QT-1 blew up the repo market. This time around, the Fed wants to avoid that type of debacle so it wouldn’t have to “prematurely” end QT-2.

By Wolf Richter for WOLF STREET.

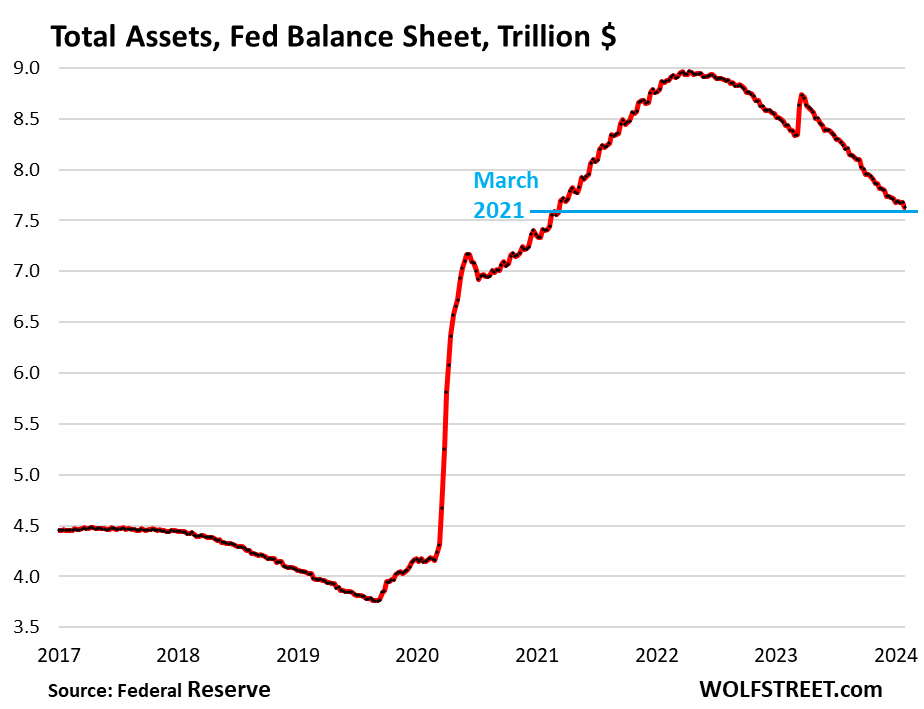

This has been in the works for a while and has come out in bits and pieces, but today the Fed made it official in the FOMC meeting minutes: It doesn’t know how far it can take QT without blowing up stuff, but it wants to reduce its balance sheet as far as possible without blowing up stuff. QT has already reduced the Fed’s balance sheet by $1.34 trillion. And so far, nothing has blown up. But last time it did QT, the repo market blew up.

The issue with withdrawing liquidity from the market via Quantitative Tightening is that this liquidity is taken out through a couple of drains that are close together – the Fed’s roll-off of Treasury securities and MBS – but liquidity has to flow there from all directions, and it may drain out faster in one corner, and that corner then runs out of liquidity and blows up, while there is still excess liquidity in other corners.

Yields solve that problem normally. The corner that is running out of liquidity will be willing to pay higher yields to attract liquidity from the corner that has excess, but the process is not instant; it can take too much time, and then something runs out of liquidity and blows up while at the other side of the markets, there is too much liquidity.

This hasn’t happened yet in QT-2, which is still running “smoothly,” as the FOMC minutes said today.

But it happened with QT-1 in September 2019, when the repo market blew out because banks were running low on excess liquidity and refused to lend to the repo market, and a repo-market panic ensued and threatened with contagion, and so the Fed stepped into the repo market and helter-skelter doused it with nearly $400 billion in liquidity, which raised its balance sheet again, thereby undoing a big part of QT-1. And that is to be avoided this time.

So the Fed’s solution seems to be two-fold, that’s what we see:

1. Withdrawing the liquidity slowly enough so it has time to flow to where it’s needed with minimal disruption, allowing QT to drain liquidity evenly until the balance sheet reaches the lowest comfortable level without blowing anything up. If something blows up, it would put a premature end to QT.

This topic was first broached in early January by Dallas Fed president Lorie Logan and dealt with at the time here in our illustrious comments. Slowing QT would reduce “the likelihood that we’d have to stop prematurely,” she’s said. And today, it was officially put on the table via the FOMC minutes.

2. A Standing Repo Facility that everyone knows will be there; and its mere presence, even if inactive, will tamp down on a panic. The Fed had an SRF through 2008, that was its classic measure to deal with market issues before QE, including during 9/11 when markets froze and were shut down.

Repos mature within a day or within a week or two weeks, or some relatively short term, and if they’re not rolled over, they then vanish from the balance sheet automatically. They don’t cling to the balance sheet for years or decades like QE assets.

But in 2009, the Fed skuttled its SRF because it wasn’t needed with the huge amount of QE the Fed was doing at the time. But it didn’t revive it when QT started, and in September 2019, after nearly two years of QT, with no SRF on standby, it had to scramble and improvise as the repo market was already blowing up.

So this time around, in July 2021, a year before QT started, the Fed revived its classic SRF in preparation for QT. So that’s done.

The minutes make the beginnings of a plan official.

Logan is just one FOMC member and didn’t officially speak for the group in her long detailed speech. “As always, the views I express are mine and not necessarily those of my colleagues on the Federal Open Market Committee (FOMC),” she said at the beginning. Today, the minutes showed that the Fed’s institutional thinking is with Logan on this.

The minutes made five important points about the future of QT:

- So far, so good, everything is cool with QT. No hurry to change anything.

- QT is an important part of getting inflation down.

- The Fed doesn’t know how low the balance sheet can go without blowing up stuff.

- Slowing QT would allow the Fed to reduce its balance sheet further than if it kept going at the current speed, as it would lower the risk of something blowing up, which would force the Fed to end QT prematurely (see QT-1).

- Even after the Fed starts cutting rates, QT can continue “for some time.”

In the words of the minutes:

“Participants observed that the continuing process of reducing the size of the Federal Reserve’s balance sheet was an important part of the Committee’s overall approach to achieving its macroeconomic objectives and that balance sheet runoff had so far proceeded smoothly,” the minutes said,

“In light of ongoing reductions in usage of the ON RRP facility, many participants suggested that it would be appropriate to begin in-depth discussions of balance sheet issues at the Committee’s next meeting [mid-March] to guide an eventual decision to slow the pace of runoff,” the minutes said.

“Some participants remarked that, given the uncertainty surrounding estimates of the ample level of reserves, slowing the pace of runoff could help smooth the transition to that level of reserves or could allow the Committee to continue balance sheet runoff for longer,” the minutes said.

“In addition, a few participants noted that the process of balance sheet runoff could continue for some time even after the Committee begins to reduce the target range for the federal funds rate,” the minutes said.

What this tells us…

There will be more color on this topic at the next FOMC meeting (March 19-20), and we’re looking forward to the inane, manipulative questions the reporters will hammer Powell with at the press conference.

What this tells us is that the Fed did learn a lesson from the repo market blowout that ended up reversing part of QT-1. And it proceeded methodically to implement those lessons by re-establishing the classic SRF before QT-2 even started, and then by trying to avoid the kind of blowout it was hit in the face with in 2019, so that it won’t have to end QT prematurely.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Wolf, I know you’ve estimated how low you think the Fed balance sheet can go. Although the Fed minutes indicate “The Fed doesn’t know how low the balance sheet can go without blowing up stuff,” I think they must have made similar calculations. Do you think the Fed is concerned about being held to a number at this time or that they really haven’t estimated how far QT can go?

The basic calculation is liabilities-driven. On every balance sheet, assets = liabilities + capital. The capital is set by Congress. So any change in liabilities must be matched by an equal change in assets.

There are four big liabilities on the Fed’s balance sheet:

1. $2.33 trillion of currency in circulation (cash in your pocket). This is demand-driven. The Fed does not control this, people around the world do as they demand to hoard dollar bills.

2. $3.54 trillion of Reserves — cash that banks put on deposit at the Fed. This is liquidity in the banking system. This is the key figure they will watch. The repo market blew up when reserves fell below $1.5 trillion. So maybe $2 trillion will be the minimum this time.

3. $830 billion in the TGA — that’s the government’s checking account. It varies widely. The Fed doesn’t control it; it’s controlled by the US Treasury, whose goal is currently to have about $750 billion in it on average.

4. $900 billion in RRPs, which consist of $574 billion of ON RRPs (with domestic counterparties) and $330 billion in RRPs with foreign central banks. The ON RRPs are normally at zero and can go back to zero. The RRPs with foreign central banks (they park their excess USD there) is demand driven, and the Fed doesn’t control it.

So lets assume:

$2.33 trillion in cash in circulation

$2.0 trillion in reserves

$750 billion TGA

$0 ON RRPs

$300 billion RRPs with foreign official.

—————-

= $5.4 trillion. That would be the total absolute minimum.

Just below $6 trillion might be a somewhat realistic minimum. The balance sheet is now at $7.6 trillion. So there’s a ways to go.

Probably a dumb question, but why ~$4B was an acceptable minimum in 2019 but it’s more than $5B now?

Nothing to do with “acceptable.” It’s just basic math. It’s determined by the liabilities. Two of the big ones are outside of the Fed’s control, and they keep growing and they’re demand based: currency in circulation and the TGA, so that’s $3.2 trillion right there. ON RRPs will go to zero, repos with foreign central banks will be somewhere around $300 billion, and that is demand based and the Fed doesn’t control it. So now we’re at $3.5 trillion. All this stuff grows with the economy and inflation. Last time the repo market blew up, reserves had fallen to $1.5 trillion at which point the banks stopped lending to the repo market. So if that were the minimum this time (it’s too low), it would bring the minimum total to $5 trillion.

For one thing, there ALWAYS has to be some currency in circulation! Otherwise there would be NO business being done…

But I digress, Wolf is VERY optimistic. If the Fed can get there balance sheet below 7 trillion without $hit blowing up, I will donate $100 to Wolf. Far too much greed, fraud, and outright corruption in the system now. We have been rewarding bad behavior for far too long. The Fed has been the enabler. Case in point, buying MBS. That NEVER should have happened.

@WB,

Congress could write legislation in a matter of weeks that would incentivize residential real estate investors to dump some of their properties onto active listings. The sale of those properties would allow the Fed to finally let more of their MBS holdings roll off.

@JeffD

“The sale of those properties…”

Well, there’s the rub. At what price Jeff, and will these be cash sales or financed at these higher rates? The Fed cannot have the prices drop too much…

Rock, meet hard place.

Agree with you on this one and it makes a lot of sense, Wolf. Additional color here is they are just relying on maturity, not actually selling securities. Based on the maturity profile of the balance sheet, it seems like the QT runoff will start to slow down absent any sales of securities once they get below ~$7T. So this could just naturally slow down in late 2024 if left on autopilot. They don’t have to officially change course at all, QT just slows naturally.

Thoughts?

Yes. I’m looking at the maturity schedule of the Treasuries on the Fed’s balance sheet. Remember, they’re letting T-bills run off in months when the notes and bonds runoff is less than the cap, which is now in most months. So until the T-bills are gone, they’ll hit the cap. They still have $210 billion in T-bills, and according to my calculations, they will run out of T-bills in July 2025. Until then the Treasury runoff can continue to hit the $60 billion cap. July 2025 would be the first month when the Treasuries runoff will be below the cap, and so that’s when the Treasuries runoff will slow naturally.

MBS are entirely different. They come off mostly via pass-through principal payments from mortgage payoffs (sale, refi) and the principal portion of regular mortgage payments. If the Fed ever cuts interest rates a lot, refis will surge, so will the passthrough principal payments, and the MBS will come off much faster. Also, when home sales pick up again and go back to normal, payoffs will pick up, which will speed up the reduction in MBS.

After QT ended in Aug 2019 through February 2020, the Fed continued to let MBS run off at the cap, and it replaced the MBS with Treasuries. In the chart, which covers that time period, you can see how the MBS continued to fall until covid QE.

My guess is that they will do a similar thing: let the MBS run off until they’re gone, and if QT slows or ends, they’ll replace them with Treasuries. The Fed really doesn’t like to have MBS on its balance sheet for a variety of reasons, including that they’re so unpredictable:

Thanks Wolf!

=5.4trillion

Yes, thanks, fixed.

Longtime lurker, first time commenter here

How do we pay for exponentially increasing federal spending without QE in the end?

With exponentially rising tax receipts and more borrowing. As always. Inflation inflates tax receipts, which is why governments love inflation.

What matters is interest payments as percent of tax receipts:

Wolf,

what’s the banks balance sheet to reserves at the fed ratio and how elastic is that?

Thanks

I don’t understand your question.

But here are couple of things:

Total deposits at commercial banks = $17.5 trillion. Deposits is where banks get most of their cash, and some of it they deposit at the Fed (“reserves” in the Fed’s lingo; “interest-earning cash” or similar on the banks’ balance sheets). Banks also keep some cash on hand and keep some in T-bills. They loan out a bunch, and invest a bunch in securities. Those loans and securities can turn out to be illiquid. So they keep a lot of liquid stuff on hand in case depositors want their money back, such as at SVB.

Total assets at commercial banks: $23.3 trillion, which includes the $3.3 trillion banks keep on deposit at the Fed (“reserves”).

Until it’s NOT

Will Testosterone Pit ever be a book instead of Kindle? I’ll take one if it ever comes to pass.

He answered this a couple days ago, it’s only available in Kindle. You can buy a copy and read it on your e-device at the DMV or whatever.

I think the FED has decided low unemployment is more important than price stability. They will continue QT as long and as fast as they can without “blowing things up” so they have space on their balance sheet for the next round of QE when they get a sniff of a recession on the horizon.

They lost their appetite for QE. If something blows up, they’ll do short-term liquidity support via repos, which is how it always handled crises before 2008. That’s what the SRF is all about. And they did that in March 2023… people expected QE, but it continued QT combined with short-term liquidity support, most of which has by now vanished.

“They lost their appetite for QE.”

Wolf, I get why you say that about MBS, but why for treasuries? QE allows the FED to influence the long end of the yield curve and QT has been working just fine as you have so well described. It may not be used in the exact same way in the future, but why should we expect it to not be another tool in the toolbox for the FED?

Why do you think the Fed *wants* to manipulate the long end of the yield curve?

I agree with Wolf; the Fed has other acronyms to deal with a crisis, such as BTFP last year, and SRF today which should prevent another ‘repocalypse’ from happening.

MM, for all the same reasons they did it in the first place. I’m sure they have learned a few things and will likely make some adjustments, such as no MBS or start QT earlier. But I haven’t seen anything to suggest the FED believes QE was one massive failure never to be repeated.

I don’t think the Fed has explicitly said 13 years of interest rate repression was a failure either. But they know it was.

They might be a little embarrassed about admitting it, but they’re not that stupid or ignorant (contrary to what some commenters imply).

The Fed is on a hiding to nothing, bailing water on the Titanic.

The 2008 Fed bal sheet was $0.7trn, its now 10 X .

Cleverly the cash mostly avoided the CPI,

Pick your poison, austerity or inflation.

Govt will always choose inflation.

Thongs have changed since 2008. Thongs that would change the FED’S balance sheet without meaning anything to the overall economy.

JimL – must remark that your slip is showing…

may we all find a better day.

So we’ll never get back to the $4T prior to the pandemic let alone the $1T that Bernanke said we would get back to after the GFC?

Prices have reached a “permanently high plateau.”

Bernanke lied of course when asked if the Fed was monetizing the national debt. Here 14 years later the truth is apparent.

Maybe all we can ask for is that the Fed lets the MBS roll off naturally through repayments – and therefore stops screwing with the mortgage/housing market – and maybe gets the BS down to 15-20% of GDP like it was long ago. $5-6T in all Treasures and no MBS.

They all do, don’t they? (Politicians, or so called our leaders) Nixon’s temporary disconnect to gold ring a bell?

Agree with Wolf here that QE is likely going to be an emergency measure (depression like situation) going forward rather than a policy to build confidence in the economy.

The distortions of QE are clearly showing up now as wealth inequality and social issues. The Fed and anyone with eyes can see it. So people looking for QE will need to move to Japan.

A key thing to note would be what the Fed does with ample reserves if inflation continues to be a problem. Technically the ample reserves is inflation in waiting but it requires a sudden lost of faith in the American Dollar.

Agreed. The Fed members are smart people and learn from their mistakes. They’ve faced unpredicted crises with the GFC and COVID but have kept the economy from “blowing up”.

Yes, there were perhaps better choices and there are certainly unexpected problems but those things are insanely hard to forsee. People love to bash the Fed with the benefit of hindsight and comple disregard for what might have happened if they had acted otherwise (for which, of course, there is no hindsight).

They’ve done well. Not perfect; well.

LOL!

The Fed has been the greatest enabler of bad behavior and outright fraud in the history of mankind. Well documented. Case in point; purchasing MBS. ALL the corporations that sold these financial “products” (f-ing JOKE), should have been allowed to FAIL and their management sent to PRISON as it was a direct violation of 150+ years of contract law. Of course, these same f*&^%ers have since lobbied CONgress and changed the “laws”.

The Fed is a laughing stock with zero credibility, and the world is dumping the dollar as a result. We would be in a MUCH better position if we actually stuck to the capitalistic model and rule of law.

You can say that but you do not know that.

We do know that unfettered capitalism is utter nonsense as witnessed by its record of failure throughout history.

Totally agree 👍

BS. We absolutely know that when the rule of law is corrupted, societies degrade rather quickly.

Apologist scum. You can avoid reality indefinitely, but not the consequences of avoiding reality.

That demonstrates a very poor understanding of both history and the current value of the dollar.

@JimL

Poor understanding of the dollar? The FRN is in fact a fiat currency. It has been since 1971. There is literally thousands of years of history on fiat currencies. They are based on FAITH and RULE of LAW.

LMFAO!!!!!

“The Fed members are smart people and learn from their mistakes.”

They certainly do learn from their mistakes: they learn to make them even bigger next time.

Hahaha you forgot the sarc tag.

Wow. This is an exceptionally realistic comment on this blog considering how it seems that membership requires one to be a negative Nelly, deeply engrossed in conspiracy theories.

That was only slight sarcastic

I stand by my statement. Things would likely have been much worse much sooner had they not acted. They did bring along many of the current problems but those are small in comparison to what might have been had they done nothing.

Aman or Wolf-

I believe that this Fed or some not too distant Fed WILL use QE again, and of course to fight an emergency (originated in it’s own prior actions).

But did Wolf actually say that QE is likely to be used in emergencies. I’ve reread, and I don’t see it. Can’t see how that would not draw the ire of several commenters…

I guess I misquoted gentleman Wolf :)….he did not say or imply any such thing.

I meant to say that this Fed would likely use QE only if the financial system was in chaos or economy hit by a deep recession. Not like Bernanke who prescribed it to stimulate growth or to address imaginary deflation. And yes if it came to it, then it would be something that the Fed invited upon themselves.

I seriously doubt if QE will become the policy to address economic slowdown or even a shallow recession. My view is that the Fed has understood the true cost of the policy and the instability it has caused in financial systems and society more importantly.

But then again Fed since Greenspan has proven to be foolish and academic so nothing is certain. But it is very very unlikely. And if QE were to return, then likely will be in circumstances where dissenters here too would approve of it and welcome it.

The “financial system in chaos” and “economy hit by a deep recession” are two different things.

The way the Fed has gotten itself set up now, it would not use QE for either, but it would go back to how it used to handle these situations before 2008:

1. financial chaos: flood the system with cash via repos (which is why it revived the SRF, so that it can do that, without having to use QE)

2. Deep economic recession: cut interest rates by 500 basis points to 0.25%.

Aman and Wolf-

Thanks for your kindly elaborations. I was not at all trying to find your statement erroneous, Aman, but was somewhat surprised the group did not react.

I find the entire subject of ever-growing policy actions, enabled by Fed’s ever-growing footings to be problematic, and eventually unsustainable.

As I understand it, Weimar Germany (as retold by Constantino Bresciani Turroni) got into an ascending double helix of deficit induced debt growth, followed by money production, followed by debt growth, and on and on, till the German Mark was destroyed.

Given intractable deficits and the Fed’s inhibition toward using money production to fight the chaotic (if predictable) repercussions thereof, what hope is a central banking skeptic left with?

I dearly wish I could believe this, but I’ve seen very little to convince me that the Fed has learned from its massive policy errors, or even that they believe that QE was a policy error.

Government keeps borrowing big and spending big, and forgiving student loan which is also a stimulus. And then there is QT.

Is this a contradiction?

“Contradiction” is not the ideal word. Maybe “in conflict” would be better. What is going on is that fiscal policy (government deficit spending = stimulative) is in conflict with monetary policy (Fed tightening). That’s not a good situation.

Remember Wolf, so people think of the government as one single, all powerful entity. They are incapable of understanding the nuance that the government isn’t like that and there can be different forces at work

Why does the FED what it does?

Keep in mind that the FED consists of banks. Banks don’t like risks to be on their hands. Who does? When the FED is shedding assets, it has become more risky to hold on to those assest. If the FED goes too fast, the risk of blowing up something increases. So that has to be avoided.

QT doesn’t reduce the total risk that is out there. The risks the FED held are divided among the other participants in de market. And they don’t have the ability to print their way out of problems.

When it becomes concentrated in one part of the market, that part could blow up and domino’s start falling. The FED’s second job is to prevent that. The FED has no other jobs.

All the inflation talk is irrelevant to the banks. That’s a political issue. Banks can make money in any environment, as long as they manage their risk well. (Put it on someone else’s plate and make profits by charging fees for those ‘assets’).

The question for everybody is: “what sort of risk am i personally exposed too? What bag am i holding and can i get rid of it?”

Essentially: think as the FED does.

The Fed’s job is to prevent runs on banks caused by collapsing asset values. The underlying problem is that banks like to make loans against appreciating assets, not on speculative ventures like factories. And the very core problem is that the cause of the appreciation in asset values is the lending to start with. Housing and stock prices don’t go up by magic, they go up because banks are willing to lend against a higher price in the belief that prices will always go up and they can seize the assets and resell them if needed.

If they start going down, borrowers don’t pay the banks, and the banks can’t pay their lenders. That’s when banks start demanding each others assets, and a run starts.

So the Fed has to act as the lender of last resort. It uses the short term lending facilities to loan money to banks that are having short term issues paying their lenders. And in periods of asset depreciation it uses QE to buy depreciating assets, like mortgage backed securities, at par to keep those assets from going on a fire sale.

The risk is what happened in the Great Depression: over-leveraged banks resulting in a massive nationwide asset price collapse, lenders demanding their money back immediately, leading to a run on all the banks, a collapse in lending and the collapse of the economy. The only thing that stands in the way of that happening again is the Fed’s competence to see it coming and act accordingly. That’s what Bernanke saw in 2007 and why we had QE to start with. Individuals really can’t insulate themselves from the general economy. You can move your savings into gold, but you will still starve if you lose your job.

I know a lot of the young ‘uns here want to see a big collapse in housing prices. It’s not going to happen. The Fed won’t let it. That may make them angry, but know this: if they did collapse, it means the banking system failed and you won’t have a job anyway. So you won’t be able to afford even that lower price. Sorry. There are other answers to the problem. But that would require a significant change in political mindset.

Demographics will eventually solve the problem of housing, whether through inheritance or a massive number of relatively locked-in (paid-for, non-downsized, age-in-place) properties hitting the market; plus, we obviously continue to build. It will, however, take another decade or so. Boomers are going to be hitting the stairway to heaven across the generation in droves at that time.

So unless the Fed actively does something to inflate the market like MBS — which would inflate everything else and blow at least one mandate — there should (in theory) be, perhaps not an actively deflationary housing environment, but at a minimum, stagnation across the asset class.

I also am kind of getting tired of the concept of “locked-in” 3% mortgages. You’re only locked-in when you can cover the payments. It doesn’t matter what your mortgage rate is if you lose your job and can’t pay. The whole “locked-in” concept is completely contingent on unemployment staying at sub-5% — as if we’ll never have another recession or downturn again.

There are more housing units per poulation than there has ever been, as the following FRED graph shows:

https://fred.stlouisfed.org/graph/?g=Mc22

The current problem is overhoarding, not underbuilding.

*but know this: if they did collapse, it means the banking system failed and you won’t have a job anyway. So you won’t be able to afford even that lower price. Sorry. *

Look, the banking system failed in 2008, but not everyone lost their jobs.

And the Fed responded, but the crash lasted 5 years.

Back then, people who bought low have now won double and triple.

So there is no way that prices will always and only go up.

The moment will come when the Fed will miss the moment to react (the so-called black swan)

That’s a ridiculous false dichotomy to say that the only choices are a) have greater and greater unsustainable price increases of housing every year or b) have a total collapse that results in unemployment of 50%. Even during the GFC, unemployment only went to 8-9% if I recall correctly. Most people still had jobs.

Housing prices are set at the margins. That 8-9% unemployment led to 50% drops in many places.

”Official unemployment rate” for construction industry was 15% in 2009 Einhal.

Many more of ”senior” experienced pals who were not working thought the rate was actually closer to 85% for a short time, and the competition for $5 to 15MM projects we were bidding went from statewide to regional to national, with the big boys taking projects at zero for the cash flow.

Others, smaller subs especially, told me, they were taking projects at a clear loss to keep their best folks on board and their families eating; one knew a loss of about 10% would keep best 5 folks working who had made the contractor a TON more in previous few years.

Sure, maybe for the construction industry and certain very discretionary areas like Vegas casinos, but the unemployment rate was nowhere near 15% for the economy as a whole.

Unemployment had almost nothing to do with a big drop in house prices. As you mentioned, job losses weren’t even that bad. Debt was issued that was greater in volume than could be paid back by paychecks (liar loans, interest only, etc.). Most of the people that lost houses stayed employed or only had a short break in employment. It wasn’t a job-driven recession at all, it was a deleveraging event. Too much bad debt came due too quickly, THAT is what drove big drops in some areas. Other areas didn’t see such a huge drop because buyers in those areas were not so deeply overleveraged.

Stop being ridiculous. There’s a middle ground between total economic collapse and the Fed buying MBS and encouraging rampant speculation in assets.

Show me any time in the last 30 years — other than the last year and a half —that the Fed will shoot for the middle ground?

The problem that the Fed had in 2019 was that it kept INCREASING the amount of monthly QT while at the same time increasing interest rates. They may could have gotten away with one or the other but they refused to prioritize one or the other and so BOTH had to stop.

As I said on WolfStreet comment boards back then, the Fed’s QT plans were well developed and announced in advance so everybody was comfortable with them… but NOT the Fed’s interest rate increases which nobody understood why they were doing them, how much they wanted to do, and when they were going to do them next. Eventually the banks and Wall Street just went into hunker down mode and the whole thing came to a screeching halt. It is good to see that they learned from the experience (although I have my doubts that they will actually slow down QT… that seems more like a Fed dove’s fantasy).

I think the big question is what’s gonna happen when the RRP balance runs out later this year?

Wolf, it may be beneficial to display a graph of the RRP since its drawdown has been the most dramatic.

Oops, this was meant to be a main post rather than a reply.

The normal condition of the ON RRP is $0. It’s only during periods of excess liquidity that it spikes as a result of QE during the late phases of QE. And it will go back to normal (= $0)

I would not bet, there is a lower risk to blew up something when QT is slowed… When the central bankers mean that is the right way ok, but i fundamentally disagree with. Why i do? Because the RRP/ reserves context they is created by Wall Street and central bankers, despite the fact that doesn´t exists.

Great news. I hope outside events dont force their hand in other directions before this work is done.

Wolf,

If the Fed has already pulled over a trillion dollars out of the market, where is all the money coming from in the stock market and crypto markets? When the Fed was doing QE during the pandemic, it was directly responsible for driving up commodities and the stock market (hence why they should have stopped once it was stabilized). Something seems wrong and contradictory in the market, but maybe there is something I’m missing.

Cole, you’re falling into the “cash on the sidelines” trap. Cash doesn’t “flow into” stocks or “flow out of” stocks. Prices are set at the margins, and are based on what price a willing seller and willing buyer agree on. Printing cash inflates the markets, as those who have first access to the cash (Cantillon Effect) will be willing to pay more, now that they have this new cash, but the reverse isn’t necessarily true.

And printing doesn’t always guarantee higher prices either.

“where is all the money coming from in the stock market and crypto markets?”

The RRP drain.

I didn’t study the event deeply at the time when it occurred back in Fall 2019, but definitely remember it seemed that Jamie Dimon and JPMChase had an outsized role in the “blow-up”. Not sure that this was as innocent or accidental as it appeared.

Normally, JPM could have lent massively to the repo market and made a ton doing so because the yields had spiked. But it didn’t. And the repo market got into trouble.

So why didn’t they?

So maybe JPM didn’t have enough reserves (liquidity) at the time to comfortably do so; we don’t know. But reserves was an issue, banks need to have lots of excess liquidity in order to lend to the repo market.

Or maybe JPM they wanted to blow up the repo market, but I’m not sure how they would have benefited. So that seems less likely.

Not even Milton Friedman understood money and central banking.

Looking at the Feds current holdings of US Treasury Securities, of the ~4.7T in current holding they can let 865B roll off in the next year, MAX, if they let their shorter-term treasuries drop to 0. There are 2.4T in MBSs that will only fall off when folks start giving up their sub-3% mortgages to move into new homes. (I’ll never give up mine).

Where does the rest of the QT come from? How do we get to 1T more in QT? The Fed cannot actually start selling its holdings, can they?

They still have $210 billion in T-bills, and according to my calculations, they will run out of T-bills in July 2025. Until then the Treasury runoff can continue to hit the $60 billion cap. July 2025 would be the first month when the Treasuries runoff will be below the cap, and so that’s when the Treasuries runoff will slow naturally.

So that’s 17 months at $60 billion in Treasuries through June 2025 = $1.02 trillion. And starting in July 2025, the Treasury runoff will slow. Another $213 billion will run off from July 2025 through December 2025, for a total of $1.23 trillion through December 2025.

MBS run off has been around $17 billion a month, and if that continues to be this slow (assuming no rate cuts, which would speed up the runoff), then by December 2025, another $390 billion MBS will have run off.

For a total additional QT by Dec 2025 of $1.62 trillion, which would bring total assets down to $6.1 trillion (if QT continues for that long at the current caps).

Scott B,

“(I’ll never give up mine).”

This means your mortgage is a prison, not the asset you think it is. I gave up a low mortgage rate. The non-financial factors plus the career opportunities made it well worth it. People move for a lot of reasons, there are going to be plenty of 2-3% mortgages getting paid off early.

crazytown,

every situation and every market is different but with a 2.5% rate on an LTV of 40% (at current prices), I’ll buy a second home before I give up the free money.

crazytown,

specifically on the point of balance sheet reduction, the rate of roll-off is going to look very different this time around, In 2019 natural MBS roll-off was pacing 13-14% per year, a little over 1% a month. In the last 12 months, less than 8% rolled off. If rates go down and a more ‘normal’ sales and refi cycle resumes, I bet we’d still be quite a bit lower than 13% yearly rolloff on the fed-specific MBS portfolio.

Without selling anything, the only lever the fed really has at this point to control QT is by buying T-Bills. They can continue to buy them at slightly lower than replacement levels and let the notes, bonds, and MBSs roll off organically

When the house prices get low enough, there will be plenty of nonperforming 3% mortgages waiting their turn on foreclosure of a loan way above the current house price.

MBS doesn’t just fall off when mortgages are paid off/refinanced. They are also gradually paid off as people make their regular monthly payments. Sure it gradual, but it is part of the equation.

Is QT really helping keep inflation down ? There seems to be no proof just a guesstimate.

The question might be “How much worse would inflation be if the Fed wasn’t doing QT at the same time as it raised interest rates?”

Or even, “How high would interest rates have needed to go to combat this round of inflation if the Fed wasn’t doing QT?”

The problem the Fed is having in combatting inflation isn’t so much with QT as with a Congress and White House that are still spending as though the pandemic economic collapse is ongoing. $1.34 trillion in QT won’t have much of an impact when JUST the Federal Government is running a deficit of $1.75 trillion a year.

https://www.cbo.gov/publication/59710

It definitely drives down inflation with very solid proof. QT shapes the longer term treasury yields that drive borrowing costs. The higher interest rates have clearly flattened house price appreciation. They have driven pretty aggressive deflation in other purchases that often depend on loans like used cars. Product inflation was mostly stopped in its tracks. It’s pretty much just service inflation that’s still holding on… People don’t generally take loans out to pay for their car insurance or restaurant visits, so we probably won’t see much cooling there without a significant uptick in unemployment.

I don’t understand this.

There is not doubt QT is taking money out of the system. It is literally definitional.

How is taking money out of a system not helping keep inflation down?

Sure, it can be argued that it is not taking enough out of the system fast enough, but QT by definition is taking some liquidity out if the system.

TL; DR: The QT runoff rates are still at 60B UST and 35B MBS per month, but the Fed is floating/thinking a small reduction (not taper to 0) of QT is being planned, which will allow QT to run longer without causing market disruptions. Maybe this could be called “lower but for longer”, to be a bit sarcastic. At the same time, the resurrected standing repo facility (SRF) will be available to smooth out smaller disruptions.

QT lower but for longer (QT-LBFL) should continue to deflate the housing bubble 3.0 (2020), as mortgages will continue not to be supported by the Fed. Same goes for stock market. If people have any sense.

It been some time now with QT and not saying that QT should be stopped, but the way they are managing this (jawboning every other day/week), it seems that want assets (housing/Stock) to be in permanent plateau…..

But it happened with QT-1 in September 2019, when the repo market blew out because banks were running low on excess liquidity and refused to lend to the repo market, and a repo-market panic ensued and threatened with contagion, and so the Fed stepped into the repo market and helter-skelter doused it with nearly $400 billion in liquidity, which raised its balance sheet again, thereby undoing a big part of QT-1. And that is to be avoided this time.

I think we are about to find out how wide the flood gates will open this time.

Fed is itching, just looking for a pretext.

Are you QE-mongers still out there? Wow!

The SRF will prevent another repocalypse this time around.

The United States has a serious problem, shale gas extraction became flat, the Permian basin, which was the only one that continued to grow, has stopped doing so. This is very bad news.

The federal reserve does not have tools to combat this, in the short, medium or long term.

LOL, such BS. Shale gas production soared and exceeded demand and, with storage levels well above the 5-year range for this time of the year, the price collapsed in the US due to overproduction. Overproduction has always been the problem with shale producers. They successfully crashed the price of NG ever since 2009. US NG futures today trade at $1.67/MMBtu, down from around $9 in August 2022, and down from the $4-$13 range in the years before 2009. And producers have been throttling back production to prop up the price.

I hope the information I sent you has been useful to you.

That dude who owns the that site you linked (which I deleted) has been saying the same stuff for over 10 years. You just don’t know because you don’t pay attention. You just came across this one article of his and thought he was Jesus Christ or whatever.

I even posted some of his crap on my site 10 years ago. This is what he said in 2014, on my site, 🤣: “On the gas side, all shale gas plays except the Marcellus are in decline or flat. The growth of US supply rests solely on the Marcellus and it is unlikely that its growth can continue at present rates.”

https://wolfstreet.com/2014/03/06/shale-oil-gas-not-a-revolution-but-a-retirement-party-2/

And US NG gas production has exploded since 2014.

In 20 years, the USA will be producing more refined hydrocarbons than today. And in 50 years, the USA will be producing even more than that.

Most of the hurdles to producing refined hydrocarbons are regulatory, not geological.

I sincerely doubt in 50 years we will be producing more hydrocarbons. Just what basins would those be produced out of? What regulations are stopping oil companies?

Look at a chart of global oil & gas production going back 100 years. There’s very consistent uptrend.

Humans are resourceful and will find a way. When the permian basin is exhausted there will be another breakthrough. Exploration technology will improve etc.

There may be temporary shortages & hiccups, but long-term the trend is up. Energy is life, and peak cheap oil is a myth.

I have seen that “proven reserves” are about a 500 year supply at current fossil fuel consumption levels.

There’s a lot of regulatory pushback, including the fact that many of these reserves are under public lands.

We are an energy exporter (since Obama). We are energy independent.

We have production and refining capacity onshore. More than most of the world can say.

Breakeven costs are an issue for US producers/ fracking is expensive upfront. The Saudis poke the ground and it shoots out for $20/barrel. US needs $50-75/ bbl.

Won’t be a problem when oil is consistently above $100 in the coming decades.

I’ve worked in oil & gas in the Permian Basin for three decades. Production has never been better, especially with the new zones being developed. It’s the most prolific basin in the U.S.

It appears that the FED organization has also been learning about MMT in real time for the past 15-25 years?

The print button has been effortless to press, but even at the height of the “good times” the UN-Print is repulsive to the financial industry.

Combine this with the “Fed independence” doctrine that enables completely disjointed monetary and fiscal policies that require the “print” button… and it really does seem like MMT is mostly about the race to the bottom/ who can hit the “print” button faster?

(Obviously only “as needed”) /s

Wolf,

Thank you for the summary.

Notably absent from the Fed minutes is the biggest ‘What if’ out there. Inflation surges again, forcing the Fed to hike rates this year.

Am wondering if this prospect might force the Fed to slow QT before the process does do on its own next year (as you and another commenter have suggested).

Powell acknowledged that at the last FOMC presser. He talked about the possibility of inflation getting stuck above the Fed’s target.

Personally I feel this is the likely scenario – inflation that bounces around in the 3-5% range for years to come.

I think at best inflation will stay where it is, at worst will go back up led by energy and loose fiscal policies by government prior to the election. Those who just got their student loans forgiven can now do a lot of stimulating of the economy, or pay down other loans.

The Fed does not know. Pause,pause, pause. That’s what the Fed knows. So they don’t know. Unemployment claims down from estimate. Bond yields tick up. The Fed is in good shape for a recession with ample room for rate cuts. We all thought a recession was iminent, the lag affect etc. no recession and Fed models have rate cuts. No model for recession. Why rate cuts when no recession? Now Fed worried about hikes. PCE comes out end of month.

The FED will always be reactionary. It can try its hardest to predict the future of the economy, but the economy is too complex to predict. Especially when one considers the external shocks that can happen such as war or COVID.

People who get angry at the FED for not properly predicting the future are idiots.

At best they can use their knowledge to try and predict the future and be smart enough to react when they are wrong.

Since this fed is currently doing Qt,

and the stock markets and crypto markets continue melting up, almost daily, with all time highs printed repeatedly, even though CRE is having fits, with huge vacancy problems, this fed with its unlimited toolbox should triple down in its QT imo, resulting in a stock market super nova and the fed books will get balanced in a new york minute, and stocks can soar like its 1999 all over again! Just saying, why not?

As we have already seen, that this feds tool box is one heck of a back stop, with its unlimited resources. I guess the old fable about giving a drunk another drink to help him sober up really doesn’t apply here, in todays marketplace. No sir, this time is truely different. More BTFP, i dunno; perhaps sprinkle in some talf, some tarp too! So many options to choose from.

I think the current movement in stocks has very little to do with the Fed, and much more to do with the AI FOMO bubble.

There’s just no way Nvidia will be able to quadruple its chip sales for AI every year. Who will pay for them? What about when the buyers realize that it’s not producing the effects they thought it would?

@Einhal

This is why there are only a few truly visionary entrepreneurs in the world who can SEE what might be possible, while the VAST unwashed (like me) can only see what’s right in front of me…

The possibilities of where this technology can lead is beyond most of us’ ability to imagine. Science fiction often becomes reality over periods of time. I could give examples, but I’m sure most here can think back to things that seemed impossible only to become necessary in day-to-day life.

As to AI, I think something along the lines of the movie “Blade Runner” and much of its futuristic tapestry is one of the answers to your original question I copied and pasted above. But it’s only one thread of many of where it might lead…

Sure, tons of things CAN be, but most don’t reach that point.

For every Amazon, there were 1,000 that failed.

I don’t think the odds is in Nvidia’s favor to “grow into” its valuations.

This!!!

I think many people are confusing the actions of the stock market with the actions of the FED.

Yes, there is no doubt that the FED can influence the stock market, but overall the stock market is going to do what it does. Of it bubbles, it bubbles.

The only way the FED can influence that is to throw the whole economy into a tailspin which is the very definition of cutting off your nose to spite your face.

Great article. I love these kinds of concrete descriptions of processes that seem opaque.

But in the end doesn’t the success or failure of all these schemes depend on foreigners continuing to buy US debt.

I suppose the answer would be: “they always have and always will”. Which is a bet on the idea that the world never changes – at least on a large enough scale.

But, we can perhaps say for now, “eat drink and be merry”, the machine will continue to turn over for at least a few more years.

Oh no, you have just uttered the words of doom. Whenever anyone says things like that, something comes along to bit yer bum.

Actually they depend on SOMEONE (foreigner or not) to continue to buy the debt.

When that someone stops, yields will rise and the debt will become attractive to someone else.

Yield solves all.

Wolf, is there a relationship between QE/QT and brokerage account margin? In other words, would QT eventually show up as less margin being used to buy equities etc. Or maybe not until excess in the ON RRP gets to 0. Or, no relationship and it’s mostly a function of Fed Funds Rate. Or something else? I remember an article you published about the reduction in margin during 2022 that coincided with the Fed Funds Rate rising and QT starting. Thanks!

Margin loans are demand based, and limited by equity valuations (collateral). If markets tank, margin loans decline with them because investors get margin calls and have to sell stuff, and other investors are trying to front-run the margin calls and sell before they happen (risk-off). I have not seen a direct correlation between margin and QE/QT, only the indirect connection via asset prices.

Hopefully the Fed has learned what it can and cannot control.

“Reports on the death of the present cycle of politically motivated monetary easing, in the words of Mark Twain, grossly exaggerated.”

Our leaders and our citizens are addicted to easy money and the resulting inflation.

Cheers?

B

PS. Above quote from today’s Mises Institute letter.

“If we weaken our already anemic QT, we can be ineffectual for even longer!”

Another FED Governor (Waller) coming out today 2/22/24 and saying not going to ease soon. His Speech Title says it “What’s the Rush?”

“The hotter-than-expected data that we received validates the careful risk management approach that Chair Powell has advocated in his recent public appearances. And, with most data indicating solid economic fundamentals, the risk of waiting a little longer to ease policy is lower than the risk of acting too soon and possibly halting or reversing the progress we’ve made on inflation.”

Also “I am going to need to see at least another couple more months of inflation data before I can judge whether January was a speed bump or a pothole.”

So far FED talk is very hawkish and they are cautious. Hope they change SEP in March meeting and match their words with actions.

Yeah… this latest inflation report is like Manna from Heaven for the Fed. It gives them justification to do what they already want to do in an election year… NOTHING.

Love you for this post Wolf!

One other thing to point out. The drain on bank reserves from around $3.5T today to the low $2T range by the end of QT will destroy bank deposits.

Banks can utilize the SRF as you indicate in lieu of deposits, but this will hurt banks in some important regulatory calculations, such as the Liquidity Coverage Ratio and Loan-to-Deposit ratios.

Banks that have a dangerous cocktail of credit risk on CRE loans, underwarter securities portfolio, and shaky liablities will be most at risk in the future of an SVB-style bank run.