June (next month’s data) will be the final leg of spring selling season. Then things skid downhill till early 2024.

By Wolf Richter for WOLF STREET.

The housing data we’re seeing today – sales that closed in May – are still coming out of spring selling season when prices and sales always rise. This seasonal uptick happened even during Housing Bust 1.

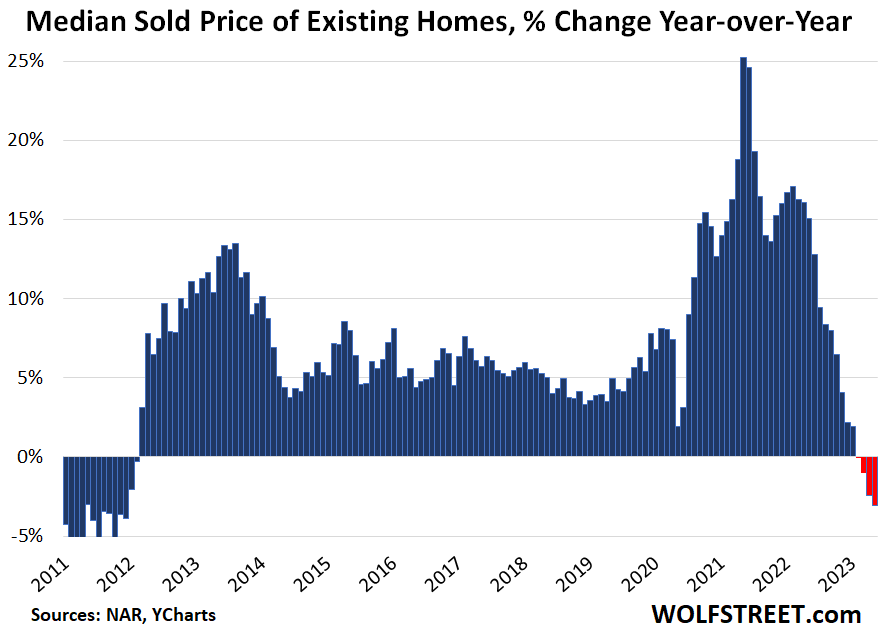

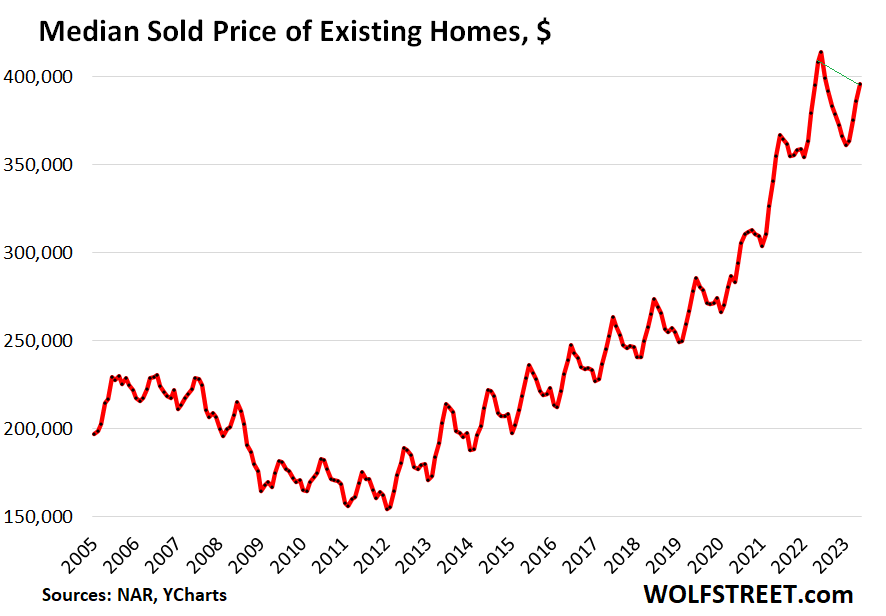

The median price of all types of previously owned homes – houses, condos, and co-ops – whose sales closed in May fell year-over-year by 3.1% to $396,100, the fourth month in a row of year-over-year declines, and the largest since December 2011 during Housing Bust 1, according to the National Association of Realtors today.

For single-family houses, the median price fell 3.4% year-over-year, the fourth decline in a row, to $401,100. For condos, the median price ticked down year-over-year by a hair for the first time since lockdown May 2020, to $353,000 (historic data via YCharts).

From the seasonal peak last June, the median price of all previously owned homes declined by 4.3%. The NAR’s median price nearly always shows a seasonal peak in June, followed by a seasonal drop-off for the rest of the year and into January/February of the next year. You can see this pattern in the chart below. This pattern occurred even during Housing Bust 1.

As 2023 follows seasonality, there will be a final month-to-month uptick in the median price data for June, followed by month-to-month declines for the rest of the year and into early 2024, before the next spring selling season kicks in. The green line connects May 2023 and May 2022 (historic data via YCharts):

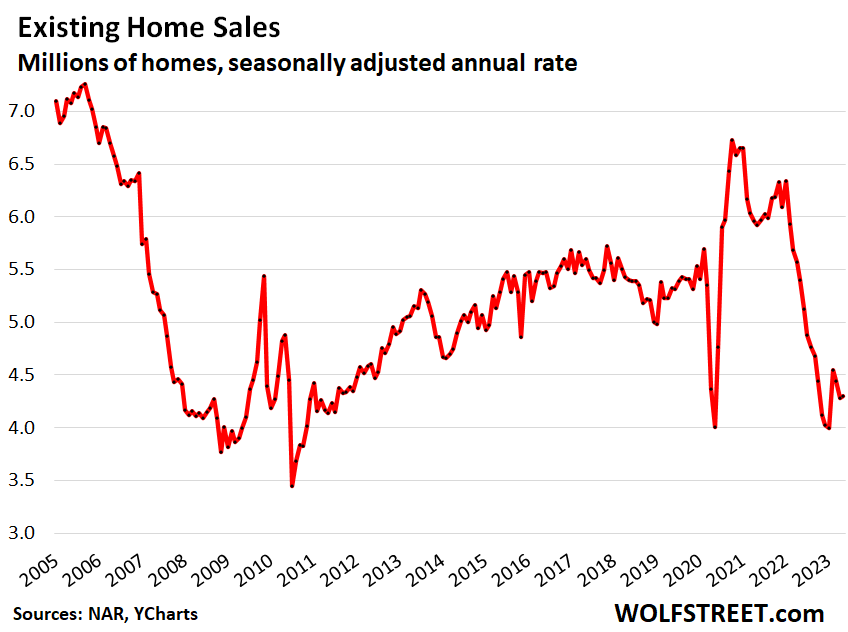

Sales of all previously owned homes, seasonally adjusted, inched up by a hair (+0.2%) in May from April, to a seasonally adjusted annual rate of sales of 4.30 million homes.

The seasonally adjusted annual rate of sales in May compared to the Mays in prior years:

- May 2022: -20.4%.

- May 2021: -27.4%.

- May 2019: -19.3%.

- May 2018: -20.4%.

Homebuilders, on the other hand – the pros who have to build and sell homes no matter what the pricing environment is – have figured out that priced right, nearly any home will sell. So they have cut prices, and they’re buying down mortgage rates, and they’re building at lower price points, and their orders have increased from the lows and the cancellations last year, as buyers have shifted to buying new houses, instead of overpriced existing houses whose sellers and potential sellers are still being delusional, hoping that this too – the 6.5% to 7% mortgage rates – shall pass.

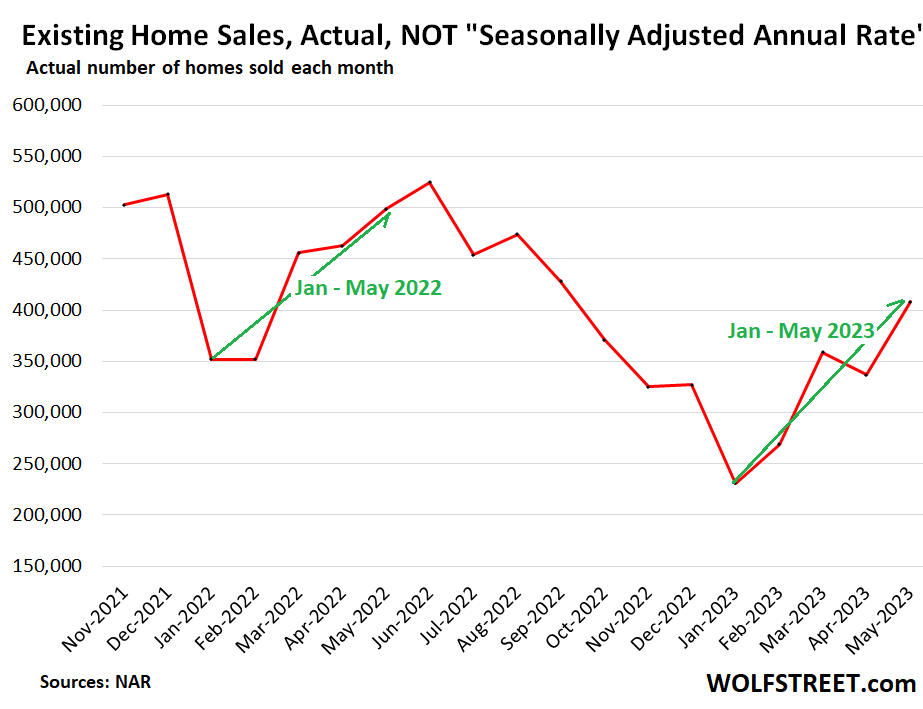

Actual sales in May – not seasonally adjusted annual rate – fell 18.2% year-over-year to 408,000 homes. You see the seasonal patterns, including the spring selling season, in the not-seasonally adjusted actual sales (data via NAR):

Investors pulled back: All-cash sales – often investors and second home buyers – plunged by 18.2% year-over-year to 102,000 homes in May 2023 (a 25% share of 408,000 sales), from 125,000 homes in May 2022 (a 25% share of 499,000 sales).

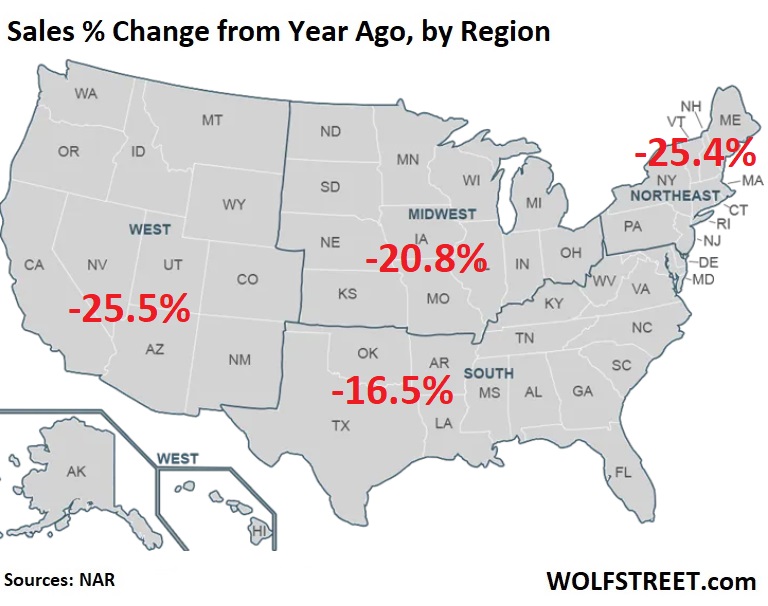

By region, year-over-year sales plunged in all regions (map via NAR):

Median days on the market lengthened year-over-year. Homes that actually sold spent 18 days on the market in May before they sold, up from 16 days in May last year, according to the NAR.

Another measure of median days on the market, which tracks how many days homes were on the market before they were either sold or were pulled off the market, jumped to 43 days in May 2023, from 30 days in May 2022, according to realtor.com.

Inventory for sale rose to 1.08 million homes, from 1.04 million homes in April, but are down from 1.15 million homes in May 2022.

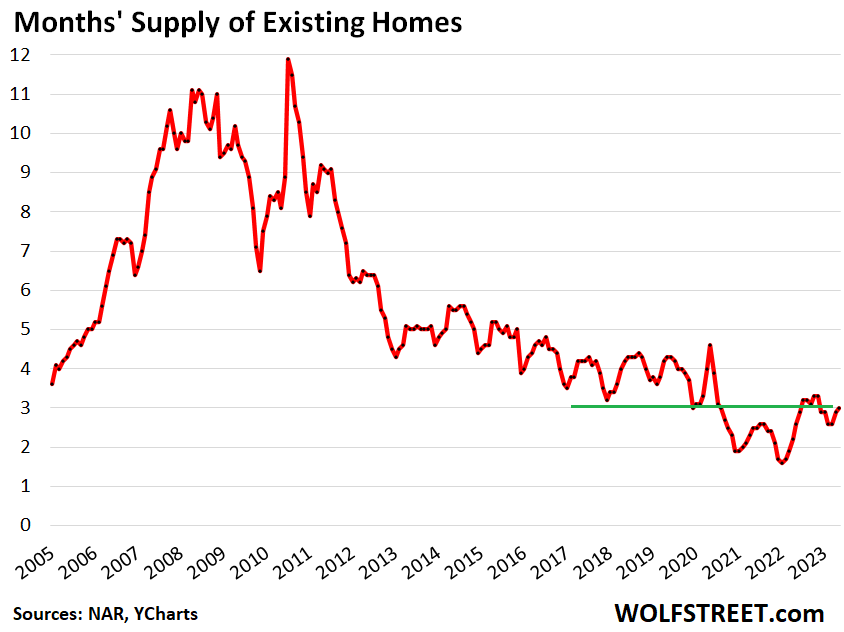

Months’ supply rose to 3.0 months, up from 2.9 months in April, and up from 2.6 months in May 2022. Between 3.0 and 4.5 months supply was normal in 2017 through 2019 (historic data via YCharts).

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Nice to see laughably absurd housing prices finally coming down!

I feel like Wolf, banging the same drum and no one listens. Sellers aren’t going to trade low taxes and low mortgage rates for higher ones unless they absolutely have to, so they aren’t flooding the market with homes. That’s why sales are down a lot and prices aren’t. The longer this continues, the bigger the backlog of buyers supporting the market. The new homes market is already 3-4 Million homes short.

I stopped building new homes in TX last year because NORMALLY, a 500%+ increase in mortgage rates would kill any market. This time it hasn’t and we’re going on 18 months now since rates started getting jacked up.

On the contrary, prices are moving higher for four months now. There was no post fed rate RE crash as predicted. No Spring market crash as predicted. No Summer market crash as predicted. It’s time to re-think all the doom and gloom predictions.

There is a lot of money out there looking for a place to go. Most folks believe real estate is a good long term investment and besides they need a place to live.

I’ll say it again. Until the fed raises rates another 2-3 points and mortgage rates hit double digits, real estate prices are going to keep increasing. It’s either that or some huge unforeseen event that crushes the economy. Regardless, only a major recession is going to lower prices.

Totally agree.

CCCB,

“Sellers aren’t going to trade low taxes and low mortgage rates for higher ones unless they absolutely have to, so they aren’t flooding the market with homes.”

Wait a minute… homeowners with 3% mortgages who cannot move to a new home and therefor don’t put their current home on the market have ZERO impact on inventory because homeowners that sell a home and also then buy a home.

Inventory: +1 -1 = 0 change.

They only provide churn.

So these locked-in homeowners are now completely out of the market, as buyers AND sellers. So the number of buyers and the number of sellers shrank by an equal amount. In other words, the who market shrank symmetrically.

NAR and Realtors keep promoting the nonsense that inventory is low because people are locked into their mortgages; that’s nonsense (+1 -1 = 0 impact on inventory); but THEIR commissions depend on this churn. But inventory doesn’t change. No one else benefits from this churn.

I discussed this in detail here, along with factors that ACTUALLY increase inventory, such as new construction or people dying or moving into rentals or long-term care facilities. This is a really important concept to understand:

https://wolfstreet.com/2023/03/29/how-3-mortgages-altered-the-housing-market-for-years-to-come-a-lot-smaller-but-more-in-balance-than-it-seems-hence-dropping-prices-despite-low-inventories/

Just went deep into property records and discovered massive Zestimates Eff up.

A seattle area home that sold for $1.1 million in Feb just got resold for $1.7 million in May as per Zillow. On deeper look found that it was bought by realtor wife of a realtor husband for $1.1 million.

Then it was sold as intra family transfer to his bank at $1.7 million. This transaction pushed the Zestimatesbof whole neighborhood up by $500,000.

Zestimates are full of crap, be careful.

Also don’t know what this realtor couple is trying to pull off here.

Correction: intra family transfer to husband at $1.7 million.

First time post, I’ll probably mess up how/where I respond…

Wolf, I have a lot of respect for your insights in for wolfstreet.

On the particular topic of inventory, I kept finding myself thinking about it while walking the dog around the neighborhood.

I think the thing is, 1-1=0 would apply if sales happened instantaneously, but the longer the sales lag, the more inventory there will be overall.

Imagining a world where we started with zero buyers and sellers, and then a new pair of buyers and sellers arrived each day for 10 days.

If the homes sold in one day or less, there would always be about two homes for sale in the market.

If it took 30 days for each sale, they would be 20 homes for sale at the end of 10 days.

Or maybe I am missing something?

I’ve referred your site to friends and family a number of times, thanks for the great work!

Causingchaos,

“Or maybe I am missing something?”

Yes. There isn’t 1 seller but 1,000 sellers in one market, and there isn’t 1 buyer but 1,000 buyers in that market, and they’re all jumbled together, some selling before buying, others selling after buying, etc. So the timing of each 1 doesn’t matter because of the large numbers in the market.

Same if an out-of-towner buys… there are also people who sell and then leave that market, like that out-of-towner did in his own market. Overall, across the US, there are 1 million of them every month, and it all washes out.

++++++++ because homeowners that sell a home and also then buy a home

No they do not.

1. They are selling a second or third house.

2. They sell and move in with other people including relatives or a new husband or wife.

3. They die and the heirs sell the house.

4. They sell the house and leave the country.

So no Wolf, you are not correct.

Better math is Needed,

Better reading is Needed,

“So no Wolf, you are not correct.

LOL. You just repeated exactly what I said are among the factors that increase inventory.

And when they do not do that, when they sell a home to buy a home, which is what most people do when they move, upgrade or downsize, then +1 -1 =0, which has no impact on inventory.

What I said in my comment that you replied to was this, quoted verbatim:

“I discussed this in detail here, along with factors that ACTUALLY increase inventory, such as new construction or people dying or moving into rentals or long-term care facilities. This is a really important concept to understand:

https://wolfstreet.com/2023/03/29/how-3-mortgages-altered-the-housing-market-for-years-to-come-a-lot-smaller-but-more-in-balance-than-it-seems-hence-dropping-prices-despite-low-inventories/

Nonsense. Even if you accept that people aren’t going to trade low mortgage rates for higher mortgage rates, that means that people who may have potentially upgraded won’t. So while that is one fewer seller, it’s also one fewer buyer, meaning it’s a net wash.

The market hasn’t crashed yet because sellers are holding out hope that the Fed pivots and rates drop back to 4%. However, houses sitting empty (currently near a record high if I remember correctly) are still eating up carrying costs. At some point, potential sellers will rent.

No one is going to just buy up houses to let them sit empty. And contrary to popular belief, renters don’t care what your costs are. The market prices for rentals are not set by the market prices for sales.

From Professional Builder’s Magazine – 6/22/23 email push:

“The total number of homes for sale in the U.S. dropped 7.1% year-over-year in May to 1.4 million on a seasonally adjusted basis, the lowest level in Redfin’s records, which date back to 2012. New listings fell 25% to the third lowest level on record, a downturn largely propelled by soaring interest rates that are discouraging sellers from relocating and refinancing.

That shortage of for-sale housing is leading to heated bidding wars and keeping prices high throughout much of the country. Roughly 37% of homes that sold in May went for more than their list price, Redfin reports.

Nearly every homeowner with a mortgage has an interest rate below 6%, meaning many are opting to stay put because selling and buying a new home would mean taking on a higher monthly mortgage payment. The average 30-year-fixed mortgage rate in May was 6.43%, up from 5.23% a year earlier and a record low of 2.65% in 2021.

Housing supply had already been lacking for years due to a steep dropoff in homebuilding following the 2008 financial crisis. The shortage intensified in 2020 and 2021 because rock-bottom mortgage rates prompted scores of people to buy homes.”

No opinion one way or another.

“Professional Builder’s Magazine” = RE propaganda. The numbers are nonsense too.

That’s not a complete argument in some respects. Selling to buy is not the only option. I get that the discussion is a response to one particular line of thinking and aggregate numbers as that relates to demand. That said…..

One can pay off a low interest mortgage (i.e., maintain status as primary dwelling) and then buy a higher interest property (for speculative purposes or second/vacation/rental – logical or not). Inventory impacts in this use case are not net zero. I know folks who have done so.

Forgot to add in: the use case I am discussing is largely driven by discretionary income impacts – at least for the folks I know who have done so.

Professional Builder is an industry insider magazine, not “RE propaganda”. Most of the articles are related to operating a construction business or feature new products/technology/building techniques. The average schlub has likely never heard of it so, if it’s “propaganda”, it’s only indoctrinating people who are already in the business. Home buyers/sellers have limited (if any) access to it.

The nonsense numbers? They’re attributed to Redfin and is based exclusively on their data.

El Katz,

New houses inventory (via Census data) PLUS existing homes inventory (via NAR) in April = 1.462 million. This does not include new condos (note the multifamily building boom we’ve been discussing here, but they’re not included).

The lowest months were February and March 2022 at 1.236 million homes each.

April 2023 was also higher than April 2022 (1.455 million), which eliminates the effects of seasonality.

Starting with May 2022, every month, for 12 months in a row, total inventory has been HIGHER year-over-year than in the prior year.

BTW, I get (for some reason) the paper-version of The American Banker, and that’s a banking promo magazine, designed to make bankers feel good.

Uh, the the overall market is crashing quite fine, as long as you remember that RE is not the stock market. Crashes take years, not days. All the indicators mentioned in this article show a shift to buyers.

But in one way RE is like stocks: prices are set on the margins, by the last transaction. So it doesn’t matter how many home owners are happy with their 3% mortgages (or no mortgage); what does matter is the owner who has to sell because of divorce, job loss, moving, etc, etc, etc.

It’s peculiar how RE bulls believe that the same economics that created the bubble (bidding wars and panic buying on marginal sales) somehow couldn’t also cause a monumental crash (panic selling / chasing the falling price on marginal sales).

Their only validation and relief is that it hasn’t happened yet; therefore it could never happen because muh inflation.

Wolf’s post clearly states that this is the Spring Housing price bubble that will deflate later in the year.

Now, I do agree that sellers wont sell because they are locked in with low interest rates. So it is going to take high interest rates for longer and job losses to begin for the market to really turn down.

This is actually a good time for builders due to the really low supply. Builders have all worked hard to reduce the cost of building back down and are selling homes at prices that make more sense, and filling some of the demand.

What will happen is as the stock market falls and inflation doesnt cool the long term rates will start back up and then we will finally get a recession and less jobs and paychecks will shrink and then we will start to see homes dumped on the market.

Tanking home prices will feed back on themselves and that will kick out a bunch of listings and demand will fall even further. Things will get downright anemic before we hit bottom.

This will take 3-5 years to hit bottom and when it hits bottom at a 50% haircut, it will coincide with an economic bottom.

Nah. This time it might just take liquidity running out, no new loan issued or debt coming due for people who are buying extra houses that they **do not personally live in**. Another stock market/bit coin crash or slump or two might do..

Home repo,s are up to 1% of homes Its coming slowly .around 2025-26 will probably be bottom my guess

CCCB

agreed

Where in the hell are taxes low in USA

Cccb, why do you ignore data? You make statements that are obviously false. It destroys your credibility.

Seems you’re conflating sobriety and numeracy with doom and gloom.

I am so tired of this take.

How many times do you think someone hassaid to themselves. “I got to sell the house that I am living in to realize some profits!”

Doesn’t happen.

People sell because they got a new job, family events, divorce, etc. They don’t sell because they think of the house they are living in as an investment.

“I stopped building new homes in TX last year because NORMALLY, a 500%+ increase in mortgage rates would kill any market”

I imagine you must only build new homes as a side gig, otherwise how do you make money without building any homes?

I thought about asking him the same question, but builders can get into remodeling, or commercial construction which still happens to be booming. There are fair weather GCs who will get a job as a project manager when business slows down. None of which are necessarily part time jobs.

layoffs.LAYOFFS.Wait for it.

This is the best metric for liquidity. Liquidity is the Big Kuhuna. Interest rates play 2nd fiddle to liquidity. Excess liquidity has driven equities and housing prices to high. Until liquidity shrinks it is unlikely that prices fall much. Also, interest rate increases act with about a 12-18 month lag. They are just now at the point were it would be expected for them to cut. Also, whether there is a housing shortage is a debatable point. It is true a lot of people have low interest rate mortgages and this is slowing things down. My guess is we will know in 4 years what happened to housing prices. There are several existential issues in the world now too, which may be far more important than housing prices. We may be talking survival.

“Liquidity is the Big Kuhuna.”

Kahuna. But here it is…

The best gift to the USA economy is for housing to have a 50%+ correction

Stonks too.

By a laughably absurdly small amount.

Im pretty bearish about housing prices. In the east bay since covid house prices increased 35% or so. since then rates increase payments another 25% and then prices dropped only 10-15%. buyers took that hit. prices were already high to begin with compared to wages which just dont seem to be going up anymore.

FOMO is kind of brain dead or investors, or Chinese buyers. I think the last one are the culprits. And guess what… YOU THE American buyer of shit at dollar store shot yourself in the foot. Housing right now is like the stupid wall street stock market, run by imbeciles for imbeciles.

Obviously you did not inspect Wolf’s graphic, that showed the reality that the recent relaxation of prices is a fools interpretation, in light of the massive increase in prices over the past 15 years.

Only fools celebrate their downfall.

To flowery & cryptic & not even an accurate summary. The surge in prices the past 11 years was because of a series of adrenaline shots plunged over & over into the housing market.

*Too

Whatever did happen to that smaller starter home idea? Everyone now starting out with a spouse and 3 kids?????

The high cost of land, and the NIMBY costs that get added to each lot, probably make building smaller, lower-cost houses impractical for most builders. Of course, this is only a guess.

Used to rehab lots of 1 and 2 bedroom homes for resale. Maybe they do not build anything that small anymore…….

900sqft start homes go for 350k in NH. Theyre probably 0.5% of all home listings though. Boomers have been building bigger and bigger “dream homes” for years.

Metro Boston housing market (which includes Southern NH) is still very hot- I know a person who bid $55k over asking for a 1600 sq ft colonial and got outbid. It’s crazy

I don’t see a market “crash” until inventory increases significantly. We have about 1M active listings and historical trend is at around 2-2.5M active listings. As wolf stated, houses don’t stay on the market long. 18 days??!?

Interest rates remaining this high will stabilize the market > but if rates come down the frenzy might pick up again. Projections show we will have more than 4M home sales this year. No crash in sight. No, not a RE cheerleader. No, not an agent. No, not a broker, lender either. Just someone who believes in supply and demand.

Richard:

“As wolf stated, houses don’t stay on the market long. 18 days??!?”

43 days before they’re either sold or get pulled off the market without having sold. Up from 30 days last year in May. That’s a big jump.

That’s the second data point I gave you (via realtor.com). This is the more important metric.

The other metric that you cite (via NAR) only counts houses that sold. It eliminates houses that didn’t sell and got pulled off the market.

Stocks will go up sooner or later, death, job change, job loss.

This is a prediction just like your prediction that there will be 4 million transactions this year

Juliab,

It’s not my prediction that there will be over 4M home sales this year. Wolf stated that as well as pretty much any other RE data company/website.

Richard

These are predictions.

No matter who makes them.

Usually the reality is different

Thanks for the reply Wolf. I have read several times about ~40 days on market (median days) in markets like San Diego and other areas in California. I believe anything below 60 days is considered a “fast moving market”.

The 18 days you mentioned seemed outrageously low. That was actually the first time I have seen that. “Homes that actually sold spent 18 days on the market in May before they sold”. Bottom line for me is that these type of metrics do not sound like a crash to me. I am in Lake Tahoe for vacation. Prices are sky high. A few years ago (prior to Covid) I believe prices were 30-40% cheaper.

But now we have 7% mortgages, plus QT (M2 money supply is contracting) AND Employers are calling their EE’s back a few days per week to work in the office. I am surprised how well prices are remaining that elevated. I am still hoping RE prices in Lake Tahoe will come down.

AIRBNB Anyone?? This is NR 1 killer of affordable housing WORLDWIDE. If you think otherwise THAN go back in the basement and never come up IMBECIL. Every Living soul wants an AIRBNB and never work again for the men.

Interesting – that’s roughly for 980sqft in southern NH in early 2021.

I’m surprised home prices haven’t come down more in this area.

1100 sq. ft. 3-2 goes for anywhere from 650k – 800k in northern SD County where I live. Starters are becoming anything but.

Condos aren’t much better.

Where in SD county do you see 1100 sqft single family homes in decent conditions for 650k? Fallbrook?

I have 2 nieces 1 traveling RN other in financial racket. Both have no homes,travel extensively,enjoy life and experiences over things,RN beds down at parents house when home,won’t buy a better car says hers is good,other lives in SD in a condo, seem our kids are in a different zone .Wish them the best.On the other side of coin my 3 kids all live here bought homes and are doing well

850k-1m in the city itself is what I’m seeing. Makes sense that way way north county would be much lower, especially as you go inland, but even the scary parts of the city are seeing prices quite a bit higher than 650k. I’m curious what part of the county you’re seeing these lower prices.

Look at your give-me-government starting from your city all the way up to con-gress screwing the housing market. Don’t forget Blackrock, Redfin, Zillow etc…

More that the government has succeeded in making the housing market so unstable and boom and bust, that no one wants to buy a “starter home.” They want to buy one home and be done with it.

LOL. Sure. Guessing very few buyers think that way. Too many of you out there give homeowners way too much credit. The “sellers are hoping for a Fed pivot” is hilarious. 90% of of homeowners don’t even know what the Fed is!

No, the death of small homes comes from the cost of land and the fixed costs of building. It makes (almost) no sense, as a developer, to build anything less than the max that will sensibly fit on a lot. I build, I know.

While it’s certainly true most people have no idea what the Fed is or does… People do know generally what rates and monthly payments are so when someone who might be selling starts looking for a new house and gets a mortgage quote at 8 percent and the payment that comes with that they quickly change there mind and sit pat.

Complete nonsense. I’ve personally spoken to many people who would rather stretch to buy a home today than buy a “starter home,” because they don’t want to risk the market crashing and have to unload one that they’re underwater on.

Regarding sellers hoping for a Fed pivot, it doesn’t matter if they don’t specifically know what the Fed does. They are being fed constant BS about “rates coming back down next year, which should support housing prices.”

So they’re figuring that if they wait a few more months, they can sell at last year’s peak price.

Einhal-not sure I follow the logic of stretching to buy a home while anticipating a market crash. Let’s lock in even bigger losses!

Because people care a lot less if they’re in their “forever home.”

No one wants to be locked into a house that they only wanted for 5 years.

“No one wants to be locked into a house that they only wanted for 5 years.”

That doesn’t make sense – why not just rent at that point? Especially now.

We live in a new subdivision and the section we are in sold out before ground was even broken ( 2021-2022). But across the street from us is a new section that only got started in 2022. They are just finishing up and the model home is open and staffed with a smiling Realtor@. But from what I have seen it is crickets. Almost never see lookers or cars parked by the model home. Not one of the homes now being finished has a sold sign on it. These are professional home builders ( big ones) that have all the tricks Wolf has discussed at their disposal.

Interesting how the real estate market/cycle tricks builders into rushing

into that one last wave of new construction. Then what do ya know, we’re overbuilt. Hold on to your hats. :-)

Wonder if this could be the perfect storm coming…sales still suck by a good time measure but yet homebuilder activities and starts are going up, prices still sky high in areas like SoCal and Norcal, interest rates still high, FOMO still out there and we’re seeing more full housing recovery narrative running rampant in mainstream media and out of almost every RE agents…there’s no question there are still plenty of optimism (or wishful thinking in the market) I sure do hope this will be another nail in that coffin to bring home price back down to reality over the next 2-3 yrs…one can fantasize perhaps..

In my local area sales are down approx 50% from last year but prices haven’t changed much.

That is WHY sales are down. The market is, in a sense, not clearing. Prices are sticky at a level that cleared the market during a feeding frenzy zero rate environment. Once it becomes necessary for homes to sell, prices will adjust accordingly and there will be a race to the the exits. These things take time….

Average time on market is <8 days for every New England state. What little inventory there is, is selling.

Last month, I bid the offer on a house one day after it was listed. Didnt get it.

The price was up 22% in past two years. A bidding war ensued and another 10% was added in the process.

Went to buy a car. The salesman said 30 to 45 days.

Finally got one….but only one key. Chip shortage.

Not much changed in front of my nose. (small sampling admitted)

Tremendous amount of apartments being built in my area. Plans and financing likely made 1.5 to 2 years ago when rates pushed to zero.

Where are you getting this information? While no doubt homes are selling fast in New England, an average of less than 8 days on the market seems like an exaggeration.

Lucca:

Zillow and first hand experience. Now their number is “Median days to pending”, theres obvious outliers. Most hosts go on the market Tues-Thurs, have an open house Saturday and Sunday, offers are due 5pm Monday and the listing is Under Contract Tuesday morning. Theres exceptions for stranger properties that are cash only, old churches, other weirdness, million dollar lake homes, but I find even “ugly” houses in the 350-750k range follow this sub 7 day cycle.

Its a strange game, the only winning move is to not play.

In the famous words of Wolf, this is BS.

I assume you bought your last house in the 70s. Its always the people most detached from the housing market that refuse to accept its current reality. Luckily data doesnt care about your feelings.

Outside of some major external force like severe recession, this stubbornness will persist for quite a long time unfortunately…after all this is the aftermath of the forever prosperity gospel (home price can only go up) burned into every homeowner’s brain over the last 3 decades. Nevermind 2008 since everyone still think that’s once in a lifetime ever drop and nothing will ever bring home price down again…don’t expect this kind of thinking to unwind anytime soon even if Federal reserve would allow it to…not that I have much faith in the latter either…

Exactly. Here is an analogy I’ve been using.

Let’s say you have a singles bar on New Year’s Eve. There’s 50 single guys and 50 single women. But let’s say that, for whatever reason, all of the women are undesirable to all of the men and vice versa. Everyone leaves the bar without having met anyone.

Would you say that there is a “low supply” or a “shortage” of singles at that bar? Of course not!

It’s just that the sellers and buyers didn’t have a meeting of the minds, so nothing “sold.”

That’s exactly what’s happening here. There is plenty of potential inventory, but sellers aren’t willing to sell at a price buyers are willing to pay and buyers aren’t willing to pay at a price sellers are willing to sell at.

So very little moves. But like I detailed up above, that won’t last forever. The carrying costs for single family homes are too high, and people aren’t going to leave them empty indefinitely so that they can wait for a fantasy pivot.

I sincerely pray to god or whatever higher being in charge that you are bang on right…I completely agree with the logic here and the data backs it up…

However, feels like we live in upside down world for too long and this insanity feels like it’s the new normal unfortunately.

Phoenix, I guess we’ll see. All I know is that the numbers don’t add up, and all of the narratives are inconsistent with each other.

For example, people say that single family home prices skyrocketed before of permanent remote work. But if that was true, city costs would have dropped, and real estate rental prices in Manhattan are at a record.

People say that “more and more people are buying homes.” But the fact remains that the population grew from 2010 to 2020 a lot slower than in the past. There is plenty of housing out there. It just isn’t being utilized correctly, because of bad government policies.

But no one will keep years of empty houses. Eventually, they’ll give up. I just don’t know the time frame.

I think that on the demand side, the psychology has not yet changed, it is the qualification that has changed. So most people simply dont qualify for a home loan at the prevailing interest rates and home prices.

So on the supply side it is mainly a lack of psychological incentive to sell, whereas on the demand side, it is financial reality that prevents a sale.

Could they not just rent them out?

Possibly, but the amount they’ll be able to get in rental income is dependent on the current state of the economy, not the owner’s carrying costs. So yes, in some places, they might make money renting them out.

In other places, they might lose money each month, and realize that being a landlord sucks.

There isn’t an unlimited supply of high-income renters with good credit.

Met two new gentlemen in my town in East Texas last month they are 66 and 68. We played golf for a day. One is from Dallas a custom home builder and commercial warehouse developer. He had 3 homes. Highland Park Texas in Dallas , Horseshoe bay near Austin , and my East Texas town. The other has a home here and a condo in Horseshoe bay . They both came here because homes were 150-200 a sq Ft vs Horseshoe bay at 400 . The Highland park home sits empty and I asked is he considering selling and he said no way that’s his annuity. I’ve not met people like this before and I’m 66 and used to middle class working families . These are two and three home folks that don’t even rent them out . Liquidity and an abundance of cash flow . They are looking for lower cost areas however . These bubbles take time for deflating . I don’t know how long but the deflation and liquidity is being drained and the Fed is determined to assist and not pivot and that’s what they are committed to. My favorite term from Wolf in that something broke and the Fed stepped in and that’s inflation. PE and commercial real estate are at the forefront of these changes but at 5 percent cash returns for companies stock buybacks may not be as attractive either and debt levels may be the target . The stock market drain in liquidity is another slow but not so steady change and still down from the highs. I do have one daughter who is trying to get into the short term rental business and has figured out that I am not interested in her endeavors. She talks lingo I had never heard of like cash on cash returns where the home debt is ignored. Leverage never a recession and the more beds in the home the higher daily rate. That won’t end well just takes one hiccup and it’s over . Leverage does that . Plenty of energy companies bankrupted over the years from this action .

@William

This is exactly my understanding of events. Sellers are waiting to drop prices, would-be sellers are waiting to list (in part because many can’t afford a similar new house in their desired market at current prices+rates), and would-be buyers are waiting for prices or rates to come back down. We’re frozen into place. It’s gonna take a long time of marginal prices creeping downward for things to get back to a healthier place. Or it’ll take a sudden glut of fear causing sellers to flood the market with new inventory. But I don’t see that happening anytime soon, as we’ve seen from Wolf’s reporting on this stubbornly robust economy. I think we’re in for the long drip, drip, drip.

I do wonder what role ongoing inflation will have in forestalling more price reduction. Perhaps prices won’t fall much more, and instead incomes will eventually catch up to create a new, much higher level of affordability. Wo be unto those who can’t keep up in a high-inflation environment. My retired family members in particular. Makes me sad, frustrated, and angry. But I digress.

Rest assured that if incomes continue to rise, housing prices will continue to rise.

This is not the solution

“Fear” has nothing to do with a robust economy. It’s more psychological about not wanting to be the bag holder.

William, do you mind elaborating on the reason why it will become necessary for homes to sell? I was finally able to buy our first home. We would do anything, including selling grandma, to keep the house. If prices do come down finally, I don’t see a single reason to sell my house. Let’s say I lose my job and there would be a massive job loss recession, wouldn’t demand for renting pick up? In other words, I could rent out rooms. I am sincerely trying to understand why some people are so certain of a crash or race to the exit. Most things I see in the data, points to the opposite (mainly low inventory and days on market). IMO, the entire system in the US is set up for people to stay put and “hodl” their house/30y fixed mortgage rates.

“Once it becomes necessary for homes to sell, prices will adjust accordingly and there will be a race to the the exits.”

> William, do you mind elaborating on the reason why it will become necessary for homes to sell?

Job losses

in addition death, divorce, urgent need for cash, children’s education, relocation, change of job, problems with neighbors or with the property.

for some investors panic from falling property prices

You must mean MASSIVE, UNPRECEDENTED job losses, right?

“Death, divorce, problems with neighbors or the property. Urgent need for cash, children education.”

I don’t understand. Are you saying death or divorces will increase dramatically? Because All those things happen daily. So how will these scenarios that happen daily be an issue in the future for the housing market?

And why would investors panic? If prices fall and their rents

*And why would investors panic? If their prices and rents fall*

Therefore, many investors buy with the aim of selling after some time at a higher price.

When prices start to fall some of them panic that they will have to wait years for the new peak.

I think Wolf said,

*in a market crash, the first to sell are profitable.*

I posted before I finished the sentence. If prices fall and rents remain stable or go up, investors have little incentive to sell. Many of them are not speculators. Instead they are in for the long haul. Meaning, they will rent out the properties for decades. Declining prices is rather an incentive to purchase more rentals, not sell. Imagine prices decline 20% from here. Institutional investors like blackrock would come in and scoop up thousands of homes.for most investors cash flow is the main reason to keep rentals, not fluctuations in price.

”I am sincerely trying to understand why some people are so certain of a crash or race to the exit. “

This vantage distorts your objectivity. You’re over-invested in the converse premise. Stop reading Wolfstreet comments and go live your life in your house.

Most people who own homes will lose their homes before they rent out rooms. Makes no sense to me either, but I’ve seen it happen many times.

there are renter shortages in recessions due to job losses.

It is weird how location/conditions affect local prices. We live in a condo complex with an ocean view near LA. In February of 2020, the condo to our right sold for $875k. Near the peak of the market (June 2022), the condo on our left sold for $925k. Unfortunately, the massive gain in house prices never happened here. Maybe we will be spared from the drop.

Only time will tell. LA is no special.

Portland/Salem OR and prices just seem to keep going up, up, up, despite the crime, homeless situation, and traffic (especially in Portland). Sellers and agents have an overinflated view of worth and blame it on scarcity and “the market”. There are TONS of homes on the market. They are just overinflated and kept out of reach for most people. They sit, but rarely come down–or they get what they are asking and more from investors or the extreme high end earners– which is certainly not the norm in this area. Realistically priced homes are subject to feeding frenzies. Asking prices are just “opening bids”. FOMO keeps this going. Eventually something has to give but it won’t happen unless people get their heads out of the clouds–or something devastating happens to the economy. It all feels just so…manipulated.

“Portland/Salem OR and prices just seem to keep going up, up, up,…”

LOL. Here is the median-price-based Zillow chart for Portland:

Most of the “good” houses in safe neighborhoods are in an unaffordable range because they went up so high in the first place. and are still rising. The SW is unaffordable for the average salary. In the 450-550K range–most of those are in the SE, NE. The prices that HAVE gone down? Crime ridden neighborhoods. Near proximity to homeless camps. So, Zillow averages that overall prices are down here. If one wants to take the risk of living in one of the areas that are really rough, and the police reports are available, they may be able to find something in that range as those prices are sometimes lowered to compensate. In Salem/Keizer, FEMA areas are down due to severe flood risk. All of that brings down the zillow average but does not paint a true picture for families wishing to buy in a safe neighborhood with (farily) decent schools.

One thing we have also noticed that is bringing the average down are the number of homes now being dumped by investors or in pre-foreclosure. Or in deplorable condition. Or, again, in neighborhoods where people are trying to get out due to the crime rate, drugs, and homeless situation. I don’t know if this is a fear response to an impending recession and market crash, so perhaps a “last-ditch” effort on the side of the sellers of these basically non-desireable homes? Whatever it is, is has messed with the average price reports.

Janela,

Good friends of mine sold their house in Portland last spring. Nice area, nice house. They had two offers. One fell through. Closing on the second was delayed. During the delay, prices dropped, and my friends had to lower the agreed-upon price to make the deal work. It finally closed at $745K. The buyer then couldn’t sell their current home because prices had dropped, and so they put my friends’ home on the rental market at $4,000 a month, but that’s too high, and so it just sat empty. They then reduced the rent to $3,750. Then they removed the rental listing. Zillow says that the price has now dropped from the already lowered closing price by another 4%, to $715k.

Don’t tell me any stories about Portland; because I’m going to tell you my own stories about Portland.

My friends didn’t leave Portland; they love it there. They’re in their 80s, and they wanted to downsize, and make their life a little easier, and so they bought a two-bedroom unit in a co-op building in Portland.

Portland’s a dump! no one goes there anymore, it’s too crowded!

I hear Tulsa is nice though

;-)

I made the mistake of visiting Salem a couple years ago. Absolute dump. Looked like they had emptied a prison and all the cons were running wild. Not as bad as Redding, CA. I had been there years ago, liked it and went back. I had to double check that I was in the right city! Needed cash but waited until early sunday morning to visit an atm at an empty shopping center.

Portland has a lot of bad areas too, complete no-go. Used to be such a great place.

I doubt they had emptied the prison. The incarceration rate in the USA is of the highest in the world. Once I looked at the numbers, USA had a higher percentage of the population in prison than China. Even if the number of political jailed and in “reeducation” centres in China are true and counted as prisoners.

This housing market is so perplexing. National builder’s gross margins are approaching 30% and there’s so little inventory, discounts are in the rear view mirror. I live in Naples and prices are up 100%+ since 2019. So, a 5 to 10% decrease doesn’t really matter to most owners. I don’t see many issues in the next few years unless we have much higher unemployment.

Home owners insurance and taxes will destroy . FLORIDUH .If thr hurricanes don’t get u first

Timothy J McLean,

“National builder’s gross margins are approaching 30% and there’s so little inventory, discounts are in the rear view mirror.”

Nationwide, homebuilders have lots of inventory. But their price cuts and mortgage-rate buydowns have made a dent into it:

True on the insurance. It’s been greatly miss-priced in hurricane-prone areas where the land is about 2 inches above mean sea level and the water table depth is measured in millimeters. Over the past decade, the number of hurricanes per season hitting FL have been below their long-term average—unlike what the global-warming cult had been predicting. However, as with most things in nature, the hurricane rate will revert back to mean. Cheaply constructed houses built on porous limestone are becoming uninsurable, which is good.

” Over the past decade, the number of hurricanes per season hitting FL have been below their long-term average”

Which goes to show it’s not an increase in storms, it’s the increase in housing prices and replacement values over the past decade.

Tons of policies getting canceled in rural California as well. It’s because of wildfire, but the companies are canceling the entire policies- not just fire coverage. What insurance is left is getting much more expensive, if you can get it. That has got to effect home prices very soon, especially as banks won’t loan without one.

It’s not just State Farm and Allstate. I had a talk with my insurer yesterday and policies are being canceled left and right by many companies.

I had thought Housing bust 2 would play out similarly to HB 1. Since leaning about how Governments will use high inflation to control their debt from Mr Wolf, HB 2 could write its own book about this RE Bust…….

Sorry, meant learning from Mr Wolf about inflation…

Your initial comment was absolutely correct. While the bankers’ cartel, called the “Federal” reserve, was paying higher interest rates on their bankers’ deposits with them before and they were having its banks hold the trillions of dollars that their “Fed” created, since 2019, after the 2017 tax cuts to benefit the rich, they would have known that inflation would result once the money the banksters held, e.g., at their “Fed,” got into the economy.

Inflation (probably over 10% a year in actuality) means that all losses in value, e.g., in real estate, are greater than they appear. All gains are lesser than they appear.

It reduces the liabilities of their bankers and over leveraged cronies by trillions a year, e.g., the real value of US deposits that they hold, so it will be continued for many years. To infinity and beyond(!) or at least until your savings and social security payments are not enough to buy even a cheap cup of coffee. Learn to live like a Russian pensioner in 1990: eating the food left in garbage cans! It will toughen you up! LOL

(Cheer up! At least we are better off than the CCP. It is trying to induce foreign investors to lend them money and invest in China. It is just like trying to rent out state rooms now in the Titanic. LOL.)

FL is played out, IMO.

Insurance will be tough to get, prices up, and there will be another hurricane…not if but when.

Oh, and there is a Chinese military post just down the pike in Cuba.

I’d estimate FL to be ground zero for HB 2 at first sign of weakness considering the amount of people that piled in there last few years, like a herd of donkeys.

I think you are right Longstreet. Lots more inventory on the FL west coast since last year. A water front home in Punta Gorda asking $1.8M just settled at $1.1M.

Gabriel

Agreed I am in PG. Still some incredibly stupid sale prices going on, but a large amount of inventory on big dollar stuff just sitting and sitting.

If reasonably priced its 40 years old and hasn’t been touched. Hurricane Ian roof issues still a major problem and new hurricane season awaits.

Also agree Fl is going to be front and center when big downturn starts. It has become unaffordable in so many areas, unless you want a mobile inland.

I think TN got played out first, now Florida. I think other states in the SE will and are benefit including KY and SC. The people in Florida are not heading back to large urban areas; they are heading to surrounding states. Inventory figures can be misleading b/c a lot of properties listed are junk. This is my personal observation.

In the two towns we were most focused on, there are buyers waiting for new good listings and sellers have jacked prices. We also see some buyers ignoring new roofing and hvac costs required on properties, so the acquition cost is higher than sale price.Some sellers seem to be accepting “contingent” offers, so that is some weakening although the offer prices are higher than a cash buyer would make.

There are still alot of people retiring in high cost urban areas looking to geo-arb their housing costs… the first to boom were no tax states but the housing costs are so much lower in the target market that they hold their nose and rationalize the buyer. Some smaller towns have no or very limited new construction and it’s hard to trust a small local builder. In these same areas homes get past down through generations.

One other observation is the crap quality of new construction.

No one wants to move across country and end up renting while realizing it will require another move when they eventually buy.

If prices decline by 5%, where does that put them in relation to 2029 prices? Right? Look at the trade-off between a 5% price difference and the cost of renting for 12-24 months.

I live in SE Florida, and while prices increased by an absurd amount there too, I can see that the tide is turning. The inventory on the market is crazy, and no one is paying the peak prices from last year.

A lot of the appreciation in Florida was due to people moving from colder climates expecting to “work remote” indefinitely, and now many of them are being told to get back to the office.

There aren’t enough jobs in Florida to sustain the prices, and many Florida cities are now the most unaffordable in the country where you compare prices to incomes. Also, regardless of what the shills say, there aren’t enough new companies moving to Florida either, even if a hedge fund or two opened a small office in Miami or West Palm.

Florida has always been boom and bust, and I don’t see this time as being different.

Price to income doesn’t work in FL.

They’re all retirees from NY/NJ/CA etc.

When you sell your home in NJ for $3 million a house in FL looks cheap at $1 mil + no state tax. Prices doubled during pandemic tho.

I know one guy that “lives” in FL for 183 days a year… Just to avoid state taxes.

Wages in FL suck and they try to screw you on COLA.

Bring your own money to FL and it’s a nice place.

WaterDog, with all due respect, your post is contradictory. Florida is not ALL retirees from NY/NJ/CA (while I concede that a lot of people retire from NY and NJ, and even midwestern states like IL and WI, there are very, very few “retirees” from California to Florida). Part of the narrative as to why Florida’s doubling of prices in many places was justified was because of “work from home” and people “bringing their New York City Wall Street incomes to Florida.”

So in that case, price to income IS important in Florida, even today. People either have to be able to keep those remote jobs and stay remote forever, OR they have to find new jobs down there, and there just aren’t enough of them.

People who are concerned with living in Florida for 183+ days a year are usually NOT retirees, as retirees are much less likely to have enough income that it really matters (contrary to popular belief, most retirees to Florida are NOT rich, and are not pulling down hundreds of thousands of dollars in investment income post-retirement). So it’s working people who care about that, NOT retirees.

My point is that Florida prices increased due to a set of unusual factors that in my opinion, are unlikely to repeat again.

While there are far more permanent work remote jobs than there were pre-pandemic, there aren’t enough of that type of income to justify that houses in Naples or Delray Beach that sold for $750k in 2019 sold for $1.6 million in 2021/2022 at the peak. Like all other assets, prices are set at the margins.

That’s why I’m seeing a huge increase in inventory throughout Florida that is just sitting on the market. Florida real estate went up by an unsustainable amount, and it will revert at some point. I just don’t know when. All I know is that it’s NOT different this time.

So true. Many retirees are former government employees escaping the high taxes in the mid-Atlantic and rust belt states. Interestingly the cause of those high taxes are the golden retirement plans the state has to fund. During the city of Detroit’s bankruptcy, the following items caught my attention: 1) Almost none of the retirees lived in Detroit, which has a high income tax rate and property tax rate. 2) Many retirees lived in low-tax southern states. 3) The city of Detroit had almost 50% more employees than needed because on any given day, 1/3 of the workers were absent.

Say what you want about it, Florida was never a nice place.

Californian here. Back in the 90s, we moved from L.A. to the Tampa Bay. The prices for homes were dirt cheap then, which was a major draw. What turned us around, wanting to head back home, was the massive differences between the two cultures, plus the differences in the ecosystems, especially those bland, humid beaches in Florida. If you grew up in FL, you no doubt love it. If not, and you’re from the West Coast, it’s not really that appealing.

In my experience, the people who hate Florida are either progressives or people who hate humidity.

‘Florida – Come for the politics, stay for the humidity!’???. (but seriously, Ein, thanks for your informative take on your pied-a-terre…).

may we all find a better day.

Timothy, this market can be confusing and super frustrating. I heard so many times that when rates will go up prices have to come down. In reality, if you had waited to buy (like us) you are paying more per month even though prices have come down. A 10-15% discount on price doesn’t mean much when mortgage rates double….:( but what to wish for? If rates come down the frenzy starts all over again. Ideally, you have low prices and low rates which only exits in a pipe dream.

the ideal time to buy property is when property prices are at rock bottom even if interest rates are high.

Today, when real estate is highly overvalued and interest rates on loans are in the sky, it is the most inappropriate time to buy a property

Hi Juliab, nobody is able to time the market though. How would you know the bottom is here? There isn’t even a guarantee prices will go further down from here.

Yes, there is a near-guarantee that prices will go down “from here.” Even in good years, prices fall in the second half of the year, on average across the US. Seasonality can be different from place to place. But overall, we’re now at the seasonal peak.

The big crash that didn’t happen. Only a little over a year since prices peaked, but the “elevator down” like in 2008 is more like a wheelchair ramp. Likely to continue until that whopping 10% price drop from 2022 highs finally occurs in a couple years. There will be some 15%+ drops (real estate is local), but high end multi fam rental living is the future for most – and it’s not bad !

>10% decrease has already occurred in many metro areas.

We have a lot of single family and multifamily underway in Sanford, NC. About 40 minutes from Raleigh. New construction appears really hot.

My department is based out of Apex, NC. One of my coworkers was showing us the progress of her new home that is being built. It looks like new homes are being packed in as tight as in Southern California.

New development close to me. Forested land was purchased for $1 million for 100 acres I think about 5 – 10 years ago. Zoned to be dense for Sanford. I think it works out to about 1/4 acre lots. Developer ran into a lot of site problems with rock.

He has water, sewer and roads in on first phase and 5 homes under construction. I thought he would go bust before finishing, but housing market is still hot, so maybe he will get it done and sell at good prices. Seems like they are about 2000 sq. ft. with 2 car garages. I have heard prices going to be around $400k.

I used to be shocked at 2000 sq Ft for 400k . I’m 65. Inflation ingrained in home ownership. My home built in 2006 for 120 a sq Ft would most likely not sell at all for 200 a sq ft . NE Texas area. New homes sell for 220 a sq ft.

Many cash buyers are on the sidelines, waiting for the bottom. Looking at Wolf’s first graph, the downturn is just getting started (compared with 2010-2012).

I am sure home builders see what is happening, but their labor costs are low, now that millions of illegals have entered the country the last few years. They will keep up a good building pace as they try to get ahead of mandatory and enforceable E-Verify, which is sort of happening in Florida.

In my suburb of Seattle it doesn’t look too good for sellers.

The limited number of buyers are offering less than asking with an escalation up to (the already lowered) asking price. There’s still some FOMO but definitely cautious and expecting lower prices.

Local mortgage lenders are advertising mortgage rate buy downs (aka a 3-year ARM… remember those lol!) on local radio. I sure hope everyone with a new “3.5%” mortgage can handle 6.5% in a few years.

And finally, we’re seeing more SFHs getting listed for rent than at any time in the last 6 years. Prices for rent are coming down quick too.

As long as mortgage rates stay up we will see the price of housing shift lower and lower until they’re in line with (non-RSU) incomes.

“And finally, we’re seeing more SFHs getting listed for rent than at any time in the last 6 years. Prices for rent are coming down quick too.”

Interestingly, on the other side of the lake I see a totally different picture. Very little inventory and when a decent home is listed for rent, it may have 30+ application within hours.

Yup. I have a condo in calgary Canada that I rent and I put it up for 40% more than prior tenant (which was a bargain) and got 30 apps in 24 hours. 8 people showed for viewings after I filtered through them with income and references requirements up front and 7 of them wanted it. Chose a guy because we are both Deloitte alum. It’s crazy out there.

I’ve owned dozens of properties in Alberta and the only thing that ever went up were condo fees. Rents fell every year non-stop forever as did home prices. Everyone must be coming in from other provinces or from abroad.

“on the other side of the lake” – I should have been more clear… HeavyC is in Seattle – I was referring to lake Washington..

I am waiting to see how the how two new WA state-wide laws on SFH recently signed will affect things. A bit more aggressive than the OR or CA laws.

1. For cities with populations of 25-75k, duplexes are

allowed outright on SFH lots, up to 4-plex if property is 1/4 mile from major transit stop or if 1 unit is “affordable”.

For cities 75k+, 4-plex are allowed outright on SFH lots, up to 6-plex if property is 1/4 mile from major transit stop or if 2 unit are “affordable”.

When the cities like Seattle update their codes, SFH will most likely be treated like a variation of multi-family, like LR1 or LR2. Even with HOAs/covenants might be pressed

with the new laws since no multifamily might not be explicitly called out in the rules. I can see some challenges

b/c folks can’t update their HOAs to exclude these laws.

I am gonna build a 6plex + 2 ADUs in Windemere or Broadmoor. That would be hilarious!

2. 2 DADU/ADUs are allowed on SFH lots. So, theoretically,

it is possible to have 6-plex + 2 DADU/ADU per lot, but we shall see. I can see folks adding 2 DADUs (1000 sqft min

and 24′ height max) but is the juice worth the squeeze.

There are 10 new laws to deal with the “middle housing shortage”. Win for tax collectors, win for developers,

and win for buyers, at the expense of incumbent SFH owners.

The truth hurts lol

Somewhat related: My Home Depot/Lowes traffic indicator has shown marked slowdown of the “bubba” handymen (decks, windows, tile) that used to flood the contractor end of the store most hours of the day.

Could be different elsewhere. Location: Asheville NC

Turned very suddenly. I have been making trips once/twice a week forever with my house restoration.

A kwik shop in Omaha is closed,occasionally because of no help ,but all the Casey,s are open . Tells me someone doesn’t pay enough.

Although volumes have gone down, prices have been stubbornly high. I guess we need higher rates for longer. But FED already paused and stock market is flirting with highs again.

FED needs to be more aggressive with QT but won’t happen for sure.

S&P 500 is still like 10% off its high. And that’s not even accounting for inflation since its peak in late 2021. Keep in mind that the “market” gains are really only due to a small number of stocks with huge market caps pushing up the index…not a broad rally. And a lot of those companies gains are due to stock buybacks (Meta, Apple, etc) and/or algo drive hype like with ai headlines. That’s not even getting into the TGA having been drained since last year (and YTD), which resulted in a $104bb+ increase in the Fed balance sheet under “Reserve balances with Federal Reserve Banks” compared to a year ago.

RE “more aggressive with QT”.

If you read Wolf’s posting “US National Debt Hits $32 Trillion, up $572 billion since Debt Ceiling Suspended. TGA Starts Refilling, Drains Liquidity from Markets” you would note that TGA is now acting with QT instead of against QT so it is happening for sure.

Expect to see the stock market get hit as “TGA Starts Refilling, Drains Liquidity from Markets”.

The supply of homes for sale in California has not increased nearly as much as it usually does this time of year. New listings down 20% year over year. The month before was down 17%

Source:redfin

Buyers are way down too.

So let me just repeat what I said above because this is a really important concept:

Homeowners with 3% mortgages who cannot move to a new home and therefor don’t put their current home on the market have ZERO impact on inventory because homeowners that move sell a home and buy a home:

Inventory: +1 -1 = 0 change.

They only provide churn. And only Realtors benefit from that churn by getting big fat commissions coming and going.

So these locked-in homeowners are now completely out of the market, as buyers AND sellers. So the number of buyers and the number of sellers shrank by an equal amount. In other words, the who market shrank symmetrically.

https://wolfstreet.com/2023/03/29/how-3-mortgages-altered-the-housing-market-for-years-to-come-a-lot-smaller-but-more-in-balance-than-it-seems-hence-dropping-prices-despite-low-inventories/

The other folks (other than realtors) impacted will be State governments who will be missing out on transfer taxes.

A lot of people depends on housing transactions and if it slows sown then their income goes down quite a lot.

Few of them are : real estate agent, inspectors, mortgage brokers, attorneys, city/county office people, transfer tax, etc etc.

“because homeowners that move sell a home and buy a home”

Some people sell a home and then rent an apartment. Some older people sell a home and move into facilities or nursing homes. Some pass away. The net effect of any of these actions is usually to increase the supply of homes for sale, and decrease potential buyers. For sure, the house that is sold is usually eventually bought, so inventory is not changed. But not all homeowners sell a home and then buy a home.

READ THE ARTICLE that I linked in the comment you replied to.

Its like these people never once in their lives played musical chairs.

I get the math – while this may have little impact on the numbers, i sold my house to an internet buyer last year – never put it on the market – took their quote and sold. So, was my house ever in the inventory of houses for sale – i think not. When the internet buyer sold it is was a +1 sale (I think?).

While this number may be a fraction of the total in the US ( i have no idea of the magnitude) it is still a number

where did you move to? Did you buy another home, or rent, or move to Mexico…? That’s the real question here to determine if it was +1 -1 =0.

I was looking to move up from my starter home the past few years, but I’m glad I didn’t. Instead, I’ll remain in this small home I’ve been improving for 20 years and pay it off here in a year or two. 💪👌🤙 Good luck selling your monopoly money Boomer mansion, likely funded with massively inflated real estate gains. *I sure as hell will not be paying for your over indulgence. 🫡😁. …yes, I’m aware my home is valued higher than it should be, and I’m fine with a haircut. 😉

Gabe. This old fool wants to say congrats. Spent my life doing the same thing. Moved the family numerous times to rehab a personal residence and do it again and again. No taxes to pay either on your gain.

Medium price data is very misleading as Wolf has posted many times before. But right now affordable houses (low end) are selling in less that 18 days on the market here for full price. Every piece of crap is selling. We appraised a house the other day that had a freight train carrying hazardous materials passing right through the back yard. Another one was a condo in a crime infested, drug infested cesspool in Chinatown DC which was as bad or worse than the Tenderloin district of SFO. Realtors are starving because there are no listings. Its’ all about supply and demand.

Everyone relax. As Wolf mentioned RE is not crypto. It’s not stocks. It does not go down 20% or 30% in a day or a month or even a year. These things take a long time like a slow-motion train wreck. The last housing bust took at least 5 years! This deflation of the bubble will take time.

I have this idea to start a housing bust trade school. All the out of work house flippers, RE pumpers, RE Agents and RE skimmers of various kinds can come to a kind of work camp where they can learn useful skills like sewing wallets, fixing hydraulic jacks, feeding chickens and sharpening scissors. Since Jerome knows he kicked these folks to the curb, and they were once his pets, he might feel guilty and kick in for tuition.

In bay area (San Jose) prices started going up in last 2 months. houses going up over $150k of listing price. For houses in the range of $1.1M to $1.4M

Nah— not seeing that at all. Down YoY. Maybe there’re some isolated instances of sellers mispricing homes far enough below market value to stoke some mania — but that’s not the same thing as what you’re intimating.

It’s really telling the way that so many RE bulls come to this site. Why would they do that? Because they are very alarmed by the truth that is exposed by Wolf. Truth is deeply feared by these people. So they make up nonsense and report it in the hope that it might somehow influence readers of the comments. Consider this: Wolf provides data that tells the truth very clearly. The RE bulls have little other than anecdotes that can’t even be verified. Gee, I wonder who’s correct.

On RE threads I advise to only read Wolf’s comments and skip all of the rest because these threads get inundated by lying RE shills. It gets exhausting having to filter their nonsense everytime one of these threads gets started. So I just do ctrl-f “wolf” — and voila, much better experience !

In other words, those among us with resources are thriving while everyone else is, well, living what is commonly referred to as ‘life’.

I don’t know how housing market would turn up but using my little brain, I see that this is the worst time to buy a house and best time to sell if you have 2.

Unless people become very rich, can’t see people able to afford homes at these rates or rates go down quite a lot.

*people can’t afford homes at these prices or prices are falling a lot.*

Even my 11 year old son figured it out

Wolf – In my market, home prices remain stubbornly sticky high, there is very little inventory, new listings have crashed, and homes still sell quite fast. It is shocking to me how resilient this market continues to be at 6-7% rates. I am a buyer on the sidelines and being patient has backfired on me and my family. I think what we have to consider is the old location factor. So let’s say the headline says “prices going down in Portland”. Ok they are going down a lot more in the city, but hardly at all in the sub/exurbs. This is what I am seeing and so if we say nationwide house prices are going down, we’ll yes and no. Take SF for example. It may have higher percentage drops than other areas that are not dropping at all, or very little. Also house prices down 3%.?…yawn….Give me a break, they just went up 35-60% in 2 years! Powell is not doing enough QT, no MBS SALES, he still has rates at maybe neutral or negative versus real life inflation. There is no meaningful and impactful fight vs inflation at all. Plus the govt will do crazy fha loans, 40 year loan mods, on and on lol of which keep inventory low and prices and property taxes high. House prices have been bumping higher since January and this seems much more than seasonal to me…we will see. Not good for buyers at all.

Buyers and Sellers create the market, we all saw what low interest rates and extensive QE does and open markets and speculation. There is no pot of gold at the end of the rainbow for RE, normalization or decline is all natural. There will always be areas of the country where extreme wealth has the upper hand to keep the pinions out. The free money monsoon has ended, you got a 2.65% mortgage and tons of crypto and stock market gains. The cherry on top is now money markets and T-Bills collecting 5-6% ROI. I’m staying my foxhole, life is good.

Same old song and dance with the housing market. It’s actually quite shocking that 6-7% mortgage rates haven’t generated a steeper YoY drop in single family housing prices. Strong employment, healthy wage gains and underwhelming supply are likely preventing a steeper decline.

Lots of people my age (late 20’s to mid 30’s) are still looking for houses despite lofty prices and high rates. Should you continue sitting on the sidelines paying 3000/mo for rent or wait two more years for another 5-10% decline in housing prices? You’re hosed either way. The only way we see a stronger decline in housing is if the economy tilts into a legitimate recession. Even more demand destruction + forced sales from job loss.

I mentioned this before but was shot down when I said my realtor friend told me there is plenty of demand. Just not at current prices. So that is why any housing downside will be limited unlike the HB1 run for the doors crash.

I am curious, since most people house price they can afford is limited to the monthly payment. What is the size of the house (3 bedroom or 4 bedroom) and what is a monthly payment you would seem reasonable for that size of a house.

If housing drops, that is were the prices will find support IMHO. This low sales volume means there is pent up demand growing MOM.

During HB1, by 2008 and 2009, builders over built and wanted to unload as fast as they could when they could not find any buyers. Anyone who wanted to buy a home bought a home from 2003 to 2008 and the demand dried up. The demand was gone at the same time as excess housing stock.

This time we still have a lot of demand/interest and no excess housing stock. (that could change as builders are building a lot of units).

Of course this is all regional. Cities that have a negative net migration probably has an excess of homes while place in the Southeast with positive net migration are struggling with low inventory.

But we have lot of supply coming in , in the next few quarters.

There is no dearth of supply of new homes.

Once the psychology shift ( if it shifts ), then there would be stampede.

On top of this, there would be forced sale.

For years I was told the adage, “for every 1% increase in mortgage rates, home prices drop 10%”

Whatever happened to that? Shouldn’t we be seeing minimum 20-30% drops by now since rates increased 3%? It seems the fed’s trillion dollar MBS buying spree has broken the transmission mechanism between mortgage rates and home prices. Or maybe I’m being impatient.

Anyone have a better explanation?

Yes. 20-30% is the % when adjusted for inflation over a 3 to 5 year downturn.

The current 3.4% YoY drop nominal is actually a 9.4% drop when you correct for YoY inflation of around 6%, so 3 years at a real drop of 9.4% YoY and you have your 30% drop.

Also, do you think we will go another 2 years without some type of recession or slump? Forced selling increases when unemployment increases from a 50 year low.

No. During the GFR the prices went down by actual percentage and that is what everyone means when they talk about prices going down. Not some odd calculation for inflation.

In my area during the GFR prices went down 40 – 70% depending on town and neighborhood. I’d say an average of 50%. For reals.

I’ve never heard of that “adage” and I’ve been around a long while. It doesn’t make much sense. If the rates are extraordinarily low, as they have been, a 1% rise in rates will have a different impact than if rates are at 6% and move up 1%. In markets with high average income levels, the impact will be less than in markets with lower average incomes. Just a wild idea… “Rules of thumb” are good if you only have two thumbs; not good if you have 8 thumbs and only two fingers.

That adage he stated has been around virtually forever.

The adage probably means a 1% increase means a 10% less purchasing power.

But I saw a 4 quadrant plot chart on VisualCapalitst comparing rising/dropping house prices vs rising/dropping mortgage rates from 1992 through 2022 (240 months), . Basically their conclusion is housing prices and mortgage rarely drop simultaneously per month. Only 2% of the time.

Only 6 months did house price declined when mortgage rates YOY rose during the same month (2%). 44% of the time, housing prices rose when YOY mortgage rates rose. Probably because the housing market it hot and the FED is raising rates.

What was interesting is that 20% of the time housing prices dropped when mortgage rates dropped. That is probably because we are now in a recession and housing is dropping and the FED is dropping interest rates.

Maybe their needs to be calculation that shows housing prices 6 months after a rise in mortgage rates.

The percentage of people paying all cash for homes has risen sharply compared to the distant past. Also foreign money is not affected by interest rates.

Actually foreign buyers are all time low and so are cash buyers.

where do you get these data ?

Any AIRBNB influence here? Everyone and their mother want in the game. Easy money.

Home prices simply dropping is not fair. We need a debt jubilee for all of us true americans who keep the american dream alive by owning a home. I love my subdivision. My life has been so much better since we moved to this house. I don’t understand why property taxes are so much. Can’t they be less? Ugh. And why was wood so expensive when we needed to build a deck over a year ago but now it’s like a regular price. Being in HR and my hubby being a in finance, we do pretty well but it doesn’t leave enough extra for the kinds of vaccays we like. Probably going to be selling the camper and side by side later this year just because it’s not worth it right now. Plus hubby has student loan payments restarting. I should probably be glad he’s sterile from all the chemicals, i’d hate to get pregnant right now. Kids would totally kill our budget. If the government starts up that child tax money thing again that they were doing during the pandemic I might try to get pregnant. Hopefully the government does the right thing and makes one of those debt jubilee things for home mortgages like i keep reading about lately on a lot of the news websites. I come here to see what’s up because I want to see if there is any info on the jubilee here. My boss at work likes this website.

This is hilarious. I hope you meant it to be hilarious. Either way, it’s a true jewel of humor.

Truly hilarious :-)

Thank You!

“…all the chemicals.”

Indeed!

Would help if you add /S but if this is serious then may I ask where you located, sounds very South OC like to me..lol

And to imagine we live in a modern world with a cumulative financial model and a great financial crisis to guide us through times like the pandemic , ZIRP for ever period. Bigger homes cars refi and ever increasing assets with unlimited work home vacations !

WTF are you drinking lately? Your drink mix is going to be worth billions 🤣🤣🤣 ARE you really an educated person? Or pure an SIMPLE really clueless and stupid. OMG😲🤦♂️

Same thing in Germany. From the FT:

German house prices fell at a record year-on-year rate of 6.8 per cent in the first quarter of this year, as higher borrowing costs and weaker economic growth took their toll on Europe’s largest property market.

The federal statistical office said its index of German residential property prices fell at the fastest annual rate since its records began in 2000.

Where I live in Markham, Canada inventory is down to 1.3 months and every new build sells out the second the sales office opens.

Saw that in 2007 too. Others saw that with tulips, but they were buying tulips much faster.

People are really something.

I have a friend complaining to me that he is trying to sell his 2 homes for last 1 year but he could not. I asked him why, he said, he could not find buyer at his asking price:-).

He’d do fine as he is renting them out.

People who invested in real estate have come out quite ahead in their life and prices in my hood have gone up 75% in last 5 year or so. These tiny drop of 5-7% would do absolutely nothing to affordability.

Let’s see how things look after couple of years.

All the magic of J Powell, serving the rich masters.