Spiking Interest payments will hopefully, knock on wood, force the drunken sailors in Washington to go through detox.

By Wolf Richter for WOLF STREET.

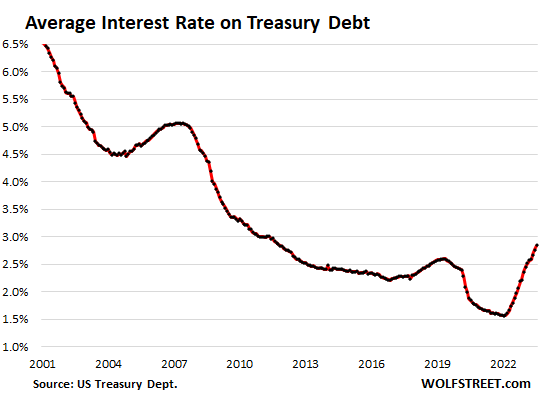

The gigantic US government debt is now approaching $33 trillion, amid a tsunami of issuance of Treasury securities to fund the mind-blowing government deficits and roll over maturing securities. At the same time, the Fed has hiked its policy rates where borrowing with short-term Treasury bills costs the government now close to 5.5% in interest, and borrowing longer-term costs over 4%.

But the higher interest rates that the government pays now apply only to the new Treasury securities to fund the new deficits and to replace maturing securities with lower rates. The securities issued years ago will cost the government whatever coupon interest they came with until they mature.

So the average interest rate that the government is paying on all its interest-bearing debt has been ticking up gradually from the historic low point of 1.57% in February 2022 to 2.84% in July. And it will continue to rise as new securities with higher interest rates take on a larger share. Back in 2001, the average interest rate was over 6%:

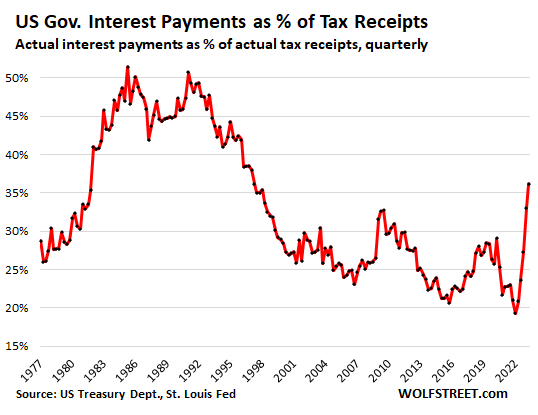

To what extent interest payments eat up tax revenues.

So first the primary measure of the burden of the national debt on government finances, and then into the components: The chart below shows interest expense as a percent of tax revenues. This measure of tax revenues – total tax revenues minus contributions to social insurance and some other factors – was released today by the Bureau of Economic Analysis as part of its GDP revision. This is what’s available to pay for regular government expenditures, including interest expense.

The ratio of interest expense as percent of tax revenues spiked to 36.2% in Q2, up from 33.0% in Q1, and up from 20.9% a year ago, a huge jump in just one year.

- The ratio (36.2%) is back where it had been in Q1 1997

- In Q1 2022, the ratio had dropped to 19.3%, lowest since 1969.

- Between 1983 and 1993, the ratio ranged from 45% to 52%. Oh, those crazy times! Eventually, it triggered a lot of fretting, including in Congress.

Detox not yet. As we saw back when interest expense ate nearly half of the federal tax revenues in the 1980s through early 1990s, a high interest burden might be the only discipline available that will sober up our drunken sailors in Congress. But I’m not taking any bets on it. Drunken sailors don’t want to sober up. Free booze for this long is a terrible thing. Hard to detox.

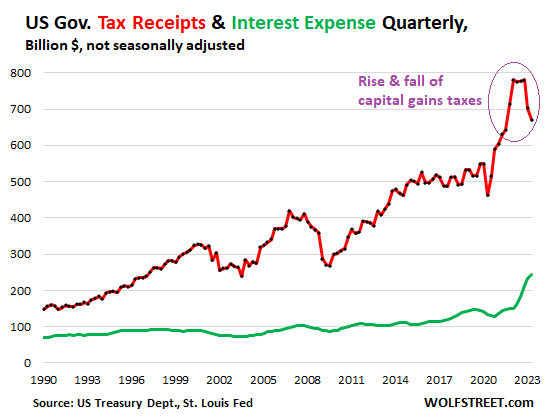

Tax revenues and interest payments.

Tax revenues fell to $670 billion, from capital-gains-inflated spike. Tax revenues fell because 2022 was a lousy year for investors, with all kinds of asset classes getting bashed down, some brutally. As a consequence, capital gains taxes for the tax year 2022, paid by April 15, 2023, plunged.

The plunge of the capital gains taxes came off the enormous high that had been caused by the asset-price spike in 2020 and 2021, that the Fed had fueled with trillions of dollars of QE.

But personal income taxes have continued to surge as a record number of people worked, earning the biggest pay increases in 40 years, of which the government extracted its pound of flesh. Income tax revenues rise with growing employment and wage inflation.

The red line in the chart below shows tax revenues. The trend line shows how crazy the capital-gains-driven spike in tax revenues was in 2020 through Q1 2022 (biggest and final leg of the spike).

Interest payments spiked to $242 billion, having nearly doubled since Q4 2020. Ballooning debts funded with higher average interest rates did do that (green).

The chart shows tax receipts (red) and interest payments (green) together for a better sense of proportion of both of them:

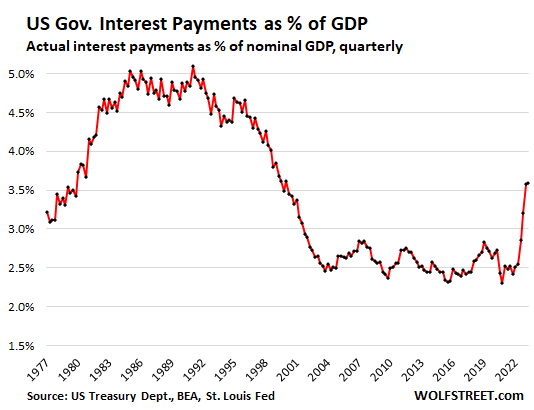

Interest payments as percent of GDP edged up to 3.6% in Q2, the highest since 2000, but well below the budget-nightmare times of the 1980s when it exceeded 5% of GDP for a few quarters.

This ratio is quarterly interest expense (not adjusted for inflation, not seasonally adjusted annual rate) divided by quarterly nominal GDP (not adjusted for inflation, not seasonally adjusted annual rate). So, it too gets our attention – not yet in the nightmare shape of the 1980s, but it doesn’t take much imagination to see where this might be going.

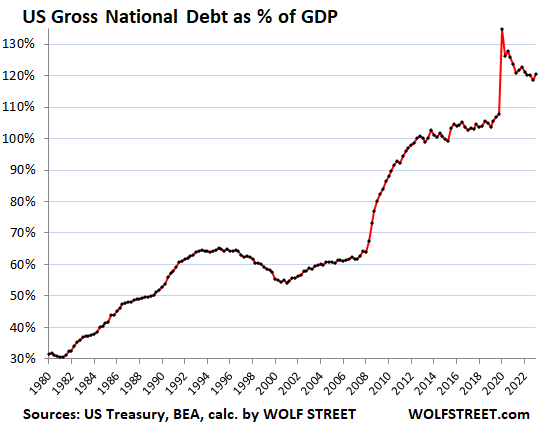

The US debt-to-GDP ratio edged up to 122.8%. This is based on the gross national debt at the end of Q2 (not adjusted for inflation) divided by the revised nominal GDP (seasonally adjusted annual rate, not adjusted for inflation) released today by the BEA. The spike to over 130% had occurred because GDP had plunged and the debt had spiked.

Economic growth and inflation increase nominal GDP, and the debt is growing with the deficits. If nominal GDP grows faster than the debt, the ratio comes down, and it did come down some from the spike, but in Q2 it edged back up:

All these reckless deficits over the many years, and still today, were made possible by Easy Money when the cost of debt just didn’t matter much. Now it matters, but now the country is stuck with this mountain of debt, and it continues to swell, amid the worst resurgence of inflation in 40 years. The interest payments will eat an ever-larger share of taxpayer money until hopefully, knock on wood, they will force our drunken sailors in Washington into detox.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Thanks for the report WR.

I don’t think Govt would ever curb spending.

Few things can happen:

Tax increase

and/or

Fed cute rates and QE happens, inflation can be tamed using manipulated metrics as usual.

If the Fed makes your second guess, we can all say goodbye to the dollar as a reserve currency and as a currency in general.

I assume you have to expect a tax increase.

Fear mongers have been talking about death of USD as reserve currency for long time.

It may happen but after long time.

TLDR: At this time, there is no alternate to USD as reserve currency.

You forget Inflation.

If the Fed refuses to fight it, end your currency.

The kooky part is that the USD is the cleanest dirty shirt in the hamper, and it will be for the foreseeable future.

Perhaps I’m mistaken, but the ECB (Euro) appears to basically mimic the Fed more or less. If the Fed decided to hyperinflate the USD, the ECB would also likely hyperinflate the Euro. Same with the BOJ, etc. Thus the USD would remain the reserve currency.

*Cue the bitcoin shills.*

“It may happen but after long time.”

“How did you go bankrupt? Slowly…then all at once.”

Responsible leaders don’t act like crack-addled children for decades on the (terminally dubious) assumption that every other nation/store of value supervisor is a *bigger* crack addict.

Responsible people look only to their own behaviour.

America has grown comfortable in the (terminally dubious) assumption that every other nation on earth “must be” bigger a-holes than we are.

With a Republican controlled House, there will be no tax increase… and especially with 2024 a presidential election year.

= Expect a nasty govt. shutdown starting in October, as House Republicans try to force spending cuts, while Biden will not want to reduce spending in an election year.

——

If you want to see the extent of the problems the U.S. faces from a mountain of debt, and out of control deficits, please search for this Wall St Journal article:

“The Scary Math Behind the World’s Safest Assets”

“Washington has laid the seeds of a crisis that Wall Street can no longer ignore”

———————-

While U.S. govt financial situation is very troubling, but its even worse in china and Japan…. and Europe is not much better.

= The U.S. dollar is still one of the least dirty shirts

= 5% from a money market fund is still one of the best/safest investments around… because it compensates for current inflation, while providing safety from a global stock market/real estate meltdown.

5% is great…but not if inflation is 10%.

During the 20 years of ZIRP, low interest rates were purchased at the cost of future inflation (low Treasury rates because Fed would buy Treasury’s bad-risk paper at low rates no other non-governmental actor would. But the Fed isn’t a magical leprechaun (“they’re after me lucky charms!”)…the only place for the Fed to get *their* money was printing it…inevitable result…inflation.

ZIRP is (temporarily) over…but 20 years of excess printing has long been baked into the inflationary cake.

There’s already a tax increase passed into law that WILL raise taxes on most working Americans unless it is changed. It’s called the Tax Cuts and Jobs Act. As it was passed, in 2025 tax rates will revert back to the higher brackets that existed before it was passed while the rest of the changes that expose more of your gross income to those higher rates remain in effect, which will increase most people’s tax burden to exceed what they paid before the Act was implemented. But don’t worry, the lower tax rates on corporations were permanent so we will get the trickle down effect. It should have been called the Temporary for most of us Tax Cuts and Jobs Act at yours and future generations expense.

Are you referring to the Trump tax cuts? If the old rates come back, does that mean that the more generous treatment of itemized deductions also comes back?

It seems to me that the difference between tax revenues and printed money is not as great as it once was. As an example, say AWS ( amazon web services) gets a contract to provide web hosting services for the CIA. They then use that revenue to pay their employees and from that pay tax revenues are collected. Its kind of like giving your kid and allowance and then taking half of it back and calling it household revenue to pay the mortgage with.

In the old days when a significant portion of tax revenue came from corporate income tax and payroll tax of companies exporting products, or commodities or agricultural products.

To take my analogy to the extreme, what if 100% of all employees worked for the government, or business’s that only provided services to the government. At that point wouldn’t tax revenues be kind of an illusion, or a snake eating its own tail?

That’s not the correct way to look at it. Tax revenues reduce the buying power of the person paying the tax and increases the spending power (or power to distribute wealth) of the government. Printing money also increases the spending power of the government, but it does so by reducing the value of all other money held by people in the economy. Printing money is much easier for most governments in the short-term because the consequences are so much more diffuse than imposing a tax. In the longer-term it can become problematic. In any event, there’s an enormous difference between taxing and printing.

Your AWS example is too simplistic because it doesn’t account for differences in circumstances, and thus tax rates, paid by the AWS employees, as well as the varying government benefits they receive. Each employee contributes and receives benefits based on the tax and spend policies of the government, thus everyone’s outcome is different. Some pay more than the benefits they receive and others pay less.

Our social security safety net is a prime example of a tax on a tax scam. We pay taxes on money confiscated from us. Then we have to pay taxes on it again when we receive it. And we pay for healthcare again we have funded our entire working lives. The cola is also manipulated to suppress the benefits.

Social Security was tax free until Ronald Reagan saved the program back in 1984.

and in 1950 the fica tax was 1.5%.

“They then use that revenue to pay their employees and from that pay tax revenues are collected.”

Nothing new. That’s how it has always been with government contracts. The gov pays you $1 million, and you pay your employees $500k, and they pay $100k in taxes. Then you got to deal with the remaining $500k to pay your expenses, etc. and what’s left over, maybe $100k is your profit, and you pay $20K in taxes on that.

So you get $1 million, spend $900k and make $100K profit before taxes, and pay $20K in taxes, and have a net profit of $80k.

The people and businesses who get that $900k also pay taxes on that, and it goes around and around. Government stimulus is powerful. But it’s not “printed money,” as you say, but it is borrowed money.

That’s ultimately a symptom of the fact that America’s expectations were set during our hey day, when we had a virtual monopoly on manufacturing and a car industry that was the envy of the world. Our decline started in the 70s, and we’ve really been riding the coattails till then.

Ultimately, our standard of living will drop, and will drop substantially. We simply don’t produce enough to offset what we consume.

I will upgrade my analogy. Rich family with 5 kids has unexpected tragedy where mom and dad die in a plane crash in a remote part of the world so no one knows about it.

Oldest daughter ( the responsible one) finds a treasure trove of high limit , unused credit cards in dads drawer. She implements her plan to keep the family going by make cash withdrawals on the cards each month and then divides that. money equaly among all the kids. But then she takes back part of that money from each kid as a tax. The new ” tax revenue” is used to pay household expenses plus the minimum payments on the credit cards.

She figures this can go on forever as she is running the household on tax revenues and not credit card debt. But she can be forgiven as she is only 18. It is a good thing adults would never think that way.

LOL. The scheme the daughter devised — making minimum payments on credit cards and borrowing on those credit cards to make these minimum payment while also borrowing on the credit cards to pay for all kinds of other stuff — is a common scheme that has been tried gazillion times, and it always ends in default, and often bankruptcy of the borrower when the credit cards hit the credit limit, and no new cards are issued as a result of all the existing debt and not enough income.

@Wolf – The trick with this credit card scheme is to not do it at 18 but at 70. The idea is to carefully manage the kites until the credit card limits are almost reached about the time they lower you in a box to rest.

Yes, but if you miscalculate, and you have the misfortune of living to 104, you’ve got one heck of a time for 25 years trying to escape from creditors by shuffling away with your walker.

So what is the market value of all this old, low-interest paying Government debt?

That is, what is the haircut for the bond/bag holders?

Great analysis Mr. Richter. You’ll never hear this in the main stream financial media.

“So, it too gets our attention – not yet in the nightmare shape of the 1980s, but it doesn’t take much imagination to see where this might be going.”

Personally, I like this graph, at $970B just through Q2. Q3 & 4 should be blockbuster, but you all already know this.

https://fred.stlouisfed.org/series/A091RC1Q027SBEA

Nice write up.

Cheers!

RTGDFA.

BS. You have no idea what the article said and didn’t even look at the pictures. Your link and your clueless comment is about interest payments alone, without relationship to tax revenues. Only idiot bloggers out there spread this kind of braindead context-less clickbait that makes a rational discussion of the real problem impossible. And you gobbled up their clueless BS hook line and sinker. And then you fell compelled to spread this clueless BS here? Kudos.

I gave you the same chart in the article, but in relationship to tax revenues. Green line = the interest expense that you linked. Red line = tax revenues.

It is leaning deeper into the spectrum of Communism/socialism when more people are working for the government, and government related services.

If interest/revenue is at 35% with an average interest rate of 2.84%, it would go to 74% if average interest rate returns to 6%. At 8% we are at 100%. This is assuming no new debt.

A small recession with low tax collection for a year can put us past 100% pretty quick. Bottom line is it looks like we are in better shape than 1986 only because of artificial interest rates. Seems to me we’re playing with fire.

Mattf

Only 2 ways out of it.

1st is, .gov stops spending & start paying down principal on the debt (a concept they seem oblivious to). i.e., work our way out of it, that will take a generation.

2nd. is w.w. III, which tptb seem hell bent on provoking (the “fire” game you allude to…) i.e., fight our way out of it, and that will be over in a flash.

Agreed, If the revenues stayed the same, but they would probably go down incrementaly due to the revenue shortfalls from the interest rates rising over time to get to 6%, therefore most likely even more than 74%

Meanwhile, the concentration of wealth in this country is growing at an unprecedented rate.

Wolf. TBT, Would love your comment on 2008. Looking at the last chart, perhaps the most famous “national debt clock” metrics. Debt as % GDP spike in 2008-10 seemed even bigger than the one today, from just over 60% to almost 100%. People looked on at this and screamed “Obama!!” Yet on the chart immediately before it, interest payment as % of GDP barely moved for the same 08-10 period, and so other people looked on and say “Deficit spending works and here’s the proof!!” And “no government need ever to pay down the debt!!”

For fear of being asked read the entire article again, I understand you have adequately explained the interplay of growth, inflation, deficit, and interest rates. But what I want to ask is this; did we spend more like a drunken sailer today? Or were we the drunkest back in ‘08?

Thanks Wolf,

Very interesting and informative. Seems like a lot going on between Fed rate hikes with the market. Between rate hikes or pausing hikes the government could have big capital gains this year. Very complex scenarios are going to play out this year it seems. Especially between a hike and not a hike in rates. In my thinking with your writings a prolonged eventual recession sometime.

And when interest expense ate nearly half of the federal tax revenues in the 1980s what did Reagan do??? He cut taxes of course and routinely requested budgets that were larger than what Congress came up with. Difference then is that the government was coming off decades of high tax revenues and so the lower taxes juiced spending…..it was really a one trick pony that republicans keep trying to implement.

Lower taxes equal more growth but that was that moment in time. It’s the law of diminishing returns now…lower taxes with increased spending just like Reagan did isn’t producing the same results today as if did back then.

Cataclysm maybe the only thing that inspires change.

“And when interest expense ate nearly half of the federal tax revenues in the 1980s what did Reagan do??? He cut taxes…”

Just to clarify here: Reagan came to the White House in Jan 2081. And the surge to 50% came after the tax cuts and was in part a result of the tax cuts, and in part a result to the increase in spending at the time.

LOL… ” Reagan came to the White House in Jan 2081.”

Back to the future!! :)

Trickle down, don’t forget that the wealth trickles down. :)

He raised capital gains tax on foreigner’s before he left office. At the time it was directly aimed at the Japanese who tried to buy up all of Hawaii real estate.

Sigh. Lower taxes are not the problem here, the problem is dramatically higher spending mostly on entitlements (Medicare, Social Security, and Medicaid expansion of 2008), and now, the ridiculous pork fest ironically labeled “Inflation Reduction Act”. There is simply no limit on spending and both parties are to blame, but one party is a heck of lot more culpable. Take away Medicaid expansion and the IRA and make the hard adjustments to means test Social Security and start to limit Medicare and we would have a massive budget surplus. Return the role of Federal government to 1930.

LOL, sigh all you want, you are still incorrect. The tax system the U.S. currently has is ridiculous. It is one of the most regressive in the world. The ultra wealthy pay lower rates than people making far less than them. A more logical tax system would bring in far for revenues for the federal government while not costing 98% of the population any more money.

Its easier imo to think of the government as having been sucked into a loan shark agreement.

A large portion of the money lent to the US government has in fact come from printed funds from the Fed, then lost to the financial sector, that have then established this -real- income stream from tax i.e. it is the inflationary losses of the population at large that have captured the income stream for the wealthy. You can see why some people think a socialist reset is needed..

The UK government is currently losing 10% of income to this creditor trap. There is no plausible escape for the UK government (or the US) apart from inflating the debt away.

Wolf, you are awfully tough on drunk sailors. They are just out for a good time, not like the powers in Washington DC. And, drunken sailors eventually run out of money, return to ship, and suffer hangovers. Maybe the pols in Washington will get a hangover, but more likely it will be the People who will reap the ill effects of fiscal irresponsibility.

Wait till I talk about the drunken sailors that are whipping consumer spending into a frenzy. Later today.

Great information! Thanks.

Kind of depressing when you think about it. Keep going!

Great article.

Both charts cover a time frame that coincides with the 40 year cycle of declining interest rates. If rates have finally reversed upward, should we expect decades of sporadically rising rates (as in 1946 to 1982), and doesn’t that argue for a return to double digit rates?

Not predicting a time frame, but perhaps our kids (grandkids in my case) will get their own version of what my generation went through in the 1970’s and early 80’s. Talk about confusing times!

Better bone up on The History of Interest Rates by Homer & Sylla. The Chart on page 335 (3rd ed., 1996) tells a mean story of long-term high grade US corporate rate cycle over 200 years. Why would it be different this time?

LOL!!!!

This is not the 70’s 80’s, not by a long shot. What was the DEBT/GDP in the 70’s/80’s?

Try the 1930’s on steroids! But I get it, math is hard…

Double digit mortgage rates aren’t far off

So what shenannagans will “Our Representatives” come up with to avoid the doom loop of higher interest expenses than tax income?

I assume this means the Fed will be limited as to how far they will raise the rates, or is this all market driven?

If they lower rates before inflation is dealt with presumably that’s where we all take it in the shorts instead of a national default of some version… I expect that “Our Representatives” would rather do that than detox.

Financial repression, bond holders lose. Forced purchase of bonds by institutions retail have to use. Government deficit spending to protect pensioners living standards. Massive, massive immigration to force down wages of non pensioners, force up housing costs, paid entirely by non pensioners. Increasing punishment for anyone who critiques immigration, conflating it with hate speech.

Basically what’s been happening for 20 years but turned up to 11.

Some areas of China are beginning to pay young people to get married. Also they are subsidizing invitro fertilization if there are conception problems.

Natron-

“… is this all market driven?”

My understanding from the 80’s was that for a while, the government IS the market and can dictate yields. But only until the Vigilantes revolt by calling BS on the government manipulations.

When that occurs, full faith in government, and demand for long bonds, recedes. In the second great U.S. bond bear market (1946-1981), when the bond vigilantes had done their worst, the 30 treasury rose from about 2.5% to about 12.5%. Homer and Sylla (see my previous post) estimate this would have equated to a 80+% decline in value if there had been a constant maturity 30 year treasury over that period (page 337).

The government can only control the interest rate markets so far, then markets take over…

Thanks for the history. So another Volker might be needed to get things stabilized Plus lower spending (MIC cuts anyone? I’d like my SS back…) and higher taxes.

That last assumes fiscal responsibility on the income front too, but all I see is GOP tax cut measures left right and center so not really hopeful there yet. Personally I don’t have any problems paying taxes as I see that is the price to pay to not live in a 3rd world economy with dead people laying in the gutters. Lots of places like that in the world.

For the record generally, I do feel entitled to social security considering I paid into it all these years. If that’s “Entitlement” so be it… but the Framing on that lately is ludicrous.

not “printed $$” but is borrowed $$ – Question? aren’t they the same thing? Simple explanation please for this farm boy idiot. First saw you with Max and Stacey been a fan ever since. “Where we talk about business, finance, and money!” love that. Logo should be at the entrance of every public school!

“not “printed $$” but is borrowed $$ – Question? aren’t they the same thing?”

“Printing dollars” is one-sided. There is no other side to it. The Fed prints dollars and hands them out (well, actually, it doesn’t “print dollars,” that’s a figure of speech, but it gets the massage across.

Borrowing is two-sided. If I lend you $100, I take my asset “cash” and by lending it convert it to another asset, called “loan.” So now you have my $100 (which is debt to you) to build an empire with, and I no longer have that $100 cash, but I get some income from that, and after some time, I get my $100 back. There was no money created. Money changed hands, interest was paid and earned, and then the loan is paid back.

I understand the value of time in one’s life. So thank you for the explanation and all of your work here.

Pensioners will *never* stop asking for more.

We are actually in times of what will be seen as low debt. Healthcare demands will rise exponentially. They will demand constant spending on pensions to maintain their standard of living.

School class sizes will rocket. Today the usa government spends six times as much on pensioners as youths.

The collapse of pensions for the next generation didn’t stop them.

The collapse of housing for the next generation didn’t stop them.

The collapse of the economy for the next generation didn’t stop them.

The collapse of the ecosystem for *the rest of time* didn’t stop them.

The trend on debt to GDP this far supports this assertion.

You ain’t seen nuffink yet.

This sums it up well. American society is sitting on a powder keg.

The keg has already exploded

I just hope it does not blow up while I am still alive. But we do seem to be going through our own version of Weimar 2.0. In the meantime, my standard of living is much higher than it was back in the 1950’s and I have already outlived my father by more than two decades.

That seems like a selfish attitude. Do you have children?

“If there must be trouble, let it be in my day, that my child may have peace; and this single reflection, well applied, is sufficient to awaken every man to duty.”

Yes, I was referring to the Trump Tax Cuts, or more appropriately the Trump Temporary for most of us Tax Cuts, and No, the more generous treatment of itemized deductions does not come back when the “tax cut” part disappears in 2025. That’s when the smoke and mirrors of the fun house go away and your tax cut magically turns into what it was when it was passed, which is a permanent tax increase. Unless of course your a corporations, in which case you enjoy the tax cut indefinitely at the current and all future income earners expense. What a great piece of legislation.

Nice rant, georgist. As a pensioner, I can tell you that inflation has greatly depleted the purchasing power of my life savings. Furthermore, COLAs are not keeping up with inflation. I have written to various officials (elected and appointed) to ask them to kill inflation ASAP by increasing interest rates and the rate of QT. I have not demanded anything of them. On the other hand, people keep arguing that the Fed pivot or maintain its slow QT rate, so they can keep their government-created, inflated asset prices as long as possible. By the way, I realize that people of good faith can have different opinions about how fast QT should be.

In general, people believe that what they want is justified and what other people want is illegitimate. I suppose that’s human nature.

Oh my god your purchasing power has gone down?

You mean *like everyone*?

You only offered an anecdote, my post was macro.

My fellow commenter, your post was absurd on its face.

With higher for longer and longer, this interest rate will surge to 3.5-4% in a year or two, adding in another 2 Trillions of debt. I don’t think the picture is looking good. Next year is an election year. Our GOV will push this under the rug and nothing will be done. Well, nothing had been done in the past many years.

Can you look at the % of long-term bonds that will be rolling over in the next few years and predict a what will be an effective bond interest in 5 years? Let hope it’s not 5% but I don’t hold my breath on this.

Thanks for the perspective. Get your share of those interest payments while you can. The last 13-week T-bill auction paid 5.5%, 4-week was 5.3% (which means inflation is really running 10% or greater on essentials)!!!

No wonder regional banks are struggling, why keep you money with them when they cannot at least match the interest on T-bills?

Regardless, taxes will go up, they already have in many cases.

Whoa, it looks like the Fed is trying to break a long standing Wolfstreet rule… Interest as a % of tax receipts is going to heck in a very straight line. And look at the rate of increase on that bad boy! We’ll be gettinh close to 50% if not crossing it by Christmas. That’s just nuts.

The FED will continue to take such “support” measures as are necessary to assure success of the Treasury’s debt-management operations.

This is in direct contrast to the 1951 Treasury-Federal Reserve Accord where Fed Chair William McChesney Martin, Jr. “took away the punch bowel.”

…to some, taking away the punch bowl is equivalent to a punch in the bowel…

may we all find a better day.

Fiscal policy over the last 30 years created this distorted economy. It “works” because it creates enough personal wealth and security to go around, but the underlying engineering is unsound. The wealth is over-inflated, the security illusionary, and denial is the name of the game. People think things will just keep on keeping on.

But a single tiny event can cause a huge and sudden deviation from the existing pattern. In non-linear dynamics (chaos theory) it’s called a phase shift, and it’s a function of time. The more time that passes, the more likely it is that things will violently change and go in a totally unpredictable and radically different direction.

When that happens, I can guarantee that a lot of people will lose their shirts. The economy is so hot right now that Starbucks are unionizing, Elon Musk can throw away tens of billions on frivolous acquisitions, and every idiot with a computer can make a living selling click-bait on YouTube.

Anyway. it won’t be the apocalypse… probably. But I think we’re all in for a very hard time. I thought it would happen when Trump got elected waaay back in ’16, and it didn’t. So really that proves my point. You can’t predict these things except to say that it WILL change, and more time that passes, the more likely a radical change will happen.

Hope you all have a great day.

Maybe none of that will happen. Because it already happened? Now we suddenly got many years of stubborn inflation — which no one expected, it’s THE Black Swan, it changed everything, and continues to change everything. 40 years of declining interest rates are history. All the prior assumptions are out the window. This is just the kind of “phase shift” you describe. And it’s huge, and it’s already here.

It very well could be. Time will tell!

We elderly can only HOPE that the inflation, bad as it SO clearly IS for those on fixed income IS the Black Swan…

Maybe SO Wolf, maybe NO, as the entire geopolitical scenario is SO very similar to 1956 for Britain.

While I know full well that Hope is NOT a strategy, it may very well be our best policy.

Spot on WR!!! I am in 100% agreement. They have to save the dollar, period. F’ everything else.

“many people have been calling for collapse

predicting collapse

prepping for collapse

fantasizing about collapse

welcoming collapse

and now, many years into it, they cannot even see it”

The Black Swan was the arrival of Modern Monetary Theory for running the US economy. The GR & COVID were simply the enabling events. A moron could have predicted the arrival of 70-80’s inflation.

QE is the worst Fed policy ever. It shoves huge sums of monies into big banks / hedge funds / uber wealthy which in turn is used to fund budget deficits once QE dries up.

Am I wrong in thinking that a lot of the draw down in reverse repo funds is being invested into treasuries?

If I’m right, then again this is another example of how QE is distorting the bond market. QE stashes away huge sums of money that is fake demand. Without this money, demand for treasuries would be much less and therefore would mean even higher yields.

Please let me know if I’m right, wrong or in the ballpark.

“Am I wrong in thinking that a lot of the draw down in reverse repo funds is being invested into treasuries?”

Correct, that’s the natural progression.

Reverse repos are cash that money market funds put on deposit at the Fed to earn interest and have lots of liquidity. They used to deposit this cash at banks, but RRPs pay more, so the cash went from being on deposit at banks to being on deposit at the Fed. Those deposits ballooned at investors put more and more of their cash into money market funds, and their balances ballooned.

T-bills are now earning more than RRPs, and so gradually, MM funds are buying more T-bills with cash they have on deposit at the Fed. So you see that drawdown.

The debt is being inflated away. Three plus percent of inflation times 33 trillion in debt equals one trillion of debt that left last year in real terms.

So…..the government has got to stop fooling around and start spending more cash……..

OK…….just pulling your legs……but the drunken sailors are thinking about this crazy stuff. Sort of like the Laffer curve in the 80’s.

No end to the madness.

It’s money we owe ourselves…..not exactly…….44 trillion floating around overseas.

For the first time the fed is in a box.

It has been very expensive to meddle in the affairs of foreign countries. So far, we have been able to put off the day of reckoning, but I am convinced that it will eventually come.

Anon – just one of the many costs of assuming the mantle and entitlements of empire…

may we all find a better day.

Wow, that interest expense as a % of tax reciepts graph sure looks like its going to heck in a straight line.

Rates are rising, and if we get a recession I’d assume tax rev will decline accordingly… not a good combo for Uncle Sam.

Say Wolf, are the government interest payments on the debt included in GDP as part of government spending?

Would really boost the “GDP” fantasy.

No, government interest payments are not included in GDP, just like the interest income for holders of these Treasury securities is not included. It would cancel out anyway: government pays the interest and consumers and firms receive the interest. If one would be included, the other one would be included too. Neither one is included.

May be not. but whoever holding these bonds (lot of Americans) are able to get their money and pump this into the economy adding to GDP. It’s basically another stimulus to the rich.

Wolf went to Costco for gas ,had a sign on pump will no longer be selling diesel fuel after sept 24 seemed strange. Not enough demand hahaha

Diesel never took off in the US as passenger-car fuel, unlike in Europe. Only a very small number of mostly older passenger cars burn diesel.

It the gas station isn’t built specifically for trucks, it won’t have demand for diesel.

…but as a goodly segment of pick’emuptruck fuel, though???

may we all find a better day.

Thank you. Always a trusted source of information. I read a lot but trust little.

Are you saying the “Debt to GDP Ratio” is really just the “Debt to Debt Ratio”?

With the likes of McConnell, Federman, Feinstein and Biden, detox might not be the biggest problem. I wonder if they even remember what day it is let alone worry about their spending. Apparenlty, just remaining consious is a daily challenge for our so called leaders.

Reading your well thought out, and laser focused daily articles, then watching these people trying and failing to put together a coherent sentence, is akin to a severe case of mental whiplash.

I have to go lie down now before I stroke out.

Obviously, the Federal Deficit needs to be reduced to avoid trouble.

Yet, how low does the Federal Deficit need to go to avoid trouble? If the deficit only needs to only grow the national debt at a rate lower than the nominal gdp growth, then that is 2-5% of the US GDP per year.

Back of the envelope calculation suggests that a deficit, including interest, below 780 billion to 1.3 trillion would avoid trouble. The current deficit is roughly 1.5 trillion. Finding ~200 billion of cuts or tax increases shouldn’t be “that” hard out of a 4.8 trillion dollar budget. Even 720 billion should be that hard.

If the Fed can actually reduce the inflation rate to 2% per year then this is largely solved. If inflation really is 2% a year, then US treasury bills should be on the order of 2.5% or so, and that’ll do a significant part of the spending cuts on its own.

Reducing the federal deficit might also reduce inflation at the same time, making this all easier. Such a muddle-through looks fairly easy.

The US federal government is totally insolvent, but there is no way for it to declare bankruptcy and seek protection from creditors. I would consider that Congress take that issue up immediately and modify the federal bankruptcy statutes accordingly.

How is the federal government insolvent?

That literally does not make any economic sense.

Having back-to-back incompetent presidents, fits perfectly with our nation being guided by AI.

AI apparently is making America great yet again, but, from my understanding, the hallucinating modeling applied to these gorgeous economic models, don’t include deep dives into financial footnotes.

That lack of perspective is probably fueling the Schrodinger’s Cat Box economy we have, which superficially appears to be healthy, while there’s unaccounted for cancer below the surface.

That also sums up the choices for a president next year, with two decrepit humans that are supported by synthetic alien life support. If there was honesty, we would be able to choose the best algorithms and programming team, versus picking between two morons.

Amen

Someone’s hitting the bottle a bit early in the day.

We all use different analogies to parallel complex economics. But I agree with his point. We have two parties to choose from and neither one is fiscally responsible, taking turns buying votes via tax breaks and social programs, and whose policy decision is beholden to the indexs.

Where would we find a fiscally responsible president/party/candidate, if the voter base is so educated to enjoy these handouts, the bailouts, the high asset prices, and the 0% downs?

“…we have met the enemy, and he is us…”

Walt Kelly (RIP)’s ‘Pogo’ (over half a century ago…).

We don’t have fiscally responsible parties because we don’t have fiscally informed voters.

Agree! I thank Wolf for his public service!!

But Paul Krugman says none of this is a problem because we can just borrow more money to cover the interest payments. See how easy that was?

Continuous and increasing new borrowings to pay prior borrowing was the City of Detroit model.

That that all ended well didn’t it.

The city of Detroit did not have its own currency.

I am not arguing that the deficit (federal revenues – federal spending) hasn’t gotten out of control so don’t go there.

I am saying comparing federal deficits to the city of Detroit misses lots of key information.

1) A war is breaking out between labor and businesses. It’s all about

power : WFH, 40% pay increases, retirement, health benefits, 32 hours/week… It’s a fight for survival, corp US life and death.

2) A war was declared against small businesses. Small business owners cannot finance themselves with c/c loans at 25%/30%. They stretched 30

days payments to 90 days, or 120 days. Suppliers cannot take it anymore.

3) A war was declared about gov $33T debt and spending.

4) There is a bloody war in congress between the two parties and the leading presidential candidates.

5) Inflation is caused by exogenous “events”. Endogenous “events” might

lead to a spiral destruction, to deflation.

I sincerely hope so. D2 will remove a lot of insanity built up over the decades.

Blood will flow and a lot of innocents will suffer, just like before historically. But exponential increase in climate changes may precede and make other events irrelevant. when? 2050 or before!?

Does anyone remember 1 1/2% 10 net 30?

There warnings, though too few. Simpson Bowles comes to mind. Unfortunately, the only remaining elements of bipartisanship are corruption and incompetence. The former needs no examples. Recent evidence of the latter us the failure to term out the national debt when rates were lower. Add to that cowardly abdication by the whorish economics profession of any responsibility to provide common sense insight re growing indebtedness and tax reductions without any corresponding increases in productivity: only increases in asset prices largely to benefit the elite class. The consequences border on treason.

The US was on a path to eliminate the national debt when Bill Clinton left office in January 2001. It was based largely on Newt Gingrich’s “Contract with America”. But Bush 43 upended the path with his two tax cuts and costly Middle East wars. Now it is time to pay the piper.

“The US was on a path to eliminate the national debt when …”

LOL. You’re confusing “debt” with “deficit.”

The national debt continued to grow during that time, it did not decline.

The annual deficit (which adds new debt to the old debt) declined and became fairly small for a little while. So less debt was added, but debt was still added.

Tip and Ronald solved it last time.

Hi Wolf,

Thank you for all the work you do.

I’m a CPA working in California, and I know I’m late to the game, but I have a comment/question regarding 2022 and 2023 tax receipt amounts. You mention the following –

“Tax revenues fell because 2022 was a lousy year for investors, with all kinds of asset classes getting bashed down, some brutally. As a consequence, capital gains taxes for the tax year 2022, paid by April 15, 2023, plunged.”

I agree, its what I’m seeing across returns held by the state’s 1% (largely the client base I work with) as we continue to prepare their forms for filing. These capital losses though are limited to a degree, and are largely benefiting those with capital gains to offset the losses (“tax loss harvesting” this past year was the top buzz-term)

I’m also wondering the impact of the atmospheric rivers that drenched California in December of 2022 and January of 2023 which forced the IRS/Treasury Dept/Biden to provide full, automatic extensions of both payment and filing requirements to everyone located in the declared disaster zones (pretty much the whole state except for 3 counties in the north) till October 16th. I have a theory that this automatic extension also drove down receipts through the first 10 months of 2023, because California’s top earners kept their money, rather than forking it over to the government. My question is – how much of an impact did this have? Is it negligible or material? I’m curious if you’ve come across any data to support the theory.

Little more background for the curious – Normally, you have to request a 6 month extension, and it only provides for an extension of filing, but not payment, so the Fed/state governments get most of their money in April, even if the forms are filed later. This was different. Come April 15th everyone affected wasn’t required to pay outside of what they had already estimated and paid in during 2022 for quarterly purposes (excluding 2022 Q4 due January 15th 2023, which was also postponed). They got to keep the balance of their 2022 taxes owed, penalty/interest free, for 6 additional months. Not only that, but 2023 Q1 – Q3 quarterly payments they normally have to pay in throughout the 2023 year (due April 15th, June 15th, and September 15th, respectfully) were also postponed. Come October 16th when all of the above are due, I expect an uptick in the receipts received by both Fed/CA governments.

W-2 workers, which have their wages withheld from each pay check, had already paid their share into the federal and local government, and were largely unaffected by this automatic extension.

1. “These capital losses though are limited to a degree,…”

I wasn’t talking about “capital losses.” That’s your twist. I was talking about the plunge in “capital gains taxes” paid in 2023 due to losses in the markets in 2022. If in 2021, you owed $100,000 in capital gains taxes, and paid them in 2022, and for 2022, you had a loss, and capital gains taxes paid in 2023 dropped to $0, then this is a plunge of $100,000 in capital gains taxes paid in 2023, and thereby a plunge of $100,000 in capital gains taxes received by the government. You twisted this around.

2. Every year, there are disasters somewhere. The disaster areas were not where 35 million of the 39 million Californians live. The disasters didn’t shut any of the big cities down. They hit the mostly rural areas, smaller towns, mountain areas, etc.

Thank you Wolf for responding. You’re absolutely right, I did mix up raw tax gains/losses, with taxes owed on capital gains. Apologies for twisting it.

For the second point, despite not shutting the cities down, or having any long term adverse affects on most individuals and their ways of life, the federal and state government still allowed a postponement for CPAs in affected areas, where the books and records of clients are stored. CPAs from LA to SF took advantage of the postponement for their clients. Normally if their client owed say, $1M through the first 9 months of the 2023 tax year via estimated payments, they are still are sitting on that money because its due in October, rather than ratably throughout the year.

Thank you again!

1. Reduce spending.

2. Increase tax revenue.

There is a third way. Mint coinage that bypasses the federal reserve.

A couple 1 trillion dollar platinum coins seem more likely than small denominations (10,100,1,000), only because those in charge wish to move towards digital.

I was watching CNBC last week, and there was someone on there calling for the Fed to lower interest rates because the interest on the national debt at the current rate can’t be serviced much with the increasing deficits.

I don’t see how interest rates fall below the inflation rate without the Fed resuming quantitative easing in order to manipulate debt markets.

And it is my theory that once the Fed is required to print in order to keep interest rates in check, a Ponzi aspect (never ending need for new money) will have been introduced.

I think/hope the Fed realizes printing isn’t an option, precicely because the current inflation rate is well above their target.

“once the Fed is required to print”

I don’t think we’ll get to that point. The Fed has other tools at its disposal, i.e. temporary bond purchases like what the BoE did during the recent Glit crisis.

Rate Hikes + Acronyms.

The thing to keep an eye on is the trajectory. If the debt/GDP ratio keeps rising, then, the interest will be a problem. At 5%, interest on a $33 trillion debt would be $1.65 trillion per year. Meanwhile, the military budget passed by the Senate was $886 billion? There may be problems already.

I don’t for the life of me understand why they are running a $1.5 trillion deficit at a time when the labor market is overheated. That’s the kind of stimulus that should have been kept in reserve for leaner times.

The policy seems reckless, and therefore, I don’t think all is clear on that printing requirement. Hope I’m wrong.

No one is talking about cutting ‘waste’ in spending especially at MIC.

Since 2003, 8 Trillions have been spent in wars across many countries ( USA has attacked more than 20 countries since WWII!) in ME, including Iraq, Libya Syria ++. Oh of course trillions in Afghanistan for over 20 yrs! Now back under Taliban. What did we achieve? Not even a hint of retrospective inspection of these ‘failed’ policies by the Congress or in the MSM.

Howdy Folks. Our Govern ment will never spend less. Even new tax revenues are always spent. The other thing Govern ment is good at? Making people into thinking it was and is the other guys fault. They made sure to divide the country so each side blames the other.

Nice Report!

Do you know where I can download historical capital gain tax data?

Thanks!!

I have not found a handy spreadsheet with the data to download. But it has been pointed out in various places, including here:

https://www.cbo.gov/system/files/2023-06/59134-MBR.pdf

and here:

https://www.cbo.gov/publication/58914

and here:

https://www.bloomberg.com/opinion/articles/2023-04-12/how-2022-became-a-record-year-for-us-income-taxes#xj4y7vzkg