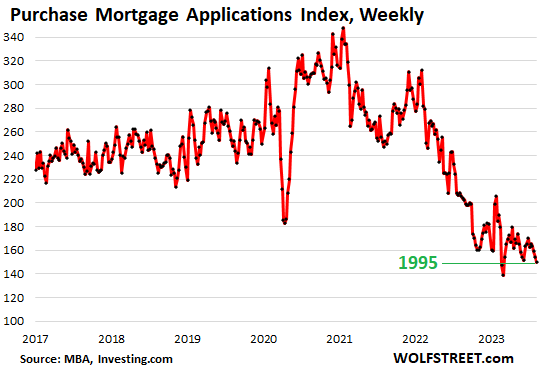

Mortgage applications to purchase a home: -40% from 2022 and 2019, 3rd worst week since 1995, behind only two weeks in February.

By Wolf Richter for WOLF STREET.

The 7%+ mortgages are doing their magic on the housing market as they keep buyers out of the market, and home sales sagged further in late July and August, from already dismal levels, as indicated by weekly applications for mortgages to purchase a home.

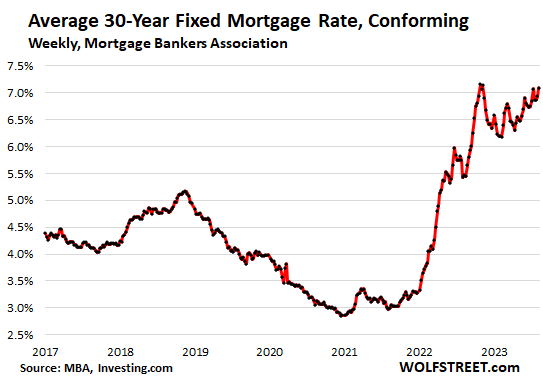

The average interest rate on 30-year fixed-rate mortgages with conforming balances jumped to 7.09%, from 6.93% in the prior reporting week, the third highest since January 2002, with only two weeks last November having been marginally higher than this reporting week, according to data from the Mortgage Bankers Association today.

FHA mortgage rates rose to 7.02%, highest rate since 2002. Rates on jumbo mortgages (greater than $726,200) rose to 7.04%.

“Treasury yields rates rose last week and mortgage rates followed suit due to a combination of the Treasury’s funding announcement and the downgrading of the U.S. government debt rating,” the MBA said.

Yup, the Treasury Department’s announcement a week ago of a tsunami of issuance of longer-term Treasury notes and bonds to fund the ballooning government deficits was followed the next day by Fitch’s downgrade of the US credit rating from ‘AAA’ to ‘AA+’. And they’re now getting blamed for the jump in mortgage rates.

In other words, the government’s reckless deficits and borrowing going back many years are now getting blamed for our holy-moly mortgage rates. It surely plays a part; inflation and the Fed’s reaction to tamp down on inflation play another part, as do a bunch of other interrelated things. The whole thing is a mess, and the result is that mortgage rates are over 7%.

And amid these holy-moly mortgage rates, home buyers have vanished, we have seen that for a while, and it got worse.

Applications for mortgages to purchase a home dropped for the fourth week in a row, from the already low levels that had prevailed for months, to the third-lowest volume since 1995, the two lowest volume-weeks having been in late February this year, according to the MBA today.

Purchase mortgage applications, compared to the same week in:

- 2022 which was already in the middle of the downturn: -27%

- 2021: -41%

- 2019: -40%.

These are very big drops. Mortgage applications to purchase a home are a forward-looking indicator of where home sales as measured by closed deals are headed in a month or two, so for July and August. They show that demand for homes to be funded with a mortgage is at dismal levels compared to the period before the pandemic.

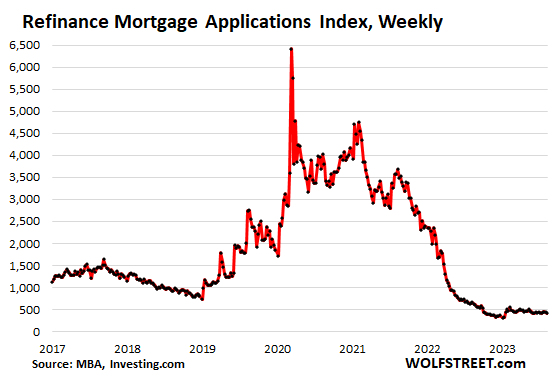

Applications to refinance existing mortgages dropped this week, according to the data by the MBA, and remain in the same low range since refi applications collapsed in early 2022.

The collapse in mortgage refis has crushed mortgage lenders and mortgage brokers, which responded with mass layoffs in late 2021 and into 2022. Refis were a big part of their revenues, and they vanished.

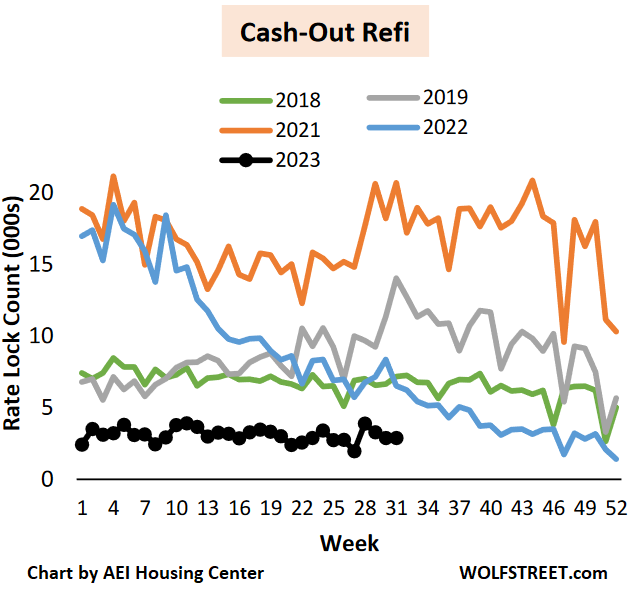

No one who can avoid it is going to refi a 3% mortgage with a 7% mortgage. The only logical reason in this environment to refi a 3% mortgage is for cash-out purposes. And that’s what is happening.

Non-cash-out refis have collapsed by 97% from 2019, according to the AEI Housing Center.

There are some reasons for trying to pull cash out of the home with a cash-out refi, with the expectations that either mortgage rates will be back at 3% next year, LOL, to allow the homeowner to refi the home back into a 3% mortgage; or that the home will be sold within a fairly short time, and maybe some cash was needed to spruce it up, or whatever. And some people have been forced by a major medical or other emergency to pull cash out of the home.

So cash-out refis have also plunged, but not quite as much:

- by 56% from 2022

- by 86% from 2021

- by 80% from 2019

- by 60% from 2018

Chart by the AEI Housing Center, in thousand rate locks per week. Note how in 2018 (green line) cash-out refis also collapsed as mortgage rates headed to 5%, and in November 2018 briefly exceeded 5%. This is a very cyclical and mortgage-rate-dependent industry.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Historically, the current home mortgage rates are really very cheap.

This is true, but with housing prices also going up roughly 40% since 2020, and the increased mortgage rates, and many houses still going for over asking (at least near me in Boston) many wisely just don’t want to be house poor and don’t buy.

People don’t have to bid any more for houses than what they want to pay and if they don’t like the prices, then just don’t bid. It all comes down to simple supply and demand.

If I can get 20% down and 8%+ on mortgage

I’ll consider carrying

always willing to take it back and sell again

helps ROI

Guess you missed this part that I wrote:

“many wisely just don’t want to be house poor and don’t buy”

Problem is, in my area people are buying homes outright cash or still going into bidding wars in some weird FOMO craze. 100yr old homes in the 600k range and still bidding wars or getting asking price and all these concessions. It’s insanity. I love my career and the fact I have almost all my family around here but it’s getting to the point we might have to pack up and move. Not trying to start my first mortgage at 50 years old.

In Eugene Oregon between 1980-1986 housing lost 40 percent of its value. Interest rates were dropping a little from 12.5% in 1982 to 10% in 1986. A house that was 14 years old cost me $28 per sq foot. My payment was roughly the same as the person who purchased it in 1979. It did have seven extra years of wear and tear. I suspect residential real estate has a few more years to the downside. Patience may be rewarded. You can refinance interest, you cannot refinance purchase price.

Everyone thought the market HAS to crash when rates go up. Instead in some markets you have all time highs.

San Francisco is down 20%, many markets are down similarly.

If you are not being sarcastic, please refer to adjusted for inflation home price back then with double digit rates to price now and 7%. It’s the most expensive housing market in the US in the last 3 decades, soon enough it will put Hong Kong house price insanity soon

I do not think that was a coherent statement.

I am more confused by reading it.

I hope it isn’t true that you couldn’t figure out what Phoenix_Ikki was expressing. The message wasn’t clearly, nor concisely, written; but it isn’t exceedingly difficult to figure out what the gist of the message is.

(How does that feel?)

Exactly right.

And meanwhile the BLS bean counters continue to low ball the CPI on behalf of the Fed’s “inflation is contained” happy talk. My BCBS health insurance is going up 14%. The BLS BS artists will never allow the double digit REALITY of inflation in the US to be officially admitted.

My 30 year fixed mortgage rate in 1993 was 7 1/2% when I purchased my home in San Francisco.

Today that home is worth roughly 7 or eight times what I purchased at four.

My pay has only gone up about 3 to 4 times what I was making then.

I was not even be able to purchase my own home back at today’s prices, even if interest rates were 0%.

I guess that the point that I’m trying to make is that because home prices have gone up so much and P has not kept up with that, a 7% mortgage today means a lot more than it did in 1993.

Same here. I paid to ght around 7% in 1993 and I was happy with it. How is 7.09 “Holy-Moly”? I have much older friends who were paying double that when they bought their first home.

Exactly true on the ”double that” part b:

We were paying more than double for our first house, close to 18% IIRC,,, BUT,,, and it is definitely a very big but,,, the house price was exactly $40K…

Same house, last time I looked, was ”valued” at $800K in ’22.

And THAT is the crazy part for the young folks who want to ”settle down” these days.

Not so sure those kinds of numbers are true in ”flyover”,,, as we had a friend there who was buying houses for $2-4K cash at the courthouse steps, fixing them to current codes for another $10K or so, , and then either selling them for $30-40K or renting and refinancing to buy another, etc.

Not claiming any prescience, etc., but certainly seems to this old boy watching RE for over six decades now, we are going to have another major crash of RE and all other fixed assets, likely not so fixed assets crashing similarly also.

Current 7% rates are a “Holly-Molly” for a house priced at $1.4 M

-here where I live- same house I bought in 1990 for $90 K with 10% rates. I wonder how the “goofy” buyers can come up with 20% down payments and afford a $6000-$7000/month mortgage payments.

Location location location.

You can still buy a 3 bedroom/2 bath house in Mississippi for $25k.

There is a distinct set of reasons for that.

Your Home is “worth” what you get for it if you sell it. Funny numbers on Zillow Have nothing to do with that.

Not the case. Superficially they may look that way to you, but think about the last time mortgage rates were meaningfully higher and what home prices looked like back then. 7% on a million dollar SFH is a lot higher than 12% on a $200K back then – in fact three times higher in terms of interest you’d have to pay. And that does not even touch on the crazy insurance and property tax costs these days. Think about it.

It absolutely is the case. The fact that prices, and thus mortgage payments, are batshit high with those historically normal mortgage rates doesn’t make the rates not historically normal.

People, as ever, are confusing mortgage rates, home prices, and what really matters monthly payments respective to income. Home prices are generally what they were a year and a half ago. Monthly payments aka affordability, is not. Fed tracks this all

https://www.atlantafed.org/center-for-housing-and-policy/data-and-tools/home-ownership-affordability-monitor

You should add that per your link, affordability collapsed over the past 12 months to levels not seen since the very peak of the Housing Bubble 1, before prices plunged.

Yea Wolf, theres no way the status quo is sustainable. Without a recession jolt forcing people to sell it may be a much longer and slower burn down though. You wrote June to June peak prices were down 1.5% this year nationally. We have a ways to go. My gut (super reliable) tells me this year will yield a greater drop than 1.5% come next June when you write a similar piece.

The historic breakdown in relationship between interest rate and prices speaks volumes about the batshit manipulation of asset prices by the authorities.

Free markets when? 😂🤣

Exactly, I had a 12% mortgage on my first house but it only cost me $200/ month after 20% down on a $25,000 house.

Which doesn’t help at all when the houses themselves are soul-crushingly expensive.

Very good news.

We expect them here in Europe soon

How is that good news?

Lucca,

I’m sorry I didn’t specify.

I meant that the collapse in mortgage demand, which leads to a decrease in transactions, which will lead to a collapse in prices is very good news to me

Sure, when an expensive house was 50K, not when they are 400K.

I noticed the same My young wife’s and my first home was 10.75% , in Burbank Ca.

My first home was in Pasadena. $115,000 at 13.5%, with 20% down. My monthly nut was just over $1300. That same home sold 2 years ago for $1.100,000. At 2% with 5% down that’s approximately $4500/mo. If you look at the monthly cost that’s an increase of 300%. Wages in that area have easily met that COLA. That’s what easy money did to housing prices.

People complaining about the cost of housing tend to forget just how cheap it actually was. We will get cheaper housing costs, but the payoff is going to be a much higher, and harder to get, loan.

That’s very true but a lot of people have short memories.

True, but historically they didn’t print money like CVS receipts.

LOL! Those things are a mile long! They must go through a ton of paper.

My first mortgage in 1972 was 7.5%

Normal is all about expectations.

In ’82, my first was 13% – OUCH!

And the house was probably $35,000?

And he had 32 acres “for the kids to roam”

Hehe

And their annual income was probably 50% of the home value and probably increasing pretty rapidly with a fixed mortgage.

We built our first house and had a 30 year, 10.2% $32,000 mortgage. This was In 1974, and as I recall, it was not a very good time for real estate, but that was decades ago. The mortgage rates and qualification, pretty much drove the decisioins on the size and location of our build. It was a 1,008 square foot 3 bed ranch. Not sure if relevant, but the builder went into bankruptcy 5 months after the close. So much for his warranties.

I guess if we could have borrowed then at 7.5% maybe a family room and air conditioning might have been an option, or a little better location.

Come to think of it, do they even build “starter” homes any more? All I see are 5,000+ square foot mini mansions being built and sold to DINKs.

Many cities have minimum sizes for houses now. Mesquite TX, for example, has a minimum size of 2,000 sqft.

1999 30yr = 6.375

But if it is anywhere with decent employment oppertunities the base cost has gone way up so that is 7.5% of a smaller principle = more affordable.

Someone: “Wow, I got a 7% return on 1 million dollars over the last year!”

You: “pshhhh, I loned a freind 100 bucks and he paid it back with an extra $7.50.”

Yes, your %return is better, but these are not the same thing, the money involved is much large in the first one. Yes this is a more extreme example, but that is for the purposes of clear illistration, the underlying point is the same. You can check, as Wolf points out in these comments the effective affordability is now worse than any time other than right before the 2008 crash.

Be careful standing on any rug these days.

you think mortgage rates are high now? just wait! After factoring in real inflation they still are too low

And, yet, in my neighborhood in San Jose, there is still very little inventory and homes that come on the market are gone in a few days. Zillow (yeah, I know) predicts a 5-6% increase in homes prices in the next year. Apparently, 7% rates don’t faze these buyers.

California does probably take the FOMO cake to another level. Doesn’t seem to faze SoCal buyers either apparently…

Its no longer FOMO running house prices up. Theres simply not enough supply, either existing or new, for sale

Per Wolf, “7%+ mortgages are doing their magic on the housing market”

No theyre not. Prices are higher now than pre pandemic in many parts of the country. The fed stopped most buyers from buying, but they haven’t figured out how to force all the existing homeowners to sell.

Sellers wont increase until interest rates drop – who knows when – and falling interest rates ater a huge runup generally signals recession. So were back to the same story. No recession, no lower house prices. Couple of years from now? … MAYBE

Existing homeowners are not selling because they’re waiting for the pivot. If the pivot doesn’t come, they will sell.

The NAR’s national median price for July will likely be lower than June’s price — changing the up-trajectory in recent months to a down-trajectory.

That measure has been down YOY for several months and that looks like it will continue.

Sure some markets are up, but others are down bigly. Every market runs on its own clock.

Perhaps thou art fortunate, Bill C, to live in an affluent neighborhood where the buyers are wealthy – largely unrestricted in their spending by inflation – and paying cash ?

Yes most houses that sell in my state are all Cash, 85% are from other states that sold for nose bleed prices, so they bid up and pay way over value. The do not have a Mortgage and they do have new “everything”… But they are either retired or working part time because the jobs market is tight for “blow ins”

Such a fantastically dull town, too. Climate’s nice enough, though.

Building and selling tract homes like crazy in Sacramento region. I get investor cash offers to buy my rentals 3-5 times a week albeit at a 30-70 grand discount. Looking at land in Montana, Idaho and Wyoming. Still extremely pricey and there are places still selling. I’m not phased at all by this. As long as jobs are abundant and two people work then the buying will continue.

Don’t confuse automatically produced junk-emails from a marketing company under a quarterly or annual contract with actual “investor cash offers.” Those emails will keep coming until their contract is up.

I cannot tell you how many “buyout offers” or similar that I have gotten for this website. Some of them are already tagged as spam. It’s just junk email that gets sent out to a gazillion people.

I live in eastern Washington state. Its dry here. Gets hot in summer. This one not too bad only 23 90 degree days this year.

We’ve had 45 to 50 previous 2 years quite a bit above average. Hit 113 2021 summer and we are close to 200 miles north of Minneapolis !!

Sacramento… unbelievably dry in the summer. Too dry for me… I like it dry but it just seems too extreme.

I’ve seen the statistics at Wikipedia. Summary…two Sacramento locations per

Wikipedia data i an summarizing.

May thru October, 6 months:

Average total precipitation:

2.17 inches, 1.96 inches.

June thru Sept., 4 months:

Average total precipitation:

0.38 inches, 0.36 inches.

Both locations average ZERO, 0.00, inches in July and less than 0.05 inch for July and August combined. One location has an average high temperature of 92, the other 94 for July-August combined.

Heck, people spit more than that in the 4 months June thru September !

(a lot more if baseball players).

Eastern Washington state and 200 miles north of Minneapolis?

Washington and Minnesota states have the Dakotas, Montana, and Idaho in between.

Jack … in response to your question:

Minneapolis at 44.97° latitude.

Spokane st 47.65°.

Approximately 70 miles per degree latitude. So 2.68 * 70 or about

187 miles north of Minneapolis.

We get cold in the winter but not nearly as cold as you. Then again you don’t get nearly as cold as Yakutsk in eastern Siberia… check it out via accuweather (winter) or Wikipedia (select Geography tab then scroll down past Geography stuff to weather table and discussion).

1000 miles south of Yakutsk is Harbin, China. Its at same latitude as Portland Oregon but colder than Anchorage but not as cold as Fairbanks. Not much snow though.

So so so many house deals are failing appraisal right now. While home sellers still think they can price at 21/22 prices, mortgage underwriters and appraisers are not on-board.

What’s more delusional is I see those houses come back to For Sale after sitting on Pending, and they don’t come back with any price drop. Like they just cannot believe that the value of a home can go down.

Isn’t it America’s main religion now that housing and stonks only go up?

With ZIRP its true. The question is how many years till the feds’s handlers demand they bring back ZIRP.

I have never once overheard anyone in Vegas discussing the vital guttage they had pulled out from this that or the other orifice by the house. It’s always about the winnings…no matter where you go.

…typing the word ‘stocks’ like that — like your qwerty had inflamed adenoids.

why

The poster was making a point about a fanatical mindset and used jargon from that mindset (stonks) to illustrate the point.

This is happening in my neck of the woods in the East Bay Area.

What bad is east bay with its appraisal failing?

A large chunk of people in Real Estate have their livelihood tied to not understanding that the imputed value of an asset is tied directly to the borrowers interest rates. I fully expect Commercial Real Estate to go up in flames long before Realtors gain some sense of reality.

People don’t care. Unless you have a small down payment 3-10% down, it’s really doesn’t affect the loan much.

With such limited product, people just want a place to live and a low appraisal will not stop them.

Heres to praying this gridlocked market leads to the mother of all overbuilds in the new construction front and craters home values for a generation so no one else has to play this game again.

Seems like nothing but apartment complexes being built in Omaha and there full,

Went past a new *luxury* apartment complex under construction in Gilbert, AZ yesterday. Architecturally, they rival the Russian apartment blocks from the 1960’s. Of course, they had an exciting name…. “Trevi”.

They looked about as Italian as a packing crate.

The only thing luxurious about the new apartments is the general lack of bedbugs and overall lead contamination you find in older units. With some epoxy composite faux granite counter top you can charge a few hundred dollars more a month on rent. Normally break even as a renter going for these outfits since the electrical and heating bill will be 50% lower every month since the windows likely shut properly.

They built one near here where the developer “forgot” to install any noise isolation. The build quality of these new “luxury” apartments make them nearly unlivable.

$400,000 @ 7.0% running about $2600 mo. Affordable options out there in no man’s land. This means more money will be spent on T/E for upcoming holidays. USA last half will be a blowout spending spree, America loves Santa clause. I’m not hearing the same thirst and chatter about homeownership these days. Almost like when everyone was getting a Peleton delivered to their residence. All smiles STOP together.

Ah yes the Peloton craze! Maybe Wolf should analyze that….

Where the housing prices and interest rates meet, not a soul to be found,

All these Fools buying houses think one or two things will bail them out ,wage inflation, or lower interest rates .Blackrock is on a different page ouch

Where do you get this BlackRock junk??? They don’t buy houses. Or neighborhoods.

He could have really meant Blackstone,

which if I recall, is more directly involved

in single family homes. I sort of expect

that they chose the name just to sow

confusion.

Blackstone doesn’t buy very many either, compared to “mom and pop” investors.

Blackstone bought entire portfolios of already rented out SFH from another big landlord and it bought build-to-rent communities from homebuilders. That’s all its doing.

https://wolfstreet.com/2021/06/22/no-blackstone-didnt-buy-17000-houses-out-from-under-desperate-homebuyers-and-blackrock-didnt-buy-a-whole-neighborhood-but-built-to-rent-is-a-h/

They sold IH in late 2019 too.

As always terrific analytical. A point of view from a Global Retiree with homes around world including USA>

Prices for homes in the USA compared to almost anywhere in the world are extremely high eg in the key “global” cites like Bi Coastal LA SF NY Boston Philly Miami and adjacent burbs,

What makes the USA absurdly expensive is unlike most countries in the world have a permanent penalty legal expropriation in the form of property tax which in most areas (ex California ) are in the 2% of value of home and absurb mantainance HOA etc costs another 2% . Many countries around the world follow Latin model or Asia model of no property tax and low maintenance ,

Key point of above when you take in real costs USA higher end properties are priced to perfection and have escalated due to money printing , inflation and income gains at top 1% range, Go short ………..

It’s really not true that US real estate is expensive relative to other countries. By some metrics like price to income ratio, US real estate is actually among the cheapest in the world. Obviously this considers the entire US market, not just certain areas or cities

This is really encouraging, that as rents had slightly been headed lower, at a glacial pace, the landlords have to rethink inflation versus disinflation and crank rents higher to gouge people a bit more — this’ll also play out well with Airbnb and the unlimited amount of income everyone has.

Obviously, in our booming recovery, 7%+ mortgages don’t matter, because people still have tons of endless stimulus money — and stocks are making everyone rich, including a tsunami wave of students who all have excellent jobs, and increasing income growth. Between massively wealthy baby boomers and rolling in dough millennials, this is tribal — & AI and the Fed have everyone’s back. Additionally, this gives banks some breathing room going into Fall, and everyone knows stocks are going way higher in a Santa Claus rally— there’s nothing going to stop the expansion of this pandemic hallucination!

Does this post come with a sarcasm tag?

One of my family members is a realtor and her two buyers just dropped out of the market, presumably from mortgages rates pushing above 7%. Unless you’re a cash buyer, there’s really no reason to enter the market right now. With so many mortgage holders in the 3-4% range, I suspect mortgage applications and consequently home sales will suffer significantly as we head into a more seasonally weak period for home buying activity.

Despite this collapsed home buying activity, I don’t foresee much downward momentum in housing prices beyond what’s seasonally expected. The job market remains too tight to lead to an increase in forced sales. I suppose rates going even higher could erode enough demand to force prices meaningfully lower, although rates going to 8%+ through the end of the year seems fairly unlikely.

From my perspective, the likelihood of home prices going down is quite a lot and home prices going up is minimal.

I think its a matter of time for home prices to go down unless something drastic happens..

I agree mostly with you. No matter what a certain number of life situations will bring forced selling to market. I think even cash buyers are out however at these prices. I wonder how many veterans of the GFC are on the sidelines. Maybe history wont repeat exactly but maybe it might rhyme somewhat. I think the sellers really haven’t gotten the memo yet. But I think some warning bells in their brains might start going off if Powell bumps in Sept and we continue to get dismal stats out of the housing sector, which seasonally is expected. But if you think about it, if you ever tried selling anything you list high and incrementally come down depending on your motivation level. Motivation usually requires some reason or duress, else it’s just fishing. In line with mortgage applications falling off a cliff, I’m looking at ‘time on the market’ going up. Another thing I am on the look out for as the market slowly gets the memo with ‘higher longer’ is those who bought a second home years and years ago are still sitting on big appreciation wins. The old adage is he who panics first panics best. Pretty sure that’s a Wolfism. These are folks who can still sell their properties and make significant money while the getting is good. These are also the people who start putting the newer buyers in trouble with negative equity. Once enough undercutting starts happening — that could change some of these dynamics.

Here is one reason the 3% mortgage holders do not want to sell

A 30 year $400k loan @3% means you will pay 207k in interest over 30 years. Total cost of your loan is 607k

A 30 year $400k loan at 7% means you will pay $558k in interest over 30 years. Total cost of loan e is $958k.

At 7%, you will be paying more way more interest than principle.

But most people are still only concerned with monthly payments and not the total cost.

Does that seem myopic to you? Focusing on the monthly payment? I used to think so, too. I also to make finding a “forever home” as my main objective. I guess from a purely bookkeeping vantage, that may still be attractive, but I’m moved away from that thinking.

I know of only one person in all my years who stayed in their home for more than 30 years — Mr. Wheeler. I’m not even sure if he paid it off — I think he double mortgaged when he hit a hard patch in the early aughts. The point here, though, is that he’s rare; people stay in a place ~ 7-8 years on average. As a homebody even I have never lived in a single domicile for ten years across 45.

Mr. Wheeler’s wife left in the 90’s, his kids are all middle-aged and his grandkids are all grown and moved far away. All the neighbors he was once so familiar with have long since gone three or four waves over…his pride of ownership in the place started to evaporate, too, with blue tarps on sections of the roof and overgrowth needing a month of Sundays with a machete. I would think one would feel utterly haunted staying in any place that long. Way too many memories and reminders everywhere.

That people have not used to stay in one home may not prove that more may stay long in a home.

I live at a different place and I know neigbourhoods wher few have lived there less than seven – eight years. Some places people move in when they are young and leave when they die.

(The work needed to clear out the house afterwards might then be monumental.)

“overgrowth needing a month of Sundays with a machete”

Just picturing that in my head cracks me up. Lol

bul – key that observation to the fact that very few of us now work twenty years at one firm that doesn’t move or close the local plant/office itself, and the evaporation of formerly-‘healthy’ working-American neighborhoods makes perfect sense…

may we all find a better day.

“The point here, though, is that he’s rare; people stay in a place ~ 7-8 years on average. ”

People own the same house (at least the same mortgage), keep the same job, and keep the same spouse an average of 7-10 years.

I think it is sad but it seems to be human nature. For houses, historically a house should be owned 10-15 years to guarantee it is above water. For marriages, 7 years is when the kids need both parents and not 2 poor parents living apart. However, staying on a job for 7 years gives you the skills to move to a better paying job. After 7 years at one company, you are likely underpaid and under-appreciated.

Studies and movies call it the “7 Year Itch”.

My down payment is now in treasuries earning a decent return that easily covers the rent increase. Waiting to buy is getting easier everyday.

People sell because they have to sell.. period. They aren’t thinking “Hey let’s cash out of this home and realize some gains!” They move, they die, they divorce.

However, if there are no buyers because the payments are through the roof.. something has to give. Or they can just eat the nut every month.

Rates “higher for longer” is going to mean a return to 5% minimum rate mortgage for decades. These are just normal rates. What’s obvious to everyone (a timely return to 2% inflation) is obviously wrong.

The Federal Home Loan Bank (FHLB) loaning to stabilize banks would seem to be a very positive force to remove excess liquidity from the mortgage market, thereby tightening credit to soften housing market FOMO.

I got another letter from Opendoor last week. I average about 1 letter every 2 months. I’m in Southern California.

These mailouts are on automatic pilot. They’ve been farmed out to a marketing company on a contract. So they’ll keep coming until the contract is up, come hell or high water.

Gasoline is up 20% since July 1.

Rates aren’t coming down anytime soon.

SPR drawdown has stopped, or paused.

That’s what happens when you can see the bottom of the “tank”.

Ltiftc

The daily use of gasoline in USA is 20 millions a day!

Does release of 50 millions, off and on out of 650 millions in SPR has any perceptible effect? OMG!

Joe drained it to buy votes forthe midterms. Insanity. And running up to next November I see a drop in rates despite the fact that it will be economic insanity. Our political class sees reelection and campaign funds as their only goal. The rest be damned.

“In other words, the government’s reckless deficits and borrowing going back many years are now getting blamed for our holy-moly mortgage rates.”

Every unit of purchasing power the government spends comes from somewhere. It’s not manna from heaven. If it’s not taken in direct taxes, it’s extracted through the capital markets, in the form of more expensive money or it’s reduced purchasing power, or both.

Yeah. Everyone wants their free government cheese and then complains about gas prices or (insert complaint here). Few can (or are willing to) connect the dots.

“Every unit of purchasing power the government spends comes from somewhere. It’s not manna from heaven. If it’s not taken in direct taxes, it’s extracted through the capital markets, in the form of more expensive money or it’s reduced purchasing power, or both.”

Yep. Paul Volcker knew this well, it’s a shame that Greenspan, Bernanke, Yellen and JPow in his first few years (before he finally got religion and wised up to inflation’s wreckage last year) largely ignored his wisdom on this.

Now tell us the mortgage rates in Japan……

Who cares? People pay cash to live near SocalJim. They all strive to be the next SocalJim, but there’s no beating the original. The sun will never set on SocalJim’s real estate.

All hail socaljim

SoCal, Texans, Florida state, NYCers…

Like to hype their locals.

SoCal… some find the climate too dull.

Good for older folks sure, but many young like

to ski, hike, or experience 4 seasons.

Texas… too hot too long. 7 months more or less pretty good, but my how you pay late May to early October. Lived there 11 years…No question about it November was my favorite month.

Cool air was unbelievably welcome.

NYCers… humid summers… low temps 65 to low 70s. Nice falls but you can get them anywhere back east. Never will understand its appeal I lived in Jersey 3 years 30 miles from ha ha

“The City”.

Florida… humid and hot. Hurricanes. Older folks attraction.

They are all overrated. Not saying the

Upper Midwest for instance is right for everyone.

Tough climate for sure. But it depends on how

fit you are to some extent.

I liked Seattle’s climate, 4 years. But too expensive. Chillier than I’d prefer but pretty good.

Redwood City, CA nice but expensive.

Too monotonous for some although winter rains nice.

Some love the Rockies states. They do get cold at night, but definitely some plusses.

I’m in eastern Washington… dry nice but wildfire concerns are a reality in late summer fall.

OK climate not great. Similar to my birthplace, NE Ohio in some ways, different in others.

Slight edge to eastern Washington if one ignores the smoke from fires. But neither is paradise

by any s t r e t c h of the imagination climate wise. But not too bad either.

FWIW or not.

Real Estate market is broken. Wide gaps between buyer and sellers.

Buyers expect lower prices due to rates….Sellers expect prices from last year.

Now, add in CA and FL insurers backing away from home insurance….insurance required for mortgages. More illiquidity.

Mortgage rates are similar in Canada. About 6-7% for a 5-year fixed and 6.5%-9% for variable mortgages.

But house prices are tremendously high. Houses sell for C$1MM in Barrie and in the middle of nowhere.

As of recent, Bloomberg reported that the Minister of Immigration aims to revise immigration quotas higher.

The CBC posted today that a [suspected diploma mill] cancelled the offers for several hundred ‘international students’ because of recklessness. It was just the other day that almost 1,000 ‘international students’ were given clemency after being caught up in a fraud scandal with their immigration consultant agency.

The rule of law in Canada is being eroded to prop up the housing bubble. In America, it’s very difficult to obtain a student visa, and they give 10 year bans on Canadians for overstaying their maximum visa free stay.

The question is: long will this Canadian Ponzi scheme housing bubble go on?

All the thousands of foreign students buying 5+ million dollar homes in Vancouver is well documented. Now with the ban on foreign buyers in British Columbia more and more foreign students are flooding in as buyers.

Pathetic. Apps like Wealthsimple temporarily freeze your account if you start transferring large sums to buy stonks, but bogus students are allowed to buy million-dollar mansions in Canada, and no one bats an eye?

In breaking news, the Auditor-General revealed yesterday that the Greenbelt sale absolutely stinks of insider trading, collusion and corruption with the Ontario government.

The developers stand to make billions of dollars in revaluation profits because they bought the land cheap from the government.

The avg net savings of a Canadian immigrant is 23k.

Outside of Van and TO, foreign buying is negligible. The blaming of sky high RE EVERYWHERE on them is a classic case of projection. The main driver of the Canadian bubble are ‘born in Canada’ 30-50 years ago. The main motive is the desire for wealth. Note how every ethnicity is accused of loving money, when it is actually universal.

I’ve been a realtor albeit a long time ago. Due to an amicable split we sold our Nanaimo house for 370 in 2014. To white Albertans BTW. It may have hit a million last year, might be a tad lower now. Since then I’ve been wanting to get back in and started looking everywhere, incl New Brunswick, which has about as much appeal to Chinese as the moon. But it is up 50 to 100 % in 2 years.

Main culprit on Vancouver Island and BC, an artificial land shortage. When I was a young realtor in the eighties, I had serviced lots listed in a new subdivision. A nice one was 25 K and you would need to spend about 75 to meet building scheme. So lot was 25 % of 100K package. Today it would be at least 50%. Or worse. Yr cheapest lot would be 200K and if you were careful you could prob get 2 bed ranch built for 150.

BC has the land mass of Western Europe with the population of Paris. About ninety % of it is Crown owned, not available for habitation. As soon as you look across the border in Washington, prices for small acreages drops 50%. Of course these won’t be serviced, except with power, but people can put in septic and drill wells. BC developed an aversion to the 5 acre subdivision a long time ago.

But most people want full services. Are services expensive? Yes but at 200K per lot, or 100K, you can put in services to a multi acre block. Nothing has inflated in price as much as existing buildable serviced lots. The % of price attributable to services has fallen.

A new attitude is needed, and maybe a new party. We have a supposed left- wing party here. In most to the parts of the world this would be associated with easing land ownership for middle class. Not this one

Maybe party called ‘Land to The People’

“BC developed an aversion to the 5 acre subdivision a long time ago”. On a tangent, a long time ago I did read that the British had done the numbers and found that rows of houses like built in England was the most cost effective way to build housing. Efficient use of land and materials.

A kind of housing that also gives quite good living qualities. Every house is a “family home”, there is driveway and parking space in front with a garden at the back. Still “compact” enough to make it possible to walk to the grocery store and public transport.

Oh for sure. Most people want serviced lots anyway so even as small as 50 by 100 would do and be economical to service. But going to sixty by 125 would not be a budget buster at these prices. And btw, that is the UK, whereas Canada I believe has the lowest pop density in the world.

But re: small acreages, since province is mostly empty, what is the harm? My feeling is that the urge of bureaucracy is to control.

Get this: a piece in the Globe and Mail chastised Vancouver etc. for not being more like Tokyo, where land use is really, really efficient. But maybe we don’t want live in cubicles.

Have to add my nephew just picked up 2 more houses in northern Japan for close to nothing. I don’t know why domestic demand for these is so low. Is desire for rural life not part of the psyche?

I gather from him via sis that all the stuff is included as old folks died and I guess no one wants stuff.

If the foreign buyers ban was negligible, then why did the Federal Liberals adjust and change the law when the listings started piling up and there were fewer and fewer sales?

Canada is set up like one giant Ponzi scheme where they rely on the capital from newcomers to either pay rent, or buy an overpriced developer home, on land that was either bought cheap by billionaire developers from insider trading with the government or given assent to build by changing the laws- Green Belt controversy.

Canada is a nightmare and greedy Canadians created the problem.

In fact, the Fed is sitting in the MBS trap! They had purchased far too much and too long, and now they have no chance to roll of, because mortage refi activitiy and housing sales activity crashing, and the mortgage rates spikes to new all time highs.

And outright sales are now also a bad way, because why should a primary dealer buy the low interest rate MBS from the Fed, when they can get from the banks and Fannie and Freddie mortages with a interest of 5,6 or 7% ?

The Fed can sell the MBS just fine at market price, which will be lower than what the Fed has them on the books for, and so the Fed would have a loss of some kind on these securities. But the Fed doesn’t care about losses. It creates its own money and therefore can never run out of money. It’s just a question of how to account for the losses, and the Fed figured that out too since it’s already losing money, and so it has a special “deferred assets” account where it tracks those losses for everyone to see. No biggie.

I agree, the losses are not really a big deal for central banks. What i dont understand, why is the Fed not doing outright sales of MBS?

Of what benefit of value would that be?

Right now, the FDIC is selling MBS every week as it unloads the stuff it picked up from the failed banks. That alone will guarantee that the Fed isn’t going to add to it. After the FDIC is finished, there might be more discussions about it.

Doesn’t the Fed lose credibility, potentially hurting the value of the dollar? If that’s not the case they might as well acquire common stock and homes during the next downturn…

Also, as the run up the “deferred asset” account, aren’t they pushing out the date when they can once again remit excess revenues to the Treasury, thus increasing federal deficits?

Probably naive, but those seem like big issues to me.

Do losses on sales of bonds reduce the amount of interest revenue remitted by the Fed to the Teeasury?

Yes, the Fed won’t remit anything anymore to the Treasury until all its cumulative losses have been made up with gains, which is going to take years.

No chance to have the MBS roll of?

Well, they will roll of within at the most 29 years. At least most of them.

No, they’ll roll off a LOT faster.

If the Fed ever cuts interest rates, the roll-off of MBS will become a HUGE torrent because there will be a tsunami of refis, which means mortgage payoffs, and the principal is passed through to MBS holders. And those MBS will vanish.

Back during the pandemic when interest rates dropped, and refis exploded, the roll-offs were in excess of $100 billion a month. And the Fed had to buy a HUGE amount in MBS to replace them, and to add to its balance sheet.

In addition, the ongoing mortgage payoffs cause the pool of mortgages backing the MBS to shrink to such a point that it’s not worth maintaining the MBS. The issuer (such as Fannie Mae) will then call the MBS, meaning pay holders for it and withdraw it, and repackage the remaining mortgages into new MBS and sell the new MBS.

This is why 30-year MBS never live to be 30. They keep shrinkging, and after some years, they’re called – sooner during a refi boom, and later when there are fewer refis.

So don’t worry, those MBS will come off quickly if mortgage rates drop.

Thanks Wolf!

I appreciate the information that MBS get called and repacked. That was new to me.

Hohoho, CPI has remained sticky and seems to be on the way up again. Happy times are just around the corner.

Bend, Oregon just hit new ATH. $800k median for a home here. Folks are loving those new 7% interest rates.

“All time high?” 🤣 This what Zillow says:

You should know by now that I’m going to zillow out this kind of RE-hype comment, LOL

Thanks WR

People live in their own bubble especially real estate pampers.

It is not surprising to see people even in this comment section who thinks home prices have reached a permanent plateau.

As someone who works in hi tech think Amazon Google Microsoft i can tell you first hand job market is not good and more layoffs offs coming.

The average salary in my field is 150k plus 150k of other bonuses and benefits.

But at the lower and middle end of wage spectrum.. job market is hot .

In my hood the median home prices is 1 millions. The low end job per hour wage increased 60 percent in last 3 years but with $18 per hour they still can’t afford decent housing.

Something has to give in.

I know you meant real estate pumpers, but real estate pampers made me legitimately LOL. It works on at least a couple different levels.

Bend is kind of like a snake eating its own tail. Most of its economy is based on the RE and residential construction industry. As the interest rates go up, that will all shrivel and die forcing home prices down even more. Sure there are a few WFH’s but as that whole fad shrinks, and the skimpy air service tanks that too will shrink. The good thing is that home prices will be held up a bit because forest fires will sweep through the place cleaning out the excess inventory from time to time.

Well, we can either kill the sacred housing cow or have higher inflation. The Fed wants hamburger.

Price discovery is slow.

Have home insurance increased?

Of course. And in some places by a lot.

Minimum 40%+ in south Florida. Many condo associations are getting killed and considering selling out at land value to developers vs. 200-300% condo fee increases.

High insurance premiums are actually doing more harm to the market here than high interest rates

Home insurance has indeed increased. That is to be considered a good thing compared to the alternative of having it cancelled due to being in what the Insurance company deems a hazardous area.

Would you rather pay more for something and have it available, or have it unavailable at all?

Tough choice….

IN So Cal, my home insurance increase almost 100% in last 2 years and in last 4 years, by 300%.

Similar outrageous increase in auto.

More EVs on the road would increase insurance for all I guess as even a small accident on EV means battery pack replacement which can be hugely expensive.

Corelogic:

“And while higher mortgage rates are impacting affordability for buyers with loans, almost four in 10 sales are all-cash transactions. Also, most baby-boomer homeowners have substantial equity, which could be putting pressure on prices in markets where that generation is currently migrating.”

From Liberty Street :

“In the end, fourteen million mortgages were refinanced during the COVID refinance boom, and these refinances will have effects on the mortgage market for years to come. Many borrowers who refinanced during the boom have improved either their cash flow, through a reduction in payments on their existing properties, or their liquidity by extracting equity from those properties“

Fed needs to raise rates in a few weeks, because inflation is being brushed off as inconsequential— home prices need to crash and people with excess cash need to be crushed. Policy is way to easy and loose.

In the monetary system homes, that is real estate act as part of the backing of the currency. All those houses are the collateral for the mortgages on them. If the home prices crash the value of the collateral crash and suddenly there are a lot of loans with no collateral and there goes the “backing” of the currency.

The banks are of the hook as long as the they have got rid of the loans as MBS sold to others. Still the holders of those MBS may have problems if the underlying collateral loses its value.

It has become apparent we are going to be in for a long slog of “adjustment” in the real estate markets. In short, a long slog of down, because maths.

If you need to sell in the next five years, you might as well git it done now. Not in three years, not next year, now. But emotions tied up with homes make economic transactions “reluctant”, and that is the death of so much equity.

Rates now have more than doubled. And now we get to the underwater buyer stage again. So, in essence, nothing has changed, and here we go again. Want that house by the shore, just wait until the Airbnb crowd finds out that houses as investments.

Someday this war’s gonna end…

Much of the price of new houses is determined by development restrictions.

They’re building lots of houses still.

A few days ago I saw a web video. The person presented regional median sales prices for new homes. Per memory:

West: $547k

Midwest: $397k (or was it 390k ?)

South: $370k

Northeast: $789k

These figures were obtained from either Zillow or Redfin… I think Zillow.

I believe these were sales prices, not list prices but will not stake my life on it.

I was surprised how much more expensive the Northeast new home construction was.

Is everybody that well to do in NH, VT, ME, and MA ? Probably not but they are apparently pleased to restrict supply to the upper middle class ?

The West is HUGE and very diverse with vast rural areas. It doesn’t mean “West Coast.” The Northeast is small with a concentration of big cities.

Compare the Northeast to the West Coast.

Wolf,

Lived in NY and NJ. I know about the Northeast.

Pennsylvania and New York states have a lot of rural area. In fact NYC, Philadelphia and Boston are the ONLY big cities (Pittsburgh marginal) in the NE. West has a ten or so big cities.

Did I say West was West coast ? No.

Yes, the NE is much smaller than the other regions in area.

Were you disagreeing with anything I wrote ? Specifically what ?

The major point was that the NE new homes are much more expensive…

NYC , Philly, and Boston skew the numbers but then so do SF, Seattle, LA, Denver, Portland in the West.

If you are suggesting NYC, Boston, Philly make up a bigger percentage of NE population than do the major cities of the West… maybe.

I actually called someone on the Burlington VT city council and let them know about this info.

I didn’t disagree with anything you said. I tried to address why you may have been “surprised” – you said: “I was surprised how much more expensive the Northeast new home construction was.” So I pointed out that the West is vast and diverse and is not the super-expensive West Coast. That’s all.

Wolf,

Okay, sorry if I misinterpreted your response.

It probably is true that the new homes being constructed near large cities (whatever region of the country) are more expensive on average than those near smaller cities, towns.

I was glad to see the Midwest and South had somewhat affordable new home construction… you’ve been reporting on the new home construction. Many commentators at your site and elsewhere complain about the quality of new construction but I have no idea how anomalous these criticisms are or not.

All too true: Americans in general state a lot of things which to some degree are true. But not knowing to what extent they are true (percentages, absolute numbers and yes standard deviations !) is a very significant thing.

This seems to be lost on too many Americans.

Standard deviations are almost never reported by the media.

But if we knew, say, 200 homes in city X sold for a median price of $400k with a standard deviation of $10k that is different from those 200 selling for $400k with a standard deviation of $100k.

Clearly in the latter case there is a greater variety of homes being sold.

I realize you understand this, just pointing it out in general.

The population standard deviation (or its estimate) is significant in a lot of statistical inferencing.

From my findings in my area. If your looking for an affordable home under $450k, there is very little inventory to choose from and most sell quickly.

$450k to $600k it starts to transition and that is because this is where new home prices start. So existing sellers have to compete with builders. If you above $600k, you have a lot of choices and ample inventory. Most of the price cuts are in this area.

Summary: For the median household income in my area, affordable homes need to be below $450k. Slim pickings.

I am not sure if this is what others are seeing in their neck of the woods too? The new home price entry point is the cutoff. Inventory below that price point slim.

Check out days on market for homes over 2M. It’s climbing like no tomorrow in colorado. For example my home in Nov 2021 sold in 5 days, same neighborhood I see homes on the market now for 150+ days already haha.

Glad I sold off all of excess investments between late 2021 and early 2022, friends in boulder are now down from an offer they turned down in mid 2022 at 2.9M and can’t find any traction at almost 500k less. Still overpriced but they thought 150k under asking them was too much off. Now that is listed at 2.45M over 200 days on the market and still no offers.

It’s really simple the cash buyers are earning 5%, so a 2.5 million dollar home cost $125,000 of lost income.

Those people are idiots. I never understand why people like that would get greedy. What did the Boulder person who got an offer at $2.9 million pay? $1.2 10 years ago?

No one ever lost by taking a profit.

This is a good insight about the opportunity costs incurred by cash buyers.

I wonder when investors in rental properties will realize that they can sell and earn 5% on their money for doing nothing…

My friend sold a home in socal for $850K. It was bought by someone for cash and now in the market for rent for $4K/month.

Ru82,

There are plenty of homes built in the 50s to 80s

in Ohio priced $150k to $300k. Even lower than that but then its usually a really older home.

Undoubtedly true throughout most of the Midwest.

West Virginia has some very affordable housing too and not a bad climate (humidity yes).

Tennessee on the other hand has had a huge run up in prices in Nashville and surrounding areas.

Knoxville as well just not so much. Out of staters I understand.

Quote:

“No one who can avoid it is going to refi a 3% mortgage with a 7% mortgage. The only logical reason in this environment to refi a 3% mortgage is for cash-out purposes. And that’s what is happening.”

Precisely. I have this story as well and many times.

Since mid 2021 mortgage costs (interest + repying principal) have – more or less – doubled. In that regard real estate price have to come down by some 50% to make the affordability of an average house improve to mid 2021 levels. Ouch & OMG.

Could we get another update on Canadian real estate? Thanks in advance!

In a wealthy Seattle suburb neighborhood I’m watching, the inventory shot up 30% last week. The new listings are dominated by people who bought in the 2020 to 2022 time frame.

These people are out on the price limb, and they know it. Many of them are watching their deposits evaporate as home prices deteriorate. If price declines accelerate, they are at risk of financial disaster. I suppose many of these people bought a home equal to 5-10x their household income. Not much room for error.

I’ve also noticed time on market in this neighborhood is drastically understated. The only houses selling are those priced correctly, and they sell in a day or two (but very few of them sale, as transactions are very low). Alongside them, are lots of houses that have been for sale for 100 days or more. Thus, the days-on-market for homes actually sold is very low. But, the days-on-market for all active listings is astronomical and rising.

Seller frustration is setting in, and it won’t be long before prices plummet. Tis the season. Could get really bad if the stock market declines too.

I wonder why they will sell when their mortgage is rock botttom low

My point is they are selling, because prices are dropping, and they have little if any equity cushion.

I’ve seen that phenomenon on the other side of the country as well. Houses that sold in 2020 or 2021 coming onto the market for close to the same price as they sold back then. After closing costs and realtor shake-down, oops I mean commission, that’s a mighty fine loss.

In the words of a famous announcer, “let’s get ready to rumble”

No, no, no….don’cha know when they get rid of the payment they “break even”

SoCalJim’s real estate does Not need insurance or maintenance.

Also, he walks on water.

I buy RE at bottoms. It’s a feel of desperation that I see on people’s faces, no bids, empty open houses, skittish banks etc… SF down 20% sure is a sign but we’re not at an obvious bottom. I’m not buying anything. Even all cash. I don’t feel it.

When mortgage interest rates were going up in 2022, I heard so many people say, just buy the house now and refinance next year when interest rates drop. I wonder how many people bought into that strategy and now almost 1 year later we are not seeing any signs of interest rate dropping. There may be some stressed homeowners contemplating folding but if the home prices are declining in that location it will be painful or impossible to sell.

I saw a house listed for sale near Portland, OR metro. It was asking $1.65M in Feb., kept reducing to $1.4M, still on the market. It was sold for 900k in 2019 and sold again in June 2022 for 1.5M (almost 250k over asking prize). For some reason they need to sell 7 months after purchase and now it’s going to be at a loss.

It’s evident how unpredictable the housing market can be, especially with fluctuating interest rates. The Portland example underscores the risks of trying to time the market. Buyers should prioritize personal financial stability over market speculations and always be prepared for unforeseen shifts. Making well-informed decisions is key in such volatile environments.