How do you lose 47% on 30-year Treasuries? Buy at auction in Aug 2020. Or you can carry them at purchase price and hide the “unrealized loss” in the footnotes.

By Wolf Richter for WOLF STREET.

“Unrealized losses” on securities triggered the bank panic earlier this year, in that uninsured depositors with millions or billions of dollars at these banks suddenly started looking at the footnote on page 125 of Silicon Valley Bank’s Q4 2022 quarterly report, and saw this thing about “unrealized losses,” and got scared and yanked their money out, electronically, all together in no time, engineering the fastest bank runs in history that took down Silvergate Capital, Silicon Valley Bank, Signature Bank, and First Republic. And this formerly boring line item hidden deep down in the footnotes was transformed into a hotly important indicator of where the entire financial system stands.

“Unrealized losses” are paper losses on securities that banks hold, but via a quirk in bank regulations, they don’t have to mark them to market value, but can carry them at purchase price.

On one level, it makes sense.

The closer the bonds get to the maturity date, the closer the market value gets to face value, and the unrealized losses vanish, and on the day the bonds mature, the banks get paid face value, and there are no losses, and everyone smiles.

On another level, the bank collapses.

During a bank run, when scared uninsured depositors yank their money out, banks have to sell assets to cover their cash outflows from the run. But now the banks only get market value for those securities – if that, during a fire sale – and not their original purchase price, and they have huge losses on those sales that vaporize their capital. No cash, no capital, no problem? Big problem.

That’s why we now have to pay attention to unrealized losses in the banking system.

Banks can hedge against rising interest rates, but some banks prefer to collapse.

Hedges against the risk of rising interest rates, such as interest-rate swaps, can be costly, and some banks don’t hedge, or don’t hedge enough, because executives prefer to show a little extra income to prop up the banks falling stock price and to fatten up their compensation.

SVB terminated or let expire nearly all its remaining interest-rate hedges in 2022, to where by the end of 2022, they were nearly all gone, and three months later it collapsed.

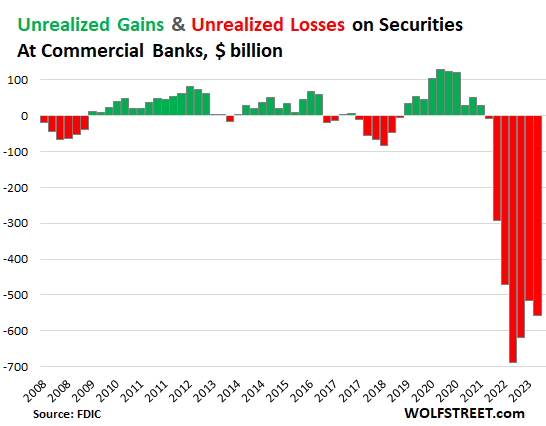

Where are banks now? Unrealized losses rise by 8% to $558 billion.

The balance of unrealized losses on securities – mostly Treasury securities and government-guaranteed mortgage-backed securities – at FDIC-insured commercial banks rose by $43 billion, or by 8%, to $558 billion in Q2, after two months of declines, according to the FDIC’s bank data on Thursday.

This $558 billion is the cumulative loss balance over time on all securities. The balance rose because longer-term yields rose in Q2: The 10-year Treasury yield rose to 3.84% on June 30, from 3.47% on March 31, and so bond prices fell over the period.

In the free-money periods, when yields fell and bond prices rose, banks had “unrealized gains” (green). And in the periods when yields rose and prices fell, banks had “unrealized losses” (red).

These unrealized losses of $558 billion were spread over two categories of bank accounting treatments:

- Unrealized losses on held-to-maturity (HTM) securities: $309.6 billion

- Unrealized losses on available-for-sale (AFS) securities: $248.9 billion.

The balance of unrealized losses is down by $131 billion from the peak in Q3 2022, in part because three banks with big unrealized losses collapsed, and their balance sheets vanished from the system, with losses getting transferred to the FDIC.

Already gotten worse in Q3 so far.

Thing is, today, the 10-year yield closed at 4.27%, and if it’s still at 4.27% at the end of September, it would be another 43 basis points higher than at the end of Q2, and the balance of unrealized losses will be higher yet again.

Bad-case scenarios: How big can the losses be on specific bonds?

A bank that bought $1 million of 10-year T-notes at the Treasury auction on August 12, 2020, at the very tippy-top of the 40-year bond bull market, ended up with a security that paid a coupon interest rate of 0.625% per year. Today, this security has seven more years to run before maturity, and so trades like a 7-year Treasury security, and the 7-year yield today in the market is 4.35%.

So how much is a security worth today with a coupon of 0.625% per year and with seven years to maturity, when the equivalent market yield is 4.35%?

Roughly, that $1,000,000 in 10-year T-notes might be worth $778,000 in the market today – thank you, bond-price calculator. Results may vary.

The bank that purchased this security at auction and carries it under HTM accounting rules on its books would show no loss on its income statement, and its earnings-per-share would be just fine, and it would pay its executives big-fat bonuses.

But on its balance sheet way down somewhere in the footnotes, it would show an “unrealized loss” of roughly $222,000, or roughly 22.2% of the purchase price.

And that $1,000,000 in 30-year T-bonds that a hapless bank bought at auction in August 2020, with a coupon of 1.375% might sell for about $529,000 today, for a loss of about $471,000, or 47%. That’s about the worst-case scenario, the punishment for buying at the peak of the 40-year bond bull market.

Uninsured depositors figured out where to look.

SVB, in its final quarterly report as a living bank for Q4 2022, in a footnote on page 125, disclosed unrealized losses of $15.2 billion on its HTM securities and unrealized losses of $2.5 billion on its AFS securities, for a total of $17.7 billion in unrealized losses.

The $15.2 billion in unrealized losses on its HTM bonds amounted to 16.7% of the carrying value of $91 billion of its HTM bonds.

Once uninsured depositors, some with billions on deposit at the bank, figured out where to look, they started yanking their money out, and SVB collapsed.

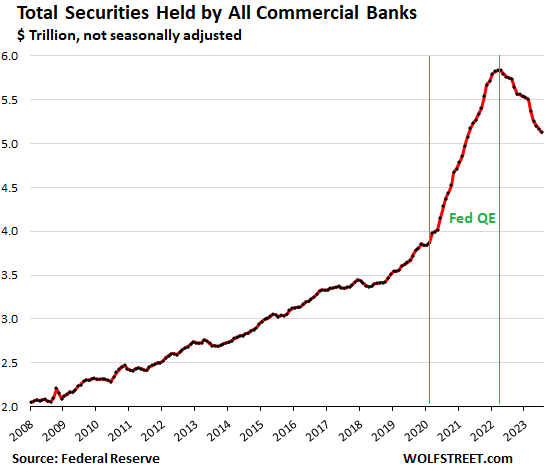

The declining pile of securities held by commercial banks.

The total balance of securities held by all commercial banks has been declining for 16 months in a row to $5.13 trillion in July, down by 10% or by $705 billion, from the peak in March 2022 ($5.84 trillion) when the Fed’s rate hikes began.

Several factors make up the $705 billion decline:

- Securities of the collapsed banks that the FDIC sold to the market (not to other banks) are no longer part of this.

- Banks have written down AFS securities to market value.

- Banks may have sold some securities.

The $558 billion in unrealized losses amount to about 11% of the total securities held by banks.

The chart also shows how banks gorged on these low-yielding securities at the worst possible time just before, during, and after the peak of the 40-year bond bull market – on the ancient strategy of buying high and selling low – as a result of the reckless money-printing by the Fed starting in March 2020 through early 2022. “Free money is a virus that turns investors’ brains to mush” is a well-documented and generally undisputed scientific fact I have been pointing out for a while now.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

0% bonds are trash. Did the banks choose to buy them? Wasn’t it mandated during the stimulus period?

No, they bought willingly. They thought rates would go negative as in Europe.

gee even hedgies knew to use derivatives to minimize potential losses

no sympathy

yeah and then they compounded those foolish decisions going into 2022 and 2023 by buying into the pivot-monger Kool-Aid from all the squawkers deluding themselves into thinking that the Fed would just clueless ignore the worst inflation in 4 decades and pivot right back to easy money. Consensual hallucination like Wolf likes to say. And these idiots are still peddling the pivot-monger nonsense now even though JPow has explicitly warned that US inflation is heating back up again and the Fed is going to have to not only continue but get tougher in monetary policy tightening. Even the MMT evangelists admitted that the “create free money” charade could go on only long as inflation stayed low or nonexistent. Now we have ongoing sticky inflation on top of earlier massive inflation with incomes in the US not keeping up, and these pivot-mongers keep peddling this same line.

Don’t worry, there are:

“but via a quirk in bank regulations”

for everything, or they can dream up a new one. OR print more cash to cover.

Sleep well.

Lawful versus legal.

There is a huge difference and that underlies much of the rot.

A variant admitted by some politicians:

It isn’t what is illegal that is the problem.

It is what is legal.

There are lessons for all within those short statements. Those splitting hairs and seeking constant advantage without regard to consequences will cause themselves and many others harm.

This is mostly a PSA about a brilliant indictment by John Hussman of the deranged Fed policies of the last 2 decades and the dramatic consequences to expect – article titled “Central Bankers Wandering in the Woods” (search it online)

That should be prerequisite reading for a serious discussion in this forum.

Im so confused by this. T-bills are liquid. You would have thought they would offloaded the t-bills after each rate hike for some new ones. Regardless of the maturity date, they could still get out of them. I suppose they thought we would return to zero interest rates? Dumb.

@Tony

That’s the beauty of the market, for every seller there is a buyer. When prices go down and yield goes up, some buyers believe they still can make money at some point in the future.

if they sold bills after a rate hike they would have locked in smaller losses and then if they bought again they would have lost on those bills. they needed to hedge the interest rate risk.

if they had bought bills that were really short term, they could have just held to maturity and not lost anything, but once again, they were trying to get an incremental yield to juice profits.

bottom line, they should have believed that the Fed was going to raise interest rates.

gametv, in order to hedge you need counterparties. Where are those going to be found if “everybody” knows that the Fed is raising rates?

Are you talking about 0% coupon bonds or bonds with an actual effective yield of 0%?

3 month and 6 month T-bills are zero coupon. You buy them at some discount price, which varies from week to week, and then you always get $100 back when they mature. There is no periodic interest to speak of. For example, the 6-month auction for this week closed at $97.32, which gives you an effective yield of ~5.5% with no interest payments.

I don’t know who would have bought bonds with actual yield of 0% in USD when most if not all bonds priced in USD had at least some positive yield, however tiny.

Real yield was far more negative than what existed during the “bond bull market” during QE.

He’s not talking about 0% literally, but 2 and 10 year treasuries and such that were almost zero.

One of the reasons to buy zero/negative yield bonds is because they are discounted. That is coupon = 0%, value of the bond = 100%, discounted price = 85%. At this point you make a profit even if inflation is between 4% & 5%, let alone when inflation is between 0% & 2%.

Currency hedging. This one depends on the relative difference between short term interest rates (interest rate in the country with the negative coupon bond has to be lower then the interest rate in the country with the positive coupon bond). That makes it possible to have an effective coupon rate of 1% if the coupon for the German bond is -.5% and the coupon for an equivalent US bond is 0.5%.

Government bonds are some of the safest bonds to buy. Turning negative coupon rents into cost to store money. An example of this happening is when there is uncertainty in the stock market and investors decide to temporarily park their money in a safe spot.

Some of the bigger investors have no choice, there is a list of what they must buy (granted this is usually not so inflexible that when Germany issues a bond with a -0.5% coupon that they can’t buy an equivalent amount of US treasuries/bonds with a positive coupon).

Tulip bulbs. That is this bond might be negative but we can make a profit out of it if the next bonds issued are deeper into negative territory and we can sell before we have to pay the coupon.

In the EU and Japan an added reason was that negative yield bonds, if the buyer was a bank, cost the buyer less then stashing the same amount of cash at their respective central banks.

Deflation, if the deflation causes a greater contraction then the negative coupon of a bond the bond is a safe way to store value.

There are probably a few more reasons to buy zero or negative yield bonds.

I am confused .

How do you make money when buying bonds with a negative yield unless there is actual deflation ( lower prices of consumer goods ) over the lifetime of the bond .

Nice explanation, Who Cares, of the rationale for holding these securities when it made some sense. Of course now it seems like idiocy.

Intriguing how you use the Tulip Bulb analogy. It brings up a terrifying thought, another “unprecedented” financial catastrophe that is quite possible.

If you had any kind of momentum towards negative interest rates, especially in long dated bonds, starting from 0% and heading to -1%, -2%, etc, the real money would be made in buying and holding bonds, selling them later (“flipping”) for massive profit.

Just imagine if that became the next bubble and the economic horrors it would inflict. Savers would not only be hit with massive inflation but also a destruction of the nominal balance of their savings, as Wall Street feasts on their corpses.

Unfortunately, it’s not too out of reach for this to actually happen, given the shit show we’ve seen the last 3 years.

“One of the reasons to buy zero/negative yield bonds is because they are discounted. That is coupon = 0%, value of the bond = 100%, discounted price = 85%. At this point you make a profit even if inflation is between 4% & 5%, let alone when inflation is between 0% & 2%.”

You’re confusing zero coupon bonds (where the interest is reflected in a discounted price of the bond) with zero/negative yield bonds. If a bond has a negative yield, the price will actually be more than the par value of the bond. As a result, you will get less money back when the bond matures than you paid for the bond. If the bond has a discounted price, by definition it can’t have a zero/negative yield. The difference between the discounted price of the bond and its par value is the interest.

Yes, Yes, of course, incoming cash has to be invested ! There is no discretion for a professional money manager but to purchase what is available. After 15 years of zirp, it became normal.

*on the ancient strategy of buying high and selling low*

Wow!

Unfortunately, this is the strategy of the mass of people. It’s valid for all assets. Therefore, there are already many investors who are and others who will be under water.

Which begs the question, who cares ? Who cares if the morons lose their nest egg betting in the financial markets ?

Maybe some empathy is appropriate if one were to believe that the financial markets are rigged and not appropriate for Joe Lunchbucket to invest his hard earned cash with, now that it is about to lose value.

That’s the real question here isn’t it. Why on earth would a bank buy a bond with 0 interest when there are other options available. Answer, they are prestine collateral and can be used for more than just collecting interest.

I mentioned many times that I could not believe anyone would buy any treasury at zero or even 1% as one may as well keep the cash under the mattress.

Damn good article!!!

Fractional Banking always was such an easy and fun way to get rich. And looks like it will even finally trash those interfering government pests at the same time! Hell, even Central Banking will vanish, (with the government) and the whole stupid “sorta democratic” construct will FINALLY fit in that gold bathtub where it can be drowned and reshaped however our private equity organization (party?) and IT’s country sees fit. (Have to keep the military and their associated chummy organizations REAL happy, though)

Winner take all, just the way ALL the winners like it…..and all the BS’d “rugged individuals” can hardly wait for….well…..whatever……they don’t know, but it’ll be better for sure….like it WAS in each of their “mush minds”.

Little do they know that the most “rugged” individuals currently……are…….

The homeless!!!

FN media (all of it) WORKS!

SHOWTIME!

They might still play ‘red and Blue”…(tradition?)….but only .as long as it works for advertising purposes……..but once too few eyeballs are delivered, then that game show is over.

Wolf, what is $558B as a percentage of all assets held by banks?

What is $558B as a percentage of total bank deposits held?

What is the average duration of these bonds?

What is $558B as percentage of total market-cap of these banks?

That would help understand the fragility or lack-of of the banking system when it comes to these bonds

The important question is what percentage is the $588 billion of total bank capital. So:

And this is the FDIC’s chart of average remaining maturities. In Q2, of the total assets, 8.7% had 3-5 years; 15.1% had 5-15 years, and 14.5% had over 15 years in remaining maturities:

Wolf, I think you’re double counting the losses on the AFS assets in these calculations. I mean, you can do whatever you want of course, it’s your site etc.

These AFS losses should already be reflected on the banks’ balance sheets (asset valuations, and thus equity and Tier 1 capital) whereas the HTM assets are carried at cost.

The numerator should be the 309.6bn in unrealized losses on the HTM securities.

Alternatively, you can add the AFS losses to the denominator to avoid such double counting. Maybe you did that already, I don’t know.

Valid comment. Fully agree.

Wolf/interested onlooker, could you kindly expand on the “double counting” comment, specifically why the AFS unrealized loss should not be counted as part of total unrealized losses? Thanks!

Peeping Tom,

Phogetaboutit’s comment was about my calculations in my comment in reply to Narasimhan’s comment above where I said:

Unrealized losses on AFS securities ($248.9 billion) are part of the total unrealized losses ($588 billion), but they have already been subtracted from regulatory capital calculations. That’s what Phogetaboutit correctly said. The unrealized losses on HTM securities ($309.6 billion) ARE counted as part of regulatory capital. So in my percentages in my comment, I “counted” the AFS losses when I shouldn’t have counted them because they’d already been subtracted from regulator capital, and I should have just used the $309.6 billion HTM unrealized losses.

So I should have said that “unrealized losses on HTM securities” amount to 13.8% of total equity capital and 14.7% of Tier 1 capital.

Huge depression similar to 2029 I maybe off 3 years up or down but it’s a 70% likely and maybe not global but going to be a shocking experience

>>>”hotly important indicator of where the entire financial system stands.”<<<

Wolf,

Those are your words not mine… Now factor in the collapse of office building values, (that you have documented here) which is a significant portion of all real estate loans by the banking industry….which I don't think is anywhere close to being accurately and fully reserved on the books of the banking system …

This actual situation seems to me to negate your contention that I was "pulling in a Black Swan *** by its feathers", as a cause of the next recession.

I had a friend who made a lot of money off The Big Short trade who told about a year ahead of the financial collapse that it was coming and the banks were in real trouble because of their exposure to subprime mortgages.

I highly suggest you connect the dots on this current banking system situation, because it is similar to what happened back in 2008, which is why a recession is lot closer than you realize.

*** If someone as informed as you cannot see the potential for this banking system to melt down then that is the clear definition of a Black swan

“Now factor in the collapse of office building values, (that you have documented here) which is a significant portion of all real estate loans by the banking industry…”

Not a single office building loan that generated big losses that I ran across and discussed here was held by a bank. Every single one of them was either securitized into CMBS and CLOs and sold to investors or was held by mortgage REITs and PE firms. Same thing with mall loans, which I have been discussing here since 2016, because mall debt has been in horrible shape since then, far worse than office debt now, and it wasn’t a big deal for banks because they’d sold their riskiest mall mortgages to investors.

Which led me to the theory – which I have explained here a few times — that the banks sold off their riskiest CRE mortgages and only kept the less risky stuff on their books, and that investors are losing their shirts, not banks. And that has been the case so far.

How could you have missed that??? YOU need to connect the actual dots, not the imaginary dots in your brain, and quit dragging black swans around by their feathers.

We already have a black swan, and it’s INFLATION, the worst in 40 years, and it’s not going away, and it has changed everything, including central bank actions. So there is our black swan, and it’s real and it’s here, but you refuse to look at it because you want to drag a prettier black swan into here by its feathers?

Yes, but the continuation of this Goldilocks economy requires the collapse of the asset bubbles that the Fed blew.

I’m not sure if that qualifies as a black swan or common sense.

The Fed has to reduce it’s balance sheet faster. They continue too encourage speculators over investors.

Wolf:

Can you make an attempt to calculate “unrealized losses” on loans due solely to higher rates, not deteriorating credit quality. Your chart shows 42% of bank assets > 3 years. 42% it $20T is $8.4T. The bonds were $5T. If these $3.4T of term loans averaged a duration of 5 years then I calculate , with rates up 4.5% as follows. $3.4T volume x 4.5% rate drop x 5 year duration =$750 B unrealized losses due to rate only on loans?

It’s funny, When I hold a CD in a traditional savings account, it shows the book value. When I hold a brokered CD in an investment account, then that thing actually show daily market value and “unrealized losses” .

Cash flow problems, plus the combined psychological effect of being underwater, realizing a mistake overpaying for something in the past, and having to endure years of low expected returns is simply too powerful. That the way to quickly get out of “unrealized losses” is to just rip the band-aid and turn them into “realized losses.”

If the cash flow problem belongs to somebody else, then….

those statistics of 26 and 28% of capital are averages and it is far worse at some banks and far better at others. this is only the losses on bonds. it doesnt include potential losses on CRE or loan losses if the economy goes south.

it seems that there needs to be major reform of the banking system.

“it seems that there needs to be major reform of the banking system.”

You jest? The Club will save it’s friends even if all the women and children drown.

.ps. Thanks for this, Wolf.

Jeffery Snider has a term for where this phenomena would fall into broadly: “Footnote Dollars”

sad to say when leverage at bank is 10:1

this represent 26% of their reserves

tic toc goes bankster clock

Just spitballin but what if JPow cuts to Zero and then the banks can sell all their bonds and JPow can just hike back to 5.5%.

Crisis averted. You can thank me later.

You clearly don’t understand banks. If JPow cuts to 0% and bond prices (bong prices?) spike, the banks wouldn’t sell them; they’d buy even more, just like they did in 2020-2022. Banks figured out how to time the market 🤣

I don’t follow interest rates much since one would have to be in market for said products

bankster told me today 30 year is at 8%

wow-so I can then carry back at 9%

Heh, heh.

So, why couldn’t JPowell hold a secret meeting with the top dogs of the TBTF major banks at Jekyll Island (1910 anyone?) and tell the bankers, “here’s what I’m going to do. I’m going to save your butts; I’ll cut rates to 0% for a month or so, giving you all a chance to sell your bonds. Then I’m going to start jacking up rates again back to 5+%.

As Carlin said, “It’s a big club, and you ain’t in it.”

The Fed controls short term interest rates not long terms rates. So setting the short rate to 0% would not cause long term rates to go to 0%.

Of course the Fed could drive long terms rates back to 0% or below via massive QE. Stay tuned kids…don’t touch that dial!

“and bond prices (bong prices?)”

lol, concisely stated and so true in the implication

Even if the banks hold the treasuries until maturity and get all the bond face value back, what would the inflation adjusted maturity value be after 30 years of inflation and receiving a less than inflation interest rate from the bond?

It certainly appears the bonds are losers whether they are held or sold.

Yep hilarious! Forever QE!

Sell to whom? Social Security Fund or 401ks?

For every one of the US Treasuries there is a buyer, and that included all $33 TRILLION of them which will soon be $40 TRILLION and about 50% mature each year and have to be paid in full to the owners and then replaced through new issuance.

Is it not correct that With the average financial recommendation of 60 percent stocks and 40 percent bonds, financial money managers, pension funds, insurance companies , etc. must have been purchasing them also.

Insurance companies that issue fixed annuities might buy such securities at the right price. Matching assets and liabilities cancels the impact of rising rates as the value of both assets and liabilities would fall together.

Indeed. Insurance companies had to buy a shitload of zirp securities too insure the future cash outflow to pensioners.

We still don’t understand the extent of the incompetence of the Fed these past 100 years.

Banks are not allowed to fail via BTFP, real estate is not allowed to fall via enormous MBS holdings, government debt will certainly be rescued via QE, CRE will be backdoor bailed out, pensions will be bailed out, the stock market hasn’t corrected in almost 15 years. How is this not Socialism? Where is the howling? Have the plebs figured out that they can vote themselves more money and it’s all going to work out – to the moon?

“Banks are not allowed to fail via BTFP…”

They’re allowed to fail just fine. Three of the bigger ones already did. The BTFP is minuscule, $107 billion for 4,000 banks with $22.8 trillion with a T in assets.

BTFP is targeted YCC.

BTFP is going to grow more than what the Fed has allocated as rates continue to go up.

Didnt they insure deposits in excess of the FDIC amount for many account holders in said “bank failures”

Would you let all the criminals out the front door in broad daylight for all to see, or out the back under cover of darkness?

First Republic, SVB et al, have already been taken out the back door and shot…

So between this and the commercial MBS failures, do you expect more regional bank failures this year?

1. I can’t even imagine people having more than 250,000 in their accounts. I have to work hard to keep this much money in my account. Hence, no worries.

2. Ok, if there might be a bank run or general panic. This issue can be easily solved.

3. Banks can go to FDIC. Give all their bonds (T-notes)

4. FDIC will go to FED’s

5. FEDs print money and give to FDIC and keep the bonds and redeem them on their maturity date.

6. FDIC pays all the little people.

Golly, it’s the magic MMT unicorn that poops inflation.

lol just loving the colorful monetary policy metaphors tonight. And true too, when the “adults in charge” abdicate their responsibility to preserve American’s buying power to this level, they might as well of been eating magic mushrooms the whole time. In fact they probably could’ve come up with better policies while high than what they actually did in the last 3 years, with such genius ideas like QE with mass MBS purchases when the US housing bubble was already turning 1 BR starter homes in crime ridden neighborhoods into luxury items.

No quirks here, it was deliberate.

Obviously not.

“All US Treasuries are ALWAYS SOLD TO WILLING INVESTORS and there has never been a case where that isn’t true.”

Obviously deliberate.

$700 billions is but a key stroke on Fed’s balance sheet.

I have seen figures that the Fed’s balance sheet for May 2023 was $540billions in the red on her treasuries and MBS.

If true, and considering Fed owns about 20% of the total market, this would mean that true losses by the remaining banks and institutions who own the other 80% would be over $2trillion, not?

NO.

The Fed controls a helluva lot more than 20% which is an absurd assertion. What would be the price of assets if the Fed wasn’t controlling them.

About 50% lower.

“ and the 7-year yield today in the market is 4.35%”

Where do I go to see the current “yield today in the market?”

Google “7 year Treasury Rate”.

Almost everything in the fixed income market is priced at a spread to “riskless” Treasury rates of same/similar maturity.

To the U.S. Treasury web page titled “Daily Treasury Par Yield Curve Rates.”

Google: US treasury yield 7 years

Schwab is quoting a Treasury maturing on August 31, 2030 priced to yield 4.348%. So real people can get that rate.

Hmm, why would anyone buy a 7 year treasury at 4.348% when the FFR is 5.25-5.5%?

The bet is that two years from now, the Fed’s policy rates are 2%, but then you’ve got another 5 years of 4.35%, while T-bills yield 2%. So that would turn that 7-year into a good deal.

If the Fed’s policy rates are still 5.5% two, three, and four years from now, the bet didn’t work out, but you could have done worse with some other bet.

Wolf, can you recommend a short book that explains how macroeconomic forces influence bond yields? The bond market is wild these days, I don’t understand it.

The bond market has turned into a casino. Once you understand that, you’re well on our way to understanding the bond market.

Wherein our esteemed host channels his inner Keynes: “When the capital development of a country becomes a by-product of the activities of a casino, the job is likely to be ill-done.”

Fidelity has a bond site and I suspect Yahoo does as well

I like this site for 1 month all the way thru 30 year treasuries:

https://www.barchart.com/economy/interest-rates

First chart in the article shows how buying these low rate bonds were picking up pennies in front of the steamroller. The tiny upside available (unless they truly believed rates would go deeply negative) was way outweighed by the risk of rates rising.

Well, SOMEBODY had to buy the nearly $33 trillion in US Treasuries. And many more TRILLIONS of net new issuance are in the works along with repaying around $15 trillion of year at maturity and replacing those with around $15 trillion a year with newly issued US Treasuries.

Basically, the Dude abides. Plenty of inside players knew about the insanity/stupidity, but felt they *had* to play along.

Imagine you were a bank…the money keeps coming in/rolling over and it has to go *someplace* (that’s your business…earning a spread on lendable funds).

There are only so many stupid, doomed CRE loans even *you* can stomach (*another* mattress store?!!)…so where does the rest of the depositors’ money go?

The “safest” place?

The perpetually ZIRP’ed Treasuries of our master-counterfeiting Federal government.

Sure, you remember from Econ 201 that increasing market rates destroy the value of older, lower yielding bonds…but the G has you cornered in the killing pen. Essentially everything in fixed income is priced at a spread to Treasuries…but those are crappy, crappy (crappy) risks with a tiny risk premium anyway.

(Junk bonds issued by paint-huffing hypesters with a brother-in-law at Goldman were costing/paying under 4% at one point, with loan “covenants” making actual repayment sorta optional…). Sheesh – I got 5% on my “Child’s Savings Account” of $37.89 in 1975…

But that’s what happens when the G counterfeits enough “money” (maney, mony, miney, myney, mangy, monkey?) to force interest rates from a natural 8%+ (likely future default incorporated…) to under 3% (the MMT special).

The entire lending ecosystem gets badly, badly distorted. And there is always a price to pay, if not today then tomorrow.

So you, Bank X, buy Treasuries yielding 3%, pay depositors little more than a flirty smile from your tellers, and plan defenestration for when rates inevitably rise.

This was all baked in the poisoned cake once the Fed committed to ZIRP for any length of time.

Yes, there is a price to pay for ZIRP, but who will pay it?

The people that benefited from ZIRP are the assets holders – the bondholders, the homeowners, the stockholders. Now that the gig is up, the Fed has chosen to protect those asset holders and punish people that had nothing to do with the problem – renters, younger generations of workers, the asset poor.

Rather than let asset prices adjust to normal levels, the Fed is supporting asset prices and handing the hapless class a “bag” of inflation. You’d expect nothing else from a Fed leadership that has catered to a wealthy class of asset holders for decades, via pursuit of a “wealth effect”.

Bobber, I believe you are correct. Central banks are, by design, aristocratic institutions inimical to labour.

The bigger balance that is neglected is the unrealized fmv losses on loans. That is also disclosed in the footnotes. That is simply interest rate risk, not tagging on any credit risk.

Perhaps the banks believed Ben Bernanke when he dais he does not expect the federal funds rate to rise back to its long term average of around 4% in his lifetime.

Sarcasm off.

The Federal Reserve said it failed Silicon Valley Bank (SVB) in its oversight. Now here we are with about $600 billion in unrealized loses, about twice what the Fed added with SVB & company. This Federal Reserve bond ballast is limiting Bank liquidity, lending, and perhaps worse the stock price. So, why not exchange that old low interest (loss) paper for new high interest bonds. Since the Fed rolls the bonds off at maturity, there isn’t any loss realized at all ever. Finally, since SVB was considered “systemic” the Fed has to bail out all these banks anyway.

I don’t feel sorry for these banks that made these stupid investments. Let them lose their shirts and even go under. No bailouts, or bail ins. Let the stockholders take the losses, as well as all the uninsured depositors who put their money in these banks.

How is investing in US government Treasuries a stupid investment?

Is that a serious question? I’m happy to explain if it is.

All US Treasuries are ALWAYS SOLD TO WILLING INVESTORS and there has never been a case where that isn’t true.

SCBD-

What if the largest buyer of the bonds is a government agency charged by congress with managing the unemployment rate??

The annual remittance of earnings to the Treasury, combined with the full employment mandate, tie the Fed to the US Treasury and so to the taxpayer.

As a taxpayer, I am emphatically NOT a “willing buyer” of US Treasuries. I’ve been coerced.

Rate suppression by the Fed is/was unethical and coercive, IMHO

Time to re-think the goals and methods of central banking.

SoCalBeachDude,

“All US Treasuries are ALWAYS SOLD TO WILLING INVESTORS and there has never been a case where that isn’t true.”

I guess you were serious. How does your reply refute purchasing US Treasuries under certain circumstances can be stupid? Are you suggesting investors never make stupid investments?

You need to read Wolf’s article again (or maybe for the first time) and try to understand it. Pay close attention to the section: “Bad-case scenarios: How big can the losses be on specific bonds?” When banks, or any investor, buys 10-yr bonds paying .625%, they have virtually no upside in terms of yields going lower, and a very small coupon if inflation and/or yields rise. To me, an investment is stupid if it has very little upside and big downside risks. YMMV.

All US Treasures – all $33+ TRILLION of them – will always be held by buyers and must be held by buyers by definition and to fund the US government whether you ‘think’ it is a ‘good investment’ or not and that will always be the case regardless of any interest rate percentages paid on those investments.

Lending the Treasury your money for less than .7 % return.

Comic relief from Canada: an old finance guy in the Globe said the Gov screwed up not borrowing more when rates were so low. He was funny: ‘shove the bonds out till the market chokes on them, till you see the whites of their eyes’

OK for gov. but its gain is someone’s loss when rates go up so far so fast.

There are three types of risks in bonds

1. Credit risk or risk of default . The US government has very low credit risk. Junk bonds have much higher credit risk , but current junk bond rates are not reflecting their increased credit risk vs Treasuries

2. Interest rate risk. Dependent on a number of factors-maturity , coupon and the price paid among them .

Those who bought Treasuries bonds 2 years ago had little credit risk , but high amount of interest rate risk

3. Real return risk . To determine this risk , one needs to have an idea of inflation rates over the course of the bond

SCBD-

“ How is investing in US government Treasuries a stupid investment? “

Taking short term deposits and investing in long-dated US Treasuries is stupid, if/when it leads to loss of depositor confidence.

While it works, it’s bonus time for management.

Thats the way fractional reserve banking works.

(Disregard this message if you were being sarcastic.)

You appear to completely fail to comprehend how US Treasuries work and how the US federal government funds itself. The yield or return to investors is absolutely irrelevant and the yield will continue moving higher as more and more US Treasuries are issued into the marketplace. That, of course, benefits new investors with higher yields. That is also the consequences of yields that were ridiculously low but were driven there by exuberant speculators who wanted to (and benefited from) US Treasury prices being excessively high as bonds (US Treasury) prices and yields have an inverse relationship. That’s simply how the bond markets work, and that has nothing whatsoever to do with ‘fractional reserve banking’ which merely means that banks must hold around 10% in reserves on all deposits in banks.

SCBD-

You asked: “How is investing in US government Treasuries a stupid investment?”

I inferred from your question that you were asking form the bond-buyer’s perspective, not from the bond-issuer’s perspective.

Yields were “ridiculously low” due largely to unprecedented Fed intervention.

Reliance on continued price support from a fickle and political institution that’s jointly operated by congress and the banking industry seems to me to be the very epitome of “stupid” investing!

Fractional reserve banking magnifies the potential for trouble by adding layers of leverage, magnifying the policy errors that the eggheads invariably commit.

How the Treasury funds its debt is secondary to your question of investor acumen.

Stupid is as stupid does, I guess.

Finally, to your point of my failure to understand US Treasury market, I am self-admittedly mystified and stymied by what has occurred over the last 50 years. I remain steadfast in my desire to learn. I enjoy your comments and will continue to read them with interest and, sometimes, amusement…

Yes! A good banking crisis will finally pop the everything bubbles and purge the disgorgement of 10 years of ZIRP and QE.

That’s the twisted thinking of lots of people, including our favorite recession-mongers here, LOL

Stupid bankers, much dumber regulators. Lower for longer! Yeah, until you get inflation and lot of malinvestment. Government complicity at taxpayer expense.

Except for GSIPs, bank examiners only need to understand credit and interest rate risk. Stupid accounting rules aside, the examiner must account for fixed rate interest rate exposure in the banking book regardless of whether they derive from loans, e.g. fixed rate term loans or mortgages, or from fixed rate securities.

Even without a bank run, you’ll bleed $$’s due to higher funding costs crushing your NIM.

I was a bank examiner for over twenty years before I retired. My experience is that most examiners know nothing about risk. Too much focus on CRA, loan tying, money, bank secrecy, etc.

Anecdote from the crash of twenty nine:

We had a hardware store. When the market crashed my dad said: good, about time those leeches got it in the neck. Six months later we lost the store.

Nick Kelly,

Thank you. While an anecdote, this is the best response to the burn it all down crowd I have heard yet. They know not what they are cheering for.

Yeah, I don’t really understand why anyone would wish for a calamity — our economic well being is mutual.

I feared that the interest rate hikes would cause a recession, but that doesn’t mean that I wanted one. I’ve also come to appreciate that the simplistic story sold to me about the effects of interest rates don’t take into account the stimulative effects of the interest income channel, and lately I’m beginning to think that the US economy cannot be in recession when the US Federal government is running such large deficits.

Everything is more complicated than anyone’s model can possibly hold and there’s always more to learn. That’s why I keep coming back here — empirical data is useful.

Exactly. You know how I say that I blame the people for bidding up the price of housing over the past few years because they, collectively, have zero self control?

The same applies to banks and investment funds. Had private entities said “I refuse to buy 30 year treasuries yielding 1.2% or 10 year treasuries yielding 0.55%. I don’t care what the Fed does,” the whole market would have adjusted. This is what people mean when they say “bond vigilantes.”

But idiots were all over themselves to buy this stuff at crap yields figuring they could front run the Fed. So the same rule applies to institutions. Had you not bid up the price of crap, the market wouldn’t have gotten as distorted as it did.

Indeed.

I find it amazing they bought such low yields. I passed on so many of these bonds – Uber, Apple, you name it- I am not lending long term for 1-2%!

I have some sympathy for big corporations that need to have more than $250,000 (insured amount) in an account just for payroll.

So I would love to see FDIC cover all accounts up to $250,000 plus short term account that offered zero percent interest (or some nominally small amount). This would cover corporate accounts that were just for liquidity (like payroll) who were not chasing yield.

‘ well-documented and generally undisputed scientific fact…’

Argh, No, come back from the clouds of scientific fallacy!!

Your point belongs more on the sure ground of uncomfortable reality!

If SVB had paid a market interest rate to its high net-worth customers, they would have stayed.

So now the Fed cannot raise rates to fight inflation for fear that banks will collapse further or have they been given enough time to prepare?

No. And most huge banks still only pay around 0.02% on deposits including my favorite bank, JPMC, which is extremely stable and where I keep most of my funds.

If you’re still getting only 0.02% at JPMC, I guess you deserve what you get?

That’s the choice of all JPMC customers which is why it is now the biggest bank in the United States.

I guess I invert it. Why is anyone keeping money they expect a decent return on in a bank?

To me, banks are a place to keep extremely short term money that I expect to use in the next few weeks. Anything I plan on investing I move into an investment accout.

If you keep under $250k in each account, who cares if it’s stable? I don’t.

I’m getting between 5-5.26% on all of mine. No reason to be getting 0.02% on anything.

Jpmc = thieves. No different from any of the others. They are not charities. Caveat emptor.

JPMC is the biggest and best large bank in the United States and provided excellent Private Client Banking services.

In the last 6 months , JPM has issued $ hundreds of millions of dollars of callable CDs paying 5.50% and above. Other large banks have also done so.

If you insist on keeping your money at JPM , why not put your money in these CDs. Worst case scenario , your CDs are called and you will be in the same position as you currently are

SoCal, you need to think of two words:

Treasury Direct.

Open an account with them. You can link it to your 0% checking account, and buy Treasuries with durations anywhere from 1 month to 30 years.

When you buy a Treasury, it’s automatically taken out of your account. When it matures, it automatically goes back in, unless you’ve chosen to automatically roll it over. Simple and convenient.

If socal is using private banking at jpm he has probably heard of treasury direct

try and get someone on the phone at T dir

Why would anyone want to bother with that nonsense?

SoCalBeachDude,

If you’re happy with the 0.01% you’re getting at JPMC, I think you should keep all your money there. Do what makes you happy. Why bother with 5.5% that’s exempt from California income taxes, if you can get 0.01% and be happy? Happiness is finally what matters the most in life, and you’ve found the path to it, so go for it!

Wolf,

LOL! Although, .01% is effectively exempt from both State AND Federal taxes. ;-)

I think most Money Market Funds are safer than banks when over the FDIC limits due to diversification. It takes a lot to break the buck. Anyone who is reading Wolf’s articles should have a good idea when it’s time to move to safer waters.

I like PCOXX with a 7-day yield of 5.38% (annualized that’s 5.53%) — pretty good considering it’s liquid in one day. Higher yield than most CDs and Treasuries. (It can be bought at eTrade–$500k minimum).

A friend of mine just bought a $100,000 JPMC CD paying about 5.5%. Why are you getting less?

SCBD,

JPMC is really sticking it to you. I just picked up one of their CDs paying 5.7%…What’s up with that?

Recent crap from a September 7, 2023 FDIC bank profile thing:

“Our next chart shows that the allowance for credit losses grew at a faster pace than noncurrent loan balances, resulting in an increase in the reserve coverage ratio. The ratio of the allowance for credit losses to noncurrent loans increased from 203.6 percent one year ago to 224.8 percent this quarter, the highest level since we began publishing the Quarterly Banking Profile in 1986.”

Everything is fine, relax, banks are great investments, and the FDIC has unlimited cash to bail out banks, because they have an insurance fund stuffed with long term Treasuries…

Sure, where did you think the CRE problem loans would show up? On your shopping list? And do you even know what an “allowance for credit losses” even is?

Note that the “noncurrent loans and leases” (blue line) remain very low:

And here are the changes in loan-loss provisions:

The reckoning has not even begun.

Can I buy my 2.375% 30y mortgage back at market price today?

7.22% today, 27 years left, your “buy back” would be 43cents on the dollar on that 80% loan. Congrats you only need to pay 65% of that offer you signed on on the purchasing contract due to “Interest Rate Shock.”

What could be sweeter than a sweet deal? But they’d rather you refinance instead.

Doesn’t anyone make a decision and stick with it anymore?

I was about to comment the same… wondering the mark2market value on my 2.7% mortgage is.

Can you buy your own mortgage back?

Of course you can. It’s a strategy called “selling your house”.

Or simply paying off that mortgage with a cash payment to the lender and then there is no loan anymore.

Noop. If you sell your house ordinarily the loan gets paid back at par not market value.

The loan discount has morphed into home appreciation. The home appreciation would not be there absent ZIRP. People need to sell the house to lock in the financing benefit.

Bobber – I’m not talking about selling the home. I just want to buy the mortgage back from the bank at its current mark2market value.

Keeping a mortgage with a low interest rate is the way to go. You’re making monthly payments into the future with cheaper and cheaper dollars, and the cost of that amortizing loan is about half of today’s rate. And, you may be able to write-off that interest payment against your taxable income.

But remember, it makes zero financial sense to pay any amount of interest to own a declining asset. Sure, Rover will have a yard to pee in, but is that worth the financial risk.

I have the same question.

If ii purchased a house for a 1M 30 year mortgage in 2020, its market value is 47% less now. Ie around 530K.

Can I find who owns my mortgage and offer them 600K cash? They would unload their loser loan and I’d get my house at a 40% discount when I forgave the par value loan. Win-Win! Maybe I could get a tax deduction for the 400K loss?

I suspect their is something wrong with my logic.

“They would unload their loser loan” … “Win-Win!”

The only way they quickly get out of this “unrealized loss” is to turn that into “realized loss”. Sure they would “get it off their books” but it’s not a win for them. If you paid 40% less on that principle, someone is not getting 100% of their investment back. Why would they do that? Because they are between that and holding on and watching their cash earn a measly 2.x% interest rate for the next 30 years. Either way, the loss was already baked in the cake the moment they “bought” in.

This thread showed many people want to just buy back our mortgages, while it is a good thought experiment, it’s not how it works today. You did not sell a callable bond, you took out a home mortgage. It does have many consumer protection features though, such as a fixed interest rate, no principle pre-payment penalties, and a foreclosing procedure.

Below 3% interest is the deal of the century. Many people are not selling, not refinancing, and not pre-paying their principles. You have their money already! Instead, why not save the cash you wanted to use to buyback your mortgage and investing in something that has risk free return of 5%?

“Below 3% interest is the deal of the century. Many people are not selling, not refinancing, and not pre-paying their principles. You have their money already! Instead, why not save the cash you wanted to use to buyback your mortgage and investing in something that has risk free return of 5%?”

I wouldn’t say “you have their money already”. The benefit of the low interest loan accrues each month in the form of a lower monthly payment, so the financing benefit accrues gradually over a long period of time. The risk is that home prices can decline a lot faster than the financing benefit accrues, causing a quick loss of that financing “benefit” and then some.

The way to quickly unlock and secure the finance benefit is to sell the house and realize the price appreciation. The equity you’ve unlocked will result in a much smaller mortgage on your next home, so the higher mortgage rates won’t matter so much. This is the play that people don’t currently understand or appreciate, but they will figure this out soon as home prices continue dropping.

“Maybe I could get a tax deduction for the 400K loss?”

If you could pay your mortgage off at a discount, then the entity that loaned you the money would have a tax deduction because they will have turned an unrealized loss into a realized loss. You, on the other hand, would have 400K in taxable income representing the amount of the loan that was forgiven. People may hesitate to pay off their mortgage at a discount for this very reason.

rojogrande, HS86, and Bobber,

You all have good points.

I think rojogrande has the best point. The 400K is likely a short term capital gain which would put most single filers in the 35% tax bracket. Paying taxes on money not realized is probably a poor choice.

However, if I was a bank in trouble needing cash, selling off the loan is a solution even if they take a loss. Over the years, I’ve had many of my loans sold off by banks to other banks. They are sold at market value and not par value.

1) If it was sold at market value, the bank would collect 530k in much-needed cash. They’d take a loss on paper for tax purposes of 470K on the 1M loan.

2) If they offered the homeowner a deal of 750K. ie if they split the difference. The bank would collect the 750K in cash instead of 530K and the homeowner would get a great deal on buying off their mortgage (if they wanted to pay off the house, today they’d have to come up with close to 1M to pay it off at par value.) This is what I meant by Win-Win.

3) If the bank didn’t need the cash, they could keep the 3% mortgage and gamble that in the next 30 years rates will drop again and the mortgage would be worth par value. It is a gamble for the bank. It is also a safe gamble for the bank to wait the mortgage out. It is unlikely that any homeowner will hold their loan for 30 years. Most get the 7 year itch and sell the house and the bank collects par value.

Why would a homeowner want to pay off their house?

1) The best reason I’ve heard on this blog is “Peace of Mind”. Many people believe in paying off their house before they retire.

2) People may have received a windfall inheritance and want to pay off all debt. Being debt-free is freeing to many.

3) Some may think the 5.5% they are earning now on 3 month CDs/Treasuries may not go on forever. Paying off a 3% mortgage now at a discount may be a good long-term strategy. It is a gamble for the homeowner.

Why wouldn’t a homeowner pay off their 3% mortgage?

1) No discount. If the loan holder doesn’t offer a market rate discount to pay off the loan, their is no reason to pay par value for the mortgage when they can take the money and invest in safe CDs at a higher rate.

2) The tax implication of the 400K short term gain when buying the loan at a discount.

3) The ability to take any cash and make more in 5.5% secure Treasuries/CDs and use that to pay the 3% mortgage.

I’ve said before that my parents held their 6% loan through the late 70’s and 80’s when mortgages reached 18% and Treasuries were paying 15+%. No bank offered them a discount then.

I’ll keep checking my snail mail for any offers and let you know.

To clarify my statement:

“Most get the 7 year itch and sell the house and the bank collects par value. ”

Most get the 7 year itch in their marriages (sadly 50% for first marriages and 70% for second marriages end in divorce), jobs, and owning the same house. Either a divorce or boredom with the same house/job will cause a sale and the bank wins and gets rid of the 3% loser loan.

Will the 7 year itch be extended to a longer period for people holding 3% mortgages?

Of course there is also death. With the miracles of modern medicine, most can hold on 30 years. I plan on it

“That’s why we now have to pay attention to unrealized losses in the banking system.”

Pay attention? The Fed will always step in with their balance sheet firehose of money to erase the problem and make depositors whole. Even the bankers that made bad decisions will largely walk away in good shape.

Why would somebody like me worry about unrealized losses in the banking system? Even though I’m middle aged, the fed has helicoptered money into every financial event that gave off the slightest scent of a banking panic throughout my entire adult life. They even backtracked on their balance sheet reduction by hundreds of billions of dollars just last March. As far as the Fed is concerned, it worked beautifully, so they’ll do it again for the next panic in a heartbeat. If the next panic is bigger, they’ll get a bigger helicopter to douse the fire with even more money.

The Fed is stuck. We’re in a spiral that we will not be able to get out of without pain so immense that it would even hurt the rich. Pain for the rich is clearly not acceptable and must be delayed as long as possible, so we will continue to spiral until the dollar is dead, however many years that takes.

“They even backtracked on their balance sheet reduction by hundreds of billions of dollars just last March.”

LOL, they backtracked on their backtracked on the balance sheet reduction:

https://wolfstreet.com/2023/09/07/fed-balance-sheet-qt-105-billion-in-august-864-billion-from-peak-to-8-1-trillion-lowest-since-july-2021/

Wolf, they did backtrack by close to a half a trillion dollars at a time when they were supposed to be focused on balance sheet reduction and the #1 goal of fighting inflation. The balance sheet is still higher than it otherwise would have been by the amount that they backtracked (a ratchet effect that we’ve become so used to). We can laugh all we want, but March showed us that the Fed is still very willing to put their inflation fighting tools on temporary pause if needed, and all know how long temporary can be for these people. Price stability is not the #1 goal of the Fed, not a by a long long long shot. Bank stability is. And since we have more banks out there that will probably be in rough shape, you can bet that March won’t be the last time we see this kind of behavior from the Fed. They will be forced to do it again.

QT continued unchanged, see the charts for Treasury securities and MBS. There was no “temporary pause.”

The Fed briefly added bank liquidity measures on a separate track, which has nothing to do with QE or QT, and most of those liquidity measures have by now vanished.

The balance sheet today is down by $864 billion. It would be down by $1 trillion without the tail-end of those liquidity measures. It will be down by $1 trillion in late October or early November.

100% correct the US policy is for $1 Trillion Year Debt to be rolled off their balance sheet. And you made your conclusion using different methodology. But, if the US has $31.5 Trillion Debt and just raised the debt ceiling by $2 Trillion and they reduce our debt by $1 Trillion per year how long will it take to pay down the debt? Over 30 Years.

There are some fundamental misunderstandings here:

1. The Fed is NOT the US Treasury Dept.

2. The Fed (not the Treasury Dept.) is rolling $1 trillion off its balance sheet, and investors are picking them up. That $1 trillion does NOT go away, it just shifts from the Fed to investors.

3. The US debt of nearly $33 trillion continues to grow, no matter what the Fed does. The Fed’s action only impact yields, not the amount of debt outstanding.

4. Congress decides what to spend, which determines how much needs to be borrowed, which determines how fast the US debt grows.

5.. There is no plan to “reduce” the US debt. This effort would have to take place in Congress. There may be half-hearted efforts in Congress to slow the GROWTH of this debt.

6. If the debt grows by 2% per year, and the economy grows by 2% and inflation is 5% (meaning tax receipts rise with wage inflation, profit inflation, and economic growth), then the burden of the debt as a percent of tax receipts and as a percent of GDP will decline. This article spells out the relationship with debt, interest payments, tax revenues, and GDP:

https://wolfstreet.com/2023/08/30/curse-of-easy-money-us-government-interest-payments-v-tax-receipts-average-interest-on-treasury-debt-debt-to-gdp-in-q2/

Executives at the banks just bet on others monies for their own golden parachute. They are always the winner no matter bond yield turning positive or negative. Obviously, this is a clear arena on the accounting front that require amendment to reflect the “Mark to Market” value.

The past Enron accounting scandal should serve as a valuable textbook materials to made changes to these accounting loophole that better serve an average joe.

The c suite in this country is very corrupt and constantly stealing from shareholders.

Love the self quote. Lol

RRP is down $1T from $2.5T to $1.5T. Fed Total Assets are down $0.9T

Fed net = Total Assets – RRP ==> n/c.

🤣 RRPs are a LIABILITY. On every balance sheet in the world, when assets go down, liabilities go down in equal measure, if capital remains unchanged, as is the case with the Fed’s capital (which is set by Congress).

Assets = liabilities + capital. ALWAYS. It always “balances,” which is why it’s called a “balance sheet.”

What about unrealised losses by US investment banks on Chinese corporate bonds? Who’s holding the bag there?

1. Investment banks cannot carry bonds at purchase price. They have to take the losses as they occur (mark to market). And they therefore do not have unrealized losses.

2. Those bonds were likely in some EM bond fund that people have in their well-diversified 401ks, and after the bonds collapsed, those bond funds likely sold the bonds for cents on the dollar to hedge funds and PE firms that specialize in distressed debt.

3. The amounts of these dollar-bonds are pretty small though, in comparison.

Well, that would explain all the talking heads on Youtube and Bloomberg shilling EM funds through 2021. I remember laughing at that a few times.

Can I currently repurchase my 2.375% 30-year mortgage at the going rate?

What this also means is that the underlying asst has gone down 43% in value. If you buy a $1M house with a 2.375 mortgage your payment is $3880/month. If mortgage rates go up to 7.3%, that same payment will only buy you a $560k house. Value of bonds is another way of saying what will the payment allow me to buy.

The way that housing would be forced to mark to market would be if you were foreclosed on and the bank had to sell your house at a “cover the mortgage” price.

The Fed (Bernanke) deviated from its history of NOT being in the long end of the market…….to manipulating the long end with Trillions of dollars, pushing rates to 4000 yr lows. Bernanke polishes his Nobel as the ramifications of this policy shift are yet to be dealt with.

Former Fed President Fisher admitted in the PBS documentary “The Power of the Federal Reserve” (can be seen on the PBS web site) that the Fed intentionally FORCED (his word) investors to take more risk by pounding long rates. This of course tended to steer banks into the mess in which they currently find themselves.

So the Fed’s “forcing” worked in one way, but set the stage for a banking mess in another way.

Why is the Fed involved in long maturities when their heralded “dual mandate” deals with two real time and current issues (employment and prices)?

The banking mess and the inverted yield curve can be directly attributed to the Fed’s manipulations. And they sit in their own trap.

In economics as in physics, for every action there is an equal and opposite reaction. Painting over the rust just doesnt work.

And as the banks deal with their unrealized losses, the Fed has over $1 Trillion of the same problem, though accounting magic lessens the immediate concern.

I don’t even pay attention to Nobel anymore, ever since they gave a peace prize to Arafat and Obama.

Did you include the MBS in those losses? Why are these criminals still holdin mortgage derivatives 15 years after the housing crisis? Why are they are slow-walking some pitiful QT but sitting on the piles of MBS while the housing market has locked up? How does this benefit the American people?

Although Congressional is a ridiculous construct, they seem to be an extremely weak link in the balance of power within government.

The Fed has usurped too much authority and has become its own political branch, playing by rules it creates on the fly, without having the authority to do so.

The core problem is a tsunami of stupid politicians that either have no clue about accounting, or, on the other hand, politicians that are clever, abuse their public positions for enrichment.

Perhaps AI will make America great again?

LONGSTREET wrote: ” Why is the Fed involved in long maturities when their heralded “dual mandate” deals with two real time and current issues (employment and prices)?”

Why? Because the FED is a cartel owned by it’s member banks. Protecting their members is the real mandate. If you recall the rampant and widespread fraud of 2007/08, the member banks needed to borrow cheap money from the FED that they could turn around and lend out at a nice profit (to cover their own loses).

But the cheap money available from the FED went on for too long. And now it has become the PROBLEM.

The FED fixed one problem (loses from mortgage fraud), but created a whole new problem with the solution.

To be fair, Greenspan is ignored a part of the cause of the problem simply because Bernanke was even worse. Greenspan made some pretty ridiculous arguments about how low rates were fine.

We also need to include congress and the Clinton and Bush administrations that made it that buying a home was a lottery ticket with little to no downside (until everything crashed).

Hmmm, sounds like someone else has read “Griftopia” and/ or maybe “Fed Up”, or “Too Big To Fail”. All good, scary reading.

RE: The bank that purchased this security at auction and carries it under HTM accounting rules on its books would show no loss on its income statement, and its earnings-per-share would be just fine.

I agree with your overall premise but disagree with the above statement. If you write down the bond to market then you would take a one-time loss now and then realize income at the market rate of 4.35% until maturity. If you do not mark that bond to market then your go-forward earnings would be 0.625% until maturity. The problem is that you are funding that bond with short-term borrowings where the funding rate is now a multiple of your 0.625% bond yield, which means accounting losses (and EPS declines) over the remaining holding period.

The point – If you mark that bond to market now then you take the loss now. If you do not mark the bond then you take that loss over the holding period. There is no free lunch.

Apparently, bank examiners don’t have to read footnotes.

They do, which is why the FDIC tracks unrealized losses.

The problem is that they’re allowed and even encouraged under HTM accounting rules for banks. Banks could be forced to mark to market all their bond holdings, like investment banks and hedge funds and other firms already are. That would solve that problem and discourage that kind of risk-taking.

Rather than assume that there’s a conspiracy afoot, I think it’s likely to be human error – “unknown unknowns”. The S & L failure was a result of deregulation. The S & L lenders with new lending license didn’t understand commercial banking operations and were hoodwinked by daisy-chain jacking-up of appraisals, the lack of controlled dispersals of money for contractual work by developers, etc. They (the S & L principals) were out of their depth and didn’t understand the risks nor the controls.

Extraordinary measures taken by the Fed were under crisis circumstances – some were reasonable, but some had unanticipated consequences (unknown unknowns), like suspending mark-to-market accounting.

Wait a minute… the S&L principals knew exactly what they were doing, and lots of these perpetrators went to jail for that reason! They didn’t get sent to jail for making honest errors.

I mean now everything has changed. We no longer send bank executives to jail. That’s just way too brutish. In a worst-case scenario, we might fire them. We can’t even claw back their bonuses.

Any entity that accepts federal help must be subject to clawbacks IMO

compulsory

Wolf, jail time was served, primarily, for outright fraud, e.g. posterchild Chas. Keating bribed 5 senators and sold worthless bonds to naive investors who thought that they had FDIC coverage.

Why are capital calls not used to shift the cost of unsuccessful management to the owners of the bank (aka stockholders), rather than to socialize those costs via direct and indirect subsidy via Treasury/Fed/FDIC.

Voluntary capital calls, so to speak, can be used when the banks are still stable enough to have valuable shares and preferred stock that can be issued that investors want to buy. But when SVB tried to raise capital that way, investors refused, and it collapsed. So this should have happened a year earlier.

Banks are now issuing lots of long-term bonds and preferred stock to give them liquidity and capital, so they ARE doing that.

What the big banks SHOULD do now is stop paying dividends and stop share buybacks. That would shore up capital every quarter. The Fed can force banks to do that, and it forced them to do that during the pandemic, but then opened up the valves again.

Not sure if this if I asked the question right, or if you answered the question I was trying to ask.

I read a paper on banking system risk management that discussed “double liability” in the 1930’s. This blurb from the summary refers to double liability used to incentivize shareholders to reign in management risk-taking, and approach bank stability by connecting a painful capital call in the event of falling below a certain capital ratio:

“ Since the beginning of modern banking in the early 19th century, policy makers and regulators have tried to rein in bank risk. One often-used tool was to force bank shareholders to face some form of additional liability. From 1817 onwards, shareholders in most U.S. banks had so-called “double liability.” Double liability stipulates that, in case of bank failure, the banking supervisor levies a penalty on shareholders (up to the par or paid-in value of their shares) that is used to satisfy the bank’s depositors and other creditors.”

It only kicks in when risk ratio declines below a proscribed minimum. Attaches a shareholder “cost” when management result is poor.

Here’s the paper:

https://corpgov.law.harvard.edu/2021/07/06/shareholder-liability-and-bank-failure/

Sounds fair and effective to me, and I’d love to hear what others think of it…

Thank you for your response and for the thought provoking article.

Imaginary email to the margin department:

“Don’t worry. I am going to hold to maturity”

Thanks to Wolf for showing the mechanics of simple bond pricing. Now, this has huge implications for the economy, and will eventually allow immense profit for the survivors as they ride the yield curve down again. Michael Milken is a famous winner. On the other hand, those losses are going to be tough for financial institutions that can’t HTM.

When we spike to 10 percent, the 30 year zero is going to be a very cheap asset, LoL.

I was commenting at the beginning of this mess that this would be an issue, and here it starts.

*some banks don’t hedge, or don’t hedge enough, because executives prefer to show a little extra income to prop up the banks falling stock price and to fatten up their compensation.*

Seems like misplaced incentives. Wouldn’t it be easy enough for regulators to a) change the rules so everything is mark to market, and b) ensure bankers have skin in the game, e.g. consequences of being the big boss include claw backs and jail time.

Me? I’m still agog at the remuneration of Lucid’s CEO. This whole pay for CEO at public companies is whacked. Strikes me the pay at private companies can be whatever, but the pay at public companies needs another look see.

Best line of the year, “the ancient strategy of buying high and selling low.”

On the plus side, bond issuers are sitting on unrealized gains. Those who are in the financial position to buy back their bonds at a discount can reap a tidy profit. Alas that class of issuers does not include the us government…

Yes. Any day now we’ll probably get a mortgage buy-out offer from our lien-holder with a cash bonus for my 3 3/4%/30-yr., provided I repurchase a new one at the current market rate.

If I were interested in moving, it would be a good deal and would really stiff the lender if there was no prepayment penalty.

So I imagine I’ll never get that offer…

For stupidity there is absolutely no limit. But a lack of economic expertise also played a role, I think.

As a former financial principal for a couple of small regional broker/dealers, I strongly advocate for banks being forced to mark their bond portfolios to market for each reporting period. Life insurance companies and pensions are a different animals, and they can hold to maturity.

Markets can often be very short-sighted and irrational which is precisely what caused the 2008-2009 ‘crisis’ with FASB Rule 57 ‘market to market’ accounting requirement which were repealed in March 2009 at which time the markets fully recovered.

We see things differently. The 2008 meltdown started once prices rose to the point of creating an affordability problem, in other words the lack of qualified buyers was the genesis of the meltdown despite the shoddy underwriting. Once the market became soft and prices started to decline, this exposed the shoddy underwriting and the whole thing spun out of control after that.

The whole point of marking to market is to force financial institutions to only inventory and hold what they can afford in the event of unforeseen market volatility.

Much of this is down to the fact that most large Corporations are not owned. At best they are controlled. Management are not owners. They enjoy the fundamental benefits of ownership with none of the substance of ownership.

Owners enjoy the fruits of success AND have full liability for failure.

Today Capitalism has been redefined as Corporatism with the most important aspect of incorporation being limited liability.

Capitalism means giving workers a financial stake in increased productivity (share in profits, etc.).

🤣😍 No. That concept might be socialism? Capitalisms is for the owners of capital to reap all the benefits off cheap labor (the workers).

In the US, obviously we have a hybrid system incorporating elements from everything.

With real growth down to 1% per year, our economic results collapse to a zero same game. Wealth is being transferred from one party to another by market speculators, whims of Congress, and the fruitless and mindless experiments of the Federal Reserve.

Are our problems economic in nature, or are they really just allocation issues resulting from improper influence, lack of representation, and corruption?

Big banks, of course, receive an oversized allocation of wealth, relative to their inputs. They receive unlimited profits, compensation, stock buybacks, etc., while big bank losses are practically prohibited by the Fed and Congress.

Where is real growth down to 1%? In the US, real GDP growth has run between 2% and 3% over the past four quarters. Q3 looks to be higher than 3% at this point.

LT growth potential is equal to the increase in productivity, which is around 1%. I don’t add in population growth because that doesn’t provide much GDP benefit on a per capita basis.

Where? Um, every article on “HeroWedge” and from every word out of the right wing. You know, from “the front lines of truth”…. :-)

How does you assessment factor in inflation? Are we seeing economic growth or are the increased costs of goods and services driving the level of increase in GDP

All numbers I cited are “real” GDP = adjusted for inflation.

Nominal GDP growth (not adjusted for inflation) is much higher: for the same last four quarters, nominal GDP growth was between 7.7% and 4.1%.

Two years from today , are we going to look back upon buying the largest 7 S+P stocks on 9/1/23 with the same disdain as we are now looking upon buying bonds in 2020?

Im betting on it. Buying OTM puts from June ’24 to Jan ’25. Will buy more if current wobblness continues.

What am I missing?

If you have to hold a 30-year bond paying 1% while depositors want 4% you are losing 3% per year times 25-30 years to get no “realized losses”?

What good it that?

The US federal government gets funds at WHATEVER the yield on US Treasuries is at any given time, and without getting fully funded the US federal government could not function at all. It now has $33+ trillion in federal debt (US Treasuries) outstanding and needs to be fully funded at all times regardless of what yields are.

“A whopping $7.6 trillion in interest-bearing US public debt will mature within a year, Apollo’s chief economist said”

That’s called “crowding out”.

The Fed has an App for that….

You’re missing the principle of “sticky deposits” that banks take advantage of.