“Neutral rate” creeping higher? Oh dearie! Bloodbath at the long end.

By Wolf Richter for WOLF STREET.

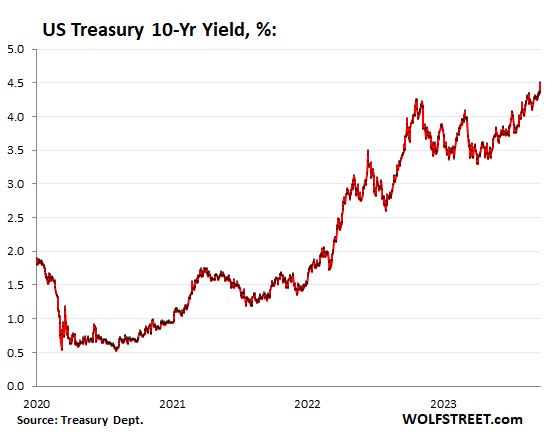

The 10-year Treasury yield jumped 14 basis points today to 4.49%, the highest since October 2007. Bond prices fall when yields rise, so this was quite a bloodbath today at the long end of the Treasury market.

“Neutral rate” creeping higher? Oh dearie!

It seems the Treasury market is gradually reading the memo that has been passed around for about a year. The subject line says: “Higher for longer,” and yesterday someone scribbled next to it, “maybe forever?”

Yesterday’s “dot plot” from the Fed underlined a few things in that memo. It indicated shockingly that the policy rates might still be 5.25% at the end of 2024, rather than 4.75% top of range, as it had indicated in June.

And there was discussion about the “neutral rate” creeping higher, which Powell cited as a possible reason why the economy has performed surprisingly well despite higher rates. The neutral rate creeping up and returning to the pre-QE levels of 2007 and before would introduce the “higher for maybe forever?” nuance, where the whole rate framework shifts higher, where rate cuts might not be as deep, and wouldn’t be maintained for long — unlike perma-ZIRP of yore — before getting raised to the neutral level again, which would be much higher than it was over the past 15 years (I posted an explanation and example of the neutral rate into the comments below).

The 40-year bond bull market ended in August 2020, when the 10-year yield kissed 0.5%. With hindsight, we can say that predictions at the time of the 10-yield yield dropping below 0%, as it had done in Europe, were rather silly. But on that day, we were biting our nails, because crazy things were happening all over the place, with central banks were printing trillions of dollars and throwing them at the markets.

At any rate, that zoo is over now, thank-goodness. The 10-year yield has jumped by 400 basis points since then. The world is normalizing – maybe even the “neutral rate.” And that’s a good thing.

Turns out, historically, the 10-year yield is still relatively low. We’re just not used to it anymore:

Bond bloodbath at the long end.

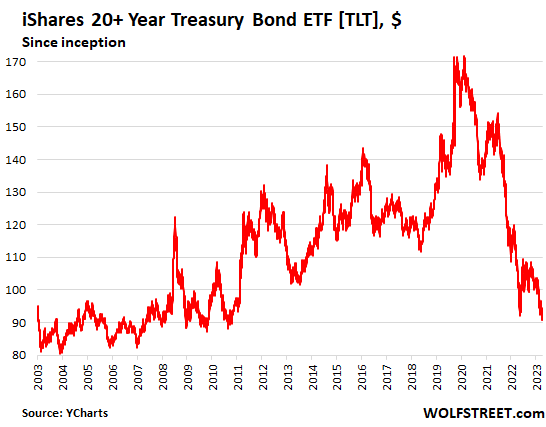

Future bond buyers are licking their chops at the juicy future yields they see coming at them. Current bondholders that intend to hold to maturity don’t need to worry about it. But bondholders that are wanting to trade, or that have to mark to market, or that invested in a long-term bond fund that by definition trades, that’s where the bloodbath happened.

For example, the iShares 20+ Year Treasury Bond ETF [TLT], which focuses on Treasury bonds with a remaining maturity of 20 years or more, fell 2.6% today and has plunged by 47% from the peak in said August 2020. If long-term interest rates continue to rise, the price will continue to fall.

This instrument is good for betting on the direction of interest rates. But as interest rates fell for most of the 20 years of the life of this fund, interrupted by some increases, the price of the ETF kept rising and made great money, and buy-and-holders began confusing it with a low-risk long-term yield investment, which it is not.

The unloved 20-year yield – “unloved” because it has been higher than the 30-year yield ever since the 20-year Treasury security was introduced in May 2020 – spiked 17 basis points today, to 4.74%, closing in on that fabulous 5%. By contrast, the 30-year yield spiked 16 basis points to 4.56%.

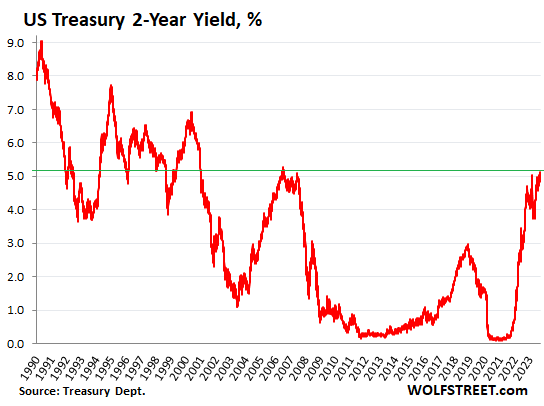

Sanguine at the shorter end today.

The two-year yield closed at 5.12%, same as yesterday, and just a few basis points higher than in the prior days. So that’s the highest since 2006. But compared to the 1990s and 1980s, the yield remains relatively moderate:

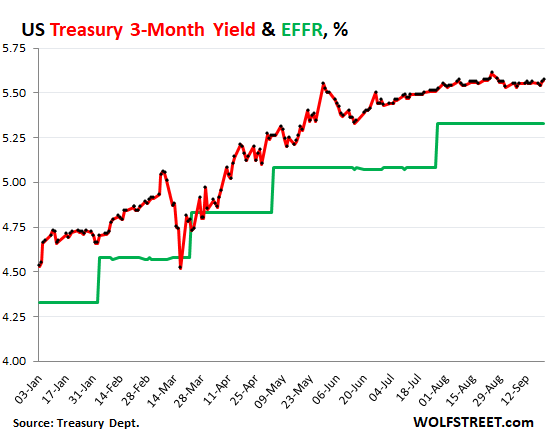

The three-month yield has been steady, closing at 5.57% today. The Effective Federal Funds Rate (green) has been at 5.33% since the last rate hike in July, with a spread of 26 basis points to today’s three-month yield. This spread shows that the three-month yield has fully priced in a rate hike by November.

The drama is on the long end of the Treasury yield curve, with the 10-year yield, and up, where the reckoning has been taking place for months that the bond market is in a new era, that the 40-year bond bull market died, that long-term yields are no longer repressed by massive QE, that in fact the Fed is shedding assets, closing in on the $1-trillion mark in terms of what it has shed since the beginning of QT, just when the government is issuing a tsunami of longer-term Treasuries, and that there is now the suspicion floating around that the “neutral rate” has been creeping up.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

We stand in grave risk of the central bank doing what is actually best for most Americans.

Told ja… but everyone here said I was nuts and my forecast would be “crushed!”

lol

Higher forever!

the curve has inverted back to where it makes sense, what is wrong with THAT? 4.5% is hardly a bloodbath, even I remember when we got 6% for one year from the local bank.

It’s a bloodbath if you bought a 30-year Treasury bond at auction in Aug 2020, and you lost over 50% now; or if you’re in the TLT Treasury ETF fund and are down 47%. Pretty bloodbathy for investments in Treasuries… these are not cryptos.

Those people didn’t give a toss when us self funded retirees where getting near zero interest all those years.

Yes, that was a bloodbath too, a very slow one that lasted 15 years.

I’d love to see an updated estimate of how much total interest income was lost to savers during those 15 years. Last I saw YEARS ago was $500 billion according to David Stockman if I recall correctly.

We have to add all their savings and near-cash assets, not just savings products. So that includes savings products (CDs, savings accounts), money market funds, and T-bills. The amounts are substantial.

If you figure $15 trillion in total, times 2% lost interest income per year, you’re already at $300 billion per year in lost interest income, times x number of years.

Now try 4% in lost interest income.

Stripping these types of investors off their income streams was part of the reason for the slow recovery after the financial crisis.

We’re government programs like social security and Medicaid hurt during these 15 years?

One would think they could not find a good return on their investment. I’m not even sure how all that mountains of money is invested to make more?

** oops meant Medicare not Medicaid.

But perhaps medicaid money is invested as well? Till the people need it.

Ouch, this will not last for too much longer with many banks lining up at the Feds emergency window.

Borrowing at the emergency window declined and remains minuscule: $107 billion for a $24 trillion banking system.

If Jay jumps through the Feds emergency window, would that be defendestration?

…yer attit again, XC…

may we get all find a better day.

@ Wolf –

Wolf said: ” a $24 trillion banking system.”

————————————————–

How do you compute the total size of the banking system?

The standard way, total assets in the banking system. The Fed as banking regulator collects that for you weekly; and the FDIC does it quarterly.

I was going off memory. I now looked it up, total assets dipped a little to $22.9 trillion

If the banks were wobbly with a 3.7% ten year…..

what now?

One can guess the coming headlines….

and here comes the avalanche of new borrowings by the Treasury.

Easy solution. Hold to maturity.

That isn’t really much different. The price change comes from a present-value-calculation of all future returns so whether you hold to maturity or sell now at a loss to buy at the current, higher, interest rate, you’ll get approximately the same return. (simplistically, not accounting for taxes, etc.)

I’d word this advice differently:

Don’t buy anything you don’t intend to hold till maturity.

Good plan if you can live for the 30 years of this TBill then re-invent in a higher TBill and live for a subsequent 30 years!

Yep, I’m 62 , retired and bought a sizable amount of the 20 year this month at 4.5% . Holding till maturity and collect my interest . If the yield goes higher maybe to 5%, .I’ll load up even more

30 year bond holders will be lucky to get 25 cents on a dollar before this is over. This could take down some big banks in the process.

As long as those losers are not oversees investors,like China, who are probably a bit annoyed at theUSA at the moment

They’ll get 100 cents on the dollar when the bond matures, plus collect whatever coupon interest along the way.

Guess what they’ll get in the case of Default??

…zero

1931 approaches!

“The neutral rate creeping up and returning to the pre-QE levels of 2007 and before would introduce the “higher for maybe forever?” nuance, where the whole rate framework shifts higher”

No body should be surprised by this glacial shift in Fed. Nobody!

Rent, fuel, utility, medical, education, etc are all slowly headed higher. We don’t have $2T annual deficits without extra inflation. That just doesn’t happen. This isn’t inflation that’s “creeping” into the system. It’s all there in plain sight. Government spending is singlehandedly holdng off the recession.

So JPowell is finally hinting at what we’ve known for a year now. Transitory inflation has morphed into a higher than 2% core PCE inflation rate.

DUH!!!

Great write up, Wolf! Excellent reporting.

Higher forever usually happens when governments keep piling on debt.

Just ask Argentina. I think their interest rate has crept up to 118%. Yep. That is right. 118% as of today. It was 97% earlier in the year.

If you don’t like today’s situation, wait until the economy hits the wall and the Fed does YCC with inflation at 3% or more and 8% unemployment. Nowhere to hide. The only way to get rid of the debt is financial repression AND inflation 😅

ZROZ treasury ETF is the one with the longest duration, that’s down 59% from the highs.

I avoid all bond mutual funds and etfs. I just buy the bonds myself.

I do wonder if all this turbulence will hit the big funds like Vanguard’s and Fidelity’s.

You have to think they bought a bunch of bonds at the wrong time.

Powell has his apron on and he’s breaking eggs!

Sooner than later the “bloodbath” in long Treasury bonds will cause a bloodbath for highly leveraged borrowers…. There is about $3 Trillion of floating rate loans that will be causing distress in the corporate sector….

When the stock market collapses, 20% of the biggest spenders will feel a lot less rich, and that will be immediately reflected as the start of a recession.

While margin borrowing and rates are not as high as they were prior to the 1929 crash, there is a similar amount of leverage in the corporate sector from all the highly leveraged private companies.

While the bottom 50% of Americans were struggling in 1929 prior to the crash, the top 20% were partying… which is quite similar to the current situation we are in.

The difference is that Govt spending and inflation are relatively high today, whereas prior to the crash in 1929 deflationary pressures were what was causing pains for 50% of Americans who still worked on farms.

What is the same is the amount of leverage employed by the upper 20% and highly leveraged corporations/banks.

The amount of systemic inflation (read sticky) today means the Fed cannot lower interest rates much when the economy rolls over….

Which is similar to the 1970s situation… except that real estate was very cheap at the beginning of the 1970s…. Nice houses in desirable areas of the country could be bought for about 1 times annual income…. While now houses are selling for 8 times annual incomes.

——————————-

Bottom line:

The “everything bubble” will soon burst because of rising interest rates….

The pain will be felt mainly by speculators in stocks and real estate, and by those companies that sell luxury end products and services.

The top 20% will save a lot more, while sticky inflation and higher rates mean the bottom 50% will continue to struggle.

The remaining 30% will also save more as they witness the carnage of falling asset prices, and the attractiveness of 5% money market rates.

How I wish I could be a fly in the room of the board of directors at SVB the day that 25% of all deposits were being withdrawn from the bank.

And I would have loved to see their faces as they went tell sell their MBS securities they bought at 2.7% when it’s now at 7.5%. What’s that? A 90% lose on principle?

…Or 10.5% MMA’s

Why is it taking the bond market so long to get the memo? It’s like the new guard are clueless. Being short long-term bonds makes more sense than being long at these prices. 4.6% to lock your money up for 30 years; and what buying power will it have after that?

If they had a clue long rates would never have gotten so low…

“Why is it taking the bond market so long to get the memo?”

There are people in the financial business who experience has been the years from 2009 to 2022.

The attitude acquired? THE FED WILL SAVE US. They always do.

MSNBC and Bloomberg are full of these types.

Not Kramer, he used to sleep in his car.

That guy is insane. Lol

Cramer is doing ultimate damage in the market now with his NVDA AI long. Wait till that crashes!

When your paid not to see, you do not see

I’m waiting for something to break. Worse than the regional bank crisis.

Soon, their is an election in approx 1 year so they must deliver the pain now which will give us a year to see where all the dead bodies are buried.

Buckel up

The break may come from Europe. The Credit Suisse and SVB crises were easily contained. I am surprised Deutsche Bank is still solvent. Anyway, something is going to happen. The Black Swan is just waiting to pounce.

Didn’t Deustche bank save Credit Suisse?

The government of Germany would have to go insolvent for Deustche to go down.

UBS and Central Banks pitched in to avoid a Credit Suisse fiasco. Deutsche Bank could collapse and Germany would survive, although it would throw the world financial markets into turmoil. Since we are talking about it, it no longer fits the definition of a Black Swan event.

Our illusiory economy is now so manipulated into that it will go out of control sooner or later. If the billionaire class is willing to treat the Supremes to life styles of the ultra rich and famous, secretly until now, (like LA judges reportedly get) think about the amounts of money offered to US government officials and politicians, who can really hurt that class. (America will be ok; most Americans, the less wealthy 95%, not so much.) We are now in early 2007 or 1928.

I read today them complaining about loan shark type credit card interest rates averaging about 18%. I’m pretty sure I had about $10k on a credit card in the 90s at 28% interest. They have no idea.

Credit cards increased from 20% to 23-26% recently here in Canada. Unless you’re a hnw individual at Nesbitt-Burns-BMO, you’re not getting the 15% credit card rates.

Why would a HNW person need 15% rates on a credit card?

HNW people only care for high credit limit ~100k is norm.

I pay my credit cards monthly and recently the bank snuck a finance charge in on 2 statements.

I still do not know the reasoning, they said I didn’t pay the full amount. But I did and do every month. I’m now paying every week, which is a hassle. But I put a healthy amount on there every month and I do not want interest.

Watch your statements ya’ll

Why would you pay it? Or switch to monthly payments which is just batsh*t crazy?

Your next response should have been to close the account at which point they would have absolutely “forgiven” the finance charges.

Speak up for yourself man.

I use cash.

Soon I will use gold.

Then I will barter.

Soon after that we will all have loot and riot for a loaf of bread

JD they did waive it.

I can go there when needed, ;)

Ozzy taught me of the crazy train. Lol

HEAL loans for medical school !8% in 1981 Chase.

Those had to be penalty rates.

WOLF…COULD YOU PLEASE EXPLAIN the significance of the “neutral rate

creeping up?” Didn’t Jerome P make some illusion to it recently about

the stars etc etc? I hope your not going to tell me to RTGDFA!

The “neutral rate” is a theoretical but unknown short-term interest rate that is neither stimulative nor restrictive for the economy. The rate is usually expressed as “real” = adjusted for inflation.

This means that if the real “neutral rate” is 2%, and inflation (core PCE) is 4%, then the Fed policy rate would need to be 6% to be neutral, neither stimulative nor restrictive.

But “real” neutral had recently been considered to be around 0.5%. So with core PCE inflation at 4%, it would mean a Fed policy rate of 4.5% would be neutral, and 5.5% would be restrictive. So the Fed thought that 5.5% policy rate would start slowing the economy. But that hasn’t happened yet, maybe because the neutral rate is much higher.

If in fact, the real neutral rate is 2% and core PCE inflation is 4% then a Fed policy of 6% would be neutral, and to slow inflation, the Fed might have to push rates to 7% or higher. That’s sort of the thinking.

This explanation was super helpful. Thank you, Wolf.

I agree, thanks.

(continued) .. obfuscate reality. The reality that central banks’ credibility and faith in fiat money has been badly hurt by the inflation shock unleashed by those in charge.

My layman’s big picture take on this: Core PCE is a backward looking concept, whereas whether rates restrictive or stimulative is a forward looking concept. Therefore, we should look at inflation expectations (rather than realized inflation) to determine the real rate. However, the inflation shock has introduced extreme uncertainty into any estimates of future inflation. Moreover, as a result of bloated central bank balance sheets and financial repression, the bond market has been distorted and also cannot be relied on to provide reliable information on inflation expectations. Therefore, it seems to me that a neutral real rate is currently a totally useless concept whose only added value is to help obfuscate reality.

“Therefore, we should look at inflation expectations (rather than realized inflation) to determine the real rate.

Clueless BS. I stopped reading after that line. It shows you’re not even familiar with the basic numbers and are just blabbering.

Consumers are clueless in their expectations and forecasts. They just react to what they see in the media and at the pump/grocery store. Inflation expectations lag CPI and are horribly wrong for the period they forecast. Everyone knows that except you? Businesses are no better in their inflation expectations. They too totally missed this wave of inflation.

In Jan 2021, inflation expectations (NY Fed) were at 3% for 1 year out and 3 years out, same as in 2018 and early 2019: they didn’t foreshadow at all the biggest wave of inflation in 40 years that was then already in the process and that I was already screaming about.

In July 2021, the 1-year-out inflation expectations (for July 2022) were 4.8%. But actual CPI in July 2021 was already 5.2%. So consumers were just aping current CPI reports, but with a lag of a couple of months. Then a year later, their 1-year-out expectation of 4.8% for July 2022 was horribly wrong because at the 1-year-out date, July 2022, CPI was 8.4%.

Inflation expectations aren’t tracked to forecast inflation. That’s just BS. They’re tracked to check on the current inflationary mindset of consumers.

I’d like to propose a simpler system. Set the federal funds rate at 2 to 3 percent above headline inflation.

Or just set the fed funds rate at 5% and leave it. We’d probably have much more long term stability.

Back in the 20th century, in what were deemed “normal times”, the Fed Funds rate seemed to be set at a level that covered the inflation rate and also a bit higher to account for what might be taxation on the interest. In other words, IMO, it seemed the Fed had rates at a level that would keep the holders of dollars from going backwards.

One might call that the “neutral rate”.

And this all changed in 2009 with the “new Fed” which took the tactic of making it a losing proposition to hold money and FORCED investment…the ZIRP and NIRP era.

Just my observation, not a declaration.

Yeah, that’s about when we went from ‘Cash is King’ to ‘Cash is Crap’!

It seems to me that the neutral rate exists only as figment of the Fed’s imagination. It probably gives them peace of mind to imagine it be at some value that when when you add the gamed PCE number to it, you arrive at a target Fed Funds rate which will reign in inflation.

Newsflash! It won’t…

The neutral rate is a theoretical concept. It’s important to understand that. It’s not an actual interest rate that someone sets or trades on. Powell himself said that it cannot be observed. But it helps with thinking through the issue of how high policy rates should be.

Brazil lowered their rate by 50 basis points to 12.75% yesterday. Their Aug CPI is 4.61% yoy and has been falling because the real rate is over 8%. What’s a 0.5% real neutral rate tell us about how effective Fed policy is going to be? We should expect inflation to continue for a long time; ie anticipated rate cuts will vaporize.

Brazil started a year before the Fed, and they hit with surprise monster-hikes and got their policy rate to 13.75% by July 2022. Inflation peaked at 12%. So they took harsher measures to crush bigger inflation.

So now they cut twice and are still at 12.75%. Inflation had dropped to 3.2%, but then started ticking up again and is back to 4.6% and heading higher. Jury still out.

They cracked down hard in part to protect the real against Fed tightening. Mexico did the same, front-running the Fed by about a year with big rate hikes. The real and the peso were among the few currencies that held up to the USD, while the laggards (such as the euro and especially yen) got crushed.

Ben Bernanke is muttering to himself somewhere.

If you didn’t know any better you would think he was reenacting scenes from Rain Man.

Hehe

Wolf — what was the basis for 0.5% being considered the neutral rate? And any idea how long this has been the case, eg. as of this tightening cycle, since ’07, etc. Thanks!

Besotted economists such as Bernanke and others decided that the new normal would be ZRIP and QE. I think that was the basis. “QE is a virus that turns brains to mush,” is a simple scientific fact that I have stated many times.

Finally the FED rate may have some rationally. Historically I thought the neutral rate was about 3%. We are globalized now and I am not sure what it is. I hope this helps reverse the very problematic income inequality in America. In your article you noted most inequality occurs in Stocks and Bonds. This concerns me as the have nots may come after mine.

Fascinating to have Knut Wicksell’s theory of neutral rate being revisited by the broad market. But finally what’s most intriguing is the fact that people start to question about where this neutral rate actually shall be – and think and act according to the believe that this rate shall be much higher than generally thought.. wow… !!

The apparent economic strength has absolutely nothing to do with the equilibrium rate of the US economy. The US still runs a 6-7% fiscal deficit while accumulated savings remain still beyond the norm. Fiscal steroids still in full swing. Monetary transition takes its time and indeed needs more time to filter through as debt duration is way longer than what it was ever before.

The FED has already been over tightening, by a substantial degree, as the full blown impact of monetary transmission will only start over the upcoming 1-2 years. Powell questioning the neutral rate is just a signal reminiscent to the discussions I remember before the 2008 debacle (in different form, but basically the complacency was no different). I am a happy buyer of 10-30yr UST at these 4.5% levels and will continue to buy more the higher it goes, as pain will seep in…

The mainstream media mantra—recited ad infinitum—“the hiking is over, the hiking is over…” is getting mighty tedious.

Wolf, with interest rates at the highest level in 15 years, do you think we will get a recession in one to two years? Sure consumers may make some money from money market interest but I read that the consumers’ savings have dwindled from $2t two years ago to just $100b now and they have to rack up credit card debts.

I know for sure for sure that we’re going to get a recession someday because there always is a recession eventually because it’s part of the business cycle — but whether that’s going to be next year or in 10 years… predicting the timing, that part I’m going to leave to others. Most people that predict the timing of the next recession end up making a fool of themselves.

My take is to bet on the Fed being wrong. The Fed’s track record of making big bad forecasts is very good.

The last one was to paraphrase: “inflation is under control”. as they pumped, pumped & pumped to make excessive spending a slam dunk.

Cheers,

b

All you have to do is look at dot plots in 2021 to see how wrong the Fed can be.

which Powell cited as a possible reason why the economy has performed surprisingly well despite higher rates

—–

tell that mor$on USA federal budget is funded by printing money.

about 30% more or less!

cut printing by 500 or 1000 bln $ and he will see how economy is doing well !

alx

ps

shall I mention that gov expenses is biggest part of nominal GDP after final sales to consumer ?

“gov expenses is biggest part of nominal GDP after final sales to consumer ?”

Consumer spending was 70% of GDP in Q2. So that leaves 30% for business investment and consumption, government investment and consumption, net exports, and changes in inventories. So it turns out that government investment and consumption was 17.2% of GDP in Q2.

“Economic activities have been stronger than we expected, stronger than I think everyone expected, … ”

Fxxx the Fed and Powell. It simply means the Rate is still WAY BELOW Neutral, and Fed QT pace is pathetic after 1.5 years. It’s that SIMPLE, stupid. Got it, Wolf?!

Folks, only in America, when a recession happen that SPX Doubled, and Housing Price went up 50%. Only in America!

And Fed is doing a GREAT job at Saving The Rich. All these Low Interest Rate at 5.5%, and still Sky High Balance Sheet after 1.5 years lift off, means SPX is near historic high, and Housing Price is back to near high. That means RATE is too low and Balance still Too High. Simple and Stupid!

While all the hard-workers and savers already got screwed by cumulative 50% increase in Inflation last 3 years. You think they look forward to “ONLY” 2% forward inflation?!!!

And we got Fed minions like Wolf praising Powell and Fed as the BEST Ever.

Of course, Wolf is in the top 1%. What’s more to say here.

🤣😎

too much 🍺?

❤

Nah, not enough fiber.

Well, you are the highest paid person in your massive enterprise.

Thanks for great explanations on this.

Sean, you’ll be pleased to know that his nomination for a MacArthur Fellowship was withdrawn some months ago after several years of promotion. Let’s just say they had reservations. It is, after all, an honor that has to be earned, not acquired as the result of a fortuitous gimmick. Plus something about being stale and otherwise lacking meaningful value. And so forth:

The rich are the scum of the earth in every country.

– Chesterton

Germany has been in recession for a good while, their industry is being crushed, and DAX is at ATH.

Germany has been in a shallow technical recession for the past two quarters, -0.4% and -0.1%. But consumers hate inflation, and there has been a lot of it in Germany. And Germany is a big exporter to China, and those exports to China have dropped sharply. Germany is more exposed to a slowdown in China than the US.

We shall see how this develops. I fear there is more reduction of industrial output of Germany ahead thanks to geo-political factors (“thank you USA” as the Poles say). In any case I meant to provide a handy counterexample to Sean’s assertion that it it a unique anomaly to have an economy in recession(-ish state) and simultaneously its stock market showing robust gains. Another great example on hand would be the UK that’s also languishing under years of austerity, double digit inflation, contraction and chaos due to brexit et al. (optimists forecast a 0.4% growth for 2023 so not quite in recession if near margin of error) while the FTSE is pretty near ATH.

Wolf, do you see anything in the near future that might cause short term 4 week or 8 week T-Bill interest rates to also advance higher?

Today’s 4 week T-Bill remained at 5.390%, pretty much where it’s been for the past month or so.

Thanks for your great website!

Bills are pricing in a rate hike in Nov. The 4-week yield matures in 4 weeks, so it will not get to the next rate hike. I don’t expect a big change in T-bill yields over the short term.

If inflation data, labor market data, and other economic data comes out hot over the next few months, we might start seeing another rate hike getting priced in for early 2024 (this would move up yields that extend past the expected rate-hike date).

Thanks for the reply.

I’ll still take today’s 4 week T-Bill rate of 5.390% any day over my credit union’s somewhat paltry 2.125%!

Buying the longer end of the rate curve is surely fraught with peril since the 30 year could very well drop another 15% (or perhaps even 30%). But, since recessions are inevitable, a subsequent drop in rates are likely as well.

So, in the near term that light at the end of the tunnel may indeed be a train coming, but in the longer term these long dated bonds and bond funds should appreciate nicely when rates eventually drop back down again.

*IF* rates eventually drop back down again. Did you not catch the part in the headline about “maybe forever”???

This isn’t even a case of RTDGFA, it’s simply RTGDFH. c’mon man!

What it means is that during the growth period, the Fed make keep rate above 5% somewhere, and when the recession comes, it can for a few quarters cut rates to 2.5% or 2% to be very simulative, and then after a few quarters, with growth back on, it can go back to neutral around 5%. As opposed to perma-ZIRP, which we used to have. That’s the thinking here.

It’s not that the Fed will never cut rates again — it will — but that the whole rate framework has shifted higher, similar to what it was in the 1990s.

Re: “shifted higher”

The probable reason is the change in the composition of the money stock. Contrary to George Selgin, banks don’t lend deposits.

spencer,

“banks don’t lend deposits.”

Clueless BS. You keep posting it, and I’m really tired of seeing it and deleting it. So take this to heart. I will say this only once:

1. The banks have a liability called “deposits” on their balance sheet. This is the amount they owe their depositors.

2. When you put $100 in the bank, the bank makes two simultaneous entries on its balance sheet:

3. The bank can then do whatever with this cash in its asset account, such as lending it to consumers, lending it to the government (buying Treasuries), or lending it to the Fed (depositing the cash in its reserve account at the Fed).

4. If the bank lends this $100 cash to a consumer, it credits its asset account “cash” with $100 (lowers its balance) and debits its asset account “consumer loans” with $100 (increases its balance).

This is a hugely important concept for you to understand. If you deposit $100 in the bank, the bank takes this cash and does whatever with it, including lending it out. What else is it going to do with your $100 in cash? Eat it? Plus it notes down that it owes you $100.

If you and everyone else want each their $100 back at once, the bank will say, sorry, we lent this cash to some people to buy a house with, so we no longer have this cash that we owe you, and if you all keep wanting your cash back, we’re going to collapse (= run on the bank = SVB).

A basic accounting course (where you learn about debits and credits) at your junior college is the best investment ever. I encourage everyone to do that.

I suspect when spencer says “banks don’t lend deposits” he ought to say “loans create deposits.”

Bank use the cash from their deposits to make loans, and the recipient bank gets that cash from that loan, which on its books becomes cash (asset) and deposit (liability).

@ Wolf –

Can a bank create new dollars when it makes a loan?

Hell no. Why do you keep asking?

@ Wolf –

Now for more non-intentional antagonism,

Can the banking system create new dollars when banks within the system make loans?

Yes, with rising asset prices = rising collateral values.

He forgot to say forever until we get closer to the November 2024 election date. So between March 2024 and June 2024 we should see the first rate cut.

If there is much of a rate cut where we drop below 4%, than we will probably be in a recession or soft landing.

That will also mean the Government will need to spend money to keep us from a hard recession. Most likely push the deficit to over $2 trillion yearly mark.

Who will want to buy those extra treasuries with falling rates and increasing debt? The FED I guess?

When I was born, the 10 year was at 6%!

It looks like the bonds have way more to go, looking at the graph.

I wonder if Congresspeople are complaining to the Federal Reserve Chair like Doug Ford and Eby did to Tiff Macklem, because those on variable and renewal will have to pay more interest on their mortgages?

I’m 20% TLT.

This has not been fun but I do believe that the index is at a place now where it’ll serve it’s purpose as a strong asset during deflationary times.

At least that’s what I tell myself…

Deflation in what exactly? That is what you should be asking yourself. With over 8 billion of us on this rock now and millions fleeing war, famine, and drug cartels I see plenty of future demand for housing, energy, food, a safe neighborhood etc.

Who has ever seen deflation?

We need to undo about 11% of inflation… the amount accrued OVER the Fed’s self authored 2% per annum goal since the inflation began

I moved money into SCHQ playing chicken with the Fed, betting they are outta gas. Talk is cheap, but when another bank run occurs, or interest paid on debt as % of tax receipts keeps spiking, or Pocahantas goes on the warpath with Schumer about JPOW “hurting” the little people, or an election. MR WR showed us the economy is running on 2T deficit spending recently. This admin lies about economic numbers then revises lower.

I ain’t buying this. This is where the money is made, making a stand. I also like money market too.

“Deflationary times?”

In my entire adult life, the core PCE price index – the Fed’s favored measure – was never ever negative, never, and therefore never even hinted at “deflation.” This “deflation” monster is just a figment of deflation-mongers’ imagination. Overall PCE and CPI figures may dip into the negative briefly, when the price of oil collapses after a HUGE spike, as it does periodically. But that’s not deflation, that’s oil coming off a spike, and it’s over in a few months.

Your outlook might be different if you were Japanese or lived in the 1930’s…

No argument that economic cycles can take a long time. But I can’t count on your generational story to be the same as mine.

Well this is the US, not Japan

and now we have the internet

and steam engines are gone.

© 😎

There are a lot of reasons why the Great Depression is unlikely to happen in the US, including the government safety nets that will keep consumers afloat and spending, bank regulations and bank safety nets that will keep damage to depositors to a minimum, etc. You can no longer compare the two economies.

But anyway, if you enjoy preparing for, and betting on, long bouts of deflation, go ahead.

I think Wolf is right here, at least in part because both governments and their independent central banks dread deflation (for good reason) and will use all of the levers at their disposal to avoid it at all costs. And those levers are incredibly powerful.

Ummmmm…..just by TBills with 3-6mo durations and keep rolling over until inverted yield curve resolves. Better than TLT….imho

Dr J

Great analysis, and yes it is about damn time, BUT, even 5% does not come close to covering the real risk or time value of my money.

Powell is NO Volcker and this is NOT the 70’s/80’s! Remind us Wolf, what was the debt/GPD ratio in the 80’s again?

Hedge accordingly.

Love watching the treasury curve slowly realize that rates aren’t imminently going to zero. Significant steepening in the curve since July.

Bonds, LoL. We have a long way to go to tighten up. The math of bond pricing dictated this bloodbath. The same math will work on all assets. Productive assets WITH A POSITIVE REAL RETURN will go up in nominal and real terms.

What does mean? Returning to the 70s show for finance. People need a clue, it’s 1970, not 1981. So much wreckage to come.

Just look at our retail rust belt….

Houses have huge running costs, oh yeah what’s a hurdle rate?

“But bondholders that … invested in a long-term bond fund that by definition trades…”

If interest rates were to remain steady and an investor holds the ETF for the same duration as the bonds it trades, would the market value of the ETF be expected to return to par much like holding the bonds themselves to maturity?

I think it would be pretty close, if yields don’t change, and if there is no run on the fund that forces the fund to sell bonds (big ifs).

The ETF has expenses that bonds don’t have, so your yield is going to be a little lower than the yields from equivalent bonds.

The Fed Balance sheet dropped $75 billion to around $8.025 trillion. I said a few months ago that I never thought the balance sheet would have a “7” in front of it again, and that something would break, and they’d be back with another “emergency program.”

It looks like I am going to be wrong, and I’m happy for that.

Oh it is probably going to have a six or even a five in front of it before they are done. Make no mistake… these people are at the pinnacle of their careers… so NOW they are making a play for their historical reputations. They want to be listed among the Fed greats rather than have wikipedia articles for all eternity declaring that they were unable to control inflation, foolishly allowed an asset bubble, etc.

Prior to the 2020 shut down people were hoping the feds balance sheet would get closer down to prior to the 2008 financial crisis levels. Now they are hoping it will get closer down to prior to the 2020 shut down. The next crisis will come, yes it will, the balance sheet will expand and we will hope it will get down closer to the “x crisis level”.

When draw a line through it all, it is up up up. This is what happens when an empire dies.

For nearly 100 years, from the Fed’s inception through 2007, the balance sheet grew with “cash in circulation” and “required reserves,” which are liabilities on the Fed’s balance sheet.

JPM and some other banks used to handle the government’s checking accounts. During the Financial Crisis, this was shifted to the NY Fed what we now know as the TGA. So now that’s another liability on the Fed’s balance sheet ($700 billion) that caused the balance sheet to grow.

And now the Fed pays interest on “reserves” and these reserves have piled up. They’re also liabilities.

So there is all kinds of stuff on the liability side that must be counter-balanced on the asset side because always on every balance sheet:

assets = liabilities minus capital.

So the balance sheet over the decades will keep growing, but the economy keeps growing too.

A good way of looking at it is Fed assets as percent of GDP.

That chart — Fed Assets as a & of GDP — is a blockbuster.

Even if the Fed Footprint declines to 15% (which, by the way, promises to be a painful ride with starts and stops), it’ll still twice where it was in 2008, which was double the low point in the prior 20 years.

That Fed Assets have rocketed from 7% to 32% over 15 years is emblematic of an alarming lurch toward planned economics.

Form a preparedness standpoint, I believe it makes sense to account for both strong inflations, sharp depression, and currency devaluation. All three will likely pop up sporadically, and occasionally concomitantly.

Thank you Senator Aldrich, Woodrow Wilson, Ben Strong, Hubert Humphrey, Aurthur Burns, Allen Greenspan, Ben Bernanke and the rest of the cast of supporters of a managed economy.

Two more weeks left before the balance sheet falls below $8T (my guess). So I’m crossing my fingers, knock on wood.

Wolf….

What are your thoughts on Powell’s declaration of March 2021…that

“We must unlearn what we know about M2”?

Curious he said that as M2 was exploding and he was NOT predicting an inflation, which certainly came to be.

Well, M2 did explode during the pandemic, but now is is plunging … negative yoy for the first time ever, LOL, while inflation is high and re-accelerating. So what do you make of that?

The correlation between M2 and CPI inflation is not convincing if you look back over the decades. There was some lagged correlation in the 1980s, and then there was very little correlation for decades. So you have to cherry-pick your correlation to fit your narrative. Chart shows M2 yoy v CPI yoy:

Powell is trying to rebuke the unreconstructed vulgar Monetarists who still think that central banks target the money supply, a practice they gave up attempting almost 30 years ago now.

Sometime around March or April 2024 you might see a “6” in front of the Fed balance sheet again….

If you want housing prices to fall, then you drain reserves. That’s how Greenspan caused “Black Monday”.

For the next 20 years…..I don’t think we see 3% again in the FF rate.

OK…….why……. a collision between the largest generation in history just coming into its biggest spending and the second largest generation demanding plenty more than daddy in retirement while producing nothing.

All the while the US dollar needing a bit of support to ensure it does not contribute to inflation.

A federal government that controlled by either side has its reasons for spend spend spend.

Reinforced by a new Cold War no matter who gets in resulting in fewer cheap goods, and potentially new tariffs.

Tempered by AI productivity.

Rates higher for a lot longer than anyone anticipates.

Eccles is in a box……whether they recognize it or not….who cares.

LOL……so much for the good news.

The great news about the almighty buck cratering in value due to inflation is the housing bubble never ends, as the scramble to get rid of greenbacks goes on in earnest.

The US Dollar is doing extraordinarily well and is over 105.00 on the DXY. Didn’t you get the memo?

Wolf, as always, awesome commentary.

My problem with “higher forever” is that the math just doesn’t jive with reality. There’s no future where the US government can fund itself at these rates (or higher) without intense inflation to bring down the parabolic trajectory of the debt, or near-zero rates to control the interest servicing costs (or a sudden explosion in population and productivity growth… doubt it). Fed rates are high to control inflation, but inflation is what the govt needs to control the debt…

Hussman’s latest article has a great chart that shows the Fed used to control rates using money supply, but a money supply at 16% of GDP drives rates to zero, and we are way above that, so the only way to control rates at that point is with the reverse repo and interest on reserves nonsense that the Fed is using now to basically pay banks not to lower yields with their demand. That’s just trick-f*&king the system, similar to how QE was a new way to trickf*&k the system in ’08 when the math didn’t add up.

So what’s going to be the next trick? When the math *requires* lower rates or higher inflation to keep the government funded, what new instrument will the Fed use to force the math to work for another decade? Will it be the dollar milkshake that saves us as the rest of the world gobbles up treasures? Will the govt start to guarantee loans from non-Fed lenders so the debt doesn’t show up on the balance sheet unless it defaults?

I just can’t see how if we do get a recession or unemployment gets ugly, how the Fed resists the call to slash rates when they couldn’t even keep strong in 2018/19 at much lower rates. Looking at our debt and the current growth rates, I just can’t see how we don’t end up at YCC and massive inflation at the end of this “experiment.”

What’s the next trick? The Treasury could mint a platinum $1T coin and deposit it (or multiple) at the Fed and pay off debt that way. The pain is then spread through currency devaluation by minting it and not asking the Fed to print on their end or foreign CBs to keep buying their debts either. I think many would lose faith in the USD that way and try to barter (and do things under the table) as much as they could.

The equation isn’t that simple with interest payments as percent of tax receipts.

Higher inflation and economic growth are whittling down the burden of the debt because tax receipts go up with incomes which rise with employment growth plus wage inflation.

So if the government runs a 4% deficit year-after-year (not adjusted for inflation), and the economy grows 6% GDP (not adjusted for inflation), then tax receipts will grow by about 6% (not adjusted for inflation), and gradually the burden of the debt declines.

This is all very long-term stuff. Nothing happens in a year when it comes to government finances. There is huge demand for government debt, you can see that with the 10-year yield STILL below 4.5%. So the government is able to fund the higher interest payments just fine.

A bit bout of long-term inflation will solve the US debt problem, even if initially the interest payments could look a little scary.

“I just can’t see how if we do get a recession or unemployment gets ugly, how the Fed resists the call to slash rates when they couldn’t even keep strong in 2018/19 at much lower rates. Looking at our debt and the current growth rates, I just can’t see how we don’t end up at YCC and massive inflation at the end of this “experiment.”

Wolf likes to say he will believe student loan payments resume when the data shows it, but not until then.

In the same vein, I will believe the Fed won’t cave and lower rates to zero, restart QE and circumvent their charter to buy bonds….when I see the crap hit the fan and they don’t wilt. They haven’t been tested yet. Until then, none of this blather about the future direction of rates, Fed balance sheet, M2 or unemployment matters.

Spencer,

I think it’s too late to avoid the conclusion “they were unable to control inflation, foolishly allowed an asset bubble, etc.” Now it’s just damage control.

Einhal,

I remembered someone said that about a 7 handle when Wolf had his last Fed balance sheet article and it was clear a 7 was coming in the next month or so. I’m glad you were wrong too, but after the last 15 years that mistake is understandable.

I’ve heard it said that a recession is nearly upon us not when the yield curve inverts, but when it un-inverts. It seems we’re getting closer.

1. The yield curve is supposed to predict a business cycle recession.

2. The last time the yield curve un-inverted was in April 2019, and there was no recession.

3. Then a year later, in March 2020, we got a pandemic and lockdown, totally unrelated to the business cycle, and the yield curve cannot predict and is not supposed to predict pandemics and lockdowns. And it didn’t predict it because it came a year after the un-invert.

4. So, the last time the yield curve inverted and un-inverted it predicted a business cycle recession that didn’t come.

5. Since the era of QE started, the yield curve has become useless as a predictor. It reflects what the Fed is doing: pushing up the short rates and still weighing on the long end with its gigantic balance sheet. And that’s all.

Yes. Many traditional metrics are useless in the central bank distorted economy.

The yield curve still “predicted” a recession in the sense that it sure would be dumb for people to be paying that much for long duration bonds unless a recession is imminent.

The prediction was correct. People *were* dumb.

Michael Harrington-

Yes.

For example gold used to fall with rising rates, but this time around has stayed relatively solid in spite of trebling of rates.

Seems like a noteworthy shift that coincided with shift from bond bull market to bond bear…

“Since the era of QE started, the yield curve has become useless as a predictor.”

The era of QE has ended, and QT has started.

ipso facto, the yield curve is again useful as a predictor?

Eventually, once the balance sheet is worked down far enough and the liquidity has been burned off, which will still take years.

Yield curve believer…

” the yield curve is again useful as a predictor?”

Based on what? Historical references? No, IMO.

Pre 2009 references are worthless for the Fed was not manipulating long rates and had little to no positions in the long end.

Now, they still have absorbed, taken off the market about $5 Trillion in long debt, intentionally inverting the curve to force investment.

Imagine what the curve would look like if that $5 TRILLION was out there in the free market looking for a bid?

Historical analysis of the yield curve went out the window when the Fed took over. The curve looks just like the Fed wants it to look.

“Since the era of QE started, the yield curve has become useless as a predictor.”

Exactly. Can you tell the talking heads on Bloomberg and CNBC that “news”?

Thanks, Wolf. I guess I should stop listening to these traditional investment mantras that are endlessly passed around. ;-)

Howdy Folks. The Lone Wolf will be nominated for the Nobel, under one condition. Lower the truth a notch. On a personal note, the prize means nothing. Keep your individuality and truth telling…. THANKS

It’s amazing to me that people don’t consider that the yield curve could correct by reversing its tilt. So short rates go towards zero as the Fed provides ample bank credits, but long rates inch up from where they are because the market understands the inflation outlook. The Fed has to control the long-end of the yield curve by buying TBonds itself with blank checks. That would merely cause the US$ to tank and inflation is off to the races. Who really wants to lend out 30 years under this scenario?

“…long rates inch up from where they are because the market understands the inflation outlook.”

Wait a minute. There’s a self-contradiction here. If the market “understands the inflation outlook,” meaning, I suppose, higher inflation, then the Fed understands this too, as will you and I, and the Fed won’t cut to zero, it’ll keep short rates high and long rates will go higher.

Note to ru82:

Argentina’s inflation is supposed to check in at 190% by year end.

That’s about a 15% monthly rate of inflation. It’s not unusual, for Argentina. I cannot imagine how people can continue to live with that going on.

I’ve heard that during serious bouts of Argentinian inflation, people would have price increases in the meal they ordered from the time they sat down to when they left the restaurant.

I don’t know if that would qualify as hyperinflation, but it must surely lead to hypertension.

They should ask for the bill when they order.

I think that people think of the bond markets as something that is not impacted by supply and demand and traders and I just dont think that is true.

Even if long term rates are eventually going to normalize around 4.5 – 5%, that doesnt mean the rates cant spike first and fall back down later. The bond market is subject to the same kind of irrational buying and selling as any other market.

A big part of the reason I think long term rates will move higher is simply that there is too much supply and too little demand.

My longer term thesis is that in the short term higher rates in the US will lead to a strong dollar, but that at some point, the dollar falls while long term rates remain higher. I am watching a chart of the correlation of these two assets.

Another potential thing I want to start watching is corporate and junk bonds. Do they start to show some higher premium versus the “risk free rate” of Treasuries? Although I think that bonds in Apple might actually have less risk than Treasuries in the future.

Alot of trading systems on a variety of assets already set RFR to 0 because the notion of anything being risk free is a joke and will get your azz blown out eventually when things change.

Helps that it also simplifies the math :P

Even if everything in life has some kind of risk, the risk-free rate can still existing as a theoretical limit construct. Sort of like how we can never achieve an absolute zero temperature, but we can see what absolute zero should be given that temperature and the pressure of a gas are proportional and extrapolating back to where pressure would drop to zero.

Yes, anything can exist as a theoretical construct, even things we haven’t even thought of yet.

1) UAW precision targeting – not a war to destroy the big 3 – cont. Within

a week the pour house might shut the gov down.

2) The Dow reflected fear. The Dow 1W opened > Jan 12 high, but closed above Jan 12 low. A big red bar on low vol. The weekly Dow flipped lower this week, a warning sign.

3) There are 5TD until Sept 29. If the Dow can’t get it up above June 16

high :

Option #1 : the plunge started on Aug 1. The Dow is H&S. The neckline

was breached.

Option #2 : In Q4 the Dow will close above Aug 1 high on the way to 37K/40K.

4) Xmas hiring started. Amazon is hiring 200K, Target…consumers cash

in the bank is $17.3T, thanks to JP. CL is still under BB : Nov 5/12 2007, 98.72/ 90.13.

In an environment, where the federal reserve has to keep creating four letter programs to patch all the leaky holes and just muddle along with nothing out of their direct ability control in markets happening, I can see higher for longer.

Fed reserve balance sheet post 2008 says otherwise, no way that goes back pre 2008 levels, and the rate of run off now is a joke when having that in mind. no matter what their rate policy framework is.

Granted federal reserve system is a lot better than nearly every central bank system out there… but thats not saying much.

“and buy-and-holders began confusing it with a low-risk long-term yield investment, which it is not.”

This is the problem with so many of the supposedly “sure thing” pieces of advice that the “experts” kept dishing out to investors over the past bunch of years, why so many of us come to WS to see Wolf’s charts esp ones like the 4th one. It’s historical perspective that got lost due to the outrageously naive loose monetary policy set in motion by Greenspan and Bernanke, and then adopted by Yellen and (until recently, thankfully) by JPow. So many of the “common sense” conventions like “house prices only go up! stonks only go up!” came about due the outrageously extended (but historically unusual, before the 1980’s) way too loose policies and “wealth effect” obsession of Greenspan and Bernanke.

That’s 40 years of accomodative policy to inflate asset bubbles and like this article points out, encourage the now more and more-infamous gold rush in the bond market that was supposedly “a safe and guaranteed investment”–but only because economists and central bankers had deluded themselves into believing that we could basically just do near ZIRP and QE ad-infinitum without consequences. This foolish thinking got so common that the Nobel Prizes put another nail in the coffin in their credibility by awarding Bernanke, of all people, the Nobel for basically setting the stage for the inflationary mess we’re currently in. This may in fact be one of the more important longer term consequences of Covid–the pandemic pushed the Fed and Congress to brrr the money printer so much that the inflationary crush of all that loose monetary policy became impossible to ignore. So much that real and very painful consequences are now being felt by more Americans, the same kinds of things that caused inflation to bring down previous empires and great powers–massive unsustainable increases in cost of shelter and record homelessness, higher crime and even looting, crushing healthcare and vehicle costs, retailers basically turning their shops into military bases to reduce theft of basic items. It forced the Fed, other institutions and investors to finally wake up and smell the coffee, including the bond market. And finally we may be close to learning back at least some of the wisdom that Volcker had 40 years ago too.

“finally we may be close to learning back at least some of the wisdom that Volcker had 40 years ago”

I hope you’re right, but that could be wishful thinking. The difference between now and then was the percentage of sovereign debt to GDP.

Now, with sovereign debt north of 100% of GDP and rising, servicing the interest on the debt is at some point going to become formidable.

Since they’ve been following Japanese monetary policy with this QE business since the financial collapse in 2008, I look at Japan as the canary in the coal mine.

What I’m seeing now is inflation at or above 3%, while the central bank wants new sovereign debt at 1%. According to Deloitte, the BoJ is buying all of newly issued debt. I see Weirmar Republic economics over there with a QE veneer.

We’re going to be in the same shape if the fiscal policy carries on with this “deficits don’t matter” approach because the interest costs on the deficits will start mattering more and more. The Fed can only do so much with monetary policy to counteract fiscal policy that is out of whack.

The best thing about the TNX blowing out to 4.5%:

it beclowned a bunch of pivot-mongers and amateur chart monkeys who were crowing only a few weeks ago that it had made a “double top” at 4.33.

Eat crow, pivot mongers!