They’re making good money and got on with their lives. This demand, fueled by low interest rates and FOMO, was part of the force behind the price surge.

By Wolf Richter for WOLF STREET.

It has never been easy for young people, when they start out, to buy a home. “House poor” and “house broke” are time-honored expressions that have been around for many decades, and for a good reason, because when people are starting out, they go way out on a limb to buy a home, and then cannot afford anything else because the mortgage payments eat up much of their income.

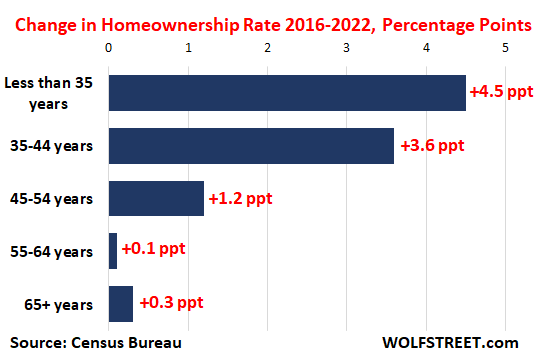

Yet homeownership rates of younger people have actually increased. In fact, most of the increase in the overall homeownership rate from 2016, and nearly all of the increase since 2019, through 2022, was driven by people under 45.

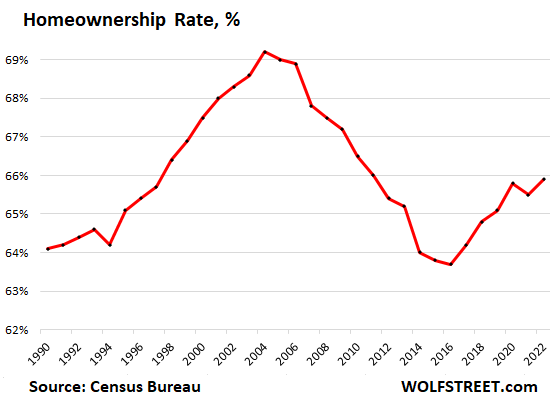

The homeownership rate overall peaked in 2004 at 69.2% and then fell for 12 years until it bottomed out in 2016 at 63.7%, according Census Bureau data. What we’ll look at in a moment is what age groups were behind the growth in homeownership rates from 2016 through 2022, and from 2019 through 2022.

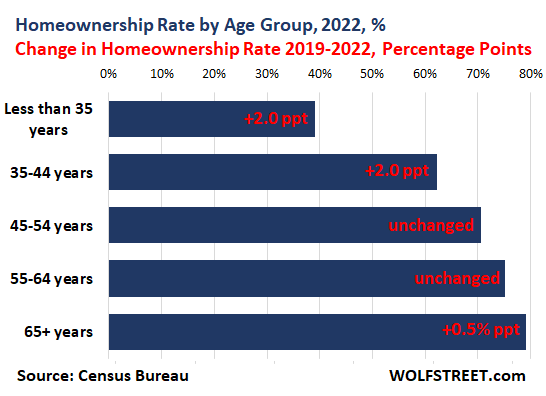

The Census Bureau’s report on its Population Survey/Housing Vacancy Survey, released today, sorts out the homeownership rate of “householders” – people in whose name the home is owned, being bought, or rented – by age group for two time periods: from 2016 through 2022, and from 2019 through 2022. And growth in homeownership rates for both periods was driven by people under 45 years of age.

Homeownership rates between 2019 and 2022 include the year before the pandemic and the year afterwards. By age group:

- Less than 35 years, homeownership rate: +2 percentage points to 39.0%.

- 35-44 years, homeownership rate: +2 percentage points to 62.2%.

- 45-54 years, homeownership rate: unchanged at 70.5%.

- 55-64 years, homeownership rate: unchanged at 75.1%.

- Over 65 years, homeownership rate: +0.5% to 79.1%.

From 2016 through 2019, homeownership rates increased by age group:

This is an interesting revelation – but not a surprise – because it leans against the often-repeated media story that younger people have been locked out of the housing market or whatever.

It has always been tough to get started for people on their own. But many young people in the 44 years and below age groups have moved their careers into high gear, some are running companies, some are in Congress, some are in state and local governments. Tech and social media companies and lots of other companies are largely staffed by them, and they’re making good money and have gotten on with their lives.

And their demand (millennials are a huge generation), fueled also by the low interest rates at the time and likely by the fear of missing out (FOMO), was part of the force behind the surge in prices.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I appreciate not only the % increases but also a % of the under 35 yo age group ownership. We’ve all seen what the last few years has done to the home prices, and I’m still in disbelief that after a maybe small pullback fall of 22′ things are just crazy again. I know things are regional. I can’t figure out where all the money is coming from for the houses.. so to speak. I think when people say younger crowd priced out, I think that means a starter home under 100k days are gone forever…

I also wonder where the money comes from. I hope it isn’t that more recent buyers were told “marry the house date the rate” and figure they can live house poor for a while and then refi to make their payment more manageable.

A lot of the money has come from parents who have accumulated money or downsized homes and have spare cash. My daughter and her partner were able to put 50% down on their (overpriced) purchase, but they’re now paying 30% less than their previous rent.

Where I live, buying is a MUCH worse deal than renting at today’s prices. I imagine that’s true in a lot of places.

Also stock market gains over the last decade.

I arguably overpaid for my house, but put 30% down and my PITI is less than what I previously paid in rent.

The advantage to renting — including renting beneath your means — is a gambit of gradually diminishing advantage. Our rent is going up nearly 20% this year. Never seen a hike like that in my life. Currently debating options…

Rick Vincent,

“and figure they can…”

It is also possible that it is less than “reasoned process” than the Real Estate Industrial Complex simply cycling through the newest generation of suckers…who may have been too young/inattentive to fully grasp the mechanics/consequences of the the 2008-2012 housing apocalypse.

I always hope that the internet’s dissemination of knowledge works against things like this, but it may not…or may not *completely*.

The RE industry has grown addicted to moving hugely overpriced houses and is apparently willing to pump out a firehouse of horsesh*t to keep the grift going, rather than simply return to pre-2002 semi-sanity.

“too young/inattentive to fully grasp the mechanics/consequences of the the 2008-2012 housing apocalypse.”

We’ll see how this current situation plays out, but during the period you describe, my daughter bought her house in 2010 and subsequently sold it in 2016 to fund a career change. She made $255,000 net after fees.

As a byproduct of the purchase, her cost of housing was @$1,700 per month – all in (PITI, gardener, yada yada) for a 3/2 house of 1,200 square feet. The apartment that she vacated… all 850 square feet of it…. was $2,800 per month with one bath and outdoor parking. So… let’s see… $1,100 per month savings in purchase vs. rental ($72K)….. made $255K on the sale in 5.5 years…. the government paid her $10K to buy the house (remember that program?)…. and she got to deduct the taxes and insurance from her income taxes. And, no, she didn’t move to “the hood”. The house was in Clayton, CA.

Maybe some of the youngsters WERE paying attention.

Taxes and *insurance* should have been “taxes and interest”.

Im finding that sudden unwitting windfalls like your daughter’s were surprisingly common these past 7-8 years. I personally know of a bartender who made nearly that much selling her little hovel in Lockhart TX to some credulous, innumerate out-of-state buyers last summer.

I also suspect that these winnings and the insouciance they often effectuate have provided some of the fuel you’re seeing inflaming manias in various markets. EZ come, EZ go.

El Katz,

It is possible that somebody who bought mid/post collapse did okay if they held long enough.

That’s what happens if you are lucky enough to buy near a bottom.

But that’s very few people.

And…you are ignoring all the 2002-2007 buyers who might have had to hold to 2016 (or later) to break even.

In point of fact, about 8 *million* “homeowners” (16% of all households with a mortgage) lost all their equity to a foreclosure during the collapse.

That is a huge and unprecedented number – it was a ruinous collapse and there is no way to recast it.

All ZIRP did post 2009 was to partially re-inflate another massive idiot bubble, equally destined to pop.

I find it interesting how many comments over the past few years have been folks crying for the poor young next generations who will have to live in mud huts because they can’t afford to buy homes that the big bad investors are all buying up.

Well, it turns out, like all the other unresearched comments parroting the press and other uninformed newsmongers, to be totally unfounded BS. On the contrary, the younger generations are doing just fine and in fact are running the investors out of the housing markets.

I see now why Wolf gets frustrated about dumb and just plain wrong comments on his site. Why are these buyers suckers? They’re probably happy as clams, having locked in great mortgage rates we won’t see for generations to come?

Like lambs to the slaughter. A new generation of bagholders.

Occasionally some commenters allude to the drawbacks of home ownership. If you’re interested, google gbf delusions of home ownership. If you’re too far in, it’ll make you uncomfortable. But, there’s nothing wrong with delusions. As long as you’re not hurting anyone!:)

For tens of thousands of years human beings have been on the move. This entire idea of being stuck in one place – it doesn’t appeal to everyone. Maybe it’s genetic! You should probably invest in something, but not necessarily a house.

These people that go on and on about home ownership – they seem so . . . . so shallow. Everyone needs some sort of home, but not necessarily a house.

Agree. I’ve always been a troll and one of my favorite looks on a young persons face when I show up to a party is when they are brimming with pride. They exclaim ‘we’re finally homeowners!!!!’ My response has always been, “Wow! how did it feel to pay off the mortgage?” –I wait. And they look at me cross eyed. What do you mean? Oh… I say…. you have a mortgage, so, really, you are a Renter… from a bank. Lol. If the labor market turns, these people are certainly holding the bag. They just don’t know it yet… just like all those youngters who bought just before 08.

Your name seems appropriate. Why not say “Congratulations”… or say nothing at all.

March 8. 1975 – Episode S5 E25 – Mike Makes His Move

Archie and Edith are all excited and throw a mortgage burning party because they have finally payed off their mortgage. Meanwhile, Mike has completed his graduate classes and begins a fruitless search for new lodgings. Later, Mike and Gloria agree to rent George Jefferson’s old house-even though it means living next door to Archie.

Fact IS, without ANY DOUBT,,, no ”owner” in USA, anywhere or any how, actually ”owns outright” ANY real estate…

Don’t believe me, just try NOT PAYING TAXES,,,

GUV MINT(s) will and DO take away your property,,, and ASAP

IF you dare NOT PAY TAXes

TRY it,,, and you will find the reality of so called REAL Estate…

Just saying for all those everywhere, including the now

BARONS and DUKES and LORDs and LADIES,,, who, eventually, in spite of their ”connections” will get the same outcome

IF ”they”,,, in this case the they usually dumped on these days

One of the reasons we lived in an old coalminer’s home for 30 plus years. It was built upon sandstone piers and slowly rotted away underneath. After retiring we built a home directly behind and removed the old one.

Taxes went from $800 to over $4,000 after moving in. In those thirty years the difference in taxes paid the cost of the new house.

Oh I don’t know about that. Seems there was a certain group that got bailed out of a banking failure with greater than 250k in accounts…. jus sayin

We’re all lessors in some manner or other, making our monthly installments. I can count up all the things I truly possess free & clear on one finger.

Dick:

You pretty much *rent* everything. Even beer.

Some people find that there’s a lot more to life than counting nickels. At some point, there’s a need to have a sense of belonging. If you’re a gypsy that chases dollars, fine. Good on you. If you want to be part of a community, buy. Communities where home ownership is higher are more stable and normally have better schools and lower crime.

“If” the labor market turns… “If” someone launches a nuke. “If” there is famine and pestilence. “If”…..

But what if it doesn’t?

Looking back on history, what is the single largest asset a middle class family can have? It’s usually their house. Houses funded my parents’ retirement.. my in-law’s retirement… and, from 40 odd years of home ownership, the shack I live in now is a “free” house as the last one I sold I got every dime back we ever invested in real estate (which is presently invested and paying me), got the tax advantages and reduced income taxes for decades, and had enough left over to buy this joint in it’s entirety. How’d your renting work out for you?

Taxes? Out here in the boonies it’s $200 per month. Unincorporated Scottsdale zip code. Just got a notice that the county miscalculated property taxes a few years back and they’re refunding those excess taxes paid. Get any money back on your rent?

Look at a housing price chart Dick. I bought properties from 1990 thru 2007 and every one of them is worth a hell of a lot more than I paid. They’ve also been producing cash flow and tax write-offs for the past decade. Actually, it feels pretty good to have renters pay my mortgages down every month.

The losers are the permabear pessimists who never pull the trigger on anything and ridicule those who are willing to put their money where their mouths are. Don’t be a Dick, Dick. Congratulate them. One day their properties will be worth millions and free and clear, just like yours.

Bought my first home at 23. Bought second home at 33, kept old home and rented out. Sold both homes at 37. Bought third home at 38. Current living in it.

I did not need a home at 23, but it was 2008 and the prices were hard to resist. For those people thinking it’s over and they have no hope, don’t believe the hype.

You’re a regular Warren Buffett. And they say Millennials suck at math.

Here’s hoping

None of this applies to the current market.

Ethan,

It absolutely applies. When you look at the charts, depending on locality, home prices are peaking/have already peaked/are on the way down. This is the same period back in 2006. It’s just tough to accept it and the “I want it and I want it NOW!” attitude of some people clash with the market conditions.

For those that can afford it, it’s not a problem. But for most people trying to buy their first home, they don’t have a ton of cash to throw around and most have to stick to some sort of budget. I was a first time home buyer in 2008, and even though I had cash for a small down payment and could cover the closing costs, I negotiated a substantial seller’s credit at closing which essentially meant zero out of my own pocket. I need a co-signer because my credit score was not the greatest at the time.

The home was 1,500 SF, built in 1950, post WWII expansion of suburban America. Absolutely great construction, all solid wood joists, full plywood sheathing, 1″ tongue and groove boards on the roof, original oak cabinets. They don’t build homes like that anymore. The home needed new windows, new roof, bathrooms remodeled, kitchen remodeled, oak flooring refinished, etc. But I slowly tackled one project at a time, with cash. Different perspective today when a “starter home” for most people I know is a 3,000 SF home built in the last 10 years because they don’t WANT and “old” house. Or deal with the “horrors” of lead paint or they don’t WANT to do any work.

Rome wasn’t built in a day.

Great post. 50’s houses represent the last period in what was a zenith of construction methods & materials in America — asbestos, lead and Radon gas be damned!

Asbestos…. not as scary as it sounds. It can be remediated. If it’s in floor tile, cover it with another floor. I had some asbestos ductwork removed a few years ago. A guy with proper PPE, a plastic bag, and some properly marked tape to seal the bag (hazardous)… it was out in about 10 minutes. And, yes, he was licensed.

Lead paint? Only an issue if it’s flaking or you have a habit of chewing on the woodwork. It can be encapsulated.

Don’t look now, but radon is everywhere. Even in new builds. It can even be emitting from your granite countertop…..

Hell, I know — every other damned material is off-gassing this or that baneful compound. I’m ok with it. I love asbestos tile, and I lead paint looks amazing…deeper color and a gorgeous glassy finish.

Granite countertops need to die. Formica over Baltic birch ply is the modern man’s solution.

The problem with asbestos, cracking/leaking foundations and other charms of old post War housing is getting it to pass inspection and financed.

In this market, and especially for the past 2 years, a non-cash buyer can’t negotiate concessions for those kind of deal breakers and FHA rules can be prohibitively restrictive. Peeled paint? That’s a paddlin’. Now imagine trying to mortgage a house with asbestos tiles or a buried oil tank.

I had to walk away from accepted offers on all above mentioned issues. The cute, tiny, no frills 3BR/1bath 900sq ft in a Levitt community had cracked foundation causing roof leak and black mold, an issue that plagued the whole neighborhood. Once the bank insisted on structural engineer inspections and mold testing before contract, it was time to walk.

Old septic tanks, the suspiciously muddy front yard with a failing water main, etc. And at a time when contractors were few and far between and lumbar/materials were sky high. Rehab loan, FHA, conventional, didn’t matter, just wasn’t worth it.

Conditions will change sooner or later, but some of the assumptions made about first time buyers not wanting to roll up their sleeves on an old small home is not thought through. Even with financing secured, it wasn’t worth mortgaging $300k+ ($200k+ if you’re not in an expensive market) on a tiny fixer upper that needs another $130k in significant repairs most of which couldn’t wait/be tackled slowly over time, only to end up underwater with property taxes jacking up and student loans looming.

Survivorship Bias. Thats not quite the right term.

How about: Successful Bias. Yes thats it.

Lots of different posters here but 2 predominate:

1. More or less doom and gloom. Some have historical data to back up their concerns. Others its not much more than “you’re making a big mistake !” w.o. anything to support it

2. People who claim to have had huge success with buying real estate. I’m guessing most are telling the truth as to financial success. They perhaps exaggerate a bit if only in downplaying shortcomings of homeownership.

I’ve read probably 80,000 +/- 15,000 housing comments over the last 16 months.

Take a wild guess how many of these posts indicated their (not a statistic) real estate purchase did not work out well financially ?

Other than my own, two or three max !

You won’t read about it today, but huge number of homeowners in TX were seriously underwater in the late 80s, early 90s. Some walked away from their homes. My neighbors home sold for 23% less than what he paid for just 3 years earlier (new home 101k => 77k). My new home appraised in 1980 for 22% less than what I paid.

(89k => 67k). It sold 10 years after I bought it for 82.5k, 7% loss.

TX economy had taken a hit, S&L crisis, oil industry downturn.

Yet no one ever writes about this. Oh sure if you held on long enough (12 or so years) or if you sold for a loss but bought another home on the cheap and held long enough you probably profitted. But even after 15 years your profit was not anywhere near as good as investing in stocks (1985 to 2000… stocks averaged probably close to 15% annually).

Some though sold for a loss and couldn’t buy again. Or walked away from the home…bad for credit. These results… they never are told.

Why ?

Think of how many homeowners in Dallas, Austin, Houston, etc and surrounding suburbs this affected. Yet not one mention of it.

I find this bizarre.

Plenty of Californians (and others) have their glorious success stories.

Homes in Ohio, Illinois, Iowa, etc probably saw MUCH LESS gains in real estate than found in California in the 80s thru say 2020.

But its gloating Californians we so typically here from.

Successful Bias.

No that’s not it. Its:

EXTREME Successful Bias.

So lopsided as to make one seriously wonder if negative posts get deleted regularly. Either that or people are amazingly consistent in not wanting to discuss their failures in home ownership. Failures in the financial sense… they, like me, may have enjoyed the benefits of home ownership. I was lucky in one sense… I didn’t have any major maintenance issues in my 10 years of home ownership.

One of the most important things to understand about the US media: there are very important things that never or almost never get discussed.

Huge “errors” (I would call them) of omission.

So, yes, I have read hundreds of accounts of giddy homeowners who will brag no end about what a financial success it was. And I can count on one hand (with a couple fingers left over) how many times I’ve read of homeownership being a bad financial move for somewhere.

Its all good homeowners, its all good.

2 minor updates, just for the record:

1. “My new home appraised in 1980 for 22% less than what I paid.” 1980 should be 1990.

I bought the home in 1986 after all.

2. “I’ve read probably 80,000 +/- 15,000 housing comments over the last 16 months.”

These comments were in response to Wolfstreet, Yahoo finance, and numerous Utube housing related presentations (some of these people are realtors while others are not).

Of course the quality of these comments varies substantially. Trite ones are obvious.

Its the interesting ones with plenty of factual (presumably) support that provide difficulty.

How much can I believe ? Just how trustworthy are the facts really ? How sound are the inferences used by the

poster ? And as already stated, what relevant factors is this poster innocently or purposely omitting ?

Young folks pressured to take on debt at an early age for fearing of being locked out forever. Distortions from the Fed’s deranged policy.

Likely the most financially repressed (a.k.a portfolio balanced channel policy) generation…..courtesy the Economic Nobel prize winner who couldn’t see a gigantic bubble as clear as the nose on his face.

Young people being able to buy homes is good news, although how they are able to manage bubble prices is a mystery. In 2008 it turned out that people were acting irrationally and buying homes they clearly couldn’t afford, leading to mass defaults. Let’s hope that WR is correct and that the money is actually there for the bubble this time.

I saw data that on average down payments and mortgage to income ratios are now worse than the last housing bust. Common sense says we didn’t solve a debt problem with more debt, buy central bank staff have Phds that allow them to know what to do.

It seems a lot clearer if you break out another period – change in home ownership rate 2016-2018 – you get +2.5, +1.6, +1.2 etc. So this means that there was roughly the same or slightly less growth in home ownership within all age groups during 2019-2022 vs 2016-2018.

In other words, the crazy price growth of the pandemic did basically nothing much to overall trend of homeownership rates, which I guess is Wolf’s point. As to whether that rate is historically going better or worse for young people we’d have to go back a lot further.

My pet theory is that home buying for many young people is driven by inheritances, so inequality aside, you’d expect it to trend upwards now that we are entering peak boomer death (sorry guys).

Maybe it is inheritance… or maybe it’s DINK’s with significant incomes that can handle the nut.

Son and DIL are the latter as her Dad died broke, her Mom is nearly a welfare case (if not for their financial support, she would be), and we didn’t give them a dime because they’re ferociously independent. We did buy him some really nice tools, though. My son played the property ladder… bought a junk house, lived in dirt and drywall dust for a few years, sold it and made several bucks… he also learned, during that process, what not to buy.

The key, in my case, is always buy the smallest, crappiest house in the best neighborhood you can afford. Sure, it takes a few years to make it into what you want, but anyone who has ever bought knows that even the *perfect* house is going to get changed over time. Colors… flooring… lighting…. and why pay for someone else’s poor taste when you can incorporate your own poor taste instead?

Didn’t you do an article a while back about the coming generational cliff working it’s way through the US? So these young people surged buying a house, and boomers already own 2 and 3 houses a piece. As boomers age out and die all that product comes to market likely from heirs. Millennials might be a huge group as you say but they’re tiny compared to boomers.

Whenever the day arrives in 10 – 15 years and interest rates drop….boomers have left the stage and everyone that was holding a low rate mortgage finally feel like selling so will the heirs….all that hits market at same time….it’ll be glorious

I don’t think I have ever written about generations. I don’t do that sort of thing.

What exactly is this article about Wolf, if not that???

Just asking, cause my off spring and at this point almost all their first cousins are clearly within the generations you mention in this article???

It’s about homeownership by age group.

Aging population is a trend in the majority of developed nations–the US demographics almost mirror Australia for example. The reality is the 2 largest age segments in the US are still 30-34 and 35-39 year olds, aka prime homebuying years. The points made in the comments above might be part of what you’re dreaming will happen, that is, parents are selling some of those assets or passing them to their heirs early. Time will tell, but we’ll be looking at the greatest wealth transfer in history as Boomers die off and we’ll all learn together how that impacts financial markets as a whole.

Millennials are already the largest generation in the US. They passed Boomers a few years ago.

I don’t know where you got the idea that the Millennial age group is “tiny” compared to Boomers. In point of fact the Millennials surpassed the Boomers in 2019 as the largest generation. While there were about 12 million fewer live births (inside the US) of Millennials… immigration was fairly stagnant during the Baby Boomer generation. In the end the difference is only about two million people… so far!

https://www.pewresearch.org/short-reads/2020/04/28/millennials-overtake-baby-boomers-as-americas-largest-generation/

Just keep the Healthcare industry from getting it first.

“boomers already own two to three houses apiece”. Hahahaha!

Yeah… maybe one in a hundred thousand. There’s probably more living below the poverty level.

The wealthiest people I know, and they are very very well off, Lease a place of residence and every other depreciating item. They then claim it against taxable income. They put their money to work elsewhere and have the ability to move quickly should something happen that requires a quick transfer of Capital to purchase something that is a distressed asset, for sale quick.

Me, I just keep paying to hold the old home I own, paint and repair it, replace ALL the things and they…… go on Silversea cruises. I am a dumb schmuck

Thunder,

Leasing property doesn’t automatically make the payments tax deductible. In particular, a leased personal residence is seldom even partly tax deductible.

I’m guessing they are claiming that big part of it (65%) is used for business activities.

Nissan fan,

Here is some tax information about using your home for business purposes. Frankly, I doubt that anyone can legitimately claim 65 percent or anything close to that percentage.

https://www.irs.gov/publications/p587#:~:text=You%20can%20have%20more%20than,for%20that%20trade%20or%20business.

“I’m guessing they are claiming that big part of it (65%) is used for business activities.”

Can you spell “IRS audit”?

I’ve been on Silversea cruises too. Leasing a vehicle is only worthwhile if you can write it off – but don’t try and do 100%. A personal vehicle lease is kind of a waste unless it’s heavily subsidized or you hit the lottery on residual roulette.

The best *fib* is depreciating asset and house in the same sentence. The b*tching is about how houses have increased in value and are unaffordable. If they *depreciate* as you claim, then the value at some point should fall to zero. Please show me where the free house is.

The idea way back when was to park money in Switzerland and into offshore tax havens. All the people I know did this.

As long as you don’t try to spend it, you’re fine. I know a character who would hire a private plane and go to the Caymans with a suitcase full of cash every year.

Was a great plan until someone narc’d on him.

Whoops. He’s now BK. You can get a good deal on his manse in Huntington Beach. I’m waiting for the IRS to go after the houses he bought for his kids.

How many of those young folks who bought homes did so while on student loan forbearance expecting forgiveness? Now that payments are restarting, we are about to find out.

If you look at Wolf’s house price charts, house prices have now become nearly as volatile as SP500 with ups or downs 20% plus in a single year. Surely this is poor monetary policy. I think it all started with Greenspan.

I was reviewing some of the magnificent 7 last night. If I remember correctly Microsoft had a P/S of 12, and a PE of 36. Its like the tech bubble never happened. Its all momentum I suppose. I don’t think there is enough growth in the world for trillion dollar companies to grow into 30 – 50 PEs. Math doesn’t work.

When you print trillions of dollars for no reason, no one has any idea what money is worth. That’s why we’ve had this volatility over the past few years.

If you give free money to people for not working no one has any idea of what money is worth either.

The student loan stuff is all political theater. The current repayment plans are all stated income, and they restrict payments to, I think, 5 or 10 percent of income now. There’s really no reason that student loan payments would cause a default or excessive hardship at least from a monthly payment perspective.

But, I know some of those same young folks who have received raises of 20% to 40% over the past 3 years.

Maybe it is a wash

If you have sizable student loans – you were probably never going to qualify for any mortgage.

As I suggested elsewhere – I think Wolf’s article is probably a red-herring because a lot of elderly parents are quickly implementing Life Estates that name their children.

In other words – young people are showing up as homeowners not because they are buying homes – but because they are being quasi-gifted them.

A mortgage loan officer who can’t look at an applicant’s credit report and include future student loan payments in a DTI calc should be fired.

I applied for a mortgage with student loans during the pause. They estimated what my payment should be and included it in my DTI. Lots of risk models exist for this very purpose.

Head over to the subreddit thread /FirstTimeHomeBuyer and take a read there. There has been a significant uptick in the number of posts about buyers’ remorse, primarily from FOMO purchases made during the pandemic.

I’ve been watching Zillow listings in my area. A few things I’ve noticed are that the houses that sell sell for far below listing price (although still way more than 2019 prices).

Another thing I’ve noticed are a huge flurry of listings by people who only bought in the past 2-3 years. I don’t know whether that’s a result of people being made to come back to their office (in another location) or whether it’s a result of people regretting having paid bubble prices in 2021 and 2022 and trying to get out unscathed. Either way, it’s interesting.

In my area I’m seeing them selling for 5 sometimes 6-7 percent HIGHER than the upper-end of the Zillow range.

And it’s not all that hard to verify this because there are very, very properties that are being placed on the market at all.

Yeah, my wife and I have given up on ever owning a home.

We were initially planning on 3 kids, but we have also decided that kids are probably not in our future either. We don’t think it’s fair to bring kids into this world without a stable home.

So sad.

Kids don’t care about the house that much. They don’t know any different. Parents use the kids as an excuse to justify the house. Growing up the kids that lived in the big rich houses were often the boring ones.

I raised 2 boys in a rental until they were 8 and 6, when I jumped back into owning. Owning the house vs rental didn’t make one difference to them.

Home ownership has been a coyote/roadrunner situation for me as well and I’ve been renting long before two lines appeared. So as far as renting with kids, it’s difficult if you rent from typical scummy landlords and have to inevitably move every year or two. Especially hard on them moving in the middle of the school year and out of school districts. If you are in a good renting situation with halfway decent landlords, which certainly seems increasingly rare, its not bad at all.

Has there ever been a time when the growth of home purchases WASN’T the age group of under 45?

You misunderstood the entire topic (did you even read the article?). This was NOT about “growth of home purchases” but “increases in the homeownership rates.” Meaning a larger percentage of young people owning homes. And yes, homeownership rates plunged from the peak in 2004 until 2016. And since then, homeownership rates have risen.

I like your article – but I can’t help suspecting the “ownership” %s are being inflated by Life Estates (or similar). Those have become very common in Massachusetts in the past 10.

Two kids, both in there late 20’s just bought the house across the street for $400k. The hubby is an engineer for Lockheed and the wife works in sales. I’m sure they’re knocking down well over $200k at that tender age.

My niece is a purchasing agent for Lockheed in Fort Worth. She makes $125k at age 32. Good to be funded by the government.

Seems everyone wants an F-35 these days.

‘Good to be funded by the government.’

At the next large gathering where you know a bit about the people, look to your left, look to your right, look all around you. Any questions?

Smaller government would be terrific and a smaller defense budget as well. However government spending generally rises with inflation until the next crisis then jumps higher accordingly with new divisions of government.

I’m in my late 30s, making good money (a physician with no student loans), and renting a small apartment. As far as I’m concerned, if you have to borrow money from a bank to pay for something, then you can’t afford it—and if you’re making payments on it to a bank, then you don’t really own it.

You can live your life however you choose. But I find your justifications stated here to be in a word… “Absurd.”

You will NEVER be a owner of a home that you rent… but a home that you “buy” you will in fact be a ten percent owner of from the day that you sign the paperwork… and that stake in the property will only grow with time (and payments). Even better… your “partner” in this endeavor (the bank) will have pretty much ALL of the risk for the 30-year life of the loan. At the end, you will have an asset that you can sell for ALL of the principal PLUS all of the accumulated growth in the value of the property. Meanwhile the bank got stuck holding the bag… earning one to two percent for the life of the loan… the difference between the mortgage interest rate and the cost of borrowing that money from depositors, investors, and the Fed. The same inflation that makes the asset grow in value for you absolutely destroys the value of the bank’s percentage of the endeavor.

You assume asset prices never decrease and that leverage has no risk to you. There are real costs to ownership that aren’t all that different from renting. Granted no one works for free and the land lord will take their cut, but don’t pretend that homes are an investment. They’re just a place to live. Even if you sell your inflated asset free and clear, then you can either rent or buy another inflated asset for the same or greater price. You still need a place to live.

This article needs to be shared widely.

At some point or another mortgage rates will slow demand but the other day Wolf made a good point that supply of existing is restricted due to folks not wanting to give up those sweet rates by selling.

This ought to driver rates up some.

Interesting that for the first time in a long time Alaska air admitted slowing in their business. They are big on the west coast. Airlines and housing used to be considered canaries in the coal mine. Airline stocks are starting to crumble. Could be the price of oil or it could be business conditions. Something to watch.

Alaska Airlines used to be a notch above most other airlines in service and pleasurable to fly with but in the past few years all that has disappeared and now they’re among the more shitty airlines so I’m not sure if their decline in business is due to the economy or just the fact that people like me don’t like to fly with them anymore.

Fedex is another company that is considered a bellwether company but anyone that uses them knows their service is an absolute nightmare so any decline in business is probably due to that rather than the economy.

Paul

I believe your opinion about Alaska Air are your own, not all would agree. We have category 000,000`s miles having lived on the west coast. Now live on east coast, but still fly to Seattle often. Has there been some decline, due to competition, yes. Are they still way better than most, yes. Importantly they still employ operators that live here in US, and speak English as native tongue, most whom will go extra mile to help.

A few big things to watch:

a) Oil prices are rising steadily. As I’ve pointed out for the past 4 weeks, the market for Heavy-Sour crude blends is moving into obvious under-supply.

b) Japan wants to double its defense spending. It’s going to have to repatriate some of its excess savings to do that. It’s the largest foreign holder of US Treasuries – that could have substantial implications

c) The CPC pledged greater stimulus for the economy on Monday. There have been similar efforts before, but the latest round really does seem intended to boost domestic consumption (dual circulation). This could raise the cost of exports.

d) Drewry Index has reversed and is rising now. This appears to be due to higher shipping costs rather than increased container volumes.

And thus far – after 500 points of Fed increases – consumers have only barely slowed their spending.

Good summary IMHO BA.

Please continue to share your observations/thinking, etc., on here with us.

Thanks

Don’t forget the SPR continues to drain. Pretty amazing…obviously that is a finite reserve so if/when it stops being drained prices of oil will keep going back up (even more) along with headline inflation.

The SPR is being drained to lower gas prices in the near term and to make the USA less resilient to oil price shocks in the longer term. Higher gas prices will accelerate the shift to EVs and increase resentment of Big Oil, leading to greater regulation. The SPR will not be refilled.

I don’t think the SPR drawdown is continuing. They recently approved a purchase of 6M last month to *begin* refilling it.

But I doubt there will be more repurchases – at least nowhere near the $72 WTI trigger price.

Based on my recent field trips to Floriduh, planes are packed. Car rentals cost are in nosebleed territory. I only take direct flights and the only option from PHX to MCO is Southworst…. and there hasn’t been an open seat on any of the 14 or so flights I’ve taken in the last 10 months. Yesterday’s included. There is no parking available at PHX. You spend 20 minutes circling level by level in the parking garage just to find an open space.

My daughter is a pilot for a major airline. She’s working as many hours as she is legally allowed. And not entirely by choice.

Real estate threatens to be a millstone that sinks the next generation.

Until a couple of years ago, I always got a kick from reading the comments section under a homebuying/owning article in a national paper like the Journal.

The Millenials always chimed in about how great it was to rent an apartment in a big city to Uber around to good restaurants, and they would never own a home because they wanted to job hop and never do yard work.

Anyone older than them knew one day they would grow up, want a family and not want to haul a baby and 15 grocery bags up to the 11th floor of an apartment. But you couldn’t tell them that without an online fight.

Yes only a few years ago the narrative was that the younger generation doesn’t want to own a home. They will be transient and rent and travel their whole life. Now they’re in their 30’s or 40’s and they’ve basically lost 10-15 years of their life with nothing to show for it. They’ve spent all their money they made on “experiences”. Now they’re angry at the world because of their situation unwilling to acknowledge that the real problem is financial mismanagement and a consumeristic spending addiction.

Nemo300BLK and Paul,

“how great it was to rent an apartment in a big city to Uber around to good restaurants, and they would never own a home because they wanted to job hop and never do yard work.”

That’s still the most desirable choice for many people. And it’s still a widely popular way of living. Nothing in this article says otherwise. The article said that homeownership of that age group rose by 2 percentage points, to 62%, not to 100%. It will never be 100% because everyone likes something different.

Homeownership also includes owning condos in urban cores. Lots of people who buy don’t want to live in a house out in the boonies. And so you have a gazillion condos in big cities that all kinds of people own.

SO true Wolf, and if it were at all possible, I would be one of those who would choose to live in a ”flat” in SF.

“Working off KARMA” is definitely otherwise, as MIL at age 93 needs and gets lots of help and support now,,,

Well that was before rent inflation hit double digits and most of those restaurants closed down because they couldn’t afford to stay open.

An interesting article. But I think there’s an enormous variation in what is actually going on from local market to local market.

Looking at Boston, MA….

We barely missed a beat. We had *perhaps* a few months of relative weakness from 11/22 – 2/23, especially in the Metro North area. But it’s hard to be sure since housing prices often drop during the winter in NE.

Right now, the housing market might actually be *running hotter* in Boston than it did in Summer 2020 – Summer 2022.

Right now it’s all bidding wars, all-cash transactions, and a large share of the purchases are being made by institutional investors. And I’d have to drive *miles* away from my house (located about 7 miles North of Boston in a town of 26K or so) before I’d stumble upon a house that is publicly-listed.

The only thing that’s different now vs. a couple years ago is that the daily calls I receive that ask me if I’m interested in selling my house are coming *directly* from prospective institutional buyers rather than real estate agencies.

Exactly why the purchase of SFH by investors should be harshly punished by tax laws.

I’d love to see that – but it won’t happen.

First off – anything that lowers home values is harshly-penalized by voters. It’s a political suicide note.

Second off – cities & towns require house price appreciation now more than at any time in history because lots of them used state-provided pandemic aid to take own new projects. In many cases the state aid doesn’t cover the full cost of the projects – and they took on some additional debt along the way. Also remember that the pandemic wiped out lots of local businesses – so cities & towns are more dependent on property tax receipts than ever. Basically, they are trying to ward off a Muni bond crisis.

Why tax laws ?

Why not either and/or:

1. Limit investors of all kinds to 1 or 2 purchases. Maybe ZERO for a couple of years

2. In conjunction with 1, only allow investors to buy homes that have been on the market for a year (maybe 18 months). This needs careful thought, maybe enhancement, to ensure home sellers can’t subvert it easily.

BigAl below says it won’t happen because of the voting clout of homeowners. He could well be right. Its interesting…the MSM reports low number of active listings (SFH) and lack of apartment vacancies as matter of fact. There is never an ethical consideration. Never any condemnation of investors buying too many homes.

Just the facts. The media is especially pathetic in that regard. Four out of 10 homes bought by investors in Dallas County in 2021, 5 put of 10 next door in Tarrant County. No problem. Atlanta 33% bought by investors, 2021.

Less than 1% vacancy rate for apartments in Spokane County 2021 or so (don’t know current rate).

I like to ask: what if the wealthiest 30% in outer country decided to focus all their investments in real estate. Most likely all others would be shutout (outbid).

Could this lead to social upheaval ?

One would think so, but Americans are a resilient lot… but is that being resilient or something else ?

What are the major industries / corporate employers in Boston Metro?

@Shiloh1,

Varies a bit but:

– Higher-Education

– Healthcare

– BioTech

– Business & Professional Services

– BigTech (Google, Microsoft, Oracle, Amazon, SAP all have major campuses in the Metro Boston Area)

– Other Tech Plays (WayFair, Draft Kings)

But the last two on my list are *definitely* seeing job losses now. Some of this is because they were heavily-tied into Pandemic-related spending – which began to ebb at the end of 2021. But, increasingly, this is due to outsourcing and outright offshoring of the jobs.

Howdy Folks A Starter Home has been X ed out by most folks… A Starter Home is a home that is less of a home that you can afford. Needs work, or updating. Takes time and cash dollars ( NOT borrowed dollars ) for repairs and builds equity to beat the Banksters. Old school way lost by most generations. Works well, and have 2 sons that also did the same thing. Their generation has youtube also and mine did not……..

If you have such a home – you’re probably going to want to hold onto it like grim death because those homes are going to be a heck of a lot less expensive to heat & cool in the coming years.

And nobody is building new starter homes.

You misunderstand my definition of a starter home?

Did you mean a smaller footprint home that you can easily afford the mortgage payments for and – with a little bit of know-how & elbow grease – minimize the expenditure to maintain?

If so, I did not.

No, he meant that people are compromising on living space and quality to barely squeeze a mortgage into 40% of their take home pay.

Choice has been boiled down to two options: a) get yourself into crippling debt, but you’ll at least have this shitbox, or b) good luck renting with sky-high inflation.

Any starter home now is either bought a flipped or bought to rent. In my market you can pay $650K for the starter townhouse or $900K for the okay house. Stretch a little and you are in the actually nice houses.

Howdy Ethan. Seems most people do not understand my definition of a starter home. No big deal, to each his or hers own…. Some folks think a new construction home is considered a starter home ….. HEE HEE

Wolf,

There’s an angle here that I think your article *could* be missing.

The subject of your article seems to be “ownership” of homes rather than actual “purchase” of homes.

So here is what I think you missed…

Life Estates

If an elderly parent enters into a Life Estate agreement with his/her child or children – those other person effectively are considered joint owners of the property.

Last January I spoke to an acquaintance of mine who is an Estate Lawyer in Massachusetts. He told me that his firm’s volume of Life Estate work had increased FIFTEEN FOLD over the past ten years.

Thoughts?

If I was 28 and looking at $8k a month mortgage in the big house for 30 years to life for a starter home in LA or SF, i’d be thinking of living somewhere else.

Wolf,

I wonder if there is any historical data on the ownership rate of the huge, key 65+ cohort. (My guess is that the census has been tracking this for a long time).

Pre post-2002 insanity, there were plenty of papers projecting *reductions* in 65+ ownership rates (seniors moving to sunnier climes, where they would rent/downsize) with big implications for the housing market.

2002-2022 ZIRP madness seems to have completely de-railed that logic.

But…people still get old, want to live out their days somewhere sunnier, get massively sick of never-ending housing upkeep, worry about another housing collapse, etc.

I think the *bigger* long-term story may be the dynamics of 65+ ownership rates from 2000 through 2040.

So far, thanks to ZIRP, what we have seen seems pretty counter-intuitive.

And when that happens, I always start thinking about Wily Coyote and his Acme anvils.

(PS – People are definitely moving to sunnier climes – the data shows that. But the downsizing dynamic seems heavily derailed…and somehow the US has managed to somehow sucker foreign nationals into roughly replacing the American internal refugees fleeing from the cold, overpriced, decaying metros)

Does this include the late 20-something guy I saw bragging out his “Instagram level” Airbnb a few years ago who is now pitting his shants because his bookings are 25% of what he counted on?

Where are the Airbnb’s located? I would love for Airbnb to go away completely but in Florida bookings still seem to be very strong from what I see when searching.

The AirBnb market is there for a reason. It created a new product, much different from hotels. Now, multiple families can get together for reunions, vacations, and other celebrations, while staying at the same residence, which adds to the interaction and fun. People will pay a premium for that.

The AirBnB’s basically created new demand, plus they stole some demand from the hotel market that will never go back.

People who bought AirBnB properties early, in vacation areas, at low interest rates, are making a killing. Over the past few years, however, its clear that some vacation areas are now saturated with AirBnB supply. The rental rates may be coming down as a result. A combination of reducing rental rates, stagnating or lowering housing prices, higher RE taxes, and higher management costs, will be reducing the comfortable margins that AirBnB owners once realized.

I doubt anybody will be buying an AirBnB property with a 7% financing rate. The numbers don’t pencil out, especially in a declining market.

In short, those who hopped into the AirBnB market early made a killing, and they’ll likely continue to make some cash flow profit because their financing costs are low. That business opportunity is now gone.

Yeah, I honestly don’t know what Depth Charge is talking about.

The total relaxation of Pandemic-related air travel restrictions in the past 12 months has resulted in a *tidal wave* of AirBnb bookings around Boston.

You’d have to be incredibly-dumb to be losing money on an AirBnb-listable property right now. In Boston at least.

When I was 27 in 2008 I owned 3 houses. Lost them all by 2010. Guess we’ll see how things shake out this time.

Not for me, I’m debt free…

You were the stripper from The Big Short? Glad to know things worked out well for you, thanks for the update!

The trouble with the younger generation is that they all think that social media is how they should live their lives. They max out their spending so they can live the “dream life” that they see online.

This will end very badly for them. Home and stock prices are going to be headed down for the coming 5 years and the economy and job opportunities will also tank with it. Energy prices are going to start to skyrocket again, due to a substantial decline in the number of wells producing in the Permian Basin. Rents are continuing their massive rise.

The problem is that the Fed hasnt really pushed up long term rates, which would bring down asset bubbles. The rate of selling off the balance sheet is tepid.

At some point I believe the dollar will crash as well, but not sure about timing. It isnt about the central bank ownership of the dollar as a reserve currency so much as the switch to trade between nations not based on the dollar. Just wait until Saudi Arabia stops selling its oil in dollars.

I don’t see the price of *anything* heading down in dollar terms once the USD reserve currency status ends. Or at least is greatly reduced.

Sure, your house may worth fewer gallons of gas or gallons of milk – but I’m quite sure it will be worth quite a bit more in $.

FOMO is now CARTA – Crazies are Running the Asylum.

The big driver of this was COVID and the rise of WFH – living with parents or roommates got less attractive the more time people started spending at home. And WFH meant people could look farther afield for less expensive housing without facing a multi-hour commute to city jobs.

No, the big driver of this was PPP and QE. Not only did that promise future inflation – which causes investors to chase hard assets – it handed these investors stacks of money with which to chase them.