Where’s the hangover from the party?

By Wolf Richter for WOLF STREET.

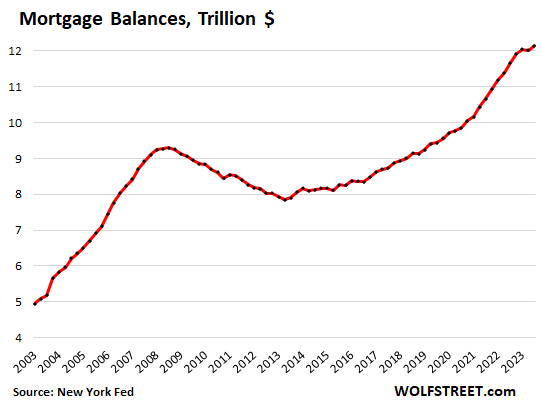

Mortgage balances outstanding ticked up 1.0% in Q3 from Q2, to a new record of $12.1 trillion, after having dipped in Q2, according to data from the New York Fed’s Household Debt and Credit Report. This increase is less than half the pace than the big jumps during the era of the 3% mortgages, when mortgage balances had soared quarter-to-quarter by as much as 2.8% in Q2 2021.

Year-over-year, mortgage balances rose 4.0%, down by over half from the year-over-year increases in 2021 and 2022 that had reached 10%. In a moment, we’ll look at what could cause an uptick in mortgage balances even as home sales have plunged and as mortgage applications to purchase a home have collapsed.

Mortgage balances rise or fall based on diverging dynamics, on the plus side and on the minus side.

What adds to mortgage balances:

- The growing total inventory of homes (it constantly increases due to new construction) owned by a growing population.

- Prices rise over the years (newly purchased homes are financed with bigger mortgages). Price soared in 2020-2022, dictating today’s big mortgages.

- A boom in cash-out refis (nope, not now).

What subtracts from mortgage balances:

- Regular mortgage principal payments.

- Mortgage payoffs — and people with 3% mortgages are clinging to them.

- Falling home prices mixed with a wave of foreclosures – which caused mortgage balances to fall during the housing bust.

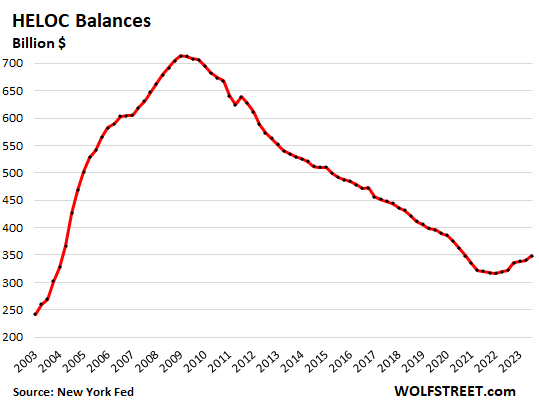

HELOC balances have been rising for four quarters from historic lows. Homeowners with 3% mortgages can no longer cash-out-refi their homes without causing a catastrophic increase of their mortgage payment, as the entire 3% mortgage would be replaced with a 7%-plus mortgage. A HELOC accomplishes the same thing but the 3% mortgage stays in place, and only the HELOC portion comes with a 7%-plus price tag.

HELOC balances rose by $9 billion, or by 2.6% in Q3 from Q2, to $349 billion. They remain extremely low, considering the increase in home prices over the 20-year period, as homeowners used refis, instead of HELOCs, to draw out cash over the past decade:

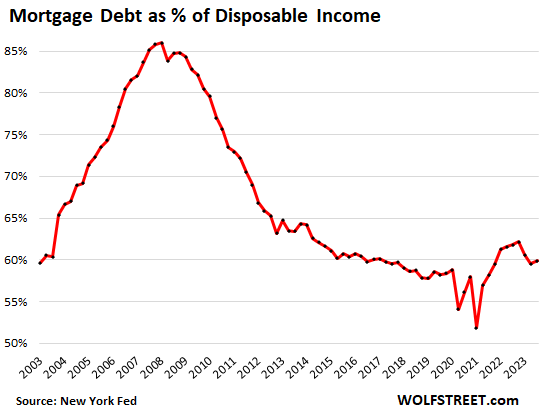

The burden of mortgage debt. Homes are lot more expensive today than they were 20 years ago, but consumers make a lot more money too, and there are lot more homes and a lot more consumers owning them. Turns out, after massive gyrations, overall mortgage debt as a percent of disposable income is roughly where it had been in 2003.

Disposable income is income from all sources except capital gains, minus taxes and social insurance payments. This is the cash that consumers have left to spend on housing, food, cars, etc.

Note the impact of the pandemic-era funds that consumers got (stimulus payments, PPP loans, etc.) that caused disposable income to spike, and therefore the burden ratio to fall. And note the impact in recent quarters of the biggest pay increases in 40 years, even as mortgage debt barely increased.

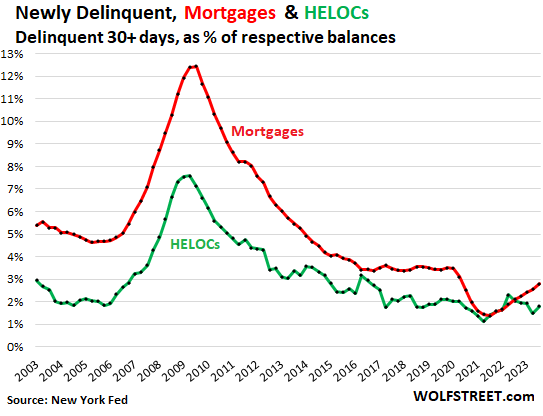

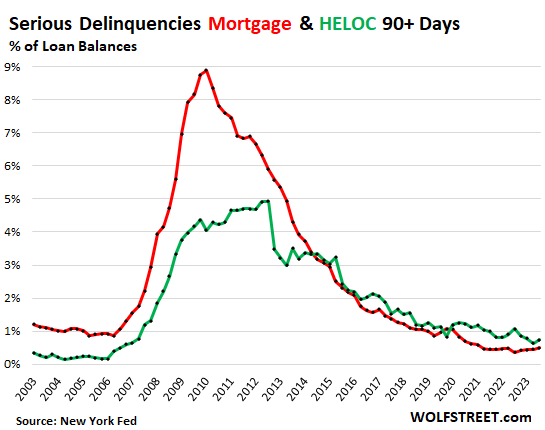

Transitioning into delinquency: 30+ days. Mortgage balances that were newly delinquent by 30 days or more at the end of the quarter ticked up to 2.8% of total balances, which is still lower than anytime before the pandemic and down from the 3.5% range during the Good Times in 2017-2019 (red line in the chart below).

For HELOCs, the 30-plus-day delinquency rate rose to 1.8% in Q3, after having dropped to 1.5% in the prior quarter and remains ultra-low (green line).

Serious delinquency: 90+ days. Mortgage balances that were 90 days or more delinquent by the end of the quarter edged up to 0.50% in Q3 from 0.46% in the prior quarter, about half the rate from the Good Times before the pandemic and from the Good Times before the housing bust (red line in the chart below).

For HELOCs, the 90+ day delinquency rate inched up to 0.74% in Q3, from 0.64% in the prior quarter, which had been the lowest since before the Housing Bust (green line).

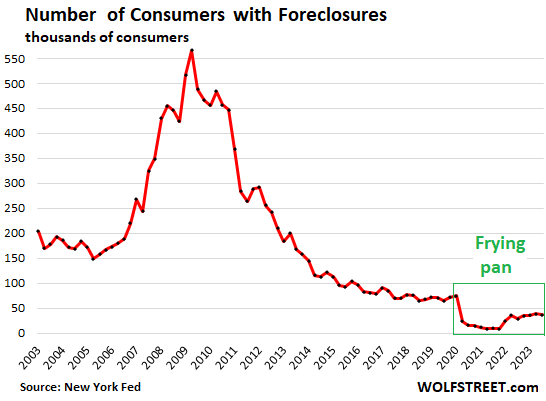

Foreclosures in a frying-pan pattern. The number of consumers with foreclosures fell by 7% quarter-to-quarter to 36,100 in Q3, down by about 45% from the Good Times before the pandemic in 2017-2019, and down by 75% from the Good Times in 2003-2004 when the housing market was approaching the peak of the prior housing bubble.

The fiscal and monetary excesses during the pandemic, the forbearance programs, and foreclosure bans reduced foreclosures to near zero. Now they’ve come up a little from these lows but remain ultra-low.

So sure, someone clever could come up with a clickbait-title about foreclosures “exploding by 345%,” OMG, from Q2 2021. And we’ll just laugh about it and move on.

Note the frying-pan pattern, as I call it, of which we’re going to see more as things normalize from the crazy times:

Where’s the hangover from the party? In terms of financial stress that households have with mortgages, a massive hangover doesn’t set in until home prices decline substantially and homeowners are losing their jobs in large numbers.

Homeowners are at risk of foreclosure if they lose their income and can’t make their mortgage payments and if at the same time the market value of their house drops substantially below the loan value of the mortgage.

A homeowner that cannot make the payment, but can sell the home for the loan value or more, can just sell the home and move on, perhaps with some cash to go.

But when the net proceeds from the sale fall below the loan balance, homeowners who lost their jobs would have to come up with extra cash to pay off the mortgages, and that’s where the problems arise.

Homeowners who bought over the past two years in some markets where home prices have dropped and who skimped on the down-payment could fall into trouble if they lose their jobs for long enough. For now, the job market is strong, so this fate would be limited to a small number of homeowners, which is why delinquency rates and foreclosures are still extremely low. But a substantial rise in unemployment combined with a substantial decline in home prices across many big markets would increase the delinquency rates and foreclosure rates.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Wolf – Could there be bad news buried in the mortgage debt as a percent of disposable income chart? For example if it was stratified across income levels, could it be that the wealthier tiers have increased disposable income so much that it is drowning out the pain being felt by the middle and lower tiers? I know incomes have risen and many people are locked into low mortgage rates, it just seems like that long slope in the Case Schiller would have had a bigger impact on affordability. Thanks as always for your insights, which always seem to be the best at drowning out the noise and sticking to the data.

This time around, the lower end of the income spectrum got the biggest pay increases — and they’re still getting them.

You need to look somewhere else for problems with mortgages. Check the last section of the article… if there are problems, that’s where they will be.

I’ve checked two sources on this, neither is institutional, regarding current interest rates on mortgages in America: One stated: 80% are below 5%, the other was at 82% for <5%. One third are approx. 3%, due to low rates for original loans and refi's.

It'll probably be a long time before these homeowners abandon their loans.

I’m in a brand new subdivision of SFH (1,250 – 2,850 Sq. ft. homes) and it’s about 1/2 built out (in Texas). Two empty lots sold last week and the foundations/drain pipe are started. The builder is buying down the mortgage rates to 5.99% (big sign in front of the sales office). I hear they are not moving on prices though.

In other words, mortgage markets and homeowners have never been in better health.

The old rules still apply. Until there is massive unemployment, the economy will keep plowing forward, and there will be no recession or housing crash any time soon.

I economists are busy writing papers explaining that they are still correct that higher interest rates cause higher unemployment.

Yes, but “mortgages” not “mortgage market.” The mortgage market, from the mortgage bankers’ point of view, has collapsed, and their business has collapsed.

Doesn’t have to be massive unemployment. Just enough to make people tighten their belts because they’re worried that they will be next. I’d say unemployment rising to 6-7% would do the trick.

Nice upwards trajectory of the newly delinquent mortgaged. Would like to see the slope of the seriously delinquent match the former. Let’s check back in 6 months.

Thanks, Wolf!

Until July, the IRS was handing business owners nearly $20 billion a month in ERC credits.

Due to the enormous amount of obvious fraud on the claims filed, it stopped processing them in August. This was manna from heaven for those who got it.

Ticket to jail for those who got it fraudulently.

When will the fraudulent be held accountable and if that happens do we recoup our monies so freely/fraudulently given?

I make the bare minimum , and my husband who worked since he was 15 now has health problems at 61 and doesn’t qualify for medicaid due to I make too much money .

My salary after paying 270 a month for my healthcare pre tax, then add the federal and state taxes shaves off 12,000 dollars leaving me with next to nothing in net that is dwindling every quarter despite what inflation BS is pushed.

Peter Schiff, of Euro-Pacific Capital, tells the story where he was talking to a female real estate agent about how he was renting, not buying, a property. She was disapproving. “But real estate always goes up!”

This was before the Crash of 2008. Where real estate debt sliced tranches and then financial institutions got burned holding them.

Schiff was proven right. Sometimes you want to skip the mortgage and just rent for a while.

For the vast majority of people in today’s market, it’s not even much of a question whether to rent or buy. Most potential buyers are HAVING to rent because they CAN’T buy. And most who could buy in this market have to either overextend on their budget, liquidate assets, or go well below their current standard of living.

The buyers’ strike will outlast the sellers’ strike because the buyers CAN’T buy, while the sellers will likely eventually be forced to.

Surely, anyone sitting with a second home should be running the numbers. Proceeds of a home sale can start earning a safe 5% immediately, plus cut off the increasing RE tax and maintenance. Holding out for continued home price gains seems like a losing bet at this stage.

This also applies to owners of rental homes, even those with positive cash flow…

@Bobber, most people with second homes and cars own them because they want a second home at the beach or the mountains, or a car that is fun to drive and won’t be selling them to “start earning a safe 5% immediately”. The “market value” of my cabin in Tahoe and my 993 Cabrio have more than doubled in the past decade, but I don’t plan to sell either of them even if the values of both dropped every year for the next 20 years since I don’t look at either as “investments”, but rather “things I want to own”.

@kramartini unless someone owns a rental home in a declining area or wants to get out of the rental business it will almost never make sense to sell a cash flow positive rental home to “start earning a safe 5% immediately” due to the high cost of selling real estate and the capital gains tax hit you would take.

I was on a train back to Seoul after completing a military exercise in South Korea in 2005 or 2006. One of the other Reserve officers on the train was telling us how he was making a fortune “flipping” bigger and bigger properties in Orange County, CA. I warned him to be careful… that the market was getting overheated and that he might want to bank some profits.

He looked at me like I had two heads. “The market is just going to keep going up-and-up-and-up.” I told him those words were last uttered to me by my sister in early 2000 when she was investing in the stock market. He responded with, “You just don’t understand the Orange County real estate market.”

I never saw him again. I wonder if he got out okay.

Spencer G-

Great observation and re-telling. Thank you.

Reminded me of this quote from John Kenneth Galbraith’s A Short History of Financial Euphoria:

“There can be few fields of human endeavor in which history counts for so little as in the world of finance. Past experience, to the extent that it is part of memory at all, is dismissed as the primitive refuge of those who do not have the insight to appreciate the incredible wonders of the present.”

Worth reading or revisiting, especially by anyone who didn’t live through the gyrations of the 2000 or 2008 investment markets…

…even in that case, it remains likely one will still hear: “…but it’s different THIS time!…” (anecdotally legion in the comments over the years in Wolf’s most-excellent establishment…).

may we all find a better day.

Hi, Wolf, you wrote

“a massive hangover doesn’t set in until home prices decline substantially and homeowners are losing their jobs in large numbers.”

Do you have a theory on why the US would see layoffs this cycle, and how it would play out? What can cause people to start losing jobs, it seems people are getting extra jobs to make-do with increased cost of living?

This labor market should have keeled over a year ago when we had all these layoff announcements. But no, there were some wobbles, and there are still some wobbles, but it’s still surprisingly tight.

For foreclosures to surge, it takes a big increase in unemployment, with people out of a job for a long time, not just a month or two, combined with a big drop in home prices. We may still get this scenario, but I’m just not seeing the weakness in the labor market.

1. Though what things or developments can cause a big increase in unemployment?

Lower consumption/sales – lower production need – lower earnings – layoffs?

2. What can cause lower consumption in this economy? It seems that wages are set to progressively rise for the next couple years (gluttony of union contracts and their pressures).

3. It seems that wages will somewhat keep up with costs, thereby preventing significant demand destruction, layoffs, and recession, but not necessarily producing strong growth?

Maybe fiscal tightening by the US Federal government? I’m beginning to appreciate that it’s difficult for the US to tip into recession while the US Federal government is running record peacetime deficits (though maybe Ukraine assistance means this really isn’t peacetime anymore).

When we eventually have a recession, it doesn’t seem like the housing market will be the primary cause. Like most of Wolf’s followers, I have a sub 4% mortgage rate and I’m staying put for at least 5 years. There a fair amount of “housing crash” peeps on you tube, but I don’t see this happening with huge difference between housing values and relatively low debt levels.

Yup housing inventory will stay low forever and market will not crash and stay flat the worse case scenario but probably go up YoY because everyone got low rate mortgage and will never move especially given how high interest rates are now.

Those house crash peeps are all just fear mongering, anything I am missing here?

You forgot the /s or you’re deluding yourself.

I dont know if a RE correction or crash…nationwide… will occur anytime soon.

I do KNOW of 4 utubers who were predicting a RE crash…nationwide… a year and a half ago. Lots of drama too.

Occasionally I would read a commentator (to a video) claiming the crash forecasts from this particular “Crash Bro” began what would have been spring or summer 2021. One of the 4 persons did not stipulate that RE would crash, just our economy. The first 2 times I listened to the guy I thought he was pretty convincing, but that changed. In July this year he was predicting serious economic problems here in the US by late summer (my interpretation). Once August came and went so did his videos as far as i was concerned.

Am I more gullible than most ? Of course I prefer to think not but who knows. I do get annoyed with people who speculate in vague terms.

There are an infinite number of ways people can be misleading.

To repeat… I dont claim to know if a nationwide RE correction or crash is imminent in the next year or two. I am quite aware of price declines in Austin, Boise, Seattle. But am equally aware of the Midwest and most parts of the East…many cities there at or near all time highs in sales price.

One thing for sure. It makes little sense to pay ANY amount of interest for the right to hold an asset that is declining in value. The “savings” of a low rate mortgage accrue gradually over time, say $1,000 a month. If a $600k home declines just .5% per month, that’s a loss of $3,000, with $2,000 loss to net worth.

Many people will disregard the risks to maintain a home ownership lifestyle. Others, including RE investors, will be trying to maximize financial opportunities, and they will move the market.

Also seems that a record percentage (33%) of sales are all cash which makes sense given increases in home values over last few years with high mortgage rates. That reduces but doesn’t eliminate the issue of future delinquencies. At 3% you would do better in the market, although I took the approach of paying down when I could, but today you don’t want to assume more in market.

No recession in sight !

Really? Europe is in recession and China is likely in one as well.

No recession indicators in the US.

I think your recession could come when the deficit hits and congress forces the government to cut spending

Replying to Julian – I agree with your sentiment; doing away with $2T (more?) in deficit spending would go a long way toward reducing GDP and increasing unemployment -> recession.

But does any serious person see a scenario on the 10-20 year horizon where this actually happens? Last time it was even tried was 2011. Last time it was successful was 1997.

Best advice – learn to play the game by these rules cause they’re not gonna change much in your lifetime

fullbellyemptymind

If the US government continues to spend like a ”drunken sailor”, interest on the debt will exceed 50 percent of revenue in the near future.

Interest on this debt will continue to rise, which is sure to alarm Congress at some point.

Any sane person would take measures to stop this madness.

Be sure!

Julian – we agree on everything except the number of “sane person(s)” in congress.

Even if sanity did prevail in the near term it would all get thrown out the window next time someone or something insulted our collective national privilege (9-11, great recession, COVID).

The good news is that there’s a lot of money to be made here if one can work past the sheer loathsomeness of it all. I think of it as the difference between nihilism and acceptance.

Today Redfin posted an article reporting that 7% of for-sale houses posted a price drop during the four weeks ending October 29, on average, the highest % on record.

Oddly, Redfin reported in October of 2022 that 7.9% of listings had a price drop (which was a record then) 👉 https://nypost.com/2022/10/17/home-asking-prices-tumble-at-record-pace-as-mortgage-rates-surge/

I see it every day.

@Wire …. Good catch!!!

I think Redfin’s data only goes back to like 2012. I seriously doubt it’s worse than 08 or 09

When the balance of payments is balanced by foreigners acquiring net holdings of our equities, bonds, and real estate, and capital outflows (interest, dividends, rentals, etc.) exceed inflows, we are either decreasing our net creditor position in the world or increasing our net debtor position.

Beginning 1985 it has been the latter. The trade deficits, plus the unilateral transfer of funds by the Federal Government to foreigners (our far-flung military bases, etc.), transformed this country from this world’s largest creditor to the world’s largest debtor – for the first time since 1917. Since 1985 we now have a net debtor position exceeding 17 trillion dollars, but the principal villain (since 1973) was our dependence on foreign oil.

And 17 + trillion dollars buys a lot of real estate.

I am reminded of how Japanese investors got clobbered buying Rockefeller Center. Perhaps history will repeat itself?

Drunken Sailors? Nah, we need a better name than that, like one of my buddy, I think we need to call them permanently stoned, this type of spending will be the new norm for many years to come apparently.

I have always likened it to a rogue… someone who lives in the moment without considering the future.

Happy the man, and happy he alone,

He who can call today his own:

He who, secure within, can say,

Tomorrow do thy worst, for I have lived today.

Sadly… I am too conservative. I need to learn how to live for today a little bit.

It’s a far far better thing…

One lesson folks in 90s Russia took from their economic turmoil is that inflation can whittle away your savings, and other fiscal calamity or irresponsibility can make your wealth worthless in very short order.

Many in Russia learned the hard and unfortunate “lesson” that it’s better to spend what you have while you have it. Because it may be gone tomorrow.

So, while I live exactly as you prescribe, with minimal expenditures and maximum saving, this behavior also carries some risk. If you always live for tomorrow, then you may end up dying not having lived at all.

There were wealthy Russians in the 90’s?

Russians may have already been pre-programmed to spend that way. During the Communist years the Russian people weren’t joking about scarcity when they said that if they saw a line they got into it because that meant there was SOMETHING on the other end that was worth having.

Communism in Russia couldn’t help but fuel their robust “black market” for scarce goods and the illegal swapping of rubles for other currencies when anyone could get away with it.

The GFC is not comparable to C-19. The FED is refusing to “bite the bullet”.

M1 NSA money stock (our means-of-payment money) peaked on 12/27/2004 @ 1467.7. It didn’t exceed that # until 10/27/2008 @ 1514.2.

The GINI coefficient will continue to rise.

The FED has achieved its objective, that there’s no difference between money and liquid assets (the Gurley-Shaw thesis).

Wolf, I assume most of the sub 4% mortgages were sold to other lenders or financial institutions. With the Fed raising rates, how does that adversely affect the institutions who bought them? Are they between a rock and a hard place?

I don’t think it is the Fed’s raising of interest rates that puts them in a bind… it is WHY the Fed is raising interest rates that puts them there.

An institution that bought 4% mortgages when inflation was 2% expected to make 2%. Pretty thin spread but it can be profitable if you do enough of it… just ask a grocery store or a casino. But if inflation is running at 6% to 8% then you are LOSING 2% to 4% a year on those bundled mortgages… for 30 LONG years! That will put you in bankruptcy in a hurry if you don’t have sufficient reserves. It is not like anybody is going to buy that paper off you at full value.

Given that the Case-Shiller national home price index (FRED: CSUSHPISA) has risen for 7 straight months (Jan-Aug 2023) to a new record, why do Wall Street economists seem so confident that inflation is killed & won’t reappear?

They keep screaming at the Federal Reserve to stop tightening, because “lagged” housing data is causing inflation to be overstated. But wouldn’t this year’s home price increases eventually show up in OER, also with a lag, at some point in 2024?

Part of the problem is that 1/3 of all US home purchases are being made in cash. Who cares what the Fed does as long as I sold my $1 million house in a high cost market and am moving to a low cost market where I have my pick? I happen to live in a real estate market where prices have appreciated 50% in the last three years… and people from out of state are still moving in and buying because they consider the area a bargain.

Are you in Portland, OR? @Greg P

Wolf,

Some industrious person has produced the headline you’re looking for!

On investmentwatchblog:

“foreclosures-exploding-as-bidens-economy-falls-off-the-cliff-greg-mannarino-says-buy-silver-now”

The site describes itself as “A fine selection of independent media sources.”

Must be accurate, right?

/sarc!

🤣❤ Thank you for digging it up. When I wrote my remark — “So sure, someone clever could come up with a clickbait-title about foreclosures “exploding by 345%,” OMG, from Q2 2021. And we’ll just laugh about it and move on” — I figured I would see something like that.

So for the folks that only read the comments, you need to go upstairs here and look at the picture of the foreclosures, or you’ll miss the entire joke forever.

While there are people that want to rent and choose to do so there are also plenty of people who want to purchase a house and get some equity. When I bought my house 7 years ago at 405K neighbors thought it was high. It then shot up to 700K and has likely settled into the 650K range or so. I think the challenge a high asset market creates with high interest rates, high rent, and a slow down in construction is the opportunity for people that wish to start accumulating wealth. These cycles come and go but unfortunate for those that don’t have the means. My area could drop a little but our area has benefitted from Bay Area transplants where a $2500 sqft house for 700K is considered a bargain.

I agree with you

Same thing.. not in my neighborhood.:-)

Lemme guess…you’re in Austin.

If so, $450K very probably was too high! Anticipate a decent over-correction.

Sacramento, CA

bul/Glen – State Capitol correlations, mebbe?

may we all find a better day.

Living in a house will “accumulate” no wealth going forward, it’s just a place to live. The era of free money for doing nothing is over and the bay area transplants that do the same will dry up. The only price increases or even stability will be because your money is now worth less. There is no foundation under asset valuations at 8% rates. The zombie companies that burn cash will take a few years to die off, but that doesn’t mean it won’t happen.

That may be true in some areas but when rents are as high as mortgages one of creates equity and one does not. There is also no way to know how long existing rates will stay but certainly not that long. In my situation inflation has not been overwhelming as I have cut back spending some and search more for deals, plus plenty of credit cards and banks that throw money your way just to open up accounts for a few months. Admittedly this is different for everyone and especially difficult for those barely hanging on. Plus, if I retire and move out of CA or even the US my house here will take me farther elsewhere especially when downsizing.

Rent is nowhere near mortgages at this point and won’t be until real valuations crash. Equity, which you can only tap if you downsize or move to a less desirable area with the associated transaction costs, doesn’t mean much except to your heirs.

If someone bought a home here (eastern Washington) 15 to 20 years ago their mortgage might match my rent: $895. Possibly lower if its a lower end home.

Mortgages here today are typically $2300 to $3000. Yes they are in a house, I am in a 1BR apartment.

They have risks i dont have (major repairs, etc), property taxes,, higher utility bills.. High inflation is a risk I incur.

Nice for the 1/3 cash buyers…if rich. As to mortgages,

8% fixed, 30 year: 10 years accrue 12-13% equity, 15 years about 23%, 22.5 years 50% equity.

Last 7.5 years … if you haven’t sold long before then… only then do you obtain half your equity.

Readers here are generally more financially astute than I so this is ho hum I suppose.

Risks in RE tend to be underplayed in my opinion. Its akin to survivorship bias, call it success bias.

Can’t get hungover if you don’t stop drinking.

Interesting article. I live in a destination resort area that has attracted a huge amount of short-term rental investment. Some neighborhoods have attracted up to 20% short term rentals. Should the long-predicted recession ever develop, it will be interesting to see how many of these properties end up on the market once they go cash flow negative. In the aftermath of 2008, and at the depths, there were up to 1,000 foreclosures on the market in cities of approximately 40,000 people. It took about 4 years to clean up the mess.

@Desert Dweller, I don’t know your market (I’m guessing Palm Springs) , but in Lake Tahoe almost all the short term rental cabins are owned by people that want some extra income to make owning a “family cabin” less expensive and few are pure “investment properties”. For the people with W2 income that actively manage their short term rentals there is the is the “short term rental loophole” that allows losses from the short term rental to lower their taxable income that makes it easier to hang on when rental income drops.

The people who speculated on short term rentals won’t be able to sell, there will be foreclosures. Many of them will likely be underwater on their loans and even if they weren’t underwater they probably took the depreciation to defer taxes and the tax implications of selling would destroy them.

Wolf it’s great to cover housing and cars, will you please also start covering boats? You keep mentioning drunken sailors…

🤣

Freewary, if you want to know what’s happening to boats, just check the stocks of boat companies: e.g. Malibu Boats is very close to a 52 week low.

“Homeowners who bought over the past two years in some markets where home prices have dropped and who skimped on the down-payment could fall into trouble if they lose their jobs for long enough.”

Prices don’t have to have dropped. Just stayed flat, and they’re down 5-6% from selling costs.

“…in some markets where home prices have dropped…”

For example, 5-county San Francisco Bay Area – that’s a drop of around $150K:

but but but that’s only in NorCal, not SoCal like South OC or SD, it will stay flat worse case, as for SF, it’s just a gully, it will stay flat for now, peak in 2022 was just too insane…the current pricing is insanity we can tolerate

The housing market is vulnerable to a crash because of prices and rates. Much of what has supported consumer spending has been access to home equity. That money has churned. Home equity is not going to rescue consumer spending again. I’m concerned about the uptick in unemployment causing a housing correction and the cycle of pain that could create.

People with 3% mortgages may be smart to take cash out refinancing at 7% if they got enough cash out. When the next recession hits they will get mortgage forbearance from the government plus have a cash cushion to ride out job loss.

Gary, if you invest the way you’ve described above, you’re headed for the poor house.

I have a <3% mortgage. No way in hell am I going to borrow at 7+%.

Gary, did you forget the /sarc at the end of your comment?

I think you may need a good crystal ball to predict if forbearance will happen again. It has a precedent with Covid where mortgages, rent, and student loans all went into forbearance. However, nobody was left off the hook and are paying for it today. In 2008, people were let off the hook with massive foreclosures. It could happen again.

If you are correct, then taxpayers and more government debt will cover all of your debt and you enjoyed one last YOLO.

If you are wrong, you will likely end up on welfare with 20 feral cats in your old age living in a trailer in Podunk USA.

It is a gamble similar to putting all of your money on one number on the roulette wheel.

If my crystal ball hadn’t rolled off the shelf and broke during the 1994 Northridge Quake, I would have done this 3 years ago when rates were sub-3% and patiently waited to roll my windfall into 5.5% TBills, or AI stocks. It is very obvious in retrospect that I missed out, even though at the time, Wolf and others predicted this would happen.

We may repeat the late 70’s and early 80’s and mortgage rates will go to 18% and 30 year Treasuries will go to 15%.

I will then be saying “Gary was right.” I should have borrowed everything I could at 7% and lived off my 15% 30 year Treasuries without ever having to work again.

I don’t think you should ever fight the fed, Powell long ago said that house prices needed to come down. If shelter costs in CPI continue to stay hot, either Powell will have to acknowledge 2% target has moved or higher interest rates we shall go. I’m betting 2% target moves, cause US can’t afford another 2008 with our debt load.

I find it frustrating that with all our innovation, we cannot affect monetary policy without affecting residential real estate. It’s too easy to get a 30-year mortgage. The creation and destruction of trillions in annuity value is far to easy/fast. This is a place where regulation may be helpful in providing stability and reducing overall risk and inflation.

Financial ‘innovation’ = DOOM

Government intervention = DOOM

#EndTheFed

A house is to live in not to live for !

Been seeing lots of overpriced listings near Seattle with a long record of price reductions. Each week, a group of sellers on hopium realizes their listing price is not realistic, and they reduce the price. I see many listings with four to eight consecutive price reductions. Reasonably priced homes are still selling, tepidly.

The days of people listing their homes for crazy prices and expecting a huge windfall are going away, as the most unrealistic market players come to grips with reality.

As I’ve said before, a seller near me listed their home saying that “offers will be reviewed on Monday”. That was many Mondays ago. Seller had high hopes and is likely disappointed at the weak response.

Also, what I’ve noticed is that Redfin estimates the value of a listed home at near its listing price, so when a listing price is reduced, it reduces the value of that home plus other homes in the vicinity. Other realtor outfits may be doing the same. The listing price reductions of unrealistic sellers appear to have consequences for the market as a whole.

Bobber,

I’m a renter, the other end of the Evergreen state.

Thats Seattle. It sounds pretty different in parts of the Northeast and Midwest. Home prices more resilient, some cities at or near all time highs.

I’ve lived in the Pac NW 27 years (4 near Seattle) and one more bad wildfire season and I am outta here. This year wasn’t bad, one day toxic air (AQI over 300) and maybe 6 or 7 smokey days. Nothing compared to some of the last 8 years. Certainly won’t consider California, Oregon, anyplace out west or Texas as a destination (lived in TX 11 years).

Sort of unrelated, but then maybe it is related.

Are HELOCs the “last pot of cash” available to middle and lower incomers (and maybe high earners who overspend) whose incomes are no longer enough to support their “drunken spender” life styles???

I’m thinking of some recent reports of reduced savings, and increased credit card debt. I don’t have the specifics on those but have to wonder, are HELOC’s just a larger credit card of last resort to keep the the “lifestyle” going for another year? If so, will these folks “tap out” when their maxed out debt has them in a choke hold?

“increased credit card debt”

This is a poor measure of consumer stress, because lots of folks (myself included) run all purchases thru a CC to scoop up the points, but pay the full balance every month and don’t accrue interest.

Imposter,

This stuff is just funny. In liquid assets, consumers have $6 trillion in money market funds, and about $10 trillion in bank savings products (savings and CDs), and they have a gazillion in Treasury bills, notes, and bonds, and they have many trillions in stocks that they can sell any moment and turn to cash. This idea that American consumers don’t have anything is just hogwash and needs to die.

In addition, a record number of consumers are working, and with the biggest pay increases in 40 years, they make the most money ever.

People who cling to the hoary belief that Americans don’t have anything and are poor, and tapped out or whatever, will never understand the US economy and US consumers, and will always be surprised by them.

I made the speadsheet for the ratio of median home price annual payment to median income, with a 30 mortgage at current rates, perfect credit, and 6% down (the typical downpayment for first time buyer). The results are brutal. California is the worst,

of course, requiring 76.9% of median *household income to buy the median priced house. Doesn’t sound hoary to me.

1. LOL, you’re completely ignoring what I said and pretend to argue with something I didn’t even talk about. So re-read what I actually said. That’s step one.

2. Just to blow you out of the water: Despite your spreadsheet, Californians have so much money and income that they buy lots of homes. Or who else do you think is buying all these homes that are sold in California every day? Martians?

3. Median income = HALF of the households in California MAKE MORE than $84,100 (2021 Census figures, higher now). That’s 7 million households in CA make over $84,000. Try to wrap your brains around that.

I am bit old fashioned but if “Buy low, sell high.” is to work you have to execute on the “Sell high” part. Wages will not go very much higher, and real estate is an illiquid market. Home prices need “bigger fools.” The buyers smell blood.

In a capitalist market there are always smaller operators who can put up a new single family home at reduced labor and materials and make a decent margin. AS they did in 2001 they will undercut established home values.

Maintenance, taxes and home owners insurance have really hit the owners of rental properties. The competition is on for an affordable home where a family can get ahead. For young people seeking to get on the map and start a family, new megasites beckon and being fully mobile, they are tired of being priced out of home ownership.

Now is the time when the economy shifts again and determines winners and losers. The rust belt formed slowly, and then all at once.

“foreclosures “exploding by 345%,” OMG, from Q2 2021. And we’ll just laugh about it and move on”

This is why I enjoy reading your blog @wolfrichter. Everything else is just noise compared to how you produce your work in a genuine way. Thanks!

I am starting to think the consumer will hold up and that what will take this all down is the financial community, specifically financing the government debt.

Consumers have received raises, much higher interest payments, ballooning home prices and forebearance on student loan debts. So they are still stocked with cash (depending upon where they fall on the income scale).

Within just one year, the Treasury dept decision to move to bill issuance instead of bonds wont matter – the problem of financing the deficit will be real. This was a short term solution that only lasts until they empty the reverse repo trillion dollar stash into short term Treasuries.

Faux Business headline, ” mortgage demand stirs back to life as interest rates plummet.” Lolol.

Not until you get way past the headline do they mention purchase and refi were up over the week but remained at low levels.

Good old Ministry of Truth.

Always a healthy dose of reality.

I think the possibility of a residential RE crash is still a few years away. Here’s what could trigger it.

1. Rates stay high and/or increase.

2. Investors who typically buy with 3-5 year ARMs run out of time.

3. Properties no longer cash-flow.

This would need to happen in large waves to flood the market with inventory as investors list their rentals for sale and the buying pool dries up.

Airbnb as well as “savvy” investors would wind up walking away from upside down non-cash flowing properties.

It would be interesting to see what percentage of foreclosures are primary residences.

Given the sheer volume of monetary inflation in the USA over the past decade, especially the past 3-4 years, those numbers are quite healthy. Mortgage debt in real terms may seem high, but relative to money supply and circulation, the total debt is very small. The significant surge in illegal (but somehow sanctioned) immigrants is likely to further drive the need for additional housing. Yes the affordability seems dire, but the demand is still far greater than the supply. Affordability is bound to put downward pressure on the housing market, but supply/demand mismatch will put upward pressure on the market, likely to stagnate or further inch up prices.