Year-over-year price drops in San Francisco, Seattle, Las Vegas, Phoenix, Denver, Portland, Dallas, San Diego, Los Angeles, and Tampa suddenly.

By Wolf Richter for WOLF STREET.

Today’s S&P CoreLogic Case-Shiller Home Price Index for “June” is a three-month moving average of home prices whose sales were entered into public records in April, May, and June, and it still shows the seasonal effects of spring selling season, when prices typically rise on a month-to-month basis, but the effects began to fade, and the index rose month-to-month at a much slower rate (+0.9%) than in the prior three months of spring selling season (+1.5% to +1.7%).

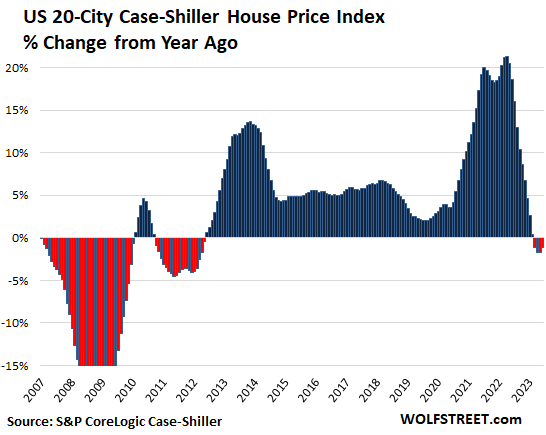

Year-over-year, the Case-Shiller index fell 1.2%, the fourth month in a row of declines, and the biggest and only declines since the end of the Housing Bust.

By contrast, the National Association of Realtors’ median-price index for July has already been released, and for July, it shows the first month-to-month dip in home prices after spring selling season, amid plunging sales. June 2022 had been the peak in the NAR’s index. The Case-Shiller index lags the NAR’s median-price index by a couple of months.

Of the 20 metros in the index, 10 had year-over-year declines:

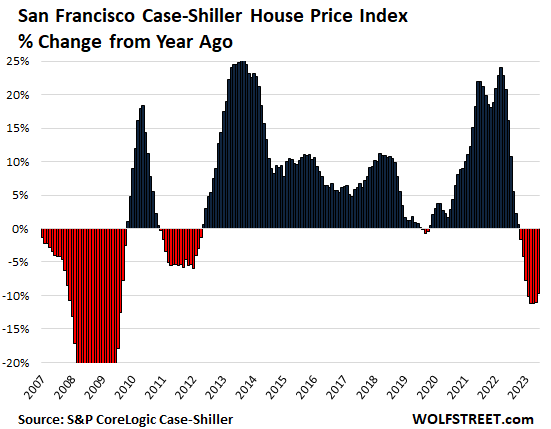

- San Francisco Bay Area: -9.7%

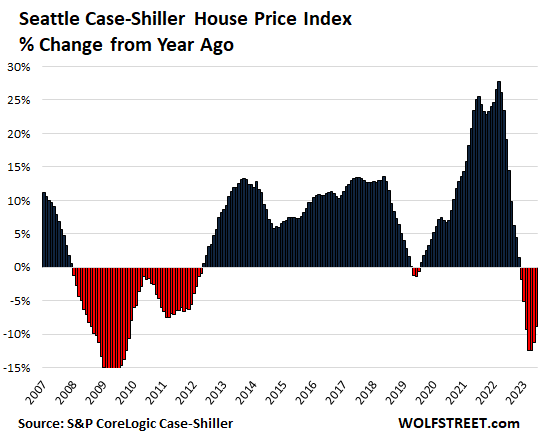

- Seattle: -8.8%

- Las Vegas: -8.2%

- Phoenix: -7.5%

- Denver: -4.4%

- Portland: -4.2%

- Dallas: -4.1%

- San Diego: -2.5%

- Los Angeles: -1.8%

- Tampa: -0.9%

Of the 20 metros in the index, 10 set new highs (YoY %):

- Minneapolis: +0.7%

- Washington DC: +0.6%

- Boston: +0.9%

- Charlotte: +1.7%

- Atlanta: +2.1%

- Detroit: +2.2%

- Miami: +2.5%

- New York: +3.4%

- Cleveland: +4.1%

- Chicago: +4.2%

The most splendid housing bubbles by metro.

The San Francisco Bay Area:

- Month to month: +0.1%.

- From the peak in May 2022: -10.9%.

- Year over year: -9.7%.

This was the 8th month in a row of year-over-year declines. Note during Housing Bust 1 the waves of declines interrupted by year-over-year increases that didn’t mean that the Housing Bust was over:

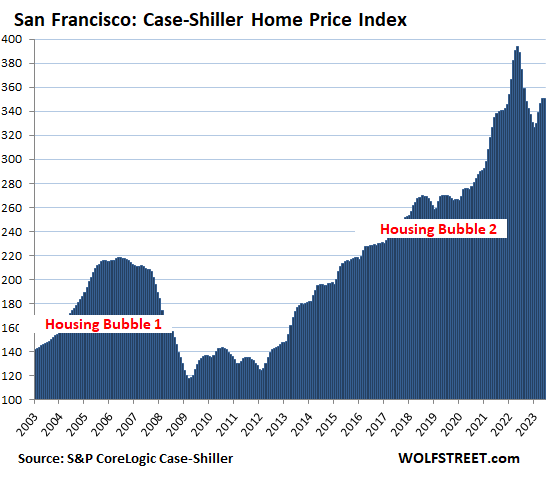

And San Francisco’s most splendid Housing Bubble in its full glory:

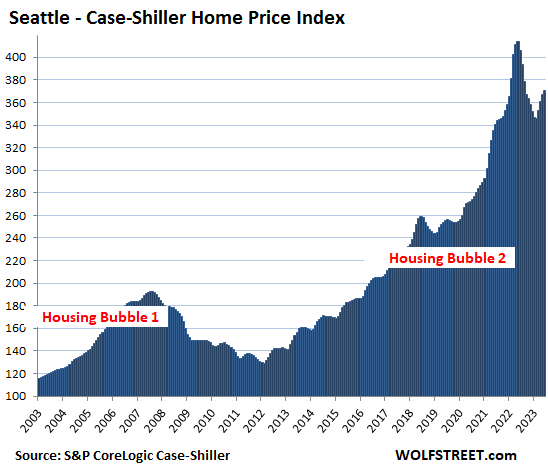

Seattle metro:

- Month to month: +0.8%.

- From the peak in May 2022: -10.5%.

- Year over year: -8.8%.

This was the seventh year-over-year decline in a row:

And Seattle’s most splendid Housing Bubble:

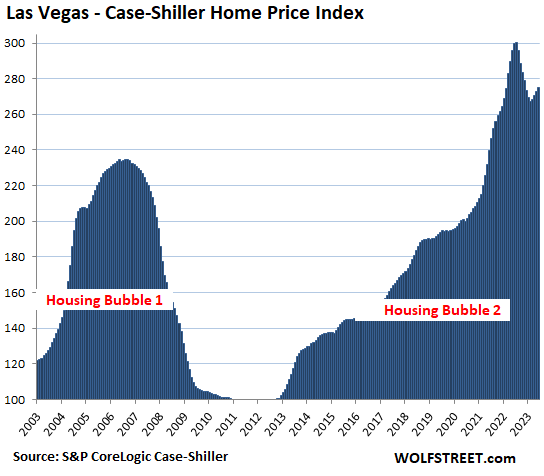

Las Vegas metro:

- Month to month: +0.9%.

- From the peak in July 2022: -8.2%.

- Year over year: -8.2%

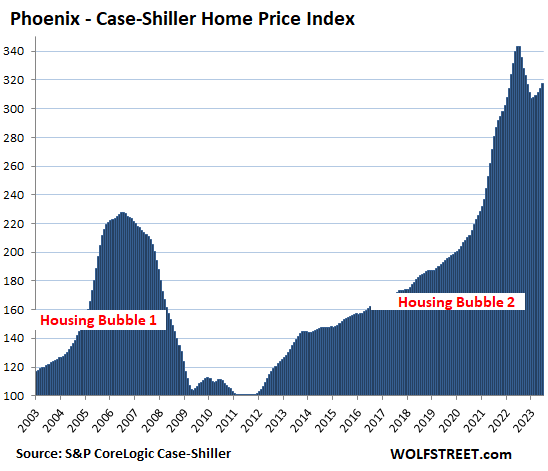

Phoenix metro:

- Month to month: +1.1%.

- From the peak in June: -7.5%.

- Year over year: -7.5%

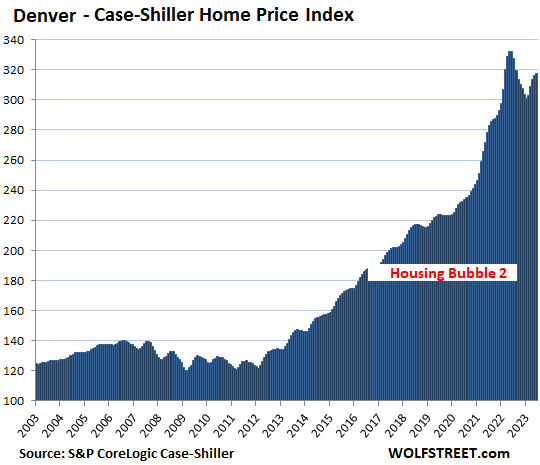

Denver metro:

- Month to month: +0.4%.

- From the peak in May 2022: -4.5%.

- Year over year: -4.4%.

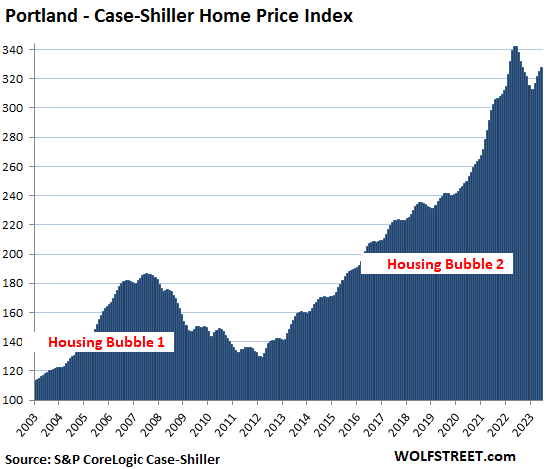

Portland metro:

- Month to month: +0.8%.

- From the peak in May 2022: -4.3%.

- Year over year: -4.2%.

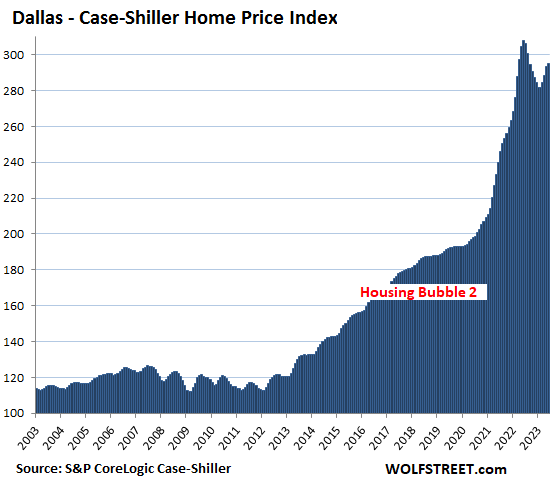

Dallas metro:

- Month to month: +0.7%.

- From the peak in June 2022: -4.1%.

- Year over year: -4.1%

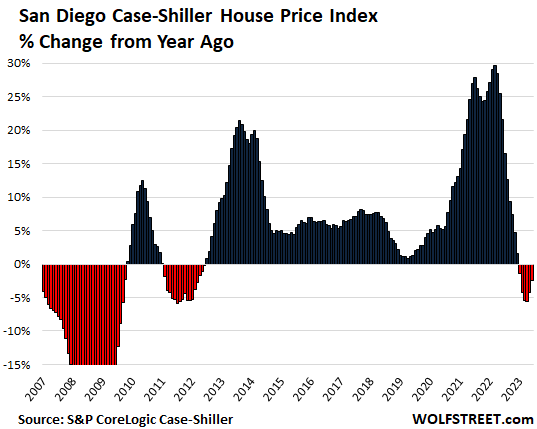

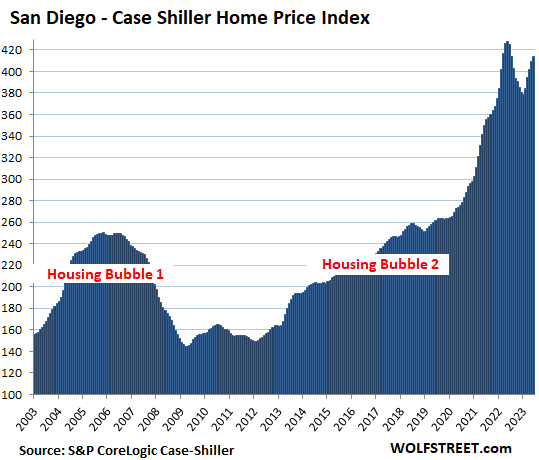

San Diego metro:

- Month to month: +1.1%.

- From the peak in May 2022: -3.2%.

- Year over year: -2.5%.

This was the sixth month in a row of year-over-year declines:

And San Diego’s most splendid Housing Bubble:

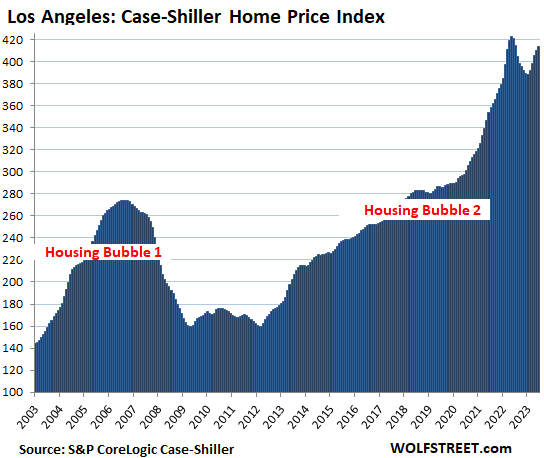

Los Angeles metro:

- Month to month: +0.9%.

- From the peak in May 2022: -2.3%.

- Year over year: -1.8%.

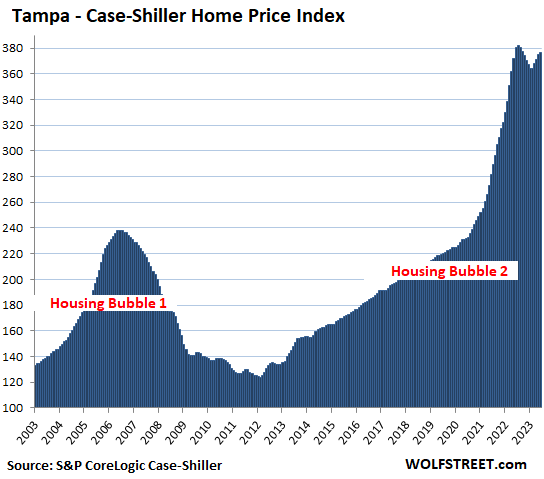

Tampa metro:

- Month to month: +0.5%.

- From peak in July 2022: -1.5%

- Year over year: -0.5% (first month of year-over-year declines).

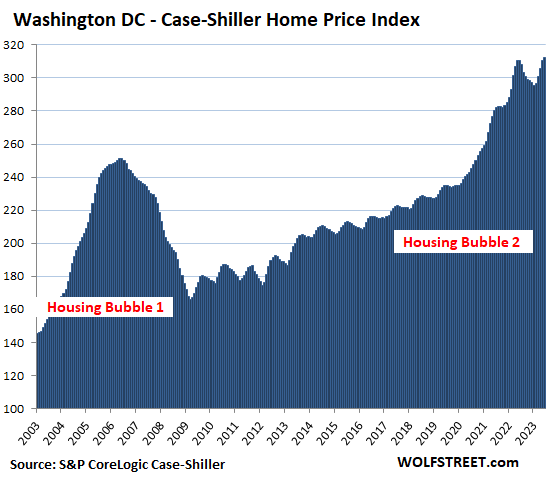

Washington D.C. metro:

- Month to month: +0.7%.

- Set new high in June 2023.

- Year over year: +0.6%

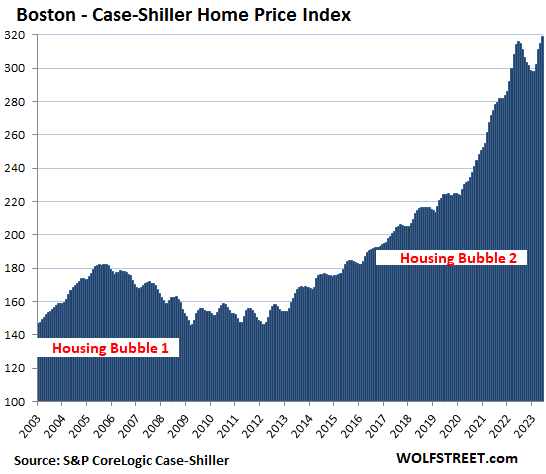

Boston metro:

- Month to month: +1.3%.

- Set new high in June 2023.

- Year over year: +0.9%

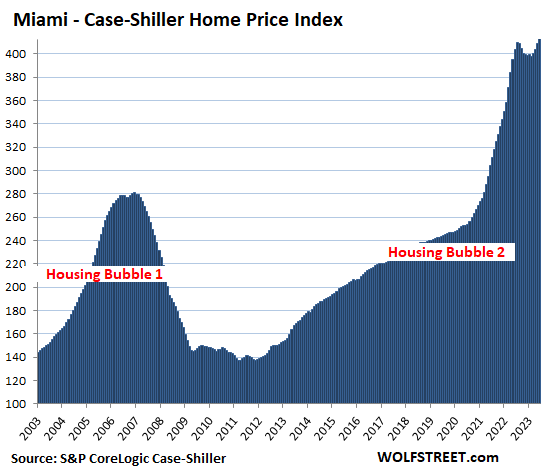

Miami metro:

- Month to month: +1.4%

- Set new high in June 2023.

- Year over year: +2.5%

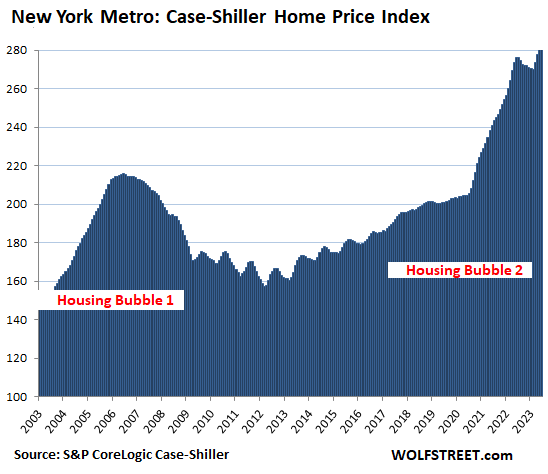

New York metro:

- Month to month: 1.1%.

- Set new high in June 2023.

- Year over year: +3.4%

The Case-Shiller indices were set at 100 for the year 2000. Miami’s and San Diego’s index values of 414 today are up by 314% since 2000. This makes Miami and San Diego share the spotlight of the #1 Most Splendid Housing Bubbles in terms of price increases since 2000, followed by Los Angeles.

Methodology. The Case-Shiller Index uses the “sales pairs” method, comparing sales in the current month to when the same houses sold previously. The price changes are weighted based on how long ago the prior sale occurred, and adjustments are made for home improvements and other factors. This “sales pairs” method makes the Case-Shiller index a more reliable indicator than median price indices, but it lags months behind.

The remaining six of the 20 markets in the Case-Shiller index (Chicago, Charlotte, Minneapolis, Atlanta, Detroit, and Cleveland) have experienced far less house price inflation since 2000, and don’t qualify for this list of the Most Splendid Housing Bubbles.

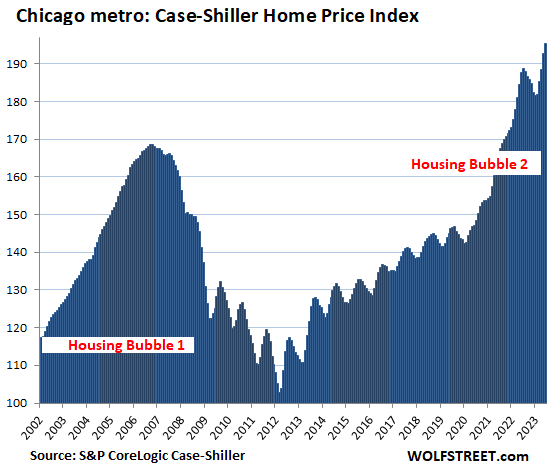

OK, Chicago anyway.

- Month to month: 1.1%.

- Set new high in June 2023.

- Year over year: +4.2%

Chicago’s index value of 195 is up by 95% from 2000 – nearly doubling in 20 years. While this is still a huge increase, the increase is 90 percentage points smaller than the smallest increase on the list of the Most Splendid Housing Bubbles, the New York metro, whose index increased by 185% in 20 years. And so Chicago doesn’t qualify for a spot on this list of the most splendid Housing Bubbles in America. But it’s trying for sure:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Housing bubbles have a way of popping.

The problem is that humans are herd creatures. The majority of people are inferior, always looking over their shoulder at what the Jones are doing. The true independents, like Warren Buffett, the Oracle of Omaha, are rather thin on the ground.

As herd creatures, the herd has previously “decided” that houses are “hot.” Therefore, prices rise to stratospheric levels. When a wave of pessimism sweeps the land, prices return to “economic” levels — meaning their near-rational value.

The lesson here is that the value of things is EMOTIONAL, not FACTUAL. Until we live in a land of Warren Buffetts by the million, this is going to continue to be the case. The End.

A fractal stroll down the yellow brick road to the reversion to the mean. Great values going to abound.

Sorry not in my area..Socal/oc paradise..

Buy now..date the rates, marry the house..lol

Ugh. I am selling a rental in Portland next week. It’s on the low end of the price around here so hopefully I can sell quickly. The new tenant laws give very little choice as when to sell. Pretty much have to wait til someone moves out now.

Thank you for pointing out so robustly what is wrong with the Fed policy on monetary policy, as opposed to they’re undisclosed policies on politics, ownership, religion, etc.

Housing bubbles may have a way of popping but this one is still inflated.

You do know that the story of Robin Hood from Omaha is a fairy tale ? Regardless, the equilibrium may very well be distributed, like a cloud, around the transition between when the market psychology flips from emotional to factual.

At this moment in time, it is my opinion, that the Fed policy is more protective of the aristocracy’s asset values than squelching a producer led inflation in full bloom.

Surely, it must be increased union activity and other little people demanding a pay increase so they can pay the company store economy they find themselves caught up in.

I used to think that, but I think it’s more that they’re terrified of a collapse under their watch.

I’m with Einhal…terrified blowhards promoted far, far, far beyond their abilities (vs. “status”/”rank”/”office”/”credentials”) = 20 years of Afghanistan, ZIRP, etc…with little resembling course correction, original thought, courage, leadership, etc.

In DC, it is far, far better to perpetually fail conventionally than fight the Establishment consensus.

“The majority of people are inferior,”

There a nicer way to say that and it’s not always the same people over time. If it helps, that rope tied around your ankle is attached to those of the “herd” and we are always stampeding towards one cliff or another!

That’s interesting and everything. But money is money in our bank account.

Housing, just like every other asset is governed by supply and demand. We simply still have an economy and market situation that supports high home prices.

The government continues policies that reward asset holders more than wage earners and stokes housing demand.

– The immigration policies create more people that need housing.

– Airbnb and other short term rental markets have created more demand

– Ownership by large funds is another demand creator

– Although there is a building boom in some sectors, government policies still add significantly to the cost and time to get new projects completed

– The mortgage interest deductions continue to reward people for putting money into equities.

For the housing market to really crash we need one of two things 1) distressed borrowers who are forced to sell due to job losses 2) a longer term decline that changes the psychology to a belief that not every home price will move higher.

I personally think that by 2024 we will see a bad recession and that will cause housing to begin the long downward process.

Ah, der untermensch. I really like you saying most people are inferior, sub human. Basically, you are a Canadian simp who does not have game. Clicked on your blog and it is mostly about you not getting girls and railing against rich folks. Peeping across the border expert of Americana, like a cheap voyeur.

Pathetic. Go rub your two Canadian nickels in anticipation of the fall of the U.S. I like my burger well done, no gravy on the fries.

“Think of how stupid the average person is, and realize half of them are stupider than that.”

– George Carlin

Thanks for the breakdown, Wolf. Where is the .02%/or virtually unchanged yoy I’m seeing being reported in other places coming from?

In addition to the “20-City” Index, Case-Shiller also has a “National” index (the data you saw), but CS itself only tracks data in the 20 cities. So this “National” index is based on the same 20 cities, but it’s configured differently and includes FHFA data (government). They’re close and usually it doesn’t make a big difference. I use the 20-City index because I know what’s in it. And it doesn’t pretend to be anything else.

Ah ok – thanks, I appreciate the response.

Boy that first graph sure is scary isn’t it? sarc

Sorry, but it’s almost a joke to write a home article about this. And the red looks like a trough. This has been the biggest sales recession non-event that anyone could have imagined.

As I’ve said many times over the past two years, the massive gain in population because we all know what down south is creating significant inflationary pressures across all sorts of things from housing to food.

But, it’s too much of a hot potato to talk about. Wouldn’t want to get labeled the wrong thing. And I’m not singling out any particular person. It’s just the times we live in today.

Good luck, JPowell, taming inflation under these circumstances with Congress running $2T deficits.

The crypto mentality has polluted people’s minds: If it doesn’t plunge overnight, it’s nothing. Housing is not crypto.

Housing markets at the national level move very slowly because the local markets tend to balance each other out, as you can see in the article!

Housing Bust 1 took FIVE YEARS at the national level on the way down.

“The crypto mentality has polluted people’s minds: If it doesn’t plunge overnight, it’s nothing. Housing is not crypto.”

But it sure moved like crypto on the way up. $40%+ gains YOY in some markets. That’s crypto-like insanity. We should see a wipeout in house prices, and quickly. Instead, we get the whole “watching paint dry” thing because the FED stubbornly refuses to sell their MBS in a timely manner, and all sorts of other shenanigans.

I read an article that stated and showed the numbers that the current Government stimulus programs has been higher then the Fed balance sheet reduction amount. Thus more liquidity is actually being created…..not reduced

This money has to go somewhere

On that point, I have to agree with Depth Charge. The shocking increases that were clearly happening in real time should have spurred Congress and the Fed into action, not to “monitor it” for over two years. It was one thing to dismiss goods inflation as “transitory” with supply chains and what not, but the price of housing should not have been so dismissed.

So, Einhal, do I understand you correctly that you’re advocating that the government (Congress, the Fed) should have been “spurred into action” and curb the precious “market forces”?? What happened to the “free market” mantra? Have you put a “socialist” hat on and put the invisible hand back into your pocket?

HowNow, are you an idiot or a troll? Your response only leaves those two possibilities.

Einhal – In reading some of Yellen’s notes during QE, the FED knew QE would cause asset prices to increase and the rich would become richer but the goal was to knock unemployment rates down. At the time unemployment rates were stuck in the 8% to 9% range. Hindsight is they probably did to much QE and kept rates to low.

It is better to have people employed and complaining about inflation then to have people unemployed with nothing to do and a lot of free time on their hands to maybe go out and cause problems.

When your working two jobs to make ends meet, you do not have time to go protest high prices.

But cheap money, has created high housing prices but at least it did spur a the building of a lot of multi-family homes (apartments). So there is plenty of housing units and this abundance of apartments should keep rent tame. (we hope)

The FED will not say so but I think they are okay with high SFH prices as long as unemployment is within their range. IMHO.

QE did zero for employment. QE was done specifically to drive up asset prices, and in particular home prices, to save investors, and in particular investors in banks. QE was a huge mistake, and there is now some recognition that it was a huge mistake.

there is a paper on one of the regional Fed bank sites that says that economists are divided on whether QE even does anything to increase economic output.

it was definitely ONLY a way of bailing out asset holders because the Fed cares only about rich people and was willing to screw over poor people with much higher inflation.

Wolf – From a Yellen FED speech in 2/11/2013. Your right about QE helping asset prices. Unemployment….your probably right about that too. Yellen specifically said they want to increase home prices. It did help the banks and investors but for the 65% of people who owned a home, I am not sure they are complaining too much. They have seen their home equity increase by 200% from about 75k on average to 230k. But these home owners are probably complaining about inflation in everything else

“Beyond the direct effects on residential investment from GFC, the extraordinary collapse in house prices resulted in a huge loss of household wealth–at last count, net home equity is still down 40 percent, or about $5 trillion, from 2005-7. This loss of wealth has weighed on the finances and spending of many homeowners. Households are less able to tap their home equity to deal with economic shocks, fund their children’s education, or start new businesses. For some households, the collapse in house prices has left them underwater on their mortgages, and thus less able to refinance or sell their homes.”

I guess the FED accomplished the goal of increasing Home Equity so people can send their kids to college. Home Equity exploded from around 10 trillion at the time of this speech to about 32 trillion now. Basically from 75k per house to 240k per house. Not

“What happened to the “free market” mantra? Have you put a “socialist” hat on and put the invisible hand back into your pocket?”

What kind of asz clown are you? Expecting the FED to DO THEIR JOB is not “socialist.” What an absolutely imbecilic comment.

“It is better to have people employed and complaining about inflation then to have people unemployed with nothing to do and a lot of free time on their hands to maybe go out and cause problems.”

It’s better to drive shelter prices out of the reach of workers, and create the largest homeless population in history, and at the same time anger people immensely? That’s some plan.

It’s really interesting how different one’s perspective on the market can be depending on whether you look at the chart showing percentage change in price y-o-y or if you look at absolute prices.

In the first case, it looks like we could be headed for a correction. In the second, the correction happened already and we’re headed higher after a brief pullback.

“and we’re headed higher after a brief pullback.”

No, what you’re looking at is the effect of spring selling season. And it’s already over. The NAR data already fell month-to-month in July, and will continue to fall for the rest of the year and into early next year.

The CS lags the NAR median price by about two months, and it’s going to fall with a two-month lag behind the NAR’s median price. So look for the first month-to-month declines in the CS about a more or two.

I did explain all that in the article. I’m not sure why I have to re-explain the same thing in the comments?

Below is the NAR’s median price. It shows you the seasonality of home prices, and that prices will drop for the next seven months. The question is how much. The NAR’s peak was June 2022.

It has always struck me the the graph for Portland looks like a scaled down version of San Francisco.

Could be, I know that some of the Portlanders’ think of the Californian migration into what they consider they’re state as an infestation by an invasive species. Some of the Montanan’s too, from what I hear.

Also Colorado and Idaho. I once saw an Idaho license plate reading GOBK2CA.

The infestation of California came from the Midwest, Northeast and South.

How – always overlooked history (ref: Woody Guthrie’s ‘Do Re Mi’. Massive numbers of folks moving here from the dirty thirties, through WWII and after, becoming the most-populous state in the Union by the ’70’s. Little surprise Master Berra’s saying of “…nobody goes there anymore, it’s too-crowded…” rings true, today (one person’s ‘crowd’ is another’s ‘community’). As one complains about the invasion of your heavenly slice by whoever, strongly suggest you get involved with your state’s gov’t and get long-term thoughtful about the management of future population increases other than wishing they’ll just go away (one might use the Golden State as a template of what, and what not, to do and avoid some wheel reinvention…). Otherwise, take the risk of a local analogue of that grim battle summary: ‘hit and overrun’…).

may we all find a better day.

Californians have absolutely ruined Portland, and parts of Western and Central Oregon. They come here with their “California” dollars and increase the cost of housing beyond what us working Oregonians can afford.

We can’t give all the credit to Californians though… wealthy folks from WA and other states come here to price us out of our own housing market too. If I had a dollar for every person I met here from the “Bay Area”, I’d have a down payment.

In the Halcyon days of my youth we had a great governor here in Oregon. ( Tom McCall ) who once gave a speech at the Oregon_California border. In short it was, ” please come to visit but don’t stay.”

…no doubt sold to them by your fellow Oryguniuns…

may we all find a better day.

The issue is bosses working young people to the bone and relying on them quiting and moving to your cheaper state with their savings. If young people were not treated like a disposable resource, perhaps less of them would leave Cali

No Houston graph? 4th largest city in America.

Houston is not included in the Case-Shiller Index. Back in the 1990s, when the CS was designed, they ran into big problems getting public records data in Texas, which doesn’t allow public access to deeds. But that’s where the CS data comes from.

To get the data for the Dallas metro, the CS people at the time worked out a deal with a Realtor association to get data from their multiple listing service.

And in terms of Houston, one of the founders of the CS said this:

“And when it was all put together, the decision was that was a bit of a hassle, so we’d stick with one city,” he said. Also, “we had Boston, New York and Washington so we decided that was enough for the Northeast, with apologies to Philadelphia.”

“The crypto mentality has polluted people’s minds: If it doesn’t plunge overnight, it’s nothing. Housing is not crypto.”

I do NOT have a crypto mentality. I am fully aware that GR 1.0 took 5-6 years to play out.

WE DID NOT HAVE $2T in deficit spending propping up housing / the entire economy. We didn’t have all of the influx of new people living here without the proper paperwork. And most importantly, we didn’t have the QE that Bernanke conjured into existence and the solidified into the running of the economy via COVID.

We are in a completely different world now, and you know this better than anyone. Making comparisons to GR 1.0 is totally apples to oranges.

Yeah I won’t believe the in the death of QE until I see what happens when the shit truly hits the fan. They’ve established the playbook and it’s one of their only plays. I really want housing prices to return to a saner world so I can afford one, but I don’t trust the Fed or the gov for one instance not to balk when the consequences of high rates start to really show up.

The Fed will do liquidity support, like they did during SVB, or after 9/11 or any time before 2008, which runs off the balance sheet quickly, as it did with SVB or any time before 2008 — they’ll return to how they used to do things before 2008, and they already reestablished the facilities they had for this before 2008 (standing repo facility) — unlike QE which balloons the balance sheet for years and then is hard to get off the balance sheet.

You can see the effects here:

BENW,

This “influx” of undocumented immigrants that keeps worrying you so much.

Have you even stopped to consider it might be your political masters trying to take advantage of you by scaring you with propaganda?

Here is a serious question for you:

Over the past 40 years, do you think the illegal immigration problem has gotten worse or better?

1. May be I am earning low or live in high COL, housing prices are no where lower for an older millennial to buy. Obviously, I am single and no need to buy other than food and rent.

2. DC metro area did not slowed down. There are so many cities nearby in VA or MD. The main reason is fed bucks. All real estate is local indeed.

3. Most millennials, you own nothing and be happy (?)

4. The paradigm is changing. Low fertility rate and no more marriages (or cohabitation), millennials and gen Z will not buy a house or make it a home. (May be i am wrong)

5. Who is really buying these homes? how they got money? What is their purpose?

“3. Most millennials, you own nothing and be happy (?)”

and

“4. The paradigm is changing… millennials and gen Z will not buy a house or make it a home.”

Those two are patently and ridiculously wrong. This is the kind of BS that only people post that never ever read any articles here. You said in your last post that you never read any articles here, and it shows. Ignorance is shining brightly.

Millennials are the biggest home buyers out there. They’re the ones that drove up the prices in recent years by trampling on each other and outbidding each other and buying sight-unseen. That’s a huge generation that are now earning big money, and they’re all over the place buying stuff. And Gen Zers are not far behind.

https://wolfstreet.com/2023/07/25/younger-people-drove-the-increase-in-homeownership-rates-over-the-past-few-years-census/

Wolf,

Excellent response. And analysis in the article too.

Not only are The Millennials making big money, they also stand to inherit $TRILLION$ of dollars over the next couple of decades as we aging boomers pass away.

Always find it entertaining nobody mentions younger Gen Xers (of which I am) as a child of boomers and who are also out there starting families, buying houses and buying things we need to start lives. The forgotten generation.

“That’s a huge generation that are now earning big money, and they’re all over the place buying stuff. ”

Thanks for pointing this stuff out!

We sold in 2021. Suburban location on an acre lot. House was well “used” needing updating but solid otherwise. Listed on Thursday, and signed a deal 10% above asking on Monday, yes with a Millennial. I was amazed, they waived all the usual contingencies. Over that weekend, there were 4 competing offers and several “lookers”. Offers were roughly same price but some had the contingencies, winning offer didn’t.

Both sides happy.

COBOL wrong again LOL

https://en.wikipedia.org/wiki/COBOL

https://en.wikipedia.org/wiki/Cobalt

A couple of years ago, “Cobalt Programmer” changed the screen name from whatever it was at the time to “Cobalt Programmer” as a joke, because someone had written “cobalt programmer” instead of “COBOL programmer.” If WOLF STREET comments weren’t so hard to search, I would try to find it for you. It was pretty funny, which is why I still remember it today.

I feel similar anecdotally. I know Wolfs data is true but my lived experience is that my circle of Millenial humans (I work in medicine in a hospital in Hawaii) is that my “generation” cannot afford SFH, even among the lower paid doctors ( IM/FM/peds). I do see the SFHs in the area are getting snapped up by people my age though.. .the people buying just aren’t from my island or in medicine… Im just bummed that it’s not me doing the buying and that I need to accrue more sheckles before I can make it work for my family. It’s the cost of living in a desirable place. Wolf thanks for the awesome work. To add the anecdotes though… the velocity of increase on my island is no longer 20% YOY. wohoo!

About southern CA: So after a massive run up in price in last 3 years, so cal has so far seen very little negligible drop.

For SoCal at least: These are noises.

So now SD is down 3% over 13 months, instead of being up 25% over the same period a year earlier.

So, I’ll just repeat:

The crypto mentality has polluted people’s minds: If it doesn’t plunge overnight, it’s nothing. Housing is not crypto.

Housing markets move very slowly. Housing Bust 1 took 5 YEARS at the national level on the way down. In San Diego, the Housing Bust took three years on the way down, from mid-2006 through mid-2009, and then revisited the low in early 2012. So that’s 5.5 years on the way down. Prices declined slowly at first, and over the years took on momentum, with steeper and steeper declines. Then there was a bounce, and then prices declined again to the 2009 low. That’s pretty typical. Nothing happens overnight in housing.

There are many cities whose housing bust lasted several decades.

I agree with you and hope you are right.

It went up like crazy and the downturn is sooo slooow and frustrating.

I believe affordable housing to be cornerstone of American dream and healthy society lest we turn ours in a rentier’s society.

I think housing won’t really go down unless we have a stock market crash and deep recession.

The power in place would prevent crash in ay of these assets and I hope I am wrong.

Wolf,

I don’t have a crypto mentality, but still think you need to modify your housing market analysis. From what I have observed in my nearly 73 years, the federal government never interferes with the housing market when prices are rising, even when the cause of the rising prices appears to be based on fraud. Think Liar Loans. The FBI was warning government officials about the fraud at the time. The federal government always interferes with the housing market when prices are falling. When HB1 burst, the Obama administration convinced Wall Street to buy up foreclosed houses rather than let those houses hit the market and lower the comps. Now, the Biden administration is inventing new mortgage programs to allow defaulting homeowners to stay in their houses rather than allow those houses to be purchased by other people who probably can afford to pay for them and maintain them. And as many of us have observed before, the Fed has been too slow to act. Sure, the Fed doesn’t want to break everything or anything. But why don’t our brilliant government leaders ever realize that a 50 percent increase in house prices in less than two years will inevitably break things?

1. “the Biden administration is inventing new mortgage programs to allow defaulting homeowners to stay in their houses rather than allow…”

Mortgage modifications are a classic way to prevent defaults – they have been done for eons. The lender doesn’t want the house, they want the payments. So they will do what they can to get the payments and avoid getting stuck with the house. This is standard practice. And it works in many cases. Same in CRE.

2. What’s different this time is inflation. Now we have big inflation, and it’s reaccelerating. And the Fed WANTS the housing market to come down as part of its fight against inflation. Instead of QE, it’s doing QT at the fastest rate ever, and it has hiked rates… this is the opposite of what the Fed did in 2008 and on.

3. In 2008, the Fed cut rates to 0% and started QE. Even then, home prices continue to drop for four years until they bottomed out in 2012. EVEN THEN! Now the Fed is doing the opposite.

4. “but still think you need to modify your housing market analysis.” 🤣😍 You need to get a grip on the new reality: higher for longer and QT.

“Now, the Biden administration is inventing new mortgage programs to allow defaulting homeowners to stay in their houses…”

You need to get better sources of information. The ones you are currently using are taking advantage of you.

Look for sources of information that actually inform you rather than ones that try to scare you.

There are many cities whose housing bust lasted several decades.

Would I be wrong in thinking, given the stochastic dominance of housing bubble 2 over housing bubble #1, that the reprecussions might be significantly greater than the collapse of housing bubble 1.

A tembler compared to hurricane Katrina, kind of thing.

As a 75 year old ex-Realtor I remember Housing Bust #0. In 1988 in CT, Days On Market started to lengthen. They were down to 18 days from listing to contract, a sure sign of mania. It started downstate in the Greeenwich area, where the Eighties Housing Mania started. It didn’t stop for TEN YEARS. Houses for working people dropped 50% in price ( I don’t use the word “value” now because I don’t know what it means). It took a decade to reach bottom and slowly come back to February 1988 prices. This was in CT, not Rust Belt Ohio, Coal Country WV, or Abandoned Potato Farm in Northern Maine. There’s a shitstorm coming, but I lived through one already. We won’t mention the price I paid. OK, I will. Divorce, foreclosure, and bankruptcy, the financial trifecta.

That was pre 1997. Since that time governments have pushed high prices relentlessly via:

1. massive push on immigration to increase demand

2. ZIRP

3. suppression of building permits to create artificial scarcity

4. endless rounds of bailouts

All of those are political decisions.

Not doing this will also be a political decision.

you should put that on a mug…

Wolf, so greatly appreciate your blog. I wish there was a thumbs up (or down) feature as I would give you a thumbs up for half your comments. Especially when you write, did you read the article? Or was it TL/DR?

Then there are markets like Bend, OR where prices hit ATH last month. No decreases here. Median $800k.

Official inflation from 2003 – June 2023 is 68% (more in real life) and should be deducted from the percentage increases, IMO.

Supply, demand and emotions…

Supply isn’t going to increase much until some external event causes homeowners to suddenly rush to the exits and dump their once in a lifetime 3% thirty-year mortgages. Most couldn’t afford to buy their same home back. Recession maybe? 2024? 2025? Election chaos 2024? Class warfare?

Meanwhile, buyers who aren’t buying new construction are stacking up like rush hour traffic in LA. Not everyone is priced out of the market by 7.5% mortgages.

Emotions? I don’t see any FOMO at this point, and I definitely don’t see any mad rush to sell either. The markets seem pretty stable.

The Case Shiller index IS AN INFLATION INDEX, it measure house price inflation. It is conceptually wrong to adjust one inflation index by another inflation index, such as adjusting “consumer price inflation” (CPI or PCE) by “wholesale inflation” (PPI), or “wholesale inflation” by “wage inflation,” or “home price inflation” (CS) by “consumer price inflation” (CPI or PCE).

You don’t like the argument that “if you adjust for the increase in house prices then house prices haven’t gone up”?

This is always a particularly silly thing when talking about housing because it accounts for something like 30% of the inflation weight.

CCCB, here’s some food for thought:

Case Shiller National Home Price Index June 2003 = 133.225

Case Shiller National Home Price Index June 2023 = 308.254

Do your own math and compare that to your 68%.

#5…may need to look at sale volumes otherwise it’s easy to assume everyone is doing this.

I’m continually amazed at what people can afford and not be house poor but Wolf’s other posts indicate people have money to spend so go figure.

Sales volume plunged around the country. But the Case-Shiller index is based on sales pairs, the price of the same house at various transactions over time. So it’s not skewed by a change in mix (median prices are skewed that way). This is the national sales volume, per NAR:

People are in two types:

1. people who earn money

2. people who were gifted money because they bought before housing detached from wages

The latter are able to own a home and upsize/downsize. The former are in the main not.

Chicago? As in within the city limits?

“metro” it says, LOL.

They’re all “metros” not “cities.”

I’ve seen other credible starts recently showing in the city of Chicago prcies have fallen about 4% in the year ending 6/30 while the rest of the metro area was up over 4%.

This downturn is starting to look interesting…keep up (or down) on that trend..looks promising..too bad the speed is like watch paint dry..only silver lining is when it’s dry it will be bright red, at least for most FOMO house humpers anyway.

I can’t wait for the comment that is about the comment that can’t wait for some anecdotal comment that well a housing in my area is different because down the street a house just sold over asking and this time is different! Someone always makes that comment and then someone else makes the other comment only to gets eviscerated or called out as a realtor. I thought I would just add to the conversation! Wolf love your analysis, and it will be interesting to watch as we go forward!

I’ll take the bait. I haven’t gotten torn to shreds in a while and am a glutton for punishment. I’ll do my best to hit every point with the best red meat I can. Here goes:

San Diego is different. There’s a geographic limitation here that creates a natural barrier to having land to build on…Mexico to the south, mountains to the east, Camp Pendleton to the north, and California’s largest untapped reservoir to the west. The politics, especially within the city of SD, are to destroy all SFR’s with multi family, which is a major increase in demand from developers. On a macro level, anything locked below 5% isn’t gonna sell anytime soon, and on the micro level in SD county, things cost so much here and there’s nothing available for replacement, you’d be nuts to sell.

How am I doing? I’ll let you know I’m not a realtor, but I know plenty of them and they tell me that there are gobs of buyers out there and demand is super strong, just not enough houses to buy.

Here’s the anecdote. A friend sold their house off the market as what I gather was a pocket listing. It sold for just a hair more than what the folks paid for it a year earlier (no work was done, same as it was). Small place in an older neighborhood, but it went for close to 1.2mil. They went to buy another place and made an offer, place was pulled off the market and relisted for 100,000 more because of all the demand. They asked sellers of another place they offered on to cover some fees, etc and were denied due to all the interest in it, and it was a POS flip.

Of note here in San Diego is that the m-o-m increases have been the case for a while and we’re pretty close to where we were a year ago. Wolf’s right, these things take time, but this time, San Diego is different. Cue the Wolf, and all his pups to feast on this.

Some Midwest Guy, was that pretty close to the comment you were looking for?

I livd in New England for 65 years. I don’t see how having Mexico as a border is a plus.

I am sorry. I didn’t communicate this well. Hopefully this helps although it may not. Your comment is the last in string of anticipated comments.

So my comment is in anticipation of comments like this from Jack M:

Jack M

Aug 22, 2023 at 12:59 pm

“insert anecdote about my local market behaving differently despite being provided contradicting data in 3…2…1…”

These kind of comments have been made in many of the threads concerning housing.

And Jack’s comment is in anticipation of comments like yours.

So I was just anticipating the anticipatory comments. So the irony of it is lost and it’s never funny if you have to explain it, so I guess a big swing and a miss on my part.

Anyway, thanks for commenting and look forward to other people’s posts.

Really enjoy what Wolf has to share and it’s been helpful as I am not all that financially savvy but have been able to learn and take advantage of short term bills in order to passively build our down payment fund without gambling it in the stock market!

How do you reconcile this:

“I’ll let you know I’m not a realtor, but I know plenty of them and they tell me that there are gobs of buyers out there and demand is super strong, just not enough houses to buy.”

With this:

“Of note here in San Diego is that the m-o-m increases have been the case for a while and we’re pretty close to where we were a year ago.”

With demand “super strong” and gobs of buyers with not enough houses to buy, it doesn’t seem possible SD can be down, even slightly, YOY. I don’t pretend to know how this plays out in SD, but what realtors are telling you doesn’t reconcile with what the market is actually doing.

The drug cartels from South Of The Border have no rules or treaties to abide by. They are a large, extremely well-armed guerilla army. They are well practiced in asymetrical warfare. If the US Air Force bombs one of their large drug labs, an entire innocent neighborhood in San Diego will be slaughtered and their headless bodies will be strung from highway overpasses. Hundreds of severed heads will be dumped on the front steps of the local grammar school. America does not have the stomach for this kind of war, but they have no problem supplying the demand for the drugs that cause all the problems.

I’ve lived in a lot of different places in the US.

My favorite places to live would be near the wine country of the Bay Area in northern California (where I live now), and various parts of San Diego County (and maybe places in and within 40-50 miles of Santa Barbara).

While these areas can and certainly have had housing price pullbacks at various times, usually related to economic problems, they are undeniably attractive in many ways, and will always have high demand over the long term. In my humble opinion.

It pays to keep an eye on economic cycles, buy during downturns, and hold for the long run, in desirable places like these.

In the long run? What did Keynes say about the long run . . .

The reason you just gave as to why San Diego RE is different are the same things that people said in 2005, just before the market began a 5 year implosion where values went down 40% countywide.

40%.

Yes — this was the party line back then, too.

roddy, that’s an incredibly grim assessment, but probably realistic. The problem is and always has been demand, the demand for those drugs.

Houses are not nearly the permanent store of value that many people think them to be. Home values can be affected by many things from crime to flooding to economic shifts.

A few weeks ago the most quaint, historic and beautiful beachfront town in America ( my wife’s hometown ) was wiped off the map by fire. Everyone one who owns property there ( from locals to tourists) will find the once high value of their property locked up for a very long time.

The towns infrastructure has to be rebuilt before any home construction can begin ( the water and power systems are gone) and this takes a very long time in Hawaii. All the debris have to be hauled to a toxic waste landfill ( of which there are none on Maui). Lawsuits between insurance companies, homeowners, the county and the power company will drag on forever. Then the entire town might have to be redesigned if it is to ever be insured again.

Once all that is done and people can start rebuilding homes and business’s the age of jet tourism will probably be mostly over.

Yeah another example of massive failures by the various governments in Hawaii from the local level all the way to state level.

All those wooden buildings jammed together along Front Street were a disaster waiting to happen along with idiots running the show.

Those poor people in the town suffered as a result.

As far as I know none of the areas in Kaanapali or Napili were damagaed by the fire though. The Whaler and Sherton Maui are up and running and all sold out.

Sheraton Maui was a great place to stay.

All those things are true, but the biggest problem is all the sugarcane and pineapple fields turned to tinder dry weeds. When my wife was at Lahainaluna high school the land on both sides of it down to town ( where the fire started) were planted in irrigated sugar cane and pineapple, as was all the land from Lahaina to Napili. There was a big sugar mill in the middle of town and lots of empty space around it. Those cane fields were burned off every year so the town was filled with tough men who knew how to handle fire.

When the sugar and pineapple industries shut down the fields were allowed to fill with invasive weeds that burn well.

The third generation descendants of the sugar cane workers are still there but the town has been built out toward the dry fields and filled with good-time-charlies instead of tough plantation men.

The wooden buildings on front street were a fire trap, but the condos and such built in the 2000’s burnt up just as well in the 80 mph fueled blaze.

fires, floods, hurricanes, tsunamis, tornadoes, volcanoes, sinkholes, earthquakes, collapsing buildings, crashing planes, asteroids . . . . despite great technological advances, mankind remains defenseless before the whim of fate . . . . .

vis – in referring to the various natural processes and their results, would say humanity remains defenseless in the face of its own willful ignorance and disrespect of them (though not discounting ‘bad luck’)…

may we all find a better day.

Very interesting that every one of the Case-Shiller home price index charts shows a sharp V-shaped upward trend at a time we are experiencing the highest mortgage rates in more than 20 years. I figured that as long as rates and inflation remained high the index would either stay flat or continue its downward trend, but the charts show otherwise. Is the bottom in for the home price index? I believe that its possible that the worst is over but this strongly depends on mortgage rates and wage inflation, which at this point basically translates to affordability. If mortgage rates continue to rise due to the Fed’s fight with inflation, affordability will decrease and this could lead us to a lower low in the home price index charts. This decrease in affordability is offset by the fact that wages are starting to move up as a reaction to inflation, which suggests that if there is a lower low it wont be significant. I recognized early on that this downturn would be different than Housing Bubble 1, and so far it looks like that was the right call. If mortgage rates/inflation stabilizes, then the worst is over and we should see a steady rise in the home price index. If mortgage rates/inflation starts declining, you will see an acceleration in the appreciation of housing prices. Buyers are not going on strike because they expect housing prices to rise just like everything else has in this inflationary environment. If negative amortization loans where offered today you would see a significant increase in sales and housing prices because what is limiting demand right now is not sentiment but affordability.

This is just the beginning of whatever has started. I thought the same in 2008 that home prices can’t go down in any meaningful way.

As WR stated, this may take few years to settle down whatever it is.

Something has to give to address the affordability issue.

You’re ignoring seasonality. Home prices have already peaked for 2023 and are headed down.

Look at the charts, do you see seasonality having a meaningful impact during the bust of Housing Bubble 1? In my opinion there is more to it than seasonality here.

Geez, that’s a long way of saying this time if different. Next time, save yourself the trouble and just quote what Lawrence Yun like to tell his believers..

You forgot to include, not in my area in your comments…you’re welcome

Hahaha….I don’t know what Lawrence Yun is saying but if he is saying what I am saying then good for him, although I highly doubt it.

NY up 3% — hahaha no wonder many of our friends here think the market can only go up. The returning of working from the office is forcing many to find houses around NY – pushing the market higher. Not sure how long this will last. I guess until there are some stress in the labor market.

I was just about to say the same…wtf NY, not making it any harder for a small family to buy their first home.

A small family in NY can absolutely buy their first home! Just not any of those poor or middle class working families. That’s not who this state wants nor caters to.

Perfect weather year round, no crime and low taxes to boot! Who wouldn’t want to live here?

Don’t forget the totally down to earth metro NYC culture of that is in no way painfully narcissistic, superficial and would throw down their own Grandma for a shiney nickel. Or so I’ve heard.

Wolf,

As I read your discussion about why house prices decline slowly, I got the impression that you were describing how you think a free housing market naturally works. In my opinion, what you were describing is partly the result of the fact that we don’t have a free housing market. Beyond that, I certainly agree that a free housing market typically will move up and down more slowly than the stock market.

Now with record QT and with 7% mortgage rates, it’s a lot freer than it was. And you can see it because sales volume has plunged. It’s not the same market anymore. Buyers have become scarce.

A Triple Black Diamond slope is the only way off this chairlift.

Maybe the buyers are scarce in other metros because they’ve all come to San Diego. There is no scarcity of buyers here. I just went through Redfin solds (last month) in 92115 and I’m seeing multiple properties that were on the market for no more than two weeks. I was stunned to also see that things are being overbid again, in some cases of $100k or more. Fixers are going for close to 900K in some parts of the zip. Before you rip me a new one, I can back this up but I’m certain the links will get removed. I then ran a check of all active “house” listings (not apartment, etc) and there are only 22 active listing in the entire zip as of today. This plays into exactly what realtors are telling me…they’ve got tons of buyers, but there’s nothing to buy. I suppose there can still be a slow motion crash going on, but it sure doesn’t feel like it here. The main caveat to this is that absolute junk is still sitting, which wasn’t the case a few years ago as people were desperately buying that up, too, but even marginally junk is selling again.

How are the geographic areas of these metros defined?

I realize this is just an academic question as the data is what it is, but… does the Boston metro include just the core cities (Boston/Cambridge)? Or anything inside rte 128? Or 495? Anywhere the T goes?

I briefly googled for this info but couldn’t find it. I’m wondering if homes in southern NH (arguably a Boston suburb) are included in the price pairs.

You can see them all listed and defined here:

https://www.spglobal.com/spdji/en/documents/methodologies/methodology-sp-corelogic-cs-home-price-indices.pdf

Whatever the message of the Case-Schiller Index may demonstrate it never was recognized as the only likely value it may have in catologuing the nominal rise in price of the asset.

Obviously, no one that is anyone recognized that it was a talisman, the precursor, to an out of control general price inflation.

At this juncture, the Index is suggesting that uncertainty deigns the future, Who the hell knows what’s about too happen.

In Chicagoland area, I have noticed more short sales showing up. I haven’t see them for a very long time. Today I saw two popup on Redfin. Upon quick look in public records, both of them show foreclosure notice date back to 2018, 2019 respectively. Both of them had second mortgage.

I think we are about to see foreclosure moratorium aftermath. Sure the number of foreclosures per year might not be out of ordinary, but when stacked up during “covid payment holidays” and suddenly released onto the market? This might increase available inventory significantly. Time will tell folks.

Been hearing about CCP is cracking down hard on outflow of capitals even more as they are dealing with some major economic headwinds. Which leads me to wonder if all this increase outflow of capital, it will just end up causing more demand for Chinese nationals to park their money in Chinese prefer neighborhood in SoCal, therefore keeping the price high. They have been that for years but will this cause this particular stream of demand to increase even more? (Hopefully not..)

Park money salvaged from one housing bubble thats popping (China) into another bubble that didn’t get a chance to pop yet (US)? I doubt it.

While I expect it will be 4-5 years before this inflationary cycle is over I’m starting to wonder just how much housing prices will actually drop. As inflation weakens buying power that’s going to have an impact.

I just can’t see housing dropping 30-40% without other manufactured goods doing the same, and I just don’t see automobiles, appliances, or machine tools dropping anywhere near that in cost. Especially when the unions are asking for, and getting, 40% pay raises.

Back when you could buy a house for $100,000 you could buy a new car for $7,000. When todays median car cost is over $34,000 that’s going to impact expected housing costs.

During HB1/2008, we had lot of people with similar mindset.

They had good reasons to believe that home prices can never go down, at least in my neighborhood.

As they say, the rest is history.

I don’t know if home prices would go down or not in the future.

Second hand price may drop a lot even if new prices do not. If price of new drop to much supply of new may vanish as builders go out of business. Not so with second hand, prices may drop without a drop in supply. At least not for a long time, houses last a long time.

Houses last a long time . . . with a lot of maintenance. $15,000 available for home repairs – Orlando- American Rescue Plan Act. Come and get it! Offer good while supply lasts – $1,000,000. What’s not to love! Don’t let that bubble pop!

If someone can’t do basic math, most likely being a homeowner is the least of their problems. I must be cold-hearted. Seems like this entire American Dream of home ownership is so . . . oversold.

It’s not sustainable. The percentage difference between current home prices and real disposable income (after taxes) is something like 80%. I don’t see how anyone can’t see this market for what it is — gonzo clown show overpriced.

So is the best option to continue to rent, if I’m a single Gen X first time homebuyer who missed out on the mad rush over the past couple of years in Phoenix?

My rent did not go up this year, I feel like I should count my small blessings where I can.

Simplify your life. Save, save, save. My wife and I did this. We rented and saved. We saved enough in 8 years to buy a house cash and have significant retirement money left over. I was 56 when we started this. Owning a house means unexpected expenses and a large piece of your personal time.

I am a married with kids Gen X first time home buyer in Tucson who is and will continue to rent and save. Don’t see any alternative as local home prices make absolutely zero sense. My rent went up slightly this year, but is still well below the insane rental listings I’m seeing online. I may end up paying cash for a home by the time these market distortions work themselves out.

google things like – regrets of first time home buyers, delusions of home ownership. Read everything you can find . . . and then . . . do whatever you want!

If you think these are bubbles wait until you see Eastern European RE market.

Tell us more?

I get daily emails from a few realtor sites about homes available in my area of Portland Maine located on the water (either ocean or lake). I’ve been getting these for many years now because I don’t currently live on the water and I would love to, but so far I either haven’t been able to afford them or I don’t like them. So the emails keep coming.

I also get emails when the homes are sold. And what is just crazy to me is all the recent ones are still selling way above asking price. Here are the two from this morning:

1. Asking Price $440K; Sold for $472.5K

2. Asking Price $720K; Sold for $779K

I think this will need to stop before the market starts really going down.

NE still has a lot of buyer pressure. Not seeing the exodus major metros have seen. Brother in central MA sold his house a month back, closed two weeks ago for 80k over asking (460k). Had north of 20 offers. Cute house, but corner lot. They waved inspection. People probably figure every year they rent is another 25 grand into the ether so it only takes 2-3 years before any premium on the house you pay is made up in rent avoidance. And rent will only continue to go up by double/triple inflation. Pure madness. Im just glad Im in a comfy spot to try and wait it all out.

Do they send you emails of homes that sold below asking price, or that didn’t sell at all, and that they want YOU to buy, LOL?

Just wanted to point out that looking at the highs vs. lows list, the geographical bifurcation is quite stunning. The housing “crash” (if you can call it that) is practically an exclusively Western US affair. The East is basically not impacted by any of this.

That’s one way to look at it. Another way would be to overlap the indexes and try to find a correlation with regards to timing. As with any analysis, there are lagging indicators, leading indicators and then there’s noise. For anyone who is in the market to buy/sell a home, these indicators should factor into their analysis.

But analyzing this stuff and charting it and finding trends is exhausting for the normal person. So emotions take over. It’s my hobby, how I keep my mind occupied.

Do they have special lower mortgage rates on the east coast?

No they have more buyers it seems likely due to generally lower prices.

Boston is strong.

Southern California is also doing well.

California Association of Realtors recently released July 2023 Report. Orange County, +5.6% YoY. LA, +0.6% YoY. San Diego, +4.2% YoY. Ventura, +1.0% YoY.

But, the Bay Area has weak spots. SF, -14.1% YoY. Napa, -13.1% YoY, Santa Clara, +3.4%. Marin, -8%.

So much for the housing crash.

From the California Association of Realtors, Southern California:

Looks like home prices following stock market.

In some markets, such as San Francisco, there is a relationship between home prices and the Nasdaq. I’ve charted that relation ship in the past. Now I may have to include cryptos. But it’s not in lockstep, and there’s a lag. And it’s not every little sell-off but startup-related problems that include a Nasdaq swoon.

Looks like socal came off its dip and is going up again. Is the bust over?

Double top?

That’s why SoCal is paradise, no housing bubble here and price will never crash, worst-case scenario is just a flat line for a little bit as most around here will repeat like the gospel or some kind of scientific truth…

The FED deliberately stoked housing prices, it’s called the “wealth effect” {sic}

But anyone who expects housing prices to collapse is going to be disappointed. This is not the GFC. Housing prices still fell when interest rates fell during the GFC. This time it will be the other way around.

But you’re not seeing that all. Look at the charts. It’s a slow motion train wreck. Collective delusion is powerful — there are some good and very thick books written on the subject — but all the manias & wishful thinking and willful ignorance in the world isn’t going to alter the course of that dot plot from its slalom toward overcorrection. That’s the way it goes. No big deal.

It’s almost as if people have forgotten that its entirely possible for home prices to not decline much at all even in the face of higher unemployment, like the early 90s…or even just keep going straight up, like the early 2000s. The difference is that housing was still pretty cheap in the late 90s so the Fed will probably be happy to achieve a sideways trend for the next few years.

So we have 2 housing bubbles, the second much bigger than the first. So what came after Bubble 1 as it deflated: the GFC.

What will come after Bubble 2 as it deflates: a recession. Hopefully it won’t equal the GFC, but given recent downgrades of banks as it is just beginning, who knows.

This talk and even expectation of ‘soft landing’ or ‘no landing’, is like saying ‘it’ll just keep bubbling along’.

Apparently it isn’t politically correct for Powell to say: ‘I’m trying to induce a recession’ but he did say ‘house prices must come down so Americans can afford houses’. But what else could cause values of the largest asset class to drop other than a recession?

Everyone’s role model for this situation seems to be Volcker. He laid the foundation for decades of prosperity, but first came the recession.

Inflation-adjusted Case-Shiller smooths it out a bit, at least on the national scale:

But we are still looking at historically high prices coupled with the highest mortage rates in a generation.

Something will have to give.

The CS IS AN INFLATION INDEX, of house price inflation. It’s conceptually wrong to adjust one inflation index by another inflation index, such as adjusting CPI by PPI, or wage inflation by PPI, or the CS Index by CPI.

Just because it’s conceptually wrong doesn’t stop people from doing it, obviously. But it’s still conceptually wrong. You can adjust anything by anything.

Now, how would GDP look if the Case-Shiller inflation index was used to correct for inflation. ;)

Sales and prices of previously owned homes are NOT in GDP either, or else GDP would be much higher, LOL. So why would you use house price inflation to deflate GDP when house prices are not part of GDP? The sale of assets, asset prices, and asset price inflation are not included — whether houses, stocks, or cryptos.

IF, I had a 3% mortgage, and WAS thinking about selling and moving, now would not be the time I’d trade that 3% for a new 6% or 7% mortgage.

I can’t remember if one of Wolf’s excellent articles had cited the number of outstanding mortgages counted by the interest rate. But I’d guess most of the currently outstanding are under 4% or 5%.

But you would move if the cost of the house you want ( equal or better than the one you have) dropped low enough so that even with a 7% mortgage you had equal or lower monthly payments than you do now. The only way for that to happen is house prices have to drop a long way. Hang on, that is where things are heading.

90% are under 6%

I also believe that it will pop as hell at some point, but all I see now it’s still inflates..

It wouldn’t surprise me if the ramp back in metro areas was due, at least in part, to a return to part time in office work.

Decelerating price increases do not necessarily signal the impending burst of a bubble. In fact, I remain unconvinced that a bubble even exists in our current housing market. Beyond the striking graph, could you present us with compelling evidence that supports your stance on the presence of a housing bubble? Thus far, I have not come across anything that has truly swayed my opinion.

“could you present us with compelling evidence that supports your stance on the presence of a housing bubble?”

LOL. You don’t see the evidence because you REFUSE to see it. There was no housing bubble 1, and there is no housing bubble 2 because I don’t want to see them. Problem solved.

Price to income are the highest ever. Simply not sustainable at rock bottom IRs, and far less sustainable at those interest rates. It’s a bubble all right. Bubbles can stay bubbly for a long time because of monetary conditions or loose underwriting standards, but eventually they just don’t make financial sense. The investors are already gone. The only ones left are the greater fool crowd: they win at first, then they cry then they go under. Usual story.

Exactly what cresus said. The only reason we even have a bubble right now is because of ZIRP. Just wait until those rates go back up above 5% and you’re gonna see what happens to all of those suckers that got sucked into this everything bubble (As old decrepit man shakes his fist aimlessly into the air)

Who cares, if you are not convinced, go buy more houses as your local RE will tell you, it’s the best time to buy now..before rate will go up more, if that doesn’t work how about rate will go down soon..either way great time to buy…bubble, what bubble pssh…

Good thing we don’t need to sway your opinion in anyway as you likely aren’t the one setting monetary policy or control the interest rate so your opinion matter very little

‘Beyond the striking graph…’

Like, the one that shows the reality?

That Boston market (which I believe includes southern NH Manchester/Nashua) is still cooking.

Was speaking with my realtor in Manhattan yesterday who listed a property for me. She’s very sharp and knowledge, no hype, no fluff. She said prices in Manhattan are already down 6% which I believe. Very little activity (although Aug is usually dead). She listed the rental at $8500 for 1850 sqft. Was gone in 2 days. Those graphs are scary. The last property I bought there was dec 2018 simply because it was a steal. Haven’t touched anything in the US since.

Wolf, is cresus your pseudonym? LOL

🤣😍 no

Homes don’t exist anymore. Only investment (properties). Even if the housing bubble truly pops, the would-be buyers will not be competitive enough–not enough cash, not enough down payment, maybe subjected to the layoffs through job insecurity. It will be corporations circling cheap(er) housing like vultures–ready to flip for profit or become landlords. The rich get richer; the middle gets more hollowed out; the poor have no chance. As an elder millenial, my heart is broken.

But just think of all the wonderful property tax increases that our renters are oblivious of! Civil servants should be overjoyed. Politicians even more so. My guess is the big increase in property taxes will probably result in increased rents. Maybe the Fed can keep goosing stock prices enough to keep up.

You have to zoom out and look at the macro, and resist getting all frantic or FOMO over a handful of innumerate jackasses who’ve been buying houses at or near the top. It’s like when some genius in a 10 year-old Nissan comes tearing down the interstate at 30+mph over the speed limit and gets a few other jackasses riled up to follow suit.

Look, there’s a blah ass’d-looking Apt B a few streets up from me…it was rented for $1650 just one little month ago in an area of Austin where the rents are falling. It went for sale last Sunday and is pending or active under contract or whatever the hell for $425K as of tonight. That leaves a carrying cost of over 3K a month and the buyer’s out almost $100K in cash for which they could’ve been getting ~5% annually parked in a CD somewhere. Instead, they’re now instantly upside down and paying nearly double what they could’ve rented the place for. Now I could extrapolate from this how hot the market is and how there’s just no stopping the appetite for real estate; but it’s ultimately an isolated incident of another fool and their money. It’s not a trend, it’s not a bellwether…it’s not an indication of this time/this place is different; it’s that last gasp thrashing you see as a housing market dies. If you see two instances like this in a week, it’s easy to miss the forest…but it’s there, and it’s burning down.

Bravo, well said and 100% agree. Unfortunately, even now it seems like we’re the crazy guy at time square yelling at the wind…

With the exception of HB1 and let’s say the period between mid 2021 and mid 2023, what you are saying is pure and complete nonsense for the majority of people who are interested in building long-term wealth in a diversified way. I am sure you’ll agree that counting on 5% CDs is not a long-germ strategy and that it does not build wealth – especially when inflation is higher than that. And if you agree with that, then think about what you are actually saying in your post and how nonsensical it is.

Also – you have to realize that a lot of people are making a lot of money these days. And yes, some get laid off and others – many others – keep their jobs. In the present day, an average sales rep in their 30s working in tech or healthcare earns $250K per year. Some reps earn $500K or more. The best reps at my company earn $750K per year and get nice watches to go along with that. So can you see how that $3K carrying cost can be completely justifiable? The savings from not having to pay income tax in Austin more than pay for property taxes and in fact almost pay for the entire nut in your example. You really should not call such folks jackasses if you can help it at all.

The way it works for most people is that they pay off their real estate loans before they retire, or downsize by leveraging the equity in their home. It’s a lot better way than having to paying rent for the rest of your life. And you have an asset you can leave to your offspring or charity. Or both, if you were wise to own rather than rent multiple properties.

Totally wrong in your comment about QE not increasing employment.

How do you think all those companies losing millions and billions were able to raise funds at cheap rates and then hire people?

A lot of them are on your imploded stocks list.