NAR, the Realtor lobbying group, demands its easy-money heroin back that the Fed has confiscated.

By Wolf Richter for WOLF STREET.

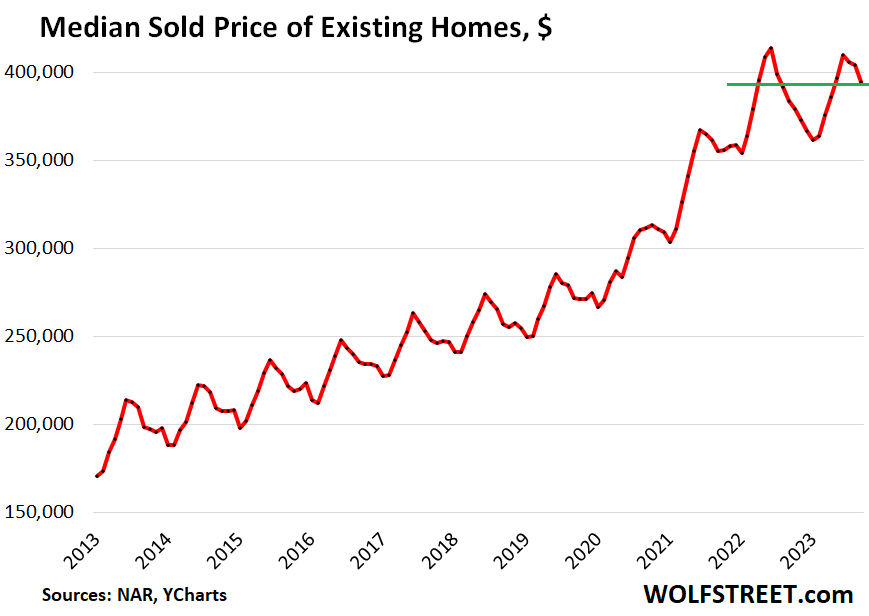

The national median price of previously owned houses, condos, and co-ops fell to $394,300 in September, down by 4.7% from the peak 18 months ago, in June 2022, according to data from the National Association of Realtors (NAR) today.

June is usually the seasonal price-peak of the year, but June 2023 was below the peak in June 2022 for the first time since the Housing Bust, and prices skidded lower since then.

Due to the price plunge last year in July through September, the median price was up year-over-year by 2.8%, but that was a lower rate than the 3.2% year-over-year in August (historic data via YCharts):

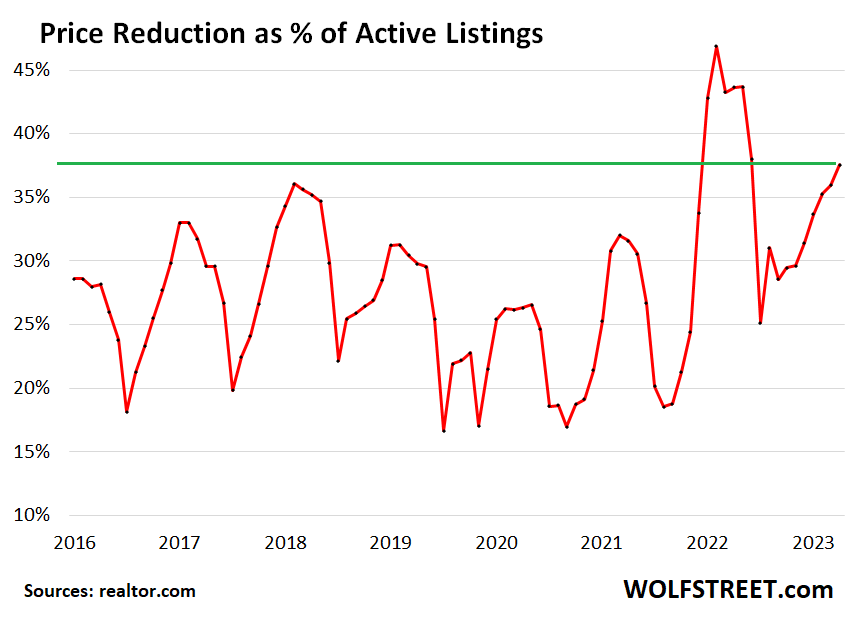

Price reductions jumped to 37.5% of active listings in September, blowing by the pre-pandemic highs, as sellers are getting more motivated to sell their homes while buyers have vanished at these prices (data via realtor.com):

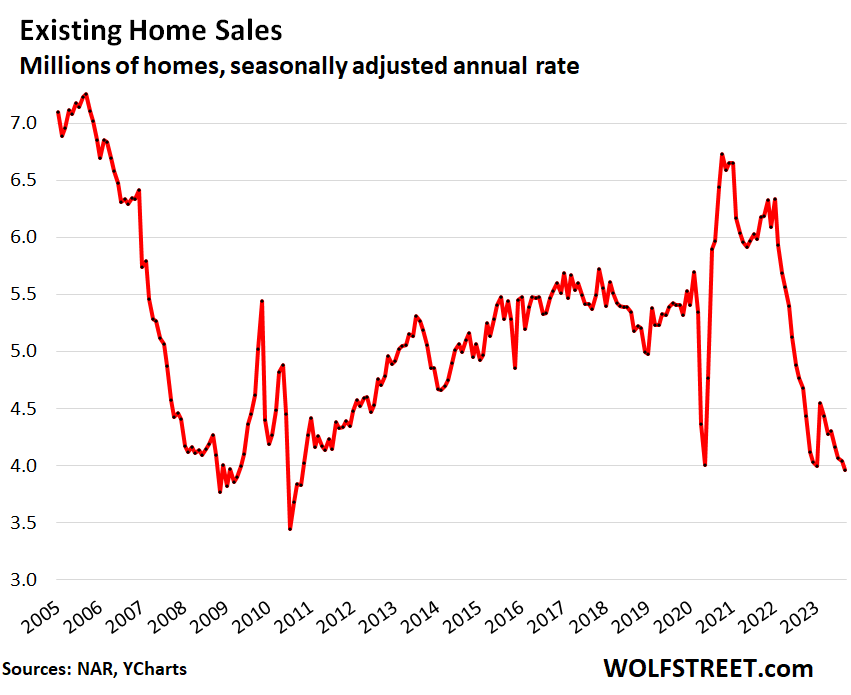

Sales of previously owned houses, condos, and co-ops crashed to a seasonally adjusted annual rate of 3.96 million homes in September, the lowest since the depth of the housing bust in 2010. Compared to the Septembers in prior years (historic data via YCharts):

- From 2022: -15.4% from already depressed levels

- From 2021: -35.9%.

- From 2019: -26.8%.

- From 2018: -23.6%.

The NAR demands its easy-money heroin back from the Fed.

“The Federal Reserve simply cannot keep raising interest rates in light of softening inflation and weakening job gains,” whined NAR Chief Economist Lawrence Yun in the press release, because the NAR is a lobbying group for Realtors, and Realtors make commissions off every sale they handle, coming and going, and as sales volume plunges, their income plunges.

The industry has gotten hooked on the heroin of the Fed’s easy money between 2008 and 2022 that caused mortgage rates to plunge below 3%, and home prices to inflate to the moon, and now they hate the normalization of interest rates, and they want their heroin back.

Obviously, Realtors and the NAR could boost sales volume by pressuring their clients to lower asking prices by a big chunk to bring them in line with 8% mortgage rates, and these lower prices would bring out the buyers, and that would help getting the market out of the deep-freeze, but no. It’s much better to whine to the Fed about handing out more heroin.

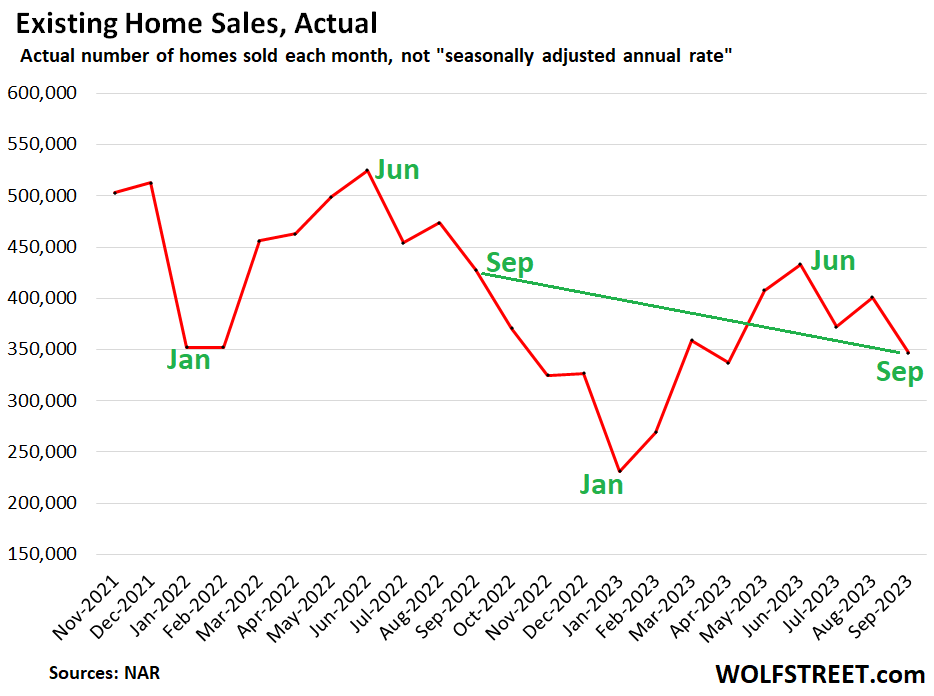

Actual sales – not seasonally adjusted annual rate – fell 18.9% from the already depressed levels in September 2022 to 347,000 homes.

January and February usually mark the low points of the year; June marks the peak volume and the end of “spring selling season.” During the second half, sales careen lower. The actual sales data offer a better picture of sales and seasonality than the seasonally adjusted annual rate of sales above (data via NAR):

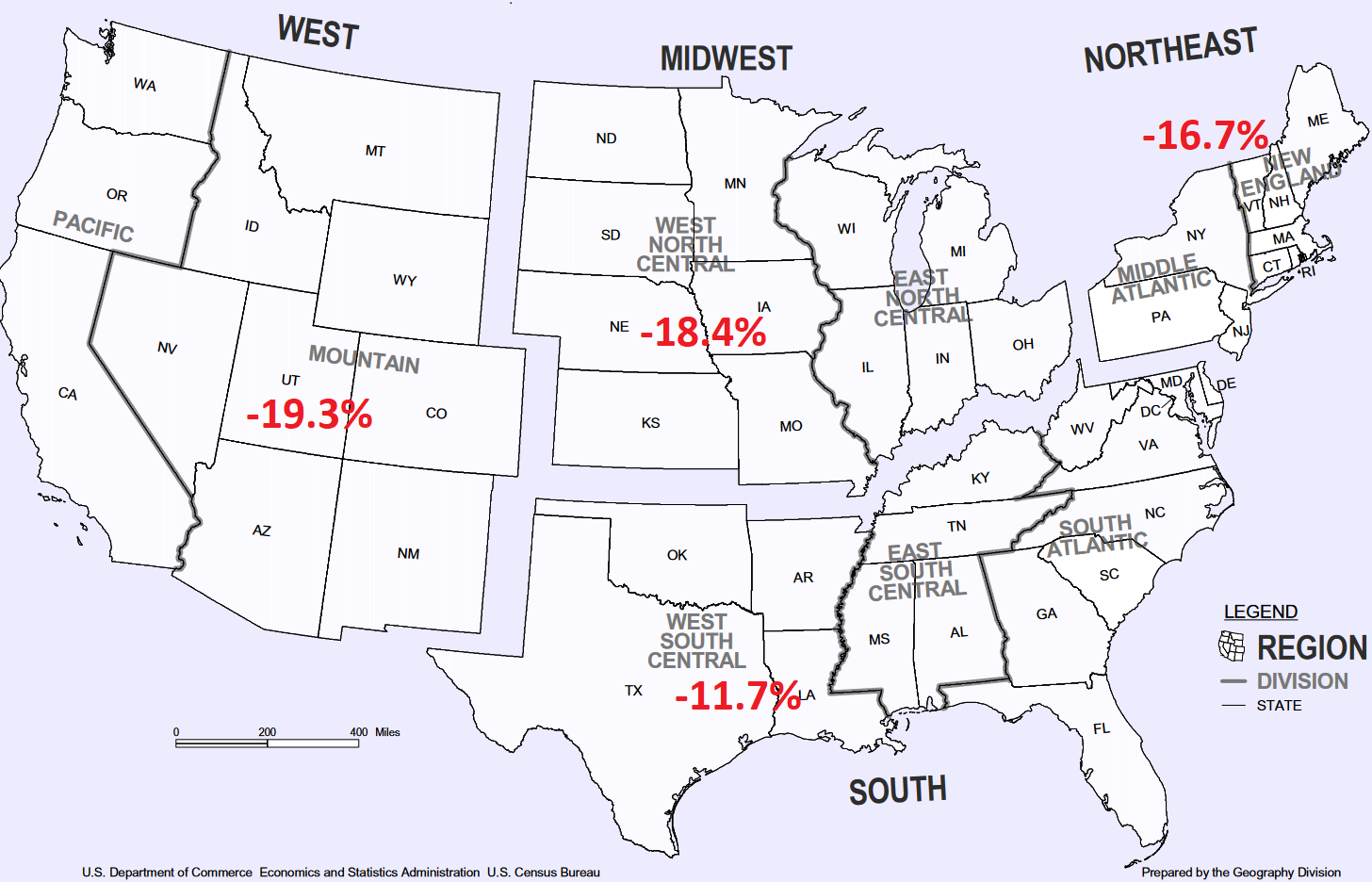

By region, sales plunged in all regions from the already beaten-down levels last year:

Demand and supply have vanished in equal measure.

I have described this phenomenon here: Homeowners with a 3% mortgage are not buying a new home, so they have vanished as buyers; and they’re therefore not listing their current home, and so they have also vanished as sellers. This phenomenon, according to my estimates, caused the entire housing market – buyers and sellers – to shrink by about 20%.

These homeowners vanished as both buyers and sellers at the same time. They left the market as buyers and sellers. As a result, there is less churn, and Realtors make money off the churn coming and going, and so the NAR whines about this situation that is so dire for them.

But as far as the market is concerned, with both buyers and sellers gone in equal measure, the balance is still there, but it’s just a lot lower: lower demand, lower supply, and lower churn, and less money for Realtors.

Realtors could help fix this situation by exhorting sellers to bring their asking prices in line with 8% mortgages, which would help this market emerge from the deepfreeze.

Cash buyers have pulled back too starting in mid-2022. Sales to cash buyers have stabilized at about 100,000 per month over the past five months, down about 20% from early 2022.

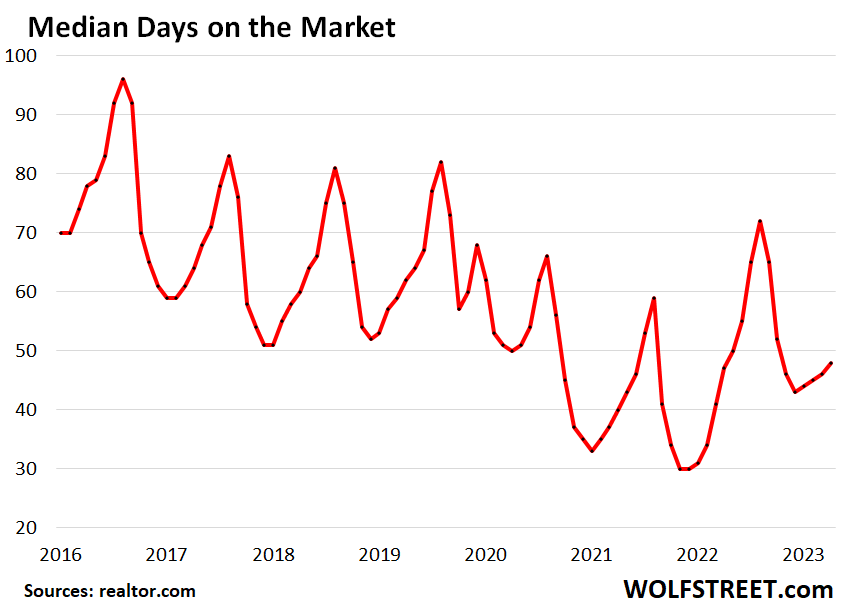

Days on the market lengthened further: Homes spent 48 days on the market in September before they were either sold or pulled off the market, up from 47 days in September 2022, according to data from realtor.com.

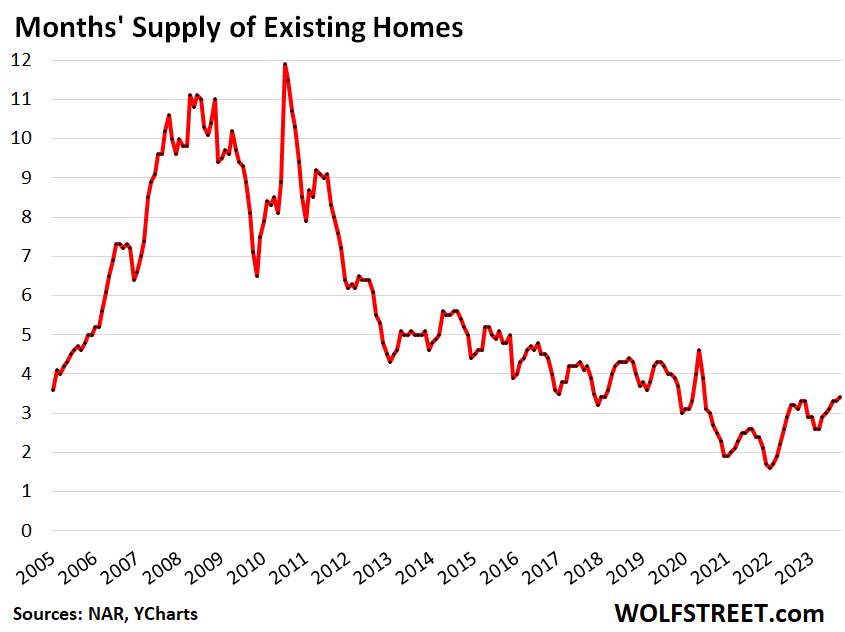

Supply rose to 3.4 months, the highest since June 2020, with 1.13 million homes for sale in September, according to NAR. Supply in 2017 through 2019 ranged between 3.0 and 4.3 months (historic data via YCharts).

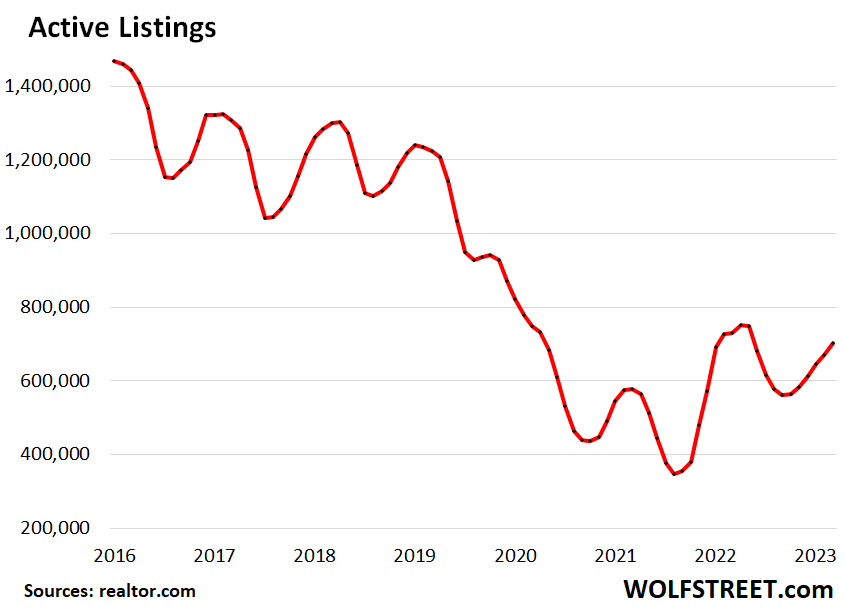

Active listings rose by 4.9% in September from August — much more sharply than the slight increases or even decreases that were normal from August to September before the pandemic – to 702,000 homes. This cut the year-over-year gap by nearly half, to 4% (data via realtor.com):

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Lawrence Yun’s ass should be out on the street. He’s no economist, he’s a cheerleader, just like the rest of that organization.

+1 to that. Greed machine.

So NAR sent letter to Fed asking it to stop raising rates. Their reason: they want to help the “little guy” by making housing more affordable.

The truth is that NAR narrative of higher housing prices is causing unaffordability. NAR leadership now consists of big REIT investors, REIT managers, Wall Street RE funds and other Real Estate investors that hold multiple houses. So, the NAR leadership doesn’t earn from commissions, but from appreciation of their assets. So as the mortgage rates rises to 8%, NAR leadership spreads misinformation to protect their leveraged bets.

This result is lower house sales (now 50% lower in Northwest) and lower commissions for real estate agents. So this year bankruptcies in Real Estate sector has exploded to highes in 10 years, and is leading all other sectors in bankruptcy filings.

So NAR is bankrupting and screwing the 2 million smaller real estate agents and other professionals (Appraisers, Inspectors etc). Before thousands of these professionals go bankrupt, they must fight. Best is to refuse sellers and builders who want to list properties at unreasonable prices from when mortgage rate was only 4%.

Already in Seattle area, 80% of the listings above $1.5 million have stopped selling causing agents to lose time and money. These houses either keep sitting in market or get pulled. The only properties that are selling in this range are the ones from motivated sellers. E.g. Recently owner of a good house passed away and the trust put the luxury maydenbauer house on sale at reasonable price of $2.1 million for a house that sold new for $1.7 million in 2017. This house sold for close to $2 million. There are many other houses on market in area that were worth $1.2 million in 2017, missing the luxury features, and are asking for $2.5 million now with no chances of selling.

So the NAR narrative around locked-in low rates is BS. Life does happen (marriage, divorce, retirement, layoffs, passing away) and these house sales will determine sale price and value going forward. NAR should change narrative to protect RE professionals by educating sellers that mortgage rate rise has both stretched and disinterested buyers, so to sell they need to drop listing prices significantly below the stupid Zestimates, and just below the value assessed for property tax.

Correct. Pure GREED. F’em. It’s long past time we STOP rewarding bad/predatory behavior and allow the good/helpful real estate agents and property managers to actually flourish. There are some, and if you own investment properties, you know they are actually very valuable.

You shouldn’t need a life event for inventive to sell an overpriced home that appreciated 300% in 10 years. All you need is a small bit of financial opportunism.

For people sitting on that 200-300% appreciated Seattle home, particularly those relying on it for retirement security, there’s an amazing opportunity right now to sell the home and put the proceeds in safe fixed income investments generating interest income of 5-7% per year, out to as far as 30 years.

After a sale (near the top), you can downsize to smaller digs or rent a fabulous place under a long-term lease. Truth be told, a $2M home is Seattle is the equivalent to a $500k home in the Midwest or a $300k home in Florida, in terms of quality, age, and finishings, so you could sell the Seattle home, migrate to another location, and live in a home that is twice as nice, plus have tons of additional income to spend.

The window for accomplishing this grand play might last only a couple years, because home price drops may accelerate, causing the Fed to reduce interest rates, and the ability to lock in high interest rates may dissipate, as the window closes from both ends.

I’m already seeing several homes purchased in 2021/2022 timeframe with Redfin values 10-20% below original purchase price, and the sellers of those homes are glad they sold, particularly if they are retirees that locked up a huge interest income stream.

Another part of the NAR lie is that home prices will not fall. That narrative convinces people to hold onto their “asset” instead of putting it on the market and selling, thereby preventing the clearance of prices to lower levels.

This will end badly for homeowners. Once price decreases become entrenched, the buyers will demand much lower prices and many will just wait out this situation.

See South Park episode “City people”.

About real estate agents….good laughs.

Seems like 99% of the readership are renters.

LOL. This site has about 600,000 visitors over a 30-day period. You have no idea who they are. I’ve heard from a bunch of them, so I have somewhat of a feel. They’re high income and skew male. Many work in finance.

What you’re seeing are commenters — there are about 100 on each article. And some of them are renters as per their own comments. Others are owners, as per their own comments.

I might consider some of these homes with 3% mortgages

will offer wrap and cash to mortgage

take it or I’ll offer less than owed

I’d love to know how much the average initial mortgage payment has increased over time. Home prices and interest rates are up so surely it’s more than the official inflation rate, but how much more?

@Andrew,

You can calculate that using a spreadsheet such as MS Excel. You use the PMT() function.

Here is the monthly payment for a 30year mortgage at 3.5%, on $600,000

($2694.27)

If we increase the mortgage rate to 8%, the payment becomes ($4,402.59)

So in the example above, a 4.5% increase in the mortgage rate caused the monthly payment to increase by 63%

Similarly, it is possible to calculate increased household income required to meet greatly increased monthly mortgage payments, using traditional lending ratios.

Spoiler – it is a huge increase, in line with greatly increased monthly mortgage payments.

Shocker…home prices doubled or tripled from 2000 to 2021, not because median household incomes doubled or tripled (far, far from it) but because the G strangled interest/mortgage rates from 8% to 3% (by printing money and other tactics that grossly engorged funds available to loan as mortgages).

All that is happening now is that the fraud is unravelling.

DC/the F created a delusional economic fantasy land (at the cost of inflation, both hidden and later uncontrolled) that animated the corpse of the American real economy…Housing’s Zombie Economy…the Walking Dead.

Another more comprehensive way is to actually factor in property tax, down payment size, mortgage rate, HOA (if applicable) and also opportunity cost. Did some numbers around based on SoCal current housing price in decent neighborhood and the disparity is quite amusing to say the least….I often run these numbers just for a good laugh and to get an idea when it’s good time to buy compare to rent..on a rate like this you’re paying over $875K in interest for the duration…yup it’s a great time to buy.

Using a 3 bedroom 2 bath house you can rent, same neighborhood, similar style. Difference is close to $2K a month and this is after putting $350K also assuming 5.5% opportunity cost, which is pretty easy to do consider T bill pay close to that.

Rent $4500 a month

vs

Monthly total $6300 a month (Mortgage, HOA, maint, property tax)

$350k down on a $920K house 30yrs fix at 7.8%

Plus taxes & insurance. Maybe HOA. All expense qualifiers for mortgage approval. Plus car payments etc.

I think the $4,402.59 sounds great for those who suffer of FOMO :)

Basically a 2.75% mortgage of a $500k house is $1000 a month cheaper than 5.5%

And $500 a month cheaper than 8.0% rates.

Give or take, rough math.

I just always say, the$ 500k home families are doing wheelbarrows full out of Costco with their savings.

And just think, what if the fed ever cuts rates from 8-10% back to 3%… oh boy! 2 wheel barrows at Costco!

The Fed won’t cuts rates back to 3% unless something really bad happens. In that case, the homeowner in your example maybe loses his/her job and therefore can no longer afford the 3% mortgage.

Harvey, one guy was rattling around here at the halls of wolf. I think he was 60+ years old and lost his job.

He had so much equity that the bank worked with him. I’d guess if your equity was less than 20%, they may give them the boot. But maybe not!

Ah yes, good point!

When home prices are increasing, the increased equity value offsets that higher cost, but once prices fall for a sustained period of time, the whole equation changes.

We have neighbors nearby. Theirs is a two-story home with lower income/middle income areas.

The owners and the realtor are asking $595,000+

Are they crazy! To make matters worse, we live in a State that heavily taxes any homes that sell.

They’re a relatively young couple. We hope they realize what is going on in the real estate market here along with Big Taxes when selling a home.

To call that shill an economist would be an insult to a real economist…at least one that doesn’t preach QE and easy money is the way to fix all of our economy’s problem

Then again he can just carry his “economist” title like how banks like to call their middle manager VP…

Most economists are shills.

To your point, just take a look at California Proposition 19 from 2020 funded by The National and California Association of Realtors.

I recall the tv ads had elderly couples getting kicked out of their homes because they couldn’t afford to stay. What they didn’t mention is that the increase was due, as it had always been, to the purchase of another home with a typically higher tax assessesment. More importantly, they didn’t mention that upon death a house left to a child would be reassessed at the current value unless that child made it their primary residence. In other words, most people inheriting property would not be able to afford the new tax assessment and would thereby have to sell the property.

The realtors stood to make a ton of money, as a state proposition cost analysis pointed out. When confronted with this, Jeanne Radsick, president of the Realtors group, said, “It is not about making money for the Realtors, for crying out loud. It’s about tax fairness for people who need help.”

Um …riiiiiggghht.

Needless to say, it passed because the typical voter didn’t bother to read the actual proposition.

He’s shark chum, to me.

Perhaps if we step back a bit and look at the bigger picture. Keep in mind that it was not only NAR, but also MBA and NHBA that requested rates come back down.

It’s certainly a damn if you do/damn if you don’t.

But, the reality is slowing the housing market with higher interest rates has a side effect of slowing economic US growth as well.

Point being, housing is approx. 16% of annual GDP.

We NEED HIGHER GDP due to insanity levels of the deficit and national debt.

We’re spending 113% of every tax $1 revenue.

Also, new loans for more $ means more new money in the system, i.e. Increasing Liquidity.. Liquidity is what drives interest rates up and down. It also drives prices up and down.

Fewer new loans on higher prices means less liquidity in the system.

Kind of bizarre that a speculative fervor can drive rates down due to increasing lending against the same asset creating more liquidity whereas the opposite happens when a peak in affordability or ability to repay ends the growth in new higher loans being created and gravity take back over.

Thing is, it takes actual an increase in productivity to create the wealth to make the payments (service increasing amounts of debt). There really is no free ride. Just cycles.

As in a house, just because it costs more, doesn’t mean it is actually worth more. After all it is the same house.

This all goes back to Minsky’s Financial Instability Hypothesis.

My dad built a house in 1991 as a spec. He fell in love and we moved in, always planning to go back to our first home and sell the spec. For 15 years he priced it at the top of the market, it was hand built and had details and a layout that made it unique and special. No one could meet his ask, which was almost 2 million. In the early 2000s he stopped trying to sell and we settled in. 2009 rolls around and the house obviously lost value, but we weren’t selling anymore. Right now it’s estimated at nearly 4 million. Will it go down? Maybe.

The point is we survived the 2009 bubble and it’s more than doubled. The next bubble will pop and in 15 years people will wish they had bought at the top of the last market. Profits and losses are only had if you enter or exit. Ideally you don’t want to wait 10 years to break even, but it’s a home not a speculative stock purchase. It’s a place to live and raise a family. If you lose money on a home but you love it, that’s OK. Homes should have intrinsic value beyond numbers.

For me, besides being a place to live and a place of solace away from society, it’s also an inflation hedge and an entrance fee towards my eventual retirement village. Quite a great deal really. It’s too bad we screwed the younger folks out of the same possibility. The best option for them right now is inheritance or family support on the mortgage.

Just placed an offer for a buyer 13 other offers tried another house 5 offers don’t see the prices coming down

Honestly how realtor’s continue to get paid 3% (each?!?) on transactions both saddens and befuddles me. Personally I’d rather pay them $xxx per hour and let the great ones earn more and the terrible ones find new careers. Leeches IMO.

6% is a tremendous amount to pay to sell a house.

Plenty of realtors out there are willing to work for less, Though still overpriced for the service they provide. Redfin has a program where if you list/sell/buy with them it ends up being around 4% If I recall correctly.

These days when everyone is looking on Zillow anyway, it’s hard to justify the price of admission to have a realtor hold your hand while you sell. You can list FSBO on Zillow directly and offer a 2.5% commission to buyer’s agents and still get showings.

Possibly depends on the location price of home and the buyer agent commission. 3 percent to a buying agent is a base case in my rural area. That leaves 3 percent to negotiate with and agents that are not brokers usually are at 2 percent of a 6 percent sell. So cut them 50 percent ? I am not a realtor just a realist

Which is why I always try to find the owners and contact them directly somehow…eff both agents, what do we need them for? Get two lawyers to draft something up and be done with it.

We did that when we lived in California. It save the two parties lots of $$$. :)

Agreed. They hardly do anything aside from forwarding listing in the MLS and processing a few standardized documents at closing. They surely don’t deserve $12k for that effort.

$12k? On a pedestrian coastal area $2m tract home, try $120k. Might have something to do with why there are so many realtors….

Got fooled by a so called “great one” then the screwing started. Lesson learned never ever trust a RE agent!

“Get all the house you deserve”

The living pile of slime who sold me my home in 2005 actually said that. And like an idiot, I fell for it. So then I ended up underwater. And not by a small amount either. So far under water I could see Navy Seals training by looking up.

“May you live in interesting times”…that ring a bell for anyone?

Never again. The next time I bought was in 2013. Bottom of the market where I lived, and THIS TIME, I picked up a modest 3 bed 2 bath 1 floor 1500 sq ft. On track to having it paid off in 13.5 years not 30

Hopefully you refinanced at around 3% and if so, wouldn’t it be better to not pay down your low interest mortgage when you can earn more in interest with that money?

yes awesome we live we learn debt free is the only way to not be a slave.

“Get all the house you deserve”

Yolo!!!

The battle cry of modern day salespeople, everywhere and selling anything, trained in nothing but the crack cocaine business model (“first one’s free/Yolo!”).

The truly horrific/tragic part of it is that the American consumer economy has been so deeply addicted, for so long, to the Debt Lifestyle Lie, that going cold turkey would likely flatline the American economy.

sorry to hear about your experience. my realtor was great, no pressure tactics at all. I saw about 40 homes then decided against buying altogether, in 2012! I missed out a lot. I actually wish they would have pushed me somewhat. No fault of theirs, just got bad advice from a friend.

I just see so many negative comments, I’ve to say that’s not all to it. Point is, we have to learn our own lessons and build good instincts.

I do think 6% is ridiculous. That itself creates upwards price pressure.

I think an hourly rate structured with some fixed bonus upon closing is a good way forward.

@Natalie,

“Lesson learned never ever trust a RE agent!”

Don’t trust the escrow company either. Make sure their math is correct.

We should sponsor a law which states all realtors have to wear a CLOWN outfit…. :)

And with our never ending tip culture only unique to US…I wouldn’t be surprise these RE agents stick you with the commission and then bust out the smartphone with the screen showing 15%/18%/20% tips on top…

LOLOLOLOL

I’ve used Assist2Sell before, they charged a flat fee.

We can’t get the Realtors to even open the house up for the appraisal. They want us to use lock boxes, while they sit on their asses in their homes or on the beach doing nothing. A few of them do a good job, but most are lazy and incompetent. My personal experiences are total failures. 6 transactions and all disasters in part because of the Realtors.

In high home price markets like bay area agent commission on a $2M+ average home is about $120k. Very few consumer industries have that kind of outrageous commissions for the level of service. Politicians from both sides protect these lobby groups.

There have been flat fee realty companies for at least 10 years. $400 – $600: sign, pictures and MLS listing, The listing agreement provides for you to allow for split of a standard commission to buyer broker, if any. I could provide names and links for Chicago area, but Wolf doesn’t go for that here. Sold 4 unit apt building in 2016 and house in 2021 this way. No prob.

Thanks! My wife and I were thinking about selling our home earlier this year and decided not to because of the massive realtor fees.

I sold my condo by myself which cost me $100. I used an MLS listing service, no realtors. An investor bought it so I didn’t have to pay any commission, even though my listing said 2% buyer’s agent commission. It’s up to you how much commission you wanna pay to buyer’s agent, it can be as low as 0%.

I also sold my condo myself, didn’t even list it or advertise it, just shopped it around verbally with people I knew, and people they knew. Worked great. Took a couple of months from the first moment till close. Cash buyer, retired couple, who’d heard about it from someone I knew. But it was a unique big condo, with lots of appeal for a couple without kids, or as a bachelor pad (my case). People knew about the condo. And maybe I was lucky. A sale like that may be harder to pull off with a standard-issue home. But people should try it first, and when there is no movement, work with a professional.

Realtors have only exhorted buyers to overpay to “win the bid”.

Perhaps a not insignificant number of realtors are also speculating on homes and strs.

I’ve only dealt with a few realtors in my life so this is very anecdotal but three quarters of them “invested” in RE. Most memorably the last one I used to make a sale, between him and his wife who also is a realtor they owned around 20 properties together. I think probably most of the “successful” agents own more than just their primary, durring the huge run up it’s hard to imagine they could watch the large appreciation and not jump in if they had the means. There are however a lot of realtors and many are not that successful

Exactly. And this is why there are so many realtors, even as sales fall dramatically.

Boston globe just reported a new (opened one year ago) high-end condo building in the seaport reduced their price by 20% below recent sales in the same building because no one is buying.

The seaport was massively overpriced in the first place.

I worked on a boat that docked in the seaport this past summer. When leaving work at night, I’d note how many lights were on in all the ritzy new towers.

I’d estimate a 20% occupancy rate in these towers, based on the number of windows with lights on.

I agree, it was and still is massively overpriced but now the condo someone bought just few months ago worth 20% less according to the building developers.

Boston globe also just reported that “Mass. home prices hit new highs in September”. Google it.

Yes, but in downtown Boston condo prices were 10% lower compared to last semester, did you see that part SocalJim?

Overall, prices in metro Boston have hit an all-time high. People are moving to the suburbs from downtown condos. Suburb prices in metro Boston are hot.

🤣 skipped over that section

Funny stuff. Something is wrong with your comment that Boston condo prices dropped 10%. Just now, the Boston globe just posted a new article titled “Condo prices in Seaport and Back Bay soar”. This article discusses condo prices in all areas of downtown Boston. Google it.

Here is the text:

The average sales price of a condo in the Seaport and Back Bay surged in the third quarter this year, according to a report Douglas Elliman Real Estate released Thursday.

The average sale prices of $1,573,159 in the Back Bay and $2,319,610 in the Seaport in the third quarter reflect cost jumps of 63.9% and 61.3% year over year.

Meanwhile, the average cost per square foot hit a record high in Downtown Boston: $1,360. And sales rose year over year there for the first time in seven quarters, according to the report.

In a faint ray of hope for condo buyers, prices slipped, but only slightly, in Charlestown, the Back Bay, and the South End, Douglas Elliman reported.

Case Shiller sez Boston condos peaked in Feb 2023.

That is because Case-Shiller does not have the September data. Their numbers are months behind.

BTW, here is Zillow’s median price index for condos in Boston, seasonally adjusted. It barely edged up from Aug to Sep and remains well below the peak. Everyone’s got a different story:

How does it feel to be such a sleazy shill, SocalJim? I mean, seriously….

may be he is a realtor…….

I never use a Realtor to sell real estate.

However, I always work with the Listing Agent to buy real estate. Buyers using a Buyer’s Agent have to offer twice as much for the Listing Agent to make the same commission.

You might be surprised how hard they work to get the Seller to accept your lowball cash offer.

The Fed voluntarily took control of the economy. Now it is unfair to blame these folks. They aren’t economist and shouldn’t have to be. They are trying to earn a living like the rest of us.

The fed should took blame for all these distortions in the economy because of a deranged monetary policy. Not sure what good came out of it. But ordinary folks will now bear the brunt

Who could have known locking 65% of the population, homeowners, into a 30 year mortgage rate based on ZIRP would create problems?

Let’s give the Fed a pass.

Sarc.

Bobber,

I think Aman is blaming the Fed for the economic distortions, but absolving Realtors. I’d point out that Realtors cheered on the boom created by easy money, and will now need to endure the bust caused by the end of easy money.

Aman notes Realtors are not economists, but as professionals they should understand the link between interest rates and the “product” they sell for a living. Perhaps this experience will teach Realtors that easy money policies and ZIRP are not good for the long-term stability of their industry. Who am I kidding…

If Bezos can get carried away with ZIRP and hire an army of people (assuming it to be the new norm) then consider the plight of ordinary real estate agents.

FYI Bezos has a high profile chief economist to guide him.

The reason monetary policy swings cause distortions is that at the time it feels real, the demand is real paid with real dollars.

And this time the Fed outdid itself. We had to create new fictitious assets (think NFT, crypto etc.) to absorb the deluge of cash that was injected.

I think we have to blame the Fed because such craziness was relatively rare prior to arrival of the maestro a.k.a Greenspan and his disciple Mr. Bernanke (who couldn’t see the greatest financial crisis brewing under his very nose yet was very confident in all his policies and decision)

The more I read about this stuff the more sympathy I have for the common man and the more I feel that the Fed has done great disservice to this country…..maybe I am being harsh :)

@Aman: No, you’re not being harsh. Zirp is a policy for the rich, to the rich, and by the rich – just executed by the so-called independent Fed.

It encourages risky behavior and penalizes the prudent.

It forces people to take huge risks on their savings – by chasing a decent return in the stock market which benefits “smart investors” who sit at the top of the food chain and know when to buy and when to exit. It also leaves people no choice but to buy high-priced essential assets like homes with the hope that the prices will increase or at least hold up.

Companies benefit from low interest rates while channeling all the profits to top management.

In summary, it is a pyramid scheme with people at the top of the pyramid sucking up all the money from those at the bottom. Unfortunately, this is how our economy has operated for the last 40+ years.

Aman,

I guess Bezos and the NAR have something in common: a high profile Chief Economist to guide them. Did Realtors get bad advice about the long-term consequences of ZIRP and QE from the NAR? Realtors purport to be professionals and are advised by a professional body that seems to have dropped the ball to their detriment. I may be wrong, but I’ve never heard the NAR discuss the potential negative impacts on the market resulting from ZIRP and QE if interest rates ever went up. The current situation is an outcome they should have considered by the NAR, but apparently it wasn’t.

I agree with nearly everything you say and am definitely sympathetic with the plight of the common man resulting from all of this financial folly, but I don’t necessarily put Realtors in that category. They are part of a professional organization with a strong lobbying component. They should have known the risks, but the easy money was just too good. Probably because, as you say, it was paid with real dollars.

I admit to not having a good experience with Realtors both times I used them. I’m sure there are many exceptions, but I learned that I’m my only advocate in a real estate negotiation and my grasp of my market is probably better than theirs. Either that, or they were lying to try and close a deal. Closing the deal seemed far more important than my interests as the client. The first time I was young, naive and let the deal close. The second time I called off the transaction and haven’t used a Realtor since.

“The Fed voluntarily took control of the economy.”

Their “purview” expands over time and with each emergency (usually created by the Fed)

Agency “creep” I think they call it…..(I know, the Fed really isnt a federal agency)….but they push their borders out and no one is there to stop them.

From initially being a backstop, lender of last resort in banking problems…to the minter of digital money.

That’s a leap.

Much like the “necessary and proper” and “promote the general welfare” language in the Constitution which can be taken as open ended (though not intended)…..the Fed’s mandate to promote economic stability morphed into pushing never ending GDP growth and a stock market that goes up every year. From lenders of last resort to central planners. Autonomously.

Lower prices + no sales + rising mortgage rates = the dam breaks

Illiquidity is a symptom of a broken market.

The gyrations of the Fed have pushed buyers and sellers away from each other.

I’m wondering is there anywhere to get the change in sold prices on a sq footage basis? i.e. how much is price changing of the same size house? Median prices of housing sales overall could impacted by many factors depending on the type of buyer, if the middle class is tapped out and only the upper middle class and wealthy keep buying it will trend higher, if people are buying smaller houses but paying more per sq ft that “price increase” could still theoretically show up as a price decrease because they’re buying much smaller homes at 8%. Even better would be change in price paid for SQ ft by zip code because if there’s a significant shift in where people are buying that could alter how comparable year over sold home prices are.

The Case-Shiller Home Price index is based on “sales pairs,” comparing the price of the same house when it sells over time. It’s the best index we have. It eliminates all kinds of mix issues, including those you reference. But it has huge drawbacks, including that it lags about 3-4 months, and that it only covers 20 metros.

I cover the Case-Shiller index in my “Most Splendid Housing Bubbles in America” series. Next one coming on Oct 25. Here is the last one:

https://wolfstreet.com/2023/09/26/the-most-splendid-housing-bubbles-in-america-september-update-spring-bounce-fades-20-city-index-0-6-from-peak-in-2022-flat-year-over-year/

Howdy Folks. Have to brag on my 2 sons. Each purchased starter homes

( a home you can afford and needs work ) . They currently sit with 50 to 60 percent equity in todays market…. 3 % mortgages or less also. Still have all their fingers but got a little bloody at times… Don t be afraid of work folks.

Physical labor is good for the soul. I enjoy it, especially since I had an office job most of my life. I welcome getting out and sweating.

YEP, one is a CPA and loves getting his hands dirty the other way…

The greatest works of American fiction aren’t in bookstores.

Good luck to both…..

All hope is on hard working and sensible Americans. I have given up on Congress and Fed :)

Howdy Aman and thanks. Most of their friends and inlaws and both wives were against the idea. The wives now have beautiful homes and a small mortgage….

that looks like a double top to me. if that means anything.

meanwhile supply trend looks bullish.

i have no clue obviously but that’s how i see the charts.

Fed balance sheet only dropped by $20 billion this week. Pathetic.

You still don’t get it? The roll-offs are on automatic pilot based on what matures and on pass-through principal payments. Treasury securities roll off mid-month and end of month. By looking at just one week, you have no idea what the month will look like.

No, I get it. My frustration is that when the natural roll offs are this crappy, that they don’t sell any. I don’t like how the $90 billion cap is a one way ratchet.

The FED has us on a stretcher rack, Einhal, and they are slowly turning the screws while telling us they’re loosening them. QE like a tidal wave, QT like a drip.

The NAR, NAHB, and MBAs joint whiny letter to the uncle Powell begging for help shows how desperate they are. Hopefully, this forces many realtors into minimum wage jobs where most belong. Wal-Mart is still hiring greeters.

Howdy Fed up. Most RE agents were part time years ago.

Plus taxes & insurance. Maybe HOA. All expense qualifiers for mortgage approval. Plus car payments etc.

Sounds like some here need to go get their real estate license and have a go of it. Probably only a $10-$20k investment. Ongoing annual fees probably $8-$10k. Oh and by the way, you only get paid if transaction closes. Single listing expenses probably $2-$3k. Auto expenses. E & O insurance annual. Continuing education. 95% of all for sale by owners eventually hire a realtor. You all sound so smart but so bitter. Go get your own license. It’s so easy.

Realtors are incredibly overpaid and I have been endlessly disappointed with the value for money they provide. Your arrogance is typical of realtors. I don’t believe your 95% FSBO failure rate. I will FSBO and pay 2 or 3% for a high school grad Buyers agent to bring people to my house in their their very EXPENSIVE… car, toting huge brain from the RE CONTINUING EDUCATION, to sign some standard forms. I’m not bitter, I just see almost zero value in realtors. It is an industry overdue for Uberization or robots.

Realtors are typical sales people. Sales attracts people who want to make the most amount of money for the least amount of work. I’ve never met a sales person I considered to be smart and hardworking.

It’s strange to me how personal this stuff seems to get. If you don’t like realtors, don’t use them. They are just people doing a job.

ChS, easier said than done. You try to contact a seller’s realtor directly, and they’ll often ignore you. These filthy parasites protect their own.

Oh, I have an AZ RE license for the purpose of knowing my enemy. It’s inactive. Easiest test I’ve ever taken. Oh, and online CEUs cost me $52 for 24 units. That’s all you need in AZ every two years. The excessive fees come in when you join the disgusting NAR but nothing like you mentioned, so please exaggerate to someone who will buy your line of crap. And I have sold two of my own homes before I had a license. Nothing hard about it. Nope, not bitter but think your industry is a disgrace.

Gomp: there’s a lot of truth in what you said. My mom got ripped off by her realtor when she bought her first house when I was a teenager. She still paid off her 30 year morgage in about 15 years. The realtor I randomly found on FB Marketplace found us the house we currently live in, and she was amazing and talked the sellers down when prices were going up. There are some good ones, and there are some bad ones.

I deal with homeowners who price my work against unlicensed handymen and do-it-yourselfers as their “competitive bids.” I know what the work is worth, I happen to know how much it costs to run my business, and I have the freedom to politely walk away from tire-kickers. Don’t let the haters get you down.

There is a difference between your line of work and a realtor. Sounds like you fix things or build things. Realtors provide little value with many creating more problems than if you had transacted without them. The housing market would be much better off without them. Gomp is exaggerating the costs.

I think we need the Pow Pow’s pulling his hair out avatar pic modified with Lawrence Yun’s face instead….What a sack of S$$$….do they want some cheese with all that whine? I am still waiting for the letter from 2021 when the FED helped goose the market, where’s the whining then…oh it doesn’t work that way….

“The Federal Reserve simply cannot keep raising interest rates in light of softening inflation and weakening job gains,” whined NAR Chief Economist Lawrence Yun in the press release, because the NAR is a lobbying group for Realtors, and Realtors make commissions off every sale they handle, coming and going, and as sales volume plunges, their income plunges”

Howdy Phoenix. Pretty sure the NAR could continue cash RE sales when most businesses could not. They have quite a bit of power….

Nar part of the corrupt system of puppet purchasers

Wolf,

Here in my lil’ neck of the Seattle woods, we are seeing a strange phenomenon- spec builders touching the number from the top of the market, which you noted was in Jun’22. It’s now Oct’23 and that seems like a lifetime ago.

2.7 mil that was the bell.

ALL Four houses that have been rushed on the market, basically starter tract homes, are in and around this BIG number. None of them have big lots or great views or nice finishes.

Figure with the land permits and build out, these soon-to-broke spec builders / realtor/ investors could come down a MILLION or so on price…. And still nobody will buy these.

By the time they get around to pricing these houses right, mortgages might be at 10 percent. And there will be better homes back on the market, with better prices.

Already a nice house with a recent remodel is on the market for 1.5 mil and is just around the corner.

Spring is gonna be bloodbath

I think Mr. Yun is worried about lower for longer – lower NAR membership dues.

A few things to keep in mind:

1. There are several good papers that show people will continue to pay their mortgage even when underwater unless there is an adverse event like job loss.

2. Work from the Centre for Economic Policy Research (CEPR) on the individual-level foreclosure data from the NY Fed found that “investors were responsible for most of the growth in balances and virtually all of the rise in defaults for prime borrowers”. Additionally, “borrowing by individuals with low credit scores was virtually constant during this period” (01-06).

To me this says that we could easily see home prices continue to fall and homeowners with fixed rate mortgage will continue to make payments even if they go underwater. AND that investors could start to unload properties as prices fall causing inventory to go up.

So, if we don’t need subprime to create a housing bubble, and we don’t need subprime to generate foreclosures, and falling house prices don’t necessarily lead to foreclosure among owner-occupiers; then I can totally see a scenario where home prices come down (ideally to a level incomes can support at 6% mortgage rates) which causes investors to walk (good) and existing owners locked into low rate mortgages to go under water but not face foreclosure (not great but not horrible either).

A soft landing for me but not for thee.

“There are several good papers that show people will continue to pay their mortgage even when underwater unless there is an adverse event like job loss.”

This is me: I like my house and can afford my monthly payment/expenses. I don’t care what it is “worth” because to me it’s a roof over my head. I’ve put blood sweat and tears into this place and wouldn’t think of selling it.

It’s not people like you .

Think about peplek who have bought multiple homes .

I know people who have 5 homes or so and they think home prices can only go up.

This time around rich people holding many homes is a very common theme.

Some are even vacant and 67 percent of short term rentals were bought in last 3 years .

“I can totally see a scenario where home prices come down, which causes investors to walk, and existing owners locked into low rate mortgages to go under water but not face foreclosure”

And on top of that, investors walking brings more inventory to the market, which further helps affordability for new homebuyers stuck with higher rates.

This would be a positive outcome.

Then there’s the appraiser comin’ round to jack up your property tax and the insurance companies “catching up.” My guess is the tax bite will be sticky and lag well behind market value. A real bonanza for our local government betters. And won’t they want those taxes as downtowns slide into jingle mail!

Family member passed away and we just listed their house. We can’t sell it quick enough since it’s just a headache of bills we never asked for.

Sellers can spit in the face of buyers and stay on strike all they want. But fact is a lot of houses just need to get moved and get moved at whatever sellers can pay, they will.

Post some fliers at Starbucks and Petco

Petco is a good idea. People (like me) with too many cats pretty much need to own…

To save some people from posting…yup not in my neighborhood, LA county still going on, these graphs are all applicable to rest of the country/state except for mine…which in this case is SoCal…

Oh..and this time is definitely different..

Transactions seems like the only statistic that really shows the effect of higher interest rates. The other stats, incremental so far. Stalemate right now, sellers want 2021 prices, buyers can’t afford them. I would be on sellers breaking first, a bit surprised the numbers do not show much movement yet. Perhaps sellers do not want to get out of their existing mortgage either.

Most cash buyers are not stupid. Nobody wants to buy “high”, i.e., when it is clear home prices have to drop a lot more to make them interesting again, at least from an historical perspective.

I imagine a lot of Uber drivers nowadays are former realtors. I needed an in-home notary to come by the other day. She said she is also a realtor. I chuckled. At least she didn’t tell me “It is a good time to buy”.

The new part timer at my office day job is a realtor, but took the job because of the slowdown in sales.

My friend sold a home for 875k which has property tax and hoa and insurance of about $1.8k per month.

So 1.8k per month id even before mortgage payment.

The buyer bought it with all cash and rented it out for 4k per month .

Is he a smart buyer?

No, not at all. In your figure, he’s making $2,200 per month on his $875,000 investment. That’s a cap rate of about 3%.

Instead, he could have put the $875k in a 10 year instrument (CD/Treasury/etc.) making 5%, and he’d get $3,645 per month, and that’s not even including repairs, gap months, deadbeat tenants, or anything else that could easily eat into his $2,200 profit.

Thank you for replying first, but I was about to publicly commit a math faux pas, but I came up with a yield just under 3% (not including vacancy, management costs and sinking fund costs) vs. short term yields north of 5% and likely rising. That doesn’t even address the potential depreciation of his investment in a rising rate environment. What happens when the $4000/month tenants dry up?

The smart buyers bought 10 years ago and sold a year ago.

Not smart at all as Einhal mentioned, $2200 a month is generous, since he left out maint cost and also income tax from rental income. real cap rate is close to 2.5% or less.

All this at an opportunity cost, he can park that $875K in 30 yrs if he wants to go long and earn 5%+ with every 6 months interest payout, best part no state/local tax, not to mention if there’s a remote chance bond price go back up again way down the road and he can sell and capture profit that way as well.

So overall, not smart at all but then again your friend likely bought into the narrative of this house is a goldmine and I can just sit on double digital percentage gain in value every year while collecting rent..guess time will tell which method is better but keep in mind we’re not at a TINA type of environment.

900 k at 5 percent is 4000 a month they are getting about 2000 a month with lots of risk . I think that’s a horrible investment

The lower highs and lower lows in the Existing Home Sales (Actual) graph is comforting.

Look out below!

I noticed the condo sales here in the Swamp have taken a beating in the last 6 months. They are still selling but the prices have crashed. We are looking at 15% price drops YoY. This has to do with affordability issues. Most of the buyers are 1st time buyers, and condos are their entry into the housing market. The rise in mortgage rates are the primary culprit.

Condo prices also have to factor the HOA fee into their monthly payment. If the HOA is going up due to inflation, then prices will have to fall *even further* to maintin the same affordability (vs a prop w/ no HOA).

Just layers of inflation in modern times keeps clown world turning. The general consensus is ‘no thank you’ to a HOA but corporate-socialism-merica says that’s the only option available. Like a lot of what is taking place the consensus is somewhere else but the sheep just lie down and force their own children into it. Corporate and .gov developers inflating something as simple as housing in concert with themselves .gov, education system, real estate agents, HOA boards, etc. Basic needs, basic vision of the American dream being torched in broad daylight

For houses, maybe. For condos, no.

People complain about HOA fees, but those fees cover a lot of things people would otherwise have to pay for themselves.

You’re assuming the HOA is properly managing their (your) money, and will remain solvent / able to pay for future repairs.

I would rather not assume that, and instead manage my own repair fund.

Ask the people who lived in / owned condos in the Surfside building in FL how that HOA maintenance thing worked out.

That *exact* building was on my mind when typing my last reply.

MM, how are you going to do that on a condo, with common area and common walls and roofs?

El Katz, so you can name one example of a negligent HOA. Again, how do you plan on having people in a several hundred unit building apportion costs and repairs without an HOA?

Wolf, don’t you live in a condo? You never discuss your HOA, would be curious to hear about it sometime.

The national median price fell 4.7% from the peak 18 months ago. That’s nothing to be excited about considering home prices went up 40%.

The home builders association complaining about interest rates being too high wouldn’t have anything to complain about if they would just lower their prices. If the Fed were to lower the rates it would just fuel another buying frenzy and prices would go up even higher.

If builders would just lower their prices. Naïveté at its best.

Wolf:

Great article as usual.

You mentioned free money from 2008 to 2022. If I recall correctly, the FED is (or was?) also sitting on large amount of mortgage bonds and in the initial stages of the great recession, there were articles about banks sitting on houses that are on default (on mortgage payment) so as not to flood the housing market. Do you have any new information on this angle?

Also, you said, “Realtors could help fix this situation by exhorting sellers to bring their asking prices in line with 8% mortgages, which would help this market emerge from the deepfreeze.”. Well, I am sure they do (they will be happy with small reduction in the commission rather than no commission). So, a better suggestion would be, “Why can’t they reduce the total commission from 6% to 3%” to bring down the price overall? A house price and purchase decision are based on emotion and not related to what the realtor does (Yes, I sold my house in Cincinnati in June 2023 via word of mouth and two or three text messages and emails, based on openly available data on price around my neighborhood, taking into account what improvements I made or I did not and my carrying cost for moving to Tucson in April etc. I figured I shared part of the commission with the buyer and retained part with me).

Thank you.

“there were articles about banks sitting on houses that are on default”

This occurred in 2008-2012. Not now. Most homeowners that bought a couple of years ago or before can just sell the home, pay off the mortgage, and walk away with some cash — due to the price surge in recent years. Mortgage defaults now are minuscule.

“Why can’t they reduce the total commission from 6% to 3%” to bring down the price overall?”

That would be good just because it ends a monopolistic ripoff. But a 3% reduction is nothing. They need to start with a 20% reduction and go down from there to make 8% mortgages work.

Bullshit. The commission is not the problem. There is a commission built into every sale of everything on the planet. Either the seller earns the commission or the buyer earns the commission or the salesperson earns the commission. Everyone likes to blame the salesperson. Truth be told if all salespeople failed to make a sale tomorrow, the world would come to a screeching halt and everyone would be flung into orbit.

Lemme just take a wild ass’d guess, here…yer in sales?

In any event, I think you’re exactly & totally wrong. If all the seedy, louche, ever-angling salespeople on this poor planet fell into a giant pit of chainsaws tomorrow, the world would not only turn smoother on it’s axis mundi, but the audible spectrum would likely expand by several dBs, thanks to the absence of greedy little men & the din of their interminable BS, football analogies and self-congratulation.

Otto: “So how much do I get paid, twenty-five bucks a car?”

Bud: “Paid? You don’t get paid. Are you kidding, you work on commission, that’s better than getting paid.”

hahaha… this is funny…. guess realtor identified.

“Truth be told if all salespeople failed to make a sale tomorrow, the world would come to a screeching halt and everyone would be flung into orbit.”

A god complex often causes people to back away slowly.

Yes, how would we ever get along without those shiny personalities? The mind reels.

You call me naive, I call you a realtor, which is a worse thing to be.

Bulfinch

He’s a realtor. See earlier post above.

They built a 40 house development 2000-2006 in the neighborhood I grew up in and ending up sitting on half the houses there. It wasn’t just ‘owners’ under water as the narrative goes. Now more recently started another smaller 20 house development around 2010 on the opposite side of the house I grew up in and it will be a 15 year buildout for what should/was be 3-5 (2 without an extensive permit process) for 40 houses into the first ‘housing’ crisis. You can’t make it up. It’s so controlled and manipulated (there is no supply for a reason, like you just stated the banks got caught). And without the destruction of the most basic rules, rights, fiscal responsibility, war on production of anything with actual value none of this happens. They want bombs and pharmaceuticals manufactured here, the rest need not apply.

The 6% commission structure may change. There is a anti-trust lawsuit probe going on right now.

————————————-]

The moneymaking real estate-commission system where brokers pocket as much as 6% of a sale — and critics charge inflates home prices — could face a federal antitrust probe after a years-long investigation, people familiar with the matter told Bloomberg.

The reported scrutiny by the Justice Department comes amid two private class-action lawsuits that look to loosen the stranglehold the powerful National Association of Realtors has over the residential housing market.

The moneymaking real estate-commission system where brokers pocket as much as 6% of a sale — and critics charge inflates home prices — could face a federal antitrust probe after a years-long investigation, people familiar with the matter told Bloomberg.

The reported scrutiny by the Justice Department comes amid two private class-action lawsuits that look to loosen the stranglehold the powerful National Association of Realtors has over the residential housing market.

All the finger pointing is funny. Markets are buyers and sellers, nothing else.

The world is on fire, are you laughing? – the Buddha

If markets are only buyers and sellers, then why is the NAR whining about interest rates? I think market dynamics can be impacted by things other than buyers and sellers.

Two points

1. The Fed broke the real estate market with their errant policies. We would be better off if 30yr mortgages had stayed st 5% for the past 13 years. Who benefited by the gyrations snd pegging rates to all time lows? Ive got some names.

2. The giant increases in FL home insurance have blind sided many and will have a surprise effect and those prices. Imagine you live in a community in which half have skipped their home insurance. Then a storm hits. The people without insurance throw their keys in the mailbox and walk away. Now what is your property worth?

The whole piece is great, but this paragraph really made me smile:

“Obviously, Realtors and the NAR could boost sales volume by pressuring their clients to lower asking prices by a big chunk to bring them in line with 8% mortgage rates, and these lower prices would bring out the buyers, and that would help getting the market out of the deep-freeze, but no. It’s much better to whine to the Fed about handing out more heroin.”

*applause*

Actually, I’m pretty sure the realtors do say that. Because they’re in a volume business. If their clients reduce their price by 10% and thereby sell their home say 2 weeks faster, the realtor is only down 0.3% and on balance, they come ahead if they can flip the home faster and move on to the next one.

Freakonomics had a really interesting chapter where they compared the price at which realtors sell *their own* home vs. the local average representing what realtors sell other people’s homes at. And it turns out realtors consistently sold their own homes at higher prices than their clients. The reason? Again, on a $500k home, if the owner keeps the house on the market for another month and gets a 10% higher price, they make $50k which is not bad compensation for waiting a month. OTOH, the realtor only makes an extra $1k, which is not worth the extra work of showing the house for another month.

So the truth is, realtors push their clients into bad deals all the time (convince sellers to accept lower offers, and convince buyers to make higher offers) because they’re not served with working an extra month for a slight bump in their gross compensation.

Yeah I was going to quote the same. The funny thing is, most people who aren’t realtors hate realtors because they feel conned into getting into a pricier home than they intended or whatever when they were buyers. However, when people become sellers and invite realtors to sell their home who will they choose? They almost always pick the realtor that promises they can sell for the highest price, then when it doesn’t happen the realtor has to convince the seller to try dropping the price a little (not 20% lol), at which point the seller either tries dropping the price or gives up and takes the property off the market then tries again with another agent. So realtors who are honest and realistic likely don’t get the business. On the sell side I’d argue it’s the owners who are the bottleneck, because an agent would probably much prefer to make a few sales quickly at a lower price and commission than wait forever to make 1 sale even if their take is higher on it. RE is going to take a long time to reset, people won’t sell unless they really have to, and when a lot of people “have to” sell we will already be in a recession, whenever the hell that comes.

Very astute Seba. Realtors don’t set market price. The market does. A ready, willing and able buyer and a ready, willing and able Seller. Period.

Alright I was sort of with you until this one Gomp. It’s not exactly fair to lump housing in with every day to day transaction. McKinsey really helped shove opioids down rural America’s throat and I’m not going to act for a second like they were just encouraging buyers to meet sellers lol. Housing is a highly regulated industry under huge government influence and anyone playing in that sandbox knows exactly who they are taking advantage of and how. If it wasn’t a racket the fee wouldn’t always be 6%, it too would be subject to the market forces you mention.

Gomp,

You’re not paying attention. Sales have collapsed! They have collapsed because sellers won’t lower their prices to make sense with current mortgage rates. So buyers have vanished. As I pointed out in the article — so RTGDFA — , the NAR is complaining to the Fed about those interest rates, instead of talking sense into their clients (sellers) about pricing. Eventually they figure it out.

Yes this is simply about the market clearing.

Liquidity is low, spreads are wide.

The market will clear when either sellers *need* to sell or buyers *need* to buy.

At some point sellers or buyers will capitulate.

Most paths lead to sellers capitulating as real growth means higher for longer, whereas a recession means job losses. Only a mild recession with an unexpected pivot is bullish for housing.

I don’t hate realtors but looking at the qualification to get realtor license and the money they make at least in so cal is outrageous.

Most of the realtors I met are not really smart.

A simple home in so cal is 1 million dollar, realtors commison is $60K.

Say in another cheaper location, a home sells for $300K, the commission is $18K.

It’d take more or less same effort to complete the transaction in both the location, so why this discrepancy.

Real estate may take some time to reset but reset it’d be. what we have is not sustainable.

People are still forced to sell for multitude of reasons and real estate prices are set at the margins like all assets.

Either the rates go down, or price down.

I guess we need more gritty information to know what is really happening, Like:

What % of homes are with speculators including the realtors.

What % of homes owned by AirBnB and other corporations.

What % of homes technically owned by FED and the banks (mortgage under water or unpaid).

What % are foreigners parking their hard earned or ll-gotten wealth here.

I am sure all these would be different from city to city.

I notice in Tucson listings, many houses getting marked as Pending or Closing (whatever fancy terminology they uses) and few days or weeks later they reappear (the buyer wanted a garage!). I will notice many listings saying Owner/Agent. The same phenomena for rentals.

I guess they are playing a game here to reset the number of days the house has been on the market. But I notice the some buyers are also naive. Can’t they look at the historical price (now that they are easily available) and see that prices have doubled in the last 3 or 4 years and this is a sleepy town and is not booming with new industries. Few I notice trying to sell at a loss after buying at the top a year ago.

“What % of homes technically owned by FED and the banks…”

The Fed doesn’t own any homes, not even indirectly, because the MBS it holds are guaranteed by the government, and if a mortgage fails, it’s up the to government entity to deal with the home and the mortgage, and it just pays off the MBS holders, including the Fed.

The Fed is now rolling off about 200B per year off their balance sheet. At this pace it will take them 12 years to liquidate the 2.5T of MBS that they should have never held, by law. In reality, it’ll probably start going back up when the wheels fall off the ‘economy’ or ‘financial system’, in a year or two. How do people feel about housing market being stealth nationalized? 🤔

In terms of the 12 years…

1. If the Fed ever cuts interest rates, the roll-off of MBS will become a HUGE torrent because there will be a tsunami of refis, which means mortgage payoffs, and the principal is passed through to MBS holders. And those MBS will vanish.

Back during the pandemic when interest rates dropped, and refis exploded, the roll-offs were in excess of $100 billion a month. And the Fed had to buy a HUGE amount in MBS to replace them, and to add to its balance sheet.

2. The ongoing mortgage payoffs cause the pool of mortgages backing the MBS to shrink to such a point that it’s not worth maintaining the MBS. The issuer (such as Fannie Mae) will then call the MBS, meaning pay holders for it and withdraw it, and repackage the remaining mortgages into new MBS and sell the new MBS.

This is why 30-year MBS never live to be 30. They keep shrinking, and after some years, they’re called – sooner during a refi boom, and later when there are fewer refis.

So don’t worry, those MBS will come off quickly if mortgage rates drop even a little.

Considering the over 7% mortgage rates at that time, these prices are extremely exorbitant. But people around me are still buying. Their common motto is “I will refinance when the rates get lower”. I am not sure this idea is fueled by the realtors or not. This may be one of the reasons why prices are still ridiculous squared. The other is the rounds of reckless and extravagant rounds of money printing (the last one in March 2023) by the irresponsible FED.

The vast majority don’t understand how prices are set.

Ask someone to explain what might happen to house prices if interest rates rise, and why.

They won’t have a clue. For them it’s about how much the house next door sold for and this one has a nicer kitchen. Plus their whole lives prices always went up, so the more you buy for the more it will go up nominal.

I love your graphs, but why are they not always zero based on the x axis? Makes the movement sometimes look more dramatic than reality, if it is not zero based.

Why does a 10-year S&P 500 chart not start at 0? Why does a 10-year GDP chart not start at 0? Why do people make stupid suggestions?

I much prefer straight numbers. How about starting at 11? And can you change the lines to blue? That would make the data more relevant. ;-)

“Why don’t you just make 10 louder?”

“Why do the charts not go back to 1776?”

When you’ve had an eleven for years, and then you get a twelve, it’s hard to go back to just an eleven.

You see, the eleven, a 2010 Campagnolo Super-Record, has an 11-25. But the twelve, a 2020 SRAM Red Etap, has a 10-25. So, the eleven only has an eleven, but the twelve has a ten.

And yes, ten is bigger than eleven.

I feel another commenting guideline coming soon….

“Don’t ask for a zero start point on the charts. If you ask for a log scale you will be permanently banned”.

The Federal and State governments still give too much real estate stimulus. What kind of insanity allows a tax deduction for second home mortgage interest? We have tax coffers that need to be filled with an economy flush with an obscene excess of private equity liquidity. California has made a good start in limiting mortgage interest deductions, but the second home is still there, in a state that has a hard time zoning a first home. These treasuries need money desperately; it is amazing that real estate lobbyists could outweigh defense money to essentially maintain our empire, that doesn’t even collect money in the historically successful method of tribute from vassal states.

Not surprising given that the people passing the laws often are the ones that own a 2nd house or more.

Well it is capped at $750k. So one home or two homes. You can only deduct up to 750k.

And it isn’t as much as you think.

Standard deduction $13850 standard deduction and $27,700 for married FJ.

I buy a $750,000 home @8% internet. The first year Is like $60,000 in interest paid.

So I do not take the standard deduction, I use itemized.

Say my income is $99,000.

$99,000

-60,000

$39,000 is my adjusted gross income

Now I’m taxed say as a single.

So the first 10,275 is 10% =$ 1027.50

Next 28,725 is taxes at 12% = $ 3447.00

Taxes are $4,474.50

What I did save was the other

60k minus the standard deduction being taxed or

60k -13850 = 46,150.

So we run that thru the tax brackets and realize we’re saving $10,153 in fed taxes by paying out 60k to a bank.

So pay out 60k, get 10k back.

It’s not that great.

Just one correction, it’s not a $750k home. It’s $750k in a mortgage. So if you put 20% down, it’s a $937.5k home.

You’re also not accounting for the fact that you also can deduct $10k in property taxes and/or state income taxes.

That’s huge and more importantly it incentivizes being a landlord, which crowds more people in, which drives capital gains up.

Canada is such a mess.

Gary, the “tribute” you seek is transferred directly to US consumers in the form of cheap manufactures, cheaper labor and cheapest of all commodities. All without the nuisance of actually governing the periphery, since comprador elites do it on your behalf. You’re welcome …

Wolf, something missing from the article is the fact that new home builders are buying down the mortgage rates, in essence hiding the fact that they sold the home for a lot less than the loan amount.

This is NOT about new homes, but about USED homes. There are NO mortgage rate buydowns on used homes. One topic per article.

New homes are treated here, including mortgage rate buydowns.

https://wolfstreet.com/2023/09/10/mortgage-rate-buydowns-by-homebuilders-are-now-all-the-rage-to-prop-up-sales-lowering-effective-house-prices-in-a-big-way-but-dont-get-picked-up-by-house-price-data/

https://wolfstreet.com/2023/09/26/prices-of-new-houses-drop-sales-drop-inventory-supply-jump/

There are mortgage rate buydowns or seller-bought points for used homes, they’re just not as common as for new

Ah thanks for the clarification.

LA:

“in essence hiding the fact that they sold the home for a lot less than the loan amount.”

In some ways that’s correct, but I would make a small wager that the mortgage rate buydown is placed against the marketing budget more so than “hiding” anything from the transaction price. The basis for this is that is where auto manufacturers place the expense of the reduced financing rates offered to new car customers.

Aren’t realty companies abandoning NAR like a sinking ship?

Oh and now it looks like the DOJ is going after them.

While both buyers and sellers appear to be on strike, the capitulation seems to be primarily buyers. A 4% decline in price is nothing compared to the > 2x rise in interest rates.

While there are non-economic reasons that force people to sell (job loss, divorce, etc), there are also non-economic reasons that force people to buy (getting married, having a baby, needing to move to a good school district, etc). In a crappy economy, forces like job loss are greater and so more sellers capitulate than buyers. But in a good economy like our current one, fewer sellers are forced to sell, while more buyers are willing to capitulate and pay whatever is needed (if your kids start school in August then like it or not, you’re getting a house in a good district by then, whatever the price).

IMHO, we won’t see drastic price drops unless we go into a recession (and the Fed is aiming for a mild recession), when sell-side pressure starts to increase.

Agree Lune. Except sometimes Seller has to sell. Buyers can usually rent if need be. Unemployment picture will dictate some or a lot of future.

Depends on the wife. My wife is more demanding on particulars of housing than any other single factor. Non-negotiable.

My wife had the same attitude, until I told her any sacrifices in the housing arena will go to the kids education and travel.

I’ve owned a castle with all the fancy furniture, chef kitchen, etc. I found it to be a superficial unrewarding existence. The real friends aren’t impressed. Nowadays, I’d rather spend my time outdoors or at friendly unpretentious gatherings without need for “show”.

Buyers always have the option of waiting and renting out for some time but sellers may not have this luxury.

I don’t believe in forced buyer theory.

Really tired of this bs… “buyers are willing to capitulate and pay whatever is needed”. I keep hearing this nonsense. Do you have no understanding of the loan qualification process? That vast majority of buyers borrow money to make a purchase. The amount they can borrow is limited by their income, interest rates, etc. They cannot “pay whatever is needed”. I feel like I’m explaining this to a child.

Also, there’s no such thing as forced buying. Any of the needs stated (getting married, having a baby, needing to move to a good school district, etc) can be fulfilled by renting.

There are motivated buyers and sellers right now, but as mortgage rates increase, the number of sellers increases and the number of buyers decreases.

For a seller, the idea of cashing out at the top and putting the proceeds into safe fixed income instruments earning 5-7% is getting very attractive. You essentially ride two wonderful waves. First, you benefit from outsized home price appreciation. Next, you benefit from the spike in interest rates and avoid any RE price crash.

A lot of m0r0ns were indoctrinated into hooms only go up mentality after 15 years of ZIRP and QEnfinity. Same with stonks. Hard to break old habits, and who can blame them? It’s the fault of our captured, unfit government.

Aren’t most mortgages swapped at the 10 year mark?

People refi, sell, do a heloc or start a magnum PI reverse mortgage.

Double rates are not the end of the world in a 40-50 year career. They do suck, for a bit.

” . . .down by 4.7% from the peak 18 months ago, in June 2022

. . . the median price was up year-over-year by 2.8%, but that was a lower rate than the 3.2% year-over-year in August”

I trimmed off the fat. So all of that is to say, it’s been a BIG FAT NOTHING BURGER.

Who for goodness sake would have thought that housing would have held up like it has as 30YFRM raced past 7% and are now at 8%?

NOBODY! That’s who. Go dig into the bowels of mortgage applications and tell us what % of the mortgages from the last 15 months have been 30YFR vs adjustable in some manner?

Anyone who’s bought a house out of FOMO over the last 12 months is just utterly crazy.

In Canada 20% of mortgages are *increasing* in length because the borrower cannot even pay the interest.

Heating bills are far higher in winter in Canada, the Canadian yield curve suggests a big recession.

USA borrowers are protected by 30 year mortgages. Not so in Aus/Can/uk. One or more of these countries will fall first, this time the crisis will start outside the USA. USA bonds up, USD up, CAD,GBP,AUD down.

Sounds like we need higher interest rates and let’s bring back 12% mortgages.

That was my question about what % have take out 30YFR over the last 18 months. From talking to friends in real estate, almost no one over the last 12 months has been taking out FRM. Most people have been doing so form of ARMs. So granted it’s not a huge % of mortgages, but these will become stressed if rates stay higher for longer like they should.

Our problem in the US is that our Fed & politicians are gone hog wild on MMT-based means for managing our economy, without the tax increases of course.

But, THEY WILL scream to high heavens to bring back rent & mortgage relief when the time comes.

I firmly believe that the US has entered into a very extended period (i.e., since ~ 2012) that the people running the show aren’t going to allow the US to have anything close to the level of foreclosures that we say from 2008 – 2012.

It’s just not going to happen.

From Betterdwelling:

OCTOBER 19, 2023

The future of Canadian real estate is starting to dim as one of the country’s most ambitious projects experiences a hiccup. Lenders just foreclosed on The One, a Toronto development once sold as Canada’s tallest residential tower. Lenders moved in after a default on a massive $1.35 billion loan. Yes, billion—with a B, and that’s not even the total outstanding credit on the project.

The One Is Supposed To Be Canada’s Tallest Residential Skyscraper

The One isn’t just a large project, it was supposed to be the Crown Jewel of Toronto real estate. Marketed as Canada’s tallest residential tower, the 85 story skyscraper is currently under construction at 1 Bloor Street West. The tallest residential building, in the most expensive district, in one of the most expensive cities in the world. Impressive plan, but it’s hitting quite a few roadblocks.

The One Defaulted On Over $1.35 Billion In Loans

The project entered receivership today, after defaulting on a $1.24 billion loan held by a subsidiary of the South Korea-based KEB Hana Bank. Alvarez & Marsal Canada have been appointed the receiver, with total outstanding liabilities estimated at a whopping $1.66 billion.

You don’t want to be a supplier or contractor on this baby. You will be way down the line up. Unless refi by someone, this may take out some big outfits in the trades. Wouldn’t surprise me if To or Ontario gov gets involved. But you can’t turn it into social housing!

PS: a lot of units ‘sold’…so what happens to deposits?

Maybe they will be paid back with unused construction materials like bricks and floor tiles. LOL!

Could these dynamics of the housing market effect the churn in the labor market? I have seen you indicate that the layoff news that never really materialized may have helped scare people into not changing jobs, but could this also be a contributor? I would need an awfully big incentive at a new job in order to change jobs if I had to sell my 3% mortgage home and re-purchase at 7-8%, which would limit my search for a better job geographically, but maybe most folks have plenty of options within driving distance of their existing home….