Sales of used houses are dismal, even as supply & days on the market rise. Homeowners await inspiration. Homebuilders got the memo.

By Wolf Richter for WOLF STREET.

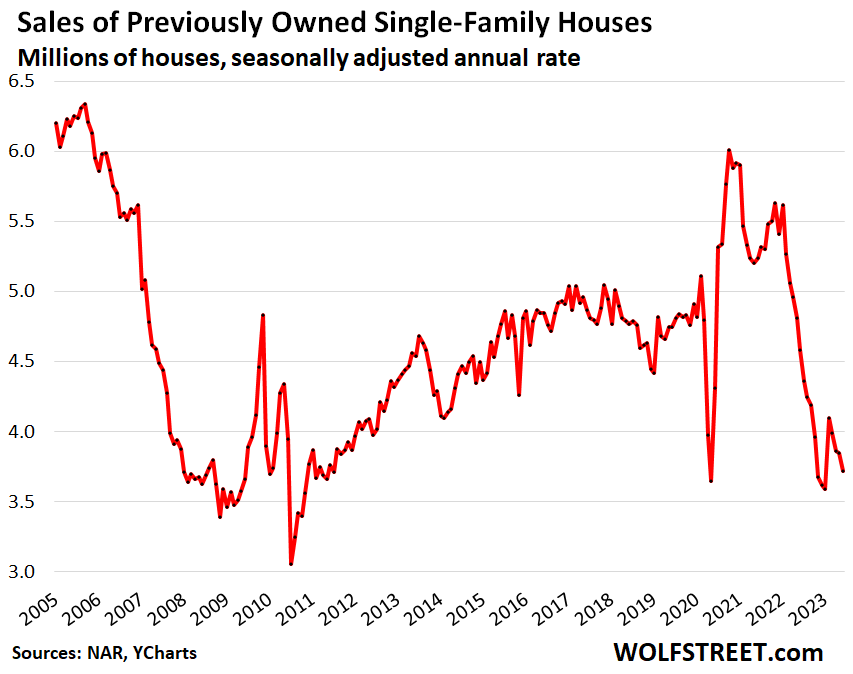

Sales of previously owned single-family houses fell by 3.4% in June from May, to a seasonally adjusted annual rate of sales of 3.72 million houses, the lowest since January, according to the National Association of Realtors today. This is deep-dismal sales territory, even as supply rose to 3.1 months, and inventories to 960,000 houses, both the highest since November.

Compared to June 2022, sales of let’s just call them “used” houses were down by 18.9%. Compared to June 2021, sales were down by 29.0% (historic data via YCharts):

A bizarre twist in the market.

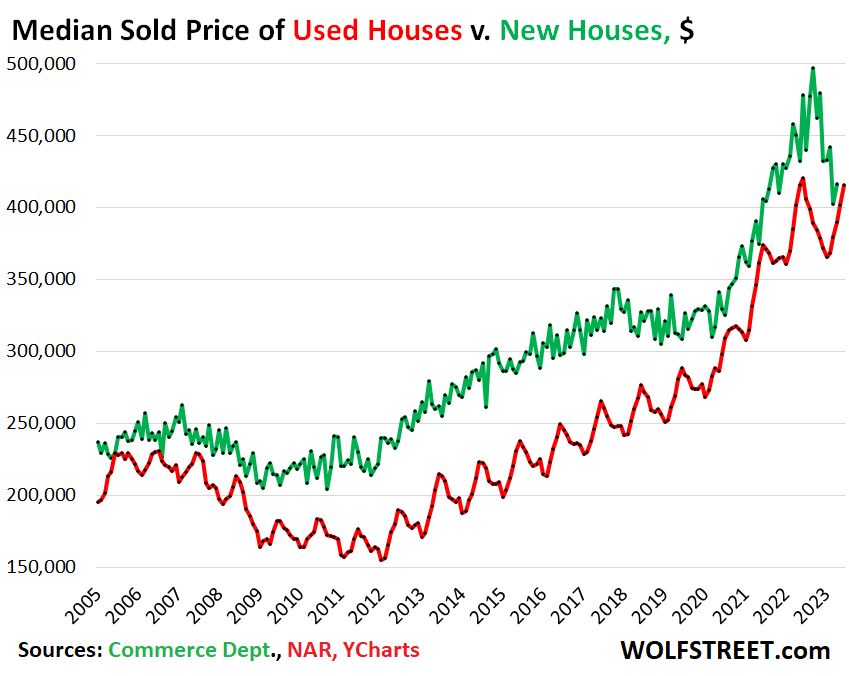

The median price of used houses has dropped from a year ago, but just a hair. The median price of new houses has dropped more sharply, as homebuilders got the memo, and now the median price of used houses is the same as the median price of new houses. This is a historic pricing disconnect that will correct.

The median price of used single-family houses, at $416,000 in June, was down 1.2% from June last year. The month of June is normally the seasonal price peak for the year. Prices normally decline in the second half. This comes amid rising supply and rising days on the market.

The median price of new single-family houses, at $416,000 in May (last data available), was down by 16% from the peak in October, and by 7.6% year-over-year.

Potential home sellers are going to figure this out eventually. But they haven’t yet. And so you get this crazy-looking chart (historic data via YCharts):

This is a reality check. Homebuilders are the pros; they have figured out what it takes in this market amid the 7% mortgage rates. They cut prices and they’re building at lower price points, and they’re buying down mortgage rates and throwing incentives at buyers to make deals. And they can because some of their costs have gone down. And they’re selling homes to buyers that would have bought a used home.

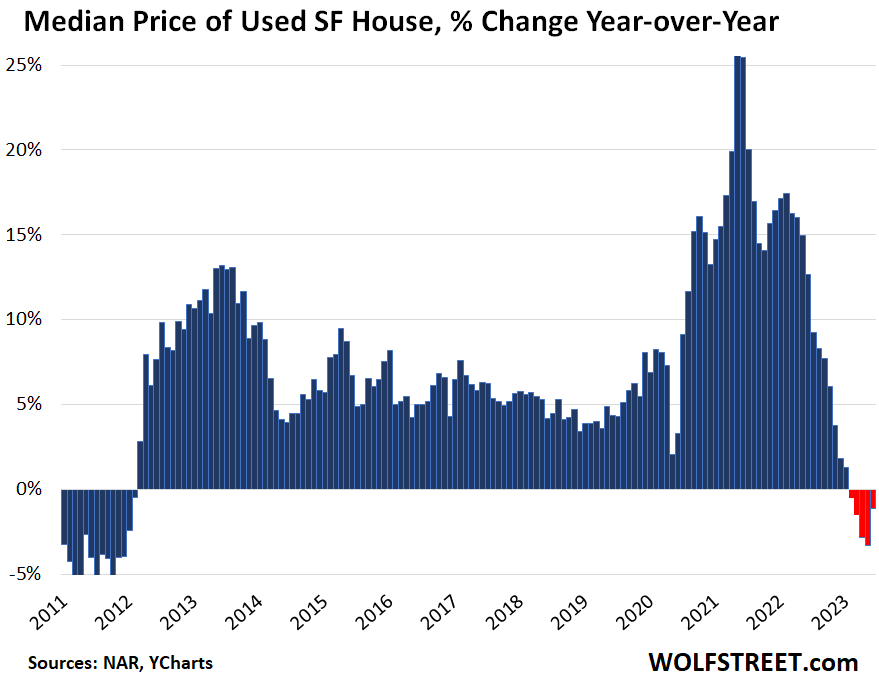

Year-over-year, the median price of existing single-family houses fell by 1.2%, the fifth month in a row of year-over-year declines (historic data via YCharts):

Median days on the market lengthened year-over-year, by both measures:

- Homes, whether they sold or not, spent 44 days on the market before they either sold or were pulled off the market, up from 34 days a year ago, according to realtor.com.

- Homes that sold spent 18 days on the market in June before they sold, up from 14 days in June last year, according to the NAR. This excludes homes that failed to sell.

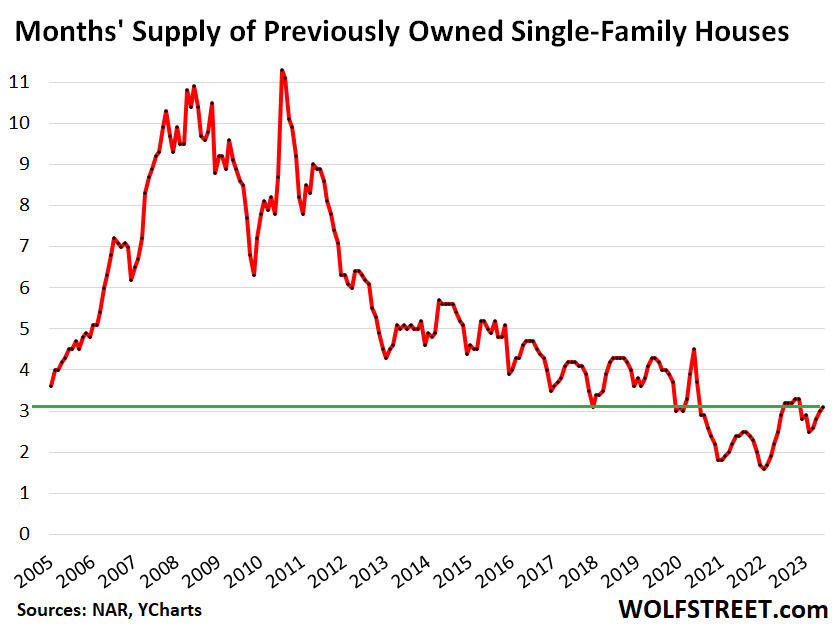

Inventory for sale rose to 960,000 houses in June, the highest since November.

Months’ supply rose to 3.1 months, the highest since November. The range in 2017 through 2019 was between 3.0 and 4.3 months (historic data via YCharts).

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

As a FTHB, these trends are finally moving in the right direction. As a Seattle renter, I’m focusing on tripling my income by up-skilling as fast as possible to better job-hop because that’s the only way these mortgages will ever make sense. Our housing market is absolutely dismal right now – little on the market, and what is there is ludicrously overpriced.

Wolf, if you happen across this comment – what would you do in my shoes? FOMO now? Wait it out indefinitely? I don’t have a ton saved up ($15k in stocks, $11k in savings), or any family I could borrow from, so I only have one shot at getting this right. My credit score is 800 though (and my partners is 830), so I’m a solid borrower.

“what would you do in my shoes?”

I’m not in your shoes, thankfully. Only you can make that decision.

good to have been a few decades earlier. before all this bubble bullshyt.

We had housing bubbles too, and housing became unaffordable, and then they blew up massively in our faces and crapped all over us during the oil bust and the S&L crisis – TX and OK. Lots of people lost everything. The housing market in Tulsa, where I lived, spent the next 30 years not recovering. You’re naïve to think that this is the first RE bubble — though it may be the first for you. RE bubbles and implosions are quite common at the local level. They’re just uncommon all at the same time at the national level. But for individuals living at that location, the effects are the same.

*They’re just uncommon all at the same time at the national level.*

I would supplement at the world level

As a guy who lost money in RE in Los Angeles a few decades back I can only say it’s not the first time, and there’s plenty of room to fall left.

Not naïve wolf. Been there done that. Have the tee shirts. Was there in 08. Saw the blood in the streets. But we’re not going to get that this time. Not with this labor market. This will be a long slog of denial on both sides. Years, without some major event dislocating the labor market, for which the boomers — they already got theirs. They’re retiring.

Hartford, CT in the early 1990’s (insurance company and defense contraction (United Technologies)

Pittsburgh, PA (steel mill closures / coal) in the early mid-1980’s.

Chicago @ 1984

It’s amazing that people think that this is the *first time* there has been a housing bubble and housing price collapses/market freezes. These same folks don’t realize how many people got destroyed back then…. when the geezers were their age.

Here’s the secret to real estate success: Don’t buy a house to make money on. Buy one to live in. Buy one you can afford. Pick a good location as you can always change the house, but you can’t move it (unless it’s a mobile home, but even then….). If you wake up every morning worrying about the value of your house, then there’s something wrong with you.

This is so much worse than prior bubbles. Housing has been detached from wages since 2002.

There are now no free markets.

Annoying to see comparisons drawn with prior bubbles.

Plain talk from truthful Wolf. That’s why I come here.

Howdy Pusheen, How about a starter home? Old school way but could still work for certain people. A smaller home that needs work. But if you are job hopping and hop into a different state for a job, then renting should work out better.

Starter homes dont really exist. Anything in the lowest price bracket has more potential buyers and thus drives its price a little higher than otherwise. A 800sqft home may sell for 380k when a 1300sqft home sells for 420k. Fixer uppers dont exist. They’re food for flippers. You could find a teardown, but then you might as well just work with the homebuilders without the hassle of clearing out some superfund site.

Not true. Some Millennials said this on twitter and I found a $25K home in St Louis that needed work, and they scoffed that it was a high crime area (i.e., minority area and they were racists).

Maybe things are worse now due to Dem local governments, but back in the day the Boomers would buy exactly those as starter homes and then fix them up.

I can show you a house in St Louis for $15K if you like, but I know you don’t want that, you want a $500K home w granite countertops and tile floors.

In Tacoma, if anything comes on the market listed at $399k, it looks like a feeding frenzy. There are a lot of people who are pre-qualified at $400k, and they drive up anything which is possible for them to buy.

If you can pay 10% above the bottom of the market, you get a much better deal.

This is despite the recent unpleasant mortgage rates. . .

Well said. Especially last sentence as government permit requirements can be an eye opener

No Dale, Boomers never bought exactly those as starter homes. Maybe the silent generation had a migration to the worst parts of the country during the dust bowl, the boomers never did though, they had it easy. And I wish I could buy a real starter home, not some gawdy mcmansion with tacky granite countertops a boomer high on leaded gasoline thought would be their “dream home”.

Dale:

I see what you’re saying in St. Louis. Lots of foreclosures available, and many houses for less than $20,000.

My take is that they’re not exactly “move in ready.” With broken windows, boarded up and tarps over the neighbors’ houses; I can only imagine what squalor is inside.

On top of that I am curious about the job market?

There’s a difference between having a well paying job and finding a place to live and buying a complete remodel, having to be a house flipper just to get a place.

St. Louis is the next Detroit?

As Wolf would say, plenty of affordable starter homes in Tulsa.

My propaganda about moving to Tulsa for cheap housing is working. Home prices have shot up over the past couple of years. Still cheap though.

I need some people in Tulsa to thank me for this. I have the most thankless job ever, LOL.

@ Dale

I’m familiar with St Louis, the 25K homes there are in disrepair and also typically in neighborhoods that are demonstrably high in crime. This isn’t racist, it’s a fact. And St Louis has lost more population since 1950 than any large city in the US, more even than Detroit, so you are buying in a falling market with no clear bottom in sight. People are happy to buy a starter home but not a crap hole in a neighborhood that isn’t safe.

I have seen a few recent glow ups of Tulsa. I guess there are a few very wealthy people putting an enormous amount money back into the city. Didn’t Tulsa offer to help people buy a house there at one point?

> starter home

This only works if housing doubles every few years.

That’s over

Howdy Herpderp and Georgist, My definition of Starter home is defined as less of a home than you can afford. Live within your means and life is good. It also means a home that needs work and todays buyers have thousands of reasons against that word.

Starter homes are batshit expensive too.

Sure starter homes are expensive… if you’re looking for one in a beach community, 15 seconds away from The Domain, or in a trendy community with 12 Starbux within walking distance.

A “starter home” is a small house, likely with one bathroom without 300 shower heads – but a bathtub with a shower, has laminate countertops not granite, and maybe missing a dishwasher as there’s no room for one. What you have to understand is that there’s a line of people behind you that will be looking for such a house if and when you decide to move if you doll it up. Is it work? Yes. Does it take time? Absolutely. Will you learn a lot? You betcha.

Then you can enter what was formerly know as the “property ladder”…. which was a quaint concept where you step up to your next house when you have a kid (or can reasonably afford to upgrade). Before you all jump on “the realtor fees will eat up any profit… blah blah blah…. that’s not necessarily true. Certainly wasn’t ever true for me…. and I’ve owned 8 houses. You just have to be prepared to ride out downturns and not angst over it. Put away the game console and live a life.

Flippers don’t get every house. That’s what HGTV will have you believe. We played on heart strings when we bought our first house… wrote a letter to the owners basically begging them to pick us. It worked. And if you think that’s “old fashioned”, we had the same experience with the buyers of our last house – which sold in the 7 figures.

As mentioned in another comment, there’s websites featuring cheap old houses. Historical districts (i.e., Wheeling, WV) also have listings of homes for sale – some owned by the city and available for next to nothing. Are they move in ready? No. But there’s a group of not lazy millennials that are buying these and fixing them up as they go. Google Betsy Sweeny.. Another thirty something single female bought a farmette and a 100 year old plus house and outbuildings. She and her family have done a number on it…. and there’s a network of like minded people that she tapped into – to the point that these folks take “vacations” to help another with a project.

In our last move, we sought a simpler life. We can see stars at night. We live in a dark sky community. We hear birds, not freeway traffic wash. No sirens. No car alarms. No Civics with fart pipes. Only air traffic is at high altitudes. Mountain views in 3 directions. Sure, the grocery store is 13 miles away…. OMG! But, sincere there’s only one traffic light and two stop signs in that entire distance, it takes less time to get there than it did when there was a grocery store that was 1.5 miles away – with 9 stop lights and two stop signs – in the cityburbs. I could never be a “cliff dweller” or live in a condo. Closest thing to torture I could imagine.

As I’ve said before, the world is different now. 40 years ago, there weren’t as many absurd permitting requirements and hassles from every municipality when you’re trying to do a fixer upper.

You didn’t have to worry about the Fed deciding to start printing again and letting the next “step” house running away from you.

When people committed violent crimes in bad neighborhoods, they didn’t have Soros DAs letting them run wild.

El Katz: Today’s buyers get an exceptionally bad deal because the new homes, dollar-for-dollar, are built with cheaper materials; while the used homes have been tinkered with and might need expensive repairs. Put down the coping saw!

Starter homes are, as discussed, generally few and far between. Fine few 2-3br/1 bath homes up for sale, certainly in the North East. In my area they were the first to be gobbled up by early pandemic Brooklyn transplants primarily for AirBnb and ‘passive income’ landlords. And what is out there is insanely overpriced and typically in rough shape, far too rough to be able to finance with FHA, or even a rehab loan which a lot of first time buyers need given how high rents have been relative to income the past decade or so. I was fine with taking on a 203(k), but couldn’t find one that was workable or the offer was rejected for another cash offer by a flipper.

For jollie, google the Million Dollar small Cape Cod home in Beacon, NY that went viral recently. Its an extremist example of what is happening to the ‘starter homes’, most of which are 50-80 years old in this area.

I bought a starter home in 04. It was a super competitive market, and we got so lucky to get it. 5 years later we owed more than what we could sell it for. By 2015 we got lucky enough to sell it for a very small loss.

Great starter home!

Similar story here… Bought in ’06 and eleven years later (2017) was able to sell for close to what we paid. At one point our starter condo was down 60% in value!

Pusheen,

A lot of this depends on your salary, your age and your personal situation (in terms of putting down roots and having children).

You said you were focused on tripling your income. So I’m assuming you’re making less than 6 figures, would that be correct?

Right now, you should absolutely focus on maximizing your income. You don’t know what that might lead to in the future, including having to move away for further salary increases.

Once you have had a higher income for at least a few years (be wary of fluke years), then you should consider a purchase.

You’ve got $15k in stocks, $11k in savings. Right, those are numbers that need to go up first before you even consider purchasing a house.

Pusheen, are you dead set on staying in overpriced Seattle? I moved from CA to NM. I make exactly the same money, but almost everything is 60% of my previous cost of living here. House was $335k in a good part of town with good schools which would have been $550k to $600k in a mediocre part of CA’s inland empire in rougher parts 50 miles outside of L.A. My summer electric bill is $70 vs. at least $300 in CA. Similar ratio for most other bills.

Basically, my wife and I were struggling to keep our family barely in the middle class on a very good combined income in CA. But we have a better standard of living here on just my income, and my wife can comfortably take a few or even several years off of work to get my son established in school. Life is vastly better for us, not just a little. We moved 750 miles away, but it feels like we moved to a different galaxy in terms of quality of life.

Meanwhile we have friends in other places (Seattle included) overstretching themselves financially into ludicrously dangerous waters and hugely stressful situations. My advice is, “Don’t be them.”

If you can’t make it in Seattle, maybe consider relocating. Life is very very good in lots of other places.

I agree, completely. There’s a “cool” factor that is very expensive to maintain. Kick the habit, asap.

You’re absolutely right. I see many of my generation (millenials) trying to keep up with the Joneses. They make more than me, but they also spend way more than me to stay with the cool crowd.

The flipside though is that if we all lose our jobs, I’ll be in a significantly more comfortable financial position than them. I can cover over a decade of living expenses, my friends can barely cover a year.

Definitely agree with above, especially if you don’t have kids/aren’t divorced yet. If things go south with your partner, state custody laws have this funny tendency to trap you in their suffocatingly expensive state as a struggling single parent for up to18 years. Or so I’ve heard.

I totally agree with you.

I am in SoCal but would love to leave it but for 2 reasons:

1==> Waiting on my kid to graduate high school.

2==> Have a cushy job.

My auto insurance increased by 100% in last 3 years and home insurance by 300% in last 3 years,

I’m from CA. Moved to NM 20 years ago. All that you mention is correct. NE ABQ has good, if boring neighborhoods. I am so over this place, however, and miss the ocean. Besides, unless you’re work from home, or work for the labs, this place comes with a LOT lower wages than other states. It’s also sort of low energy while at the same time being high crime.

I’ve got friends from graduate school working at Los Alamos. It seems to be a common phenomenon for the STEM PhDs – many move to LCOL places where the national labs are and live very comfortable albeit in boring circumstances.

We’re in the NE heights, and like it a lot. The neighborhood is fairly quiet and we have a couple of nice parks within short walking distance. I quite like the laid back atmosphere. The fast pace of life coupled with the slow pace of traffic had become unbearable in CA. I’m in manufacturing & automation and can’t complain about pay. Had no problem finding a great job here very fast. I agree that low skilled jobs don’t pay much here, but there are solid opportunities for skilled folks certainly not limited to work-from-home. My perception is that crime is pretty regional here, certainly no less safe than CA’s inland empire where I lived. There are some homeless folks here or there just like all cities, but homelessness isn’t remotely on the scale of CA’s problem. In theory, there is so much to do around L.A., but every activity is crowded beyond belief, ludicrously overpriced with impossible parking, and you get to sit in a couple hours of traffic there and back. For example, I could spend $500 to visit Disneyland and wait in line all day for like 3 rides with the family, or I could put down 100 bucks here at Cliff’s and have a perfectly fun day with the family packing in rides non-stop after a 10 minute drive from home. Disney is far more grand in theory, but miserable in practice. That pretty much sums up southern CA in general… Great in theory, but ruined by crowds, cost, and wasted time.

Hey Not Sure,

What part of NM?

Albuquerque. So far I really like it. It’s a big enough city to have most of the amenities I’m used to, but small enough that people are quite nice and I’m not stuck in traffic for half of my waking hours.

Good luck to you, seriously. You sound like a good person doing the right things with your credit and trying to better yourself. I truly hope it works out for you. Our government and the Fed have screwed over good people like yourself, and it sucks. It’s sickening what’s happening.

We have 470k active listings (single family homes) today. In 2015 we had 1.2M active listings (single family). Let that sink in.

Historic low inventory….

We have 12M vacant homes! No forced selling so they will remain vacant until the labor market turns.

Also, out of all owned homes, 38% are owned free and clear. Unless there is massive unemployment this market won’t go down.

I am hoping for lower prices in the next couple years.

Richard,

But demand plunged too. That’s the thing. Prices are down year-over-year. The price increase through June was seasonal. NAR prices always peak in June and then drop. See the red line in the second chart.

The people with their 3% mortgages cannot sell but they cannot buy either. So they’re out of the market entirely, as buyers and as sellers. Their homes are out of the market, and they’re out of the market as buyers. This means that the entire market may have shrunk by 25%. Inventory down 25%, demand down 25% just from that one factor. It that’s the only factor, the market would be in balance. Buyers and sellers decline in equal measure. But there are other factors too.

Are you sure it is the state of the labour market that decide if vacant «homes» comes on the market? What if these «homes» are «investments» or maybe parking of money?

If so other considerations than the state of the labour market decide if they are offerered for sale.

Sorry. You are collateral damage in the Fed scheme of things.

Why would you buy a house if you plan job hopping? Or why would you have $15K in stocks if you only have $26K.

How about you read a book or something.

Agree about buying a house when the future is uncertain but $15K in stocks and $11K in “cash” isn’t bad if that $11K is six months worth of living expenses and he doesn’t expect to need the money from the stocks for at least 5 years.

Consider, too, the carrying-cost and the buying and selling costs of home ownership: buying is about 3% of price – depending on how you deal with “points”; selling is about 8% of sales price assuming you pay the typical realtor cost. Replacing an A/C unit? Repainting? Interest, insurance, HOA?, property tax. Buying an old “fixer” may require “fixing” forever.

Yes, it provides the shelter that you’d pay in rent, otherwise. But there IS risk. Suppose you catch a downdraft in home valuations? Or there’s a surprise change in your job(s). And then there’s inflation: that price increase may only keep pace with inflation or possibly less.

Lots of factors. Is this the best investment possible? When it comes to investing, there’s a strong desire to buy when everyone else is buying – be fearful when others are greedy; greedy when others are fearful (Buffet).

Or you could get hit by a meteorite. The world could end.

Mortgage interest and property taxes are tax deductible. Right now, they’re capped…. but just the same.

You have renters insurance, correct? If not, you’re stupid if not only for liability reasons (someone breaks their neck in your apartment…. renters plus umbrella.)

Houses are not an investment. They’re a place to live.

How much does it cost to move your apartment/rental when the landlord raises the rent or the complex deteriorates? How often do you get your damage deposit back? If my daughter is any indication, it’s rare if ever.

If you buy a house to live in, the future realtor fees are not an issue.

Buyer’s points you roll into the mortgage. Adds pennies per month.

Air conditioner? They have insurance for that (home systems insurance through many homeowner’s policies and underwritten by a third party commercial insurer. Costs next to nothing and covers up to $50K in repairs. Same for supply lines – water and sewer.)

There is no home ownership boogeyman. Use your head, buy good tools (number one mistake people make is trying to use a hammer for everything), look at online videos that show you how to repair just about anything…. and have a partner that’s not enthralled with granite and likes to get dirty.

I always love these folks that declare “a house is a place to live, not an investment” as if they somehow make the rules and everyone else is.. what? Supposed to fall in line?

It is probably safe to say that 99% of houses were at some point an investment. The land, infrastructure, the subdivision or just the house. At some point in the creation of a home, some form of investment was made. Even the current owner/resident is investing in the property, even if it is paid off. But please, enlighten us all about the true purpose of a house, I’m taking notes.. or not.

“tripling my income by up-skilling…”

could you please sir explain what you mean by this, and how exactly that is even possible?

It’s called education / professional licensing. Increased (up) skilling “skills”. Becoming more valuable to your existing employer or more attractive to a prospective employer.

el katz?

how is it that you seem to know what pusheen meant?

there was no detail in their statement.

perhaps they are a freelancer and have no employer. you PRESUME an employer/employee relationship for some reason.

its a pretty bold claim that anybody is going to TRIPLE their income by ‘upskilling’.

in fact, the only thing pusheen defined was the AMOUNT of increase. this would seem to indicate some type of plan to get there.. a series of actions, or a strategy. THAT is what i asked about.

you claim to know it?

since you replied and not pusheen,

id like to hear a scenario from you where ‘upskilling’ as you claim to understand it.. TRIPLES an employees income with their current employer, or a prospective one.

Pusheen, 26k in funds doesn’t get you anywhere. If you had 260k for a DP you would buy in Seattle (that’s at least what most people who have the cash and the willingness to own do).

Keep saving lots of money and buy when you can comfortably afford it.

Agreed. Save up 20% down and plan for a payment that is no more than 25% of your take home pay on a 15-year note. Until you can afford that, don’t buy. Increase your income or move to another area. Pay off your mortgage early, shun all other debts. Oh, and don’t buy a house with a “partner” to whom you are not married.

@Corey, this advice makes sense in theory, but in almost every major market it’s impossible and thus not practical advice.

$250K/yr gross = $187K-ish net

$15,625 gross per month

25% = $3,906 per month gross

Based on these figures and your above stipulations, anything over $500K would be out of budget, and that’s assuming household income of $250K a year, which in the Chicagoland area (where I’m from) would put you in the top 8% of incomes.

Lower it down to median income at $75K and your max payment under your stipulations would be $1,172 per month, so anything over 200K would be out of budget, which here in Chicagoland gets you literally nothing aside from maybe a 2 bedroom condo. Good luck.

Right out of the Dave Ramsey bible. 15 year mortgage, payments not to exceed more than 25% of your income.

I agree, everything Ramsey says sounds great in theory, but I think it’s all outdated by about 30 years. We are all going to be debt free living on beans and rice and will be paying our kids college.

Not so sure..

You know the rent you’re paying now, and you know what the mortgage payment + HOA would be on buying a similar house. How do they compare for *you*, after taking taxes into account (that requires knowing your own top marginal tax rate and whether or not the mortgage interest would be enough to itemize)? If renting is still cheaper, just do that. No reason to expect runaway home appreciation in Seattle at this point.

This “hellhole” business refers to Seattle proper, and only parts of that. Whether Pusheen decides to live in Seattle or Bellevue or Kirkland has very little to do with the buy vs. rent question.

“….what is there is ludicrously overpriced.”

I believe you answered your own question of what you should do. That said, come on down to greater Tacoma and Pierce County and see what’s out there. Best wishes.

Don’t listen to the morons. This situation is so effed up it isn’t funny. Only hope for propping up the insanity is the fed. If they make one minor misstep, this whole thing implodes. That’s why QT is anemic.

Don’t give up hope. We all have been there. If you are a first time home buyer you can qualify for grants to get you over the down payment hurdle. Don’t be scared to look out of your comfort zone. We purchased a fixer upper almost for cash and rebuild it from the studs with family help. It is a much better house in an established area. Takes a lot of work and patience, but worth it. Plus little debt and good employment it allows us to be debt free in 4 years by paying cash. That is the advice I gathered through Wolfs sage advice for the last few years. Live below means = freedom.

Late comment…

Move to Spokane or Tri Cities…save yourself 10k a year on rent. Better yet move to a medium size city in Ohio, save a little mord and avoid wildfire smoke and sizzling summers. Enjoy the long autumns… they last only about 6 or 7 weeks in Spokane. Humidity… yes there’s that in the summer maybe a problem half to 65% of the days. 4 decades ago lived there.

Or try New Jersey, or Pennsylvania.

West Virginia is pretty cheap and not so much snow but not too hot either. Perhaps the best of all worlds Morgantown or Charleston.

As somebody living in one of the most inflated housing market’s in the world (Australia), I find this article confusing.

Down under we’d generally expect that buying a “used” home would be much more expensive than buying a “new” home. Here it is not uncommon to pay $2mil for a 50-100 year old house.

I’d be curious to understand the dynamics of this separation more. Over here it is definitely to do with the concentration of desirability of property around our city centres. Is the reverse still applying in many areas in the US? Hollowing out of the city centres?

Don’t you have a problem with foreigners buying real estate for investment driving prices up for everyone?

That issue is massively exaggerated. Sure it is present, but it is a marginal effect. We do a great (terrible) job ourselves of buying up real-estate and pricing our younger generations out of the market.

It is extend and pretend. In the US you guys seem to be great doing it with your share market. Down here we do it with our residential real estate market.

(But there is also demographic and geographic difference in the real estate market which is what inspired my first comment. I was completely unaware that older real estate is generally cheaper in in the US as the opposite is the case here.

We have more ‘mega’ cities here, so land value plays a much bigger role in the cost of housing than it does in the US. And we have largely kept our downtown area healthy so hollowing out to suburbia is something the poor do and not the rich.)

This is a great point.

The markets I know best are Chicago, DFW, and Houston.

Definitely there are a lot of neighborhoods of “used homes” close to the downtown/central city that are much more expensive than new homes in the suburbs.

It would be pretty easy to research.

The vast majority of “used” single-family houses in the US are not in city centers. They’re outside the center, urban sprawl has been a huge factor for many decades. So you’re comparing a relatively small number of used SFH near city centers to that vast mass of used SFH in the urban sprawl that has developed over the past 70 years. In the urban cores of big cities, just about everything that has been built over the past few decades has been multifamily. The median price is much more determined by the used SFH in the vast urban sprawl than the relatively small number used SFH in city cores.

The problem is that your post is not correct.

Foreigner purchase of used residential real estate is basically prohibited and only allowed in a very, very few limited circumstances.

And when they do get approval to purchase any type of real estate they have to apply for a licence and pay for it prior to the final closing.

The median price of a house in Sydney is still well over A$1 million and Melbourne way under that.

Prices of houses in Australia are high, but still cheap compared to houses in the USA. Yes, houses in the big cities near the CBD areas are sky high, but are much cheaper the farther out you go. There are of course pockets of high priced areas between areas of depressed low cost ones too.

And there are other differences between the Australian residential real estate markets and USA ones too.

One is the cost of selling is cheaper here than the USA with RE commissions about 1/3rd that of the USA.

Buying costs are higher as you have to pay stamp duty to most states when you buy a property. I think that the state of Victoria has the highest rate at 5% of the selling price on property over A$1 million.

Property taxes or rates on as we call them on your own home are one of the few things in Australia that is still relatively cheap compared to the USA. The rates bill just for the property taxes varies between areas, but paying A$1000 to A$2000 on a million dollar plus property is quite common.

And insurance on the property is probably a lot cheaper too in many areas as we don’t have a lot of the natural disasters common in the USA in our big cities. Usually no typhoons in Sydney, Melbourne, Canberra, and Adelaide. Very few tornadoes, earthquakes, and bush fires in the big cities either.

We also have much lower crime and property damage claims as well.

And of course the two biggest differences:

1. No capital gains on your principal place of residence;

2. No inheritance taxes at all in the country.

So owning and carrying costs here are overall much cheaper than in the USA.

Apples and oranges, mate.

Good points, but regarding #1, the first $250k for singles and $500k for married are exempt from capital gains on primary residences here too. For most people, that’s the entire gain.

So, one big issue with buying an older house is insurance. Insurance for a 40 yro house may be $20k and a new house is $3k.

Wow, where do you live? My family has been in insurance for generations and while it is true that insurance can be more expensive in some older neighborhoods due to various risks (fire due to older wiring, theft, water damage due to bad mains, etc.) and it can also be more expensive in older developments with solid masonry construction vs. wood framing; but I have never in my life seen a quote for two similar sized homes that would be anywhere near the difference you mentioned. Not even close.

It’s funny how Americans get a little squirrely when questioned about cultural differences (valuing suburbia vs urban living). Some of the comments on here are outrageous, I don’t want to live in North Saint Louis because it’s still burned out, but Clayton, MO is wonderful. I couldn’t imagine living in one of the many, many destitute suburbs of Saint Louis as I’d be living with a bunch of uneducated, prickish morons who don’t seem to understand much about the USA. Cheers!

Why is insurance lower for a new house?

Cheaper for the insurance companies to replace chipboard and pex than antique tube and knob or asbestos. Things get real pricey if they have to find lead paint, r-12 is liquid gold at this point.

That is B.S., I live in 5,000 SqFt house in Denver, built in 1893, and I pay $5K for property insurance. And I assure you my house is sturdier and certainly better made than 90% of the homes they will make in 2023. Most modern construction is pretty darn janky, and certainly not made to last 130 years.

Richardsonian Romanesque is my favorite of the period. New electrical and plumbing can be laborious, but improving the insulation can be difficult. Do you have fireplace inserts?

TJM:

You’re on crack. $20K for insurance? Maybe in a hurricane prone area… but usually, they’ll just drop you like a bad habit.

I own a 45 year old house…. I have a HO5 insurance policy and the cost is @ $1,500 for 12 months… with a structure replacement cost value of $600K + inflation endorsement and $500K in contents coverage – plus the other gingerbread endorsements that I added.

I believe, in this article, the correlation between used and new home price points is comparing production/tract homes.

These types of homes are built where land as well as the construction standards are cheap.

The lack of appreciable equity in the suburbia used homes because the corporate builders will build 1000 new homes in a new development phase directly next to the 1000 used homes.

Always by location, location, location first. I’m assuming the $2M home you’re referring to is in a desirable part of town. Maybe 50 years ago it was a production house on the edge of town. But now, it’s in the center of the city.

The article compares the median price of ALL homes that sold. The median price is the price in the middle. If 1,000 homes sell, you put them all on a list, sort the list by price, and then the price of house #500 from top or bottom is the median price.

Wolf, I think what you are talking about is called the Median, it is right in the middle of the column.

The average price is generally the arithmetic mean.

Juliab,

Everything in this article and in my comments about price is the “median” price. In my article, I specifically say “median price” 8 times. In my comment, I explained the “median price” with the 1,000 homes example. There was NOTHING mentioned about “average” price. Is Google translate throwing you for a loop? (idiom for “confusing you”). At some point, you have to look at the actual English here, not just at the Google translate version into your language.

Isn’t that, in large part, the conundrum of trying to level these figures out as comparable? If the majority of new construction is in the South and Southwest, generally those prices would be lower than the Northeast, far West, etc. If we localized these stats, the difference might be more telling. Purely anecdotal, the most recent 2 sales to me were a new construction split level, legitimately no yard cut out around the house to the point of trees are almost touching it, small lot, house right on a main road, you get the picture. The other was built 25 years ago, custom cape, meticulously maintained and the list goes on. Guess which sold for more? Data doesn’t look at product in every scenario.

Kentucky

IMO you have it nailed. I love Wolf’s analysis, but in this case, Location Value in established homes is acting as the boat in a rising tide that is pulling up aggregate values of the cohort. Desirable building locations do not grow on trees. Unfortunately, it seems that the First Three Rules of Real Estate have been forgotten, or at least often overlooked to focus on Amenities.

Houses built here in the last 10-20 years are garbage. Low density Douglas Fir or white wood lumber, 5/8″ imported drywall known to make inhabitants sick, PEX plastic plumbing that will definitely leak causing massive water damage within a few years. Particle board cabinets and only the cheapest laminate flooring that’s only a hair stronger than cardboard. Wiring is just thick enough in gauge to squeak by minimum code requirements. Also thrown together by the lowest-bidder unskilled labor scrounged up in the pandemic years. Not to mention the minimal landscaping and tiny sapling trees that may or may-not grow into big greenery. Oh, and the owners get the nearly guaranteed excitement of participating in a class action lawsuit against the developer for building a hilariously sub-par product full of egregious defects.

I’ll take my 1978 build with dense old-growth lumber, 3/4″ drywall made with pure domestic gypsum, copper tubing & heavier gauge copper wiring plus durable tile floors any day. Big green fully-grown trees in the neighborhood add charm. This place will easily be here 100 years from now with just basic maintenance. In comparison, people buying new houses here in the states will be lucky if their cardboard & stucco shizboxes are still standing in 50 years.

‘PEX plastic plumbing that will definitely leak causing massive water damage within a few years.’

Nope. Pex is fine. You may be confused with some of its predessors.

My guess is we’re going to be seeing lawsuits in the future when someone discovers toxic chemicals leaching from PEX – either all of it or just that from specific manufacturers. There are some papers on that already.

Not Sure

Add, make sure you have good fire insurance. If you live on a block with these cardboard homes, if one catches fire the whole block may go up in flames.

Nonsense. Your 1978 will creak, squeak have a lousy insulation and generally have outdated layout aka time capsule (Huge living room, small kitchen). Might not even have a garage. 1978 house will use 3/4 drywall, but will be generally built with 2×4, paper insulation, while new one will be built with 2×6 and r19 insulation per most local build codes. Your house will probably have a better lumber, that I agree. Quality of work by contractors used by builder is a key.

Building cable is AWG12 or AWG14 in the US,other than installation or lightning damage it’s fine with appropriately sized circuit breakers. Connections are the weak point as residential new-construction electricians are the least experienced and lowest-paid. Quite agree with your other points.

haha, I just looked at a house built in 1974 that has copper clad aluminum wiring, early particle board floors, crappy insulation and doug fir framing. It’s rotten, literally.

They’ve been building well and building crappy for many many decades. Honestly not seeing much in the way of used homes that don’t need at least some structural work here, and many that need more work than is anywhere near realistic for the price..

Since house sales are plunging in the US to the lowest level in 14 years, why aren’t housing prices falling accordingly in most US markets?

Sales plunging could be symptom of less supply (house owners waiting for rate cutes or “knowing what they have”).

Price is detemined by supply vs demand. If supply drops, but demand is still roughly the same, prices may stay the same or even increase.

This feels like the quiet before the storm – actually it feels like the last frenzy at the end of a party – we’re simply waiting for the tsunami of sales as panic finally sets in. We’re not there yet.

Realtors, Sellers, and Builders all want the highest asset price as possible. Even if anyone in those groups could predict where the market was going, his greed will make him want to hold out just a tad longer for that highest paying buyer. This causes a lag where sales must be fewer and for longer. Lack of sales must prelude a drop in asset price because of man’s nature. And since we are in a downward trend, it behooves them to adhere to what Wolff has said, “the one who panicks first panicks best”

This is much different for homeowners vs. builders. Homeowners can simply change their minds about selling based on whatever market predictions they have in their heads and continue living in their homes. Builders are not free to do this; if they are not continually building and selling new homes, they have no revenue and yet still have salaries to pay, etc., so they might as well permanently close up shop.

Wolf has done recent articles on the current margins of publicly traded homebuilders. Those margins are great, so don’t expect any of them to close up shop soon.

You are correct in that homebuilders are like Sharks. They meet to keep moving (turnover houses). They have zero attachment to the property, they just want to aquire land, build, sell and move on.

However, it should also be noted that homebuilders are also more experienced and knowledgeable than the average seller. So if they are dropping prices quickly relative to used house sellers, it is probably a good harbinger of where used house prices are going to go.

This is how every market crash begins.

Deals fall first, but prices take more time.

This is the time when supply increases and deals remain few.

Because people know in a inflationary environment to hold assets ,

Thanks for the update Wolf. Definitely the craziest housing market I’ve seen, and very thankful to be fully retired from five decades of construction and rehabbing of homes, as well as commercial and institutional facilities.

Question is, what are folks going to do when faced with interest rate rises and incredible increases in property insurances, especially with increased losses?

Just saw report of a condo in FL facing a 1,000% increase THIS YEAR!

Anecdotal for sure, but other reports have insurance companies leaving FL and CA, etc.

Celt, in the last ~200 years, people have dug up billions of years worth of dead plants and animals, then proceeded to burn them in the funeral pyre of their lifted dually diesels, on the way to Walmart, for the third time in a week. Yet, the airborne carbon dioxide levels, while much higher than they were, are still only ~400 ppm. Most of the CO2 has been absorbed by water, in the ocean. I don’t have space to discuss why this is important… my main point is that nobody I ever met denies how much carbon humans have oxidized for fuel over the last two centuries, yet people deny the ramifications of doing this. I can’t understand this denial… the mass balance and energy balance equations for this are not at all theoretical.

They’ll go bankrupt.

That’s the only way out of this huge mess. Everything eventually ends up in bankruptcy.

VintageVNvet

Why are the premiums going up so much in Fla and Texas? I also believe the insurance companies may be cost shifting their large claims to other states. I recently noticed a high premium increase from my USAA homeowners ins here in Maryland for no apparent reason.

SC:

Roof replacement fraud in FL. It’s a big business down there (actually “here” at the moment).

Also: roofs here in FL (allegedly) have a 14 year life span. Insurance companies want some assurance that the roof has been replaced after that window or they kick you to the curb.

Son lives in TX. Roof fraud there too. Hail damage claims.

14 year life span of a roof? What kind of roof is that? I had the roof on my house redone after close to 100 years service life. If maintained the roof should be good for close to 100 years more.

Ok natural stone roofs are of the more durable kind, but even galvanized steel may last 50 years.

Your drywall thickness understanding needs updating. 1/2 drywall for walls ( 16″ centers ) and 5/8 for ceiling ( 24″ trusses or joists) has been the standard since the 50’s, never seen the 3/4 you state. Even if 1″ or 1 1/4 required for fire or code separation esp in commercial, usage just doubles up the 1/2 or 5/8 to achieve the thickness. Even curved surfaces use doubled 1/4″ to get to 1/2.

Your understanding of Pex versus the older discontinued grey poly needs updating. Air contamination pitting and pin hole leaks of copper is very common, requiring re-piping.

Correct on all details RH.

Copper challenge is the fact that we put copper pipes directly through concrete without any sleeves for many decades, and the chemicals in the concrete eats away at the copper.

Once had a client that insisted we jack hammer out the floor of the bathroom where the copper was leaking, so we did. Came back a couple months later and did it again.

Finally convinced them to run pvc at the perimeter of the slab and just go in through the exterior walls to the fixtures, as had been standard practice for years by reputable plumbers once this problem became understood.

Plaster used to be common in approximate thickness of 3/4 inch, with a 3/8 scratch coat, 1/4 brown coat and 1/8 finish coat; good exterior plaster, AKA stucco is at least 7/8,,, but both can and do vary a bit depending on how straight is underlying framing. I have seen both 1&3/8 thick on top of older rough cut framing that varied from 4&1/4 to 3&3/4, put up before planering of framing to net sizes was common.

We use 1/2″ ultra-light drywall on ceiling and 24″ stud bays now, works great and easier to hang. I think the aeration makes it stronger and the lighter weight resists sagging. I’ve also been using FM1960 PEX (expansion) for a couple of decades, good stuff. I’ve replaced a lot of leaking copper with PEX, even non-buried copper will develop pin holes if you don’t control your water’s PH.

18 days on market. Doesnt look like home buyers got the memo either. Cant blame the home sellers for not dropping prices. Until that pent up demand fades I dont see these numbers going south in a hurry outside the major metros that are being emptied.

Their memo is different than ours. It reads “There’s no tomorrow”

At least Wolf and many of the commenters here are coming out of denial regarding used house prices shooting back up nearly to the peak. All spring some of us were trying to sound the alarm–prices rising, multiple offers and swarmed open houses returning–and were dismissed over and over again.

Accepting reality makes for healthier analysis and better forecasting.

Pea Sea, I would not characterize Wolf’s analysis as being in denial. He shared the data at the time, and the data did not support your contention, until now. Thank you for bringing forward insight from a specific market area.

Pea Sea,

LOL. I don’t know how many times I hafta repeat it, but I will:

It’s seasonal. The peaks every year are in June (see the red line in the second chart). Today we reported June. Prices will drop for the rest of the year. We know that. What we don’t know is by how much they will drop.

No one is coming out of denial. The spring season was pathetic period. Only a few homes had multiple offers from the very few buyers who were in the market.

What metro?

Herp

Most metros. It’s BS that there is a robust housing market with huge, dare I say it, “pent up demand.” 🤮 There is low inventory but also low demand. During the spring FOMO, a few morons came out of the woodwork and bid up a few homes period.

Yeah, that must be why prices are almost back where they were at the June 2022 peak.

Lol, are you a realtor Pea Sea? Because that’s exactly what my realtor friends sound like, except since they are friends and I know them I can see the wishful thinking behind the facade of confidence they try to sell. I can’t blame them because RE is a tough business in the best of times, and it isn’t the best of times right now given the sales volumes.

That “are you a realtor” bullshit is exactly the response we got for the last six months while we tried to tell you that the bubble was reinflating.

Nope, I’m just a person who doesn’t see any point in being delusional.

Pea Sea,

Later this summer and in the fall and winter, when the red line on my charts heads south, as it will because this increase through June is seasonal and happens every year, to be followed by a decline, are you going to recant?

Wolf is not alone in thinking home prices will drop later this year. Plenty of Utube video people as well… he is not so fond of.

Wolf has his pretty convincing graph demonstrating the seasonality effect… I’ve let others (yahoo finance) know about it.

The utube people usually cite median house price to median household income or median household income to median mortgage payment, etc … as reasons for a downturn in prices.

Of course if the 30% wealthiest segment in our country decided to invest strictly in real estate these median based ratios wouldn’t be of much use.

Others have pointed out that the median priced home is not bought by the median priced household. Rather by a higher (perhaps 60 to 65% decile ranking) than median income household.

BTW, a lot of renters have high incomes and are “renters of choice.” Nearly all multifamily that got built since 2008 was built for people with above median incomes, because that’s where the money is. The big landlords of SFH are also marketing to renters of choice with nice houses and fairly high rents. This whole thing that the only people who rent are lower-income people who cannot afford to buy a house is nonsense. That’s not how the rental market works. The median rents of a 2BR in New York City, San Francisco, Miami, Jersey City, and many smaller markets is at or above $4,000 a month. This changes the equation that a “household with median income doesn’t buy a median-priced house,” considering that about 65% of households are homeowners; 35% are renters, and of those 35%, many are renters of choice with above-median incomes.

The point is not that there aren’t plenty of wealthy people who rent.

I am ALL TOO AWARE of that otherwise CBS would not have had an article recently about a gal paying 2400 a month for a 800 ft² apartment in Dallas.

Don’t know that she is wealthy but there are (per websites) plenty of 1 BR apartments in Dallas in the 700 to 1000 price range.

The point is that a large percentage of people who are poor or lower middle class can not afford a house. I’m guessing you agree with that ?

I am sick and tired of the media telling the world that apartments only rent for 2k and up.

Please stop it.

About HALF of the apartments on the market in June asked for over $2k; the other half on the market in June asked for less than $2k. Because $2k is about the median asking rent in the US now (Zillow has it at $2,054).

I’m sick of this stuff about only poor people are renting. It misrepresents the vast and complex rental market.

Yes, there are lots of people who cannot afford the kind of house they want where they want; but they can probably buy a halfway decent house in Tulsa or Omaha (50% of the houses there sell for less than $275K, so $200k should buy something halfway decent). But they don’t want Tulsa or Omaha, and they don’t want halfway decent.

Replying to Wolf,

We’re bothnrihht yo some extent you are simply ignoring my point.

As for Tulsa…its ok. Already 30 90 degree highs, 3 100s with 9 more 100 degree highs forecasted per accuweather website.

Tornado issues. Too religious for my liking. And it gets cold as it’s windy in winter so wind chill is for real.

Correction in brief response to Wolf,

We’re both right… to some extent you are simply ignoring my point.

There isn’t a lot of pent up demand, only propaganda,. There are very few buyers period. If I hear that phrase “pent up demand” one more time I’m going to lose it. It’s so overused by the mainstream propaganda sites.

My brother sold his house just this last monday, he had over 30 offers. I put offers in on 3 houses in NH this spring, 5%, 8% and 11% over asking, respectively. Outbid on all three.

If theres no “pent up demand” then why are there so many additional buyers for every house being sold? The housing market is simple supply and demand. If there was no demand we would have seen more than a 1% yoy drop in prices with these high mortgage rates, and yet the sharks still feed.

Lololololololol whatever!

Great chat

Herp

Likewise

Plenty of metros are way over 1% drop. Geez, you believe that all homes are only down 1%? Wow!

Millennials, while several years late to the buy a house game, are definitely in the game now. That’s a sizable chunk of the demand. Combine that with very few houses being built. My first loan back in 93 was at around 6.5 or so. These rates aren’t the abnormal rates; it was the fire sale rates that were abnormal, and people got used to them so thought that was normal. All that happened was folks who otherwise couldn’t afford a place got lucky with super low rates so bought. Don’t count on them selling anytime soon.

This was a Fed created mess.

They were obviously investor purchases. When great homes come on the market, investors step across “the sidelines” to create dynamic demand that will match the supply of great homes. What your brother sold, and what you are bidding on are obviously “great homes” only.

Fed Up,

I’ve been sort-of looking to buy in

the Boston metro for a long while

now. At the low end of the market,

anything that is remotely reasonable

sells extremely quickly.

If HerpDerp’s brother had his house

priced in line with everything else or

a tad under, and let it sit on MLS for

two or three days, I can totally

believe he gathered up 30 offers.

I’m not even looking that diligently

anymore, since the last three times

I contacted a used house salesman

with a question about a property, the

answer has been a variation of

“already accepted an offer”. One of

those was the same morning it was

listed.

It’s still stupid out there.

J.

Differing opinions create a healthy market.

Based on historical data prices should reduce after spring price increases, however historical performance does not tell the future.

There’s also a lot of games played. The house “sold the day it listed” was probably what is referred to as a pocket listing for a week or so. The realtor contacted a few of their customers to see if there was interest in that property. They wrote a contract, listed it on the MLS, and then it went “under contract” 5 seconds later. Ethical? No. But it happens.

Those of you trying to buy a house with 5% down and an FHA loan…. most sellers won’t even talk to you – in good times and bad. I know I wouldn’t. Why would anyone in their right mind take their house off the market, suffer through a “get me done” sale, and potentially miss a qualified buyer that walks past a house showing under contract? Too much brain damage.

The Boston & NH markets haven’t come down much, but never got ridiculosly overpriced like Seattle or coastal CA.

Housing is coming down overall nationwide, but there are still local differences.

The greater Boston area has always been an expensive market to rent in – perhaps this has kept home prices elevated?

El Katz,

It’s possible that there were shenanigans

happening with that listing, I don’t know

about “probably”, though.

Things really are silly enough that a offer

of $35k over asking on a 850-square–

foot 3 bed, 1 bath sight unseen or with a

drive-by, but with a stipulation that “you

have to agree right now, and cancel the

open house you have scheduled for noon”

seems like a reasonable strategy.

Almost nothing that makes me stroke my

chin and go “Hm” lasts for more than a

handful of days on the market. Like I said,

I’m sort of tuning out, and hoping for things

to calm down. (That is calm down from my

perspective; panic on the part of sellers

would suit my own situation.)

J

J

Also in the Boston market.. the houses are just sitting there now in my town. The only sale I have seen in the past month was waterfront.

Kurtismayfield,

I’d really like something cheap in

the Cambridge/Somerville/Arlington/-

Belmont/Watertown/Newton/Waltham

area. I’ll browse through stuff for sale

at far as Billerica or Framingham, but

I’d really like something closer. Of the

houses that catch my eye, the ones

that tend to last the longest are the

ones with open houses over a weekend,

and go under contract on Monday or

Tuesday.

MM,

My current rent is actually way below

the going market rate, so that’s sort of

a disincentive to buy a place. (The

landlord seems to like us, he thinks we

are good tenants because we have

never hassled him, and if something

breaks, we just fix it ourselves.) If you

took the 71 or 73 bus regularly in the

last couple of decades, you might be

a familiar face, by the way.

J.

Yes — and pent up does not equal realistic or qualified.

I’ve been p

I’ve been pent up for years where a house on the Big Sur coast is concerned.

And your expertise in the real estate industry comes from where, Fedup???

I own a brokerage in south Florida, a single family construction business in Texas and investment properties and land in both places and you are 100% wrong.

Florida and Texas had some of the biggest bust last time with no work. This time? Just look at the upside of the graph from bubble to bubble and imagine the scale of downside coming this time. All these theories why “this time is different” by R.E. investors is so fully laughed at by equilibrium. I said this two years ago and still believe its coming that a Costco job will be considered a good job and buy you a house, and people will be giving away houses for free to get out from under the tax burden. NOT doom and gloom just what I see as a global economist(my hobby).

I lived near Dallas in the 1980s, 1990s.

Mid May to early October the weather was quite bad. Has only gotten worse.

I think people are foolish to move to Florida, TX, Arizona… I live in eastern Washington and the summers starting in 2013 have gotten hotter, not unusual to average 90 for July August. We never have a below average month…always hotter just a matter of how much.

Two years ago it hit 113, five days over 100 in June. Per the accuweather website for Spokane. We are almost a 1000 miles north of Atlanta, just north of Quebec, Canada.

Will I move back to Texas… not likely !

Per my comment below… I follow weather temps just looking at monthly data from accuweather website.

Dallas-Austin is having its 2nd very hot summer. I noticed 2021 was average possibly even a degree or two before.

But last year and so far this year…as nature seems to do… its way more than making up for the slack provided in 2021.

Wish I could brag about Spokane’s climate. Its not the worst in the world, but its closer to the worst than the best imo. Been here 24 years know what I am talking about.

I’d move back east but still remember the humidity difficulties. And deluges of rain. Not a problem here… just wildfires and potential smoke August thru mid October.

Just today I saw a house pop up on Zillow I had marked as a reference. Listed in May 2023 for $1.5M, dropped to $1M today. I have seen about 20 like it over the past month. It is in an area that was up 80% from covid at its peak, but it is a start.

I have the sense that some sellers are starting to take their 40% gains in 3 years instead of waiting for the mythical 100%.

I’m seeing that too. Basically, there are a lot of empty houses. People aren’t going to hold them empty forever, paying the carrying costs (taxes and insurance are increasing every year, sometimes by double digit percentages), before they realize to cut their losses.

We’ve seen this movie before, and we know how it ends. I heard the same nonsense in 2007 about it being different this time because of Gen X buying new houses…

Not only that, unless they are just concrete shells, an empty house rots. It decays faster from condensation than damage a normal tenant will do to it. And that decay is structural and inside walls, not just cosmetic wear and tear.

Huh?

Unless you live in some wierd area that has severe condensation damage (like say saltwater damage on the coasts) or have been lucky and have had the best renters ever, your comments about an empty house decaying faster than renters damage is crazy.

Sure an empty house generates no income, but it doesn’t depreciate that fast. There is a reason houses have a 30 year depreciation schedule in the tax code.

Look at how irrational the used-home market is. Huge spikes and drops every year.

I think that’s seasonality but the ridiculous gains over the last decade aren’t. Nearly 3X the 2012 bottom!

Outpacing median income I’d venture to guess.

Another great illustration pointing to the damage done by juicing asset prices in the years before COVID.

If we only would have had the COVID relief nonsense but not had an already inflated base the world economy wouldn’t be so F’d

At least stocks may have topped today🤷

Digger Dave,

Seasonal. The peaks every year are in June. Today we reported June. Prices will drop for the rest of the year. We know that. What we don’t know is by how much they will drop.

I should have clarified. I was commenting on the magnitude of the seasonal changes in the used market versus the new one. The used market, with irrational parties on both sides, swings greatly seasonally compared to the tight swings in the new sales market, where one party is completely rational. It just shows to me that used buyers can be duped into paying inflated prices in the spring when demand is up marginally and that used sellers can panic in the off season in the same manner. Like you’ve said, someone in the business of making these things knows what they need to do to move it, so they price it appropriately.

Wolf,

I’m not disagreeing with your opinion…only the confidence in your opinion.

Bill Miller (at Legg Mason i believe) beat the S&P 500 index 15 years in a row, 1991 to 2005. It came to an end. I think it underperformed badly for one year thereafter anyhow.

There were 8000 funds at one time.

You can make some simple assumptions, pretty reasonable, and see that it could be expected that one of these funds might be expected by chance alone to beat the market 13 years in a row (2¹³ is just over 8000).

Humans can be quite surprised by what probabilities tells us sometimes.

The assumptions in my 8000 funds discussion are pretty strong. They actually aren’t all that reasonable… all 8000 funds would have to have stayed in existence the full 15 years (each with probability of 0.5 of beating the S&P 500 in any given year, i.e. mimicking an SPX index fund. Fund performances independent of each other.

Probability none beat it all 13 years is only

(1 – 0.5¹³)⁸⁰⁰⁰ …giving it brief thought).

Nevertheless, in the same neighborhood, and with the same square footage, new houses are more desirable (if of equivalent quality), and many neighborhoods now have new and old houses. In 2006, and earlier, I was telling clients that real estate agents were being crooked in claiming they had to buy real estate or its price would increase later to infinity and beyond. One was even convinced to max out his credit cards and business’s credit line to be able to buy a mini mansion that he could ill afford and abandoned years later when it went underwater!

Now, the same thing is starting to happen: inflation and comparatively limited wage hikes are making higher and mid level homes less affordable: new homes decline less, because they are more desirable. Smaller, used homes are also over valued, so will sell less until the correction in prices occurs. That (and their car loan debacle, loss of their temporary “investments” in CCP, Ponzi companies, over leveraged crony companies, and even in the value of their longer term bonds and Treasuries paying lower interest rates) means banks’ are again legally insolvent.

These banks incredible greed and consequent reckless risk taking repeatedly get their total assets’ realizable, fair market, value reduced below the value of their debt so that they are like the mythical lemmings –financially speaking. Their not really “Federal” Reserve will have to give them gigantic ultra low interest ratr (below the real rate of inflation), gift loans to recapitalize them again: i.e., it will give more US tax payer capital (in real dollar terms) to its bankers and their cronies, yet again! As Simon Johnson’s “A quiet coup” pointed out, their control of politicians makes them our new aristocracy –since they got their not “Federal” Reserve con job passed into law in the last century and repealed the Glass Steagal Act.

Before you start beating the correction drum there’s a couple reasons why this phenomenon may not “correct” as you seem to believe. First has to do with location. When buying a home unlike a new car the location is of utmost importance. New homes although shiney may not be in the best location. Certainly the case for cities like San Fran, New York and others with very limited space. Second reason is very few are will give up a 2.5% interest rate to buy anything new at 7%! So relax with the correction drum beat 🪘!

“Very few are will give up a 2.5% interest rate to buy anything new at 7%!”

Correct. But they also then vanish as BUYERS. So supply and demand drop in equal measure, and the entire market, buyers and sellers, drop by 20% to 25%.

Hot off the press:

“They’re not listing their homes because they’re not moving out because they’re not buying a home to move into because they don’t want to give up their 3% gift from God.”

https://wolfstreet.com/2023/07/21/entire-housing-market-buyers-and-sellers-may-have-shrunk-by-20-25-because-of-the-3-mortgages/

Do they all vanish as buyers, though?

A house with a 3% mortgage makes for a pretty nice investment. I would expect the rent covers your mortgage and costs in most areas, and often with money left over. That’s before you even take into account house price appreciation, which is where you likely need the long view, and yearly rent increases.

You don’t think there will be an increase in people who just buy a second home and rent out the first?

One topic at a time. What you outline is another topic that may be coming soon here. This article discussed homeowners living in their homes.

You’re discussing how a homeowner becomes an investor. This is happening a lot: condos listed as vacation rentals or permanent rentals, rent-controlled apartments where the tenant doesn’t live in it anymore but subleases the apartment or lists it as vacation rental (rent arbitrage); homeowners that move from a touristy city to somewhere else and list their house as vacation rental… This is a very different topic, and it does have an impact on the housing market, but it doesn’t belong here.

Sales of used (resale) single-family (SF) homes is going to remain at low levels as long as the 30Y fixed rate remains high. Existing homeowners are locked into record low mortgages rates from refinancings during ZIRP. Unlike many countries, US homeowners typically have the luxury of no prepayment penalty and 30Y fixed rates. So intelligent consumers locked in 30Y rates ~3%. Now that 30Y rate is closer to 7% and existing homeowners cannot qualify for a new mortgage to buy a larger home or change locations. Unlike some other countries, US mortgages are non-portable. So you have a whole epoch of homeowners who are handcuffed into their existing living situation by their golden mortgage rate.

Further, newly built new home sales, mostly the large public homebuilders, are devouring market share and have more than doubled their share of overall home sales (new & resale) to over 30% from historic 13%. And they have tools that resale sellers simply do not. Namely, mortgage finance divisions offering permanent 30Y rate buydowns so that home buyers can afford that new house, because they are getting a discounted mortgage rate (5% is the magic number). It’s 1/3 the price to buydown the rate as it is to cut the home price to qualify the same buyer income. Builder margins remain well above long term averages, so there is room to accommodate buyers. Resale cannot compete, not that there is inventory anyways.

Personally, I think the YoY drops from peak market in 2022 are still fairly inconsequential. Homeowners are sitting pat on high home equity and are still deep in the money. Even if you bought at peak, you don’t care because you locked in a low mortgage rate so even if the sale value has decreased, you are still ahead on cash flow at current rates.

So what’s it mean? My predictions: SF home sales are going to keep ticking because that’s the only way many buyers can afford it, (and those incomes are still juicing with service inflation but new grads are about to get a kick in the groin). Resale home volumes (and prices) will stay in the gutter until rates come down and the next wave of opportunistic high-value home sale transactions. Sure, there is a valuation bubble, but which event will pop it remains unclear.

Well said. What will pop it is the incoming srock market crash ( entire market hangs on 5 stocks). Then layoffs. Then foreclosures. Every third house will be for sale.

Of this I am certain, even though many have Low LOW mortgages and Yes they will never give them up…. Death, divorce and the vicissitudes of employment are the acid that eat those binds away in short time.

Thus the 7 year turnover rule.

Slowly slowly catch the monkey.

It will fall and it will fall until they, who hold the reins, panic …. that may not be for a long time as we are not yet out of the woods of Inflation.

I’d rather buy a new house than a used one. At least I can get some kind of warranty, for whatever that is worth. Sellers of used homes are still in greed mode, or imprisoned in their 3% mortgages. Cash buyers like me can just wait, and collect 5.5% while waiting. Or rent a nice place cheaper than a 7% mortgage on a $500K house, plus all the other crap you have to pay for when “owning” a house.

“Cash buyers like me can just wait, and collect 5.5% while waiting. Or rent a nice place cheaper than a 7% mortgage on a $500K house.

that don’t make sense to me, what did I miss?

if you pay cash then you have no 7% mortgage payment.

if you collect the 5% but pay rent its a wash at best.

a paid off house is the end game, anything else is just spinning your wheels imo

Renting is much cheaper than buying right now, almost everywhere. And by a lot. I’m renting a place for $2000/month, and I could buy a comparable sqft condo, making a 20% down payment, and still be paying $4150 a month.

Historically rentals have been cheaper than purchasing.

Percent home ownership has increased over last 50 years as SFH new builds increased and multi-unit dwelling new builds decreased.

Between 1950-1975 baby boom increased population and there was not enough housing so multi-units were built as rentals.

Since 1980s less people wanted to rent. Kids started to live longer with their parents and move out directly buying a house.

However, recent trend shows multi-unit new builds increasing again. Some rental builds, some condo builds.

“Renting is much cheaper than buying right now”. If you say so, I built a beautiful custom home 3 years ago for $375k a slightly bigger( but older) house across the street just rented for $4950/month.

I was just saying it is not a good time to buy a house, whether with cash or using a bank. I could have been clearer. I imagine a lot of buyers are on the sidelines now.

I wonder what percent of the new homes built are built for rent.

Its not a wash. Its much better to rent and collect 5% then buy a house right now. Play around with some rent vs owning calculators. Prices have to come down a lot for me to trade in my cash for a house.

100% agree.

I have seen rentals for $1500/mth in a lot of metros.

Same house next door on the market for $1.5mil.

Does not take a rocket scientist to figure that math.

Elbow, that’s my opinion too.

You can rent a $1.5M house for $1,500 a month?

Or is it the tear down next to the $1.5M house that’s for sale?

Don’t forget property taxes. The property taxes get paid out of your rent, and that’s something you would have to pay even if you owned the home free and clear, anyway. The 5% on your cash only needs to cover the remaining rent.

“I have seen rentals for $1500/mth in a lot of metros.”

Nonsense. In any area where the hoses are “worth” that much (even w/ today’s bubble prices), the landlord can and will charge much more.

It also doesn’t make sense that a landlord would rent below the property’s carrying costs – that’s happening now only bc rents haven’t caught up to home prices.

elbow, I agree.

For instance: if you buy a $500K house with 20% down, and an interest rate (straight interest, no principle), you have a $2300+/mo. cost. In some cities, a $500K house is in a marginal neighborhood. When it comes to home ownership, nothing is more important than the school district.

Now factor in: property tax: $850/mo, give or take. Homeowners insurance at ? Maybe HOA costs (which only go up over time), some utilities or landscape maintenance costs that you wouldn’t have if you were a renter.

Deferred maintenance set-aside for carpets, paint, appliances, HVAC, water heater, misc. expenses. And these numbers are worse for a used home. Add up the pieces and you’re probably well over the cost of renting that house. Youtube videos and some good hand tools won’t help with most of those costs.

Bottom line: at the current nosebleed house prices, “value” of a real estate investment is not being considered and RISK is being ignored. Everyone is duped into believing that housing prices can grow to the sky. Bubbles pop. Ask Isaac Newton.

Many urban areas 1 BR 700 to 1100.

Mortgage for 300 to 500k house 2000 to

3000. So on average 1500 difference…hey I can’t buy a 1 BR, 1 bath house.

Condos very dangerous i have read on resale… Boston late 80s, early 90s i read (Dallas Morning News) some condo owners could not sell them for half what they had paid. Nevermind them.

So 1500 savings per month, 18k annually.

Save utilities, property tax (4k), maintenance total 6k.

So 24k saved, more time to read Wolf street and other stuff.

Not insignificant.

If I invest that 24k at 5% CDs an extra 1200.

(Sorry Wolf, I still do CDs, maybe treasuries in the future).

I owned a 3/2/1 SFH, 1650 ft² for 10 years. It was much more than I needed, now at

575 ft².