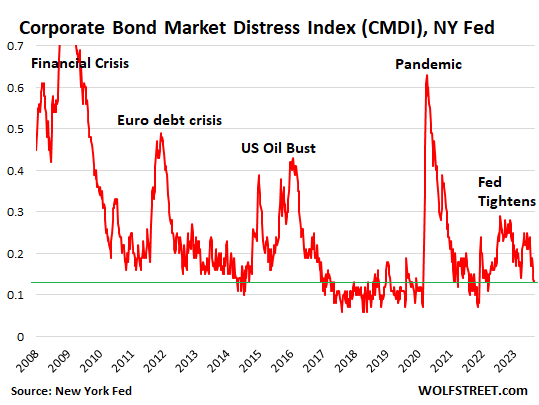

Record QT and big Rate Hikes no problem: Corporate Bond Market Distress Index drops to lowest level since before the Fed started tightening.

By Wolf Richter for WOLF STREET.

The New York Fed’s update today of its weekly Corporate Bond Market Distress Index (CMDI) shows just how much liquidity there is still sloshing around from years of mega-QE, and how yield-chasing has resurged this year, despite the Fed’s hiking its policy rates to the highest levels in 22 years and despite the biggest QT ever.

This index of distress in the corporate bond market, after spiking early in the tightening cycle, fell to 0.13 over the past two weeks, the lowest level since before this tightening cycle began:

“The index identifies as ‘distress’ periods during which a large number of individual measures of market functioning indicate deteriorating conditions in both the primary and the secondary markets for corporate bonds,” the New York Fed says.

“Corporate bond market functioning appears healthy. The end-of-month market-level CMDI is below its historical 20th percentile,” the New York Fed says.

“Market functioning in both the high-yield and investment-grade sectors improved during the course of August,” the New York Fed says.

In other words, after some initial wavering, the corporate bond market has easily adjusted to the much tighter monetary policies and returned to la-la-land.

One reason to track distress is to see how far the Fed can go with its tightening before it does some real damage to the corporate bond market. And the index shows that compared to the other moments of damage – even the lesser ones of the Euro debt crisis and the US Oil Bust – there hasn’t been any damage. The index is now back in its historical comfort zone.

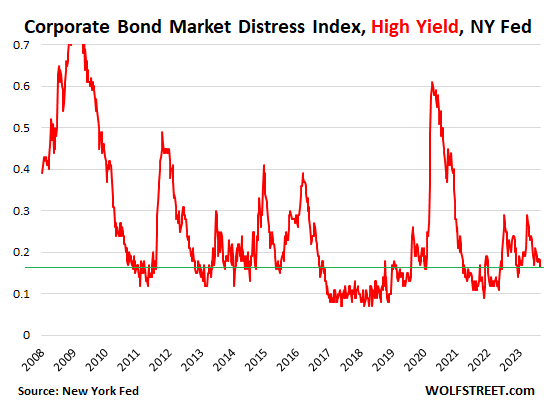

Even the junk-bond market remains in its comfort zone. The New York Fed also provides the sub-indices for distress in the investment-grade segment and in the junk-rated (high-yield) segment of the corporate bond market. The High Yield CMDI tracks junk bonds that are rated BB+ and below but above CCC/C, so not including the low end of the junk-bond market (here is my table of corporate bond credit ratings by ratings agency).

This High-Yield CMDI fell to 0.16 this today, and after the two brief spikes has returned to its comfort zone:

To deal with the worst inflation in 40 years, the Fed has attempted to “tighten” financial conditions with rate hikes and QT. Tighter financial conditions would make borrowing for companies and consumers harder to get and more expensive, and would create a little more distress among borrowers, especially those with weaker credit, such as junk-rated companies, and would therefore reduce investment and demand in the economy and thereby remove some inflationary pressures. So the theory goes.

During this tightening cycle, the New York Fed came up with the CMDI to track the effects of this tightening on the corporate bond market. It complements a whole slew of indices attempting to measure financial stress, but is specifically addressing distress in the corporate bond market.

And at first, the effects were as promised: In late 2021, when the Fed started talking about tapering, rate hikes, and QT, financial distress in the corporate bond market began to rise from historically low levels, in anticipation of what might come. By November 2022, with rate hikes and QT in full swing, the CMDI had risen to 0.28, the highest level since November 2020, when it was coming down from the lockdown shock.

But since then, it has wobbled lower, showing that there is now less distress in the corporate bond market than before the Fed even started tightening.

The CMDI includes primary market measures from the Mergent Fixed Income Securities Database (FISD), such as issuance volumes, primary market pricing, and issuer characteristics. It includes secondary market measures, such as trading data from TRACE, and measures that reflect central tendencies and other aspects of the distributions, of volume, liquidity, nontraded bonds, spreads, and default-adjusted spreads. And it includes quoted prices from ICE Bank of America to track the differential secondary market conditions for traded and non-traded bonds.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

To deal with the worst inflation in 40 years …

…

Me: How’d that happen ?

Politician/bureaucrat/’journalist’: greedy corporations.

Me: Why weren’t they greedy before?

Thank you everybody – questions have now ended – please clear the room.

I know, right? Corporations always *want* to charge more. The question is whether they *can* charge more and have customers still pay it.

In an oligopoly, inflated pricing is more than possible — it is likely.

Look at the profits of the tech giants. They exist in a near-monopoly state, from Apple to Google, and reap the benefits in spades in cash flow.

The lesson here is that it pays to reduce or eliminate competition. There’s a reason mergers are so popular, and the government often looks with suspicion upon them. Because they work to corner the market, reduce competitive pressure, and free up pricing domain space so that the prices CAN be jacked up.

A breakdown of supply chains.

It’s the same reason it’s illegal to price gouge during natural disasters.

E.g. – $20 water during hurricane

Are you forgetting the Great TP Shortage of 2020?

The index shows signs of distress in 2023 that appears to coincide with the failure of SVB and the subsequent banking crisis.

The credit facility to offset bond losses in HTM portfolios and a guarantee of 100% of deposits on accounts appears to have quashed any anxiety.

That last little hump that you see on the first chart started in late March with the SVB crisis.

Thats what it looked like 👍

Pretty amazing how quickly La-La got restored to the Land

Stonks McLuvin it.

IF early Sept. inflation report is greater than the market expects, combined with no very low stress in the corporate bond market, combined with the largest union wage gains in decades ( maybe ever)

= The Fed will probably raise Fed funds at Sept. meeting, while greedy myopic investors are again bidding up stocks to unsustainable valuations.

= All the ingredients for a stock market crash are now in place.

There’s some amazing money to be made trading corporate bonds.

Viz.: Michael Milken, who while at Drexel Burnham Lambert made a salary of ONE BILLION DOLLARS over the course of four years.

DBL was interesting, because they would back junk bonds with their word alone. “Drexel believes this junk bond to be sold and redeemable” and lo and presto! it would sell on the market.

Unfortunately, Milken was convicted of racketeering and fraud. He lost his license to trade, and only received a presidential pardon after years of attempts. The world of finance is a dangerous and sticky one. If you want a safe life, stay away from it. Being on the cutting edge is something that can spring back in your face.

The money those guys made was unbelievable. And they were all doped up.

Trivia: Milken while a ‘master of the universe’ was vain about being bald. He had a wig? No, he had 30 wigs, each costing thousands and each slightly longer than the one worn the previous day. After 30 days, he would pretend to get a haircut and revert to Wig One.

Now he’s just bald, but even that is sort of a new power look.

Financial “experts” are telling Canadians that the Bank of Canada will cut interest rates like day trading because 1 person got laid off from their job to make the CEO richer.

Lolol

If you’re J-Pow himself, which way are you feeling then?

(1) Great news team! We’ve tightened monetary policy at the fastest rate since the 80’s and the corporate bond markets haven’t fallen apart! In fact, they’re even slightly looser than before we started. Success, let’s keep tightening!

OR

(2) Bad news team! We’ve tightened monetary policy at the fastest rate since the 80’s and the corporate bond markets haven’t tightened at all! In fact, they’re even slightly looser than before we started. Failure, let’s keep tightening!

Good questions. My guess is J-Pow is in camp #2.

Correction to your comment.

JPow is in camp 2% and will be high

Jackson’s Hole-

Are you referring to the Fed’s 2% “currency devaluation” target.

“2% Inflation Target” gets the job done, but “2% Devaluation Target” tells the real story.

(PS-love your handle!)

Or 3

After injecting ample liquidity and going insane along with friends across the Atlantic….the Fed and other central bankers accepts that monetary policy no longer has any effect on the real economy but has been highly successful at controlling emotions in the asset economy

FUBAR! Time to burn the entire system down. Not worth salvaging IMO. Can’t stand it much longer.

= Tighten more,

OR

Tighten more

Meanwhile Wall St. thinks the opposite, and is again bidding stocks up to unsustainably high valuations.

= The ingredients for a 1987 type stock crash are now in place…

Mr. Wolf wrote: “… the Fed has attempted to “tighten” financial conditions with rate hikes and QT. Tighter financial conditions … junk-rated companies, and would therefore reduce investment and demand in the economy and thereby remove some inflationary pressures. So the theory goes.”

From this article, the increase in borrowing costs from the Federal Reserve’s still historically very low interest rates, compared to last equivalent inflation episode, is not working. Fortunately, there is another “tool” available, and that is reforming the Trump Era tax cut for these companies. The USA is running huge deficits that were predicted when the tax cut was debated. Simply remove the tax cut to what existed prior; still decades of President Reagan style cuts would exist. Lower the deficit, let off the gas on corporation inflation, sounds like a win- win. Increasing corporate tax to lower the deficit instead of shrinking Social Security would be politically very popular.

Doubtful reinstating the previous tax rates would close much of the gap. the old cliche still applies: we don’t have a revenue problem, we have a spending problem. A very big one.

Gary: Bingo! A half century of tax cuts benefiting the wealthy has caused chronic asset inflation episodes and created a class of Oligarchs.

Raise taxes on the super rich. That will quell inflation faster than any other fiscal tool.

You’re delusional.

Inflation took off 4 years after tax rate cuts.

And what else happened? Interest rates plummeted. Stimmie money. Rent moratoriums. Suspension of student loan payments. Extra unemployment payments. PPP.

People bought $100K pickup trucks at 0% interest. They’re not oligarchs. Oligarchs have drivers. Those folks were simply stupid.

Ditto RV’s. Covid reaction. Escape the “plague”. Real estate in flyover which were previously reasonably priced markets suffered from the following… Covid, low interest rates, stimmies, and work from underwear.

If you only look at one aspect, you’ll likely draw the wrong conclusion. If you feel tax receipts are too low, feel free to personally send Uncle Sam a few grand extra. No one will prevent you from doing so. After all, taxes are “voluntary”.

I’ll bet you turned down the increase in the standard deduction too, correct? That was part of the same tax reduction act. Probably didn’t benefit the oligarchs much, but would likely bite you in the shorts.

The issue is the tax code is too complex. The oligarchs, as you call them, have teams of bean counters who figure out loopholes that the well meaning, but ill informed, forgot to close or didn’t even anticipate when they wrote the law (too busy stuffing pork into the bills to concern themselves with that). The folks with the resources to do so exploit them to the fullest.

Say no to a continuing resolution in September. Shut down the worthless federal government permanently. That’s a good start on fiscal policy.

NAH f’up: But certainly very rational to shut down permanently about 76 per cent, far damn shore…

While no one with any common sense and any connection to reality of BIG GUV MINT wants it to go away tomorrow due to the damage to the proletariat that would certainly occur with such a sudden move,,,

Many, possible most, would certainly like to see some clear reduction along with VASTLY, repeat vastly better direct communication, while ALL recipients being completely free to address those and all, GUV or other, communications with/to the censorship of THEIR choice,,,,,,

NO CENSORSHIP BY GUV MINT, OR their buds in BIG Tech, etc., should be the mantra IMHO, of everyone even close to ambient consciousness, eh

Inflation is falling, conditions are still loose, most consumers and businesses aren’t distressed. I can’t figure out how all three of these things are simultaneously true.

FYI: Inflation is re-accelerating. You missed it?

I’m honestly confused. I understand that inflation is ticking back up, but thought that to be mostly due to the base effect.

And I don’t get how we came down from 9% inflation to around 3-4% when almost everything seems unscathed. People are still spending like crazy.

Inflation is exploding as we speak: Here are the figures in my mandatory budget items (note these are not discretionary spending items.)

Utilities – up 10%

Property taxes – up15%

Home insurance premiums – up 20%

Transportation – up 10%

Health ins premiums – up 9%

Groceries – up 10%

If you believe the government’s bogus inflation numbers, then I’ve got a bridge over the East River in NYC I can sell ya.

Thanks SC. I’m up in Canada (moving to the US this spring), and it’s hard to get a sense of what the hell’s goin on down there.

I agree.

Per the govt metric inflation is going down and is down from 9 percent to 3 to 4 percent.

Fed acts on the basis of govt metric and asset market reacts accordingly.

It does not matter whats the real inflation in the ground is.

What matter is govt metric

@Captive,

Come on down, we’re partying like its 1999!

@Captive:

I think the answer to your question is (as usual) “it depends”.

In our case, our electric bills are less than last year. Why? We have solar hot water (huge cost associated with heating an 60 gallon tank that gets tapped 3 or 4 times per day) and HVAC thermostats connected to the NWS. The ‘stats automatically adjust to the forecast temperature. Ditto our irrigation water (“smart” controller) is only slightly higher and that is due to our behavior (deep watering trees so we don’t lose them in this ridiculous heat). We have a hot water circulation pump (runs on demand) to eliminate running 10 gallons of water down the drain waiting for hot water.

Food? I agree. I simply stopped looking at prices, use coupons, shop on “geezer day” (first Monday of the month for a 10% discount). I started boycotting certain brands that subscribe to “shrinkflation”. The blue corn chips my spousal unit prefers were $.60 an ounce in the “Simply” brands vs. $.30 an ounce from another organic brand.

I hear you can get great deals on Bud Light….. /s

Home insurance? Didn’t move much at all in the SW. Certain parts of the country have high incidence of what some consider “victimless crimes” aka, insurance fraud, that revolves around the roof replacement scams prevalent on the east coast. My car insurance didn’t move much either. I just paid my sister’s and hers went up $80… but I reduced it by reducing the annual mileage limit (it sits in a garage 98% of the time, so reducing from 10K to 7.5K is no biggie) and the premium dropped below the prior term’s rate.

Health insurance? Just paid my sister’s BC/BS Medigap policy. Just about flat for the same coverage. The difference for 2022/2023 vs 2023/2024 annual term was about the price of a 12-pack.

Our cable TV dropped $9…. lord knows why. Didn’t change anything. Canceled a streaming service that raised their fee 25%. Now they need 3 more subscribers to break even (and they’re losing them). Went with an alternative broadband provider and cut the monthly cost on that by 75% for faster speed and includes equipment vs. BYO from our prior purveyor.

Surviving in this climate takes a bit of work…. in our house, it’s a blood sport.

Gasoline is up. Car maintenance costs are about flat if you use the coupons from the dealer or go to an indy. I do a lot of minor things myself (like replacing a cabin air filter that the dealer wanted $90 to do for the cost of the OEM filter which was about $18 and 5 minutes of my time). Tire costs are flat with 3.5 years ago (bought another set of the same tire for a different vehicle and they were still $250 apiece plus installation just like they were in January 2020).

If by “transportation” you’re referring to public transportation, that’s a function of reduced ridership from “work from underwear”, increased fixed costs, legacy costs (union contracts), and the like. Airfare is high because of fuel costs, hefty increases in pilot compensation, and airport taxes. I rented a car in Orlando and the taxes and fees were more than the actual rental cost for a 10 day period. One of the perils of renting a car on the airport property.

The point is… even essentials are somewhat controllable.

ElK – a good reminder that one of the many votes one can seriously-control and make is the one from your wallet (not necessarily painless, though…).

may we all find a better day.

yep. I just had to replace the rear tires on my venerable old honda ATV spot sprayer. $400 to have a local tire dealer mount the new tires or ~$180 to have Walmart mount the tires. (huh? &#&&@!!! WTF! Either way, I had to remove and replace the rims.) Walmart got the job.

I just replaced 2 tires on an old diesel pickup (same local tire dealer mentioned above): just under $700! I just replaced 1 tire on another diesel pickup at another dealer: ~$350

Price gouging is alive and well.

I am using ancient equipment and repair costs are through the roof. This is not sustainable even with careful shopping and alot of DIY.

US industry cant compete given these costs of doing business.

This post must be sarcasm,

Inflation is falling: Says the media and Biden. If you shop or pay bills you know the truth

Conditions are loose: Treasury bonds say false

Consumers/ businesses not distressed: Ignore the layoffs, repossession rates increasing everything is fine

I wonder if the lack of distress is related to all the corporations that were able to issue bonds at rock bottom interest rates before the tightening. They may be sitting on cash earning a higher rate than their interest expense. Obviously some corporations need to refinance and are distressed, but perhaps it’s not a big problem in aggregate. Or at least the corporate bond market doesn’t perceive it as a big problem right now. The failure of the fastest tightening in history to cause more distress in the corporate bond market may be another distortion caused by ZIRP. Higher for longer seems like the best response.

Only really good companies were able to borrow for long term. Most get two to three years, and they will have to refinance at much higher rates, if they can.

An August 6 report entitled “The Corporate Debt Maturity Wall: Implications for Capex and Employment” from Goldman Sachs states:

“The path for interest expense depends on future refinancing needs and interest rates. Refinancing needs will remain historically low over the next two years—about 16% of corporate debt will mature over the next two years.”

If that’s true, it may explain the lack of distress now despite the rapid rise in interest rates.

Perhaps, but it doesn’t take a lot to cause disruption. Remember, an increase in unemployment from 4% to 8% is considered a major recession.

Even if most debt doesn’t roll over and most companies are healthy, the zombies going out of business and laying off their employees will cause plenty of damage.

when folks on the rational side of investing, etc., were wondering and asking why the federal reserve board, etc., were SO slow to raise rates,,,

folks forgot about the very clear time needed for the federal reserve board to communicate to their bankster owners what WAS going to happen

folks in those corporations connections, etc., ”borrowed” all the cash they could get their hands on knowing what was coming from the federal reserve board…

BTW, it should be clear ”corporation” is not the problem,,, as always, greed is.

any more questions??? LOL

Is it truly “greed” to refinance debt in anticipation of coming higher interest rates or is it simply good business?

Is it “greed” to refinance your home to a lower interest rate or is it fiscal prudence? Is it “greed” to move funds from a 0.01% bank account to one paying 5% or is it simply good money management?

As always, it’s YOUR job to protect yourself and your self-interests, not that of another. If you’re waiting around for someone to save you, good luck.

Inflation is sky high. We’re waiting on the numbers to catch up.

The interest rate spread between Treasurys and corporate bonds is not determined by the absolute level of interest rates.

The spread between corporates and Treasurys is determined by the perceived health of the companies which issued them, usually by looking at their stock price. The question you should be asking is not why increased interest rates have not affected corporate bonds but why increased interest rates have not affected the stock price of the companies which issued them.

FOMO.

There is no such thing as an ABCT curative recession. There’s too much money to mop up.

The economy is being run in reverse. The GINI coefficient has headed higher. Asset prices need deflated.

Tightening has been offset by massive government deficit spending. That’s taking pent-up low velocity money laying around from years of QE and injecting it into the greater economy via gov spending where it is now moving around, keeping revenues up and inflation hot because deficit spending is happening faster than QT. Deficit spending cannot run indefinitely without some form of printing to fuel it. Yield curves cannot be inverted forever. Over time, bond buyers (for both gov and corp debt) will demand ever increasing yields. The government will eventually be forced to start growing the money supply again, either when bond buyer’s money dries up or the next financial crisis hits. Maybe they’ll open up a frosty can of not-QE like they did last March, but on a larger scale. It’s going to look a lot like smooth sailing until then.

Right on! The failure of the Fed to even mention the elephant of government spending while addressing the abject failure of their monetary policy indicates that they are complicit in the dollar devaluation. They are just going through the motion pretending to fight inflation. Gold hasn’t been buying it, has finally decoupled from the phony rates that impact no-one.

Liquidity and the worst inflatiion in 40 years. Higher for longer please. So many firms bankers bond traders etc only know low rates because that’s all they have seen. Higher please Mr Fed Chairman.

I wonder, does this signal a decoupling of an allegedly viable consumer class from the bottom 50ish percent who seem to be edging toward credit delinquencies? Have the well-to-do found a discrete perpetual motion machine that can take flight from the negative stuff going on in this political economy, and just, like, trade bonds in circles with small risk premia?

We all heard about the K shaped recovery coming out of the pandemic, and it really hasn’t stopped. The reason there are so many contradicting narratives is because it depends which branch of that K you’re looking at. One group is doing great, another group isn’t.

The group doing great has all the money, are corporate beneficiaries or have wage leverage, and they are a bigger group, so that pulls up the averages and overall we still look good as an economy. The other group is stealing HVAC units from libraries and cat converters from cars, walking into fast food outlets demanding free food, camping in tents everywhere, boarding busses without paying or even glancing at the driver and raising default rates on subprime loans.

I don’t think income inequality has been solved yet. That to me seems like the eternal problem that is driving our decline into the abyss. But I digress, corporate bond volatility looks great!

IMHO, income inequality has plagued humanity for it’s entire existence on this rotating rock. There is no solution.. not even UBI as with UBI things would simply inflate to mop up those funds.

At least in the U.S., we have equal opportunity…. but the part that’s wasted on the masses is that there is no guarantee of equal outcome.

I understand that the most recent “little hump” occurred during the SVB failure.

For context, it might be helpful to get a brief replay of the main reasons for the 5 spikes where CMDI moved up to .4 reading or higher, and perhaps your view of policy actions that brought the CMDI back down again after each spike.

Thanks for your work, Wolf!

“Consensual Hallucination” is now baked into the current times. It is not just in finance but in medical, gender,education,”science” and other areas. This is a “post truth” epoch where lies are worshiped and truth has been kicked to the curb. Now that we are dealing in complete fantasy, it is impossible to predict what will happen. Anything is possible in delusions. And we all know that money is actually a fiction… don’t we?

that was a pretty powerful ‘non-bailout’

Ultimately it will be a falling money supply that causes the distress level to get uncomfortable. So… $2T to go?

If they continue to run off ~$70B/mo (big if) M2 won’t be back to 2010-2019 trend until Q1-26. I’ll be watching that one closely as well.

We’re definitely floating upside down in Schrodinger’s CatBox

In some respect, this is a post pandemic political stimulus game — but, it’s kinda working with infrastructure spending and running up a deficit that nobody cares about. The ratings agency downgrades are obviously pointing at the core rot in the system, but it’s acting like benign cancer cells.

That stealth political stimulus is working, but my on the ground reaction is, these projects won’t last forever and as time is being bought to juice the economy — time is running out with stupid stuff like bank stability, commercial office space and a long list of loans that are pretending to be unaffected by higher for longer rates.

Ultimately, the can will be kicked along, but eventually this hot potato dance with musical chairs is gonna slow way down, and as usual, all the obese stupid humans that are over leveraged, standing naked on the shore, will scream for swimsuits. Duh

The last of the euphoria and hopium being smoked. We’ll see just how long this lasts with the FFR north of 5% now. Took only a year at the same rates before the bottom fell out last time, and we’re just a couple months into it at this point. Plus last time we didn’t have trillions of stimmie-bucks thrown at us, though most of the herd probably used all that on consumer crap they’ll be hocking soon enough to pay the bills.

Wolf,

Have you found any precedent for this sort of market behavior? I would have expected junk bonds to react by now. Even in the late 1960s there was far less complacency.

Thoughts on this, and when it might end?

I’ve been marveling wide-eyed at the distortions of this economy over the past three years. There are a gazillion things that I thought could ever happen, and they did happen. Now I kind of take this stuff in stride.

Like the mortgage backed securities issued by Fannie Mae and Freddie Mac with Moodys and S&P giving them a low risk rating.

During the Great Recession, housing was clearly tanking and the credit default swaps were being priced oppositely for a long time. During times of trouble, there is much manipulation to hide bad news. We don’t find out who is doing the manipulation until all hell breaks lose.

Remember Enron silently losing 5%, day by day, for many months, on zero news, as people bought the never-ending dip. Then, when the stock price was $1 or so, the news of fraud finally broke.

Yes, it will be interesting to look back in 3-5year’s time I think.