Bond yields jump as they begin to price in more BOE rate hikes, and higher for longer than previously imagined.

By Wolf Richter for WOLF STREET.

Inflation is infamous for its head-fakes and has a tendency to dish out one nasty surprise after another – at least for observers that keep expecting that inflation will somehow go down on its own. Today, the inflation shocker occurred in the UK. And this is a warning for all economies: inflation has gotten solidly entrenched in services, and is getting even worse.

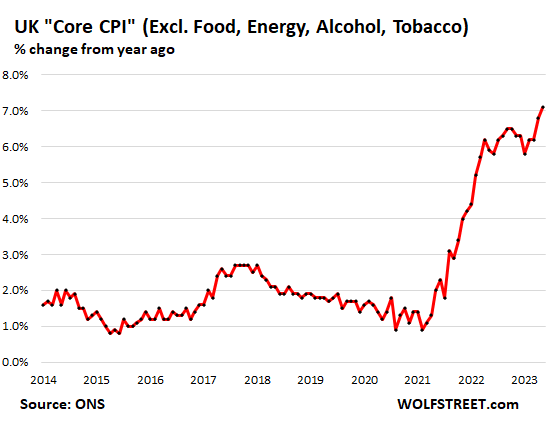

Core CPI spiked month-to-month by a scary 0.8% in May, which translates into an annualized spike of 10%, according to data from the UK Office of National Statistics (ONS) today.

Year-over-year, core CPI spiked by 7.1%, the worst since March 1992. Core CPI excludes energy, food, alcohol, and tobacco. It has now left in the dust the false-hope declines that started in November.

| Major Components, Core CPI | MoM | YoY |

| Clothing, footwear | 1.3% | 7.0% |

| Housing, household services | 0.3% | 7.3% |

| Furniture and household goods | 1.1% | 7.5% |

| Health | 0.6% | 8.5% |

| Transport | 0.3% | 1.3% |

| Communication | 0.9% | 9.0% |

| Recreation and culture | 0.7% | 6.8% |

| Education | 0.0% | 3.2% |

| Restaurants and hotels | 1.0% | 10.3% |

| New and used vehicles | 0.5% | 4.2% |

| Miscellaneous goods & services | 0.6% | 6.7% |

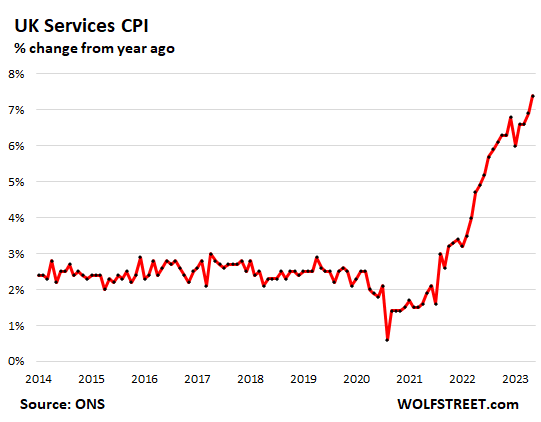

Services CPI spiked by 0.8% in May from April (10% annualized) powered by the spikes in routine maintenance +1.2%, transportation services +3.3%, including air fares +20%, recreational and cultural services +1.1%, insurance +1.1%.

Housing and household services rose “only” 0.3% for the month (but was up 7.3% year-over-year).

Year-over-year, the service CPI spiked by 7.4% in May. Inflation in services is notoriously hard to stamp out. And it’s where all heck has now broken loose – in what is a global phenomenon.

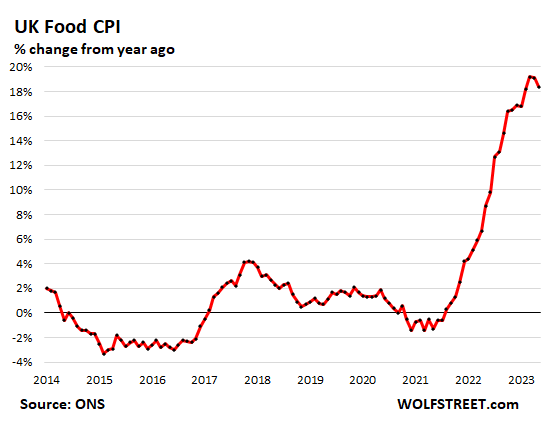

Food inflation rages at a slightly less horrible pace. The CPI for food and non-alcoholic beverages spiked by 0.9% in May from April (11% annualized), which is terrible, but it’s less terrible than in prior months. Bread and cereal: +0.8%; fish +1.8%; oils and fats +0.9%; vegetables +2.1%; sugar, jam, syrups, chocolate, and confectionary +1.7%; mineral water 1.1%.

But coffee, tea, and cocoa fell 1.6% month-to-month; fruit and meat rose “only” 0.4%; and milk, cheese, and eggs rose “only” 0.5% (that’s still 6.2% annualized).

Year-over-year, the CPI for food soared by 18.4% in May, and while horrible, it was down from 19.1% in April and from 19.2% in March, the worst since 1977, according to the ONS’s “indicative modelled estimates” (its actual CPI data don’t go back that far).

But don’t blame Brexit for food inflation: there are countries in Europe with worse food inflation, including 34% in Hungary. In Germany, which didn’t have a Dexit or whatever, food inflation was 14.9% in May.

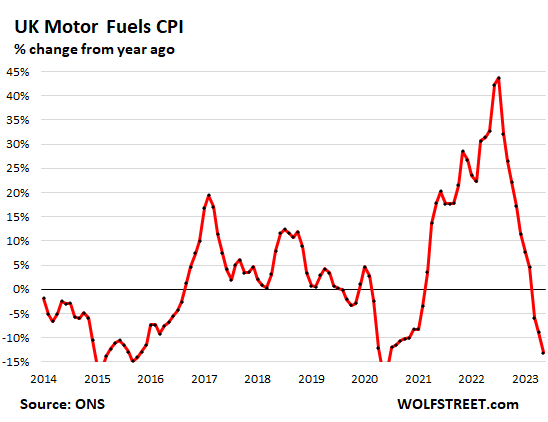

But motor fuel prices plunged by 13.1% year-over-year, after having spiked by as much as 44% last summer.

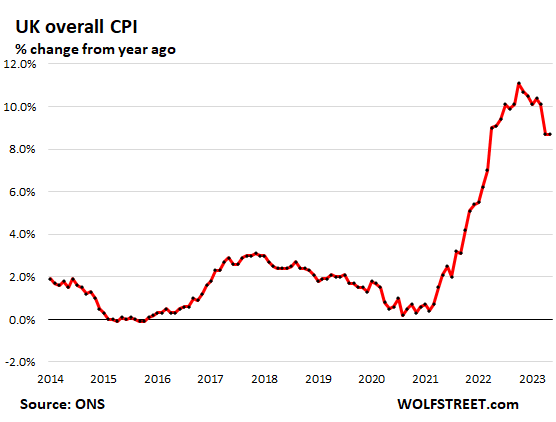

Overall CPI jumped 8.7% in May year-over-year, same as in April, and by 0.7% month-over-month (8.7% annualized), despite the plunge in motor fuels. Overall inflation had peaked at 11.1% in October.

This is the case everywhere globally: Plunging energy costs have pulled down overall inflation indices, even as the indices for underlying inflation, such as core CPI and services CPI, continue to rage near or at multi-decade worst levels. This scenario is now playing out wonderfully in the US and in the Eurozone:

But don’t blame Brexit for inflation in the UK: there are 10 countries in continental Europe with worse overall CPI inflation:

| Austria | 8.8% |

| Romania | 9.6% |

| Lithuania | 10.7% |

| Serbia | 10.7% |

| Estonia | 11.2% |

| Latvia | 12.3% |

| Slovakia | 12.3% |

| Czechia | 12.5% |

| Poland | 12.5% |

| Hungary | 21.9% |

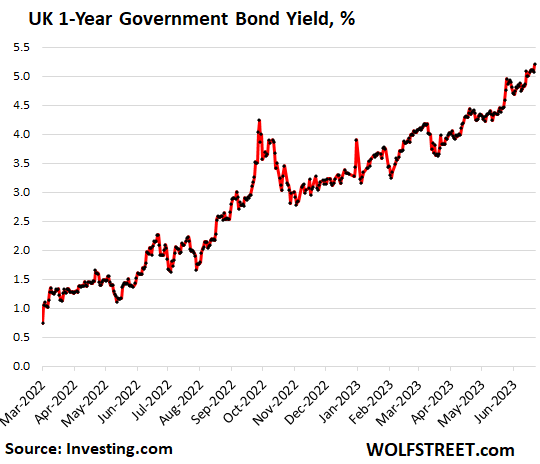

The one-year UK government bond yield, in reaction to the inflation news, rose by 12 basis points to 5.20%, the highest since 2008, as it begins to price in higher BOE policy rates than previously expected:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Don ‘t You Sleep? HEE HEE

THANKS AGAIN SIR

We ‘Big Like’ and appreciate you Wolf… consider taking two weeks and just relax- hate to lose you to burnout.

No go. I have the WORST BOSS EVER. Won’t let me, LOL

Why is bitcoin jumping despite harsh QT words from J Pow?

Is it because:

1. People lost trust on pounds and euro and now consider them to be in same league as Bitcoin crap?

2. People lost trust on J Pow’s Jawboning and focus more on excess liquidity?

3. People expecting Pivot soon and think J Pow has lost it.

4. Bitcoin is just inflating like everything else.

5. Bitcoin was also blessed by AI like Nasdaq.

What would you say if home prices were down 55% from a couple of years ago???

Bitcoin is STILL down 55%, despite the recent bounce.

It’s interesting that the cryptos rocketed higher while precious metals were destroyed. The dollar was down sharply but it didn’t help the gold bugs.

Escierto,

Can you do me a favor and change your screen name to something else for the next five comments. Some internet-based firewall seems to tag your comments as “spam.” After I see those five comments, and it works, I’ll let you know how we might proceed. Thanks.

Firewalls frequently have trouble with anything that might be true.

No because of fedcoin.

Motor fuel may be cheaper but home heating costs are not.

Britain was once ruled by Kings and queens, so screwing the working class is acceptable from cultural angle.

US was born free. Still people tolerating high inflation now!

Leo, I think you need to re-read US history a little to get that “cultural angle” straight, so to speak.

The union movement began in England, and England granted concessions to its working class before the United States even HAD a real working class (we industrialized later), so I have no idea what you are talking about. Maybe go read about the “robber baron” era in US history, as well as worker accounts of working conditions during the height of our industrialization process, before making assertions that we ‘Muricans don’t screw over the working class just as much as any industrialized nation.

Zari – fourple-check. Dismayed to find these aspects of our history no longer appear to be seriously-taught at my grandchildren’s high school (did my part, subsequently…).

may we all find a better day.

My heating ( gas and electricity) is dropping 17% from July 1st,(for now) here in sunny England

Thank You WR. You have been awesomely productive with these articles coming out so fast and frequent.

Looks like neither BoE nor FED subscribe to the idea that inflation is raging else they would have been more aggressive.

The FED probably knows, and getting to Ludicrous Speed (hikes) takes time.

Not in a BMW 540i V8!

old woman car

They subscribe to inflation is raging, at least in the US.

The problem they have is that they think the economy is fragile and doing 1% raises 8 times in a year will crash it spectacularly. And it won’t crash now but in a years time. That is the main reason behind both the 0.25% increments and the pauses from time to time. It is to both get the economy used to higher rates (even if that blunts the effect of the higher rates on inflation somewhat) and to gauge if the raises in the past have been enough. They are rather afraid to overshoot it seems.

The UK though is between a rock and a hard place. Backfiring sanctions on Russia compounding the problems of Brexit on one side and the effects of an easy money policy on the other. The UK won’t get out of this without a recession and maybe even dip their toes in a depression.

From my very basic understanding, the UK is a financialized economy. Little resources is easy to see. Relatively little manufacturing. So they export intellectual property and financing tools. Not great in this global economy.

Inflation in America only affects most people who overpaid for things. Like cars,boats homes .I am getting groceries on sale cheap .But if u are like my kids and order online =OUCH. To lazy to buy sales .Also feel sorry for poor folks so give to FOOD bank monthly,I wish more would help,if you have the means . It makes you feel good

They don’t believe in being aggressive. Except on the way up.

Today BOЕ raised the interest rate by 0.50 b.p. up to 5 percent. More hikes are looming. Markets are forecasting up to 6 percent by the end of this year

To a certain extent, comparing the M2M to Y2Y changes, we might be seeing a real time example of “rolling” inflation – first a few, key, heavily weighted subsectors go nuts (housing, fuel, med) then, with a lag, lesser weighted subsectors (restaurants, clothing, furniture, etc) attempt to pass their own costs on with a lag (their employees have to pay for housing, fuel, med).

But those lagging inflators are more optional/have more alternatives – so lagging inflation might not “take”…unless a lot of businesses in these sectors fail due to lack of transactions at inflated prices.

Either way it is bad/disruptive – that is why printed-money driven inflation is an economic cancer.

But Pols always prefer systemic fraud (printing) to painful honesty (ie, “we can’t start/continue this goodie I buy votes with”).

This services inflation is a symptom of the inflation problem, not a cause, just people trying to regain their purchasing power from the fundamental problem.

The concept of the Politicians spending too much causing inflation is a half truth. Most expenditures are essentially fixed, i.e., non-discretionary.

The revenue side of the equation is the other half. In this country the tax cuts during the Trump administration were only projected to 10 years and were deficit producing significantly in every year.

The concept of tax cut to the rich stimulating growth in the economy; i.e., President Reagan’s “trickle down” has been officially discredited. Interesting that the Trump era’s 2.0 version is not discussed anywhere, just endless looking at the economic symptoms, but never root causation.

The Federal Reserve simply prints worthless money to balance the accounting books. The Federal Reserve knows what it is doing. Just read the Constitution that says money will be gold and silver. Debasing currency happened through recorded history; Rome of 300 AD is most prominent with base metals adulterating the precious metals, then wage and price controls under pain of death that didn’t work. Hyper inflation all over, and it’s results destroying whole nations, best example is Germany’s inflation that directly facilitated the Nazi’s. 10s of millions of people have died as a result of money printing. Here in this country, there are far less deaths, but an incredible amount of permanently destroyed families.

Bottom line is the Oligarchs/family equity funds, anti-trust size equity funds are going to have to pay more taxes.

Are you serious? The Federal government doesn’t have a revenue problem, revenue has increased significantly even with lower tax rates, not just with the cuts in the 80s and 2017, but also with the Kennedy cuts in the early 60s that people of your ilk seem to want to forget. When tax rates become confiscatory, like combined Federal and State near 50%, people figure out ways to avoid or delay earnings, raising taxes on the wealthy isn’t going to work, and the taxes will “trickle down”, to use your term, to the middle class, which is where the real money is for tax mongers like you. Remember, when the Federal income tax started, it only applied to a few thousand people, now between income, social security, and Medicare taxes, the middle class pays way more than Elon.

And your assertion that entitlement spending is somehow static is BS. We have massive increases in that spending because the population is aging, and benefits that apply at age 65 were one thing when life expectancy was 67 and completely another now that it is 77.

And both parties continue to increase spending at an alarming rate, there has been a 20% increase in Federal spending since 2020 for no similar increase in population.

And one party thinks we need to expand Medicare and Medicaid even more, plus forgive all student debt, pay reparations the ancestors of slaves, subsidize green fantasy electricity, and generally have the public sector eat the economy.

That’s the real problem.

Hit the nail on the head with one caveat. The tax cuts of 2017 were not really tax cuts for the wealthy as it removed the ability to deduct state, local and property taxes for anything more then 10k and increased the standard deduction making the mortgage interest tax deduction almost useless. The upper middle class and the wealthy actually saw a net increase in taxes in high tax blue states. The middle class saw meaningful tax cuts with the increased standard deduction, especially in states where home prices are low so they never were taking advantage of the mortgage interest deduction. Corporate tax revenues didnt drop and have actually increased.

I think Fed has unleased a monster that they will have a tough time taming which gets multiplied around the world. Just heard that Warren Buffett has given away to charity 5% of Berkshire shares each year for about 15 years, but he is a lot wealthier than when he started. That money went from an asset sell to being spent out in the real world each year.

The risks in the system are unknowable as the Fed tries to press on the brakes. Biggest problem in my mind is Fed has got everyone trained including politicians to easy money recency bias. If the US stock market falls to even median long term valuation metrics so many things including pensions would be insolvent.

Stock market is most over valued compared to t-bills in a very long time.

MW: ‘Take-under’ deal for Silicon Valley Bank fuels $9.5 billion profit for First Citizens Bancshares

MW: Fed chair says ‘it will be appropriate to raise interest rates somewhat further.’ 10 CDs and savings accounts paying more than 5% APY.

BoE balance sheet reduction has been anemic. I don’t see how the developed world is going to stop inflation without either destroying a lot of money or allowing inflation to rip until currencies find their new normal valued against larger money supplies. Following an era of global QE, I have to question if rate hikes will have the intended effect. They don’t seem to be cutting it. Rate hikes may beat up the spending power of heavily debt-dependent people or industries and blow up some weaker banks, but they also drive up interest income. And as many WS articles have pointed out, people and institutions that benefit from that income are out there spending generously (almost as if their currency is going out of style). I still hold that interest rate hikes are just a diversion… If central banks were serious about inflation, rate hikes would only be a small part of the news. Aggressive QT would be the gorilla in the room, not the background afterthought. Inflation was the goal all along. Rate hikes back to just their historically normal levels aren’t doing much for the BoE just like they’re not doing much for the Fed.

The USA has fixed term, Canada and the UK have short fixes.

The USA can stay higher for longer without it feeding through into a housing implosion.

The UK and Canada have to match the USA rate. But they can’t write a blank cheque for housing because their currencies are too small.

Canada and the UK authorities made a huge mistake in heading down the rentier path. They didn’t understand the dynamics and now it’s too late to avoid a disorderly repricing. They will try to avoid it using insanely high levels of immigration, further moving the Overton window to the right. It won’t work.

Buckle up.

Mr. Wolf Richter,

Would it be possible to publish China’s CPI?

Thank you for all your research!

I no longer do China stuff. Don’t really feel like it — unless there’s something big and interesting happening.

In terms of detailed inflation coverage, I do US, Eurozone, UK, and Japan. And that’s enough.

Living in the U.K. I feel that a large part of the problem the BoE has now is massive wealth and income inequality. By all accounts, skilled workers in London are making out like bandits, with big pay rises and bonuses. If anyone bought a house in the last few years and is on a 1.5% fixed rate, they are swimming in cash with 10-20% pay rises for the last couple of years plus covid savings blitzing the value of their debt.

Those in the public sector or in less desirable jobs are getting hammered, but many have cheap mortgage fixes as well so are still managing.

But the considerable number of workers with no capital (mostly they don’t own a house, or much of one) are being absolutely crushed. But they didn’t have much to spend anyway so crushing them is not really reducing inflation.

The BoE will have to absolutely destroy these people to start hurting the cashed up Londoners and wealthy who are driving inflation. Politically this is going to cause huge problems aka to the regional voter backlash that caused Brexit.

I expect the BoE will have to let inflation rip, and will just hope that the fed fixes global inflationary pressures so that this feeds into the U.K. economy.

Just to add, in the last few days politicians have been calling for a mortgage assistance fund, and today there has been talk of bringing back tax deductibility for mortgage interest to help struggling households.

Similarly there are prominent political commenters pushing the idea that high interest rates are causing the inflation (um…ok) and a recent survey showed that your average voter thinks 5% inflation means prices stop rising.

It’s becoming economics looney land over here. And we have an election in a year…

What happened to that Brexit bump they were expecting?

The ‘bump’ turned into a hump!!!

“…there are prominent political commenters pushing the idea that high interest rates are causing the inflation…”

Yeah right. There is a guy in Turkey called Erdogan who says the same thing. He forces the central bank to lower interest rates to combat inflation.

Look at their latest figures to see how that is working out.

Interest rates are inflationary in the sense that interests causes monetary inflation as they inflate the amount of money they work on. Quite obvious when you look at the math of interests.

Now, the copling between monetary inflation and “inflation” measured by consumer price index is not a straight one to one.

Neither is there a strong coupling between interest rates and monetary inflation. High interest rates may discurage credit expansion, that is monetary inflation, but it do by itself slow credit expansion.

Switch to serial number accounting and fix the amount of money, in other words use bitcoin technology and you would have zero interest rates and no monetary inflation. CPI “inflation would then by time go towards zero.

Would never happen as all governmnets could then not spend more than they could tax. And all trade between countries would have to balance over time.

In the case of Turkey, they probably have high inflation due to high monetary inflation and trade imbalance. High or low interst rates do not necessary change this.

Turkey raised one of it’s central bank rates from 8.5% to 15% today JO!

Surely Erdogan knows what it takes to ”win” an election, eh?

Erdogan backtracked. The central bank of Turkey hiked today by 650 basis points, not a typo, LOL, to 15%, nearly doubling the rate.

Excellent on the ground comments. Thank you.

I think the UK is in big, big trouble. They don’t have any energy supply left (North Sea), they don’t make anything much worth exporting. Their main source of wealth (much like the US) has been exporting their currency.

It’s no small surprise that the UK is THE most vocal and active supporter of Ukraine and against Russia. Besides the historical hatred, they know that their ship will sink should international money flows change as some expect.

The UK is in massive trouble because the population see the following as *identical* in worth b/c both make the same profit:

1. property speculator buys a house, does zero renovation, sells it for a 20% profit of 200k

2. entrepreneur starts a business employing 5 people in manufacturing, first year profit 200k

The UK has disappeared up its own backside, nothing relates to barrels of oil, trade deficits are just numbers that mean nothing, national debt means nothing, everything is about gaming the system to get the numbers so you can afford to eat out regularly. People believe that at scale this isn’t a problem.

“2. entrepreneur starts a business employing 5 people in manufacturing, first year profit 200k”

That’s the best-case scenario. Normally, in a manufacturing company during the first year, as you ramp up production, and sales have yet to take off, you’re facing large losses.

I don’t think there is any historical hatred of Russia in the U.K. There is a realisation that the failure to stand up to aggression means paying a higher price later. We have a large population of Eastern Europeans living here and they understand this and no doubt add to the political pressure to do more.

“I expect the BoE will have to let inflation rip, and will just hope that the fed fixes global inflationary pressures so that this feeds into the U.K. economy.”

That’d be pretty worrisome if Mr. Richter’s other assertion is true in that the FED will allow inflation to stay elevated for some time in order to devalue US national debt. Living in Canada we are dealing with slightly lower inflation levels than Europe but it’s not a given that we won’t see big spikes down the line. Regardless, my raises from a year ago don’t look like they’ll continue so an extended period of inflation means my butt’s squarely on the chopping block now. Silver lining may be the fact I’ve been bracing for it for a while thanks to the info on wolfstreet, significantly reduced my spending over the past year and am looking to do more to boost savings, we’ll see how I come out the other end of this.

You are ready, but good luck. As some say here, may we all face better days.

BoE or FED won’t do anything that would hurt wealthy.

I enjoy watching a guy on youtube who lives in London and loves all things cars and motorcycles. Travels a lot all around UK and EU and details out costs comparing to UK prices. He does a great job producing the videos. Name is Freddie Dobbs.

Thanks for the Freddie Dobbs heads-up, ‘old school.’

I tuned in to his review of the Triumph Thruxton RS motorbike, and it is a beauty of a machine. Freddie talks about the combination of art and performance, and he’s so right. Well engineered and fast machines are almost always as beautiful to look at as they are to use.

He is a really good enthusiastic presenter. He did about a 6 month stay in the Canary islands, which I was totally ignorant of. If you like his style you will have many hours of joy ahead.

Apparently the BOE is not thinking of letting inflation run its course.

0.5 bp today.

MW: Wait for T-bills to cheapen (as yields soar upwards) as Treasury keeps up issuance deluge, says BofA Global

I believe I know two things about the US stock market if you are not a short term trader.

1. Stock market is priced about 2X – 3X too high based on price to sales, market cap to GDP, value of the dividends or simple regression to the mean analysis.

2. When inflation broke out in the seventies stocks and bonds got killed, but t-bills allowed you to keep up with inflation til inflation finally got crushed.

I have been wrong so long I am due for the stopped clock confirmation that I am a genius.

In all seriousness, I am too old to take a

lot of stock market risk.

Politicians spend too much and then leave it up to the central bank to be the bad cop. UK politicians spending $130 billion pounds that they don’t have.

When all of this is over I am not sure central banks will be allowed to operate with such freedom of monetary policy as politicians have proven you can’t give them easy money and expect responsible behaviour.

The problem is: CBs are not independent, but are part of Govt.

If CBs are independent and care about fiscal responsibility then they won’t keep rates low to enable govts take more and more debt.

In essence, Govt and CBs all work for wealthy people.

Yes yes yes

This is the most underrated opinion imo. Central banks including the Fed are foremost a government agency. I know I know the whole ‘private’ thing and constitution and all that, but if it quacks like a duck…..

This is very true. Congress has almost unlimited power to tax and central banks have almost unlimited power to devalue, but in reality they need the system to be fair enough that most of us want to participate in the financial system.

The individual’s main power is to order our affairs in our own interest according to our understanding of what is going on and to be nimble. If the situation gets oppressive enough it becomes in the individual’s interest to use gray markets and black markets and to not participate in the banking system. Hopefully we don’t get there.

We live under capitalism. Money supply is *everything*.

We “vote” each and every day on the survival of all enterprises by spending money. Our collective “votes” really do decide who stays and who goes.

Contrast that with democracy. We vote once every four years. Politicians lie about what they will do and omit what they will actually do. They are swayed by the rich. Our vote changes very little, if anything.

In spite of the lack of power of our vote, it’s still something. To cede control of the biggest lever (monetary policy) to a completely unelected set of officials was nuts. The sooner we have central banks back under democratic control the better.

The idea that central banks would take the hard decisions has been proven to be totally wrong. They’ve taken the easy decision for over 15 years.

Wolf quote — “Removing liquidity out of the overleveraged financial system is already blowing up all kinds of stuff. This MUST BE a reasonably slow process if you don’t want the financial system to collapse. .. What’s wrong with having many years of slow methodical liquidity withdrawal and higher interest rates and no financial-system collapse?”

We are already 2 years into High Inflation — the last time annual CPI below 2%, is March 2021. And not mentioning all the bubbles — House Price runaway, SPX now is close to all time high.

All because Powell dragging his feet in fighting inflation, and mostly making lip service, while pretending like a Virgin not understanding why Inflation is persistent when we are still having Negative Real Interest Rate.

And you nodded that he is a Virgin. lol. And a real good virgin.

Every time Fed prints money, I am the loser as I work hard and saved diligently. All my savings is now close to worthless. I am preparing to leverage to buy rental properties soon, all thanks to Fed relentless printing when GDP was growing 10+ % in 2021 and unemployment was historical low in 2022.

Soon, I would tell my kids no need to work hard, no need of inspiration to study Science Engineering to solve problems. Just max leverage buy 1 rental property a year, and Fed would make them all rich by year 10.

All around me, max leverage people get their ass saved and become richer. Only in America, when recession happen, that Housing Price up 50% and SPX up 100%, because USD is world reserve currency. This is the same path like all historical super power that went down hill — people discovered FREE Money!

All in the name of “Stability”, such that Investment world becomes a Heaven without Hell/Punishment. And Thanks to minions like you who praise Fed even when they are doing the wrong thing — Still Promoting Negative Real Interest Rate during Raging Inflation today.

Perhaps, instead of complaining about the heat of the sun and hoping that this will make it change its immoral ways, you should go out there, get a beer, grow a tan, partake, enjoy it. While that flow of money is still there, even for you.

PS:

I told my kids to study science/IT in order for them to *not* work hard.

Forgot to mention another reason why I am angry — By the way how Fed fight inflation, by Year 2025 if Inflation does come down to 2%, all items prices would be like 50% more than Year 2020 before Pandemic.

In other words, my savings is becoming useless. And all the max leverage idiots are becoming Gods that walk on water.

Thanks to Powell still promoting Negative Interest Rate during raging inflation today. And Thanks to those minions who keep praising him for doing it.

I understand your anger…

But I’m urging you to shop around if you aren’t now getting at least 5% on your savings. Treasury bills pay 5.3%+; Brokered CDs are in the same range. Money market funds are at around 5%.

If you’re still getting 0.2% or whatever, yank your money out of your bank, for crying out loud.

How to shop now when the prices of all assets are so inflated that it is more profitable to keep saving and hope that at some point something will break!?

Seriously getting 0.2% to 2% at one bank beats getting 5% (+ these days) at another bank (do note that you cannot access this money until the certificate matures)? What kind of twisted logic is that.

As for assets US treasury bills are the safest asset in the world for roughly the next two years, they don’t do asset inflation either and you can pretty much dial in the period you want to park your money.

Something similar goes on with money market funds. These invest in short term debt, cash (or equivalents). Usually only the stuff that has an A or higher rating (maybe BBB and higher for BBB is still considered investment grade) thus safe. And none of it is subject to asset inflation.

Wolf gave 3 very safe options to park money, all 3 with short to medium term periods where the money invested is unavailable that would give at several percent more of a return on money then the 0.2% Wolf used or the 2%, 3% my bank offers for medium term money parking.

It is as you say.

Maybe I didn’t specify that I’m not American and I don’t live in the US. Also, I have no idea how or if I could invest in US stocks. Banks do not offer such services here.

Yep,

Take your money out! I told Wells Fargo to go pound sand with their .0000000000001% interest rates on savings.

WF is offering 4.5% seven-month CDs to existing customers now. Even they got religion. Too much cash fleeing.

Just checked the current rates

3month Treasuries 5.28

6month Treasuries 5.40

9 month Treasuries 5.34

1year Treasuries 5.32

18 month. Treasuries 5.18

And interest on Treasuries is exempt from state tax

Even JP Morgan is offering 1 year brokered CDs that yield 5.50.

I would guess that those low cost deposits at banks are going to be a thing of the past by the end of the year as banks are forced to

raise their interest rates to avoid hemorrhaging deposits .

Sean,

If you have $3000 you can get a Vanguard m/m paying 5.03%.

My parents just got a 5 year FDIC CD through Edward Jones Paying 4. 45%. I think Edward Jones. Jones bought the CD from one of the big banks.

Is there still a concern about the UK pension system as yields get higher? I recall last year they nearly got blown up by bond yields that were lower than they currently are now.

If you read between the lines, this is the reason for Boris Johnson being under attack lately.

Sunak will get the same treatment that Truss got and get the boot in whatever manufactured situation needs to be presented to the public to balance out the pensions & GILT conflict and Boris can win elections.

Apparently the plebs need to be crushed into submission and that is how this equation will be balanced out.

That was just politics. The Conservatives chose Liz Truss as leader and the wealthy people who run the UK were not impressed so they ‘encouraged’ a change to their original choice, billionaire Sunak by creating an economic crisis. Once the leader was changed as directed, the crisis magically ended.

MW: Lawrence Lindsey sees Fed continuing rate hikes into 2024, with terminal rate having a ‘6 handle’

Lawrence Lindsey is a good man. Trump should have had him in his administration instead of the morons he hired.

Swamp – think you may have provided your own perfect illustration…

may we all find a better day.

This especially hurts as income per capita in the UK for most jobs pays significantly less than the same job in the US, and wage increases in the UK have been flatter than US wage increases.

Honestly, both USA and UK are gradually descending to being a 3rd world country ( huge wealth inequality, poorer Quality of Life ) but UK is going down faster than USA.

I come to USA 25 years back from a developing/3rd world country and can see the signs from miles away and sad to see these countries going down like this.

A expanding number of people at the bottom seem to see no way in, but a way out: onto the streets. Good intentions plus “easy” answers (printing more scrip, and a public structured on freebies) is worse than I imagined.

Because of technology and size of scale, most industries will be dominated by a few companies. The days of the mom and pop shops are disappearing. This hollows out the middle class as it gets smaller.

10% of the people that leave the middle class move up to the upper class as they are managers, directors, and executives in the monopolistic companies. The other 90% drop down.

Honestly, I buy 80% of my day to day household goods and personal goods, and clothing (not including food) from Amazon and Walmart and Costco. A little sprinkled in at Target. I really do not shop anywhere else.

If I need an Auto part. O’Riley’s Auto Parts.

If I need home maintenance items for myself. Home Depot mostly…sometimes Lowes.

I buy Groceries at Aldi.

I put all transactions into Quicken. 95% of my shopping is concentrated in 6 or 7 stores.

Really, the only thing I buy that is locally owned is restaurant food.

When I make these purchases at these stores I listed above, the profits leave my community and state and go to the headquarters of these companies or stock holders.

Health Care is pretty much the same way. Over the past 20 years I have seen all the mom and pop individually owned Hospitals, Doctor offices, Dental offices, and eye doctors be bought out.

Ru82 you might be interested in Monbiot’s book ‘out of the wreckage’. The thing is that we make these big corps oligopolies by constantly buying from them. There are alternatives, and it is up to us to push for more of them by supporting local stores and small business owners.

I have a simple but very functional ubuntu computer, an old iphone I’m waiting to replace by a linux one, I shop at farmers market and local grocery stores and only fill gaps at the big stores, I grow veggies, go to the local hardware store, ditched my amazon membership and spending much less without it, my doctors are not incorporated, I keep my vehicles and clothing until they become irreparable, I boycot AirBnB, I camp w friends and find local guides rather than waste big bucks in resorts and herd tours, … many ways to counter corporate greed and parasitic fees of all kinds. The only way out of this hole is to take things in our hands through our wallets and votes.

…might also take a gander at John Ruskin…

may we all find a better day.

Hardly shocking. Look at all the money-printing. The only people “shocked” are the ones who are watching their purchasing power disappear at the fastest rate in their lifetime. Central bankers are liars. This inflation is intentional.

Intentional or incompetent, it’s a heck of a problem.

It’s 100% intentional. What they did is the equivalent of a fire captain dousing a forest of dry tinder with an accelerant, lighting a match and burning down the whole forest, then saying “I had no idea it would do that.” Only an absolute fool would buy that.

Fed and other CB rates take the stairs up and the elevator down. This fundamental asymmetry, it is claimed, is to avoid “breaking something”. It is also intended to have inflation run over target periodically; it’s an indirect tax that everyone pays and also reduces debt to GDP ratios. Governments love inflation as long as it doesn’t cost the ruling class its jobs. The fact that target price stability is 200 basis points of inflation annually, rather than 0 basis points, proves the point. Half of the electorate loves free money, and the rich do very well as long as things don’t get out of hand. Those in the private sector middle get squeezed, and eventually become diminished in numbers. The massive Covid giveaways to closely held businesses in the US were an inflationary middle and upper middle class bonanza that is unlikely ever to be repeated.

As I posted before, inflation benefits a lot of people. There is a large inflation lobby out there. It’s basically an income distribution mechanism from the poor and middle class to the rich. The low information masses don’t know this so they believe all the bull s$it from the politicians and corporate shills that enable this massive income redistribution. Its’ not complicated.

What does a person with plenty of liquidity, care about debt and its associated interest, compared to someone depending on credit?

How does this ‘shocker’ effect England’s 14 commonwealths?

At a congressional hearing, Fed Chair Powell analogized the Fed’s approach to interest rate hikes as driving a car from an Interstate Highway onto the roads in a city. The Fed moves fast on the Interstate Highway but slows down as it enters the city. Perhaps Powell thinks inflation is like a pothole.

No worries, potholes are transitory……

Inflation is more like the bad neighborhood where a drug dealer named J-POW! hijacks your car, floors the gas pedal and drives it into a ditch with you in it.

It seems like in the US the government has done 30 years of magic to keep the economy going.

1. Outsource manufacturing

2. Import cheap labor

3. Run up Fed debt to $32T

4. Drop rates to zero for a decade

5. Run up $9T balance sheet

6. Blow 3 stock market bubbles

7. Blow student loan bubble

8. Fight 3 wars

9. Blow 2 housing market bubbles

I think the UK had a similar 25 years with some minor differences. Most of western world went for the same ride. What is next?

More inflation, then perhaps hyperinflation. These guys are high on their own supply.

The difference is that the UK believed in the religion of “free markets”, and “globalisation” and “not picking winners”.

Whereas the US has the financial and the political capacity for being totally hypocritical, providing huge subsidies and other incentives to the picked winners :).

“Next” is that the US will pull strategically important business back home while taking everyone to the cleaners in WTO-arbitration for attempting the same.

The UK goes back to living like in the 1970’s, where it always yearned to be, without the North Sea oil.

You are overestimating how much the US can get out of the WTO. Especially when the US effectively walked away from the WTO while abusing its position to enact petty revenge because the WTO dared to rule against the US. And while that happened under the Trump administration, the Biden administration has kept the Trump era policies in place.

It gets better, that petty revenge? Well the US paralyzed the WTO settlement court so they cannot even start arbitration at the moment.

This really isnt rocket science. Massive central bank balance sheets have blown up asset bubbles. The best way to stop inflation is to sell off those balance sheets much more aggressively. The amount of QT has been hardly noticeable to date. Force the markets to absorb a trillion or two of debt over a couple months and we will start to see a reversion to the mean and that will help to kill inflation.

These central bankers are all just patsies of the rich/financial community.

The earlier they reverse inflation the sooner they can bring interest rates down which is necessary to stop the debt spiral that is raging out of control.

Exceptionally well put. My best guess is that high inflation is tolerable, for those in control. Just my hunch…

Central banks have reason to love inflation. Not only does it erase debts, it allows them more room to artificially stimulate, delaying the ultimate reckoning. For example, with steady inflation at 5%, they can repress ST and LT interest rates to the 0% to 2% range via rate setting and QE, to deal with the next economic burp.

The Fed has shown us it doesn’t care how the chips fall within the population. The Fed stated it takes no responsibility in that area, like a child takes no responsibility to keep her room clean.

So why is core inflations so sticky? I suggest four reasons: 1. rapid and massive increase in interest income, 2. inherited money from the excess mortality of covid, 3. inherited money as baby boomers pass away at a faster pace, 4. pent-up demand unleashing itself after two years of covid lockdowns.

I am sure there are plenty of text-book reasons, but I was trying to think of unusual reasons, since this sticky core inflation seems to have stymied most everybody.

Inflation is sticky because the Gov’t printed a unprecedented amount of money and won’t quit spending it.

The US government does not and cannot ‘print’ any money.

1. Savers don’t magically become spenders. Hence, “rapid and massive increases in interest income” don’t have as much impact as one might think. In our case, some of the funds from those “rapid and massive” increases are going to increased income tax quarterlies and the potential of increased Medicare premiums (both B and D) because we’re now “high income”.

2. Inherited money: Possible, but not likely as prevalent as you might think. I’m still kicking. My kids are independent of me and are all making more due to salary increases and job changes. I’m a “saver” and our spending habits haven’t changed much, if at all.

3. Baby boomers aren’t all wealthy. If you had any experience with dealing with the passing or incapacity of an elderly person, you’d realize that getting your mitts on their money and disposing of assets – even with living trusts avoiding probate – ain’t immediate nor easy. I’d also like to add that, in my experience, many of the skilled nursing facilities and ALF’s are full of Medicaid recipients, not people spending their own nickel. One facility that I checked for my sister has an queue of 83 Medicaid people ahead of her – and she would pay nearly double what the Medicaid tariff is. But they can’t discriminate….

4. Pent up demand. Yes. YOLO and FOMO on steroids. However, I would wait for the student loan moratorium payments to begin again. That might make some difference. That behavior (YOLO/FOMO) will likely end up biting the spenders in the arse as they will be less able to tread water.

1. My expenses are not rising nearly as fast as the interest I am getting. I am not high income. Many well-to-do old people have relatively low income and relatively high net worth. Still, with higher income from, say, windfall interest, they will buy stuff that didn’t buy in the past. Like if they own a house, they will be able to have repairs made that they have put off (note the current high and persistent inflation in services).

2. and 3. Inherited money is an important factor, especially when it’s from an excess mortality event like covid. This is free money to the heirs. I am not talking about people on Medicaid because they by definition will have nothing to give their heirs when they pass away.

4. People have put off much as a result of the covid lockdowns. That dam is bursting.

It takes only a little increase in these categories to increase demand, which drives up inflation. Even just a few people willing to pay more for an item will raise its price. Anecdote: often on Amazon I will put a low-volume item in my cart, and come back the next day and the price has risen, sometimes a lot. I learned not to put anything in my cart until the moment I want to buy it.

2 and 3: The point was that inherited money is not that prevalent that it would drive inflation by the amount that it has. Not everyone has $3M to leave to their kids. Not both parents succumbed in all cases and the survivor gets that coin. The point of the Medicaid comment was to affirm the previous statement. Of course they have nothing to leave…. but here’s more of them than folks that can pay $15K per month for a private skilled nursing room. My DIL is supplementing her near retirement mother’s income because mom can’t afford to pay attention. Her dad is dead. He left bills to be paid. He owned a fairly sizeable commercial plumbing business in Houston. “Assets on paper”. No commercial value without someone to run it. Equipment was leased or buried in debt. Building was leased. Going concern value turned to zero when he passed on.

1. We have hard assets…. plus we have income producing assets…. plus a pension…. plus SS. Doesn’t take much to change your tax bracket nor does it take much to push you into higher Medicare brackets. So the “big windfall” gets clipped unless your dumb enough not to pay attention to the impact and will get smacked later. If you’re spending it, and not considering those realities, you’re gonna get a big surprise in April 2024 and again in November 2024.

Our spending hasn’t changed much, if at all.

Amazon? Use a different device to shop and another to buy. My wife and I – by accident – discovered that their algorithms must adjust prices based on your behavior. Her prices were higher because she always shopped for ladies stuff. I didn’t and got a better price on the same item while sitting next to her in our family room using my non-logged in iPad.

UK has some serious energy problems. They already have some of the lowest energy consumption in the developed world (and not because they all ride bikes everywhere like the Danes or the Dutch, but because they are too poor to afford to consume much energy and because they have next to no industry left.).

As such, it is understandable that inflation will hit them harder than places with a better supply of lower cost energy. Not that that is the only factor, but it really doesn’t help.

…brings to mind the postwar period as depicted by leCarre, wherein cooking/heating gas was coin-metered like a vending machine for many…

may we all find a better day.

When travelling in Germany in the 1970s, I stayed in a few student dorms. To get hot water in a shower, I had to insert one Deutschmark into a device. It gave about five minutes of warm water.

Was even the case in the 1970s …

My prediction is that the British is headed to some kind of societal collapse. There are some places in the UK that are still doing very well, mostly London and a couple of surrounding areas, but everywhere else it’s pretty grim, at least that’s what’s been told to me by some people who visited the country recently for example homelessness is now pretty visible in Bath, a tourist hotspot.

London is doing well because in every other part of the country they do all the work, then in London at the company HQ they book the profits and dish out the bonuses. Then The City cashes out the gains on the share price rise, and goes for a slap up lunch.

Profit taking centralized.

But what happens when the music stops?

…the conclusion of ‘privatize all profit, socialize all risk’?

may we all find a better day.

So true.

Have recently been to both London and Bath, very few homeless in either city, 3 days in London walking 5 to 10 miles a day, less than 10 homeless people, maybe 1 in Bath? I see more people than that on an off ramp tent camp here in suburban Denver.

If things are bad, why does GBPJPY keep rising and my short position keeps worsening? The inflations etc news does not translate to FX, it seems.

It is the opposite. If inflation is getting worse, UK central bank has to increase interest rate higher and keep it high longer. On the other hand JPY has vowed to keep at 0.25%. it works for them as they have capital surplus though trade is in defecit last 1 year. Short yen carry trade against all major Hard currencies is the hedge fund favourite. you also get interest credit if you are Long GBP/short JPY. Economy can go to hell in a handbasket, Interest rate difference matters in forex. japanese central bank threaten to intervene all the time to make the hedgies not to over do short yen trade.

mantra is long GBP short Yen or even USD/JPY

You probably read some article on Interest Rates Differential and how a currency with higher rates will is supposed to lose value? A friend of mine told me once “that’s the kind of BS they teach you in the CFA”. Yeah unfortunately in real life, that’s not how it works.

WSJ June 22, 2023 7:14 am ET “Bank of England Outpaces Peers With Rate Rise of Half Percentage Point”

“The move to raise the lending rate to 5%, its highest level since April 2008, follows smaller rate increases in recent weeks by the European Central Bank, the Bank of Canada and the Reserve Bank of Australia. “

Ha ha

Captain Jrome must feel like $shit today after seeing SNB, Norje and BOE hikes. Proves again Jrome was/is NOT serious at all.

MarketWatch: Peer central banks proves Fed ‘pause’ isn’t contagious

Jrome does not feel anything. He already is minting money and is already worth 100s of millions of dollars.

Common people are the one facing the brunt of his decisions.

But Jrome would do what is best for him and his friends and masters.

O/N RRP volumes dipped below 2 trillion. MMMF rates, T-bills, are now higher than the award rate. That increases liquidity.

ON RRPs moved back over $2 trillion yesterday. We’ll get today’s numbers shortly. I suspect that dip following June 15 was due to quarterly tax payments getting paid as companies/individuals moved some dough out of their money market funds to pay for them. And now money is flowing back into MM funds.

Looks to be below $2T again, but at least TGA is refilling. Today the “Total factors, other than reserve balances, absorbing reserve funds” is up $56bb thanks to TGA offsetting o/n RRP outflows. In total looks like balance sheet changes resulted in liquidity going down nearly $74bb (Reserve balances with Federal Reserve Banks) from the week prior.

The Fed pausing was to help the banks. No other reason.

Then they will HAVE to pause again.

Using “services” as a category is deceptive. Providing a service is not just some guy sitting at a desk writing with a pencil. To provide most any service requires: School and recurring training, licensing, facilities, utilities, banking and credit, insurance, specialized equipment, computers and communications, advertising, and the taxes – county business gross and property, state income, federal income. All of which are inflating.

And you can’t forget employment taxes, disability, SS, Medicare and other gubmint costs that add insult to injury.

Just had a guy call me and complain that an engineer assessed a structural issue in a house he’s selling (idiot cut a support beam with a 22′ span for clearance for his garage door opener rail) and the contractor wants $2K to do the work (plates, installation, etc.). I told him it was a bargain. Then I asked captain cheapness if that included the stamped engineering drawing and certificate of compliance to avoid future legal issues. I thought the top of his head was going to blow off.

Jack it up level then get good welder to weld it. Then put a couple of straps with bolts.

That’s what we do where I live. Works great.

We call it a MacGyver.

Easy to do if it wasn’t discovered by the buyer’s (the house is under contract) home inspector. If it was plated it may have escaped unnoticed…. but it wasn’t and it didn’t. Now it could become a legal hot potato or crash the sale – and you can’t not disclose it once it’s been established as a problem.

Captain Cheapness should have fixed it before, but that new golf cart was more important I guess.

I don’t think it’s “deceptive” to designate services as a category when measuring inflation. How else are you going to distinguish providing services from other economic activities such as manufacturing? I think most people realize the expenses involved in providing many services are going up in an inflationary environment, particularly employee wages.

rojo – have always found the concept of ‘overheads’ (among several others) to be enduringly obscure to many,…

may we all find a better day.

Perhaps, but what does that say about the understanding of many people? The concept shouldn’t be too difficult since everyone has ‘overheads’ in their own lives. In this way, running a household isn’t much different then running a business though the actual expenses differ.

rojo – exactly…best.

may we all find a better day.

DM: Bed, Bath and Beyond help: Failed retailer is snapped up at auction for $21.5 million – but its stores will still shut and the brand will only be available on a discount website

Laid bare by court documents Thursday, the purchase comes week after the e-commerce firm filed for Chapter 11 – attempting to reorganize its assets and pawn them off to the highest bidder. The buyer, dot-com juggernaut Overstock.com, has already liquidated at least 18 failed companies at below-wholesale prices, and now holds the rights to the retailer’s name – as well as its intellectual property and all of its assets. It’s a stark fall from grace for a brand once worth well over $17billion, and the latest example of investment firms scooping up recognizable assets for dirt-cheap prices. The strategy has already been implemented on other failed fixtures such as Toy ‘R’ Us and Radio Shack, and is generally executed with the goal of reviving them, usually online. A hearing is set for next Tuesday to finalize the purchase – after which the brand’s 360 remaining stores and 120 Buybuy Baby locations will permanently close.