That arbitrage is now happening among homebuyers. But regular homeowners wanting to sell haven’t figured it out yet.

By Wolf Richter for WOLF STREET.

Homebuilders, unlike homeowners that want to sell a house, are not emotionally attached to prices. Their business is to build homes and sell them, no matter what interest rates are doing, and they cannot sit there and wait, praying, “and this too shall pass.”

So, unlike many homeowners that are thinking about selling, homebuilders started cutting prices in the fall of 2022, and they used mortgage-rate buydowns and other incentives to stimulate demand for their unsold inventory that had been piling up. And it worked. Cutting prices enough always works.

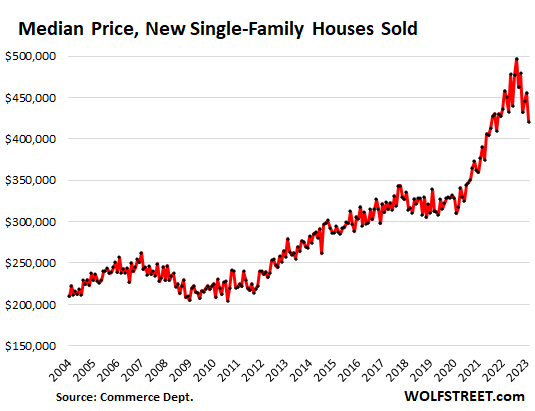

The median price of new single-family houses sold in April fell to $420,800, down by 8.2% from a year ago, and down by 15% from the peak in October, according to data from the Census Bureau today. This does not include the mortgage-rate buydowns. A different measure, the average price of new single-family houses dropped by 11% year-over-year to $501,000.

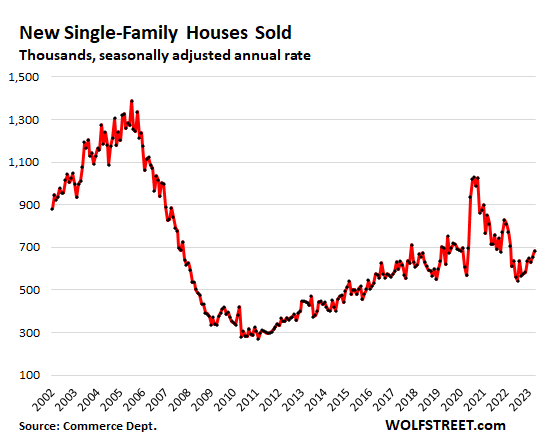

Sales of new houses, in response to lower prices, mortgage-rate buydowns, and incentives, ticked up to a seasonally adjusted annual rate of 683,000 houses.

Not seasonally adjusted, and in terms of actual sales, not annual rate, homebuilders sold 62,000 houses in April, just a hair below April 2019, but far below the booms during the pandemic and during Housing Bubble 1 from 2001 through 2006:

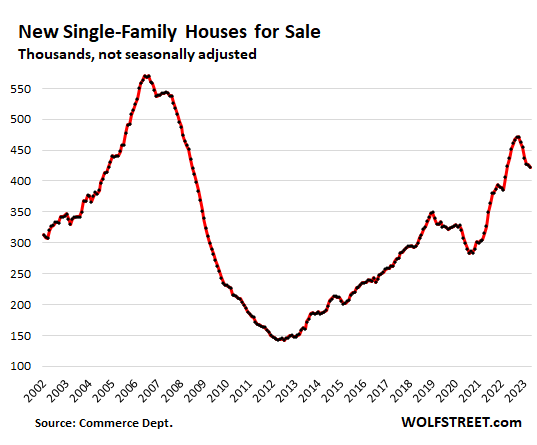

Inventory for sale in all stages of construction declined to 422,000 houses, not seasonally adjusted, roughly even with April last year, as homebuilders succeeded in working down part of their pileup of inventory.

Supply has come down too, from an astronomical 10-month supply last July, to 7.6 months in April.

Arbitrage with previously owned homes.

Homebuilders, by cutting prices when homeowners were loath to, have attracted some buyers that would have bought a previously owned home.

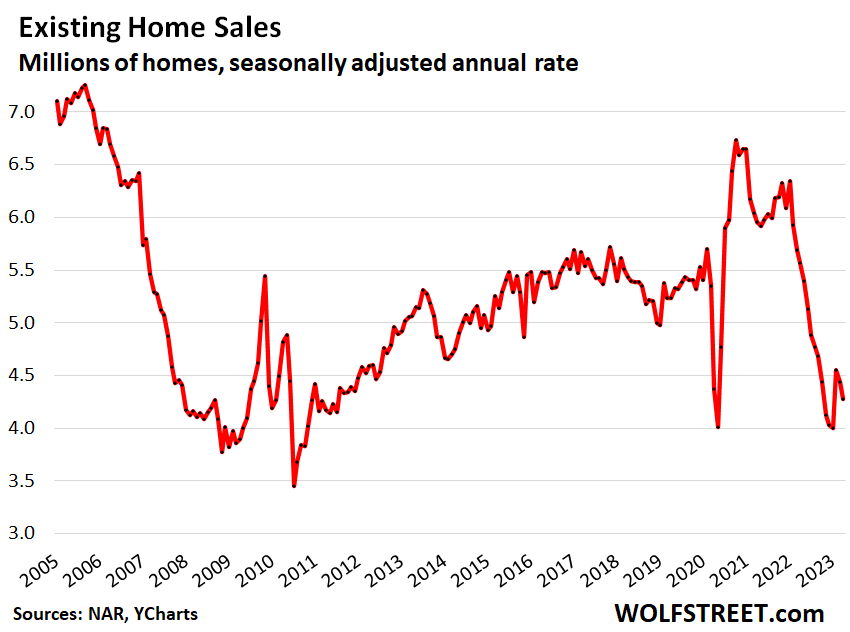

That arbitrage is now happening among homebuyers: even as price cuts and incentives brought sales of new houses back to 2019 levels, sales of existing homes fell again in April to the dismally low levels of the bottom of the lockdowns and then of Housing Bust 1.

While prices of previously owned houses have also dropped, they’re down only 2.1% year-over-year, and sales have plunged, as potential sellers are still trying to outwait this situation, while at least some buyers have switched to buy from the pros that know how to offer deals.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

If the prices doesn’t significantly drop, then home builders will be happy to build and sell them at (market top – 10%) prices. With lumber etc prices at pre pandemic level, they can still make money. It will eventually lead to over supply.

The real estate agents are still selling the idea that real estate always goes up, instead of educating sellers that there are no buyers at this price point because mortgage rates have made houses 50% more expensive to buy even at 2020 price.

Soon an agent will drop here claiming that his city is different and house prices are still increasing and there is lot of demand and ver low supply.

Exactly. I was looking on Realtor.com and the average days on market in many places has increased to around 50% from less than a year ago. But realtors will still claim everything is selling like hotcakes.

Well priced houses are selling fast where I’m at.

Leo,

“instead of educating sellers that there are no buyers at this price point ”

There are no home buyers left???? Look at Wolf’s chart. We will have over 4M house sales this year.

There are LESS home buyers due to affordability issues and LESS transactions (sales volume) due to lower demand and very low inventory. That doesn’t meant there are no buyers.

We finally bought!!!!! A new construction, thanks to the builder for the rate buydown and discounts. We are beyond happy to finally get our first home!!!

Another real estate agent posing as a knife catcher?

If not, do keep checking how red your hands get. Many folks tried this stunt around a year back and are now very frank about their home being underwater.

Leo,

Look, don’t blame people for buying a house. It was a dream, and now they finally turned it into reality, for better or worse. Without people like Richard, there wouldn’t be any home sales at all, and the market would just dry up completely. So now the Richards are going to spend a shitload of money to furnish the house, and buy towels and chairs and a couch and a grill for the backyard, and what not, and consumer spending, adjusted for inflation, will jump noticeably. And the Realtors are going to get paid, and they will spend the money, and consumer spending will jump further. And then the taxing authorities will extract their pound of flesh from the Richards, and then they will spend the money thus extracted, and government spending will jump further. All of this spending combined will cause GDP to leap, and it will cause inflation to rise further, which will cause the Fed to hike rates further, thanks to the hard work and sacrifice of the Richards in buying that house. That’s how the economy works.

Congrats on the home purchase!

Thank you Bs ini! We are stoked!

And wolf, yep, plus we gotta figure out the BY and FY landscaping. Since this is a new build home it comes with a dirt lot. A pool would be nice but neighbors have told me they spent north of 100K to get a pool. That doesn’t include the surrounding landscaping and FY.

Maybe in a few years we see low rates again and home values increase and we get to do a cash-out refi. Fingers crossed.

Agreed Wolf. I cannot assume that Richard is a real estate agent. Also he is right that there will be home sales irrespective of how insane the pricing is.

Richard may be a genuine first time buyer who could not control his happiness, so had to post this to defend his book.

Congrats Richard.

However, that doesn’t change the core logic of my comment. Richard most probably bought at a very wrong time and he would realize it over the next year.

Wolf, read your own articles from 2020 and you would realize that you wrote that housing was a bubble even in 2020. So, today priced 50% higher at a 50% higher mortgage rate, housing is effed up.

I too am closing on a new build in two weeks here in the Bay Area. I was offered a 2/1 buy down from their “preferred lender” but was able to get a fixed 5.375% from a bank that I have a relationship with.

I have a family with small children and looking for stability to raise them in a safe environment. Not all of us look at home like an investment. It’s like shoes or cars, some people buy them for their utility. They break and you either replace them or fix them. At least you got to enjoy them. As long as you’re able to afford the payment and keep on investing, building your business, and making money. You should be good. People need to wait for the right time to buy an home and the right time is different for everyone. It really depends on what stage of life you’re in. If you’re young enough why not live in a SRO in Chinatown make money save on living expenses and spend it solid investments. Once you get married and have children then you will need something else. Particularly safety for your young ones and your lovely woman.

Real estate is not always an investment, sometimes it is just a home.

Looking for a home,

Congrats. But after you close, you gotta change your screen name 🤣

Leo,

Your comment on “bought at the wrong time” doesn’t make sense to me. As long as you don’t overstretch and as long as you can comfortably afford the home it’s a good time to buy. Timing the market is impossible IMO. We got the house we wanted. I don’t need to justify it or gain confirmation by others. I just shared it because we are insanely happy with the purchase. There is a saying: the best time to buy was yesterday. The second best time to buy is today. I believe this applies to stocks and RE. Are there ups and downs in the stock market. Sure. Just dollar cost avg and ride out the waves. In RE, time is on your side. 19 years from now people probably wish they could buy the house at todays prices. It’s all relative. I am not worried about RE prices going down for a couple of years. That’s a blip on a chart. A blink of an eye. We will most likely spend the next 30years in this house and my kids may inherit it. By that time RE will likely have tripled in value. Buy when you can afford it and enjoy it, create memories. The rest is noise.

4m sales this year is down 2m from pandemic high (-33%).

Useful metric for measuring just how much the Fed’s central mismanagement of interest rates (money printing) distorts the US housing market (50% volume hike on phony baloney rates).

And the Fed’s post 2009 perma-baloney, goosed sales volumes to a typical 5.3m per year, even while inflating/fellating median homeprices (largest living cost expense by far) upwards by 40%-100%.

Congrats on purchasing a home that brings you happiness.

Don’t let people like Leo get you down. There are always doomsayers. I am always surprised by the arguments the doomsayers make which are often conflicting (oddly, they ignore those conflicts).

For example, on one hand they will bemoan the rate of inflation, expecting that inflation will be outsized and sticky for a while. On the other hand, they say home prices are insane and are due for a huge fall.

They cannot see the conflict in those statements.

My thought is that if you can afford the home right now then you will be fine. If inflation is truly going to be outsized and stick around for a while then eventually inflation will take care of any reasonable overpayment of the house you buy.

Even if your salary doesn’t keep up with inflation on a year by year basis, it will still increase somewhat due to inflation, but your loan will never get more expensive (unless you get a variable rate loan, then beware).

My guess is that home prices will decline ever so slightly and very gradually over the short/medium term, but inflation will keep prices close enough to current prices not to make a big difference over the life of a 30 year loan.

This is a good point I hadn’t thought of. Thanks.

Around here in “Swampland” there is such a shortage of homes for sale that buyers are purchasing “dogs” just to get a starter home. We did one last month in a marginal area, that had a freight train running right through the back yard of the house. Some dude bought the home and moved in and is happy as can be.

My predictions for debt ceiling outcome, The Most probable scenario:

1. An agreement will be reached to print $3.5 trillion per year backed by taxpayers.

2. The markets will rally 10%, so will crypto crap.

3. 10 year will fall below 3.5 again.

4. Both parties will celebrate victory as they throw cents at their constituents while handing taxpayer funded trillions to the “To big to Fail” to make them bigger.

Leo

YEP, gonna be a long ride this time though. May take decades for any kind of normalcy. This should be greater than the 70s 80s ride. Time will tell…

Disagree. In one corner, enter Marjorie Taylor Green with Matt Geatze or whatever. In the other corner, enter Alexandria Octavio Cortez & the crazy rep from Seattle area.

These people don’t care what their leadership wants. I kinda want to see what happens if a deal doesn’t get done…

Yellen would be a yellin’, Jerome would say something needs bailing out cause it’s too big to fail and, our guy- the one and only, Lawrence Yun would go on CNN and tell everyone it’s a great time to buy a house.

But aside from thinking this thing drags out for weeks, you’re probably spot-on.

Only takes a few GOP to cross party lines and the deal is done. MTG doesn’t matter.

Not gonna happen. The Former Guy said default. Anyone who doesn’t fall in line will be primaried.

That’s not the case anymore with the new rules in the House of Representatives, it’s no longer a matter of a few party-crossers because the House has radically change it’s way of doing business in a way we haven’t seen in over 200 years of American legislative history. To get his speakership after more than a dozen rounds of balloting, Kevin McCarthy had to give in to demands that a single Congressperson–not 20, not 10, not 5 or 3–one member of Congress, if dissatisfied, can halt all House business and call a new Speaker’s election. That means in practice that basically any single member of the House can filibuster, basically has veto power over all House business. The Freedom Caucus pushed a hard bargain there for exactly this reason, it doesn’t matter if a few members of Congress want to cross the aisle, if even a hint of that were to start to take shape, then a member of the Freedom Caucus can throw down the gantlet and halt all House business, kicking out Speaker McCarthy. And that’s all she wrote.

Ten year yield won’t fall if the treasury is allowed to increase issuance. Most likely it will go up, but that assumes a rational reaction to increased supply, and there ain’t much rational behavior anymore.

The Federal government CANNOT ‘PRINT’ any money at all. Markets are set to fall significant as RISK OF DEFAULT SOARS across all levels of the US economy, and that will cause INTEREST RATE TO CONTINUE TO RISE dramatically in the years ahead.

Wolf,

I don’t see how buying now, at any price, isn’t a ticket to the Knife Catchers convention. Interest rates still have room to rise and inventory of investor-owned is still big, AND the speculative froth of the last three years hasn’t come off for prices. They need to come WAY down so that they are even close to correct ratio with wages.

Living in the Seattle area for now fifty years, i lived through a one hundred fold increase in prices from when my parents bought a starter house in Bellevue for 23,250$. Houses in that same neighborhood now go for 2.3 mil.

West Coast real estate has to be the greatest bubble in the history of humanity

You must not travel a lot. Bubble prices are spread world wide and in some cases put the now dumpy west coast to shame

This is because monetary insanity has been worldwide. If the CBs are really shifting back to more normal policy, RE will suffer for years.

If they keep slapping Vancouver, Canada real estate with more and more taxes like the 3 percent empty home tax, just like back on April 20th 2017 more and more money from the Chinese will move to Seattle.

Or the best investment in history

Ok, you say interst rates have room to rise (I agree with you by the way).

Why would they rise? Because of high inflation (duh…).

So you think home prices are going to drop in a high inflationary environment?

That doesn’t make sense.

As someone currently having a new house built, a second issue is that – at least in our area – the price of new homes had gotten way out of line with value even relative to (also extremely high-priced!) existing homes. The prices that we were quoted by the many builders that we consulted were so far out of line with what a similar house would cost that we almost gave up and sold the land that we bought for the purpose. And we could see the same phenomenon for other new houses on the market. Prices for new houses needed the downward relative adjustment that they have been getting over the past year.

Cordelia Congrats on your new home

The following is just a general comment from an old fool. Old fools way of thinking was to purchase a starter home. Small, used, needing updating, and guessing times have changed for the majority of people? Mind my asking? Ist home, 2nd?

To retire to, actually. We wanted a small house and couldn’t find one in the place we wanted to be. Hope it turns out okay!

YEP, Dont let the worry in. Congrats again. Life is good.

We are building a retirement home too. However, we are building in Mexico in a beautiful ecological community. There is so much building going on here it’s hard to believe that everything isn’t just peachy. Here you have to pay cash as there really aren’t mortgages. I figure might as well put the money in something real as keep it in dollars. One thing that has been troubling is the peso’s strength. Overall we will be retiring to a stunning home at about a quarter of the cost as a similar home in the USA and without most of the craziness up north.

Starter home always smacked of NAR propaganda. I guess it can work, but I never saw anything starter-grade that seemed worth the sweat.

My first wife and I rented below our means for several years to hold out for the house we really wanted…it was a fixer, too — but worth fixing.

From what I’ve read, many foreign investors prefer either condos or newly built homes. They and large conglomerates are in a large part the ones paying cash. Like Wolf says (over and over) someone selling their current home to buy one other home does not influence the market much.

Makes sense. If I were invested in buying homes far away and ruining that economy for it’s citizens, there is no way in hell I’d buy used. Too many variables and long distance managing construction has to be difficult to say the least.

I think also all these “internet buyers” both foreign and domestic are beginning to learn their lessons while being stuck with rotting studs and faulty foundations covered up with paint and cheap vinyl flooring.

That’s LVP sir! High grade 5 star LVP!

Nothing better! Unless of course you count any wood product, or tiles or yeah real wood. Gosh real wood is nice. Look, let’s not dream here pal. You’re getting the good stuff! LVP ;)

I lived overseas for 15 years 5 different countries and expats from foreign countries would buy USA housing in California and Florida or condos with cash for their retirement plans and rent them out. The transactions were usually cash

Agree strongly. Stagnating price appreciation while carrying costs increase could make investors look elsewhere for gains. All it would take is for a couple of the big players to decide they are overweight residential in their portfolio. Say rates are anywhere near 5% or higher in 2024 then many pandemic buyers will be looking at 3 years in a row of price-downs, which would be enough to call it a trend, and the nasty question of “When will this stickbox make money?” starts to creep in. The forces of finance and demographics and are aligning in a way which to me could accelerate home prices to the downside. The only wildcard is if the US congress decides home price depreciation is bad for business.

Tom S. yeah, it will take that.

But really, the only way for the US to break this new cycle of global investors ruining housing for our own citizens is to put a cap on investment in residential properties. SFRs should not be an investment, period, and any multifamily units need a severe cap unless they are actively being rented out. Foreign ownership of more than one unit, both in whole and in part (stocks) should be illegal. And Enforced.

The problem is our congress people are highly invested in this model and are selling our basic necessities on the open global market. They need an incentive to stop it. Both parties.

Maybe some more cities will burn this summer as extra food stamps disappear and the homeless population grows.

It’s nice to finally see some real YoY median price declines.

One can only hope this continues throughout 2023 and brings a recession in 2024 to finish the job. Next up, let’s get new car prices falling.

Deflation across a wide range of products is needed to corral inflation.

If prices go down but interest rates go up I am not that the real price a home has gone down for the buyer.

Of course the seller gets less money

Not all brands have excess supply. Stellantis does. GM does. Ford does. Honda and Toyota, not so much. Per Automotive News

The best thing to happen for the American economy would be a housing crash in the 50%+ range. The parasites would wither, and young hard working people would flourish.

Agree with the benefits. Aside from that, it would end the relentless “tap home equity” to fund the future game many homeowners play. 👌 People tend to think the asset bubble really just applies to stocks…WRONG. 😱

Correct, but many peoples brains would explode from reverse wealth effect…even though they could buy a bigger better house for the same price.

Amen!

Why do posters on this blog want to see great misery afflicted upon the American people?

Posters here just want sanity back to asset markets which is enriching 1 percent at the cost of middle class.

You may not ask this questions if you can see the big picture

Exactly! I want my 27-year-old daughter to be able to afford a home.

The converse to Apple’s question is:

Why are so many people happy with housing doubling in value in as little as 2.5 to 4 years which is the case for a good portion of the US housing market?

On what planet do these people think this is healthy & won’t lead to long-term affordability issues?

They’re probably are going to be the one screaming for rent & mortgage relief once the going gets bad.

Jon,

Yes, the poor and lower middle class have been left behind with housing, stock gains.

Many in the middle class have done well. They bought homes 2012 thru 2020.

Ben, below…

“They’re probably are going to be the one screaming for rent & mortgage relief once the going gets bad.”

Over 1 million homeowners have already gotten assistance from the government to keep them in their homes. Its ongoing. Some received a 30% reduction in mortgage payments, tacked onto the back of their loan.

See January 30th, 2023 HUD document “Expansion of the COVID-19 Recovery Loss Mitigation Options”.

The misery has already been inflicted. A housing crash would right the wrong.

I’m sorry but inflation is the big misery. My prop taxes in Texas are now slated to increase 10 percent a year since the market value of my home increased 60 percent. The 10 percent cap is built in. I could get taxed and insurance premium out of my home and my electric costs have gone up 50 percent. Inflation becomes the norm. I am retired on no income but interest income. I can not afford inflation. I am miserable. A change would remove my misery.

You certainly get what you vote for in Texas. The legislature is all focused on drag queens this session ( which ends next week ).

Maybe when they reconvene in 2026 they might act on fixing your issues.

Apple,

How does continuing the asset bubble and inflation make people less miserable?

But there’s been so much inflation. Where’s the true bottom? Because the bottom has been steadily raising while sellers are holding and buyers are thinking.

In Texas about 50 miles north of Houston. I am looking to downsize as I am now a widower. New tract homes are being built in several rural areas near me: Builders are cutting all trees down and plopping 1,500 – 2800 sq. ft.” stick built homes down. Some are already sold and have “For Rent” sings in the dirt front yards.

I looked at one this weekend (unguided tour) and they are very cheaply thrown together with low end appliances and fake wood floors. Pricing is about` $200 per sq. ft. although, the builders are offering discounts of 10% or thereabouts.

Real crapshacks in areas where there are no trees or any shade for that matter. I saw some young couples in a few yards. No landscaping is included and there are no yard sprinkler systems installed for the ones I walked. Real hot boxes when the outside summer temps hit 105 F.

There are a few of these areas under development around here. According to my friend who is a licensed RE broker, the builders are trying to sell the inventory and if they don’t find a buyer by the time a house is completed, it becomes a rental for around $2 + K per month.

Ahem — luxury vinyl flooring! Italian-grade plastic!

The undying appetite for ugliness is really something to behold.

You can say that again. Design for houses these days was inspired by funeral homes!

“Oh I love this room, what’s it called?”

“The Embalming room”

“So hot! So in. Rufus, are you getting pictures of in here? This room goes in the book.”

I went to a hardware store to buy a linoleum knife, to use to divide hostas. Nobody knew what I was talking about, (what’s linoleum?) but I did find one there.

Shiloh – an ultimate result of the ‘self-serve’ economy, as product knowledge and history slowly fade from the purchasing departments (mostly gone from the counter for cost reasons…).

may we all find a better day.

@Anthony A,

My condolences to you.

Harvey, I’m not buying those crapshacks. I’m holding out for an older home in good condition. No rush needed on my part.

That sounds like a good plan. I gave you my condolences because you mentioned that you are now a widower. Houses are just houses.

“Low end appliances” used to be normal appliances. By all means, get the cheaply made stainless steel fridge with incomprehensible circuitry that will break down in five years and cost a fortune to repair/replace. And our forests are just flush with mature hardwoods waiting for cookie cutter homes. Those laminates, despite some being tough as nails, are extremely inferior to high maintenance hardwoods!

Appliances and floors are replaceable fixtures and finishes. If someone can be bamboozled into paying $30,000 more for $5,000 in additional finish costs then more power to the seller.

What you need is a well built home, especially in Texas, where mother nature can be a b@tch. Will it hold up to rot, hurricanes, floods? That’s what matters. But buyers are enthralled with things that don’t matter instead.

Yes, I stay in one of these subdivisions during the week for work. They took every tree down in sight. Insane and ugly, yet expensive. DR Horton community.

A big part of homeowners’ reluctance to settle for lower prices may be perfectly rational, having to do with many facing a big step up in mortgage rates. If you’re comfortably ensconced in a 2-3-4% mortgage and looking at your costs to borrow for your next home, you may be calculating you’re better off staying put than selling at a much lower price.

I think being “rate locked” is a big factor in people not wanting to sell unless that have to.

That is why high unemployment is needed, which will cause some of these people to sell

But will that actually happen if they can’t rent for any cheaper than their mortgage payment? People have to live somewhere.

I would imagine the banks will work with folks to keep them in their homes (and the payments flowing) rather than kicking them out and taking the house.

MM,

Rents are now much cheaper than mortgages in many cities. I watched someone make the comparisons.

He made the case it was twice as expensive in Seattle to own vs. rent.

Other cities from 20% to 80% more expensive.

Of course it needs to be an apple to apple comparison.

Typical mortgage here on 400k home is around $2500. My rent is $825 for a 1 BR.

In this case its not an apple to apple comparison.

But no. I dont want a larger place.

You are right about banks.

Over 1 million homeowners have already gotten assistance from the government to keep them in their homes. Its ongoing. Some received a 30% reduction in mortgage payments, tacked onto the back of their loan.

HUD has a January 30th, 2023 twenty-two page document that explains the assistance in detail.

This has already happened with us in 2020.

Banks imposed a moratorium on loan payments. But this lasts for 1 year. No bank could afford it for much longer and then it was force majeure with covid. So there will certainly be such an action, but it depends on how broken the labor market will be.

1) Apr dots : new single family home sold : 62K. In construction : 263K.

Completed, but not sold : 70K. // 62K + 263K + 70K = 395K total inventory.

2) Turnover : 62K sold/ 395K total inventory = 16%. That’s a disaster.

3) The banks will tell the home builders : add money, or we takeover.

4) The multi family reached the 1973 highs. The difference : in the 70’s most multi were built in the salt cities : the Bronx, Queens, Bklyn and LA.

In 2023 in the flyover.

A note to homeowners who are selling — homebuilders can drop the price even more and still make a very nice profit. Material costs have come down substantially from the peak and most of these builders have sat of the land since before 2020.

Superior product (new home) at a lower price + lower financing costs (temporarily) vs. inferior product (used/old home) at a higher price. Not a hard decision.

Also home builders always squeeze the contractors.

Newsflash: New homes are not always a “superior product”. Many are made with new growth lumber (weak), OSB (chip board), and unproven technologies.

Think of the synthetic stucco rage of the 90’s…. was great on paper until people realized that it trapped moisture because they had no clue how to apply it nor maintain it. The homes rotted from the inside out.

Yes, many lawsuits and insurance claims on EIFS. Even with good products it must be installed correctly.

But they already overpaid for the land, development & gov regulations.

I agree in general (that’s in part why I got a new build 2 years ago), however:

1) timelines – most new builds are slow, much slower than promised. My house took 12 months to build instead of promised 6-8 and based on what I see around it got worse lately (no idea why). Some lots have a foundation and nothing else for 6+ months.

2) price flexibility – someone who bought for 350k in 2021 may gladly sell for 450k today. Some people would say it is a market crash as this house could’ve been sold for 500k a year ago, but others would say it is still a 100k gain out of nowhere in just 2 years.

Interestingly, #2 is what is going on across the street from me – last Saturday a For sale sign popped up and today the house is already listed as Under

Contract on Zillow. We had cars coming in an endless stream all weekend. Apparently there are still lots of buyers out there, enough to put the house priced right out of the market in just a few days.

I do not know the USA, but around here the best spots where built on hundred years ago.

And as other have pointed out, new build may not equal better quality. A lot of houses where built a hundred yars ago or more. Not all standing, but those standing have proved build quality.

Exactly my experience. Closed yesterday on a built to order home that original buyers didn’t close on and builder was motivated to sell.

Moving from Austin, where we don’t put enough cops on the street, to New Braunfels, with cops living down the street…

Nice choice! Hill Country!

Hah. Lived here 30 years, and I cam attest that there cops-o-plenty in Austin.

If only we had a lot more cops in every city, town, and rural area the world would be a much better place.

LOL!

If only Uvlade Texas had more than 307 cops show up one year ago….

I’ve watched the new construction all around me. If you want to live as a millennial professional in a sterile clinic box at twice the price per sqft fine. I’ll take the older places with bigger spaces and private wooded areas and mixed cultures. And I am very happy to report that the mixed group of children resulting from the increase in families are very well behaved and a credit to their parents.

Yep I’ll take classic all day long too. Got some room for elbows around me and don’t have to mow the field if i don’t want to. ;-) This whole new is better concept, on average, sounds like a sales pitch to me considering what I see going up around here.

In the sunshine state, every new development has the houses built too close to the street, and most houses have 4 or more cars in the driveway and street. It feels claustrophobic to drive down the street, and would be incredibly dangerous to humans walking around (since there is no visibility around the dozens of cars everyone) if there were any humans ever seen outside. Cars everywhere but no sign of people. No trees either, even though there are beautiful, hardy trees that could provide much needed shade, they all get clear cut to jam a house, strip mall, or some form of pavement on every single square foot of land.

1) Higher interest rates reduce RE value, including new home prices.

2) The DC split might nuke the Dow. There might be a short term solution to kick the can down, sending SPX to 4,500/4,600, but Saint McC are no Newt Gingrich. They might say : Niet !

3) It’s a payback for all the harm that was done in the last seven years.

4) Investors are complacent as they were in Dec 2019 & Jan 2020.

5) If the gov use the fourteen amendment Moody and S&P might reduce US gov rating.

Zillow has my Portland home price going up 3 months in a row now. Also Zillow now predicting 3.9 percent house appreciation this year thats up from old prediction going down 1 percent.

Nothing goes up or down in a straight line

Just look at the big picture

The population of Portland has now declined for a second year in row ( like SF) but Zillow and home owners still imagine that prices can keep going up. More new single family and multi-family units are being built every day. I don’t see how these two trends ( more supply and reduced population ) won’t come together in drastically reduced prices in the very near future.

Zillow is junk. Use case shiller. Everything else is junk.

Zillow could say your house is worth 45 trillion dollars and that would be just as meaningful and accurate as any of their current estimates.

They had revised down the last month’s number sold, too. I guerantee they’ll revise this one down too.

Is it time to sell new home builder stocks? Their stock prices have been rising against the data that says sales and prices are coming down. Toll Brothers has had a nice ride.

So how are they making money? If labor and material prices are not coming down, they must be getting the land dirt cheap (no pun intended).

One advantage of many older homes over the new lower cost 3/2’s is more street frontage. This means you have a living room looking out onto the street. The econo boxes are typically on narrow lots, so you have a bedroom window as the only way to see out front. The rest of the frontage is taken up by a 2 car garage. I guess you can just stare at your ring camera to see what everybody’s up to.

Much nicer to look at the backyard yard instead of the frontyard / street. We looked at many older homes and remodeled older homes. It’s a turn off…..the outside looks, the floor plans. It’s just a different feel to buy and live in a new construction. Plus our new community has lots of younger professionals with kids. Versus older communities you deal with Karen’s and older people that have nothing better to do than to be in your business. Often, older communities have no hoa either. So if a Neighboor decides to have his house painted green or trash all over his BY it bring your house value down……no thanks.

HOA as a selling point is a new spin.

And anyway, who cares about the value of your home? It’s going down for a while anyway, irrespective of your neighbors (gasp! shudder) green house. Just live your life and stop worrying about your Zestimate.

Well no……my in-laws bought their first house in a Hoa free zone. They still live there. Yes over time some gentrification happens but man, it’s a rough hood with all kinds of crap going on. Some houses are very well maintained while others go down the drain. Some yards are nice while others are a train wreck. Some neighbors play their music too loud and have trash all over their BY. Would you wanna live there and invest in such a community? Hell no. An hoa cuts a lot of that crap out. Buying a house is not just for the moment in time. This is our biggest investment. So location is key to ensure the asset increases over time. Buying a house in a HOA free community is a risk I am not willing to take. Walk through a neighborhood that has an HOA and then compare that to one without an HOA. Night and day. And you will see at least one bright green house or maybe even pink. :D

Richard,

Respectfully, that just sounds like the way that neighborhood is… nothing to do with the absense of a HOA.

I specifically purchased in a neighborhood w/o a HOA as I didn’t want another governing body charging me $$ and telling me what I can and can’t do on my own property (my city already does this).

Its a wonderful neighborhood: no run-down properties, loud music, or trash in the streets. And if I have a busy week at work and don’t get to cutting my lawn as often as my neighbors, no one bats an eye.

HOA is a good thing ?

Risky (who are the members, what if they get replaced by bad people). Property taxes and HOA increase with time.

You seem to want everyone to know just how much you love your new home a bit too much.

I bought a lovely new home in 1986.

Economy tanked in Texas. 10 years later sold for 8% loss. Home was in excellent condition. No one posts these things except me.

What doesn’t increase over time? There is no perfect solution but some people like me prefer an HOA. Time will tell, maybe I think about it differently in a few years once I had more experience with them. I said it a few times already, I have seen and experienced myself just how bad certain neighborhoods get. Some people rather pay a monthly fee to have the neighborhood maintained (which ultimately means higher property values) over calling the cops and city. I think not many people post these examples of yours online because most people sell their house at a very nice profit? House prices more than 5 folded since the 80’s. And of course I am a little out of my mind excited right now. We are first time home buyers. Waited a looong time for this. My wife can’t stop smiling.

…people. Can’t live with ’em, can’t live without ’em…(as the Firesign Theater opined: ‘…we’re ALL bozos on this bus…).

may we all find a better day.

This excerpt from an article in the San Diego Union Tribune seems to back up that new home builders are aggressively pricing their product to move. Resale SFR is up from last month as are resale condos, but newly built are down from last month.

“Resale single-family: Median of $900,000 with 1,416 sales, up from $880,000 last month. Down from its peak of $950,000 in April 2022.

Resale condo: Median of $651,000, with 777 sales, up from $650,000 last month. Down from its peak of $663,000 in May 2022.

Newly built: Median of $798,000 with 168 sales, down from $801,000 last month. This figure combines single-family homes, townhouses and condos. It is down from the peak of $890,500 in August 2022.”

Source (paywalled): https://www.sandiegouniontribune.com/business/story/2023-05-23/people-waiting-for-prices-to-come-down-will-be-disappointed-san-diego-home-prices-rise-again?utm_id=98537&sfmc_id=404290

This article basically says this in the headline..

People waiting for San Diego home prices would be disappointed.

San diego home prices rose for the last w months .

Basically it is saying not in San Diego

Nothing goes down or up in a straight line

The home prices are yet to catch up to increase in mortgage rates

It’s happen for sure albeit bit slow

If you can get past the paywall and read the whole article it definitely paints a different picture of what’s happening here and details some of the many reasons why. I did find it interesting, though, that despite things being hot in San Diego the newly built pricing was showing exactly what Wolf presented in his post.

Thanks

It means the headline is misleading

I would like to see a ratio chart of average earnings to house cost, say from 1940 to present.

In the 1950s, when vetrans needed to buy houses for their 3.5 children to grow up in, average salaries for both blue and white collar men was, what? ..

Unions made blue collar salaries enough to raise such families, and in the 1960s the middle class spread out to all these burbs, and people in North America felt “upperly mobile.”.

Now a poorly built working class tiny home in Toronto’s Beaches on a busy street costs around 1.% million.

Judith, that’s a difficult comparison. Average (or median) earners are not the buyers of average (or median) homes. That average for earnings will include a lot of kids, young adults, immigrants, and other low paid workers. None of them are home buyers. Well, except in the “become a real estate millionaire!” infomercials.

Maybe you could construct a comparison of the top 70% (or whatever) of earners against the median home price. Something like that. I dunno.

My Grandfather built and sold houses on his old dairy farm in Salem Oregon when he retired in the late 60’s and early 70’s. Nearly all of the people who purchased his one story ranch homes were state workers who had a very narrow pay range and this locked in the final price that could be financed. He always complained that no matter what he did he could not get more than $17,000 for a house.

It’s really interesting to see how the prices fluctuate on new construction that has been listed for a while. Where I live there is a house that was first listed in April 2022 and has been active since, including one pending sale that must have fallen through in Feb of this year. The listing prices are as follows:

Feb 14, 2023 $749,990

Nov 5, 2022 $674,990

Oct 18, 2022 $724,990

Oct 17, 2022 $674,990

Aug 26, 2022 $799,990

Jul 27, 2022 $854,175

Jul 19, 2022 $853,975

Apr 15, 2022 $853,175

Maybe I’m oversimplifying, but the range seems borderline insane. If a new house can be offered for sale in a years time for anywhere from $675k to $854k depending on what is the perceived market value, then the margins must be huge, and there is little correlation between price and cost.

At some point, assuming money isn’t dropped from helicopters, I think the builders are going to drop their shorts in order to sell these places. Real estate comp valuations are based on the greater fool theorem, and we may be running out of fools.

Sorry not in my neighborhood as everyone in SoCal, especially in South OC and West LA still saying… don’t forger the ones from SD too.. /s

DM: Rents have risen almost TWICE as fast as incomes since 1999 and now swallow up to 30% of earnings – but it’s still less than the average mortgage… unless you live in these four metros

Rent growth is outpacing increases in income across the country – adding to the financial squeeze on tenants. Average rents have increased by 134.9 percent since 1999, while incomes have gone up by 76.8 percent in the same period.

The Moody’s analysis found that, in 2022, the proportion of American household income needed to rent an average-priced apartment breached 30 percent for the first time in 25 years of tracking the trend. The benchmark, called rent-to-income ratio (RTI), fell slightly at the start of 2023 to 29.6 percent.

Separate research by Refin found that only four metro areas in the country have average mortgage prices that are lower than average rents. The four areas where mortgages are highest compared to rents are all in California.

Does anyone ever look at the historical charts? It’s eerie how the last 2 years mimic 2006-2007. Can anyone recall how 2008 turned out?

Will be interesting to see what happens over the next few months to see if more inventory comes online, and what that will do to pricing.

The 7% mortgage rates are back already, as of last week.