Another sign the economy is flying a cruising altitude and refuses to land, even with short-term interest rates over 5%.

By Wolf Richter for WOLF STREET.

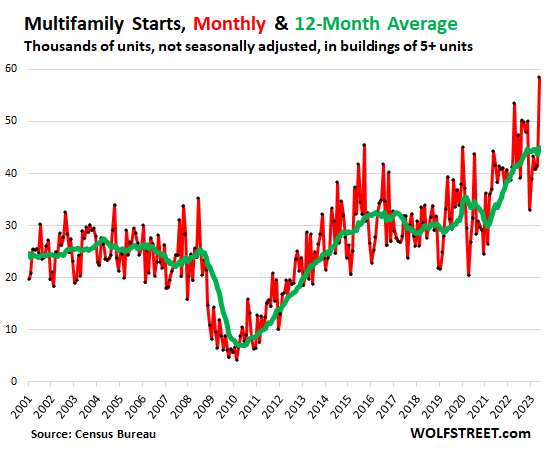

Seasonally, May is one of the best month for construction starts of single-family houses and multi-family buildings. Typically, residential construction starts hit their annual peaks between April and July. Today, the Census Bureau released the May constructions starts, and they were a blowout, with even single-family construction starts further bouncing off their January lows, and multifamily spiking to the highest level since the mania of the mid-1980s. Both are far above any kind of recessionary scenario.

Construction starts of multifamily housing units in buildings with five or more units (such as in large condo and apartment buildings) spiked in May to 58,500 units (not seasonally adjusted), the highest since 1986, up by 42% from May last year, and up by 49% from May 2019.

More importantly, the 12-month average, which irons out the huge seasonal and month-to-month fluctuations and shows the longer-term trends, rose to 45,100 units, also the highest since 1986 (green line).

Big multifamily projects have long lead times, and planning for these buildings whose units show up in the May data started quite a while ago – with big projects, years ago.

In big, densely populated urban cores, higher-end multifamily buildings with lots of amenities have been just about the only type of housing that is getting built – a trend going back many years – while the bulk of single-family construction takes place further away from urban cores.

For buyers and renters alike, the decision whether to live in a new multifamily building in an urban core or in a new house further out comes down to lifestyle choice – not necessarily price, because both are now expensive.

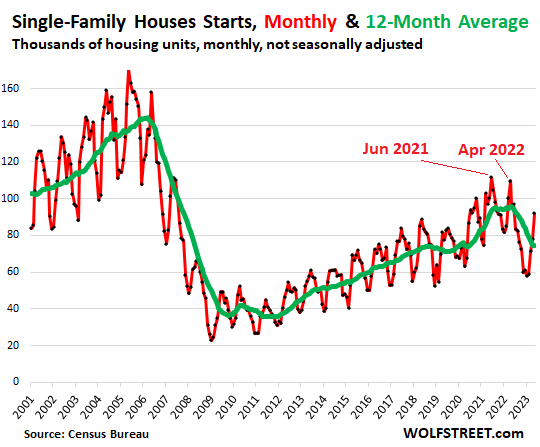

Construction starts of single-family houses, after a big drop that started last summer as unsold inventory was piling up, jumped by 18% in May from April, to 91,900 houses (not seasonally adjusted), the fourth month in a row of seasonal increases from the January low. Not included are manufactured homes (mobile homes).

- Compared to May 2022, starts were down 5%.

- Compared to the blowout boom months of April 2022 and June 2021, starts were down 16% and 18% respectively.

- But compared to the more normal times of May 2019, starts were up by 18%.

For the longer trend, the 12-month average dipped further in May to 74,200, just above the high end of pre-pandemic levels, and up by 4% from 2019. Starts have essentially unwound the pandemic boom – and based on monthly starts, are now accelerating again (green line).

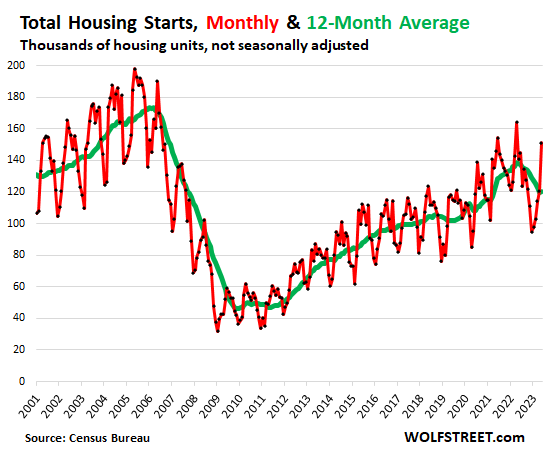

Total residential construction starts – single-family houses and multifamily buildings combined – jumped to 128,600 housing units in May (not seasonally adjusted), up by 7.5% from a year ago, and by 28% from May 2019.

For the longer trend, the 12-month moving average edged up to 120,400 starts, which was down from the pandemic boom, but was still up by 18% from May 2019.

Shares, Booms, and Busts.

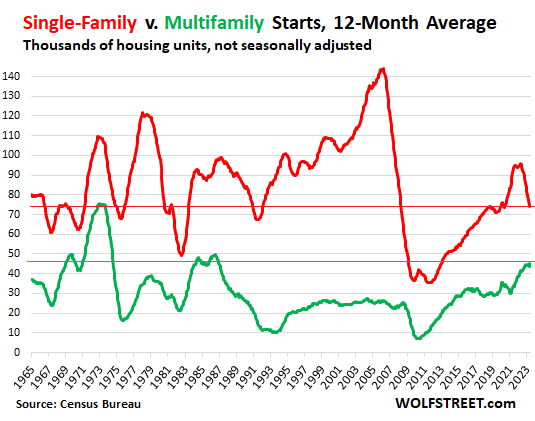

The share of single-family housing starts dropped to 61.5% of total housing starts over the past 12 months through May, the lowest share since 1986.

The share of multifamily starts in buildings of 5+ units rose to 38.7%, the highest share since 1974.

The share of multifamily starts of buildings with 2 to 4 units has declined over the years to less than 1%.

And this trend makes sense longer term as urban sprawl in big cities makes for ever more hellish commutes. Working from home cut down on commute-hell for office workers, but now many employers are trying to get their people back to the office at least a few times a week. And non-office workers can’t work at home anyway.

Over the long term, housing starts come and go in huge waves of booms and busts. Housing Bubble 1 was an epic creature for single-family starts; the 12-month average peaked in 2005 at around 142,000 houses per month, nearly double today’s rate.

Multifamily had its moment in the bubble sun in 1973 when the 12-month average peaked at 75,000 units per month, and then again in the mid-1980s, when starts peaked at 50,000 per month. But those were years with far higher population growth. Population growth has dwindled in recent years. And the recent multifamily starts are getting close to the mid-1980s high.

The long-term view, 12-month average — on a month-to-month basis, last year’s decline in single-family starts reversed this year and this reversal will show up in the 12-month average over the summer).

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

YEP. Higher for longer. A VERY long way to go. ZIRP should be put back in its coffin and buried forever……

While that might be true, expect mortgage rates to actually come down over the next 3-6 months as the spread between the 10 year bond yield and the 30-year mortgage rate reverts to more historical levels, even if the Fed keeps short term rates relatively high. As a reminder, the 10-year yield is still well under 4%.

MP Sounds good to me. We could have done just fine over the years without ZIRP.

ZIRP has caused untold collateral damage worldwide. You think countries would have looked at what happened to Japan under zero interest rate policy and gotten a clue? Japan today is now a basket case all thanks to 25 years of zero interest rate policy.

The 10-year yield is only well under 4% still because longer higher inflation is not priced in.

10 year isn’t making anything. Tie up your money to break even w/ inflation.

TIPS make way more sense at these prices.

The expectations that inflation will be 3.5% 2023 bottles my mind.

Morningstar thinks it will run UNDER 2% for several years. “Why We Expect Inflation to Fall in 2023”

Magical thinking on inflation!

People are so smart they’re dumb.

Core PCE still high and not budging. People still spending like drunk sailors. Housing still high. Unemployment low.

Inflation blips due to energy and everyone is psyched.

What will eventually kill the housing market will be the inability or excessive cost to get homeowners insurance. No insurance – no mortgage. No mortgage – no sales. Insurance is doubling and tripling in many of the strongest markets.

Creating a housing bubble is just a bad idea. But, try convincing Government that. Same as providing Government incentives for purchasing something. Like a Electric Car?

unfortunately insurance is based on COST of rebuilding

and since our FIAT $DOLLAR is exploding higher due to congress spend spend spend policies

up up and away it goes(ie premiums)

up 15-30% in 2023

can’t wait to see what it is next year

Mine only went up 70% this year. I called in and argued a few valuations and also found out a couple of discounts they offer for ridiculous reasons so I’m doing ridiculous things. Now my increase is only 33%-45%. They blame the cost of lumber which is a lot lower than last year. What a racket.

Here in Florida, homeowner’s is going through the roof. They’re blaming it on global warming causing much stronger hurricanes. I increased my deductible to $25,000 and my premium is still $1,100. Talked to a contractor friend of mine and he said material costs aren’t a problem anymore but labor is tough to find.

Kent….I experienced a whopping increase (percentage basis) in HOA rates the last two years (FL). Most of it is driven by new state laws (following the Miami building collapse) vis capital reserve estimates for future repairs. State now inspects annual HOA budgets/paperwork for compliance.

Interestingly, my auto insurance rates have also increased by a large percentage (FL). I was informed (by a provider rep) that hurricane Ian, inflation and “competition with other insurance providers in the state” were the primary drivers (pun intended). Since our family driving patterns haven’t changed one iota, we drive less than 200 mis/mo anyway and (no infractions running on three years now) and I’m not the one who bought a home on way exposed sand bars…..I am not happy. Since the provider had the lowest rates in the state I took the competition statement to mean they increased rates to close the margin.

What I see happening in the big picture of all of this is more risk taking by those of us who are not “insiders” to maintain our lifestyles over the next many years. Inflating away debt is going to result in serious unrest at some point.

Find out who is behind the continuing multi-family boom and you’ll have some insight as to why it is continuing.

Hint: The Federal Government.

I have roots in Charlotte NC where a boom that started way back under Obama is continuing. From intel on the ground (renters) it is appearing that they are already overbuilt and still adding inventory.

These 4 story wood framed multifamily bldgs that took off after 2009/10 are a result of the decision to support/promote this housing by the government (Obama was involved). The thinking being when (not if) all the younger people tire of these rentals (as they move up to a house), they will provide great subsidized housing for poor and seniors.

Regarding single family starts, numbers are statistically insignificant. What starts are occurring in our area seem to be high end stuff by buyers who don’t have money concerns.

our multi-unit apartment market is still red hot

now with higher rents they are even higher priced

Mike R.,

Agree.

In addition 15 Minute cities and who knows what else is going on behind the scenes that is influencing this. In Germany huge incentives will go out to owners of large Karl Marx type multifamily communes while big disincentives in terms of taxes will be levied on single family homeowners.

Moving more and more towards centralised everything.

What’s wrong with 15 minute cities? I am looking forward to the day when I can put a brick on my car’s gas pedal and let it drive itself off a cliff. Hate the thing. Have lived in and would love to again live in (but can’t because of career) something like a 15min / truly walkable city. But as a consumer and would be home owner, you put that in my vicinity and I will pay a premium for it. Consumer demand and market forces and all that yada yada.

I’m 100% in support of 15 minute cities which grow all their own food, recycle all their own garbage, and use their own effluent to grow their food, all within 15 minutes of their Politburo.

Automobiles have become a status symbol in the US like having a big house.

Walkable cities take both of those status symbols away, and many Americans would feel very lost without them.

Besides, 15 min cities make lockdown operations so much more efficient!

Have at it! Nothing wrong with slavery so long as it is opted for through freedom of choice!

What’s wrong with multi family buildings?

Nothing.

Fees, in perpetuity

“Fees in perpetuity”

Unlike, say, property taxes, “homeowners” insurance, repair bills, etc?

Any that is even before we get to the issue of overpaying by 100% due to ZIRP seduction.

I get your point, but in practice it is easily possible for “ownership” (period between positive equity and foreclosure…) to be easily converted into a losing proposition.

A ZIRP doubling/tripling of home prices during 20 yrs of some of the worst employment growth in US history will do that…

Quality of construction (ie health of inhabitants) – Houston, TX for ref.

Your on the wrong blog.

Parking?

Nothing.

They provide a space to live when moving out of your parent’s house before you can afford to buy your own house.

They are useful and necessary.

the multitude of families living next to, above, and bleow you

Do you hate people so much that you don’t want neighbors as a matter of principle? Live out by yourself in the sticks? I mean, if that’s what you want, great. But not everyone is that way.

Mike R.

+1000 … from DuPage County Illinois

Not sure, though, if our area was ever “over built”.

But driving around doing errands it seems that any NEW homes being built are HUGE. My late Mother-in-Law referred to them as ‘Garage Mahals’ 🤪

Maybe, since we’ve been living in a 1950’s era “starter home” for decades it’s a case of

‘Sour Grapes’ on our part.

Also, numerous very large apartment/Condo buildings are going up near local Train Stations.

” NEW homes being built are HUGE.”

Latest iteration of McMansions for McMorons – Homes for the Thousandaires.

That is a lot of assertions without providing any evidence.

New construction is the only way out of the current housing pressure. There are more buyers than sellers nationally.

Historically, housing has been an “investment” that increases in value over time. After this boom is finished I dont think that will be true. The boomers will die off and the millennials will never regain the lost time to start families to replace them. We will eventually have more housing than people, and the economic forces will work in reverse.

Just so.

Japan with its aging population has this problem now. Italy with its lack of opportunity for young people leading them to move elsewhere has a similar housing problem in the same vein in many areas. None of these are exactly analagous but it is proof that housing doesn’t always go up everywhere all the time. But hey as long as I have a nice place to live I don’t really care if the people who owned the place before lose out on their investment. Screw ’em.

Prices flat/falling in Italy? Not that I am aware of. More like up significantly for the last few years, and now cumulatively probably 50%. I wish this weren’t the case, but it is…..

The 5+ units peaked in July 1973 at 901K. The downhill was steep. The low

was 108K in Aug 1993.

After the 2010/2011 flatbed of about 150K the multi 5+ units reached 978K in May 2023, a new all time high.

The multi will deflate rent and the CPI.

I’m looking at the slide in single family starting late 2005 while it didn’t appear in multi family until 2008. Interesting lag.

A more useful stat might be to compare median SFH prices from 2000 to 2023 relative to median income growth over the same period.

When you have SFH prices double or triple over a period when income growth was a tiny fraction of that…demand for multifamily is…inevitable.

Stripped of ZIRP phony interest rates, SFH sales have dropped 25% (after a mere year of unZIRP). The only thing holding Wiley Coyote (and his Acme anvil) up is the historically unprecedented lack of for sale inventory.

But people will still pass away, get transferred to, get fired, etc.

Not surprising in the least.

With new residential listings critically low, homebuilders are the only ones who can bring new inventory to market, and do so with scant competition from existing homes. Homebuilders also have access to rate buydowns and other incentives that existing home sellers can’t offer as easily. With home prices still very high, new home builders (as the “swing producers” of the housing market) should do well in this environment.

I was going to say the same thing. I suspect the reason that new housing starts were so high is that existing home sellers are still hallucinating.

If someone is listing their 1987 4 BR home for $1.2 million that sold for $650,000 only 4 years ago, a lot of people will decide that they’d rather pay $1.2 million for a brand new home.

Right, high prices are often times cures for high prices. High prices attract supply, but also attract delusional people. A home built 20+ years ago will need upgrades that are not just visual, they have wear and tear, and might have worse building materials. A new home also comes with incentives and usually a builder warranty. I am not going to purchase a $450,000 used home when I can get new for not much different monthly payment.

Exactly. In a lot of markets, I’m seeing listings that (according to Zillow) sold in 2021 or 2022. That says to me that some people are facing the sobering reality that they made a bad financial decision, and are trying to get out of it by selling today. We’ll see what happens.

You might buy that older home if it saves you an hour commute each way.

Location.

The USA may be different, but the best places to build on was built on a hundred year ago. Or at last a long time ago.

As for building materials, there was a lot of crap 20 years ago and there is a lot of crap today. In houses built a hundred year ago that still stand the materials is usually not crap. (The building built long time ago with crap materials are long gone…)

Zombie companies and unemployment are the missing pieces. This ain’t over.

I would buy new if I could afford it. I’m looking at absolute crap that is so horribly overpriced. When doing the math on repairs and value after repairs not one of them is a good deal. And I have no intention of re-selling, I just want to live in one. Sellers and realtors seem to deduct the cost of materials ONLY, if even that, and expect the buyer to be happy fixing these crap shacks and murder cabins.

Many of these houses have the worst ever lack of maintenance. I mean, some have been owned for decades, rented out at good to great profit and are now just falling apart. I just saw one that could have lasted decades more if the owner had just fixed a portion of the cap ridge on the roof several years ago. A good 3 hours and $70 worth of materials. WTF? And you can see the top of the roof right from the street – it’s not like they couldn’t know about it.

And just out of curiosity I looked at houses out of my price range. LOL. For the love of your sanity, if you have never done construction, I’d recommend anyone looking at a house to just forget the realtor recommended inspector and pay a general contractor good money to inspect the house and give estimates on repair before you buy.

Realize that most realtors (who come up with those asking prices in the first place) have never seriously used a hammer or skill saw, have no idea why 1970’s electrical may be a hazard and don’t know what those cracks in the foundation, stains on the ceiling or irregular floors mean. And if by any slight chance they do – they will pretend not to.

GOOD IDEA Lynn:

Used to work with several more conscientious RE brokers in SF bay area doing exactly that…

They would call me when a potential buyer became serious about a specific house; I would walk through with them, listening carefully, sometimes for hours, then give them either a ”ball park” for what they wanted, or tell them I needed more clear instructions in writing if they were vague.

After the first such, I knew to ”pad” the initial oral estimate so that the final cost was under it,,, IF the new owners didn’t add a bunch of upgrades, which did happen a lot, but I was careful to price additional work very very clearly before starting it.

Never had to advertise, as the word of mouth brought me more work than I could do.

HUD OWNED Homes used to be great for first time home buyers. Not sure if that is a viable option anymore or not???

“HUD OWNED Homes used to be great for first time home buyers. Not sure if that is a viable option anymore or not???”

It’s not. That would require HUD to actually own enough homes to be worth speaking of.

You seem to be explaining how a free market works? NO Government intervention? You typing crazy typing? HEE HEE

At the first of the month I will be going down to LA to help my youngest son move from his current apartment in Santa Monica to one in a new complex of apartments, shops, restaurants and offices just being completed on the site of the old Olympic Drive-in in West L.A.

His employer, one of the big video game companies, leased up all the office space when the project was announced. He doesn’t drive so he is looking forward to tumbling out of bed and walking across the courtyard to work. He has been working at home a lot the last year, but he will be going in to the office everyday once he moves because of the free food and drink in his office . A little bit like a fancy version of one of the old company towns, but maybe that is where things will have to go to lease office space.

He needs to wake up because AI will eat his free lunch and dinner.

Throw in a CBDC and you’ve got the company script to complete the devolution to serfdom.

Lots of good rhyming possibilities for the acronym ‘CBDC’, maybe we can revive the old American culture with blues and folk songs about the bleak future.

What on earth are you talking about? Do you even know exactly what you’re mad at, here?

It’s CBDC fearmongering.

you guys that complain about housing prices, what were you doing 2008-2020?

Housing bust 2 is officially over!

I think housing bust 2 is just getting started. But that is just me?

I agree that housing bust 2 is just getting started as well. Problem is that inflation is so high that if the federal reserve doesn’t get cracking on rate rises, then it’ll take so long that you’ll miss half your life waiting for a good corrected price to buy at… This moving goalpost situation is exhausting to monitor.

Fed is risking political disaster with their endless fiddling. Swallow the pill now, dummies

Housing vs rent is at all time highs just like stock market price to revenue is back to 1929 highs.

Bingo

“you guys that complain about housing prices, what were you doing 2008-2020?”

I would suspect a good chunk of them were amassing ever larger student debt, looking for their first proper job and then beginning to pay some of that debt down. Most of the people negatively affected by the RE rocketship are younger people without inheritances. Interest rates were low, but valuations high so they needed to save ever larger sums for downpaynents as prices ran away from them and growing rents squeezed their ability to save. For anyone who managed to get in earlier (I did) it was a party, but for the vast majority of kids without any luck it was a total bummer, and at current prices still is so I can’t blame them wishing for a bust to materialize. I don’t have the article saved so can’t reference but few years ago I was reading that the wealth gap among millenials was found to be massive at the time, the conclusion if I remember correctly was that the large gulf between the wealth classes of that generation was down to asset prices, inheritances and family help. For me and my family a solid correction would probably not be ideal right now, but I think it’s needed and I’ll survive if it happens.

Thats the big difference. With a price correction, the haves will survive. Without one, the have-nots wont.

Actually, the “have-nots” that are stretched will not survive anyway.

A housing correction or stock market correction. Housing correction will effect 65% of the household population. A stock market correction will effect the top10% a lot. maybe the next 10% (Top 20%) will feel a big bite, and the next 10% (top 30%) will feel a little bite. The bottom 70% wealth during a stock market will not feel much pain.

I guess we need to pick the poison.

+1

It took 3 years for the GR housing bust to move from peak to trough. And that was with an actual recession playing out for 2 of those 3 years.

Furthermore, it’s silly that you call the last 12 months a bust. The top 8 or so markets were only down 12-18%. Everything else only dropped between 3-5%. The later is nothing.

If a recession is in the cards by next year, it will result from these ingredients:

1) Higher for longer inflation & interest rates which force 70% of Americans’ to increase their credit card debt well past sustainable debt servicing costs.

2) CMRE implosion of some sort, again due to higher for longer interest rates.

3) A slowly deteriorating labor market that sees 1st time unemployment claims break through and stay above 300K by this fall.

4) The Fed’s continued draining of liquidity.

5) A 10% drop markets by early next year that starts to spook consumers into recognizing their wealth effect is going down & not up.

6) Increased chance of a black swan as we enter Biden’s final year in office.

The exports of the US to China are and have long been minimal, despite the export deals that the CCP basically ignored. However, the ongoing implosion of the economy of China, which I predicted more than a year ago, will cut EU, Australian, and other countries’s exports. Hence, because the world economy is a big web, we will see a recession. US banks and Wall Streeters, who lost hundreds of billions or trillions in China will also be getting another covert series of bailouts from their “Federal” Reserve cartel, which will create US stagflation thereby by digitally “printing” even more money than in late 2019 to the present. See e.g., the St Louis Fed’s own M2 charts.

They wilk need their cartel’s golden goose (their “Fed”) to bail them out. The US government has wised up so another Tarp freeby gifting program to insolvent banks will not pass: due to massive losses, e.g. in commercial real estate, most larger, US banks are now insolvent, yet again.

Nice post Ben. Still think over leveraged zombie companies are the Black Swan.

Great point, absolutely!

Dude, bail me out nation is the gig today. Get out from under the table and face reality . SOCIALISM. From your beloved Tesla to your local government are all on the take. Give me more handouts. 32 trillion of handouts for what? You to pay more taxes. Good deal for us the serfdom.

*Socialism for the rich. The poor are still poor and could lose their homes, savings everything because of a single medical emergency. Hell, my relatively well off friend recently was diagnosed with something potentially life threatening and has had to drain a chunk of her savings and may sell her house to pay for surgeries and care. Thank God she got to keep her private employer-provided insurance that ultimately screwed her over.

Socialized losses, privatised gains for the rich,,, total socializm for those folks who really are poor…

Screw the middle classes as whatsname says…

I have been totally disabled, and found free everything for a while until able to recover, so I have been there, and did not care for the waiting for hours and hours for the freebies, along with the barely sufficient support, attitudes of provider personnel, etc., but that motivated me to recovery and get and stay as far from that life as possible.

Socialism means the government owns and operates the means of production. We have large private corporations with huge influence on government actions. This is closer to fascism.

We bought in 2011.

The place is now worth 5 times what we paid and is paid off.

5x??? Vegas? Phoenix? Florida?

And? Try and move. That 5 times gain will evaporate in today market. YOU might end up under the water if you move.

It is only “worth” what you get when you sell.

In devalued dollars= gains are not realistic

If you look at the numbers then you are absolutely right the bust never really came.

Small dip in prices and and big crash in volume but the prices are now going up nationwide for last few months.

Same with stock market as well.

Spring bump. Almost always happens. Like you say, look at the numbers.

The “pause” was another MASSIVE policy error by Jerome Powell, who will go down as the worst FED chair in history.

History will show pats on the back and some prizes for some. History is crazy.

Didn’t wish to inconvenience the gamblers. Gotta have all time highs in 2023 to “whip inflation” (in 2033?)

If the Fed had raised rates .25% you would also have called it a MASSIVE policy error, so ….

I normally agree with DC but come on: no way is he worse than Bernanke, Greenspan or Yellen who gave us “too low for too long” in the first place.

I do however agree that he’s not taking the problem seriously enough.

Bernanke had to be the absolute worst ever.

Nobel prize for Powell like Bernanke 😀

How do you adequately compare fed chairs when they all get an F? Yellen gets 2 FFs and Powell gets 3 FFFs?

Pre-recession spike? The stock market is on a tear, AI stocks are causing a new wave of riches, who cares about the little guys eating their savings if any, and working two jobs? Enough people are doing well and can buy from the housing inventory. The recession is brewing at the other end of the spectrum, leave it time to ferment – nothing goes to heck in a straight line, lol.

Are AI stocks creating “a new wave of riches,” or just facilitating the transfer of riches from one person to another person? We shall see, but I think it will largely turn out to be the latter.

Yes, this. AI is creating a new wave of riches if those companies actually are transformational and make tons of money. People selling the same shares of stock back and forth at ever higher prices is not creating wealth. It’s creating an illusion.

As is selling old houses back and forth. No wealth created, just another illusion.

It is a huge bet on the future with massive……

…energy consumption.

Which kind of contradicts other agendas.

As with crypto, at the starting line is the big “gee whIz” flying-cars narrative. It takes time for the holes in the story, the scams and downsides to manifest. meanwhile, guaranteed, plenty of suckers will be cleaned out. Some screwups will be at scale, and dazzling.

Looks like an increase in multi-family housing starts are associated with negative real interest rates to me

Don’t forget to factor in the massive illegal immigration that is occuring under the current administration. These people are living somewhere. Not sure of its effect but seems logical it boosts demand for housing and is inflationary. Too bad for the people waiting in line for legal entry.

You really think illegal immigrants are buying houses?

No theyre renting, and often very densely. So their pressure on the housing market is understated relative to a standard family. But it still exists. The idea that people can move into a country and not consume any housing units at all is nonsensical.

Theres also the argument that “Illegal immigrants are who build houses!”, which Im sure also has some truth, but its almost certainly false that they build more than they consume.

Doolittle et al.

Sheesh.

Before you get all tangled up in your own underwear with statements like “massive illegal immigration that is occuring (sic) under the current administration,” let’s look at the ACTUAL NUMBERS OF POPULATION GROWTH and HOUSEHOLD GROWTH, because that’s what matters when it comes to housing demand, not clickbait BS.

2021 (first year of Biden) was the lowest ever population growth of 0.1%.

2022 (second year of Biden) matched the second lowest ever population growth of 0.5%

The 12 months through April also show the second-lowest population growth of 0.5%.

Year – pop growth:

2008: 1.0%

2009: 0.9%

2010: 0.8%

2011: 0.7%

2012; 0.7%

2013: 0.7%

2014: 0.7%

2015: 0.7%

2016: 0.7%

2017: 0.6%

2018: 0.5%

2019: 0.5%

2020: 1.0%

2021: 0.1%

2022: 0.5%

Population growth in millions:

2019: 1.72 million

2020: 1.27 million (third lowest ever)

2021: 0.56 million (lowest ever)

2022: 1.24 million (second lowest ever)

Meanwhile, HOUSING STARTS during these years:

2019: 1.29 million

2020: 1.38 million

2021: 1.60 million

2022: 1.55 million

Over the four years from 2019 through 2022, 5.82 million housings units were started.

Over the same four-year period, the number of households grew by only 3.61 million households.

=> So new construction exceeded household growth by 2.2 million housing units over those four years (5.82 minus 3.61)

Thanks for the numbers Wolf, I think your post shows the real issue here is not the growth in population from whatever source, but the pent up demand from a decade of depressed new construction. People are living with others, and have been, and want out. A bulge working its way though the system.

Hi Wolf,

Are your numbers from government census?

I don’t think that population growth numbers you are using tell the whole picture for 2 reasons:

#1 Covid killed many elderly/ residents of nursing homes. This will decrease the population growth and make it look smaller than it might pre-covid years. However in regards to the housing market, nursing home residents do not occupy homes. So when they die, it doesn’t create a new glut of homes but rather a glut of nursing home beds. The new illegal immigrants need housing (not nursing beds). So the demand brought by illegals may be hidden by nursing home deaths from COVID (a huge #), in a way that disproportionately affects housing demand and supply outlook that cannot be evaluated by overall population changes. I suspect the reason why the last 3 years are low are due to COVID rather than some change in illegal immigration.

#2 I also don’t think government ever gets truly accurate numbers from census calculations.

Of course, if the fed raised rates and the government stopped spending, we might get a better idea of whats going on. Given how goosed everything is, its really hard to pick out things with all the confounding data. But it wouldn’t surprise me if there was a small contributing factor affecting the SoCal and El Paso Texas real estate markets… not really sure how much given we are seeing inflated prices everywhere…but could be…

Figure 2.5 people per household, so these housing status are vastly outrunning population growth. Eventually it’ll be a big problem. Not really surprised new construction popped here, easy to justify with not much inventory— no net housing supply but a lot of friction for those looking to move kids, jobs, etc. People will pay for now but it won’t last longer than the credit cycle.

I think he is referring to people buying homes and renting to illegals, which can keep people hold on to homes that they otherwise would have to foreclose on? If there’s less demand, those people would have to give up their homes and prices may drop? Not sure if I agree w this theory but it might be contributing in places like San Diego and LA/inland empire?

LOL?

Noire examples like the one you described will turn that neighborhood into a ghetto.

saw just that it the hood we were in in 2004-6

”cousins” and such buying as a family of 4,,, six weeks after closing there were 12 people there including a couple of preschool age children…

meanwhile, the place became a staging/waiting area for dozens of folks every morning, and most of them went to work almost every day

got to know some of them,,,, they said they had the right papers to pass E-verify — purchased for $500 just south of the border

all of them were hard workers, including+ those who ”stayed home” and took very good care of the place

bought the house next door about a year later

Nobody believes your story.

I have seen this happening in Southern Ca.

Not sure if they are illegal as I didn’t ask for their status but saw that a 1.5 million dollar house was bought.. 4 bedroom and 8 people moved it .

Very common in socal to have multiple families living in single house due to affordability

Huge immigrant/laborer population in suburban NYC (decades before the publicized/politicized busses and planes nonsense on the news. Its always been like this here). An acquaintence who’s not afraid to wear their prejudice on their sleeve, is selling their home and joked that they’ll spite their uppity neighbors by selling it to the ‘truck full of illegals’ that showed up with a cash offer. Then made more off color remarks about 12 mattresses on the floor and yadda yadda.

Said acquaintence was a bit annoyed when I reminded them the neighbors should be pleased as those ‘laborers’ will transform the place into a near mansion and do a quality job improving property values, unlike the local flippers who tan easily and will put the panel box half wired in the shower stall if it means a speedy profit.

‘They’ by and large keep a spotless home even if rented, its the predatory landlords who rent to them that don’t keep their dwellings neary close to code.

Total B’S lie.Nobody can fake A number for E-verify.And close to impossible to get a fake green card looking like real.HR will detect it with closed eyes.

Would like to mention the Bosnian Influx in the St. Louis Mo area some years ago. During that time, it sure seemed to me, they had quite an impact in the RE market. First in the St. Louis City Area and within 2 to 4 years were moving into the St. Louis County Area. Many were business owners also. Not sure if statistics are available but I sure remember them having an impact on the area in many ways……

We have the Bulgarian Mafia where I am, along with cartels etc. Those guys are not something to mess around with. Local LEOs are afraid of them. Bought up a lot of large properties for cannabis and imported their own labor. They were some of the people buying high end massive Spanish hacienda mansions many miles out on 4WD dirt roads. Many of those mansions will be abandoned and left to rot back into the earth as the illegal cannabis industry is slowly dying now in the rugged mountains.

We had an invasion of people from Rhode Island a couple years back. There was one couple on my street and a family of four a couple blocks down. Just completely overrunning the place and driving up housing costs. Don’t know what they’re up to but seems not good. The two on my street leave every morning in separate cars and come back at night, and they occasionally drive somewhere together and return with a bunch brown bags full of something I don’t know what but I’m sure it’s not good. I called the FBI and they thanked me for my honorable diligence and gave me an award. I can also smell cannabis coming from their house sometimes so I think they are drug lords.

/s

Is cannibis illegal?

For last several years in Northern FL environs multiple, large multi-family projects basically laid as dormant fields for several years. All of a sudden, there has been rapid construction activity everywhere. We’re talking thousands of units in a fairly tight radius. Who knows, maybe the 10,001 state and local bureaucrats who have to sign off on everything suffered some cash flow needs. It’s somewhat intuitive that the original investment incentives were predicated on migration from other states. We’ll see how this evolves (occupancy), no way the local infrastructure (particularly roads) can support the potential population increase.

Whenever I see someone say something like “massive illegal immigration that is occuring under the current administration.” I know that person uses poor sources of information. They use sources of information that prey on their ignorance through fear.

You should really use better sources of information.

Architect here, 30+ years of working for some of the biggest multi-family office/residential high- and mid-rise firms in this nation (and a few others.) As we say in the shop, count the cranes on the skyline: that’s your economic indicator for 2-4 years out (at least for our business), and whether or not institutional money will back more of the same. 75%+ of our SF office’s work is in LA or Seattle suburbs, more and more in Montana, Idaho; almost nothing in the SFBay area anymore, and very few inquiries. By end of July we will have dropped almost 40% of our staff. If history is a guide, strong headwinds indeed ahead, despite the rosy snapshots :/ ps anyone need a suburban mall re-entitled as multi-family? I know a guy

Great industry info…and humor to boot. Following.

“ps anyone need a suburban mall re-entitled as multi-family? I know a guy”

Lego, *seriously*, you should advertise in outlaying areas. Or contact city govs and blind mail mall owners. I know of one in Eureka, Ca that sorely needs you.

In transportation equipment here. Similar feel from chatting with several of our steel suppliers. The feeling was that commercial construction metals demand is getting pretty weak, but they’re still busy keeping up with strong demand in farm equipment and trucking equipment.

– New single homes sales fell to : 683K. Demand for new units at peak season is low. Aug 2020 peak was over one million houses sold.

In July 2005 1.39M new homes were sold.

– Total Completions in May 2023 : 1.518M slightly below 1,577K in Feb 2023, during the winter. Down 1,720K from 2,240K in Mar 2006 to 520K in Jan 2011. //

[1,577K – 520] : 1730K = 1,060 : 1,720 = 61,7%.

Total completions peaked 50 years ago in May 1973 at 2.3M units.

Your numbers are BS. All of them.

1. You’re citing “seasonally adjusted annual rates” and promoting them as actual monthly sales. Huge difference.

For example, your “New single homes sales fell to : 683K” = seasonally adjusted annual rate.

Actual sales in April = 62,000.

2. You’re citing month-to-month changes, without disclosing it:

YOY, the SAAR of sales in April: +12%

YOY, actual sales in April: +11%

3. Same BS with your numbers on completions.

Fred, New one family sale : 683. Frequency m/m. Units : thousands, seasonally adjusted annual rate. I am not promoting actual monthly sales. Wolf can provide the actual dots and the 3M/6M moving averages.

At this rate housing will soon take up 80% of many families take home pay. On the bright side, new construction is rock solid, so there will never be any worry about paying out for major repairs once warranty expires. ;)

You can’t get a loan for 80% DTI.

Max DTI is 50.0% on a conventional loan, 57.00% for FHA.

MultiFam is the future. The more they build, the better – Millennials and Gen Z will have nice places to live with reasonable pricing.

I hope mortgages amortizations extended to ninety years like in Canada isn’t the future.

“Millennials and Gen Z will have nice places to live with reasonable pricing.”

We grew up hearing that promise many a time over and were burned too often to believe it. Particularly damaging was something to do with taking student loans out the nose to ‘get a good job’.

To quote the venerable Philip J. Fry, that dog won’t hunt.

“…have nice places to live with reasonable pricing”

No one ever made me that promise. For the first 12 years of my independent life, I lived in what would be today unspeakable shitholes because that’s all I could afford. Lots of people did at the time. I don’t wish this on anyone. But that’s what we did because we couldn’t afford anything better.

What was your worst digs?

Briefly subsisted in a glorified tool shed downwind from a crematorium in my early twenties. Tissue-thin walls, dicey plumbing and no heat. Perfect little spot for long evenings spent playing mumbletypeg or drafting a manifesto. The loathing a place like that might otherwise induce was offset by youth dew and hopes eternal spring.

“But that’s what we did because we couldn’t afford anything better.”

Living in my car straight out of high school, I don’t recall ever being picky about where I lived just struggled to meet the rent on pre-college degree pay. Windowless basements, a neigborhood so bad the cops used to regularly pull me over thinking I was lost to tell me I needed to turn around. Took a good ten years to find relatively safe & healthy accomodations. Hell I still can’t find quality affordable housing in my 40s.

But rent was over 80% of my income throughout the 00’s. Someone now couldn’t afford a studio on minimum/low wage.

My situation was a bit extreme but there is no denying Millenials/tail end of Gen X came into adulthood at a horrid time in housing affordability vs income. My boomer parent bought a condo working minimum wage at a gas station in the early 70s fresh out of high school hence they assumed I would be just fine when I was handed a cardboard box to pack up and get out on graduation day. Not one Millenial I know was able to leave their parents’ house and afford independence unless they were well set up financially by their parents, or also booted out and living in their car in parking lots and rest stops. Even the dark basements and dangerous neighborhoods have been outrageously expensive and increasingly so. Gen X at least had college flop house apartments, not sure where those were in the early 00’s but I never found a single one under $1k/month and now, forget it.

The direction things are going, its deeply concerning for the next gens coming up.

As for multifamily… the last condo I lived in had a downstairs neighbor with a penchant for crack cocaine and slapping his girlfriend around, but she was Section 8 and the landlord couldn’t get them out without a long, drawn out battle. As an owner in a multifamily, you’re also at the whim of how the Board handles co op fees, so one bad storm or expensive upgrade could land you with exhorbitant increase in dues. Plus, multifamily simply isn’t for everyone, I’d sooner return to car life. FHA has strict rules what multifamily units meet its approval guidelines, those rules will need to evolve as condos become the new SFH.

There’s clearly no developers in the comment section. As wolf predicated, these projects started 2 to 4 years ago. Money panicked at the beginning of the year and much of it remains so. But there is institutional equity to start these projects and the investors and MF builders figure that when the recession is done (or mostly) in 2 years the recession will be over. They’ll likely lose that bet.

The SF builders or relying on the low Supply and new forms of financing. They’ll likely do okay.

As far as the huge four of undocumented. They will mostly take up existing vacant homes or apartments and their occupancies are usually considerably more dense than typical units.

Lastly the MF industry is strong because corporate money flows easily to those projects who prefer long-term holds. Very different capital for SF. However the build -for-rent is changing that and will be a long term boon to the SF market as well as a mitigator to the SF supply in general.

I built previously… in Texas. Stopped late last year because I mistakenly figured the huge spike in interest rates would virtually stop sales. It didn’t happen.

New home sales have slowed a bit and prices have dipped some, but the shortage of existing home inventory has pushed buyers into the new home market, supporting both sales and prices.

Meanwhile land prices have tripled, and construction costs are still well above 2019 levels, so the bulk of new construction is luxury homes and luxury condos and TH’s. These are all selling like hotcakes.

New home construction & supply is still 3-4 million homes behind demand and playing catchup from massive underbuilding between 2009 and 2019.

Stupid Wall Street money keeps pouring into multifamily and will saturate that market eventually.

Until the fed raises rates a few more points and causes a major recession, the housing market isn’t headed down. Sorry doomsayers.

Calling someone a doomsayer because the call out a coked-up market for what it is seems like someone berating the designated driver as a big square.

This guy is full of crap too. Typical RE shill who can’t read a chart. Housing is not “selling like hotcakes” compared with 2020-21.

Amazing how many people are fooled by the usual spring bump.

– Between 2020 and 2022 1,300,000 people expired. Meanwhile construction for WFH expanded. The WFH mania is over. Layoffs announcements in the first 5 months exceeded 2022 total.

– Greedy landlords, who contribute little to the econ, cont to expand the multis, demanding higher dividends from the lowest quintiles, charging higher rent, because commercial loans rates tripled.

– The impaierd are still dying from what we know.

Cyclically speaking: those who watch will know when we are overbuilt. For instance in 2006, we were overbuilt. It’s just picking up steam right now so it will take a few years. That phase is what the actual “splendid” (to borrow Wolf’s adjective) devaluation phase follows. The blip we just went through is the notorious mid-cycle slowdown.

We’re back to pre-pandemic activity in the home purchase market around here in Swampland. People have gotten used to the new reality in the mortgage rates and are out there putting RE contracts on every piece of crap that goes on the market. Gone are the quality new builder renovated properties. Everything selling now is in bad neighborhoods, with high crime and drugs. That’s what’s affordable. They are being snapped up. Inflation in housing is back and this will show up in the data in the very near future. We’re working 18 hours/day. That doesn’t sound like a recession to me.

NCR is its own world. A very messed up world. Tons of money because uncle Sam sucks it out of the rest of the country.

I wish socal jim would make comments. His forecasting was 100%. My firm discussed his posts in investment meetings.

LOL, in your city, the median price is down 2% year-over-year. So that’s not a big decline yet, but it’s a decline. SocalJim said that this could never happen.

In SocalJim’s city, the median price is down 4% year-over-year, something he said could never ever happen.

He said that prices will always rise. But they’re not. It’s all quite embarrassing.

New construction is a great thing for the economy, and it’s a great thing in creating new supply.

Home builders are selling by cutting prices and buying down mortgage rates. This makes new houses a better deal than resale houses. They’re the pros, they have figured it out.

The resale market is frozen because sellers haven’t figured it out yet. They will eventually.

MFH and SFH is going up like crazy here in central FL (mainly MFH in Orlando given space limitations and SFH in suburbs/outer areas like Winter Garden). That should help cool prices. I saw it published a year ago, but FL had like 1.6 million vacant houses and 500k of those seasonal use so still over 1 million just vacant…wish that supply would come online but so far not so much. In 32819 zip code there are barely over 100 places for sale listed (that area includes Bay Hill for those not familiar with Orlando). I remember over 300 regularly listed pre-COVID in 2019.

California is second highest in numbers of empty homes at 1.2M of them. Not the highest pr capita though.m This doesn’t include vacation rentals.

Homelessness in Ca is highest in the nation at 171K as of 2022, although, I would guess that number is much higher.

There needs to be very high taxes on unused vacant homes.

second that

Same he was the gold standard.

Is the OP sarcasm? Must be.

When Jerome Powell was buying MBS, like a hurricane, there was a whimper of a question to Jerome Powell from some beaten down news representative of corporate media. Basically, something along the line of his MBS buying was generating high prices, his comment was “the solution to high prices is high prices.” A deflection of his devastation and ignoring the compounding of his disaster by the fact that housing has a myriad of price fixing from “local zoning issues” to import of building lumber since we clear cutted our own lumber decades ago; when flying over the Pacific Northwest look for yourself.

In a let them eat cake attitude Jerome Powell rolled up to some homeless camp on the way to work; the movie: “Trading Places” can help understand that.

Go to a lumber store, look at the price of the materials; yes it costs some money, but it doesn’t add up to today’s housing prices. Look at the price of hookup, lot improvements, etc. yes some money to pay for a slice of infrastructure. Then take at look at houses “actively” being built in various stages, see anyone there in Any labor condition time. The answer is no for decades, as crews every now and then knock out a few 2 ×4’s with sheetrock (paper with gypsum clay mined out of the ground as is more or less), it’s the next best thing to printing money. Why isn’t there more construction, because the local city father’s have a Theory of Relativity breakthrough in using the land, let’s squeeze down to the stuff owned by [left to the student …]. Take a look at the edges of any non geographic locked city in California, you see worthless dried out land as far as the eye can see. Travel to the Bodie California ghost town, talk to the ranger or read the brochure, town lots in the 1880s were at a high premium because of their “value;” there is nothing out in that semi arid land for tens of miles.

A lot of places have a 20 year plan required between the city and county, where the city asks the county for 20 years worth of land; however, there is no one with any interest in making sure an adequate foresight for the people occurs.

There was some Roman that became a monk. When the Barbarians came he sent his wife and child away. However, when the Barbarians came they only sent a letter asking to purchase a small piece of his estate at what he said he thought was a below market rate (while family fleeing), he sold, found religion, and so his story found its way preserved. The Roman ruling class faced many places where the Barbarians were welcomed as liberators, but the Barbarians had to promise that the population would never again be subject to Roman administration.

A history lesson everyone has read is the problem of high priced food and the starving masses; food inflation is the most regressive inflation tax in human history and the destruction of countless historical civilizations or ruling regimes. Since food, shelter, and clothing inflation goes right to basic human life or death survival throughout recorded history, maybe Jerome Powell should stop his slow roll as it crushes his thatched roof, medieval serfs (this isn’t a Renaissance festival). The new plan of broadcasting FOMC meetings to shift blame focus to the committee is “nice,” but maybe a good look at the committee that has a sizeable portion of members not even nominated by democratically elected government representatives is a story for another day.

I’m in Charlotte. Sweeping new zoning changes took effect on June 1, which completely rejiggered development here, even as development has already been pretty bonkers for years.

For example, SFH .25 acre properties were previously zoned standard R-3 (3 SFH per acre). Under the new zoning (search charlotte UDO), that same .25 acre property can be redeveloped with up to triplexes per 3k, 5k or 10k sqft…..and even quadplex “multi-family affordable housing” structures in some cases where the property is on or close to a city artery. It’s part of the Agenda 2030 sustainable development stuff.

Right as the new zoning rules took effect, the city/county revalued properties which jacked taxes up big time and increased the land values, while keeping or lowering house values. What we are seeing is an inversion of the traditional model of the structure holding the value while the land was relatively low value. That’s ending in areas with older SFH houses on smallish lots. Now, the land is what is becoming valuable but the existing SFH structure not so much. The developers want to demo the old SFH homes and replace with the multi-units instead. The city/county helps the developers accomplish it by raising taxes so high that fixed income elderly who own most of the properties can’t afford the taxes anymore and sell to the developers (ask Cali how this works Prop 215). The permitting process for the new zoning building was allowed to start in April. I expect these same zoning changes have taken effect in many other cities that have a lot of older (1940s-50s-60s) SFH on small lots. THIS is why the new boom in permits and planned builds out of nowhere.

Gotta rack & stack them, take away polluting cars, and feed them bugs.

I’m sure they are doing the same thing with Martha’s vineyard.

Delete Facebook. You’ll thank me later.

I am up near Raleigh.

A minor point, I believe that historically land has been what has maintained its value and the housing stock on it devalues at a somewhat normal rate relative to usage. Obviously, in an area like Raleigh/Charlotte, where growth has been so extreme, that can get inverted for a time.

Back when I was looking into business cycle stuff, I recall a classic book on real estate: Homer Hoyt – One Hundred Years of Land Values in Chicago. It noted that the biggest swings in prices were areas on the periphery with the core areas rising and falling. In Raleigh, at least, that sometimes falls apart when you have changes in neighborhood demographics, but it still is mostly true.

Wolf,

I wonder if the impact of rising interest rates is overstated. One person’s interest expense is another person’s interest income. For something like the dollar debt market, which is largely domestically held, interest payments merely transfer money from one segment of the economy to another, but don’t really lower the total amount of money available to spend (discounting wealth effect from asset prices for now).

That’s why when the Fed slashed rates at the last GFC, asset prices exploded but the economy just sort of limped along: for every debtor that saved some money on interest payments, a saver lost income. Not only that but lots of people started saving even more because, if expected rates of return were now 1-2% you had to save a lot more for retirement than when you can expect 5-10%. So the economy didn’t recover as fast as you would expect.

And maybe the reverse is happening now? Maybe the rising interest rates are dropping money into savers who are happy to spend it. Indeed, maybe we’re in a goldilocks moment: asset prices are still close to record highs (though just starting to turn ) so we’re still seeing wealth effects, *and* savers are getting interest income they weren’t getting before.

Personally, I’m fine with pausing on rate hikes for a month, but Powell really should increase QT. It’s clear the economy can sustain it. And withdrawing excess money will likely have a bigger effect on asset prices that rate hikes have had thus far.

Almost answered your own question…wealth transfer from the poor to the rich, in the style of the early 2010’s. Personally I prefer the rich get richer and poor get richer policies of the late 2010’s.

Printing money doesnt make anyone richer. It makes numbers go up. We are not paying the tab for the “everyone is richer” policies of the late 10s, and really the early 10s too. Little difference

Correction to my (pj) comment above: It’s not Cali Prop 215. That’s medical mj. I can’t find the prop number offhand but same plan was done in San Fran and other CA cities years ago. It’s happening in other cities now.

A genius is a person who knows when to stop : Sam Zell.

Is it better to be with the geniuses or the manipulators?

G

“A genius is someone who refuses to learn anything new, otherwise they couldn’t call themselves a genius” : Harry Truman

LIHTC under IRC Section 42 is becoming a significant factor in some regions

And it is about 99% multi-residential in the program (an estimate)

The “Era of Great Deficits” will be paying for the subsidy for decades

PS: First post…keep up the good work at WolfStreet

I thought everyone was just going to live in a Sprinter van. Wonder how the RV industry is doing these days.

It is a real thing. I have a female friend that lost her significant other to cancer.

She had some health issues and fell out of the middle class and is out in a Van.

She paid a pretty big fee for a campground membership and stays free at member campgrounds usually a week at a time. Too early to say if its going to be a fling or permanent. I think she is tying to make it on roughly $1500 / month.

There are those who travel in a customized van to experience an exceptionally high quality of life, and those who do it out of necessity. Their impact on the housing sector is mixed because many of them rent or own a place…sometimes where they live most of the year.

One of my brothers just finished a 2 year tour of the US in a fifth wheel camper. He and his wife had just retired. Something he always wanted to do. At a lot of the less prestigious and non-chain RV parks, there are full time residents living in units that cannot move on their own power. They are one step above homeless, and a growing factor.

Interestingly, the rv industry cycle is in a trough. Surprised me too.

In my area lots of people leaped in and bought an RV for travel during Covid. After a few years a good number of those will be realizing they aren’t really into RVing now the old travel options have returned and will be looking to unload the gas-guzzling albatross in their driveway.

Mike G,

Winnebago reported today that it agrees with you. Sales plunged as people returned to their old habits of traveling. And unloading a used RV is tough, and those unwanted driveway-clogging two-year old RVs are now competing with new RVs. This was like the most predictable turn of events ever.

The American people did really stupid things over the past 2-3 years. Bought RVs and pelotons that they could have foreseen they wouldn’t want in a year or two, buying houses at 50% more than they’re worth, and so forth.

I blame the American people for this inflation, for having 0 self control.

Mike G. I agree and really appreciate those kinds of people. Rving and boating go hand in hand. Love the the deals I’ve gotten on used boats and rvs. Most people buy these things without really thinking about it first……..

From a lifelong boat and rv owner……

In Mar 2020 the Fed raided in “other” people money, creating a money

tsunami. RRP is under $2T for the first time since June 2022.

As usual, in every historical chart here the time period of 2021-2023 is best mimicked by 2006-2008, albeit at varying levels. Most pundits in 2008 predicted no recession. Well history isn’t perfect but it’s wise not to bet against it. Look around, how is real estate doing in your neck of the woods? In ours, the rich are doing fine and everyone else is hunkering down or suffering. Yep that happened in 2008-2009 as well.

Note that student loan forbearance ends soon and that will play a much bigger role than commonly estimated.

In China they also had a boom in “multi-family construction”, all created by gubment incentives and Programs paid for with debt.

Some of it in the middle of the mongolian desert. Did Wonders to their GDP. But, as a famous Economist would put it, lt was – temporary.

What was that Beatles Song? Oh yeah – i’m back in the USSA.

Not a lot of apartment towers going up in the Mojave desert. So somehow the US government is not doing a very good job, compared to China, LOL

I don’t have much faith housing starts as a bellwether for the economy. Builders continue to put up buildings long after the economy has turned sour and no buyers are in sight. Part of this is the long term nature of the process. However, when there are stalled-out subdivisions and projects sitting unsold in a down market, the builders are still responding favorably to surveys about “builder sentiment”. It’s probably caused by too much nose candy.

Modi yoga Iran kuba.

Translation please …………

Glad to see multifamily housing having it’s day in the sun again since single family housing has basically destroyed America’s landscape and social fabric with it’s car dependency. This senseless personal automobile centricity taxes people to the tune of $10K to 15K annually for the right to sit in gridlock on America’s streets and freeways.

Single family has never been the problem. Doubling our population in 60 years against the will of the people was the problem.

The population doubled against the will of the people?

Say what?

The government forced people into having sex and producing babies?

MW: Federal Reserve Chairman Jerome Powell tells Congress to expect higher interest rates this year…

CNBC: Federal Reserve Chairman Jerome Powell expects more rate hikes ahead as inflation fight ‘has long way to go’…

But the dude Powell Paused even though the raging inflation ( per WR ) signs are everywhere :-)

The 12 member FOMC makes all policy decisions at the Federal Reserve by consensus, and none are made exclusively by the Federal Reserve Chairman.

If the inflation goal is 2%, why has inflation been several points above that for two years now?

Why are assets on the Fed’s balance sheet near all-time highs and trending up, despite recent slight decreases? Why has the Fed monetized federal debt (i.e. printing money), which clearly leads to inflation? Why did the Fed purchase home mortgages , which elevated home prices 300% in many regions this past decade and shut out future generations?

The Federal Reserve did not purchase any ‘home mortgages’ ever and only holds some MBS instruments and that has nothing to do whatsoever with the prices of housing in the US. Moreover, the Federal Reserve did not ‘monetize’ any federal debt.

You betcha.

FED Reserve is up to its eyeballs in accountability for creating the context for many asset bubbles (QE, ZIRP. Bueller? Bueller?) including housing.

You are joking, correct?

MBS are packs of mortgages. Do we need to enroll you in finance 101?

Cmon now! We all know gov’t was hands off when it came to subprime housing loans!

/s

MBS instruments are mortgage backed securities with the operative word being SECURITIES and they are not mortgages and it doesn’t matter a hoot who owns them and the Federal Reserve is winding down any holdings in them. All MBS instruments only involved fully-conforming plain-vanilla standard conforming mortgages in any event and are self-liquidating.

You think a security consisting of a bunch of mortgages is materially different than owning mortgages directly.

Don’t be ridiculous.

I have a bag of sheat to sell you. Don’t worry, its not sheat, it’s a bag.

Read up on the Great Recession, then get back to me.

‘Big multifamily projects have long lead times, and planning for these buildings whose units show up in the May data started quite a while ago – with big projects, years ago.’

This is an example of momentum in the economy. The economy, like a Very Large Crude Carrier can’t stop on a dime, or for the latter in much less than a mile.

At the ultra-inflated prices of developable land, there was really no such thing as ‘holding property’ even before interest rates took off. Once you’ve closed on the land, pretty much the only alternative is to proceed. Or find a bigger fool, probably still taking a loss.

As the quote from WR indicates, the commitment to the project may have occurred 2-3 years ago, when it seemed like a good idea. It can’t be turned off just because the outfit wouldn’t make the same commitment today.

It would be interesting to know how many condo projects are going to be offered as rentals.

Bitcoin is now up 10% in a few days. There is still way too much speculation and other non-productive uses of capital. Until we have a recession, that isn’t changing, and until that changes, inflation isn’t going anywhere.

what all matter is: Liquidity. Liquidity trumps all: valuation, fundamentals, macro etc.

Too much money sloshing around.

Only way is to hike more and do more QT but FED has failed here in our eyes on purpose as FED works for the elite. From FED’s perspective, they have succeeded as they have hawkish tone but dovish actions.

FED is not making any mistake, they are doing this on purpose.

100% agreed. I don’t support removing all $4 trillion all at once, but they could certainly be going much faster than they are.

And just what would that do? You do realize that the US economy is a $22 trillion a year GDP economy with hundreds of trillions of dollars in assets, don’t you? Just how do you expect the economy to function if the Federal Reserve balance sheet would shrink to a miniscule tiny fraction of that?

Or was it US dollars down? 😉

The o/n RRP was under $2T yesterday and last week for first time in over a year and down like $250bb from more recent levels. That’s a lot of money moving out and it has to go somewhere either directly or indirectly…Still $2T sitting around in there is a ton of dry powder.

RRPs are back over $2 trillion today.

RRPs are to money market funds what reserves are to banks. And there is a flow of cash from bank deposits (because banks don’t want to pay enough interest) to money market funds, and money market funds put some of the cash in RRPs, rather than buy Treasury bills. So you see reserves decline and RRPs rise, and we have seen that. Since Dec 2021, reserves have dropped by about $1 trillion. You really have to look at them combined.

So I guess this means housing prices are gonna start going up again in Long Island. They came down a slight amount and hovered there for a while, was hoping they’d go down more.

Since my neighbors sold out to the Asians from flushing more than a month ago, I’ve only seen the new people 2 times. No furniture has been moved in yet.

Is it me, or does it take over a month to move your stuff in? Or is there an ulterior motive (planning to rent it)….it’s one middle aged lady and her two 80yr old parents walking with canes. They just had a contractor in the other day for an estimate to close in the basement. Not sure why you’d need a finished basement when you have 3 people living in a 5 bedroom/ 3 bathroom home.

If I see them putting a separate entrance on the back/side of the home I have a bad feeling about what’s going to happen. A friend of mine who’s family owned several apartment buildings in Flushing told me they had to deal with them subletting the apartments out and overcrowding them with 4-8 illegals per room. It wasn’t uncommon to go in, open the door and then find a locked door immediately behind it.

One breaking that door open he’d find mattresses and belonging strewed out on the floor. ICE would come in and check papers or deport (before we became a sanctuary city) and the owner would get fined, but it would then happen all over again.

Don’t need that nonsense on my deadend block.

A dollar bill which turns over 5 times can do the same “work” as one five dollar bill that turns over only once.