Builders have to build and sell homes, no matter what the market conditions. More price cuts may be needed to get this moving.

By Wolf Richter for WOLF STREET.

Cut the price, and they will come. Maybe. Homebuilders have been cutting prices, they’ve been building at lower price points, they’ve been buying down mortgage rates, and they’ve been throwing incentives into the mix, as their costs have come down from the spike in 2021 and 2022, and as the supply-chain chaos has largely faded and endless delays have ended. They’re doing this because the 7% mortgage rates have slashed demand at sky-high prices. And builders have to build and sell homes, no matter what the market conditions.

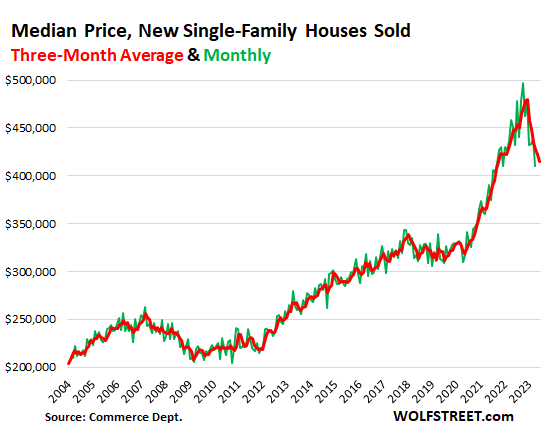

The median price of new single-family houses sold in June dipped to $415,400, down by 16% from the peak in October 2022, and down 5% year-over-year (green line), according to data from the Census Bureau today.

The three month-moving average, which irons out the monthly ups and downs and revisions of the median price, fell to $414,433, the lowest since October 2021, down by 14% from the peak in December 2022 (red line). But these prices do not include the costs to the builder of mortgage-rate buydowns and other incentives.

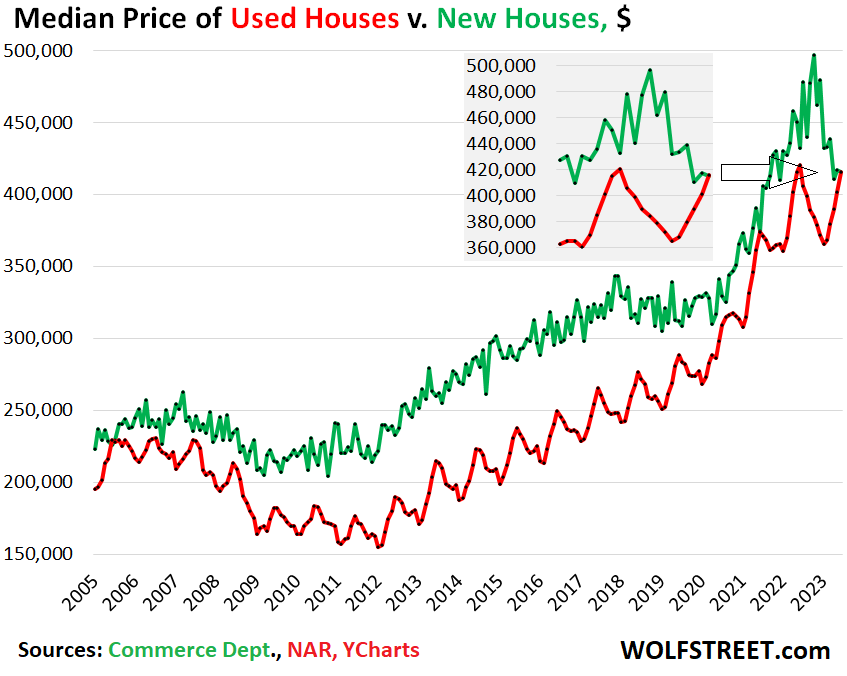

These price cuts and lower price points pushed the median price of new houses just a hair below the median price of “used” houses – what the National Association of Realtors euphemistically calls “existing” houses, as if new houses didn’t exist. The last time this phenomenon occurred was in 2005, which tells us that the housing market is in for a reckoning.

Builders, by offering homes that now compete on price with “used” homes, amid a very limited number of buyers for both types, are elbowing in on sales by homeowners and are pulling buyers out of that market and are taking share – and sales of “existing” houses have plunged 19% year-over-year and 29% from June 2021. So something is up.

Homebuilders have to build and sell houses no matter where the market is. And in time-honored fashion, they responded with deals to address dropping demand. Homeowners haven’t figured out yet what is happening here.

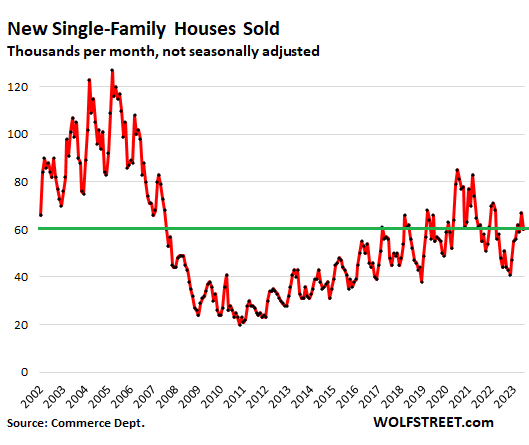

The seasonally adjusted annual rate of sales of new single-family houses fell in June to 697,000 houses, but was up by 24% from June 2022, which had been, along with July 2022, a multi-year low. Compared to June 2019, the seasonally adjusted rate of sales was down 7%.

Actual sales, not seasonally adjusted and not annual rate of sales, also fell in June, to 60,000 houses, which was up by 25% from the beaten-down levels last year. But compared to June 2019, it was still down by 9%.

This chart shows the not-seasonally-adjusted actual monthly sales – so despite the price cuts, sales volume remains sluggish, which gives us an indication that more price cuts may be needed.

These are “sales orders,” not closed sales. Cancellations are not subtracted. Many of the sales orders in late 2021 and early 2022 were then cancelled in late 2022, as the new mortgage rates suddenly put those contractual prices out of reach, and buyers were unwilling or unable to stick to the deals.

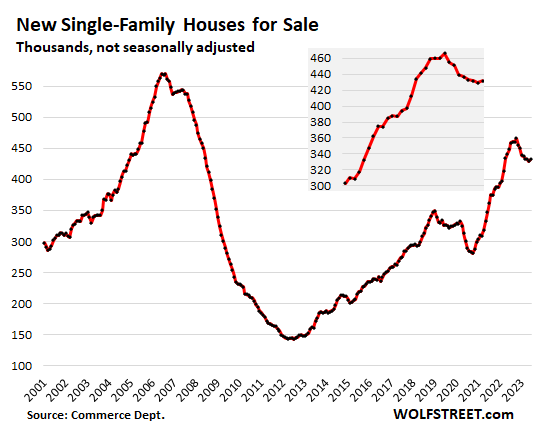

Inventory for sale in all stages of construction ticked up to 432,000 houses in June, the first month-to-month increase after seven months of declines from the inventory pileup in 2022. It seems lower prices and mortgage-rate buydowns, but also the unsnarling of supply chains and reduction in lead-times, delays, and shortages, worked in bringing down those inventories at least a little.

So there is more than plenty of inventory of houses in all stages of construction, amid fairly languid sales despite price cuts and incentives, which tells us that homebuilders will continue to aggressively pursue their business and offer deals, and homeowners will eventually figure it out.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

In crowded metropolitan areas such as NY/NJ, nearly all the housing is “existing” and already over $1M, especially in the NY commuter belt. New houses are built when land value is higher than improvements, and easily cost $1.5M+. To find a new house, one has to look into the exurban counties or even PA, where prices are much lower and empty land more plentiful.

On the other hand, most of new houses were built in south/southwest, where prices tend to be much lower than the northeast. Is this regional difference in type of housing (new vs existing) the reason why the prices at the national average/median are looking comparable? Looking at regional splits may explain this convergence of prices.

Too bad in SoCal, especially the desirable part of town, there are just not that many new home development so the decrease in pricing for new houses still won’t the needle for a lot of the potential buyers. Guess potential buyers be screwed much longer until used home sellers are under pressure to sell and a discount to the current insane price…

SB 9 might change that.

Buyer beware. Builders “WILL” cut corners in order to reduce their inventory. Our 3rd phase built home had manufacturing defects. The homeowners,myself included, filed a lawsuit against the builder and won. Forcing the contractor to repair all the problems.

In sweden the banks makes record profits from mottages now. They raising intrestrates for mortgages but not the savingsaccounts. So homeowners struggling when banks makes recordprofits…

Canada also. This is a sign of a banking monopoly. Technically oligopoly in Canada.

Perfect opportunity to lock in Stonk bubble profits and park large quantities of cash in real estate.

Even if market values go down, LTR market will increase. As I saw on SM the other day “the bank doesn’t think I can cover a $1400 mortgage, so I have to keep paying $2200 in rent!”

Vacation rentals are still a thing… for now. Van life will eventually get old for many. We know “real estate has found a new, higher level” and so will attract the only buyers who can afford it: investors!

Investors aren’t buying in this market. I bought/built (rentals) 25 houses the last 2 years.

This year. ONE. It only works because I have a niche market that can cover the higher payments.

In the Midwest, houses nearly doubled in price over the last few years. Not because local families got a sudden wash of money, but because “investors” (eg. scalpers) from California and the like swooped in and decided to play Monopoly in small town America. Local families were forced to compete with these scalpers but often got bid out. Many of these houses now sit empty or are partially rented out.

The latecomers to this scalping bonanza paid a high cost basis, thinking they are “protecting” their money from inflation, because the Midwest is “stable” and doesn’t have the downside risk. But little do they consider that they are collectively creating that downside risk by inflating the Midwest bubble.

Often folks don’t think of the Midwest as bubbly, but in 2008, there were huge drops, just at lower amounts. A $600K McMansion dropped to $300K, and a $25K shitbox became a $10K shitbox (later listing for $80K in 2023 of course, with no remodel improvements).

It’s going to be spectacular if this shitstorm implodes.

I’ve been getting more mail and texts about buying my house than ever before. Not sure what they’re thinking but “investors” are still doing there thing, at least in some places.

I think you need to refresh your SM feed. These days the rent would be $1400 and the mortgage $2200, if not more.

In my neck of the woods a 1400 sqft rental is 2100/mo and the current mortgages are 4000/mo. Not even in the same ball park.

Existing home median price has risin seasonally to nearly the 2022 high and I fully expect it to exceed that level by end of August.

Existing homes in desirable locations are selling to affluent buyers at higher prices while the builders have become housing subsidizers.

I forsee more of the same until the affluent run out of money.

As far as old vs new homes – I think the terrible build quality and really awful workmanship in new homes might be a factor.

LOL. Build quality didn’t change in six months.

Lots of used homes are require a lot of work = money down the drain.

I own, but am looking to move closer to the beach (sooner or later). This week I heard a lot of denial in FL:

New house saleswoman:

“Interest rates have not yet affected this price point of the housing market”.

Old house realtor:

“I verified the comps, $950k is a deal for this desirable neighborhood despite condition of the property”.

I couldn’t agree with you more I have a custom home homes you see now have hollow doors not custom stained no tiled showers they’re horrible

The new homes in my neighborhood seem to have more construction vehicles in front of them than they did when the homes were built. Must be home construction defects being corrected. I asked one dude new homeowner whether that was the case and he didn’t like the question. No one wants to admit that they bought a piece of crap.

Watch for the White House to start in with Canadian lumber tariffs like 2020; or worse yet the discussed Canadian lumber quotas to choke off building supplies. Maybe this time there will be some “supply chain” problem in sheetrock or the asphalt to make roof shingles, some one will use their imagination. There are dozens of ways for governments to stop houses being built affordable.

Not here in the rural red south, where they still can’t build owner-financed custom homes fast enough, and there’s no such thing as a builder spec house at the moment due to interest rates and economic uncertainties.

I did see where an entire neighborhood of 35 stack-a-shacks is for sale in Philly for $7 Million.

Brand name builders are building hundreds of new homes here on the north side of houston, TX. Many are 1,200 – 2,200+ sq. ft. in size on small lots and are selling for $220,000 – $300,000. I just bought a mid size one for me and the dog (wife passed last December). I sold our bigger house earlier this year at the top (got over asking) that was 24 years old in a 55+ community.

They are selling like hotcakes and many will be rentals in the $1,700 – $2,500 per month range. Builders are offering to buy down the mortgage to the tune of $5,000.

Goes to show that if they build in the “ affordable” range, they sell. Typically land costs and zoning get in the way however. Need more smaller housing, duplex and quads for the smaller family sizes typical now a days.

On a $250,000 mortgage, a $5,000 subsidy will buy down the rate approximately 1/2% (from say 7% to 6.5%). For what it’s worth.

Is it below construction costs? I guess it depends where. But when it does you can’t really lose too much money. Not good.

They’re not losing money at those prices. Margins are pretty good because costs have dropped so much. They can cut further.

I know it’s only one builder, but as an example Pulte reported a gross margin of 29.6% for Q2 2023. I believe that’s higher than the 2004-2007ish housing boom, and maybe 3x of what it was after the first crash. I think they have so much room to move that rate buydowns will be the norm for the foreseeable future as that allows them to hold prices with an acceptable drop in gross margin.

New houses are increasingly far out from city centers with few services nearby. Close-in neighborhoods with nearby restaurants, shops, schools, parks, libraries, etc. are increasingly what more people want — especially if they are less car dependent neighborhoods and more walkable and bikeable. These neighborhoods also often have much more character. People are done with sprawl and massive commutes.

That didn’t change over the past six months.

“are increasingly what more people want” No, a tiny group of people intensely want everyone else to want this. What “more people want” is big house, big yard, and big truck to drive everywhere.

I don’t know. You may have a euro bias here. Which I understand as I am exactly like you. No commute, walkable and character, estavlished neighborhood and old money is what I like. I’m half euro and half US but clearly in the euro camp for housing. Americans do love their suburban lifestyle meaning space and an enormous time spent driving (meaning a bigger wasteline) . They grow up driving and don’t mind.

100 percent agree. Why drive half an hour to go to a grocery store? People want to move quickly and own their time. These massive developments in the suburbs are inefficient and 100% car dependent. The US economy depends on it; we will never have cities that resemble Amsterdam or Zurich for political reasons. It’s a shame.

As Wolf reports new homes are a better deal right now. You may see historic lows in new home cancelations in the coming months as the interest rates are holding at the current level. Todays rate on a 30 yr should have todays hike and the next fed increase cooked in already so we may be here for a long while or a tad lower as winter sets in. Buyers are funny but will usually follow thru as long as the media cheerleaders are positive regarding real estate. Last year rates were fluctuating greatly causing a lot of buyers to cancel in the 11th hour. New homes #s are better than they look because of a lower cancelation rete and the other other improvements listed in Wolf’s report.

I wonder if there’s a geographical skew to the “existing” vs “new” home price comparison. In southern New England, what little new construction is being developed is markedly higher than most existing homes. You’re lucky to find anything new <800k in the greater Boston area with most new construction listed north of a million. This is probably a side effect of very limited buildable acreage as opposed to southern and western areas of the country that have thousand of acres ready to be turned into developments.

You also have to wonder if newer construction homes are, on average, of smaller square footage and on smaller lots compared with existing homes. A $/ft2 comparison of new vs existing would be interesting. It's also possible this was covered in the blog post and I completely missed it…

I was also thinking that?

Looking at the MLS in my area in a section I follow closely.

The “used” shows an average price of $450.000 built in 2017 and 2004. 1720 sq ft These homes have minimal upgrades. Same builder as the new ones and similar if not the same floor plan. The homes are really apples to apples. No incentives listed on the used homes.

The “new” homes have an average price of $480,000 1720sq ft These homes have some upgrades like granite but not much more. but here is the kicker. They are showing the built date of 2022 so they are not flying off the shelf and this is the remarks in the listings.

ONLY 13 HOMES LEFT!!!! PREFERRED LENDER INCENTIVES – $15,000 TOWARDS RECURRING AND NON RECURRING COSTS ON MOVE- IN- READY HOMES!!! $5,000 preferred lender incentives on upcoming homes! CALL US TODAY FOR MORE INFORMATION!!!

So the pricing is really close and what young family would not go for the new one? I know the arguments pro and con like you will need to landscape the back yard on the new one and so on, but would you want your infant crawling around in a brand new home or in a used one with god knows what’s in the corners or carpet.

There is also a used 1720 sq ft built in 2022 listed @ $495,000 . Most likely what they owe. Don’t think it will go anywhere soon. Could be one of the first short sales or foreclosures in the area?

Lots of realtors on here scrambling to prop up their market.

I’m a Realtor but far from a cheerleader! I am one of the few bears in my area.

Alec

Realtors should think about a new career. The market is frozen, and will be so for the next 5 years or until the market crashes and cleans itself up. GCAAR, which is the local RE servicing organization here, has practically suspended operations and has gone on to on-line only.

With historic low inventory there isn’t really a reason for existing homes to go down in price…..worst thing is they don’t sell and keep their 3% mortgage rate….

No, I am not a RE agent. No, I am not paid for propaganda.

“historic low inventory”

Can you not even look at the pictures in the article, for crying out loud???

Builders are awash in a historic amount of inventory and are trying to work it down. Last chart in the article. I post it here again because it’s clearly too challenging for you to even look at the pictures in the article:

I believe Richard was referring to the inventory of used homes, which is low. The chart shows the inventory of new homes, which is high.

This was an article about new houses and inventories of new houses price declines of new houses. And how new house sales are taking share from “used” house sales.

This is especially true since price reductions don’t generally help nearly as much as lower interest rates.

While I can only speak for the Twin Cities, MN, a used house has a better chance of being in a desirable location, i.e. 2nd and 3rd ring suburb. In the wealthy suburb of Minnetonka, well-built, used $750k homes are still being bought as “tear downs” to make room for $2m homes. Very ordinary homes end up costing more each year as they’re slowly replaced by mansions.

I saw exactly that in Pacific palissades late last year. Some very modest bungalows north of 1M waiting to be torn down for giant mansions. Even the driveway cars were vastly different. Even the clothes of the 2 groups and the grooming was different. The collision of 2 worlds.

Mitry

Tear downs here are getting nearly $800K. That implies Lot value – demolishion is even higher. I wonder what happens when the tear down rate exceeds the market value? Essentially, that means your house is totaled out. Sort of like my used car that needed $4,000 worth of repairs but only had a market value of 1.5K.

One of the problems with new houses is that a majority of them aren’t built in desirable neighborhoods where the “walking score” is high. You know, the hoods with bars, restaurants and other amenities that people want, especially young couples looking to have kids. In addition, schools and services come into play. In Seattle currently there is a ton of “in fill” housing being constructed. Shoddy construction for the most part I would say.

I see a return to urban neighborhoods in the future. The infrastructure is already there. Nobody wants suburbia and strip malls anymore with gas at $5 a gallon and traffic jams up the rear end. Well, I guess some do.

Home ownership is about to get a lot more discerning considering the interest they will be paying.

Good times.

Kunal K also pointed this out above (first comment) and I think you are both right. Regional differences, and also locations within a region. It’s almost impossible to build new homes in my area of coastal California. I wish it wasn’t, but it is. I’d love to see a comparison between new and used homes within, say, 5 miles of each other. Blocking for location.

BE HONEST mortgage rates have jumped up to 7% for New Homes. Therefore, the costs of a new home with a 30 year Mortgage costs 2X or 3X more over the long haul compared to before the Pandemic? Higher Interest rates are probably killing new home sales directly due to Interest Rate Hikes. The US is choking to death off the $32 Trillion in US Government Debt?