They’re not listing their homes because they’re not moving out because they’re not buying a home to move into because they don’t want to give up their 3% gift from God.

By Wolf Richter for WOLF STREET.

The exact numbers are hard to nail down, but we can guesstimate from the figures we have that the entire housing market, both buyers and sellers, has shrunk this year by about 20% to 25% compared to pre-pandemic years.

Meaning 20% to 25% less demand and sales and 20% to 25% less inventory and new listings, with prices down a tad year-over-year, showing that the market is roughly balanced at this smaller size because buyers and sellers have vanished in equal number.

And we know who they are: the homeowners in 3%-mortgage jail that now cannot buy, and therefore cannot sell.

The 3% mortgages that a lot of homeowners now have after the huge refinancing boom during the pandemic prevent those people from buying a new home because they might have to finance it at about 7%, which would increase the monthly payment on the same size mortgage by 50% or more.

So these people aren’t buying. They aren’t even looking. They have left the market as buyers, and so there may be 20% to 25% fewer buyers.

At the same time, and in equal number, these people, who cannot buy a new home, therefore cannot sell their current home because they continue to live in it, and so they’re not putting their home on the market, and inventory shrinks by the same number as buyers have left. Less inventory and fewer buyers in equal amount.

These homeowners with 3% mortgages don’t want to, or cannot, upsize or downsize, or move to a different location, move closer to the kids or parents, or whatever – unless they want to give up their sacred 3% mortgage that now increasingly looks like a gift from God.

And for Realtors, the 3% mortgage – as much as they loved it at the time – has now turned into a gift from hell, because the real estate industry is making commissions coming and going: One, when these homeowners sell their old home, and two, when they buy a new home.

Each household that is now prevented from changing homes because they’re locked in by this 3% gift from God subtracts two transactions from the market – one when they buy a new home, and the other when they sell their old home. And Realtors are losing both of those deals.

The fact that Realtors are losing both of those deals is why the industry is so upset about these homeowners that refuse to sell – and it consistently blames them for the low inventory.

But the industry fails to state the other half of this reality, though they all know it: That these homeowners who refuse to sell have also vanished as buyers, and therefore this portion of demand has dropped in equal measure with inventories.

This is happening with a fairly large group of homeowners: They have left the market as both sellers and buyers at the same time and in equal number.

Which explains in part why sales volume has plunged so far because those potential buyers with 3% mortgages have left the market. And it explains in part why inventories have dropped because the same people that cannot buy aren’t putting their homes on the market.

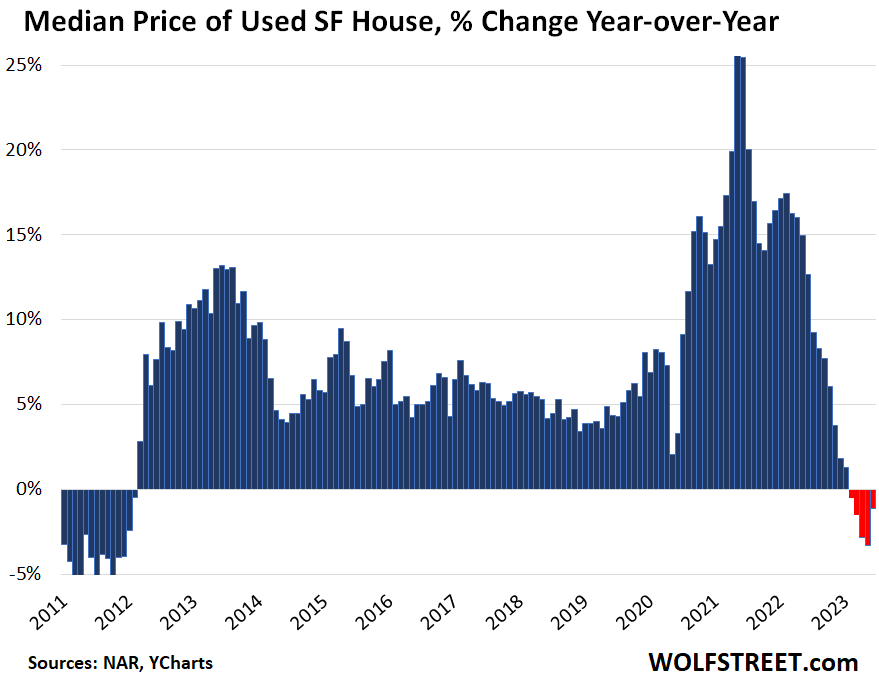

That’s the big reason why we have this strange combination of plunging sales along with a national median price that has dropped year-over-year for the first time since the Housing Bust, with homes spending an increasing number of days on the market, amid growing but still tight inventory (all data here from the National Association of Realtors).

To set the scene: The national median price has been down slightly year-over-year for the fifth month in a row, a sign that the market is at a deadlock because mortgage-jailed potential buyers and potential sellers are the same people, and they’re not buying and they’re not selling.

Seasonally, the median prices released by the National Association of Realtors generally increase in the first half of the year, peak in June, and decline in the second half of the year (though part of the seasonality was upended during the pandemic). That’s just the normal seasonality of the housing market. Yesterday, we reported June’s median price of single-family houses; and based on seasonality, prices can be expected to go down for the rest of the year.

But the year-over-year comparison eliminates this seasonality. On a year-over-year basis, the median price of single-family houses dipped 1.2% in June, the fifth month in a row of year-over-year declines.

Second: Sales of single-family houses in June were down by 22% from June 2019 and by 23% from 2018. Since October last year, the declines in the current month from the same months in 2019 and 2018 ranged from -15% to -28%, because the mortgage-jailed households aren’t buying.

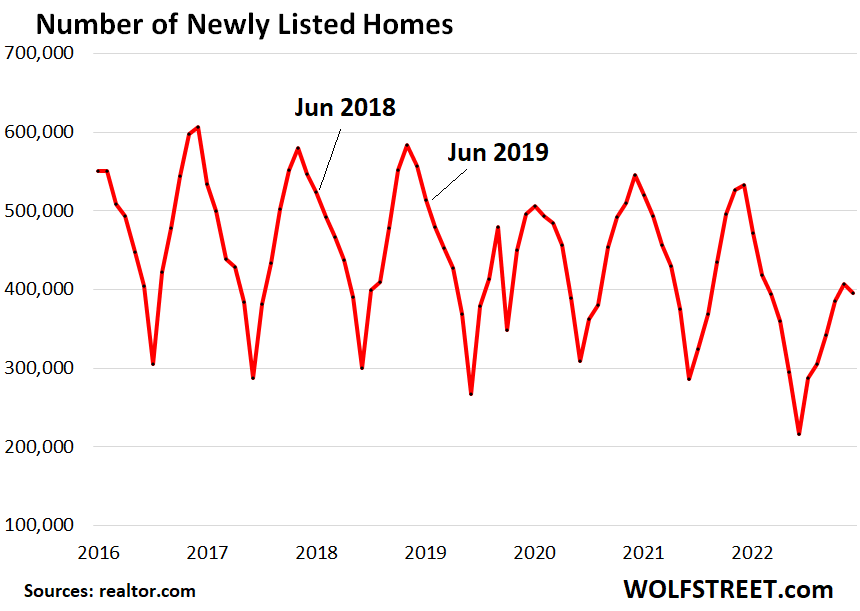

Third: New listings in June (396,100) were down by 23% from June 2019 and by 24% from June 2018, according to data from realtor.com, in part because the mortgage-jailed are not listing their homes because they’re not moving out because they’re not buying a new home to move into because they don’t want the payment of a 7% mortgage:

These declines in the 20% to 25% range keep cropping up across the demand and supply measures, compared to pre-pandemic times, indicating that a substantial portion of the normal buyers-sellers have vanished as buyers and as sellers because they got their 3% gift from God, and they’re not going to give it up, and so they’re not buying a new home and so they’re not selling their old home, and the whole market, buyers and sellers, has shrunk by their number. And that may be the new normal for years to come.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The fed gives and the fed taketh away.

The Fed giveth to some and taketh away from others. If you’re a saver, someone trying to buy a house, or someone who works for a living (and therefore must live on wages rather than the income from a pile of assets), you’re one of those from whom the Fed taketh, and taketh, and taketh.

I feel this, all day, everyday.

income from a pile of assets

where they taxest taxest, increase costs/insurance 30%

all day long

========

and remember those who bought pre-covid and have sub 4% have MANAGEABLE mortgages given their income

with substantial increases in utilities, insurance, property taxes, maintenance of home

I felt like I’m month to month all year

saving?? what and for what given rapid decline in value of fiat $dollar

I have house to finish and will decide to flip or make rental

$18k v. 25% profit and cash for next one

I wouldn’t want to give up my 4% mortgage either. Even a 5 or 6 looks pretty good right now. Sad for my real estate industry friends.

Forever

Amen.

I wouldn’t give up my 2.375%. No way in hell haha

Yep, the society is called capitalism. Not that other structures have shown great promise on a large scale. I’m not sure democracy is compatible with capitalism. Especially when wealthy elites control the media narrative from both ‘parties’

No, it’s not called capitalism. What we have is a form of socialism called “crony capitalism,” which is the worst excesses of both socialism and capitalism.

No, Einhal. Crony capitalism is capitalism. You must be a crony, confusing socialism with capitalism. The oligarchs who control the political system, the news, and the financial system are not socialists. But they do have lap dogs who dole out the b.s.

Hello BH Lincoln, Totally concur with your take on the total corruption of media. But I do concur also with Einhal on his description of “crony capitalism” as a form of socialism. It’s the skimming of the cream by the wealthy elite. and the socializing of the loss and theft from the plebes. Just my take.

–Geezer

NAH to socialism OR capitalism per above:

It should be clear enough from the very definitive examples of the 20th century that when corporations and large private companies are in total control of GUV MINT, as is now the case in USA, it is FASCISM.

Consider the situation of the average German or Italian peon during the Fascism of 20th century, and then compare it with the case for the average Joe and Jane today:::

Same ol Same ol…

Now you know what is most likely to be on the way, or maybe, due to the control of the MSM, already here.

The meaning of words is adrift. I suppose today by “Capitalist” we mean corporatist and/or financier.

I believe in free enterprise and competitive markets. I’m not sure that I am a capitalist because I am anti-corporate.

I believe in ownership. The problem with a large corporation is that the enterprise is not longer owned by human beings. At best it is controlled. There is no longer owner liability or an owners vision or humanity. Large corporations are a form of artificial intelligence and could even be considered a alien life form in the manner of a hive mind.

…to restate, the goal of contemporary corporate capitalism has been to privatize all profit, and socialize all risk. If not seriously recognized and mitigated by it’s people, there’s a historic PNR for a well-functioning society (…at base: ‘laws for thee, but not for me…).

may we all find a better day.

Einhal’s take is correct. This is not capitalism. It is crony capitalism.

Adam Smith foresaw what we are experiencing now as a major weakness of capitalism. He hated rentiers, and suggested that returns of greater than 5% should be taxed away to eliminate the incentive to speculate.

Let’s sober up about this. Capitalists are not philosophers or good boys while the crony capitalists are underhanded bastards that game the system and are often, gasp, “Rentiers”.

Capitalists, historically, did not care squat about Adam Smith or John Locke. The robber barons decimated their competitors, cut outrageous deals with government, bribed their way through business, and so on.

There was never a level playing field. “Capitalism” is not some pure Platonic form that’s been corrupted by cronies. It’s an inevitable pitfall of the system. Laws emerged to put guard rails alongside egregious capitalist behavior and excesses, but, the regulators have been captured and turned inside out, the cronies are the regulators.

So go on witch your bad self and think that “Capitalism” is this immaculate conception and that only the bad boys are on the dark side.

Capitalism has its flaws of regulatory capture and cronyism but is so far superior socialism that it’s laughable to even compare our economy with true socialist economies like Venezuela and Cuba and North Korea, which are all basket cases with no freedom, economic or otherwise, and with far more corruption and cronyism.

Democracy is somewhat overrated, at least in the US and probably in general.

Here’s just two reasons:

1. Its limited in the US. We don’t vote for Supreme Court justices, no small thing these days.

2. It’s pretty typical for an election to be close. Many are 60-40 or closer.

If just over one in six (17%) of those voting for the winner instead voted for the loser the outcome is flipped (assuming the rest voted the same).

I’m just guessing but would think about 10% of elections are 55-45 or closer.

The problem is that its WINNER takes ALL. You lost by 2 or 3 percent too bad.

And American candidates can be so laughable (not picking on Biden or Trump here specifically)… they will win a very close election and proclaim:

“The American people have spoken” as if they had won in a landslide.

I dont even roll my eyes any more.

But yes, no matter how close the election result, the loser gets nothing.

I’m not suggesting we get rid of Democracy, just pointing out its obvious (to me if not to others) shortcomings (limitations if you prefer).

At no point have I advocated that socialism is a decent substitute for capitalism. I’m objecting to the fanciful notion that capitalism, in and of itself, is ideal, while crony capitalism is a warping of that pure system. Readers here are saying, if you criticize capitalism, you’ve got to be a socialist.

Government needs to have a controlling interest in what capitalists should and should not be able to do. Right now, immensely powerful capitalists are choking the beneficial elements of capitalism. But the notion that there’s a free market out there in never neverland and that capitalists will participate by staying “in bounds” is b.s. Ayn Rand’s hero-characters are two-dimensional cartoons that children would recognize as phony.

We have an increasing degree of corruption of the system. Ancient civilizations, China and India, are saturated with corruption. Can we prevent it? Not if we condemn Government as the cause. That’s just propaganda from the oligarchs.

Back in the day, Teddy Roosevelt who recognized and fought the corruption of “trusts” would have been labeled a “communist” by the oligarchs of today. They are now trying to paint any efforts to control excesses of corporations as “socialist” and characterizing those efforts as the biggest threats to our way of life.

It’s a matter of degree and the need for balance. Not condemnation of government although the capitalists have twisted regulations in their effort to garner power and greater and greater wealth and effectively control regulatory agencies.

How – excellent description of our redux of the Gilded Age and pickup of the 7-10 ‘capitalism/socialism’ split. Kudos.

(…for those unfamiliar with that period of world/U.S. history, again highly recommend Tuchman’s ‘The Proud Tower’…).

may we all find a better day.

Thank you for this discussion. I’m an independent, so I don’t like either party, but it always seems like the comment board here is mostly for Libertarians and small government types.

I hate that our country has been captured by wealthy donors infiltrating both parties AND the media. People who berate the “liberal media” don’t seem to appreciate that it’s by and large owned by the wealthy who don’t want their boats rocked any more than the wealthy on the Republican side. Most mainstream media is very neoliberal (i.e in favor of the corporate state).

Think back, when was the last time the mainstream media investigated issues that affected the middle and working classes in a way that called out greed, unfairness, and crony capitalism? Or reported on political malfeasance for what it is, rather than turning it into a both sideism circus that doesn’t expressly call out blatant and obvious crimes?

Zero interest rate policy consequences going to live a long time.

For every action, there is an equal and opposite reaction.

RE brokers made a killing….now the pipeline is empty…for the same reason they made the killing.

The Fed BROKE the RE market….

and next is the stock market….

for bottom 95%

top 5% moving like always

flipper put property out and had multiple full price offers within 24 hours

I say the FED gives, not takes. I “was” a newly retired cash buyer for a $500,000 home, but decided instead to rent a townhome apartment, paid by the 5%, 7 year CD I took out at a local credit union. Thank you Mr Powell.

Kudos!

I am from India. Here, we only have floating rate mortgages and not fixed rate mortgages unlike US. ALM problem solved for banks. From the sense I drive from US economy, it might fizzle out with huge banks going bust due to these ALM problems (banks earnings 3% from fixed rate mortgage while cost of liability is 5-6%)

“And we know who they are: the homeowners in 3%-mortgage jail that now cannot buy, and therefore cannot sell.”

The first thought I had after reading this was the quote, “I cried because I had no shoes until I met a man who had no feet.”

It’s all relative…

You could always turn it into a rental. Here in Phoenix, rents are quite high and you can easily pay the mortgage and maintenance with money left over for profit.

I mean you could sell and buy at a much another home higher rate, but you would really have to have the need to upgrade the home to take that size of a financial hit.

The only people around me I see selling are those who have inherited a property and don’t want the hassle of property management.

It gets sold fairly quickly at a starter home price. The buyers remodel and are happy. Or an investor buys and rehabs to flip or rent it out.

Phx Metro, working class area. Although there are $1M within a half mile down the street. Very walkable are when it isn’t a thousand degrees outside.

Walkable area

The problem with this is that a lot of people live paycheck to paycheck, so if they lose their jobs, they won’t be able to pay the rent for more than a month or so.

I do think though that what everyone says is true, that there won’t be any real changes in the economy until job losses start.

Oh yeah! Grandma’s memory and her stuff all turn to Cash!

Pretty sad people do not remember and cherish longer these days. It’s all so transactional.

Just sold Grannie’s home in N Scottsdale – just as you stated. List 1.85M (wishful), sale at 1.525M (19 year old home with almost no improvements.)

Rents are coming down big time, especially in the west valley. New apartments and build to rents came online at the same time. Many are offering two months free concessions. It’s starting to turn.

Yep I’m seeing that in NC which is ‘booming’ (it is kind of, very strange times we live in).

“I cry because I only have $10 million , and Jay Powell and his friends all have $100 million” .

It’s all relative.

Mortgage Jailed!

Brilliant.

Better get a trademark on that.

Sorry, but it’s either dumb or one sided, actually.

I call it mortgage HEAVEN. I would love to be locked into a huge 30 year mortgage at 3% !!!!! And hell no, I would never sell that property either. It’s probably the lowest mortgage rae anyone will see again for 50+ years.

If that’s jail, please lock me up.

Maybe not dumb or one sided, maybe sarcasm or juxtaposition.

Nah, “3%-mortgage jail” is an apt metaphor for the situation. Wolf also calls it a “gift from God,” but it has a downside in that it can distort decisions going forward such as whether to purchase a bigger house or move to another area for better job prospects. It’s simultaneously a gift from God and locks the homeowner into a narrower set of options, at least in terms of mortgage costs, if their circumstances change.

“golden handcuffs”.

Kind of like a grandfathered property tax basis. Moving means a big jump in costs from losing a big windfall.

We’d all be better off in the past 14 years if mortgage rates had stayed at 5% and Fed Funds had stayed at 2%.

Flat lined at those rates.

The Fed first used the 2008 financial debacle, then the COVID to wield their mighty powers to fluff the pillows of their pals, IMO.

Another blog that I follow referred to old timer Prop 13 homes as a “Golden Sarcophagus” since Prop 13 forced people to stay in their homes to maintain their ultra-low property tax rate. That has changed in CA the last few years with changes to allow homeowners to move and transfer their low tax rate to a new house as long as they stay in CA.

Now the mortgage rate disparity is causing the same effect. Older homeowners cannot move from their 3% gift for god homes without paying a higher mortgage payments.

They are trapped in their Golden Sarcophagi.

Another golden handcuff in CA for older folks is the $500k cap gains exception. Many homes have appreciated more than that since the 80’s & 90’s, so the incentive is to stay put rather than face a giant tax bill by selling.

You’ll be locked in to underwater mortgage for 27 years. If you love it so much, why don”t you marry it.

Definitely situation dependent. The person who wants to downsize and move away from a certain area or closer to family or move for a better job, will feel like they are in jail.

Some people will just be slightly relieved but probably not since people not trying to move or sell/buy their home do not look at interest rates or care how high they are.

Until a real recession comes along and lots of people start losing their jobs.

What if the home value is also the highest we’ll see for 50 years?

I totally agree with you that a 3% locked in mortgage rate must be heaven to those lucky to have achieved that. Hats off! Especially, if they managed a five years lock in or even longer! To call it Mortgage Jail only sounds like envy to me 🤔

Ingrid L. Larssen,

You people don’t read anything, do you? Not even the subtitle? But then feel compelled to comment on the article without having read it? It says “gift from God” in the subtitle and in the text. Those are the two aspects: “gift from God” and “mortgage jail.”

The mortgages at 3% and less cost someone 440- 460 billion dollars. That is what I read in a fed report.

So if we add that to the losses the mortgage and real estate industries are experiencing, it’s epic amounts of decline. It’s grinding industry and the economy to a halt. You literally can hear the gears screeching.

On a side note, there were some who refinanced to shorten their mortgage terms. They used the lower rate (3% of less) to move into a shorter period of payback. These people get their pot of gold after 5,10,15 and 20 years when they no longer have to pay a mortgage. Luckily they won’t spend it all till then.

+1 ! x10 !

To many homeowners this 3% jail might not be that bad. Less mobility, but other places a lot of people newer mine from their home town. To the banks it is not that bad if the end result is only slowly changing prices. Their collateral then hold the value and the money they have lent into existence is backed. For the same reason the FED is ok with the situation.

If no other crisis tople everything there wil be a «soft landing».😉

Kinda😄

big if. corporate bankruptcies are rising. once the stock market tumbles to fresh lows, and long term rates move higher, the whole thing falls apart.

I think you are closer than anyone else but I see it going down when rates are moved towards 0 again not higher which will produce too many screams and complaints.

20% of companies are zombie cos and many others borrowed at 1% rates to keep their stock prices up but when we see recession with much higher unemployment, more evictions, more foreclosures (while the dollar goes down with lower interest rates) and a deep discount of 80% in the stock market, homeowners will see their values go down slowly at first and then with a whoosh. This is a process and as we head toward a depression that will last at least 5 years with no growth, there will be a stampede out where they will not even consider their 3 % a gift. These downturns usually take about 5-6 years and I think this will be a douzy!

good comment chris, and after 50+ years working in construction and especially rehab of real estate, I AGREE on every one of your points…

thanks, and please continue to help us on Wolf’s Wonder on here

It falls apart from a geo political event, IMO.

Until then, APPLE, Microsoft, Tesla holders frolic.

When interest rates rises and property prices tumble, here in the UK we sing; “And down will come Baby, Rishi and All lol 😂👍🥂

What did Japan do when rates were near 1% for like 20 years? That’ll give you the answers you’re looking for and how to invest wisely to take advantage of the current situation 😉!

If you’re in the 25-45 year old range the biggest issue is going to be a lack of mobility if/when your job situation changes. Being stuck in a house you can’t or won’t sell can be a burden. It’s hard to work around when most people only see a promotion or pay raise when they move, and if you become unemployed it gets worse.

…and we wonder at a seeming lack of ‘stability’…

may we all find a better day.

3% mortgage = Debtor/speculator’s “Gift from God” = 0% “Satan’s Anus” for savers.

For essentially 20 years.

All effectuated by money printing/currency dilution (inflation).

Nice observation! I was skeptical of the 50% higher payment until I ran the numbers. For a 30y fixed $1m loan at 3.25% (pretty easy to get at the bottom), the P+I payment is $4352; at 7.25% (the current prevailing rate according to bankrate), the P+I payment is $6822, or 57% higher (!) Looks like 30 year rates first hit ~7% around October 2022

It’s much higher than 50 percent…buying the same house from 2021 to now costs 75 to 100 percent more between higher rates, higher prices, higher taxes, higher maintenance, etc.

How tight are people on their payments, in various parts of the country? How many people own, but tax plus insurance increases could force them to sell, even if they remain employed? Did a bunch of people do a cash out refi to get their 3 % mortgage and turn equity into Sprinter vans, so they may be underwater on the house now?

I am noticed way more listings in Cook Cty, IL-more than ever the last 3 years. It’s the 3 year tax reassessment in 2023. Taxes have gone up and looks like some are dumping their properties. My realtor said many homeowners were hit with a 20-30% tax increase this year. 9k to 11k in one year. Ouch. Higher house price, higher interest rate and bigger tax payment. Renting cheaper now

Lisa what I see coming is property taxes and insurance are becoming unsustainable. People will just squat in houses . Happened in Spain last time ,blackrock got devestaed

@Flea… “Happened in Spain last time ,blackrock got devestaed”

Where do you get this b.s. garbage???

Gattopardo,

I think I figured out where Flea got it: from the combo of YouTube BS garbage and his own imagination and confusion.

This is a problem for those on fixed incomes. It’s why you see retired people selling. If you lived in Seattle (for instance) and saw you property value go up 200% over the past 15 years you also saw your taxes and insurance go up. The mortgage may stay the same, in fact it may be paid off, but the other costs keep going up faster than any cost of living increase those folks are going to see. And when they sell they’re back to being renters or trying to find a cheaper pace to live.

No, Sam, it doesn’t if you’re a seller. You’re hedged on principal. So it’s +50%.

Lisa, they don’t call it Crook County for nothing. Pay the tollway on the way out and don’t look back.

The value of replacement cost on your home as seen by inflation in services like house insurance has been brutal.

I wonder if employee productivity will suffer because many employees are locked in low rate mortgages and can’t move for a better job. Employers will have more difficulty attracting talent, especially in areas with high RE prices.

Already planning on it yup and we are in that boat.

Employers will have to increase pay enough to attract employees since WFH is dead. Basic economics.

And that’s inflationary, which drives up mortgage rates

Moron said WFH is dead 😭😭😭

WFH isn’t dead. It wasn’t dead before the pandemic, and it’s not dead now.

I do agree though, that there are many fewer permanent WFH (as opposed to remote) than there were 2 years ago, and much fewer than people expected.

Or get more tolerant on remote work, as has happened at my workplace. Housing prices are so excruciating here they just can’t attract enough applicants unless they allow them to WFH full time from elsewhere.

Don’t forget training remotely. I’ve seen employers expecting already experienced, (advertised) fully remote-position applicants to train ‘hybrid’ in office for 4-6 months.

Nice trap, but I know the job already and have done it remotely just fine for years before the first bat sneezed, hence you want to interview me. But 4-6 months of ‘training’? Lol. Pound sand.

Lol this mouse knows the maze.

3% mortgage just means they probably overpaid, if a cashout refi, set themselves up to be underwater.

Or if they were smart, they bought when rates were 5% 10 years ago, refinanced into a 3% mortgage, did a cash out, and took the cash and put it in tbills making >5%.

Yes sir the 3 percent Mtg crowd has many players including reverse Mtg at 3 percent on paid for home. I considered such when the rates were below 3 percent for my home and had some quotes just did not like the cost of the Mtg. Right now my equity offered (600k) in a 20 year Mtg would be cash flowing me 1 percent on 600k for 20 years. 500 a month ! That’s a 15 percent raise on my social security . But I did not pull the trigger (hind sight ) some may have

Most reverse mortgages are variable rate loans like the old heloc home equity loans.

My ederly mother in law took one out and was below 3% for many years. She’s almost at 7% now. You’d be underwater like the banks that just went bankrupt, borrowing high and lending low.

….Or took the cash out and bought an $80 K pickup truck!

… a pickup that is made from aluminum foil and a sizeable pebble on the road puts a $10,000 dent in it. Which will HAVE to be fixed or my gosh the male driver will not be right until it is! Lol

What happened to rugged cowboys? A pebble dent would not phase them.

took the cash and put it in tbills making >5%. ….

you describe a tiny fraction of the American mortgage holders who behave economically rationally; however, the vast majority invested its windfall into assets with much greater financial returns – new and used trucks/SUV’s, motor homes, boats, motorcycles, plastic surgery, revenge vacations, and similar.

Plastic surgery wasn’t a good investment idea for Ivana. She was thrown under the bus anyway.

For many, this is spot on. The low rates coincided with the peak in price and the largest number of sales, so for those buying during that time (not simply refi-ing) – its not that they cant or wont sell because they have it so good. They may be forced to sell as those payments are very high, even with a low rate. It really comes down to the economy and it seems the middle class is getting squeezed by inflation.

I still see people desperately trying to buy a home, even when everything points to wait. These are some of the same people who did not want to buy during the lowest mortgage rates of their lives because prices were “too high.” I explained it’s not the price, it’s the monthly payment. You are still up when you do the math. They said “I can’t buy at these prices.” Today, they tell me “F*ck, I should have bought, the same type of home is now for sale at the same price, but with a 6.5% mortgage instead of 2.75%. My life is over….at this rate I’ll be renting forever!”

If you are a buyer, take your time, grab some popcorn. I’ve seen this movie before, and it takes a while before it gets good.

I have first hand experience with young couples buying homes with zero down. They get FHA financing with 3.5% down, then get assistance from local programs to fund the down payment.

We’re talking about couples in their early 20’s.

It’s sheer lunacy, at taxpayer’s expense.

Thankfully, most of this ridiculousness is confined to the lower end of the housing market.

Why is it lunacy? Young people shouldn’t be buying houses?

Arnold,

It’s lunacy because the state should not be encouraging anyone to buy a house during the biggest housing bubble in history. Moreover, people who can’t afford to pay for a house probably can’t afford to maintain their house. Do we really want the country’s housing stock to be in the same condition as our bridges?

And the Pretzel-Logic Award goes to…

That’s not what Bobber said or meant. Sheesh.

The lunacy is the 3.5% down. Horrible debt to equity ratio.

I’d wager that most sellers would rather not sell to a potential buyer coming in with an FHA loan either.

Arnold,

I think he was talking about the subsidies from, and the risks to, taxpayers, who carry all the risks and get hit by all the losses.

it is lunacy because if they cant save up for a decent down payment, then they cant really afford the home and they have no “skin” in the game.

and when the loans are backed by government loans, the risk is transferred to taxpayers.

it isnt that we dont want young people to buy houses. we just dont want bubble prices.

these bubble prices are what bankers and rich people want to prop up their wealth. wealth should be based on creation of value, not on massive price appreciation for one generation to steal from the next generation.

I don’t care if the FHA buyer offered 100K more…. it’s not worth the brain damage to deal with the appraisals, repair requirements (much of which is irrational), and all the delays – only to have the deal blow up.

Why is that lunacy ?

Worked like a Charm in 2007 and quite a while into 2008.

Thankfully, most of this ridiculousness is confined to the lower end of the housing market. …. hopefully, few compassionate and powerful politicians facing the threat of losing the next election will band together and solve this “housing injustice” by extending the program to struggling first time buyers with $700,000 annual household incomes and mortgages up to $1,950,000.

If we forgive student loans to millionaires, donate tax dollars lavishly for TESLA EV purchases, why should not the mortgages of these financially struggling individuals receive a modicum of assistance from the US Government?

With the proper spin, it could be characterized as a “job creation” program, or “deflation” fighting for the real estate sector.

Effing funny. Thank you.

Same thing going on with VA loans. A lot of fake disability cases.

“I still see people desperately trying to buy a home”

If the 20 to 40 generation knew… KNEW that their future was mortgaged to inflate these assets, they would be outraged. The debt creation and money printing sets a dismal future for them….homes and fair entry into stocks inflated…..yet the wheeler dealers have fluffed their own pillow off the theft from the future of these young to middle aged…with the actions of the Fed. Stealing from the future to “fluff” the present.

Oh believe me, we know, and we are outraged.

they would be outraged??

hahaaa.. and do what about it exactly?

the level of ‘outrage’ you cite here is but a FRACTION of the total amount of outrage IN GENERAL which should be (justifiably) felt about things going on in this country.

but i think you forget what country this is.. Americans dont do ‘direct action’ anymore unless PUSHED by an outside narrative. do you really think people were that upset about george floyd? seen any antiwar protests lately? seen any protests AT ALL? naah. didnt think so.

its funny when the french protest for months on end, millions of people, when their pension age gets raised a couple years.. cue that over here. yeah i bet there would be some social media ranting and MAYBE a few phone calls to legislators, but that would be the extent of it.. everyone would be back to ‘doing what they do’ in no time: buying stuff, going to work, watching sports, whatever.. like good little sheep.

i think perhaps you confuse genuine OUTRAGE with passive indignation. thats about all Americans are capable of feeling these days. its disgustingly pathetic really.

And that’s assuming they’re paying any attention at all.

So true 🤣 only the French know how to kick up a good storm and relentlessly continue.

The bottom 90% wastes all its energy on spoon-fed controversies, as part of the larger Rep v Dem fiction. They don’t have the background or desire to think critically. They take what gets handed to them, provided they put in the requisite hours of labor.

It’s the top 10% that has potential to cause systematic change, but they see no reason for change. It’s hard to fight against a system that favors you, and grows your assets 300% every decade.

Well they did watch from the sidelines as homeowners were rewarded by an almost 100% equity gift for no other reason than demand and QE.

Can you blame them? They do not want to miss out when the next “gifts” are given.

Its only a gift if you are going to sell. If you aren’t selling the “equity” is actually a burden because the taxman wants a bigger cut.

I wish my house was “worth” less.

Sufferin, whoever watched from the sidelines should not be complaining in my opinion. They did not want to play the game and therefore do not get to enjoy the rewards. They also do not get to take any of the risks involved while chasing said rewards. Then some of them complain and say “Wahhh, wahhhh, I want a house, it’s not fair….” Give me a break. It’s silly. It’s like those same people who are “savers” and stayed out of the stock market after taking losses in 2008. Same cry babies. They stayed out of the stock market to avoid the “risks” so therefore you don’t participate in the rewards.

To answer your question, yes, it’s their fault. They sat out this long, sit out for a little longer. It’s not going to kill you.

Germany:

I built an appartment during the financial crisis and refinanced in 2019 at 0.94% for 10 years.

When I went to banks to discuss what is possible or not I brought my computer where I programmed a payment plan so I was able to see what a 0.05% difference would mean.

The man in the bank looked at it and said there is hardly anything he can tell me except the raw number and I’m the first person ever he saw programming this (easy) program in excel.

He told me that almost everybody he ever talked to in his career had no clue about math.

Most people in Germany have no skills in math.

(Most likely this is different for people who do this for a living)

Payment calculators have been freely available on the internet; you can just Google it. They also show how much interest is paid over the term of the loan, etc. You could have just walked into the bank with your smartphone, pulled up the website with the payment calculator, and plugged in the numbers. The time to do this with your HP 12c or on an Excel are long gone.

It was a forced gift from savers.

Given by the Fed pretending to be God.

Golden handcuffs. Wish we could give them a taste of the 10-14% mortgages some of us had back in the day. Shouldn’t someone tell them that a 7% mortgage would actually be a good thing because then they’d have enough mortgage interest expense to surpass the standard deduction LOL?

We haven’t had a mortgage on a house since 2001. The LOWEST rate we ever had was 6.9% in the late 1990s

Anyone commenting about how high their interest rate was back in the day should also mention the average price homes. 10 percent on a $100k mortgage isn’t worse than a 7 percent interest rate on a $400k mortgage.

Old mortgages are todays student loans and the futures car payments

You’re forgetting that the salaries at that time were also markedly lower.

A $30,000 income in 1984 is the equivalent of nearly $90K today. The $100K mortgage in 1984 is the equivalent of $293,000 today. My payment at that time was $911 a month….. take that chunk out of $30K and get back to me how “easy” it was with a spouse and two kids.

Yet we still made it work. Ate a lot of beanie weenies, but we survived.

It’s priorities…. if you’re a “lookitme” and need an emotional support truck to prove your manliness, then you need not apply.

Just for comparison to El Katz comment and not to ruffle any feathers, but the median household income for Denver County Colorado (my neck of the woods) , according to the latest census bureau info I could look up is $72,661 (2021). The median price for homes sold on data for May 2023, according to Denver Metro Association of Realtors is $595,000.

Best numbers I could come up with.

Sorry Correction: $78,177.

https://www.census.gov/quickfacts/fact/table/denvercountycolorado/INC110221

1986. Bought new home near Dallas.

89k, 8% mortgage.

Income about 34k. So after taxes maybe cleared 28k.

Small down payment on house but dont recall exact amount.

But 8% on 88k, 30 year loan =>

about 630 monthly payment.

So about 7600 in mortgage payments annually. (I actually foolishly (?) made advance payments but nevermind that).

So my mortgage payments were about 27% of my after tax income. Not bad.

Unfortunately my new 89k home only sold for 82.5k 10 years later.

TX economy took a bad hit: S&L fiasco (Michael Millikan, etc) and oil industry problems. TX is a non recourse state and one of my neighbors walked away from their home around ? 1989. Maybe they had to, I didn’t know them (not adjacent neighbor).

One of the 3 builders in our subdivision went bankrupt (1986) and so we had a few lots that 10 years later were still empty. I’m sure by now they have a home sitting in them.

Neighbor sold his home for 77k (per new neighbor)… 3 years after purchase.

Sold for 101k new in 1986.

My home bottomed out at around 67k in the 89-90 timeframe per appraisal.

Rates from 12 to 18 percent in 1980-1983 and I bought 2 homes during that period. My 60k home had 1000 usd payment

Lin, “Back in the day” men could work with one income and women could stay home and take care of their children without the need to pay for childcare, and the price tag of a house was within reason.

This scenario should definitely benefit the multifamily market.

Absolutely lots of home owners and buyers have disappeared until something gives. Another area of two are reverse mtgs low rates locked in at higher equity prices and like for my case my 600k locked in Texas property tax rate of 10k is now 20k and downsizing if I could find a buyer would cost me the same in property tax for half the house roughly speaking though I would get some equity and reduced cost of living. Several variables to account for the evaporation of sellers and buyers

A family member on Long Island recently sold his house and downsized to a nearby townhouse of same square footage. Price was lower, lower too the taxes and insurance. I never thought he would sell his house, but it didn’t make sense to keep it anymore at his age and current costs. For now this was the best way to control his expenses and recoup equity.

How might employment at realtors, mortgage providers and mortgage brokers unfold if mortgage jailed phenomenon is indeed a “new normal?”

Seems right-sizing might be a logical step for these house-sale dependent industries.

If the entire turnover of the housing market has shrunk by 25% then the real estate, and mortgage industries will have to shrink by 25%. Every 4th Realtor@ will have to be taking those “become a bus driver” banners on the back of the school buses seriously.

It would be poetic justice if those banners are changed to, “There’s never been a better time to drive!”

Love it!

Or they just make less money.

Actually, in times like these, good professional brokers can put deals together and do just fine. But a bunch of the easy-money brokers might drop out.

Agreed. This is the best thing to happen to good realtors – the top 10% who do 90% of the business.

Weeding out hundreds of thousands of incompetent or part time or 5 deal a year realtors is good for good realtors and for buyers and sellers too. Theyre left with the best to work with.

Bus drivers here in Bend start at $25/hr. That’s pretty good money if it’s 2019!

My friend, the “successful mortgage broker” who was lighting his big cigars with $100 dollar bills during the pandemic is now unemployed and had to give up his Texans seasons tickets, among other things.

Sounds like you’re happy about it.

No, I am just stating what happened to my friend the broker once the ReFi’s dried up. He was one of many around here. Entire mortgage broker’s offices went bust. His wife works for Exxon here so they are OK, for now.

This is not Real Estate LaLa Land like on the coasts.

No one wants the Texan’s season tickets anyway. He practically gave them away.

I’d be overjoyed. Schadenfreude is real.

It’s no different than feeling overjoyed when the bad guys are destroyed by their own hubris.

…there’s a reason excess is oft-termed ‘wretched’…

may we all find a better day.

I do mortgages for a credit union and it is most definitely like a neutron bomb hit my borrower pipeline. I have friends in the business who have been doing it for a long time and are good loan officers who are considering getting out. I’ve never seen a market like this one.

Many Mortgage lenders and Realtors better start looking for a new career effective immediately. I saw this happening after the Pandemic ended. They can join the hundreds of thousands of small business owners who went out of business and are now unemployed or had to change careers.

They will just go on vacation for 5 years until the next bubble starts building.

Then they can dust of their rolley chairs, upgrade their laptop, get a spiffy new doo and get on one of the many twitters to advertise!

They’re not alone. Used truck sales are the worst in 20 yrs since I’ve been a dealer this year. I have never seen it like this and expect it to get much worse. I figure the pandemic brought forward years and years of sales now we sit into a crash for how many years for the next cycle?

Assuming we’re taking about “pickup trucks”, not real trucks. Pandemic brought forward years of sales and also amplified idiotic buying trends among a society that is rife with poor consumers. So when you think your truck with 7 years on it, 150,000 miles and rust showing in places is worth $40,000, as a rational buyer, I say no thanks, especially when that was a sub $20k purchase in 2019. Not to mention that the average and largest group of truck buyers are extremely vain, inflation and offerings in this segment is abysmal, especially if you’re like me and it’s a 100% business vehicle.

My tax lady always raises a red flag when I file because the truck always gets 100% business miles. She says that’s a red flag because “no one” uses their pickups only for business. Well, I do. It’s a regular cab (if those exist anymore) and if it’s not pushing, pulling or hauling something it sits in my yard with somewhere less than 3,000 miles in the typical year. Guess I was raised that these are tools for real men (and women, if they’re laborers, as few as they are) and if you need leather seats and infotainment and a cushy ride, then you’re soft!

Amen to Digger Dave.

Digger Dave I have had the 2 seat pickup for 4 decades never for business but great for hauling stuff. Yard work tools etc not a necessity but convenient

I remember when the Dodge Tradesman and Ford Econoline vans were what working tradesmen men drove, not some auto show pickup.

My local credit union manager said they went a whole month without making a single mortgage loan.

There are still loans to be had out there, but it is most definitely a more challenging market for mortgage professionals.

If significant downsizing occurs due to depressed home sales, how big an increase in unemployment will likely be, I wonder?

Wonder what unfolded in that respect during GFC?

Some have 2.5% or even 2.3% 30Y fixed mortgage.

And it is gift from US government.

I’m at 2.25% for 30 years. Everything in this article echoes loudly in my ears.

I wonder how many of those three percenters will be forced to sell due to job losses, job changes, divorces, growing families, death and other such unpleasant events. A minuscule fraction? A more significant one?

A minuscule fraction will be forced sellers within the next 5 years in my humble opinion. Even foreclosures takes a few years

How many would normally sell, in a flat market? How many are going to just really want to sell, for the newness or a greener grass, and only stay because it is logical? Logically it could be a gift, while emotionally it could be a mortgage jail, as it was aptly put.

mol – indeed, there are always two ways to look through the telescope…

may we all find a better day.

I’d be surprised if the government doesn’t stop foreclosures from happening somehow this time around. Seems to be their style these days.

I have a feeling divorces are going to or have been spiking post pandemic. Just a thought…

Higher inventory of houses *and* singles can’t be a totally bad thing given both markets are dry as charity.

Open a gym! Seperated people need to look good for the dating scene. Lol, ok that’s kind of sad actually.

Do folks really not have emergency cash on-hand? Not trying sound condescending, but I’m genuinely curious because I keep seeing these “just wait until the job losses” comments.

Losing my home is one of my biggest fears personally. I keep enough cash and liquid assets (T-bills) on hand to cover the next ~year of my mortgage & other bills, even if all my sources of income dried up tomorrow.

Sounds like you’ve contracted a rare dose of common sense.

But don’t worry, there’s a drug to cure it. Ask your doctor about Dumshitol.

Judging by the way the world’s acting, they must be handing out free samples.

During the pandemic, massively, people who would not have been able to buy a home under normal conditions took out loans on the edge of their possibilities.

In my opinion, they are more than those who buy and have money set aside.

I’m the same way, but just from my small circle of mostly middle-class friends and family, we are the rare ones. Most are leveraged to the hilt and if a crisis happens they borrow to stay a-float. Sometimes that works, and sometimes it doesn’t.

You’d get a job and you’d pay that mortgage, even if you had to move your a** to Kentucky and live out of hotels to pay it.

Layoffs. Look at all the strikers not getting that paycheck. Same result. An already crashed economy with so many disguises. I wonder how many get back to work. So so many disguises. For a tad more only.

They want to be respected for their work, they want to be compensated correctly.

They are tired of corporations claiming poverty, when they are rich!

It’s their right to strike and more power to them.

On a side note Netflix needs to die. Their stuff is pretty horrible nowadays. Just an opinion!

This is a salient point that has been made for future forced inventory. Maybe not the job changes —that would have to make up for things. Not growing family; just do an addition. And job losses seem not systemic in this labor market. Divorces will force a sale because the other would have to buy the other out. Most don’t have that cash. Death would force the sale if both were needed to cover the note. Disability might be another reason for forced selling, though… between govt and insurance, maybe not. Quick google says 700k divorces per year. This assumes title in both names. Fuzzy. Death would force a lot less selling because it would have to be younger borrowers still owing on the note that they other couldn’t cover alone. Average age statistics. The boomers mostly own their shyt so them dying isn’t impacting that. Interesting thought experiment though. But this forced selling would be the same as it has been for years and probably not noticeable from a trend/RE perspective. This stuff has been a part of the economy for years.

Realistically, we are one hell of a long way away from “forced selling”.

Welcome to the unintended consequences of mishandling market forces,

Over time a divorce, illness, accident, death and the vicissitudes of employment will force the hand.

Then the real horror of what easy money does cost, will hit home hard.

It looks like this spinning toy top has the wobbles anyway

Sheesh. Being a bit dramatic aren’t we?

It is certainly a confusing time in the debt based economy. What is smart money doing? Berkshire $130 B cash, debt mostly long term at $123 B. Its been the trend for Buffet for a good while to have cash greater than debt. Got to be ready if Fed can’t soft land the plane.

And the long term 123m debt is at low cost

Most probably they hold cash as T-Bills.

And it is 4%+ interest.

Warren Buffet bought big into technology – Apple, and oil & gas – Occidental Petroleum and Chevron

Brk-b shares are probably 30% inflated

30% inflated? Huh?

I wonder if you realize that for the past 30 years Berkshire has faced terrible headwinds because during that time money was cheap. Insurance is a terrible business when any idiot can set up a Cayman Islands insurer financed by cheap money. For 30 plus years it has been hard for Buffett to find truly cheap companies to buy because cheap money inflated asset prices.

If money ever gets even mildly tight, Buffett and Berkshire will be kids in a candy store.

ready for what?

warren buffet is 92 years old.

one would think, at that age (or earlier really) the guy would like.. i dont know, ENJOY all the money he’s made over the past several decades? maybe transition his company into some younger hands? or do SOMETHING instead of just make even MORE money he cant take with him?

he’s a great investor, nobody can take that away…

but there is a pathology here which is alarming, if you really think about it.

i am nowhere near my 90s and nowhere near being a billionaire, so maybe i have a different perspective.. but not may people make it to their 90s, and only a handful will see the triple digits.

i guess what i mean to say is.. once you are that old (and that rich), what is the point of making any more money or worrying about investing or any of that stuff? you’re at the end.. the only thing to get ready for is the final departure.

Maybe he just enjoys the game?

Maybe he’d rather wear out than rust out.

My sentiments exactly. Its a big game to him. No different then all the retirees at the casino.

…indeed, the joys experienced by the human creature are myriad, and oft-inscrutable one human to another…

may we all find a better day.

All his personal money is going to charity. He doesn’t believe in leaving huge windfalls for family members.

Berkshire Hathaway shareholders hope this is true so his estate won’t have to sell his half of his shares all at once to pay death taxes…

He’s doing what he most enjoys, and applying the wisdom of his years, money is only a byproduct, sounds like freedom to me. He always seems impishly happy.

He has enjoyed it. He’s like an excited school boy whenever he talks about making money. He’s still out there winning.

Who can say that at 92? Most are feeling the sides of a lazy boy looking at cheers reruns and waiting for dinner.

If his babymama has to work he’s a zero. Just saying.

Anyone who even knows the slightest about Buffett knows he absolutely enjoys allocating capital. There is nothing on this earth he would rather be doing. He is literally doing something that he enjoys the most. Why would he quit to do something he enjoys doing less?

As for it being a pathology, please know that he has given away more money than anyone currently alive and at least 5% more is being given away each year. Plus 99%+ of the remaining amount will go to charities upon his death.

I haven’t done the math in a long time, but I would bet that if the amount of money that Buffett has given away were instead kept in a trust invested in Berkshire, that trust would probably be among the top 30 – 50 among wealthy individuals on the planet.

But Wolf – this doesn’t address the shadow inventory that you have so eloquently described in the past.

With YOY prices declining, investors should be dumping real estate – why hasn’t this started to break?

Is it simply the belief on “this too shall pass”?

Why would they dump RE if they are cash flow positive on rents.

One topic at a time.

Me thinks you have a beautiful new article on the way. :) As always, great reporting wolf!

Who would an investor sell to? If the home is to stay as a rental, then the sale would be to another investor and there would be no net reduction in investor ownership. Would the investor not renew the lease in order to allow the house to be sold to an owner-occupier? Would this get a better price than selling an already leased home to another investor? Would an investor sell to a current tenant? Or perhaps wait until the tenant decided not to renew?

I am curious as to how disinvestment in housing works in the real world.

It’s starting just that manipulated media = owned by rich isn’t reporting it .

This is a gift to builders. Prices are staying at bubble levels. Commodity prices back to pre pandemic levels. So builders will be happy to build new homes with good margin. Eventually will result in over supply.

Prices of new houses = green line. Builders have been cutting prices and building at lower price points, and they’re buying down mortgage rates to get volume. And now the median price of new houses is the same as the median price of used (existing) houses. (I mean look, folks, the price of “existing cars” is something we watch carefully).

So churn in the used market is minimal. New supply from builders controls the market price right now. If builders can drop home prices to 2019 levels, how many homeowners become underwater? How much of a unemployment rate increase would equal twice that same number of underwater homeowners? … Assumes that half the newly unemployed would own an underwater house.

Fish gotta swim, birds gotta fly, builders gotta build.

They can keep driving the price down and compete with existing homeowners until the point it doesn’t make sense for them economically.

Cause you know – *housing shortage*

Thanks Wolf.

What I meant is because existing home sales volume is low, that sets good floor for new home sales right now. If median price of existing homes falls then new homes also need to fall, which is not case right now and advantage builders.

Let’s make some ballpark calculations:

Let’s assume that there are only two classes of interest rates: above 5.5 percent and below 5.5 percent. So, 11,207,000 homes are at or above 5.5 percent, and 48,407,000 homes are below 5.5 percent.

Let’s further assume that all of the 48,407,000 homes did no-cash-out refinance at 2.75 percent.

Now, assuming that the average price of the house before the virus was $300,000(median price pre virus), and everyone who is below 5.5 percent has bought the house at $300,000 at 5.5 percent before the virus and then immediately refinanced at 2.75 percent, this would give us the maximum theoretical amount saved by every one of those households in interest payments.

The 30-year payment for a $300,000 house at 5 percent is $579,000, excluding property tax. Whereas, the 30-year payment for a $300,000 house at 2.75 percent is $440,000, excluding property tax.

We know that not everyone got the house at exact moment before virus but $139,000 is the maximum difference between above two payment plans for any average household.

Let’s assume that by forgiving $139,000 per household, the fed has created a deficit of $6,728,573,000,000.00.

Now, it’s safe to assume that property tax, insurance, etc., on the average house, went up by $3000. So, for the 48,407,000 homes below 5.5 percent, the total increase over 30 years amounts to $4,356,630,000,000.00.

48,407,000 x 3000 x 30 years = $ 4,356,630,000,000.00

Additionally, for the 11,207,000 homes above 5.5 percent, the total increase in property tax, insurance, etc., over 30 years also amounts to $1,008,630,000,000.00.

11,207,000 x 3000 x 30 years = $ 1,008,630,000,000.00

In summary, the $6,728,573,000,000.00 deficit will be turned into a surplus by $3,294,858,000,000.00 payment from the above 5.5 percent group and $4,356,630,000,000.00 from the below 5.5 percent group. This would create a surplus of about $900 Billion.

This is assuming the perfect world. However, like any murder mystery we don’t know all the details about the crime scene but we know that federal reserve will not get away with murder.

These are some broad assumptions. Feel free to poke holes.

And now you’ve found the true source of inflation and the continued spending. All the sudden people refinanced their 4 or 5% mortgages to 2 or 3% unlocking additional monthly cashflow. This isn’t going away and these people are not moving. This extra cashflow needs to be eaten by other expenses before inflation will return to normal. I think we’re just starting to get their with the extra amount groceries and utilities cost.

Property tax and insurance increases = poof it’s gone

Dont most towns adjust the mil rate once theres mass appreciation? Round here they do. Property taxes largely stay the same

You don’t live in Illinois, that’s for sure!

(Neither do I, thankfully, but I know from family)

Not in East Texas prop taxes have increased 50 percent in 2 years but their homes have been flat lined priced for a decade

Nor Texas.

“And that may be the new normal for years to come. ” YES SIR Mr Wolf. I also believe a lot of crazy new normals is aheadin our way. Lots and lots of them….. Higher for Longer should be real interesting……..Bring it FED……

Some creative genius will come up with homeowners able to retain their mortgage, but move the security from present home to another home. Fees would be added, maybe even a little boost in interest, and the new house would have to offer the lender more security than he had with the initial mortgage. But it would end with a homeowner able to change homes without losing so much. And it would cause a big boost in sales compared to the way things are now.

A similar scenario: In California, you can under Prop 13 in its present configuration, if you are over 55, you can sell you home and buy another (smaller home) in the state, and keep your tax basis.

Howdy Folks. My 2 sons purchased starter homes ( less of a home than one can afford ) needed work, refinanced at the low rates. HELOC s allow other real estate investments….. NOT Mortgage jail but heaven for some……

Free money from pops (you) always helps with those starter homes. Hope they appreciate you. Most are a long ways away from that heaven.

Son and DIL bought their starter home all by themselves. No FNBOD (First National Bank of Dad) involved.

Howdy Dick. Most of my sons friends and inlaws told them NOT to do what they did. Too much work, and should purchase something else. Am sure the friends and inlaws still feel the same way. But , my sons know they did it their way and are very happy. Financially secure with a large amount of Real Estate Equity because of the extra labor intensive work… Real men and very proud of them…….. Once they left my home, they were one their own……..Thanks for letting me type about my sons…….

C’mon….

The overblown pseudo-libertarian myth of the rugged individual is a cliche which begs for retirement. Not even Teddy Roosevelt was as much the self-made maverick as what some on here allege their children to be.

I’m certain you helped your kids in various material ways that helped accelerate their pursuit of happiness, even if it wasn’t in the form of a Halliburton attaché case chock full of C notes.

…have always wondered at the sketchy balance of the three-legged stool of ‘generational wealth’, ‘inheritance taxes’ , and ‘Murican chest-thumping belief in the ‘rugged individualist’…

may we all find a better day.

@Miatadon,

“A similar scenario: In California, you can under Prop 13 in its present configuration, if you are over 55, you can sell you home and buy another (smaller home) in the state, and keep your tax basis.”

What does this mean exactly?

You buy another house at the same price or lower and you keep your tax basis. Eg if you bought your house for $100,000 in 1979, you can sell it for $2,000,000, buy another house for $2,000,000 and your taxes stay the same and do not increase.

Instead of paying $16,000 a year in taxes, you continue to only pay $900.

This is limited to only certain counties though.

No, carrying your property tax basis is now statewide in CA if you’re 55 or older. I want to downsize and take advantage of this but can’t find anything to buy. I don’t care about interest rates, just can’t find a smaller house in the area I want, so I sit here in a giant house with kids gone and lots of empty rooms waiting and waiting for something to come to market that I like.

CA property tax resets when ownership changes and is based on purchase price. Prop 13 simply limits the percentage that property taxes can go up each year thereafter. Props 60 and 90 allow an over 55 to, if they are in the right counties, sell their home, buy a cheaper one, and keep their old, lower tax basis. These props have saved me a pile of money over the years, and I am grateful for them.

Thanks, I was completely unaware of this.

But those props also help necessitate California’s income tax, and they heavily favor certain groups for dumb reasons.

“I got mine,” I guess, right?

Or the mortgage follow the house. As long as there is a large mortgage on the house, it is the bank that own the house anyway. Just a different kind of leasing/renting.

I understand this article from Wolf totally. I usually have a hard time with the complicated (to me anyway) articles. Thanks.

The reduced supply and reduced demand happening in tandem makes sense.

But two questions eat at me.

1) if supply isn’t a problem, why haven’t home prices meaningfully dropped in the last year given much higher interest rates. I mean it’s nearly sideways in most areas YoY.

2) if supply IS the problem, why is supply low? It makes sense in Canada with how high immigration currently rests (and their values have still dropped more significantly YoY), but in the US I’m just baffled. Investors holding multiple properties?

Or is this just a long lag effect?

Respect and thanks to any who reply.

Imprisoned at 3%. I hope their neighborhood does not decline, their neighbors stay reasonably sane, the school district does not go to hell, they don’t need to relocate because of jobs, they don’t get barking dog(s) for neighbors, property taxes don’t go through the roof. Other than that, they should be okay.

I moved into this rental in 2019. Opened my bedroom window the first night to let in the cool high desert air. In came my neighbor’s cigarette and bong smoke.

I haven’t slept with my window open in 4 years.

Don’t underestimate the power of society. A married man with a 3% mortgage is still a slave to many masters.

🤣❤

For the peanut gallery: the key word in that sentence was: *married*

*married* men live longer. You’re welcome.

“Freedom is just another word for nothing left to lose” Joplin

Imp – actually Kristofferson (credit where it’s due, etc.)…

may we all find a better day.

Fed might bring back 3% loans during next down turn. For any problem Fed solution is ZIRP+QE. Oddly the solution for this problem is to have recession so that Fed can do its work.

If your belief were remotely true, interest rates never would have peaked at 1981 levels.

The FRB or other central banks don’t have any new tools and there are no wizards behind the curtain either.

My local newspaper published this online @ 2:13 PM CDT today.

“Afraid of high interest rates, Twin Cities area homeowners stay put — creating a bottleneck. New home listings are plunging as higher mortgage payments scare off move-up buyers, who don’t want to pay twice the interest of their current rate.”

Maybe it’s not a bad thing to slow down housing turnover rates?

Here’s a good quote at the end of the article in my newspaper:

“While I worry that our dream home may become more and more expensive the more we wait, this payment comparison just makes me realize that our current situation is just so easy and comfortable,” he said. “Who doesn’t like easy and comfortable?”

“Maybe it’s not a bad thing to slow down housing turnover rates?”

Possibly. In lots of countries, turnover is much lower. I don’t have stats, but it’s pretty obvious that in Italy you don’t really move much. Even renting, the norm is a very long stay.

There’s at least one significant benefit to low turnover. Less money burned in transaction costs (realtors, lawyers, escrow, appraisal, mortgage banking fees). None of those are value-add, only de facto taxes, dead weight losses for society.

Wolf, another great entertaining article.

I love your “3% Gift From god” vs “3% mortgage jail/golden handcuffs” analogy comparison.

It is a classic “Glass Half Full” vs “Glass Half Empty” that forces decisions that are not comfortable but either is a good position to be in.

For example, You purchased in 2000 with an 8.6% mortgage but refi’d without cash-out every time the rates dropped 2%. You now have 7 years left on the mortgage(you refi’d a few times for 30 years and finally refi’d at 2.1% for 10 years at the low in 2020).

Is the glass half full?

1) You can live comfortably for the rest of your life at an affordable payment (barring taxes and insurance). Do you love your house and the area?

2) Have you planned to move in the short term anyway? Why not sell now and buy a smaller house and use your equity to buy down the mortgage?

Is satan luring you from god’s gift making you think the glass is half empty?

1) Will house prices crash tomorrow?? Gasp!

2) Have you been tempted by a RE agent (satan? :-) ) to sell now and pull out 1M in equity making you a REAL millionaire overnight?

3) Have people been shaking their heads and looking down upon thou because your 1.5M house is smaller than thars? Nevermind they can’t walk to the beach and it is currently 120F in Phoenix.

Temptation is the root of all evil. Don’t let satan lure you from god’s gift and make you think you are trapped

All humor aside, these decisions are hard. You are never trapped but the decisions often come down to money vs quality of life. I try not to let peer pressure drive my decisions (except for my ultimate peer spouse).

Retirement is another one of those hard decisions.

1) Do you collect SS/pension at 62 or keep working for the golden payoff later?

2) Do you leave before all of your RSU stock has vested even though you are working 80 hour weeks and sleeping on a cot in your office? Satan already has you working in heck.

So many hard decisions.

The glass is half full

The glass is half empty

The glass is at half capacity

The glass is always full, half by water

Half by water vapor, nitrogen, and oxygen

But water, nitrogen, oxygen and the glass itself

Are all made of atoms, which are mostly empty space

So the glass is almost empty

And the glass itself, barely exists

lol. So how then should I think of myself? I am either a half brain, an airhead or a jarhead!

A bong.

mol – to reprise the punchline from the old engineering joke: ‘…the glass is the wrong size…’.

may we all find a better day.

Defining something and then measuring it always did seem sorta “circular” to me….I see the joke possibilities.

I also wish the Ancient Greeks had REALLY become totally fascinated with static electricity and magnetism. They could play with/see/feel both happening very easily….but…….nothing.

Newton’s model (I read he was a big bully, btw….but I have a newer, stronger, and also more unpleasant worldview about bullies since 45 got in) and trial and error will do nicely as a shared worldview for as long as we are likely to be around, if nothing really BIG changes. Maybe this nasty heat/storm thing will open closed eyes?

NBay – 102’F here at 1500ft and 1230hrs five crow-flown miles from the blue Pacific…best.

may we all find a better day.

…re: the Greeks-kinda like archaeological finds of wheeled kids toys in digs of societies that didn’t appear to employ those round things on anything larger…

may we all find a better day.

Scientifically, the glass is at 50% capacity.

The GLASS is twice as big as necessary

I made my decision in 2001 when a 38-year-old -colleague of mine dropped dead while we were chewing the fat on the options exchange. I closed up shop and moved to the southwest of France.

CBOE?

Do you know The Chief on Stocks & Jocks in Chicago? He’s still going strong at 70, hanging out at neighborhood gin mills and suburban supper clubs.

When I started working, 6 of my 50+ engineering mentors and co-workers had heart attacks within the next 5 years. Fortunately, only 2 died.

I was only a stupid 22 at the time and believed it couldn’t happen to me. Now I am pushing 60. I remember.

Family history plays a big part in longevity. However, work stress likely subtracts from that significantly. How many take-out Chinese and cheeseburgers can I eat while working 80 hour weeks and make it to 60? Should I wait for the first major heart attack to retire like many of my peers? Decisions….. Money vs Quality of Life.

I read a story that back in the 1940’s workers at a WW2 munitions factory had achieved the golden age for retirement. Within a year of retiring, they all died. That led to the scientific discovery of nitroglycerin to save people from heart attacks. Their work had kept them alive. Just a side note. I don’t think cheeseburgers will keep me alive.

1. Breakeven when taking SS at 62 is age 84. See how old your parents and grandparents lived.

2. Try to work until vested, no matter what. Then quit.

WL – …hopefully with management that doesn’t terminate the pension plan sixty days ahead of that vestment date (my experience with my last suit ‘n tie back in the ’80’s)…

may we all find a better day.

My pension money “disappeared” during the JPM buyout of Bear Stearns.

WL,

Take the money as soon as you can stop working full time. I took my SS early because I needed the money and it has been a good decision.

My 27% reduction will be made up somewhat when my husband retires and I can get a spousal bump up. Overall, I expect my reduction to decrease to ~10% with 5 years of benefits already banked.

Decisions are great including having them . The SS decision is very personal and depends on many health income factors and location and spare time commute etc. for those I know that retired on SS at 62 made the right decisions I personally plan to wait until max age something around 70 counting on a long healthy old age life . All personal decisions and remember no decisions are decisions.

If the Dow will plunge below Oct 2022 homeowners will be free… in a jail

break.

You think the Fed will go to ZIRP if the Dow drops 20%? Nope.

It may go to 6% if the Dow drops 20%, and if inflation does in the fall what it has a good chance of doing.

It seems to me the housing inventory problem is likely to be transitory since forced selling should eventually add some inventory. This would likely also result in price rediscovery since people buying with financing can’t pay that extra 1, 2, or 3K more each month until either the prices or interest rates drop.

As to what causes the forced selling, I don’t know. Maybe a tough economy followed by job losses, or perhaps boomers moving into assisted living, etc. Some of this might be organic, the rest might be from an economic shock.

Question to mortgage brokers/lawyers among u : is it possible to sell a home and transfer the 3% mortgage to the buyers ?

Micheal Engel

The answer is NO! I went through this in the late 70s. I asked the lender if my loan rate was assumable. He lied and said yes. After the loan was closed I found out that the loan was assumable but not at the low rate I had. He left out that fact.

Loans used to be assumable, at least they were in Calif. But that ended in about 1980. Today, maybe adjustable ones are, definitely fixed rate ones.

“not” fixed rate ones. It’s getting late.

It really depends on the individual mortgage as to whether or not it is assurance.

Loans backed by Fannie Mae and Freddie Mac are generally not assumable

I have a VA mortgage that is assumable, 2.75%, but If I recall correctly it’s only assumable by another VA-eligible buyer.

This is incorrect. A non Veteran can assume it if they qualify with the mortgage servicer. This is the good news.

The bad news is:

The problem is the down payment required between the principal balance of the VA loan and the sales price. Buyer must bring cash and/or arrange a second lien.

The second piece of bad news is for the seller/Veteran. The Veteran/Seller does not restore his eligibility either, which makes it difficulty to use his VA benefits.

That’s good to know. I might have been explained that at some point when buying the house, but it’s been a while.

This is a great article and is right on the money. I posted similar thoughts about a week ago, though not as comprehensive as detailed as in this article. It hasn’t been broadcast much in the mainstream media, I think because the crooked RE and lending industry wants the churn to generate income and sales commissions. The state wants the churn to generate tax revenues from the state transfer taxes.

Those who paid cash might spit out their purchases if rates rise.

It is my observation that much of the RE purchased in vacation destinations are locked in and long term held by big and small operators.

You will rent that which you might have owned as a second home.

VRBO and the like changed RE dramatically.

San Francisco housing prices are about to explode higher once again, now that high-flying “tech” stocks have come roaring back. The freshly-minted IPO millionaires and NVIDIA employees aren’t going to care about 7% mortgages.

People have been praying for this fervently. But it’s not working. The median price in June dropped again, instead of rising, now down 18% year-over-year and 20% from the peak. And sales plunged 32% from June 2022, when sales had already been down 21% from June 2021.