Inflation might not go back into the bottle voluntarily, and these mortgage rates – considered low in 1970-2000 – might stick around.

By Wolf Richter for WOLF STREET.

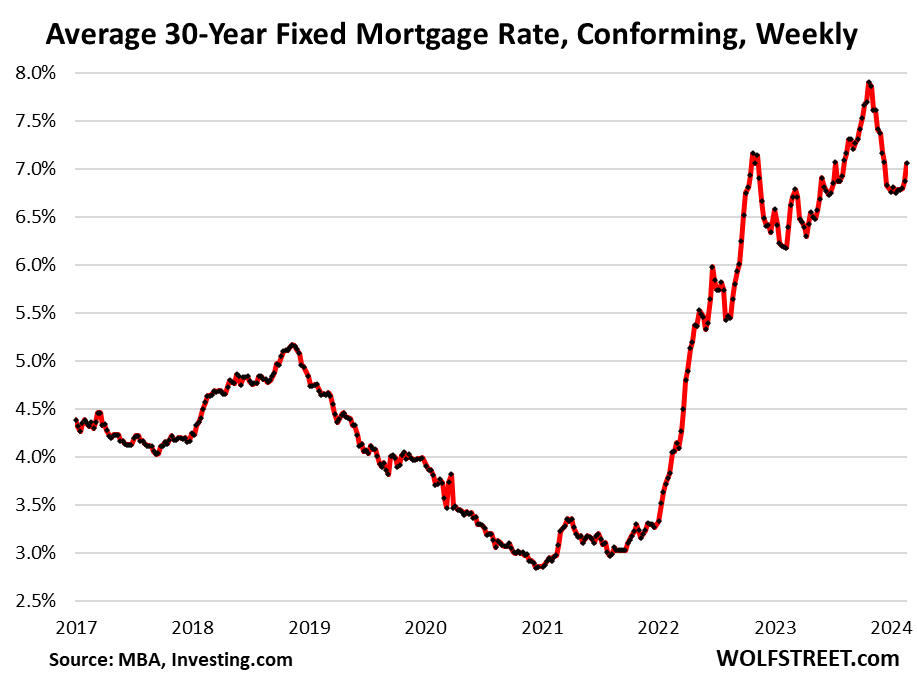

The average conforming 30-year fixed mortgage rate rose to 7.0% in the latest week, according to the Mortgage Bankers Association today. The daily measure by Mortgage News Daily has been over 7% for days. These are the highest rates since mid-December, when they were on their way down.

Mortgage rates had been flirting with 8% back in October last year when the rate-cut mongers fanned out in droves all over the media. Amid enormous hoopla about a gazillion rate cuts in 2024, starting in January, longer-term yields plunged. Mortgage rates plunged with them, with the average 30-year fixed mortgage rate, as tracked by the MBA, falling as low as 6.75% in mid-January. And it was going to be the next boom in the housing market. And then inflation data came in and called for order.

Housing market still frozen.

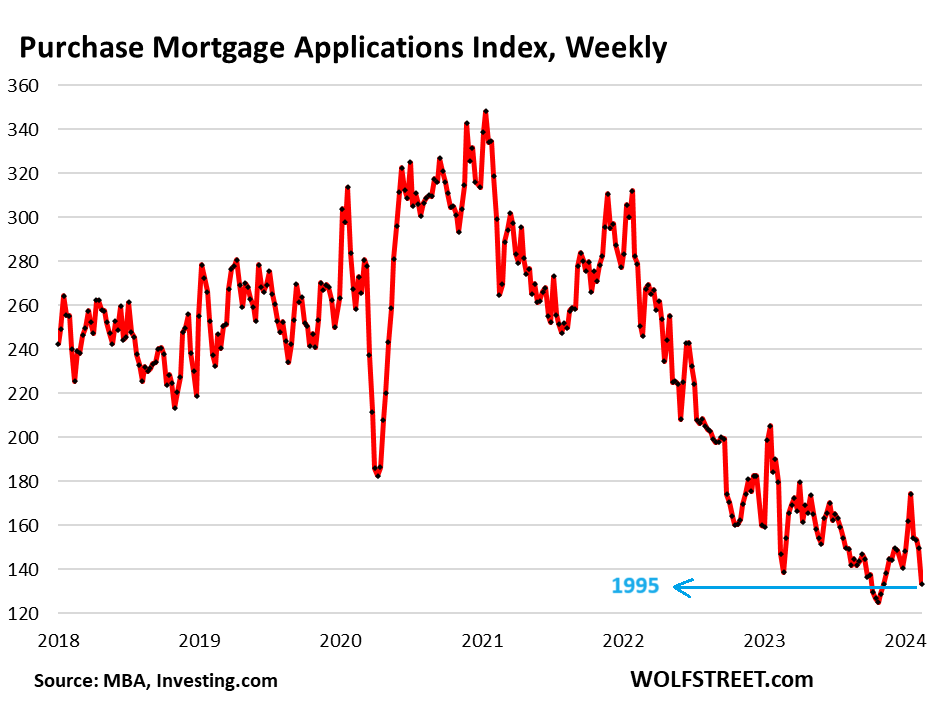

That relatively small increase in mortgage rates caused mortgage applications to re-plunge – after they’d barely risen from the record lows going back to 1995 – a sign that the housing market remains frozen because prices are still too high, and potential sellers are still thinking that this too shall pass, and potential buyers have figured it out.

Mortgage applications to purchase a home plunged by 10% in the latest week from the prior week, seasonally adjusted, according to the MBA.

Mortgage applications were down by 9% from the already depressed levels in the same week a year ago. They were just a hair above the late-October record lows in the data going back to 1995. They’re down by:

- 2022: -47%

- 2021: -42%

- 2019: -43%

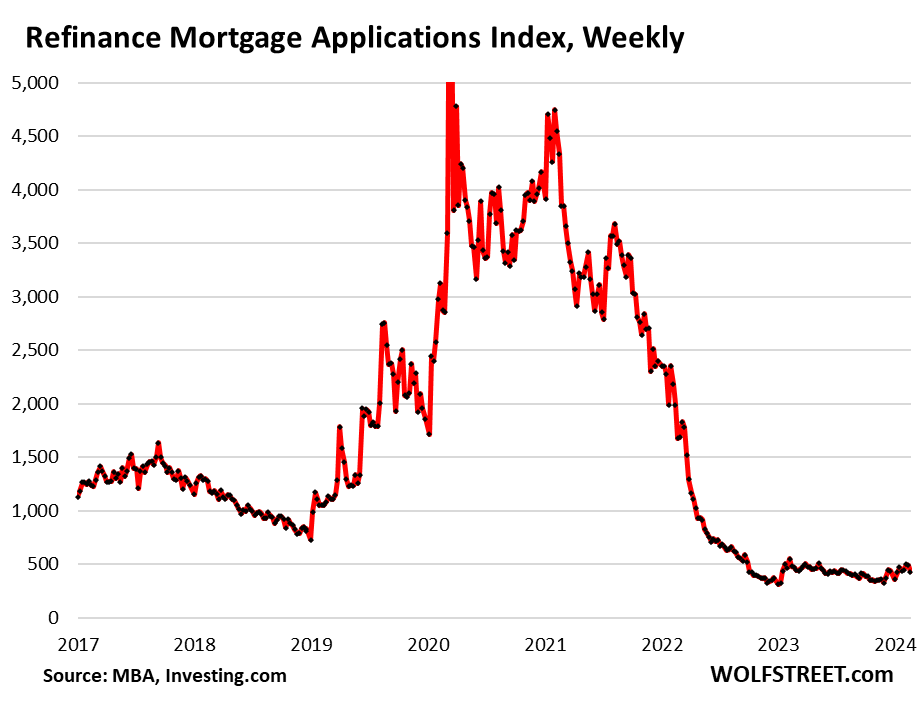

Mortgage applications to refinance a home plunged by 11% from the prior week, but that drop is barely visible amid the collapsed levels since mid-2022. Refinance applications were down by 89% from the same week in 2021:

Buyers’ strike continues.

There is always the issue that the hope of lower mortgage rates is freezing the market further, beyond what the far-too-high prices are already doing.

Inflation doesn’t look like it’s wanting to go back into the bottle voluntarily, but needs to be forced back into the bottle. If prior episodes with this type of inflation are any guidance, this will take years or maybe decades, interrupted by several massive inflation head-fakes where inflation goes down temporarily, leading to rate cuts, only to resurge to even worse levels, leading to even higher rates.

This idea that inflation will be back to 2% and stay there may turn out to be “transitory,” to borrow Powell’s infamous term. And then these higher mortgage rates are going to be with us for years, and maybe for decades, as they had been in past decades.

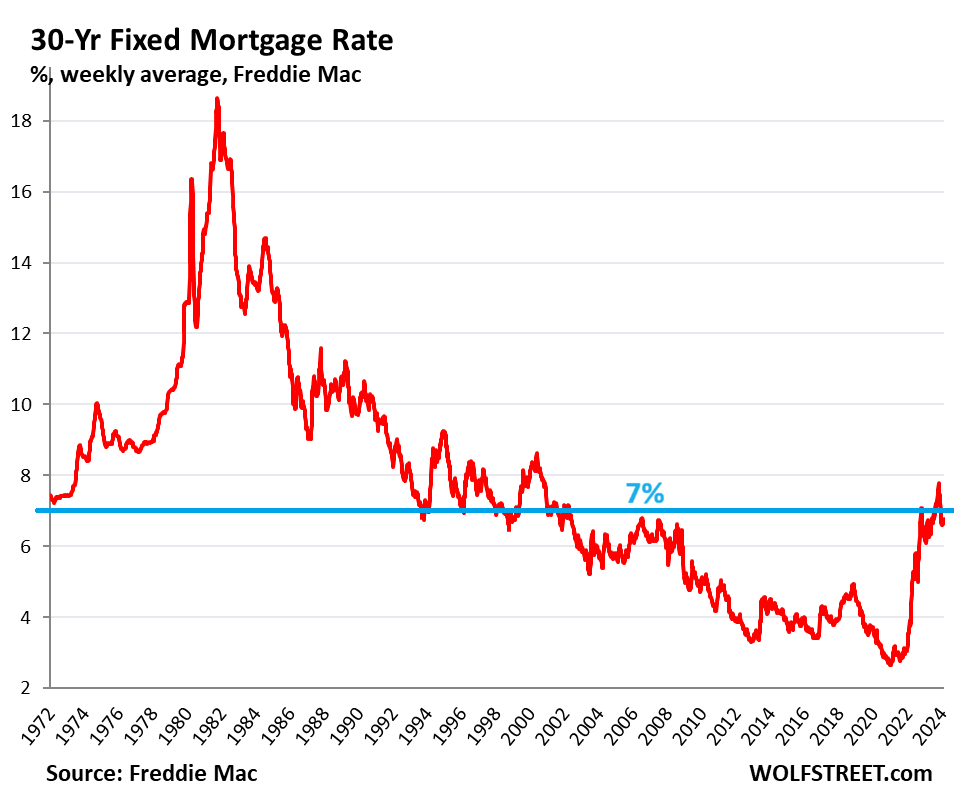

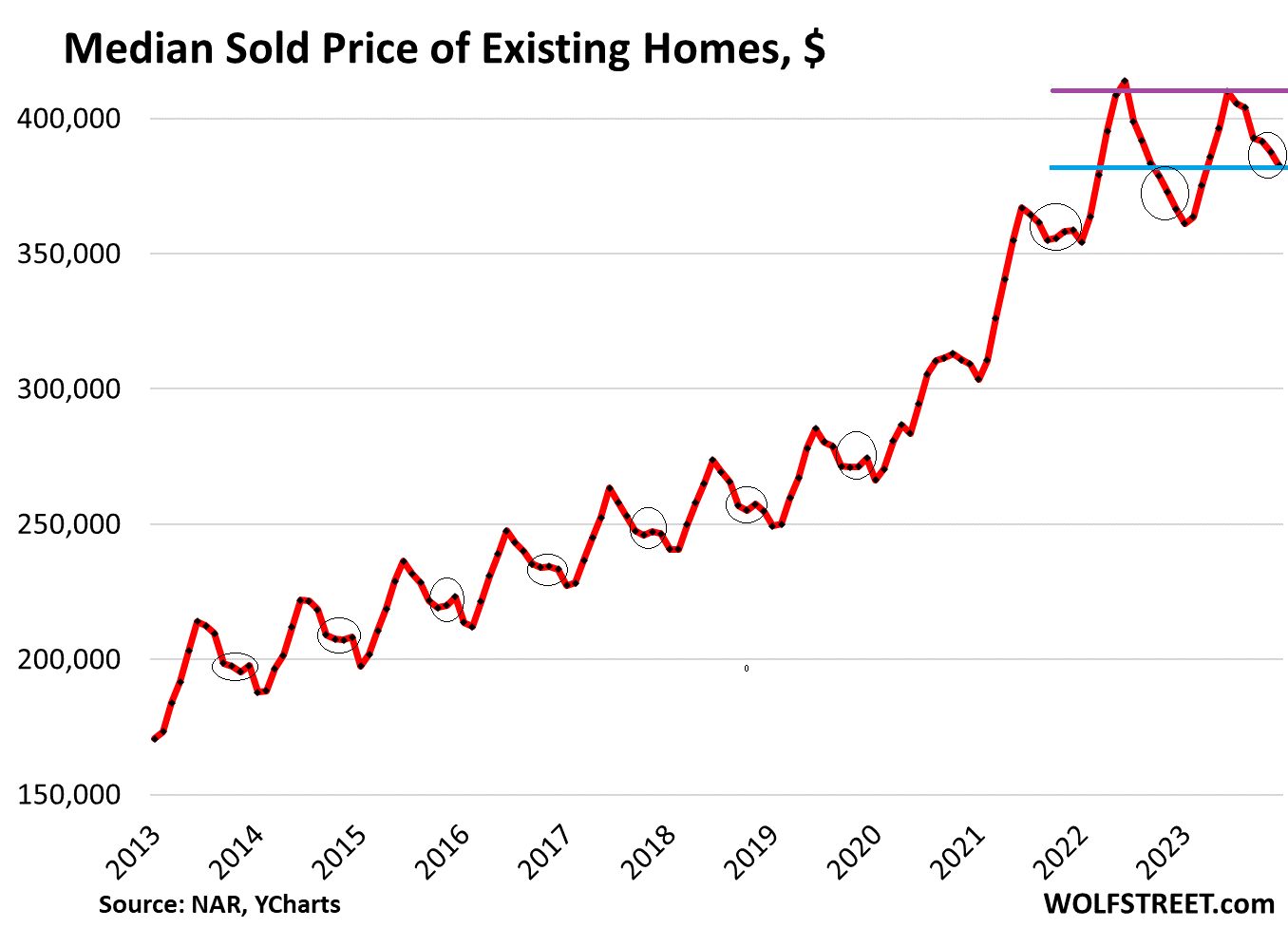

A 7% mortgage rate was considered low – or impossibly low – in the three decades from 1970 through 2000. And homes sold just fine, but at lower prices. Here is the average 30-year fixed, as tracked by Freddie Mac through last week (it will release the new data tomorrow), with the 7% line in blue:

What is over is the frenzied no-questions-asked national mania in 2021 and early 2022, when mostly Millennials – in their peak earnings years – and GenZers were trampling all over each other and knocked each other out, and outbid each other to “nab” that overpriced house, and thereby bid up prices in a historic manner, in order to lock in the low mortgage rates that were beginning to rise as inflation was kicking off.

Now the hope for lower mortgage rates is holding back potential buyers and potential sellers alike – sellers that already bought a home but didn’t put their vacant home on the market because they wanted to ride up the spike all the way. There was a lot of that. Now they’re trying to rent it out, or turn it into a vacation rental, and there’s a lot of that too, but it’s not easy, and the carrying costs of a house are high. So waiting for much lower mortgage rates is lining up to become an expensive bet.

Homebuilders have figured out the drill and kept sales at decent levels by cutting prices, building at lower price points, and buying down mortgage rates. The median price of new houses has dropped 17% from a year earlier to a two year low, not including the costs of the mortgage-rate buydowns, which come out of builders’ profit margins.

But homeowners that want to sell have not figured it out. Sales of existing homes have collapsed. And the national median price has put in a double top, with the high point in June 2022, the first such situation since the housing bust. In some markets prices are still rising, but in others prices are spiraling down, and that’s how it washed out nationally, according to the National Association of Realtors:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Home Prices were much lower during 1970-2000 at 7+% mortgages.

1/5 the current prices, along with maintenances, insurance & utilities also at a 1/5 or lower. Now you can’t even get insurance in CA, it will be interesting to see what the Cal state run Fair Plan will actually cover when it all goes up in smoke. Probably will just cover the banks mortgages & some small pittance so there’s not a mass homeless issue, like the last fires. Most of Those folks 2017-2020 fires didn’t have sufficient or any insurance, but got paid something thanks to Newsome’s reaming of deep pocket PGE, which we will all pay for ever after. But that won’t happen again. If FEMA had to come in to replace a mass fire, flood etc., the insurance would become obscene. If FEMA replaces your disaster struck property your insurance goes through the roof forever (reason why many of the Sonoma & Paradise folks didn’t carry sufficient insurance).

Nevertheless, the tilt meter is in place for failure again without any apparent safety net.

So a few realtors, mortgage brokers etc.. will have to go work another job for a few years.

It might encourage large profitable corporations to provide or invest in local housing development for their employees as a perk.

My future in-laws, recently moved from Texas, bought a house in a suburb of Portland, Oregon, in 1978 for $75k at 12.8% interest. That was the going rate then.

dec 2023 paid off 30 year mortgage – initial interest rate was 7.825%

orig date 11/1994

was ARM == adjustable rate mortgage – walked it down to 2.625% by 2000(1% max per year FHA)

turned into rental so we couldn’t streamline FHA(cause it was no longer primary)

did conventional after that one

——

TODAY

you have devalued fiat $dollar and higher rates with limited inventory

squawk all you want = if I don’t get price I’ll turn it into rental

btw total debt = $0

“large profitable corporations to provide or invest in local housing development for their employees as a perk.”

Google tried to do this, proposing what were essentially college dormitories, but Mountain View wouldn’t allow it. Google also had started on a large mixed use project on several lots around the downtown San Jose train station. They got as far as tearing down all the existing buildings before the current downturn caused them to abruptly cancel the project. Now neighbors are left staring at a bunch of denuded lots (which Google still owns).

And that is usually a scam. Apartment’s that go up now are usually subsidized by the city with cash paid out of the taxpayers pocket then given tax breakouts for the next decade out. Then they charge exuberant rent. It’s all corruption starting from city governments to federal. It’s corporate welfare and it’s everywhere!

Right now houses are owned as investments not places to live. 40% of all housing is owned by investors. You either have vacant houses sitting there doing nothing but increasing in value or maybe for sale, rent and now the undesired airbnb in your neighborhood. People who rent the house for short term.

This is all Fed created. And frankly I get tired of hearing that word Inflation by the Bureau of Lying Statistics, a much better measurement is Purchasing Power. How many hours did it take to buy the same thing in the past. 10 year mortgages turned into 30 year and if you look on your deed all houses have a life expectancy. Most people are buying houses that have already reached or exceeded that life expectancy. But the scam goes on 89,000 regulations and laws keep this financial scam in everything going on. I heard Wolf talking about the fat lady singing but that fat lady is gonna be a total collapse of the financial system. This debt is unsustainable and has to blow up.

“40% of all housing is owned by investors.”

OK, let’s clarify this:

100% of all multifamily rental housing is owned by investors by definition. There are about 30 million multifamily rental units. So take multifam out of the picture.

Single-family houses: total housing stock about 90 million houses (including single-family attached). Of them, 15.1 million are rental properties (=17%). 80% of those 15.1 million rentals are owned by mom-and-pop landlords, owning 1-10 houses. The 32 largest institutional investors hold only 500,000 rental houses.

The 32 largest institutional investors hold only 500,000 rental houses.

really – you’re saying BLACKSTONE worth of $100 TRILLION

only owns less than 3% rental homes

did they sell to someone else???

like numbers = makes me feel like I’m one of FEW LANDLORDS in neighborhood

Yup. Blackstone isn’t even close to being #1. Invitation Homes [INVH] is #1 with 80,000 SFRs. And from there it drops rapidly.

Blackstone started Invitation Homes and sold it to the public years ago, starting in 2014, and by 2019 it had sold its entire stake. Recently, Blackstone bought Tricon with 38,000 rentals. Tricon was #3. American Homes 4 Rent [AMH] is #2 with 59,000 SFRs.

A couple of multifamily landlords are a little larger in terms number of rental apartments vs. number of rental houses.

“Home Prices were much lower during 1970-2000 at 7+% mortgages.

1/5 the current prices, along with maintenances, insurance & utilities also at a 1/5 or lower.”

Purchasing power of 100k in 1970 was about equal to 800k today. How far off are prices really?

Just to examine this a little further, in 1980 the average price per square foot was $41. Using an inflation calculator, that is $162.53 in todays money. Average new single family home size has increased to 2,469 sf. Using Wolf’s numbers from December, the median new single family home price dropped to $413,200 or $167.36 per square foot.

I’m sure my math or numbers aren’t perfect, but again, how high are prices relative to 40 years ago?

To answer your question, you would be much better served to look at what a reasonably maintained house that sold in 1980 will sell for today. In different parts of the country the results will be very different. I grew up in Cerritos, CA, and a 3/2 ranch tract home that sold for around $52,000 in 1976 (my parents bought one) is now worth a little over a million if it’s in reasonably decent shape.

Another couple things worth considering. First, smaller homes tend to cost more per square foot than larger homes. The average size of new homes has increased substantially since 1980. Looking at the price per square foot doesn’t take this trend into account when comparing home prices from 40 years ago to new home prices today on a per square foot basis. Second, comparing the cost of new homes today to house prices from 1980 ignores the fact that many new home developments are far from city centers where land is much less expensive. Buying a new home in Corona is not the same as buying an old home in Cerritos. Using national averages and prices per square foot obscures these differences. The problem is avoided using a simple sales pairs methodology like the Case Shiller index if you really want to know how high prices are today relative to 40 years ago.

Guesstimating @rojogrande observations into some rough numbers, I’d say a per sqft pricing discount of 20% (due to larger sizes) needs to be applied, and another 30% for location penalty comparing current housing to the one from the early 80’s.

That gives current per sqft pricing to be twice more expensive.

Also whenever something overreacts in one direction, this always translates into an overreaction to the opposite side.

Vadim: No disrespect, but a 50% drop in prices is just silly, unless we are enduring something like the GFC.

My rough numbers don’t even address hedonic adjustments for improved construction. I’ve owned houses built from 1906 to 2019, including one built in 1980. The house built in 2019 is so far superior it is hard to compare them.

ChS,

“50% drop in prices is just silly, unless we are enduring something like the GFC.”

Why is a 50% drop silly, when a 100% spike wasn’t insane?

National median SFH home prices pre-ZIRP were perhaps $180k in 2000 (vs. maybe $360k today).

And the only “positive” (sarcastic bunny ears) economic development for the US over those 23 years was DC printing money (in one form or another) to gut interest rates…in order to maintain the illusion that the US wasn’t getting its ass handed to it in terms of international economic competitiveness.

The US is *just starting* to wake up from a government cultivated economic opium dream.

And the “stately pleasure domes”/McMansions for McMorons financed under that Dream Scheme?…they’re toast.

Here in British Columbia, Canada, $300/Square foot gets you particle board sheeting with vinyl siding, carpets and Linoleum. I’m currently building with plywood, triple paned windows and hardwood floors at $400/Square foot.

Prices aren’t the major driving factor here. Sure they’re not crazy high compared to 40 years ago, but you also have to look at how household income has stalled. Buyers see that they must break the 35% guideline in order to enter the market, with most seemingly having to spend closer to 45-50% or more of their household income just for housing. Meanwhile people are almost forced to “side hustle” in order to make up the gap there, putting a damper on living and enjoying the thing called life!

sold MH park 2 years ago but our multi-unit rental market was out of control(still is)

so I bought 3 homes in nice area’s (paid up using CASH) and would like when time comes(if it does) to sell these and use as down payments on multi-units and LEVERAGE(50% max)

but right now still looking at SFR as rentals

Exactly. Every time home prices come up, someone makes a dumb analogy about the price of houses in the 1800’s.

The price of milk used to be 25 cents a gallon. Good luck finding milk for $3 a gallon today. Your cereal’s gonna get mighty soggy while you wait for $1 milk.

And that house you’ll never buy is going to get really expensive while you wait for the price to drop 75%

CCCB – Just because… How is your cereal going to get soggy without milk? Maybe stale?

Russell beat me to the punch here.

There are many insurers issuing new homeowner and dwelling policies here in California now. A few are not.

Aside from fires, the insurance companies may also be anticipating another “Great Flood” scenario here in California’s central valley. The state’s climate models are predicting two of them this century under RCP 8.5 (as opposed to a 1000 year return time historically). A 2010 USGS study conservatively estimated 700 billion in damage if that were to happen; realistically probably over a trillion today. I don’t really blame the insurance company for moonwalking their way out of the state.

I spent 43 years as an independent insurance agent (Ga not Ca). I recall when one of the companies we represented pulled out of Ca citing a hostile state regulatory climate. This was about 1975. I remember the company president telling me that he had made plenty of business mistakes in his career but leaving Ca was not one of them.

Two things are going to happen…insurance will be either unaffordable or unavailable. Look for the state to step in and stick the taxpayers to subsidize your policy (the taxpayers who haven’t fled the state yet).

Yes, expected. Higher for longer…

…most recently the 20 year auction saw weaker demand and higher yields. More to come. A lot more…

CONgress better balance that f&^%ing budget ASAP. LOL! Don’t hold your breath gentlemen.

All that Congress needs to do is to cut around $2 trillion a year in spending and that is a very easy task with across the board spending cuts before even evaluating specific programs.

They don’t need to. They’re already wealthy and soon will be increasing their salaries they receive for what amounts to zero productivity and increase in global warming to due all their hot air. Debt and wealth matters a lot on a personal level but seldom in the abstract.

Sorry, the debt and the dollar will matter, even for these congressional folks. I don’t think they will go “full Argentina” (that’s essentially what you are implying).

If they don’t improve the fiscal situation, the dollar, and their dollar-denominated “wealth” and power goes bye-bye, in a myriad of ways.

Argentina and the US are bad equivalents for a lot of reasons. Hard to see anything resembling hyperinflation plus the current plan always seems to be cutting back things that are essential for people to survive.

A country,like a person, can go from riches to rags. “Argentina has historically vacillated between periods of economic growth and crisis. Between 1860 and 1930, it became an economic powerhouse; in 1913, Argentina was one of the ten wealthiest countries per capita in the world, ahead of France, Germany, and Italy.”

Perhaps an astute conjecture that may come to pass. The unknown is the timeline, which is a regressive variable.

Constructed by the evidence.

Good article. I insisted that my 30 something children take a look at your graph of the 30 tear mortgage rate versus time as the basis of the discussion of how I, as a representative boomer, ruined their ability to afford housing.

It’s funny reading the vitriol here. I opined that the pathway was on the trajectory towards sovereign default years ago…and was mercilessly derided here. You people study market ‘trends.’ Try history.

Great article Wolf, thanks for the deeper insight, as always.

With Inflation seemingly ready to continue with its head fakes, where does this market go from here?

I know the elevated interest rates should put downward pressure on prices, as shown by the double top. But, due to inflation wouldn’t a devalued dollar, in terms of purchasing power, buy less house? Especially as this 4-6% inflation rages onward?

I’d love to stop burning money in rent and build some equity, and due to the builder incentives we are considering new builds. However, currently still waiting for some form of inflection point.

Where’s the tipping point where inflation beats out interest rates or vice versa? Is there one? Is this current market Un-precedented historically?

Thanks for your hard work!

-Bio

Short-term bonds currently yield 5.7%. This beats inflation and gives a nice real yield. Time is on your side.

100% this. You’re getting paid to sit & wait right now.

Waiting gets better and better. The interest earned on what would have been my down-payment has more than covered my most recent rent increase. I am likely moving this year too and each time I’ve done that, I’ve lowered my rent. Realizing I need less things, makes this possible. It’s finally good to be a saver again.

Wait for what?

Not too steal Wolf’s fire, I just throw something against the wall and see if it sticks, which is a regressive variable.

Without a doubt, the current price of assets are in an unprecedented, historic state of unsubstantiated valuation,

Like Chuck Prince of Citigroup warned just before Lehman, you have to keep dancing as long as the music plays.

Prices need to respond accordingly. I can’t hear about how these rates are normal when the increase in prices over the last few years was not normal. That is, it’s great that grandma got a house in 1977 and paid 12% but guess what, the house cost 65k. A house is a place to live.

I’m originally from northern Minnesota and I joke that it’s a great place to be FROM. I have family there and have gone back many times, and I have always been amazed at how affordable homes were. Cheap actually. Obviously the cost of a house is relative to location and the local job market.

But if someone could work remotely and didn’t mind wickedly cold winters, swarms of mosquitos in the summer, leech in each and every of the 10,000 lakes, and blue-state politics, it’s a great place to live!

You really know how to sell a place, lol!

Tourism bureau needs to put you on the payroll.

🤣😍

The climate of our frozen blue state is a feature, not a bug 😜. You gotta want to be here, not want to be comfortable. It’s far from perfect, but the company is above average.

“You’re not a lady, you’re a Tiger!”

Everyone either believes rates will fall again or they’re very happy sitting on their 2.5% mortgage. Cash buyers are enough to keep the market afloat in terms of pricing.

No correction will come without unemployment increasing and the economy taking a dive. Rates won’t fall either without that happening or the government realizing it can’t spend forever (apparently unlikely). Eventually ultra low mortgages will churn and inflation will claw away at house prices relative to wages, but we’ll be stuck like this for a long while it would seem.

“A house is a place to live” hasn’t been accurate since your grandma purchased. These persistent, personal ditties often blind people. Many become wealthy in real estate right up to the present, even at high rates. We do this precisely by buying homes we will NEVER live in.

Option: adjust paradigm then create wealth where available. Or not.

This works well until prices crash. Then I wish you the best.

OK, the fact is that monthly mortgage payment by someone paying 7 pct in 2000 on a home that cost 215000 was less than someone paying 14.5 pct on 60000 in 1980.

That person also earned one third of the wages and benefits they earned in 2000.

Understanding context is the key. Someone of my era was raised by WW2 veteran mother and father.

The biggest mistake this Fed made was to reflate the asset price bubbles. It will taught in schools about what not to do. Obviously, the rich idiots are in charge.

“A 7% mortgage rate was considered low – or impossibly low – in the three decades from 1970 through 2000. And homes sold just fine, but at lower prices.”

Very much a material point!

Bank of America CEO just said the same thing. Get used to 6% and 7% mortgage rates. He made the point that 7% used be considered a good rate. He said people will come to terms that 7% is the new rate.

There are at least two versions of the world, the hopeful and the realistic. Scaled by age, of course.

The CEO of a bailed out bank doesn’t carry much with me, no matter how much false integrity he or she projects.

The job itself has come to promise that the banking industry may essentially, be a mob style operation, sweating the golden goose for unearned profits.

Yes, but, but, but … how much were the prices of homes compared to income? When I bought my first home interest rates were 8.4%, I was making ~$35K, and the home (townhouse) price was $109K.

The lending standards were always 25% of your income allowed for mortgage and 36% for total liability.

Neither the price nor the rate are relative to the past. Waiting for either to align with the past is gambling with time and is likely to cost far more than simply buying when needing to buy or renting when it makes more sense. Price-to-rate comparisons are fantasy as they do not consider the money supply, population, or square footage growth over the same period.

Speculating on appreciation should be focused on the three largest factors for price. Location, location, and location. That is why an 800 sq. ft. pre-war shack sells for a million dollars on the coast and you can pick up a newly constructed 3000 sq. house in the midwest for 400K.

Those differences play out in numerous ways. Property taxes are vastly different, as are renovation costs to value. The latter is why you see most flipping shows in those high-value areas.

The housing market is way too random for an asset class that underlies the very essence of good life thoughts, given that we American citizens pay our fare share of the cost of a democracy.

The election is in 9 months. That would be the first time that the government may consider reigning in deficit spending.

Is it time too pay the piper or a permanently high plateau.

It’s a regressive variable.

Prices are made at the margins, this 25 to 55 yr olds haven’t experienced such an increase in the financial cost of housing in 25 yrs?? Doesn’t matter about 78 or 84 or any prior analog. The frog has been thrown in boiling water. But for 3 d’s and new family creation it should remain chilly for at least 2 years likely a couple more.

Why was the Federal Reserve Board buying mortgage-backed securities through mid-2022 when housing prices were clearly skyrocketing?

Why does the government provide a subsidy to an industry that is overheating?

I’d like the Fed to answer that question, or the same models will be used to make the same errors.

Yes they should tell you why they spent so much for so little. On the other hand they could punish you like a bad guy, deserving of a stretch in the penitentiary,

An AI robot will root out all rebellious tendencies that you have that have previously been judged as undesirable in the training set that was used to train the robot. They will construct a narrative to convict you of the crime that the robot accuses you of.

Agree Bobber,

The MBS purchases still stand out to me.

Arguments “can” be made about covid govt spending and the Fed enabling that response via liquidity/QE. However, the MBS purchases were bizarre, especially as long as they lasted after the dust had settled.

The Fed NEVER should have bought MBS! Totally unconstitutional, borderline criminal. I think Wolf agrees. Goldman should have gone bankrupt, instead, they became a primary dealer…

This should tell you everything you need to know about what is really happening.

” Goldman should have gone bankrupt”

Instead they were converted to a bank and bailed out by the taxpayers. Paulsen once called the people who bailed them out

“Taxable units”

I couldn’t agree more, a lesson that was recently forgotten.

MBS, CRMBS, now mid size banks. China’s main export will be equity loss due to property loss realization and price discovery. Now we see who was swimming naked in CRE China , Europe and Merica.

Because they are fantastically, shockingly incompetent. Their models don’t work. Their policies–including the self-imposed policy of telegraphing their moves months or years in advance lest they “surprise the markets”–are asinine. They are very, very, very, very bad at their jobs.

Were you expecting a more reassuring answer?

Bobber-

“Why does the government provide a subsidy to an industry that is overheating?”

Because they have an inflationary bias as evidenced by the evolution to 2% target policy. And because they have grown even more accustomed and unafraid to pick winners and losers within the economy.

Government manipulation of bond markets in order to protect the job market and the financial system (however well-intentioned) works until the law of unintended consequences rears its head.

If history repeats, a bond-buyers strike (aka vigilante-ism) will address the issue. As always, timing and sequence unknown.

IMHO

Evidence be damned, the mentality of folks with real estate as an investment, generational wealth building and prices only go up has a long time to go before it is shaken.

They’ve been fed the line since they were young. Like religion. I just let them be because I can’t reason with them.

MBS, CRMBS, now mid size banks. China’s main export will be equity loss due to property loss realization and price discovery. Now we see who was swimming naked in CRE China , Europe and Merica.

Let’s be real about this, the FED appears to do whatever it takes to elevate prices. They don’t seem to mind the new investor/renter class division.

Ok. Since we are “being real”, what is the FED doing right now to elevate prices?

I know in the past they have done some stupid stuff (maybe with the best intentions, but still…), but RIGHT NOW what are they doing to elevate prices?

The raised interest rates at a historically fast pace. They have started QT. They have continued to maintain rates and QT in the face of huge pressure from Wall Street to stop both.

Inflation had been dropping, and now has leveled off and maybe started to go back up. Righr now it is possible to read whatever inflation forecast a person desires by cherry picking whatever sub-set of inflation data fits the story you want to tell. It should also be noted that two major economies (UK and Japan) have entered into technical recessions (mild, but still..).

All this to say that the future of Inflation is very vague right now.

Despite this, the FED has maintained rates and continued QT. They have also publicly stated numerous times that they will adjust rates as future inflation determines it should.

So given all of that, how can you say the FED is doing whatever it takes to keep prices elevated?

I think you are confusing the FED with the delusions of the market. Contrary to the nuts on here, the FED does not control the markets.

“mostly Millennials – in their peak earnings years – and GenZers were trampling all over each other and knocked each other out, and outbid each other to “nab” that overpriced house, and thereby bid up prices in a historic manner”

Not possible. Everything is the fault of the boomers. /s

Of course there were other reasons homes were less expensive in the ’70s through 2000. Far fewer double incomes. And far fewer DINKs. And the women who did work were earning less. These changes have armed couples with a lot more purchasing power, and that’s been reflected in prices.

Many crazy-eyed Millennials are over-paying for everything, not just houses. Under Boomers’ watch, the government has been increasing the debt-to-GDP and liquidity-to-GDP ratios, the financial equivalent of meth and heroine. The brains have now been permanently altered.

And they’ll get altered even more when prices greatly plunge.

IMHO I would not put the debt on Boomers. Normal Boomers really do not have a say in this government debt spending. None of us do. We can only vote for candidates that have already been the chosen by dark money. Frontline has an interesting documentary called Big Sky, Big Money.

Corporations sometimes pick their candidates before they even campaign.

There were far fewer dollars in existance in 1970 and far fewer financial instruments through which to channel those dollars. Today, our money supply is well north of $20 Trillion. In 2000, it was about a quarter of that at ~$5 Trillion. In 1970, it was only about $600 billion. In the last 5 decades, our population hasn’t even doubled, but our money supply is perhaps 30 times larger. AND we have invented many new ways to channel all of those dollars into assets. It’s not the price of the house that is so far out of whack. It’s not DINKS, or working women, or boomers, or millenials, or gen-z that changed everything. The goverment has pumped and pumped and pumped new cash into the economy without a commensurate increase in actual value-added output for years and years. Generational values haven’t changed nearly as much as the average boomer likes to gripe about. It’s the value of the dollar that changed. This isn’t rocket surgery.

Maybe GenX is to blame- they never seem to get blamed for anything ;)

RV – interesting that the house of every generation appears to suffer from a shortage of mirrors (…or mebbe we all live and wander in a fun-house hall of them…).

may we all find a better day.

Rocket surgery?

Too bad it isn’t, that’s a GenX specialty.

Many of my more well read acquaintances think that America will collapse in the next 20-30 years, so might as well spend the money now.

That’s not exactly a reassuring thing in terms of rationalizing spending. It means that they fear a crack up boom.

I seem to recall boomers buying houses and moving like mad during said time period.

Great piece as always, Wolf, I’m always looking forward to your housing reports!

Somewhat relatedly: I don’t know if it’s within the scope of what you write about, but any thoughts about maybe taking a similar look at the Korean housing market? I’m far from qualified to have much of an opinion myself, but hear reports from friends that—due largely to their rental deposit system (jeonse) that there’s a massive household debt to income vulnerability with cracks already showing in home prices. The fear here is one of contagion potentially worse than what’s going on in the Chinese housing market, particularly insofar as it will crush many Korean renters (whose life savings are often tied up in jeonse deposits they won’t be getting back).

Totally fine if not in the scope of what you report on, I just thought it might make an interesting piece for us readers. Cheers!

After asking Chatbot about the Korean housing market, it gave me this:

Some articles suggest that there is a consolidation of faith to break out in the market in 2024. There are also discussions about real estate agents cheating customers by charging two commissions and offering flats.

Additionally, there is news about the increase in sales of apartments by tens of percent, indicating a resurgence in the real estate market.

There are reports about the rental market becoming more expensive due to decreasing supply, as well as discussions about political boosts that could benefit the real estate market.

A major factor that should be a downward drag on real estate prices in S. Korea with decreased demand over the next several years and decades is the rapid population decline happening there due to their refusal to procreate.

This problem(?) is not restricted to South Korea, Fruitful.

eg – “…problem(?)…”, so true. Population shrinkage a longtime feature of achieving ‘first-world’ status (and of course, creating a lower labor cost working-class population vacuum that seems to draw so many of those pesky second/third-world folks…).

may we all find a better day.

True, many countries outside of Africa and a scattered few others are below replacement fertility rates today. But Korea is an outlier at 0.68 child per woman (2.1 is the replacement rate). Even the lowest EU countries are over 1. Italy is one of the lowest at 1.2. The US is around 1.6.

To 91B20’s point, the US imports a large amount of new people to offset an otherwise declining native population. Korea, on the other hand, strictly restricts immigration.

I do see it as a problem. The world is far from full and can support multiple times more people. There will not be enough young to support the old. Once a worldwide population decline takes hold, it will be hard to reverse. People should be “fruitful.”

Fruitful – would advise much-deeper consideration of the spaceship’s (planet’s) ecological base and it’s availability/sustainability in the face of the increasing demand-vortex of our modern technoindustrial culture upon it, especially in terms of global living-standards. The economic stability you foresee from further population increase is, unfortunately, colliding with it’s massive consumption of the ‘seed corn’ it needs to exist, the ongoing impact (general availability of adequate freshwater, healthy air, arable land, and relatively-stable sea levels and local climates not available, or easily-generated, on large swaths of our ‘far from full’ world) playing out now.

Adapt we must, as we always have, but to increase a world population that has more than doubled in my lifetime (an effect of the aforementioned ‘vortex’) in the face of the planetary environmental degradation easily witnessed over the same period (I’m 70+), can only increase the probability of ecological, and associated human, collateral damage (the argument of resource maldistribution being the real issue is attractive, but if we are not achieving some effective fixes now, how can we going forward?). Non-first world populations are redistributing themselves as we speak, in search of those better living standards (as they always have), to the apparent chagrin of their first-world destinations-a present indicator, imho, that the world is indeed, ‘full’. Best to you, and-

may we all find a better day.

The Fed needs to make clear that they will not cut rates until inflation is dealt with.

I watch my market closely and people are still buying and telling me that “cuts are around the corner and they’re getting in before RE sky rockets again”. FOMO messes with people’s minds especially if they didn’t get to benefit from the last run up.

Prices will stay elevated until the general public believes the Fed isn’t cutting rates down anytime soon.

This is real talk. I’m cautiously optimistic that, after the recent CPI and PPI data, the next FOMC meeting will hit this note. I honestly think at this point the next rate move should be about equally likely to be a hike as it is a cut, and I hope the Fed makes this clear. “The market” has shown, repeatedly over the last ~3 years or so, that it is extremely eager to sound the alarm on easing of monetary conditions, and it really needs to be disabused of this tendency.

What really needs to happen is for Congress to pass a statute prohibiting the Fed from EVER dropping rates below 4% again.

The benefit from being able to drop lower during a downturn is far outweighed by the harm they can cause with reckless monetary policy.

But that goes against the concept of Fed independance.

Congress should tell Yellen to stop manipulating long bond rates down by skewing new issuance to bills… but her doing that helps congress to continue their drunken sailor spending…

That goes for all assets, not just housing.

The reason people are willing to pay the multiples they are for stocks and $51,000 for a gambling token (I’m stealing that from Wolf) is because they believe ZIRP is around the corner.

No one would pay current prices for stonks if they thought 5% rates were here to stay.

At this point that gambling token limited as it is the number that can be created is a better store of wealth that that gambling token called the dollar which is being debased every hour of every day.

LOL at bitcoin believers.

Before comparing Bitcoin to dollars, look at reality.

Right now so much computing power and energy are dedicated to bitcoin and it barely handles a tiny, miniscule, fraction of the transactions that are done in dollars.

For it to it to handle even 1% of the transactions done in dollars would require exponential more amount of computing power and energy. An utterly ridiculous amount.

Bitcoin is not serious among those who understand computers and currency.

It is nothing more than electronic Beanie Babies. Currently a way to engage in illicit activity (while quickly turning those Bitcoin into actually usable dollars), or a way to engage in greater fool theory.

Neither is a reliable store of purchasing power that is easy to use.

If you told me rates were going to be 5% for a really long time I would buy Berkshire Hathaway right now despite its recent run up. I probably wouldn’t buy, but I would definitely hold the defense stocks I own right now (LMT, HII, RTX). I would definitely buy the oil stocks I own at current prices (OXY, CVN, and others).

Healthcare depends on the company and its valuation. Semiconductor stocks are a lot high, but I am pretty sure both Apple and Intel will be relevant 20 years from now.

They might go up, might go down, but I bet 25 years from now i am sure the stocks i own will be worth more than they are right now (and most importantly, will keep up with inflation).

fair point

If rates are cut. Doesn’t it add to the buying power of the 50 million buyers on the sideline?

Re. Prices should go insane again, right?

I am sure by Spring selling season people will be saying the housing market is back. Then again SoCal has been spring season all around when it comes to demand and price according to many..

“Now the hope for lower mortgage rates is holding back potential buyers and potential sellers alike – sellers that already bought a home but didn’t put their vacant home on the market because they wanted to ride up the spike all the way. There was a lot of that. Now they’re trying to rent it out, or turn it into a vacation rental, and there’s a lot of that too, but it’s not easy, and the carrying costs of a house are high. So waiting for much lower mortgage rates is lining up to become an expensive bet.”

I’ve been waiting to buy for nearly 5-years. I’ll keep waiting too. Thanks, Wolf.

The 3% mortgage holders are effectively out of the market. This is a big chunk of supply. When supply goes down, prices go up, assuming a fairly constant or rising demand. This is one problem. The other problem is that people who need a mortgage to buy a house are competing with all cash buyers, many of whom are foreigners. Unless we have a fairly huge recession, housing prices will not come down much.

Look at the current crazy high prices in the housing and stock markets. Inflation is entrenched, and I doubt the Fed can do much about it, unless Powell goes full Volcker, which he will not. A quarter point rise every couple of months will do nothing long term.

What would the 3% mortgage holders do that they are not doing now if their mortgages were at 6%?

Selling.

“The 3% mortgage holders are effectively out of the market. This is a big chunk of supply.”

Why does this BS keep getting repeated?

If a homeowner sells the house, they have to buy a new house, so they put one on the market and take one off the market, and the result is zero change in the overall supply: +1 -1 = 0.

Only Realtors make money when a homeowner sells and buys. overall inventory doesn’t change.

There are a few exceptions to the +1 -1 = 0: they sell because they died, or are going to die, or moved into a special place to die, or decided to rent and sit out this craziness, or move to a foreign country to retire.

https://wolfstreet.com/2023/07/21/entire-housing-market-buyers-and-sellers-may-have-shrunk-by-20-25-because-of-the-3-mortgages/

Wolf said it himself, the housing market is frozen, mainly because of the 3 percent mortgage holders. I am not sure what he is ranting about. It has nothing to do with my comment. Perhaps he should have another beer.

This math of overall supply works if a home owner sells and buys in the same market (meaning MLS area AND price range). Since this is not common, to just sell your starter home for another one in the same area, do you think it’s worth considering supply of home type (starter, move-up, dream-home, etc.) or supply by area as opposed to just the overall bulk supply? After all, a $400k 3/2 in is not competing with the move-up house down the road the seller wants to buy.

But since there are between 4 and 6 million transactions around the US per year, it averages out, which is precisely what a market does, except in some pockets were people are leaving in large numbers without being replaced by new arrivals.

@William Leake I think he maybe misinterpreted what you said. It’s true that they are a big chunk of supply, but they’re an equally big chunk of demand. I take it you understand this, I think we’ve all just seen so many commenters who act like it only impacts the supply side of the equation that—without an express comment to the effect that it’s a wash due to it’s equivalent impact on demand—it may have sounded like one of those.

@wolf

I think your reader meant to say that the three percenters are not selling unless absolutely forced to. That’s one of the reasons the market is frozen. The other is that the prices are too high for the current mortgage rates, as you pointed you in your article.

Anecdotal evidence follows.

Family friend 1: three percenter, should sell because housing needs changed and should downsize, but thinks it’s not a good idea. Points to the current mortgage rates as reason. In the meantime, continues to pay high taxes and high maintenance costs on the current property.

Family friend 2: three percenter, should sell due to moving to another state, and has to purchase a property in that state. Also thinks it’s not a good idea to “give up the savings” of the current low mortgage rate. Can’t even rent the current property, due to HOA rules. Will look for workarounds and wait it out.

Local housing market (blue collar Boston suburb): super low inventory of properties for sale, very high inventory of properties for rent, for very high costs. Put the two together and you get a bunch of three percenters who don’t want to sell, have purchased a second property, and are trying to rent the first. Because they’re so smart and housing only goes up, everybody knows that.

Nearby vacation destination’s (Cape Cod’s) short term rental market: much higher inventory of properties available for rental, for the upcoming season. The smart people all bought in the past few years and now, rather than selling those expensive to own and maintain properties, they’re being smart again and looking to rent them.

Good luck to us all.

I wonder how long those new vacation rentals will last. The cape already had a ton of them and no one goes there in the winter except the yearround residents.

“After all, a $400k 3/2 in is not competing with the move-up house down the road the seller wants to buy.”

Part of the problem could be that realtors try to reframe buyer perceptions such that a $400k house is a now a humble “starter home.” That’s right up there with calling a 650 sq ft block house with on-street parking a “charmer!”

It is the Mortgage payment I find to be insane.

A 7% payment is a whole lot more than a 3% payment.

Even thousands more per month. Who would choose to spend thousands more on housing just to move?

Simply amazing that Wolf has to continue to set people straight on the math of +1 – 1 = 0.

William Leake says “[t]he 3% mortgage holders are effectively out of the market. This is a big chunk of supply. When supply goes down, prices go up, assuming a fairly constant or rising demand. This is one problem.”

The obvious problem with Sir William’s analysis is that demand is not constant or rising, demand is down along with supply. This is what draws Wolf’s ire and frustration, and rightfully so.

Wolf, your math (a seller sells a house and buys another so inventory is unchanged) is corrct in the long term, but over the short term it isn’t.

Over the short term people do all sorts of things. Move in with a friend (or parents) while looking to buy, sign a short term lease while looking in a new city, etc.

My point is, the velocity of the housing market directly affects the supply of houses on the market in the short term.

So yes, you are correct that someone locked into their house with a 3% mortgage is neither a seller nor a buyer, it misses the fact that house transactions (buy and sell) do not always happen instantaneously. More velocity would require more supply.

Put a more succinct way, the friction (time delay) of selling a house and buying another house would naturally increase supply.

I can only say that many are not “trading up”- they choose to keep the starter home and instead of getting a larger home when kids, dogs and cats come into the home, they instead finish the basement, add a dormer, knock down a wall to make the kitchen bigger, make a 1/2 bathroom that used to be a closet etc on the home they bought with/or refid into a 3% rate on. I have to imagine the lack of “moving up” is also hurting affordability for first time homebuyers since those starter homes become forever homes given the circumstances.

You just described my family. We should be “trading up,” but our payment would skyrocket for marginally more space and it’s just not worth it, so we’re making the starter home condo—which was originally my bachelor pad, and now houses me, my wife, a 4 year-old, and an almost 2 year-old—work for us however we can.

I remember when bunk beds for the kids was a thing.

The problem is with your assumption that demand is constant or rising. At today’s prices demand is in the gutter which is why the market is frozen and prices are sliding sideways at best in a market with high inflation.

WL – What’s changed is the speculative investor has pulled out of the market. There are no less homes required but, the lubrication has been removed. Once they give up on the idea that they can make less money flipping houses and more investing in the stock market, they will sell these assets and free up homes for the general population. Prices will adjust accordingly.

We live in San Fernando Valley in Los Angeles. Prices have been going nuts for years. Right now $1.2 mil gets you a 1,900 Sq Ft (6,000 lot) shack which requires an additional $200k+ to even make it livable. We will continue to rent and wait. I am not going to lie, it has been super frustrating, especially post COVID. How big of price drops are we expecting and/or is realistic?

Would love to hear some opinions on what happens to RE in Los Angeles if the SALT cap is either repealed or significantly raised in 2025, leading up to the sunset of the Trump tax cuts. Is that going to keep the market strong due to the tax benefits crowd.

It’s a fact that the Trump tax cuts will sunset, even if they are extended, I failed to see a situation where the blue states reps do not insist on a significant increase or elimination of SALT for their constituents.

I live in the OC and things here are the same or worse. I do a lot of work in the stock market on sentiment and how the market is driven by it.

I can tell you, under work we’ve done for many years that is usually very good at predicting major turning points, that we are likely VERY close to a MAJOR top in the stock market (on the order or

The Great Depression, not gfc). It’s on that same magnitude, though it may not occur in the same way.

Ultimately, if we do get this perhaps two decade long bear market, it will mean that we are currently witnessing the peak of craziness in the housing market. All of the inflated numbers will begin to unwind.

You do not need to look for a reason as “why”. The market is irrational and driven by emotion. There could be some catalyst event that starts the downturn or it could just be our collective craziness has reaches a peak.

The tough thing is that whenever this downturn does come, there’s no telling who is going to be hit by it. It may well be the people who do not have a home or any assets who still don’t get a chance to get in because of job losses for other things. If there is a big downturn, it may not be an opportunity. It may just be collective realignment with a new reality.

So this year, despite a poor time to buy, will be one of those people we talk about who have to buy. My grandmother passed away in January so my mother who was taking care of her is selling the co-op and is moving out. Weve come up with a plan for her to move in with us and I will be setting up a place to have a downstairs apartment where she can come and go as she pleases.

On her end, shes bringing an additional $100k to the table for downpayment plus $1000 a month to help with the mortgage.

Despite this windfall of cash, you would think putting up 200k on a home (more than 20% down) would be enticing to a buyer. Weve searched tons of homes, and put bids on 3, 2 of which went 50 and 70 over asking (pretty much move in ready) and the third which we fell in love with, the RE Agent was a complete sleazy scumbag and she treated people showing up without an agent like second class citizens. I understand they dont have to tell us what kind of offers they already have on the home, but I havent met an agent that didnt give an answer, until this one.

She was tight lipped the entire time he response was ‘highest and best offer’. Like talking to a fecking brick wall. Obviously our offer for 10 over +20% down was rejected and my agent cant even get a number out of her as to what the best offer was.

Friend of mine during the shark frenzy of 2022, bid 135 over on a 3 story with a current tenant occupying the property on the North SHore of Long Island. Due to this ‘highest and best’ offer BS he lost out on the deal by 5k. Worked out for him in the end because he snagged a 1.1m property a year later for 880, that was in better condition.

It makes me sick to see these prices but Im going to have to bite the bullet to get my family a place to live. Dumps are still sitting on the market for months on end with the usual de-list and re-list to get to the top of the algorithm, and weve thrown out a few offers in the past with almost immediate rejection on these overpriced hunks. Sellers still in the ‘no lowballs I know what I got’ mentality and buyers are like sharks with blood in the water. Every open house I attempted to go to, had a line down the front walk and down the sidewalk 3 houses down….so the market may be frozen but (and I really hate to do this) NIMBY.

Rant over, thanks for your patience.

“Due to this ‘highest and best’ offer BS he lost out on the deal by 5k. Worked out for him in the end because he snagged a 1.1m property a year later for 880, that was in better condition.”

I’m not crapping on you at all here, but this is great example of the difference between the price of something and the value of something. That house your friend bought wasn’t a 1.1m property. You could argue it’s an 880k property, but that takes at least two parties to agree on that. Under all this psychological pricing, there’s the actual value, i.e., the land value (somewhat arbitrary) and the input costs of building and/or replacing the house. Probably should adjust for expected hits to cashflow, too, for maintenance, taxes, etc.

Here in the Great Dumb North, we are still staring down the spectacle of mediocre places (at least here on Vancouver Island) pushing a million bucks. The real reason? People have no idea what a million bucks can do. I have to compete against fools who are all in and have no understanding of opportunity cost at all (dividends, capital gains, etc.). It boggles my mind houses are selling at such a premium over their intrinsic and constantly depreciating real value.

TEMPLE

Itsbrokeagain,

YOU are part of the problem, my friend. If you don’t like the prices, quit driving them higher — quit bidding, quit overbidding… that behavior is precisely what drives prices higher.

I’m really getting tired of people who are feverishly overbidding on everything and then complain about high prices. YOU are causing those prices! So quit complaining!

Wolf,

I dont have much of a choice. We’re trying to be in a home by the summer. Any home for sale in Long Island that isn’t a complete dump sells for over asking. Do I want that? Of course not.

But if I want to follow your advice and ‘stop overbidding’ then I am guaranteed to never secure a home here for as long as I live. I’m not the problem with overbidding, it’s everyone else who’s a freakin NPC that buys the BS and will spend 110% of their income just to say they got a home. And no I’m not renting a place for $3500/month. We’re in my in laws basement apartment paying them 1000 and that’s good enough.

It’s an island, good housing is in short supply, Queens is a dump with all the migrants moving in and the residents are fleeing to Nassau and Suffolk County with large sums of $.

Do I want to leave this place? You bet. But the wife and kid have their say in it too and with all the family here, this is where we are staying.

Itsbrokeagain,

My “advice” — hell no, it’s not advice, I don’t give advice, it’s an admonishment — to you is: Either stop complaining about high prices; Or stop driving them higher by bidding them up.

You’re doing both, you’re driving them higher and then you are complaining about prices being too high, and there are lots of people doing both, and it’s really fatiguing to listen to after you’ve been around the block a few times. People have to learn to live with their actions.

Itsbrokeagain,

You have plenty of choice. You could rent, but, no, you are too good for that. Like Wolf said, you are part of the problem. You and your instant gratification. Whine somewhere else.

What’s NPC?

In any case, I think this is a classic collective action problem. Everyone can realize, on some level, that prices are too high, and that people need to stop getting into bidding wars bidding them up.

But as long as everyone else is doing it, you only get behind by not participating. Buyers aren’t organized well enough to take a stand, collectively.

ItsBrokeAgain,

I think your case is common and highlights a key problem with Federal Reserve interest rate suppression and QE. It is actually damaging families. Many people can’t buy in the same area they grew up because prices are too high and the risk of financial loss is too great. I’m referring to East and West Coastal areas. The experimental Fed policy helped housing speculators and investors, but hurt families who need reasonably priced housing.

It’s anxiety-producing to say the least.

It must be creating marriage stress as well, and maybe forcing some people to defer marriage and family creation.

We know darn well buying a home on the coasts is a huge financial risk. In ten years, will anyone want the large, outdated homes people think are worth so much today? In reality, it’s a depreciating asset, boosted only by speculation (momentum) and rent inflation worries.

It’s high time the Fed stops supporting speculators and investors and starts supporting Average Joe.

Einhal, NPC means “non-player character” from the gaming world.

Frankly, anyone who uses it to refer to real human beings without some sense of irony is at the very least a solipsist, if not a sociopath. They’re basically claiming that only they are subjects and everyone else are objects. Hopefully irony was intended.

Bobber, Einhal and EG you guys all hit it on the head.

We as buyers all need to stop and say no more, but like it was during the pandemic where people fought over rolls of paper towels, the majority will say no but there’s always that one who will buck the trend because of less competition for a home.

And NPCs I say it with irony because a ton of people here do not critical think and blindly follow the news/media. I’m sure the majority of my friends have never heard of this site, which I’m grateful to have found because it provides a reality to how things are, despite MSM saying otherwise.

Itsbrokeagain,

Wolf has it right. You can participate in the market or complain about it. Full stop. Either or. But doing both is wrong. If you are going to participate in the market, then you are part of the group that is driving high prices (unless you are one of those people who do nothing but constantly submit lowball bids that never get accepted). If you have almost bought, or almost sold a home then you are a participant driving the prices in the market.

Personally, while I never actually complained about the market (I rarely complain about markets, I take them at face value for the information they provide), I was not happy with housing prices while I was looking.

I then came to realize what I had always known, when my view of prices and market prices are out of whack, one of us is missing something. I came to realize there were some factors I was was missing in my local market (Las Vegas).

I was able to find a place that I was not ecstatic about paying the price for, I also wasn’t cringing. I fully expect that I will be able to sell my house in 10 years for +/- 10% of what I bought it for. Maybe not the best investment, but housing is an expense, not an investment. I also bought a place that might have some upside surprise in it.

That is what makes a market.

@Temple,

Building a home here will set you back 1.2-1.5 on the South Shore. I agree, most of these actual values of homes should be in the 3-500k range, but stupid money has inflated what should have been your return after 30 years, and did it in 3 years. And people think like stonk, housing should still increase at that rate.

And you your stupid money is helping to put a floor under housing pricesl

@Desert Rat,

To good to rent? Re-read my last post about where I’m renting. Already doing it dolt. And my stupid money? The wife and I worked our asses off, and not only paid off 6 figures in student loan debt but in this period of high inflation, we put it all back in the bank in less than 3 years. So if you think I got stupid money like everyone else did, you’re gravely mistaken.

eg – My son calls me an NPC because I have a programmed answer for everything he tells me. Most likely, he just doesn’t like my fatherly response. He also refers to me a Boomer when I am being too practical for him.

I have asked all of my friends to not look for homes for next 2 years or so.

Buying a home at these price levels is not a must and can wait while renting for a year or two.

Home prices can go up or down but going down is much more probable than up.

The cost of everything has included a lot and honestly I think we are living in a very tricky time.

All asset bubbles are field by cheap money and cheap money is gone only hole is left for cheap money to come back.

Everyone is holding on to their assets hoping to get better price with cheaper money as enabled by the fed.

Recently was in a subd division where monthly cost to carry a home was 6.5k but median home income is 65k.

Something has to give .

Itsbrokenagain:

I purchased my first home in a trendy Seattle neighborhood in 2001 with very little down since I was practically broke. FOMO.

My new neighbors smirked when they met the guy who overpaid but the timing was right for me on a personal level and fortunately, prices accelerate from there.

No one has any idea where prices will be in the years to come. People think they know, but they don’t.

It could turn out to be an investment opportunity of a lifetime for you, or a turd that haunts you financially.

Also known as, “market forces”. Markets are never fair or efficient. In fact, likely the opposite. The outliers set the market prices, not the median buyer. The more people there are on the planet, the more “stupid” outliers there are to make the market.

So true. And many of those ‘stupid’ outliers who make the market have been right for the past few decades in the US.

It’s also about momentum. The outliers are usually the first to reverse course when momentum shifts. I wouldn’t say momentum has significantly shifted yet, but we are close.

I see a lot of overpriced houses for sale that were purchased in the 2021 to 2023 period. Why are they selling? Seems like a confidence problem to me. Whatever the case, these places aren’t selling. They usually list them high enough to recover the original purchase price plus RE commission, but they just sit.

Perhaps buyers can sniff what’s in the bag.

That is literally the opposite definition of a market.

Outwest that’s great. We’ve come to the same realization, that shelter is the main priority. If the prices continue to go up, great but whatever it is in 30 years, is what it is. Not concerned with return on investment, just a good place with solid bones (most homes in our range are getting to or have exceeded 100yrs old) in a good school district we can raise our daughter in.

If you follow Wolf, you would have seen the last Case Shiller post and noticed the NY metro hit another record. Most of the metros/cities on the list already peaked and are now coming down. We are entering “peak” buying season, yet mortgage applications are near record lows. Mortgage rates are pointing back up.

NOTHING in this market points to “it’s a great time to buy a house”. Very few people are forced to buy a house. Some people are forced to sell due to death, divorce, relocation, etc. Don’t confuse the two.

You mentioned Long Island in your other comment. LI is and always will be overpriced for everything.

You could always live in CT and take the ferry over to see your family. I imagine regular trips on the bridgeport & port jeff will run less than the inflated costs of owning property on LI.

I don’t think he is even from Long Island. I am from LI, and nobody there says “in Long Island”, like he did a few posts up.

I live in West Hempstead, bud. I say Long Island because if I abbreviate LI here I’m not sure everyone knows what I mean. So I say it for clarity.

We thought about moving out of state, but I’m trying to make career moves to a Utility closer to home with a significant jump in pay. If that doesn’t pan out, our only resort would be to pack it up and head out. Id rather prefer sunny blue skies and a beach however lol

My situation is a bit similar to yours. Need a bigger house for a growing family. I feel your frustration.

I’m in the Bay Area where houses are sold at insane price levels again in some cities. Other cities seem to be catching up as well. A month ago, a house with foundation problem, termite infestation, water damage, cracked roof tiles, outlets and chandelier that should be museum show pieces et al was listed for 1.66M and went pending within a week.

Yet I as a stubborn person, unfortunately for my wife of course, am still holding the line and not giving in.

Wish you good luck with your decision.

Many spouses want to hurry up and buy something overpriced, but I keep mine at bay by saying we need to consider the kids’ education cost, retirement medical, and retirement travel. We need things covered in case asset prices collapse. Better safe than sorry. FOMO is for financially unsophisticated fools and speculators.

Itsbrokeagain,

For the love of logic, do some MATH. Unprompted analysis if was faced with your situation:

I always have a choice.

Quit the “I’m trying to be in a house by summer” non-sense. Unless you have kids, which you haven’t mentioned, WHO CARES when you get a house?

Is my time in my in-laws’ basement coming to an end? If answer is no, keep staying in the basement.

Find an apartment for my mother while we sort out the housing situation. She could be there for 1-2 years. She had choices too.

Keep looking weekly until the right house is listed, for the right price, that I can afford, and won’t be bitter about.

BTW, my son who is 17 uses the word NPC. You’re an adult, don’t use that word.

Unwanted advice/analysis rant over.

Yes I have a 5 yr old. Its not coming to an end, but without that second influx of cash we are priced out of Long Island unless we want to move somewhere deep Suffolk and I commute back to College Point in Queens.

To be clear, when the pandemic happened I was all for the recession that shouldve happened and was happy our due diligence in paying off our debts and still having adequate cash to put down for a home would allow us to get in ‘at this right time’, but alas that never happened and Wolf’s articles showed how that was true, so I eat my shoes on that one.

You need to go to a few open houses for sale in San Antonio where no one even bothers to show up. I have never seen anything remotely like a line of people to an open house here.

Excellent article and comments. Totally echoes what is happening in my area of Vancouver Island. Investment owners are in denial, with some still trying to catch the B&B wave as an alternative to selling. I would guess B&B will also be in decline as Govt here is trying to restrict the rampant B&B trend in the hope to increase rental supply. Maybe renters and new buyers will finally get a break. It hasn’t been a fair marketplace for a long long time.

I went through the high interest rate nightmare of the early 80s. Bought a rancher on a 1/2 acre with a peek view for 63K. I sold it almost 20 years ago but it is now worth close to 1 million. And now it is 60+ years old. Crazy. I drove by it the other day and noticed the same old single pane windows and obviously the walls are still 2X4 with r12 insulation. There is a long way for prices to fall.

To illustrate Vancouver Island: Here is the price chart of the metro of Victoria (Vancouver Island, BC):

Thank you. Saw that one. Last week CHEK News reported on a starter condo price of 1.1 million in Victoria. My nephew lives there and can barely afford his apartment. We send him $300 per month to help him out as he works through his apprenticeship. He is the first to admit he will be moving away when he finds a different job.

Yesterday big announcement by both Govts (Fed and Provincial) unlocking public lands, offering lower rate builder loans, reduction of permitting window, all to put more multi family rentals and smaller homes on the market asap.

This is the official policy:

delivering more middle-income small-scale, multi-unit housing that people can afford, including town homes, duplexes and triplexes through zoning changes and proactive partnerships;

offering forgivable loans for homeowners to build and rent secondary suites below market rates to increase affordable rental supply quickly;

building thousands more affordable homes for renters, Indigenous Peoples on and off reserve, women and children leaving violence, and building thousands more on-campus student housing units;

delivering thousands of new homes near public transit, and launching BC Builds to use public land to deliver affordable homes for people;

introducing a flipping tax to discourage short-term speculation;

providing an annual income-tested tax credit of up to $400 per year for renters;

providing more homes and supports for people experiencing or at risk of homelessness;

streamlining and modernizing permitting to reduce costs and speed up approvals to get homes built faster; and

strengthening enforcement of short-term rentals.

It will make a difference over the next few years. They have pretty much declared war on B&B investors and flippers.

There are 15 properties for sale in the valley where I live. They have been on the market for almost 1 year. Not one has sold. None have dropped their price. The buying season is upon us but I would be surprised if any of them sell at listed price.

The only thing that will resolve the supply problem in Canada is when governments take back their responsibility for building low income housing. The market will never build enough of that. Never.

Wolf, might be too small potatoes for you to bother with, but there’s lots of data at the VIREB website for all the major communities on the rest of Vancouver Island, i.e., everything north of Victoria, including Nanaimo (my stomping grounds and the area I collect data on). Trends are basically the same but it’s interesting to see the volatility of some of the smaller places in particular (Port Alberni, for example).

TEMPLE

I think housing is a big part of the economy. Keeping rates low was firing up all kinds of construction jobs and housing all over again after the GFC. There was really never any fiscal stimulus compared to the monetary stimulus until Covid. Fiscal stimulus went over and beyond what was needed during Covid. That stimulus was surreal.

Howdy John. When they sent me some $ while being ZIRPed, the last of my head hair left me. Thought I had seen it all at 65…..Surprise Surprise Surprise Bubba

85 now and pretty sure I haven’t seen it all yet. I’ve still got the $1200 check with Donald J Trump’s name on it. Pretty sure someday it will be worth more than the cash value was when I got it. I don’t think anyone can possibly live long enough to see it all LOL.

Bubba:

I’m young (40s) and I was disgusted with the stimulus. I figured it would hurt my kids but rather is hurting me and the rest of the 90% immediately.

I remember hearing Buffet discussing market valuations in the ZIRP era, stating that prices are to be considered relative to interest rates.

I’m now learning about MMT in real time, wondering how the money supply will play out and up?

The Great Reset will be a rug pull for most of us.

Sadly the can will be kicked further yet, beyond what most people think possible.

Fire insurance is being non-renewed throughout Colorado. FEMA is weighing in on the flood insurance too.

Having a mortgage is great… except in case of a total loss? I’m confident that the housing market (and others) will remain considerably irrational for at least a while.

I see no evidence from this post that you’re learning anything about MMT other than the lazy, uninformed misrepresentation of it in the public discourse as a synonym for “unconstrained money printing.”

Which it is not. It’s a description of fiat monetary operations, with a series of implications for maximizing (or minimizing) fiscal policy space.

EG:

Correct. No evidence of my knowledge or existence is presented in the comments section, nor is intended to be.

You definitely know the words and stuff tho, awesome!

Wolf,

If Testorerone Pit is ever offered as hard copy, sign me up for one because I don’t do Kindle.

Same here.

Me as well. Very sorry to see it only in Kindle. Been following this blog for over a decade, when the domain name matched the book title. Keep up the great work, Wolf. We love how you do it.

–geezer

It won’t be, sorry. You can read the kindle version on your smartphone while you’re on a plane or wait at the DMV.

At my age, reading anything long on a smart phone is pure punishment!

I guess I can read it on my Chromebook with the download of Kindle software.

To be fair, I bought a Kindle copy of TP. I was going to read it on the plane, but after just 3 or 4 pages I realized that this was a book that deserved to be consumed and digested in the proper environment where it can really be understood. Not on an airplane with the consummate interruptions.

I closed it and opened up some airplane dreck.

I am looking forward to reading it after I finish my current project.

Howdy Folks. How awful, you mean I can no longer get a NO money down home at 3% interest. The Horror.

D-F-B,I agree, it really is patently unfair!

MW: 10-, 30-year Treasury yields end at highest levels since November following ugly 20-year bond auction

TLT is going to take quite the spanking.

I live in one of the hottest and craziest housing market cities, since about 2002. Up, down, up, down, up, up, up. Not Las Vegas but close.

I think best case right now is for housing prices to stay flat for about 6-8 years, while inflation is 3-5% the whole time. I know, I know, the Fed “is gonna” get it back down to 2.0%. Ok sure, they’re working on it with talks of softening QT already.

It could very well be that the buyer from 2021 who paid $600k and locked in at 3% is going to have a new neighbor in 2030 who also pays $600k but is at 7%.

“Wait, I thought this house was going to be worth $1.2 by now??”. Bummer.

This is also my prediction. Home prices stay rangebound, while inflation lifts income & rents till both are more in line with home prices.

The highest real estate prices in Canada, in Victoria and Vancouver, have made rental units so high that seniors and people in service industries cannot afford it. They must transit in from Pitt Meadows or PoCo or North Van. I heard a 75 year old lady telling her butcher her landlord raised her rent and she could not find anywhere else in Vancouver to move with her dog. She had to go as far as Fort Langley, leaving her network of supportive friends behind. Hers is a typical story.

But the thing is, Vancouver has no industry! 20% of people are civil service. Foreign students maybe 15%. Retail and restaurants have closed ~ 15%. That leaves most people involved in money laundering, as in most ports!

While not common yet, developers are building rent only developments. Perhaps this isn’t new but first time I have heard of it. 3 and 4 bedrooms homes are rent only and start at $3,059 a month.

There’s many houses in subdivisions that aren’t explicitly build-to-rent, but are often bought and rented out.

True but not the developer as landlord.

I live on a street that has a about 20 homes, I think 15 are owned by different LLCs that all use the same property management company that is directly related to the developer.

Looks to me like they offered some kind of investment package where they sell to individual investors and the builder manages it.

They get the cash now and some cut forever.

Parents bought the house we grew up in for $12,000 in the early 70s.

My Dad was making $20/hr in ’79.

Interest at the time didn’t even matter.

Never heard them talk about it.

My parents were the same way and times were similar (without a housing bubble though).

They bought a house in 1970 for 45K at 6.5% (assumable loan) in S. CA. This was a little hardship since he was making 9K/year and back then, Mom stayed home.

They only had one car and Dad carpooled so Mom could leave the house to get groceries. My grandparents who purchased their house in the 40’s for 5K couldn’t believe how much houses had skyrocketed. 9X!!