But that’s how inflation is, once out of the bottle: It serves up nasty surprises.

By Wolf Richter for WOLF STREET.

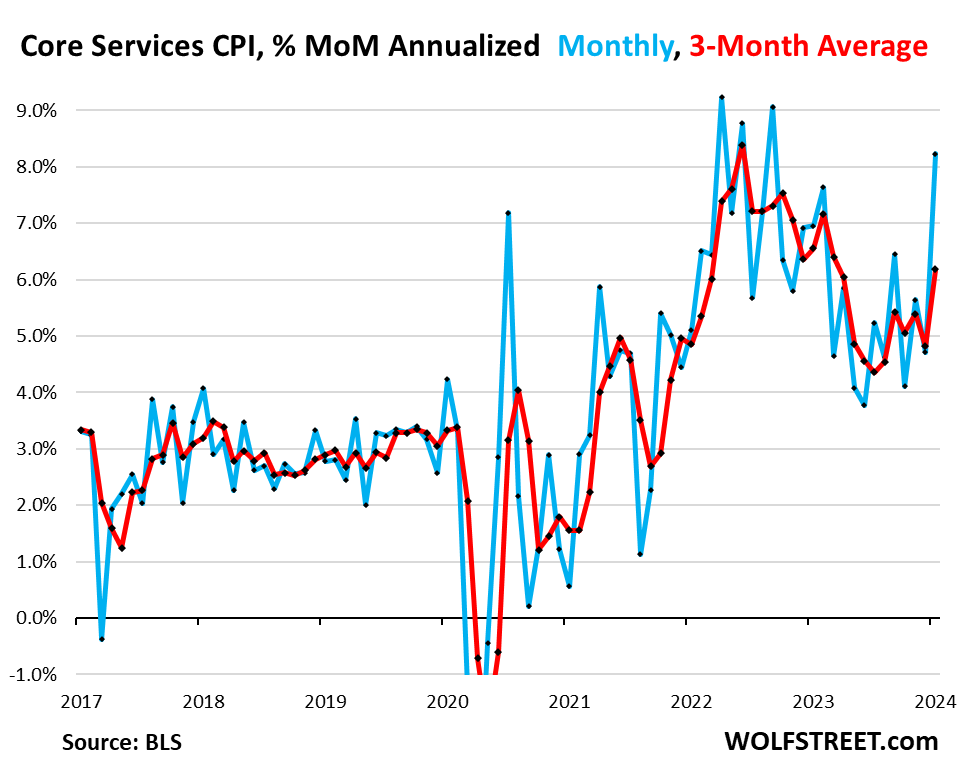

We’ll start with the “core services” CPI (services minus energy services) because this is so crucial, and because Powell keeps talking about it. We have been concerned here for months about the refusal of core services inflation to ease off, and we’ve found the acceleration in the fall last year “very disconcerting.” But that’s how inflation is – it tends to serve up nasty surprises. And now it did.

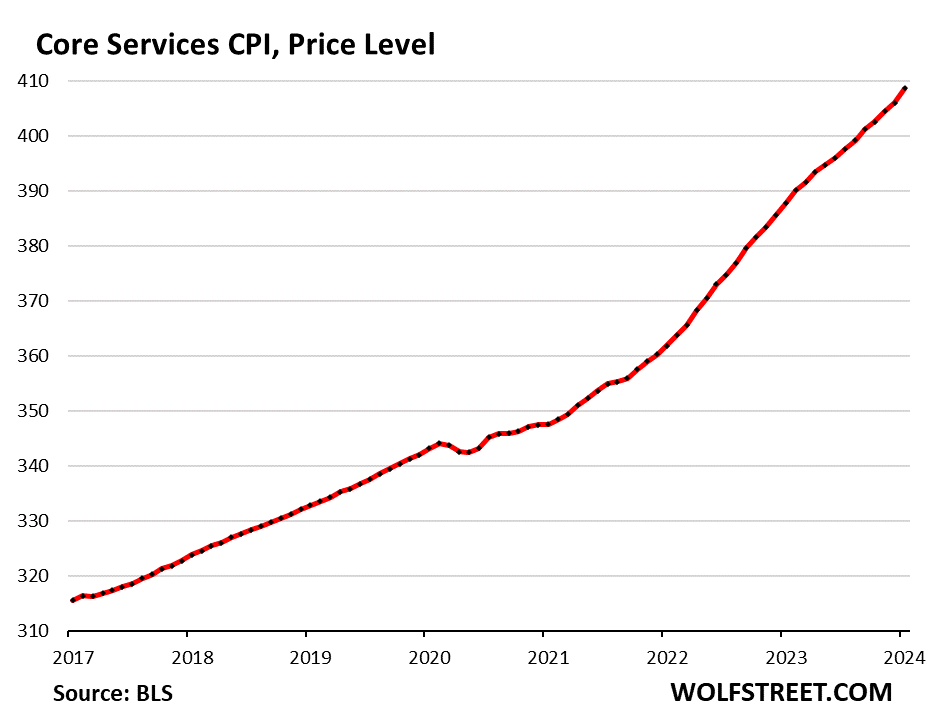

“Core services” CPI jumped by 0.66% in January from December, or by 8.2% annualized (blue). In this inflation cycle, only three months were worse (April, June, and September 2022). It includes housing, insurance, health care, subscriptions, etc., but not energy services. Core services is where consumers do the majority of their spending – and it’s re-heating from already hot levels.

The three-month moving average, which irons out the month-to-month squiggles, jumped by 0.50%, or by 6.2% annualized (red), the worst since March 2023. All this according to the CPI data released today by the Bureau of Labor Statistics.

Inflation in January boiled down to this:

- Energy prices continued their plunge (-10.4% annualized in Jan. from Dec.).

- Prices of durable goods continued their decline (-5.4% annualized in Jan. from Dec.), on a plunge in used-vehicle prices.

- But food prices rose (+4.5% annualized in Jan. from Dec.).

- And “core services” were red hot (+8.2% annualized).

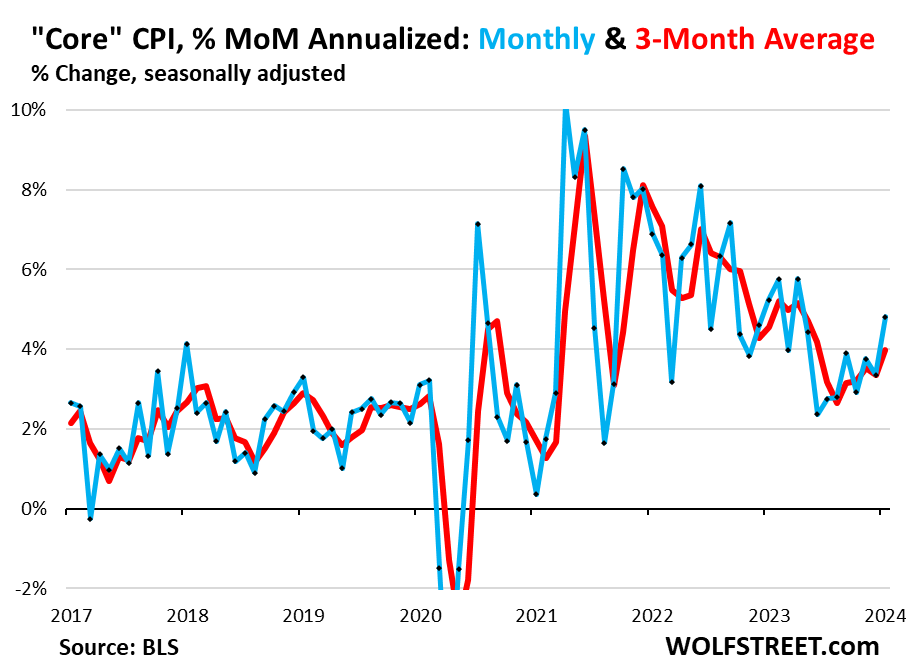

“Core CPI,” a measure of underlying inflation that excludes food and energy products, accelerated to an increase of 0.39% in January from December, or 4.8% annualized (blue line), the highest since April last year. It was held down some by the decline in durable goods CPI, but pushed up more forcefully by core services CPI.

The three-month moving average of core CPI accelerated to 4.0% annualized in January from December, the worst reading since June (red line).

Overall CPI accelerated to an increase of 0.31% month-to-month, or 3.8% annualized, the worst reading since September.

The BLS adjusted its seasonal adjustment factors last week going back five years, as it does every year at this time. These adjustments were relatively minor, with the effect of seasonally adjusted figures getting moved up a little in some months and getting moved down a little in other months. Everything here is based on the adjusted data.

Year-over-year:

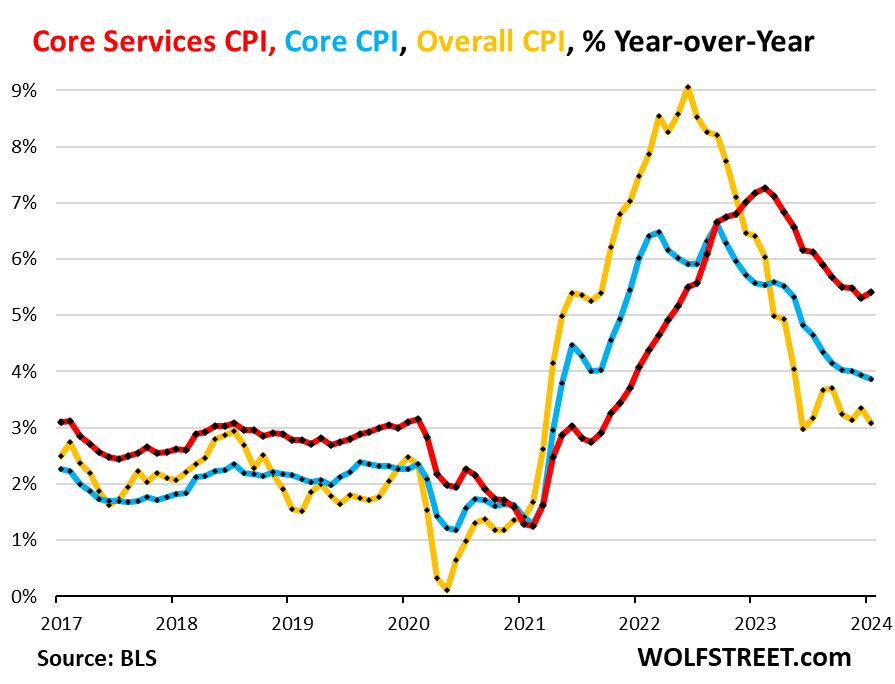

- “Core services CPI” re-accelerated to 5.4% (red).

- “Core CPI” rose by 3.9%, roughly the same as in the prior month (blue).

- Overall CPI decelerated to 3.1% (yellow), pushed down by the 4.3% plunge in energy prices and the 1.6% drop in durable goods prices:

Core CPI (blue) has hovered near the 4% line for the fourth month in a row. Core services CPI (red) has been in the same range around 5.4% for the fourth month in a row, as this inflation proves to be resilient:

Core services CPI components.

Above we discussed core services CPI’s nasty surprise spike. Here is what goes into core services CPI.

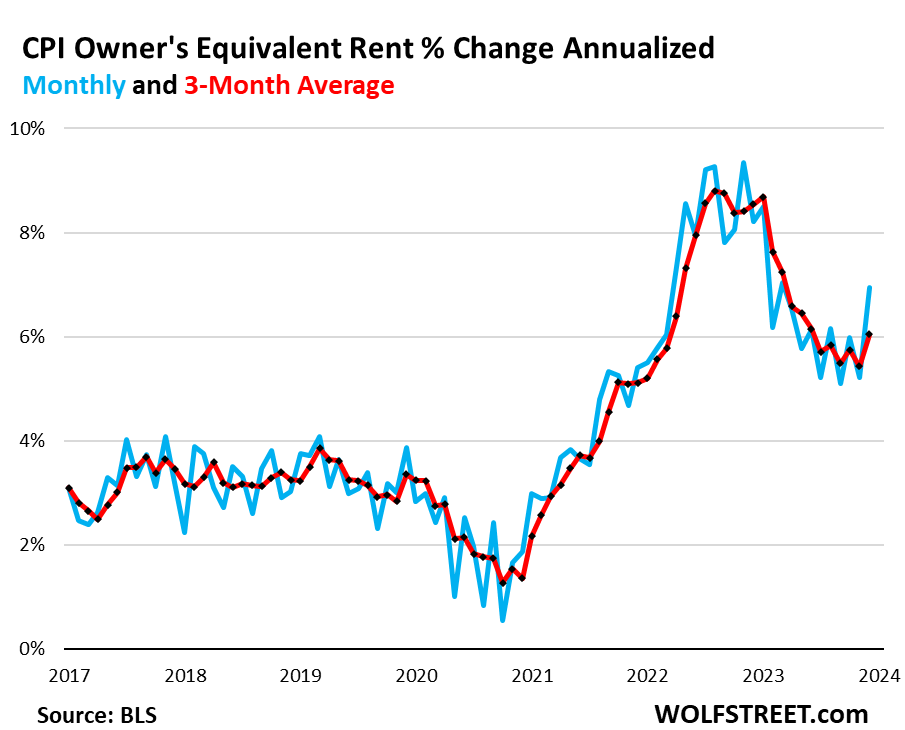

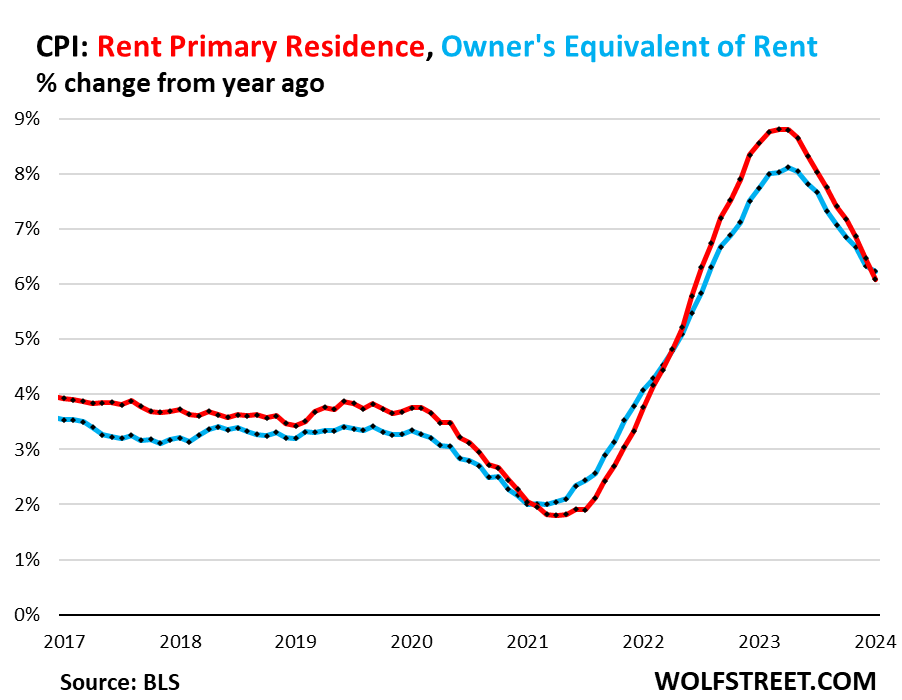

The Owners’ Equivalent of Rent CPI jumped by 0.56% in January from December, or 6.9% annualized, the worst since April.

The three-month moving average jumped by 6.0% annualized, the worst since July.

The OER index accounts for 26.8% of overall CPI. It is designed to estimate inflation of “shelter” as a service for homeowners and is based on what a large group of homeowners estimates their home would rent for.

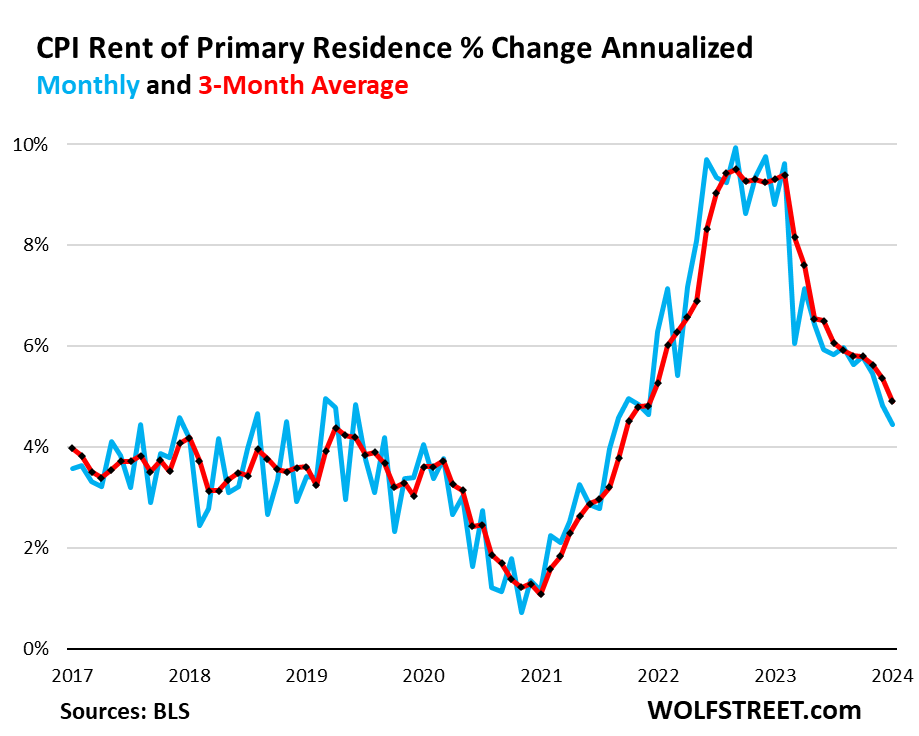

The Rent of Primary Residence” CPI rose by +0.36% in January from December, or by 4.4% annualized, a deceleration from prior months. The three-month moving average rose by 0.40%, or by 4.9% annualized.

The Rent CPI accounts for 7.7% of overall CPI. It is based on rents that tenants actually paid. The survey follows the same large group of rental houses and apartments over time and tracks the rents that the current tenants actually paid in these units.

Year-over-year, the OER CPI rose by 6.2% (blue in the chart below) and Rent of Primary Residence rose by 6.1% (red).

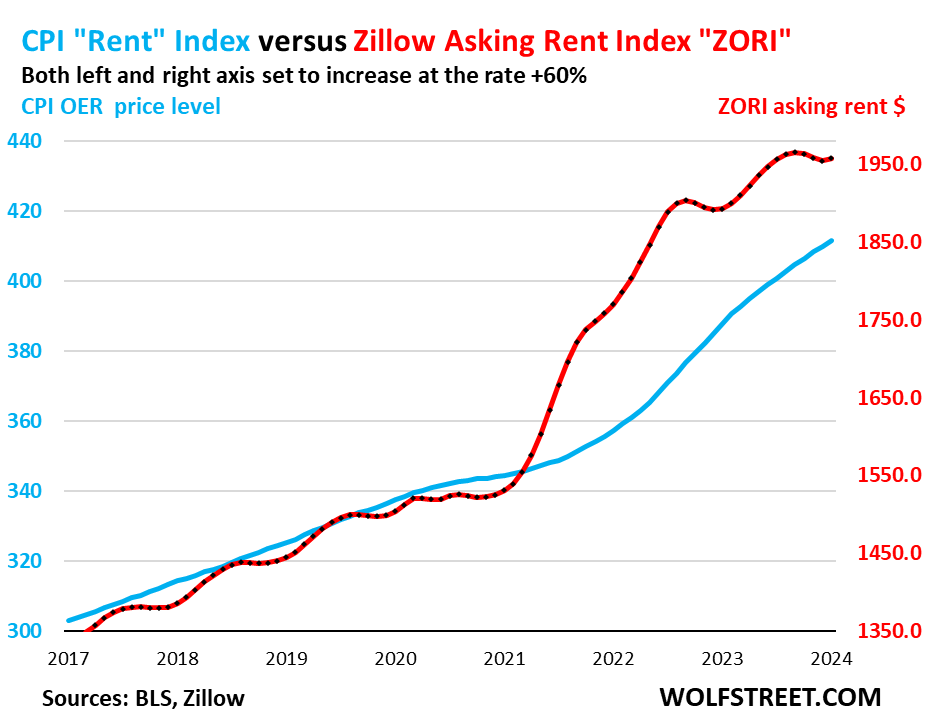

“Asking rents…” The Zillow Observed Rent Index (ZORI) and similar private-sector rent indices track “asking rents,” which are advertised rents of vacant units on the market. Because rentals don’t turn over that much, the ZORI’s spike in 2021 through mid-2022 never fully translated into the CPI indices because not many people actually ended up paying those asking rents.

The ZORI rose to $1,957 in January, after the seasonal dip late last year.

The chart shows the CPI Rent of Primary Residence (blue, left scale) as index values, not percentage change; and the ZORI in dollars (red, right scale). The left and right axes are set so that they both increase each by 50% from January 2017, with the ZORI up by 47% and the CPI Rent up by 36% since 2017:

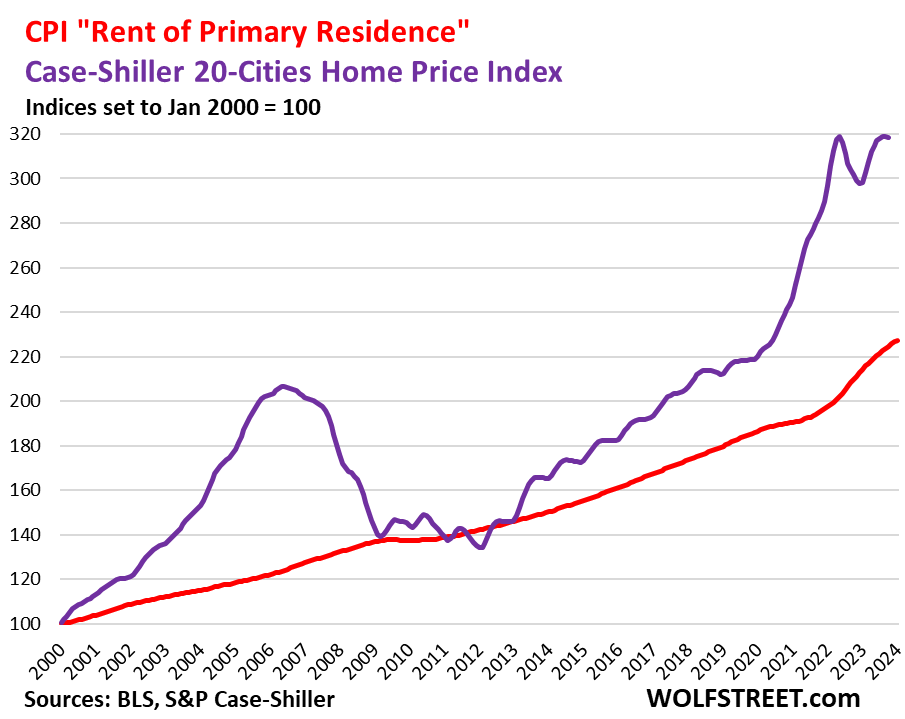

Rent inflation vs. home-price inflation: The red line represents the CPI for Rent of Primary Residence (tracking actual rents). The purple line represents the Case-Shiller Home Price 20-Cities Composite Index, which lags a few months and has now put in a double top, with the last reading showing the first decline (see our “Most Splendid Housing Bubbles in America”). Both lines are index values set to 100 for January 2000

Medical care services, including health insurance. Since October 2022, we’ve lambasted the method the BLS uses to estimate health insurance inflation, and the grotesque results this produced. January was the fourth month after the BLS tweaked the system.

Starting in October, the crazy pendulum has been swinging back. Health insurance CPI rose by 1.1% month-to-month each in October, November, and December. In January, this accelerated to an increase of 1.4%.

But these increases are still far below the grotesque 3.9%-per-month plunges (-38% annualized) during the prior 12 months that had caused the year-over-year health insurance CPI to collapse by 37% through September 2023.

Now, with these month-to-month increases for four months in a row, the year-over-year collapse is being gradually undone, so far from -37% in September to -23.3% in January.

Medical care services, which includes health insurance, jumped month-to-month by 0.7% (8.7% annualized), but the year-over-year collapse of its health insurance component (-23.3%) still caused the medical care services CPI to rise only slightly year-over-year (+0.6%). It will become more positive each month for a while.

The table is sorted by weight of each service category in the overall CPI. The CPI for medical care services is the third largest item, with a weight of 6.5% in overall CPI, and over 10% in the core services CPI, and it will continue to gain momentum year-over-year as the health insurance CPI within it continues to revert.

Also note the continued spike in motor vehicle insurance. The 1.4% month-to-month spike translates into an annualized spike of 18%, compared to the year-over-year spike of 20.6%, so this isn’t slowing down much.

Six of the 17 services items, accounting for 40% of overall CPI, have year-over-year inflation rates of over 6%!

| Major Services without Energy | Weight in CPI | MoM | YoY |

| Services without Energy | 64.3% | 0.7% | 5.4% |

| Owner’s equivalent of rent | 26.8% | 0.6% | 6.2% |

| Rent of primary residence | 7.7% | 0.4% | 6.1% |

| Medical care services & insurance | 6.5% | 0.7% | 0.6% |

| Food services (food away from home) | 5.4% | 0.5% | 5.1% |

| Education and communication services | 5.0% | 0.4% | 1.3% |

| Motor vehicle insurance | 2.8% | 1.4% | 20.6% |

| Admission, movies, concerts, sports events, club memberships | 1.9% | 0.4% | 4.8% |

| Other personal services (dry-cleaning, haircuts, legal services…) | 1.5% | 1.0% | 6.8% |

| Motor vehicle maintenance & repair | 1.2% | 0.8% | 6.5% |

| Water, sewer, trash collection services | 1.1% | 1.1% | 5.5% |

| Video and audio services, cable, streaming | 0.9% | 0.3% | 5.3% |

| Hotels, motels, etc. | 1.3% | 1.8% | 1.0% |

| Pet services, including veterinary | 0.4% | 0.9% | 7.0% |

| Airline fares, other public transportation | 1.1% | 1.3% | -4.8% |

| Tenants’ & Household insurance | 0.4% | 0.7% | 4.1% |

| Car and truck rental | 0.1% | -0.7% | -14.1% |

| Postage & delivery services | 0.1% | 1.2% | 1.2% |

Core services price level. Since March 2020, the core services CPI has increased by 18.9%. This chart shows the core services CPI as a price index, using the index value, not as percentage-change of that index value.

You can see how the curve has become steeper in recent months. This is not a confidence-inspiring chart, now that the Fed is searching for “confidence” that the disinflation (cooling inflation) last year will actually continue.

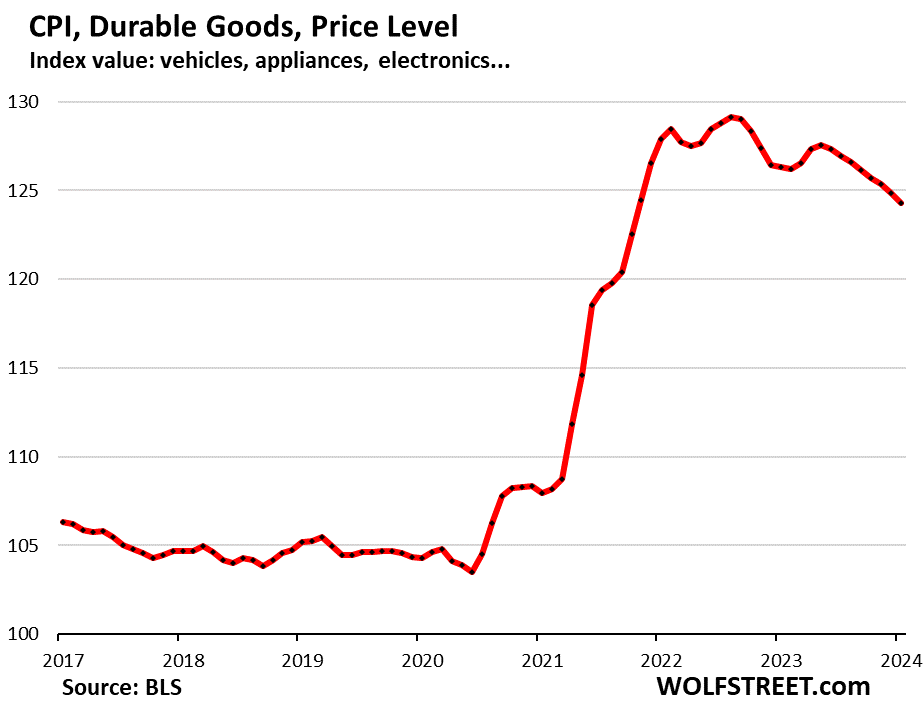

Durable goods.

New and used vehicles dominate the durable goods CPI. It also includes information technology products (computers, smartphones, home network equipment, etc.), appliances, furniture, etc.

The index dropped 0.46% for the month (-5.4% annualized) and by 1.6% year-over-year. It has meandered lower ever since the peak in July 2022, as the shortages, supply bottlenecks, and transportation chaos have receded.

This chart shows the price level of the index (index value). From March 2020 to the peak in August 2022, durable goods prices spiked by 23.4%. Since then, they have dropped 3.8%. In other words, prices have given up about 20% of the pandemic spike.

| Major durable goods categories | MoM | YoY |

| Durable goods overall | -0.5% | -1.6% |

| New vehicles | 0.0% | 0.7% |

| Used vehicles | -3.4% | -3.5% |

| Information technology (computers, smartphones, etc.) | 0.8% | -6.9% |

| Sporting goods (bicycles, equipment, etc.) | -1.1% | 2.0% |

| Household furnishings (furniture, appliances, floor coverings, tools) | -0.1% | -1.3% |

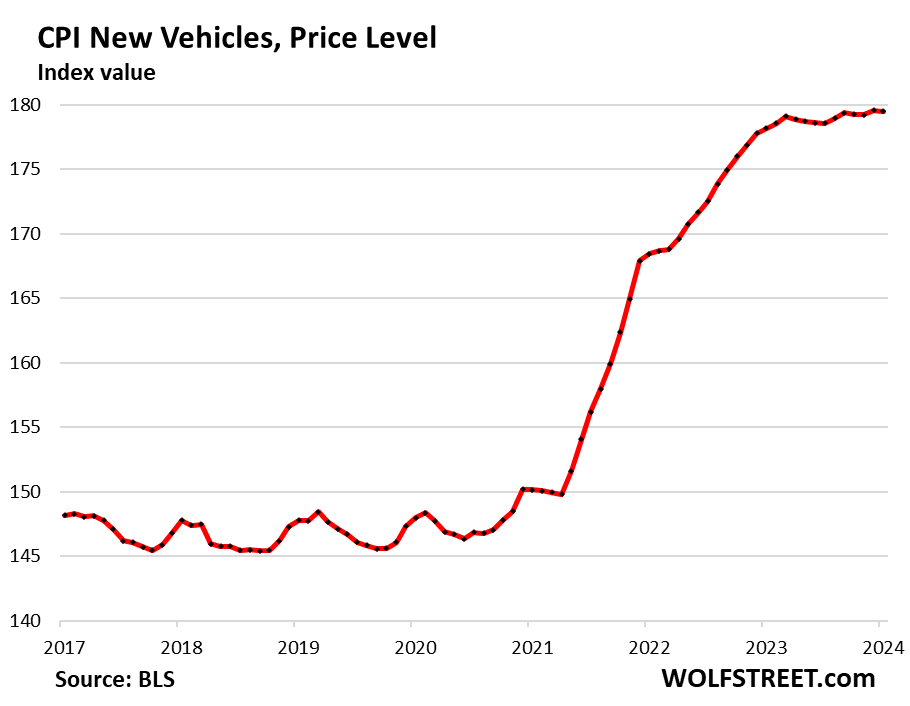

New vehicles CPI remained essentially unchanged. So the crazy price increases, addendum stickers, etc. are gone. But prices have not retraced any of the 20% spike during the shortages.

For the years before the pandemic, the new vehicle CPI was also meandering along a flat line, though vehicles were getting more expensive. This is the effect of “hedonic quality adjustments” applied to the CPIs for new and used vehicles and other products (chart and detailed explanation of CPI hedonic quality adjustments).

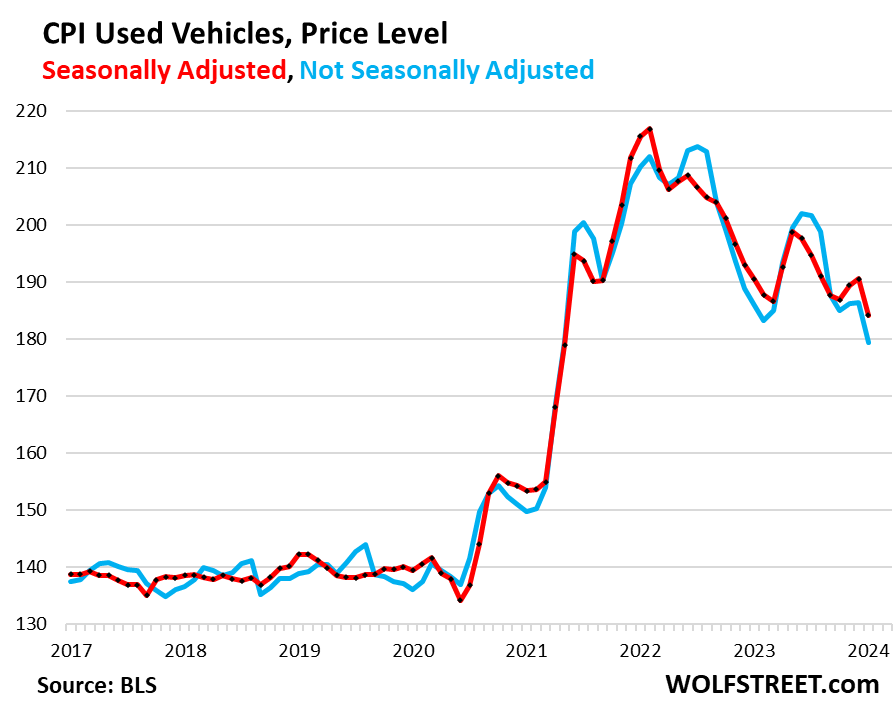

Used vehicle CPI plunged by 3.4% for the month (34% annualized!), seasonally adjusted, now catching up with the historic declines in used-vehicle wholesale prices.

The used vehicle CPI had spiked by 55% from February 2020 through January 2022. Since that peak, it has dropped by 14.5% (seasonally adjusted). In other words, it has given up 41% of its crazy spike during the pandemic.

Food & Energy.

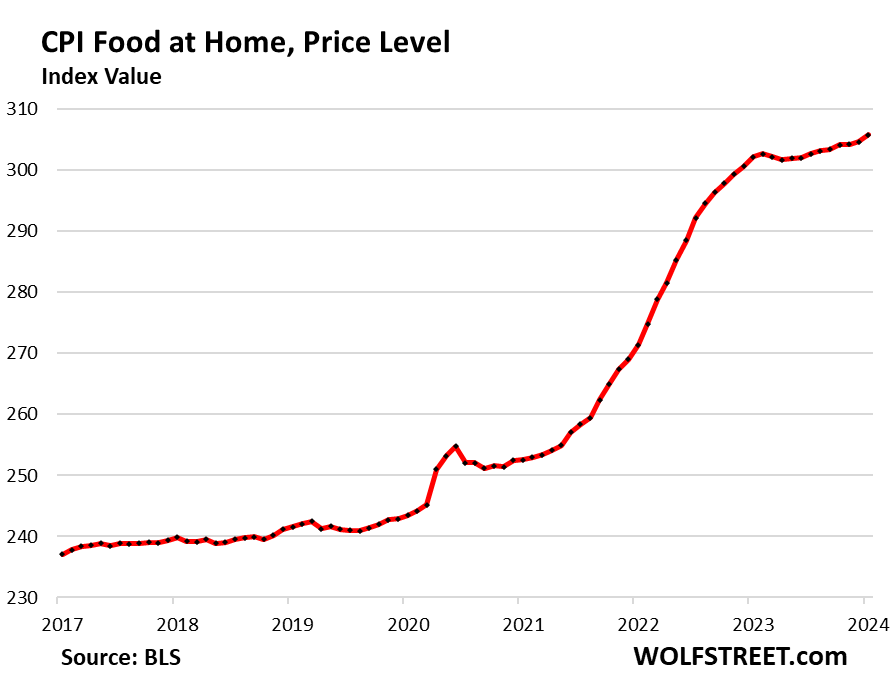

Food inflation accelerated. The CPI for food at home – food purchased at grocery stores and markets and eaten off premises – accelerated to a rise of 0.37% for the month (4.5% annualized), the worst increase since January 2023. Year-over-year, the index rose by 1.2%.

These increases come on top of already painfully high food prices that had spiked by 25% since the beginning of the pandemic. So this isn’t going in the right direction either:

| Food at home by category | MoM | YoY |

| Overall Food at home | 0.4% | 1.2% |

| Cereals and bakery products | -0.2% | 1.5% |

| Beef and veal | -0.3% | 7.7% |

| Pork | -0.3% | -0.4% |

| Poultry | 0.3% | 1.7% |

| Fish and seafood | -1.3% | -2.6% |

| Eggs | 3.4% | -28.6% |

| Dairy and related products | 0.2% | -1.1% |

| Fresh fruits | -1.2% | 1.9% |

| Fresh vegetables | 2.4% | -0.9% |

| Juices and nonalcoholic drinks | 1.4% | 4.8% |

| Coffee | 0.6% | -1.4% |

| Fats and oils | -0.3% | 1.9% |

| Baby food & formula | 0.7% | 8.7% |

| Alcoholic beverages at home | 0.3% | 2.3% |

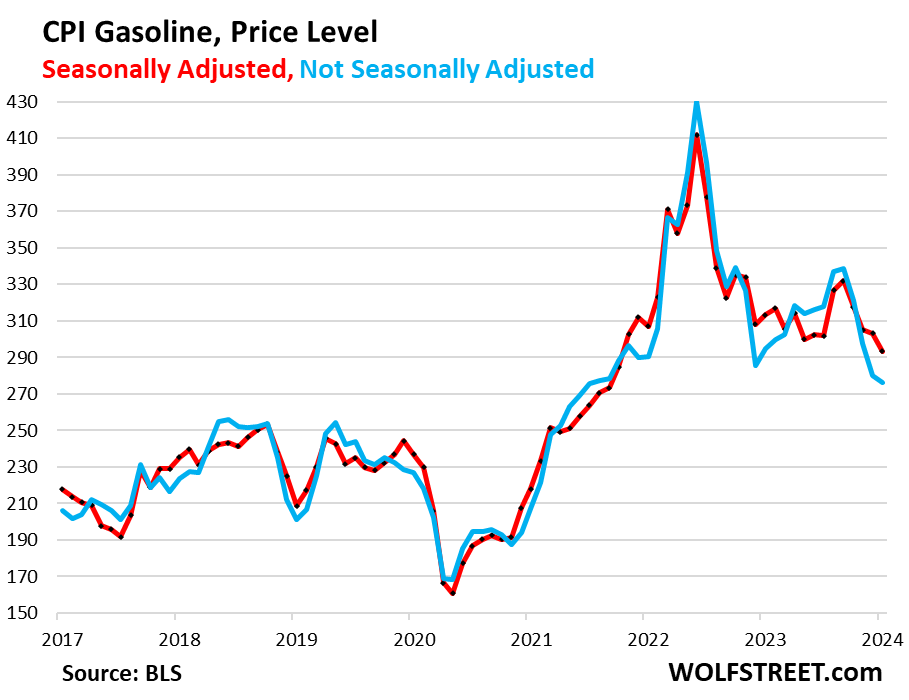

The CPI for energy products and services fell by 0.9% for the month seasonally adjusted (-10.4% annualized), as gasoline prices plunged by 3.3% seasonally adjusted for the month (-33% annualized).

Not seasonally adjusted (blue line), the gasoline CPI dropped by 1.5% for the month (-16.6% annualized).

Since the peak in June 2022, gasoline, which accounts for about half of the energy CPI, has plunged by 28.8%:

| Overall Energy CPI | -0.9% | -4.6% |

| Gasoline | -3.3% | -6.4% |

| Utility natural gas to home | 2.0% | -17.8% |

| Electricity service | 1.2% | 3.8% |

| Heating oil, propane, kerosene, firewood | -2.3% | -10.5% |

This is Fed Chair Jerome Powell’s reaction when he saw the inflation resurging in core services, as captured by cartoonist Marco Ricolli for WOLF STREET:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Dow dropped 700 today at one point. I think the Algo’s read this report.

And then the algos started the buying at 3:30. I’m really tired of watching the market either jump .5% or drop .5% in the last 15-30 minutes. It shows that individual investors don’t stand a chance if the algos go the other way.

This is a pattern we used to see over and over on big down days in 2008. Gap down, then a reversal up at about 10:30est, then a leveling out in mid day, followed by a rollover and acceleration down to new lows. Then a sharp rally in the final half hour, which was commonly attributed to day traders covering their shorts. Used to happen like clockwork. Kind of made me nostalgic.

And a low around noon. I see the pattern for some time too. But why be unhappy about it? Just take advantage of it.

I’m sick to death of it.

Get out of stocks then. Good time to do so anyways.

Lots of opportunity in agency & corporate bonds right now.

MM

I’m not in stonks. I sick of the BS in the casino. I’m sick to death of our entire corrupt financial system. No way would I be in stonks.

I feel thr dame but come what may fed won’t hike this March.

Infact it is very much possible that they would cut rates in May.

This inflation report already inflicted big damage to stock market which was down a whopping 2 percent after being up for some ungodly percentage.

When inflation was high .. fed came out with transitory term

When it was going doing did they ever use the inflation going down as transitory ?

DOW 100,000 or whatever. That’s all they care about. Oh, and keeping shelter out of reach for the young.

If next month’s CPI remains hot, they should totally do a rate hike. But there is no way Powell would do it. His premature mentioning of rate cut in November’s press conference is totally unwarranted and gave the market three month’s of reckless speculation.

Anything is possible in Jerome Powell’s casino.

Are there a lot of homeless youths in your area? Here in my area unskilled minimum wage jobs pay $16.50/hour and semi-skilled around $25-30/hour. Minimum wage comes to $2750/month, minus what the government steals of course. A perfectly decent and safe (but by no means luxurious) 2BR apartment can be rented for $1800/mo. With a roommate, someone working a single minimum wage job could easily afford his $900 share. And there are cheaper apartments. And there’s always a second part- or full-time job. And there’s the option of going to night school and getting a certificate or degree and increasing one’s earnings. It all seems perfectly realistic to me, maybe because I remember doing all that when I was young.

Corey,

They are all lazy and stupid, unlike you. Not everyone is born with your planet killing abilities or ambitions….or head start?

Not many more will be, and not that it matters anymore.

PS: Isn’t punching down fun? I notice that from your type.

Just be aware plenty are punching down at you, most of which you are totally blind to.

Enjoy!

And yeah, there ARE lots of homeless in my area.

Confession;

In hindsight I’m ashamed of being a fun loving but MOSTLY ENTIRELY APOLITICAL ex-hippie….sorry you caught that regret.

I’ll shut up now and let ya’ll discuss getting richer.

Kevin

“ totally unwarranted and gave the market three month’s of reckless speculation”

Well on the bright side at least we have a relative time table to work with. Pull out of positions the day before FOMC meeting, wait a day or two for bottoms to hit then buy back in for a three month gravy train.

If you are trying to time the market by 15-30 minute increments then you will always lose to thise who have bigger, faster computers with better algorithms.

Playing long term is so much easier.

And those bigger faster computers are directly connected to the systems that generate the data in the exchange. They see the data and execute the algorithm before the ticker on your chosen platform even has a chance to update. In sports terms they are on the field playing the game and you are watching the instant replay.

Investors aren’t concerned about any 15 minute period on a given trading day. Speculators and traders probably do.

Playing the wrong game my friend. You aren’t going to beat them. It’s like playing against the house. You have to invest and not trade.

We should have all quit those games at marbles….lotta skill, and quite a bit of luck.

Now future humans are gonna fry for it.

The religious freaks were right after all………

Replace “invest” with “pay into a Ponzi scheme”, and you will quickly see the problem with that logic.

The only way to win is to already be at the top of the Ponzi scheme, or be part of the professional/government class running it.

Who says, “Cow!” Anymore. Showing your age.

ver 50 years, the average inflation rate was 3.8% per year. So the Fed

2% goal is stupid.

Over 73 years, Bank Lending Rate in the United States averaged 6.52%.

Over 50 years, 30-year fixed-rate mortgages averaged 7.74%.

Over 30 years, average credit card rates were between 14% and 15%.

They need to crush the shelter bubble, literally reset shelter prices to a sustainable 2018ish price to stop raising effective minimum wage. I’ve been living in Paris and Tokyo where shelter costs half to one third the stupid USA cost and people are getting by just fine (minimum wage in paris is around $13/hour, in Tokyo it’s $8/hour, in LA it’s effectively $18-20/hour). This idiocy is not remotely sustainable (3 hours away from LA in Mex it is $13/DAY). Other countries are not losing the battle and the USA needs to rip off the bandaid and CRUSH the stupid asset bubbles already.

But Corey above says the situation is perfectly manageable and you are just complaining too much. In his youth, he would have made it work just fine. So stop complaining about the Federal Reserve making life impossible and just keep paying into Ponzi scheme that keeps his real estate and stock portfolio elevated. He’s ready for retirement and you need to pay for it.

In other words, “look over there”: the real problem is with our lazy youth.

5.25 just might not do it.

It WILL “do it,” if you understand what their goal is. They want a slow burn inflation event like this for years on end. If they wanted to, they could snuff inflation out immediately. They don’t want to.

Is Bezos ready for another new yacht yet? His latest one might be almost 2 years old now and ready for an upgrade. Or maybe Bill Gates needs another million acres of farmland. These are the things to be considered when messing with rates. Wouldn’t want a billionaire to get the sniffles and part with a buck.

That is like saying that people want to get rid of the roaches in their house by only accepting 3 applications of ranch killing treatment a few weeks apart.

If they wanted to they could kill all of the roaches right away by burning the building down.

There is a reason people are not following your suggestions and it has absolutely nothing to do with Bezos getting another yacht. You are just using that conspiracy to justify nuttiness.

Pausing rate hikes last year was clearly the wrong thing to do. A couple more increases would hardly have burned down the economy, but they would’ve brought down inflation. And the Fed went out of their way to encourage speculative excess late last year. It’s disingenuous to claim that the only options are standing pat or “burning the economy down”.

There is absolutely no conspiracy.

The data speaks for themselves.

You should change your name to Strawman Argument, JimL, because that’s what you just did. Do you have NPD, maybe?

“It’s disingenuous to claim that the only options are standing pat or ‘burning the economy down.'”

It really is hilarious to see people react as though any suggestion that the Fed didn’t do enough must imply that the critic wants to burn things down, blow them up, or inflict other Hollywood special effects upon the broader economy.

Hindsight is 20/20, but it is obvious in retrospect that the Fed stopped hiking too early. They should have hiked a few more times. Not to vaporize, pulverize, grate, or mash the entire global economy, but to achieve the actual healthy objective of stopping rampant inflation and deflating the batshit insane asset and housing bubbles that they helped blow up with their pandemic policy error. But because they chickened out when they did, the first objective is taking an excruciatingly long time, and the second objective hasn’t been achieved at all.

(They also should have sold MBS outright, as Powell once bluffed that they might, but of course they were and are scared to do that as well.)

I don’t think the mistake was pausing rate hikes per se, but in doing QT as slowly as they have. They added $3 trillion in 3 weeks, they could have removed $3 trillion in one year.

I don’t entirely disagree. A good argument can be made (although I don’t subscribe to it) that QT should have been more aggressive and rate hiking less so.

There are many of us here who believe a more aggressive QT was needed along with the rate cut path the Fed took.

CSH,

The person I am responding to has a long record of wanting to burn it down and that is what I was responding to.

I fully agree that another rate hike or two over the past few months wouldn’t have crushed the economy.

However, I think the economy and the FED are in a tight spot. Inflation has generally been falling since they stopped raising rates, but there has been worrisome inflation fires in certain portions of the economy. Furthermore, there are very strong forces right now both pushing and pulling in different directions as well. The budget deficit is a huge factor, but then there is also a war in the Middle East which usually means much higher energy prices which hasn’t happened. There is Ukraine and China’s and Russia’s economy are a mess.

Basically there are multiple conflicting forces and there is enough confusion in the inflation numbers that it is possible to draw whatever conclusion a viewer wishs.

I think the FED is worried about the persistent inflation in services and even more worried of it taking off out of control. I think the chances of a future rate increase have greatly gone up in the past few months.

However I also think the FED doesn’t want to overreact to month to month (or even three month moving averages). It is easy to see a scenario where the FED raises rates a quarter percent. Two days later a Houthi missile hits a random oil tanker and sinks it, violence escalates in the Middle East and oil goes to $100 (or more), gas goes to $5+ per gallon just in time for summer driving season, and the economy goes into the tank.

I agree that a quarter point hike or two probably wouldn’t hurt, but I can also see why they are waiting.

Put another way, I think the FED is reluctant to hike, but if it becomes obvious they should, I think it will be multiple rate hikes in a row. I also don’t think the FED is going to lower rates until it becomes obvious that is they way to go. The last thing they want to do is to get caught in a trap where they are raising and lowering rates in reaction to events.

I think this FEDs biggest fear though is that they don’t want to crash the economy and face political pressure to restart QE. I really think this FED is doing everything they can to avoid QE, even if it means reacting a bit late to inflation.

Jim L…..maybe spell check is getting MUCH smarter…..”ranch killing applications” IS more accurate, but the roaches WILL still be around when the building is burnt down……less than 100 years? (and that’s being generous)

Depth Charge…..you are really improving…..maybe change your handle to Willie Peter…more appropriate and equally fearsome if you are on the wrong end of it.

Inflation is the answer- because it solves everyone’s problem. Government can’t raise taxes or shrink spending- inflation is the answer. The Fed, can’t monetize the debt, can’t keep rates this high forever- inflation is the answer.

Get with the program.

Venezuela your solution?

Gimp, you mean use USA Econ power to destroy a government if our corps don’t like their oil deal and gov’t style?

That’s just old fashioned schoolyard bullying……..not related to any comment I can see here.

…and CIA-like ops…..

DC,

The Fed is doing all it can, but the Treasury has been blunting the effects of QT by skewing new debt issuance towards bills and away from coupon issuance.

I’d blame Yellen more than Powell on this one.

Ah, the good cop / bad cop routine. The system has you focused on all the wrong things.

If treasury is blunting feds efforts then simply solution is to increase the qt little bit.

This blame is entirely on Fed.

Think about it.. parents gave kids to spend money. Kids spent money on all stupid things.

Whom do you blame ?

Andrew,

I’m not looking at it from a moral perspective. The Fed controls demand for (long) bonds via QE & QT. The Treasury controls the supply of bonds by skewing new issuance towards bills when they want to reduce the supply.

The Fed is trying to reduce demand by no longer being a buyer (QT), but the Treasury is countering this by also reducing supply.

Depth –

Leave no billionaire or multi- millionaire behind …..

Above all, keep spending obscenely , and keep mouse-clicking counterfeit money out of thin air to pay for it.

When you’re in a hole – just keep digging ……

Howdy Depth Charge and old folks understand your frustration having had the same feelings for a half century or more. Only comfort to offer, is our current situation has only just begun. Who knows what tool or duration is next……Youngins could be in leisure suits and Disco dancing in a few years……..

5.25 has been failing to do it for a while now.

2023 had multiple instances where FOMC members offered essentially frivolous, non-sequitur excuses as to why the Fed would not need to “do more”, most notably in February and in September. So it’s unsurprising that the chickens are coming home to roost.

New “crisis” needed in 3….2….1….

Agreed.

5.25% , actually historically in the realm of normal, suppressed nothing.

Yes, I think everyone is finding out, to their great surprise, that the US economy hums along just fine on 5.25% (though assets, such as real estate, are being repriced), and that, after everyone got over the shock of 5.25%, demand and inflationary pressures continue to build.

The problem is that the economy doesn’t actually have 5.25%. Yields are only 5.25% at the very short end of the Treasury market where they don’t impact the economy. The long end — which is what really matters — has not played along with it, and the 10-year yield is not at 6.5%. If the 10-year yield were at 6.5%, we would see much tighter financial conditions and more success at repressing inflation.

Howdy Longstreet. Govern ment ZIRPed minds to mush…..Will we ever recover??????

Wolf, and the 10 year is where it was because no one trusts that the Fed won’t resume QE and ZIRP when the next “crisis” occurs.

The Fed hasn’t done a good job getting people to believe them.

5.25-5.5 would have been fine if there no excess liquidity. Bond market never came around and believed in Fed’s resolve to bring inflation down. 10 year went 5% for few moments and it all came down to 3.75% level and now again 4.25% level. So Financial Conditions didnt tighten much. Treasury played smart tactic to issue more Bills and less Notes and Bonds. That also helped.

5.25 is historical normal rate and Economy did well that time too.

If FED doesnt want to go higher, they should speed up QT pace at least.

Only then Financial conditions will tighten.

I am doubtful either will happen in near term.

Fed will stay and they keep same QT pace. So we are going to get higher inflation print till FED realizes.

FED is longer time to fight inflation and bring it in control.

Somewhere Mosler is chuckling to himself.

If I’m not mistaken, the whole concept of the 2 percent inflation target was based upon the average of new gold mined in a year back when we were actually on the gold standard. We are a fiat economy now, most 35 trillion in debt. Next month, a wave of CRE’s, many at 50 percent occupancy will have to refinance at current rates but at discounted valuation. Prepare for regional bank collapses. I forsee Powell being fired before the end of the year.

The 2% inflation concept was an off the collar remark by Roger Douglas, the Labour Party finance minister in New Zealand in 1990.

CBO has just said $54 trillion in 10 years.

Which really means $59 trillion. Their estimates always are to low. They do not count for any crisis or wars in their predictions

The concept of 2% comes from the fact that while runaway inflation is bad, spiraling deflation is way worse. Imagine working at a job where you get annual pay decreases. Imagine the federal government announcing how monthly social security payments are decreasing.

So the FED knows that it will never be perfect in keeping inflation at its target (the economy is just to complicated and there is too much going on in the world) and there is going to be variance. So better to have a margin of safety.

Just like if you had to shoot an apple off of someone’s head, you want to make sure that your mistakes are slightly high rather than slightly low. You give yourself a margin of safety.

A 2% inflation target does that.

It does no such thing.

Jim L-

In your William Tell analogy, upon whose head does the apple sit?

Separately, is a 2% target (or any other non-zero number) constitutionally defensible?

I think this 2% inflation as a (rather stupid) “steady state” goal, is a result of fractional banking. And it is “decorated” with a lot of other nasty greed-driven SHIT that varies in time…..call them business cycles if you want, but that 2%…..

THAT is a (very?) generous banker’s cut for “maintaining” the money pipelines and storage depots…..sorta…….

Very hot CPI number. Rent seems to be killing it, along with motor insurance and medical service readjustment that Wolf had been stressing before. But Wall Street still resilient with the sharp bounce in the last 30 minutes of trading.

Right, and those things are things you can’t easily avoid.

that last minute bounce was disgusting. They were bent on messing with investor psychology. I hope it will truly crash one day and justice will be served

Rents have a long way to go before they match new mortgage payments. Renters are a captive audience for now. Plenty more to milk from them.

I agree with you. I know you’re also in the Southern NH/Boston area. I see rents in the Manchester market (where I invest) still largely at the pre-COVID level when I see any new multi-family properties hit the market looking at the rider the listing agent provides. When new buyers get these properties at a price 50-75% more than they last sold for somehow they have to make up that gap.

Why is it that rents must obviously rise to reach equilibrium with sale prices, rather than sale prices dropping to reach equilibrium with rents?

Both can (and will) be true: rents will rise and prop prices will fall.

That said, I agree with Rick: rents north of the NH border have remained surprisingly tame, in spite of the stubbornly-high property prices.

But once you go inside rte 128, forget it. Rents are insane esp in all the new developments that have been springing up. Even in traditionally “cheap” areas like Somerville, Everett, Lynn etc I still couldn’t afford to rent without roommates.

Why cant rent prices AND home prices fall? Wouldn’t that be a treat. Multi family housing supply is growing quite rapidly.

Imagine that modern day dystopia: Rent prices falling, home prices falling, and WAGES GOING UP. Can you imagine the uproar we would have from the non productive members of society freeloading off the backs of the working class?….. Talk about equilibrium, it would be like the American dream returned or something weird like that. The country might implode if that happened though.

Einhal, if theres pressure on sellers to sell that would be the case. On the east coast there is little, and for those forced therese still buyers to meet them. What you describe has been seen on the west coast. Dynamics could change in the future but its hard to say what the cause would be.

Generally though, rents go up. Theyve trended higher than general inflation for more than a decade. And in the current environment theres little escape for renters by jumping to homeownership, hence the captive audience comment.

New construction can provide negative pressure, but its slow.

Have you considered “investing” in something that makes society better, instead of profiteering off structural inequality?

OOPS!

There is another turd in the punchbowl. (pnwguy)

Besides me and Luci’s “lynch mob” below….that she shouldn’t ignore!

Tar and feathers, too, anyone?

I live on the north shore between I-95 and I-495 and in the last 6 years my rent has already gone up over 50%. Pretty painful, but it still beats commuting into the Boston Metro area from southern NH.

This is the sad result of very little new multifamily housing having been built in the greater Boston metro area for the last 50+ years.

It may be another decade before the MBTA rezoning efforts have any positive effect for renters as it’s all a case of far too little, far too late.

Herpderp,

“Rents have a long way to go before they match new mortgage payments.”

I agree but we have seen it before in 2012 when HB1 bottomed out housing prices but hardly affected rent (From Wolf’s excellent charts).

This time is different. Inflation is high, (unlike last time) even though housing prices are still in a bubble (Like last time).

I think there are forces that will continue to push rent higher.

Home prices are still too high for most to purchase so they have to rent. Short term, this is a good choice since the disparity between a mortgage and rent is high.

Landlords are experiencing high inflation and taxes so they either have to raise rents or sell.

1) Homeowners insurance for houses/condos have increased at least 20% in many areas.

2) Property taxes in many states have increased with home values. I have friends who have seen 15-80% increases in property taxes. CA is somewhat immune due to Prop 13 and a 2% increase cap. I suspect Prop 13-like bills will be appearing in other states soon. It is sadly ironic that the county that increased property taxes 80% is actively pushing for more affordable housing.

3) Services such as gardening, snow shoveling, plumbing/heating repairs, roofing, etc have all increased double digits (If you can find someone). HOA’s on rented condos/houses have increased due to this.

4) As Corey pointed out above, if minimum wage still allows someone to their own room in a 2 bedroom apartment, renters with jobs still have money to cover rent increases. Where there is money, landlords will find it.

All of these have to be covered by rent. A landlord will eventually have to sell if they are losing money. Rents will increase (and likely homelessness will increase for those with fixed income).

These same factors will push housing prices down since they are hard costs of ownership. I had a co-worker who purchased a house a couple of years ago and they neglected to consider unsuspected increases in their new property taxes ($12,000/year), and their insurance ($10,000/year). They are struggling to keep the house. Any new owner will be informed of these new increased costs and it will factor into the new price.

Eventually Wolf’s charts will show the gap narrow enough that it will incentivize buying a home again vs renting. Just like it did in 2012.

I think at this point there’s a better chance of a rate hike than there is a rate cut in 2024.

These numbers are insane.

Good. Jack the rates up.

Get that interest payment on the federal debt up to 75% of all federal individual income tax receipts.

Slap these tax donkey idiot citizens in the face as we lose wars abroad and as entire school districts in Baltimore have not one single student that passes math and reading.

And shove money into boomers pockets. I want boomers so flush with cash that they’re eating out at restaurants 4 nights a week. I want every boomer to genuinely think everything has never been better.

Then, while you’re at it let’s narrow down the magnificent 7 further. Magnificent 5 isn’t doing it for me. I want the magnificent 1. I want Nvidia to go up 233% from here and dump the rest. The entire stock market should be just one company.

Keep that music playing.

Don’t you dare turn on the lights.

And the next bouncer that accidentally let’s another homeless man in to use the bathroom is fired.

Excellent rant! A+

Hear hear!

Bitter or angry much? Anyone besides yourself that you don’t hate? Nothing constructive here. This is the playing field we have to win on. Emotional responses are bad for investors.

If you’re not angry you’re not paying attention.

Your complacency is concerning.

True, but winning at investing doesn’t make you a good human. Emotional responses to gross unfairness are good for humanity. Great rant Ryan, just what we needed!

Luci,

What are the boundaries of this “playing field”? What are the rules? How well is the “game” regulated? How does one “WIN”?

Your little fantasy world is PATHETIC…you act like nature (or some deity, most likely) “created this game” for all of us to play.

And just what in the hell do you “imagine” should be “constructed”?

Good rant above, and I AM ashamed to be a boomer. We could have changed this so-called “game” before it was too late……sorry Abe.

couldn’t have said it better….

Spot on.

Toward Ryan Merrit’s understandable anger, the real purpose of economics in general, and perhaps this site:

“Only a crisis – actual or perceived – produces real change. When that crisis occurs, the actions that are taken depend on the ideas that are lying around. That, I believe, is our basic function: to develop alternatives to existing policies, to keep them alive and available until the politically impossible becomes politically inevitable.”

— Milton Friedman

Yeah, like Uncle Milty said, just let it all ride!

And ignore the men behind the curtain. A savior will show up for the rest of ya, don’t worry…… (just not for very damned many, as only the best should “win”, anyway…and devil take the hindmost.)

and Milty never even saw War of the Worlds!…..second one, don’t know if John and Milty’s line was in the first

Ryan-

Love it ! Luci is on the wrong site – Business Insider for her …..

Wolf gives facts and thoughtful insight. I was mistakenly expecting the same from commenters. Sadly, there are several here who use this as an echo chamber; angry folks who don’t seem open to different ideas. If you’re upset with ‘others’ why are you venting in a finance / business forum? Why not spew your crap on X like other self righteous know it all narcissists who love to hear themselves talk?

Well said, Luci. Don’t let the lynch mob get you down. Conspiratorial b.s.

Luci, I remember the Volcker interest rate hikes in ’82 vividly. People were ranting about inflation before the hikes. Then he jacked the rate up. Then the ranting was about high interest rates that were crushing the economy.

Volcker was hated. He didn’t give a shit. No, he did, but didn’t want to show it. The Fed tried to do it gently, raising then lowering, but inflation blew higher. Volcker had to apply a tourniquet.

Several commentors here want to see the market crash only so they can buy in at fire-sale prices. That’s what is behind much of the phony righteousness.

Guilty as charged, Luci! Ya got me.

Except anger over your “different ideas”….I think they are, sadly, the biggest problem on the planet, at least for humans.

And the cause of war, along with organized religion, which I would LOVE to see taxed, along with a lot of other things, and at 50’s rates….and IRS a FULL part of Military, of course, now that things are so far gone.

But I can’t afford WSJ, Barrons, Forbes, etc, or Kramer’s club….or an Econ class……actually, I wouldn’t pay for any even if I could. It might get me thrown out of my cheaper rent over 62 hotel style 500 sq ft, very cheap interior apt (indoor/outdoor carpet, 4” plastic baseboard, genuine peeling paper wood grain cabinets…just got upgrade! Handles!) Plus I have transport and food.

I consider myself as intelligent, formally educated, and as much of a winner (and learner) as anyone else here in this great ongoing book, maybe more, especially because I’m old, have seen a LOT plus Biology BA plus Chem minor and grad work, year of Pharm School, and still study it online. Therefore, I am luckily NOT going out like my poor mom, so don’t sweat my Medicare charges in your tax “burden”……put in way more than I took out, still do, and will keep it that way until I don’t like my quality of life anymore and deal with it myself.

I am here for Econ, Econ heads up, and Sociology, which I think is what you object to….sorry, but I am tolerated so far.

I’m doing Max/Min on the various scenarios if the government was forced to cut spending by 20-50% in order to pay the interest on the debt.

Lots fewer new $100K cars in N. Virginia and Maryland.

“Slap these tax donkey idiot citizens” is not an option as I’ve seen projections of the government raising taxes to 100%. More likely the government will public/private “nationalize” everything and set domestic company store prices and pay in script unrelated to international dollars.

BTW Wolf, thanks for all that detail work.

You might want to direct your anger towards those that are the reason that children *educated* in public schools can’t add 2+2 and come up with the right answer. Odds are, their teachers aren’t Boomers. And it’s not a money shortage – IMHO, it’s more of a misdirection of the funds available and too much classroom time spent on the wrong subjects. Check out the number of administrators and the payroll associated with that vs. that directed at actually educating. Grade inflation is an issue… and that’s to move the problems along. You have to wonder if it isn’t part of some plan as not all of this can be an accident.

There’s many homeless Boomers. There’s many Boomers that are on fixed incomes and suffering – and they don’t get significant raises nor can they shop for another job as they might just be too old and frail to do so. There’s many Boomers living in trailer parks that are getting forced out due to corporate owners buying the mobile home parks and raising rents beyond their ability to pay… and they can’t afford to move their dump of a trailer because, if they could, the rising rent wouldn’t be an issue. So their “owned” trailer gets abandoned and they are out on the street. I’ve read articles claiming that Veterans are being forced out of housing to accommodate illegal immigrants. Got lots of moola for Ukraine but not to care for our own.

The current crop of pols have been put in place with the help of the non-Boomers. Boomers are an increasingly less forceful demographic, yet the same group of idiots keeps getting elected (or foisted upon all of us by TPTB). How does that happen?

As my daughter said to me recently… we have a lot more in common (me being a geezer and she a Millennial) than not. Time to work on the stuff we find ridiculous (from both perspectives) and quit picking the fly-sh*t out of the pepper fighting over stupid stuff – which is intended to divide and conquer.

*puts soap box back in the closet*

EK, glad to know the soap box has been put away. I won’t pick a fight with most of your complaints except for this one: “Grade inflation is an issue… and that’s to move the problems along.” Many people bitch about this, as I did when I first started teaching. But it’s a profound problem and many responsible, thoughtful research has gone to try to figure out how to keep kids on track.

In a class of 30+ kids, there’s a wide range of capabilities. Kids that are held back (flunked) for more than a year are statistically going to quit well before they finish high school. Back in the early part of the last century, drop out rates were very high – many people quit school by the 8th grade. Now they’re trying to extend that to h.s. graduation so the kids aren’t stigmatized for the rest of their lives.

I had one girl who had been held back for two years and she was starting to mature pretty dramatically in what was her 7th grade, yet she was still doing math work at 2nd grade level and could barely read. Nice girl but totally alienated from all her classmates who were much less mature, socially.

This is a sad but real problem that can’t be fixed with tough love and more rigor.

I rather like your comments so I will bother to post on the education rant as I have been on a school board for 5 years and taught in a classroom briefly.

There is no concerted “plan” in education policy except to provide childcare services, meals, and whatever curriculum is mandated by the political winds in order ro keep funding.

Local control is a bit of a joke unless you have a very united, very brave, and well-supported group of five or seven on the board. Or an eloquent superintendent willing to go rogue (about as likely to appear as Bigfoot).

So yeah, the states and federal gov’t push agendas into the classroom all the time. And some of it is quite destructive, like NCLB, Common Core, IEPs, etc. But to call it a conspiracy is giving too much credit. These are vote-pandering schemes, special interest agendas dreamt up by think-tanks and academians, and so on. There is no overall plan, which is why it is all so dysfunctional, why teachers are so disaffected no matter how much they get paid, and why local boards feel so overwhelmed and helpless every time a new law or regulation gets passed.

It is also why the cost of education (and attending administation) has roughly doubled in real dollars every 30 years since the 1870’s but the quality has not. Because education became, and has remained, one of the most politicized professions in America that I know. More funding, more mandates, more frustration and confusion. It’s hard to describe the ludicrous demands placed upon teachers unless you actually observe it firsthand.

I love the vocation of teaching. The profession is wreck, however, through no fault of teachers. (Well most of them anyway) New teachers don’t even get to write their own tests!

I could go on in great detail, but it would not be appropriate for this blog. Suffice to say that yes, graduates today (particularly those of the Covid cohort) are woefully illiterate in math and finance. I would guess that, based on tests, about 60% of our grads cannot solve real-world problems involving fractions. Yet we stess Algebra and Trig and Calculus because the state tells us to. Sigh.

It’s been said before, I’ll say it again, I blame service inflation on Wolf splashing cash around the ski chalet this past weekend.

Yes, I think that added at least one basis point. They saw us coming and jacked up the prices. “Here comes the dumb money,” I heard them say.

My gut tells me we could see more data like this coming which in normal times would prod the fed to hike. But they may not because they could appear political – they would be trapped in a damned if you do, damned if you don’t situation no matter what they do. Another argument to end the fed and have a simple rules based system to handle short rates based on a basket of economic metrics. No QE, no BTFP, no bailouts and no insider trading. Lay off those 100s of economists employed by the fed and save a ton of money.

Agree, like totally NYguy:

IF and WHEN ”WE” in this case the totality Wolfsters WE can and DO come up with a superior method to PROTECT THE RICH AND BANKSTERS,,, while NOT harming we working folks who actually make and do stuff and other things to help people live better,,, absolutely end the FRB.

At this point in time it is, or should be, very very clear to anyone paying attention that the FRB exists ONLY to protect the rich and banksters,,, and maybe only the banksters from their own very clear stupidity as clearly shown by recent ”bank failures.”

Many decades ago, an MD doc mentor invited a dozen or so MDs to a dinner to show me that they were not exactly the brightest bulbs, and one must consider that the banksters are what is left over from the docs, dentists, etc.

On being the “brightest bulbs”, I saw a YouTube history of the Rothchild’s recently. I doubt your MDs are as focused and ruthless and successful as they are.

Until you can point to the “bank failure” bankers in cardboard boxes on the streets, I don’t think you can count them as personal failures. And remember, there are always the heavyweights and then their useful idiots.

Good post. Would love to fill in all the MANY blanks as I see them.

I lied above.

Better go pay DMV registration while I have a fat checking account. A 2012, but it’s going up, too…..about $10, which is around 4%.

“FRB exists ONLY to protect the rich and banksters”

*Or* so ordinary citizens can irk out a living on the fumes of all the excess fake money created by the immoral speculators.

Yep. They are going to continue to slowly boil the working class and the poor until the misery index goes over 20. There will be no rate hikes unless and until they just cannot possibly ignore the crisis. They LIKE this inflation. “Transitory.” Never forget.

Can we expect Treasury yields to go up? Stay the same?

Howdy Sally. Bubba believes the time has come. The can has been kicked too many times.

UP in time

The 10 year Treasury rate has gone up to nearly 4.5%. The FOMO is hitting the real estate market here and properties are now recovering nearly all of their losses from 2022. I see a buying panic going into the spring selling selling season. Properties are moving. More listings are coming on the market. You see “Sold” signs everywhere. Lawrence Yun was right on the money.

Also noticed the bars are packed. The drunken sailors are out in full force.

Howdy Swamp. Lets not forget about the old sober sailors that waited a lifetime to finally spend. ZIRP is dead, YEAH….

General Powell sitting high on the hill observing the battlefield on his cow.

I’m also observing, wondering if the rise in treasury yields are going to cover the cost of all my necessities, so far so good.

Looks like Wolf’s team (49rs) got done in on the Super Bowl this year. Missing that extra point cost them the game as it turns out. Everyone in this town was betting on SFO. Fortunately, I had all my money on KC. I joined the drunken sailors at a popular sports bar. People were crying on the way out when that dude caught a 3 yard pass and won the game. That pass was so easy to catch a 4 year old could have made it.

Yea that was too bad. Rule change in 23 did the 49s in. They scored first and should have been the winner. Kansas should have an asterisk with them on a three peat record. Oh, and Higher for Longer! Thanks Wolf!

John,

What ironic is they changed the rule because of the Chiefs victory over the Bills 2 years ago in the AFC championship game. People did not think it was fair that the Bills did not have a final chance to get ball to tie or win the game after the Chiefs scored 1st.

I guess 49 fans can thank the Bills for the 49s loss?

Niners didn’t know the rules well. If both get possession then you start on defense. That way after the Chief first possession you know if you need touchdown or field goal.

Glen, that’s not the rule in the NFL.

If the first team scores a touchdown, the game is over and the second team never gets the ball. Maybe you’re thinking of the sport formerly known as college football.

Cookie doggie,

Perhaps read the recent rule changes. It is more or less similar to college and of course the niners did score a field goal and then KC scored a touchdown. Game over.

So where is here, swamp creature?

One bubble market I keep an eye on is Kalispell MT (I’ve mentioned it before). In December there were seventeen (count-em 17) houses sold. Median price was $550k – so 8 below and 8 above. Nothing, of course about the mix so you don’t know if the $550k sold 18 months ago was a run-down 3/2 and the one sold in December was a nice 4/3.

Where are we today? 192 SFR for sale, average price $799k, of the 192 about 44 are at or below the median. Lots of wishing prices (IOW – I want 3x what I paid in 2019). And I get a daily email of new listings – anywhere between 3 and 8 new listings a day.

With listing coming on the market and interest rates increasing, what is driving the the “panic”? Simply FOMO? What about affordability?

Let’s talk again in August.

He’s in the DC area.

Everything West of Billings in Montana is a bubble. The entire Western states are bubbles just not as frothy. Lest we forget places like North Idaho where many jobs are paying 13 dollars an hour and a 1br apartment is renting for 1500 dollars a month.

If I didn’t have an in on cheap rent I’d be struggling in Spokane to save a down payment while making 80k+ a year. My previous employer was paying 3 extra dollars an hour for Seattle based employees. They couldn’t get anything other than Hispanics on work visas because nobody could live within 1.5 hours commute and afford to pay rent. The Hispanics they’d bring in primarily from Honduras and IIRC Ecuador would live 20 people to a small ranch home all chipping in on costs.

Of course those visa workers would get 1/3 of the pay the American citizens would get. When I’d be occasionally conscripted for the Seattle division I’d not get the Seattle worker pay and not be able to understand anyone there.

I always wonder how places like San Fran, Big Sky, Seattle, etc function. The low wage crowd must either drive 2 hours one way a day or live out of their cars to work a crappy service job. Which I’ve seen that a lot in Montana. I knew a girl who drove from Livingston to Four Corners in Belgrade (45 minutes in clear weather) to get on a bus to go down to Big Sky (About 1 hr ride) to work at a gas station for 14 dollars an hour. All over the West I see people living out of their car working a job, sometimes 2 or 3. It’s insane.

Don’t forget this is the highest period of wealth inequality since the 1920s. The pandemic and the economic policy response was just a big transfer of wealth to the ruling class.

Is this a tourist area, a retirement area, or is this a jobs growth area?

Those make difference I think when comparing apples to apples.

Fast Eddie, the worst is living here in Florida seeing people ask absurd retard prices for their total junk homes. No, I don’t want to buy your 1987 single-wide buddy trailer for $500k. The market is completely frozen here and I cringe every time I hear some realtor who got their license in 2022 mention “but but but muh inventory shortage.” Derp. Hey, don’t make me smack you in the forehead. Did you even look at the numbers? Inventory shortage and Florida don’t belong in the same sentence.

Florida has the #1 (numero uno) highest active inventory in the entire country, and it keeps rising. That’s a fact Jack. And they keep building new homes here like there’s no tomorrow. You’d think they’re planning on the entire country moving here. Give it 10-20 years and the United States of Florida will be a literal ghost town once all the boomers here kick the bucket.

Fast Eddie

I’m talking about the Swamp RE, Washington DC Metro area. Prices are going up again. There is a shortage of listings.

Did you forget your sarc tag? I’m not seeing that at all where I live. No, Yun wasn’t right.

Long bond yields will continue to rise. Bear steepening.

Short yields (bills) are basically set by the Fed. These rates won’t move much unless the Fed hikes more.

The dollar kicked sand in the faces of all the other assets on the beach. Stocks, precious metals, crypto – all of them beaten up by the big bully. I thought gold was an inflation hedge? I guess not!!!

Gold is an inflation hedge over years and decades, not days and weeks.

I respect that. You might laugh at my misfortunes someday. I like interest I can see and spend. “In the long run, we are all dead.” J.M. Keynes

GR, take a look at the long-term return on gold vs. the stock market. Gold bugs have gotten crushed.

Gold is definitely an inflation hedge in nearly every country except the U.S. The dollar being the dominating currency, gold doesn’t look so hot at the moment, which makes sense. But perhaps the times they are a changing.

I beginning to think the worst enemy of the dollar status is the U.S. government.

Gold is not an inflation hedge. It is a CDS against the solvency of the US Gov’t.

Gold is just metallic stuff used in most jewelry until its demand for such fell to new lows as prices preposterously inflated.

Did you really say that. Gold was $32oz in 1970. Gold was $329 in 1999. It is $2020 now. When the USD is strong, gold is on sale.

I ran a little calculation. In 1999 when I bought my current house ($186k house price) , it would have taken 563 gold coins for the purchase. Now it would only takes 200 coins for the current $410k house price. So if I would have kept those gold coins under a mattress and delayed my purchase by 25 years, I would be able to buy 2.5 of my exact same house.

Basically, my 563 gold coins will buy me a $1.1 million dollar house now. Gold has been a much better inflation hedge than buying real estate in the area I live over this time frame.

I am not saying gold is the best investment but it has been a good store of value.

Of course if you want to hold such an amount of gold for that period of time you have to have the money to buy it in the first place, not require the money in the meantime and a place (a secure one, no less) to store it. These are not trivial considerations in the real world, unlike thought experiments.

Ru82,

And in parallel to your comment, the cost of a barrel of oil, priced in gold, has been remarkably stable for the last 50+ years.

I sort of agree with you.

Investing in a Dow or S&P 500 ETF in 1999 would have provide the about same return as gold.

Investing in Apple stock in 1999 would have bought you an $85M house today.

Houses are a poor investment in terms of ROR but I think you also have to consider rent increases from 1999. This is about a 2.5X increase from Wolf’s chart above. Since renters likely move more often, there are also moving costs involved.

“Gold has been a much better inflation hedge than buying real estate in the area I live over this time frameh. ”

In the area you live is the key.

My old house in S. CA went from about $300K in 1999 to 1.3M now. That is about 4-5X which is a little less than gold (even though it had 1990’s gold fixtures, there was no gold involved.)

Rents went from 2000/month to 4500/month so with the rent savings, I would have been better off living in the house than investing in gold.

186k in 1999 until today you would have made $2 million easy in the stock market.

Which stock market?

There’s an S&P calculator you can use to calculate returns:

“If you invested $186000 in the S&P 500 at the beginning of 1999, you would have about $1,049,162.48 at the end of 2023, assuming you reinvested all dividends. This is a return on investment of 464.07%, or 7.27% per year.”

Yep, doesn’t make sense to me.

Howdy Folks. So does this mean rates in March will not be lowered???

HEE HEE. YEA HAW and the truth will set you free. I use to pay attention to all the nonsense everyone else put forth……..

Wolf street is all I need.

THANKS

Rate cuts coming in May??? HEE HEE

Higher For Longer!

Howdy Dirty YEP. Higher for Forever. Never to ZIRP again.

Let’s hope the soft landing crowd isn’t flying Boeing

We’re gonna need a bigger boat

Howdy grimp. Wait till Congress sees what the FED brung em……

Sadly Congress does not see and will continue doing what it does best i.e. spend money it does not have. This it either has to borrow or have printed. All of which will only further increase inflation.

But sir, you forgot to get down on your knees and say “please” for the rate cuts? Everyone knows you have to say the magic word, duh.

The funniest one for me was a realtor back in Nov 2022 try to explain to me with a straight face how the Fed was going to start cutting in January 2023. Still makes me chuckle.

Helpful. Thank you.

A month ago, the CME Fedwatch tool indicated a 0% chance that the Fed Funds rate would be higher than 4.5% at the end of 2024. After today’s release, there is now a 51.5% expectation that the Fed Funds rate will be higher than 4.5% at the end of the year. What a difference a day makes.

“As long as we see this gradual progress down, they should be in a position where they can feel confident of wanting to cut,” said Pooja Sriram, US economist at Barclays, referring to Fed policymakers. “It still looks like we are at a place where interest rates are elevated, they could bite into the economy and maybe there is scope for those to start to be pared. There really is no reason to keep rates at these levels for very long,” she added in an interview with Bloomberg TV.

These people won’t stop the gaslighting. They feel like if they keep repeating that rates are too high, that’ll make it true.

Amazing they want the free money back but that’s how they boost their company btm line profits which is QE lower for longer but not happening

Howdy JeffD So glad the Lone Wolf taught me about the dot plots.

This is what happens when the FED is composed of 100% Keynesian political hacks making economic decisions instead of economists that ignore political economic decisions. Half of the decision makers should subscribe to the Austrian school of economics. Why have there been so many trips to the White House over the years? The Federal reserve Act

of 1913 prohibits political interference.

What happens? Rates stay higher for longer?

Seems simple and not necessarily a bad thing.

The Austrians were anti-democratic, aristocratic loons.

See Quinn Slobodian’s “Globalists”

This. Common sense beats ideological purity in either direction. “Austrian school” is a distraction and a red herring.

Name 3 countries that have set up an economic system using the Austrian principles. Trick question. There are none. It is all speculation, theory, and hot air.

Our own Chicago School of Econ has at least 9 “Nobel Prize” winners!

Americans must be smarter?

It’s history is sordid, but a damn good story.

Lotsa names involved. Big ones and interesting unknown ones.

What a great opportunity to pump the brake on QT!

AMIRITE?

/s

My own observed services inflation index showed double digit inflation YoY for the last few months. These are all necessities, not discretionary items. So the figures that just came out today just confirm what I was experiencing already.

Car ins – up 20%

Homeowners ins – up 25%

Property taxes – up 11%

Medical premiums – up 9%

Utilities across the board – up 10%

Real estate rents – up 8%

Home prices – up 7 – 8% YoY

The chance of a rate cut before the election have gone to zero.

I think healthcare costs are going to jump a lot the next couple of years. Lots of reasons. Example of one is below. The Denver Health hospital had a lot of uninsured unpaid ER visits. It was bad even before the migrant crisis. I did a little research but I am guessing an average ER visit averages over $7k?

——————————————————

In 2020, the Denver health system had about $60 million in uncompensated care costs. Last year, costs sprung to $136 million, a quarter now of which came from caring for non-Denver residents. Denver Health has treated more than 8,000 migrants who lack legal documentation in the past year, totaling about 20,000 visits (that is an average of 54 a day), according to Steven Federico, MD, a pediatrician at the health system.

I am waiting for the happy day this year in California when all undocumenteds show up in my clinic in line with me, but with their tickets in hand for free health care. The California legislature and Governor are straight out of their minds.

You two seem to like to get outraged. Plenty outrageous goings on in health care here for ya, 100% guaranteed!

https://khn.org

While I absolutely appreciate your many comments and hope you will continue to ”tell it as you see it” the following:

”The chance of a rate cut before the election have gone to zero.”

Indicates you do not understand the nasty and nefarious nature of USA politics IMO.

Not only likely, but almost 100%.

As in wait till the primaries are over……..shit happens.

It’s just one month anomaly. Things will improve next time.

That’s why I gave you some charts so you can see for yourself if this was an anomaly or a trend, LOL.

A while back Wolf was arguing monthly data is just noise. Well this one month of data sure made a lot of noise.

That is why I gave you the 3-month moving average — THE BIG FAT RED LINE

And I gave you this text:

“The three-month moving average, which irons out the month-to-month squiggles, jumped by 0.50%, or by 6.2% annualized (red), the worst since March 2023.”

RTGDFA.

I have nothing against moving averages. I use them all the time. However, I will not call monthly data noise, because monthly data are not noise. What is useless to me are YoY rates, since they include data that are over six months old. The three and six month moving averages are more interesting (Wolf provides these). But I look closely at the monthly data, as does Wolf (look how much of his article is devoted to one month of data).

Wow! There’s not a lot of positive news here in this report. Is it fair to say The Fed should have raised 25 or 50 bps instead of holding? I’m getting concerned that they didn’t do enough and the inflation fire is coming back again.

Also, I had a question regarding services. Wolf, you’ve reported that the workforce participation rate for 25-54 year-olds is at a level not seen since 2002. Given that, and the fact services inflation is too hot, are we just in need of more workers?

We may need more workers. I was at Home Depot the other day. There was no one to help me load 16 fifty lbs bags of heavy topsoil into my SUV, That’s the only reason I go there. To avoid this heavy duty task. I wound up loading them all myself. Meanwhile, in the store itself there were many part timers standing around doing nothing productive, trying to sell credit cards and doing other useless tasks. Something is wrong with the management at Home Depot to allow this to happen.

That’s a corporate decision to reduce their labor costs. They will soon give you AI to help you load your truck because that’s more efficient than paying someone a salary.

Or you could hire some help from the parking lot, if you speak their language. Home Depot would peremptorily move employees to other locations at short or no notice in the past, and each time I’ve asked where something is, the employee invariably reaches for the phone. I can do that on my own. At least in the electrical section, nothing is in the correct location and employees are trying to make out the SKU numbers written in marksalot on stacks of cardboard boxes ten feet in the air. Have to check your purchase to make sure it’s not a defective return somebody reshelved. You have to budget time now for the bigbox building centers, whereas the supply house counter is quick, and often cheaper now than Lowe’s and HD.

If you know what you want, a professional trade supplier will deliver it to the job site. Remember, you are not getting paid when you are at Home Depot or driving to or from there. It pays to do what you are paid the big bucks for, not for being an errand boy. Before I was a Realtor, I worked in the building trades. It is an expensive waste of time to pick up lumber yourself. You are spending dollars to save dimes.

I rarely go to Home Depot anymore since I can get most of what they sell shipped to my home for LESS $ with Amazon.

Here in Canada if you go to Home Depot these days you better be prepared to find your own items, I do it all the time on my phone now because if you find someone to ask and tell them you need a paint marker they’ll take you to the spray paint section and point at marking paint or something. What’s worse is this happened to me at the Hilti store last time too, it’s the main distribution warehouse for Canada and after telling the guy what I’m after and showing him a picture he came up with the wrong Item and asked me if I’m showing him a hilti product, yes I was, it had the hilti logo on the item itself LOL, this stuff sells for a premium for commercial applications.

Labour shortage is right, there are bodies here to fill position but if you need more than a set of flailing arms good luck

Howdy Swamp. Takes longer but make them load it. Code 50 to register 1.

“are we just in need of more workers?”

It’s in the works. Millions of recent immigrants will enter the work force eventually and put downward pressure on lower wage jobs.

Recent?

Other than COVID, there have always been lots of immigrants (some legal, some not) coming into this country. Even under your Cult leader.

BTW, long term, taking in immigrants when employment is tight is a net positive long term for an economy. It is always productive for an economy to bring in productive workers when employment is tight. They work hard and pay taxes. Some start new businesses that increase the employment pie. Other get educated and invent some new tool that increases the quality of life for U.S. citizens.

“Even under your Cult leader.”

And who exactly do you think my cult leader is? Perhaps you are projecting about being in a cult. For clarity, I have never affiliated with either of the political cults.

Immigration underpins the success of our nation. However, the numbers of new immigrants should not be to the detriment of citizens. The “recent” influx is historically unprecedented.

CHS, what history books are you using?

It should also be noted that your original comment is still wrong about more workers being on the way. Look at the unemployment rate and use real history books to put it in context.

Businesses are going short handed because their only choices are go shirt handed or pay more.

Not sure why I would consult “history books”, I would refer you to U.S. Customs and Border Protection statistics.

Regardless, if your point is that addressing a historically tight job market with historically high numbers of illegal immigrants is a good, then just state that I happen to disagree.

No, we don’t. Prices of some of the biggest services that are hot are not driven by wages: shelter, auto insurance, health insurance, etc. Others, such as food services and auto repairs are driven by wages, among other factors.

But bringing in more workers to suppress wages is a bullshit strategy that suits only the rich because they get the cheap labor.

Wait, how is the cost of auto insurance not indirectly driven by wages? Isn’t it the higher repair costs (driven in part by labor costs) at body shops part of the reason for car insurance increases?

I kind of see it how you do, indirectly driven by wages (for at least a big portion). Shelter is expensive because of materials costs and labor costs to build (and consequently… insurance costs for replacement/repairs). Auto the same (I do know what we pay for parts and what we pay the folks to assemble them, and its all gone up substantially post covid). Healthcare the same, kind of. I do feel like labor is playing in, but maybe indirectly at a tiered level so hard to fully quantify easily.

I had a hunch, so a quick google search brought this up

“U.S. insurance companies’ overall exposure to commercial real estate—encompassing commercial mortgage loans, CMBS, real estate, and REITs—totaled $982 billion as of year-end 2022.”

Some of it is labor increases. Some of it is parts increases. Cars have become so complex that it is no longer easy to fix a car by replacing one little broken metal part with a similar whole part.

Now you have to replace whole modules because it is all computerized.

Not a complaint, just pointing out modern cars have become very complex.

I recently had someone tap my rear bumper. Just a minor indentation. Should be easy to fix right? Maybe just tapping out the dent and some paint touch-up. Easy.

Nope.

Backup sensor was damaged. Needed to replace the whole bumper. Couple of thousand dollars.

Car repair is no longer about Bondo and paint…..

Go price a LED headlamp assembly. One lamp is over a grand. And that wasn’t even a total LED. I hazard to guess what the replacement would cost on my new Technomobile.

Vehicles are no longer a distributor with a set of points, a cap, and a rotor. Now it’s computerized and connected to multiple sensors. If a sensor is damaged, entire assemblies must be replaced. Once upon a time, if you left your windows down and the interior got wet during a storm, your worst case scenario was mildewed carpets. Now? The *brain* under the driver’s seat gets toasted and you’re talking thousands…. (the module and the programming of said module to the vehicle). No more going to the boneyard and harvesting one out of a like vehicle. You still have to have someone with the proper gizmo to mate the vehicle to the module.

That’s why they’re now called “technicians” rather than mechanics.

“But bringing in more workers to suppress wages is a bullshit strategy that suits only the rich because they get the cheap labor.”

AMEN

A new twist on indentured servitude. At some point you have to reflect on the decisions being made.

Impacts go beyond that. The focus is often on the US but we are also negatively impacting other countries who have invested via their system to develop people and they leave. I don’t blame the people of course but the system which chases low cost labor as easiest thing to cut and often a big expense.

My workplace is a tale of two companies. The corporation and the contractor.

It’s been increasing on the contractor side too. My corporate boss loves contractors “because I don’t have to pay them benefits.” However meager.

Our insurance is unaffordable meaning a 401 match is one of the best things I get.

The guy who is in charge of the contractor side has another business he runs, involving the purchase of $80,000 SUVs for a limo service.

Glen: it goes both ways.

Many of the contractors support families in their home country. The coordinator (who probably makes 10%) probably gets investment money from his family to increase his business.

Meanwhile one of my coworkers is curious why they allow him to work and pay taxes but he doesn’t have good papers, while simultaneously wondering about welfare abuse and American ls who don’t want to work. Another takes home more money than I do, although with considerably more time.

It’s a new “outsourcing” argument. Now insourcing. The problem with both is the inferior skillset, subpar training and overall quality decrease. It doesn’t happen all at once and the upfront savings is welcome.

I am only and directly serving the wealthy: the LOVE a good deal more than anything.

Work them so thin they can’t have kids and import the cheaper replacements.

God bless America

You will know when interest rates are restrictive enough when congress actually cuts spending. Until then, good luck with inflation.

For the rent vs home price graph, adding a 3rd line could prove very, very interesting: median P&I mortgage payment, calculated by historical median home price and mortgagenewsdaily interest rate throughout the time period being plotted.

Thanks, useful! Some crazy numbers here.

Would be interesting to see what the trend in YoY and 3 month annualized inflation is on core services minus shelter and medical. Looks like its around 5% right now, but its difficult to work out what the trend is.

If you take shelter and medical out of core services, you only have a few categories left. You no longer have core services. Then you can take out a few more items, and you have nothing left. What’s the purpose?

Why not just look at specific categories separately. If you want to know about auto insurance, look at auto insurance, etc.