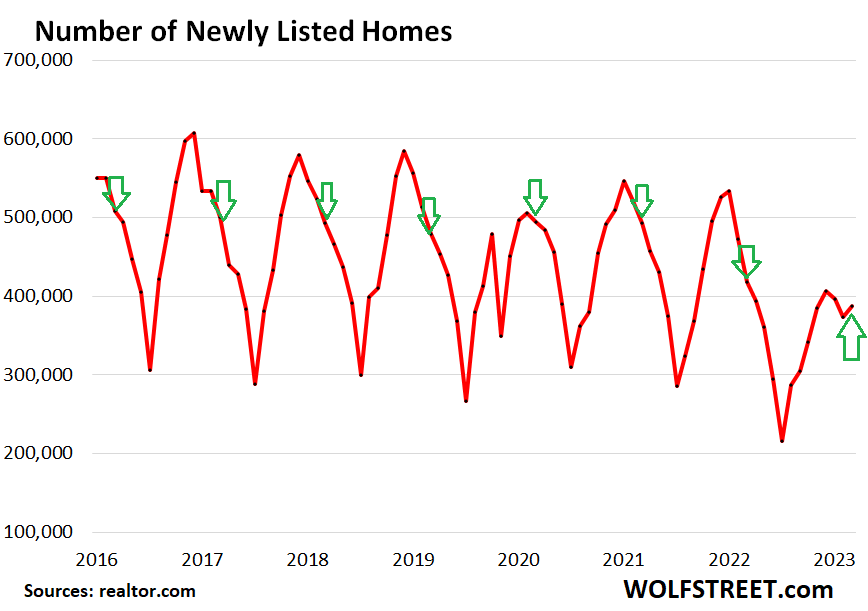

New listings rose in August, when they normally fall in August, an interesting break in the seasonal pattern.

By Wolf Richter for WOLF STREET.

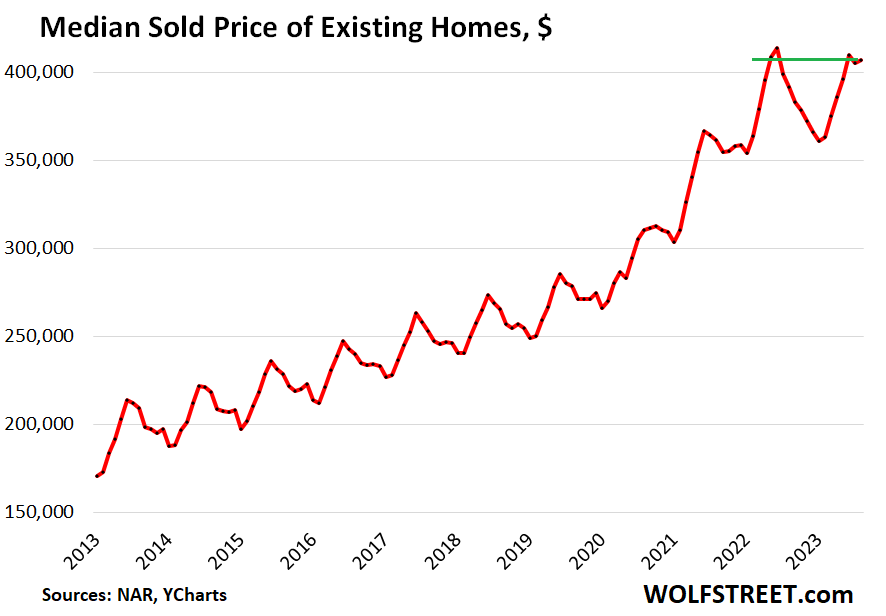

Let’s start with the median price, which in August was $407,100, roughly flat with a month ago, but that month-ago figure was revised down today by $1,000, and after that downward revision, today’s price ticked up by a hair. Due to the plunge in July and August 2022, the median price was up 3.9% year-over-year. From the peak in June 2022, the median price was down 1.6% (historic data via YCharts):

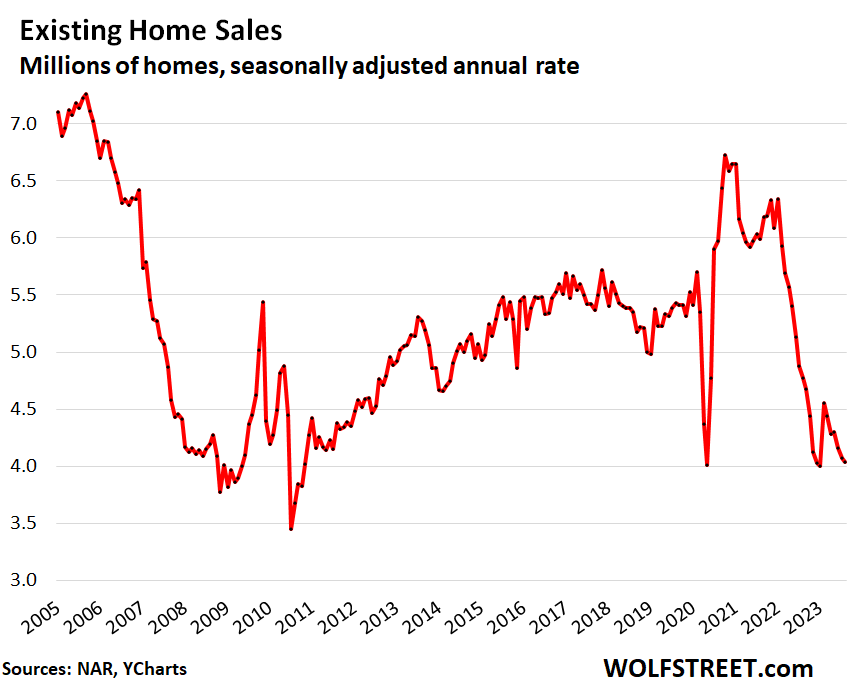

Sales of previously owned houses, condos, and co-ops continued to fall on a seasonally adjusted basis, to an annual rate of 4.04 million homes in August, roughly level with the deep-dismal rate of March 2020, which had been the lowest since the Housing Bust in 2010, according to data from the National Association of Realtors today.

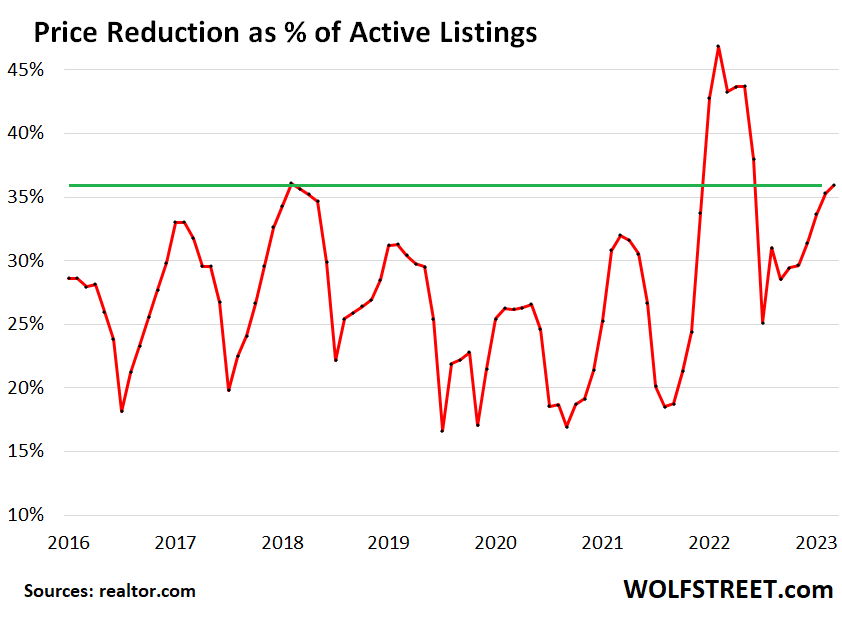

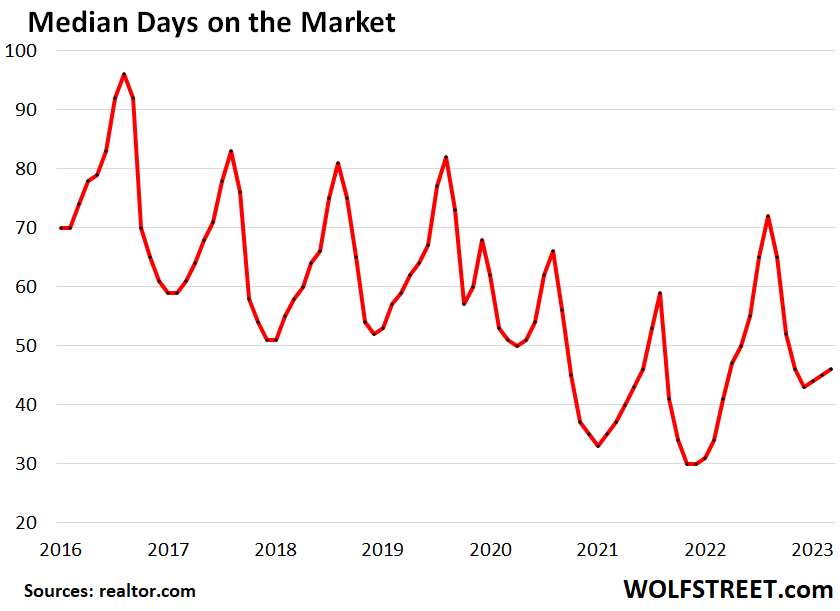

But new listings rose, which they never do in August, and median days on the market rose, active listings rose, and price reductions as a percent of active listings jumped to the second highest level for any pre-pandemic month in the data, behind only July 2018, according to realtor.com.

The seasonally adjusted annual rate of sales of 4.04 million homes was down 15.3% from the already depressed levels a year ago. Compared to the Augusts in prior years (historic data via YCharts):

- August 2021: -32.6%.

- August 2019: -25.6%.

- August 2018: -24.5%.

Demand and supply have vanished in equal measure because the homeowners with a 3% mortgage are not buying a new home, so they have vanished as buyers; and they’re therefore not listing their current home, and so they have also vanished as sellers. This phenomenon caused the entire housing market – buyers and sellers – to shrink by about 20%, I estimated here.

Because these homeowners vanished as both buyers and sellers at the same time, there is less churn, and Realtors make money off the churn coming and going, and so they loudly lament this situation that is so dire for them. But as far as the market is concerned, with both buyers and sellers gone in equal measure, the balance is still there, but it’s just a lot lower: lower demand, lower supply, and lower churn.

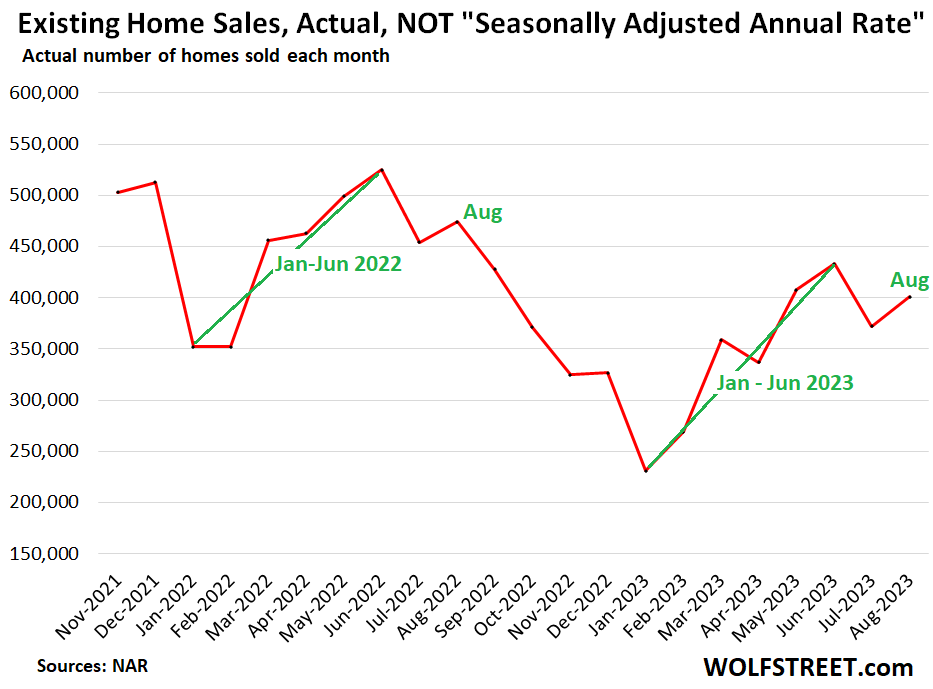

Actual sales in August – not seasonally adjusted annual rate – at 401,000 homes, was up from July due to seasonality. Year-over-year, actual sales fell 15.4%.

Note the seasonal patterns: the “spring selling season” (green) that culminated in June, followed by the drop in July, the rise in August, to be followed by declines the rest of the year. The actual sales data provide a better understanding of sales and seasonality than the seasonally adjusted annual rate of sales above (data via NAR):

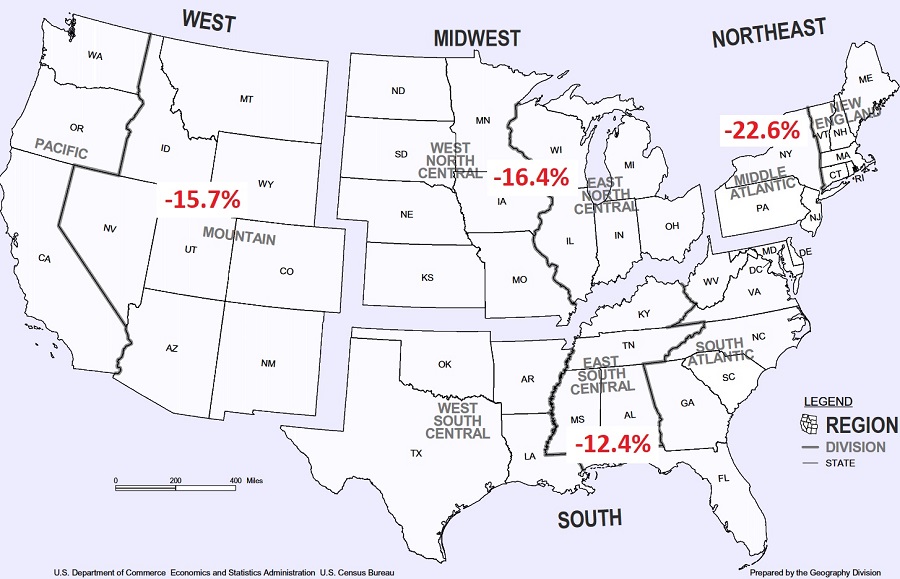

By region, year-over-year sales plunged in all regions from the already beaten-down levels last year:

Cash buyers and Investors pulled back too: All-cash sales – often investors and second home buyers – dropped by 5% year-over-year to 108,000 homes in August, or a share of 26% of total sales.

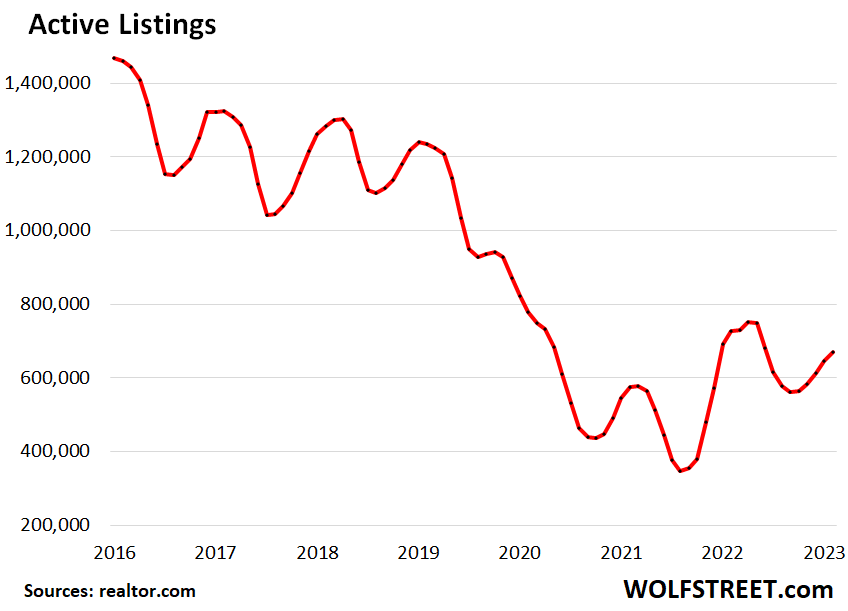

New listings rose in August, which they never do in August. New listings seasonally fall in August. June is generally the peak of new listings in every year. July is the beginning of their decline through the rest of the year. But this August, for the first time in the data, new listings rose. And that is an interesting break from the normal seasonal pattern (data via realtor.com):

Price reductions as a percent of active listings jumped to 35.9%, which about matched the pre-pandemic high in July 2018, as sellers are getting more motivated to sell their homes. Lower the price, and they will come (data via realtor.com):

Days on the market lengthened: Homes spent 46 days on the market in August before they were either sold or pulled off the market, up from 41 days in August 2022, according to data from realtor.com.

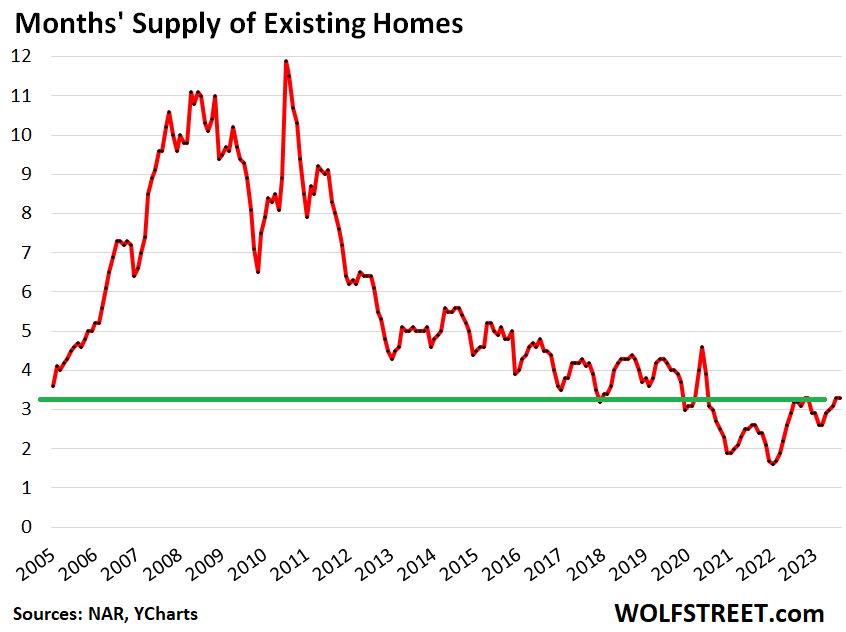

Supply remained at 3.3 months, matching the highs in 2022 (October and November) and beyond that, the most supply since June 2020, according to NAR. Supply in 2017 through 2019 ranged between 3.0 and 4.3 months (historic data via YCharts).

Inventory for sale dipped to 1.1 million homes in August, from 1.11 million in July. But wait…

Inventories have been declining ever since 2007. The reason is how technological innovation in RE has hit “inventory” the way inventory is defined: A home enters inventory when it is initially listed for sale in the MLS, and it exits inventory when the sale closes or when the home is pulled off the market. The time it takes to do all the processes from marketing the home to getting a mortgage approved, shuffling documents around, and closing the sale determine how long a home sits in “inventory.” Technology has dramatically shrunk the time it takes to do all this, and so homes spent less time in inventory waiting for these processes to happen, and because each home spent less time in inventory, overall inventory drops. So inventory shrank year after year for 15 years because the processes sped up. This is a crucial concept; my detailed discussion is here.

Active listings rose in August from July, to 669,173 homes and were down 7.8% year-over-year. The same technological changes, but to a lesser extent, also speed up processes and thereby reduce the amount of time a home spends in the active listings (data via realtor.com):

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The cure for high interest rates… lower prices. Funny how the financial twits over at Twitter keep forgetting that half of the equation.

What do we say to higher rates?

Not today! ;)

Fascinating. I’m the rare CFP/ financial advisor that has steered clients away from home ownership for years now (most of my clients were in Southern California before the escaped… The equation is different and other places). I accurately predicted that we were going to freeze up. It was pretty obvious but for some reason a lot of people didn’t see it coming. Unfortunately, I think a lot of people are still way too positive on their future outlooks for equity appreciation.

Sounds like you have bad advice for years. Maybe now would not be a good time to buy but if they bought 2 years ago they would have doubled their money. The fact that you are proud that you steered them away from this is odd to me

Rare? Virtually all financial advisors don’t recommend real estate because there is no compensation structure when their clients put their money in real estate. That’s like a realtor telling their clients don’t buy a home, put your money into life insurance and stocks.

This forum is high quality. Thanks guys. I might come back 😎

Does the inventory being listed for a shorter time result in sellers not reducing as much as they would, believing that there are not as many homes for sale in their neighborhood?

Interesting questions. Price cuts as a % of active listings are very high right now. So that seems to answer your question with a “no.” But I don’t have data on price cuts that go back past 2016.

Sellers are reducing their prices, but for the most part not by nearly enough and not fast enough. As a result, the houses aren’t selling.

Until we have some huge event that causes a multitude of property owners to put their houses for sale, this market is not going down any time soon.

Real estate is one of my businesses, so I’m not making this up.

Real estate moves at snail’s pace.

Current prices, albeit bit down are absolutely insane.

It has now where to go but down but it’d take time.

We also don’t want a sudden crash. We want orderly down in price like what is happening in stock market.

Good to see all assets are going down slowly and surely.

Value or quality Housing for families non existent. Housing for investment/ short term rental, newly minted pension recipients still intact but flatlining. And alongside .gov coordinated investment inflated housing is .gov corrupt developer programs. Artificial inflate housing, regulate construction (also inflationary), destroy supply, then dictate development. The snake has eaten itself multiple times, your looking at $8-9k in framing material for a 1000 sqft family ranch valued at $500k in woke-ville merica and the labor comes from another country but then .gov wants $30k in insulation to save the climate on someone 2nd or 3rd home. The rivers are filled with foam and .gov screams more foam in the housing, double the foam and fiberglass insulation. You can’t make it up

we dont need a huge event, we just need time.

unlike 2008, when we had loans that caused people to default which pushed tons of foreclosures into the market, we have a frozen market. what gets owners to sell in a frozen market? the belief that the price of their home will decline, not rise in the future. what convinces them of that? a sustained decline.

it is like the boiling water and the frog. a slow decline in prices will not get many to jump, but the longer the prices decline, the more inventory will come out.

in a typical market that extra inventory at lower prices will find buyers, but we have a pretty serious buyers strike right now. a good recession will help bring prices down

I get Zillow emailed notices of every single family home in my market, including price drops. For the past several months I have been getting a lot of price drop emails. The problem? Every single price drop that has come through my mailbox has been by $1 to game the system and “bump” the property back into people’s attention spans. I have not seen a single legitimate price drop. Note I am in a small Northern New England market that has increasingly (and bafflingly, at least to me) become a retirement home masquerading as a town.

What a lot of folks are overlooking is that prices will not go down if wages increase a significant amount to make up the difference.

If wages rise 20% that’s 20% that assets (like housing) will not reduce.

If you’re on a fixed income this is how you get screwed.

Housing costs relative to income are at absolute all time highs, and incomes have no chance of keeping up without inflation. Something’s gonna give.

As a parallel to this, I think what is also skewing the market/specs is the high number of phishing attempts. While every dump priced at $425k or less in my town goes almost immediately (and anything good above a million also goes immediately), we have a crazy number of absolute audacious listings from shysters trying to unload their gross rentals in the worst parts of town and trying to ask near a $M. Those sit on the market for a super long time until they get real or give up. I think this is making the time to sale look longer when it’s actually not.

DiggerDave, I have an active RE account still alive since before I bought my current house. They are no longer bumping price decreases to the top of the list, likely because of what you said. It’s a never ending game of trying to not be played.

I see a lot of homeowner complacency on the ground. I just investigated a home in a Seattle suburb. Owner bought it for $800k several years ago, probably got low-rate financing, and tried to sell it for $1.6M this summer. No luck. Now the home is being offered for rent for $4,900/month, with no takers so far.

The obvious question is, assuming the person doesn’t need the home, why not just reduce the price and sell it for, say, $1.3M. At that sales price, you could put the money in other safe investments and earn an easy 5%, or $65,000 a year. As a rental, even if $4,900/mo is realistic, you aren’t going to generate more than $20,000 profit, even considering a low-rate mortgage on the owner’s $800k purchase price.

Homeowners seem to be thinking there is going to be continued massive price appreciation ahead, which is a pretty shaky assumption in a market that is trending down after a LONG uptrend. They are forgoing easy money in the bank, today, for a slim chance at continued home price appreciation.

I bet this guy just doesn’t want to “lose” $300k. Someone set a price expectation of $1.6m and he can’t shake it.

I have been buying and selling both cars and real estate for almost 40 years and it is very hard to get anyone to sell a home or car for less than they think it is “worth”. It is even harder to get anyone to sell if they need to write a check at close. I used to go to a “flippers in trouble” site and the lowest most list prices got was “loan balance + cost of sale” since for some reason most people would rather ruin their credit with a foreclosure than bring a check for even $1K to escrow.

P.S. I’m guessing that someone is going to start a “STR investors in trouble” site soon since with the government “Covid cash” drying up and student loans starting again things are slowing down in the STR world…

This makes PERFECT sense to me — in line with the neuroeconomic discovery that pain of loss outweighs joy of gain by 2:1. (Is this an example of the cognitive bias called anchoring?)

I wonder if there are similarities with pricing on finished goods? Manufacturers are usually happy to raise prices when input costs go up; are they equally loathe to lower prices when input costs decline? (Honest question, I really don’t know.)

“are they equally loathe to lower prices when input costs decline?”

In consumer electronics, the tactic is to keep the MSRP at the higher level, but perpetully have the product “on sale” with some fixed discount.

Apt. – …still trying to square this discovery with the seemingly-timeless mass-appeal of casinos (…and now, online gambling…)…

may we all find a better day.

…and lotteries… (AI editor/palsied fingers strike again…).

may we all find a better day.

How does the pain of job loss compare to the pain of real estate loss? 🤔

Cause there are plenty of greedy c**t out there, this seller fits the profile.

IF and a big IF this type takes a bath, I have plenty of crocodile tears on reserve for them. Like you said, profit from $1.3 or $1.0M and be done with it but nope, these people are entitled to a point to think they deserve to make double in a couple of years on an asset that typically through 100 years of history appreciate at roughly 3% a year…

And someone doesn’t “deserve” to buy it for a lower price. It’s interesting to see the vitriol over this issue.

Maybe the seller has decided to test the market or maybe the seller is a bad businessman…but it is just business, nothing personal.

I think the vitriol comes from the fact that the Fed juiced home prices at the expense of those that were not yet in a position to be homeowners.

Fair point it is just business for the individual, but these massive “gains” are made at the expense of the non-asset owning class, raising the barrier to entry.

Actually, people do “deserve” to buy things at a price that is what the market would be absent government interference.

Anyone trying to buy a house today either wasn’t the age or in a position to buy it 3-4 years ago, before the Fed nonsense. To say that they “deserve” to have to buy double, and people who were lucky enough to already own “deserve” to make a profit of double is an odd way of looking at the world.

If it were up to me as a regulator/lawmaker, I would retroactively adjust everyone’s 3% mortgage to 6% and let the chips then adjust as they would.

“but it is just business, nothing personal.”

20 years of ZIRP (which powered this stupidity/greed) was pretty damn personal for anyone on the planet who had USD savings.

“If it were up to me as a regulator/lawmaker, I would retroactively adjust everyone’s 3% mortgage to 6% and let the chips then adjust as they would.”

And how exactly would you accomplish that Einhal? By dictatorial fiat? By violating the commerce clause and suspending constitutional rights? By staging a bloody coup?

We’re used to some amount of idiocy from you, but it’s nice to know in keeping with these inflationary times, we can always count on your conspiracies and BS to keep pace.

It wouldn’t be the Commerce Clause, it would be the Contracts Clause, if anything. But at this point, the political left is so used to violating the Constitution to get its goals achieved, that I would do the same.

Yeah, people REALLY do conflate price with value. Maybe they’re thinking at a subconscious level, “Surely SOMEONE will take this off my hands — cause there’s NO WAY I could possibly be the greater fool…”

George – one of the wisest observations I’ve ever read, here (…and, reprising the words of the immortal Firesign Theater: “we’re all Bozos on this bus”…).

may we all find a better day.

Greater fools approach to markets

Because everyone thinks once inflation is licked and ZIRP returns the house will once again be gaining 50k a year in value and 200k a year the next time the fed helicopter dumps money into the economy, so in maybe 10 years.

Hesh,

Right now, there isn’t necessarily alot of safe investments. The stock market could fall quite alot at any time. Bonds currently issued, likely will fall behind inflation. And many people are worried if bonds will indeed be repaid.

Even if that house falls in value, it will still possibly stay ahead of most forms of investments.

There is also the possibility that if high inflation does hit/stay for awhile, it will to a great extent, effectively erode the liability of the mortgage (in real terms the size of the mortgage falls rapidly). If over the next 10 years, say inflation causes prices to rise 2.5x; that house might be worth 3 million, which in real terms is less than it is currently worth, but the mortgage price will stay the same, minus the part he paid off over those 10 years, so he comes out ahead by quite alot. Plus he makes rent money in the meantime (which will probably, be better able to track inflation).

If inflation goes stays high or goes up, mortgage rates stay high or higher, and home prices drop, or stagnate at best. I’d take the easy 5-6% for the next five years, plus the opportunity to redeploy the cash in stocks or housing if things really crash.

If there truly are not good long-term investments, then take the 5-6% short term. You know it goes in your pocket, and you can’t lose.

Wisely said. Nobody that owns real estate should ignore the Sword of Damocles known as the expected MASSIVE (i.e. inflation “adjusted”) INCREASE in Property Taxes now being formulated by the bean counters in almost evey single state in the USA. That INCREASE will make every greedball and his dog wish he/she/it/we/they had sold when they had a chance to sell without a LOSS (i.e. breakeven), never mind a “profit”.

Eventually the high inflation period ends (hopefully), which allows the home prices to recover.

One of my concerns is that if the stock market crashes, there seems to be alot of nonsense occurring in the background, which might allow the bigger guys to offload before the smaller guys, meaning that by the time most smart people know it going to crash, you will have already lost most of your investment.

The main concern I have with the hold the cash route, is that in a severe enough recession, is if the banks collapse. Everyone is dependent on the FDIC to bail them out. There is the cap on that as well, the FDIC was previously tapped to bail out silicon bank and can’t really keep up with any major crash. I think the federal government will step in to bail out the banks savings and checking accounts, but it will be slow for the smaller guys, taking months to over a year plus, depending on the amounts before they are made whole, meanwhile, them doing this will cause a substantial drop in value for the dollar. The bigger guys will get their money quickly.

Basically, I think this time around the game will be rigged in various ways that allow the bigger guys to make all their moves first.

It is certainly possible to get the 5 to 6% annual returns, beat the crash and buy at the bottom, but it not a safe bet by any means. For most people, if they have any confidence in their local economy, sticking with the housing is probably safer.

True. And let us not forget the expected MASSIVE (i.e. inflation “adjusted”) INCREASE in Property Taxes that will make every greedball and his dog wish he/she/it/we/they had sold when they had a chance to sell without a LOSS (i.e. breakeven), never mind a “profit”.

The decision seems to me to be more complicated when a person has locked in a 2.6% mortgage, that is seriously cheap debt. Barring something cataclysmic, prices will recover. Its just a matter of when. Same goes for every other investment.

@Chs:

For home prices that cataclysm has already happened: High inflation, High rates => low affordability => lower price.

Unless, rates go back to zero, or everyone becomes millionaire, home prices should go down.

If you look at the bigger picture, it’s simple math but people with vested interest can’t see this.

Also, a different decision for investors vs someone who bought the home to live in.

Even after hiking my prop taxes 10% last year, my monthly PITI is still less than the rent at any apartment I’ve ever lived in.

Nah. Do the math. Real estate over the long term appreciates at 2 – 4%. Fact. Check it. If your interest rate over 30 years averages 3% (not likely but doesn’t matter for this calculation) then you’re basic paying for every dollar of appreciation. Notice that I left out maintenance costs, property taxes, etc. There’s a reason why banks stay on the lending side instead of the purchasing side of the equation. People are gullible and have bought into an idea that doesn’t work if you actually work out the numbers long term. In my financial planning world we basically concede that it’s still a good idea to be a homeowner but only because it’s form of forced savings for the American population that is typically very bad at saving.

When did housing become a money making scheme? Has it always been like this? Was there ever a time when a house was just a home?

Most of the home owners live in a bubble where home prices never go down when given enough time.

I am not surprised at this home owner.

In So Cal, real estate is religion and people think home prices can never go down.

This time is more precarious because of STRs and millions of SFRs are owned by big corps. I read stories that these big corps are selling their homes as with current rates, they make more money in interest than being a landlord/renting out.

Smart money would quit the market soon. Common Joe would be the bag holders as it always happen.

I have a friend who hold large chunk of Nvidia stock, hinted him to sell at at least 50% when it was trading at $490. He didn’t sell any as he didn’t want to pay taxes :-).

I know a guy who bought a 900K home for cash last month and is trying to rent out for 4K/month. His property tax and HOA fee alone is $1.2K/month.

“In So Cal, real estate is religion and people think home prices can never go down”

Ain’t that the true, especially when you talk to anyone from South OC, especially in Irvine..

This article of faith isn’t totally irrational given the fact that the federal government usually does everything within its power to prevent house prices from falling (e.g., substituting 40-year mortgages for 30-year mortgages; putting restrictions on foreclosures; lowering lending standards; granting tax credits for first-time suckers).

there is a simple reason homeowners have come to believe that home prices always go up – because they have. and the reason is pretty simple – a 30 year bull bond market, which is now gone.

the marginal owners, those that need to move or have multiple homes, should sell as soon as they can. once inventories build, price decreases will gain momentum. declining prices will not bring many buyers at these interest rates.

timber, watch out below

I’d argue the bond bull market has been 40yrs – 1981 – 2021.

“bond bull market”

Er, I think for the sake of the peanut gallery, we should call things by their proper name.

Corp debt (bonds) didn’t become safer/higher yielding over 40 years (of huge increases in absolute debt levels).

All that happened was that our extremely dubious G printed money, bought its own debt at uneconomically low rates, and therefore drove all interest rates down…which had the effect of increasing the value of earlier issued, higher yielding debt (the fabled “bull”).

Absolutely none of this was a sign of economic health…it was entirely rooted in real economic decay, papered over by money supply manipulation/interest rate destruction by the G (see long overdue inflation).

Terms like “bull market in bonds” (as cause of housing appreciation/inflation) simply confuse the hell out of people trying to figure things out (like why the hell rising bond prices have anything to do with home values…).

This example just goes to show how much people’s labour has been devalued. A huge pay cut has taken place (again).

800k profit (or 700k if he cuts). Well over ten times the median wage.

They can create fiat any time they want to steal from us.

Same game being played in Bend. A lot of buyers from 2020-2022 trying to sell, then trying to rent.

Well yeah that’s the hope of 90% of people addicted to spending. They just tune into Powell in hopes he will drop the rates and then it’s back to the races.

But prudent people would think more of the same would just flame up inflation again, albeit it in a few years.

So these people buying properties and betting on them going higher just want the rates dropped. Cuz they profit on the turn. It annoys the s*** outta me that it actually works sometimes.

Unless/until prices start coming down meaningfully, most of these sellers are holding out hope that we get rate relief in the not-distant future and that this reinvigorates demand so as to support recent prices.

And even if you think near-term rate relief isn’t likely, the general premise behind this thinking isn’t irrational. With prices staying more or less flat, is it worth holding out hope on say a 20% chance of rates being cut vs. taking a $100k price cut? Probably so for most who don’t face an urgent need to sell. (I personally disagree, because I think the risk of getting caught in a race to the exits isn’t worth it, but I’m also not in their position so hard for me to say exactly what I’d do.)

The problem with this thinking is that it doesn’t account for the macro conditions that would most likely trigger, and therefore accompany, rate cuts. These recessionary conditions will also hurt demand, thus offsetting the demand increase the rate cuts by themselves would have brought.

But maybe they’re holding out hope for the “soft landing,” where we can get 250-300 bps of rate relief without going into recession because inflation just quietly goes away. In that scenario, maybe they do actually win by holding on.

I suspect cash buyers (individuals) are waiting on the sidelines for a more substantial drop in prices, meanwhile getting 5.5% APY on their cash. The question is do I want to buy a $400,000 house now, knowing the odds are extremely high that it will be worth less in a year or more. Or do I want to get $22,000 in interest on Treasuries for one year instead. If the price remains the same, in one year I will be able to buy the $400,000 house (which will likely be selling for less) and have $22,000 to goof around with. For simplicity, I leave tax stuff out of this.

I do not know what corporate house buyers are doing. I suspect they have backed off to.

There comes a point in time when housing price bubbles burst, and we are in an all time housing price bubble. Air is coming out of the bubble, but it has not popped. We have seen it in the past. Throw in the likely collapse of the Airbnb market and we are set up for a substantial drop.

That is my position, being real estate-free at the moment. I still don’t like paying rent even from interest but nothing is perfect in such a messed up situation.

Anecdotally, in the commuter towns to ski resorts I watch, prices are still sticky but inventory is way up due to less moving and more new listings over the last month, something I thought was very strange at this time of year. Some are very obvious flips. Maybe some are returning to the metro office?

A lot of people ‘city’ folk bought rural, on remote employment or retirement plus other ‘pandemic’ pressures. But now live next to ‘undesirable’ renters in quiet towns that are trending down in quality of life but getting busier from inhabitants and diversity (financial, social, etc) perspectives. It’s like media propaganda come to reality and it in many cases will either be short term (resell if you can) or end in disaster with destroyed relationships, families and communities being the ultimate victims of trillions of dollars of pandemic crisis stimulus.

Any houses for rent around me are not updated at all. They are big but the interiors are 30-40 years old.

I would never want to spend even a year in them. People relocate and want nice new house insides to live in.

Whoever owns these run down McMansions prob are just trying to turn a quick buck.

On top of foregoing investment interest, potential and to top-tick prices, most costs associated with ownership (taxes, insurance, upkeep of almost any kind, etc.) have risen substantially and seem likely to continue rising.

Unknown ongoing cost might keep the marginal or opportunistic cash buyer on the sidelines for a while, too.

If the RE tax bill goes up, say $2,000 this year, you have to consider it the start of an annuity paid by the homeowner, because future RE tax bills will include that increase. In present value terms, that’s a $20,000 economic loss to the homeowner.

Then the following year’s RE tax increase starts an additional annuity, and so on. Ouch.

“I suspect cash buyers (individuals) are waiting on the sidelines for a more substantial drop in prices, meanwhile getting 5.5% APY on their cash.”

Yep!

The smart cash is waiting & the time to borrow way below inflation is over.

5%+ risk free vs risky overpriced houses with taxes/maintenance & insurance.

That’s a no brainer.

Only people buying now actually want to live in it. Almost like they way it’s supposed to be.

My wife and I are full cash buyers, but we’re 50%+ down payment buyers, and we’re doing exactly what you described. (No state income tax on short-term t-bill interest is also a nice cherry on top.)

The risk of home prices running up further on us under these conditions seems small, and much less than the risk of home prices going down on us if we were to buy. We intend to own what we buy for a long time and live in CA so Prop 13 only amplifies this risk: the price we pay now will “lock-in” our property tax assessment, and thus every extra dollar we pay in purchase price is an extra 1.25% in property tax that we’ll pay on this thing, every year, for hopefully the next 40+ years.

We’re not particularly rate-sensitive, but we’re very price-sensitive, and the risk/reward calculus right now keeps us firmly on the sidelines, even in a part of the country where very few new single-family homes are being, or can be, built.

aren’t* full cash buyers, dang it.

New housing under construction 5+ units : 995K slightly below 997K

in July 2023.

Commercial loans to office buildings in SF and NYC are in trouble,

but commercial loans in non-union states : industrial, multi rentals and

office buildings are not. Regional banks in the south are not equal to

the ones in SF.

Office and retail are in trouble in ALL states. And multifamily is starting to be in trouble. This has to do with interest rates having doubled. In addition, office CRE has problems with huge availability everywhere. And retail CRE has been a basket case since 2017.

Bed bath and beyond is killing it on some quantum galaxy level, signs still up, lights always on but not a product or customer to be found. I’ve never imagined a business could be ran like that for decades, but there still doing it year after year.

You would think some hot shot new bank, real estate office or urgent care facilities would be able to fill the space for the past 20 years. Someone with a ‘direct’ fed line but ‘no’ they’re busy filling all the other empty spaces or developing some new multi million dollar development across the way

MCW – (like your handle, btw), go back aways and review Wolf’s observations on ‘MatressFirm’ for extra credit…

may we all find a better day.

LOL, I already forgot all about them. Here they are:

https://wolfstreet.com/tag/mattress-firm/

“And multifamily is starting to be in trouble.”

Can you expand upon that? It’s a fairly opaque market, not a lot of info out there. I know it’s fairly illiquid now.

I’ve posted a few things on it. The issue are the rates. Occupancy is ok. But loans that mature now and variable rate loans are becoming toast. Cap rates have surged, so it’s hard to sell these defaulted properties

The owners of multi-family buildings do not generally take out 30 year mortgages. Over the past 3 decades, why would they? They could always get better rates going shorter and building prices always went up. So now many of those shorter loans are coming due, or will be coming due in the next few years, and mortgage rates are high and are not coming down. Furthermore, building prices are no longer doubling ever couple of years and are actually slightly declining.

This means the owners that were aggressive and barely put up any equity arr now facing huge financing increases (on an asset that is declining in price).

Here’s a prediction: in the coming recession, the government will force RTO under the threat of job losses. Fixes housing market, no more WFH, fixes CRE, fixes cities, helps the job market, stimulates commute spending. What’s not to love about it?

Well,there’s the cost to the environment of increased CO2 being put into the air due to those workers being forced to drive back into the city office buildings, not to mention the lost productivity due to the stress those workers now have to endure again. Don’t believe all the stuff they say on CNBC and Fox Business about WFH being less productive. Those memes are being driven by the CEO’S and not the workers.

So from chart one it’s hilarious that there basically was little to no seasonal price decline from 2021 through mid 2022. And annual appreciation was easily 2X what it was the few year before.

Housing is completely out of whack. The only cure is a real recession. I think the Fed would like to see a 10% national price decline and possibly even up to 15%. But I just don’t see that on the near-term horizon.

The economy has a lot more rolling over to do before that even becomes a possibility.

‘The only cure is a real recession. I think the Fed would like to see a 10% national price decline and possibly even up to 15%.’

Agree. That’s why all this ‘soft landing’ talk doesn’t make sense. To quote JP: ‘house prices must come down so Americans can afford houses’

With housing being such a huge part of the economy, worse in Canada, asking for a big housing correction without a recession is like wanting rain on the crops but not on the parade.

“With housing being such a huge part of the economy, worse in Canada, asking for a big housing correction without a recession is like wanting rain on the crops but not on the parade.”

Exactly right.

As to the price declines in real estate the Fed would like to see, they are in for a large dose of self imposed pain. I say that because it was the Fed’s golden boy Greenspan who gamed the CPI so that HOUSE (i.e. “shelter”) sales prices skyrocketing UP would barely make it budge upwards. SO, for the last 25 years or so, the Fed has been happy as clams with their “wealth effect” BLS CPI “math” fun and games. Looky here, folks, our infaltion target of 2% is “well in hand”. “Nothing to see here, move along and enjoy the wealth effect”.

In total contrast to the Fed’s quarter century long reality based math challenged CPI party, the present plate of CROW the Fed has been SERVED is that, as prices of “shelter” TANK, the CPI will ALSO BARELY BUDGE down.

Oh, the irony of JP wanting the opposite of Greenspan’s “wealth effect”.

Yes but will the “come down” be just enough so you have to claw together all your finances and struggle to make the mortgage?

Just to get into the equity paradise.

You know who you are… sipping your coffee looking all smug. “Wasting away in Equity Paradiseville” lol

…wha? This is coffee?!?

may we all find a better day.

“That’s why all this ‘soft landing’ talk doesn’t make sense. To quote JP: ‘house prices must come down so Americans can afford houses’”

Many are missing the bigger point/problem here. Home prices are set by the market, which is basically the intersection of buyers’ willingness and ability to pay. If prices fall, it’s because either willingness or ability has declined. It’s not like a drop in home prices would make it more “affordable”, because the very buyers would now be less able/willing to buy. By definition.

YOU CANNOT FIX THIS with policy or rates. A mindset has to change. Buyers need to stop being so desperate to stretch themselves so much for a damn house. That’s the willingness part. Good luck, because I have been pissed about the American buyer’s willingness to push so hard, making prices always feel too high for me. I think the willingness component is mostly a constant, and so prices are driven by ability to pay.

And for those still wishing for a housing crash after reading the above, ask yourself who will really be buying if a crash happens. Those with cash ready to risk on the sidelines…investors and corps.

There seems to be a psychological element at play here.

So at a lot of jobs the corporation demands you be more productive.

In the 80’s and 90’s they would have told the corps to go pound sand.

But now the corps have immense power and can intimidate their workers, with little government relief.

This type of psychology may be playing out in real estate. The “powers that be” could be creating a landscape where one is seduced into working more for the same property. The person in the 80’s and 90’s would tell them to go pound sand.

Another scary element, slightly unrelated, is how hard we push our college students. The state school near me NC State, has had countless suicides. Does the dean do anything? Not really. “Just keep paying your tuition kids”.

It’s a weird reality we’re in

sufferin’ – the transition of the degree from one of demonstrating self-improvement in thought and knowledge about the world to one of merely purchasing a tarnished glitzy object complete with fine-print warranty disclaimer appears to be near-complete…

(…man, am I having a tussle with the AI/fingers today!).

may we all find a better day.

It works both ways. Housing can come down slightly and inflation can push workers wages higher.

In the last 3 years home prices have increased by 60% or more. This piddly 15% decline won’t do anything to affordability.

It takes a 37.5% decline to reverse a 60% rise. A 15% fall will get you 40% of the way there…

A 50% decline will reduce a 100% increase to zero change. People often fail to understand basic math. “My million dollar house increased 400%, but then declined 100%. It is now worth zero dollars. Oh sh*t.”

Actually, several years with high inflation as measured by CPI and stagnant housing prices will bring down the real estate price as well. Not the sticker price, but relative wages and other expenses.

CPI “inflation” and asset price stagnaition realign prices slow, where a crash do it quick. That way inflation may even be called the soft landing.

Wolf: Thanks for the great info, do you have the ability to get Median sold price “per square foot”? Every time that market cools the “mix” of homes that sell changes and it is nice to see price per foot data.

With the 10 year Treasuries climbing to 5% look for the mortgage rates to run up to over 8% making housing completely unaffordable for all those who have not entered the housing market (1st time home buyers). They will all be forced into the rental market which will see double digit inflation rates. This is what irresponsible Federal Spending and incompetent Federal reserve policies has brought the next generation. And now we expect the same clowns to fix the mess that they created. Not going to happen. No one can fix this at this point. The least bad option is to push up interest rates until the inflation is broken and housing industry collapses, like in 2008/2009 and then pick up the pieces after that.

I’d imagine if Volcker were alive today he’d be saying just that. It’s pretty much necessary at this point to push the economy into a deep freeze for a good 12-18 months and let some inflationary dynamics shift back to reality.

Don’t be so sure about a increase in the rental market. It is also dropping from what I’m seeing. The economy is beginning to thaw.

Incorrect. Rents are increasing across nearly every market.

Do you have any evidence to support that assertion? My experience in 3 different markets say otherwise.

All the major publicly landlords are reporting that they’re getting rent increases in the 6% range both on renewals and new lease signings.

Also check this out:

Or let inflation as measured by CPI and vages run hot for an extended period while asset prices are keept stagnant. If wages and consumables doubles the next ten years with assets staying in price housing do come more affordable. Even at high interest rates.

Interest rates high enough to supress asset prices without causing a crash or stop inflation will, rather slow, bring housing price down. It just do not show in the sticker price.

Sams, see my point above. In your scenario, home prices would rise along with those wages.

There is a very, very, very simple and fair solution to fix the housing affordability crisis.

The Federal government should create a new graduated scale tax on unrealized gains for all homes that are not a primary residence.

Think about this.

A ton of properties would come on the market very rapidly and prices would fall dramatically. It wouldnt apply to anyone actually living in a home or increase their property taxes one iota. It wouldnt hit any investor that has not seen their wealth expand greatly.

The government could use this money to decrease the runaway deficit.

I actually think that the biggest problem with our tax system is the unequal treatment of long term capital gains and the lack of taxes on unrealized gains. Warren Buffet has literally made billions on the stock of companies like Coke that he has owned forever and has never paid a dime of taxes. This is what keeps his tax rate so low.

A small tax on unrealized gains would also potentially stop rewarding people for just sitting on investments, including homes, and instead actively look to move capital into the most productive returns. This would disincentize non-productive investment.

I also think that a wealth tax of 1% on anyone with more than say $10 million dollars would be a good idea. If the government is going to take 1% on your wealth it increases your incentive to get a higher return, which is probably going to stimulate the economy.

An investor who owns and rents out a home gets alot of tax advantages. But is this the type of activity we want to incentivize? Simply buying a home and renting it is not a huge value-add to the economy. It doesnt create jobs or create more housing or create new technology development. It is the type of investing that we should dis-incentivize.

Taxing unrealized gains is a slippery slope. What about deductions for unrealized losses? Anyway, a significant tax on any purchaser who does not fully occupy his house for the ensuing year would put a dent in corporate buying. The tax would decrease somewhat for the second year, and so on for the following years. It would also ruffle the feathers of petty landlords and airbnb types.

Taxing unrealized gains is slippery “cliff” when it comes to property taxes, which are calculated yearly on “unrealized gains”. I have a neighbor who 12 years ago was paying $8,000 property taxes, and today they are paying $44,000 the same exact house, with no improvements, that is now 12 years older?!? I feel “lucky” that mine has “only” gone up 3x, versus 5x like my neighbor…HA

Property taxes based on unrealized gains have the effect of pushing the natives out of their homes, which is cruel to say the least as shelter is basically like food, energy, and water—>necessities for human existence on planet Earth..

As far as the current housing market, there is a chance we get a spike in prices in early 2025 “IF” a team red wins 2024 elections, and the new Pres bully pulpits rates down, as was promised last week on “X”. Mortgages at 5.75 to 6.25% from a 8.0 to 8.75% peak rate would have buyers flooding back into the market who are sitting on the sidelines with FOMO and kicking themselves for not predicting an impossible to predict housing market by buying in 2020/2021.

Other than that short window of “possibility”, I’m not sure how housing is going to rise back to former bubble territory, unless inflation stays high for the next decade and pushes housing prices up with the price of everything else.

“ we get a spike in prices in early 2025 “IF” a team red wins 2024 elections, and the new Pres bully pulpits rates down”

Strange how red is the new blue.

Wealth tax on unrealized gains is clearly unconstitutional. And remember, original income tax was only 1% rate applied to only 3,000 taxpayers. A wealth tax would start the same way and end up applying to half of the population.

California’s recent Prop 19 (funded by Realtors) ended the ability for parents to pass their low property tax basis vacation homes on to their kids (under Prop 13 CA property tax can not go up more than 2% a year). In the early 60’s you could by nice waterfront homes in Stinson Beach or Lake Tahoe for under $50K that are worth over $10 million today. Before Prop 19 the “kids” usually pushing 60 when their parents pushing 90 died would keep the homes since the vacation home property tax was just a couple grand a year (and it was easy to cover that with a few off the books short term rentals to friends), but now after Prop 19 the taxes will go up to over 1% of the “current value” or over $100K on a $10mm waterfront vacation home forcing most (that did not plan ahead with a LLC) to sell.

“but now after Prop 19 the taxes will go up to over 1% of the “current value” or over $100K on a $10mm waterfront vacation home forcing most (that did not plan ahead with a LLC) to sell”

So now only the super wealthy can afford to own property…not sure that’s exactly mission accomplished.

“So now only the super wealthy can afford to own property…not sure that’s exactly mission accomplished.”

No – it means only the super wealthy can afford to own $10mm properties, which… kinda makes sense.

Maybe if a bunch of these $10mm waterfront properties hit the market, they’ll start selling for <$10mm. That's the point.

They won’t sell for $10 million if the supply is no longer artificially constrained as it was prior to the proposition.

This 2,200sf place on the Seadrift sandspit just sold for this summer for $13mm:

https://www.zillow.com/homedetails/214-Seadrift-Rd-Stinson-Beach-CA-94970/19307098_zpid/

In the last ten years I have done nothing but watch the “super rich” get “super richer”.

We have a multi-million dollar Tahoe “cabin” and actual “Billionaire” that own the place across the street but I still feel poor when I go to dinner at Martis Camp (a gated community for the “super richer”).

https://www.zillow.com/homedetails/8101-Villandry-Dr-Truckee-CA-96161/114451427_zpid/?

This is good. Ending Prop 13 entirely for properties that aren’t primary residents is the next step. There is zero justification for landlords, AirBNB investors, and vacation home owners not to pay property tax based on the full amount their homes are worth.

“I actually think that the biggest problem with our tax system is the unequal treatment of long term capital gains and the lack of taxes on unrealized gains.”

I assume you would also then support tax deductions for unrealized loses?

HA, like the realized loses on negative capital gains, in which losses are capped at $3,000/year versus the unlimited no-cap on positive capital gains.

Like wash sales, carried interest, partnerships, special trusts, etc…the casino is rigged for the upper class.

Yeah, and how about indexing capital gains for inflation so we don’t pay tax when assets are increasing less than the rate of inflation.

“A small tax on unrealized gains would also potentially stop rewarding people for just sitting on investments…. a wealth tax of 1% on anyone with more than say $10 million dollars would be a good idea.”

This would only benefit accountants. Taxes are too complex enough already – tax code should be one page long – not more complicated.

If we did this, capital gains would be more hellish than today to keep track of if unrealized gains were taxed.

And 1% wealth tax – really? This is asking for everyone to evaluate things that are often difficult to measure in dollar terms, e.g., houses, cars, art, jewelry, etc… Just look at Trump’s games when evaluating his property worth.

How about we ask everyone to pay 1% wealth tax. If you do not have much wealth the tax would not be too much. But let’s have everyone feel the pain at tax filing time going through this non-value add activity.

Geez, we need to put our societies wealth to better use being productive and not all simply become economy sucking accountants.

You obviously do not have much money and want to free load more on those who have made better decisions in life than you.

Not in my neighborhood…sorry just have to do it since I am in SoCal :)

But seriously, I know housing moving slower than Titanic but it sure doesn’t feel like it in OC/LA….sellers still constantly listing anything with a floor of $1M like it’s out of style and checking on some random saves that I have on Redfin and Zillow…some people are still buying…freaking ridiculous

$1M will probably continue to be a good floor for large parts of LA/OC. It will drop, but that doesn’t mean it will drop to zero.

San Diego here. I couldn’t believe it, but a few sales have set new records in the high end, $4m+ market, selling 10% over ask price. Inventory is still basically nil, but those few that listed a month or two ago obviously too high are still sitting. Weird.

Myself and others have gotten beaten down several times here for pointing out our anecdotal observations, but not so much anymore. All one has to do is go to redfin or Zillow and search actives, pending, but most importantly solds to see that what we’re observing is actually happening, and I’m not talking about just the coastal areas. This is happening in the older inner city neighborhoods as well as just about every part of the city. The most challenged areas and absolute junk locations within good areas aren’t seeing numbers like this, though, but basically it’s a gentrification opportunity for those areas and that’s exactly what’s happening.

Askings of over a mil are common in San Diego and solds of over asking are becoming a thing again.

It seems San Diego didn’t get the memo.

Upcoming most amazing housing bubbles will continue to surprise us is my guess.

This how bubbles work. Nothing strange at all. It just hasn’t popped yet. But it will. The one thing all sides seem to agree on is that prices are irrational. That’s why the bubble will pop.

Looking at the housing markets decline is like watching paint dry.

Ha!

I think it has to do with human nature/psychology. People easily accept their house has appreciated 40% in 2 years but won’t accept that it could fall the same amount. It causes a stickiness at housing highs that means a longer period of decline. It also seems like forever for people waiting for prices to fall.

Currently, most homeowners are well above water. The psychology reverses if houses fall enough that a significant number of houses are underwater. Then the foreclosures start and a fairly rapid plunge in house prices will likely occur causing further drops, causing more foreclosures.

I hope the Fed keeps price declines to a max of 20% (down payment and refi equity) to avoid this. The Fed may not care though since most mortgages are held by Fannie, Freddie, FHA, VA now and not by banks like in 2007.

I’m unfamiliar with this concept. How does a significant number of house market values falling below their loan balance owed increase the number of people who can’t make their mortgage payment?

Beautiful data as ever Wolf, thanks.

My brain would tell me, logically, if months supply of homes is high, there would be less pressure on buyers and more on sellers to lower prices, and yet the months supply was very high during Housing Bubble #1. Is that just a result of the glut of new construction at the time and the bubble having other causes that ignored the excess supply?

Herpderp I never pay much attention to “months of supply” since in most towns not many homes sell and a just half dozen homes listed, sold or taken off the market in a week can really change the “months of supply” number (below is a link to the SF Peninsula city of about 30K people where I own some property that has just averaged a couple home sales a month this year)

https://www.redfin.com/city/2350/CA/Burlingame/housing-market

New construction is a big driver of months of supply in growing areas but in mostly built out areas like the SF Peninsula months of supply is often higher when values are going up since Realtors will take an “overpriced” listing hoping the market values will increase enough to sell it before the listing expires. When values are going down like they are now the number of Realtors interested in putting an overpriced properly in the MLS is way less.

Wolf,

We know that prices are set at the margins. I saw somewhere that the last 20% of this ghastly real estate bubble was the pressures of boomers, recently retired, reaching for yield and being told to invest in STRs.

The AIRBNB lure was you could get a 1000 bux a night on the weekends…. Do you see inside your numbers the influence of these ‘cash buyers’, who in reality were liquidating another asset (stocks, 401ks) or levering themselves up to make this purchase?

OMG it’s not just one generation. Sick of the propaganda around boomers. There are many generations in STRs. There are many poor boomers who don’t even own their own homes. Quit with the Business Insider generation baiting garbage.

KurtZ,

Your boomer stuff is silly.

The biggest group of buyers by far are millennials and Gen-Zers. And that’s how it should be, they’re young and they’re starting out and they’re buying. And millennials are the biggest generation ever. Those are the people that are trampling on each other to outbid each other and they’re the ones driving up prices.

READ THIS:

https://wolfstreet.com/2023/07/25/younger-people-drove-the-increase-in-homeownership-rates-over-the-past-few-years-census/

MW: US stocks finish lower, Dow falls 370 points, S&P 500 drops third straight day as Treasury yields jump

Demystifying macro data well brings Peeping Toms. Appreciate the no frills style you bring here, Wolf.

That said, a thought: if the number of monthly homes sold has temporarily or permanently shrunk then the months’ supply of existing homes must be overstated by this amount too, no?

Or at the very least months’ supply of existing homes is not necessarily comparable to prior periods because of this (assuming the numerator and denominator went down by an equal amount), perhaps much like your thesis that supply of homes today is apples to oranges with data from 20 years ago given the speed with which homes are sold now v back then.

Waiting for someone refute Wolf and say: “But not in my neighborhood…”

But back in my neighborhood, I have been tracking homes (albeit over 1.5 million) with two 100k price cuts in just 60 days, and still no takers.

Mortgage rates will top 8% very soon. As someone mentioned on another site:

“if you purchase a $1 million house with a $200,000 down payment and get an $800,000 mortgage at a 7% interest rate, in the first three years you’ll be paying $193,000.”

But because of the high-interest rate, a significant portion of your payments would go toward interest, leaving a substantial amount still owed on the principal.

“After those $193,000 of payments your $800,000 mortgage is now at $774,500,” he said. “You paid $166,000 in interest, $25,500 in principal.”

P.S. My realtor still says there has never been a better time to buy.

In my neighborhood:

– In less than 2 weeks we had over 20 jobs come in for new construction.

– Existing home inventory? If there is a large group of youngsters needing a house….it will take awhile longer for that inventory to build.

A lot of rentals & b&b will hit the market when loan goes from 2.5 – 9%.

“P.S. My realtor still says there has never been a better time to buy.”

If there was ever a Realtor(TM) child’s toy, when you pull the string in it’s back, that’s what it would say.

The official NAR Realtor (R) toy would say “There has never been a better time to buy OR sell”

https://www.nar.realtor/logos-and-trademark-rules/the-realtor-logo

I am amazed that 99% of Realtors (R) can say that with a straight face but I’m pretty sure most don’t really understand that why it is not always a great time to buy or sell and like politicians just keep talking and saying they think sounds good in the hope of getting a commission.

Good one Dirty Work, and very true. Thanks for the laugh.

In my neighborhood, we just had a bidding war on an old tired 2BD/2BA home. Realtors told the seller they could never get more than low 3s, if that. Some realtors turned the listing down because the seller wanted high 3s. Too much they said. Home gets listed at $3.8M, and it gets hit with multiple offers. The people that recently sold their properties in the low 3s feel like fools.

Address: 406 Snug Harbor Road, Newport Beach, 92663.

Seeing this here in San Diego, too. Some overbids but mostly stuff that that’s getting close to asking price, and those asking prices are north of a mil now. A few years ago anything above a mil was the talk of the place, but it’s become very common. Even major fixers are going for 900k plus. My observations tend to be of housing south of the 8, so for any of you who know San Diego know how impressive these numbers are. North of the 8, and more so north of the 52 are seeing numbers much higher than I’m seeing. Things are still moving despite it being August.

I’m not a financial buff, but I owned a home long ago that lost money. Interest Amortization Tables have Remaining Balance Tables. I’m assuming these tables have not changed over the last few decades ?

For 8.00%, 15 year loan:

After 5 years: about 79% left on loan.

After 10 years: 47% left on loan.

The loan is half paid off about 9.5 years into the loan.

For 8.00%, 30 year loan:

After 10 years: about 88% left on loan.

After 20 years: 60% left on loan.

After 28 years: 16% left on loan.

The loan is half paid off about 22 and a half years into the loan.

It gets worse for 40 years. After 10 years one has only paid off just over 5% of the loan, after 20 years all of 17%. After 30 years one still has 57% of the loan to pay off.

Not sure realtors want buyers pondering this too much.

If you want housing prices to fall, then you drain reserves. That’s how Greenspan caused “Black Monday”.

About those three percenters. In the blue collar Boston suburb where I live suddenly there’s a huge number of 4-7 bedroom properties to rent. Condos, two level houses and two family houses. For years and years it was a rarity to find 3 bedroom 2 bathroom for rent!

My conclusion is that a bunch of people are trying to wait this out. Are they investors with multiple properties? People who had to move and now may have a 7% mortgage on a new property? Something else? I don’t know. But I think eventually they’ll all rush for the exit at the same time.

Yeah a place down from me started life as a rental at oh $1800 a month.

Now it is renting comfortably over $2900

These owners all over just want to cover their super low mortgages, while their equity builds up and then flip it later on.

Time for the NAR to get their lobbying operation in gear and get congress to pass the Cash for Casas legislation which would require that all mortgages would be fully assumable with 5% down.

No qualifying plus a new program of federal government guaranteed second mortgages to cover the difference between current mortgage balance and sales price.

With this fantastic new program folks sitting on low rates can sell and also assume loans on new homes of their dreams. And those folks waiting in the wings would be able to find an assumable at 3% with a second at subsidized rates to complete the purchase.

Call your congressperson today.

What do you think Lawrence?

Yeah, prices would increase and become just as unaffordable. Not a solution.

Housings spring recovery happened at the same time as the stock recovery rally. Any relation between housing and stock market? If stocks decline does that hurt housing?

In the tech-heavy markets of Seattle and SF, I would imagine that a lot of young FAANG programmers use their big vest of RSUs as a down payment.

Screw the stock market. Let’s flush out all the excess and dirty speculation and go back to the era of intelligent investing. The Fed has been rewarding speculators and dumb investors for more than a decade. It is time for a change.

Howdy Folks. YEP, a world gone Mad. No $ down home loans, No income verification loans, ZIRP, QE, Print $, and lets lock the world up. Don t worry, they know what they are doing….. Anything bad happens, just blame it on the other guy.

It is my opinion – correct or otherwise – that the residential real estate market is highly localized.

Anecdotally, for what it is worth, it seems the residential RE market here in DuPage county never zoomed up in price too much.

Friends I know who pay attention to such tell that prices have “stabilized”. They haven’t gone down too much, maybe a percent or two, from the local market top.

But just like everyone who goes to Vegas SAY they won enough to pay for their trip, I’m guessing sellers are SAYING their home sold for asking price in just a few weeks.

I do agree with all the comments above that most everyone thinks their homes are worth $X and stubbornly – greedily – refuse to budge on the number they have in mind.

Another great post and comment section Wolf!

I listed a small apartment building in August and closed last week. I listed at the price my agent’s market analysis indicated it was worth and had multiple offers the first week – all about 10% below list. I then told my agent I would be willing to carry a mortgage and had a full price offer that day. The offer was 25% down with an interest only 6% loan and a balloon payment for the balance in three years. My attorney vetted both the contract and the buyers and I went ahead and did the deal. I also consulted my accountant and was told they are seeing a lot of these deals now with interest rates around 6 – 7% because the banks are charging 8% for mortgages on residential investment properties. Fortunately I didn’t need all the money right away.

Wait, so you did a seller’s mortgage (providing financing to the buyer?

One metric that is useful to track is the price/rent ratio (similar to price/earnings ratio for stocks), i.e. house-price divided by annual rent. Think of it as the rental yield.

This tends to normalize for supply-demand variations since if prices were increasing rents would too.

For the Bay Area this ratio was historically around 20-25 (i.e. yield of about 4-5%). But over the last few years prices have increased much faster than rents. Now mean reversion seems to be setting in. While rents are still increasing, prices are falling faster bringing the ratios steadily back to historical norms.

Zillow now has median price data since 2000 but median rent data only since 2015. I ran a few calculations

1. San Francisco – in 2015 the ratio was 26, went upto 35 at peak of the covid boom. And is now back to 30 and still falling. Quite a few houses selling at their 2016-17 prices.

2. San Jose – was 23 in 2015. Went up to 36 and now back to 33.

3. Sunnyvale – was 34 in 2016, reached a peak of 47(!!) and now at 44.

Austin Texas where the price correction has been the sharpest – the ratio was 20 in 2015, went up to 27 and now is at 24. The news is that prices there are still falling.

It feels like a long way to go yet for the Bay Area. But note this is a ratio so prices can be flat and rents can catch up till the rental yield is healthier.

With higher inflation would expect ratio to be on the low end of historical norm, e.g., 5% yield).

Ratio of 25 or more (yield of 4% or less) makes sense in a low interest, low inflation environment.

Yes, prices haven’t fallen. But sales volume has been about 40% lower in much of the country for over a year now. Realtors, mortgage lenders, escrow, title, furniture, home depots, moving companies, etc… are all making 40% less income. There has to be some knock on effects that show up at some point from this very large industry in the USA (residential real estate), doing literally HALF the business now it had been doing for years.

I wonder how many realtors are now Uber drivers.

What a nightmare for those of us who take Ubers for business and either want to work, take calls or enjoy the silence.

RE agents are notoriously chatty and would be terrible rideshare drivers.

Things I have heard RE Agent Uber Driver say:

“It’s always a good time to start driving for Uber.”

“No matter where I drive the road just keeps going up.”

“Book me for a future ride, you can always sell your seat to someone else later and make a profit.”

“That’s not a sinkhole on the road, it’s just an itsy bitsy little gully.”

“You’re just throwing time away as a walker.”

“ There has to be some knock on effects that show up at some point from this very large industry in the USA (residential real estate), doing literally HALF the business now it had been doing for years.”

Maybe this is another reason why people have more money these days – no more throwing away money to realtors – people are keeping this cash to themselves.

Realtors suck up a lot of money that could go to better purposes.

I was expecting the housing market to correct to some levels (though still higher than prepandemic levels), but at this point, that seems like not the base scenario. Housing valuations settled at the crazy high levels, thanks to …. you guessed it : FED. They made many huge mistakes to make the housing unaffordable for possibly decades:

1) They started buying mortgage BS, without a real necessity in 2020.

2) When people flocked like crazy to open houses in 2021, buyers writing love letters to sellers, they still didn’t stop mortgage BS.

3) When they stopped QE, unlike treasury bonds, they still kept buying mortgage BS in crazy 2022 summer, to replace the ones that are rolling off.

4) March 2023 bank collapse could deflate the asset bubble completely. Instead of letting it burst, FED printed $300 billion almost overnight, and invented the ridiculous BTFP, which treats garbage bonds like gold. This prevented the credit tightening and caused the asset bubble become permanent. Almost all the asset prices (housing, stocks, bitcoin) went up like crazy after the invention of BFTP in March 2023. This was the final nail in the coffin.

Sorry Gen Z, you will have to live as a renter and with high inflation for a long time for ridiculous, irresponsible money printing.

Someone understands and is able to summarize the events and situation well.

Or current homeowners will be tasked to give up a portion of their gains, or maybe all of their gains, or more than their gains? Not unheard of. Very common in fact on a market by market basis. Not so common on a national basis, all at once.

Thanks for the comment Wolf. That’s certainly a possibility. Based on the fed actions in March 2023, my impression is that the fed will not allow a sharp decline in asset prices. And the markets seem they will not allow smooth corrections in asset prices. It is like make or break. And in my view, fed does not have the intention (or guts) to break the asset prices. On the other hand markets and consumers are extremely resistant to bending the asset prices. So there seems no middle solution. Somebody has to loose. And the poor is loosing and the asset holders are winning unfortunately. I hope I could be more optimistic but March 2023 changed my view. I hope i come out to be terribly wrong.

@Jason, in the words of our kind friend Klaus Schwab, “You will own nothing and be happy.”

In the major cities office CRE are mostly big bank assets. Most

commercial loans were issued by regional banks, that’s true, but the troubles, the cancer is in the big cities. The malls died a long time ago.

Multifamily construction might slow down, but they aren’t in trouble.

Rent is rising and the vacancy rate is low. Less multi ==> higher rent,

unless…

Is it possible the housing market is being buoyed by things like wash trading and money laundering?

Western countries are the prime destination of monies coming from ill gotten means.

Criminals of various sorts ( e.g. dictators, corrupt bureaucrats, politicians , biz men etc ) love to park their money in real estates in prime locations.

No, it is just reckless money printing with the speed of light and snail pace QT.

and people thought tulips at $5.00 were too expensive.

A home near me here in NC just sold today for 1.195 Million. It was built in 2016 for I think $560k ish.

Anybody want to analyze why they got so much more than they built it for?

Are these asset prices here to stay? Or is this just some risk takers with good jobs, maybe some out of staters flush with cash?

New asset prices are here to stay. The Fed increased the money supply by 40%, so prices will stay up 40%.

That money didn’t get spread equally nor did wage increases. My gut feeling is the people who made off with most of the cash are comfortable sitting on it until asset prices correct to where they should be.

There’s a lot of liquidity and a lot of stupid people but there’s not enough stupid people to keep these prices. There actually are some rational investors out there who have been paying close attention. Some of the biggest names like Buffet are sitting in billions upon billions of cash.

Agreed. There’s obviously much more to it, but when they printed so much money it all had to go somewhere. It’s not simply going to disappear. Essentially they devalued our dollar as they’ve been doing for decades now. The house is still the house just as the steak is still the steak and the gallon of gas is still just that. It’s all backed by a bunch of pieces of paper and when they print more it takes more to buy the same thing. Unfortunately, this time around, they didn’t even try to hide their money supply meddling and now we’re in this mess.

They had the cover of the pandemic this time.

No, no, no. Money diffuses. Some people can buy now at insane prices because the printed money is still somewhat concentrated. But as it gets spent on things like housing and other crap it gradually diffuses. The process is slow. But unless we have another round of printing housing prices will decline simply because there are fewer people with big wads of recently printed fiat. Eventually there will be eqilibration between income and prices, unless we relapse back into monetary insanity. The process is slow, and many are confused by the slow pace.

I guess I should also point out that diffusion may be poorly understood. But I think the fed understands it, particularly regarding the associated time scales. We’ll either have a trigger that causes a relatively rapid correction or a slow grinding correction. All the talk about STR could form a trigger, I suppose. At any rate, current prices are unsustainable unless QE resumes. The only question is the pace of the correction. Right now it is slow though it was more rapid before the recent bump. Seasonality makes it very hard to interpret data.

Look I’ve got brain horsepower equivalent to a ’74 Pinto but I thought the money supply doubled from the mid-late ’90’s (post-recession) to the RE Bubble 1 peak, yet nevertheless the SoCal RE market crashed and so did the stock market. I generally get how money supply can impact asset prices but i’m so confused as to how asset values would be permanently fixed at a certain percentage higher directly equivalent to the percentage increase in the money supply.

Would a would-be Hilton type put much of a down when buying garages with attached homes to flog on AirBnB?

I know this is an article about existing home sales but how does it effect New Home Builder’s? Builders can control their prices to some extent but don’t they also make their profit on the volume or churn as well? Less buyers for them too, right? Are new home sales trending downward? I noticed some of the larger builder stocks have eased slightly. Not sure if this is an adjustment or the start of a trend?

This will answer your questions:

Mortgage-Rate Buydowns by Homebuilders Are Now All the Rage to Prop Up Sales, Lowering Effective House Prices in a Big Way, but Don’t Get Picked Up by House Price Data. Appraisers have not yet caught on to it either.

https://wolfstreet.com/2023/09/10/mortgage-rate-buydowns-by-homebuilders-are-now-all-the-rage-to-prop-up-sales-lowering-effective-house-prices-in-a-big-way-but-dont-get-picked-up-by-house-price-data/

And here are sales, prices, and inventories of new houses. August data will come out next week:

Lennar Homes said they will offer customers 4.5% loans. They can do so because they are making more profit per home than in 2019. So they will buy down the interest rate. I guess you still pay full price.

Maybe if your a cash buyer you can ask for a price reduction?

They’re all cutting prices, building at lower price points, AND buying down mortgages. They’re doing all three.

See my chart just above of new house prices.

Then Builders are hurting. Lay off the stocks.

Does anyone have a sense of how homeowners insurers pulling out of California due to wildfires could impact the market?

They’re pulling out of Florida too, of course for hurricanes, not wildfires, but same principle.

My friend in Orlando told me last week that his HO insurance premium was $1500/yr a few years back and is now $6K/yr.

Holeyy Moley!

At what point do we all just invest 10k in CDs a year and then rebuild the house with however much is saved?

It probably doesn’t affect it that much because its a fairly small proportion of homes that are in wildfire prone areas. Anyone who has flown into LAX, SNA, SAN can see that most populated parts of the state are dense and fully urbanized. I pay less than 1000 a year for homeowners and earthquake insurance

Insurance is getting to be a BIG problem in CA even in non wildfire areas, the cabin in Tahoe is almost 10x higher than just ten years ago, but I’m also seeing missive increases for apartment properties I own in the Sacramento area and on the SF Peninsula where premiums are now 4x higher than ten years ago.

Ok, it’s my turn to say – not in my neighborhood – look at this lot price history

https://www.zillow.com/homedetails/1627-Laird-St-Key-West-FL-33040/45801441_zpid/

It’s just an empty lot, no one is building, they only buy it and sell it, isn’t this ridiculous?

But they haven’t sold it yet. That’s just an ad with a price.

Yes, and I hope it’s not happening, but it’s a nice illustration of greed and speculation..

Speculation, yes. Greed? What is so greedy about this? I guarantee you if you had the chance to make 100% profit on something you would jump on the opportunity to do it. You wouldn’t consider yourself greedy at that point. You would consider yourself smart.

The more proper word IMO is opportunistic. But somehow, opportunists are mostly labeled “evil”. Life is a poker game. You play with the cards you were dealt. Just because someone bluffed you out of a good hand doesn’t make them a bad person. It’s a game.

If you ask for more money, because your work is getting harder, that’s not greed..This here is pure greed and gluttony from my point of view.

Not to worry – the housing bros on fintwit have all the answers. they can’t understand why any loser would work a W2 job.

But you still believe in inflation. Laughable

You’re a joker. I don’t “believe” in anything. But there IS inflation. It’s right there in front of you. Got my auto insurance renewal, LOL. Only willful blindness keeps you from seeing inflation. Inflation is very much in your face. And it’s in services now, such as insurance, and rent inflation is still hot, and healthcare inflation is red-hot, etc.