No one knows, not even Fed, but here is our guess: $5.8 trillion, limited by the liabilities.

By Wolf Richter for WOLF STREET.

The Fed has been talking a lot about its liabilities recently, including Powell at the FOMC press conference the other day, the FOMC members as reported in the meeting minutes, and in speeches Fed governor Chris Waller and Dallas Fed president Lori Logan. The discussions have centered on how to get to the smallest possible balance sheet. And it’s the liabilities that determine how far QT can drive down the balance sheet’s assets.

During periods of QE, the balance sheet is driven by the assets that the Fed buys, which inflate its liabilities in equal amounts.

During QT, it’s the liabilities that determine how far the balance sheet can theoretically drop – the lowest theoretically possible level – which is now the red-hot topic because the Fed doesn’t know either. But as Powell said, the Fed needs to be careful as it gets closer to that point, wherever it is, because stuff happens when it gets below that point. The issue are reserves.

Liabilities represent liquidity of others in the market. They’re cash that the Fed owes others. Two of them represent liquidity that banks (reserves) and money market funds and other entities (ON RRPs) have stashed at the Fed, and those two are now being drained by QT. The other three are independent of QT.

Total liabilities: $7.47 trillion, down by $1.45 trillion from the peak in April 2022.

Every balance sheet, including the Fed’s, has to balance (Asset = Liabilities + Capital). The Fed’s capital is set by Congress. So for every dollar that assets decline, liabilities must also decline by a dollar. And so far, QT pushed down both assets and liabilities by $1.45 trillion from the peak in April 2022.

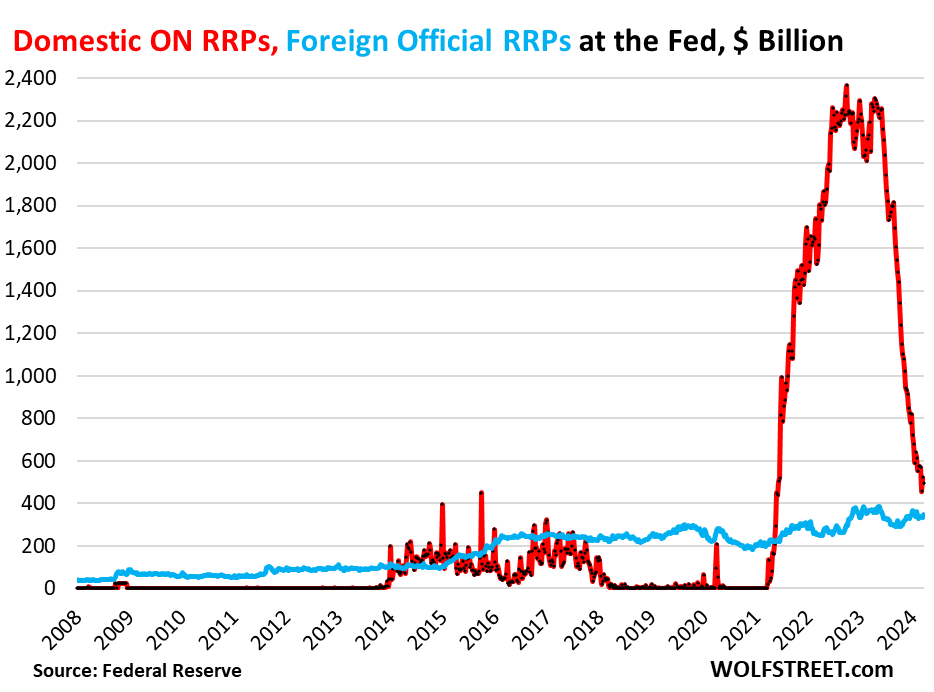

The big five liabilities. We split RRPs into two separate parts because they’re so different: ON RRPs with domestic counterparties (#2), and RRPs with foreign official counterparties (#5).

- Reserves (cash that banks deposit at the Fed)

- Overnight reverse repurchase agreements (ON RRPs) with domestic counterparties (cash from money market funds and other domestic entities)

- Currency in circulation (paper dollars in pockets and under mattresses globally)

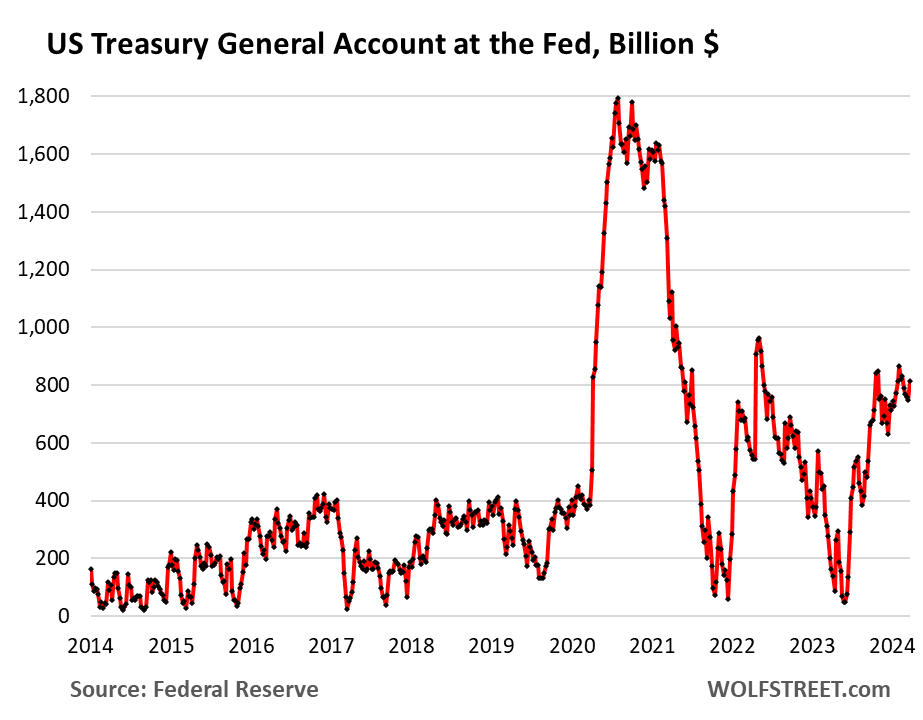

- Treasury General Account (TGA), the government’s checking account

- Reverse repurchase agreements with foreign official counterparties.

The two liabilities that are reduced by QT: Reserves and ON RRPs.

Reserves: $3.55 trillion, -$722 billion since Dec 2021 peak. Reserves are instant liquidity in the banking system. Since the last rate hike in July, the Fed has been paying banks 5.4% in interest on their reserve balances. For banks, on their balance sheets, reserves are “interest-earning cash” or similar.

QT is draining liquidity from the financial system, and reserves are one place where the drainage shows up.

Reserves are what the Fed looks at to determine how far it can take QT. Toward the end of QT-1, reserve balances dropped so low (below $1.4 trillion) that banks stopped lending to the repo market, even as repo rates began to rise sharply and it would have been profitable for banks to lend. And so the $5-trillion repo market blew out, and the Fed ended up stepping in to douse the panic.

So $1.4 trillion back in 2019 was too low. This time around the lowest level will be higher since everything has grown, and Powell has said that no one knows what that level will be, but they will keep their eyes out for signs that they’re approaching that level.

Note the sharp drop in reserves from December 2021 (QT started in July 2022) until the March 2023 bank panic, after which cash started flowing back into reserves.

This time around, the Fed intends to be smart about it. In July 2021, it put back in place its old Standing Repo Facility that it had killed in 2009 during QE. And it will eventually reduce the pace of QT so that it can approach the lowest possible level of reserves slowly, and back off before it gets there, rather than bumble into it and watch something blow up.

Banks use their reserve accounts at the Fed to transfer cash between banks; every transaction between two banks goes through their reserve accounts, with every bank paying every bank and getting paid by every bank once every day. These reserves are not a static inventory of cash, but a huge daily churn between banks.

ON RRPs: $496 billion, -1.87 trillion from peak. The Fed offers overnight reverse repos (ON RRPs) to domestic counterparties, mostly money market funds. But other approved counterparties are the banks, government-sponsored enterprises (Fannie Mae, Freddie Mac, etc.), the Federal Home Loan Banks, etc. These entities use RRPs to park excess cash at the Fed and collect 5.3% in interest.

ON RRPs represent excess liquidity that money markets don’t know what to do with. ON RRPs have existed for decades, but in normal times, they’re zero or near zero. It’s only in the later stages of QE through early QT that the balances balloon as excess liquidity is everywhere. And now they’re going back to zero, which is their normal state.

The liabilities that are not reduced by QT: Currency in circulation, the TGA, and foreign official RRPs.

Currency in circulation: $2.34 trillion. Currency in circulation reflects the paper dollars – officially, “Federal Reserve Notes” – In wallets under mattresses in the US and globally. Demand for Federal Reserve Notes soars during uncertain times, such as Y2K (will the ATMs work on January 1, 2000?), the months following the Lehman bankruptcy, and Covid.

The amount of currency in circulation is demand-based through the US banking system. If customers demand paper dollars, the banking system must have enough on hand. Foreign banks have relationships with US banks to get paper dollars for their customers.

Banks get those paper dollars from the Fed in exchange for collateral, such as Treasury securities, which are assets on the Fed’s balance sheet.

So every dollar of currency must be counterbalanced by a dollar in assets. As currency grows, so do assets. That has always been that way. Before QE, currency in circulation was the primary driver of the size of the Fed’s balance sheet. So the Fed’s balance sheet can never fall below the level of currency in circulation.

Currency in circulation has roughly flatlined since July 2023 at around $2.34 trillion. It is very unusual for currency to flatline for so long, it normally just grows. But maybe higher T-bill rates are persuading some holders to deposit their paper dollars in the bank and buy T-bills with them to earn 5.3%, rather than nothing.

Treasury General Account (TGA): $813 billion. The Treasury Department’s checking account at the New York Fed has massive inflows from debt sales, taxes, fees, etc., and massive outflows to pay for the actual government spending every day. The amount in the TGA is a liability for the Fed – money that the Fed owes the government.

During periods when debt sales are limited by a debt-ceiling fight in Congress, the TGA gets drawn down to very low levels. After the debt ceiling fight is resolved, the government issues a lot of T-bills quickly to bring the TGA back up to operational levels.

So account balances are not influenced by QT or QE, but by the Treasury Departments management of the government’s finances.

RRPs with foreign official counterparties: $349 billion. The Fed also offers reverse repurchase agreements to “foreign official” accounts, where other central banks can park their dollar cash. The account balances are determined by decisions of foreign central banks and are not a result of QE or QT.

The chart shows both, ON RRPs with domestic counterparties (red) and RRPs with foreign official accounts (blue). ON RRPs will go to zero; foreign official RRPs will not go to zero, but will likely remain near the recent range.

The “lowest possible level” of the Fed’s balance sheet in 2026?

No one knows, not even Fed, but here is our guess: $5.8 trillion, limited by the liabilities.

The minimum balance sheet level is determined by the liabilities. In the current setup at the Fed of “ample reserves,” it’s the reserve balances that the Fed will watch. If reserve balances drop too low, as they did in 2019, bad things can happen. Let’s say this theoretically lowest possible level of ample reserves is $2 trillion in two years. Add a little margin of safety, so maybe $2.2 trillion.

In this scenario, this lowest possible level of the balance sheet in this scenario would be $5.8 trillion, below which the balance sheet cannot decline without something blowing up:

- $2.2 trillion reserves

- $0 ON RRPs

- $2.38 trillion currency in circulation, tends to grow over the years.

- $900 billion TGA

- $350 billion foreign official RRPs.

Realistically speaking, getting the balance sheet close to $6 trillion by the end of 2026, so shedding another $1.5 trillion, after the $1.45 trillion that have already been shed, will be a big improvement, meaning that the Fed’s balance sheet will by then have shed about $3 trillion, assuming that nothing blows up along the way.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I have serious doubt the reserves will ever reduce to $6T or so. FED will much more likely to stop earlier. Even if it reduced to 6T, the balance is more than 50% higher than prepandemic (little less then $4T). I know it is not that simple, but some simple principles hold in macro-economy overall. It partially explains why most assets are 50% or more expensive when compared to prepandemic. Goods and services will probably follow slowly. Dollar lost 17% of its value compared to Jan 2020 already.

The era of 2% inflation is over. We need to get used to 3-4% inflation rates at least until the end of this decade at least. We are in a new era now. Bulls are in charge. FED is not strong as it was before. There was a rule in the past: “Don’t fight the FED”. Now it is: “Don’t fight the bulls and never trust on currency.” Assets will never go down in the long term. If you don’t believe, look at BTC.

“Don’t fight the bulls and never trust on currency.” this is the most stupid statement I’ve ever read

“The era of 2% inflation is over. We need to get used to 3-4% inflation rates at least until the end of this decade at least.”

So – what would the Fed accepting 50-100% more inflation in one move do to Wolf’s “no pivot” argument ?

In my book ,The Fed accepting 50-100% more inflation is a massive pivot.

….(now about that wonderful EV revolution sweeping the country ) ha

It means higher rates for longer, that simple. There is no pivot. Rates are going to stay high. Maybe they’ll do one-and-done cut this year, or no cut this year, and then hike again later, or something like that. We’re back to how it used to be. I hope you kissed those low interest rates goodbye.

This kind of $34.5 trillion debt can only be managed with inflation and big nominal economic growth, everyone knows that, because even if you cut the deficit to zero (not ever gonna happen), that $34.5 trillion in debt is still out there and has to be dealt with, and inflation will do it.

And, say 1960 Tax tables (adjusted) are simply just out of the question because our “CCP equivalent” just doesn’t like them?

Also, the Democratic National Corporation and the Republican National Corporation “workers” sure make a lot of money mostly for just putting on ever more crappy show….wonder how long they will last?

Here’s a good website Dustoff suggested I monitor, he does. https://www.noaa.gov.

I just found WS (maybe 1/2 or a year before the SF reader/commenter party…..forgot date of that) and that article gave me a real headache and still generated a lot of questions I won’t bother you with.

But I have a better econ picture than I got from CNBC or anywhere else…..and the chance to see my 2 cents in print, FWIW.

Time for a wealth inequality article?…it’s getting bad, I think.

Thanks

I added link because or Mark’s last sentence….Ha=sarc? and is a ref to the “debate” that always accompanies mention of EVs, I guess….

“Managing” debt by inflation is a sick and pathetic way to do it. It isn’t managing at all, it’s cop out quitter crap and whatever officials and citizens choose it ’cause they can’t stand up for austerity are acting with the opposite of real leadership and courage.

shameful,

Sure, but inflation is how it is done. And inflation is the broadest tax of all because it also applies to asset holders. They cannot escape it. Anything denominated in dollars – assets and labor both – is going to lose purchasing power with the dollar. So for asset holders, the hope is that 1.6% dividends, or 5% interest, and/or asset price increases, if any, make up for the loss of purchasing power due to inflation. The Nasdaq is about flat with Nov 2021. But it lost 10% of its purchasing power due to inflation since Nov 2021. So holders of the Nasdaq composite paid that 10% inflation tax, and they got no capital gains to make up for it, and they got only something like 3.5% in dividend yield since Nov 2021. That’s why everyone hates inflation for their personal lives, though companies like moderate inflation because it equals price increases with means revenue increases and so they look better, even if their costs go up.

Sorry for my impertinence. I got upset failed to hold my peace. Thanks for your patience.

Yup the markets are totally deluded !!! No rate cuts until Sep 2024 !!! Then in next 3 months till Dec 2024, the Fed has to decide to reverse course by RAISING RATES 1X OR 2X, not cutting rates !!! All bcos of stubborn inflation !!! You read it here first !!! Dont say you were not warned !!!

The Fed is wrong from time to time in their predictions of the future (of course – everyone is) but they seem pretty resolved at getting inflation back to 2% and are taking steps to ensure they don’t get sidetracked, barring some dictator for one day.

It could indeed take until the end of the decade because of the bulls but there are worse possibilities.

The Fed is publicly signaling that CONgress needs to balance the budget. Of course, we all know that the corporate owners of the Fed also OWN our “representation”.

I respect Wolf’s analysis, but will maintain that the Fed will not be able to get their balance sheet below 7 trillion, mainly because of the political puppets in DC. You can call me a cynic, but then you should also consider the last time we actually balanced the budget. Really getting tired of conspiracy theories becoming conspiracy facts…

You should save the links to your comments of this type so you can hit me over the head with them when I post my regular monthly QT update with the headline, “Fed Balance Sheet QT: -$2.0 Trillion from Peak, to $6.9 Trillion, Lowest since….”

Just do some basic math. The BTFP ($160B) will go to zero by March 11, 2025. RRPs ($480B) will go to zero this year, and so without reserves changing at all, we’ll be below $7 trillion. But reserves will be coming down too because that’s the actual goal of QT.

The year isn’t over yet Wolf. It’s just a fact. We are not below 7 trillion yet. PERIOD.

If you are so sure, then take my bet and put your money where your mouth is.

WB,

Why would Wolf take the bet of a loudmouth when he can bet on the markets?

We have this site and his articles and comments to hit him over the head with if that’s what you want to do should that ever happen.

So approximately 50 percent done with QT from your analysis which I think is pretty good assumptions . Over time as they taper QT so they don’t blow something up the target would still land around 3t total based on your analysis. Since the first half has taken 2 years the 2nd half will take 4?? That’s my guess

The first half, including the slow phase-in, has not taken “2 years” but 20 months.

From the beginning, the Fed said that this would take years, that it would run in the background for years. Through the end of 2026 should get pretty close

Thank you for that clarity and your focus! Your posts always stimulate me to look for additional educational opportunities, but this is a great example of you being an excellent factual resource and authority.

My only curiosity now, is how a lack of rate cuts dovetails with this QT. Boston says he’s thinking one cut, which is slightly different than what a lot of people were pondering.

Just wondering how the next three trillion of deficit spending affect the Fed balance sheet?

The balance sheet will keep declining, that’s how the deficit affects the balance sheet, same as over the past 18 months.

@ Wolf –

How about how the deficit has affected the balance sheet over the last 36 months?

What is the cause and effect between the deficit and the FED’s Balance Sheet?

cb,

The balance sheet today ($7.51 Tn) declined by 2.7% over the 36 months since March 2021 ($7.72 Tn), while the debt as surged over the same period by 22% from $28.1 Tn to $34.5 Tn.

Can I see “cause and effect between the deficit and the FED’s Balance Sheet?” I cannot, to be honest. I mean, why would the balance sheet decline over the 36-month period, while the deficit soars?

But interest rate repression since 2008 certainly encouraged Congress to borrow like a maniac. And we’re seeing the fruits of that.

Thanks for asking that question cb, (and the other questions & comments). The more I read the more I understand. It’s like being in a class.

I really HATE econ, (hence the headache mentioned above….not a real one) but it is too much a part of my life to ignore.

Thanks NBay,

I really appreciate being a part of the Wolf Street community. He is the best I know on finance anad money, and he is willing to answer questions and to help ,,,,, most of the time. Also there are some very strong, smart commenters on this board. Just by hanging around, most of us get better informed and figure more out —- me at least, or so I think. I wish I had more bandwidth to better absorp all the great stuff he puts out.

The year 2026 is interessting timing since the Tax Cuts and Jobs Act will create a significant shock to the pocketbooks of almost every taxpayer that year. The standard deduction will be cut in half and the standard exemption might come back, but at what dollar level? Also, every tax bracket above 10% will pay a step funtion of higher taxes. Finally, concerning that a third of the population lives their life from paycheck-to-paycheck at all income levels, I’m not sure how they will close the gap in additional taxes due. I’m sure people hope current tax policy will be extended in lieu of the TCJA scheduled changes, but that is not a done deal in the current/future political environment.

Another interesting thing about 2026 is that it’s about when money supply will fall back in line with its long term trendline growth, assuming that recent money supply trends continue. Factoring in LordSunbeamTheThird’s comment below, the confluence of factors could prove “interesting”.

“Finally, concerning that a third of the population lives their life from paycheck-to-paycheck at all income levels, I’m not sure how they will close the gap in additional taxes due.”

It was generally accepted that the tax cuts did very little for middle income and lower. So unwinding it shouldn’t do much in the other direction. The biggest problem might be from SALT deductions not getting restored.

Specific example: Married couple, 3 kids, $200K annual household income. Federal taxes are expected to rise from $40,191.30 to $47,640.86. This is a $7500 gap that a paycheck-to-paycheck household will have to close, on top of any inflationary pressures that year. Only $620 extra a month, for the type of household that theoretically can’t handle a $400 emergency without borrowing. Also, the 20% QBI deduction will expire, which will be an additional ouch to sole proprietors.

The additional tax for said family due to the QBI deduction loss would be $40K*28%, so $11,200. Add that to $7450 for $18650 in additional tsxes that year, meaning an additional $1550 suddenly out of pocket each month. Ouch!

Jeff, remember that just 12% of U.S. households earn $200,000 or more annually – using your example below.

My neighbor who has a very simple tax filing, makes $100k – only looks at the size of his refund in April to determine if tax rates “went up or down”. The fact withholding tables change is a mystery to him. Most people don’t budget, they just spend a little more than they have in checking….

Plus 40+% of households do not pay federal income tax. I think the changes in tax rates in a couple of years will not be noticeable to 75% of the population.

The average household will likely see an extra $100-$200 a month in sudden additional federal taxes. Can the average *paycheck-to-paycheck* household handle the sudden hit? I don’t know. That’s the question. Two thirds of all households will be just fine. It’s that one third of all households I wonder about.

Fed still holds 2.6T in MBS. A percentage which gets bigger while other assets are run off. Dropping MBS puts further pressure on mortgage rates. This is 1/3 of their balance sheet, which combined with volatility in Crypto could pull the rug on their (other) assets (your taxpayer assets). When Fannie blew up, the Fed took on the load, and now? It’s a real witches brew, the Fed throwing regional banks under the bus, (for the crime of holding treasuries – regionals are the primary mortgage lenders) while they bail out charter banks who represent Wall Street speculators, the liquidity machine. The Fed basically said, we see inflation, so we need to raise interest rates. Big banks, we’ll pay your depositors, but not you community banks. The farther they take their balance sheet down the more these secondary markets, Crypto, Real Estate and Regional banks, come into play. RE is riding the wave of foreign investment (scared red cabbage – out of one RE problem and into another) and pumping the (forex) dollar. Once the (forex) dollar heads south, bond yields rise and Moody’s issues credit downgrade 2.0. (Not beforehand). Qt is all moot, and Feds balance sheet is already huge. When they need to buy more assets. Congress will do what they couldn’t do in 2008, say NO.

BINGO

The Fed NEVER should have purchased MBS. CONgress should have revoked their charter immediately. Unfortunately, you are being very naive. CONgress is fully OWNED. They will do what their corporate owners say, just like they did in 2008.

The Fed needs to dare to blow up a few egregious offenders, otherwise we’ll have more of the same mischief that got us into the current mess.

I’m going to go out in a limb and say that Inflation won’t subside unless we go back to genuinely tight credit – a regime of constrained reserves forcing prioritizations – rather than the current “ample reserves regime” where anyone can make a loan if they want to because nothing is really stopping them, where Congress drags us deeper into debt at a speed of $100,000 per second.

The current QT approach lacks testicular fortitude. If they think landmines lie ahead, they should sweep them (anticipate, plan ahead, crack down on likely offenders beforehand … actually be ready for stuff – unlike with SVB). They shouldn’t stop to pat themselves on the back every 2 months while inflation rages out of control, overall monetary conditions remain looser than before they started, and Wall Street laughs in their face in blatant denial of their ability to execute. Every time they do a policy meeting it’s an embarrassment how badly they Just Don’t Get It…

Thanks. I misogynistic explanation always clears things up for me.

Thanks Wolf! Could you put some color on this sentence: “Toward the end of QT-1, reserve balances dropped so low (below $1.4 trillion) that banks stopped lending to the repo market, even as repo rates began to rise sharply and it would have been profitable for banks to lend.”

Why would banks not do something that was profitable for them to do? I’m sure there is a good explanation and would appreciate yours.

Yes, all kinds of things were happening. Money market funds, who are primary lenders to the repo market, got cold feed also, in addition to the banks. At the time, some big mortgage REITs that borrowed short-term in the repo market and invested long-term in MBS (a risky leveraged bet) got in trouble, and they were forced borrowers in the repo market. I believe there was talk of some hedge funds being in a similar situation. What happened then was a crisis of confidence possibly, where the big lenders to the repo market didn’t lend enough.

Repo rates at the time were 6%,7%, even 10% while short-term rates were 2%. So this would have been hugely profitable for banks and money markets, and maybe worth the risk (which is small since this is collateralized).

This reason could have been: not enough reserves at banks plus not enough liquidity at money market funds to jump in big. And I think that’s what the Fed wants to forestall next time.

That’s how liquidity problems blow stuff up. There is liquidity somewhere, but it doesn’t get to where it’s needed, and some big players collapse because they’re forced borrowers and suddenly cannot borrow.

Wolf-

You said: “What happened then was a crisis of confidence…” — “confidence in what,” I ask sincerely.

In past articles, the dictum was used that “yield solves demand” in the credit markets. Why did this seem not to be the case in this situation?

Must systemic confidence be bought with progressively growing Fed interventions, as implied by the upward trend line on the Total Liabilities chart between 2008 and 2024 ($1 trillion to $6 trillion).

Painful as it promises to be, perhaps allowing more firms to fail (replete with layoffs and rising but transitory unemployment) would actually raise systemic confidence and make the financial system mor realistic, responsible and resilient.

I’m not trying to be argumentative… just to understand.

Thanks for your smart analysis and explanations.

Yes, agreed. Yield would have solved the demand issue just fine. It would have entailed some financial turmoil. I think that is what the Fed should have allowed to happen, but it didn’t allow it, it didn’t allow the system to fix the issue, the issue being an overreliance on the overnight repo market for borrowing, and some big players in the repo market blowing up — because they took a huge risk by borrowing short and lending long — would have put repo borrowing back down to earth where it belongs.

But it doesn’t matter what I think the Fed should have done (not done); what matters is what the Fed did, and what it will do again if something threatens to blow up the repo market. This is why the Fed’s approach to going slowly with QT as it approaches some magic line makes sense from the perspective that they will not allow the $5 trillion repo market to descend into turmoil, and if it blows out again, they will once again end QT and use repos the calm the market. And that would be the worst outcome.

I see your point on stretching QT in an attempt to disrupt market as little as possible and avoid a chaotic emergency responses. That seems sensible in the short-run.

What I fail to understand is the acceptance by so many (academia, Washington DC, and even many here) of an institution with a dangerous split personality. The Fed divides its time and efforts between goosing employment, and then mopping up the inflationary aftermath, and by its efforts encouraging public and private debt growth.

It is both arsonist and fireman, as charged by Congressional mandate. Meanwhile, over it’s 110 year history, it has grown like a weed in both size (balance sheet) and global influence.

It’s 3 mandates should be reformed, in my opinion.

> So this would have been hugely profitable for banks and money markets, and maybe worth the risk (which is small since this is collateralized).

This assumes that the collateral doesn’t have multiple claims on it at CCP’s/etc and that hair cut rates on such collateral are reflective of what you can actually get if you went to liquidate from a repo fail (often time its not when a ust repo is often only one leg of many for a position).

Their was a huge run on collateral leading up into the sept 19′ repo blow up and this was seen in swap spreads and the premium on treasuries imbedded in them, esp xccy swap spreads.

When stuff like this is being put out there: “ISDA is recommending a permanent exemption of Treasuries from Basel III leverage calculations” va fedguy[dot]com, you really have to question your assumptions on whether a risk is small, esp going forward.

It’s money and banking 101. Funds flowing back to the banks decreases the supply of loanable funds.

It was simply the FED picking winners and losers.

Fluff from the internet that dovetails with another excellent Wolf report. I was looking for something about SLR, but this was supportive enough.

“ In August 2023, St. Louis Fed economists Amalia Estenssoro and Kevin L. Kliesen suggested that, given the evolution of financial markets, reserves equal to 10% to 12% of nominal GDP ($2.7 trillion to $3.4 trillion, at the year-end 2023 GDP level) would be ample. Federal Reserve Governor Christopher Waller, speaking at the Hutchins Center in January 2024, said 10% to 11% of GDP would be “an approximate end point for draining reserves out of the system.” The median response in a December 2023 survey of the two dozen firms with which the Fed trades directly (known as primary dealers) was that bank reserves would fall steadily to about $3 trillion by the end of 2025. As of January 17, 2024, bank reserves totaled more than $3.7 trillion.”

Powell shot that down specifically and majestically at the last press conference. He said the Fed would NOT go by % of GDP to find out how far it could go. It would go as low as possible without blowing anything up, and when it would see stuff go wrong in the short-term markets, indicating liquidity problems, it would stop QT.

It’s right here, Powell’s own words:

https://wolfstreet.com/2024/03/20/what-powell-said-about-slowing-the-pace-of-qt-by-going-slower-you-can-get-farther/

“Right now, we would characterize reserves as abundant. We’re aiming for ample which is a little lower than abundant. There’s not a dollar amount or percent of GDP where we think we have a pretty clear understanding. We’re going to be looking at what’s happening in money markets in particular – a bunch of different indicators, including the ones I mentioned, to tell us when we’re getting close.”

The FED’s been managing monetary policy through interest rate manipulation since 1965.

And Powell is right in that approach. But it could well be that the “observed” limit he is seeking will be close to the model prediction of ~10% GDP. Time will tell.

Like predicting the weather, models are useful but should not be relied upon too much.

Re; Powell’s words

As a lifelong clock puncher and LOW level consumer (by choice, I had options VERY few if any of you here did), when a manger was cornered (usually lying or not stating the obvious, and began speaking (and squirming a bit), we called it “tapdancing”.

It appears economists have another word for it;

https://en.m.wikipedia.org/wiki/Goodhart%27s_law

I intend to learn what narrow and broad money are, IIRC, and what today’s equivalents are, and who uses them.

NBay-

RE: your quest to learn about definitions of “money”

Came across poem this some years ago and thought it might interest you. (Apologies if format gets messed up in comment format):

“We must have a good definition of Money,

For if we do not, then what have we got,

But a Quantity Theory of no-one knows what,

And that would be almost to true to be funny.

Now, Banks secrete something, like bees secrete honey;

(It sticks to their fingers some even when hot!),

But what things are liquid and what things are not,

Rests on whether the climate for business is sunny.

For both Stores of Value and Means of Exchange

Include, among Assets, a very wide range,

So your definition’s no better than mine.

Still, with credit-card-clever computers it’s clear,

That money as such will some day disappear,

Then, what isn’t there we won’t have to define.”

— Sonnet by economist Kenneth Boulding (Michigan Business Review, March 1969), as quoted in Melchior Palyi’s Twilight of Gold

Also- you could do much worse than starting with Milton Friedman/Anna Schwartz’s

A Monetary History of the United States

for a practical examination of “broad money.”

As a bonus, this classic provides a great retrospective of 93 years of US history from an economic perspective

Thanks. Fits my worldview fine…it’s like Lewis Carroll’s. It all seems (to me) to come down to Epistemology; How do we know what we know? The human condition.

You can cop out and invoke the supernatural for peace of mind, or you can keep banging your head against the wall. In my case I can’t think of a better way to spend my retirement since my trashed back prevents much standing or walking. The computer/internet is great, we all have a better library than Rockefeller or Carnegie could even image, plus thousands of servants to go chase down reference books. FWIW this site is the ONLY social media I do….it just struck me right. Thanks Wolf , I have never been a “Joiner”.

But I can spot a distinct difference between someone who lives in a ghetto, or on the street and the filthy rich (or mildly) and it isn’t right and that is just wired into me and that’s how it is.

PERIOD.

I’ve recited my pipe dream before and I’ll do it again;

There should be a constitution max net wealth and the IRS should be a full blown part of the Military, with access to all Agency info and special ops teams to parachute on top of Cayman banks and blow a hole in the roof and take what they want. Then over ambitious/greedy people can lie and cheat “or use their business acumen” all they want with REAL “risk analysis” involved. Law breakers go to prison if they are lucky, otherwise they might be “accidentally” shot…..it’s what happens when you deal with the Military.

Wolf says “money” in a way that sounds REALLY sinister to me, don’t know about the rest of you. Wonder if he practices it?

PS: “broad and narrow” money are just “tap-dancing”….no there there.

Don’t follow leaders and watch the parking meters!

PS I DO NOT like Uncle Milty AT ALL or “The Chicago School of Economics” AT ALL. I have read quite a bit about how and who put it all together.

Sure gets a lot of “Nobel Prizes”, eh? Rather odd don’t you think?

Maybe YOU should pursue all of the above? Sorry I can’t recommend a book, but I haven’t read one for years…..just bounce around internet, as mentioned above.

Haven’t even gotten into everybody’s problem.

TRASHING THE PLANET!

See NOAA address above if you want something more than your net worth or take home to worry about.

Well it goes to the heart of the argument. What is the appropriate description of the overweight Fed sponsored liquidity balance sheet,

Certainly not the founding principle of the Fed’s directive which they tended to adhere too which was a system of a counter balance referred too as the partial reserves regime. Now we hope that the obese Fed will at least lose enough girth that they will fall under the umbrella of an ample reserve regime.

Being as they have declared that the Fed is committed to the ample reserves regime. Disturbing for me because I believe in the sanctity of America, my Dad being awarded medals for his selfless efforts in a tank under fire in the American assault of Germany in 1944.

Can they cut rates and continue their balance sheet runoff?

Yes, most def. The Fed has officially separated interest rate policy from QT. So yes, rate cuts, if any, will not have any impact on QT.

The Fed already did that once: it bailed out the depositors with $300 billion in short-term liquidity in March 2023, AND hiked rates.

It did the same in 1966.

Yep, I believe Powell has stated that in his press conferences before.

They already blew stuff up, Wolf. They took away shelter – a roof over peoples’ heads. I don’t know how much more damage you could do. We need to go back to old prices, no matter how many billionaires lose everything. In fact, let’s just seize all assets of all billionaires. At this point we need to.

Amen. I love the theatrics of pretending the USD can be fixed. The Pound Sterling exists, but it did collapse and was replaced by the USD. Societies don’t truly collapse: Russia still exists decades after the fall of the USSR, China exists after how many revolutions (and failed currencies!), Rome is still standing in Italy.

It isn’t that the USD won’t continue into the future, but we are at the point where it’s pointless to pretend that the Fed hasn’t ruined the currency. Why does it matter if they pay down QT at this point? It’s just a game, and the only people that are concerned about how this ends are the ones who stand to gain. Whether a Snickers bar ends of costing $4 or $40, the value of the currency has been brought to the point of being worthless. Congresspeople suggesting raising the minimum wage to $50/hour aren’t crazy, they understand it is a great way to temporarily raise living standards (while paying down the debt through debasement). This is where we are at folks. The game actually ended a few years ago. We just haven’t accepted this yet and we are literally pretending that this charade is truly going to what? Solve things? This is laughable. If we have a $30/hour minimum wage in five years, it will need to be well over $100/hour by the end of the century (and likely much sooner).

Once the world finds a viable replacement, things will change quickly. The political will hasn’t gotten there yet, but it is certainly heading in that direction.

Even many hard working semi sophisticated upper middle class people were completely screwed (especially older folks) over last 15 years. I know people who effectively have inflation adjusted the same amount of money they did 15 years ago and they weren’t fools just a little conservative and unable to understand a zero interest rate environment living through the 70s and 80s.

Buffalo Billion,

Send me all your trashed dollars, and I will dispose of them properly.

You may want to take a look at various dollar indices.

This copy-and-paste BS about the dollars long-hoped-for collapse is just hilarious.

And what do you suggest? Lol nothing will happen, this is America, people rather watch Netflix than come together to demand change

There already is a replacement, most ppl can’t see it yet, it starts with a B and ends with an N. I was a non believer until this year about it, but education is everything, and now I see the trend and it’s here to stay.

Jon,

LOL. I can’t believe people still post this self-serving BS. Bitcoin has plunged 12% against the hated USD over the past 10 days. BTC is a gambling token, and nothing more.

BTC is an officially sanctioned (SEC) off balance sheet ponzi scheme, the various ETFs represent a weighted draw on the underlying. For every dollar that goes into BTC, and comes out as two, that’s an extra dollar of spending power, also highly inflationary. As a risk, its only 2T, while in 2008 the mortgage market represented about 12T, which was able to adversely leverage a much smaller economy. There are various coins, are they all going to agree to limits on issuance? Of course not. If it replaces the dollar it will be by force.

Buffalo Billion,

Send me all your trashed dollars, and I will dispose of them properly.

You may want to take a look at various dollar indices.

This copy-and-paste BS about the dollars long-hoped-for collapse is just hilarious.

“LOL. I can’t believe people still post this self-serving BS. Bitcoin has plunged 12% against the hated USD over the past 10 days. BTC is a gambling token, and nothing more.”

With all due respect, Wolf, BitCON is at more than $66,000 right now. The FED has basically created that with their grotesque money printing.

Ambrose, think this through:

Every trade has both a buyer and a seller, and a price paid.

So for every dollar that “goes into” a trade (from the buyer), the same dollar simultaneously “goes out” (to the seller).

Your claim that $1 went into bitcoin and came out as $2 is horsefeathers!

What happened is that an early buyer sold out to a late buyer. But the number of bit pins and number of dollars never changed.

I defer to Bruce Schneier on Bitcoin, so I was thinking BullioN.

“it starts with a B and ends with an N”

LOL. If that or any other cryptocurrency other than a central bank one EVER became anything more that a speculative instrument and income source for trading houses charging fees and actually became a threat to the fiat currency kick the debt-based economic collapse down the road game or provided an escape from it, governments which everywhere have coercive controls over businesses would simply make it illegal tender for any business to accept. The end of the illusion.

Wolf said: “Bitcoin has plunged 12% against the hated USD over the past 10 days. BTC is a gambling token, and nothing more.”

———————————

Not an advocate of Bitcoin, but how has Bitcoin fared against the dollar since Bitcoin’s inception?

And, since the FED along with other GOV actions has turned many financial market’s into a casino, including holding the dollar, it is no surprise that gambling would proliferate.

a couple of things affecting American culture right now:

1. concentrated wealth and power

2. rewarding gamblers and punishing prudence

of course, winning gamblers might say otherwise ……

Cb,

“but how has Bitcoin fared against the dollar since Bitcoin’s inception”

READ THE COMMENT I REPLIED TO. The commenter stated that bitcoin was replacing the USD as currency. And I replied to that dumb BS. These massive gains and losses are precisely why it’s just a gambling token, driven by huge mass-hysteria bubble gains. Consensual hallucination is what drives the price of cryptos, and something like that can never be a functional currency. That’s what this was about.

I’m not opposed to gambling. Let people have some fun. But understand that cryptos are gambling on consensual hallucination, and nothing else.

AB- (BTW, I learned you took your screen name from a guy who rivals Twain, and others like him.)

You are right about “by force”. Having grown up among some really powerful MIC guys, it is VERY obvious to me where the REAL power lies if push comes to shove.

I think that is wrong headed thinking because the USD is the fiat currency that is universally accepted as the preferred currency of exchange.

Bitcoin is only valuable if it can be converted into good old USD.

“Once the world finds a viable replacement, things will change quickly”, is ignorant nonsense. For the foreseeable future the USD will be the world gold standard currency.

Dang-

Dang-

“… USD will be the world gold standard currency.”

Funny use of the term “gold standard,” as the US closed the gold opt-out option to citizen’s in 1933 and to foreign central banks in 1972.

That the term “gold standard” is still in use while the actual gold standard has become a scornful reference to past barbarism is an ongoing delight and horror to the Austrian schoolers…

Agreed. Like I tell my husband, stop waiting for the collapse. It’s already happened, we’re just witnessing and living through the aftermath.

🤣

Your husband is the most patient man in the world. I hope you treasure him and let him know that you treasure him, for listening to your stuff.

Whatsthepoint, the people who sound the warning bells early are always called kooks. We’ll be vindicated, in my view, in the next 10 years or so.

@Whatsinthepoint,

My wife has a different metaphor. She says the supernova has already happened, it just takes the light that reveals it eight minutes to reach us here on earth.

Financially the economy is doing fine right now. In general, households are doing fine unless you are trying to buy your first home. However looking at the deficit and about 20 other things, things could / maybe get bad in the future. But the idea that the US has suffered any kind of collapse yet is crazy.

Bob, firstly, trying to buy a home is a big thing to exclude. Secondly, in a lot of ways, we’ve had moral and cultural rot/collapse. Financial and economic always follows that.

Bob said: “households are doing fine unless you are trying to buy your first home.”

——————————–

or unless they are paying rent …………

a large number of households are trying to maintain there place on the plantation.

debt slaves, rent slaves, wage slaves, welfare slaves (an oxymoron I know)

the financiers and rentiers are winning …….

JeffD – 😆. the local joke when I lived in the Spokane area back in the ’90’s was that it was a great place to be, because if the world ended, residents wouldn’t learn of it until five years after…

may we all find a better day.

That is literally insane. If you think the U.S. currency is worthless you can send me all you own. I will gladly accept it. I will send you rubles or yuan in exchange.

No one in Argentina would agree with your comments about the US dollar. The US dollar will eventually wind up as worthless as the Argentine peso but that day is a long way off.

This planet will end up worthless to large mammals before that, IMHO.

Damn we are smart critters, eh?

I’m down with that, DC! A real recession is the only cure for entrenched inflation. But with Uncle Same spending $1.7T & $2.1T in deficit spending last year and this year, I don’t think we’re going to get our wish anytime soon. And the Fed, despite persistently high core PCE inflation, is going to start lowering rates later this year. I can’t wait to see what that does to the housing prices. It’ll certainly help with the sales crash everyone is so distressed about.

No, you do as Bernanke did, drain reserves and drop interest rates.

They blew the hell out of the purchasing power of past earnings saved as dollars. They have been doing this for decades, but really stepped it up the past few years. That is their program, all for the benefit of financiers.

Actually, I agree that the Fed’s program which I assume we are discussing, is and has been for the benefit of the financiers.

We are standing on the outcome which seems to have fostered a resentment by the consumers who are paying for the program.

Exactly. The Fed can’t create wealth. All it can do is transfer it. The fact that assets are up so much does not mean society is wealthier. All it means is that the dollar is worth less.

The dollar’s purchasing power has DOUBLED with regards to office CRE over the past few years.

The dollar’s purchasing power has soared by 20% to 50% in the other CRE sectors.

The dollar’s purchasing power has soared by 15% and more with regards to single-family houses and condos in cities such as San Francisco, Austin, Seattle, Portland, and a bunch of others.

Yes, rate hikes and QT causes the purchasing power of the dollar to INCREASE with regards to assets.

HA-HA…..Ein…..

Another RTGDF OTHER As, too, guy bits the dust…….;-)

I bet you inherited a trust fund or business, didn’t you?

Nope. I grew up lower middle class. I knew what food stamps were. The boundaries of my high school included a town that was statistically the poorest suburb in America based on average income.

I just have always had a strong desire to learn about how things work.

Only a true mouthbreather would blame the victims of the FED’s currency debasement and class warfare schemes.

Thanks for demonstrating my point.

Don’t learn, just sit and complain and blame others.

or a Libertarian in training?

Let’s blow the thing up and get it over with.

Our first feature is WOLFCHOW, staring, JimL.

So far the Fed has not hit the combined $60 billion Treasury and $35 billion AMBS total of $95 billion a month. The Fed’s domestic SOMA account (as of March 20, 2024) stands at $6,910,335,061,100.00. Will the continued reduction (supply) of “$dollars” drive up their price(demand)? Is this the FOMC’s intended effect? Gold, which broke $2200 an ounce this week, is certainly not behaving like this will happen. What about the $1.3 trillion increase in US government spending for 2024?

Wes says: “The Fed’s domestic SOMA account (as of March 20, 2024) stands at $6,910,335,061,100.00.”

Wolf says: “Total liabilities: $7.47 trillion,”

————————————————-

should these two numbers equal each other?

Nope. There’s a lot of stuff on the Fed’s balance sheet, including Capital.

Yes, but if total liabilities is 7.47 trillion and SOMA is 6.9+ trillion, that leaves only about half a trillion for that other “lot of stuff.”

cb,

Like I said, lots of other stuff: #1 capital, and #2 other assets including gold, loans (BTFP, Discount Window, and other loans, see may articles on the Fed’s assets), the remnants of the Fed’s SPVs (most of those assets have been sold off, as I discussed a while back), foreign currency asset, Treasury currency (US coins except gold coins), IMF Special Drawing Rights, etc.

That’s not a secret. All you have to do is look at a Fed balance sheet (I’ve linked them many times).

Gold certificates, too. In distant past, bullion and coins…

The Fed has its fingers in a lot more pies with the transition from Fed Funds to secured (repo) lending, along with the global dollar complex (FIMA).

Getting long treasuries & MBS off the balance sheet via continued QT is the important thing here.

Well, as an old man that has survived six or so declines in the SandP index by over 50 pct, it seems to me the situation is ripe for a repeat.

I have been wrong for the past 18 years, expecting these yo yos to make a move that the criminal banks haven’t approved before hand.

What does tightening mean for the interest rates that money market funds are paying? I became nervous when Mr. Powell mentioned that he’s watching them “specifically”.

I have my cash in Fidelity’s SPAXX which is paying 4.7% and would hate to go back to the dark days of less than 1%. I have been assuming that the MM rates are tied to the FF rate, hope I’m right.

I think Wolf would say, and has said, that the MM rates are at least supported by the rates the FED chooses to pay on overnight reverse repo’s (ON RRPs).

Wolf said: “The Fed offers overnight reverse repos (ON RRPs) to domestic counterparties, mostly money market funds. But other approved counterparties are the banks, government-sponsored enterprises (Fannie Mae, Freddie Mac, etc.), the Federal Home Loan Banks, etc. These entities use RRPs to park excess cash at the Fed and collect 5.3% in interest.”

Shchwab SWVXX IS PAYING 5.3 FYI

If you have a million dollars it is 5.32.

Less than that is “only’ 5.17

“The Fed’s capital is set by Congress” ( quote this article). Looking at all the depression, inflation and ordinary boom & bust that has taken place in the 100+ years the Federal Reserve has been created, it would appear that Congress has no effect whatsoever on the machinations of the Federal Reserve.

That’s probably a good thing. The last entity on earth that I would want to run monetary policy is Congress.

And yet they’re in charge of fiscal policy, which is by orders of magnitude more flexible and powerful an economic instrument/lever.

I’m not saying they shouldn’t be in charge of fiscal policy — it’s appropriate that elected representatives exercise such authority in a democratic republic, assuming that this makes them accountable to the electorate (debatable in the US, but that’s a whole nother conversation) — just that it’s amusing you think that keeping them away from monetary policy is somehow sterilizing with respect to their economic impact.

What I don’t want is Congress being in charge of BOTH, fiscal and monetary policy.

“What I don’t want is Congress being in charge of BOTH, fiscal and monetary policy.”

Like those 20 members who were trying to force the FED to cut rates in the face of soaring inflation. These people are scary stupid, or reckless, or both.

Stuff blows up in a recession, and it is the weak unsustainable stuff. Is supposed to be a bad thing?

With asset prices and debts and deficits at record levels, and inflation running hot, it is clearly time to do some pruning for the long-term benefit of the economy and society.

If they don’t throw a few enterprises out of business regularly, they are poor stewards of the economy and have no business intervening in anything.

Won’t happen. It’s not in the best interest of those in power or with money.

So “Jon”, but not “John” is on here saying (over and over) ‘you won’t do s%&t’.

I’m noticing a pattern.

Lots of companies are going bankrupt just fine, big ones too, and we’ve covered some of them here. No one gets in the way of that.

Bankruptcy would greatly enhance competition, and therefore kill a lot of monopolies. Companies that make it through bankruptcy can operate at a much lower cost base until/unless private equity firms take them over.

“Banks get those paper dollars from the Fed in exchange for collateral, such as Treasury securities, which are assets on the Fed’s balance sheet.”

The picture entitled “Currency in Circulation” shows the trend is inexorably up. If Treasury securities are one example of collateral for paper dollars, should not those dollars be returned to the Fed and incinerated once the asset matures?

Is it within the Fed’s power to stop issuing paper dollars? Seems to me, this, combined with the above, would reduce the money supply, in addition to QT.

I know…the banks buy new debt and thus, paper dollars are never returned to the Fed. So really, the only answer to reducing currency in circulation is to stop issuing new debt. Correct?

Paper dollars are entirely demand based. If you go to an ATM to take out $400, it needs to have those paper dollars.

But where do those dollars come from? Are they already printed (which means they exist ‘somewhere’), or are they printed “on demand”?

Dollars are a unit of measure, such as miles or gallons or barrels. There are only assets and liabilities. And they’ve always been around, and new ones get created all the time, and old ones get destroyed, which is what humans do. Today, those assets and liabilities in the US are denominated in dollars, but they could be denominated in euros or pesos or whatever, it doesn’t matter — like you can express the distance on a highway in miles or kilometers. In the old colonies, assets and liabilities were denominated in pounds, shillings, and pence. Some of those assets still exist, and today they’re denominated in dollars. Makes no difference. Dollars are just a unit of measure.

Extremely important comment.

The public determines the denominations (although my bank tells me what they are giving me at the ATM)

However, the amount of currency outstanding is the public’s choice. That is until they force us to convert to digital. Will it happen? “Who knows what evil lurks in the hearts of men?” The Shadow Knows.

B

QT need not be slowed in order to go further. By definition ( and thanks to this installment) the limit is defined. Further is not an option.

You missed the issue: the limit is NOT defined. You know when you’re over that limit when something blows up. What I gave you here is an estimate of how far the Fed can go without blowing things up, if it goes slowly enough, because liquidity needs to have time to flow where it is needed.

Since no one knows where the limit is, it is very prudent to approach it slowly and watch for signs that you’re getting closer to the limit.

What I don’t understand is that it looks, from the chart, like reserve balances at the Fed in 2008 were $0… but by the end of QT1, those balances had to be over a trillion dollars, and now will need to be even higher than that, to avoid blowout? How were things ok before with $0 in reserves, but now the Fed needs likely trillions to avoid crisis?

Was QE a genie that can’t be put back into the bottle, so this is a permanent feature now?

In 2008, there were “required reserves,” and they were not zero, but much lower (roughly 10% of banks’ deposits). Before 2009, the Fed had a Standing Repo Facility (SRF) with which it supplied cash to the banks on a daily basis because banks were very tight on reserves. When QE started in 2008/2009, it flooded the banking system with cash, and the SRF was shut down. So now the SRF is back – the Fed revived it in Jul 2021, and reserves are going to be drained. But for now, the SRF remains unused.

The Fed could theoretically go back to its scarce-reserves regime and using the SRF extensively to supply liquidity to the banking system on a daily basis. But I don’t see that happening. But it could.

“When QE started in 2008/2009, it flooded the banking system with cash”

And this establishes the reverse Robinhood point DepthCharge is making. The Fed floods banks with cash. And these banks sit on large portions of this cash, in addition to lending it out at insanely low rates for 2.5 years after the pandemic, and then make bank to the tuns of hundreds of billions of dollars on the reserves as the Fed jacks up the FFR to fight sky high inflation that a lot of people believe the BLS under reports, in part, to ensure SS COLAs aren’t as high a they should be. And where do these billions of dollars go? They go into the pockets of the rich who work for & own banks.

And the part that the Fed doesn’t talk about is how all this QE lasts for years into the future and ensures there’s ample monies to fund federal deficit spending without the Fed having to buy treasuries. So the Fed looks good but they already pumped trillions of dollars into the system so they’ve “indirectly” are still funding the deficits. But, the best part for the rich is their ability to earn interest off this trillions of dollars.

For example, all those hundreds of billions of dollars Fidelity has parked at the Fed via ON RRP turn into billions in interest paid over the course of the year. What does Fidelity do with all that money? Do they use it to pay the uber low interest rate to MMF deposit holders?

“But, the best part for the rich is their ability to earn interest off this trillions of dollars.”

Lots of commenters here enjoy finally earning 5%-plus on their savings in CDs, MMF, and T-bills. Most of them I don’t think consider themselves “the rich.”

As I said: “The only tool, credit control device, at the disposal of the monetary authority in a free capitalistic system through which the volume of money can be properly controlled is legal reserves. The FED will obviously, sometime in the future, lose control of the money stock. May 8, 2020. 10:38 AMLink

Ahhh, this makes sense and resolves my confusion. Thanks for the explanation!

I think there were three things that changed in 2008. Moving from the old “scarce reserves” regime to ample reserves is one. Another is that the Treasury started keeping all of its cash balance in the TGA instead of with other banks, so the TGA balance is much higher now than before. The third is that demand for currency increased (you can see the change in the currency chart after 2008). I imagine that with zero interest in the US, euro and yen, there was more incentive to hold physical cash. With 5% interest, it will be interesting to see how that cash graph changes. Will it return to the slope before 2020? Or 2008?

Yes, correct all three of them.

Once banks start failing it’s going to be a problem for continued qt.

Might not need qt tho to keep rates up with all this debt

Great work Wolf,thanks!

Could you say the “currency in circulation” curb is flatening because people are leaving fiat money for stocks,bitcoin,gold or whatever concrete investment they can find?

And what fuels the currency in circulation curb growth?

Deficits?

So far FED did QT at moderate pace. They started with low limits till Sep 2022 and then went to 60B and 35B limits. MBS limits are bogus. We all know they are not going to hit those in first few years until Rates gets normalized. In last meeting presser, Powell already gave signal that QT is going slow down. He emphasized on Fairly soon. It means May 2024 in play. I understand slowing down so that we can go further concept. Buts it is too early to slowdown. We still have 400 B in ON RRP. Even though Reserves have come down from Peak, in last 3-4 months 500B is added to Bank reserves. Financial conditions are very loose. This can be seen in long term rates as well as thin Credit spreads for high risk bonds. They already have opened SRF to mitigate the risk.

So whats rush to slow down? They can easily go for another 6 months. This is Fed’s version of Premature ejaculation :) Jumping the gun too soon.

I don’t understand the rush to criticize the FED for slowing down QT before they have even started to slow down QT.

Yes, they are talking about it. This just means they are looking ahead.

How can you accuse them of being too early when they haven’t even started slowing down yet?

JimL

Once i tried to explain to someone why the elephant fell out of the tree, obvious to me it was the hippo that pushed him. I was met with disbelief and ridicule.

SRK,

“So whats rush to slow down?”

There is no rush to slow down. They’re in the talking stage. They’re preparing markets. Eventually, they will announce a decision on the slowdown, to start at a later date. What they said is that when ON RRPs approach zero, that’s when it’s time to slow down QT. ON RRPs will approach zero this summer.

“Lots of commenters here enjoy finally earning 5%-plus on their savings in CDs, MMF, and T-bills.”

That’s fine & dandy. I myself have the vast majority of my $500K in brokered CDs waiting for the next market downturn, but I’d still like to know more about how QE flows into MMFs, how it provides liquidity to the treasuries market during QT and what’s done with all that “free interest” monies paid to MMFs. It sure isn’t going into my pocket.

Like seriously. How much of the trillions of dollars in QE flows into bank reserves and what’s the total amount of interest paid by the Fed on ON RRPs until that number goes or approaches zero? It’s got to be into the billions of dollars.

During QE, the Fed buys securities from its primary dealers; the Fed gets the securities and the dealers get the cash, and it’s in their reserve accounts at the Fed because that’s where the Fed puts it. So now the Fed’s cash is in the banking system in what the Fed calls reserves. Then the dealer buys other securities with this cash from the Fed, so that cash leaves that dealer’s account at the Fed (reserves) and goes to the reserve account of the seller’s brokerage because all banks pay each other through their reserve accounts at the Fed, and so the cash stays in the banking system. The seller then uses the proceeds from the sale to buy different securities, and his cash moves on to the sellers of those securities, and to their bank accounts, and their banks then get this cash in their reserve accounts at the Fed, because that’s how banks pay each other, and the cash stays in the banking system and starts swirling around from buyers to sellers that then become buyers because you gotta do something with cash… and it moves to CRE and cryptos and what not, but because the seller always gets the cash, and the cash stays in the banking system, the reserves swell up with QE, but the cash is out there swirling around chasing assets from buyers to sellers who then become buyers….

There are some exceptions, for example:

When a seller of securities takes this cash and buys Treasury securities at auction, the government gets the cash into its TGA at the Fed, so the cash moves from reserves to the TGA, and it stays in the TGA until the government spends it, and then the cash goes to recipients, from Intel down to the welfare recipient, and the cash thereby goes from the TGA back to the reserves.

A similar process happens when someone buys shares of a Treasury money market mutual fund. The cash goes from the buyer’s bank’s reserve account at the Fed to the MMF fund’s bank, namely its reserve account at the Fed; the fund then deposits this cash as ON RRPs at the Fed, so the cash goes from reserves to ON RRPs. And when the MMF then buys T-bills at auction with this cash, the cash goes from ON RRPs via reserves to the TGA, where it stays until the government spends it, which is when it goes back to reserves.

In terms of interest paid by the Fed to banks (on their reserve balances) and to MMFs on their ON RRPs, and interest earned by the Fed on its securities holdings, and its profit or loss, and the remittances to the Treasury Department, or lack thereof, I tally this up once a year:

https://wolfstreet.com/2024/01/12/fed-reports-operating-loss-of-114-billion-for-2023-as-interest-expense-blows-out/

Wolf-

I’m probably missing it, but isn’t there a sort of “multiplier effect” in the process you describe above, due to the leverage at the commercial bank level?

Does a $1 trillion QE intervention lead to a $1*x trillion increase in bank lending (or investments)?

Am I right to assume this as the likely source of Fed policy “over and under-shoots?”

John H.

“Does a $1 trillion QE intervention lead to a $1*x trillion increase in bank lending (or investments)?”

No. And you can see that in the numbers. Bank leverage didn’t rise. QE didn’t do anything like that.

QE supplied new cash that did NOT need to be borrowed and it triggered a new wave of buying, which by definition entails an equal wave of selling, but the buying pressure changed since there was suddenly so much un-borrowed extra cash swirling around.

Sounds suspiciously like the Fed has been stood up to run one big confidence game, eh?

And that’s it folks. Your purchasing power is going in one direction. Straight down to hell.

I wish these folks would do the right thing, but ther not gonna. Plan accordingly.

Higher interest rates for much longer. That’s what you’re saying. Those low rates of yesteryear aren’t coming back, that’s what you’re saying. And you’re right.

The dollar’s purchasing power has DOUBLED with regards to office CRE over the past few years.

The dollar’s purchasing power has soared by 20% to 50% in the other CRE sectors.

The dollar’s purchasing power has soared by 15% and more with regards to single-family houses and condos in cities such as San Francisco, Austin, Seattle, Portland, and a bunch of others.

Yes, rate hikes and QT causes the purchasing power of the dollar to INCREASE with regards to assets.

To me, we are all blind men describing the elephant in the room based on touching only various parts.

Wolf has allowed me see the whole elephant. Thank you, Wolf!

I have a different viewpoint than someone who owns a home and an office building in Austin or San Francisco where I may have lost 50% of my net worth in the last year.

I’ve made this point before but surely its impossible to avoid a recession (not that they are bad and more of them would be healthier), because on the one hand you have the economy expanding to fit an increase in the money supply, but on the other hand, invisibly above this ongoing expansion, the money supply is shrinking.

There is momentum to economic expansion.

So at some point the size (quantity) of the economy will expand -past- the quantity(size) of money expected to support all the investments/industries etc and at that point the weaker ones will go the wall, unemployment will spike and there will be a hard few years.

This is why the Fed will probably go back to QE at some point. This is a balance-sheet recession that must be chosen.

The idea that $2.38 trillion dollars is held in stacks of paper around the globe is mind boggling. Theft, fire, flood, war, anything – that wealth is gone. If the Fed gets real collateral from the banks for those paper notes and then the notes are destroyed, does the Fed ever have to return the collateral? To who? Those are zero interest bearer bonds in effect – no paper, no claim. Like an unused Walmart gift card that was lost in the couch cushions with a few dollars remaining. Walmart got something for nothing.

It looks like the cash in circulation has topped out. Not surprising as people are running low on money in the US (Stimmy long since over, dollar stores warning) and the international community is moving away from dollars. The last time the growth in cash flatlined as it’s doing now was right before the GFC it appears.

“…and then the notes are destroyed, does the Fed ever have to return the collateral?”

The banks don’t gift those paper dollars, they sell them. So if you’re in Japan and want to buy $1,000 in paper dollars for your trip to the USA, you go to a bank branch and pay around ¥150,000 to the bank. So if you destroy those $1,000, nothing happens. You’re just out $1,000. The bank doesn’t care, it already has your ¥150,000 and won’t give them back to you. And its correspondent US bank got its money from the Japanese bank and is happy and doesn’t care. And its collateral with the Fed stays there forever. And you just gifted the Fed $1,000. You should ask the Fed to send you a thank-you note.

When banks were paying near zero percent interest, it was a hedge against risk to hold some physical cash. Now that short term Treasuries pay 5%+ interest and inflation is high, the benefit/cost of that risk hedge unwinds. Wolf mentioned yields as a reason to hold less cash, and I think his instincts were spot on.

No, issuing new debt (by the treasury) and creating new money (by the Fed) is not the same thing.

When the treasury issues debt, it takes money from the financial markets, and then spends this money in some other part of the economy. The net effect on the total money supply is 0. It’s just moving liquidity around in the economy.

From investors.

Wolf,

I am just theorizing, so I am not sure I believe this. More just thinking out loud.

You are basing the lowest amount the reserves can go based on how low they went recently when things started breaking. However, what if things started breaking not because of the reserves, but because if other things?

What I mean by that is you point out yourself that at that time, there were trades the banks could have made that would have made them pretty good money but they were too scared to make them. You assume that they were scared because of the level if reserves. What if they were scared because of previous problems. One of the problems is that generals always fight the last war. They assume recent problems will happen again.

When markets locked up in 2007-09 it was because nobody could trust the other side of the trade. They were afraid of ending up with a bunch of stuff on their balance sheet that wasn’t worth what they thought it was worth. There were plenty of trades available during that time that were extremely profitable in retrospect, but no one was willing to pull the trigger because they were scared.

So fast forward to the next calamity. Even though there were trades that were fairly obvious, the banks were scared to make them. Were they concerned about reserves, or were they looking to the recent past?

Where I am going with this is that if banks are a bit more optimistic and freewheeling, reserves can probably go lower before causing problems. Doesn’t that make the reserve limit subject to an ever changing “bank sentiment” than an absolute numerical limit?

Yes, agreed, low reserves didn’t cause the repo market issue. Something else did. But they then weren’t there to help resolve the issue — that’s the Fed’s take and lesson.

If the Fed had had a standing repo facility (SRF), it would have allowed the banks to borrow at the SRF at 2% at the time and lend to the regular repo market at 6% or 8% or whatever, and that might have solved the problem on the spot for the overall market, while a couple of big mortgage REITs might have blown up without causing too much of a wider problem. But the Fed had shut down the SRF in 2009.

Before the ample-reserves regime which started with QE in 2008, though it wasn’t formalized until the repo market blowout in 2019, the Fed had a scarce-reserves regime, and it provided daily funding to the banks via repos at its SRF. That’s how it was set up until 2008. When QE started, banks were awash in cash and no longer used the SFR and the Fed shut it down in 2009.

So in theory, the Fed is now set up to slowly get back to a scarce-reserves regime, since it has the SRF back online. And maybe it will head that way over the years, who knows. That old system worked well, and the Fed knows it worked well until Bernanke scuttled it.

You mean when it blew up ie. Bernanke?

If I remember correctly the “ample reserves” were there to recapitalize the banks first.

No, reserves don’t recapitalize the banks. They’re liquidity. What recapitalizes the banks is profits (from the Fed’s interest rate repression on deposits at the time; from trading the QE craziness, etc.) and raising new capital by selling shares, preferred stock, warrants, etc., including to the government (TARP). And banks did all of those.

Yes. Thanks. You put into words the thoughts I was thinking, but could not express clearly.

I been meaning to ask you a question regarding QT and MBS. If you have answered this somewhere, I apologize.

Since it looks like the runoff in MBS is going to take much longer than QT continues (even as QT slows down), is it safe to assume that once QT ends, the FED will just replace rolling off MBSs with short term treasury bills?

In other words, the goal is to get MBSs completely off of the balance sheet eventually? Is that a correct assumption?

One of the Fed board members (I forget who) did explicitly say its the Fed’s goal to eventually not have any MBS on the bal sheet. I think Powell himself has also said this but not 100% sure.

What a breath of fresh air this straightforward analysis of QT is. Thank you, Wolf. It’s a much needed corrective to all manner of hysterical speculation and misdirection by motivated actors.

Thank you for an interesting and very informative article. I’m going to read it a few times more.

And while I am pleased interest rates are are higher these days as the FED picks its way along, I am going to take exception with all of the posters here this morning wishing for a recession. Or, as my old old father in law said in the 80s when I was laid off from permanent employment and had to work away in 3 month stints (500 miles away from home)……”It’s always trimming the fat when the other guy loses his job, but it’s just the shi*s when it’s you”. And if there are mass layoffs and dislocation due to contraction, there will be anger and unrest to be addressed which will probably require rapid loosening. And who will be that next saviour with all the answers?

There are problems these days, but these are not desperate times like the 30s.

The Fed is juggling and trying to keep the system working. Yes, the rich get richer and the poor get poorer, and the aphorism often finished up with ‘ever thus’. But I dispute there is some grand conspiracy of insiders pulling the strings to reach into your pocket. Get rid of personal debt, and if it takes a plan and time to accomplish then so be it. With no debt and some cash in the bank it is all just a sideshow. This system has inertia. It doesn’t care about individuals.

Spoken like a true beneficiary of the FED’s “wealth effect.” Get out much?

Spoken like a true poster on Zerohedge with 100,000 net upvotes.

“But I dispute there is some grand conspiracy of insiders pulling the strings to reach into your pocket.”

Spend some time reading the Congressional legislation concerning taxes, and you will likely quickly change your mind.

“But I dispute there is some grand conspiracy of insiders pulling the strings to reach into your pocket.”

Sounds to me like a pretty good definition of most of our totally unregulated Corporations….their upper and maybe some ambitious middle management……FWIW.

One of these days I might go to Zero Hedge…to see why it’s a “hot button” here………have a lot more things to check out first.

New debt is NOT new money, that’s just ignorant BS. Investors have to buy this new debt, every single dollar of it, so the money just gets transferred from investors to the government, which then redistributes it by spending it, such as by giving Intel $23 billion over the next five years. Investors get paid interest for handing their money to the government.

How will the reduction in the Fed balance sheet effect GDP growth ?

It won’t. As you can see: $1.5 trillion in QT and red-hot GDP growth.

Powell stated in the last press conference that as the balance sheet begins to level out. Currency in circulation would increase “organically” while decreasing reserves slowly. But all the evidence is pointing to the fact they operate on different rules rather than inversely related ? According to the graphs to posted. It seems like a stretch by Powell to make that claim.