Back to the future: With repos, not QE, is how central banks handled issues before 2008. The Fed also revived tools to go back into that direction.

By Wolf Richter for WOLF STREET.

“The Bank of England is not alone in facing these choices. Central banks around the world are grappling with similar questions as crisis-era asset purchase programs and funding schemes are withdrawn,” Bank of England Governor Andrew Bailey said towards the end of his lecture at the London School of Economics this week, after he had laid out:

- How much more the BOE’s balance sheet might drop (a lot more).

- How it would get there (including through outright sales of bonds).

- How the BOE would continue shedding bonds even after the balance sheet is low enough and stays level, until all bonds are essentially gone.

- How repos would then provide liquidity as-needed to the banks.

- And how this would change the composition of the balance sheet from long-dated bonds to short-term repos.

The BOE’s outline of a plan harkens back to how it was before the Financial Crisis – before QE showed up. With repos was in essence how the BOE, the Fed, and other central banks had handled liquidity issues and market disfunctions for decades until the Financial Crisis in 2008.

And the BOE is now the first major central bank discussing how it plans to revert to a similar system as before, draining reserves, then using repos – instead of bond purchases (QE) – to deal with issues.

In general, central bank repos are short-term instruments by which the central bank lends cash to approved counterparties (such as banks) against approved collateral (such as government bonds). They mature the next day, or in a week, or in 30 days, etc. And when they mature, the central bank gets its cash back, and the counterparty gets its collateral back. If repos are not renewed, they come off the balance sheet automatically and don’t cling to the balance sheet for years or decades like longer-term bonds do.

The Fed has set itself up to be able to go into a similar direction when it revived the Standing Repo Facility (SRF) in July 2021 before it had even announced that it would pivot to QT. The Bernanke Fed had skuttled the SRF in 2009 because under the large-scale QE, the SRF wasn’t needed.

But under enough QT, the SRF was suddenly needed, as the Fed found out in 2019 when the repo market blew out because QT-1 had drained liquidity unevenly, and it wasn’t going fast enough where it was needed, and there was no SRF to deal with it, and instead the Fed ended up undoing part of QT-1 to calm the crisis. Now, with the SRF in place, the Fed is ready to deal with these situations, even as QT goes on.

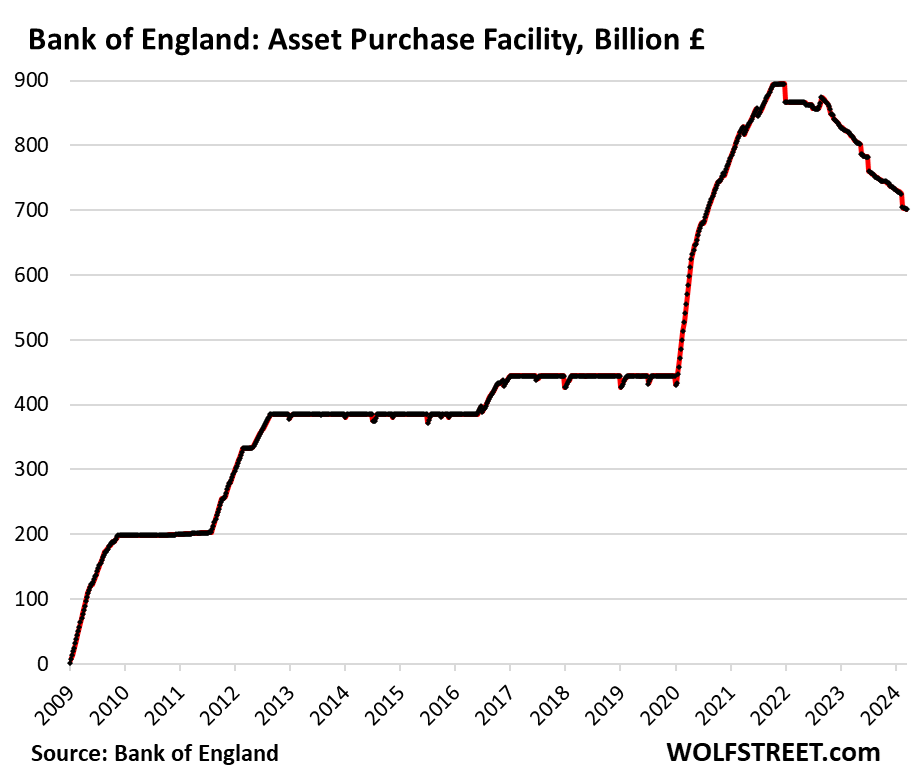

The BOE’s bond holdings and QT.

During QE, the BOE lent funds to its off-balance-sheet entity, “Asset Purchase Facility,” which then purchased the bonds. What the BOE carries as asset on its balance sheet are these loans to the APF. Now, as QT is whittling down the assets in the APF, the APFis paying back those loans to the BOE, and they come off the balance sheet in those amounts.

The APF bought assets in four big waves: During the financial crisis (2009), the Euro Debt Crisis (2011-2012), Brexit (2016), and the pandemic (2020-2021). During the pandemic, the BOE added £440 billion, nearly doubling its bond holdings to £895 billion.

QT started in March 2022, when the first big bond issue matured and wasn’t replaced. In September 2022, when leveraged pension funds blew out and threw the market for UK government bonds (gilts) into turmoil, the BOE briefly bought gilts, that it then started selling in November; and three months later, it had sold them all.

The BOE is the only major central bank that has a policy of actually selling bonds, not just waiting for them to come off the balance sheet when they mature. Since November 2022, it has been selling bonds every week.

Under QT, the APF has dropped by £194 billion, or by 22%, from the peak, to £701 billion. In other words, the BOE has now shed 44% of its pandemic bond purchases, including all of its corporate bonds.

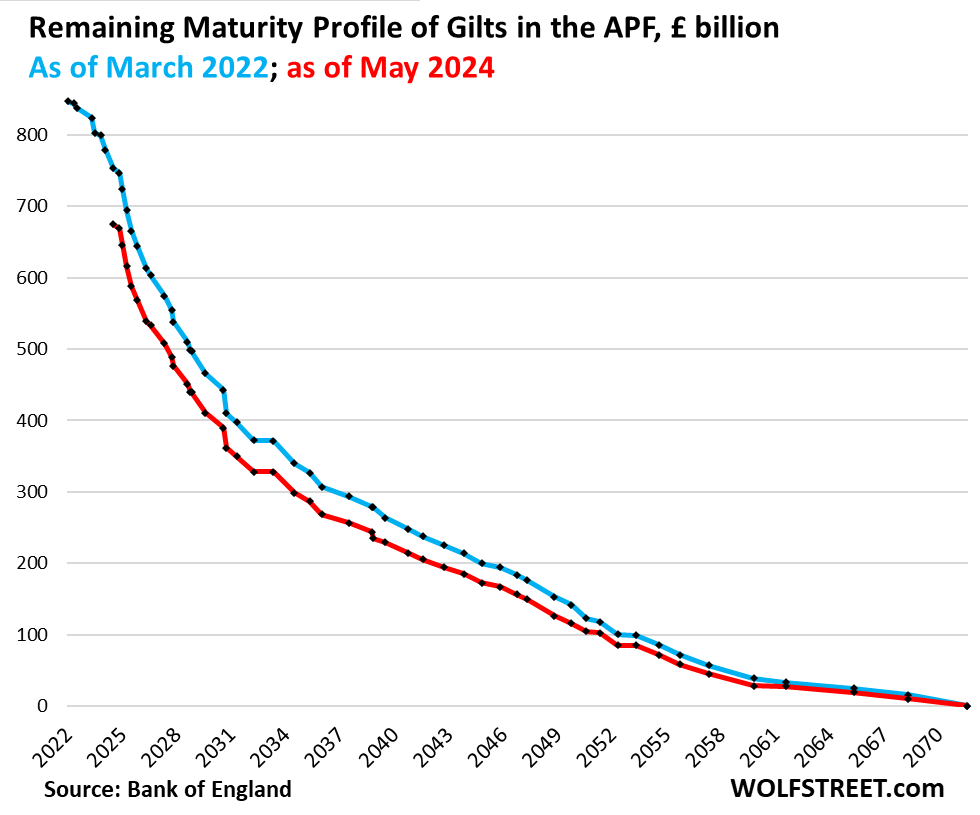

The BOE sells bonds outright.

At the peak of its holdings in February 2022, the BOE held about 55 gilt issues with varying maturities: Three issues matured in 2022, two in 2023, three in 2024, etc., all the way out to the year 2071. Obviously, waiting for these long-dated gilts to roll off when they mature would require a lot of patience. So the BOE has been selling bits and pieces of each issue week after week.

For example, one small issue, maturing in 2039, has already been sold off entirely. The issue maturing in 2071 has been sold down by one-third, to £10.2 billion currently, from £15.5 billion at the peak. The issue maturing in 2068 has been sold down to £8.9 billion, from £9.3 billion at the peak, etc.

The chart shows the maturity profile of the remaining bonds in the APF as they had been on two dates: in February 2022 (blue line) and now in May 2024 (red line).

The difference between the blue line and the red line reflects the bonds with maturity dates in the future that the BOE has already sold outright:

QT draws down reserves. How low can they go?

Reserves are cash that banks keep on deposit at the BOE. They’re the most liquid form of money with which banks settle transactions with each other. They are also essential for financial stability if banks need liquidity, or need to provide liquidity to the financial system, as Governor Bailey explained at the lecture.

QE ballooned the reserves. QT draws down reserves. And now it’s a question of how far they can be drawn down before the financial system runs short on liquidity, he said.

“Before the financial crisis, monetary policy was implemented with a much lower level of reserves than we have today. That worked well enough for monetary policy. But as we discovered to our cost, the level of liquid assets in the system, including central bank reserves, was too low for financial stability purposes, and this contributed to the scale of the financial crisis,” he said.

“Equally, at some point the costs of an increase in reserve supply are likely to outweigh the benefits. Generally speaking, as reserves levels grow, the incentives for the banking sector to manage its own liquidity fall. And to the extent that reserve supply crowds out healthy market intermediation in normal market conditions, a large part of the financial system’s ability to manage its liquidity will be affected. Mindful of these costs, we do not seek a larger balance sheet than is strictly necessary,” he said.

And this is where the concept of “Preferred Minimum Range of Reserves” (PMRR) comes in. It’s “an estimated range for the minimum level of reserves that satisfies commercial banks’ aggregate demand, both to settle their everyday transactions and to hold cash as a precaution against potential outflows in times of stress,” he said.

Except the PMRR “cannot be objectively observed,” “is likely to evolve over time,” and will be affected by a number of factors, that he listed.

Reserves are down to £760 billion. The latest assessments for the PMRR are in the range of £345 billion to £490 billion. So the balance sheet could drop by an additional £270 billion to £415 billion. At the current pace of QT, and the unwinding of the pandemic-era “Term Funding Scheme for Small and Medium-sized Enterprises” (TFSME), reserves might fall into the £345-490-billion range at the earliest in the second half of 2025.

Repos will deal with the “bumps in the road” on the way.

“But as we approach the minimum level of reserves demanded by banks, things get a little more complicated. We cannot be sure exactly where it is, and as we approach it, we may face a few bumps in the road with temporary frictions in money markets as firms adjusts to the falling supply of central bank reserves,” he said.

To deal with these frictions, the BOE established its a weekly Short-Term Repo (STR) facility in 2022, “complementing our other reserve supply operations – including our Indexed Long-Term Repo, or ILTR, which supplies reserves for six-months at a price related to demand, against a wide range of collateral,” he said.

“The STR allows banks to borrow unlimited amounts of reserves, against gilt collateral, at Bank Rate,” he said.

“In combination, these facilities will allow the unwind of QE and the TFSME to continue without the risk of any loss of monetary control on the way to the PMRR,” he said.

The “new phase” of QT after the balance sheet levels out.

“As this QT process progresses, the gilts held in the APF may eventually fall below the PMRR. Lending through the STR in the first instance, and eventually alongside our other facilities, will start to pick up the shortfall in reserves supply, to meet prudential needs for reserves and maintain monetary control through the setting of Bank Rate,” he said.

At that point, “the QT process enters a new phase,” he said. As QT (shedding bonds) continues, with the APF unwinding, while reserves remain steady at much lower levels, it will change the mix of assets from bonds to repos.

He defines QE as asset purchases; and QT as shedding those assets; while repos are short-term loans secured by collateral, and are not QE, and don’t have the effect of QE.

“For much of the Bank’s history we have lent on a secured basis, primarily against government securities and trade bills. Perhaps it is time to return to such an approach,” he said.

Handing interest rate risk (and losses) back to the financial sector.

Repos replacing gilts also eliminates interest rate risk for BOE. It has lost billions as gilt prices plunged when yields rose over the past two years. It loaded up on interest rate risk during QE by purchasing longer-term gilts.

QE “removed interest rate risk from the private sector and transferred it to the central bank balance sheet,” he said.

“QT is now reversing this process and unwinding the interest rate risk held by the central bank,” he said.

“While we will meet the demand for reserves, it does not mean that we should retain the interest rate risk,” he said, which is another reason to shed its longer-term gilts entirely.

But the transition from gilts to repos will take a while, as the remaining £701 billion of gilts in the APF “will take time to unwind,” he said.

So “we would expect a significant increase in our repo operations as we look ahead to the future, and the market should continue to ready itself for this,” he said.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Finally, BoE and the Fed took the right direction, now it remains for the BCE to do it too!

So, instead of the tapdance they’ll go back to the foxtrot. I would suggest the salsa but the English doing the salsa is no bueno.

Not really sure how the switcheroo is going to accomplish anything other than protecting the banks, but as an investor, “there’s got to be an opportunity here somewhere”

You are in the Wealth Conga line whether you like it or not. Can’t see the front. and if lucky enough, can’t see the tail, either.

The conga line, right off the cliff, onto the sharp rocks below.

The British empire a mere 100 years ago was the largest empire in the world…now reduced to a few pubs and a barking dog.

I’d be happy with a pub and a mangy dog…don’t need much.

Not so much Conga as Human Centipede.

Despite all the convoluted operational details involved/described, the only thing that make such things work is…

1) The G’s ability to incrementally/perpetually print money – faster than real asset growth,

Inescapably/definitionally resulting in

2) Inflation in one form or another.

There is no free lunch, magic unicorn pooping diamonds.

All these Fed “salvage” operations come at a cost to the general public, which the most powerful entities in the nation do their best to obscure.

This article is about the unwinding of such operations, but we’ve seen this horror movie enough times, in a short enough period, to expect all this is simply the prelude to the next “fix” – because the fundamental issue (lack of US intl competitiveness) is aggressively distorted by the transitory powers that be.

Seems like the BOE is sobering up the fastest and is going to return to the pre-2008 way of things first. I suppose they’ve been around a lot longer than the US Fed and probably also the BOJ – a postwar creation I’m sure. I’d like to see US QT continue until all that’s left is balanced equal to global cash issuance as it was pre-08. These days that might be $3T but as the BRICS de-dollarize those suitcases of Benjamin’s are going to work there way home to buy assets. Anyway, good to see something responsible happening. Sound as a Pound.

All I can say is “best laid plans of Mice and Englishmen”. We will see how it goes. With the UK still running fiscal deficits, and an overall debt load of close to 100% of GDP, I am not optimistic that things will go according to plan. God forbid that market forces are allowed to set the future path, rather than our Government Oveords.

And don’t get me started on the U.S., which is in an even tougher spot.

Sound as a Pound?? That might have been true in the days of old when knights were bold and one Pound would buy you 6 Dollars, but alas and alack! That is no longer the case. Cable is now close to parity and the perceived ineptitude of the British Reserve Bank governer is one of the reasons that the Conservative Party is going to be consigned to temporary oblivion in July.

Forget the Fed. I would like to see the federal government’s purse reduced to a wallet!

Wolf, I think you have written about why the Fed is justified in ending QT because of its growing impact on the inner plumbing of the U.S. financial system.

I admit to not fully understanding why QT shouldn’t go on much further and reducing the Fed’s balance sheet to levels much closer to pre financial crisis 2008 levels.

Are you suggesting that the Fed could replace its bonds and mbs with repos to manage liquidity in the system like the BoE apparently is trying to do?

So, you’re twisting the issues at little.

The issues are twofold:

1. How low can the balance sheet drop. All central banks have the same issue. The balance sheets CANNOT drop back to the level that prevailed at the time of Adam and Eve, which we have discussed a million times.

The BOE gave you an answer now – see the part about reserves. We have struggled to guess how far the Fed could go at a maximum, which we discussed here. The Bank of Canada also outlined its drawdown limit, to occur in Sep 2025, which we discussed here.

2. What to do with the remaining longer-term bonds after the balance sheet flattens out. The BOE explained its position today: get rid of them and replace them with repos. Fed speakers have said that they would like to see ALL MBS come off the balance sheet, and replace longer-term Treasury securities with short-term T-bills. And they also mentioned the SRF as a way to draw down bond holdings further, while preventing reserves to drop too low, which we discussed in a bunch of places, including here.

The BOE calls shedding gilts “QT,” even when the balance sheet stays level, and guilts are replaced by repos. That language is justified, as QE refers to bond purchases, and repos refer to short-term liquidity supply to the banks, along with facilities such as the Discount Window or the now moribund BTFP.

“Fed speakers have said that they would like to see ALL MBS come off the balance sheet, and replace longer-term Treasury securities with short-term T-bills.”

And, I want to win the lottery, but neither of these outcomes is likely to happen. What the Fed should be saying is that they’ll sign a pledge to never buy MBS again. Then, I wouldn’t be so cynical about how unexpectedly long it’s going to take for MBS to zero out. The Fed can talk all day long. What matters is decisive action. Assuming core inflation stays in the mid threes or rise slightly, how much longer & how much evidence will the Fed need to raise rates, even if it’s 25 basis points to jolt the markets a bit. The best way to get a pullback in consumer spending is for there to be a 20% drop in markets over a couple of months. It’s the people with big stocks & bonds portfolios that are primarily elevating consumer spending.

Good to see BoE actually intending to sell bonds. I’d love to see that happen here in the USA, but with $1.06T in annualized interest expense and higher for longer, that’s just not going to happen. It’s about as likely as the Fed deciding to update it’s core PCE neutral rate from 2% to 3%.

“The Fed can talk all day long. What matters is decisive action.”

Fed Balance Sheet QT: -$1.60 Trillion from Peak, to $7.36 Trillion, Lowest since December 2020

Quantitative Tightening has removed 38% of Treasury securities and 27% of MBS that pandemic QE had added.

Is the MMT era is finally history?

Nope. The one thing both parties agree on is massive deficit spending. They may say they don’t espouse MMT views, but their actions speak volumes.

There was NEVER a MMT era in the US.

Since WW2, the USA military budget has always been run as MMT.

In 1960 the Defense budget was $50B, which was 50% of the Federal Budget of $100B.

The 2024 Federal Budget is $7.3T, and the Defense Budget is $900B, only 12.3%!

It’s shrunk by over 75%!

…excepting, of course, the unknowable ‘black’, and credit-carded DOD expenditures…

may we all find a better day.

“It’s shrunk by over 75%!”

Shrunk in only the narrowest sense.

Typical DC math for over 50 years and why the admitted debt to alleged GDP is well in excess of 100%.

And why both political parties should only really be viewed as self-dealing mafias.

Why on earth would you say that? If anything, it’s accelerating. We don’t have a debt cap until next year. It’s free spending galore nowadays.

That depends upon the definition of MMT — there’s a big difference between the academic version and the public discourse.

re: “While we will meet the demand for reserves”

The free market should determine interest rates, and the Central Bank should target reserves regardless of interest rates.

What “free market” do you suppose that there is where the Federal Reserve target rate is concerned? There isn’t one — the Fed sets it as a matter of policy. All other instruments are priced against that risk free rate — that’s the only “free market” in play here (provided that the Fed doesn’t interfere further out the curve).

Fed sets the shirt term duration via FFR.

Fed should not be in the business f setting long term rates via QE or QT.

Long tern rates should be set by free market.

Via FFR ie Fed fund rates Fed only controls the short term yields not long term yields .

“The best thing undeniably that a Government can do with the Money Market is to let it take care of itself.”

—Walter Bagehot, Lombard Street, (14th ed.)

Sure, John H — and yet, there’s Bagehot writing this during the era during which the British state set the rate at which sterling could be converted to gold (and the circumstances under which it could be converted) under one of its various gold standards (yeah, there have been more than one of those, in case you hadn’t noticed — they’re ALL ultimately fiat regimes in this regard).

So which is it? Bagehot’s hypocrisy or merely ignorance?

Feh.

eg-

Of Bagehot’s hypocracy, I see your point. He councils a “hands off” policy for central banking, while instructing the central bank handlers how best to handle the institution of banking.

I always thought the term “fiat money” referred to paper money, and that the alternative regime was presumed to be metal money, either gold or silver. One of the allures of the 19th century gold standard, aside from its quasi-autonmous operations, was the discipline it supplied to banking and money production. Both features — automaton-like operations and discipline — were the point I think Bagehot was trying to make in the above quote.

You point out that “the British state set the rate at which sterling could be converted to gold.” Isn’t this more of a “weights and measures” issue, in defining (and protecting) the conversion rate at which they could withdraw their deposits from the banking system altogether? My thinking was that if the public is allowed to convert their deposits to a defined amount of gold coin, then that system is metallic, and is not termed as a fiat money system. The fact that the government sets the conversion rate doesn’t make that system fiat, does it?

Maybe I’ve missed your point….

Thank you for your thoughtful reply, John H.

All currency regimes are fiat in the sense that the government sets the terms, including as you observe legal weights and measures. In this sense even metals-based currencies are fiat because the government sets the conversion rate of its tokens to the metal in question. The associated laws against defacement and counterfeit are clues that the tokens themselves, not the material from which they are made (whether paper, metal, digital — whatever, really) are the currency: this is what the government will accept as redemption for its taxes, fees and fines. It’s Knapp’s state money theory or “chartalism.”

All good points, eg.

It seems to me that your definition of “fiat money” marginalizes the most important defining feature of “good” money: disciplined money-creation. Without discipline, self-interested third parties (miners, commercial banks, central banks, crypto-authority, counterfeiters, etc) have a potentially larger impact on supply, and if unchecked, will debase the value of existing money. The “markets” (buyers and sellers of money) are always searching and opting into convenient money alternatives which they believe will better serve them in protecting their wealth/purchasing power.

The 19th century gold standard (with the BIG exceptions of gold conversion Restiction periods, when governments stepped in) did a much better job of limiting money production than our century-long and continually evolving FRS model, IMHO.

I’m guessing you’re not a big Hayek fan, but this statement of his resonates for me: “The gold standard is the only method we have yet found to place discipline on the government, and government will behave responsibly only if it is forced to do so.” (From F. A. Hayek, Toward a Free Market Monetary System lecture, 1977)

It’s interesting to me that the Central Bank in the US was originated as a superstructure to the then existing gold standard, which it eventually superseded and dissolved, an inch at a time. Is that evolution what you meant when you said: “…under one of it’s various gold standards?”

QE was a crime against anybody not wealthy.

Well, and the significant amount of privitization in the energy, healthcare, and housing sector in the UK. Not sure there will be a return to sanity in any of those areas although seems they are trying in the energy sector to some degree. Putting the tiger back in the cage takes a lot longer than letting him out however.

“WAS”?

Let’s turn that into IS. It’s not gone to the grave. That’s for sure.

The rich elderly people had all their savings accounts pilfered by QE. Now they’re the once rich.

The only entity that really profits from QE in the long run is the one in control of the money printer – they create spending power (which they direct) by expropriating the earning/spending power of every other entity.

That is the very definition and destructive power of inflation.

“QE was a crime against anybody not wealthy.”

Agreed.

Bailouts seem always engineered to flip lots of super-cheapened credit into the hands of the wealthy. Then paying for that, long term, is spread across the economy. The little guys got stimmies, but are paying it back in inflation. The rich flipped that extra credit into assets that are soaring, holding value against the debased currency.

That’s been my take on the whole thing too. All that cheap printed money has gotten plowed into real assets to in effect create returns/income from nothing and adding to the capital power base of the wealthy…. with a side bonus of creating jobs for the little guys for awhile I suppose. Now they’ll take that back with inflation.

Won’t QT do the opposite then? I.e. cause asset prices to crash and adding to the capital power base of the poor?

Wolf, how does the BoE account for bonds that they sell at a loss? Do they have a asset account that can go negative, like the Fed does for Treasury remittances? Or do they only take losses when they have offsetting gains? Or (this would be shocking) does the Exchequer make them whole?

The BOE has an indemnity agreement with the Treasury of the UK Government, and it gets reimbursed for any losses on its portfolio. So it’s not a loss to the BOE, but to the UK taxpayer. When the BOE was making money, it also paid all its profits to the Treasury. So it washes out over the longer term. But the government spent the money that the BOE had paid it over the years, and now, with the budget already an issue, it has to pay the BOE for the losses. The amounts that the Treasury reimbursed to the BOE for its losses is now a political issue in the UK.

Does an “indemnity agreement” serve the same function as the “earnings remittances due to the U.S. Treasury” reported on the H.4.1 weekly report of the Fed?

James Grant recently (5/10/24 Grants Interest Rate Observer) pointed out that this treatment of the Fed is tantamount to a loan from the treasury — and interest free, at that! This seems akin to an indemnity agreement between UK Government and the BOE.

Grant compares the soft treatment of the central bank by the Treasury as being “like a running bar tab.” (He avoids using the word “drunken,” though!)

Sort of throws the debate over “central bank independence” out the window, IMHO.

CBs are not at all independent of govts.

Does not matter what people says.

All this is similar in that it effectively doesn’t matter because central banks create money and can never become insolvent. So it’s just an accounting method; when central bank and government books are combined, the issue cancels out.

The Fed remitted to the US Treasury $1.36 trillion since 2001. For the government, this means $1.36 trillion in receipts, similar to tax receipts. In 2023, the Fed stopped remitting, like a company with a net operating loss (NOL) won’t pay any income taxes, and it can carry the NOL forward and take it against income in future years until it is used up. After that, it will have to pay taxes on its income again. Same with the Fed. The company with a NOL carryforward is not considered getting a “loan” from the Treasury. That’s just BS. Same with the Fed.

Thanks Wolf.

The Fed created a different balance sheet gimmick in the event they lose money on open narket operations, which in the beginning they claimed would be highly unlikely.

In essence, rather than remittances to the US Treasury, the Fed will be repaying its special fund until the fund is back to break even, then remittances of any profits will resume.

What effect might this announcement have on yields and the yield curve in UK?

Same question regarding corporate profits and employment (or unemployment) stats?

Thanks

Who will buy the $35 trillion treasuries increasing $1 trillion every 100 days?

If the Fed doesn’t allow free markets to set interest rates, as the auctions increase, they will be forced to continue support however they label it..

Repos, reverse repos and other central bank intervention “tools” are a smokescreen making hard nosed analysis difficult if not impossible.

For now t’bills work for me. Long bonds need a big adjustment to provide real returns for a lot of risk.

Cheers,

B

PS. And, how about agency debt and unfunded liabilities?

Why wouldn’t the Fed let the free market set the treasury bond and note rates? At least as long as inflation stays above 2%, and likely as long as it stays above 0% without any Fed support?

Eventually, Congress will get the memo and solve the problem with the deficit. They did in the 1980s, no reason they can’t again. It’s not even that hard, just have to slaughter a few sacred cows.

Howdy Cody. How did Congress solve the problem in the 80s? All I remember was inflation and spending…….

The problem identified by Brewski was “Who will buy the $35 trillion treasuries increasing $1 trillion every 100 days?”

If Mr. Rieter will allow me to post a link to his article on the US government’s interest expense as a fraction of revenue, the answer is there.

https://wolfstreet.com/2024/03/31/curse-of-easy-money-us-government-interest-payments-on-the-ballooning-debt-v-tax-receipts-amid-higher-interest-rates-inflation/

All though, looking back at the graph, my memory might have forsaken me, as it doesn’t seem that Congress got the memo until roughly 1992 or so.

By reducing tarrifs, setting up factories in China and killing the labor market (8% unemployment), raising taxes, they lowered the demand of goods and services from the bottom up, I assume? At least that is what I learn by reading from those times. Never lived it thou. Wolf, care to chime in?

That was the CCP’s plan, actually. The congresspersons just got “contributions” to look away and do nothing. However, BYD now reportedly is taking 275 days to pay suppliers; Nio, 295 days, etc.

Those jobs are now leaving China. Soon! LOL

If the yields go back to 14% like in 1981, just about everyone will want to buy them.

Mexico Bond yields hit a low of 5.3% in 2021. They are now above 10.1%. i wonder everyone is buying those bonds? They have not been this high since 2005. LOL

10 year bonds

Everyone will want to buy them — and is buying them now already — because the yield is high enough. And it always is high enough, because that’s how auction systems work. When the 10-year yield hit 5% in late October 2023, demand exploded, and pushed yields back down.

What happens if banks don’t have enough collateral to post at the standing repo facility due to the falling prices of bond and securities to meet the demands of a possible out flows and other stresses in the banking systems? Their idea of “Preferred minimum of reserves” seems good in theory but in practice it would depend on multiple variables. Wouldn’t the unrealized losses of their assets of the banks be a variable to take into consideration?

Hopefully this system entices banks to sweeten the deal to its depositors, thus holding on to their money and preventing what you explain from happening.

If banks don’t have enough collateral they can post, they’re toast. Happened to SVB et al.

Unrealized losses in CRE, sub-prime, auto loans, overvalued, residential real estate in states with anti-deficiency laws, loans to over-leveraged companies, some with investments in a hostile, imploding country, etc., make me wonder how many banks are still solvent. After all, their capital asset ratio has long been from fantasyland, since they do not mark their “assets” to market.

This is BS because banks are not on the hook for most of the debt you list — as we have pointed out here a million times. The taxpayer is on the hook for most residential real estate debt and a majority of multifamily CRE. Investors are on the hook for the majority of the remaining CRE debt. Investors are on the hook for the vast majority of corporate debt (bonds, corporate paper, leveraged loans, etc.). Investors are on the hook for the vast majority of investments in China, if that’s what you’re referring to. It’s investors that have lost and will lose a shitload of money. If you had read the articles here, you’d know that.

“What happens if banks don’t have enough collateral to post at the standing repo facility…”

The corollary is this encourages banks to keep enough collateral (treasuries) on hand.

Everything the Fed does is designed to keep the Treasury market liquid.

Is there a visible difference in the interest rates when comparing FED, BoE and BuBa?

I check 10 yera bond yield for US an Germany but not Brirain.

Just from a short look at the 10 year yield in Britain the upturn looks sharper and more pronounced then in the US or Germany.

It is very (bitterly) funny to watch one central bank after another tacitly admit that QE was a massive policy error.

Yes and they will be paid to screw up the system, act like they saved the sytem (without admitting they screwed it up in the first place) and offered the lectern all over the world to admit it and get paid for it. Shameless rascals would also act as if God sent them here to save the world. Greenspan is the name that springs to one’s mind

Pea Sea,

Yes, what’s funny is just how tacitly they’re doing this.

Yet QT must be moderated.

Less.

Longer.

FYI: “moderated” is a tripwire.

Roger.

Better late than never.

Any thoughts on how on earth the financial sector managed to persuade the Central banks it was necessary for them to start carrying the interest rate risk?

“Gilt” Madison Ave & 50 st NYC is permanently closed for O/N collateral.

But qe saved us. Without qe we could have had real price discovery and real interest rates. And we were told it was all to save the system. We were also told inflation was transitory. Oh, what a web they weave.

Fool me once, ah ah we won’t get fooled again!

Yes, we will. That’s about the only constant I see in the world. Bunch of people go around yammering about how they’re saving the world this time and everybody jumps on the gravytrain and Repeats till True… :(

BoE selling across the curve? Che knout the Fed sales – they aren’t touching the 10+ year notes.

A couple obvious reasons to do this, but I find it amusing all the talk of BoJ ycc when the Fed is effectively doing the same by helping the curve remain inverted.

However, the Japanese yield curve is not inverted, and has not been inverted. That was in part the purpose of YCC, and the BOJ explained it in 2016 when it started YCC. They wanted to keep the 10-year yield above 0% to keep the yield curve from inverting (with short-term rate negative). When they instituted the YCC, the 10-year had dropped into the negative already, and the yield curve had inverted in the negative. But YCC pulled it out of the negative.

The different reasons and policy goals between the two central banks are beside the point. The Fed’s reasons seem pretty straightforward – inverted curve supposed to signal slowing economy, makes it harder on banks, etc., and limiting duration losses on QT. What amuses me is in a market full of talking heads who will yammer on about every possible economic data point, I haven’t heard a single peep about this. Maybe there is nothing to see, but nobody talking how the bond market isn’t inverting the curve, the Fed is? Or, what happens to the long end when the Fed runs off the shorter duration holdings and moves into liquidating long?

Also beside the point, If I were the Fed, I’d be tempted to double the short end run off and spend half that on 10+ yr at 60 cents on the dollar (keeping runoff speed the same but adjusting their balance sheet mix).

Why does this distinction – bonds or repos – make any difference in terms of expansion/contraction of the money supply?

Why does it make any difference in terms of money supply if someone buys a CD for less than $100k (included in M2) or more than $100k (not included in M2). Money supply alone, the way we measure it, does not give you answers and is a worthless metric.

Repos with banks v. bonds purchases makes a big difference. With repos, the Fed lends money to the banks short-term against good collateral. With bond purchases, the Fed douses financial markets with cash and drives up asset prices.

Aside from reported M2 effects, isn’t the effect on actual monetary expansion the same if the repos are perpetually rolled over for as long as bonds are not retired?

No, the effects are not the same, as explained.

agreed, but it is a step closer to outright MMT.

Yellen has been issuing like crazy in Tbill market rather than coupon/duration to tap into the RRP account (which is just the excess Covid QE money) and fund the crazy deficit spending. From the government funding perspective, this has been an awesome free money pit that UK government no doubt wants a piece of.

BoE announcing a shift to short term repo funding will keep a lid all GBP money market yields which includes UK Tbill yields, thus allowing government to shift its deficit financing to short term rather than coupon/duration.

Its then only one step away for the BoE to just outright buy UK tbills in a revolving short term financing door of MMT heaven.

US Treasury is issuing more T-bills because they don’t want to lock in these higher interest rates for 10, 20, and 30 years. Their bet is that rates will come down, and then they’ll finance long-term at lower rates. That bet may be wrong. But that’s the thinking. If they’re correct, that’ll save the taxpayer money long-term.

That is very different from a central bank switching from long-term to short-term assets. Short-term rates are bracketed by central bank policy rates. These policy rates include repo rates. So if central banks switch to short-term investments (T-bills, repos, etc.), it will have no impact on short-term yields because they’re already bracketed by policy rates. But reducing the support for long-term assets might increase yield for longer-term securities.

This is all fine and mainly talk. Also, you have run a system for 15 years and you are now telling us that you have run a ruinous system. Reminds me of Jack Welch and GE.

That said, it misses the point that the central banks’ put (that it will come riding to the bank’s rescue on the way down) that creates the whole mess. Due to CBs’ put there is all the incentive for banks to take all sort of risks on the way up and put the mess on tax-payers’ plate when the SHTF. Also, it messes up capitalism which is essentially that there should be a cost to capital and the risk-taker becomes the risk-taker. But, in a lop-sided system we have, this is given a go-by. That is why these CBs are thought by some as “arsonists & fire-fighters” rolled into one.

The most sensible approach is to make sure there is significant disincentive for banks to taking risks that can bring the system down. Anyone with a bit of common sense would tell you that this means the cost of capital should be extremely high as the risk goes up. But these all-knowing jaw-boning CBs are eager to rush in to reduce interest rates as soon as they can (Dec 2023) and always late to the party when it comes to raising rates (inflation is transitory).

The irony is these guys can screw the system as much as they want and then they will come giving us lectures at different places. Slippering such guys is not a bad idea at all.

Very true and some of these bankers even got Noble prize.

Here goes the credibility of Noble prize.

The BoE maintains the QT way, while the Fed leave them… Generally, the BoE´s situation is far different, beause their portfolio have a (very) high duration, with bonds they mature in 2070. I personally expect, the BoE testing their “reverse enquiry windows” operations again as they have done with their financial stability gilt portfolio, because the experience was not so bad.

The goal must be to shift the banking system back to the repo liquidity providing, and not holding them in the ” we flood all with QE” modus.

Thanks for the clear explanation of repos.

Removing the all-consuming buyer of bonds should move more of the bond market into the open, where competition and limited demand can start to restrain borrowers. When the central bank automatically buys all bonds, there’s no restraint.

MSN: How private equity rolled Red Lobster

When a private-equity firm bought the iconic seafood chain in 2014, it sold the real estate under the restaurants for $1.5 billion. Then the restaurants struggled to pay the rents.

Angry that your favorite Red Lobster closed down? Wall Street wizardry had a lot to do with it.

Red Lobster was America’s largest casual dining operation, serving 64 million customers a year in almost 600 locations across 44 states and Canada. Its May 19 bankruptcy filing and closing of almost 100 locations across the country has devastated its legion of fans and 36,000 workers. The chain is iconic enough to be featured in a Beyoncé song.

Assigning blame for company failures is tricky. But some analysts say the root of Red Lobster’s woes was not the endless shrimp promotions that some have blamed. Yes, the company lost $11 million from the shrimp escapade, its bankruptcy filing shows, and suffered from inflation and higher labor costs. But a bigger culprit in the company’s problems is a financing technique favored by a powerful force in the financial industry known as private equity.

The technique, colloquially known as asset-stripping, has been a part of retail chain failures such as Sears, Mervyn’s and ShopKo as well as bankruptcies involving hospital and nursing home operations like Steward Healthcare and Manor Care. All had been owned by private equity.Asset-stripping occurs when an owner or investor in a company sells off some of its assets, taking the benefits for itself and hobbling the company. This practice is favored among some private-equity firms that buy companies, load them with debt to finance the purchases and hope to sell them at a profit in a few years to someone else. A common form of asset-stripping is known as a sale/leaseback and involves selling a company’s real estate; this type of transaction hobbled Red Lobster.

That Michael Douglas movie character.

The question on everyone’s mind, is when long term treasury rates will get sustainably above 5%.

They have been flirting with it off an on for about a year.

It seems like there is a ton of demand there, but this might be “speculative rate cut fever” demand, as opposed to people buying and holding.

What do people think?

I doubt if 10 year yield would go much above 5 percent as even at current rate the demand is quite strong .

But short rates are above 5%, and they’re not going down.

Inverted yield curve is unnatural and won’t stay that way forever.

Rate cut hopium is the only reason bond traders are long duration right now. Once they accept reality, long rates will rise above short rates.

I noticed something interesting with Agency bonds– it is now quite easy to get 10, 20, and 30 year agency bonds with yields around 5%, even in small and/or odd lots.

Because they are callable bonds, I am picking bonds trading at 75-85% of par, so if called would be called at 100% plus accrued interest.

This indicates to me that people buying those tenors of Treasuries are doing so because they are making a bet on future interest rates (meaning back to zero rates, QE, etc.), or that they need to have the option to pledge them as collateral.

At some point this has to stop. Losing money for 4+ years on long duration treasuries should cause people to throw in the towel.

Inverted yield curve used to be predictor of business cycle recession barring fed intervention.

Now this yield curve is broken because of Fed intervention.

Short rates are controlled directly by Fed via FFR.

Long rates are dictated by markets except Fed intervention via QE.

TulipMania – make sure you’re looking at the yield till maturity and not just the coupon. Many agency bonds have high coupons but trade for a premium on the secondary market.

Also, 5% on 10+ years of duration isn’t a very good deal imo. You’re taking on duraion risk for less than the risk-free rate.

Disclosure; I own a couple 10-year agency bonds at 5.75% & 5.98%. But they are a tiny part of my portfolio as I generally expect rates to continue rising.

Hard to say. I think inflation needs to appear entrenched, plus Dove Jay saying and doing Dove Jay things. Most scenarios seem unlikely: 1. Fed cuts prematurely, letting go of their tenuous grip on inflation. That’d send longs higher. 2. Next couple months data comes in hot while the poor comps rolling off make inflation seriously back on the upswing and the Fed doesn’t get hawkish enough. That’ll also send longs higher.

I think option 3 is most likely. Data comes in hot + poor comps rolling off PCE and CPI. Fed has to get tough again. Long creeps up, but then falls as the Fed picks the hammer back up.

Jolly O! Good Show Lads!

Spread some Marmalade old chap!

A spot O tea Longfellow!

🫖 🇬🇧

IDK, but it sounds to me like they are trying to manage everything by manipulating liquidity margins. Managing nervous actors but not fundamental actors.

It’s one thing to manage the interest rate/expectation profit of a promise versus the actual principle value of a promise.

Rollover US promises anyone?

[1D] US30Y Bond backbone : Sept 28/29 2023, 4.808%/4.648%. Options : 1) US30Y might cross the BB and reach/breach Oct 2023 high @5.178% before backing up.

2) The BB area is resistance. US30Y might drop for a sling shot up.

3) A major heart attack.

“Back to the future: With repos, not QE, is how central banks handled issues before 2008. The Fed also revived tools to go back into that direction.”

Wolf, did the UK have an unsecured interbank market (similar to Fed Funds pre-2008), or were their banks’ liquidity needs always met with repos?

Yes. LIBOR was based on unsecured interbank lending. But the interbank lending market has withered (one of the reasons LIBOR was phased out, the other reasons were related to the scandals). And that’s a good thing because during the Financial Crisis, the interbank-lending market suddenly froze because banks didn’t trust each other anymore, which is a big issue with unsecured loans, and this form of liquidity that banks had relied on dried up overnight, which was part of why there was so much contagion. Unsecured interbank lending was a big aggravator in the Financial Crisis.

US10Y – US2Y = (-)0.5. Will the 10Y rise > the 2Y.

Will the 10Y rise > the 2Y[?]

Yes.

Never Again.

hmmm, something does not add up…

– CBs cannot just simply switch from couple of huge QEs back to Repos after bubbling everything up to the Moon, otherwise Buffet is genius and S&P will be quickly back down to 1000-1500, not to mention other assets that will quickly follow.

– Any banker that post high quality short term collateral WILL NOT use received currency for high risk and/or leveraged bets, this means, there will be high degree of deleveraging of the systems, again assets quickly back to the Earth.

– PMRR will NEVER EVER be objectively observed as far as there is 2 % inflation target and destruction of purchasing power. CBs will be blindly guessing possibilities on Minimum Ranges, meaning higher volatility of balance sheets as they will try to dance on a rope.

– QTs will continue even if interest rates drop, there is still too much LIQUIDITY sloshing around.

There are things that CBs are not telling you. QE is a tool that will be used again in the future, but not in the form you know. They will have to slowly deflate bubbles, before fully rely only on Repos.

“QE is a tool that will be used again in the future, but not in the form you know.”

???

BeeKeeper-

Re: your comment “QE is a tool that will be used again in the future, but not in the form you know. They will have to slowly deflate bubbles, before fully rely only on Repos.”

This rhymes with an Econ Focus article I saw on Richmond Fed site entitled: The Fed Is Shrinking Its Balance Sheet – What Does That Mean? (Tim Sablik, Third Quarter 2022)

The author gave several reasons why they want to shrink the balance sheet. Beside “composition” (i.e. whistling down MBS holdings), and reducing loss exposure, the author included a section entitled “Reloading for the next crisis.”

Your point exactly, I think. Emergency measures are quick and relatively painless to install; mopping up the liquidity thereafter is slow and painful. The asymmetry of these actions, and the politics of pain avoidance, lend a distinct inflationary bias to central banking, IMHO.

Cheers

“Reloading for the next crisis.”

LOL, this BS in BS-Forbes never stops.

The Fed — and the BOE — have already said how they will handle it next time when have already cut rates to 0% (unlikely) and they need to stimulate further: They will shed T-bills/repos and buy longer-term securities, to where the balance sheet does NOT grow, but longer-term securities grow and short-term T-bills/repos decline in equal amounts.

I covered this here when Waller laid it out, but you people prefer this BS-Forbes-BS over what central banks are actually telling you they will do because it suits your narrative??

I blame you for dragging this BS into here, but I kind of cannot blame the blogger on Forbes (Forbes has largely become a collection of paid independent bloggers) because the Fed’s Waller explained it a couple of months ago, and the BOE explained it last week, and the BS-Forbes piece was just QE-mongering written in 2022.

Exactly as Wolf has explained many times, CBs will try to balance their Balance Sheet, dancing on a rope, balancing between short and long spectrum while at the same time trying to deflate assets bubbles. Consequently, you will not see typical QE/QT (Balance Sheet slowly QE-increasing/QT-decreasing), but instead higher volatility ups/downs while rebalancing.

Before the time of crisis, CBs will build up big enough short term Repo positions to counteract potential QE and low liquidity events.

Time of beautifully raising all inflationary bubbles is over! There will be more frequent use of QT tool, along side Repos/QE tools.

Let’s see what governments will do about it.

Looking forward to the next Fed Balance sheet update with all the nice charts breaking everything out. Spent some time in the woods over the weekend thinking about grandkids and how/if they’ll ever be able to have the houses, vacations, cars that we’ve all had for the last fifty years. It doesn’t look so rosy. So I daydreamed a little about bluer skies..

I’d like to think the Fed can get to “3 by 30” – that is $3T – all Treasuries – by 2030. If they can leave the $25+35B QT in place for 66 months they’ll make it, more or less.

I think these next five years or so are going to be pretty rough economically. Either guy is going to have a very hard time keeping it all together, I guess we just hold on for the ride.

The lecture linked in the article was an interesting read. I quote one of many passages worth highlighting from it, since this issue of money creation pops up in comments often:

“Commercial banks can create money simply by extending loans to their customers. It is worth pausing at that sentence. It is the answer to one of the simplest but most teasing questions I get asked, particularly when I visit schools: “how is money created?” The majority of money is created when banks make loans to their customers.”

from The importance of central bank reserves by Andrew Bailey

Banks DO create money. They create the vast majority of it.

Bullshit. Learn how to read. “BANKS.” The banking system as a whole, not an individual bank, and it happens when collateral prices rise that banks lend against and that get paid off at higher prices, creating bigger deposits in the banking system as a whole.

One single bank cannot create money. A bank can only lend money that it already has (borrowed or capital). If a bank runs out of money, it cannot create money to stay afloat, it just collapses, see SVB, which collapsed because ran out of money 🤣

Wrong.

Wolf, for your final graph, is it supposed to be millions of GBP rather then billions?

This graph expresses the total value of the bonds (gilts) held by the BoC at two points in time (the two colored curves) per the maturity of the bond. If that’s correct, then we should be able to sum the values across the most recent curve to arrive at the total value of the gilts currently held by the BoC… Which would be an amazingly massive number if “billions” is the right denomination!

“This graph expresses the total value of the bonds (gilts) held by the BoC at two points in time”

Bullshit. Learn how to read. Text says: “The chart shows the maturity profile of the remaining bonds in the APF as they had been on two dates: in February 2022 (blue line) and now in May 2024 (red line).”

It expresses the “maturity profile” and NOT your imagined “total value of the bonds”

Some points people may be interested in. RPI inflation in the UK has been cumulative 30% over the last 5 years. Infation is really quite a shocker here.

Additionally there is now a question over the BoE independence because their actions determine the fiscal headroom of the current government. This point being observable with the Liz Truss disaster as she announced her borrowing plans the BoE concurrently announced major gilt sales leading to a crisis of confidence.

On top of this the Conservative government, the incumbents, are widely expected to be wiped out at the election in 6 weeks and the Labour party have already announced plans which despite their denials -must- require further borrowing.

So I wonder if the BoE can actually follow through with this plan, although it does seem to be the best course of action. They might just be jawboning for the market effect.

There is no longer any amount of paper games that will address the rapidly declining standard of living for the average person on earth. The real underlying problem is 50+ years of global mismanagement and misallocation of capital and resources. How do we prevent this? ALLOW bad management to FAIL. Punish bad behavior. Unfortunately, monetary and fiscal discipline is long dead. Welcome to the techno-feudal era.

Hedge accordingly.