offers 50-60K over the asking price, buyers were writing emotional letters tasking the sellers to choose themselves and inflation was hitting the roof.

I don’t understand why the Fed can’t sell the mortgages to a bank… even for a loss. For example, I made the choice of buying a big SUV once, realized it was a mistake with all the gas, so I sold it at a loss for a smaller vehicle. Is there a law that the Fed can’t sell the mortgages for anything other than market value?

Tyler: they can’t sell it at a loss *and* keep rates low enough to keep housing high so that we are all forced to work for all of our lives.

That’s the key aim here.

Imagine if you had a factory where you employed 100 people and over time they got really good at their function, so that they were done by 2pm.

Would you just be happy with that or would you turn up the targets to make them do more so that you can get all their surplus value from 2pm to 5pm?

We’re in some kind of war. It’s labor vs capital or US vs China or something. It doesn’t matter really who vs who.

It’s an economic war.

To “win” we have to squeeze as much labor out of people as possible. But there are preconditions that have to be respected. We are “free”. Our system is worth fighting for because it “delivers better quality of life” etc. These appearances must hold or people will become demotivated and productivity will drop and we will “lose”.

Yes this sounds like a conspiracy, but really it’s just another way of describing nation state economic rivalry or a kind of class war, both of these have existed throughout history and are the norm, not the exception.

The “war” is such that the leaders are willing to risk breaching the entire conceptual hull in order to win. They are willing to fatally damage faith in capitalism with multiple bailouts, for example, rather than retaining a conceptually credible system that people buy into as a kind of pseudo-religion.

If we were not in a “war” situation viewed as an existential threat by those in power, why would we be doing this absurd parody of capitalism? Why the endless, breathless bailouts, the extreme levels of immigration that are very, very unpopular, the incredible suppression of building coupled with the ramping of asset prices far beyond wages? Why risk damaging finance and fiat fatally, when they are the systemic underpinning of our entire world?

The system wouldn’t be running this hot unless a greater threat loomed.

Absolutely agree, georgist. MBS, corporates, etcetera are outside the bounds of purely monetary assets, effectively an incursion into fiscal policy. The Fed should stick to general monetary assets like Treasuries and gold.

Why gold? Gold isn’t a monetary asset.

Was waiting anxiously for Wolf’s balance sheet update. 105 billion is actually quite respectable. It would be nice if it was 105 billion every month.

When they have reached a peak taking the Fed Funds Rate as high as they think they can go… THEN (and only then) you will see them accelerate the QT. The Fed learned an important lesson back in 2019 when they tried to be too aggressive with both QT and raising interest rates simultaneously. I don’t think you will see them repeat that mistake.

Rate hikes were in 2017 and QT began in earnest in 2018. While the fed is inept, that was no “mistake”, rather, on purpose.

Now, they’ve painted themselves into a corner. QT must continue, but at least rate hikes should be nearing an end.

Rate hikes weren’t JUST in 2017… they STARTED in 2017. The problem was that they kept increasing BOTH the FFR and the QT simultaneously. QT advanced on a schedule that was well telegraphed so everyone understood it… but the Fed Funds Rate increases were ad hoc… no one understood their purpose (inflation wasn’t looming) nor what was triggering them. THAT is what gummed up the works.

This time they are increasing the FFR while holding QT steady. I doubt that will change.

LOL

You are going to be disappointed……

Wolf,

Best case (or worst depending on how you look at it), what is the lowest limit to the Fed balance sheet taking the unwind to the bitter end?

This depends on the Fed’s liabilities. RRPs can go to $0. Reserves maybe as low as $1.5 trillion. Cash in circulation is now $2.4 trillion. TGA maybe $700 billion. So that’s about $4.6 trillion. So its assets would have to be $4.6 trillion also. That may be the lowest it can go.

Very helpful to know! Thank you, Wolf.

Great question!

Too little, too late. US fate is sealed. Inflationary debt spiral.

I thought that in 2008 when I was buying gold and silver. The economy just keeps chugging along though. I think a congressional mistake with failing to pass the next debt limit bill in time will be the final nail in the coffin- Even if the fed jumps in and prints money to loan the government (I didn’t think it was possible until they gave a loan to the fdic last spring). I’m prepared for debt-to-gdp to go to 200% before any “inflationary spiral”.

The economy has been chugging along on the surface only because of that inflationary debt spiral–the US government spending, deficits and national debt are far higher than peers and it’s a big reason Fitch yanked away the precious AAA rating last month. And the USA is basically the only major economy to be basically continuing on the covid stimulus even when we’re supposedly out of the pandemic emergency. An open question how much of it can continue if the stimulus is withdrawn.

And already signs of consumer weakness despite it–record US homelessness, plunging US life expectancy (we’re the worst in the developed world), plunging birth rates and massive increase recently in credit card and esp. auto loan delinquencies. The retailers are starting to warn and now Americans are tapping into retirement savings to pay for groceries–retail sales went up before because even unavoidable things like food and rent kept getting more expensive, but you can’ t keep squeezing blood out of a drained turnip, and now the cracks are showing. The problem is that so much of US GDP is based on things that actually impoverish Americans–healthcare and medical bills, rising rents and the housing bubble. It’s another reason why even a lot of the most staid econ professors recently have been saying nominal GDP has fatal flaws and shouldn’t be used as an indicator of how well a country is doing. A country’s economy is not healthy when it’s based on pushing up hospital bills and extracting more and more inflated rents and costs from already struggling Americans soon forced out on the street.

Facts without context are irrelevant. Life expectancy is due to opioid epidemic. Homelessness, lack of healthcare (specifically mental healthcare) and cost of living per the actual pay people can expect. Just about every store has an option to tip now to subsidize the fact that people are not paid a livable wage while companies make record profits in a time of inflation.

Honestly you are right, the cracks are showing, and widening. As long as politicians prioritize their corporate donors needs, the majority of the population will have what little subsidies and wealth they get shaved away. Not to mention what’s left of the environment. But thank god the companies are making those profits, trickle down at its best. Meanwhile, lets not focus on issues and talk about trans-rights, partisanship, and trump some more. Both parties have the majority of the country dancing to their tune and thanking them as they rob us.

Miller,

Your second paragraph contains a lot of BS. So let me just shoot it down manually.

As “signs of consumer weakness” you list:

“record US homelessness”: not a consumer weakness but a vast complex problem having to do with addiction, mental illnesses, lack of care, etc.

“plunging US life expectancy” — a disease did that, and not consumer weakness

“plunging birth rates” LOL, that’s a choice people make in an overcrowded world; the richest countries have the lowest birth rates.

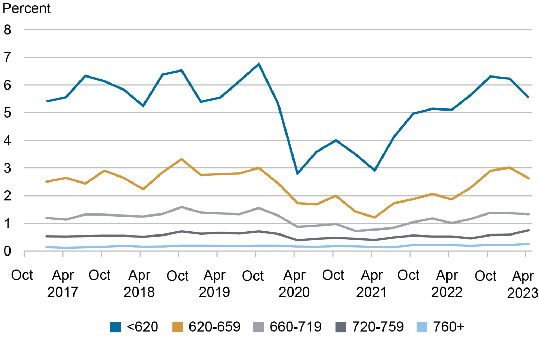

“massive increase recently in credit card and esp. auto loan delinquencies.” OK, here we go, credit card delinquencies by credit score, New York Fed:

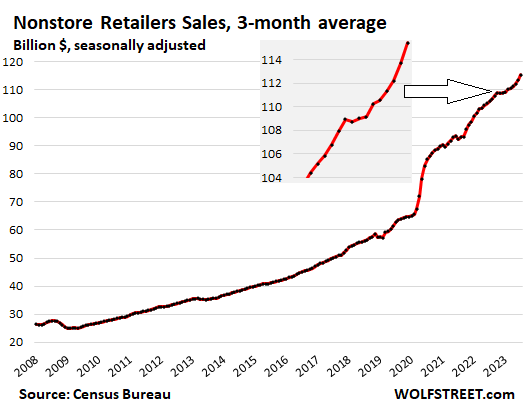

“The retailers are starting to warn…”: some sick brick-and-mortar retailers warned, because they’re in the brick-and-mortar meltdown that I have been talking about here since 2016. But auto sales are up bigly, and Walmart didn’t warn and Amazon didn’t warn and ecommerce is red hot:

“Americans are tapping into retirement savings to pay for…”– BS retirement savings are growing in leaps and bounds. IRA balances jumped by 4.3% from quarter to quarter in Q1; 401k plan balances jumped by 5.0% quarter-to-quarter (22% annualized, LOL).

“now the cracks are showing”: the cracks in your head? Sorry, couldn’t pass that one up.

I gotta go, wife is calling, dinner is ready, don’t have time to shoot down the rest. But you get the idea: You need to quit reading the BS you’re picking up somewhere.

Wolf,

I agree with your charts and analyses and have seen those but this time it seems to be a matter of conflicting signals. Yes there has been resilient consumer spending but also indications of consumer stress, both can co-exist at the same time. Macys, Foot Locker and other retailers have been warning of softening spending and consumers maxing out on store and other credit cards, and delinquencies have been reported at levels higher than pre-pandemic. And auto loans especially are also showing delinquencies and a lot higher trouble paying them off. Things like sharply increasing homelessness and dipping into retirement savings (Fortune had a long article on this) also clear as day signals that Americans can’t sustain these price increases much more esp on things like rent and are literally winding up on the street. All of these are also well documented figures so there are signs of both things, resilient consumer spending and softening and weakness as consumer budgets are stressed. But that said I totally agree with your overall points here, there’s still too much stimulus and excess savings from prior overstimulation of the economy and it’ll continue to drive inflation, and the Fed is right to keep it’s eye on the ball and continue with monetary tightening until that’s brought into check.

@ LateStageGlobalism

Boy, it sure looks like a debt spiral.

What is crazy is the USD is strong and maybe getting stronger. It appears the US is not the only country in a debt spiral.

I have some rental properties. Each of the last 3 years I keep thinking I should sell but then I look at the CBO new Government debt projections and that convinces me not to sell. They are a hedge against the coming debt spiral inflation and asset price inflation that comes with a debt spiral. LOL

A relatives Retirement home has raised her rent each of the past 3 years. $200 a pop. It has risen from $2300 to $2900 now. That is 26%. Her SSN has only risen from $1650 to $1900 during this time (15%). It is starting to bite big time and eating up her savings. She most likely will need to move into a government subsidized retirement home soon.

$USD = “Purest girl in the whorehouse”.

It’s been fluctuating way up and down recently, being fair JPow has been quite aggressive in raising interest rates and he’s done the steepest increase of anyone since Volcker. And he has made absolutely clear that the pivot-mongers are idiots, and that the Fed will continue to fight inflation aggressively and continue raising rates and QT (even if the QT part hasn’t been nearly enough). But the USD has objectively lost value by the very fact of ongoing inflation itself–it’s losing its buying power in a terrible way, and that’s not just relative to some other currencies but more importantly, relative to commodities (not just precious metals), real goods and services and other places to put investments and savings.

As dumb as the whole cryptocurrency and NFT mess are, the whole reason these financial “instruments” took off to begin with was loss of faith in the US dollar to hold its buying power. That doesn’t make them any smarter, but it shows that the people in charge of maintaining the USD’s buying power failed miserable in recent years to do their job, that a bunch of “currencies” conjured out of thin air and block-chain bits could be worth so much in actual dollars. At the very least the Fed has gotten religion on this recently to a point, but they need to read up on Paul Volcker’s prophecies and follow his wisdom if they want to avoid disaster. Above all by getting much more aggressive with QT and esp undoing the MBS mistake.

Whatever the Fed is doing or not doing with the balance sheet doesn’t seem to be working. Inflation is still out of control.

The solution? Education. It’ our only hope.

All the highly educated people at the Fed with their fancy degrees and they still can’t figure out how to fix this inflation mess. Doesn’t seem like “education” is the solution here.

“We must unlearn what we know about M2” J Powell, February 2021 ….

just before the inflation spike and just after a massive increase in M2.

…’n if you reflect on the presentations of our mass entertainment, a lotta ‘Muricans hate to go to school. Given the base architecture hasn’t really been addressed since the ‘thirties (providing a solid base of factory workers while assuming the female spouse will remain at home providing critical parenting duties), there may be little wonder at that. Learning from life, books, and mentors are not discrete propositions, but improved methods of generating a bit more of the autodidactic in using and integrating all of them could greatly ease our path…

may we all find a better day.

The genie is out of the bottle.

Producers keep charging more, and consumers keep happily paying more, with vengeful aggressiveness might I add.

Instead of going on buyer’s strike, refusing to pay obscene prices, consumers are just demanding more cash from their employers (and getting it!)

brilliant synopsis of what is “really going on today.” We’ll hit a pay-rate ceiling in early October and the fat lady will over and she’s gonna be singing too (loudly but endo of q1 ’24).

I’ve never seen a labor market with employers so afraid of layoffs at scale. The COVID labor shortage really made a lasting impression on the mentality, with employers now hoarding talent like their companies depended on it.

Something tells me that is beginning to change though. We shall see.

Hoarding talent, hoarding houses, hoarding physical items which creates a self-fulfilling prophecy for inflation.

Get a feeling that a lot of this behavior isn’t inflation (obviously *some* of it is), but much of this is just twilight zone economy fakeness?

NVmark,

Tech companies, ex-Biotech, around Boston stopped hoarding talent at the end of 2021. Most of the Biotech companies halted the practice in H2 of 2022.

The only large-ish, tech-ish company that is aggressively-hiring around Boston is DraftKings who – at the moment – are more or less fishing with dynamite courtesy of the nature of their business.

But under cover of darkness there is a steady net bleed out of jobs in the tech sector and – as far as I can tell – this is being driven as much by secular concerns (offshoring) as cyclical ones.

Buying stuff is like stealing.

I’m giving them $$ that I *know* will be worth far less soon and they’re giving me a physical good?

You sure you want to do this corporation x?

Carlos,

Right now there’s been little net demand destruction, but there definitely has been a shift in consumer staples from higher-priced brands to lower-priced brands. You only have to look at KHC stock to see that.

Some big-ticket leisure stuff – e.g. trips to theme parks like Disney – have also gone soft. And some of the pandemic-induced sector frenzies – e.g. home improvement – have gone quite cold.

But – overall? There’s not been any significant net demand destruction yet.

I would disagree with your assertion that consumers are getting big wins in wage adjustments. Unionized-areas might be an exception but A LOT of employers in non-unionized sectors are adapting and accepting a shortage of employees and beginning to reduce hiring needs. Health insurance companies are a good example here.

Kraft and Nestle all make overpriced crap too. Nestle used to make a great coffee creamer called Natural Bliss and the ingredients in the vanilla flavor were just milk, cream, sugar, and vanilla. It was more expensive than the regular soybean oil based Coffeemate but it was delicious and the ingredients all made sense. It seemed popular enough. Well about a year ago, those idiots at Nestle decided to change the formula to “improve the taste.” Their way of improving the taste (that was the reason they gave for this change) was to change the name to “Real Milk and Cream” and change the ingredients to Milk, Cream, Sugar, Buttermilk, Soybean Oil, Natural Flavor, Gellan Gum. It tastes like crap now, and the reviews of the new formula are hilariously bad.

Because of this, I discovered that Aldi makes a natural creamer with only 4 ingredients, and it comes in an even bigger bottle at a lower price. While I’m there I get to stock up on a ton of other affordable staples. I would have been perfectly happy buying the Nestle product but they go out of their way to be hostile to their customers. Big business is bad business.

Lucca – We are heading into another big election year. There will be lots of spending promises by all future candidates. It will be interesting what type of campaign promises will be made this year. Inflation is going to be a topic.

—————————————-

Annual construction investment growth has been running at 6.2% since the IRA was signed into law. But if we remove the additional manufacturing construction growth the IRA subsidized, this falls to 3.2%.

More striking, in 2023’s second quarter total construction investment growth was running at 3.1% with the additional subsidies — but without the subsidies it was contracting by 1.5%.

Using these numbers, we can model the employment growth of construction workers.

With the subsidies, construction employment is growing at around 2.6% per year in the second quarter of 2023 — without the subsidies we see a fall of just under 1%.

How is inflation out of control? It is in the 4-6% range down from 9-10% range earlier.

Sure, it isn’t at 2% yet, but that doesn’t mean it is out of control.

If you had to bet, which do you think will happen first: inflation hitting 10% or inflation hitting 3%? (I am talking real economy wide inflation, not some cherry picked inflation that the nuts usually come up with).

I am guessing that neither happens anytime soon, but that 3% eventually happens before 10%. How is that out of control?

What is the fed’s logic for a cap on MBS runoff? I dont see how theyd exceed it, but in event that they do, they would buy more to make up the difference? For what purpose? Burn those off as fast as possible and if God sends some windfall their way in that regards, take it.

The Fed would love to speed it up but it doesn’t want to cause turmoil in the MBS markets. As to what they would do if the MBS rolled off faster than the plan… in the pre-COVID past they just bought a few more to balance it all out and called them “Reinvestment Purchases.” But then they switched gears and just bought extra Treasuries instead.

Ah we can’t have the precious housing market upset, can we?

That’s the real lever.

High house prices means you’re forced to work forever.

Keep them high or we lose the economic war against Eurasia.

What they did last time after QT had ended in mid-2019 was let the MBS roll off and replace the amounts with Treasury securities. So its MBS kept rolling off until March 2020, while Treasuries increased. But they announced that they would do this.

What was the Fed’s logic to delve into the long end….when for decades they did not?

From zero to $2.5 Trillion is quite a policy decision….and now they are jumping into their own “orifice”….as they must raise rates and at the same time create over a Trillion in unrealized losses in their portfolio.

The Fed has no business in the long end just for this reason alone.

Unemployment and Stable Prices, the heralded “dual mandate” are both current and real time issues.

I have to agree with Lucca. Wolf. Too much of this seems to be ‘theoretical’. Sure you have your charts and it’s math. You can’t argue with math, supposedly. But quantitative tightening… so what? What is it doing *noticeably* in the economy? What impact does this have for us small people? I’m not seeing a damn thing change.

Asset prices are coming down. Stocks are coming down. Stocks were being inflated by QE and 0% starting in 2009. Now all that has reversed. But yes, if you don’t own assets, you might not feel QT. But you would feel its absence through even higher inflation.

I own plenty of assets, more than the average person, and I still don’t feel QT.

> it’s really bad but it would be even worse

Most regular people have completely lost all confidence in fiat money.

That’s why they’re spending like they are.

Want a new mobile phone? Yes they’re all $100 more now, but if I hold my joke $$ instead of spending them I’ll be even worse off.

That’s the mentality behind the spending. That mentality was curated by central banks over two decades. It will not be reversed easily.

“Most people have completely lost all confidence in fiat money”. Is the biggest untrue statement ever made.

In the real world, most people gladly take payment in fiat money and hold it in their wallets, bank accounts, PayPal, and Venmo accounts.

If they had completely lost all confidence in a money they wouldn’t accept it as payment.

I have zero confidence on bitcoin. I don’t accept it as payment for my services.

“Now all that has reversed.”

Except for the asset prices, themselves.

BigAl:

Exactly. That’s why I said in an earlier comment that nothing the Fed is doing seems to be working. They keep doing the same thing, hoping for a different outcome.

Definitely not in any meaningful way. At the rate they’re going it will take a decade.

Definitely not in any meaningful way. At the rate they’re going it will take a decade or more.

Big Al and Lucca,

Are you blind? You’re spreading BS on my site.

Asset prices reversed just fine. S&P 500 is down 7% from its peak on Jan 3, 2022, and the Nasdaq is down 15% from its peak in Nov 2021. Cryptos have collapsed by 60%. Longer-term bonds and bond funds are way down. The national median home prices is down from the peak in June 2022. Etc. Look at the three-year charts!!!

Lucca, Do the math. QT = $860 billion over the past year. At this rate, the balance sheet will be down by $4.3 trillion in 2027, which is about as far as the Fed can possibly go based on its liabilities, which I discussed here.

I agree. 8% inflation summer 2022 to 3% September 2023 is a big difference. I’d love to see if QT and raising rates were broke down in a chart to see how each reduced price inflation.

A lot of that was due to falling energy prices and the healthcare adjustment, not QT. Inflation is about to re-accelerate.

Hopefully, ongoing QT will keep treasury yields high.

The Magnificent Seven stocks combined market cap is 11 Trillion dollars. Sitting in everyone’s 401K. Soon to be 201K.

You got that Right – A 50 % Market Decline from Here

It’s hard to panic people on the notion of a 50% Market Decline when everybody just assumes that the inevitable Fed Pivot that would follow such a decline would result in a rapid reflation trade yielding 300% Market Gain.

Right now most everybody is front-running a Fed Pivot on a FOMO basis.

Me?

a) I’ve no doubt that the FED is willing to bring about a recession to get inflation under control once and for all.

b) I’ve got considerable doubt that a recession CAN get inflation under control once and for all.

c) I’ve no doubt that the FED will pivot if the credit markets implode

d) I’ve no doubt that the FED can be brought to heal by the US State Dept (aka “the Blob”).

Where “d” would mean – for example – an avoidance of raising interest rates in the USA so as to not antagonize Japan which an alliance partner against Russia & China.

Hi Wolf.

Would have a view on Global Liquidity over the next 3-6 month period?

Thanks

Still awash in it, but getting drained.

Thanks wolf,

I think of the cap for mbs at 35 billion way off their mark raising interest rates with their plan. I guess unintended consequences?

Comprehensive article.

For me the inflation, the continuous devaluation of labor and the constant pattern of using credit to buy housing is because no matter how much QT the Fed does, no matter how many MBS they let roll off, when the next downturn comes, we KNOW they’ll do it all again.

We’ve already had infinite deposit insurance, a full bailout of UST at par, what next? I’m not sure, but I am sure $$ won’t act as a store of value.

georgist,

” using credit to buy housing”

Whatever credit is being used, or at least *whenever* credit is being used…it is increasingly *not* from a mortgage. At least not if Metro Boston is any guide.

Housing supply in Metro Boston is incredibly-tight right now and it’s generally institutional buyers who are making the actual purchases using cash purchases – NOT mortgages. That cash almost certainly DOES come from a credit source but that’s a different story.

My comment refers to a now well trodden two decade pattern of behaviour.

It does not refer to recent “blips” that have in the past been completely erased (and then some).

Wolf, do you know the reasoning of how/why the number of $60B was chosen as the cap?

The Fed discussed this when they announced the plan. Some wanted higher caps, some wanted lower caps, and so this was the compromise. The cap is double what it was for QT #1. That reason was also cited.

I am curious about what the treasury run off would be without the $60 billion cap…

Some months it’s under the $60 billion, in which case the Fed fills in the rest by not replacing maturing T-Bill. Some months it’s over $60 billion. You can look this up on the Fed’s maturity schedule that tells you the maturity dates of various issues.

Click on the “T-Notes and T-bonds” tab” for maturity dates of the Fed’s 2-year to 30-year holdings. You can also download the Excel with all SOMA holdings and dates

https://www.newyorkfed.org/markets/soma-holdings

For example:

In September, $39.4 billion in Notes and Bonds will mature. The remaining $21 billion will be filled in with letting T-bills run off.

In October, $46.3 billion in Notes and Bonds will mature. The remaining $13.7 billion will be filled in with letting T-bills run off.

In November, $64.2 billion in Notes and Bonds will mature. The Fed will buy $4.2 billion to keep the total run-off at the cap of $60 billion.

Would the fed have to buy more than the previously rolled off notes and bonds in order to replenished the 4.2 billion in has to make up, since the notes and bonds have gone down in price ? If so, doesn’t that cause problems with reducing the balance sheet in the long run since it would be counterproductive to the goal at hand.

Would the Fed buy the same note and bond with the same maturity ? Or can the Fed buy a a four week treasury bill, so that roll off would be more aligned with monthly roll off ?

Your # 1. The Fed buys replacements at auction, and you can see its purchases when the auction results are published. So it buys like everyone else at the auction price (close to face value).

Your # 2. The Fed can buy whatever Treasuries it wants, but under the current plan, it said it will replace apples with apples, so if it needs to replace $5 billion in 10-year notes that matured, it will buy $5 billion in 10-year notes. At some point, it could switch to buying T-bills, which it did last time toward the end of QT.

From the worst its down about 850 billion according to the chart….in about a year and a half…..so about 50 billion a month.

The real question is how long til the next emergency when they decide they must stop and start providing support.

Yes, the 105 billion rate is respectable…..but how long will they the actually do it.

For example……Once the real estate mess manifests itself in the market…..will the fed hold to its policy…….we all know the answer to this question.

It’s an old story…..if you deficit spend to invest in yourself the deficit should not matter…….if you deficit spend to eat chocolate sundaes and pad over reckless policies……the deficits may cause a heart attack.

@fred flintstone,

It isn’t immediately clear what the actual “real estate mess” is…

a) I see no prospect of a meaningful correction in housing prices in the near-/mid-term. This is bad for buyers but a huge relief for cities & towns that are more dependent than ever before on receipts from real estate taxes to remain solvent. Thus, we avoid a municipal bond catastrophe.

b) I suspect that a commercial real estate deflation is coming – but it might be deferred for a long time and might take place at a slow-enough pace so as to avoid a real crisis. If Metro Boston is any judge, WFH is largely played-out and has reversed. OTOH, a secular trend of near-total offshoring of Tech jobs in various sectors is just starting to occur.

> The real question is how long til the next emergency when they decide they must stop and start providing support.

This is the nub of the problem. They are like an alcoholic who “quits” every weekday. “The Fed put” has been an absolute disaster and the only way to fix this is to wait for a recession, and then do *nothing*.

At this point the penny would drop that the Fed put is dead. Then things would drop again, more.

So in effect to kill inflation they need to have a worse recession than anything pre-Fed put to break the spell. At a time when there is zero tolerance for even a slight dip.

All this kind of psychology is covered in the most basic parenting books around discipline, and you don’t even need to read a book, it’s just common sense.

People do not believe they won’t do more QE, which means they have lost faith in fiat as even a short-term store of value.

That is very, very dangerous.

LOL… shockingly enough, most policy makers think it is their job to try to PREVENT a “worse recession” than the Great Recession of 2007-2009.

As to people not believing that the Fed won’t do more QE… give them time. Until 60 days ago even most commenters on WolfStreet thought a “pivot” was inevitable (no matter how many times Wolf told them otherwise)… to say nothing of Wall Street. Those voices are quietly starting to fade away as the “new normal” of QT keeps making idiots out of them month after month.

The bottom line is that Quantitative Tightening has been the Fed’s preferred policy direction ever since 2016 when they first announced it. They implemented it in 2017 and had to pull in the reins in 2019 when the markets started to seize up. Absent a global pandemic there is little doubt that they would have resumed QT in 2020 instead of 2022.

The Fed’s sporadic behavior reminds me of the wife-beater in white T-Shirt. He violently explodes every now and then, but then all seems better after he cries and says “I’m sorry”. There is no real conviction or need for change. The pattern works for him.

The Fed just monetized $5T, caused a 20% inflationary price step-up, and is now saying “I’m sorry”. Everything seems great, for now.

> and *had* to pull in the reins in 2019 when the markets started to seize up.

The regular guy in the street has never heard of QT. They only work on what they see. They see the $$ purchasing power going down by a noticeable amount every 12 months. So they stop holding $$ if they can exchange it for real goods.

That’s also what we see, not what the Fed say we ought to see.

That is not the only way to fix it.

That is what you are hoping will happen. There is a difference.

You premise assumes an emergency is going to happen (such as in real estate).

What if real estate continues to ever so slightly decline while wage inflation continues on a overheated pace?

Eventually wages will catch up to real estate prices and there will be no emergency requiring more QE.

This is called a soft landing.

While GDP (apparently ) explodes, servicing debt unfolds as an epic cash burn crisis, but nothing to see here, everything’s fine. Blah, blah …

Market Value of Marketable Treasury Debt (MVMTD027MNFRBDAL)

What’s your problem? Bad hair day? Just woke up and realize that Treasury prices have been down for the second year because yields rose? This has been a HUGE topic on this site for two years, and you missed it, LOL. Do you ever read anything here???

Here is the chart you pointed out (MVMTD027MNFRBDAL at the St. Louis Fed data collection), showing the market value of US Treasury securities that are publicly traded:

Perhaps the pandemic opened Pandora’s Box, or at least allowed the camel’s nose inside the tent, allowing moral hazard to be acceptable — to a point where, deficits don’t matter — is a foundational stepping stone, where greater moral hazard will be a catalyst for modern government.

Pandemic shock produced resilience and hardened society, as if we all experienced a new horror, helping us to see that we’ve seen the extreme edge of risk. In that context, it’s been clear that BTFD, FOMO, YOLO are the battle cries of post pandemic exuberance, which fully embraces a lack of fear about economic absurdity.

Although the Fed is slowly going about QT, after being so slow to stop QE, that act of caution and hesitation points to the reality that moral hazard, in fiscal and monetary policy, will be with us a very long time, and most likely, a normal state of decay.

The camel of moral hazard stuck its nose inside the tent for the first time in 1998, with the bailout of Long Term Capital Management. In 2008, it pushed the flap aside and took up full time residence inside the tent, where it has remained ever since.

No one has done more than pretend to eject the camel since then. It gains weight every year, and its temperament gets nastier, making it ever more difficult to remove.

Thank you for your factual, clear reporting, Wolf! Your work is so needed a world of opinions and predictions on this and similar topics.

Every time I see that Fed Total asset chart and the section that says “no crisis” and increasing asset purchases I laugh out loud. So true.

Well…..this is the reason I tune in to this site……difference of opinion makes one stronger not weaker. A strong main guide so we don’t go too far off path to fantasy. Enjoy it all and hopefully it all works out so we don’t end up eating cat food. Even my cats will not touch purina…..LOL.

Howdy Folks. Boy did I mess up with only getting a high school education. Getting an education might have allowed me to understand some of this nonsense. 8.1 trillion piled up somewhere, on someones books, letting it go back and forth somewhere else and then a person gets paid and prize. That s OK though, my head is spinning from vertigo anyway. Doans pills will help my back pain, and a high school diploma is good enough for me…..The world is a crazy place and I love being alive…….

If you have a high school diploma, and know how to operate a forklift, you get paid higher than the 1,000s of Bachelor’s degree and MBA graduates in Toronto applying for C$16/hr ‘administrative assistant/ bookkeeper’ jobs.

Don’t feel bad. At least you didn’t take student loan debt to become a strand of hay in a haystack of resumes in Canada.

The best financial education that I learned regarding inflation was from Dr. Milton Friedman. His documentary “Freedom to Choose” is on YouTube.

He explains the mess caused by “printing money”, and predicted the pandemic bonanza in a way. His documentary explains how Japan dealt with inflation in the early 1970s. Oddly, Japan went through decades of deflationary growth later on.

On a side note. I took a vacation recently. It was on Southwest.

The prior 2 years, I would say on by 10 to 12 flights, every flight on Southwest was 95% of the seats were occupied or totally full.

This time, on 3 of the 4 of the flights, they had 80 to 90 seats open which meant they were only about 2/3 full. Nobody really had to sit in the middle seat.

1 of the 4 flights was a full flight.

IF you look at Southwest Stock, it dropped like a rock during covid and then recovered. But the stock is back down to Covid lows. They are getting pinched buy rising labor costs and some big operational issues. But the airlines have said travel has been slowing down recently.

Does the slowdown in air travel forebode a drop in Hotel earnings and AIRBNB earnings or maybe people are driving more?

I don’t know about a slowdown in air travel. Delta announced record profits.

couple of points:

1. MBS is way below their target. I know the reasons. But it distorted housing market crazily and now average person needs to read Fed tea leaves to buy a home. Is it supposed to be this way. I know media pundits don’t care.

2. I read Fed is actually increasing their long treasuries. I.e. when they recycle matured treasuries they are buying long treasuries more. for some reason median pundits hide this. Maybe because this benefits 1% asset bubbles.

3. Lowest since July 2021 is comical. Any comparison needs to be based on 2008. How did we even survive before 2008 without QE?

Your #2 is BS for two reasons.

One, the Fed is hardly replacing any securities at all because the run-off in many months is now below the $60 billion cap, including in October and November. Everything that matures runs off and nothing is replaced in October and November. The Fed will also let T-bills run off to get to the $60 billion cap. In December, $64 billion mature, and the Fed will replace only the $4 billion over the cap. See my table of maturities in my comment above. This is now typical – replacing $4 billion in three months, minuscule, and this will go down further as more notes and bonds come off, and soon maturities will be below the cap every month and nothing at all will be replaced. What kind of moron bloggers are you reading?

Two, if they replace anything, in the few months where they do, they’re replacing a few maturing 10-year notes with new 10-year notes. Or they’re replacing a few maturing five-year notes with five-year notes, etc. Everyone who wants to maintain a bond portfolio is doing that.

Your #3 is BS because only morons that don’t understand the liabilities on a balance sheet think that the Fed can go back to 2008 assets. I have explained this a gazillion times here, including in this thread.

Do you ever read anything here, or are you just a troll, dragging in BS from some moron bloggers out there?

Gen Z wrote:

> If you have a high school diploma, and know how to operate

> a forklift, you get paid higher than the 1,000s of Bachelor’s

> degree and MBA graduates in Toronto applying for C$16/hr

> ‘administrative assistant/ bookkeeper’ jobs.

The California minimum wage goes to $16/hour at the first of the year, and the starting pay at the Truckee, CA McDonalds is $19/hour. I can’t get anyone that knows how to do even basic handyman work (I don’t even care if they are high school grads) for under $60/hour and I’m paying actual High School kids $25/hour to do basic work like sweeping, dusting and power washing).

Wow that ain’t no recession.

High school kids making double that of middle-aged Canadians and newcomers with advanced degrees.

Toronto and Los Angeles rent and real estate are similar too.

Dude, not to butt in, but it sounds like you need to leave Canada. JFC!!

Nah, Gen Z is just another whiny troll, just like in 2008. Same complaints, same blaming others, deflecting, but at the same time, dispensing his vast wisdom from someone who can’t get a $16 CAD job, while supposedly having a STEM degree and maybe even an MBA. Basically, an auto reject resume from HR. Nothing has changed in 15 years.

Kind of sad, but humorous sense of entitlement. Thought it was only in the USA, but same disease in our neighbors to the north.

Do we think that the FED will continue

to raise rate in the upcoming election

year ? They should, but will they ?

Re the question of why the FED practiced QE on MBS, this was baffling to me as well so I asked a friend who is a fixed income portfolio manager at a large firm. Like it or not, he said that the FED was afraid that QE in the Treasury market alone would create distortions in the relative prices of various FI securities. They felt they had to QE MBS. The alternative was thought to be worse.

Fed’s bond trading strategy: buy high sell low. Won’t the US gov need to recapitalize it eventually with more borrowed money?

Close. Fed’s bond strategy: Buy high to push prices even higher, sell never, hold to maturity.

… realized after commenting that, as noted here and elsewhere long before: the fed wont need to be recapitalized thanks to peculiar fed accounting practice.

But are they not selling any of their bond holdings, is it really all just roll-off? I’m pretty sure that as early as spring there were articles about notional losses incurred by the fed on their treasury holdings. I suppose if they do hold everything to maturity than this isn’t an issue (mark to market account aside). But are they really able to meet the QT targets without selling any of their bond holdings?

The Fed did sell their corporate bonds and bond ETFs that they bought in April through September 2020. They sold them in 2021 and made a profit on them.

The Fed creates money and therefore can never run out of money. So it doesn’t matter to the Fed how much it loses, but it matters to the taxpayer because the Fed remits nearly 100% of its profits to the US Treasury, and if there are no profits, the Fed won’t remit anything.

Hm, just saw one of your responses to an earlier comment above explaining that when bond maturity does not cover the QT quota then the fed makes up for it by letting T-bills viz. short-term gov debt roll off without renewal. If so, then I suppose they can avoid selling any bonds at a loss. But that is a “hybrid QT” comprised of a balance of short and long term debt rolloffs, which ought to have different impact on the market (or impact on different markets) depending on the proportions of one vs the other.

Judy Shelton was on one of the Financial news shows the other day. She said the Feds increase in interest rates is having zero effect in taming inflation. In fact, it is actually adding to the burden of small and medium size businesses while actually increasing the cost of doing business who’s costs are ultimately passed on to consumers. Big businesses can absorb the increased interest rates. Without a dramatic decrease in government spending and deficits, whatever the Fed is doing is destined to fail. Judy Shelton should have been appointed to head the Fed. Another missed oppurtunity.

Yes I think we are finding out that deficits (and subsequent debt growth) do matter. And to reduce deficits the government can either raise taxes, invoke an austerity plan, or both. Raising taxes will not go over well with the real taxpayers and austerity will not go over well with the government program takers. Doing both will make everyone upset so that is why nothing gets done.

Swamp Creature,

Judy Shelton is right about government spending, but dead wrong about the other stuff, and if she is really this clueless about the other stuff, it’s scary.

For example, she doesn’t even understand that businesses cannot raise their prices unless consumers are willing and able to pay those higher prices – the “inflationary mindset” when consumers are willing and often eager to pay whatever, as we’ve seen for used cars, for example. Inflation is primarily driven by demand and the willingness and ability to pay those higher prices.

Costs determine profit margins. The low-cost producer thrives, and the high-cost producers struggles and goes out of business. If the high-cost producer tries to raise prices to match their costs, competition will eat their revenues alive, and they die. There are very few exceptions to this, which are companies with incredible brand value, such as Apple.

Businesses will always charge the highest prices they can get away with while still achieving their sales growth goals. If their costs go down, they just make bigger profit margins.

So the question is: how do you reduce the ability and willingness among consumers to pay those higher prices. Because that’s what puts an end to inflation.

– CPI is called Consumer Price Inflation for a reason: inflation measured at the consumer level.

– Consumer spending is about 67% of the economy. The rest is business and government.

Higher interest rates are supposed to reduce demand by consumers in three ways:

If consumers spend less, businesses fear for their revenues, and if they raise their prices, consumers will abandon them and buy elsewhere, and so price increases don’t stick. And that’s how you can bring inflation back under control. It’s a painful process. Inflation doesn’t go away on its own.

Shelton was right in that government deficit spending is stimulative of the economy and inflation. But that’s only part of the inflation story, the much bigger part is consumer spending, given how much bigger consumer spending is than government spending, and for her to be so clueless and not see that is just scary. She should not be anywhere near a central bank. She should be working in the marketing department of a real estate firm.

But Shelton tells him what he wants to hear. That is all that matters.

Thank you for the information and for shutting down the miss information. I’m perplexed at how emotionally charged a lot of these comments are.

Just wait for the loan losses from CRE as walkaways and inability to refinance kick into high gear. The roller coaster heading over the cliff is just getting started.

So far, the biggest CRE loan losses were taken by investors because banks securitized the worst CRE debt into CMBS and CLOs and sold them to investors, or sold the debt to mortgage REITs and specialized PE firms. That’s where the losses have hit … and I have discussed that at length here every time we had one of the big losses. It seems banks only kept the least risky stuff on their books (some of it too will default).

You remember the statistic in the QE era of “Margin Lending”…there were some ~$850 billion of margin loans outstanding against stock. I JUST learnt, the big banks with prime brokerage operations, were also engaged in ….get this…Margin Call Lending! They would encumber their “excess reserves” against proprietary speculative gambles FOR FEES using reserves! This was seen as “safe” activity in the QE era b/c markets would only “melt up”.

I welcome QT. More. Faster.

Sooner or later the irresistible force of government deficits will overcome the immovable object of Fed intransigence, like in every other banana-republic in history.

Would like to see Wolf doing some research into comparable banana-republics and their trajectories, what lies their central banks were telling people during the early part of their demise. Maybe follow the path of how the richest country in the world in 1923 became a basket-case today (Argentina).