There will be a recession someday, there always is one eventually. But not yet.

By Wolf Richter for WOLF STREET.

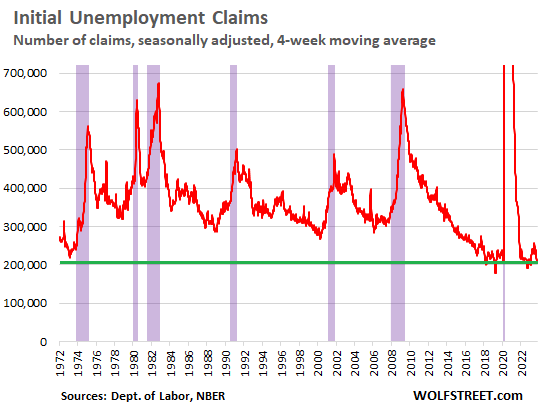

Our recession-watch here started shortly after the Fed kicked off its rate hikes in March 2022. The National Bureau of Economic Research (NBER), which calls out recessions, defines them as broad economic downturns that include downturns in the labor market. So, among other things, we’re looking for sharp increases in weekly claims for unemployment insurance benefits, our most immediate measure of the labor market; they’re highly correlated with recessions as defined by the NBER.

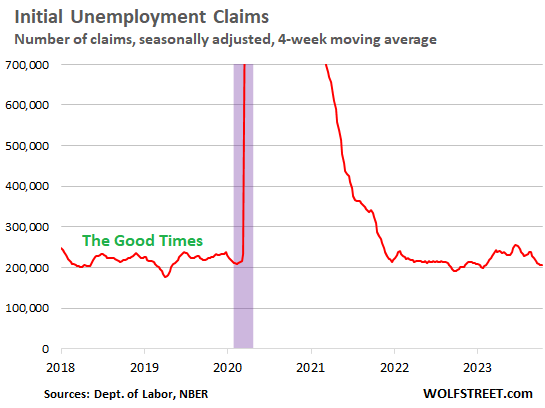

Initial unemployment insurance claims backtracked further. Initial claims for state unemployment insurance benefits by people who’ve lost their jobs have been declining since the end of June and for the reporting week fell to 198,000, according to the Labor Department today. This was the lowest since January 2023, and very near the historic lows.

The four-week moving average, which irons out the week-to-week ups and downs, fell to 205,750 initial claims, the lowest since the beginning of February.

The long-term view shows just how low this four-week moving average of 205,750 initial claims is: It has been seen over the past 50 years only in the two years just before the pandemic and in the hot labor market coming out of the pandemic. Note how unemployment claims surged shortly before recessions began (recessions indicated in purple):

- December 2007, the official beginning of the recession, initial claims pierced 340,000.

- March 2001, the official beginning of the recession, initial claims pierced 380,000.

- At the beginning of the three recessions in the 1980s and 1990s, initial claims pierced 400,000.

Unemployment claims had risen from September 2022 into early 2023, making us somewhat nervous. But then in the spring, they backtracked and fell again. And now, as we approach the end of the year, they’re telling us that there’s still no recession in sight.

My favorite recession indicator.

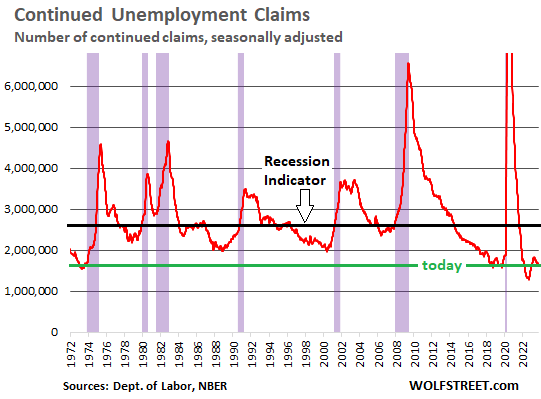

The number of people who are still claiming unemployment insurance at least one week after the initial application – people who haven’t found a job yet – started rising from historic lows in late 2022 through March 2023, but remained low, and we thought, OK, if this keeps going…. But then they backtracked substantially.

Over the last three weeks, they ticked up a little, in the latest reporting week to 1.73 million, which is still very low.

The initial claims in the charts above mean that fewer people are losing their jobs; and the continued claims in the chart below mean that those that do lose their jobs and receive unemployment benefits, find new jobs quickly and don’t remain on the unemployment rolls for long.

Recessions from the Great Recession back through the early 1980s began when continued claims for unemployment insurance spiked through about the 2.6-million mark (black line), which makes it a recession indicator. Today’s level of 1.73 million is far below recessionary levels, pointing instead at a labor market that is still tighter than in the prior 50 years.

There will be a recession someday for sure. There always eventually is a recession. But when? Not yet. Other labor market data, which lag unemployment claims data a little, gave us similar indications, and I’ve discussed them most recently here, here, and here.

What this labor market is telling us recession watchers here is that there is still no recession in sight, and we’ll just have to keep watching for it.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Of course there’s no recession. How could you have a recession during the biggest economic everything bubble in history? Nobody did the math on the money-printing/fiscal stimulus from the FED and .gov. They overdid it by like 3x. All that fake money has legs.

Yes, and we’re finding out little by little just how long those legs are.

Certainly agree. I think the exorbitant of asset prices will last some time (maybe years to come) thanks to the multiple rounds of gargantuan money printing by the FED. The good side is there is no recession. The bad side is the continuously widening gap of inequality.

*asset prices will last some time (maybe years to come.*

Is that what the wolf really said?

No recession is not a good side if a large percentage of people are priced out of the essentials.

The bad side is inflation will continue to ravage us. Funny how the market is up nicely today after Powell talk. The market will make any excuse to rally

Arya Stark,

Talking about the market while the market is still open gets everyone tripped up these days. S&P 500 took a while to grasp what Powell was saying, then came to its senses, and closed down 36 points, or -0.85%.

Einhal,

Agree to some point – if the G triggers pretty bad inflation (or potentially, “silent inflation” 2004-2020 by appropriating what would have otherwise been a China export-led price *deflation*…) that has macro consequences that are at least roughly on par with recession-related unemployment (especially if the jobs “saved” by G created inflation are G-makework, bridge/war-to-nowhere type jobs).

Inequality only matters if you’re on the wrong side of the equation!

Id est, you and I gentle readers.

Long legs and short on finding people to do work.

Can’t seem to find people to do the work we need to have done.

Hike pay.

(It would really help if we knew the kind of jobs you are looking to fill and what your pay levels are like…but hiking pay tends to fix most problems like this…as Econ 101 suggests it might).

Help! I’m turning TRANSACTIONAL!!!!!!

Tax brackets 2023 (taxes due 2024)

Tax Rate Single Married filing jointly

12% $11,001 to $44,725. $22,001 to $89,450.

22% $44,726 to $95,375. $89,451 to $190,750.

24% $95,376 to $182,100. $190,751 to $364,200.

32% $182,101 to $231,250. $364,201 to $462,500.

Yeah, I know there are two more but they only ad 5%

Wish I could get estate tax (I mean death tax), but the bigger dynasties and ability to afford get into all the hide money tricks were built on this one and similar since 1980 tax cut and union smash……that’s over 40 years of ” completely “UNILATERAL TRANSACTION”……Econ 101?

Forgot the ever increasing FRACTIONAL BANKING…..EG, MONEY PRINTING.

That was the “atmosphere” of this “transaction”.

And of course Corp and Lobbying power.

Some folks refer to both as “corruption”, yet another gas in the atmosphere.

Evidently was good environment for transactionalus americanus.

But it has a death wish and doesn’t know it…..so that’s all kinda my “recession indicator”, being ECON ignorant.

But this reverence here for Econ 101 here is silly, as I have said before, as it is just “bonehead college Econ”…..transactional, like 44 said 45 was (a clever insult, blew right past him, he may have even been proud of it, his followers sure are…..as in he mastered it……like underwater basketweaving? It is probably MUCH harder….think….if you have the education and experience for it.

SO…..Econ 1A-1B PREREQUISITES…… Calculus 1A-!B completed or in progress, puts you in classes to start learning econ with the BIG boys…..or just want to be brought uo to 1700s level concepts

That’s 1700s level mathematical skills, to clarify, like bond duration and convexity.

And think about it, underwater basket weaving would be damned complicated….who knows what the physics/math/machine tech spin-of might be? Not to mention better baskets….a lot of third world people still use them, and environmentally, it beats fossil fuel guzzling plastics.

Like I consider having a swimming pool or playing golf MUCH more of a planetary and intellectual insult than the above human actions….and I am obviously correct.

If we keep running the kinds of deficits we’re running right now, a REAL recession may never arrive. The only part of housing that’s really at risk are the people who’ve bought in the last 18 months. Everyone else is golden.

As you well know, residential construction always leads us into a recession. 6, 7, 8% rates as of yet have not created a broad significant decline in both existing & new homes across the US. Until housing really start to deteriorate, then your favorite metric will not pop meaningfully above 250K and stay there.

These may be some world record, long legs. Time unfolding SLOWLY will tell.

Real estate construction did not lead in the 1991 or 2001 recessions.

I don’t really see the value in spending $650k on a new build 50 minutes out from the city. My guess is remodeling will pick up the slack, but as a remodeler, maybe I’m biased.

Wolf, could you chime in on this: as a proportion of total residential construction spending, what percentage is residential remodeling? I remember seeing a chart of yours many months ago seeing remodeling as basically a rounding error compared to the money in new construction. I just find that hard to believe. All the roofing, windows, kitchens, baths, and siding have got to be enormous money. Is the bulk of it really getting spent on new construction?

I don’t have the data at my fingertips. But I would say, based on memory, that remodeling is more than a “rounding error” but it’s pretty small compared to new construction, which is such a huge number.

Then my theory that the remodeling industry can absorb the laid off workers from new construction (once it starts, who knows when that is) is toast.

Either way, I’m grateful for the work and the resilience of the economy. I can’t believe all the people hoping for a recession. Don’t those guys have jobs? Kids? Grandkids?

Construction is really not a major employeer, 10.8m of US work force of ~168m, or 6.5%. Not a rounding error, but much smaller than most people assume.

Builders are out ahead of it. They know what’s coming and are offering all kinds of incentives to move inventory. Thst’s the beginning.

W. Harding,

RE was probably already on the “financial masters of the universe” schedule of economy sectors to milk/trash pre 2000…..only took them a couple years to set up the grift before they struck all the marks hard, and cleared out with the loot.

This stuff is just too easy now……it’s “legal”.

Think that one was called the GFC.

CRE is a pending disaster, as are the hundreds of billions in BBB-rated bonds issued that have to refi. All the Airbnb wannabe millionaires who bought 3 when rates were 3% are choking on an 8.5% bone and will be underwater soon. So much for the housing shortage. Office space is also a disaster everywhere with WFH and rising rates. Don’t forget the Trillion or two in HYM/AFS bonds held by underwater banks. I’m surprised that somebody hasn’t started runs by tweeting and moving money out. Citi has 85% uninsured deposits, but I forget. They’re too big to jail.

What? No purple bar on the graph for 2020? LOL!

NAR sent letter to Fed asking it to stop raising rates amd start cutting them. Their reason: they want to help the “little guy” by making housing more affordable.

The truth is that NAR narrative of higher housing prices is causing unaffordability. NAR leadership now consists of big REIT investors, REIT managers, Wall Street RE funds and other Real Estate investors that hold multiple houses. So, the NAR leadership doesn’t earn from commissions, but from appreciation of their assets. So as the mortgage rates rises to 8%, NAR leadership spreads misinformation to protect their leveraged bets.

This result is lower house sales (now 50% lower in Northwest) and lower commissions for real estate agents. So this year bankruptcies in Real Estate sector has exploded to highes in 10 years, and is leading all other sectors in bankruptcy filings.

So NAR is bankrupting and screwing the 2 million smaller real estate agents and other professionals (Appraisers, Inspectors etc). Before thousands of these professionals go bankrupt, they must fight. Best is to refuse sellers and builders who want to list properties at unreasonable prices from when mortgage rate was only 4%.

Already in Seattle area, 80% of the listings above $1.5 million have stopped selling causing agents to lose time and money. These houses either keep sitting in market or get pulled. The only properties that are selling in this range are the ones from motivated sellers. E.g. Recently owner of a good house passed away and the trust put the luxury maydenbauer house on sale at reasonable price of $2.1 million for a house that sold new for $1.7 million in 2017. This house sold for close to $2 million. There are many other houses on market in area that were worth $1.2 million in 2017, missing the luxury features, and are asking for $2.5 million now with no chances of selling.

So the NAR narrative around locked-in low rates is BS. Life does happen (marriage, divorce, retirement, layoffs, passing away) and these house sales will determine sale price and value going forward. NAR should change narrative to protect RE professionals by educating sellers that mortgage rate rise has both stretched and disinterested buyers, so to sell they need to drop listing prices significantly below the stupid Zestimates, and just below the value assessed for property tax.

Sellers can eat sh!t if they still want 2021 prices when rates were under 3%. The person who bought my house in 2022 listed it for $665K and cut it to $535K before it finally sold.

Poor Leo. Trying desperately to figure out how so sell out all the other lower/mid level Realtors and save his own ass.

Thanks for telling us how YOU would like the musical chairs and circling patterns organized.

The music is getting faint and lacks a predictable melody.

Retail, especially ecommerce, has been a juggernaut for a while, but I think I’m seeing a weird sign that something might be shifting. Maybe the trouble you long for is now on the horizon, DC.

My employer’s next door neighbor is the biggest Amazon fulfillment center in the state of New Mexico. In the last few weeks we’ve seen a flood of new applicants for unskilled positions that were laid off from Amazon. Now I’m suddenly seeing maintenance and controls technicians apply here. Amazon wouldn’t lay those guys off if they’re still running their equipment hard. And all of this as we enter the holiday season when one would think they’d be hiring or at least holding steady, not laying off.

Only one anecdotal data point, but it’s a report right from the trenches on the front lines of the economic flare up. It’s certainly catching my attention.

Nonsense. Amazon is NOT laying off warehouse people. They’re hiring. For the holiday season, they’re trying to hire 250,000 people, far more than in prior years, and they’re raising pay and incentives in order to be able to hire these people in a tight market. Amazon’s retail sales are rocking and rolling.

Amazon is definitely seeing a slowdown in retail sales.

One month ago, I was being told that Amazon’s data analysts were forecasting an increase in sales through the end of this year and it did not happen.

Now, Amazon is reducing driver’s hours down to 9 hour shifts for the next few weeks as a reward for our past efforts and in preparation for the upcoming holiday rush. 4 tens is the how it normally works. Amazon doesn’t reward employees for anything. Amazon can’t dump drivers heading into the holiday

season, as sales could suddenly pick up.

I am also being assigned a new route from an entirely different fulfillment center as Amazon begins their consolidation. I laughed as my DSP explained it all, to us minion’s.

Retail is done!

“Retail is done!”

🤣

If you extrapolate from your own little situation and twisted observations to the rest of the USA, or even to a giant like Amazon, you’re likely totally wrong. This stuff is just funny.

That’s why I rely on data.

Ecommerce sales through September:

Isn’t this the time of year the fleets of RVs roll in?

Just a different type of “seasonal picker” migration.

Bet the locals hate the Bandido sewage tank dumping. (Jeff just loves counting “out of plan” computer observed/controlled bathroom breaks)

The other kind of seasonal pickers probably just do it on the finished part of the “picking floor”, and the bosses dump (the green units) on the “floor” at night and it improves the product next year. Coliform bacteria are spoiled and weak compared to their country cousins.

“Maybe the trouble you long for is now on the horizon, DC.”

Riiiiight. Hoping for an end to inflation is “longing for trouble.” You and your gaslighting can f*** off, weirdo.

Come on, I thought you were the adjective king here?

and a “gaslighter” and FOW is your best retort?

Hope you don’t want the “savior” quickly, I don’t think all the new and bigger jails have been built, although several southern states are currently spending billions on them as we comment.

Great article Wolf, this recession is still a long time coming.

Typo: ‘a recession indicators’

Best wishes from England

Thanks!

Howdy Folks. No one really knows how this will all end. ZIRP should never have happened at anytime in our history. Hopefully, it never returns. Another monumental mistake by the so called leaders…..

“Another monumental mistake by the so called leaders

When the G is the biggest debtor (by far) in the history of the planet, it ain’t a “mistake” that gutted-interest rates via money printing (a G monopoly) is the favored policy (under the new-and-improved moniker “quantitative easing).

You can’t have the world’s reserve currency without enormous debt — it’s basic accounting.

Your statement needs revision to reflect reality: There are many reserve currencies, the dollar is the dominant one with a share of 59%, the euro is #2 with a share of 20%, the yen is #3…

What is needed for a currency to become a reserve currency is that it’s big, freely convertible and traded, and the cleanest shirt in the hamper of dirty shirts so that it is trusted by market participants. That’s why the ruble cannot be a reserve currency because it’s not even toilet paper. Since early 2014, it has lost 73% of its value against the hated and doomed USD!

https://wolfstreet.com/2023/07/15/us-dollars-status-as-global-reserve-currency-on-slow-long-term-decline-but-not-going-down-in-a-straight-line/

Recessions are like earthquakes. One of those events that will definitely happen SOMEDAY.

But no one knows the most important piece of data – when?

Looking at the spiky up-slopes of previous recessions, it pretty much seems that layoffs are a panic-cascade/CYA-while-everybody’s-doing-it type phenomenon.

In all likelihood, long before the recessions, companies know they have a lot of deadwood/baloney revenue/etc. but keep hoping there is a pony buried under all that sh*t…until they don’t.

CEO/CFO departures might be a decent leading indicator. New CEOs/CFOs like to take “big baths” you can (with honesty) blame on the last simp.

“CEO/CFO departures might be a decent leading indicator.”

They’re a leading indicator of internal company problems, not a recession. In fact, they’re not even a leading indicator of internal company problems, but a hugely lagging indicator. By the time they’re forced out to spend more time with their family, it’s way too late.

Wolf,

I get your point, but I do wonder if new CEOs/CFOs take advantage of “it was the last guy’s fault” excuse (only available for a ltd time following the transition) to start airing companies’ dirty laundry (unsustainable revenue games, temporarily obscured expenses, etc).

And to the extent that the real layoff spikes are a fast accelerating phenomenon (looking at those upward slopes) based upon “cascade panic” (“OMG!!! FASBie is a lie!!! Everything is a lie!! Liquidate everything!!) then maybe a wave/wavelet of CEO/CFO firings/retirements might be a early warning system of sorts.

Because it suggests an upcoming wave/wavelet of big baths.

Which then precipitate the long-gestating panic (“We all knew the economy was BS but “you gotta dance while the music is playing/ride the broken-down horse til he dies.” Then it’s “Fire!! Fire!! Everybody head for that one exit!” – because a lotta people long suspected the economy to be a ZIRP inflated bladder of hot air).

Don’t know for sure – there is probably an academic study on “CFO transitions/big bath accounting disclosures/recessions” buried somewhere…

In my local newspaper’s Monday’s business section there’s a report on local companies’ insider trades. There is a slight time lag, but they’re pretty current. This may not indicate a company’s health as much as what the top executives think of the share price, but I find them to be fairly predictive of where the company is heading.

One of the data points given with these is the trader of note’s current stock ownership. If a trade represents a small fraction of of current ownership, it is not a big deal, to me anyway. And I certainly understand it when very profitable stock options are exercised and cashed out of. But when a top exec sells a large portion of what they have, it’s usually a warning sign.

My portfolio is diversified and on the conservative side, but I am definitely over-weighted with local companies. Since I live in the Twin Cities, it feels easier to keep my finger on the pulse of what’s happening close by.

One company I recently walked away from was Best Buy, and that was fortuitous. When news broke that they had an internal policy to hire and promote based on “Diversity, Equity & Inclusion” rather than merit and qualification and performance, there’s no way I could own it. If there’s Karma out there, Best Buy will suffer. A recession will hurt them too if we get one.

Best Buy just announced that they will stop selling hard copies of DVDs and Blu-ray DVDs after this upcoming Holiday season, but they will continue to sell music on vinyl.

Fortuitous was not the best word to use in my above comment. Profitable is a better one since the timing worked out nicely.

Clearfield, CLFD, is another local company that has been interesting to watch.

As a follow up to my reply, here’s one “Insider Trading” reported this morning on a local company that is in my portfolio:

UnitedHealth Group Inc.

Stephen J. Hemsley, Director

Exercised options: 121,515, Price $70.24-$108.97

Shares sold: 121,515, Price $540.58

Date: Oct. 17

Directly holds: 1,086,914

That is what I call, “Profitable stock options that are exercised and cashed out.” $53 million or so, give or take a few bucks.

The paradox here is low unemployment drives inflation due to more spenders in the economy. The FED has been recently vexxed by new jobs continually being added despite raising interest rates. They will have to continue raising rates to fight inflation until job losses balance their efforts. Layoffs are just getting started, and Nokia is laying off 14,000 announced today. It will be a typically devastating downturn as long as foreign investors continue to buy our debt. The FED has bet the farm on an adjustable rate mortgage on the debt, hoping they will. If not, the jig is up.

> The paradox here is low unemployment drives inflation due to more spenders in the economy.

This is true for demand-pull inflation caused by wages increasing for average people, but the inflation we’ve been dealing with is not. The pandemic stimulus was not primarily aimed at individuals, it was given to companies to continue playing wages sure, but an enormous percentage of PPP loans were fraudulent. The people who committed this fraud then used their massive amounts of money to scam wildly, this is why markets are so nuts. They speculated on homes with all cash offers, cars, everything.

Sure, you could fix this inflation by causing a 2008 style market crash, but that would also basically ensure Biden loses next year. So the fed is trying to hold rates high to deflate asset prices, hopefully without causing a marker crash.

However the thing I’m worried about is the CMBS market. Big landlords of commercial real estate are already walking away. The securities that back those loans are going to get destroyed and those investors are going to get left holding the bag, short of the government doing something huge.

Demand-Pull Inflation is a useless concept, unless you know where the major snatch blocks and pulleys are. And that’s just the OBVIOUS part of the flaws in the analogy.

We do have inflation, though, that much I have also learned.

(“Snatch blocks” has some dark humor to it, at least I think it does.)

Just wondering if there has been any change in eligibility requirements for unemployment following the various programs over the last couple of years. Is the data comparable to historical?

The changes in eligibility and the special programs during the pandemic have long expired.

If they had not expired, this data here would remove us even further from a recession, compared to historical data.

There are multiple old videos surfacing of Powell and other FED members expressing their frustrations in their failed efforts to “reach their 2% inflation target.” This “target” in and of itself is DIRECTLY in conflict with the FED’s stable prices mandate, yet it goes unquestioned as if it’s the gospel.

What is obvious for everybody but the most dull is that this inflation was intentional, and their goal is to let it run over 2% for some time, while slooooooooowly coming back to the 2%. They are attempting to inflate away the debt and set a new floor under all asset prices. Expect another “pause” next month as they regurgitate the same old nonsense ad nauseam.

Correct. The 2% goal means nothing if you don’t try to have a period of less than 2% or even deflation when you have years of overshoot. It’s clear that this arsehole isn’t concerned at all about the 20-25% he’s shaved off the dollar in the past 3 years.

I hope he gets a tumor.

He’s just following orders

Nice to know others here enjoy South Park. Might as well laugh as cry, as they say.

I second Depth Charge’s opinion. Fully agree on each sentence.

How can they inflate away the debt when it’s rising so rapidly and the cost of servicing it as well? These things make my head hurt….

“How can they inflate away the debt”

Issue a new currency like the Germans did in 1923. Give everyone $1 new dollar for $1,000 fiat dollars. Tell them they are patriotic for doing so. Remember the famous quote from you know who said to all the bondholders who were wiped out: “Thank you for your donations to the Fatherland”

Use an eagle on the bill rather than a dead president, make the colors red, white and blue and call them freedom bucks.

Howdy Depth Charge. The FED has lots of tools in its toolbox. A .25 raise is not really a pause and a pause instead of a .25 raise does nothing anyway.

HEE HEE

Inflating away the debt at 5% rates while still deficit spending nearly $2 trillion? The market is not that stupid. If they don’t get this under control, the long yield will be at 7% and that will eat up $1.5 trillion of the budget at the same time medicare spending is exploding.

How does the National Bureau of Economic Research (NBER) define a recession, and why are weekly claims for unemployment insurance benefits an important indicator for understanding economic developments?

1. “How does the National Bureau of Economic Research (NBER) define a recession,”

https://www.nber.org/research/business-cycle-dating

Quoted:

“The NBER’s definition emphasizes that a recession involves a significant decline in economic activity that is spread across the economy and lasts more than a few months. In our interpretation of this definition, we treat the three criteria—depth, diffusion, and duration—as somewhat interchangeable. That is, while each criterion needs to be met individually to some degree, extreme conditions revealed by one criterion may partially offset weaker indications from another. For example, in the case of the February 2020 peak in economic activity, the committee concluded that the subsequent drop in activity had been so great and so widely diffused throughout the economy that, even if it proved to be quite brief, the downturn should be classified as a recession.

“Because a recession must influence the economy broadly and not be confined to one sector, the committee emphasizes economy-wide measures of economic activity. The determination of the months of peaks and troughs is based on a range of monthly measures of aggregate real economic activity published by the federal statistical agencies. These include real personal income less transfers, nonfarm payroll employment, employment as measured by the household survey, real personal consumption expenditures, wholesale-retail sales adjusted for price changes, and industrial production. There is no fixed rule about what measures contribute information to the process or how they are weighted in our decisions. In recent decades, the two measures we have put the most weight on are real personal income less transfers and nonfarm payroll employment.”

2. “why are weekly claims for unemployment insurance benefits an important indicator for understanding economic developments?”

Since they’re weekly, they’re the most immediate measure of the labor market we have. They’re NOT survey-based, but based an actual claims filed for unemployment compensation. They are fairly raw and can be noisy, so they’re also presented as four-week moving averages.

Knowing/guessing based on experience, when the resolution of a statistic, media report, press release, important speaker, other inputs and one’s options are “NOISY” (or maybe even un-usable like “click-bait”), is critical for making sense out of of this world. I call it situational awareness and come here for a part of mine.

The very top layer of the human cortex is the noisiest. Hard to drag situational awareness out of it, even harder when little is first hand observation, but IT IS the human claim to fame (v. Oct 2023 USA)……(or curse). Extra hard to do in shared thinking, eg, with language, print only.

I read up briefly on NBER but as usual, lost interest.

Please normalize the unemployment # by labor force participation. Millions dropped out of the job market because of the free money, the asset bubbles, and all their Airbnb income. All of these turned out to be temporary and many of those folks will rejoin the labor market soon. Many also left due to COVID or trying to make a go of things overseas. Most of those people will be back in the next few years. The free money is nearly gone.

My #s are wrong.

They both assume 20% down.

So you ALSO have to put $64,000 more for a down payment as well as pay $3,300 more a month.

Lololol. You NY, NJ, Canadians are paying way too much for Florida.

Yes, that’s the issue. Too many idiots are moving from NY thinking “Well, my place was $2 million for 2,000 square feet in Scarsdale, so I’m getting a BAHGAIN down in Florida!”

I dunno, I watch house hunters international.

If that show is any indication, their market is:

#1: “Hot, you need to put in an offer today.”

#2: “Not many properties with the wants you two have”

#3: “one of you will not be happy”

#4: __________ <——- insert euro attitude

The Americans trying to rent:

“Ummm we need 3500 square feet for $800, doable?”

My rent in NH is 2300 for 1100 sqft. It was not easy to find this place, or any place. Most places have so many applications they will not see yours.

It’s usually not optional.

People with kids/families Airbnb.

You’re not going to take a family of 4 out to eat every single meal.

They’ll serve $1 Kraft Mac’N’Cheese for $12 on the “Kids Menu.

Honestly too, who wants to eat EVERY meal at a restaurant? I would be so fat :P and broke too!

RTGDFA at least, Jeesus. You’re confused. You have no idea what you’re talking about.

As I said, this data here based on actual claims for unemployment compensation by people who have gotten laid off.

The stuff you’re referring to is based on household surveys, which is released monthly with the jobs report. Other stuff you’re referring to is your fantasy.

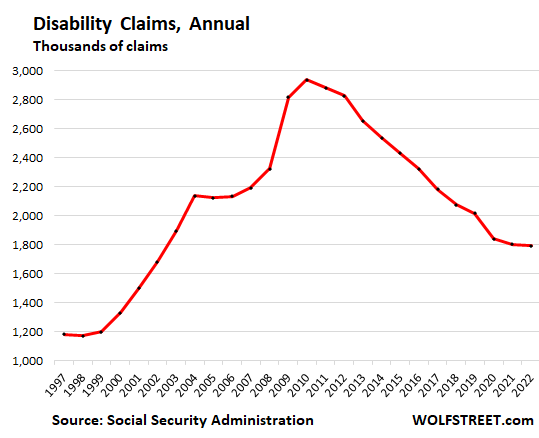

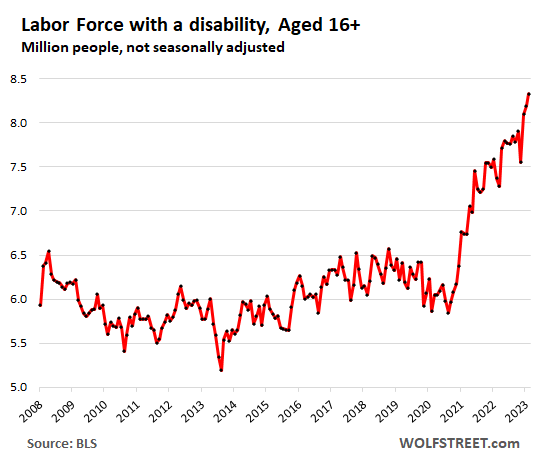

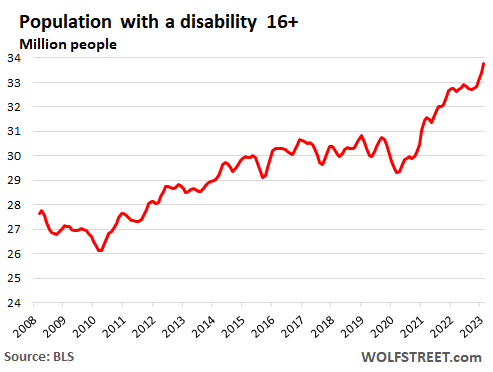

Also the number of people on social Security disability has exploded from 29.85M in January 2021 to 34.15M. That’s 4.3M fewer working age adults in the workforce. UE would be closer to 5% if the SSDI numbers had stayed on trend. There’s your shortage of workers. About 2.2M more than expected on SSDI.

white, bob,

Stupid ignorant bullshit. Do Not abuse my site to spread these effing ignorant malicious lies here.

Here are the SSDI beneficiaries, data from the SSA:

Here are the SSDI disability claims:

Below is Data from the Bureau of Labor Statistics:

The BLS measures people “WITH” a disability, such as a leg missing or an issue due to old age — who may still be working, or be looking for a job, or may be retired, and they’re NOT on SSDI:

Here are the people “with a disability” who are EMPLOYED, and they’re not on SSDI:

People with a disability in the labor force (looking for work or working):

Here is the BLS figure of the population “with a disability,” — not SSI recipients. This is the figure you cited. It includes people who are working or looking for a job, and retirees who are 98 years old and have big problems, but they’re not receiving SSDI.

Read this:

https://wolfstreet.com/2023/08/05/ill-just-crush-the-stupid-stuff-in-the-social-media-about-disability-claims-in-reality-claims-dropped-to-20-year-low-while-people-with-a-disability-are-employed-in-record-numbers/

That’s just his screen name role on South Park. Total believer in F’em all to death, and is eating memberberries.

Unemployment is a lagging indicator, and rate increases hit with a lag also, but yeah, definitely no signs of trouble in US labor market yet.

Off topic, I wonder what happened to commenter Michael Engel. I am starting to think that he was a bullfrog. I never understood a single word he said, but he helped me pass my time.

“Unemployment is a lagging indicator,” is BS that keeps getting regurgitated eternally by the recession-has-already-started-long-ago goofballs week after week, month after month forever. Look at the charts!!!

Well, I guess you could say it leads less than a number of other metrics. But yes, look at the charts, the bottom one in particular, the small run up from the trough we’ve seen is very similar to the small climb from the trough that precedes all the recessions on the chart.

But it is small (and has a small reversal in the past few months), and not every increase from trough like this leads to a recession (there are many ‘head-fakes’) so nobody (outside of the chicken littles who always see a recession coming) is taking that as a clear recession warning. When the big layoffs that people associate with a recession come, by then it is obvious that a recession is underway. This is what is meant by calling it a lagging indicator, it is hard to read a clear signal from unemployment (more than a little) ahead of time that a recession is coming.

But for sure, until continued claims turns back upward, we have to consider it is possible that the increase from the trough was just a post-Covid re-normalization (another ‘head-fake’), rather than the leadup to a recession.

@AwaitingBarneyRubble,

“I am starting to think that he was a bullfrog. I never understood a single word he said, but he helped me pass my time.”

I think only people between the ages of 59-78 would get that reference…. I got it.

Love it Harvey!

But I think it was Three Dog Night that helped Jeremiah drink his wine.

Yeee Haaa!

Maybe it’s just too simple to understand. Or maybe everybody is really that ckueless.

There can be no recession with the gubment running these gargantuan deficits. It’s impossible. Jist take a piece of paper, draw two columns, write “government” over the first and “private sector” over the second. This is your Balance sheet. Then you write “-80 billion per day” in the “government” column. And here comes the Kicker: at the end the numbers have to add up to zero. That’s why it’s called a “Balance sheet”. And here comes the trillion dollar question: what will stand in the “private sector” column if it has to balance out the gubment debt ? Now tell me about a “recession”.

This is Mosler’s point too, if I understand him correctly.

Eccles just stated that the effect of the rate increases has yet to be felt…..

He must have read that in some textbook. That book was written when Uncle Sam ran deficits of 100 billion dollars or surpluses. The weasel will say anything to avoid his job. First transitory now this nonsense.

How does a rate increase affect pure massive fiscal stimulus….it’s like putting your finger in the wall of a dike with a crack.

The rate increases thus far have taken us back to the level that was relatively normal prior to the great demographic hole. It’s not restrictive enough to stop a tidal wave of government cash mixed with demographic increases in spending.

There will be a slowdown that manifests in the next year which will become more apparent after the votes are counted……because the fiscal dollars will ebb….nothing to do with eccles…..of course another year of inflation out the wazoo in the meantime.

I’am sure his children got their calls bought yesterday evening right on time.

“So you’re saying there’s a chance?!” – from the movie Dumb and Dumber

/s

Wait a minute. What was all that one in a million talk?

/s

LVMH, the luxury retailer, is reporting declining sales and profitability.

The luxury buyers online are definitely cutting back on purchases and price points. I only shop the sales and discounters, but have dropped out until XMAS.

We are not in a recession simply because the Federal Government continues to spend at an alarming rate. That is more than making up for other downturns in the GDP calculation. They’re spending money we don’t have.

The money is going to keeping incompetent people employed and moving paper around. They never fix anything, they only study the problem. Look at congress, the fish rotting from the head. Let’s have another hearing about why they never accomplish anything.

The rotting fish heads are mostly in the C Suites (ANY large business)..or dynastic wealth derived from same, or land, years ago…..you are largely just looking at fins.

We are the (still) mostly edible part. But many still fairly nice fat fillets out there, badly in need of taxing.

Wolf what do you think about US Permanent Job Losses as a recession indicator? It’s been on the rise since The Fed started raising rates in ’22.

You need to look at permanent job losers (not “job losses”) in terms of total employment, since total employment — along with the population, the labor force, etc. – has risen over the past 20 years. So permanent job losers as % of total payrolls dipped to 0.9% in September, from 1.0% in August, near historic lows. They’re saying the same thing as other labor data: it’s a growing tight labor market with no recession in sight.

But they’re monthly, and survey based, and lag by several weeks the weekly unemployment insurance claims here. That’s why the weekly unemployment insurance claims data nail it first.

This is what you’re looking at:

Thanks Wolf

The interview with Powell today continued to be softball questions.

Powell says that inflation was a result of lots of demand and not enough supply. What about the 9 trillion of assets on your balance sheet and the interest rates approaching zero? Did that have anything to do with it?

And where is the question about why the Fed is going so slow in selling off the balance sheet? And how about a question on why long term rates are so high when the Fed still owns 8 trillion of assets? Doesnt that deserve a little discussion?

Maybe he’s tried to sell the MBS and nobody wants to buy it at par. I think it would require a huge discount to unload and that has implications beyond the immediate loses.

But let’s not talk about that, it’s embarrassing and depressing.

gametv

“And where is the question about why the Fed is going so slow in selling off the balance sheet?”

“is going to slow selling off” — What kind of BS are you fabricating here?

I think GameTV is suggesting the current rate of sell-off is too slow compared to how fast the Fed printed the money in 2020. He does have a valid point. But Wolf was saying a while ago that a fast sell-off could cause a crash in the whole financial system. So going slow might be the best option here.

There is NO SELLOFF at all. The Fed does not SELL securities.

The Fed lets the treasuries and MBS roll off the balance sheet, as they mature, at a rate of about $75 a month. Nothing is being sold.

“And where is the question about why the Fed is going so slow in selling off the balance sheet?”

I agree, it’s way too slow. By the time they get to 1st base with the roll off, we’ll be in another recession and then they will kick the can and say they have to stop and even start QE again.

The Fed and Yellen have zero credibilty, and both should resign.

Given how tight the labor market is and our aging demographics are you concerned that the job losses in the next recession might be muted, limiting this predictor’s effectiveness? 80+ percent of US CEOs are now anticipating a recession in 2024 but that has not slowed hiring. Most companies are already understaffed so CEOs may be hesitant to do massive layoffs as early in the downturn as is typical. This is my first comment on this site by the way. Been reading it for months. Most sophisticated comment section I have ever seen online. Kudos on the enlightened discussion.

Other way around: if there are no job losses, there is no recession. I posted the NBER’s definition of a recession here. Have a look.

I have a theory that partly the reason people can still spend like drunken sailors is because they’ve given up on buying a home. No amount of down payment is going to make sense to buy right now, and so that five or six-figure nest egg is earning interest and just sitting there. People chip away at their savings knowing there’s no home purchase in their future.

This happened to me in the SF bay area. I have $500k saved for a house but it’s foolish to buy right now, so in my grief I just bought a $70k car instead and will keep earning interest on the rest.

Nooo… Hold tight! Save the rest. I’m so tempted to spend on non-essential stuff, “enjoy” life. There are two reason I don’t. a) it only adds to the current problem. b) I like the high interest rates. I always hated that I was pushed to invest in stock. I never fully did and lost on a lot of opportunity. I don’t care. But this “new normal”, I understand and appreciate. It has turned the tap-off in the absurd amount of tech salaries.

We are still eating out. But the frequency is much low.

I wish you’d kept the 70K, you lose out on interest, plus your car depreciates. Keep the rest. Buy that home at some point and then buy another toy. Good luck!

I feel this pressure and see it in the people around me that are my age/demographic/income level. After rates shot up last year we retreated to the sidelines to wait to buy a home. I then bought a used tundra for 22k so I could enjoy my area camping and 4 wheeling. Not sure I would have purchased it if I was barreling into buying at these newly stratospheric prices obliterating the hard earned security of my savings. Hoard yer sheckles and wait the coming recession in 53 years… or 2 years.. or whatever it is to pounce on your dream home. ;)

Interesting that you believe your terrible (imho) decision to buy a $70,000.00 car somehow reflects on other people.

I don’t know anybody who has done that or would.

Next time, maybe rent a fancy sports car for a day and get it out of your system! Or buy an affordable sports car. They do exist…. Good luck.

Steepening yield curve = in recession.

The depth from which this has begun this time = bad recession.

But by the time the numbers say anything = we are out or close to it.

Nope.

1. The yield curve is supposed to predict a business cycle recession.

2. The last time the yield curve un-inverted was in April 2019, and there was no recession.

3. Then a year later, in March 2020, we got a pandemic and lockdown, totally unrelated to the business cycle, and the yield curve cannot predict and is not supposed to predict pandemics and lockdowns. And it didn’t predict it because it came a year after the un-invert.

4. So, the last time the yield curve inverted and un-inverted it predicted a business cycle recession that didn’t come.

5. Since the era of QE started, the yield curve has become useless as a predictor. It reflects what the Fed is doing: pushing up the short rates and still weighing on the long end with its gigantic balance sheet. And that’s all.

Yep. Learned that here. Thanks. (un-learned from CNBC)…..quite a bit of their crapp unlearned here. But I did get to see them all “lose it” and go off script during GFC…funny….real panic in their eyes….several quit.

Jerome Powell said his favorite yield curve to predict recessions was the 10 year minus the 3 month yield. This was also a subject of a Federal Reserve paper. The earliest 10 year minus 3 month graphs seem to be 1937 at a 2% in the plus; i.e., not inverted. Yet this year gave a recession that relapsed the depression and there is a photograph of people wearing full body signs saying: “I believed the bankers.” The 600 variable Atlanta Federal reserve computer simulation (“GDPnow”) is all over the place. The 1929 recession sneaked up on everyone as well, that is how the elite get “bag holders.” The more the “drunken sailors” spend now the less they have for hard times.

1. The yield curve is supposed to predict a business cycle recession.

2. The last time the yield curve un-inverted was in April 2019, and there was no recession.

3. Then a year later, in March 2020, we got a pandemic and lockdown, totally unrelated to the business cycle, and the yield curve cannot predict and is not supposed to predict pandemics and lockdowns. And it didn’t predict it because it came a year after the un-invert.

4. So, the last time the yield curve inverted and un-inverted it predicted a business cycle recession that didn’t come.

5. Since the era of QE started, the yield curve has become useless as a predictor. It reflects what the Fed is doing: pushing up the short rates and still weighing on the long end with its gigantic balance sheet. And that’s all.

With the population increase the unemployed number needs to be probably quite a bit higher in comparison to the historic numbers to serve as an recession indicator.

Yes, it should be, but it wasn’t in the past, when the population, employment, and labor force also grew, and even at a faster rate. So that’s what the past shows as indicator.

The main thing to watch here is the gap between the green line (“today”) and the black line (“Recession indicator”). As the gap shrinks, the likelihood of the beginning of a recession increases. In theory, when those two lines touch, that would be the beginning of a NBER-called recession. The NBER issues the recession call well after the beginning of the recession, but with a start date that should be right around the point where the green line and the black line met. And with this indicator, we’ll know that well in advance of the NBER’s determination.

You do realize the how fast the curve is steeping right? :)

We couldn’t be closer to a recession than we are now, lol

1. The yield curve is supposed to predict a business cycle recession.

2. The last time the yield curve un-inverted was in April 2019, and there was no recession.

3. Then a year later, in March 2020, we got a pandemic and lockdown, totally unrelated to the business cycle, and the yield curve cannot predict and is not supposed to predict pandemics and lockdowns. And it didn’t predict it because it came a year after the un-invert.

4. So, the last time the yield curve inverted and un-inverted it predicted a business cycle recession that didn’t come.

5. Since the era of QE started, the yield curve has become useless as a predictor. It reflects what the Fed is doing: pushing up the short rates and still weighing on the long end with its gigantic balance sheet. And that’s all.

😆. Third times the charm.

the curve being inverted or not by it’s value doesn’t mean anything. It just shows that interest rates are rising meaning that the long end no longer provides term premium.

It’s the funds rate or the actual interest rate level that plays a role here. In 2019 you had a 2% rates while now you have 5.50%. So, there’s a big difference. I’ve also talked to business owners and the turnovers have suddenly started to suffer. We’ll see.

Catch22,

“Turnovers” gave you away. Not a US business term. We use “revenues.” You’re in Europe, you’re using a European term, you’re logging in from Europe, and you extrapolate from “business owners” in Europe to the US, to make what kind of point, LOL?

Good morning Wolf. I was wondering if you had any recession indicators from Canada. From my perspective up here, things aren’t exactly looking too good.

Unemployment benefit denials are the highest since 1993, the amount of “discouraged” unemployed is up 43% year over year (the individuals in both are classified as non participatory by stats Can, technically not captured as unemployed). Canada also needs to create at least 50,000 jobs per month to keep GDP positive (like 0.1% levels) because of the level of population growth. GDP per capita has actually been negative at least the last few months.

One last question, how much of an effect will the misalignment of the US’s and Canada’s economic “timing” have up here. The BOC and federal government absolutely do not want to raise the interest rate any higher – effect on housing, consumer credit, and government debt – being that the “anti inflation act” juiced America’s economy more, Canada seems to be starting on the credit bust cycle now – by the time the US enters a downswing could it prolong or worsen Canada’s situation?

Excellent questions, as they say when they don’t have answers 😁

In terms of economic growth, the US and Canada are not joined at the hip. In terms of the housing market, same thing. You saw that during the Housing Bust in the US that led to the mortgage crisis, and a collapse in prices, and it was nary a ripple in Canada. Canada’s GDP is a lot more dependent on housing (and everything around it and what it triggers, such as a slowdown in consumer spending) than the US. And you’re seeing some of that now. Anyway, no answers from me, but excellent questions.

Appreciate the reply Wolf. Thought maybe a recession in America could exasperate the situation in Canada.

It usually does. The old saw from at least as far back as the’70s: “when the US sneezes, Canada catches a cold.”

You make me laugh, Wolf!

Part of my job, whether it’s intentional or not 🤣

Powell, Powell, Powell! I want to hear from the real experts: Greenspan and Bernanke.

I have no profound observations. I do think the labor reports of about 200 K per week of new UC claims suggests that the labor market is neither hot nor cold. It’s in between. For binary people, such a distinction is confusing. The continuing claims data is similar. Not dramatically hot or cold. So there is no real trend or data to confirm a trend. Sideways seems a better term to me. I am not clear as to how much the federal deficits are creating inflation and stimulating hiring. Some data takes a while to clarify.

you could at least look at the pictures before commenting, no?