Cut the price, and they will not come? Homebuilders, in a tough market, compete with homeowners who are still delusional.

By Wolf Richter for WOLF STREET.

Homebuilders are trying all kinds of stuff to get sales going in this environment of 7%-plus mortgage rates, including cutting prices, building at lower price points, piling on incentives (such as free upgrades), and the biggie, buying down mortgage rates, which can get expensive for builders. Neither incentives nor mortgage-rate buydowns are reflected in the prices of homes sold, and yet prices have dropped, and sales have dropped too below 2019 levels, and inventory increased, and months supply jumped. For homebuilders, who cannot sit out this market because their business is to build and sell homes no matter what the market does, it’s not an easy environment.

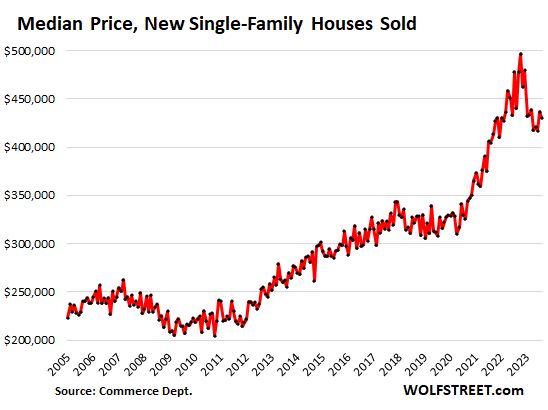

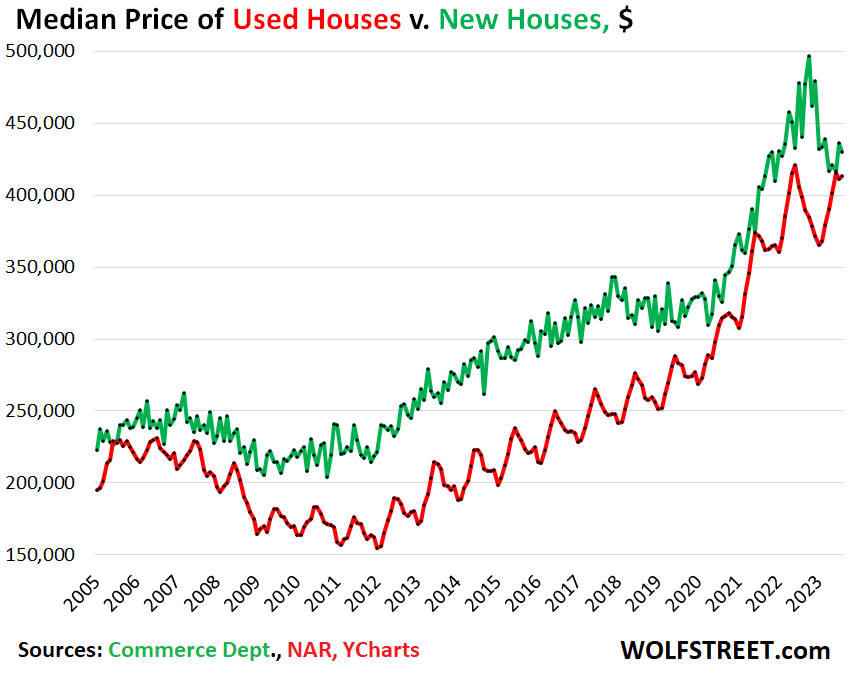

The median price of new single-family houses sold in August dipped by 1.4% from July, by 2.3% year-over-year, and by 13.4% from the peak in October, to $430,300, back where it had first been in November 2021, according to data from the Census Bureau today.

Median-price data jumps up and down a lot, but you can see in the chart that after dropping a bunch in early 2023, it has now roughly stabilized over the past five month at these lower levels. But these prices do not include the costs for builders of mortgage-rate buydowns and other incentives.

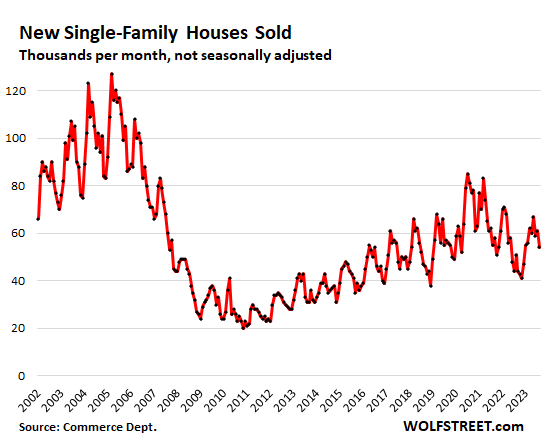

The seasonally adjusted annual rate of sales of new houses fell by 8.7% from July, to 675,000 houses, which was down by 3.4% from August 2019, but was up 5.8% from the plunge last August.

Actual sales – not seasonally adjusted, and not annual rate of sales – fell to 54,000 houses, the lowest since December last year, down by 5.3% from 2019, though compared to the sales plunge a year ago, it was up by 5.9%.

So despite lower prices, ample supply (more in a moment), and large-scale mortgage-rate buydowns, sales remain below the pre-pandemic levels and well below the activity in 2021:

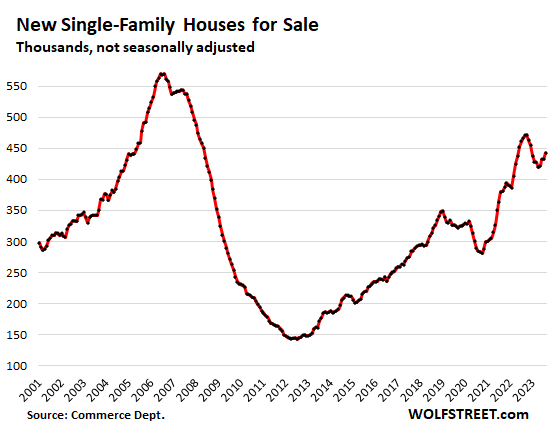

Inventory for sale in all stages of construction rose to 443,000 houses. And that’s a good thing for prices, which are still way too high and would need to come down a whole lot more to make sense, given these mortgage rates:

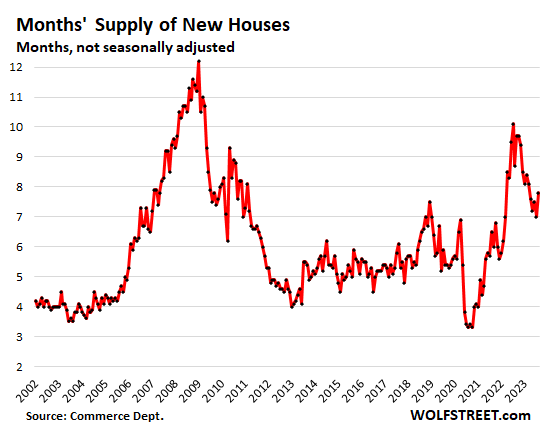

Supply, at the current rate of sales, jumped to 7.8 months, which translates into more than ample supply.

New houses now compete with used houses on price. Homebuilders have to build and sell houses no matter what the market is. And they responded by offering deals, though parts of their deals are not reflected in prices – such as mortgage-rate buydowns and incentives – while homeowners who are trying to sell are still delusional, hence the plunge in sales of existing homes.

And we can see these dynamics in the median price of new single family houses and existing (“used”) single-family houses, whose sales have plunged to the lows of the Housing Bust and the lockdown:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

MW: 20-year Treasury yield heads for record nearly 20 high of almost 4.9%…

LOL!!! Still NOT HIGH ENOUGH!!!

Of course “higher for longer” has an altogether different meaning in SoCal…

Of course, paradise don’t experience boom and bust, it can only boom…

Rates are “Lower than required for longer” => Slow grinding the 90%

Interesting to see what happens. Inflation adjusted Case-Shiller is still shockingly high, mirroring trends here.

Seems prices have to come down or wages will need to come up, likely a combo of the two. Hard to image interest rates going to the low side of historical trends.

Anecdotally, I’m shocked by the amount of people that took ARM’s during a period of the lowest effective rates in our recorded history. Maybe some pain to come in about 5-10 yrs time.

Prices don’t have to come down. All of the assets will be slowly transferred into the hands of the wealthy. That’s what’s happening here. Anybody who doesn’t see it is not paying attention. This is the greatest wealth transfer in the history of the world.

Maybe, what do I know.

But “rich people” are not a homogeneous all-knowing group that all collectively meet to wax their mustaches and plan world domination.

Rich people want ROI. If people can’t afford rent to support the high prices, there won’t be a driver to buy up all housing assets. It’s shift to another asset/investment that promises better returns.

“But “rich people” are not a homogeneous all-knowing group that all collectively meet to wax their mustaches and plan world domination.”

VERY elegantly put — kudos!

As a very wise man once famously said, “You don’t need a formal conspiracy when interests converge.”

I’m with DC on this one. Even when property values dropped to dirty toilet paper, investors jumped in with gloves on. They’ll be back.

You, and many, many others are underestimating the amount of corruption that exists and its effect on the human’s world decay.

I 100% agree with Gaston re rich people. But I’d like to add that policies which help a few rich people tend to incidentally help all of them. This can easily be mistaken for broad-scale coordination, so I have sympathy for DC’s point of view.

Cheerleaders dont get this. Renter exodus/collapse commencing. Same as in last bust. Nobody learns.

Steve,

There cannot be an “exodus” of renters. But there can be churn. All they can do is move to a different rental or buy.

But there can be an exodus of people who own 2nd, 3rd, and 4th homes that they don’t live in, they can put those on the market, no problem, and never have to move.

You don’t really understand the truly wealthy, Gaston. They are beyond caring about ROI. They buy things to own them. They have so much money they don’t know where to put it, so they spread it out far and wide. They plow billions into commercial real estate and it sits idle for decades with no tenants. They buy raw land and pay taxes on it for decades with no leases or income. ROI? Uh-huh…….

Gaston/George

Just what the hell do you think the “Heritage Foundation” IS and DOES? They had enough $$$$$$s and clout to put Reagan in AND write his script, which is still running today, unfortunately.

And Lili’s “common interests” point is a VERY good one too.

They probably don’t twist greasy mustaches, I’ll give you that. b

But they are ALWAYS working VERY HARD, have all sorts of think tanks, and are spending LOTS of $$$$$$s to get the economics of that Gilded Age you describe BACK, and anything else they can control that comes along.

Go check out the site….Check all the similar ones ,too. They show up on C-span once in a while. I saw their CEO insisting that the real goal is to “fit gov’t into a bathtub where it can be drowned”, literally, and at least 4-5 times.

They are quite serious and dedicated….and successful, unfortunately. You two are blind.

Been saving every flip I see on zillow and LOL’ing at the bi-monthly price decreases. Extra lols for the idiots that decided white paint/black trim and mica flecked jet black granite counter tops were going to give 1950s ranches appeal in rural NH. Places look like a gawdy Forever 21. Maybe theres a market for black glass fireplaces in Boston penthouse suites… or 1990s LA mansions. Wishing all the best to the builders actually giving people what they want and adding to the supply. They are literally doing Gods work.

Whoops this was not a reply to this comment. Ignore my schadenfreude ramblings as part of this thread.

The last thing rural NH folks want is for their property to look like a fancy Boston apartment LOL.

My 1970s ranch in southern NH was a flip by the prev owners, with a lot of shoddy work done that I’ve since had to fix.

” Extra lols for the idiots that decided white paint/black trim and mica flecked jet black granite counter tops”

Headline from today’s LA Times: “California workers who cut countertops are dying of an incurable disease”

Prices of residential real estate most certainly do have to and will come down very dramatically in the years ahead.

Just watch the unemployment, that is cure for high prices.

It takes time to turn any large thing around but inability to afford living sure is an incentive to get out.

Depth Charge says:

> Prices don’t have to come down. All of the assets will

> be slowly transferred into the hands of the wealthy.

> That’s what’s happening here.

Do you mind sharing where “here” is (I don’t want your home address just the basic area of the state you live in).

I keep hearing people complain (in person and online) about the “rich” (or the “Chinese”) buying up single-family real estate but I have never heard of an area where after you exclude the homes (and vacation homes) that the “rich” (and Chinese) are actually living in where it is even close to 1% of the homes.

My wife gives me a hard time about this but every time a home sells around our home or around our cabin both in Northern CA I’ll see how long it takes me to find the new owner on LinkedIn. Most of the time I’ll find the owner in a few minutes and of the times I need to “ask around” it is almost never an “investor” buying the property (I don’t consider a guy that buys a cabin to use himself and rent when he is not using it an “investor” since the cash on cash “return on his investment” is so low (if not negative).

I don’t think we need to worry about rich people snapping up all the unsold new homes at $430K .

Not sure about DepthCharge but here in Canada investors as a whole can make up somewhere in the 20%-25% in Metro Vancouver and Greater Toronto market, once you leave those centers that number starts decreasing drastically. When it comes to foreign investors (usually meaning Chinese) the last investigation into this showed about 3% and only in those “international” cities.

So investment or speculative purchases amount to quite a large percentage in some places IMO but most of it is domestic. I think people want to scapegoat so the “Chinese investor” is a perfect target. There was also an investigation into property purchases in a suburb of Vancouver years ago that found a significant number of properties sold to Chinese investors at way over asking, people didn’t like that because RE prices are affected by sales on the margins and can help fuel bubbles. However, in the end excess cash, central bank shenanigans, are the main driver.

Anyway, for some people low interest is a wealth transfer to the rich, high interest is a wealth transfer to the rich, no change in interest is a wealth transfer to the rich. In a way I can’t blame them because wealth disparity seems to have been growing for damn near 100yrs by most measures I’ve come across. Wealth is leverage and wealthy people use it to become wealthier while the rest pay bills, it’s the way things have been since I was born and probably long before

Here is the United States.

No. The assets are going to be transferred to normal people at inflated prices and money will be transferred to the rich.

With Mexican slave trade in full swing, they have lots of room between wages +material and tax-thief-assessments. The gov or some corporate conglomerate backed by gov will continue to extract everything. We all watch it in broad daylight, go look and see. Go for a stroll in your town, not only 2:1 in broad daylight, for everyone presently here 10 have come and gone. Parasite sucking off of bigger, gov-quasi-business parasites and then the ‘American’ worker.

And the gov acting as ‘wall’ GC would work a lot better if we were dealing with German Shepherds but really just enforce basic employment rights is only thing needed. If the ‘boomer’ had a backbone to enforced basic employment rights within of their own communities, the tax roles, the demand, the housing inflation all go POOF! We go back to 1978 GDP in a flash, no fancy math needed.

Yaco the magician shined a light on ww2 combined with the civil-slavery- war. It’s being ran thru .gov and wallstreet like the German Shepard handlers hand-in hand-in talledga nights.

Yacos – as discussed here several times over the years, stringently-enforced card-check would

have addressed many issues, but remains steadfastly ignored by our elected representatives (…and by extension, the voting public…).

may we all find a better day.

What is it like driving by looking in the rear view mirror?

Your comment was accurate in the past, but in this era of higher for longer, your comment is ass-backwards. Asset prices are in the process of coming down (if slowly). Wages are rising (and are the main driver of inflation). Liquidity (capital) is slowly be drained. Workers are slowly getting a larger share of the pie and higher for longer rhetoric by the FED indicates this is going to continue into the future.

Drive looking forward, not backwards.

It sucks as a buyer when the official purchase price you paid for your home doesn’t reflect the mortgage buydown, because property tax is based on the purchase price. If you’re in California with Prop 13, your property taxes are permanently higher due to the lack of transparency.

Nobody required them to be a buyer.

And the prices paid is the price paid. Buy-downs are to drive down the interest rate and it’s completely transparent.

Shouldn’t have bought, then. Everyone buying during this bubble is part of the problem.

On another bright note, did everyone see today’s Case Shiller numbers, which finally showed what anybody who has actually been watching the existing house market has known for months? Last year’s minicorrection in used house prices has been completely reversed and then some. There went Powell’s “bit of a reset” that he promised house buyers last year: it was only a bit, it only lasted a bit, it only helped you if you were paying cash, and if you blinked you missed it.

The median house price nearly tripled in the 1970’s… Was that a bubble? It doubled again in the 80’s… Was that a bubble? How about car prices over that period? Cars became much more expensive despite significant increases in manufacturing efficiency. Was that a car bubble? Or was it all because we printed money?

Pre-GFC house price increases were driven by massive debt growth, not money printing. That was a bubble. When bad debt popped, so did the bubble. But according to many of Wolf’s great articles, the average consumer’s credit situation is in excellent shape (at least nominally). This isn’t a bubble. People who call it a bubble either don’t know what a quick 35% expansion of the money supply looks like, or their memory of the 70’s/80’s has become quite foggy. It just should not be surprising that growing our money supply by 30%+ resulted in our lives becoming 30%+ more expensive. It’s the most easily understandable and reliable concept in the financial world. More dollars per person in circulation = higher nominal prices.

Cars prices rose because of government mandates. Airbags, backup cameras, ABS, emission controls, catalysts, etc., plus consumer preferences for power windows, air conditioning, leather upholstery, audio beyond an AM radio with a single speaker slapped in the dash, and so on. Price growth is not all purely tied to currency in circulation. The population of the country has likely increased, so what is the per capita currency amount that is domiciled in the U.S. (not in some drug cartel kingpin’s wine cellar in Mexico) compared to the periods described?

Houses are in similar stead. The house of the 1970’s was far smaller than today’s house and few people today are lined up to buy a <1,000 square foot 3/1 ranch house on a slab foundation with a one car attached garage (or no garage) located on a street with no curbs, no sidewalks, and no storm sewers, for their family of 4. Formica counters, no dishwasher, no microwave…. Then there's building code upgrades… wiring upgrades (GFCI's, smoke/CO detectors, increased outlets and switches, increased number of circuits/breakers, the cost of copper wire/plumbing, plumbing for multiple bathrooms along with the fixtures (sinks, commodes), wall surround and floor tile, and so on. Don't forget that often the flooring was sheet vinyl in the 70's and 80's, not individually laid tile. Central air conditioning was a luxury in the 70's and 80's, not an expectation as it is today. There's also impact fees and other costs that weren't dreamed up yet by municipal governments that also add to today's costs.

It's not quite a fair comparison.

This. End of the gold standard and start of the money printing era.

Most (but all) price growth is ties to money printing the price of a new Porsche 911 did not go from ~$7K in 1970 to ~$28K in 1980 just because the government made them add bigger bumpers and thermal reactors to lower emissions). On the SF Peninsula many of the “exact same” homes that sold for ~$50K in 1970 were selling for ~$300K in 1980 (without one dollar of upgrades)…

El Katz, I know you have huge experience in the car business, but you’re way out on a limb there. I’m talking about car prices exploding particularly in the 70s. Emissions equipment was pretty much the only meaningful change to American standard equipment over that decade. A cat thrown on a severely detuned mid-50s design small block v8 added what, 5% to cost? Lots of cars still came with roll-up windows into the early 2000s. Airbags and ABS didn’t become common in mid-market cars until well into the 90’s (mandated in 1998). And backup cameras, really? That tech isn’t even from the same millennium as the 70’s, being mandated in 2018.

As for median house price, it’s not like they bulldozed all houses and built bigger more expensive ones in the 70s. Outside of some particularly depressed areas, an average American house that was standing in 1970 sold for a lot more in 1980 and a lot more again in 1990.

I typically like your posts, but the numbers don’t really leave room for argument here. Inflation of everything in the 70s was very hot after we fully ditched the old monetary standard and printed our way out of a very costly proxy war + a cold war and space race. It’s as clear as can be. Gov mandates have certainly made cars more expensive, but lots of that has been offset by giant leaps in manfacturing efficiency. A 70’s auto plant wouldn’t even look like it’s on the same planet as a current facility inside. Simply put, nothing bumps nominal price like trillions of new dollars.

Housing affordability is sh1t.

Median payments relative to income are at all-time highs. Median house prices relative to income at all-time highs. Santa Claus or Goldilocks will solve all the problems.

On the bright side houses aren’t shooting up at light speed anymore. Time will tell where we go from here.

I wonder if, let’s say, you are buying a new build for $500k with 20% down, and hypothetically the builder offers you to prepay points and bring your interest down from 7.55% to 5.55%, presumably spending around $30k on it, would this builder agree to straight lower the price to, let’s say, $475k instead and leave you deal with the lender by yourself?

It looks like from the isolated perspective of only this transaction the latter option is better for the builder (as they “lose” 25k instead of 30k), unless you account for creation of a new lower comp point…

I think no because of comps as you said. Lowering the monthly payment without impacting comps maintains valuations.

If builders have high enough margins cooked in, then rate buydowns can continue as long as they are willing to accept lower profits.

The buyers are capital investor, ‘bit-sh!t’ crypto investors, ‘Airbnb’/rental investors, gov shill and or gov shill pension receivers, who cares about the numbers!

Thank you Wolf. I have been waiting for this article.

Hi Wolf. Is there a lead lag in terms of timeframe we can derive from this for increase in unemployment and recession? Thanks

Unemployment claims (to get unemployment benefits) and unemployment rates are historically low, and they now both point at a hot labor market and at a growing economy. They predict recessions pretty well, but they would have to JUMP a BUNCH from these levels for a recession to be even on the horizon. Here are unemployment claims and recessions.

The data is a couple of weeks old. Unemployment claims have dropped even further since then:

https://wolfstreet.com/2023/09/07/my-favorite-recession-indicator-the-next-recession-moves-further-out-of-sight/

This was the sort of data that I was very curious abut. I can clearly see that there is an extremely strong correlation between the fed balance sheet and new house prices since 2017, with a few months of lag in between. Even the fed’s limited March 2023 money expansion was reflected on the prices.

The delusion of existing home buyers is right on point. This delusion is caused by fed. In last 15 years, whenever the housing prices tend to show even some minor correction, they expanded money supply like crazy to revert the trend, so the existing home owners firmly believe that house prices never go down, almost like a religious script.

Wrong blog buddy.

Jared walked away with $2 billion from the Saudis.

It’s funny how that slipped you mind there.

*Cut the price, and they will not come*

It is foolish to try to catch a falling knife.

It’s smart to wait and get it off the ground

So many commenters here are wishing for a GFC-level crash so they can pick up a house or two for pennies the dollar. They forget that millions of Americans were financially destroyed for years after 2008. Some never really recovered. And maybe a few WS commenters could make good on the value buying plan, but let’s face it… A big crash with prices “on the ground” does you no good if your job or business is gone and your income is also, “on the ground.” The median house price could drop down to 100 bucks, and you’d still be SOL if you only have $5 to your name and no income. Prices are high because people are employed and making record nominal earnings. Prices come down when the average person isn’t generating enough income to afford the payment. Prices only crash hard when the average person’s income crashes hard, meaning major job losses. Careful what you ask for.

For the average person sure. Anyone with any financial sense would have been pocketing every last penny they could for the past few years.

Until recently when my health started going downhill and let’s just say I can see the sun setting; I was driving a 2000 dollar 40 year old truck, living out of a coworkers lean to on his barn, and working 60+ hours a week. I’d cook often on a propane Coleman grill and sleep under 20lbs of blankets in the winter. I was stacking back 4k dollars a month as a manual laboring truck driver.

If you’re willing to sacrifice everything else in life, you could be raking in a ton of cash doing low skill unfulfilled crappy jobs right now. God forbid you could swing something like elevator mechanic or industrial controls and write your own paychecks. I know a guy who left where I’m working because his dad got him into a IBEW job fixing PLCs. He drives a company truck from Spokane to Seattle, stays in a nice paid for hotel for the week, and has a 150k+ a year job before per diem pay which isn’t taxed. And he’s only averaging a 50-55 hour work week. If he didn’t ride around in a new ZL1 Camaro and could stay away from the rental women, he could be into a paid for modest house in 5 years.

But as they say, a fool and their dollar soon parts. And to be fair, such dramatic sacrifices aren’t in the wheelhouse of most normal people. It takes an unhealthy fixation on money to do without a comfy warm bed when you could give up a third of your monthly take home for an apartment.

I will still be SOL, and I will have plenty of dough ready to go.

You are right.

but you’re missing the fact that even though many people are making a lot of money now house prices have long been out of touch with the current salaries.

People can only afford them with leverage, which is not sustainable over time.

Don’t forget there are a lot of people with a lot of cash waiting for this crash to get into the game. Even if they lose their job for a while, it won’t stop them from buying a property at a low price.

Maybe it’s the salaries that are out of touch with the house prices.

“So many commenters here are wishing for a GFC-level crash so they can pick up a house or two for pennies the dollar.”

I know. How rotten of them to want affordable shelter from the storm, those assholes. The nerve.

Yeah…. there are more than a few commenters here who think a financial crash will leave them unscathed. I am not sure if their problem is having too little imagination… or too much.

They also forget that the biggest generation in history is housing buying age and are getting huge wage increases and are looking for any opportunity to buy a house they can afford.

Housing prices are likely to drop a little, even more than a little, but won’t crash absent a recession.

If only one could tell where the ground is!

At some point, I’d hope builders will start building smaller homes so they can sell at lower prices. Not every couple with a dog and no kids needs to live in a 4000 sqft McMansion.

When I look at homes for sale in my area (Boston metro), there is almost nothing available under 1000 sqft. Having more starter homes for first-time buyers would help the affordability issue.

In fact smaller houses are simply not that much cheaper to build. And now with cheap Mexican labor the big component is land and associated government costs. A four thousand SF house does not cost twice what a 2000 foot house costs. Today a starter home is an apartment.

Also, newly built starter homes are almost never built in already built up areas (such as Boston). Starter homes have traditionally been built in locations that were not built up (farmlands surrounding already built up urban areas) or in undesirable neighborhoods of already built up urban areas (gentrification of bad neighborhoods).

Smaller homes lower the margin for Sellers, while Buyers will pay more per square foot. Kind of like those “counter-depth” refrigerators with less square footage cost more than a big bulky fridge. Might as well buy the behemoth.

Already happening here in one of the hottest markets in TN. $700k new builds not selling. Several new developments of much more reasonably sized homes going up.

Also, minor typo in the Inventory for Sale section just above the graph:

“and would need to come down a whole lot more to makes sense”

I was wondering if the price of new houses is adjusted to reflect the recent mix of new houses, i.e. cheaper, almost no backyards, etc. I wish there was a way to compare if prices are actually going down or if new houses are getting worse. Perhaps New Home Sales Price/Sq Ft would be an interesting metric to track against Used Home Sales Price/Sq Ft.

Over Labor Day weekend on the way to Tahoe we stopped in Davis, CA to see a newer (not brand new) 4×3 home a friend bought for his Daughter (a UCD student) to live in and rent to friends. The 1,800sf newer two story home was on a tiny 2,000sf lot (not much of a yard). Most of the suburban CA homes built in the 60’s and 70’s that were ~1,500sf 3×2 and ~2,000sf 4×3 were on ~5,000-~8,000sf lots while most newer developments in CA seem to have homes just as big lots under 3,000sf.

Interesting that the lot sizes are so small, you measure them in sqft rather than acres.

Also, what does 4×3 / 3×2 etc refer to? Bed x bathrooms?

Yes… 4×3 is 4 bed / 3 bath. 3×2.5 is 3 bedroom / 2 full baths plus a powder room (aka half bath). 3/4 bath is commode, vanity, and shower – no tub.

What I said paragraph #1:

“Homebuilders are trying all kinds of stuff to get sales going in this environment of 7%-plus mortgage rates, including cutting prices, building at lower price points, piling on incentives (such as free upgrades), and the biggie, buying down mortgage rates, which can get expensive for builders.

“At lower price points” means smaller, but not always; it also means less fancy roof-lines and layouts, lower-priced appliances and finishes, etc.

Mortgage rates are supposedly based upon 10 year treasury rates plus some sort of risk premium. etc. The treasuries would just now give Volcker a slight glance. Some news is reported by Financial Times: “The debt-fuelled bet on US Treasuries that’s scaring regulators.” Some sort of basis trade that looks a lot of amplification and positive feedback; the hallmark of a completely unstable control loop (like feedback into a microphone at an event). That basis trade looks like it might do to the treasuries what Jerome Powell & Co. have been talking about at every opportunity, but have been unable to achieve. “Volcker is the force that binds all financial things” paraphrase of “Star Wars.”

The 10-year yield is still way too low. It should be at least 1 percentage point higher than T-bill yields, now at about 5.5%. So that would take the 10-year to 6.5%, that would be about right.

Would really love to see that, can we say 9%+ mortgage rate? Will that stop SoCal FOMO buyers from selling their mother to get that house? Probably not but amusing to see nonetheless..

Unfortunately, the consensus aming people who consider themselves “experts” seems to be that it’s the other way around–that the dreaded Inverted Yield Curve can and must be corrected by short term yields going *down*.

They’re full of crap, of course, but these are people who are taken pretty seriously in the macro econ world.

Don’t forget to insert not in SoCal (insert cities..Irvine, San Diego, West LA..etc) price still high, still bidding wars, sold over asking..listing sold in less than a month…etc. Finish it off with this time is different, at least in SoCal paradise.

Phoenix_Ikki,

… And also metro Boston.

I just (and I shit you not) made

an offer more than a $100k over

the asking price on a house. And

I will bet you dollars-to-donuts

that I don’t wind up buying it. I

will be interested to see what it

sells for, though.

Prices seem to at least not be

rising much, anymore. As a

wanna-be first-time buyer, it

is, uh, frustrating out there.

J.

————————

The place was way underpriced

by the used house salesman as

an obvious ploy to draw attention

and sell it quickly.

Another twenty percent inflation,

and lopsided bets will have to be

“donuts-to-dollars”. Weird.

… And “under contract”, but not to me.

Just as well you didn’t take up a bet, I’m

not really that big a fan of donuts, anyway.

J.

The metro Boston market is still massively overpriced. I’d suggest renting for the next year or two, and seeing where prices are then.

Also, look further outside the city itself. There’s a price premium for living inside rte 128.

MM,

Yeah, there is a certain logic in

“drive till you can buy”. I think

it’s nice to have everything in

walking distance. If I were gonna

buy far from town, I’d be tempted

to leapfrog over you and get a

place in Maine.

J.

————————

The 71/73 buses are OK.

That’s funny – I used to live in Watertown, and commuted on the 71 back when it ran as a trackless trolley.

But it still took an hour to get to Cambridge: 20min walk to W’town square, and then a 40 minute ride. My current drive in from the NH border is also about an hour commute.

MM,

You had mentioned riding

in one of Wolf’s EV articles.

I do prefer the 71/73 to the

diesel buses. I’m sure that

I saw you around sometimes

during the commute. Even

though I rode the other

direction, as I’d often keep

odd hours.

J.

Observing from 1000 miles away and not intimately researching the real estate market I would still say that the Boston metro market is not overpriced, because that is where many government-favored industries and institutions reside. The spigot is broken in the ‘on’’ position and the This Old House Plumber is not going to fix it.

You’d be surprised by how many of us are normal, working people without access to any special favors or lucrative contracts. The vast majority of us in Eastern Massachusetts are drowning from the housing crisis.

Cool. Myself I’ve been shorting homebuilders. Very early innings in a long game with lots of losers. The game is 7% where everyone will be a loser. Did you read Dimons latest warning today? He knows something(s).

I wouldn’t put too much stock into what Dimons is blahing to MSM, that guy has been flip flopping here and there, wouldn’t count on him to provide an unbiased objective outsider view of what’s really going on..

I agree about Dimons.

Bob Michele, chief investment officer of fixed income at J.P. Morgan Asset Management was on Bloomberg last week and said the 10 year treasury is a screaming buy and he is calling for a recession early next year and a rate cut.

Later the same day Dimon said he would not touch the 10 year treasury because the 10 year could go over 5%.

So the boss is not listening to his employees or maybe investment group and the banking group do not talk?

I moved back to the Coachella Valley about 18 months ago after a 3 year stay in Temecula. CV is a huge winter tourist destination with over 13mm visitors annually. As a consequence, AirBnB rental purchases have gone nuts here; in some communities short term rentals are now 20% of SFRs and condos. I wanted to buy upon moving back, but the homes prices have almost doubled in the past 3 years. My prior home the base payment for mortgage, property taxes, HOA, home insurance was around $2,100 for a nice 1800 sq ft middle class home that cost $350K. Similar homes in the same neighborhood are now selling for around $680K, the monthly base nut is now around $5,200 per month. Post 2008 the SFR market in CV was clobbered due to the huge number of second homes that went into foreclosure, prices basically were cut in half. I’m hoping for a repeat post what I believe is coming next.

The quality of the new homes being built seems to have been reduced to enable lower offering prices — but we don’t know just what was done in this regard. That tends to dilute or blur the significance of the drop in sales. The product being sold has changed. How much of the price drops are due to buyer uncertainty about the quality changes being made, not all of which (like say yard size) are obvious?

Speaking of lack of sales volume, came across this article. Kind of interesting and my question is what’s taking these agents so long to realize especially since we have seen how many agents got weeded out last time after 08…I guess people by and large are toxically optimistic even to their own detriment..nope this time is different right?

“A report from the Orange County Register. “Surviving the slowdown was a key theme at the California Association of Realtors conference last week in Anaheim. Helen Jeong’s most prosperous year as a real estate agent occurred in 2020, when five sales generated the most cash she had seen in her 17 years in the business. A year later, mortgage rates shot up like a rocket, turning the real estate industry upside down. ‘2020 was my best year,’ Jeong said, between pep talks and training sessions at the California Association of Realtors conference in Anaheim. ‘After that, I’ve only had one closing per year, and that’s terrible. … Buyers were all priced out.’”

“Burbank-based real estate broker Karol Kochova, who led the session on stress and burnout, said financial stress is taking a toll on agents’ personal lives as well as their work. ‘Unfortunately, that trickles down into the family life,’ Kochova said. ‘It’s heartbreaking … to watch people going through financial hardship and depression.’ Some agents are thinking of career changes, she said, while others are taking part-time jobs like driving for Uber or Lyft”

Any and all agent should be totally eliminated and all housing transactions should be done on the internet on exchanged at about 0.50% cost to handle and complete the sale.

One sale a year?????? They should definitely be in another business…. or as a well known RE coach says “lf you’re only going to do 10 deals a year, do them all in January and take the rest of the year off.”

Would you go to a surgeon who does one operation a year or a commercial pilot who flies one flight a year. You’d have to be a moron to use a realtor who does one deal a year

Exactly right. Our family has been using one woman for our transactions and she does well, year in and year out, no matter what the environment. She is the best real estate agent I ever saw – although the bar is not very high for that!

Investors in denial. Must be fake truth.

At my family’s Labor Day gathering the two young Realtors in the family actually used the term “Golden Handcuffs” to describe the impact on sales of so many people with 3 to 4 percent mortgages right now. Two years ago they were selling houses sight unseen for 20% more than asking price… and we do NOT live in California.

For the first time home buyers that were building families and making job changes as the good times started back and were moving to the likes of Austin and Dallas I have some sympathy but the good news is they have 2.75 percent mtg !! Higher for longer please I dont want inflation coming back.

Our local realtor is pitching “assumable mortgages” as the next great hope.

These are VA and FHA backed loans. Fannie and Freddie paper need not apply.

I can’t believe that there are enough of these out there to save the housing market, but hope springs eternal.

If you have an assumable mortgage, don’t be surprised if you start getting cold-calls, form letters in the mail, or even spy a desperate realtor camping out in your front yard with a giant “I love you, please sell!” sign.

Except for the fact that a buyer of a property with an assumable mortgage needs to show up to closing with a wheelbarrow full of cash to make up the difference in the outstanding balance owed by the seller, and the agreed-on sale price. Only the outstanding balance is assumable at the prior interest rate.

That’s why noone is selling. It has nothing to do with price. They know the gubment will bail them out eventually.

A generation or three, ago a seller may offer ‘to carry a note’. That was in a high-trust society, long-gone.

///

@Wolf

Could I kindly ask for a normalized graph QT vs median home price? (Just like the one a few articles ago)

///

Thank you

///

Eventually.

If you build it, they won’t necessarily come?

All the out of work Realtors@ will have to jump on to the bandwagon and become Instacart gig workers.😊

They can buy investment properties and rent them out!

Exactly. Have a friend who worked for a large national home builder.

Got washed out in the GFC. No hesitation. Purchased luxury homes in the Orlando area. Sold the last about 3yrs ago. Enjoying retirement.

It is humanly impossible to do anything like luxuriate in or anywhere near the Orlando, Florida area.

What are the old delusional homeowners going down with the ship supposed to do instead – camp out in a sleeping bag on a cemetery plot?

MW: US stocks finish sharply lower as Treasury yields hover at 16-year highs

In a semi-rural northern California market formerly dominated by trends in the Bay Area market, we’re seeing a disconnect in favor of the local market for the first time that I can remember. The usual pattern was for a subdued echo of Bay Area boom markets and, percentagewise, steeper corrections during downturns as the influence of gentrifying money, driven by urban housing prices, over the local market increased. Now we’re seeing a spectacular collapse of the Bay Area market after the pandemic bubble but no sign of things slowing down locally. I was a little taken aback when my own house went well into the 300s during the pandemic, after being somewhere in the low-to-mid 200s for most of the post-GFC era. An 800 sq ft 1940s crackerbox in my neighborhood just went for 370k, which would have been unthinkable even during the pandemic bubble.

The reversal of the usual pattern vis metropolitan and exurban trends makes me wonder if the metro collapse, particularly in notoriously dysfunctional Seattle, Portland, and Bay Area cities, is driven by those cities becoming so unattractive in their dysfunction that only people required to be physically present in those cities for work are remaining in their markets. We could be seeing a major shift in lifestyle choices among those whose professions allow them the flexibility to choose.

I guess that I am among the remaining few dinosaurs who buy new or used home because I actually want to live in it.

My place is used, 10 acres in the country, with great neighbors the closest at a thousand yards distant, and it is like living in a national park. No mortgage either.

Frankly, if the price went to $10 million or dropped to zero, I wouldn’t consider moving.

Shockingly enough about a third of the nation has no mortgage… and it has been that way since WWII.