The BLS tweaked the methodology after letting it go haywire for two years. This whole fiasco should be a career-ender for the top of the BLS.

By Wolf Richter for WOLF STREET.

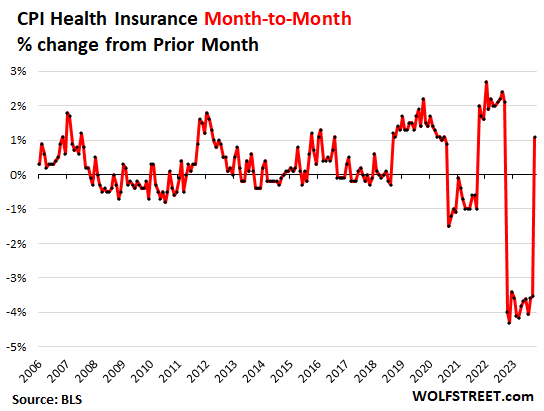

October was the first month in the Consumer Price Index without the monthly mega-push-down adjustments to the health insurance CPI, which started with the October CPI in 2022 and went for 12 months through September this year, thereby ridiculing actual health insurance expenses that continued to soar. It downward-distorted CPI, core CPI, and most of all, core Services CPI to an ever-increasing extent month after month for 12 months through September.

Conversely, in the 12 months through October 2022, the health insurance CPI increases had been overstated, but to a far smaller extent.

So in today’s CPI data — my discussion: Beneath the Skin of CPI Inflation — the Bureau of Labor Statistics tweaked the odious health insurance CPI metric in a few ways, as expected, and on a month-to-month basis, the health insurance CPI jumped 1.1%.

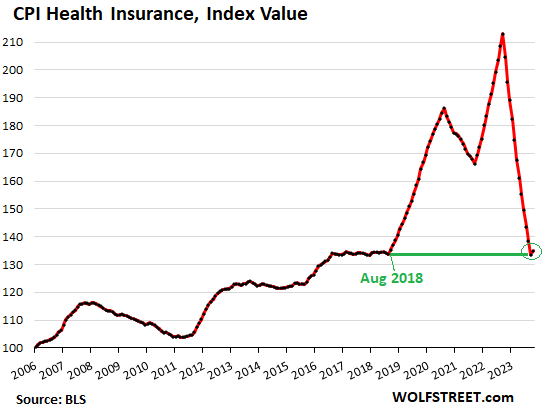

But this 1.1% jump came after 12 months in a row of month-to-month plunges of about 4% per month, ultimately a 37% collapse in the health insurance CPI in 12 months through September, that took the health insurance CPI back to where it had been in August 2018, even though health insurance expenses have skyrocketed. And it’s from this August 2018 basis that the health insurance CPI increased by 1.1%.

The increases going forward may get larger, going from +1.1% for October to perhaps +2% in November and +3% in December because the tweaked version of the index now includes “smoothening” (via a moving average) which delays the impact of the positive values on the current index (more on this in a moment).

The year-over-year change is still hugely distorted because the 1.1% increase in October was from the base that had been knocked back to August 2018 levels.

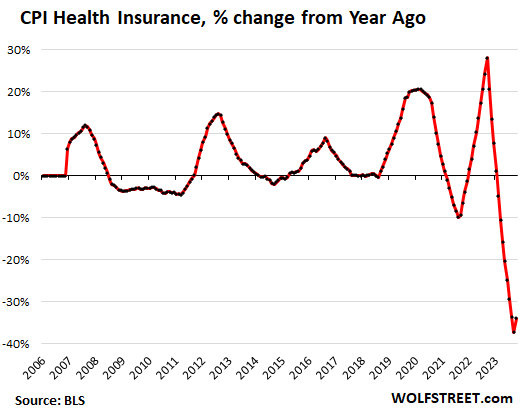

So today’s 1.1% month-to-month increase reduced the year-over-year collapse from -37% in September to -34% in October. Each month going forward, the year-over-year collapse will get smaller.

This chart shows the health insurance CPI as index values, which were knocked back to August 2018, and just ticked up a smidgen from there today – that little hook at the bottom, which was today’s 1.1% jump, after the 37% collapse. The BLS has turned the health insurance CPI into chickenshit:

On a year-over-year basis, the health insurance CPI is now down 34% (see the little hook at the bottom of the chart), after having been down 37% in September. Each month going forward, it will be down less on a year-over-year basis.

After the model blew up.

This ignominious fiasco of an important metric within the CPI data occurred because the model that the BLS used to estimate the health insurance CPI – the “retained earnings method” – after working reasonably well for years, blew up amid the distortions and money flows during the pandemic.

Rather than coming up with an alternative estimate right away, back in 2021 when these issues became apparent, the BLS let this fiasco run for two years, overestimating by a moderate amount health insurance inflation in 2022, and causing health insurance CPI to just collapse over the past 12 months through September 2023, back to 2018 levels.

So the BLS finally decided to tweak the methodology of the index, after letting the collapse run the entire 12 months. It tweaked the methodology based on recommendations of the National Academies of Science, Engineering, and Medicine, Committee on National Statistics (CNSTAT), it said.

The tweaked version: increases to get larger over the next few months.

But it only tweaked the catastrophic old version, and this new version still relies on the “retained earnings method” that exploded during the pandemic. The BLS explains its tweaked methodology here.

The two main tweaks are:

- The index is now “smoothened” (using a moving average)

- The retained-earnings data is included twice a year, rather than just once a year.

The smoothening (using a moving average) has the effect that the impact of the actual increases are delayed. The 1.1% month-to-month increase for October would then get larger for November, perhaps to +2%, and get larger again for December, perhaps to +3%, as the moving average drops the prior negative data points and picks up the new positive data points.

Nevertheless, the new version uses the chickenshit data through September as the base.

Fire everyone.

The BLS should have come up with a different way of estimating health insurance CPI starting in 2021 when it became apparent that it was going haywire. And then it should have adjusted backwards the entire data series, as it does when other adjustments are made. But no.

The metric remains a fiasco, having now contributed to a significant understatement of core CPI and even more so of core services CPI for the past 12 months, and going forward, on a year-over-year basis for the next 12 months.

All supervisory employees and top-level management at the BLS who had anything to do with the health insurance CPI since 2020, the people that tolerated the old version for so long and that approved the tweaks of the new version, should be fired. This kind of fiasco should be a career-ender for higher-level folks at the BLS.

And here is my more temperate discussion of the CPI inflation data released today: Beneath the Skin of CPI Inflation

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Would be a good start

Health insurance inflation is also hiding in its terms and because more HMOs covertly pressure doctors not to test and thereby, find medical conditions to treat, particularly for older, gullible HMO consumers. That is how, for years, we have gotten the worst and most expensive health care (insurer-caused) among developed countries. See e.g., 2023 Ars technica article.

We are # 1 baby! #1 most expensive! #1 worst! Like Los Angeles courts (where a certain film producer could safely rape dozens of women for decades knowing those bribed judges would never punish him), we achieved that because the US Congress consists of the best that money can buy: oil money, banker money, tax evaders’ money, health insurance money, etc., they take it all!

You have to shop around for doctors. Some will try to argue you out of tests or medicine. Antibiotics are a tell. I have good doctors now, but when veterinarians tell me they don’t recommend antibiotics because of possible increased germ resistance in the future, I just point to the tons of antibiotics given to cows and chickens. A couple of pills for my dog is not going to destroy the world.

Just don’t put up with crap from people who were indoctrinated and not taught.

It is not just doctors, but HMOs and corruption: read Forbes “ACA ‘savings’: paying doctors and hospitals bonuses to deny care to patients.” Remember, the ACA was passed with negotiations to get insurers’ support.

Most articles and news about suppression of care have “coincidentally” become inaccessible. However, read on CNN “These bonuses for doctors create an immoral conflict.” An elderly relative died recently because the insurer declined to do tests warranted by symptoms that would then have required expensive treatment. Their insurer used “grief” counselors to persuade the conservative family not to sue!

JFC.

I knew they would “find a way” to adjust again.

“Trust us”

Good grief. You need to understand that all science is about continuous improvement. You start with something, test it, and refine it. When conditions change, the model must too. It takes time and it never stops.

Complaining that they didn’t get it perfect from the start is pure ignorance in how science works.

And guess what: it’s still not perfect and it will change again.

Be happy that it IS changing and not some stuck-in-the mud curmudgeon that thinks change is bad.

There’s science and there’s politics and there’s greed.

When there are 10 sigma discrepancies, the models and estimates are not science.

joe2 – you left out ‘religion’…

may we all find a better day.

Thanks Wolf for keeping me informed even if it is above my pay grade and depresses me.

“and going forward, on a year-over-year basis for the next 12 months.” You mean it will increase CPI & Core CPI readings over the next 12 months, or continue to suppress it? I take it as the former.

On a year-over-year basis, the push-down will push down less hard each month.

On a month-to-month basis, it will actually push up the CPIs.

Admittedly I am cynical but the Government has every desire to keep markets high and yields low while doing it’s best to “fight” inflation. This potentially evident in an election year which is a heavier influencer than most things because it directly impacts them. Clearly spending will not be put in check, revenues likely won’t increase dramatically and the deficit will continue to rise. That doesn’t seem relevant however as plenty of ways to manipulate numbers and more importantly perceptions. My only concern is really where and how much to diversify as clearly things aren’t entirely rational. The S&P could break 5000 or drop to 3500 or lower. Not panicking or anything but would like to be able to make rational decisions. I could research and think it out but dart board after 12 beers probably still more accurate.

Glen-

“ I could research and think it out but dart board after 12 beers probably still more accurate. “

You’ll need to invest in some chimps… to augment the dartboard accuracy. No beers for the lesser primates, though.

Chimps throwing darts after 12 beers would be interesting, but you’d probably want to take cover.

No argument with regard to firing those at BLS who are responsible for the CPI chickenshit, but what should be done with those that use the chickenshit in support of actual policy decisions?

The Fed uses the PCE price index, which figures health insurance much more broadly and doesn’t have that issue.

Then I wonder who exactly is the consumer for the CPI…and how many other bespoke inflation measures the G puts out altogether…

Ditto for essentially every other G supplied metric.

We know for certain the “unemployment rate” and “money supply” aspire to be Baskin Robbins.

I’m not against customized, precision metrics.

But it is very common for the G to retail its favored “statistical narrative” via the de facto state MSM.

It was much worse in the pre-internet “dark age” days…but how to generate critical mass of public knowledge in today’s fractured media environment?

Are you fooling yourself to fit your narrative? Fine with me.

Bureaucrats cooked the books again and now we have stock market euphoria.

Nobody could have possibly seen this coming.

Thank goodness for Citizens United and the freedom of speech!

Look at the pictures. The health insurance CPI was +28% in Sep 2022.… look at the trends in those pictures, this is a model that went totally haywire, that’s what they’re telling you. It went haywire in 2020. It went haywire in BOTH directions, and they didn’t do anything about it.

In control systems, we call that “ringing” and it can be a dangerous condition. Adding “dampening” (aka smoothening) is a standard way to deal with it.

Whether some added dampening is sufficient depends on a lot of factors. Sometimes it is and sometimes you have to start from scratch, which of course means an entirely new set of problems.

I dont think the healthcare adjustments are the only things fishy with the CPI calculations. Hedonic adjustments are real questionable, after all, it is natural for products to get better over time. The actual cost of living increases has far exceeded the stated inflation rate.

You will own nothing and be happier…or else!

Was this change announced before the new numbers can out today? If not I have feeling some people made some good money today if they know before the numbers did come out.

Yes, it was announced quite a while ago. I read the BLS discussion of it quite a while ago, maybe before the last CPI came out a month ago.

I discussed it a little in the comments too back then.

This makes me wonder about the validity of all government data. Well, I always have. After all, the data are generated by government workers. No real oversight, no competition, plenty of room for error and corruption. Some government-generated data can be supported (or not) by private sector surveys, and that is the most reliable if they coincide.

If the government agencies would not change their definitions and methods, at least we could look at changes over time, and ignore the levels. For example, if they always undercount the variable X the same way and always define X the same way, we can get useful information about month-to-month changes in X that might reflect reality. But they do change their definitions and methods, as shown by Wolf above.

The CPI data is generally pretty good. That why this fiasco pisses me off so much. They should have caught and fixed this fiasco up back in 2021 when they saw right in front of them that their model was blowing. Until 2020, it worked pretty well.

Any data coming out of the govt is completely politicized. They create the outcomes they want distorting the data they have. In their defense, they learned this from Wall Street, where the model de jour creates the chart you want/need to show the clients.

Those who produce the outcome, make it align with the current agenda of the current administration. Give me a data point and I will give you a model to prove X or Y or Z.

Look at the pictures. The health insurance CPI was +28% in Sep 2022.… look at the trends in those pictures, this is a model that went totally haywire, that’s what they’re telling you. It went haywire in 2020, in BOTH directions, and they didn’t do anything about it.

The system broke down and you can’t explain that by smoothing over the timeline. They should have just shown the break and explained how and why they propped up the system during this Black Swan Period. That would have been a more honest reflection than pretending a very bad thing didn’t happen and it was just a bad dip in a normal cyclical pattern.

They ignored a distortion in the system by creating another distortion in the data. Sometimes things break and they have to be restarted by other means. Just tell the truth. We all know we will all pay for this anyway.

Petunia,

I agree. They should have scuttled this method when they first saw the model was blowing up in 2021. They should have come up with a new method. The method is madness.

Wolf, what are the annualized impacts on inflation measures resulting from these health insurance CPI methods? i.e. “health insurance CPI is now down 34%”, but what impact does this have on the overall CPI measure, both over the past couple of years and going forward?

The good thing is that in CPI, when a product index falls, it’s assumed that people buy the same amount of that product, but pay less for that amount of product, so that less of their total spending goes into this product, and more of their spending goes into other products.

So the WEIGHT of that declining index within CPI falls as the index goes down. CPI is set up that way (contrary to what you read on ZH).

In Nov 2021, the weight of health insurance CPI was 1.1% of total CPI; today, it’s down to 0.52% — the weight has dropped by over half, because the index itself has plunged so much.

CPI method assumes that consumers are still getting the same amount of health insurance but pay a whole lot less for it, and therefore less of their spending goes into it. And so the weight of the health insurance index fell in overall CPI.

Meaning the health insurance CPI has half the impact today than it had in Nov 2021.

It also means that those weights begin to increase as the health insurance CPI climbs higher.

Those two combined — the increasing health insurance CPI and the increasing weight of it — will have a good-sized impact as they build over the next 12 months.

It’s 0.525% of the CPI basket, as you can see in the detailed expenditures table:

https://www.bls.gov/news.release/cpi.t02.htm

So if the monthly CPI change is 0.200% (2.4% annualized) and included a 1% monthly change in health insurance, it would become 0.205% (2.46% annualized) if health insurance was changed to 2% or 0.211% (2.53% annualized) if it was changed to 3%

Apologize in advance if this is an ignorant question. Is there any legitimate non-government source for more realistic data?

There are lots of sources for less realistic to outright stupid inflation indices. Shadowstats is in the “stupid” category.

The government has other inflation indices, include the PCE price index which we discuss here a lot and which doesn’t have that problem.

Reporter: “Mr. Commissioner, how did the BLS fail to address these huge discrepancies when they knew the political and economic ramifications would be so dire?”

Commissioner: “Let’s just say it moved me… TO A BIGGER HOUSE! Oops.. I said the quiet part loud and the loud part quiet.”

“should be fired”

This assumes they were hired based on competency and not for other reasons: corruption, favoratism, government quotas, nepotism.

Nah, bureaucrats did that, not political appointees. Lots of things go off the rails, see Boeing’s 737Max, and they pick up momentum and no one stops them until it’s too late.

The government bureaucrats I have had contact with were pretty good and fairly hard-working, but when things go down the wrong track, they’re not getting stopped, usually until it’s too late.

Big companies in the private sector are the same, see Boeing.

“No real oversight, no competition, plenty of room for error” to quote myself from above.

In my experience, government bureaucrats fall into two categories. They’re either smart and hardworking, and really take their jobs seriously. The other types are there for the smooth 9-4 jobs with a pension and 35 days of vacation a year.

I’ve encountered very little in between. The problem is that, while in the private sector, you can get away with being the latter type for a while before people wise up to it, in government, you can get away with it FOREVER.

Apologies, my comment wasn’t directed at you, must have clicked reply on accident.

“This kind of fiasco should be a career-ender for higher-level folks at the BLS.”

Everyone will be promoted. They will “fail up” to a cushy position at Harvard and teach the next crop of leaders.

I’m sure they hired a small team of experienced consultants from McK, told them what they wanted to see and asked them to tailor the methodology to the desired output and lay it out in their recommendation whitepaper. This way they would have something to cover their sitting/beating surfaces in case something goes wrong.

I think this was the standard MO for entities like BLS all around the world.

“ Rather than pricing the full premium of health insurance plans, the CPI prices the services provided by the health insurer measured by the portion of the total premium that isn’t used to indirectly purchase medical goods and services. The premiums minus benefits spending is known as the retained earnings.”

Does it matter if someone is using their insurance or not to know the price is going up?

Does the housing cpi index subtract days the owner is away for the weekend?

Retained earnings – so they have increased 30% since 2006 according to CPI? UNH has gone from $40 to $540 in that period.

No that’s not the calculation. It’s based on a formula that is a lot more complex and figures the difference between retained earnings and premiums collected, on the theory that this was actually the healthcare services that were paid for and consumed, that were being insured. I linked the methodology in the text, go look at it.

I’m trying to understand it. from the link:

“Instead, BLS defines the price of these insurance services as the ratio of retained earnings (premiums minus benefits) and real benefits (benefits adjusted for medical inflation).”

From this, it sounds like their health insurance CPI is calculated from a fraction – if both the retained earnings (numerator) and benefits(denominator) go up together, the ratio stays pretty constant – which leads to a health insurance CPI number that doesn’t move much.

You gotta remember that in September 2022, the health insurance CPI was +28%

People forget that.

It seems that education and healthcare costs have been vastly understated for decades. If we look at “non-government” sources of price evaluations these costs have marched higher the fastest.

Of course there’s the issue of comparing quality (which is true regarding food supply, durable goods and any services), which subjectively seems to have an inverse relationship.

Still the “average” consumer is clueless as to what’s actually happening: fiat failure!

Made up paper is worth less than the paper and ink, just as the promises and policies that are supposed to be “backing” them.

This is so depressing. I have been anxiously awaiting today’s report for *months* and was hopeful that it would result in the 10 year treasury yield going back up. I’m attempting to buy our very first house (but moving from SF to Portland so we can afford to do so), so have a vested interest in mortgage rates increasing. Now instead, it looks like we will continue to get people bidding good houses up to insane prices that have no basis in reality vs what I was hoping for (some good houses sitting on the market and being forced to drop prices/negotiate more). To be clear, there ARE houses sitting in Portland, but not particularly desirable ones to me. Boo.

I’m so disgusted. Hate this country anymore. I need several beers tonight.

Until you are day drinking all is good!

I’ve given up trying to figure it all out. After the Covid deluge of stimulus and money for all the things. I realized why worry.

The system needs a massive reset. But frankly I’m 41 and I can see the fed and all the people involved kicking the van down the road my entire lifetime.

Not worried. Live life have a beer. Read this site and its analysis. At some point the system will buckle that much is certain whether it’s next week or in five centuries

Ive said it before and Ive said it again, this is likely the cheapest housing will ever be relative to the mortgage payment for the rest of our lives. Rates may go down, and prices will sky rocket. Rates may go up, and prices will flat line. It will *never* get cheaper.

What’s this based on?

Do you think there are enough cash buyers out there? New housing is still being built. Do you think low income immigrants are buying houses?

YoY we saw a 1.6% drop in sticker prices, with a +2% increase in mortgage payments. This means even now real prices have increased. Lowering rates means more buyers, prices will increase. Higher rates means mortgage payments go up, prices increase. Every year rent marches up 7%, the increased mortgage payments become less distant from the zero equity money hole that is renting. New starts will never keep pace with the backlog of millenials, approaching 40, still looking for their first house. Soon they will be competing for that supply with zoomers, and then even gen alpha for the unlucky ones. Housing for those low income immigrants? Bought by investors to rent to them. Prices increase.

Theres only ONE solution to lowering prices: more supply than demand. The spike in rates has certainly reduced demand, but we still have enough demand to keep real prices rising. Lower those rates and youll get more buyers. Theres no winning here. Now too you have boomers retiring and downsizing, giving up their 800k dream home. No one can afford that as a starter home, so the pool of first time buyers will now compete with cash buyers who may have to take a price cut on selling that 800k house to their own reduced pool of buyers. But the entry point for this system is and will be a bloodbath for everyone. And every year they attempt to abstain from that bloodbath, their landlord will raise rent pushing them to willingness to join the carnage.

I’ll take a stab at it

There continues to be a supply problem. The cost of materials and labor put a floor in prices of new construction, as do the interest rates on construction loans. It’s hard to see a significant price correction without a significant recession. And if we get a recession, we will likely get lower interest rates…

Perhaps the buying trends will shift to smaller / lower-priced properties.

E.g. someone with a $20k down payment and $400k budget would have bought a 3/2 house with 2000sqft, but now their buying power only gets them a 3/1 with 1200 sqft.

I don’t agree with this outlook, fwiw – just trying to understand it.

I 100% disagree with this. First, there is always a lag between increases in rates and a drop in sale prices. They don’t correct instantly. Second, lowering rates does not necessarily mean more buyers, and thus higher prices. It can mean more buyers and higher volume, but not at higher prices. Third, rent is not continuing to go up 7% every year. In my area (South Florida), it’s already dropped this year versus 2022, although 2021 and 2022 saw huge spikes.

Fourth, while there is a backlog of potential buyers, there are also a backlog of potential sellers, who are waiting to see what happens with prices. At some point, they won’t be able to hold out and will just cut their losses.

@Herpderp,

“giving up their 800k dream home. No one can afford that as a starter home”

Surely you jest. $800k is easily affordable as a starter home by a significant number of buyers. Hell, that was a starter home in the SF Bay Area *in the 1990s*, and there were plenty of buyers (I know, I was one of them, and frustrated). I think people get caught up in thinking that the masses of people out there have similar incomes/wealth to them, and it’s hard to imagine others affording that much more than they can. I know I do.

Gattopardo

That 800k dream home wouldnt be a starter home in SF. It would be 2.4 million dollar home.

“rent is not continuing to go up 7% every year”

No, but it is continuing to go up 6% every year per – see the following CPI article.

Home prices will continue to fall AND rents will continue to rise – both can be true at the same time.

“rest of our lives”

Maybe if you are 80.

The demographics are against you. As the largest older generation dies off, there will be a glut of houses. Millennials will not be able to absorb them all. This process will take decades, but some of us will still be alive.

There are more millennials than boomers. They’re also more likely to live alone.

yields might fall here for a little while, but there might be another surge in yields again next year.

why?

the treasury stopped rates from rising by issuing more short term paper.

over the past five months the reverse repo has been drained by 1.3 trillion. i believe it is under 1 trillion now. this is a primary source of liquidity for short term Treasury issuance. once the market sees this is getting close to zero, it might start to wonder who is going to buy Treasuries.

over the coming years, the ONLY buyer who can absorb enough Treasuries to keep yields low is the Fed. so if they dont move to QE, rates will be higher for longer.

Wait, how does the reverse repo provide liquidity for treasury issuance?

MMFs were stashing their cash in the RRP, but now bills yield more. Hence the flow from the RRP into bills.

I think that after the reverse repo is drained, the next big source of liquidity would be bank reserves???

I think that the crash in the US dollar today might be a whole other issue. If the dollar weakens significantly, then foreign investors will not buy as much Treasuries, because the interest they receive could easily be dwarfed by a currency loss, so they would tend to move money back into their own currency and domestic investments.

I really do wonder where the money to finance the US debt comes from if the Fed is sitting on the sidelines (and we still probably need to get rid of another 2 trillion in Treasuries and another 2.5 trillion in MBS. The goal of the Fed should be to eliminate these balances completely and only engage in QE for short time periods when there is economic stress.

You know, don’t sweat it too much. I am in the same situation as you, except up in Canada where the prices are even more ridiculous. So, while the action in the last week or so is a bit maddening, it’s driven by people who form their opinions based mostly on the last bit of data that happened to penetrate their skulls. This crowd has done this before when they thought rate hikes were done.

Things I like to keep in mind: (1) one low-ish inflation number does not mean much; (2) the bond market has been wrong so often about rate direction/future yields in the last few years it should probably be a contrarian indicator by now; (3) current mortgage rates and current prices cannot occupy the same space – one of these things is going to move faster than the other (and it’s probably not rates).

So, take your time. Prices are correcting, even if it feels glacial, and inflation is not done. I’d be shocked to see rate cuts in 2024, even from central banks that have made an art form out of being crappy at their jobs.

TEMPLE

It was done intentionally to make CPI look better. My opinion, and I’m sticking to it.

OK, I understand you’re sticking to it, but look at the pictures. The health insurance CPI was +28% in Sep 2022. look at the trends in those pictures, this is a model that went totally haywire, that’s what they’re telling you. It went haywire in 2020, and they didn’t do anything about it.

The difference is that insurance premiums for most of us actually DID go up 25%+ per year not only for 2022, but for several years prior to that too, while they went down 35%+ for exactly no one last year.

The data is what the data is. Wolf is just reporting on the data accurately. On the other hand I do agree with you. But hey, I did notice the price of a tub of maxwell house hasn’t increased much in the past 6 months. So we have that going for us.

We are at currently at the stage of permanently high prices, sadly

I think we are on the same page. I get it and am furious about it.

This is what you said, “Rather than coming up with an alternative estimate right away, back in 2021 when these issues became apparent, the BLS let this fiasco run for two years, overestimating by a moderate amount health insurance inflation in 2022, and causing health insurance CPI to just collapse over the past 12 months through September 2023, back to 2018 levels.”

That’s what I’m pissed about.

I get it went in both directions, but the fact they left it that way collapsing for the 12 months ending September 2023 was done intentionally. The rhetoric was different in 2022. Now Treasury and the rest of Yellen’s cronies are desperate. The lies and manipulation will only become worse. Also my opinion.

I can say the sun rises in the East without making numbers say nothing.

If any private corporations committed this sort of fraud routinely, they would be sued into oblivion. Rightly so.

The government however is immune to such accountability, so what does that tell you about the validity of anything they say.

Chicken shit as is well noted in the title of the article.

There are hundreds of companies that report non GAAP earnings that are pure fantasy numbers which then get broadcast by a corrupt complicit media. The stock price is pumped up and insiders sell to the clowns who manage 401ks for Joe and Jane Doe.

Government does nothing to these companies; in fact they set the example with their financial schemes. Thousands of lies and trillions of debt are the foundation of this country, and yet we are actually pretty good relative to much of the rest of the world.

Sometimes you just have to file it away and get on with living

I am confused. What caused the “haywire?” And did ‘retained earnings’ have anything to do with it? I don’t get the connection. If the rates went high, then went down (both ways apparently) what caused the swings? Some accountant didn’t add up the numbers? I doubt that.

My health insurance premiums for my family of 3 increased 18.3% this year. It has increased annually between 15-20+ % as long as I can remember. This is for a private health insurance plan with United Health I started 11 years ago when I became self employed again.

That is why I decided to self insure about 10 years ago after becoming self employed but I wouldn’t recommend it to anyone. Annual premiums, annual deductibles, co-pays, and out right denials of coverage add up to an astronomical amount of Benjamin’s for those who participate. Being self-insured forces one to stay healthy and reduce lifestyle risks. I know an endless amout of people who couldn’t care less about their own personal health so they are captive to the predatory healthcare industry. The healthcare most people receive is exceptionally risky to consume, most of which can be avoided.

Yeah, the problem with self-insuring is that health insurance is only partially insurance, and is also in large part a “group discount” mechanism, much like the AARP negotiates car rental or hotel rates for its members.

If you self-insure, you don’t get the benefit of those discounts, so the hospital will charge you $10,000 for what they only get $1,400 from Blue Cross Blue Shield for.

High deductible “catastrophic expense” only insurance is self-insuring to a degree, as you pay the first $1,500-$5,000 out of pocket, but it still provides the discounts and protections against getting very sick.

But it isn’t cheap either.

@SC, check your bills since you have probably not had a “15-20%+” increase EVERY year (an 18% increase in your health insurance for the past 11 years would have pushed a $2K/month policy over $12K/month).

@OutWest I have thought about self insuring (to save the ~$30K we pay Kaiser tell us that pretty much nothing is covered and/or does not count towards our $5K deductible).

@Einhal My wife has a friend that liked a dermatologist outside Kaiser and went to her about a year ago to have her look at something and paid her $150 for her time (~15 minutes). This year she went back and paid $175 on our credit card on her way out the door and we got a bill for $200. My wife called and said she already paid and they told her that she was billed the “insurance” rate by accident and owes another $200…

Excellent point, that is why I use health share, you get the discounts, you choose your deductible, at half the cost of insurance. But you have to be in good health to participate.

Mine is UHC as well. 22.x % increase in premiums in 2024.

And of course Politicians or the ‘Establishment’ don’t get their way in hiding Inflation from the ordinary Joe…another Conspiracy Theory proved correct

I think the correct term is plutocracy.

Look at the pictures. The health insurance CPI was +28% in Sep 2022.… look at the trends in those pictures, this is a model that went totally haywire, that’s what they’re telling you. It went haywire in 2020. It went haywire in BOTH directions, and they didn’t do anything about it.

Of course, but the timing of their “fix” is a little too convenient, in my opinion.

Exactly. The sentiment and rhetoric in early 2022 and before wasn’t worrying about inflation. The Fed was still in transitory denial mode much of that time. Sentiment changed in 2023 and now going forward. Now we have 2024, higher interest on the debt, and many other factors causing the government to conveniently manipulate (oops I meant overlook last year and come up with a more accurate lolol method going forward /s). I don’t trust this government as far as I can throw it.

They should have never used that method, and after they saw that it was blowing up in 2021, they should have scuttled it, and after they saw that it was OVERSTATING health insurance inflation in 2022, they should have scuttled it, they should have scuttled it every day along the way. And what did they do today? Tweak it.

Look, I’m not going to defend this method. The method is madness. But to insert politics into this clusterfuck just doesn’t make sense. You need to understand these huge bureaucracies, staffed with specialists. They resist political interference. In good ways and bad ways.

Indeed. This is double plus good conclusion. In unrelated news the chocolate ration was increased from 40 grams to 20 grams.

Adjust in time for 2024 and spring housing market.

In 2018 the monthly second lowest silver health insurance exchange plan in my county was $536.95. The same plan in 2023 is $661.48.

All you need to do is to track the increase in health insurance costs to employees by the largest 5 insurers over the past five years and correlate that to the percentage increase in profits by these health insurance companies over the period – you will come out with significant price increases to consumers and employers…just dishonest reporting.

Look at the pictures. The health insurance CPI was +28% in Sep 2022.… look at the trends in those pictures, this is a model that went totally haywire, that’s what they’re telling you. It went haywire in 2020. It went haywire in BOTH directions, and they didn’t do anything about it.

Wolf-

I don’t think the insurance CPI will go much higher in the months going forward due to the new methodology. I think it will be basically fixed at the current +1.1%/month for the next 6 months and likely for another 6 month after that. It’s a big swing from the -3.4% / month or so from the last year, but they’re going to take their sweet time getting it “normalized”.

I’ll follow up later with why I think this to be the case (to my understanding).

Maybe. The moving average is one thing; the six-month inclusion of the new data is the other thing. We just saw the first month of the moving average. It seems me it would phase in with each month, and the BLS in the text indicated that too.

The way I understand it, the insurance CPI isn’t actually calculated each month – no new data goes in. New insurance data (in the form of retained earnings) is only incorporated 1x / year and they just divide the result by 12 and blindly add that for 12 months until the next yearly update. That’s why each month is nearly exactly the same until it turns on a dime when the next round of data is included. It’s been about -3.3% / month for the last year, now it’ll be ~+1.1% / month going forward.

The new process brings in new data every 6 months instead of every 12, so the next inflection point won’t come for at least 6 more months. The next 5 adjustments have basically already been determined.

But now they’re going to moving average over 24mo instead of 12mo. Note what that does (especially if you’re a conspiratorial cynic) :

The 2023 data showed huge monthly deflation and that was largely because the 12 month base effect meant that each month a huge INCREASE from 2022 rolled off and created a big downward base effect.

Now, they’ve reset to 24mo, so for the next year we’re going to REPEAT the process of the 2022 data being the monthly roll-off base-effect. This means it going forward, insurance CPI will be suppressed for another 12 months as 2022 roll off again, for the second year in a row.

The effect will be smaller because it’s only 1 of 24 data points instead of 1 of 12, but it’s still going prevent the 2024 data from really correcting all the way.

We now have to wait until Nov 2024 for the 2023 data roll off creating a negative base effect and that will start adding a tailwind to data in 2025. And of course at that point, they’ll decide 24 months was a bad idea, go back to 12 months so that the 2023 deflation never hits as base-effect.

The 2022 base effect will end up affecting BOTH the 2023 data and the 2024 data.

That’s good. Healthcare is crazy expensive.

Great/spectacular work on this Wolf!

Exactly the right/strong take/tone on this fiasco…..

Thank you for following this like a hawk!!

For all those people that regularly question how these inflation statistics are calculated, this is nitro fuel on the fire for why they are very rightly suspicious/concerned/etc…

I hope this article gets a zillion hits to get the word out on the behind-the-scenes shenanigans going on with these cooked up economic numbers….

PS This type of article is exactly why I super gladly/willingly/regularly support your site financially.

I’m planning to mail in a check for $200 within the next week – as a small token of thanks/appreciation for your work – no mug needed….. :)

Thanks again Wolf! You have the best financial site I’ve found anywhere – and especially for cutting thru all the BS/etc…. And the BS is getting deeper and deeper (unfortunately!) – and smellier and smellier…….. :(

Hang in there and keep up the great work!! =)

I just put the $200 check in the mail…

I decided to try to put my frustration/energy into something more positive – i.e. supporting your work/site… =)

For some anecdotal evidence, I will provide the case of my Obamacare premiums (the lowest grade bronze plan available in my area – catastrophic coverage) In 2018 my annual premium was $4,950. Based on the letter I received last week from my insurer, my 2024 premium will be $6,986. That is a 41% increase since 2018 at an about 6% annualized rate.

This does not take into account that my deductible has increased every year and the network has gotten smaller. Perhaps I should include a negative hedonics adjustment in my calculations.

My personal opinion is that the CPI understates the most important components. The owners equivalent rent is another fiasco.

At least the OER tracks actual rents (CPI Rent) fairly closely.

I understand the OER tracks rents well. But shouldn’t it track the cost of home ownership? This is what I was getting at. Home ownership costs are one of the most important, if not the most important, costs to most people. It seems to be that it is not fairly reflected in the CPI.

If we compare the CPI OER index to the Case Shiller National index from Jan 2020 (when the CS was 100) to present, the OER index is up only 100% while the CS is up a little bit over 200% (from 100 to about 311).

The CPI tracks consumables. A home is an asset, like stocks, not a consumable. So the CPI tracks housing costs as a “services” (shelter). But it needs to track it for all people, not just renters.

The BLS does it this way. Canada does it differently, with rent on one side and direct homeownership costs, such as interest rates and home price indices, on the other. Different countries use different models.

OER tracks actual rents? My understanding is the BLS cold calls a set number of households and asks the owners what they would rent theirs home for. Like they have a clue… Why not use actual signed contract data?

1. That’s funny. I can see how you got there. Read that line again, out loud, but leave out the parenthesis, and you’ll see: “At least the OER tracks actual rents

(CPI Rent)fairly closely.”What it says is that it tracks CPI Rent (= actual rents) fairly closely.

2. “…the BLS cold calls a set number of households…”

That’s not how it works. The Census Bureau, which does this, has a huge panel of addresses – the same addresses – that it sends the survey to every six months, rotating them. Whoever lives at this address — rent or own, new or lived there for 20 years — responds to the survey, with how much they pay in rent now, or how much the house would rent for now. And the Census compares this to the info given by people at the SAME address in prior years.

UniParty in action: ” The most recent commissioner is William W. Beach, who assumed office on March 28, 2019. Before joining the BLS, Dr. Beach was Vice President for Policy Research at the Mercatus Center at George Mason University from February 2016 to March 2019″.

George Mason’s “Mercatus Center” being a Koch brutha outfit.

I always enjoy the comments. A survey of sorts would be interesting as clearly people aren’t happy. It could be anything from sold equities to move to more fixed position, to just don’t like government being “creative”, to missing the boat, to having zero predictability, to wanting government to fail and on and on.

I personally expect government and corporations to be as corrupt and self serving as possible so the CPI coming in where it is at wasn’t surprising but still wanted yields to move higher. Next spring perhaps we will see a cut or two even perhaps to help along the housing market.

The chart with index values going up and down by year is crazy. There is no way prices are moving up and down that much each year.

Statistics is their only job, and they couldn’t see the problem, or were they intentionally looking for ways to reduce the appearance of inflation?

Inflation reporting would be good fodder for a Congressional inquiry.

The health insurance CPI was +28% in Sep 2022.… look at the trends in those pictures, this is a model that went totally haywire, that’s what they’re telling you. It went haywire in 2020. It went haywire in BOTH directions, and they didn’t do anything about it.

That’s the crime: they saw it going haywire in both direction and DIDN’T DO anything about it until it was too late.

The model worked reasonably well until the pandemic.

I understand. I’m expressing amazement that the BLS couldn’t fix it, since it’s their job to be accurate, and not let things go haywire.

For the BLS to publish such obviously flawed data is inexcusable.

And for the Fed to not know is implausible as well in my mind. The board of governors is supposed to understand these things. If I am making decisions based on numbers I would want to understand the details and especially outside norms.

I agree with Glen that said: “I personally expect government and corporations to be as corrupt and self serving as possible so the CPI coming in where it is at wasn’t surprising” . I don’t have any idea of the reason but there is usually a reason when numbers don’t make sense (like when student test scores suddenly get 28% better the semester after teacher bonuses are tied to 25% better test scores). Working for the government must be super boring so sometimes I bet the numbers that don’t make sense are just a bet between workers saying “I bet you can’t report 28% and get away with it” (kind of like guys in the Air Force will say ” bet you can’t fly in the shape of a giant penis and get away with it”)…

Bureau of Labor Statistics? Try: “another federal theater of statistical absurdity”. Many of these federal departments are now just running reality show satires.

Reminds me of the day I tried to walk into the Dept of Public Health in Sacramento in May of 2020. I was denied entry due to the recently declared national health emergency. Looking in through glass face of bldg, I noticed that no one inside seemed to be wearing a mask. This is the dept that is supposed to have set state policy for such things as the mask mandates, the quarantine “lock downs” etc etc.

Just comedy.

If they can change the reporting algorithm as they the go, how does this report and this agency have any credibility?

If all numbers are manipulated, like CPI, earnings, etc, then yes, the SP500 can go only up, like 10 000 by the end of the year, or why not 20 000. Like bitcoin.

But I guess everyone is happy making money, looking the other way. All short-sellers must have been already exterminated, so that nobody complains.

But didn’t you americans have a word for that? Like, fraud?

We call it Non-GAAP earnings (Non Generally Accepted Accounting Principles). This way no one is accountable for the numbers reported by CNBC.

They made a model that gave them their desired numbers, not founded in reality. When their numbers blew up because they couldn’t stay on top of their fraud, they doubled down. They can’t hide the real inflation in their models anymore. Federal spending grew more than 56% on medical care since 2018, which is more than a 9% annual increase.

The health insurance CPI was +28% in Sep 2022.…

I met dude at my local breakfast stop who worked a long time for the BLS. We got into a heated argument over the data they released over a periodic basis. He swore by the data, and I told him the data was a pile of s$it. He didn’t like my answer, It got ugly. I had to leave without even finishing my breakfast

You must be a fun friend 😆

My big problem with CPI is the adjustments. In the past TVs didnt have remote controls, now they do. So even if the TV costs $25 more with a remote they might say it cost less after adjustment. This just isnt a realistic way to look at cost of living. Everything evolves over time and you cant buy the old product. It is the price you pay that matters, not the fact that it had some improvements over time.

This is how there is such a large wealth gap and money doesnt retain its value.

It’s really hard to not become conspiratorial about inflation metrics. Today’s CPI shows unadjusted 12 months ended medical care services at -2.0%. Meanwhile, the Kaiser Family Foundation released a survey last month showing premiums increased 7% this year alone. Kaiser themselves announced a 15% increase for patients coming in 2023.

*2024 increase

An excellent exhibition of why the government data is not trustworthy anymore.

Historically, every time the calculation changes, the whole series becomes useless/garbage. And the govt statisticians love to tinker to justify their jobs and hide reality.

Our ‘decision makers’ claim to be guided by this garbage data.

We are now in a post truth post reality ‘reality’. But reality has a nasty way of reminding us all what world we actually living in.

I get it that the methodoloy has to be changed if the model performs badly, but should then not utmost care be put into making sure that the overall price index remains reliable at least? If necessary by applying a one time adjustment?

If the health insurance index is the same today as in 2018 I very much doubt that this is what they actually achieved. It rather looks like overall price levels got permanently distorted, even if in the future the rate may now be more reliable. And whatever the problems withe the short term distortions were, if the adjustments have distorted the actual index level, that’s a much bigger statistical issue than those gyrations.

I just signed up for benefits, so here’s a data point:

Exact same family plan each year with same terms. Issued by one of the major insurers at a rate negotiated by a large(ish) national company. We pay the full premium with no contribution from the employer, so this is the full charged premiums on High Deductible plan (note the standard deductible plan has increased even more). .

2020 +8.8%

2021 +6.6%

2022 +9.1%

2023 +7.1%

2024 +2.6%

up 39.1% since 2019

In Sep 2022, the health insurance CPI was up 29% from a year earlier. It increased in one year almost as much as your five years of increases combined. Think about that!

Your average increase is about 6.3% a year. Not too bad.

Ouch. 39% increase in 4 years. Not unexpected. But hard to fit into a budget. Hope your wages also increased 40% over that time.

This is a big deal and ignored buy the press. The Fed can fix the problem themselves just by raising in Dec 0.25 and cite the change in the BLS data change as the reason . Any chance of a 0.25 hike? Based on the pop in markets and the short covering on small caps I think this maneuver was not leaked.

How is anyone supposed to interpret that CPI to make decisions if it pinballs around like that? That model is a step short of a white noise generator.

If I showed folks a trend like that in my job, and then said I had been making decisions based on it for years, I would be roasted alive. I would instantly lose all credibility. Everything I’d touched would be vetted.

If you find yourself in this situation, as much as it might suck, do the right thing. Be transparent, say that you know that your has got problems, start fixing it, and say when you think you’ll have it patched up. Everyone and their mother might be upset, but the alternative is a lot of people unwittingly relying on your bogus numbers to make critical decisions. It’s just not ethical, moral, or whatever the kids say these days. You’re wasting so many people’s time and your own time. That’s precious stuff.

Speaking of time, I should get back to work. I’ve got some “rough” estimates to make…

This is the Wolf I like to see! You’ve been too forgiving for most of this year. Between this and your recent “tightening won’t work until excess burned up” post, I think you’re back on track. :)

Quick primer on common barnyard epithets for non-native speakers of American English. I’m sure similar rules apply in all languages wherever domesticated animals defecate.

Bullshit – refers to something that is just plain wrong. Primarily used to denote ignorance on the part of the offender with no implication of malice or incompetence.

Horseshit – implies incompetence on the part of the offender. Very commonly directed at sports officials/referees by players/managers and unruly parents.

Chickenshit – implies malice on the part of the offender.

Frequently references inaction in the face of a clear and present danger.

Examples – In March of ’21 Powell stated that inflation was “transitory”. That was bullshit. When the FOMC waited another year to begin raising rates, that was horseshit. The BLS sitting on their hands while health insurance CPI went haywire was chickenshit.

You seem to know your shit. I always thought being a chickenshit was being scared to do something.

That’s “chicken.”

I tried to tell you interest rates would collapse before January 4th 2024 when I’ve got a boatload of money that comes due all slated for long term bonds.

There are lies, there are damn lies, and there are statistics. I do not trust the BLS period, and you have just illustrated why.

Trusting the government to not tweak numbers is a fools errand. The only reason CPI isn’t high single digits right now is the tweak that they did in the 80s tweaking/removing home ownership costs inflation as a component of CPI.

Howdy Folks and Lone Wolf. Lone Wolf seems surprised by the tricks???

You youngins aint seen nothin yet………. More insanity to come……Thanks Lone Wolf, its always been very easy to know if inflation is here or not. I just never knew how they cooked the books till finding your website…….

Does anyone know what the health insurance CPI was in Sep 2022?

Wolf likely knows.

Wait for it…………………………lol

+28%

Waited 2 hours 🤣

Hard to believe they changed the calculation to make themselves and their boss not look like idiots. Cough.

I is telling they waited until after the social security increase was set

My insurance agent was kind enough to tell me our Anthem Gold group plan is going up 18.67% in 2024. This is their best plan, with a $1000 individual deductible, which I pay 100% for my employees. $1900/pp/pm in 2024!

Being in a group of less than 25, I’ve been told we don’t have any negotiating strength, though Anthem has a deal worked out with our Chamber of Commerce, and being a member, my agent will see how much this might help me. Joy!

I mean, if we’re gonna talk about CPI components, shouldn’t we focus on the part that is actually pretend and drives 25% of the headline number “Owners’ equivalent rent” and not the also-made-up health insurance number that represents 0.5% of the index?

There are two CPIs for housing: OER and Rent of Primary Residence. And they’re close. See the chart below and this article from yesterday which explains how the data is obtained for each.

https://wolfstreet.com/2023/11/14/beneath-the-skin-of-cpi-inflation/

The Rent CPI is based on actual rents that tenants actually paid. The survey follows the same large group of rental houses and apartments over time and tracks what tenants, who come and go, actually pay in these units.

And there just isn’t a lot of difference between OER and Rent. OER is designed to show inflation in homeownership as a service (shelter), it doesn’t track rents. The Rent CPI tracks rent inflation.

My point is, 35% of CPI is shelter, 75% of which, or 25% of the headline CPI is a subjective survey question asking the owner of a dwelling how much they think it would cost to rent the home. 75% of the shelter cost data is not based on market data. It would seem there would be far better ways to estimate cost of ownership given the volume of data available in this sector. It’s very outdated. I have no issues with the actual rent survey.

The problem we have with monetary policy is it’s far too easy to get a 30-year mortgage at any price. You can inflate and deflate the bubble too easily. It’s like giving everyone a 10x margin account at Prime-3. The price of homes has far more to do with the cost of 30 year money than supply and demand for the asset itself. We should be able to design monetary policy and regulations that provide price stability for something as essential as housing.

Yeah, bad monetary policy (printing money against mortgage debt and government debt) is at the heart of the terrible housing inflation worldwide.

It is an atrocity. The Fed is a corrupt and evil institution that cares nothing about the working class and barely cares about the middle class.

Wolf, if the pre-revised calculation of health insurance was being used now, instead of what they are using now, what would that have shown in CPI this week? Forgive me if you’ve covered in the article, or even in the comments. I read and read, but comprehension isn’t my strong suit.

I did open enrollment with my employer today and kept the same default single plan. $33.80 biweekly I pay for 2024 (employer pays $341.80). That kicks in Jan 1st. Right now I’m paying $37.91 biweekly and employer pays $416.01. So both of us paying less in 2024 than 2023. I didn’t look at the details of the plan, but off the top of my head they look very similar out of pocket and deductibles, but since I never use it I don’t really look at those details. Just my n=1.

Health Insurance CPI being flat since Aug 2018 doesn’t seem right. Any idea what it _should_ be?

My guess is around 150-160 vs the current value of around 135.

They overestimated a lot, then underestimated a little, then overestimated a lot, then underestimated a lot. Now I guess they’re trying to overestimate a little, to get back to where it should be by this time next year?

Brian,

Health insurance inflation is probably the most difficult thing to measure because there are so many variables across the US. Every state has different insurance plans. With each plan, all variables are in constant flux, premiums, deductibles, co-pays, coverage (that gets really complicated), maximum out of pockets, drug formularies, what providers are included, etc.

Then there is the age of age –insurance gets more expensive when you hit age milestones, such as 50, or 55, or 60, so that by the time you hit 65, you’re glad to switch to Medicare. But those age milestones are NOT inflation. So when you hit 50 and your premium goes up 20%, part of it is inflation and part of it is the age milestone.

That’s also why purchasing health insurance is such a nightmare because it’s so tough to compare various plans — on purpose. The entire industry is totally opaque.

There has been substantial inflation in heath insurance over the years. But I wouldn’t want to guess a number.

This whole story gave me a headache, but I think I understood some of it after a while.

HII=Health Insure Inflation using profitability (profit/premiums) for HI companies is a bogus measure from a consumer standpoint because it measures the inflated cost of the insurance company itse;f (the middleman) rather than the inflated cost of the healthcare services received by the insured.

So presumably there must be another component of the CPI that measures the inflation in healthcare services.m Or if not there is something seriously wrong with CPI.

In any case, CPI ought to measure how much people spent in total relative to what they received for the spending in total. Which I am sure CPI does not measure in any realistic way.

If you go to the detailed tables you can see the component weights under each broad category. There are about a dozen. Health insurance is a little less than 10% of the “Health Services” component of Services and represents about 0.5% of CPI as a whole. Said another way 99.5% of CPI is NOT health insurance, so no matter how misstated and bad, its impact is quite limited to the story.

Hi Wolf, reading the BLS’s explanation for the change to the CPI health insurance calculation, would it be correct to say the retained earnings calculation will likely result in continuous deflation of the figure?

Historically, health insurance premiums rise almost every year, so premiums minus benefits is always negative, resulting in higher premiums the next year. Theoretically premiums would one day catch up and exceed benefits used, but this probably won’t occur until the Boomers pass away. At that future point, the BLS methodology makes sense, but in the meantime it seems like BS.

“…would it be correct to say the retained earnings calculation will likely result in continuous deflation of the figure?”

I would not say so. I don’t know where this will lead to. The health insurance CPI was 28% in Sep 2022, which was way exaggerated, so the method exaggerates in both directions.

The health insurance CPI jumped 1.1% in October (13% annualized), and the jump is being averaged out over three months, so you saw only the first part. Over the next six months at least, the health insurance CPI will increase sharply on a month to month basis; then there will be another adjustment, probably in the same direction for another six months.

The one thing I know for sure is that this whole thing is a mess.

Thank you.