But the plunge in retail prices of used cars and trucks hasn’t progressed nearly as much.

By Wolf Richter for WOLF STREET.

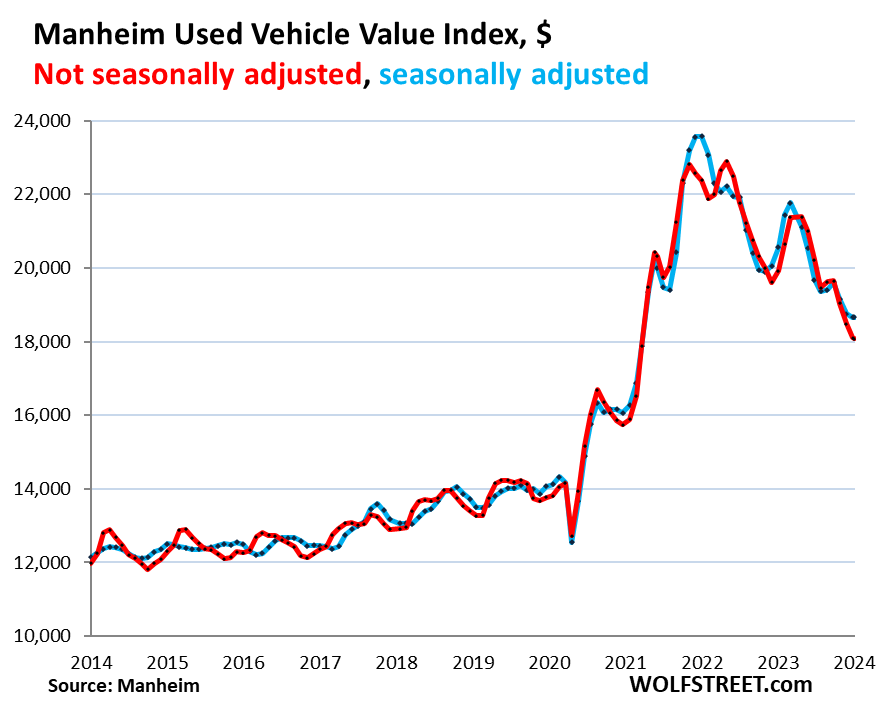

Used vehicle prices at auctions dipped another 0.2% in January 2024 from December 2023, not seasonally adjusted, to $18,074, the lowest since March 2021, and are down $4,828, or 21.1% from the peak in May 2022, according to the Manheim Used Vehicle Value Index (red line in the chart).

The plunge has now worked off over half (55%) of the historic and ridiculous 63% spike from February 2020 through March 2022, according to data from Manheim, the largest auto auction house in the US and a unit of Cox Automotive. What everyone wants to know is how much more it will work off before prices stabilize or start rising again.

Auction prices usually dip in January from December, and so seasonally adjusted, wholesale prices remained flat in January from December, and are down by 20.8% from the seasonally adjusted peak in January 2022 (blue).

These auctions are where dealers go to replenish their inventories. Supply comes from rental fleets that sell the vehicles they pull out of service (usually between 2.5-3.5 million vehicles per year), from finance companies that sell their lease returns and repos, from corporate and government fleets, etc.

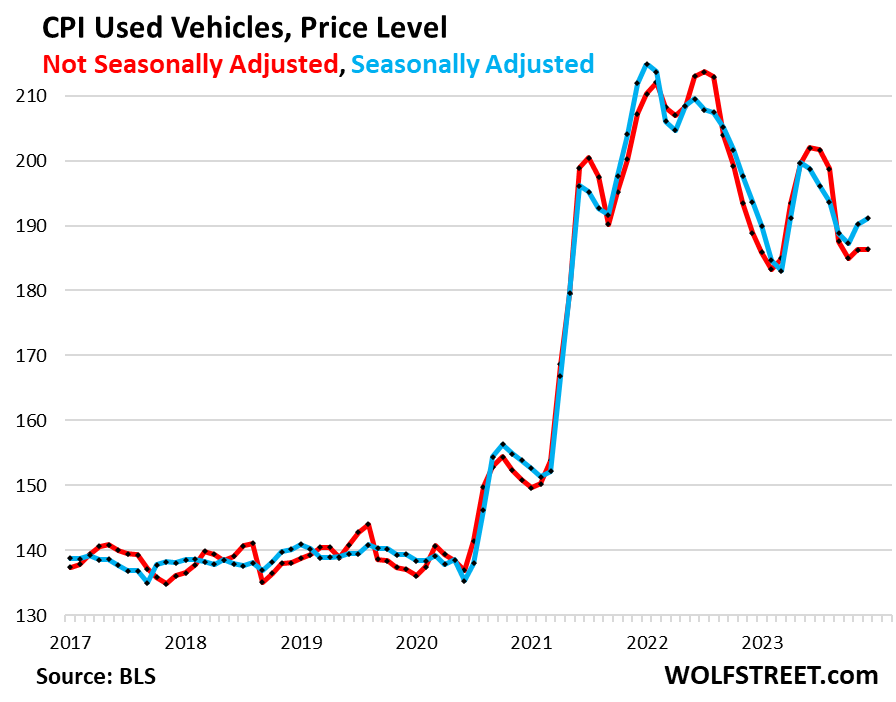

Retail prices have dropped 11% seasonally adjusted and 13% not seasonally adjusted from their respective peaks, as of December, according to the CPI for used vehicles.

They have given up about one-third of the historic crazy 55% spike from February 2020 to the seasonally adjusted peak in January 2022 and to the not-seasonally adjusted peak in July 2022.

But price declines hit a low in March 2023, then bounced off, then fell again later in 2023, and in late 2023 started ticking up again, in a marked disconnect from wholesale prices:

Wholesale prices have now given up 55% of their pandemic spike, while retail prices have only given up 36% (both not seasonally adjusted), and haven’t even made it back to the lows of early 2023, and then they ticked up again:

Inventories are rising, supply is ample.

Used retail inventory rose to 2.39 million vehicles on dealer lots at the beginning of January, the latest estimates from Cox Automotive, compared to a range of 2.8-3.0 million in 2019. Supply at the end of January was 53 days, according to preliminary estimates by Cox Automotive, up from 49 days a year ago.

So there’s not a glut of vehicles sitting on dealer lots, but inventories are ample and rising. And it looks like enough consumers are still on buyers’ strike, and that’s what it takes to put a lid on these still crazy prices.

Used vehicle retail sales in January rose 5% seasonally adjusted from December, but were down 3% year-over-year, according to preliminary estimates by Cox Automotive.

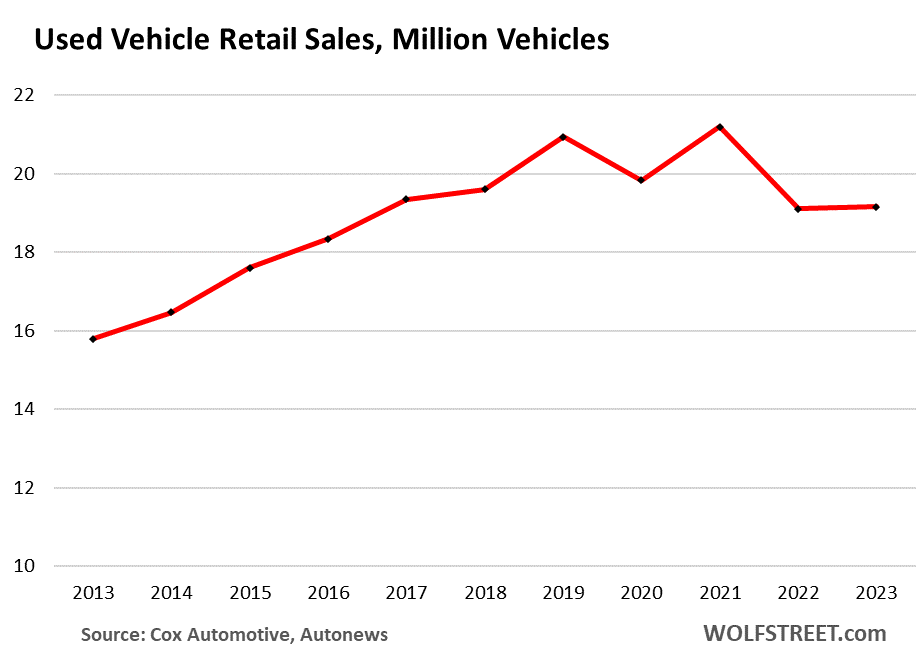

For the year 2023, used-vehicle retail sales inched up a hair, to 19.1 million vehicles (by contrast, new-vehicle sales jumped 12% to 15.5 million units, still much lower than back in the year 2000).

In 2021, when new vehicle sales collapsed due to the shortages, used-vehicle retail sales rose to 21.2 million vehicles, the highest in the data we have, while prices spiked ridiculously:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

“Inventories are rising, supply is ample.”

Inventories are rising at a good clip and that is precisely why I’m still on buyer’s strike. They’re still not quite back up to pre-pandemic levels, but the trend warms my heart. My old BMW 335i is holding together, but it honestly probably needed to be replaced a couple years ago. I just refused to pay the kind of coin that used lumps were fetching in 2021/2022. The used lot I drive by everyday is packed and nothing is moving there, but I do see them dropping prices on stagnant inventory, so it’s just a waiting game for me. I only buy cars outright, so I welcome high interest rates shutting down competition from financed buyers. I know my machine inside and out and I can fix anything on it. Parts are not that expensive and I cover my own labor. So I wait.

“The used lot I drive by everyday is packed and nothing is moving there”

Lol, every time I go to the grocery store, the shelves are packed. I seriously doubt it’s because nothing is moving. Funny how wrong anecdotal information can be and how tainted it is by our personal opinions.

Your grocery store probably doesn’t have the same blue 2019 Camry, white 2020 F150, three gray 2021 Altimas and green 2016 Elantra week after week after week.

It’s entirely possible for a layperson to correctly note that inventory on a specific used car lot is not moving, and it’s silly to suggest that they can’t, no matter how smart it may make you feel.

CCCB, ❤️🤣👍

Pea Sea,

We had 200-300 used cars and trucks on the lot and constantly moved them. The front line (which was what people saw when they drove buy) got changed at least partially about every other day. We had a couple of people whose full-time job it was to keep the used-car lot looking fresh. This was on top of the regular turnover.

We bought lots of our inventory at auction, usually 1-2-year-old rental cars that all were kind of the same. We might have had 20 Escorts LXs on the lot, in four colors, with 10-20,000 miles. Back then, the big thing was low mileage Lincoln Town Cars that came out of rental fleets. They were considered a luxury product on a Ford lot, but they were a dime a dozen, and our buyers would go from auction to auction and buy them. We lined them up for all to see. If you drove by every day, you might think that we never actually sold any of them. But they were red-hot.

We recently went to CarMax to buy a 2-year-old Ford Fusion hybrid, after ours got totaled. There were like two dozen other white Ford Fusions on the lot. They all looked the same. The only 2-year-old 22,000-mile hybrid was the one we bought, but it didn’t look any different than the 4-year-old hybrid or the 110,000-mile hybrid, or the non-hybrids. We had to get close enough to read the window stickers to see the difference. And “Hybrid” tag is really small. No way could you tell by driving by and looking at the front-ends of these cars what was going on there. And they had a huge lot on the side and behind the building — as did we — that you couldn’t see anyway by driving by.

I could no longer coax anymore life out of my car and had to buy a less used one recently. The dealer inventory is moving quite quickly if its low mileage and priced reasonably(for this point in time). I went with the intent of looking at a two Tacoma’s. Both were already gone.

I would have loved to wait another 18 months for some more price correction but my car chose early retirement.

Thanks for keeping us informed on the facts Wolf.

HA. That’s exactly what I was thinking !

No CCCB, I mean I am keeping an eye on specific vehicles they have on the lot since I am sort of in the market for a newer vehicle probably later this year. Specifically, a couple of X1s have been sitting for almost 3 months now, even though both have come down a couple thousand dollars under $20k now. I actually bought an X3 m40i from them not that long ago when my wife’s vehicle was totalled by a drunk driver and we became forced buyers with an insurance payout to spend and it was a reasonably positive experience, so they could be my goto when my car is out of steam. There are other vehicles I just recognize that have been sitting out front for a while as well. I’m sure they’re still selling cars, but their turnover is obviously slow compared to a year ago, and they are being forced to drop many of their prices. It’s not my tainted opinion, it’s simply an observation that I am seeing price drops on existing inventory which is something that just wasn’t happening in ’21/’22. But don’t take my word for it, maybe RTGDFA that clearly supports my anecdote with data!

“But the plunge in retail prices of used cars and trucks hasn’t progressed nearly as much”

This is the part that bums me out.

Off-topic but I’d argue that your 335i is a future collectible. That model blew the doors open on BMW aftermarket tuning. The N54 engine will be as highly regarded as the Mk4 Supra and Nissan Skyline of it’s day.

Yeah, my N54 is a product of a short magical moment when the engineers sneaked an unbelievably tunable twin turbo 6 past the bean counters. But being the first modern BMW turbo 6, it has its weak points. Coming up on 170k miles, if a piezo injector dies, I’m out like a fifth of the car’s value just to buy 1 injector. It’s on its third fuel pump and those have gotten quite expensive too. I’m on water pump #4. It is pretty cool to blow the doors off any SRT8 product like they’re standing still. Even Porsche 911s have fallen to my unassuming white sedan! But after 150k miles at 18psi of boost, a catastrophic failure could happen any moment. I LOVE the B58 in my wife’s X3, and it’s vastly more reliable than the N series engines, so I’m really looking to get into a B48 or B58 vehicle as prices come down a little more.

My 2014 Honda Civic has had zero failures after 145,000 miles. I do all the work on it myself too. And with its super reliable 1.8l inline 4, from a standing red light it blew the doors off a jogger on the side of the road. Well, after about the first 100 yards. After that I laughed at her in my rear view mirror!

They’re all throw away cars lol. Any unibody car is not a collectible it’s a recycled throw away. First person to jack it up in the wrong spot already has damaged the structural integrity of the vehicle. Cars today are made to crush on impact in a wreck. This is why they get totaled in wrecks, hence all unibodies are throw away cars.

Lot financing costs will eventually force dealers to mark down their inventories if there are enough sensible consumers like yourself. My 2017 is holding up fine with only 50k miles on the odo. With that said, I would like to eventually buy a small used hybrid SUV, but for now I plan on playing the waiting game as well.

It is quite amazing to see the ill-effects of trillions of dollars of money printing and its aftermath. Even though some action was warranted, the Fed did not have any sense as to what was needed and what was excessive. This clearly shows that there should be some constraints on the Fed from running amok as they did.

Sean Shasta-

David Lin interviews Judith Shelton on a Youtube (46 minutes) that’s easy to find through search. She speaks intelligently of many topics discussed by Wolf and commenters.

Sampling of subjects:

– can the Fed know r-star?

– is recession a’coming?

– how much restriction or accommodation is appropriate?

– whither the deficit?

– how independent is the Fed?

– are Fed mandates achievable?

– how has the Fed evolved since inception

– can the Fed go bankrupt?

– how do fiscal and monetary intertwine?

And, to your point, what can be done to provide some constraints on this ever-more-powerful institution? Few simple answers, but lots of good points and questions.

Some will not like her due to political affiliation, I suspect.

I’ve not read her recent book, but plan to…

@John H. Thanks for the information.

Apologies but here are my unsolicited thoughts answers..

Recession is not coming. Normal business cycles have been upended in this controlled market and economy.

As long as asset prices are going up these are good accommodation or restricted.

Fed can never go bankrupt

Deficit don’t matter

Fed is political as they are humans after all.

Don’t be fooled by feds explicit mandate.

Whatever Fed has done in last 2 decades have exacerbated the wealth inequality.

Making rich richer is what Fed implicitly wants.

Fiscal policies would dominate monetary .

Please prove me wrong.

I don’t understand your “Deficit don’t matter” thought.

If that’s so, could Congress run ANY deficit (say… $25 trillion) without drastic repurcussions?

@John H.

Yes deficit does not matter. It is just a number. It does not matter for a country deals with self printed currency. US Govt can print as much currency as they want vias FED and there is no slowness in demand for US Treasuries.

The quality of life of average US Citizens have gone down a lot due to cost of living expense.

The home prices have never been this un affordable to larger percentage.

But you think, anyone in power really cares about these. Inflation metrics can be fudged to make them look good.

Yellen in 2019 if I remember correctly was voicing concerns about US deft reaching 20T, now we are at 35T but she as no concerns.

If deficit really matters, people in power would have shown concerns.

“This clearly shows that there should be some constraints on the Fed from running amok as they did.”

There absolutely should, yes. And you don’t have to be a free market absolutist or a conspiracy theorist to believe this, either: it’s a simple matter of observing how incredibly badly the Fed has screwed up, time after time after time, with the powers that it currently has, and observing the damage done.

Pea Sea,

On the surface you seem to understand it, but in reality you don’t. At the time, the Fed was dealing with a pandemic, the outcome clearly not known. The economy had been completely shut off and the risk of a spiraling deflation/high un-employment event was looming. They did the right thing at the time. Only in retrospect can one suggest they acted irresponsibly. Long live the Fed. And, for those that really don’t understand it. The Fed is not J Powell. He is merely the spokesperson for quite a few very intelligent and responsible people.

Louie, Pandemic has nothing to do with money supply. Perhaps you should study history around the black plague to gain some perspective.

Judith Shelton should have been appointed Fed Chair instead of that clown J Powell. We wouldn’t be in the mess we are in now if that had happened. That was the worst appointment Trump made during his tenure.

Trump probably knew ahead of time he could “handle” him if needed.

Howdy Swamp C. I will bet you 50 cents you will be disappointed no matter who is appointed head clown.

Trump was on his hands and knees begging for negative rates prior to Covid lol. The Powell appointment makes sense

The Trump real estate empire likely had something to do with that.

Exactly. Congress dumped $6 trillion in fiscal stimulus and the Fed dumped $5 trillion of monetary stimulus into what was probably, at most a $1.5 trillion problem. It’s no surprise that we’ve had massive problems.

Only people like us see massive problems but people in power don’t see any of these problems.

Economy is doing great.

Job market is hot.

Inflation is coming down to 2 percent.

People are happy and spending like crazy.

Asset markets are at all time high despite very high fed rates

Nothing wrong ..

As long as people are spending.. USA would do fine .

I remember Old Yellen smiling gleefully, saying “it’s better to do too much than too little,” or some such. What a disgustingly irresponsible display of recklessness these people engaged in, sending the young and the poor financially reeling.

The housing market is absolutely destroying lives. I have never seen so many tents, car dwellers, RVs parked in driveways as I do at this very moment. Shelter has become a luxury item. These central bankers are sick, twisted people. Pure EVIL, driven solely by greed.

Housing prices are driven by speculators who use significant bank leverage to purchase and flip them. The federal government use to regulate things like how much you had to put down and the price to income ratio for borrowers. Congress got rid of most of those regulations, allowing prices to explode. Then comes along AirBNB taking millions of properties off the market and giant private equity funds buying up millions more to turn them into rentals. This is what is causing housing issues, not the Federal Reserve.

@Depth Charge the housing market is forcing many young people with good jobs to move away from their parents who live in expensive areas, but it is meth and fentanyl that is “absolutely destroying lives” and increasing the number of tent and car dwellers (not many – if any college grads with good jobs are “homeless” living in a tent or a car”. I was just talking to a friend that grew up in Burlingame south of SF who said his kids are moving to NC since they have decided they will never be able to afford a home in CA. My friend grew up in a 1,450sf 3×2 in the “poor” part of Burlingame (east of El Camino) in a home his Dad bought in the 60’s for ~$20K. He bought a little bigger and nicer home nearby in the 90’s for ~$400K. When his Mom died in 2015 they sold the family home for $1.45mm (today Zillow says it is “worth” $2.45mm way more than most kids with better than average jobs can afford).

I see them all over the place in Queens. Now. NYPD finally got around to impounding/towing most of them away. Someone didn’t wanna pay fees so they set it on fire while it was booted on the street outside the impound lot (they had no room to bring it inside).

Housing on Long Island is still a mess. We’re going to be one of those families with no choice but to have to buy this spring, talked with my agent and my broker to start looking early. Found a nice home in Bellmore we were going to take a look at. Agent gets there well ahead of schedule, there’s an effing line from the front door down the front walk and down the block. Like the first person in line is literally standing 6″ from the front door….2 hours before open house starts.

She sends me a picture, I said forget the open house I’m not playing that game. Royally pissed that it’s only February and I have to play effing games with all these retards.

I told her send me all the listings of homes 100 days or more on the market so I can see which will do best for renovating. Would be nice to get something move in ready but looks like I’ll be swinging a sledge and a nail gun to get what I want.

Wolf, what are the main drivers of the delta between wholesale prices (down 55%) and retail prices (down only 36%)? Is it safe to say the spread between these two accrues to the dealer’s bottom lines?

Greedy used car salesmen.

I’d say it’s risk premium.

They’re anticipating value drops between time of purchase and time of resale.

If they don’t materialise, profit.

If they do materialise, they can still put food on the table.

The net effect is these wave patterns down as sentiment traces values, fear/risk aversion… and greed/confidence.

Just wait longer.

AK47,

Retail prices are very sticky on the way down. Keeping retail prices high, or somehow make them go higher, that’s the entire business model of a used car dealer. The only thing that would push prices down is a much bigger drop in customers.

I’m worried that the buyers’ strike is starting to fade, and people are read to buy. Last year, used vehicle sales remained flat, when they should have dropped, and inventories should have risen a lot, and gluts should have developed, and that would have caused retail prices to sag further. But that didn’t happen. Too many people bought cars at these ridiculous prices.

This is one of the reasons why I think durable goods CPI will stop falling this year and may head higher, supporting an increase in overall CPI and core CPI, and why I think we may look back at this 6-month period of sharply lower CPI readings as a head fake.

Consumers are just really really tough right now. They’re loaded, they’re making a ton of money, and they’re spending regardless of what interest rates are, and maybe they feel lousy about whatever, so they go into retail therapy? And auto dealers are there to help them feel better.

It’s probably smart for people to dump their dollars and get what they want now rather than wait and see their dollar further devalue based on current and future govt spending. It’s probably why stocks keep going up at this point, too. I’m trying to get out of most of my cash/mmf holdings and move out of dollars into assets I want longterm even if they cost more now than I’d like to pay.

Howdy Lone Wolf. Also don t forget that millions of Americans will purchase what they want when they want it and continue on with their lives no matter what. Just as you did recently after the unfortunate car accident. You needed to make a purchase and did so. Some folks starting life out in the late 70s have seen plenty of ups and downs and will continue life full steam ahead……..

Yes, but you only need 20% of potential buyers to on strike, and the market crashes.

Perfect storm of demand I guess? Boomers are in YOLO mode, Gen Xrs making more money than they’ve ever made, Millennials making more money than they ever made (and also many of them don’t have a lot of reference on what things used to cost), and then Gen-Zrs are earning high wages, gaining more spending power, and clearly have no reference on what things used to cost either. Sounds like the perfect consumer spending storm that is keeping prices high all across-the board!!

AK – it should be noted that strong, positive correlation between these series (Manheim and UV CPI) is a recent phenomena, presenting itself only after the pandemic/money drop/consumer frenzy/supply chain fiasco.

Some boring numbers for consideration – observed correlations between monthly Manheim and UV CPI in 5 year increments going back to 2000. For reference, correlation can be simplistically interpreted as the % of observations that vary in the same (or opposite) direction:

CORRELATION*

2000-2004 -0.026

2005-2009 -0.058

2010-2014 -0.149

2015-2019 -0.631

2020-2023 0.930

From 2000-2014 there was effectively no correlation between UV CPI and Manheim. These measures functioned independently and did not vary in tandem to any statistically meaningful degree.

That changed 2015-19 with a fairy strong -0.63 correlation. But as indicated by the sign (-) the series were moving in opposite directions; Manheim trended up, UV CPI trended down.

Since 2020 they’re obviously moving in lockstep, but even this is starting to come apart. For the 12 months of 2023 the correlation is -0.36.

*Note – the historical correlations improve somewhat if we lag CPI by 1-2 months to mimic the time required to get a wholesale unit into a retail transaction, but the hypothesis holds that Manheim and UV CPI are not statistically indicative outside of the pandemic era.

CORRELATION – CPI LAGGED 2 MONTHS

2000-2004 0.040

2005-2009 0.309

2010-2014 0.0165

2015-2019 -0.556

2020-2023 0.971

Last point – all this data is freely available online if you’d care to confirm. Search “manheim used vehicle value index” and “Fred CUSR0000SETA02”

My empirical used car evidence from the last three years: there are PLENTY of used Porsche 911’s on our local dealer’s lot now. Quite a change from the late summer of 2021 when there were virtually NO new or used 911’s anywhere to be seen at the same mid-sized dealer. Being the greedy capitalist I am, and understanding the basics of supply and demand, I sold my 15-month old Porsche 911 Turbo S back to the dealer for $30K more than I paid for it, at the dealer’s behest. They were desperate for inventory. ANY inventory. And as an added bonus… I got on the dealer’s wait list for my next Porsche allocation which is now tucked away snugly in my garage. I guess timing is everything…

Depends on the 911. I’d like a 993, but those are hard to find and keep going up in price. A 996 and newer…dime a dozen and no desirable at least to me. Porsche went from low volume sports car maker to now mainly high volume SUV maker plus a ton of 911s. They overproduce and Ferrari going down the same path.

@Z33 The economy was in the tank in the early 90’s when the 993 came out so they didn’t sell many of them (Porsche averaged “under” 5,000 sales a year in the US from 1991-1995). I think the 993 is one of the best looking cars ever made but I also like the look of my daily driver (when its not raining) a 997.2 Carrera S Cabrio. Last year Porsche sold over 75,000 vehicles in the US (only 21% of them were 2door Sports Cars).

And a little known fact: 911’s are produced at a rate of 10:1 over the alleged “entry” sports car, the 718. Although I don’t consider a 718 GT4 RS/Spyder RS an entry level car. They’ve recently had a ADM’s approaching that of a GT3 Touring…

The drop in wholesale prices should show up in people’s hoods at the lots everywhere where “credit isn’t a problem.” For those who are waiting to experience the 50% lifestyle, the lots make their money on financing as well: “we carry our own paper.” It’s the same as your ridiculously overpriced home, home loan, and property tax, but with nicer people than Wall Street bankers. Just like lottery tickets are the same as your “startup” stock investments.

Only specialized subprime dealers/lenders carry their own paper for a little while. They fund those loans with a warehouse line of credit at a big bank, and when they have enough loans together for a good-size loan pool, they packaged the loans into bonds (Asset-Backed Securities) and sell them on the global markets. A bunch of them filed for bankruptcy this year.

Larger non-subprime dealers just originate the loan and sell it to a captive finance company (such as Ford Credit), or any finance company or bank, which then package the loans into ABS and sell them on the global markets. It’s a huge business.

Only a tiny note-lot on the corner with 10 old cars (usually marketing to deep-subprime or cash customers) might actually carry its own note.

A few years ago, those vanilla 1997-1999 model Toyota corollas used to sell for at least C$15,000-$25,000 with a 200k+ odometer.

Back in 2019, they were selling for $500 lol.

MW: Toyota shares hit record high in Japan after company raises earnings forecast

I am planning to buy my first “new” car if Toyota ever brings the new 300 Series Landcruiser to the US (sadly as of now we are just getting the Lexus version with “too much bling for me”).

“Gone on buyer’s strike.”

The price spike in the first place was the consumers’ fault for all piling into the market at once. Why does capitalism have to swing from radical extreme to radical extreme — a surge of interest, followed by a total buyer’s strike? It reminds me of the stock market, and the crash of ’29. Things were looking pretty good in the market too up until that fateful moment.

I wonder if there was some trend data on small car inventory vs large car/SUV inventory. When I shopped for a used subcompac a month ago I noticed a shortage of small used cars in the dealer’s lots. Conversely, I noticed a glut of large sedans/SUVs and trucks in the same lots. The recent trend in gas prices may worsen the glut of big gas guzzlers. Also, people here are moving back into the city in record numbers, and they don’t need a big car or SUV for city driving.

Wholesale prices of compact cars have dropped 13% YOY and of mid-sized cars 11% (Manheim), compared to 9% drop for the whole index. No trend data though.

There is not a lot of inventory of compact cars because Americans don’t like to buy them as new vehicles, and so many automakers have stopped making them. Americans like to buy big equipment, and they’re willing to pay out of their nose for it, encouraging automakers and dealers to make huge profit margins on them. That’s just a basic fact of life in America, like death and taxes.

Wolf,

“Americans like to buy big equipment,”

Americans on the whole may not like small cars, but they sure like them here. That’s because DC is like a European City. The city grid was designed by a Frenchman back 3 centuries ago. There is a shortage of parking, the streets are narrow, and the speed limit is 25MPH, 20MPH in school zones. People’s lifestyles support walking, biking, mopeds, scooters etc. At least the horses are gone. Subcompact cars fit right into the DC lifestyle. Big cars don’t.

Yes, there are a lot of small cars here in SF too, and hardly any pickups (I mean, where are you going to park them? They don’t even fit into the garages (too high, too wide, too long). And parallel parking out on the street, good luck?). But those cities (along with NYC, Boston, and a few others) are just a few pockets in the US. Go to Dallas or Houston or Atlanta or any of the big other cities, and to the gazillion smaller cities and towns in between, and you can see that people love big equipment.

So Cal BDude..Yeah but the Nikkei is on a tear..up 30.85% the last 12 months. What you might not have heard is that Toyota, which owns Daihatsu ( a J. manufacturer of small engine (low tax) vehicles is”taking responsibility” for the bogus, doctored crash test results of Daihatrsu.

Not to mention that the tanking in the US now in CA (as Wolf reported)

is Toyota (by a hair) #1 Tesla #2 and Honda #3.

You’re the So Cal guy so you should know this along with the prediction that Tesla is going to eat Toyota’s lunch in CA, largely due to

politics!

Toyota will continue to have record global profits by using excellent judgment and common sense to provide the types of vehicles that its customers actually want to buy as they are; doing now. I admire them, but am not a potential customer as I’m 100% BMW and have been for many decades here in SoCal.

Toyota sales in the US:

https://wolfstreet.com/2024/01/04/ugly-charts-of-auto-sales-by-gm-toyota-ford-stellantis-oh-my-got-crushed-by-hyundai-kias-record-sales-tesla-has-arrived/

And Tesla sales in the US:

Maybe people will eventually switch to electric bicycles for their secondary or tertiary vehicle. My car insurance premium had been falling for my last two bills, but the one I got in yesterday’s mail here in California jumped by over 20% (A “Covid discount” was applied bringing the increase in my paid premium to a magic 20%). At any rate, I am on a mileage based insurance plan and I calculated my wife and I are now paying $1 in insurance for every four miles driven. Yes, you read that right. We would be better off switching to ride share and rental cars at this point. My wife said we should get rid of one of our cars.

I live in Canada, in particular, Ontario, where car insurance rates are considered extortionate, like young male drivers under 25 pay at least C$1,000 a month on car insurance.

Is there an insurance where it’s pay for the amount of miles used, rather than pay $1,000 a month flat no matter how much is driven?

The median car insurance rate in Ontario is about C$350 a month.

CAA MyPace.

I never drove with insurance until it became mandatory. Way back when you just had to pay 10 dollars a car to drive without insurance then it got raised to 40 dollars a car then mandatory insurance was enacted.

Is it just me or does this big price spike seem like such a scam? Supply chain issues seem to be resolved so are the automakers costs just that much higher as compared with 2019? Huge price spike from ZIRP and inventory shortages in 2020 and 2021 explain a price spike but we are still so much higher than we were in 2019, and prices have come down but not all the way where they were in 2019. In the article Wolf talks about inventories being ample. What am I missing? Is this just a big scam by automakers? I feel like this is the same story with many other asset prices.

Actual prices are set by buyers willing and able to pay those prices. It doesn’t matter what the seller is asking for. What matters is what the buyer is willing and able to pay.

There were massive increases in wages in UAW contracts last year with those wages increasing massively for years ahead.

Ford and GM really flooded the market with a bunch of defective cars and trucks during Covid, the plethora of safety device inoperable due to the shortage of chips. I now have friends who bought 2023 $60K plus trucks that have been in out the dealership shops for major defects. Quality and reliability of American made vehicles are in the toilet and most longtime diehards know it. GM now running lease campaigns at below $500.

Sounds like Boeing. Made in America used to mean a lot to me, but now it looks like it’s in the history books. Made in Japan is basically only thing I trust at this point unfortunately…

Never buy a UAW-made car.

Doing the traditional “extending the left index finger along the line of Wolf’s chart and eye-balling it” method, it looks like wholesale prices could have another $2k to fall.

DM: Tale of two car giants – Ford loses $47k per EV sold as electric bet backfires – while gas hybrid pioneer Toyota is set to enjoy record profits

Ford has said it will slash spending on EVs because it can’t sell enough to offset costs, revealing it lost $47,000 on each electric car it sold last quarter.

Ford needs to go out of business — and EVs are speeding up the process. Tesla makes a ton of money on each EV. Ford cannot engineer itself out of a paper bag – that has been the problem for decades. At Ford, the accountants run the engineering and production divisions. Ford only knows how to make money on expensive ICE pickups and SUVs. It abandoned its sedans years ago because it was losing money on them, even as Toyota has been making money just fine on its sedans.

Wolf, you’re absolutely correct. Ford needs to go out of business. May it’ll be joined by Stellantis and GM. All of them are horrifically managed and poorly led companies who have made one strategic blunder after another. Good riddance.