Only 2% of credit card users are delinquent, according to new data from the New York Fed; 98% are current.

By Wolf Richter for WOLF STREET.

Credit card balances are among the most misreported data points out there. They’re largely a measure of spending rather than borrowing. Credit cards are the dominant consumer payments method in the US. Credit cards were used for $5.8 trillion in consumer transactions in 2022, up 18% year-over-year due to a surge in spending on travels and other services, and due to the surge in inflation at the time.

Banks charged merchants $126 billion in credit card processing fees in 2022, according to Nielsen’s annual report on merchants’ processing fees. That $126 billion in fee income is why banks love credit cards, and why they push credit-card kickbacks such as 1.5% cash-back, so people will use their credit cards to buy stuff so banks can get their cut from every purchase, often around 3% from the merchant.

Most people pay off the card every month by the due date. But reported credit card balances are statement balances and show all balances, including those that will be paid off a couple of weeks later and will never accrue interest.

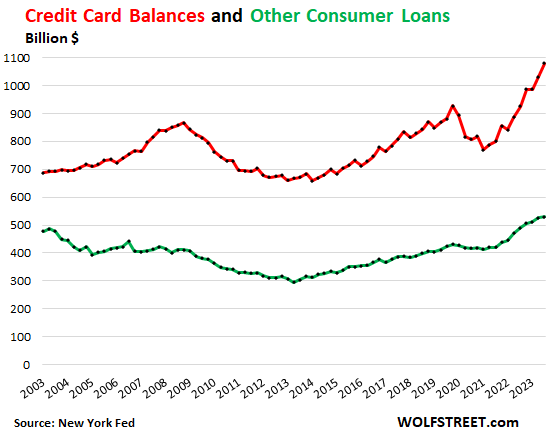

Credit card balances (red line in the chart below) rose by $48 billion in Q3 from Q2, to $1.08 trillion, according to the New York Fed’s Household Debt and Credit report. Year-over-year, credit card balances rose 16.6% on higher spending for services such as travels, restaurants, and entertainments, and on higher prices.

“Other” consumer loans (green line), such as personal loans, payday loans, and Buy-Now-Pay-Later (BNPL) loans, were essentially flat in Q3. Unlike credit card balances, most of these “other” balances are interest bearing, but not all. BNPL loans are interest-free for the consumer and are subsidized by retailers. This data is not adjusted for inflation.

Earlier, we discussed how consumers were dealing with their housing debt: Mortgage & HELOC Balances, Delinquencies, Foreclosures: How Are our Drunken Sailors Holding Up?

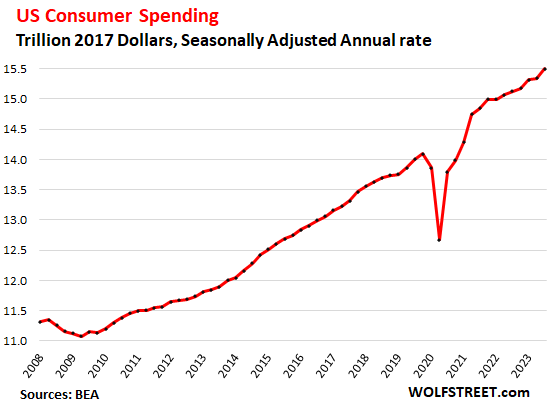

Consumer spending, even adjusted for inflation, has been on a crazy growth binge despite high interest rates, and we call them Drunken Sailors for that reason. But a record number of people are working, and they have received the biggest wage increases in four decades, and they’re making more money than ever before, and they’re spending some of it, and they’re still able to save a portion of their income.

Below is consumer spending, adjusted for inflation (via 2017 dollars), in the GDP release that caused Powell to tear out his hair. By contrast, credit card balances above are not adjusted for inflation.

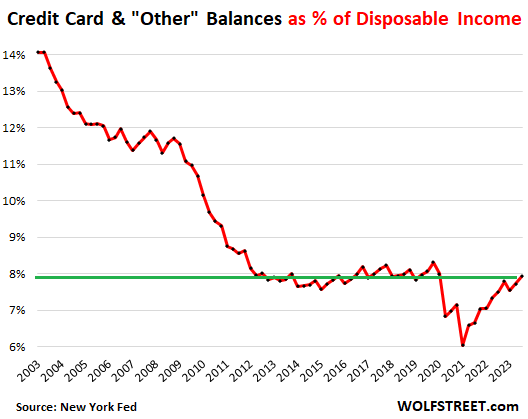

The burden of credit-card balances normalizes at low levels. Credit card balances and “other” consumer debt combined in Q2 of $1.61 trillion amounted to 7.9% of disposable income. Disposable income is income from all sources except capital gains, minus taxes and social insurance payments; it’s what consumers have left to buy stuff and pay off their credit cards.

The spike in disposable income during the stimulus era caused the ratio to plunge to record lows. The burden of credit card balances and other consumer loans has now come up from those record lows but remains below the Good Times before the pandemic.

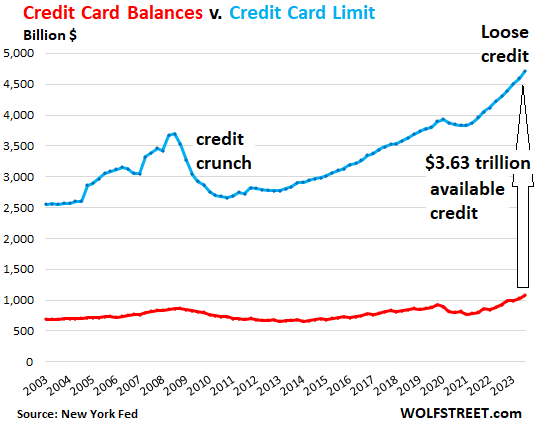

Credit is not tightening. Banks have raised the aggregate credit limits on credit cards to a record $4.7 trillion. With only $1.08 trillion in credit card balances outstanding, the total available unused credit rose to a record $3.63 trillion.

This growing amount of available credit shows that there is no sign of a “credit crunch,” though the small subsegment of subprime might experience a credit crunch – that’s what we’ve seen in vehicle financing, where subprime delinquencies have jumped and credit has tightened.

During the Financial Crisis, credit limits plunged, a sign of tightening credit. There is no sign of this now, on the contrary:

Delinquencies rose from the trough as the trough during the stimulus and forbearance era is behind us.

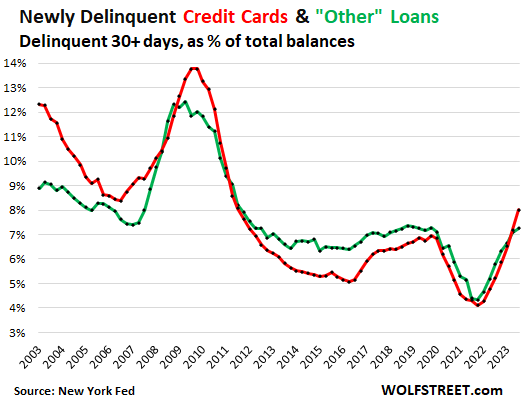

Credit card balances that transitioned into delinquency – 30 days or more past due at the end of the quarter – rose to 8.0% in Q3, higher than in recent years, but lower than any time before 2011 back to 2003. In 2019, the rate was about 7.0% (red line).

Other consumer credit transitioning into delinquency inched up to 7.3%. In Q3 2019, it was 7.2%, in 2018, it reached 7.4%; so back to Good Times levels before the pandemic (green).

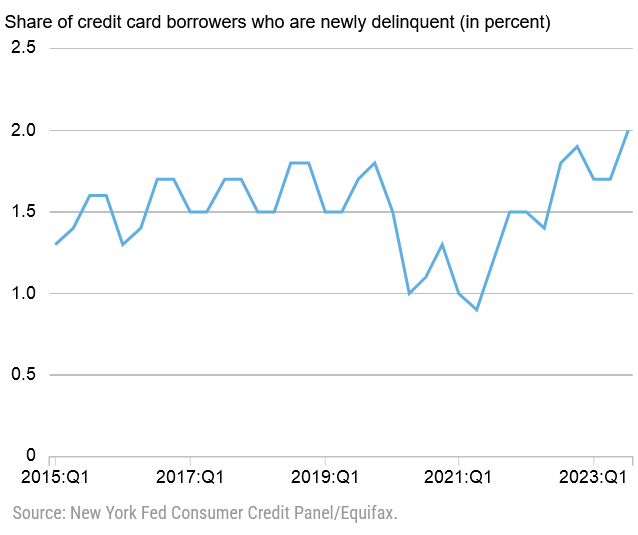

The above delinquency data from the New York Fed is based on its data from Equifax and shows the amounts that are delinquent. Below is new data from the New York Fed that shows the percentage of credit card users (people) who are delinquent.

Only 2% of credit-card users are 30+ days delinquent, according to new data from the New York Fed in a blog post, using the Equifax data and the New York Fed’s survey data from its Consumer Credit Panel.

This 2% of all credit card users being 30-plus days delinquent, while 98% of credit card users are current, that’s practically a rounding error within the overall economy. Before the pandemic, roughly 1.5% to 1.7% of all credit card users were delinquent.

The fact that 98% of credit card users are current on their credit cards — either paying them off by due date or making at least the minimum payments on time — is another sign that consumers are not Drunken Sailors, and that we use the term lovingly and facetiously.

What it does show is that this very small number of credit card users (2% in Q3) is delinquent on more than one card, and on larger balances. They’re in a heap of credit trouble, but their number is so small that when they run out of options, it has little impact on overall consumer spending.

This data goes back only to 2015; it only shows the Good Times. It would be nice to have this data going back to the Great Recession to get a feel for what it’s like when the economy gets in trouble (chart via New York Fed).

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Interesting article.

Always good to see a different perspective to much of the reporting out there.

Credit card minimum payment can be as low as 1%, so owe say $10,000 per month, you might only need to pay $100 not be “delinquent”. Yet carrying a 22% loan on a $10,000 credit card balance would kind of suggest that the individual is financially weak, as you don’t get ahead paying 20% plus rates on any loan structure, it is fiscal insanity, to be honest, end stage capitalism gone wild sort of financial instrument.

Like Tesla cyber truck “pre-orders”, a refundable $100 down deposit for over 1,000,000 cyber trucks is not a very easy statistic to calculate the financial well being of Americans. Only $100 down on a $50k-$80k product, even crazier than only $100 down on a non-recourse $10,000 loan. Kind of makes hedge fund leverage look small by comparison.

I’m curious if the statistics on the change in percentage of credit card users who pay in full each month could hold more predictive value of general credit card user health versus delinquencies. That said, it really does seem like people have more money to burn for a few more months before a possible reality check on the current “drunken sailor” spending euphoria. By mid 2024, time will tell…

On a side note, I just seen a second Bloomberg article mention “Drunken Sailors”, and it would seem like a compliment to WS as WS has been using the term for a very, very long time:

Griffin added that US fiscal spending needs to be put in order, as the country is “spending on the government level like a drunken sailor.”

The term “spending like a drunken sailor” has been around for ages, but was popularized in the mid-80s by Ronald Reagan. The idiom is more ubiquitous than you might think, so not sure Wolf gets the credit for it being used in the WSJ or BI, but it’s fun to think that our little slice of the blogosphere introduced something new to the lexicon.

Yes… but for Ronald Reagan the phrase wasn’t a joke… it was the SETUP to the joke’s punchline… “but saying that is actually an insult to sailors because unlike Congress, sailors are spending their OWN money!”

That is a point that Wolf never forgets in his use of the term. Hence the reason he says that “we use the term lovingly and facetiously.”

“I’m curious if the statistics on the change in percentage of credit card users who pay in full each month could hold more predictive value of general credit card user health versus delinquencies.”

I agree. I would also like to see that. It seems more likely that when big ticket inflation items hit like property tax and insurance premium increases, that the cash flow wobble would be first buffered in minimum vs full card balance payoffs. Temporary at first, so a leading indicator.

Don’t think the US is anywhere near end stage capitalism and we aren’t a country well versed in Marxism and dialectical materialism so going to have to live with the outcomes.

Keeping my fingers crossed though for the dictatorship of the proletariat!

The US is technically a Fascist Plutocracy, with the facade of Democratic Republic. In practice, who you’re voting for and if you’re voting doesn’t matter. The good candidates are not on the ballot, or in the corporate media. The US Democratic experiment has been dead for decades.

I would love to see, just once, someone who promotes this communist revolution junk to provide an example of it working, or when it has ever worked.

ChS – ah, but dissatisfaction, at whatever station, reigns eternal…

may we all find a better day.

Two female friends of mine pay the minimum amount on their c-card debt. They both work hard but having made choices that put them both in debt by 10s of thousands. Wish I could help but I don’t want to be a dumb a**.

TransUnion stated the average balance is $6,088, so at 20% interest, that costs $9,063 in interest over 17 years of minimum payments (CNBC calcs). Yes, such financial behavior does not qualify for delinquency, yet perhaps it qualifies as desperation instead?

^^^End stage capitalism isn’t abnormal throughout history and could last for decades, or create financial chaos in weeks. Enjoy the excess as the laws of Science and Physics can’t be conquered via money printing.

I’d even go as far as say the majority know subconsciously this can’t go on forever, and thus why the social vibe isn’t as good as it should be with all the drunken sailor spending.

Climbing the “Wall of Worry” to reach the “Fiscal Cliff” will probably not end up being exciting as the financial market cults want us to believe…HA

Yort,

“TransUnion stated the average balance is $6,088, so at 20% interest, that costs $9,063 in interest over 17 years of minimum payments (CNBC calcs).”

Wait a minute. You’re spreading unadulterated CNBC bullshit here.

I have the Q2 report from Transunion, so the numbers are a little different, but the principle is the same:

1. this $6,088 is an average of total balances outstanding (including those that are paid off by statement date) divided by the number of consumers with credit cards.

2. So in Q2, this was $963 billion in balances divided by 167.2 million consumers for an average per person of $5,972, which includes all the amounts that are paid off by statement date.

3. Most of these balances will never accrue interest because they’re paid off by statement date. The moron reporters at CNBC fail to point that out?

4. Only morons would figure 20% in interest on these balances that are paid off without ever accruing interest. This stuff is just unadulterated BS.

5. If you draw some wild conclusions and generalizations from this unadulterated BS, you will get unadulterated BS-squared, and it will pollute your brain. Drag this CNBC bullshit into here at your own risk (if CNBC even ever said this!), Yort!

Wolf, case in point, me. Typical CC bill $3k, sometimes $10k because maybe we’ll have a large item like furniture or home improvement cost. Always paid off, $0 interest.

Well your friends will either

A: get tired of the interest killing them and setup a 0% interest emergency program to help them pay those off. (They do have to close the cards)

Or

B: open a HELOC if they have a home and grab a much lower 8-9% interest rate to help them pay it off. (Versus 26%-29.9%)

I think people feel like they are in control when their spending decisions have taken them to the high interest place. But they are def not in control. 29.99% or whatever will double their balances in prob 2 years. That is serious trouble.

There is a book on Amazon you could hand them. It has some technique’s to use with the credit card issuing banks. Title is: Negotiate and Settle your debts.

@sucker in sukatash

Or

C. File for bankruptcy.

If you read the financial press headlines today, you would think that Powell’s comments were what kicked the Treasury yields higher on the day. Not so fast. It was a very poor 30 year auction where very poor demand from foreign buyers – 60%, down from 65% and higher, forced a larger percentage of the bonds into the hands of dealers (who will sell into the market).

Reading WSJ and Marketwatch, etc is completely worthless for telling the real story of what is happening financially.

“meant to hide”? The moment you disregard someone’s opinion/analysis as malicious, it shows that you really don’t have facts of your own with which to disagree but are just spouting propaganda.

Disagreement is not automatically “propaganda”, no matter how acrimonious.

The huge drop in all of these graphs since 2003 is dramatic. 2003 was before the two manufactured “crises”, so presumably typical.

The truth is that “crises”, whether real or manufactured, turn people toward caution and frugality. That’s how the 1930s worked, and it seems to be happening again now.

Bankruptcy reform occurred in 2005.

2004 was memorable as a year rife with drunken credit sailors talking at every neighborhood barbecue about getting rich (e.g., starting an online wine business) while in fact having sub-zero savings rates and running up piles of cheap credit. Since 2005 bankruptcy reform, most debtors were required to pay down (versus blow off) those debts. It was good to see somewhat more responsible personal finance in more recent years (excepting the mania of crypto, etc.). But huge snow-drifts of publicly- and privately-originated debt yet found their way onto government balance sheets, still with us.

I wonder how the changes to individual retirement contributions and the move to more mandatory contributions (escalation) at state and federal levels have propped up the market. California’s mandate on companies went from 50 employees down to 5 in June 2016. Illinois went from 500 in 2018 to 25 in 2021. That’s a lot of “dumb” money going into the market to prop things up and at least 10 other states have similar laws. Secure 2.0 is proposed to make similar mandatory contributions and escalation a federal thing. Could we support a large herd of Unicorn IPOs without this influx of broad index investments? If these contributions weigh on the overall market performance, how can we get them on a graph to help predict future water levels?

It’s maddening to see enormous government debt taken out on the life of future generations or monetized by the Fed (balance sheet) have been transferred to the Boomers for 40 years. Now the economy and the people will be much poorer because the falling rates game is over.

@Bailey,

“It’s maddening to see enormous government debt taken out on the life of future generations or monetized by the Fed (balance sheet) have been transferred to the Boomers for 40 years.”

Garbage post. I guess people ran out of class and race warfare ideas, so started age warfare.

George W’s masterpiece. Screws over anyone even thinking of bankruptcy.

Thanks GW you’re a real sweetheart

If I’m reading that chart right, consumer debt is the lowest ever (or at least as far back as thar chart goes). I’m assuming it needs to be adjusted for inflation, no?

Yes, adjusting the first chart for inflation would only make to current situation look even better.

I had read the big problem now are Millennials whom have 20k plus balances, have a car loan and school loans. This demographic is thinking of missing a school loan payment in the next few months. Also those affected make about 60k a year.

According to the news article the fed is watching this closely. As they do not want their policy to negatively affect people.

20k is a Giant problem if you make 100k, let alone 60k.

Sure, people who have lots of other debts, are more likely to be delinquent on part of it; and younger people always have higher delinquency rates that older people — part of that is the learning curve, and part of it is the big spending younger people have to do after they buy a house or start a family.

But that percentages is minuscule too, New York Fed data that you reference:

GenZ: 3.1% are behind on their credit cards, down from pre-pandemic highs topping out at 3.6%.

Millennials: 2.9% are behind on their credit cards, up from 2.6% before the pandemic.

GenX: 2.1% are behind, less than before the pandemic

Boomers: 1.1% are behind, less than before the pandemic.

Chart from the New York Fed. Data only goes back to 2015, and those were the good times. As I said, we lack a Great Recession base line:

So the data right now suggest what exactly? It seems that people are spending a LOT but not more than they can really afford, which is actually kind of remarkable. My first thought is they learned to budget during the pandemic. But that can’t be right. It’s interesting to note that delinquency trended down a lot after the GFC except in the subprime tranches. Not at all the narrative you hear on any mainstream news these days.

“It seems that people are spending a LOT but not more than they can really afford, which is actually kind of remarkable.”

Yes that’s what the data has been fairly consistent in telling us, which explains why the economy hasn’t keeled over as it was expected to, and may not keel over for a while, because for now, consumers are on a sustainable path.

But government is not a sustainable path. That’s where we have the big problem with spending borrowed money. If Congress ever comes to their senses, which I doubt, we will get a recession.

“If Congress ever comes to their senses, which I doubt”

Wolf – what’s your take on what happens if Congress *doesn’t* come to their senses?

All the articles that speculate on this seem to be fear-mongering, click-baity nonsense.

MM,

My half-assed guess, based on how they handled it last time (1990s): they will fight over it for a few years, then agree on something that will stave off the worst without really fixing the problem, and the amazing American economy will grow and create inflation and muddle through it.

What matters is interest payments as a percent of tax receipts, so if the economy grows plus creates some inflation, tax receipts will rise, and if tax receipts rise faster than interest payments, we can muddle through:

https://wolfstreet.com/2023/08/30/curse-of-easy-money-us-government-interest-payments-v-tax-receipts-average-interest-on-treasury-debt-debt-to-gdp-in-q2/

Consumers are spending a lot but they are not buying more gadgets. They are buying the same amount of gadgets or food or services but these things just cost more.

I think hotel average daily rates were mid $130 pre pandemic. Now they are over $160. A 23% increase.

Same with rental cars. I think the average daily rate was $36 in 2019 and it was over $80 in 2022. I am not sure if it is higher or lower in 2023.

On the subject of a history going back to the great recession I remember very clearly coming back (to the UK) in early 2007 after my 3 1/2 years teaching English abroad and finding out that everybody was carrying HUGE amounts of credit card debt, like 20K and because this behaviour was so common nobody thought anything of it. All spent on non-essential consumer bling. Then of course the financial crisis and the recession.

You mention the “consumer bling” that people were buying. I think this is one of the worst and most pernicious ways to go into debt — chasing bling into distant pastures. The nice things on your wrist and in your bedroom come with a cost and credit cards veil that cost by making the transaction oh-so-easy . . . the other temptress out there is the debit card — tap the Interac symbol on the reader and you’re good to go. Credit and debit cards tickle something in our deepest brains and that’s why they’re so dangerous.

That is very true. My brain is tickled by the ease and spontaneity of using a credit card. The hangover comes when I receive the bill.

Unlike with alcohol where the “I’m having a great time, just one more drink” hangover happens the next morning, the bills hangover happens once per month.

With both, remembering the hangover limits me for my own health.

The English middle class carries 20k in debt on average?

That is quite interesting. Do they think pay raises in the future will help them pay it off or have they just thrown their hands up in disgust at their non-mobility? (As in, “I will never be able to buy a home or build wealth”)

we’re kind of seeing that here in the US atm. The salary one needs to purchase a starter home has gone from perhaps 75k in 2016 all the way to 150k at the bare minimum. So it’s either married couples or successful single people who will buy them at the moment.

Wolf-

Thanks for the insights on credit-card debt.

How does the chart that shows “Credit card balances and “other” consumer debt combined” stats equate to the articles that reference “household debt” stats? Where do mortgage debt and student debt fit in, for example?

Just trying to understand different terminologies…

I don’t consider student loans “loans” anymore and stopped reporting on it.

Mortgage debt discussion is here:

https://wolfstreet.com/2023/11/07/mortgage-heloc-balances-delinquencies-foreclosures-in-q3-how-are-our-drunken-sailors-holding-up/

Auto loan discussion is here:

https://wolfstreet.com/2023/11/08/auto-loan-balances-interest-rates-cash-buyers-subprime-delinquencies-tight-credit-how-are-our-drunken-sailors-holding-up/

Wolf, people are now making payments again. I know that you said that you wouldn’t believe it until it actually happened.

SOME borrowers are making payments again. Most don’t. Everyone month or so, a new batch or borrowers gets their loans forgiven for x-y-z reasons. In addition, nothing happens to borrowers that should make payments but don’t. They’re not being pursued in any way, and their delinquent loans that they still don’t make payments on still don’t count as delinquent.

Here is the delinquency charts of student loans, which is like a bad joke, which is why they’re not loans anymore. The ONLY student loans that are delinquent are the private ones:

I think some people are, but the current administration has come up with a variety of schemes that are resulting in widespread forgiveness of those loans.

I like my credit like I like the folks i mert in the bars…

Loose and available.

Excellent! There is so much BS out there regarding credit card data.

Yep and this Christmas so many boomers have grandkids needing stuffs that i expect consumer spending to accelerate in USA and CC delinquency wont change at all. The age of millennial children is a prime age for gifts travel clothes and other discretionary items . No recession in sight but trucking is in recession probably due to the high Mtg rates and fewer furnishings transactions. Most of that furnishings came from overseas. Less impact than USA .

Re the charts of delinquent credit cards vs. income, that’s a pretty big whipsaw.

It’s not so much the fact that the overall amounts and percentages are low so much as it is potentially the canary in the coal mine that could well be the predecessor to much larger defaults on much larger debts

The whipsaw was because:

1. credit card balances dropped during the pandemic as people stopped using them for travels and restaurants and concerts, etc.

2. disposable income spiked during the pandemic

Both of those worked together and brought the ratio down. Now we’re back to Good Times normal … green line.

“charts of delinquent credit cards”

I find all of these charts to be tough to swallow. They’re real, but they defy logic. However, cc delinquency is the one chart that caught my eye in all of them. Percentage of cc delinquency is just now above pre-pandemic normal. The current level is not crazy yet, but the rate of change is breathtaking. That rate of growth in delinquency is about as steep as it was during the GFC. It’s gone from 4% to 8% in less than a couple of years and it’s been accelerating during that time. Not the end of the world yet, but it will be interesting to see where it goes through 2024. Will it eventually spread from sub-prime card holders to the middle class?

The other Wolfstreet graph that always captures me is gov interest expenditure as a % of receipts. It’s flying up at record pace and there could be a point later in the next couple of years where congress will be forced to address it by decreasing deficit spending. That would swing more debt burden back on the consumer. Maybe someday we’ll hear words like “sequestration” and “austerity” again.

No sign of recession yet, but there are definitely some rates of change that are a bit eye opening. Could be the earliest cracks developing in the hull of our sailor’s boat. Who knows?

“Maybe someday we’ll hear words like “sequestration” and “austerity” again.”

Words spoken, but there wasn’t a trace of austerity in .gov spending in at least 30 (50?) years.

I would posit that the increase in credit card balances and US consumer spending is largely attributed to the rise in prices from inflation and NOT drunken sailor spending (e.g., increased levels of spending).

As mentioned, most people with decent credit ratings use their credit card for virtually all routine expenses. Look at the credit card balance graph at the top and I derive a 20% inflation (900B to 1100B).

US consumer spending shows an 11%…..14T to 15.5T, which makes total sense since this includes lots of folks who can’t continue to spend the higher prices like those that use credit cards daily.

Again, my take is that all this increased spending is largely due to increased prices which different economic classes of folks are paying at different levels. Food for thought.

I just Googled and “Wallet Hub” popped up and said credit card interest has gone from ~15% in 2000 to ~12% in 2004 to ~21% today. With credit card interest rates over 20% it is going to get ugly fast for the kids putting rent (and three meals a day on Door Dash) on their credit cards.

No one can put “rent” on a credit card for long…

If the landlord even lets you!! Most landlords don’t let you because they’d have to pay the 3% fee on the rent amount charged, and with a cap rate of 5%, it doesn’t work out anymore.

Even if a landlord lets you, you’ll hit the credit limit soon. That’s going to be one of those “learning experiences” that young people go through. Hold my beer and watch this, LOL

Debit cards work better for paying rent since the fees are very low, but they draw directly on your checking account and are basically just an electronic fund transfer from your checking account to theirs.

“No one can put “rent” on a credit card for long…”

I didn’t think you could put rent on a credit card at all. Every landlord I’ve had (whether mom & pop or corporate) wanted either a check or an ACH transfer – payment by credit/debit card was not an option.

I commented before reading the rest of your comment Wolf… nevermind.

I was just getting ready to dust off my old double-barrel 10-gauge goose gun that I shoot down the highfliers with 🤣

That would have been a reasoable and appropriate response on your part LOL

Some landlords will let you pay rent with a credit card, but you have to pay the additional fees. My landlord started charging $1.50 a month to pay the rent when using a bank account (ACH). Seems ridiculous, just pisses off the tenants. Such actions make me think the landlord is in deep sh_t financially and/or is just a greedy as_hole. Anyway, it’s another reason why I hate landlords, all of them. Well, they are all going to burn in hell.

There is a noticeable upward trend in delinquencies in your last graph from Q1 2021, although the percentage is still tiny as you say. And the 2.0% is not much different from the historical 1.5%. Graphs can be tricky, as interpretation often depends on the start-date.

I have nice 5% off credit cards for Instacart and Amazon. So I am more likely to use them than other vendors, assuming prices are pretty much the same elsewhere for the same product.

While some Landlords are no doubt “greedy as_hole” why should any business have to pay to get paid? I frequent several retail stores that give a cash discount of up to 4%. What is wrong with that? Tire store restaurant or landlord, why should they accept less for you to choose the payment method?

Doug, ACH costs nothing. It is like Zelle. Why should a landlord charge me for a payment that costs he/she/it/she_it nothing? It is actually an illegal increase in rent (California is rent-controlled now).

Some do cost money depending on the institution to and from. Assuming that the rent arrives by the due date, I agree they should not make money off that transaction but I have no problem with them, or anyone, recovering any costs associated with non-standard payment methods.

My city charges a fee to pay prop taxes online via ACH – which is why I mail them a check instead.

Well, a lot more Kids these days have access to LOC compared to when I was fresh out of school. Those % are up as well but not at 20%. Kids are definately dumb but they have access to internet and most will figure out to pay down 20% CC with LOC, pay rent with LOC etc… the ones who can’t even qualify for LOC won’t have very high limits on CCs, so if anything the kind of trouble you’re describing might show up in LOC and not CCs. Not to mention banks seem to be shopping around for debt these days, I’ve debt consolidation offers from my banks few % points below what short dated T’bills will pay, so I’m going to rack up the debt and probably show up in some “highly indebted” statistics for instance while actually being in the black.

The world sure has changed a lot since I was young, dumb and defaulting on my loans 😆

There is a credit card (Bilt) that gives you 1% back on rent payments, at least assuming you can use it to pay your rent, which is not a given.

But then you need to make sure you autopay your full statement balance each month.

Spending will be strong when the country’s debt-to-GDP ratio continues to grow.

The real carnage begins when legislators are forced to deal with the debt and actually do something about it, which will lead to recession and asset price reductions. That said, Powell is slow-walking the inflation fight as long as he can to avoid a recession and inflate away more debt with “tolerable” 3-5% inflation. Providing excessive stimulus to avoid even small recessions has been the Fed’s weakness for decades. It allows LT problems to grow.

I was surprised to see a couple Republicans with enough guts to propose a cutback of social security in the debates yesterday. Perhaps that’s a sign the debt problem has become so dire, discussing it is unavoidable. Plus, there is the government shutdown looming again. And the IRS is ramping up efforts to get some tax by going after tax scammers. They sent a $30B tax adjustment to a single company last month. The LT fiscal outlook may be at an inflection point where some pain has to be delivered, or else.

Typical. Spent all of the extra money generated by excessive SS taxes and now don’t want to pay it back. Ron is smiling from his grave.

Cur Social Security and Medicare so all the boomers can show up on sonny’s doorstep with collapsing health and finances? The younger generation might wish to think twice on that one.

Hush: “ …propose a cutback of social security in the debates yesterday…”. I didn’t see the debate but from my reading of it, I don’t think there were any proposals to cut social security. There was some mention of “reforming” it which could be done by raising the retirement age and increasing the wage range that is taxed. The biggest problem remains Medicare/Medicaid which is now costing the equivalent of the entire annual federal deficit.

Hesh

So that’s good news, I guess. Last quarter defaults were at 2.77%. Interesting that the defaults are coming down but the balances are going up. Makes sense most people are scrambling to pay that balance off as soon as possible what with 20% interest charges these days. Still feel like they are being financially irresponsible but each to their own.

Boy though one or two payments missed on a credit card really lowers a person’s credit score. It takes what seems like forever until the bad mark falls off the credit report. I missed a payment in 2014 and sure enough it took 7 years for the bad payment to fall off.

Maybe the younger generations aren’t taught that’s how the world works in high school anymore. But then the financially savvy would have no way to get ahead of their peers if everyone knew the game, mean but true.

It’s all part of the learning curve. Most people — especially me — have to learn some things the hard way. In my younger years, if I was told something, it went in one ear and came out the other. When I then suffered the consequences of my decisions that had ignored what had gone in one ear and had come out the other, I learned and never forgot. As I got older, I got tired of learning the hard way though. Recovery gets harder, and somewhere along the line, I realized I was no longer invulnerable, invincible, and immortal.

Thanks for that, Wolf. It gives me hope for my son who I think is just now cycling into a personal RE mess after telling me how much equity he has as recently as 3 months ago. Or should I say had? learning the hard way has always been one of our family dinner conversations from age 4 to 40, and now I just shut up and hope for the best. Unfortunately, he is still in the invulnerable, invincible, and immortal stage. His folks are in the late 60s stage. :-)

Seriously, you offer great insights and a wealth of knowledge.

This is such a good comment that I screenshotted it to share with my kids. If only we wouldn’t have to learn things the hard way but ALAS, such is life!

Yes—learn from other people’s mistakes, as you’ll never long long enough to make them all yourself.

“The way of a fool is right in his own eyes, but a wise man listens to advice.”

Proverbs 12:15

I know the article is about CC debt, but noticed most Debit cards are on the Visa/Mastercard network. Are the Debit card transaction fees included in the CC $126 billion fee toal?

No, debit-card fees are not included in the $126 billion; that’s just for credit cards.

Debit cards in 2022 were used for $4.8 trillion in transactions, and merchants paid $35 billion in fees.

Debit and credit cards combined amounted to $10.6 trillion in transactions.

Credit cards alone amounted to $5.8 trillion in transactions, as I said in the article. This includes all brands, AmEx, Discover, MC, Visa, private label, gas station…).

All data from Nielsen’s annual report on merchants’ processing fees, which came out in March.

I don’t know… Anecdotally, I know how much I’m paying out-of-pocket, paid-in-full, on my credit cards for car repairs, electronics, groceries, travel, etc.; but, when I see people who look like they don’t have two nickels to rub together whipping out the card at the dealership, Best Buy, Costco, et al, I always wonder if that is being paid in full.

Thousands of dollars in float takes a certain… discipline… to commit to paying off each month without falling behind. I’m not sure I have that much faith in the average consumer.

“…when I see people who look like they don’t have two nickels to rub together whipping out the card at the dealership, Best Buy, Costco, et al, I always wonder if that is being paid in full….”

🤣 You nailed perfectly what I look like when I go shopping or anywhere else.

The only exception is when I go out with the wife, which is when I try to impress her by putting on my black dress Levi’s, my dress sweatshirt, my trusty black leather jacket (instead of my raggedy denim jacket), and shoes that don’t have holes.

I don’t dress up when I go to Costco, and I never go to Best Buy anymore because I buy their stuff online. And when we bought our vehicle recently (to replace the one that got totaled), I wore regular jeans, sweatshirt, and my raggedy denim jacket. Worked fine. They don’t care what I look like, they just want my money, LOL.

And I assure you, I’ve paid off all my credit cards in full ever since one day about 35 years ago, when I discovered that I had maxed out my credit card and was paying 21% in interest on it, at which point I went on an austerity program to get that paid off asap (young man’s learning curve).

Very true, at least in my experience — the most frugal and well-healed people I’ve known tend to also be the least preoccupied with polishing and preening. The only multi-millionaire I know personally (I knew him when) drives around in a 2008 Mazda 3.

Hmmm, if I have just a hair over $2 million, can I call myself a multi-millionaire?

(asking for a friend)

Harvy. Sure. You can call yourself anything you want.

We’ve done all right – but on the rare occasion that my wife and I leave the house for an actual destination she insists on inspecting my clothes for holes and stains – and she usually finds something…

I almost always pay cash though. Certainly for any in-person transactions.

@Harvey Mushman

Yeah, if you make $2MM a year income, you are a multi-MM.

Otherwise, you are just trying to play the part.

bul – sounds about right. Can remember a couple of decades ago when a survey of millionaires (a moniker more impressive back then than now, admittedly) revealed that their ride was most likely to be a Taurus (1st gen).

may we all find a better day.

And I assure you, I’ve paid off all my credit cards in full ever since one day about 35 years ago, when I discovered that I had maxed out my credit card and was paying 21% in interest on it, at which point I went on an austerity program to get that paid off asap (young man’s learning curve).”

I appreciate reading this, Wolf. You’re my go-to for understanding the economy and it’s refreshing to see that even you weren’t perfect when you were younger with spending. Learning the hard way happens to many of us.

Never had a credit card. I couldn’t figure out why I would want and get something, use it till it’s gone, and then still be paying for it. But back in the day rent and food and cars and beers and girls were not that expensive.

I’m sitting at my desk reading the headline from CNBC, Nov 9, 2023:

Average credit card balances top $6,000.

Total credit card debt tops $1.08 trillion.

Amid inflation, consumers are struggling to afford everyday expenses.

They’re trying to keep the house of cards from collapsing.

Balances jump 15% from a year ago.

Delinquency rates rose across the board.

Americans are addicted to credit cards.

Thank you Wolf for taking the fun out of my daily doom porn!

Most recent data points seem fine but the prevailing trend on most of those graphs do support some level of concern.

Mortgage rates are dropping. Every time it looks like housing prices could be on a path to correct, Powell opens his yapper and the tightening goes away.

Interest rates had gone nearly parabolic, and needed a break. They will rise again soon, as sure as the sun will rise tomorrow.

No no — they’re plunging, at least to hear the pundits tell it.

Apart from the fact that it sort of conjures a mental image of an uncooperative toilet, it’s also standard headline hype. A few basis point zigs or zags is no great shakes one way or another.

But…we’ll see.

Yields rising today. I guess auctions didn’t go too well today. Bwahaha!

Mortgage rates jumped today, LOL. But they did have a pretty good run for the past couple of weeks.

Thanks WR,

One of the CNN article is touting that mortgage rates plummet larges tin a year and would bring our buyers in droves to take advantage of these low rates.

Can’t help but smile.

Wolf

As usual you do a great job of parsing out and making clear the data definitions and sources like Equifax reported percent of total balances and percent of borrowers.

The FRB puts out similar data that has similar shaped curves in a report titled “Charge-Off and Delinquency Rates on Loans and Leases at Commercial Banks” that contains a breakout for credit cards. That said, while the curves share a shape, their values are VERY different and show 2.77% for 2Q2023 (seasonally adjusted).

It looks like a methods, definitions and sources difference, can you unravel it?

Yes, what the FRB reports is from “bank” balance sheets — so that’s commercial banks that the Fed regulates, as reported by the banks, according to their rules. They have rules for when something is “delinquent,” and for how long before it’s either cured or “charged off.” When it’s charged off, it’s no longer “delinquent.” It’s just gone.

The data here comes from Equifax to the NY Fed. It’s far broader data, includes credit cards from banks, non-banks, credit unions, specialized subprime lenders, private label credit cards, gas station credit cards, etc. So this is the universe of all credit cards here, including the worst kind (specialized subprime shops).

Small point to nitpick:

“BNPL loans are interest-free for the consumer and are subsidized by retailers.”

Sometimes – but more often they’re subsidized by the manufacturers whose products the retailers sell. For example, Sony has been subsidizing zero% interest promos at various electronics retailers who sell their products. Since the margins on these products are so thin, the retailers wouldn’t be able to afford it – but Sony sure can.

Same basic principle as homebuilders buying down mortgage rates – but how long can this last?

I get asked all the time where all the zero% financing promos went, by customers who are apparently unaware of the Fed’s tightening campaign over the last year+.

“BNPL loans are interest-free for the consumer and are subsidized by retailers.”

True, but these loans allow the companies to forgo paying 3% to CC companies. If viewed that way, the loan is yielding 3% compared to a CC transaction.

You are correct – the whole thing is designed to boost retailer revenue (and by extension rev to the mfgr).

But, there are other costs to the program – i.e. Synchrony Bank dings retailers with a fee if they don’t process a certain number of apps each month.

There are also customer service headaches that arise with these promotions: you have to be clear w/ customers that its DEFERRED interest, and they need to make the min monthly payment *and* pay off the bal by the promo date, in order to not get hit w/ interest.

Of course, when a customer doesn’t follow the rules and gets charged interest, it’s the retailers fault because the customer is always right. /s

Powell: Biggest mistake Fed could make would be to fail to get inflation under control

The Federal Reserve is most certainly not ‘going to pivot’ and will keep increasing the Federal Funds Rate indefinitely in the future months until ‘inflation’ drops below 2%. Tough luck to the pivoters.

Treasury auctions were a bit weak today.

– Government interest payments will hit 1 trillion sometime soon.

– CBO now says the Government will add another $20 trillion of debt by 2034 and will be $54 trillion. FYI, In 2019 the debt was 22 trillion.

So just think about this for a minute. The government wants to sell us another 20 trillion of debt in the next 10 years. I have a hard time seeing treasuries dropping in price over this time frame.

– Who is going to buy this 20 trillion in debt. People just bought 10 trillion over the past 4 years. Where is the money coming from to buy this debt? Does the public have another 20 trillion. Do other governments have 209 trillion to splurge on US Treasuries? Do banks want to buy another 500 billion or 1 trillion of 5% treasuries when rates may go to 7% and then take another loss?

This looks inflationary to me.

Do you mean to say that you have a hard time seeing treasury yields dropping in price? that would make more sense if you think there is too much treasury debt.

I would also say that people didnt buy another 10 trillion (or whatever) of Treasury debt. Alot of that was bought by the Fed and other central bankers.

If you multiply the debt times the average rate the government is paying today it is just over 1 trillion already, only going higher.

Great article as usual. Might want to add one graph next time. That is the current interest rate charged on credit cards. I think it’s inching higher.

It’s irrelevant because most people never pay interest on their credit cards because they pay them off before due date. What do I care if my credit card interest jumped from 7% to 20%? Nada, because I pay off my credit cards every month and never pay a dime in interest. The rate simply doesn’t matter. What matters are the kickbacks I’m getting for using the cards, the 1.5% or 2% cash back and other incentives I get every time I pay for something with the card.

And higher-risk borrowers, some of whom that do use their credit cards for long periods to borrow, have had 30% interest rates for years. For them, nothing changed.

So the actual interest in dollars paid on credit cards is what matters, not the rates.

It makes me wonder how many people (like myself) are paying with credit card versus cash because of the incentives? I have an Amazon Visa… 5% off everything I buy on Amazon. Costco Visa… 4% off already low gas prices – 2% off Costco or Costco.com purchases. American Airlines Visa – double miles on grocery and restaurant purchases. I pay my balances off every month, but I am charging MUCH more than I normally would because of the benefits. This month I am paying off $20K in monthly credit card debt – because of purchases associated with a new house. None of these cards charge annual fees. I know they HOPE to convince people to carry a balance, but if you refuse to be convinced, there is significant upside.

I do the same and open new credit cards when cash bonuses. For example just opened Capital One Quicksilver and if I spend $500 in 3 months I get $200. Then I just close and go into the next. Not a ton of cash but $800 a year or so and minimal impact to my credit score which is only relevant for opening new credit cards! Admittedly I am not a fan of this on principle but getting 60 days often to pay for something plus 2%-5% off is money in my pocket.

Greg P,

You’re doing precisely what the banks want you to do: use your cards a LOT and pay them off every month. Because for every $1,000 you charge, the bank collects around $30 in fees risk-free. That $20,000 charge made the banks $600 in swipe fees! It then kicks back some to you and keeps the rest. It’s the best business model ever.

Banks collected $126 billion in these credit card processing fees in 2022! And the merchants paid those $126 billion, and then add them to their prices, so then everyone ends up paying for them.

Everyone I know, including me, does exactly what you’re doing. It’s like free money (but of course, it’s not free).

Yes, I do it because we both benefit. The piece I struggle with and perhaps irrelevant is that businesses pass these costs along and while I see some of it I also get some benefit. Cash and debit holders don’t although seems like debit rewards cards are a thing now too.

” Because for every $1,000 you charge, the bank collects around $30 in fees risk-free.”-Wolf.

Well, I have a couple of cards that each pay 5% cash back, which would be $50 back on one $1000 transaction. Sounds like the vendor is out $80 ($50+$30) on a $1000 transaction. Of course the vendor has his mark-up, so I am sure he is making some money, but still that is a lot of money to pay to attract my business. Seems like it makes suckers out of those who pay cash.

Guessing most people on this site have solid credit so getting numerous $10-20K cards is no issue. Not the case for those who primarily rely on debit, but I am sure those who miss the free money.

Not sure if still common but businesses also used to get kick backs from CC companies if amount was sizable per quarter. Bank willing to do whatever to rack of fees although some they keep is for fraud/disputes but really small I would think.

The food service industry near me has been discretely tacking on credit card payment surcharges, some are quite high. Not sure when it started but it seems as though it came on all at once. Gas stations have been at it for a while.

We pay off our balance in full every month… but it is HARD to keep track and exercise discipline when blissfully swiping away.

Three weeks ago my wife and I agreed to get back on budget and go back to cash for day-to-day spending (gas, groceries, personal allowance). It’s amazing how much it feels like stepping back in time going to the bank on payday, or walking into the gas station to have the pump turned on.

It’s also incredible how much less we’re spending without feeling as though we’re making any significant sacrifice. I looked in my wallet at the bar last night shrugged and decided not to have that third beer. It’s shocking how much those little things add up to.

Is this not then a $126 billion drag on the economy? Other than the little bit it takes to keep this payment system up and running

On the contrary. It adds $126 million to GDP as part of financial services that consumers ultimately pay for.

It’s like healthcare or rent or restaurant meals.

Wolf….the majority of my monthly volume has been cash out refinances. This is how they are paying the CC bills. That won’t last long.

These numbers will continue to decay and Jerome wants at least 6% of the populace to be unemployed by Christmas.

Good luck with a “soft landing”

“the majority of my monthly volume has been cash out refinances. This is how they are paying the CC bills.”

LOL, joker. Good one. Or maybe you’re one of the last few brokers left standing doing refis?

Cash-out refis have collapsed by 67% compared to same week in 2019. Black line = 2023 (no-cash-out refis have collapsed by 95%). Data from the AEI Housing Center. You can’t pull that BS on me.

He’s cornered the cash out refi market! The only one left!

Lol

“Jerome wants at least 6% of the populace to be unemployed by Christmas”

Yes, exactly, I heard him say that 3x in his speech. Maybe 4x.

NOTE: The cash outs have been the majority of my volume since August. I am a real estate appraiser.

PS…I used to work at Fannie Mae and it only took 5% of that GSE book of business to go into full default to crash the entire Global system. It’s

NOT different this time

I opened up two credit cards with 0 interest for 15 months. Will pay the minimum, what I would otherwise pay to the cc goes in a treasury. Will pay off the cc in 15 months. I’m profiting but still feels weird to carry a balance.

I guess I’m one of those who contributed to the increase in CC balances. In the past 18 months, almost everything I buy goes on a CC and is paid off weeks before due date, soon as the billing cycle closes. Was using my bank account debit card to pay the grocery store but they had a data “incident”.

I don’t want my bank account tied to any remote card processing station. At least with a CC I have a chance of disputing anything not bought by me.

Maybe I’m fooling myself, but my bank is no longer tied to any payment portals or point of purchase

So is credit card delinquency rate (either aggregate, or by age group) a metric that has significance or influence in the mandate of the Federal Reserve Bank for stable prices and full employment? If so, is there a delinquency rate that’s an orange or red flag?

For example, would delinquency rates rise ahead of rising unemployment, or would unemployment first go higher and then people start delaying their CC payments…a chicken/egg question.

“The fact that 98% of credit card users are current on their credit cards — either paying them off by due date or making at least the minimum payments on time —”

Maybe I missed it.

Is there any data on those who just pay the minimum and roll over their debt? 2% delinquent is a small number, but a predictor of what is coming would be a reading on the % of those who are now rolling with the minimum payment. Is there data on this?

Someone should put you on the national news. This is the only place I can find that understands and reports this data in context.

But wait… articles that say that the consumer is collapsing under the weight of their credit-card debt get a lot more clicks and go viral. That’s why those articles exist. The internet is a strange place.

I believe it was on this site a year or two ago that I read:

The top 20 percent account for 80 percent of spending on goods (?) and services.

We should keep this in mind when assessing the state of the economy.

Wow. I often read your articles but never noticed the comments. I had to scroll forever to get to the bottom to add my $.02. This is a platform with very active participation! So my $.02 on credit card behavior is as follows: many people are in complete denial that they have credit card debt. OK, they know it is there but completely blot it out of their mind. They pay the minimum to avoid being “hassled” but never look at the statements. So, that way they don’t have to think about the long term consequences (could be parallels to other self destructive behavior?). I have a relative who finally saw the light, but ruined his family’s finances in the process. Ultimately, his sinking credit score got him cutoff from new credit – and then the hard times began.