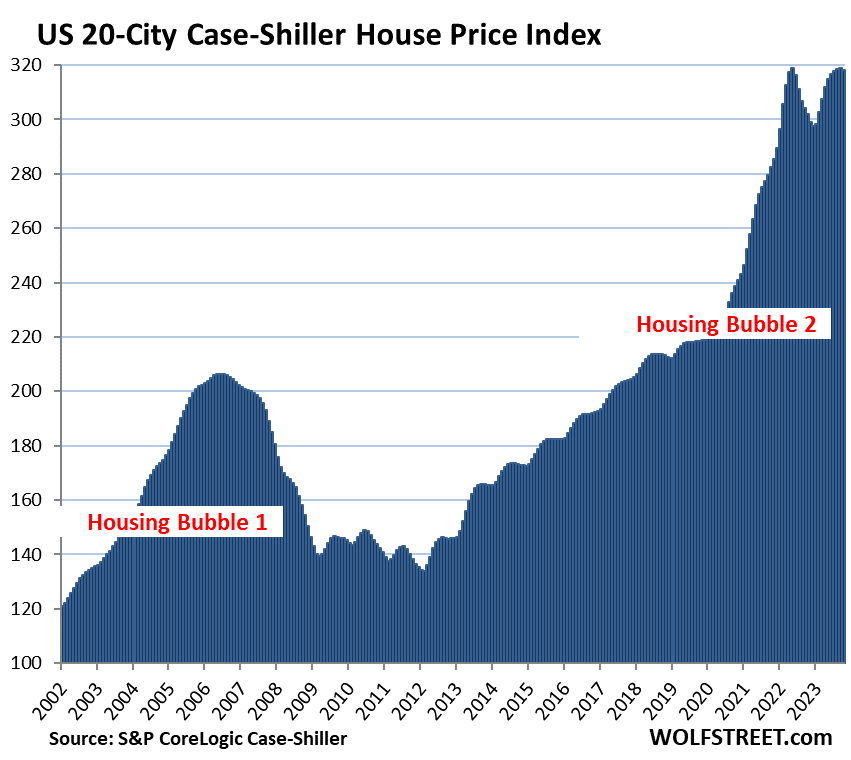

The 20-City Index dips off a beautiful double-top. Some metros saw new highs.

By Wolf Richter for WOLF STREET.

The overall home price index for the 20 metros that today’s S&P CoreLogic Case-Shiller Home Price Index covers dipped a hair from the prior month and is now forming a beautiful double-top, after a huge mind-blowing spike.

We’re going to get to the individual “most splendid housing bubbles” – as we’ve called them since 2017 to track their astounding surge – and we’ll see some big price drops from the highs in 2022 in some markets, and we’ll see some markets that put in new highs, and we’ll see a lot of double tops, and some well on their way down from the second top.

Today’s S&P CoreLogic Case-Shiller Home Price Index for “November” is a three-month moving average of home prices whose sales were entered into public records in September, October, and November, so deals made in the fall. It lags, but it uses the “sales-pairs method,” comparing the sales price of the same house over time, thereby eliminating the issues associated with median prices and average prices (see “Methodology” toward the end of the article).

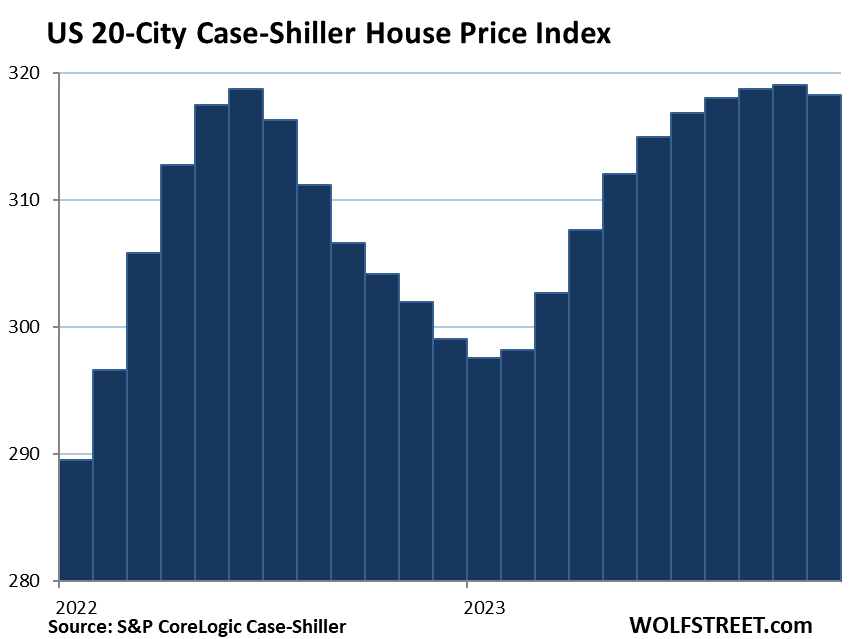

Here is the double top of the 20-City Index under the magnifying glass:

Prices were below their 2022 peaks in 9 metros of the 20 metros in the Case-Shiller index (% from their respective peak, Case-Shiller month of peak):

- San Francisco Bay Area: -12.8% (May 2022)

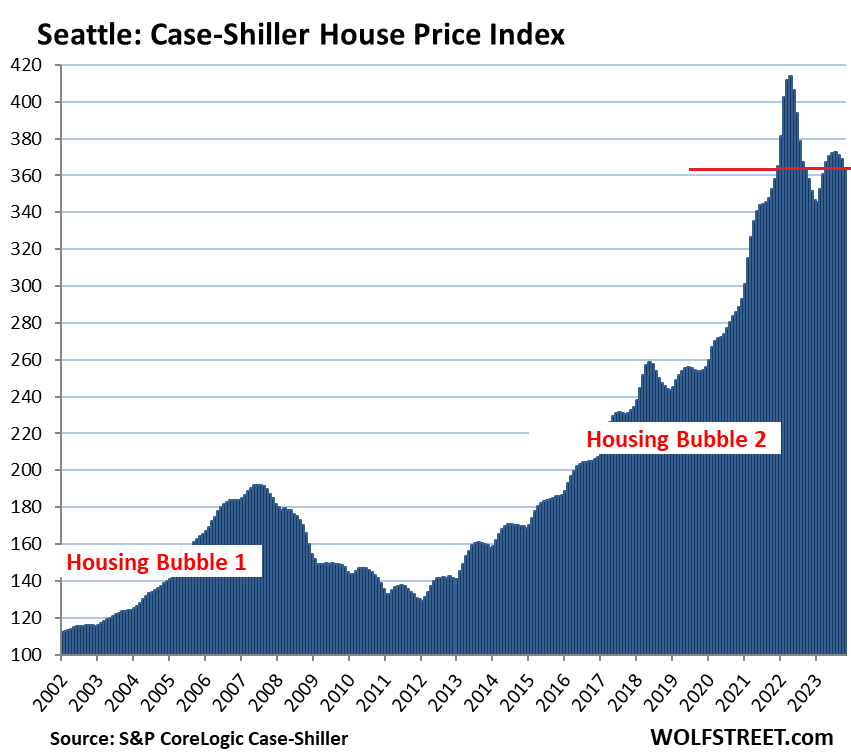

- Seattle: -12.1% (May 2022)

- Portland: -6.8% (May 2022)

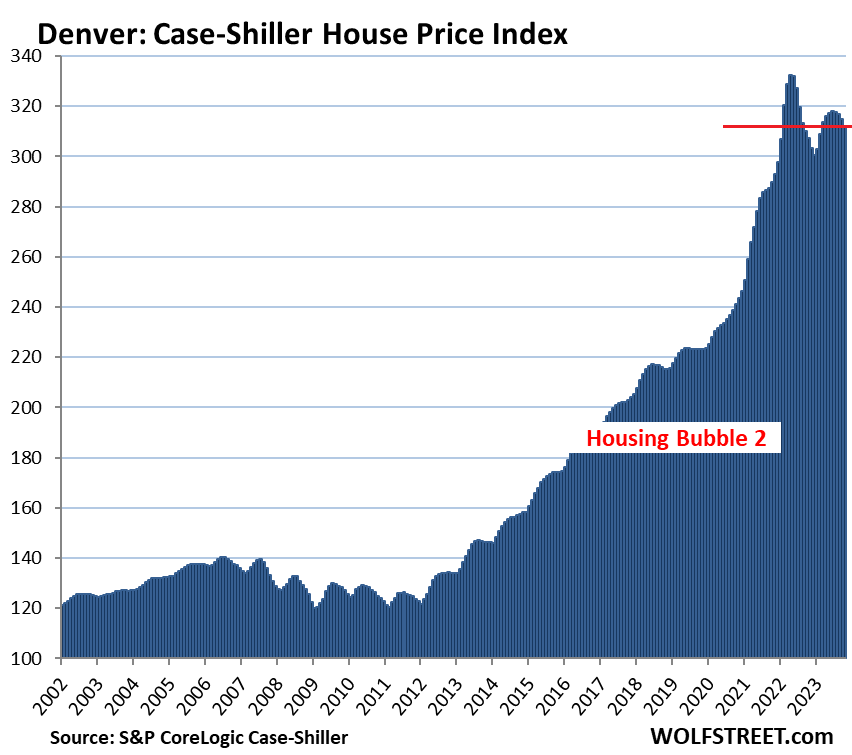

- Denver: -6.1% (May 2022)

- Phoenix: -5.4% (June 2022)

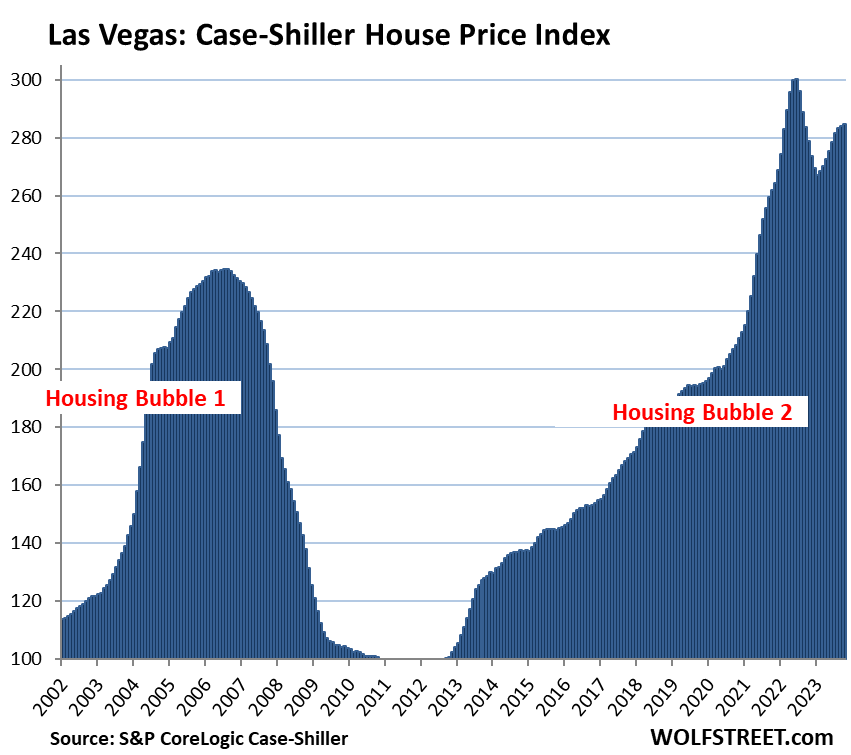

- Las Vegas: -5.1% (July 2022)

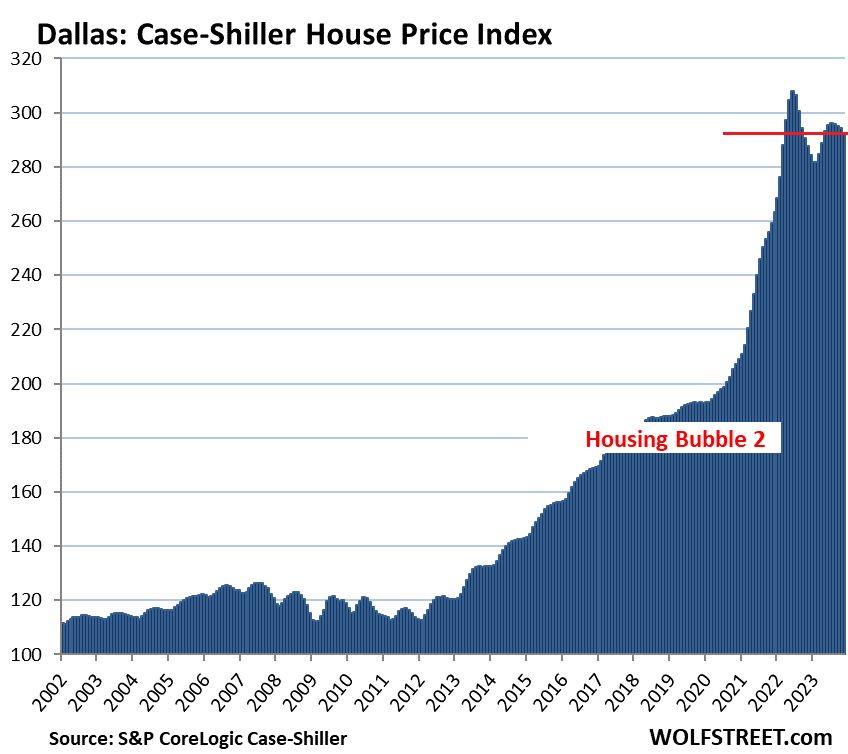

- Dallas: -5.0% (June 2022)

- San Diego: -2.7% (May 2022)

- Los Angeles: -0.6% (May 2022)

Month-to-month declines occurred in November in 13 of the 20 metros.

Prices set new highs in 7 of the 20 metros in the index (% year-over-year). Cleveland, Charlotte, and Atlanta are not part of the “most splendid housing bubbles” because their home prices haven’t risen nearly enough since 2000 to make it into this infamous list.

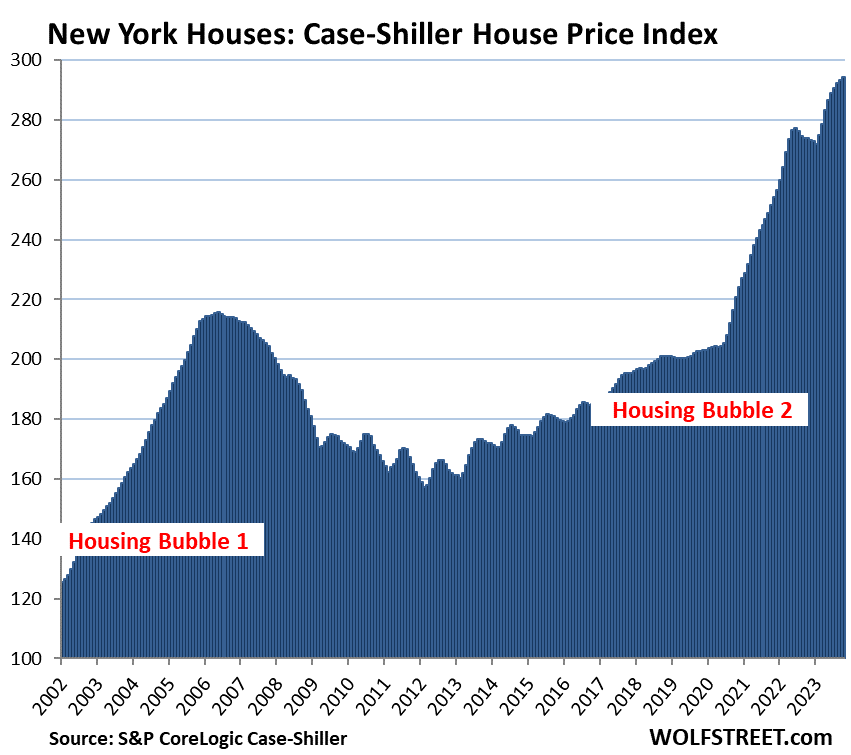

- New York metro: +7.4%

- Boston: +7.1%

- Miami: +7.2%

- Cleveland: +7.4%

- Charlotte: +7.0%

- Atlanta: +5.9%

- Tampa: +3.4%

The most splendid housing bubbles by metro.

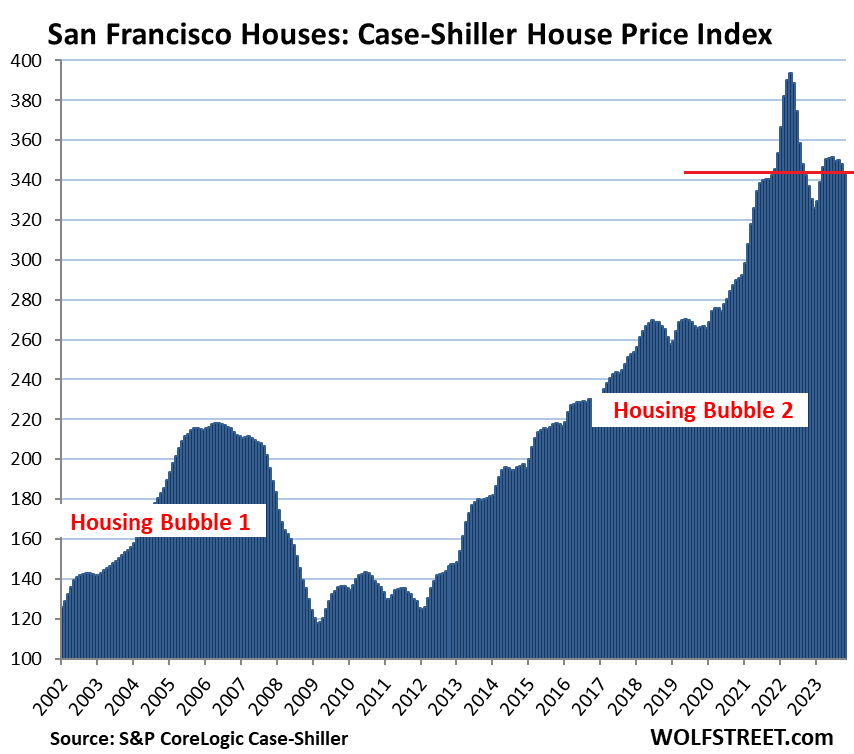

San Francisco Bay Area:

- Month to month: -1.3%

- Year over year: +2%

- From the peak in May 2022: -12.8%.

And the closeup of San Francisco:

Seattle metro:

- Month to month: -1.4%.

- Year over year: +1.6%.

- From the peak in May 2022: -12.1%.

The closeup of Seattle:

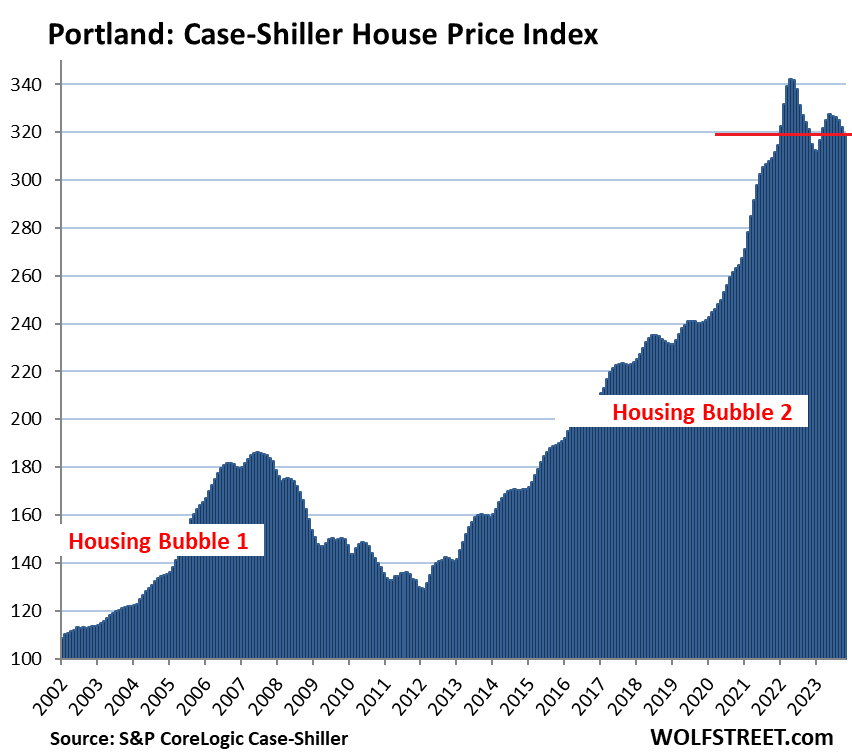

Portland metro:

- Month to month: -0.9%.

- Year over year: -0.7%.

- From the peak in May 2022: -6.8%.

Las Vegas metro:

- Month to month: +0.2%.

- Year over year: +2.1%.

- From the peak in July 2022: -5.1%.

Denver metro:

- Month to month: -0.9%.

- Year over year: +1.5%.

- From the peak in May 2022: -6.1%.

Phoenix metro:

- Month to month: -0.3%.

- Year over year: +2.5%.

- From the peak in June 2022: -5.4%.

Dallas metro:

- Month to month: -0.6%.

- Year over year: +1.7%.

- From the peak in June 2022: -5.0%.

San Diego metro:

- Month to month: -0.5%.

- Year over year: +8.0%.

- From the peak in May 2022: -2.7%.

The closeup of San Diego:

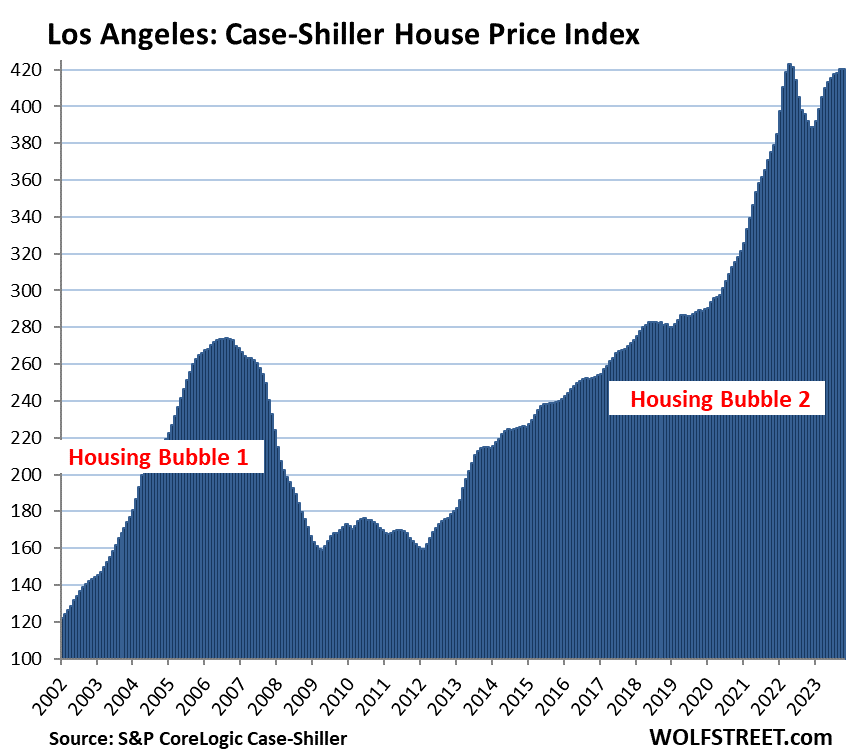

Los Angeles metro

- Month to month: +0.1%.

- Year over year: +7.2%.

- From the peak in May 2022: -0.6%.

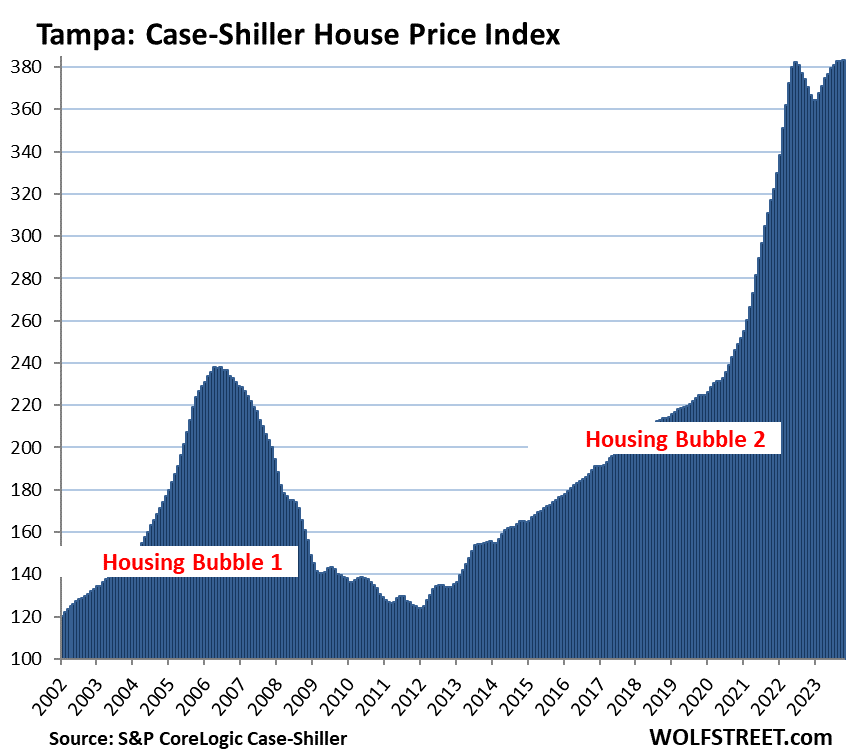

Tampa metro:

- Month to month: +0.1%.

- Year over year: +3.4%.

- New high.

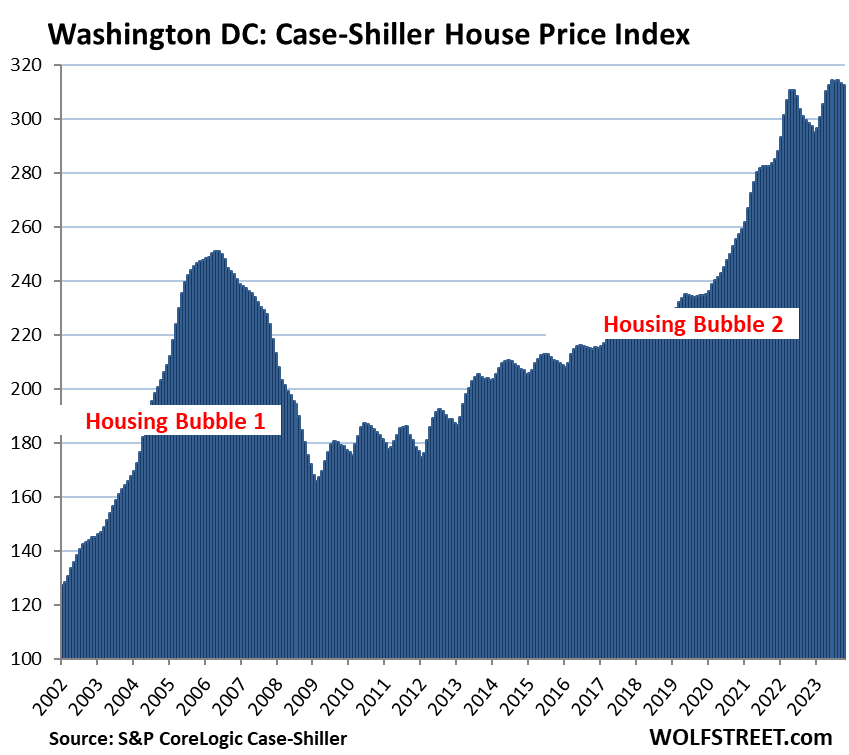

Washington D.C. metro:

- Month to month: -0.3%.

- Year over year: +4.7%.

- The high was in August.

Closeup of Washington DC:

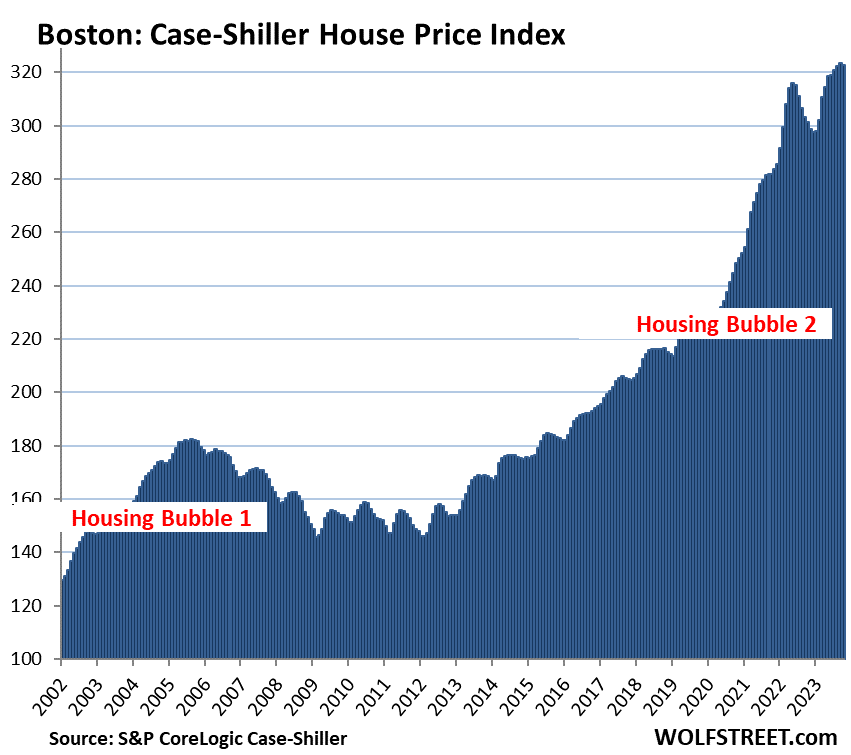

Boston metro:

- Month to month: -0.2%.

- Year over year: +7.1%.

- Prior month was the high.

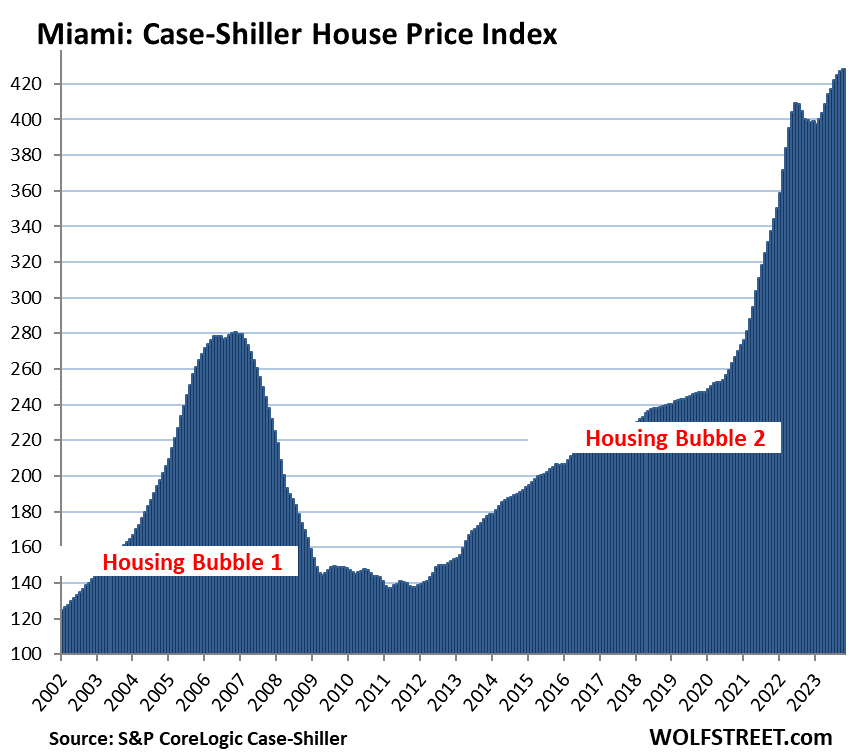

Miami metro:

- Month to month: +0.3%

- Year over year: +7.2%.

- Set new high.

New York metro:

- Month to month: +0.3%.

- Year over year: +7.4%.

- Set new high.

To qualify for the Most Splendid Housing Bubbles, the metro must have experienced home price inflation since 2000 of at least 180%. The indices were set at 100 for the year 2000. Today’s index value for Miami of 428 is up 328% since 2000, making Miami the most splendid housing bubble on this list.

The remaining 6 of the 20 metros in the Case-Shiller index (Chicago, Charlotte, Minneapolis, Atlanta, Detroit, and Cleveland) had far less home price inflation than 180% since 2000, despite the big home price increases in percentage terms in 2022 and earlier in 2023.

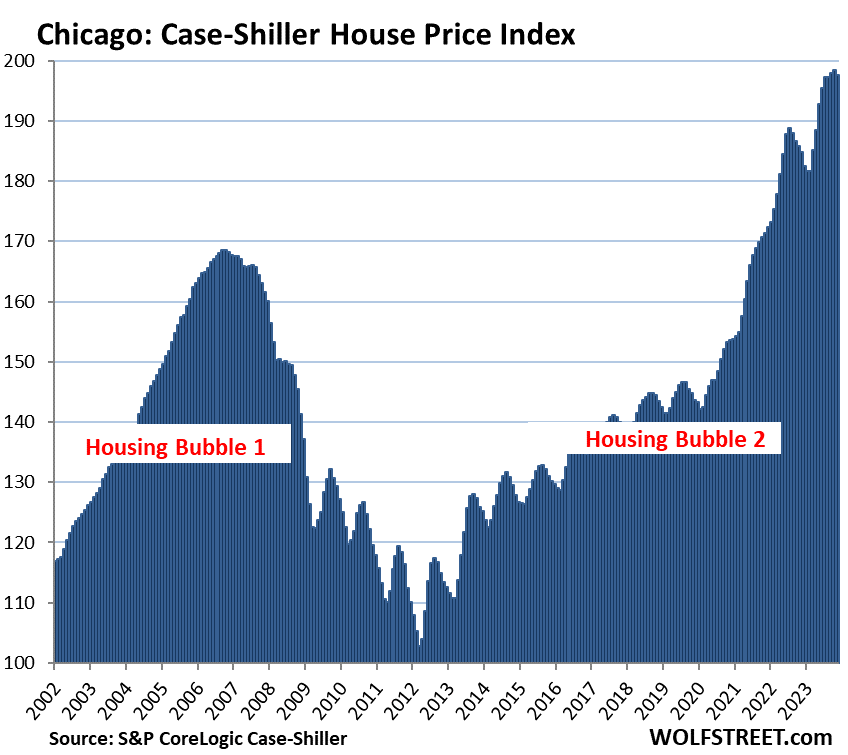

Chicago, with an index value of 197 is up by “only” 97% from 2000, and therefore does not qualify for this list of the Most Splendid Housing Bubbles, but it saw blistering price surges since May 2020, and so here it is anyway:

- Month to month: -0.4% from the high in the prior month

- Year over year: +7.0%.

Methodology. The Case-Shiller Index uses the “sales pairs” method, comparing sales in the current month to when the same houses were sold previously. The price changes are weighted based on how long ago the prior sale occurred, and adjustments are made for home improvements and other factors. This “sales pairs” method makes the Case-Shiller index a more reliable indicator than median price indices (37-page methodology).

Home-Price Inflation. By measuring how many dollars it takes to buy the same house over time – the “sales pairs” method – the Case-Shiller index is a measure of home price inflation. So Miami had 328% home price inflation since 2000. By comparison, consumer price inflation, as measured by the CPI, which tracks price changes of goods and services that consumers “consume,” was 82% over the same period (our discussion: Beneath the Skin of CPI Inflation).

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Mr Richter, what do you think of Elizabeth Warren telling the FED to lower its astonomical rates to improve home affordability? Does she not understand that lower rates could reinflate the bubble further? Or is it all just political grandstanding in this election year.

The list of all the stuff Warren said is huge. She HATES Powell. She is worried about her own RE holdings.

It’s sad to see much greed and corruption at the highest levels.

This is all fake data. Only rely on Real Estate agents for true data. You can also read articles from NAR, Zillow, Redfin and Realtor.

Housing always goes up, no correction possible.

Also, Elizabeth Warren is backing Rich investors. She genuinely wants to make housing affordable.

/s

Well said,

Pocahontas is the best

El oh el

Zillow also shows huge drops in San Francisco real estate prices. I looked at five houses in San Francisco and each was listed, didn’t sell, then taken off the market, then re-listed for 40% less.

Never rely on Real Estate agents. Leo you and all agents are so biased.

Proof of point, your inane statement “housing always goes up” LOL goofy.

Rod,

It seems you missed the sarc tag at the end of Leo’s post.

What holdings would those be, Wolf?

“A sizable portion of Elizabeth Warren’s net worth comes from properties she owns with her husband. Real estate tracker Zillow estimates their three-story Victorian home in Cambridge, Mass. to be valued at $3.8 million.”

“Warren also owns a condominium in the Penn Quarter section of Washington, D.C. “The Washington Post” reported in 2013 that she paid $740,000 for the 2-bedroom, 2-bath condo. Units with the same configuration in the area sell for up to $1.6 million, according to Zillow.

https://www.thestreet.com/lifestyle/elizabeth-warren-net-worth-15024381

I think she is misguided rather than being worried about her own RE holdings. The increased value of self-occupied properties (and I am assuming self-occupied because of where her properties are – in Cambridge and Washington D.C) is just paper money – it doesn’t mean a thing unless she is planning to sell these properties in the near-term.

There are tons of politicians and news/entertainment celebrities who won tens of properties if not hundreds. Sean Hannity comes to mind, I recall he owns dozens of homes according to an article.

Just owning two does not seem to be a compelling motivation to prop up the real estate market. Just my 2 cents.

She’s doing it for the team!

That’s pretty weak tea, Wolf! A US Senator jawboning the Chairman of the Federal Reserve on rates to protect two personal properties that are actually dwellings? You know I like you Wolf, but that’s laughable!

1. Those two properties represent the vast majority of their wealth.

2. Why else would she say such ridiculous BS? She is not dumb. She must understand that LOW interest rates led to the affordability problem. So logically, you raise rates to reverse the affordability problem. Everyone with half a brain knows that. So higher rates is the policy that she SHOULD push if she is concerned about affordability. But that’s too painful a truth if the vast majority of your wealth is tied up in RE. So you twist things around to make sure RE keeps going higher?

Not Wolf, but I just want to say that it seems to me that many of these people aren’t smart enough to understand the cause and how these things work long term. That’s why we send people checks to deal with inflation. And lower interest rates to ‘improve housing affordability’. It seems counterintuitive to someone intelligent like yourself, but I’m not sure our political leaders are always very intelligent, nor do they consider the long term consequences of their choices.

These politicians are very smart shrewd and very rich holding large assets across multiple asset classes.

It could also be they are evil. Dumb or evil. It’s definitely one of the two! Haha

…or, considering the old term: ‘banality of evil’, mebbe both (though, other than in the comics, novels or cinema, it’s unlikely the practitioner sees themself as either…).

may we all find a better day.

91B20 1stCav (AUS)

“Those people who think they know everything are a great annoyance to those of us who do.”

— Isaac Asimov

Cheers!!

Damn’d good!

Might as well offer up one more:

“Ignoramus, n. A person unacquainted with certain kinds of knowledge familiar to yourself, and having certain other kinds that you know nothing about.”

— Ambrose Bierce, The Devil’s Dictionary, 1881 to 1906 weekly

(The Bierce and Asimov quotes might seem off-subject to Wolf’s article, but since both congress and the housing market have been mentioned in these comments, I thought they might fit…)

Ah eh ee oh eew,

El burro sabe mas que tu.

Don’t follow leaders and watch the parking meters.

BS. These politicians are VERY sharp and have NO ETHICS. They are 100% concerned with the multi-billion dollar portfolios that they have built on the backs of the average American.

Wake the f$%k up.

Remember, Warren also voted for the bill that made it impossible to prosecute congressional members for insider trading. “They” (the connected “club” members) are not even bothering to hide their nefarious behavior anymore. In fact, they are changing the laws to make the bad behavior “legal”. We have been here before. Hedge accordingly.

I think you’re wrong. She actually sponsored to ban Congress from owning stocks, saying it will ‘clean up the filth on the floor’.

She went further, saying federal judges, the governors of the Federal Reserve, and “everybody who heads up a cabinet agency or of any of our independent agencies” should also face restrictions.

But don’t reality interrupt your “narrative”.

Her statements clearly demonstrate that she will do everything she can to push for rent & mortgage relief when the next recession arrives. The question is will she win or will markets (foreclosures) win?

If the former wins out, then housing will forever remain unaffordable for the vast majority of Americans.

So the first graph basically says that as a group, the top 20 housing markets haven’t seen a meaningful dip in prices. Nice job, JPowell!

During the next recession I can guarantee you that govt would come up with all kinds of loan payment moratorium.

Easiest way to buy votes.

So much brouhaha about students loan payment.. read some where most of the people didn’t even start paying their loans yet. 🙄

Where do you see Miami in the year ahead?

Miami is strong in November, by July or august I would think the splendidness should be even more splendid.

What could go wrong, just got to spend more for your splendor.

underwater aquatic splendor, just like Atlantis

Miami is the landing spot for assets from South America , Caribbean, NY and NE, EU, Middle East , and Africa . Closest landing spot from those continents and real estate available to the masses. More expensive yes but available.

I’ve read that all of Florida is having real issues with the rising cost of insurance. At some point, the cost of dealing with all their environmental issues has to make the place unaffordable in many ways.

Yeah, I live here and can tell you all about it.

While the geniuses in the GOP don’t believe in global sea level rise, global warming, etc….groups that do include:

-The Pentagon

-All the insurance companies

-99% of climate scientists

The hurricanes are getting bigger and stronger and doing BILLIONS of dollars worth of damage. Instead of doing something about it, our Gov. (old puddin’ fingers) has spent the last year getting humiliated in his run for the Presidency.

You can’t sell new homes w/out insurance.

All the insurance companies are pulling out.

Hurricane Otis that destroyed Acapulco, gained over 100MPH of windspeed in less than 24 hours (first time ever that’s happened).

So put it all together and you see where FL’s RE market is headed….

Given current interest rates and how high prices are, I’d say the housing market is holding up pretty well. I suspect much better than most expected.

No recession, barely any increase in unemployment and most get to sit on their 2.5% 30 year mortgage. No sellers, no crash.

If a recession does happen though… boy we’re in for a wild ride

/sarc

Is Chicago a bargain? It does not looks so on the chart but when compared to the amount of change as the other cities . LOL

It looks like Chicago only went up from 115 to 190 or about 70 % where other cities are up 150% to 200%? ;)

Chicago is not a bargain.

(1) Chicago two decades ago was expensive compared to most of the other cities (New York and California excepted), so the smaller increase just means it is not so relatively expensive as it was.

(2) Real estate taxes in the Chicago metro have always been high (see for example https://constructioncoverage.com/research/cities-with-the-highest-property-taxes-2023) and continue to increase, so the actual cost of owning a house is higher than a comparison of purchase prices would indicate.

(3) State and local gov’t debt and pension/opeb obligations in Chicago are quite high, which presumably will result in higher taxes and/or other problems in the future.

As a European I’m amazed to see how much Americans pay in real estate taxes. The yearly tax on my 950 square feet apartment in central Stockholm is $160.

“The yearly tax on my 950 square feet apartment in central Stockholm is $160”

and your VAT tax is 25%.

That article is based on out of date information. Property values in Texas have skyrocketed along with the taxes. The median tax rate in San Antonio is now close to 2%.

I’ve been spending a lot of time in Chicago the past six months and have been monitoring listings in my preferred neighborhood. Prices there are certainly relatively affordable for a nice ‘hood in a big city. You can get a new construction 3br/2ba condo, with a parking spot and large detached deck for 650k. Which would be a crazy steal in most major metros these days. But even at that price, with 130k down payment, you’re still gonna have a $4,500/mo payment, including HOA and taxes.

Is that a bargain? Can it even be considered affordable for even someone in the 90th percentile for income? Maybe just barely. Or maybe I’m totally out of touch with how much disposable income people have nowadays.

Lots of these units seem to be sitting on the market quite a while. So, perhaps I’m not totally off base.

It’s the bad neighborhoods bringing the prices down. It’s very expensive to own a SFH in a somewhat decent neighborhood plus the 10k+ tax bills

Innovations High School near Michigan Avenue and Madison was quite the hot spot last Friday afternoon. That would be right across from Macys (former Marshall Fields) and Art Institute for all you tourists and business travelers out there.

The SFHs in that same neighborhood are routinely into the seven figures. And in Chicago, such a house would garner a tax bill in excess of $20k/year!! Plus the new real estate transaction tax the city recently instituted on all properties purchased for over a million.

One such house is going for $1.1m. Not in bad condition, but not upgraded at all. If purchased with 20% down, the monthly payment would be $8200.

Just for fun, I looked up a house now listed for sale in San Antonio for $995,000. The property taxes are $22,860. The homeowners insurance is $9324 annually. Another house listed for $1.2 million has property taxes of $23,232 and homeowners insurance of $11,256.

Chicago is a bargain if you’re moving from a HCOL city. Otherwise, it’s over valued just like any other market. Cost to rent vs buy is out of whack with interest rates up and used homes yet to correct in any meaningful way.

New construction on the other hand is a bargain in these Midwestern cities. Builders have, for the most part, adjusted to the higher rates to stay competitive.

You can buy a used home that needs $30k in deffered maintenance for $300k or a new home that needs no maintenance for $350k..

New homes in new neighborhoods are not in desirable areas. Unless these homes are replacing old homes. I hear a lot that it’s cheaper to buy a brand new house than an old shack. That statement means nothing as real estate is all about location.

Old homes (prior to 1974 is my sweet spot) were built by tradesmen using good materials.

This crapola they slap together these days (particle board and other assorted garbage)….I would’t pay a nickel for.

Go to youtube and look up “new construction inspections” and you’ll be shocked at what people are finding.

Pre-Covid the Chicago market seemed to mostly tack to inflation due to a relatively stable population and how high property taxes are. Since then though its exploded. Given the city can’t cut property taxes because of how bad its (and the state’s) debt situation is, such increases don’t seem sustainable. Right now it must be propped up by lack of selling action going on.

Guess one can argue, this time is different and not in my precious SoCal and SD.

Slow moving Titanic for sure…

Los Angeles metro

Month to month: +0.1%.

Year over year: +7.2%.

From the peak in May 2022: -0.6%.

San Diego metro:

Month to month: -0.5%.

Year over year: +8.0%.

From the peak in May 2022: -2.7%.

Unless a deep recession come in, causes big job losses, I don’t see home prices going down meaningfully.

SD and LA went up quite a lot but just down 0.6% and -2.7% from peak which is just noise.

Is the Fed signaling their expectation of a significant recession by increasing proportion of shorter duration issuance?

(Not that their track record on market calls is particularly impressive…)

Everyone is expecting rates to return to 2% by 2026 for… reasons. That includes the Treasury. So, it would be irresponsible for them to issue 10-30 year debt at 4%.

Their argument for a return to 2% is because that’s where we were in the 2010s. The economy is in a completely different place, though. China is a mess and Boomers are retiring.

“Boomers are retiring.”

But Millennials, the biggest generation ever, are entering the peak earnings and spending years, more than replacing any retiring boomers; and GenZers are not far behind, and that’s a big generation too.

This meme that “boomers are retiring/dying and so demand will drop” is nonsense. Demand will rise because generations are a flow, and Millennials are a huge generation with lots of income.

Retiring boomers are affecting the supply and the demand. I saw this firsthand (Gen-X, IT guy and property investor 100-mile perspective of Northern Illinois, Southern Wisconsin). Mass retirements left a large Aerospace manufacturing company under-experienced. Butts were in seats, but not as productive or capable of dealing with crumbling services from other departments and vendors. Retirees from large cities were/are finding property “deals” in second, and third cities, and more rural areas.

Wolf,

I was not referring to Boomer retirements causing a drop in demand. On the contrary, their retirement causes a net increase in demand. Boomers are wealthy. Boomers have free time. Boomers want to spend on experiences post-Covid. Services are up hugely in no small part because of retired Boomers spending on flights, hotels, restaurants, and cruises. Even RV sales are up about 8% these last 2 months. All while no longer contributing to the supply of labor. This is all inflationary. They’re not going to start dying off for another 15+ years.

Then you have Millennials entering prime age as you said and federal economic policy focusing more on domestic investing (IRA) and less on China.

These all scream more demand, more growth, tighter labor, more inflation, persistently higher long-term rates. These are all great things mind you, assuming the government and Fed don’t alter course and we dodge a recession.

Three cuts this year seem possible, but the market’s anticipation (based on futures) of a return to 2010s 2% rates by 2026 is a total pipe dream.

Housing hasn’t gone down a meaningful amount because everyone still thinks the fed is bluffing and is going to reverse course.

I live in SD and the narrative is get in now before the competition returns when rates drop.

FED bluff???

J Pow Pow literally said yesterday he believes we’re at peak rates for this cycle.

They think they’ll do 3 cuts this year, prob in the fall.

The fight over March is done (he was pretty clear which was surprising).

50 minutes of reporters asking about cuts :P He prob got pissed and lost patience hahahaha

“ARE WE THERE YET DAD?”

I wonder what San Jose looks like?

There is no Case-Shiller index for San Jose. But there is the median price index by the California Association or Realtors for Santa Clara County:

Thanks Wolf!

WOW! And to think that I was upset with real estate proces when I went to work in Paulo Alto in the 90’s!

When I went to a software education class in Palo Alto in the late ’90s, I mentioned that I had bought a house in a small town outside San Antonio for $30,000. They flat out refused to believe me. They literally could not comprehend that this was possible. Of course those were the halcyon days in Texas. That same house now sells for over $300,000 and the quality of life is in the toilet.

I recently read a comment about the four groups of people who live in So. Cal. – 1) Average Joe Citizen and spouse just getting by; 2) Recent arrivals who may be living multiple families in cramped quarters; 3) People who make stupid amounts of $$$ in movies, TV, sports, business professionals, etc.; 4) People with insane wealth from all over the planet who want a “presence” in So. Cal. and don’t care how much it costs. This may explain some of what we’re seeing. Don’t see much RE for sale, but man, the number of “for lease” signs are just outta control! Wolf, as always, thanks!

You left out a very large chunk, 1a) those who earn a good living and like living in CA, and pay up to do it.

“Earn a good living” to one person could be categorized as “a stupid amount of money” to another. Not many households making the U.S. median household income of $74k aren’t living in Santa Barbara.

And you left out a fairly large chunk of people making tons of money on their stock options – both startups exiting via IPOs or getting acquired and relatively more mature companies providing RSUs (Restricted Stock Units)

Here in California, the powers that be invade formerly nice and civilized communities to erect vast Stalinesque blocks of housing, and confiscate my home equity to pay for it. And of course (despite a gaping fiscal deficit) there is the free medical care for recent northbound arrivals.

You mean people who have decided to break our laws and enter the country illegally.

Didn’t Mexico own California until the US military illegally invaded and seized control?

Polk was all about real estate acquisitions.

Illegal according to what authority? The US had no law against using military force to acquire new lands. There were no international legal bodies at the time to institute such laws, and we could probably argue whether the decisions of international bodies carry any legal weight anyway.

It’s also relevant to point out that northern Mexico was very poorly maintained and controlled by the weak Mexican government. They simply lacked the ability or resources to project their power over such a vast distance. It could be considered inevitable that they would not have been able to hold the territory under any set of circumstances for very much longer.

Furthermore, the land was only ceded upon Mexico’s signing of a treaty, under which the US also gave a large sum of money in exchange for the land.

Lastly, are you really bemoaning that the American Southwest was developed by the US rather than Mexico? Can you even imagine what that whole quadrant of our country would be like if it had developed the same way the rest of northwestern Mexico had developed? Under US rule, that region has produced a significant amount of good and value for the country and the world.

So, like, what’s even your point? That people coming from Latin America should be allowed to ignore our laws, enter illegally, and stay forever? Not sure how that would even make sense.

Makes about as much sense as panning for gold, doesn’t it?

Wow Zest! I hope you back is ok from all those gyrations attempting to justify illegal activities by the US military.

Obviously, stealing Mexico’s land was against the Mexican law at the time.

The war ended with a treaty and a payment to the government of Mexico. This is pretty typical of how borders were traditionally established.

Apple:

Mexico had already lost its northern land to the country and then the state of Deseret (from SLC to LA & SD). The Marines simply changed it from a country to a US state (for a little while at least).

Yeah, I guess a guy who just walked 1,000 miles to get here w/nothing but the clothes on his back and can’t speak English is gonna take your job!

I remember when all those illegals crashed the world economy at the end of President Cheney’s administration in 2008. Oh never mind, that was a bunch of white Republican men in DC, NY, etc.

You might want to lose the scape-goating and perhaps figure out who really is screwing over the average American. Sheesh….

Sarcasm should be done with a /s, lest we think that you are complaining about losing 1-2% on an asset class that gained 40% in a couple years. Commenting on who is and isn’t civilized is outright lazy.

P

No one cares about your home equity.

Every homeowner cares about their home equity. It’s the foundation of the argument for affordable housing and every program to increase home ownership. It cannot be the “best wealth-building” opportunity for Americans without appreciation.

You decide if this is sarcasm.

Los Angeles is getting closer and closer to hitting the June ’22 peak again. Come spring, it almost certainly will. So you’ll be able to add that to your list of “some metros” that saw new highs.

Depending on the results of the upcoming Fall election, RE could take a real beating here in the DC metro area. I heard that Trump, if elected, will be firing 50,000 federal workers, many of them owning houses in this area. They will be forced to sell, pack their bags and look for a job elsewhere. Already, I see new home developments, especially those farther out sitting with no buyers anywhere in sight. Even massive buydowns, and perks are not working to move these homes. All you see are developer’s RE signs cluttering up the entrances to these developments. I wouldn’t be surprised to see some developers going belly up and leaving houses half completed, and walking away.

😂He’ll be doing that right after he builds that wall.

I thought this was a blog post about housing prices, not your irrational, personal animus against a particular human being.

This is the one website where I can get high quality financial news and no politics. Let’s keep it that way.

Amen, to the diety of your choice…

I agree with you about keeping politics out of the comments on this blog. Unfortunately I am seeing more and more of this type of comment. If tolerated it leads to an overall degeneration in the level of discourse.

If someone like JFK jr got elected by some fluke in the electoral college you would see the defense budget slashed by 50%. That would be a good thing in my book. That would decimate properties in Northern Virgina where most of the high paying jobs are in defense related industries. Contractors there have been sucking on the Federal government’s teat for year after year. I was there and saw it 1st hand. You CAN’T take politics completely out of the equation when forecasting housing prices especially in areas like DC where most of the jobs are directly or indirectly influenced by the party in power in the executive and congressional branches of government. Those who do will do so out of their own peril. I wouldn’t touch properties in Northern Virginia with a 10 foot telephone. Meanwhile properties in downtown DC are holding up fairly well, even with the high crime rate. The MLS data supports this.

Expand your view. /s

Bombs are good business and a job creator. The markup on manufacturing them is huge, and when used to destroy property rather than shoot down a $20, 000 drones. The million-dollar missile has a great return on reconstruction and material investments.

Zorg/Gary Oldman has a great monologue about this very thing in Fifth Element. Cut short by a grape

Different month, same story… prices down out West, up in the East.

Id wager it trends closely with population shift in the post-wfh world.

Surplus of sellers relative to buyers in the west lets the current market dynamics do their thing, surplus of buyers relative to sellers (even if both groups numbers are depressed by high rates) drives the bubble upward.

With all of your splendid bubble reports across the years you made me very curious as to what Case Schiller has to offer and this morning I started digging into their numbers and they’re fascinating to say the least. What struck me most were the middle and low tier numbers, which have gone up considerably in the San Diego metro, while, unsurprisingly, the high tier has definitely dropped. The middle and low tier numbers definitely support what I’ve been seeing in the regular neighborhoods (10% up YoY and 2.5-3% above 2022 highs using seasonally adjusted numbers). Despite looking for what they consider cutoffs for each tier I couldn’t find any info; do you know what they are? I’m curious why they provide numbers in seasonally and non seasonally adjusted, why not use just the non seasonally like you use to keep it from getting confusing.

All that being said, I think there will be a lot of surprised folks when you post the February and March most splendid reports for San Diego, and maybe even Los Angeles.

How they do the price tiers divisions is somewhat complicated but makes sense. It’s described in the methodology. Search the (37-page) document for: tier

https://www.spglobal.com/spdji/en/documents/methodologies/methodology-sp-corelogic-cs-home-price-indices.pdf

I just read an article in the San Diego Union Tribune that referenced the Case Schiller numbers and indicated that the San Diego metro area includes the entire county. Is there an index for just the city of San Diego? I read the tier stuff and it’s a pretty heavy read for a non stats guy like me.

“San Diego” = the San Diego-Carlsbad-San Marcos Metropolitan Statistical Area (I think this is the entire county of San Diego).

I don’t think S&P releases data on subdivisions of the metros, such as a city.

That makes sense. Higher interest rates shove what would have been higher tier buyers into the lower tiers. Everybody’s buying power just dropped 35% or so.

Everybody’s “borrowing power” dropped 35%.

Not the same as buying power.

With talf 2, or tarp3, bank term programs, and other possibilities , and all those new tools in the feds ever expanding tool box; what could go wrong? Markets up each day, It’s like everyday is a new epiphany. What a country. Since the whole thing works so well for us in the US, why on earth don’t all countries follow this exquisite model? And say it proud and clear; we are simply following the US model! Money for nuthin and the chics for free!

Real Estate prices obviously are not driven by physical reality; the increases in the southwest are astounding considering the almost biblical nature of the cities environments.

Tens of millions drink out of one relatively small Colorado River, Las Vegas drilling a pipe into the bottom of Lake Mead to get the last like a bathtub drain, Lake Powell that never will be refilled. There is water, probably paleowater from the last ice age in Northern Nevada that is desired to be pumped to Las Vegas like a non renewable resource (in anything less than geologic time).

This real estate is definitely for speculation as future archeologists are going to scratch their heads on this one.

It’s the bad neighborhoods bringing the prices down. It’s very expensive to own a SFH in a somewhat decent neighborhood plus the 10k+ tax bills

The metropolitan area of Las Vegas is one of the most water efficient cities in the world.

https://thenevadaindependent.com/article/las-vegas-we-have-a-problem

Yes, there is a huge water shortage problem in most of the southwest U.S., but it isn’t because of Las Vegas. When you are staying on a hotel on the strip and you take an extra long shower, you are not wasting a drop because 100% of all indoor used water is recycled back into Lake Mead.

JimL – still, most of that Lake Mead water must come from somewhere else (and, reckon those downstream are not overly impressed with LV’s H2O efficiency, admirable as that is, given the numerous additional straws in the glass…).

may we all find a better day.

@wolf. This got double posted. Was meant as a reply to another comment above. Feel free to delete.

It looks as though the upcoming trough in February will be significantly above last February’s trough for many metros. So this Spring’s price ramp will begin on a much higher base than last year. At best this suggests a very minimal correction in ’24, or (maybe more likely?) a new peak by next summer. If popping this ludicrous bubble is a Fed goal, they are nowhere near reaching it.

You’ll notice something about the housing bubble list champion, Miami … Miami has beautiful weather.

When I lived there for a while over winter, I was impressed with its beaches and its warm subtropical winds. The days of Northern cities being overstretched by housing booms may be permanently over. As long as there’s room to build one more condo in the Sun Belt, that will take precedence over anything Indiana or Minnesota can muster.

Yeah Miami is great over the winter. Many people HATE the hot, humid summers which last five months.

Untakeable in summer.

The inhospitable climate of Minnesota is a feature, not a bug. You need good reasons to stay. I like being surrounded by people who have good reasons to stay. My ancestors arrived here when it was still Louisiana 😜

Not surprised with the Florida numbers. People keep moving here driving up demand still. Wages are up so prices are up. More money to be able to bid up home prices. It was slow over the holidays as expected and recently picked back up. As long as our population keeps going up and wages keep going up so will home prices.

Where are you seeing people still moving to Florida? After the 2021-2022 boom, I’m not seeing anything beyond what you see in a normal year (say 2016 or 2017)

I’m looking at FRED data series FLPOP. Up 365k in 2023, 415k in 2022, 239k in 2021, 99k in 2020, 237k in 2019, 278k in 2018, 350k in 2017, 408k in 2016, 365k in 2015, 302k in 2014, 250k in 2013, 246k in 2012, and 210k in 2011. It has more data going back, but I didn’t feel like posting more. Finite amount of space for more people that keep coming in while NY and CA losing people.

That proves my point. People have been moving to Florida in mass numbers since the 1950s. 2021 and 2022 were slightly elevated, but not crazily more than some other years you posted.

My point is that the real estate agent meme “Everyone is moving to Florida and all of the banks and hedge funds are relocating meaning that housing prices will continue to double every few years” is not supported by facts.

It’s interesting. People moving our of CA to FL. But home prices in CA are not going down in meaningful way.

I was reading that San Diego would be losing lot of people in next 10 years due to migration.

Youre kidding right? How about EVERYWHERE

Since the year 2000 the average population growth in Florida was 819… PER DAY. It was never negative for any of those 24 years and is currently 1,000 per day – 365,000 per year.

Do your research before saying ignorant stuff

No need to be an ass. My point was clear, that where is the evidence that people are moving to Florida in greater numbers (what they called the work from home/COVID shift) than in the past. There was that in 2021 and 2022, but it appears to have basically returned to the normal trends.

Z33

Florida is getting overcrowded, and South Florida is getting hotter than ever. Also, given the fact that insurance rates are skyrocketing, and insurance companies are pulling out of the state because they can’t get re-insurance, I would think hard about investing in a home down there right now. Hurricanes are now more intense as result of the warm water temperatures in the gulf stream and the gulf of Mexico. Insurance companies hire Climatologists to do risk analysis of the probability of a major hurricane strike in the near future.

Swamp Creature-

“Insurance companies hire Climatologists to do risk analysis of the probability of a major hurricane strike in the near future.“

That must be about as straight forward as predicting the level and shape of the yield curve 18 months hence.

I believe I’ll pass on that wager…

Not even close to the same thing.

The difference between predicting insurance markets versus interest rate futures is that insurance actuaries have a history to observe that has predictive power.

Insurance market history is far more predictive that interest rate history.

JimL-

How about predicting weather events? That was my point.

Respectfully

John H

I have a Masters degree in Meteorology. I studied Climatology in graduate school. Some of the jobs after graduation involved working for insurance companies doing long range climate predictions and weather cycles sometimes 2 or 3 years in advance, essentially doing risk analysis. Warm water temperatures in the gulf (3 deg above normal) are associated with intensification of tropical storms and hurricanes. You can’t ignore the science.

Swamp Creature-

Point taken, thanks. No offense intended.

I am confused though, by your reference in your original comment to hurricane strikes in the “near future,” vs your reference in your comment above to “doing long range climate predictions and weather cycles sometimes 2 or 3 years in advance”.

The ability to accurately predict the future course of weather and the ability of Fed PhDs to accurately predict future interest rate constellations is questionable, in my mind. To me it’s less about science than about man’s longer-range predictive abilities when infinitely complex systems are involved.

I am, however, very interested in compelling science regarding either.

Respectfully.

It’s not really very complex.

The earth is getting hotter.

That means the oceans are getting hotter.

Hot water is the fuel of powerful hurricanes.

Hot water is what led to Hurricane Otis increasing it’s wind speeds by over 100MPH in less than 24 hrs. That was the first time that’s happened in recorded meteorology.

So you go to bed at 10PM expecting 25-30MPH winds and by 8PM the next night, you’re facing a Cat 5 Hurricane with 165 MPH winds.

Google “insurance companies leaving FL”

Swamp, It hasn’t been my experience that people put this much research into choosing where to move. It’s most often a “what could I do” kind of choice based on jobs, lifestyle tier, or long-term plan. Retirees have forever been moving to warmer climates, Florida, Arizona, and Texas being popular and even more so with politics weighing on choices.

I’ve lived in FL most of my life. Had relatives lose everything to hurricanes (Hurricane Andrew) and been through many hurricanes myself. They are not as terrifying as the news would make you believe and it hasn’t stopped me from wanting to live here. If anything, the only weather events that happen here that cause some concern are tornadoes as you don’t have time for preparation and they are very destructive at times (I’ve lived in Alabama a few years and seen what they do there and are more frequent there).

Z33

“They are not as terrifying as the news would make you believe”

I personally toured the damage after hurricane Andrew in 1993, one year after it hit in 1992. Total devastation in a 20 miles stretch from south of Miami to homestead AFB. 50 people killed. I went back in 1995 to the same area. Still had not recovered from the hurricane. I interviewed survivors of the hurricane for a term paper my kid submitted in middle school. It was terrifying for those who lived there and almost died. I you want to buy a home there, be my guest.

Swamp, we know here in FL they can be devastating, but that it’s low chance to be directly hit by a category 5. Even more we know that being inland (like Orlando where I am), less chance of damage. It’s been decades since Andrew and it’s not a monthly or even annual thing that a cat 5 direct hit happens. Sure, if you want 0% risk move to the Midwest to avoid a hurricane and its effect, but for those of us that live here it is only temporary (50 years or less from purchase of house to death). We’re not buying a house to live for thousands of years. And we get enough warning to drive out of the area if needed.

Z33, additionally, houses built correctly under post-Andrew standards withstand category 5 storms just fine. Look at the pictures from Ian. The new houses with impact glass and garage doors and properly tethered roofs were just fine. They may have had some debris in the yards, but the houses were intact, even from 145 mph.

It’s the crap boxes built in the 60s and 70s that blew away.

I wouldn’t buy anything old in Florida for sure, but the concept of a hurricane in a new house doesn’t terrify me.

…and sea levels continue to rise with the added bonus of a lot of Karst geology (…not throwing rocks, here, live minutes away from the San Andreas Fault, meself…).

may we all find a better day.

Seems manifest destiny is near completion as all the California money has officially made it to the shitty east coast cities.

i live in Carlsbad, ca and the, 1800 SqFt , cosmetic fixer, house down the street was on the market last month for $ 1.3 million and was bid up & sold for 1.5 million . After new windows, roof , counter tops, paint , it is now on the market for $2.3 million with no bites. Another friend has lived in the Marabella apartments for 3 years that had a 2 year waiting list when he moved in. Marabella now has 12 vacancies and has renewed his lease with no increases. Also, there are many for rent signs . I’ve seen many for rent signs before but after a pause thing keep going up. We shall see!!

I live in San Diego and around me I see lots of multifamily homes being built in.

Lots of for lease signs as well.

$2.3 mil – Let me guess – 1970’s era single story ranch with new finishes just a smidge above low budget flipper grade on a decent sized lot with an “ocean view” if you stand on the roof, close one eye and squint and look through an 18 inch sliver of daylight between the neighbor’s shed and a telephone pole.

You gotta love San Diego.

you are correct Falcon except for 1960’s era . everything else is spot on

Polk was all about real estate acquisitions.

Howdy Folks. Looks like HB2 will deflate slower than HB1??? I hope it hisses for a decade instead of popping. A bubble is a bubble and they sure created a big one this time……..

Everything I’m seeing in Metro North Boston supports that chart.

Right now the housing market – in the dead of winter – looks like it did in the Summer of 2021 – i.e.

– Virtually nothing on the market

– What *is* on the market isn’t being handled by realtors

– Multiple investment buyers in competition with one another. Bidding wars that would taken 4-6 weeks to play out – are resolving in just a couple of days.

Last week I had no fewer than five people ring my doorbell representing groups interested in purchasing my house.

Ugh. Boston metro is killing me. Spoke to a broker who insisted it’s not Chinese money propping up the market, and yet every other rental we’re looking at ends up being a Chinese buyer who bought in the last few months and is renting it out for a year before knocking it down (local regulations are a pain until you’ve owned for a year. To stop developers, I suppose, but in practice of course they just rent it out instead) With listings so far down, it doesn’t take much overseas demand to heavily distort the market.

And just did a speculative drive by of a local house that listed for sale on Monday. 6 cars pulled up just while we were there. Apparently the broker has had 200 calls about the place, already has multiple offers, she’s there all day today and tomorrow for viewings even though it’s not an open house and none was advertised, and the offer deadline is 10am Friday. It’s brutal here.

Thank you for your report.

I am at a lost why would people live in Boston.

I was there decades ago and hated the weather and big city living.

My little brain fails to comprehend.

May be I am too spoilt and getting older.

Boston metro, rather than Boston.

However, I agree. My wife’s decision, not mine. I think it’s bonkers to live here when we don’t have to.

I will be interested to see what it looks like by Spring of next year as possibly a couple of rate cuts by then. Perhaps a lot of new housing coming online as well. Our downtown(Sacramento ) is transforming and housing is going up everywhere. Given most of the downtown was supported by government employees who are almost are all teleworking and will likely continue, the areas that can put up small multiunits are going up everywhere. Will be interesting to see if there is enough demand for the price of what you have to pay versus what you get.

Howdy Glen. Should the FED pull a Greenspan, ( raise and lower , lower, raise lower ) , keep an eye out for inflation too. Gonna be fun for some this time around……….

Here’s the takeaway today.

There are only two times in your life when you can make a lot of money.

The first is during good times; the second is during bad times. Prepare yourself accordingly.

Speaking of bad times, New York Community Bank is in trouble. They actually took some of Signature Bank’s assets. Today its stock is down 36%. Other banks eating eating it are the usual suspects, Valley National, and Western Alliance.

The bad times are the best, it’s were you can 4x to 10x your wealth when you have the opportunity and capital available.

Success is where preparation and opportunity meet!

Since the most likely rate move by the fed is down sometime in the second half of 2024 (barring a huge uptick in inflation), the bubble had better pop soon, because I see lot more hot air headed in the direction of housing bubble 2.

There are more folks waiting for lower interest rates to buy a home than there are to sell. And if they’re waiting for lower rates to sell, it’s because after they sell, they plan to buy something else.

That’s not a formula for the crash everyone is wishing for.

Very well said CCCB, the tide is turning and the next leg up in housing is in the making as we speak. Like you said, that can change if inflation kicks up again, but I agree that it’s more likely that rates drop. If we are wrong then we will likely get a see-saw pattern for a while.

I live in a booming area in the rural Red South where everyone seems to want to move, whether from CA, FL, or NY. In yesterday’s paper, there was a listing for a rare spec home—an open floorplan 2/2 with 1100 sq ft for $399K.

Like many desirable places in the South, $400K is your bottom for anything of decent quality that is liveable, and this particular home will sell at list price. I feel bad for working-class families because, like many other places, if they didn’t buy before 2020, they are likely priced out.

Which is exactly the fallacy that you can print tons of money just to prop up the bond or stock markets, and have the cash “remain” there.

You can’t. Once you print money, the Cantillon effect guarantees that you lose control over where that cash went.

tons of cash was printed, and most went to the top 5%. Those 5% are using that cash to not bid up the prices of all sorts of things, including housing in ruralish areas.

It’s interesting to see the difference between West Coast and East Coast in the increases/decreases. I lived in Seattle for a short time 15 years ago and now live in the Boston area. There’s not much land for building in either, both are densely populated, a similar make up of people with professional jobs making decent money. And yet Boston keeps going higher and higher and Seattle has been in correction mode for awhile now. This trend seems to have been going on for months. Will the Boston bubble will pop harder when (if??) it does?