In the free-money era, subprime auto lenders took huge risks amid seething demand from yield-chasing investors.

By Wolf Richter for WOLF STREET.

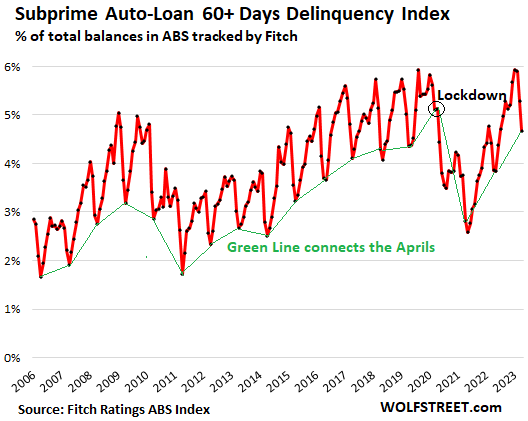

Let me just start with this chart of subprime auto-loan delinquencies of 60 days and over in the Asset-Backed Securities (ABS) rated by Fitch Ratings. In recent years, the worst delinquency rate was set in August 2019, of 5.93% of total balances, nearly matching the all-time worst record of 5.96% in October 1996. Then came the free-money era, when delinquencies plunged. When the free-money era ended, delinquencies spiked, and in January 2023 hit 5.93% again.

Every month since then, delinquencies declined. In April, they dropped to 4.67%. But wait… The drop was entirely seasonal. April is usually the month with the lowest delinquency rate of the year. If not April, then May is the lowest month. So in April 2023, the delinquency rate of 4.67% was the second worst April ever, behind only the lockdown April 2020. The green line connects the Aprils:

The reckless deals of the Free Money Era.

Auto loans are rated “subprime” for the same reason a lot of bonds are rated “junk” (BB+ and below): the borrower has a much higher risk of defaulting on the debt. And investors take big risks to make lots of money.

Subprime auto loans account for only about 14% of total outstanding auto loan balances and leases. The remaining 86% are prime-rated. Subprime auto loans are generally concentrated on older used vehicles with smaller amounts financed.

These subprime delinquencies are not a sign that the overall consumer is getting in trouble or whatever. We can see that because prime-rated auto loans are in pristine shape with a 60-day delinquency rate of only 0.2%, according to the ABS rated by Fitch. In other words, nearly all delinquencies are in the relatively small subprime-rated pocket of auto loans, and the prime delinquency rate remains near historic lows.

But these subprime delinquencies are a sign that subprime lending by specialized lenders had gotten very loosey-goosey, with ridiculous Loan-to-Value ratios and super-loose, often AI-driven underwriting standards. And this was particularly the case during the free-money era of the pandemic.

Subprime is teeming with abuses and scandals. Some subprime loans come with such high interest rates that practically guarantee the loans will default. Occasionally regulators crack down, but settlements and fines are just part of the cost of doing business.

The risk-taking is driven by potentially high profits, and by the ease with which a vehicle can be repossessed and sold at auction.

A lot of times, customers with subprime credit ratings tried and failed to get financing at a regular dealership, and they ended up going to a dealer that specializes in the subprime end of the business, a high-risk, high-profit business.

And periodically, specialized subprime auto lenders collapse, as we have seen a couple of dealer-lender chains do this year. These dealer chains held on to the loans they wrote, and once a year they securitized the big pile of loans into subprime auto-loan Asset Backed Securities (ABS) and sold them to investors, such as bond funds and pensions funds, while retaining the equity portion of the ABS.

These ABS are structured to where the lowest-rated slices take the first losses, and get wiped out first, but they’re also sold with the highest yield to compensate investors for taking those risks. As the losses increase, the holders of the higher slices begin to eat them. The highest slices might carry an “A” rating when issued, and they’re sold with the lowest yield.

Delinquency rates of these subprime auto-loan ABS had fallen to low levels during the pandemic, when the free money was washing through the system. But then they rose back to the high levels of the pre-pandemic years, plus some.

And subprime auto-loan underwriting had gotten very loosey-goosey because there had been huge demand by bond funds and pension funds to buy subprime auto-loan ABS because of their higher yield, in a world where yield had been repressed by central banks. These funds were chasing yield, and these private-equity-backed dealer-lenders made a ton of money supplying those ABS to the yield chasers. Then the loosey-goosey loans turned sour, and the Fed hiked rates, and two of those chains collapsed.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

But, but unemployment is so low jobs go begging. Hey Wolf, looking at when this article was posted I was wondering if you ever sleep.

Good article.

The total subprime auto loan amounts seem to be too small to stress the whole financial system like subprime housing loans did in 2007.

I bet that many ABS will remain “A” rated till their yields cross 50%. Our rating agencies are so good.

Yes, subprime auto loans outstanding are only about $240 billion. And they’re backed by vehicles. So if ALL of them default, and the vehicles are sold at a 50% loss to the lender, then the total loss would be about $120 billion, spread over investors holding those ABS, many of them overseas.

I’d like to invest some funds in an Asset-Backed Securities (ABS) fund that pays up to 30% interest rates on high risk auto loan securities. How can you go wrong? Any names of funds?

I remember a saying about canaries and coalmines…

And while “just” 15% of auto loan balances are subprime, I have to wonder how mutable the definition of prime/subprime may be in concept/practice (it might be hard and fast on FICO scores, or it might be based on some rating agency definition – opaque or not, or it might be defined ABS loan doc by loan doc, etc).

And it isn’t like the auto industry created the ginormous, credit-based, lending ecosystem beast (85% of all auto “sales”) because they were able to move as much iron as they wanted to/could…the auto-credit industrial complex is likely really only a creature of the last 30-40 years (Wolf, can you provide historical insight into its growth?).

With that “high consumer-credit will maximize revenue” mindset and that “sell that doggy debt off as soon as we “underwrite” it attitude…I don’t know if “prime underwriting” standards are particularly sacrosanct in an industry that hasn’t been able to lift annual sales above 17 million since *1977*.

In other words, things may not look like they are about to blow up…until they blow up…especially in a macroeconomy “founded” upon pyramiding debt (see DC).

Ditto underwriting “standards”…which are only standards until they impact sales.

FICO scores define “subprime.” Depending on the credit ratings agency, subprime is either below 600 or below 620.

The cause of any credit or financial crisis is psychological, always. That’s what cuts off credit to marginal borrowers and leads to defaults.

The US and much of the world has had the loosest credit standards in history for decades complimented by artificially cheap financing for over a decade after 2008.

What’s been considered “normal” in lending is historically reckless. It’s somewhat different now but not much. Most credit standards across the board remain at basement levels, though maybe not always sub-basement.

Along these lines, some drug addicts are functional…so long as they keep getting more drugs.

(How do think investment banking/legal “analysts” work 18 hour days, 6 days a week?)

That doesn’t mean things are “okay”.

It just means the gerbil wheel is spinning faster.

See “debt-based” “economies”.

Cas127 had a friend tell me he was a functioning alcoholic,painter was his trade

An old song from the ’80s

I owe

I owe

Its off to work I go

ed

I think Mr Wolf is going to be awake for a long time. 70s 80s are returning and that Disco music stuff ? Forget about it. Whats coming should keep everyone awake.

The big difference is that back in the 70’s once a used car got too old or poor a condition you could not get financing on it at all ( maybe loan sharks). The financial establishment was much stodgier and more risk averse in the days before Mike Millikan. This meant there was a big pool of used cars that had to be sold for cash. This of course drove down their cost so that a high school kid could afford to buy a car with his ( or her) savings from working a summer in fast food. When I was in high school ( late 70’s) you could pick up a Charger or a “Goat” or an Impalla SS for a few grand since since they were gas guzzlers and adults didn’t want them anymore. Not sure what high school kids do for cars these days.

Cars last a lot longer than in the 70’s. Toyotas and Hondas are still running at 200,000 to 300,000 miles now.

I’m not good at sleeping, but I try 🤣😍

Wolf, try reading some of the current Budget Proposals before bedtime. If you don’t get nauseous first, your eyes will roll into the back of your head and sleep will soon follow. Happy Memorial Day to all.

“Up here on the ledge

I’m getting pushed to the edge

People line up behind me to step into my shoes,

Up here on the precipice

I’m getting close to my nemesis

People fighting each other to jump into my blues

There’s a young kid inside me somewhere

He stays up all night, a vampire that never dies,

With the blood and the moon in his eyes

I hear his voice when I’m comin’ down,

Sleep is for fools, who never see the sun rise,

Who never get to live twice.”

-John Entwistle of The Who

DanRo – think Wolf must sometimes feel like the title of Entwhistle’s solo album: ‘Smash Your Head Against the Wall’. Fortunately for us, Wolf’s head remains diamond-hard!

may we all find a better day.

you didnt explain why april is the low – tax refunds!

Another example of the expected lagged impact of the rapid rate hike cycle. This will continue higher and will be amplified as unemployment starts to increase in coming months.

Wolf…

Have you seen the Fed’s 1st quarter

Federal Reserve Banks Combined Quarterly Financial Report?

It seems the Fed hasnt issued one…..and its almost June 1

That usually comes out between something like May 25 and June 3. So any day now.

Just what else did any reasonable person expect to happen?

A “security” backed by maximally insecure loans is even sillier than Bitcoin. Anyone who puts money into such nonsense is either a sucker or a smart tax-loss seeker.

It’s literally almost always bought with someone else’s money.

That’s called a loan ,and uncle provides it at about 10-1 system is in sustable

…and so it begins.

What begins is that the price for reckless auto-subprime lending during the free-money era is now coming due. And so two subprime-specialized dealer-lender chains, backed by private equity firms — they were among the worst perpetrators — have already collapsed this year.

Prime auto loans, about 86% of outstanding balances, are in pristine condition.

All this and more was miraculously revealed in the article.

“Prime auto loans, about 86% of outstanding balances, are in pristine condition.”

Never, ever go “subprime is contained.” Ever.

Just remember: banks do NOT own this stuff. These ABS are held by investors. And they got paid to lose their shirts.

Same with stocks, other bonds, cryptos, etc.

My understanding is that prime auto loans are for new vehicles mostly?

If that’s the case, we might see the uptick later on, since those loans are actually given for longer period of time these days. I haven’t bought a new vehicle using loan in forever, but I remember standard loans be 3 years max with payment of $400/month. I now see loans for 84 months (due to higher prices of those vehicles, I imagine). In Midwest many cars are eaten through with rust underneath way before that time. Using $50,000 as a price, I can imagine people getting tired of paying $500-$600 for a rust bucket (depending on deposit).

Your understanding (1st line) is not correct. “Prime” auto loans are taken out by buyers with “prime” credit ratings. Any loan to a customer with a “prime” credit rating is a “prime” loan. People with prime credit ratings buy new AND used cars. They buy whatever they want and can afford. They buy most of the 1-3-year-old used cars that now cost $25k+ (rental cars, lease turn-ins, etc) that not many subprime customers can afford to buy.

Subprime customers have trouble buying a new car, or even a recent-model used car. Many of them have to buy older cars. The subprime business is really just a small part of car sales.

Got it now. Thanks.

A high tide will float all boats higher but a significant storm will sink the most fragile.

I was flabbergasted when Wolf wrote that these, toxic securities were being purchased by pension funds. Aren’t pension funds required to invest in high quality fixed income???

The top and biggest slices were investment grade and were highly qualified for pension funds when they were issued. Pension funds are going to eat a lot of this stuff. They were among the worst in chasing yield.

Calpers, the pension fund that ate California.

The story of their investment strategy=pin the tail on the donkey.

And wall street dished up the junk, as they always do.

Ted T.,

It’s a good opportunity now to look at the fund allocation, performance numbers and unfunded obligations of your city and state pension funds. You’ll find some surprises.

Another canary in the coal mine report. The data shows the lag impact of the failed easy money approach and that the jobs reports are misleading. Neither the JOLTS report or employment reports have meaningful data that can be tested. For an example, someone losing a good job and finding two part time, low pay jobs looks like a win for the economy. The reverse is more meaningful.

Wolf, is there any particular reason why October ’96 and August ’19 were the high-water marks for this metric? Offhand I can’t think of a good reason why subprime delinquencies would peak in those months.

I think there was a natural recession in the works in the months leading up to COVID. I think Trump put a halt to interest rate increases by Powell by threatening to fire him to protect wall street in late 2018 as the signs of recession were presenting then. By 2019 the writing was on the wall. COVID really interrupted that recession and eliminated the signs with all the stimulus. Now we just have the massive inflation to deal with and eventually a much steeper and more prolonged recession hangover.

A President cannot fire a Chairman of the Federal Reserve.

There was a HUGE subprime bubble in the early 90s. It wasn’t called “subprime” at the time, it was called “special finance.” There had always been small “note lots,” but this was different. It was new and on a large scale with “special finance” companies springing up. I was running a big Ford store at the time, and I saw it first hand as some franchised dealers got into it on their franchise lots. I looked into at the time, and it was a horrible, slimy, risky business that a reputable franchised dealer should never get into, for a variety of reasons, including that it might ruin the reputation, that was my feeling back then, and is today. You treat all customers the same, and if you cannot get them financing through the regular channels, and if you cannot switch them to a lower-priced vehicle that they might be able to buy and could afford, well then, you lose the deal, and that’s OK. By the time I left the business in late 1995, the whole thing was already blowing up, amid lots of wailing and gnashing of teeth. That’s what you see in the chart.

Starting in 2014, we were getting another yield-chaser easy-money bubble after years of QE, and by 2018-19, some of the specialized subprime dealer-lenders (also PE firm backed) were blowing up. I covered some of that at the time.

…sounds like an aged-up distribution of ‘participation trophies’…

may we all find a better day.

“Subprime is teeming with abuses and scandals”

The entire industry seems sketchy at times, so “subprime” fits nicely in the scheme of things. And having just bought an auto last week at 18.3% under MSRP, it is a buyers market for some brands, although you need a pair of high waisted waders to wade through all the bullshit.

For example, I got an extra $2500 off by financing a tiny portion of the auto through Chrysler. It plainly says you pay off the loan immediately without any pre-payment penalty fee. Kick-backs of this illogical nature seem sketchy but sure, I’m guessing a majority don’t pay it off quickly so Chrysler wins on average, just like Vegas?

And then I get asked to give a perfect 10/10 review by the sales guy. So 72 hours later I give 14 “10s” on a multi-page review out of 15 questions, but gave the finance guy a “9” out of “10” as the person was completely lost and had to leave three times to ask questions to upper management.

A day later I get a text from the salesperson:

“So your 9 you gave me on Finance screwed me man. It’s a zero I don’t get 50$ This is why I said every question. Is what it is whatever”

—————

Wolf- how the hell did you work so long for the auto industry this sketchy, stupid, and full of bullshit? Was it better decades ago?

I personally think the entire industry should be allowed to fail and let the best companies take over the old auto giants that would never even exist today without repeated govt bailouts the last few decades.

The socialized corporate losses with capitalized corporate gains has somehow worked so far. Perhaps the next generation to stop the “abuses and scandals” we call current day “capitalism”, as our generation is simply not.

The “10 out of 10” nonsense was a byproduct of J.D. Power and Associates “customer satisfaction survey”. Awards were given so people started gaming the survey. Manufacturers often tie bonus money to the dealerships to their “client satisfaction” score – which it sounds like the dealer shares it with the sales consultants.

The finance game you describe is stupid for the manufacturer, but good for the finance arm. Why? The manufacturer usually pays some subsidy to the finance company – similar to a mortgage buy down – in order to provide more competitive rates. Since the buy down occurs (aka “booked”) at the issuance of the loan, the finance company keeps the subsidy, even if you pay it off shortly thereafter, thereby increasing the finance arm’s profit. The dealer still gets his commission for placing the loan as the payoff is considered the first payment so there’s no recourse.

Many years ago I was driving a semi truck heading to L.A. when I had to stop in Ontario, CA to find a tire dealer to replace a steering tire that had blown out.

I found a Goodyear dealer that was able to locate a tire for me. I got to talking with him while waiting and he explained his subprime business model.

He would sell tires to the Mexicans in his area and finance them himself. He would structure the 2 year financing so that if the buyer made the payments for at least a year, it would cover his costs and include a profit.

Any payments made for more than 1 year were a bonus. Most of the buyers would stop paying after a bit more than a year and when nothing happened, they spread the word.

He had a very good business with a lot of customers.

How is that a good business, if he kept letting them go away with not paying? Next they will stop paying after 6 months and then what will he do?

Nissan- presumably (as this is an anecdotal recounting) the number of those who defaulted too-early was small and didn’t get a second bite at the apple while the $terms to those who played the game for the year, generated a volume of business that was acceptable to the dealer’s bottom line, the default risk closely priced in (as in any prudent, credit-based commerce). Sounds like the dealer knew his market (a significant number probably undocumented, for this dealer, probably a feature, not a bug), and the issues of doing business with it…

may we all find a better day.

Field report from out west. The new car market may be settling down. I have been shopping for a new minivan. New, because used car prices are so close to new car prices, it doesn’t pay to gamble on possible problems.

Anyway, dealers were all quoting $4000-9000 above sticker. I backed out of negotiations because they wouldn’t budge an inch. A day later they offered 2500 over sticker. When I didn’t reply to the email, they dropped it to sticker. I was already in the process of paying sticker for the same car at another dealer. They both mentioned they wanted quick sales to make quotas.

So, if you are seeing crazy prices tell dealers you are ready to buy right now. Then don’t accept the high ball offers. Things are loosening up.

If economy falls farther,cars will be much cheaper. Or if uncle blows up economy,people begging to sell For anything they can get remember depression pictures of people selling nice cars for 11$

Paying msrp for a grossly overpriced car is simply not an acceptable endeavor, IMO. 30% off sounds good.

Is there anything special about subprime auto loans? Will this default pattern repeat itself for other risky loans, like certain small business loans, certain home loans, and certain personal loans?

It already is.

I’ll post this advice for the second time for any who missed it. In 1978 I bought a used 1976 Camaro 350, 4 barrel, 4 speed, and had it for 12 years. The salesman recommended I pay the car off (it took 18 months back then), and afterward keep putting the payment into savings so I could buy my next car for cash. I have never borrowed for a car since.

Did just that starting in 2018 (listened to a lot of Dave Ramsey in college). Me and the wife now drive two modest, paid-off vehicles and stick $600/month in a sinking fund. Been ready to upgrade at least one for the last two years but I am not willing to blow the whole wad on such overpriced cars. Frustrating! Should be able to wait things out a few more years, so here’s to hoping sanity returns.

We have made payments to ourselves on all big ticket items. We continue to make our monthly “house payment” even though we haven’t had a mortgage since 2003. Ditto car payment. It’s amazing how quickly you can amass a nest egg by doing that simple task. In addition, you don’t have to take a bank loan next time. Borrow it from yourself and repay it. All it takes is a little discipline.

I just read the article on Wolf Street about the delinquency rate in subprime auto loan-backed securities, and it provides a thought-provoking analysis of the current situation in the lending market! The article highlights the concerning trend of rising delinquency rates in subprime auto loans, emphasizing that April experienced the second-worst delinquency rate ever recorded, only surpassed by the lockdown period in April. It’s important to understand the potential implications of easy access to credit and the impact it has on borrowers’ ability to repay their loans. Thanks for sharing this informative article, as it sheds light on the potential risks associated with subprime auto lending. Keep up the great work!

As someone who looks at credit reports all day long, you would be AMAZED how many people have car loans north of $1,000/month. I don’t know what the average is, but I feel like the average borrower I see has a car loan somewhere in the $600/$700 monthly payment range.

EV’s and $75,000 pick up trucks are all the rage right now. Average home owner sitting on $180,000 in imaginary credit equity until the actually sell. Orlando, FL is still the number one vacation destination, $YOLO so spend like it is no tomorrow. America is made to consume depreciating assets, its in our blood. Garages full of pelotons, and $300 month payments for solar panels is a must where I live.

I feel that 20 – 25 years from now this is going to be looked back as one of the golden ages of investing.

Right now there are so many crazy/rare forces at work in numerous markets. There is inflation constantly driving up prices. In conflict with this is asset prices which are generally considered overvalued. Huge forces pushing in opposite directions.

It is taken almost as gospel that most financial assets are overvalued. This is probably true, but most does not equal all. When accounting for inflation, I have a strong feeling that far into the future that looking back there will be certain narrow sectors of assets that will end up being very cheap compared their future value.

Decades from now, people will jealously marvel that someone was able to buy certain (narrow) assets at crazy cheap prices. Thing is, these asset classes will be very narrow and there are lots (and lots) of asset classes that are going to get crushed.

Great time to be alive if you have lots of excess buying power and an intimate knowledge of those classes.