Housing market is frozen, people have gone on buyers’ strike, sellers are hoping that this too shall pass.

By Wolf Richter for WOLF STREET.

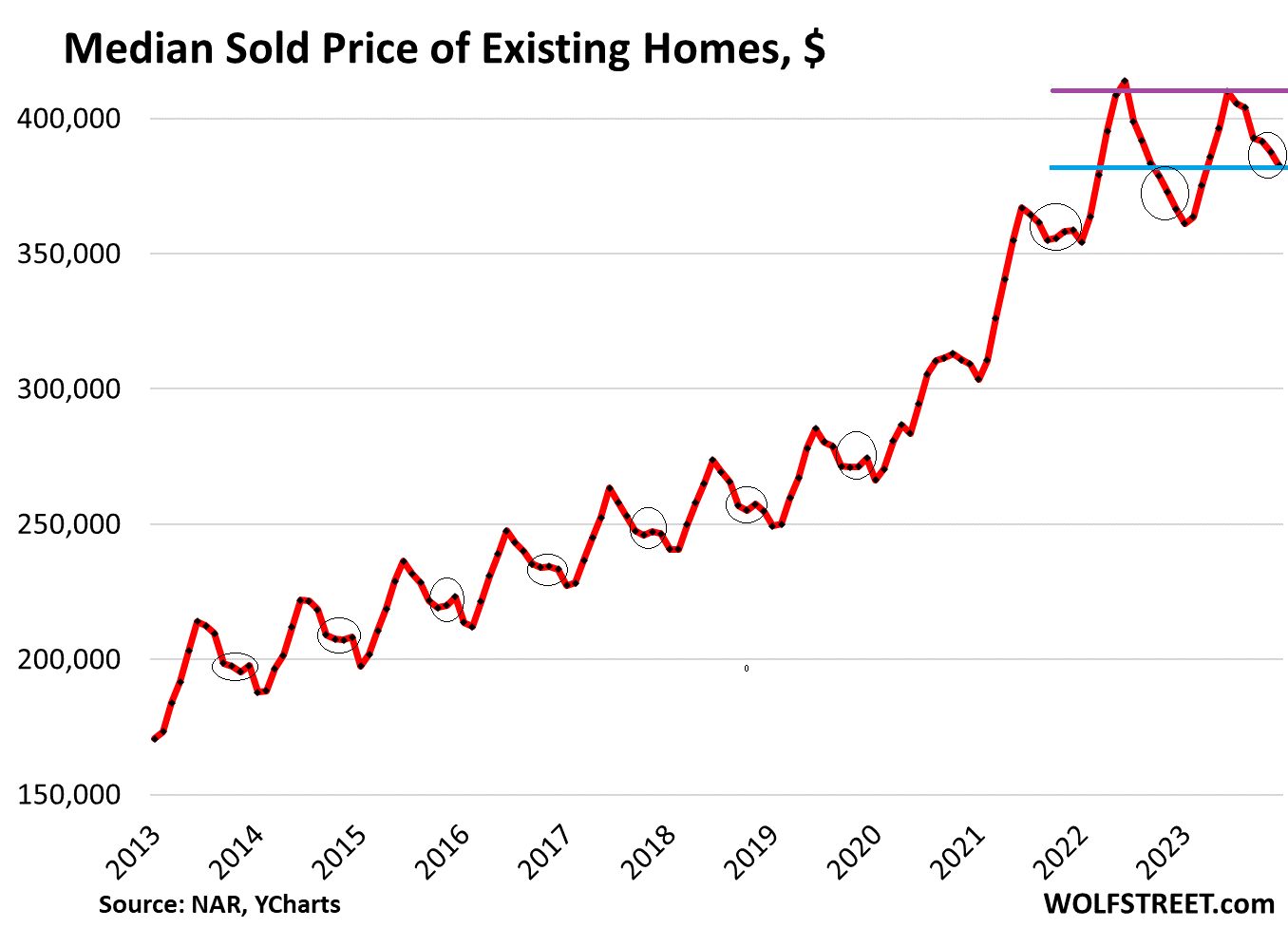

The median price of existing single-family houses, condos, and co-ops in the US whose sales closed in December dropped to $382,600, down by 7.5% from the peak in June 2022, according to data from the National Association of Realtors (NAR) today.

This puts 2023 on record as the first year since the Housing Bust when the seasonal high in June was below the seasonal high (and all-time high) a year earlier. Given the price surge in the spring 2023, the median price was 4.4% higher than in December a year ago.

In another unusual development, prices have dropped every month since June – it’s unusual because seasonally, before the pandemic, there were upticks and flat spots in October through December periods, the little hooks in the chart (circled). There were no such upticks or flat spots in 2022 and 2023, prices fell right through that October-December period (historic data via YCharts):

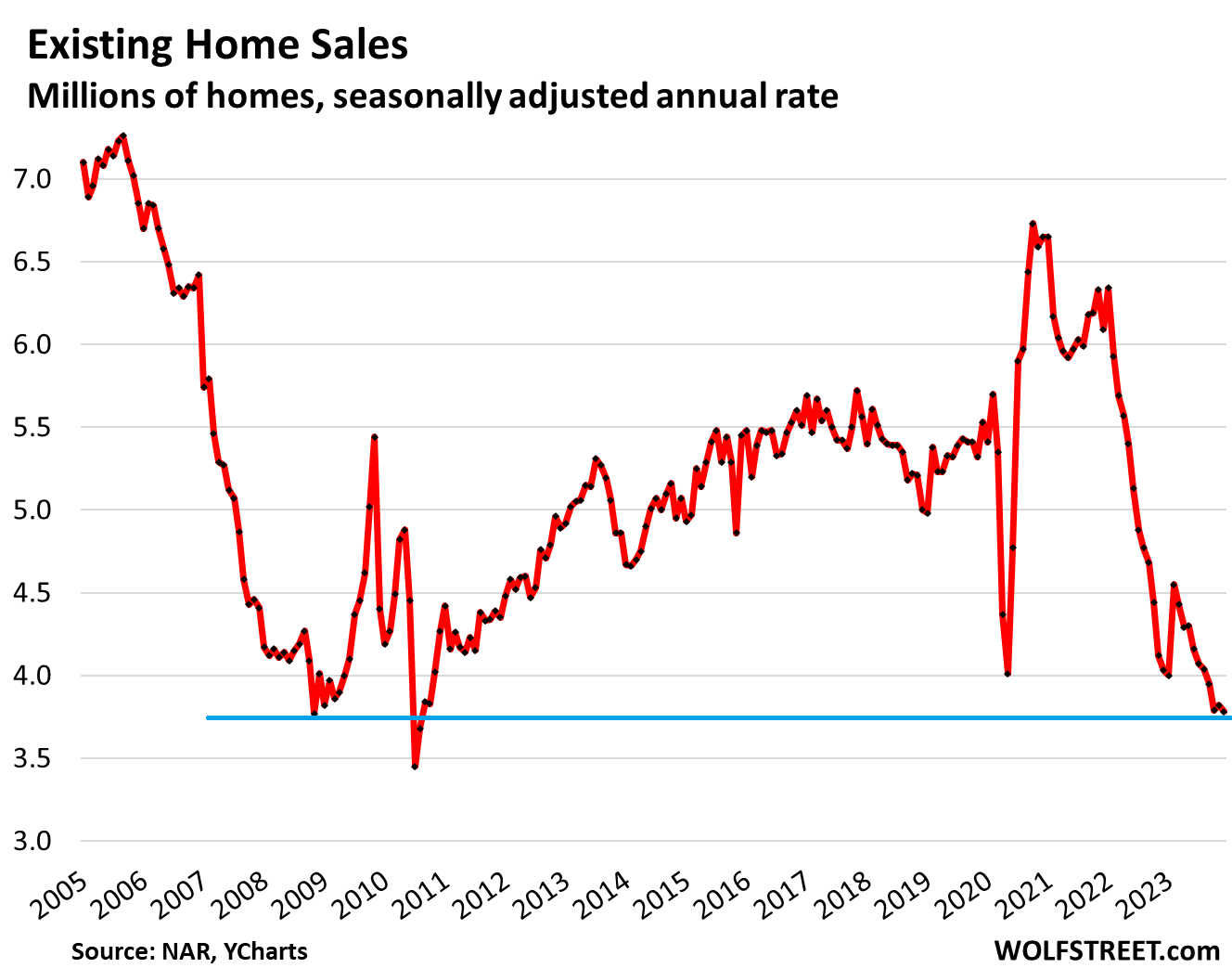

Demand for existing homes has collapsed.

The seasonally adjusted annual rate of sales of existing homes fell to 3.78 million in December, the lowest since the worst two months of the Housing Bust in 2010. For the whole year, sales fell to 4.09 million, the worst year in the NAR’s data that goes back to 1995.

Sales compared to prior Decembers (historic data via YCharts):

- From 2022: -6.2%.

- From 2021: -37.9%

- From 2020: -43.2%

- From 2019: -31.6%.

- From 2018: -24.4%.

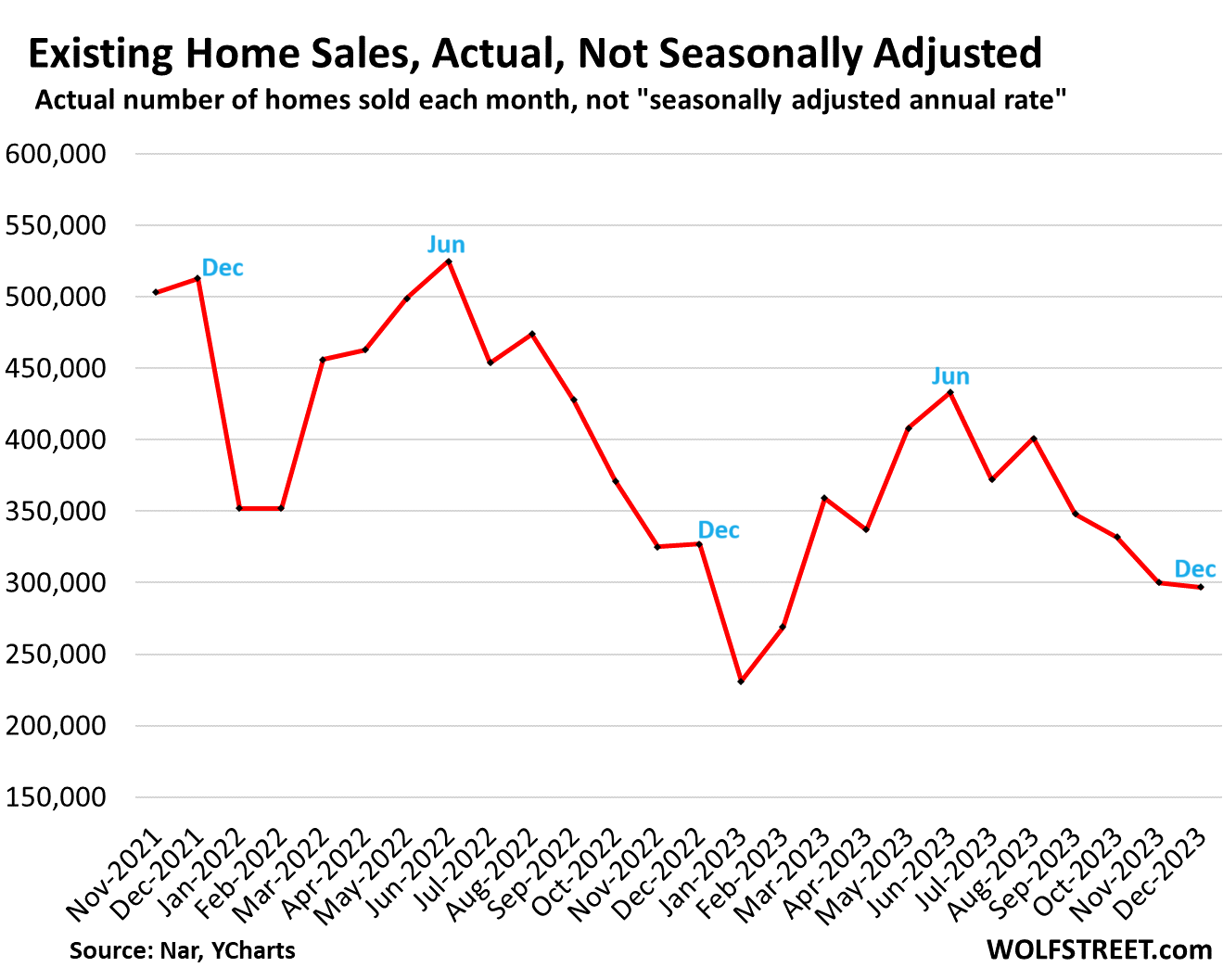

Actual sales – not the seasonally adjusted annual rate – fell to 297,000 homes, down by 42% from December 2021.

Seasonally, January and February mark the low months of the year in terms of closed sales. Sales that closed in those two months reflect the lull in deals over the holidays. June is usually when closed sales peak, reflecting deals made during the end of “spring selling season” in April and May. During the second half of the year closed sales decline (data via NAR):

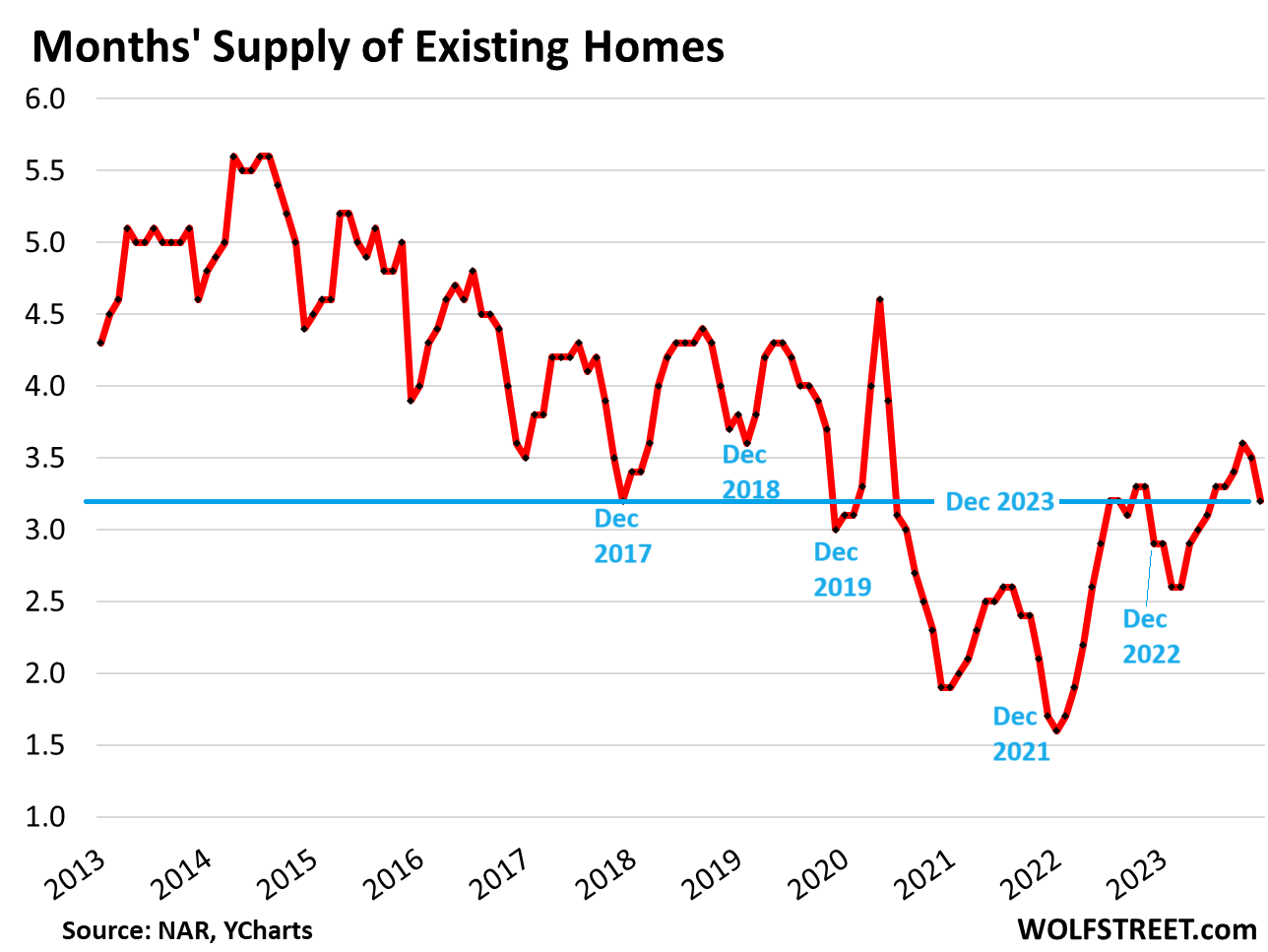

Months’ supply, at 3.2 months, was the highest for any December since 2018 (when a surge in mortgage rates due to Fed rate hikes slowed the housing market). And it matched 2017. Months’ supply is the result of sales that collapsed while sellers were still trying to outwait this situation (historic data via YCharts).

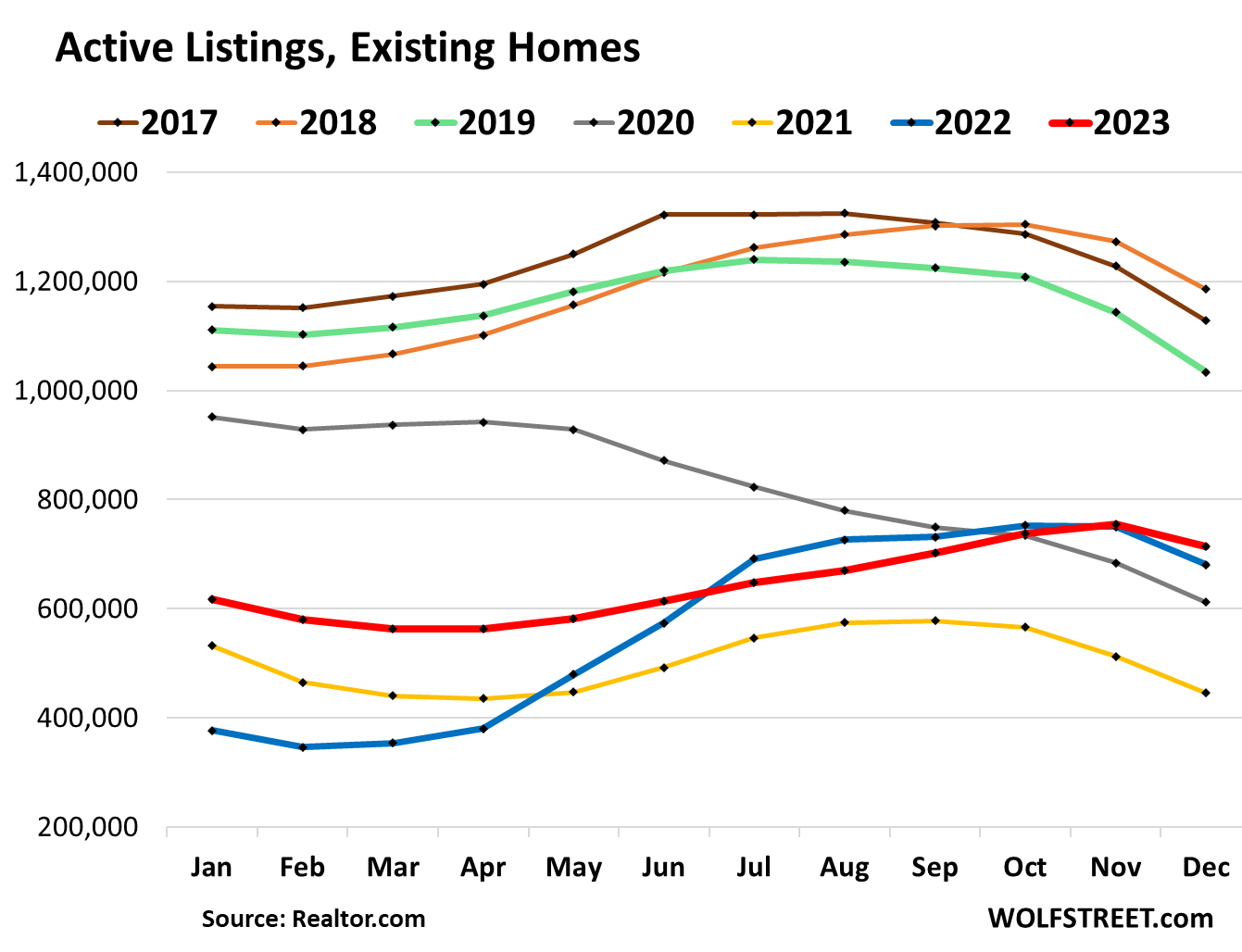

Active listings always drop sharply in November and December as sellers pull their homes off the market before the holidays. But in November 2023 they rose, and in December, they barely dipped and at 714,000, were the highest for any December since 2019. The difference between 2019 and 2023 has gotten smaller every month since May. In May 2023, active listings were 50.7% below May 2019. By December, the difference shrank to 30.9%.

Active listings are inventory minus homes listed as “sale pending” (2023 = red; 2019 = green; data via Realtor.com)

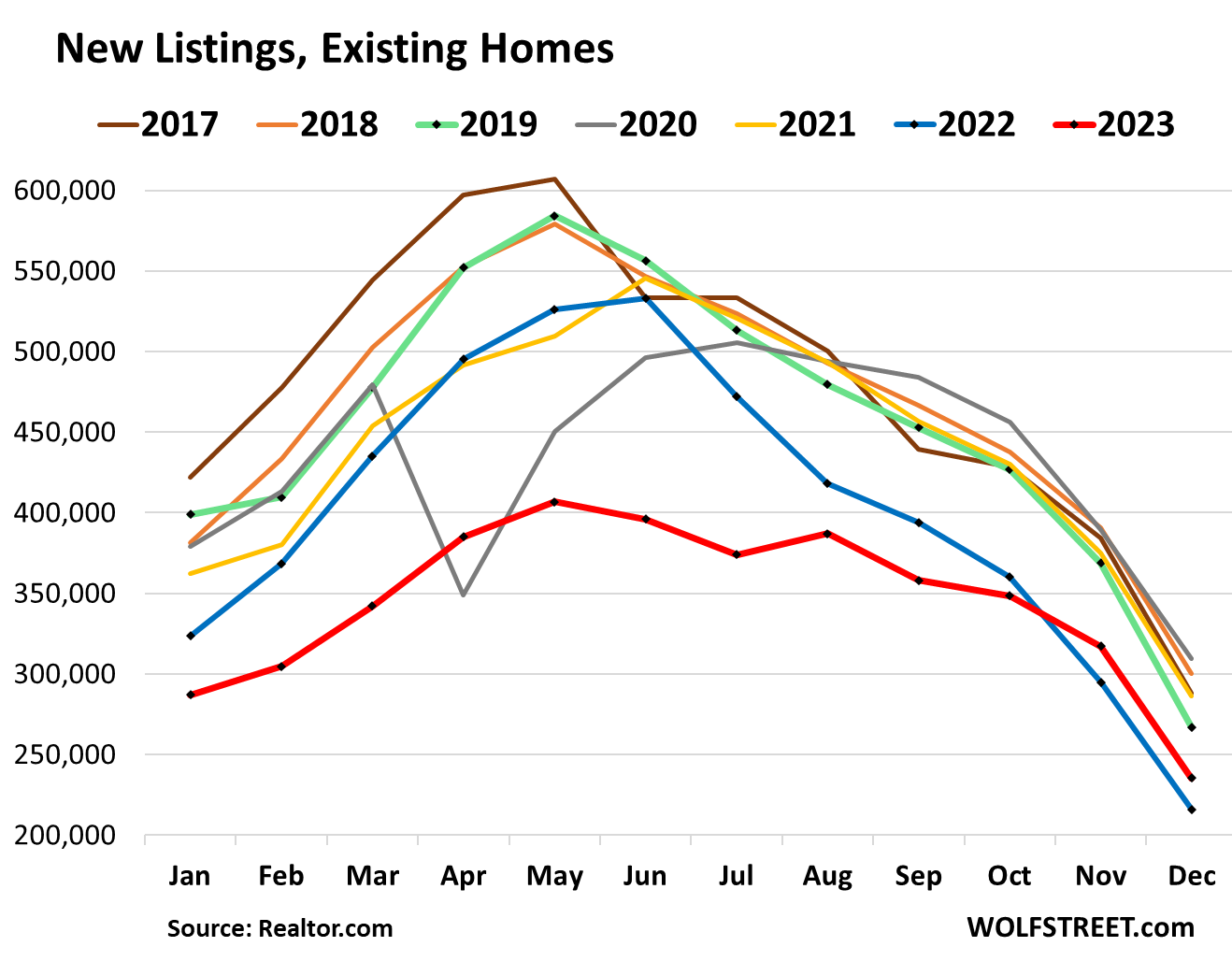

New listings of existing homes always drop in the second half of the year and particularly going into the holidays.

But in the second half of 2023, new listings have fallen less than normal, and the difference to pre-pandemic years narrowed. In December 2023 new listings (red line) were up from a year earlier, and the gap to 2019 narrowed to just 11.8%, down from a gap of over 30% in May and April 2023 (2023 = red; 2019 = green; data via Realtor.com):

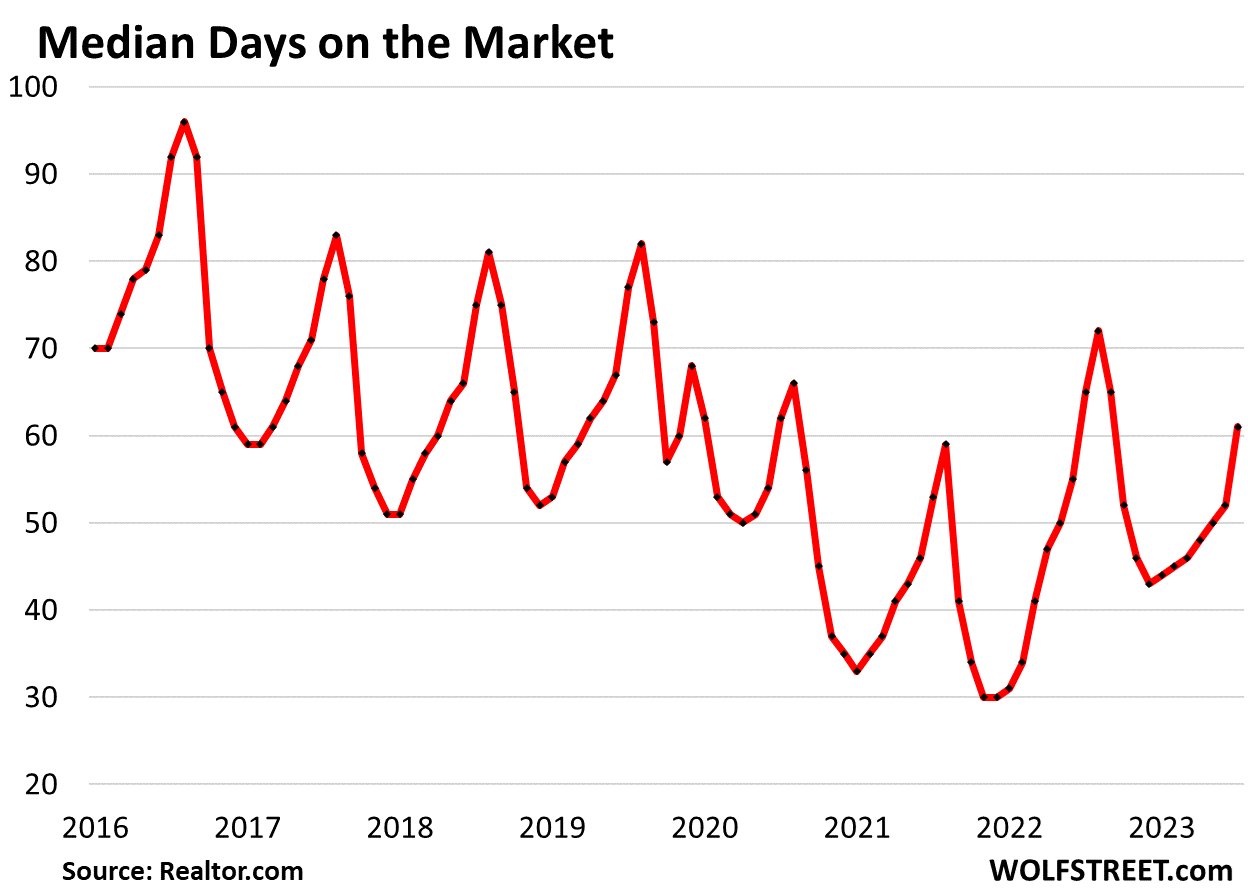

Median days on the market jumped to 61 days in December before the homes were either sold or pulled off the market, the highest since March, according to data from realtor.com. This metric reflects in part how quickly sellers pull their listings off the market when they don’t get the hoped-for response:

This is the picture of a market that is frozen. Prices are too high, buyers have gone on strike, demand has collapsed, and sellers are trying to outwait this situation, thinking that this too shall pass.

Homebuilders, however, are not thinking that this too shall pass. They’ve adjusted to the market. They’re building smaller houses with fewer amenities and sell them at lower prices, and they’re buying down mortgage rates, which is expensive and for home builders is like a price cut, and they’re throwing other incentives at buyers, and they have been able to produce decent sales of new homes, taking buyers away from existing homes, and demand for existing homes has collapsed.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Not a good sign that this December is higher than the last. Let’s pray this June peak is lower than the last, but I don’t see it happening. Horizontal saw teeth for a few years is my prediction, before the relentless surge upwards continues. If you’re saving and catching up, things may be in sight. If you’re not, tick tock. The pause won’t last forever. Your land lord knows this, and it will reflect in your renewal notice. There is no escape.

I tend to agree at this point. I think we’re in the mid stages of a crack up boom. During that, prices never decline. It’s the currency that is declining.

not sure that is case

I’m finishing home – either for sale or rental

don’t care as its F&C

but I’m not seeing lower prices due to low supply

maybe in stressed area’s like SF, CHIC, NYC, etc.

and now that PROPERTY INSURANCE is increasing 40%

time to RAISE RENTS not lower

Landlords can raise asking rents all they want, but they’re going to hit a ceiling on people’s ability to pay…

my SoCal property insurance is going up 7%. where are you seeing 40% increases?

JamesO, Florida has seen 40% increases due to hurricane risk.

Try 100+% here in NC (Raleigh are, not even the coast). My renewal came in at almost $2100/yr, up from 900-1000 for two prior years. No claims, no idea why, not happy at all.

Tax assessment (and thus property taxes) went up 50% vs last year.

Salary at work – went up 0.0% as “you are already at or above 60th percentile in your grade”.

Other than those minor annoyances, life is good!

speaking as a landlord you can only charge what the market will bare and many areas went too high and are already starting to come down as people get squeezed by inflation. if you’re going to sell. lower the price and sell now unless you want to hold onto it for at least a decade.

Einhal, although I share in your sentiments, I think we are still far from a crack-up boom. According to the formal definition you need to have:

1) excessively expansionary monetary policy that leads to out-of-control inflation expectations and

2) a resulting bout of hyperinflation which ends in the abandonment of the currency

We were going fast in this direction during 2021 when QE was at full tilt and the price of even candy wrappers (digital ones) were increasing in price, but at least for now the Fed has stepped on the breaks. Their balance sheet along with the main monetary aggregates are flatlined or trending down ever so slightly.

Not saying we won’t go there in the future (depends how long the Fed holds the line). I’ve been surprised they have held as long as they have. The out-of-control government spending will make this harder as it gets worse.

I agree with you Leonardo. However, it always starts out slow. In Weimar Germany, during 1918 it started out slow, and didn’t go out of control until 1921 and 1922 if I recall correctly.

You’re right that the Fed has anchored expectations somewhat so we’re not in a full-fledged crack-up boom yet, if they resort to printing again next time, they might lose control.

I guess we’ll see in the next 10-15 years.

100% agree, just watch what the FED does and how much the government is spending. If the Fed stops QT or even worse reverses, asset prices will go up, or to say the purchasing power of our money will go down. The FED is in total control of the markets, the FED owns the markets, if they want higher asset prices they will lower interest rates and then if that is not enough the will start QE.

I think Powell does not like Biden or Trump and he is doing the right thing by keeping rates up and QT, maybe he will be a hero, a Paul V. I have also been surprised he ahs keep interest rates high and continues QT and will be even more surprised if he continues, Wall Street will be even more surprised :)

I’m still waiting out the housing market after selling my home 2.5 yrs ago.

This past summer I switched rental houses to a newer, nicer home and talked the owner and property manager down on their rental asking price. Now I’m in a nicer home with a lower rent than my previous one.

Inflation is crushing people’s purchasing power. Yet most people won’t let go of eating out and driving new vehicles.

I’m in the Tampa,FL area.

NAR leadership turmoil continues as another president resigned due to apparent blackmail.

The NAR fight is between 2 lobbies:

First lobby is of investors that want narrative of higher housing prices and want to beg Fed for rate cuts while knowing that it won’t really help house prices rise further.

Second lobby is of real estate professionals who earn commissions and are now going bankrupt with the market freezing. Second lobby wants narrative to be changed to housing market crash so that the lower prices revive the sales.

Let’s see how this goes, I do expect bankruptcies to keep rising in real estate business and that should allow the commissions lobby to win over the investors lobby.

Why do you pray that the home prices remain high ?

I am also multiple home owners but I pray that home prices fall so that new generations can afford decent life style and have at least a shelter over their and families head.

I hope home prices fall but I have been wrong so far.

We don’t pray. I think most readers of this blog want a ~30-40% asset price correction, at least back to pre-pandemic levels.

However the Fed has made it abundantly clear they don’t want asset prices to slide by that much. Now whether this will actually be the case or not is another question. I’m hopeful that the fed will allow it and will tell the bag holders that investments carry risk.

But realistically? Considering who actually runs American society, and who the government is actually beholden to, I think we’re unlikely to get that because it would hurt rich people too much.

well if assets decline from here 30-40%

given the already 70% decline in fiat $dollar

I’d be buying everything I can and financing it all

Naren-

Is the Fed more or less benevolent toward bankers and their friends than it was in 2008-10? Prices then dropped 40-50% (more or less). Similarly drastic price reversions in various markets — from stocks to oil to farmland — arise every decade. All while the Fed’s mandates and perceived purpose center around “price stability.”

One thing HAS changed though. Systemic leverage as a percent of GDP since the 60’s has grown meaningfully (thanks more recently to Fed’s ZIRP) making policy errors even more prone to large misses.

The desire for a “soft landing” may exist, but do they really have the ability to pull it off? Past Fed policy mis-steps, price gyrations, and debt growth point to the answer: “unlikely.”

joedidee, you time it wrong with leverage and you’ll lose your house, too.

Here in LA, homes still sell. High prices, high rates. I’ve been waiting for years for the market to correct. Instead it keeps going or staying high. I am getting older and don’t know how much longer I can wait. I want my one home. Tired of paying off someone else’s mortgage.

They’re selling in Florida and they’re selling in Texas too … and all the other 48 states. It just takes a little longer, but still less than normal.

All the naysayers here are just wishing for a crash because they want to pretend they would actuallly pull the trigger and buy something.

Of course they won’t, though. They missed a gigantic 10-year bull market in housing where prices only went up. They certainly won’t buy if prices are going down dramatically.

CCCB, my cousin is 27, just got married. Housing prices went up faster than his ability to save. Was he missing a gigantic 10 year bull market in housing?

You are exactly why the younger generations detest the older people who have pulled the ladders up behind them

It’s the millennials and the Gen-Zers that are the biggest home buyers, and they’re trampling all over each other and they’re outbidding each other, and THEY are responsible for the spike in prices over the past few years. They need to calm down and quit doing this!

Guy’s a stirrer…ignore.

.

Frustrated,

Can you afford the home you want to buy? If yes, then buy it! What does it matter if the market is high or low? If you want a house and can afford it, then do it.

Now if you can’t afford it, but you still want a house, why not look at cheaper homes in another area/city/state? If owning your own home is the goal, shift the other things to make it happen.

I don’t understand these comments from people.

Nunya – seems like some want to live in expensive metros, and then complain about the prices in said expensive metros.

There are lots of affordable (ish) homes in flyover country, but living there won’t get you as many likes on tiktok vs being able to show off your “glamorous big city life”

NB: I used to live (rent) in the city (boston) and it was fun, but I bought a house farther away despite the 1 hr commute bc that’s what I could afford.

MM, I think you’re being a bit flippant. Sure, there are some people who feel they are entitled to things they shouldn’t be.

But one thing people SHOULD be entitled to is to participate in the market without government distortion.

Einhal,

Government distortion? This is the system we have collectively created for ourselves. Learn to live with it. The same principle I discussed applies here, if you don’t like what this government is doing, take on the monumental task of changing it. If you feel it can’t be changed, go to a different country which functions in a way to your liking.

You can benefit on both sides of the QE/QT/Fed actions/inactions. Open your eyes.

So your recommendation is that we just suck up government oppression/abuse if we’re not willing to try to topple the government?

LOL okay. People like you are why I wish we had an ignore function on this site.

Thank you, I have 3 kids and I would like to buy a house,l. But I can’t prices at Arizona are really skyrocket

Hachim,

I posted a similar question to “Frustrated” above. Why can’t you buy a home? You can’t afford the high prices and high rates? If not, why can’t you move? What does three kids have to do with a home?

I grew up in a 3 bedroom apartment as a family of 6 (4 kids). I got my own room when my oldest brother graduated from tech school and moved out. I somehow survived, went to college, got a job, bought my house (1,500 SF), got married, had 3 kids.

There seems to be this false requirement being put on people by other people that you must own a home and if you have kids they need all the space in the world, specifically a house of their own. This is all nonsense. The quicker you get over these stereotypes and societal pressures, the better off you will feel.

We finally paid the deposit for a new build. Our young family needs a home and we have been looking and saving for years. Now I am in fear that the market will crash. We both work and can afford the mortgage. Fingers crossed. My wife is beyond excited. I think she is nesting :)

Congratulations on your first home! That’s fantastic! No need to be in fear of a crash. As long as you can comfortably afford the mortgage you are fine. And long term, your piti can be lower if you refinance with a future lower rate. Will likely take a while though. Buying RE is a long game, forget the noise and enjoy your home and memories!

Congratulations!

If you’re going to live there, and you can afford it the payment, who cares if the value declines? You’ve got enough legitimate things to worry about, don’t let a number on paper be one of them.

New home builders have been desperate to sell and have been offering massive incentives in the way of mortgage rate buy downs and other such savings (in lieu of lowering prices so that comps still look good for future home sales). Please take advantage of these times if you’re in the position to do so. If prices drop, so what? If you can comfortably afford the mortgage without much risk of either of you becoming jobless in the near future, you should be fine and unaffected by whatever the market does other than having a refinance opportunity if rates drop significantly. Good luck and congrats!

You fear a market crash because you needed a home but we’re forced to take on a risky investment as well. If home prices were refected in inflation statistics the Fed uses to set interest rates, prices would never have gotten this high.

People complain that houses have turned into risky investments. Arguably, that shift has been encouraged by deficiencies in formal monetary policy.

It’s an issue the Fed has plenty of reason to revisit.

Hopefully you bought in an area that hasn’t risen 200% in ten years.

Home prices and rent are in the inflation stats. It’s what’s driving a lot of inflation. I don’t know that this would stop anyone from perpetuating bad policy, though.

Blake,

Home price inflation is NOT in the inflation stats. A concept called Owners Equivalent Rent, and actual rents, are in the inflation stats for shelter. Read Wolfs past articles on inflation.

That OER concept has captured maybe half the actual home price appreciation lately, and nothing close to half in many desirable areas of the country such as coastal states.

With home price inflation excluded from CPI, the Fed can say home prices are “not my problem”.

Blake, home prices are NOT in inflation stats. Owner equivalent rent is.

That market collapses, rates will come down as well. Then you can refinance.

I remember our 1st house refinancing at 10.5 %. We were sure it could not go lower.

“That market collapses, rates will come down as well. Then you can refinance.”

That’s precisely what you cannot do because when the housing market collapses, the value of your home goes south with it, and if you bought recently, you’ll be upside down in your mortgage, with the house being worth substantially less than the amount you owe, and no lender will touch that thing. You can only refinance when you have equity in your home — after prices have gone up.

You can default on your mortgage and then contact your lender and see if they’re willing to modify the mortgage with a lower rate, instead of foreclosing on the house and taking a big loss. But that’s a risky game.

It’ll be fine. Set up shop & just live your life. Don’t look at Zillow.

You are in fear because you will be upset if you discover that someone else next year gets a better deal on a house than you got.

It may help you conquer this fear if you can find a way to stop being unhappy when someone else enjoys good fortune you missed out on. You have already plenty of good fortune that some other do not get.

Amen! Envy is a terrible way to live.

Moved to Jacksonville FL this past summer for treatment at Mayo Clinic. So many new apartment buildings opening and under construction helped us to negotiate a 7 month lease with the 1’st month free (2BR / 2.5 Baths / 1 car garage). Nice property 15 minutes from Mayo and 20 minutes to Jax beach. We just renewed for another 8 months and to my surprise they did not ask for a rent increase.

I am not sure where all these people are going who are moving to FL but there are definitely a ton of vacant properties on “furnished finders” available in Jacksonville.

All real estate is local, so I am sure cities across the country are seeing different results. But we think buying now would be like catching a falling knife. Time will tell.

I am in socal and I am seeing lot of multi family homes been built to sell or rent out.

They are going to S. Florida and Tampa. I grew up down there near WPB. Long ago settled here in NE Florida because I love my home state but have no interest in dealing with the hassles of what I lovingly refer to as Califlorida down there.

I would rather live in NE Florida for the politics, but it gets a winter, unlike SE Florida where I am (in Palm Beach County).

From the first chart. On the upslope connect the lower points of the sawtooth signal and project forward gives a median house price of ~$300000. About $100000 less than the current median price. Even 25% mis-match, it may be argued is an underestimate, because the upslope was boosted by ZIRP policy. Assuming, current prices to stay the same in the coming years. Projecting further forward, it will take ~4 years for the two prices to intersect, hence achieve the soft landing. What will happen over the next 4 years cannot be forecasted with any precision.

Don’t worry. Fed chair Powell promised aspiring home buyers a “bit of a reset” back in 2022, and he’s a man of his word.

Oh…you blinked on October 22, 2022 at 3:16 P.M.? Well then, sorry, you missed it.

It would be great to see regional data. I know Texas is a very different market than California.

I don’t track Texas overall. But I’m on the mailing list of the Greater Houston Partnership, which sends all kinds of economic updates on Houston. And these are segments of their housing missive, which they sent out on Jan 12 for Dec 2023. here are annual sales and the 12-month moving averages of median prices and inventories:

Closed sales in the year 2023: 102,389 homes (single-family, duplexes, triplexes, condos, and townhomes) “the slowest level of sales since ’18. The recent peak was in ’21 when realtors sold 131,678 homes.”

“The rapid escalation in home prices which began late in ’20 reversed itself in ’22. Year-over-year price changes turned negative in February and continued along that path through much of ’23. The median price for a single-family home in metro Houston was $330,000 in December ’23, down from a peak of $354,000 in June ’22.”

This is a 12-month moving average:

“…. Since then, listings have more than doubled and months of supply more than tripled. At the end of December, there were 23,072 single-family homes listed for sale with HAR, or a 3.3-month supply, based on recent sales activity.”

Was the $330,000 price the median of the closing sales, or another method of

valuation?

the median price of all homes whose sales closed in December, meaning 50% of the sales closed at prices higher than $330k and 50% closed at prices lower than $330K.

This is from the Houston Association of Realtors, which is part of NAR. It’s based on MLS data.

most excellent for HOUSTON

but not here

and NOT LIKELY – we don’t have OVER BUILD PHOENIX/HOUSTON

as I’ve always said

I NEED ONLY 1 buyer – rest can fish

The market in my country (Sweden) is more dead than frozen. Sellers are still trying to get spring 2022 prices, buyers are … not buying it.

excellent – so as soon as I sell then I can buy more at cheaper prices

all about WHEN and HOW

that’s another story – but my experience COST BIG $$$$

good luck in HUNTING

lol you must be blind to math 🧮. I see lots of price declines, stagnant listings, and incentives for everyone.

It’s okay. Keep trying tho! Maybe one day you can read too!

Wolf,

Do you think we will ever get over the nonsense put out by the National Association of Realtors that a house is an investment? Having owned a house(s) continuously for over 60 years, I’m pretty sure houses are a form of necessary shelter but not in any way shape or form an investment. (Yes, I’m told my house would sell for more than I paid for it but I just received an estimate for new windows (90K, and just replaced the roof last fall for 40K plus. never mind, insurance and taxes, depreciating mechanicals, paint etc etc.)

It is an “investment” if you have a reckless central bank that prints its way out of any problems.

But it shouldn’t be.

It’s a form of necessary shelter but if you rent you pay for those things you listed but just built into rent. You would have to calculate all the rent you would have paid for equivalent and compare to the price of your house and money you put into it. Myself needing a new HVAC soon, fences and some windows I get your point but I am still ahead.

Have to consider the subjective pros and cons as well. I can’t be told I have to move as an owner for example.

I think however nonsense can be expected for any business built on profit in the way NAR is. Hopefully out of work realtors can retool to be educators or healthcare workers or another profession.

If the NAR was really operating in the best interests of realtors, they’d be trying to coax potential sellers with truth, not trying to swindle buyers with lies.

In my area, the truth is: Home prices have more than doubled in last 10 years.

This reinforced the thought that real estate can only go up.

It is very difficult for agents to go against historical trend and then tell sellers to sell at lower price saying crash is coming.

I digress, but IMHO

the only thing that deflates is fiat $dollar

so 100% cost INCREASE since 2020 is really 50% fiat $dollar DEVALUATION

so NO you are not getting previous prices EVER

Also don’t forget that the “hard core” can do most maintenance themselves and it may not be that expensive. There is a YouTube video for every job. I worked a cubicle desk job and knew nothing about construction and still managed to replace a hot water heater, sump pumps, repair a hole in my roof, reshingle a roof, build a shed, paint, etc. Once the mortgage is paid, insurance is optional. But those property taxes will keep going up for life, same with utilities. Yes it’s not really much of an investment except in comparison to what you would have paid if you were renting. We need low cost high quality prefab modular homes like boxable going mainstream.

The only time a house is an investment is when someone else is paying your mortgage pymt, taxes, and insurance in the for of positive rent/cash flow. Living in a house and paying all these expenses are always a liability to the owner. Even when paid in full, the taxes and insurance continue on. So it’s not an investment.

Yes. And at least in my area, anyone who bought at bubble prices in 2021 and 2022 is NOT able to cover their costs with rent.

The insurance does not carry on, necessarily. It’s optional. It only carries on for those who want the insurance policy. Your statement is only correct for taxes, which are not optional, and utilities, if you don’t shut them off.

If a person buys the right house and is willing to sell and move to others, in my experience a house is certainly an investment. We used a ladder approach and always bought a house bigger and more expensive than needed AND in an excellent micro-location. It has paid off from a monetary point of view for us. For an example of a micro-location, a house on a golf course will sell for more (and faster) than an equivalent structure across the street with no fairway view. The buyer has to be willing to occasionally move and should also be willing to hire a designer or do renovation work themselves to get the property in top shape. It also helps to find a lower-cost realtor or get your license yourself.

The NAR is immune to investment calculations. I was a member and an appraiser in the 1980s and wrote about the home as a dubious investment even though it might be a satisfying luxury. Most buyers don’t calculate ROI either. They are buying mostly intangibles: location, convenience, stability, pride, status, etc.

When mortgage rates were 2.5 to 3% buying a good quality home was an investment since you could borrow hundreds of thousands at, say, 3%, getting far more than you needed for purchase. Then invest the extra at a safe 4-5% and make 1-2% on the lender’s money.

I paid $14K for a new metal roof about 3 yrs ago and $5K for new windows about 5 yrs ago Those prices sound outrageously high.

@Wolf – what are your thoughts on lines emanating upwards from the X-axis values for your charts?

It is difficult to otherwise understand where does the trend lines intersect across the two dimensions otherwise.

A small suggestion that can help extract a lot more value from your hard work.

Not answering for Wolf, but the chart tells me that the first lower high has been shown. The next phase to show, which will be an indicator of a downtrend, will be lower lows. Once we get a second lower high, I would take that as full confirmation we are in a full on downtrend.

How people can use this information to make life altering decisions is beyond me. Life goes on, live your life. Now, if you happen to have some dry powder in the bank when prices show a bottom forming, then you could deploy as an investment in real estate or rent your existing home and buy your next one.

“Homebuilders, however, are not thinking that this too shall pass. They’ve adjusted to the market. They’re building smaller houses with fewer amenities and sell them at lower prices, and they’re buying down mortgage rates, which is expensive and for home builders is like a price cut, and they’re throwing other incentives at buyers, and they have been able to produce decent sales of new homes, taking buyers away from existing homes, and demand for existing homes has collapsed.”

This is EXACTLY what is going on in my neighborhood (new development – north of Houston, TX). There are 5 or 6 new homes going up, a few new foundations, and the others nearing completion. These homes are all sold within the last four months and there are new sold signs on some building lots that only have utilities installed. In other words, there are willing buyers.

These homes are 1,200+ to ~2,450 sq. ft. in size and are being sold to a mix of young families and retirees (like me). They are inexpensive starter homes in the price range of $230 – $280 K.

There are a half dozen builders developing these kinds of neighborhoods in this general area. No problem selling as the builders are buying down the mortgage rate to 5.99%. Essentially 5% of the list price of the home.

Why don’t the buyers just take out a shorter mortgage term at a lower rate and pay the homes off in a couple of years’ time?

Because they can’t afford to

bingo

I imagine some did.

But this type of property attracts lower income folks and rather than lower prices, the builder is offering a mortgage interest buy down (lower payment) which will help buyers qualify.

.

my son – recently bought 2nd home at age 25(married with 2nd child coming in summer)

anyway he listed his property for sale

had 1 taker who backed out after financing was issue

just rented it at very HIGH price (3 generations moving in)

he’s doing well with LONG TERM RENTERS

You don’t have to take out a shorter term…. you just make additional principal payments when you can. Shortens the loan term automatically, reduces interest paid, and you’re not stuck with a higher payment in the event you have a patch of cash flow issues.

Or you can set up a bi-weekly payment rather than monthly. Lots of ways to skin that cat.

What rate cut?

The 20 rate cuts the hallucinating Wall Street masters of the universe factored into equity prices starting in 2023 Q4.

O, that’s right. Sorry.

Carry on.

Appears that median home prices increased by 33% from 2021 to 2022, and doubled from 2015 to 2022.

Time to tighten the money supply some more.

Our hood that we walk daily is 144 square blocks in the saintly part of TPA bay area.

Older houses, including ours, are frequently ”tearer downers” if not fixers, and were selling at less than $100/SF in 2015, and now $400/SF.

2 New houses are under construction after paying above for house and lot and demolishing old house; they are selling for well over $500/SF depending on finishes, etc., and are usually at least twice the SF of the demoed house.

Lots of population pressure from 1,000 NET in migration PER DAY into FL, so gains likely to continue, though certainly would consider possibility of correction similar to last time.

FL has a glorious history of booms/busts going back….centuries. Maybe this will be a permanently high plateau, as the infamous saying goes.

I am in Pharma/ biotech. Our industry is hurting. Lower rates would help and a bit of money printing. Who’s gonna pay my mortgage if I get laid off?

You don’t have any emergency funds set aside for something like a job loss?

Whoever buys it at auction

Did you forget to add /S? Or maybe you’re serious but only taking about the SoCal invincible market?

The prices never dropped in hopes of lower rates, they never stopped expecting lower rates. Lower rates are already priced in. Good luck with that.

Hmmm.. this time is different, well at least for SoCal and especially SD/OC… no dips around there and by Spring we’ll be at bidding wars regardless of mortgage rates decrease or not.. so I have been told /s

I’ve looked at SFH rentals in south OC, and it doesn’t look like rents are rising much, if at all.

SD/OC – Buy a house and pay $12K a month in mortgage or rent the house next door for $5000. Seems like an easy choice for anyone with a brain.

This post nails it for my neighborhood in so cal.

Sadly, looks like a lot of brainless FOMO zombies in SoCal cause from where I am sitting (LBC/OC areas) houses are still selling pretty quick even at $1m+ for a 1300sq ft crapshack with a fresh coat of paint.

Also, you see how many of these flippers want someone else to cover their mortgage, listing out rental for $7K-$8K for 2k sq ft home, pretty comical if you ask me.

I think it is important to realize that lower rates do not always mean higher prices. The housing market in SoCal actually dipped for 5-7 years in the 1990’s during a period of decreasing rates. Folks were simply listing their homes at a faster rate than others were buying homes, increasing supply. Once the process of decreasing prices sustains itself, usually initiated by a recession (like in the early 90’s), it can be YEARS before prices recover. Note also there will be generational affects in the latter half of this decade that will increase supply as baby boomers put their secondary and even primary houses back on the market in increase numbers. These things take a longer time than most people are used to.

I stated earlier. I was in a new sub division, in the desert in SoCal, 100 miles away from coast.

The homes have carrying cost of $8K/month and the median income in the city is $45K with no high paying jobs or big industry within 80 miles radius.

Most of the homes are sold by the way .

Buyer not buying is often mis-interpreted. Millennials are the largest cohort buying and they have no interests in buying something OLD. They want a shiny new house with all the shiny new things like smart switches, open concept, contemporary look, etc. No millennial I know gets excited about old, small, houses with small kitchens and a formal dining room. If a seller or an old house put a 100k-150k in to remodel and make it look new, then maybe.

“No millennial I know gets excited about old, small, houses…”

Well you don’t know me, but I am a millennial with disdain for most “new” things. My house is small (<1k sqft), was built in the 70s, and I told my spouse I'm not allowing any of that smart home crap in it.

The Milennials I know won’t install smart devices that are networked to some company’s “cloud” so said companies can harvest your habits and sell the data. Granted, the ones I know are techies, but they build their own systems on a Raspberry-pi or some other such device and host it all within their own environment. Just had that conversation – twice – in the past 10 days.

Replying to MM.

I am someone who works in smart home smart thing tech for my livelihood.

Personally I stay away from new tech.

Not true. My brother bought a 90+ year old house a few months ago with minimal modern updates (single bathroom updated) and everyone who has seen it likes it way more than the 2x larger cookie cutter stucco homes with asphalt shingles all over FL. It has character and charm. I’d prefer a Sears catalog house and do my own updates to it over buying something new, but those are few and far between where I live…we’re all in our 30s btw. I do occasionally specifically search for homes listed at are no newer than 1950 build.

I am also a millenial who owns a house from the 70s and would never install “smart” devices on an Internet-connected network or which could access the cell networks.

I don’t know anybody who wants their life constantly monitored by Google, though I guess _somebody_ does because this stuff has a market..

All the old small houses I see have the most bids, because they are the most affordable. Old small houses may go 50-100k over asking. New builder special will go for asking.

Both will double in price by 2030.

Z33, I’m also in my 30s. I prefer old houses that have been updated in terms of bathrooms and kitchens. But not the crap 60s and 70s ranches and split levels that were thrown up in so much of the country. I’d rather have pre-WW2, or post-1995.

Really interesting to read this about older vs newer homes. I am renting currently and we have all the tech and gadgets you can imagine. Yuuge techies here. We are shopping for our first house and we don’t even look at existing homes. We only go to new builders or existing homes that just got built a couple of years ago. I guess to each there own but we prefer new and tech. All the concerns about Google spying on us. Who gives. Nothing to hide. They can know everything about me.

El Katz & Jon: exactly my thoughts!

If google wants my data, they can purchase it from me. They don’t get it for free.

In the meantime, I plan to stay away from wifi light bulbs and keep backing up my data on my private RAID 10 server.

Jenny B:

The problem with tech is that it becomes obsolete – kind of like the zigbee stuff, Radio Shack, CAT5 wiring, or the old home intercoms. I inherited some “smart switches” that only run on 2.4 Ghz. Guess what? They wouldn’t connect consistently with the new tech routers – even if the new router claims to be 2.4 / 5.0 automatic and “seamless”.

Your preference for “new construction” shows you probably don’t know much about what goes into a house. Fast growth framing lumber is weak. OSB is junk (think what happens to cardboard when it gets wet). Vinyl windows are, well… vinyl windows. Luxury vinyl planking is today’s vinyl sheet flooring with prettier patterns (until you realize that the pattern repeats relentlessly). Water supply lines made out of plastic (life expectancy of 20ish years if installed properly). A lot of experimental building products that can outgas forever.

I prefer old, tried and true materials. CDX plywood sheathing. Cabinets not made out of particle board with embossed contact paper covering. Framing lumber of either old growth or Doug fir. Real solid wood doors vs masonite hollow core. Real wood (not finger jointed) trim vs. genuine cardboard (MDF) trim. I’ve even seen plastic panels that are applied to the exterior of the house that have the appearance of “real stone”.

As far as nothing to hide? Hahahaha! That’s not the point. You should read what the capabilities of some of that tech are and who can ultimately turn it on and off…. on a whim… in the name of “product improvement”.

When you visit model homes or newer builds you get the excitement you would expect. Walking into an old home, you are underwhelmed with the optics, floorplan, smells.

Keep in mind that newer builds have less wood exposed on the exterior (meaning less risk of fire, termites, decay). New tech is a good thing.

Even if better building materials would be used in today’s new builds….why would it matter, if you prefer living in something new and trendy and plan on buying a brand new house every 20 years or so?

When we first came out with the microwave or the internet, people had concerns and their doubts too.

As far as spying goes…..what about your cell phone? Your future smart car, your laptop?….you can’t stop it. Gathering data about you is part of living in 2024. It will only get worse.

“As far as spying goes…..what about your cell phone? Your future smart car, your laptop?”

This is why I do not own a smartphone and refuse to buy any new vehicles (I will drive my MY 2011 until the day I die).

Yeah, I bought in 96 in coastal north county San Diego. Every street had a home or two for sale and there was absolutely no competition. My agent drove me around every weekend to look at places – doubt that would happen now! My price range was 150-200k, those places are probably going for 4-5x that now but I’m glad I left that state almost 2 decades ago as it’s a complete disaster now as the quality of life has declined tremendously.

your complete disaster is my paradise! beach workouts, year round paddle boarding and surfing, great parks for mountain biking and trail running, great fresh produce year round, etc.; been here 4 years and simply loving it!

(i’m from north jersey)

“Note also there will be generational affects in the latter half of this decade that will increase supply as baby boomers put their secondary and even primary houses back on the market”

You act like all baby boomers are the same age and all will be putting their homes on the market at the same time. The youngest baby boomers are only 59. I know many boomers who plan on dying in their homes. So, no, there won’t be an all of a sudden increase in houses on the market from baby boomers the last half of this decade. That kind of BS comes from MW and BI yellow journalism.

I diasgree. Most boomers, if they even have to, will just take out reverse mortgages on their homes and live off the huge equity they have. No payments. No need to move until you die, lol.

Aging in place is going to surprise a lot of folks waiting for the tidal wave of boomer homes for sale. And then those that can afford to, will simply leave their homes to their kids or grandkids.

I don’t know why you disagreed. I said pretty much what you said about aging in place. Plus I added most boomers are no where nearly at the end of their lifespans. Maybe you didn’t see the quotes around the first paragraph in my response to Drewman?

Many boomers will leave their homes to their kids, who will move into them because it’s way more home than they could have afforded independently. I see this happen a lot. I think it’s part of whats growing the wealth divide. If you have low income, inheriting a home or getting help with a down payment from wealthier parents is often the only way to get into the market. For people in 20’s, 30’s, 40s, this is extremely common. If you’re parents didn’t do as well, tough luck, doesn’t matter, because I’ve got mine.

It’s some sort of “accomplishment” that America has managed to recreate the Jane Austen economy, isn’t it?

Thoughts as one with exposure to different countries, cultures:

1. Is the population increasing (like in India, Indonesia)?

2. Is more percentage of population getting richer and richer?

3. Is the available land limited (think Japan where only some 11% is for a living)?

4. Is the labor cost favorable (Think India where some 60% marginally employed)?

4. Changes in technology.

5. How wealthy or indebted the country is?

6. Which direction the operating costs are moving?

Based on these, I feel the golden period for average citizens in this country was something like 1960’s to 2008 when we went from one income household to two, 1150 sq. ft., 1.5 garage to some 3000 sq. ft and 3 car garage, medical coverage for most and so on.

I’m in Mexico. It certainly appears to be booming. Lifestyle here is wonderful. People friendly. We love it.

DR_E – excellent observations. NO nation is ultimately ‘exceptional’ by these metrics and those of a workable, sustainable environmental operating budget (‘…nature bats last’…) for our spacecraft…

may we all find a better day.

I’d say from after WW2 to Reagan is much more accurate. And to expand on Blake’s silly statement, poverty trickles up…in fact I think it’s time to say “flows up” as it seems the speed is increasing. And as a nod and a hi to dustoff’s message, (the ONLY one that is worth ALL our full attention), would you say “I’ve got mine” in a lifeboat? Not good for one’s popularity at all.

My niece gave me a real nice 2′”sq. Green New Deal pin for my bald head ball cap.

BTW, is the Army using “Castro hats” again? Just before I went in they went to baseball hats and I was very disappointed…thought they were cool looking.

Make that grand niece….2nd yr @ SF State.

Silly statement?? That’s the mentality. Everyone who lucked out thinks unaffordable homes are no problem, because it doesn’t effect them. They’ve got theirs, so whatever for everyone else, they just want to see appreciation from here. If you can’t see this mentality, you are likely part of the problem. It takes a strong person to want to make sacrifices for the greater good….such as (God forbid) their home values going down. And we don’t seem to have a lot of strong people, just selfish people. ‘ive got mine’ was not a statement from me, it’s the herd mentality used to justify the problem.

I have never bought a home (2 trailers and an old camper that I still have). Built one by all myself off grid on bare land…took 16 years (about 12 working FT, 2 hrs away at vehicle saving pace) and sold unfinished, so I probably don’t belong in these comments. Have zero experience as to how most people think regarding their homes other than Wolf’s stuff.

Still think my comment was rational and as “true” as things get.

Get effect/affect straight…will ad to your “educated comment points”….if you give a shit ;)

Like to take that stupid grammar comment back…..I got your point and point of view.

Sorry. Was totally chickenshit on my part.

Ironically, you spelled ‘add’ wrong when you were correcting my grammar. To this day I still can’t understand when to use effect vs affect and I don’t care enough to learn. My mind works in numbers and patterns. Your insults don’t affect me ;). Not going for “educated comment shit” anyway.

NBay – makes my day to see your handle, again. (…looks like painter’s caps for USA fatigues are back after flirtations with baseball and berets, though the Marines seem to have stuck with them, or their ‘railroad engineer’ cousin, longterm…). Best-

may we all find a better day.

Blake – I understand that you don’t care, but the effect of that statement affects me deeply…

(best to you, as well…).

may we all find a better day.

…wait! “…numbers and patterns…”? Blake, could it be you are actually one of these ‘AI’-creatures in the digital-flesh???

may we all find a better day.

Nothing to worry …. Once mortgage rates will drop another full percentage point, the anxious renters will become buyers and will start bidding up the existing houses to new levels.

Within the next years we will see “revenge bidding” for homes.

Of course, with the higher prices, even at reduced interest rates, the monthly mortgage payment will be about same as today.

HMM… TEh sophisticated US buyer’s attitude …I refuse to take on a 30 year note at 7.50%, with monthly payments of $6500. But, I accept willingly a monthly note of $6500 at 6.50%!

the monthly nut is what allows one to buy or dictates you still have to rent a while longer. Rate or prices…..what gives. A nation of renters is what we have and get for the foreseeable future.

Yo Lurk, maybe you should lurk on a math site a little bit. More than half own their homes (many with the bank and government as partners!). I’d say that makes the US anything but a nation of renters.

What about “revenge selling”? Right now you have divorced couples continuing to live together because they can’t sell.

A double top forming on the median sales price chart?

Just a matter of time. Rates aren’t going back to zirp. Not even two years into rate hikes. Tip of the iceberg here if we zoom out. Thinking this will look quite a bit different in another 24-48 months.

hope it exists and happens – but I’m 50/50 on zirp

I wish they would build $350-400k homes here on Long Island. Every new build I’ve seen is 1.1+ and more. Idk who’s buying these at today’s rates.

I ask myself the same as I see ugly forty year old condos sell for 1.2M here in San Diego. I don’t understand who is buying these places or where first time homebuyers are getting 250-500k for a down payment or how they can afford an almost 8k a month mortgage. It’s truly baffling.

and then they sell and move into our area’s and buy mansions for same $$$

and then locals complain as everyone raises their prices to compensate

Agree. San Diego is crazy. I couldn’t find a decent place to buy in 2021 let alone at today’s prices. No way am I going to be house poor and live in an ugly building. I’m fine with renting for now. I’m assuming it’s rich foreigners and large corporates that are buying these places but who knows for sure. Do we have a breakdown of actual buyers?

I ask realtors that all the time, and have been for 10 years. “Everyone wants to live here” is the answer, and they cite the % of their clients that are from beastly cold midwest and northeast cities, as well as some Texas and a small portion from abroad. I have yet to hear any mention of migrants from the southeast. And never anything corporate.

San Diego may be the most overrated city in all of the territory. Pretty boring, atomized and miserably expensive. Austin, TX is a close second, but it’s a lot more fun — even minus the ocean.

What is the lot worth?

You cannot build at 350-400k when the lot is worth 600k. 🤷🏻♂️

Why not?

“Why not?”

We have a math whiz here.

Your sarcasm doesn’t answer the question.

What’s wrong with building a 300k house on a 600k lot and selling it for 900k?

Unless by ‘build at’ you mean that’s the price of the lot and the house… in which case yes the math doesn’t make sense, but that’s so obvious I didn’t think someone would take the time to make a comment about it.

Great to see the madness come to a grinding halt. Everyone hanging to their sub 3% mortgage rate and locked in for life. Property taxes and insurance has increased along with HOA’s fees also. Renters are the smart ones, taking on less liabilities as climate change and weather disasters will keep taking its toll across America. Gen X and Gen Y should live with parents, or communal rent with friends and family as long as you can. This housing market will mirror the empty Best Buy and Office Depot stores down the road.

WTFH? “Renters are the smart ones, taking on less liabilities as climate change and weather disasters will keep taking its toll across America.”

I’m Gen X and rent. Detest it. But I’m not about to take the wife and kids and go crash on the couch circa 1996 at my buddies place and be like “Hey bro, global warming just melted Kansas, so I don’t wanna buy right now. Can you hook me and the fam up for free?”

I think Kansas is pretty pretty pretty cold rn. 🥶 lol

Wait till this summer.

The smart ones are those who do what’s best for themselves and their families. Hard stop.

People with kids want them to not have to change schools every year or two so they can have friends and build relationships. They want stability. If their daughter wants a pink room, so be it. She can have it. If their son wants a skate board ramp. Boom. He can have it.

There’s more to life than money. Once you figure that out, you will also find that you can often achieve quality of life and still have money if you learn to curtail your impulses.

PS: It costs money to move. That ain’t free. And my daughter just moved from AZ to CA (communal living in a duplex with an ADU all occupied by friends who are not married and are comforted by having “backup” if they need help) and getting out of one of those corporately owned rentals was a nightmare – despite having photos showing missing closet parts (metal rack shelves and bars), the landlord charged her for them anyway – despite the stuff being Dollar Store quality, they charged Container Store prices. In the multitude of rentals she’s ever been in, the only one she ever got her damage deposit back from was in Oakland where an Army Airborne buddy of mine attended the inspection, along with my daughter and a Navy Seal buddy of his. She thought it was hilarious to watch the building manager who couldn’t sign off fast enough.

EK – my thoughts exactly.

When I rented w roommates, we just rented a uhaul and moved ourselves vs hiring movers. But even that is expensive – the uahul itself, taking a day off from work, rebuying the stuff you threw out bc you didn’t feel like packing it etc.

I was never able to live in one spot for more than a couple years bc: the place turned into a dump, the landlord turned into a jerk, I had roommates that screwed me out of their portion of rent etc.

On that last one: landlord was super cool and gave me the security deposit back PLUS 10% bc I helped him take care of the place. But I had a lease w 3 other roomates, and two of them stopped paying their portion of rent a few months before I moved out. They still owe me a couple thousand$$ which I’ll never get back.

All of these are the hidden costs of renting.

Can’t fathom how many new listings I’m seeing now, in the middle of winter. Something smells dodgy…

All it takes is one home seller to get nervous and low ball on the ask, and the whole hood goes south due to comps.

Thats the first stage.

Starting to see lots of open houses here too (Scottsdale). Noticeably more in the last few of weeks. I know just anecdotal, but it is in your face the increase. Several open house signs to a single corner in some areas. Reminds me of HB1 when all of a sudden I’d see a huge increase in the open house signs. I know just anecdotal and I’m not saying this is the start of a housing crash (I can only hope), but I am seeing some changes in patterns all of a sudden.

The past few years there was little need for an open house. Properties were snapped up the minute they were listed, so the fact open houses are needed is a sign in itself of a change. I can only pray it is a lasting change that brings house prices down to reality.

Out where I live (Northeast Snotsdale), there are numerous houses popping up for sale. We blame the recent rains as they seem to have caused the “sign seeds” to germinate. Mostly second homes purchased by those in the past few years that are hallucinating that they’ll hit a “home run” (like +$500K in a year with maybe only a paint job and minimal improvements). Funny thing is, they ain’t selling at these phone book prices. One dufus that bought 1.5 years ago took a $100K dump, but did sell (@15% plus realtor fees) – didn’t help that they had arguably one of the worse locations (busy street, across from a church, down from the post office right on the intersection – so lots of headlights in your windows at night).

Many are trying to escape as their eyes may have been bigger than their tummy (or wallet). Carrying empty houses for 7 months is expensive and the HOA just clamped down on the VRBO’s…. (30 day minimum now so… no cash flow, poor babies). Golf dues have skyrocketed…. and now they want to spend $15M+++ on golf course “renovations” that will hit the members with a tidy assessment. Insanity. I wasn’t dumb enough to join – even as a social member.

Katz

Glad I’m not the only one noticing it. I too am in north Snotsdale. I’m liking those germinating sign seeds. It’s great to see increasing inventory that is not moving. I hope it continues.

Agree. San Diego is crazy. I couldn’t find a decent place to buy in 2021 let alone at today’s prices. No way am I going to be house poor and live in an ugly building. I’m fine with renting for now. I’m assuming it’s rich foreigners and large corporates that are buying these places but who knows for sure. Do we have a breakdown of actual buyers?

And yet everyone says we are not in a recession. Let’s see what NBER says when the recession started when their very belated stats come out in a couple of years. The Fed and everyone else looks at lagging data. Until that second week of December when Powell crapped his pants on the GDI and other leading data. He will be cutting in March if not sooner.

Talk to small businesses. They will tell you we are in a silent depression. The stock market will be the last to know. Watch the crash come after these ATH on the few indexes with the mag 7.

“Talk to small businesses. They will tell you we are in a silent depression.”

Uh, small businesses are booming. Help wanted signs everywhere, staff saying they’re overworked, and in anything in construction, all you hear is “we have so so so much work.” Just look at the spending numbers. Look at corp earnings. This is a very strong economy.

Uhh, corporate earnings have nothing to do with small businesses. Do you have any idea what you’re talking about?

Pudget Sound area (greater Seattle area).

The biggest risk would be to step out of the market.

Any SFH priced close to reasonable goes pending in hours to days. Absolute trash that should sell at land value is bid up by investors gambling on price increases and by desperate families.

Sure we’re are not yet back to the blip that was COVID but the upward trend is back and firing on all cylinders.

The long term direction is down, for years. Real estate is not liquid, treating it as such high inherent high risk. Unless you’re highly experienced with exiting, it’s a bad time to buy.

This isn’t exactly correct. Good houses in nice areas are selling but bad ones are just sitting there bringing the overall price down (when they finally do sell). I did see also see one crap house in Redmond sell. It was a super convenient area for Microsoft workers, though, and was the only one for sale, so that’s why it got swarmed. So, how they sell a house here is by pricing it low and creating a bidding war that drives it up over what people would’ve paid anyway. Difference is now the bidding war price has to be -75k or something where it used to just be the “redfin value.” I’m not sure the Fed has the cojones to see this thing all the way through, though. There need to be more layoffs to increase housing supply and scare more people back to the office. Wouldn’t hurt to start enforcing laws again, too, to get moms to want to go downtown (civilization).

I’m in Hollywood Fla with daughter helping her stage a STR arbitrage (all short term rental terms) that she will be hosting for a client . The home is 1000 sq ft 3BR 2 ba single family 6000 sw ft yard. Built in 1950s . Met a couple of realtors who are having open house this weekend from 11-6 on a Sat. She said got to work hard no sales no commission needs to eat.

These homes are listed for around 400-500k when in 2012 they were less than 150k. The neighbor I met a retired 80 year old said I was first English speaker he has seen in a couple of years as far as new neighbors. All of these homes are in poor condition esthetic wise but bones are fine (hurricane and flood resistant). Roads are packed beach had very few retirees restaurants are half full . These bubbles take a long time to deflate but the buyers are on strike . I personally do not want asset deflation but want low inflation lower rates and stable Economic growth with a federal government that can allocate capital to economic growth businesses. AI and chips is a step in the right direction . The home demand in many parts of the country are on strike and will continue. New homes appear to be the best option for buyers a better reflection of value

My friend selling his house in Ft Lauderdale for $2m+ has had a couple low ball offers and a couple real buyers take tours, but not pending yet. Definitely a slow down there he says.

Speaking of ai and chips I look at all that tech both in the companies making them and in end users having deflationary forces in the future like tech usually has. It reminds me of Qualcomm in the late 90s. Real company with real earnings and great upcoming products but mania was getting out of control. They of course are still around making better tech and making money with deflated prices.

Did your friend buy that “$2 million house” in 2019 for $800k? If so, that might explain why it’s not selling.

No. Over 10 years prior to your year and over $1m.

Ok got it. I’ve seen people post houses for 2.5 times what they paid from 3 years ago.

High mortgage rates “freeze” the housing market, due to high Mortgage payments. Typically, the market just stops, but house prices stay high for about 2 years. Then, after a couple years of frozen housing market, house prices go down sharply. That’s what we’ve seen in the SF Bay Area and LA over the last many decades. We haven’t seen rent prices go down during periods of high mortgage rates.

My friend during HB1 listed his home for sale for 785K.

He finally sold it for 480K after 2 years.

During this 2 year period her has offers of 740k 680k 630 etc but he rejected them all.

Car biz mantra: “Your first loss is your best loss”.

Your friend proved the theory.

There’s one big buyer

Blackstone just bought Tricon which is like buying 38K homes

Don’t try to use twisted and manipulative innuendo to misrepresent this deal.

Blackstone is a PE firm that does leveraged buyouts of other companies that are publicly traded.

So what is Blackstone buying? It’s buying the shares of a publicly traded company, Tricon, where it has already been a huge investor for years.

You could have bought Tricon’s shares on Thursday for about $8.65. You would have bought shares, not houses. Then Blackstone’s bid was disclosed at $11.25 a share, and on Friday, shares jumped to $11.07. You could have made a bundle on those shares (not houses) that you could have bought on Thursday.

Howdy Folks. Housing Bust 2 has a long way to go. Doubt I will be around for Housing Bust 3 and could actually pass on during Housing Bust 2. Been watching Saturday Night Fever reruns , because, I believe the 70s 80 s are back. Learn your history youngins and find truth in the Wolfman Richter……..

Ive been getting an increased number of views lately on LinkedIn. I’d say last three months have seen a definite pickup in activity. Are skilled jobs are getting harder to fill because people won’t move for opportunities, being locked in 3% mortgages?

I have friends who got laid off from FANG companies 6 months back.

They are in HI tech and still not yet found jobs.

Job market is good at lower wage spectrum not only much for highly paid tech engineer’s.

Thanks Wolf for the numbers/charts that continually allow me to see reality better.

My view:

The FED’s interest rate control, very large research and data access and budget, QE, and QT make U.S. recessions very unlikely baring exogenous events like world war and world pand*mic.

AI, the coming coming quantum computing, and seemingly unstoppable general tech improvements indicate not a tech ‘boom’ but a much larger and longer tech ‘BLOOM’.

I don’t expect housing prices to have a large contraction, not in an economic ‘bloom’.

This technology ‘bloom’ will gradually extend all over the planet. Now is the time to invest for the long haul in both high p/e tech and low p/e companies that have a Warren Buffett ‘moat’ both in the U.S. and abroad.

The biggest growth problem is in economic equality both in the U.S. and even more with the rest of the world.

Buckle down, its going to be a hell of a ride.

Tech boom would continue but companies who would benefit from all these are still unclear and new companies would emerge.

Do you remember dotcom boom.

Everyone thought Cisco is the company to be the big winner along with Intel but we all know how do these ended up.

The other issue is that it’s questionable at this point whether improved tech is really going to solve humanity’s most pressing problems, which are finite resources (energy, water, food, etc.).

I see the seeds for a global Malthusian struggle in the coming decades, and don’t really see tech fixing it.

I disagree about the finite reources bit, specifically energy.

At lease here jn USA: we have record energy production, thanks to natural gas. And now we have all this natural gas liquids (not LNG) which refineries are discovering they can turn into other petrol products.

The real barrier to energy prodiction is gov’t regulation, not geology. Humans can decide to loosen this regulation at anytime and the problem will go away.

MM, we have record energy production, but we’re expanding our population way beyond the infrastructure’s ability to handle it.

Energy is still finite, at least in its current form.

Yeah, turning on the ice maker for your scotch with your smart phone from 50 miles away so it’s ready when you get home won’t help much……homeless or close to homeless have absolutely no need for it…..that should be proof enough.

MM should listen to Einhal’s comment, but he has already likely made that “leap of faith” into that magic kingdom of cosmic fantasyland, (even if it was taught and wired into him when he was so young he has no awareness of it). and therefore, sadly for all the rest of us, he can’t. The words Time and Finite mean nothing in the context of expecting an Eternal Life.

Has there ever been “economic equality” at any point in human history?

Didn’t think so.

There’s been times where it’s been a heck of a lot better, though

Howdy Thomas. “Buckle down, its going to be a hell of a ride.”

Would just like to add the word LONG before ride….

You have to make a case it’s not priced in already.

Bobber,

The equal weighted S&P is 16 times forward earnings and companies are making money and the world is re-knitting itself after the pandemic and the zirp.

The ‘magnigicient seven’ account for ~25% of the weighted S&P and at this point most or all of them probably deserve their high P/E’s because of the tech bloom and the fact that they are already making money.

Most of my money is in safe, low P/E, global companies that have big moats and pay big dividends but I have one high P/E with a big moat.

The world is entering another big economic expansion that will float almost all boats.

TC: what is your definition of low PE and high dividend? Personally I feel like 16 PE is still wayyy too high.

The one stock I own has a PE of 1.2 and paid out a total of 20% in dividends last month. That to me is a reasonable PE and div yield – not 16 PE and whatever the mag7 are yielding these days.

Forward earnings?

I occasionally look at homes for sale on Zillow, just to see what’s out there, and how much bang for the buck you get now. In addition to astounding increases in dollar per square foot of home, HOA fees have skyrocketed in recent years. It’s very sad. Prices on almost everything are still in Looney Land compared to just seven years ago. I went to a Home Depot to buy a half inch 2’x4′ piece of plywood. $29.99!!! Was less than $15 in 2016. That’s what $300 buys you now, ten pieces of 2×4 plywood!

Prices are regional.

I have some rental houses in the midwest and I probably they probably would sell between $120 sq ft to $150 Sq.

So here is some examples according to Redfin regarding sq ft prices. I added what a 2000 sq ft home would cost too

San Francisco = $874 sq ft (1.7 million)

Austin = $301 Sq ft ($602k)

Denver = $343 ($686k)

Kansas City = $151 ($302k)

Dallas = $234 ($486k)

Oklahoma City = $151 ($302k)

New York = $542 ($1.1 mil)

LA = $614 ($753k)

That being said, this is for median sale prices. Take out the new homes selling for $600k in the midwest then existing homes in places like KC, Dallas, and Oklahoma City are selling for $120 to $130 sq ft. That is affordable.

Yeah Debt-Free-Bubba, its going to be a hell of a LONG ride.

I don’t think I have seen a better LONG term entry point but I only have 20 years of experience.

Are you high? Stock at all time high is the best LONG term entry point? I guess so, you will have to wait LOOOOONG time to get back what you put in there.

This is wonderful insight to the general market condition but local real estate markets may differ. Where I am here in Northern NJ, the market is still frothy due to extremely low inventory. Latest house we bid on in December we bid 60k over asking and lost by 10k. (Sold for $840k) We also refuse to give up inspection. So at least in our area of limited/non-existent new building, buyers still outnumber sellers. No buyer boycott here. Nor will there be in the foreseeable future. Prices may stabilize but they’re not showing any signs of slowing down at all. As much as I wish they would! We’re in a rental that we’re being asked to leave by summer so we’re also a poster family for why it’s (sometimes) better to own than rent.

We’re in a rental that we’re being asked to leave by summer – Ha that is the same situation myself and my family are in. The first time landlord has gotten greedy he thinks he can be a slum lord now, even after being obedient and paying his rent increases over the years. Things have gotten crazy, yes we are living in the matrix.. greed knows no bounds, collectivity we are a society are trending downwards in terms of living standards with high inflationary times lead by the idiot policy makers and wall street bankers.

I hope all the housing bulls with their heads in the sand about the regime change in long rates get absolutely crushed by the financial weight of their precious leveraged wood boxes.

You’re all speculators hoping to profit from continued financial repression and de facto extortion of the next generation.

You find joy in forcing your fellow man into economic servitude… just shameful.

One day, I hope you all look back, and realize with enormous regret — you made the world worse.

Amen. I don’t know why us homeowners can’t admit that home prices NEED to come down and it’s the best thing for this country, even if you own one. I bought mine in 2012 and I’ll openly admit I got LUCKY, and I wish it’s value would approach back down to where it was back then, because that’s what’s best for the country. But everyone is just out for themselves. Live in the dang thing, but stop trying to use it as a profit center while nobody else can afford a place to live.

I own my home and want to see its theoretical resale value come down.

Prop taxes and insurance go up with the increase in theoretical resale value – so overpriced homes cost us existing homeowners more money even if we have no plans to sell.

I do not understand why people who are not looking to sell their home, care so much about its theoretical resale value.

NB: I’ve put blood, sweat, and tears into my house. Its worth more to me than it ever will be to you.

I am not looking to sell (ever) but I def want my house values to go up for obvious reasons. When rates come down you may use your house as an ATM/cash out refi to purchase another house as part of a diversified investment strategy (besides stocks etc., RE can be an excellent addition to your portfolio). Not financial advice…..just my personal experience.

Kelly….Lol see, you are the problem. People who are just out for themselves. Seems to be the norm in our country. You’ve got yours, right? To heck with everyone else , you’re here to make money! When everyone thinks like you, the system implodes itself

Blake, why will the system implode exactly? Of course people are out for themselves in a capitalist country. “A nation’s economy is described as capitalist if it’s based on private ownership and profit. ”

In a way we are all chasing and we are all in competition. If you apply for a job you have to beat out other applicants. Once you get the job you are in competition with your colleagues for the highest merit increase and bonus. If you don’t want to play the game you get left behind. Don’t hate the player, hate the game?

Was out to MS Swamp’s hairdresser 15 miles outside of DC and noticed the same things outlined in Wolf’s article. As you approached the townhouse development in the exurbs of DC the first thing you notice is the proliferation of signs of new homes for sale. Then as you get into the development of existing townhomes you see zero homes for sale. What does that tell you?

Here in the Coachella Valley (Palm Springs – Palm Desert area), the winter months are peak season due to tourist season and summer heat. Presently, there are a lot of listings on Zillow with price reductions and much higher days on market compared to last year. SFR prices have gone crazy compared to pre pandemic prices, largely due to the short term rental phenomena.

Homes in the community that I’m most interested in are up approximately 80% since 2019. The monthly base cost of ownership, mortgage, property taxes, HOA, and property insurance have more than doubled from the low $2000s to low $5,000s. Affordability is at the lowest level for middle class families since I first moved here in 2007. Something has to give.

Going back to short term rentals, I know a couple of investors who are listing their rentals due to lower rental days per month and lower rental prices, they are just barely now making money, and they are tired of the hassle of dealing with party animal idiots.

A friend of my daughter had a short term rental in Palm Springs. Cute house… MCM desert style done right. She sold it because the HOA was making noises about restricting short term rentals. No point in keeping it. She sold it and rolled the money into the ocean front duplex with an ADU that my daughter is renting space in…

The HOA restrictions of the VRBO/Air b n b thing doesn’t bode well for “investors”. Either it will be long term rentals or nothing. Ours did it due to clowns that don’t know how to behave in public.

I am guessing SFH’s without HOA’s are increasing in value over SFH with HOA’s due to those type of restrictions on short term rentals.

Starting to see new homes in the fringe suburbs around Phoenix sell for less than resale. Prices reductions in resale, but inventory is still low. If you bought in the last 2 years you are underwater to sell in most areas of phx. Vegas too with higher days on market. It could still go either way but I’ve got a bad feeling. Even though it was a different set of circumstances, I remember in 2006 it felt a lot like this, negative signs all over the place if you looked and everyone telling you why it couldn’t happen.

Sellers have missed the boat by more than 18 months, when they could sell their homes at a premium. Between the rate hikes and lack of buyers at some point home prices will come into equilibrium. This is classic suppy and demand. Wishful thinking and hoping on the part of sellers will not move their homes. The majority of homeowners are locked into lower rates from the pandemic years and before. They are not going to jump into the market where rates are over 6%. It’s going to take time, but it will iron itself out over the next 18 months or so.

That 2nd chart, Existing Home Sales is definitely interesting, it makes it seem like we should be pretty close to the point in time where enough sellers start lowering prices to get things moving.