Mortgage-rate buydowns, “smaller product footprints,” and “de-amenitizing” to bring down payments: D.R. Horton.

By Wolf Richter for WOLF STREET.

Homebuilders, in order to sell new houses at a decent clip in this new mortgage-rate environment – even as sales of previously owned homes have collapsed because sellers refuse to accept reality – are using a variety of strategies, outlined by D.R. Horton in its Q3 conference call, including:

- Mortgage-rate buydowns

- Smaller houses (“smaller product footprints”)

- “De-amenitizing” the houses (cheaper appliances, floors, countertops, simpler roof, no deck in the back?)

- And other incentives (free upgrades, etc.)

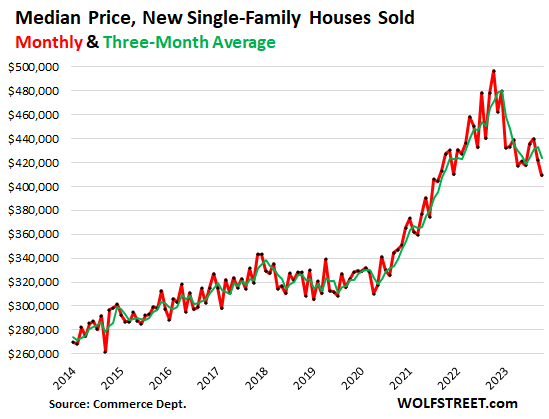

So the median price of new single-family houses sold in October fell by 3.1% from September, to $409,300 (red line), the lowest since August 2021, down by 17.6% from a year ago, which had been the peak, according to data from the Census Bureau today. The three-month moving average is down by nearly 12% from its peak in December last year (green).

These are contract prices and do not include the costs of mortgage-rate buydowns and other incentives such as free upgrades. But they do reflect the lower price points due to smaller footprints and the “de-amenitizing.”

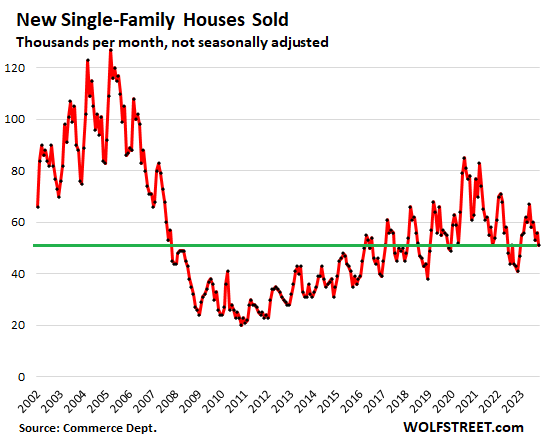

Sales of new houses – not seasonally adjusted, and not the annual rate of sales – fell to 51,000 houses in October, and while this was up by nearly 19% from a year ago, when the market was freezing up, it was still down by 7% from October 2019.

As you can see in the chart below, these sales levels would be nothing to write home about. But in the new mortgage-rate environment, and compared to the collapse in sales of previously owned homes (-27% compared to October 2019), they’re decent and document the effectiveness of bringing down payments via mortgage rate buydowns, “smaller product footprints,” and “de-amenitizing”:

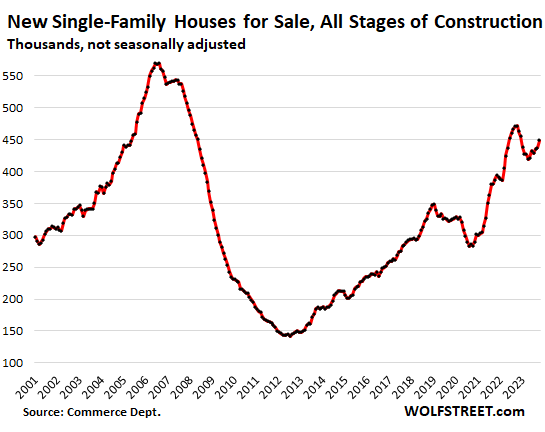

Inventory for sale of new houses at all stages of construction rose to 449,000 houses in October, which translated into 8.8 months supply at the current rate of sales – more than ample inventory and supply, and homebuilders are motivated to make deals to move this inventory:

Homebuilders have figured out this market, unlike current homeowners who are thinking about selling. Homebuilders have to build and sell homes no matter what mortgage rates are, while homeowners who’d want to sell are clinging to their hopes that “this too shall pass,” and they’re not putting their homes on the market, as the national median price, after peaking in June 2022, is on the way down.

Homebuilders are now aggressively competing with sellers of previously owned houses. And they also have to compete with the rental market, including newly-built-for-rent single-family houses by large landlords.

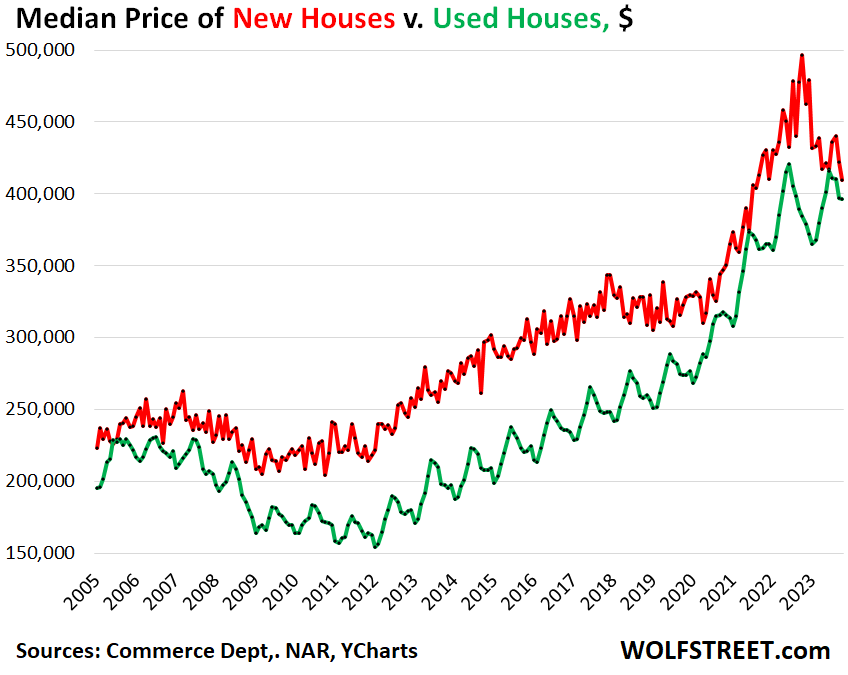

And monthly payments via bought-down mortgage rates make a difference and lower price points make a difference. The national median price of new houses has been falling faster than the national median price of existing houses (via the National Association of Realtors), and they’re now very close, which is unusual:

- Prices of new houses: -18% from peak (October 2022), $409,300

- Prices of existing houses: -6% from peak (June 2022), $396,100

What D.R. Horton said.

In their earnings call for Q3, D.R. Horton executives addressed questions about mortgage-rate buydowns and their other strategies to keep sales up in this mortgage-rate environment. Here are some of the key points (transcript via Seeking Alpha):

“To adjust to changing market conditions and higher mortgage rates, we have increased our use of incentives and are reducing the size of our homes where possible to provide better affordability for our homebuyers. We expect to continue utilizing a higher level of incentives in fiscal 2024, particularly rate buydowns in the current interest rate environment.”

“The average rate can move quite a bit through the quarter, but we tend to stay about 1 to 1.25 points below market at any given time.”

“About 60% of our total closings are used with some form of a rate buy-down … the most successful incentive we have seen.”

“Our buyers are focused primarily on affordability. And for us, the way we deliver that affordability is through the monthly payment process. And that’s obviously been a big driver for the rate buydowns, but also introducing smaller product footprints, and de-amenitizing some of the homes a bit and letting people do things to improve their homes after the closing when their financial position perhaps has changed and they can afford a little more.”

“Over half of our business [is] first-time homebuyers because despite what’s happening with interest rates, those buyers need a place to live. They don’t already own a home, so they’re not a discretionary buyer. They’re in the market looking at buy versus rent opportunities. So, if we can stay competitive with the rental market on that front, we’re going to continue to capture first-time homebuyer market share.”

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I’m seeing some stalled developments. What’s weird is one stalled out seemingly before prices peaked and when rates were still low. It’s a townhouse community “starting in the $700ks” or something. The prices are way too pho keen high.

I worked with a guy from Florida. Smart guy. He owned a townhouse in one of these new developments, and prices picked at $400K (I think) right before financial crisis. He later was buying any townhouse in his development every time price hit $45K (not sure if this was bank auctions). I think he ended up with 9 townhouses over the next year or two.

Sounds like a good buying opportunity. The biggest mistake I made back in 2008 was being a broke 20-year old college kid with zero dollars available to buy distressed equities and real estate.

I didn’t miss it. I was buying big banks on the cheap (after collapse, $4 to $8). Then they went to a dollar (B of A, Citi), or zero (Washington Mutual, Wachovia).

🤣

Ah those scars are funny 15 years later, but they weren’t funny at the time.

Let’s add some perspective, first math, then logic.

1. Let’s assume a $1 million house with 20% downpayment @ 7.5% 30 year FRM. EMI on $800K loan will be $5,594. If you get the rate buydown for entire 30 year FRM to 5.5%, EMI will be $4,542. This is same as a cash discount of $150,400 because this 7.5% FRM EMI for $649,600.

2. So that’s around @15% cash discount on a $1 million house. This discount percentage remains same irrespective of house price. You can try the Math.

3. So now the median price drop is 18% with an additional 15% cash discount, you are looking at 30.3% actual drop (0.82 × 0.85 = 0.697).

4. Add 3% BLS inflation, 1% maintenance and 1% property tax, 1% interest expense (4% @ 25% house price), and we are looking at 34.4% correction that homeowners must be willing to accept to compete with new homes!

Finally, lol to the “smart guys” that constitute the 31% mortgage applicants that used cash out refinance (whole mortgage @ 7.5%) after failing to qualify for helocs (only new loan @ 7.5%) hoping that Fed would Pivot and they would get out of this hole.

Leo,

The costs of mortgage rate buydowns are neither this simple to figure nor that high.

Homebuilders have their own mortgage companies that originate those mortgages, and they use futures contracts, etc.

In terms of figuring the value of a buydown, there’s the issue of the discounted cash flow going 30 years into the future, which dramatically reduces today’s cost of the buydown. You can look up the formula and give it a shot. Then there’s the issue that mortgages have a very high probability of being paid off entirely in less than 10 years, either when the house is sold or when the mortgage is refinanced, which also dramatically reduces the cost of the buydown.

So here is what Pulte said in its earnings call a month ago about the costs of mortgage rate buydowns:

“We continue to use the permanent 30-year buydown as probably our most powerful incentive.”

“I’ll remind everybody, what we’ve done is we’ve simply redistributed incentives that we’ve historically offered toward cabinets and countertops and things of that nature, we’ve redirected those to interest rate incentives, and I think that has been the most powerful thing for that buyer group.”

“There are other buyers that decide that they don’t need to go all the way to 5.75%, and they’d like to have a little bit higher rate and use some of the other incentive money that we’re offering for other things that they see value in. We’re seeing about 80% to 85% of our buyers are getting some form of incentive towards interest rates. That doesn’t mean everybody will go to 5.75%. Just some fraction of our total sales [25% CFO specified a minute later] end up in that very lowest category.”

About the costs of the buydowns and incentives: Their “incentive load” is about 6.3% of the average purchase price of $549,000, “about $35,000” per house, and “the majority of that incentive is rate buydown for financing support.”

When they were asked about details, they said that they didn’t want to give away their key trade secrets.

“When they were asked about details, they said that they didn’t want to give away their key trade secrets.”

Major red flag. Sounds fraudy.

No, just reality. Rate buydowns are their biggest most successful promos ever, and they want to project their secret sauce. Makes sense to me.

“Then there’s the issue that mortgages have a very high probability of being paid off entirely in less than 10 years, either when the house is sold or when the mortgage is refinanced, which also dramatically reduces the cost of the buydown.”

If the probability ends up being lower than they’re anticipating, what will be the consequences?

Those mortgages are sold to the GSEs (Fannie Mae, Freddie Mac, etc.) which securitized them into MBS. So the costs of the rate-buydowns come up front for the builders.

So the price for new homes didn’t really drop, they just give you less house for less money. Like not buying 10 gallons of gas for $50, you’re buying 5 gallons of gas for $25.

By the same rationale, in the prior years, the spiking prices of new houses didn’t actually rise because the houses just got bigger and fancier??? (they did)

But the prices did change, didn’t they? On the way up, and on the way down.

To a point, but a 900 square foot house keeps the rain off you just as well as a 3000 square foot house.

Jim, this was exactly my thought. It’s not much of a value proposition change. It’s just a downward adjustment in their target market.

And in that regard, I’m not sure how well it will even work. The folks looking for luxury townhomes are generally not the same as folks looking for moderate townhomes. And the folks willing to accept a moderate townhomes ALSO can’t afford the prices the builders will want to demand.

It makes me wonder whether the builders are trying to force their customers into a lower segment while still getting their max money.

I personally am not willing to pay $5000/mo on a new, “luxury” townhome in suburban Philly.

I’m definitely not willing to pay $3800/mo for a non-luxury townhome in suburban Philly.

Maybe they’re seeing things that are invisible and/or incomprehensible to me. But I simply can’t understand why the answer isn’t simply “We need to accept a 15% profit margin rather than 24% to provide homes to our target market segment.”

“But I simply can’t understand why the answer isn’t simply ‘We need to accept a 15% profit margin rather than 24% to provide homes to our target market segment.’ “

That’s the crux of capitalism, isn’t it? Greed. Growth. Always more. Never happy with stable profits. That’s every company I’ve worked for.

Or on the flip side look at it how the banks for an investor look at it… if you have 1 million to loan or invest and can pull 7.5% return, you will double your money in 12 years.

If you’re a buyer of a $1 million house, you will be hopeful that it’s still worth a million dollars 12 years from now. On top of that if we have 3% annual inflation for 12 years, that house needs to go up $400,000 to hold even 😳

If you’re in the 30-year alone program for a million dollar house, you’ve only paid down 30% of it the first 12 years.

Different perspective.

In Woodstock, GA, super hot market, a 72-home subdivision started buildout early in 2022. The developer got 3 homes built by May of this year, then everything stopped. None of these houses have been sold nor have new ones been started. Nothing. But what changed was the asking price went from $600Ks to $700Ks. The housing market continues to reside in insane territory.

Material cost increased by 50% since Covid, and labor is way up too. The builder just can’t build today for yesterday’s price.

Material costs have dropped by a lot over the past year, and costs of appliances, etc., have dropped some as well. But labor costs continued to increase. All builders talk about their material costs and some other costs going down, and lead times are way down, and the speed of construction is back to normal, so all these costs associated with endless delays have gone away, and overall costs have come down, despite higher labor costs, which is why builders can lower their prices directly or indirectly and still largely protect their margins (they might give up a little).

@ Wolf re: materials costs. The largest materials inputs into a building are lumber, windows/doors, concrete, drywall, sometimes steel, and all the finishes.

Futures prices for lumber are back to normal, yes, but physical supply is still about +50% pre-Covid. Concrete is at an all-time high. Copper, despite futures down, actual product is still at peak. Windows/doors still seeing price increases every few months (perhaps because of the labor component). Everything from roofing to appliances to tile to wood flooring, no drop from peak.

A mass builder gets better pricing on all the above, but they also got better pricing before all of this, so their material costs likely haven’t dropped much from peak either.

I agree with Wolf here. Labor is still high, but that’s what we need a recession for.

I’ve got a friend at work who’s got a 12×27 concrete patio on the back of his house. A contractor is charging him $30K for a no frills put a roof over it with a couple of outlets, 4 recessed cans & a ceiling fan. The materials are absolutely no more than $5K and that’s being generous.

To use the $30K as a starting point for building his entire house which cost him $290K two years ago who extrapolate to a $1M.

This is near criminal, but consumers have bought into the much higher inflation expectations, so they’re part of the problem as well. Covering a deck is discretionary. Having to pay some plumber an egregious amount to fix a bust water line running to your house is at least a critical need.

Again, we need a recession to sort out all this services inflation which is running rampant. Wolf has clearly outlined this issue here on his site over the last 18 months.

Give it up!!! That’s malarkey.. I don’t know where in Florida you are speaking of. The only discounts down here are homebuyers dropping their prices, but nothing like reductions you are speaking of. Builders are giving buy downs such as interest rate reductions and less expensive appliances and so on . But unless some bank possession not near that price, they are not given away. Nice Story.

“they are not given away”

As if -5% or even -18% is giving it away. Sheesh.

I believe he is referring to the period between 2008-2012.

Let’s take that 18% and double it, then we can talk about housing moving towards affordable. At that point, builders will cease to do these extra-large rate buy downs. Insurance is STILL sky high as are property taxes. Maintenance is STILL sky high.

With a little luck, we’ll get a real recession by Q3 next year, perfectly timed to affect the election. What would be great is to see Big Tech do their best to influence the election only to have a real recession undo all of their efforts.

I’m old enough to remember when the previous president chewed out the Fed for daring to raise interest rates.

And the president before that had seven years of 0% with one .25% increase at the very end. What’s your point?

The 08 crisis really kicked into overdrive as we went into the election that year.

There’s a difference between adjusting the rates, etc. to stabilize the economy and doing it to stabilize the government. The Fed is an independent body for just this reason. Thank goodness Powell had the fortitude to act as he felt was right against the wishes of and public pressure from others.

The Fed also did what it felt was right for the years after the GFC. You can argue all you want whether the current pain was worth the success they achieved with the economy then but it was done for the sake of the economy, not the sake of the president.

In fact, the government then cooperated with the Fed to minimize the impact of the GFC because the risk was it instead becoming Great Depression 2.0. Congratulate them both on that success.

Lastly, everybody tries to influence elections. What’s important is whether they do it by educating voters with fact or by bombarding them with fiction.

Who were LBJ and William McChesney Martin, Alex?

Did I win?

I don’t understand you people wishing for a recession.

Some of us wish for a recession because we see the current economy as the equivalent of driving on an overheated or underoiled engine. You might get a few miles farther down the road, but you’ll do far more damage in the long run.

Lol, so you’d rather blow up the engine and walk the last 40 miles?

Hope you have a warm coat and plenty of snacks stored up.

You completely misunderstood the analogy.

No. I’d rather stop driving and call for a tow before I blew my engine up.

The only way to effectively reallocate capital is through actual bankruptcy. People who burn money and waste resources should have neither.

Well, I am not wishing for one but I am pretty sure it will come. You cannot have this huge a party without a hangover. It is the natural scheme of things.

That’s why I feel that the Fed’s mandate should include sustainable growth – not blowing up bubbles and then trying to achieve a soft landing. There are enormous human costs to the latter but they never learn or just don’t care.

It seems as though the Fed guvs were most enchanted by the notion of transitory inflation when their fingers were in the pie. I sure hope that graft opportunity is gone for good.

There is no means of avoiding the final collapse of a boom brought about by credit expansion. The alternative is only whether the crisis should come sooner as the result of a voluntary abandonment of further credit expansion, or later as a final and total catastrophe of the currency system involved.”

agree with the BOOMer ranger,,,

U can take it to the bank, if any are left, it is WHEN,,, NOT IF,,, the very clearly BK USA and most of our banks crash, or at least ”deflate quickly.”

Of course it’s different this time, but only WHEN!

Well, the sustainable alternative is probably no growth. Then questions about wealth distribution quickly come to the front. Would change politics to much to the powers that bee.

You got that right, brother. WTF is wrong with people.

“I don’t understand you people wishing for a recession.”

Continuing to drink is not a valid strategy for avoiding a hangover.

Surely has worked for many folks I have worked with who came to work fully soused almost every day, and in any case ”hit” the bottle early enough each day so that they never were ”hung over.”

Used to be mandatory for all the adults on a job site to go slam beers for lunch, or just put the whiskey in those great big coolers full of ice, and ”nip” it all day long…

Almost all the older guys, when I started, had fingers missing from doing so during the transition from hand saws to power saws… but they kept on w the alc.

VVnVet – man I can’t imagine that. Every now and then I’ll have a single beer at a lunch meeting, and can barely get thru my work the rest of the day….

Well, then, let me spell it out for you: recessions are good, healthy and necessary to purge an overheated economy of malinvestment while rewarding the responsible and punishing the reckless. They re-balance everything.

Some of us like organic economies, not fake ones where central bankers just print money hand over fist and turn the entire world into one giant, speculative bubble orgy where the prudent and the working class get financially raped while the reckless gamblers are treated as a protected species.

In short, it’s not a recession we ant, per se, so much as a return to a real market. A recession being allowed to actually happen, and happen with the necessary clearing of the zombie companies and other chaff, would be the surest sign we’re on the way back to “normal.”

@Depth Charge and Zaridin

Well said. Don’t know anyone who’s actually wishing for a recession, we just want the natural balancing forces in the economy to be allowed to act. To help bring prices back normally into line with Americans incomes, pop the housing bubble and reign in all these other speculative bubbles making even essentials in the US unaffordable.

It was excessive overstimulus from both Fed policy and fiscal policy that caused this inflation and Everything Bubble to begin with, not just “printer go brrrr” but the short sightedness of massive QE and even buying MBS when US housing costs were already out of control. Like DC is saying, recessions and temporary bouts of controlled deflation aren’t always bad, esp if they happen in overheated sectors, and Wolf’s article is showing we don’t even need a recession for housing bubbles to unwind as long as we step aside and stop re-inflating the bubbles with loose monetary policy. It’s the natural corrective to keep things in the USA affordable and make price discovery possible.

“I don’t understand you people wishing for a recession.”

Fiat justitia ruat caelum

All the people who hate money.

“All the people who hate money.”

Just ill gotten money Tony. Wolf will even tell you that some have been sacrificed so you can pretend to be better then them ;)

Well you know where the “love of money” takes you…..

It’s not that complicated. I don’t wish for recession but I fully understand the sentiment.

Occasional recessions are like small fires that clear dead wood from the forest that is our economy. You can put them out, but eventually the fire that inevitably comes is far more destructive. Some of us believe it letting the little ones burn.

Money needs to be linked to what it is intended to represent – an exchange of human time. It feels as though we are drifting away from that reality, and doing so is dangerous. The more disconnected, the more painful the rebalancing.

Excellent analogy, Random guy 92

John McPhee included a vignette in his book Control of Nature about the fire control efforts in the San Gabriel mountains above Los Angeles, and the horrific results of not allowing wildfires there to clear out the dead chaparral fuel that creates uncontrollable mudslides that wipe-out expensive neighborhoods built on the gorgeous hillsides. The more authorities “control” the fire problem, the bigger the mudslide disasters.

It’s as good an analogy as I’ve ever seen:

-Fire-control/mudslide

-Maximum employment/eventual recession (or worse)

Fun reading too! John McPhee is a national treasure!!

Recessions are good for ending bubbles. Everything got very expensive while incomes stagnate for most people. Bring the recession so that prices can come down to earth.

Prices only stay high as long as there are buyers who can pay it. A major recession would transfer a huge chunk of the housing stock to large corporations, making the population even poorer.

“I don’t understand you people wishing for a recession.”

What I wish for is a normal economic cycle, without interference to prevent recessions at all costs.

Wonder how long builders can “compete” with dropping prices and their ability to give incentives run out. De-amenitizing and down sizing will eventually find its way to the bottom line.

At some point the selling price line meets the production cost line and it no longer makes sense, or money, to build houses. Then what?

Maybe a clue would be to look to some of the major builder’s P&Ls to see just how much fat there is on the old bones to keep plowing up the parched ground?

I guess there will be survivors and non survivors as all this plays out.

Thanks for keeping us up to speed on this.

Builders have 30-40% gross margins. So that’s where they can go with all other things being equal.

I have to wonder about the information provided. I don’t know, but is is possible that gross profits jumped from ~18% all the way up to 30%-40%? Net is where added “incentives” are drawn from as cost of sales.

According the HAHB’s 2020 builder survey:

“Builders averaged a gross profit margin of 18.2% and a net profit margin of 7.0% in 2020, according to the latest NAHB Builders’ Cost of Doing Business Study. The nationwide survey of single-family builders revealed profitability benchmarks for the home building industry industry.”

Lots of large cities are trying to entice home owners to build the small guest houses on their property to help with affordable housing. Phoenix I think has legalized it and Los Angeles as well as many other cities have proposal in the works.

That cannot be good for the home builders in the future.

One answer to bubble priced housing is to build more houses.

No, we need to pop bubbles

The State of WA passed that same legislation, overriding local zoning laws. Our town is updating its ordinances this month for the change. You can now add up to two Accessory Dwelling Units (ADU) on most single family lots.

Mr. Imposter…I can’t agree with you more. I have been a builder/remodeler for the past 35 years…and have survived recessions and the Great Recession(just barely). Here is the grim reality…land procurement & development, utilities, taxes, permit fees, impact fees to local governments, rising labor rates, expensive materials, truss rafters, and just the cost to finish out the interior of a home…has exceeded the production cost line to build a new home, and sell it for a worthwhile profit. Our government allows my corporation to make a minimum of 22% profit margin…which allows me to cover my staff, and put “some” money back in the corporation.

That held true up into about 15 years ago…not anymore!! After the 2008 Great Recession, ALOT of builders left this playing field, and has been slow to come back. It is predicated that this industry will eventually disappear!! Many builders have grown older, like myself, and are getting out of the business. There is a genuine lack of good quality subcontractors, because they are getting older, and leaving the business. What’s left are many young people that DO NOT want to be a part of this business, because they choose to be in a tech related field, where they don’t get there hands dirty. Most of this business now comprises people from other countries, here illegally, working for cash, don’t speak hardly any English at all, and very unskilled…why??? Because nobody else wants to do this kind of work any more.

The new housing market of today, 2023, is getting harder and harder, to sell a home, to make enough profit to justify the massive costs involved to build it!!

Higher interest rates, and the banking industry, has not made it any easier either on us builders…my advice to anyone who has the desire and the means to build a new home…DO IT NOW…in another 5-7 years…this industry will go to the wayside…just like the Edsel, the Beta tape machine, the hand held wall telephone, and the checker at your favorite Wal-Mart!!!

De-amenitization, a wonderful new noun, best since enshitification (replacement of intelligence with half-baked “AI” in customer “service”)

Ok, I was wondering what that meant. My brain was thinking it was a different way to configure interest on a 30 yr fixed mortgage, but I did not find anything when I googled it. Thanks

Do you remember the “Texas Dictionary” or Rich Hall’s, “Sniglets”? “Enshitification” is up there with the best of ’em.

Yes, I miss Rich Hall and “Sniglets.” He seemed to come up with witty one or two syllable words. But I admit “enshitification” filled a need. Many uses!

Where is commenter Ambrose Bierce when we need him?

They use it as a verb. Big red x on your english paper.

Words ending in -ion are how you turn verbs into nouns. The verb would be de-amenitize.

Will be interesting to see what the next Spring season will bring us. Will it bounce back like every time and as good as the one we just had this year or will it be just like all the housing cheerleaders will like to say “This time is different” and we continue to slide down in Spring…will be interesting.

Btw, SoCal must be tail end of the Titanic, still taking a long time for any significant decrease. Overall probably down but nowhere near as fast as markets like Austin, Boise…etc unfortunately…

I think it will come down to how motivated sellers are. Inventory is already stacking up in SoCal out of season, so there should be even more by the get into Spring because no one is buying:

http://media.sdar.com/stats/stats.htm

Austin is down, but it’s version of down is like if your house suddenly flooded up to your hips and then you managed to bail enough water to where you were only wading around knee-deep. It’s not nothing, but there’s still a ways to go. The push now seems to be to manipulate popular perception: that water up to your knees is the new dry, and that taking a John boat from your bedroom to the kitchen is what everyone’s doing.

Your analogy, bulfinch, can serve as a substitute for an entire book like: “Modern Sociology”.

Austin home prices have dropped the most in the entire country. Down 10.2% YoY.

They’ve dropped here in flyover land as well. But the lowered prices are still far too high, despite the realtor’s attempts to position these slightly decreased prices as “bargains.”

The current lowered price levels are not good. They are only less bad. Still a long way to go before I’d consider buying a house. Less bad is still bad.

Better keep your diving gear handy if you buy today. Good chance you’ll soon be underwater.

Just keep watching places like Boise and Phoenix as inventory rises and prices come down. Then the SoCal Inland Empire. People will say coastal SoCal is insulated, just like in ’06/’07, until prices come down there too. It will lag but it will follow.

I’m in Boise and haven’t noticed any significant decreases yet. We might be off from the top a bit, but we are still at nose-bleed areas. Houses that were $300k in 2021 are still priced 450k to 550k.

We just recently investigated moving to Boise and the real estate market there is in a shambles. Prices way too high (very routine that something $500k in 2019 is now $1.5m, and so forth—just add a 1 in front of any price), and sellers in denial as Wolf always says. No transactions happening. At two of the open houses we visited (out of 6), we were the only lookers who showed up. 4 of the 6 houses were completely vacant. Dead market. And will stay dead till sellers start accepting that their millionaire status was an illusion.

With new construction, builders will do anything except lower the price (or as a last resort).

Mortgage buy downs

Lower mortgage rates

Free options and upgrades

Delayed first mortgage payments

Throwing in a car, vacation, etc.

Throwing in a car, vacation, etc.

There’s an idea, maybe they can borrow a page from their timeshare cousin and offer to give you a free trip to Disneyworld if you sit down for 3-4 hrs to listen to a sales presentation on why you should buy a house with mortgage rate buy down never mind the actual price you pay for the house is still ridiculous…

Wow, double torture. Sales presentation and Disneyworld!

Yes. First prize, a week at Disneyworld.

Second prize, two weeks at Disneyworld.

I was in Tahoe last weekend cause I sat through a timeshare presentation. Is how poor people vacation. :)

Nice.

Been there, done that.

New homes in my 2 year old subdivision in south Texas are still selling. Three new foundations were poured last week and sold signs were in front of those lots. These are 1,200 – 2,600 sq. ft. starter homes on small lots with prices $230,000 – $300,000 (or so). The builder is buying down the mortgage to 5.99%.

Several other builders nearby are doing the same.

Wow that is dirt cheap! Here in my town in CA, the cheapest vacant lot is more than $300k.

I just looked and the cheapest lot in Palo Alto on Zillow was $699K for 5,532sf…

Cheapest, actually the only now vacant lot in our little local hood sold for $285K PLUS the demolition so actually well over $300K.

Now has ”doc box” for the new build, but nothing happening yet after six weeks sitting with the grass growing.

Similar house, though on double lot, farther down the block sold for under $200 per SF, then came addition and very nice rehab and then it sold for right at $500 per SF last month.

Others for sale have been sitting for months now, but may be overpriced, etc…

VERY tempting to sell, put the proceeds into short treasuries, sit out and travel for a year or two, come back and buy in again for ????

No kidding. If theyre selling thousands of homes a year, why lower the value of the other future homes by lowering prices directly.

Lower them indeirectly and when the market improves, your base line sales price per square foot is much higher.

Smart business if you ask me. Same as car dealers, retailers etc. Buy one get one free – same concept. Once the sale ends the price pops right back up to the original.

You don’t understand housing. At all.

Well, it’s greed. Understanding not required.

Wake me when they start offering toasters and dish ware sets

Good article. My area, Sacramento, is a classic mix of all of this. Lots of new building, both with new homes and large multi unit rental units. Crazy that a 300 sqft apartment is going for over $1000. The super small apartment craze with street only parking is the new thing right now. On a practical level it makes sense for a single person but pricey given a decade ago I got a 2 bedroom 1 bath rental of 1050 sqft for that plus swimming pool and gym access.

Gas is $2.84 in Indy……this is a tremendous boost to consumers…..it was over 4 last year.

Natural gas down almost by 70%.

Gas was $6.69 in Truckee, CA yesterday…

Regular gas just dipped under $3/gal in NH too… why is gas so much more expensive in Cali??

Underlying real estate is more expensive, mostly. There are also about a dollar in state taxes per gallon on gas, which is the most in the country. Truckee, specifically, is a mountain town, so there are some supply and demand factors specific to there as well. A couple bucks cheaper in, say, Fresno or Modesto. Just checked GasBuddy and Modesto is under four bucks

Because they can’t wait for 100% green energy.

California requires special blends for emissions reasons, unlike every other state.

(And would you invest in new refining capacity or expensive maintenance in the state of California?)

1. “California requires special blends for emissions reasons, unlike every other state.”

CA switched to winter blend on Sep 28. It’s the summer blend that costs most to produce.

2. “And would you invest in new refining capacity or expensive maintenance in the state of California?”

This is an ignorant BS comment. California’s refineries are big profitable exporters of gasoline, jet fuel, diesel and other petroleum products, produced mostly from imported crude oil. It’s a huge profitable business.

“Truckee, specifically, is a mountain town”

That explains the difference. Gas is higher up in the NH mountains too. The sub-$3 regular is at the “cheaper” gas stations in my town.

$2.41 9/10 at my local station here in south Texas.

4.19 in Spokane Valley, eastern Washington. Had been 4.49, even higher for months. Homes, rent pretty expensive here, but utilities about as cheap as anywhere in the country.

Hydro probably the biggest reason.

Our vacancy rate (apartments) was close to 0 during the pandemic.

I’ve been told they have built a lot of apartments… none cheap.

Bozeman Montana is amazing. Why ?

Check out apartment prices there. Can’t hardly find anything for less than $2k a month. Other Montana cities somewhat more reasonable. I read a blog of someone who grew up there and was quite upset how the RE scene had changed so much with the influx of well to do outsiders. She felt like she would have to leave the area.

Similar story in Nashville. Couple grew up there. Home prices skyrocketed… they left and bought a home in Kentucky.

I left Seattle (Lynnwood) 23 years ago, didn’t like where rent was headed. Couldn’t get a software job despite having a masters degree in compsci, 15 years experience (not Windows based though and not terribly Java savvy). Somewhat fortunate (a matter of perspective) … I’ve saved close to 200k on rent in a cheaper area of Washington state (23 years). Would I have been better off buying a home here ? Probably but then again mutual funds have worked out well so far (dot com bust and GR too interesting though). But mortgages were probably only $700 to $1000 here in 2000. My rent? $315. (Its still under $1000 but going up 7 to 8% a year recently).

One thing I feel VERY strongly about.

I dont mind people getting rich in tech or engineering or plumbing or auto mechanics, etc. I dont like people getting rich on RE if they are able to do so because their revenues exceed their costs by a large margin.

If I had the power I would regulate how large rental margins could be. Call me what you want…

Wow!

One more reason for a Californian to move to Texas… that and some fine Country Western music!

:-)

Sign of pending recession, due to reduced demand globally. Oil is telling you where the global economy already is heading. We are in a recession globally. Job layoffs will be the next leg to drop on the stool.

Mike R.,

Total nonsense. Price of gasoline is no sign of a recession. On the contrary: people LOVE saving money at the pump, and they get all giddy and spend all this extra money plus some online and wherever, and we’re seeing that.

America loves affordable oil prices. This is why Exxon, Chevron and Hess are fast tracking oil production in the Guyanas recently.

Guyana is set to produce 600,000 barrels of oil next month, with another 450,000 set to be in production before Q4 2025. OPEC is steaming mad, because they have to cut their production to keep their oil prices high using artificial scarcity.

No shortage of oil above 40 shale oil production in permian hitting all time highs again same as in 2016. Saudi only one keeping oil prices lower by curtailing production. Cheap oil as Wolf says helps generate all sorts of jobs and profits for companies and individuals.

Far from Chicago Metro – Crook County – ill noise taxes helps!

Part of me wants to say prices are going down partly due to an election year coming up…running the narrative of ‘look we got gas prices down, vote for me again and I’ll make em lower!’

Create a problem, make people unhappy/miserable and then run on fixing said problem because people’s attention span is so short these days they won’t remember the past.

@Itsbrokeagain….you should think again if you think that the government has that much clout over the world oil market and oil companies. The only lever the government has is using the SPR and I don’t think they are releasing oil from the SPR anymore.

I have long been and am getting increasingly concerned about a protracted decline in housing prices. We’re far from mid 00s risk but there was a lot of trillions rolled over and into these high values. This is a risk that is being broadly ignored by too many. Lower housing prices are a good thing, falling asset prices backed by 30-year 80% LTV loans will be more painful than people realize.

Ultimately, that pain was created when those loans were originated. Now it’s just a question of how that pain is spread.

Personally I’d like to see a protracted decline in home prices… and I own my home.

Unlike 2008, unemployment is extremely low… as long as folks can make their mortgage payments I don’t think we’ll see mass foreclosures like last time.

Unemployment is currently low. I’m worried about the negative feedback loop of consumer spending that results in unemployment and a new demand shock. This is just instinct. Housing is in a credit bubble created by low rates and stimulus. It’s not subprime, but it’s the same math. I’d argue a material contributor to the consumer spending story that continues to defy expectations has to do with the churn of home equity that happened in 20-22. It was trillions. It has been spent or reinvested and levered at a risky high water mark.

I agree with you MM.

I’d like to see a decline in home prices so my property taxes and insurance also decline. I can then retire in my forever home without being priced out.

I don’t think we will see a foreclosure crisis for primary homes while jobs are plentiful and homeowners are locked in at 3%. However, if you had excess cash during the last few years from cash-out refi’s and PPP loans and used it to buy a leveraged fleet of speculative rentals, we may see a flood of these types of homes from over-leveraged landlords. I don’t know how many there are. I just keep running into them at work and about town. Everyone I know seems to own a rental or 3 somewhere.

Anecdotally, I’ve seen people from 2008 post on blogs who lost all of their rentals and their primary home. Back then, you seemed to have qualified if your had a pulse and no down payment. This time it is different with 20% down payments. Except for VA and FHA loans. This time with the massive PPP loans, the RE mania, and run-up in cash-out refi’s, people have done the same.

Houses haven’t dropped 20% yet, so most are not underwater. We’ll know then when the speculative rats start leaping off the sinking ship with foreclosures. The decision to lose money every month from rent income minus mortgage(constant)/prop taxes(increasing)/insurance(increasing) payments OR sell at below the loan balance will cause foreclosures.

I think the Fed wants house prices to fall but not more than 20% to avoid the massive spiraling foreclosures of 2008-2012 (ie house prices drop 20%, panicked sellers flood the market so house prices drop another 15%). If inflation goes up 15%, house prices go down 15%, we will have a softer landing with a real net drop of about 30%.

We will see. This is the best Netflix drama I have ever watched.

“In a significant policy change, Fannie Mae has announced that, starting from the weekend after November 18, 2023, it will accept 5% down payments for owner-occupied 2-, 3-, and 4-unit homes.”

So much for 20% down payments.

JeffD,

Make sure you understand that these are apartment buildings (multifamily). “Owner-occupied” means that the owner of the building lives in one of the units in the building.

“owner-occupied 2-, 3-, and 4-unit homes”

Sounds like they’re trying to incentivize folks to become a landlord and rent out the other side/floors.

When house hunting years back, my realtor asked if I wanted to buy a duplex and rent the other side. “No way” was my response – I rented one side of a duplex at one point, and heard all the horror stories from the landlord/owner living on the other side. Tenants setting his garden on fire, letting cat pee soak thru the floor etc. Just not worth the hassle.

Do Lennar “Next Gen” floorplans that have a separate entrance and kitchenette count as two units, for mortgage brokers with an eye towards creative accounting? At any rate, lowering the down payment barrier to entry could result in higher prices, and now with a 2x to 4x multiplier, since that is how many units will be consumed.

During HB1 (2008), lots of loans were no down payment or interest only loans. You could also take out a HELOC up to 110% LTV. Lots of loans were underwater even before prices crashed. It did not take much of a drop for people to be underwater with very little home equity. In fact, if I recall, by 2011, 30% of loans were underwater. At peak housing during HB1, Home Equity was only 3 trillion greater than total mortgage debt. Even after the crash, home equity only dropped 5 Trillion from the peak during HB1. Currently, home equity is over 20 trillion. We would have to see 25 trillion wipe in Home Equity for something similar to HB1 to create the same amount of underwater loans. Not going to happen.

We would have to see home price drop almost 40% across the board to see a 25 trillion home equity wipeout. Only in very bubbly places like California, Vegas, Phoenix, Florida did home prices drop over 30% during HB1. Most of the rest of the US only experienced a 5% to 15% drop. But that small 10% dropped caused a lot of underwater loans and jingle mail.

We won’t see a housing crash like that again unless we have another great recession. The FED has multiple tools to stop any great recession this time. They were given freedom in 2010 or 2011 to do anything in their power to stop a future financial crisis.

FYI. In 2007 through 2009, I was a huge housing Bear. I told everyone who would listen to me that housing was going to crash and the Fannie Mae and Freddy Mac would go bankrupt (They did) . I just don’t see a big crash this time because of multiple reasons (Mainly, the FED has the tools to stop it this time). Of course, I could be wrong.

ru82-

Sensible comments and well presented.

I’m curious though — what are the side-effects of those “multiple tools to stop any Great Recession,” do you think.

As with drugs, it strike me that new (and presumably relatively un-tested) tools might lead to substantial indigestion at least.

JohnH

I was off on my Home Equity drop. We would need to see around a 10 to 12 Trillion drop in home equity to hit the same amount of underwater loans.

The FED tools would me more inflation I think. Rich get richer. Poorer get poorer. It would be a replay of 2010 -2012 and they would be saving the GSEs ….again

Sure the 3% mortgage has become the ‘asset’. But for the holders – banks, pension funds, insurance companies, other funds these are distressed assets, when interest rates are now far above 3%. And about 50% of MBS are sitting on the Fed’s balance sheet, accumulating losses (deferred assets, haha). If the holders of these liabilities become impaired, can the Fed bail out the entire MBS market? Or is it better to shake some owners out of these assets- through default due to income stress (recession), and let the banks remortgage the house at higher interest rates? If rates really stay higher for much longer, it’s the only way out of this mess.

The subdivision next to us that I have been watching has been finishing up in Slo-Motion. But it was finally completed a couple of months ago or so. No crowds, but little by little the 3 story townhouse type units ( each on own lot) seem to be selling. Most of the buyers seem to be H1B engineers and scientists that work at Intel. I have yet to quiz any of them but it seems they have their own financing.

HC: That reminds me what happened to those H1B’s in 2008 — Leaving their new shiny cars (with huge payments due) at the airport lots and leaving the country.

I also wonder if they (H1Bs) play a much bigger part in the stock and RE bubble we face now. Their % has gone up, their incomes have gone up (we need all data scientists!), perhaps the WFH allows them to do multi-jobs and unlike average Americans, they spend on essentials only and save the rest. When you mention Intel, think about the CHIPs act and the money associated with it.

Here it comes!

Wolf:

“Who’re”? I never used this contraction. Interesting one…

It’ll take another year or two…or three but we will end up back at 2020 prices.

“Watch and learn”

It will be better for the job market for home prices to come down to allow more job mobility for those looking elsewhere and for employers trying to recruit new employees that would have to make the move. I’ve turned down a few job offers the past two years as the housing market in those places simply didn’t make financial sense compared to my current situation.

Right — because a sudden wave of house-hungry contract lawyers & Cardiothoracic Surgeon DINK buyers is projected to converge on the market.

It’s different this time in pretty much the same way it was different all the other times.

Watch & yearn.

Wolf,

Any chance of getting the new vs. old median house price chart stretched backed as far from 2005 as readability allows (at least 2000 or 1995, if possible).

Starting at 2005 really doesn’t capture the Fed’s ZIRP induced macroeconomic dementia (and the honest baseline we should have been dealing with for 25-30 years) instead of DC’s meth fantasies.

I hate requests like this. If you want to study history, go somewhere else. This site is not for you. This site is about NOW. I give you what I think is the best compromise between perspective over the years and the DETAILS OF NOW, so that you can actually see the details of NOW. I gave you the base line. The only time I go back that far into history is when I want to point out something specific that happened back then, as compared to NOW. I think about it carefully and don’t do it frivolously.

I generally delete this type of request. It’s just infuriating. A chart like this is pure BS for the NOW. There is nothing specific that happened in the 1990s that didn’t happen in the 2010s, and I gave you 2005 through 2023 as reference points. So you see the relationship. That’s enough. If you don’t believe me, do your own freaking research.

Hehe I enjoyed your snark.

Ask him for a log scale.

I understand and appreciate that this sight is about the “NOW,” Wolf. You do a fabulous job interpreting today’s financial subjects and trends, and presenting them with an appropriate historical lense, based on what YOU know.

I can’t speak for CAS127, but, for me, trying to interpret the madness of the current real estate bubble leads to a desire to view a pictorial of the prior 2006 bubble — including the “Greenspan Years.” Thanks for providing the expanded chart.

For what it’s worth, I believe the generally upward march of home sizes and prices is inextricably linked to the general upward march of debt per capita, which has occurred since WWII. A by-product of an activist Fed, the advance of debt financing throughout the economy is a multi-generational phenomenon, IMHO.

“For what it’s worth, I believe the generally upward march of home sizes and prices is inextricably linked to the general upward march of debt per capita, which has occurred since WWII.” That’s one way of looking at our situation.

Improved standard of living is another.

Excessive? Yes all ye dogmatists. Today’s Americans have it too good. “Their foot shall slide in due time!” sayeth Jonathan Edwards back in the 1700s. “Due time” for him is… sometime… anytime…grace time… But it’s always somewhere in the future. No specifics, mind you. The prophets never seemed to have included times or dates. Gee, I wonder why??

@John H. We were just talking about the change in Americans taking on debt after Thanksgiving when my niece said she does not know a “single person” that did NOT spend a semester in Europe as an undergrad. A “semester in Europe” used to be something that “rich” kids did now an increasing number of “regular” kids are adding $15K to $30K to their massive six figure student loan balance to spend a semester in Europe (or at sea).

Reply to HowNow below:

Bigger is better sometimes, not always.

My apartment is 580 ft². Would I prefer it were 2000 ft². Definitely not. More utility costs. Of course more rent cost.

But if I could pay the same rent for ANY size apartment I’d probably stick with 1 BR, 1 bath… more closet space yes. Maybe a little more cupboard space.

700 ft would be more than plenty, 580 works SURPRISINGLY well.

I owned a 1650 ft² 3/2/1 home for 10 years. No I dont miss it. Lived in a 2 BR, 2 (?) bath 1000 ft² apartment… bigger than my needs. It was older and had quite a few maintenance issues which was annoying at best (leaky roofs…flat roof near Seattle how dumb was that !).

Price reductions are inevitable. If a homeowner has a 30 yr mtg with a Loan to Value of 85%. Then the market drops 35% as it did in 2009 then

the new home purchased at a 35% discount will provide even cheaper

monthly payments with a much better home in a better location? People will also lose their jobs soon and this will bring the inevitable supply to the market to allow first time purchasers to the market.

Rate hikes are working. This bullet point jumped out at me:

-Smaller houses (“smaller product footprints”)

…which wouldn’t have happened w/o 8% mortgages – builders would have kept building McMansions in suburbia.

Part of the solution to home affordability is smaller homes, i.e. 500-1500sqft. Plenty of single people / couples w/o kids don’t need more space than that.

Fully agreed. When I was still house hunting these homes were almost impossible to find, and always had the greatest bidding wars, since they were often cheaper and thus closer to something most could afford. After the bidding war premium youd be left with a 1000sqft house selling for 400k when a 1500sqft commands maybe 480k. Long term benefits to having a smaller house too. Cheaper to heat, cheaper to cool.

The problem is the land cost. If the lot you build on costs $75,000, youre not going to build a 1,000 sq ft house on it.

In order to make a profit, you need to build a 2500 sq ft house that you can sell for $450,000 and maybe make 15-20% gross if youre lucky. A lot less if youre not.

Not necessarily, I’ve built a lot of small houses on nice lots and people love them. I built a 1400 sq.ft. one bedroom house (with an ADU) on a $140k lot in the PNW. My total cost was $300k and I sold it for $600k. I lived in it for 2 years while building on the lot next door and paid zero tax on the gain. I’m building a 1300 sq.ft. 2 bedroom house on 1.33 acres of beautiful desert property in AZ right now. I’ll have 400k into this and it would probably only sell in the low 5’s but it’s going to be our winter retreat so I’m not concerned with resale. It’s also in a 1948 plat of elegant older estates with super friendly neighbors who are way out of my economic class. Legislators, Lawyers, airline pilots, 2 ex-ambassadors, 2 alleged mafia families. We haven’t even started drywall yet and have already been invited to the neighborhood Christmas party.

I’ve posted that for two years.

My apartment is 580 ft². Add on a balcony and nice storage unit, at most 700 ft².

Its big enough for me. I’d go for a 700 to 800 ft² home with a little space between the homes.

I dont want shared walls, floors if possible.

On the other hand, its just as important (to me) that renters have good living conditions.

I can’t remember when the media carried a story about a renter having a problem getting something repaired or a neighbor quieted down (say). The media could do much better in that regard.

We have a “Code Enforcement” department as part of city government. Our apartment parking lot had 7 inch ice with ruts (6 or 7 years ago).

This department told us to get a lawyer, they wouldn’t get involved. Code Enforcement huh ?

Low inventory here in north county SD, multiple offers if anything decent comes up, selling quickly at all high time prices. Don’t see prices coming down with this inventory.

People are locked in with low mortgage rates, their pay as kind of kept up with inflation while their mortgage payments are fixed. Home prices didn’t come down during the high inflation of the 70s, still haven’t seen a convincing argument as to why they will come down this time other than wishful thinking from those wanting to buy.

This article is about NEW houses, not USED houses. You’re talking about USED houses, which the homebuilders compete with. Future sellers of used houses are going to have a hard time selling unless they can outcompete new houses. And so used house sales have collapsed, even in your area, and buyers have left, and homeowners don’t want to put their vacant home on the market because they think this too shall pass RTGDFA.

Sometimes the numbers data just don’t match up with the boots on the ground data. Hopefully this will change.

Wrong boots on the wrong ground = BS.

Hello From SD

I thought the same in 2008 2009.

SD would stay high if there are no recession.

Funny how the stock market wants rates to come down (from their historically normal level now), which will only happen if the Fed sees a strong slow-down in the economy, perhaps a recession. It is as if the stock market wants an economic slow-down or recession, which, as I recall, is not particularly good for stock prices.

As for new houses, Wolf’s last chart clearly indicates the trend in median prices is down. They peaked about twelve months ago. There seems little reason to think this trend will reverse. In general, I would rather buy a new house than an old one, at least I get a one year warranty. It will be interesting to see what the greedy existing house sellers will do when the median price of new houses starts dropping below the median price of existing houses. Should happen soon, see Wolf’s last graph.

“It is as if the stock market wants an economic slow-down or recession, which, as I recall, is not particularly good for stock prices.”

Perhaps bolstering the point that asset prices are more a reflection of QE than the real economy.

“Perhaps bolstering the point that asset prices are more a reflection of QE than the real economy.”

That, if true, would be a pretty sad commentary on the stock market. However, if you spend some time listening to stock market “pundits”, you would get the impression the stock market, if it was a human, was psychotic.

The only “psychotics” are those who think the stock market “is” human. Plenty of those are making comments on this website.

“Mister Market” my butt.

New houses vs used houses is not that linear. A “used house” is often built in the most convenient / best areas whereas the “new” developments are more remote from amenities. That’s why “scrapers” are selling at the prices that they are. Think Hinsdale, IL or Naperville, IL as examples. The stuff “downtown” is big dollars and the tract whacks are “less” for “more”.

Personally, I’d rather have an “old” house built out of real materials than those out of cardboard, sawdust, and SYP vs. redwood, doug fir, or old growth pine.

Think West Oakland vs. tract homes in San Ramon, Dublin, Pleasanton. It is just the opposite of your example. Or central Las Vegas vs. tract homes in Summerlin. Just the opposite of your example.

I have been in a lot of older houses that are best suited for tear-downs. It all varies, of course. The new homes I have been looking at come with a one year warranty on most everything, for whatever that is worth.

Amen — those old timbers were virtually immune to termites, mould & rot and the plaster used had a much higher flashpoint. Also looked miles better than most of what’s going today.

Unless it’s a custom job, new homes are mostly designed to be ‘new’ (one of the most compelling words in propaganda next the word ‘free’); an unblemished space in which one can swan from room to room being fabulous. Once the newness wares out, though, you’re left with a rectilinear box that aged badly and isn’t even worth rehabbing.

Anecdotally, from what I’ve heard and seen here in Carolinas, folks who had plenty of time to shop around and barely any money issues (e.g. moving from Northeast with huge equity in their old houses), almost always gave preference to 5-10 yo houses vs brand new builds.

Unlike them, I had no real choice in 2021 and had to go with the new build, as I was a year or two too late to the party (still kicking myself for not pulling the plug and moving down south right after I got divorced in 2019). After two years in a new development I kind of see why people prefer a little more established places. Even locations aside (as this can be debatable as rightly noted above), almost all my neighbors have been going through some extensive repairs over first years of their homeownership, and those are results of bad builder craftsmanship and poor design choices, not extended wear and tear. I already had both bathrooms redone under warranty because of extensive leaks, and a year later I see that the story is probably not over as there are some signs of moisture in the same spot again. My across the street neighbors are now doing huge repairs after a burst pex pipe inside the wall and there’s yet another trade van in front of their house almost every day.

The logic behind “5-10 yo house preference”, again, based purely on what I’ve heard from people, was based on two assumptions: 1) all those major issues (if any) with bad plumbing, electrical or foundation/grading are likely to surface during the first years of ownership, and hopefully get fixed and not pop up later again, at least for the next 15-20 years, and 2) specifically in Carolinas, the market in, let’s say, 2010-2015 was presumably way different than in 2021-2022, which reflected a lot in how houses were built. Starting in 2020, everyone and their grandmother (quite literally – we have several extended families owning multiple houses in our development) was seemingly moving down south from NY/CT/MA and sucking everything they could off the market (= no real incentive for builders to invest much in quality knowing that houses will be bought anyway), whereas back 10-15 years ago it was much more of a “niche” market without such an inbound migration craze where builders actually had to do their best to sell.

Again, it is, of course, very anecdotal and based on just a handful of data points, but if I had no time/money constraints, I would’ve probably went after 5-10 yo house too, even in the same town I live now.

The key is to keep pressure on local zoning officials to allow construction. While no government can handle a population that is “ungovernable,” the local governments are even weaker. The Federal Reserve has set up the perfect problem on their own for a government; and that historically is the give them a problem that either way they solve it they lose. For the Federal Reserve the masses have high interest so they cannot get on with life or high inflation and they can’t eat. For the majority (poor) there is no relief from either no matter what economic choice is made; the only choice is pressing local officials on housing and that is something the masses can easily do.

How does one “press local officials” when said “officials” don’t have the where-with-all to build a dog house? Zoning? Not for nothing, but I wouldn’t want to live in an ADU (aka garage) and most people seeking housing (those with spousal units and kids) can’t fit in them. It’s another get rich quick scheme for those that have for it allows them to subdivide a single family property into multiple dwellings and sell at higher multiples. The bulk of the value is in the land and infrastructure, not the pile of bricks and sticks.

The Washington Post has an interesting article today on new housing: “Where we build homes helps explain America’s political divide.” What is interesting is not the politics, but the collection of statistics- somewhat lagging behind Wolf, though looking at the market from the perspective of average monthly mortgage payments and land availability. The map by county of building permits is fascinating. The political part of the article seems mostly inconclusive at best. I would post a link but assume it would be forbidden here. I was surprised the story came out the same day as Wolf’s.

Cheers, Tom

Financial gymnastics. The new Olympic sport of the 2020’s.

Not yet deflationary since home builders are providing less for less money. May actually help support the prices for existing larger homes because it will reduce supply increases.

Home builders are still recognizing huge profits, which are about double the 2019 levels. Lots of fat still needs to burn.

Hi Wolf. Do you have an inflation adjusted housing price chart (I.e. in constant year 2000 dollars)? Curious if the loss of value in the dollar bit into the actual value of housing.

This is “House-Price Inflation.” It measures the purchasing power of the dollar with regards to houses.

It’s conceptually NUTS to adjust one inflation gauge for another inflation gauge, such as adjusting CPI for PPI, or adjusting “House Price Inflation” for “Consumer Price Inflation.” All that tells you is which is worse.

If the outcome is zero, it doesn’t mean there is no house price inflation. It means that both house price inflation and consumer price inflation have moved in the same direction by the same amount. And so what?

Repeat after me, “THIS IS HOUSE PRICE INFLATION.”

Let’s say you bought a new wrench in 2000 for $3. In 2023, the exact same new wrench (same brand, same material) costs $9. No hedonic adjustment.

If the CPI in 2000 was say 100, and in 2023 is 200, you could say the price of the wrench exceeded the inflation rate. The inflation adjusted cost of the wrench should be $6, but alas, it costs $9.

You could substitute “house” or “any commodity” for “wrench”. If you use “house”, you should probably use CPI minus housing cost (or owners’ equivalent rent or whatever bullshit measure BLS uses). So what am I missing?

No, this is BS. Because a wrench is a “consumable” (consumer price inflation), not an asset (asset price inflation). A house is an asset. You don’t adjust the S&P 500 for consumer price inflation either — that’s just braindead stupid, though it’s easy to do, and any idiot can do it, but it’s stupid. Lots of people do stupid things all the time, but it’s still stupid.

Not quite. The land is an asset, the houses built on top are not and are consumable (you need to maintain them and even after some time may require significant rebuilding for compliance, changes in preference).

Also, housing doesn’t really operate the same way as other assets do. You don’t have to pay a huge carrying cost on most investable assets (gold for example), but you do with houses (taxes, maintenance).

Finally, a majority of houses are owned by people who sell to buy again. You don’t really do that with most assets. So still useful to see the affect of inflation on the pricing

Interesting comments by Wolf and Mastercrab. Accountants “define” a house as an asset. To me, if I am living in it, a house is more like a durable good. It lasts more than three years. I get some value from it, but it requires maintenance, like all durable goods. Unlike most durable goods, I have to pay rent (property tax) to the county. A car is also a durable good, and l pay annual rent, usually called the annual vehicle tax (registration) so I can get my little sticker. It also requires maintenance, like a house.

If I rent the house, then the house is more like an asset. I suppose I could draw up a lease, pay myself rent, write a check to myself for the rent, and then deposit it into my checking account. If I violate my lease, I suppose I could evict myself.

Finally, BLS, which makes the Consumer Price Index, considers housing as part of its index. But they measure it as rent or owners’ equivalent rent . It would make more sense to me if they considered a house as a durable good, because that is what it is.

The house itself may be a durable good, of sorts, but it comes with land. In accounting for commercial purposes, the building itself gets deprecated to $0 over usually 30 years, and the land retains its book value. You’re paying for only the land if you buy a teardown. So these clickbait stories you see about the sale of a collapsed shack that went for $1 million, that’s the value of the land.

William Leake,

A house comes with land. In accounting for commercial purposes, the building itself gets depreciated to $0 over usually 30 years, and the land retains its book value. Both are assets. You’re paying for only the land if you buy a teardown.

The BLS considers housing a service – “shelter.” So you’re paying for this service. The BLS measures this “shelter” inflation in two ways:

1. Rent CPI which tracks rents directly as paid by tenants, what they’re paying for monthly, and that’s pretty clear.

2. It also tracks housing costs of homeowners as a service, also “shelter,” and so it uses Owners Equivalent Rent index for homeowners.

Wolf, okay, the land is more like an asset. The house is more like a durable good, unless it is rented out, then it becomes an asset. I guess my point is a lot of this stuff is definitional, as in arbitrary. The value of the house should be included in the CPI, not just what it might rent for. I think you have shown some nice graphs where the price of houses have increased much more than rents.

As for BLS treating housing as a service, well, a house is also a durable good if you are living in it. Many goods in fact provide a service. For example, food is a good, but without it you would be dead, so it provides a necessary service if you want to live. Yet BLS does not treat food as a service.

Sell everything!

Just read Roubinis latest missive. He does tend to focus on the ‘long tails’ but THERE ARE an awful lot of now and too many aren’t all that long

He makes a strong case for stagflation which he says will be bad for bonds and equities. He makes a reasonable argument that inflation (not core but total) will remain at 4-5% for possibly decades and certainly for years to come.

Here is a short excerpt:

“This bloodbath is likely to continue. With average inflation running 5%, rather than 2%, long-term bond yields would need to be closer to 7.5% (5% for inflation and 2.5% for a real return). But if bond yields rise from their current 4.5% to 7.5%, that will cause a crash in both bond prices (by 30%) and equities (with a serious bear market), because the discount factor for dividends will be much higher. Globally, losses for bondholders and equity investors alike could grow into the tens of trillions of dollars over the next decade.”

I am not this bearish but I do not ignore Roubini by labeling him as “Dr. Doom”. His book Megathreats from last year keeps getting more real and there are a bunch of threats.

From another source I read an article that explained too reasonably that the development of AI has no off-button. Think about that…

If I owned a second house I would sell it now. Last summer I diversified around the world as best I could.

I am not sure diversifying around the world will help, since we pretty much have a global economy. Diversifying within our Universe might help if it were possible. Life was easier when we had economies that did not act in concert.

Seriously, I tend to be in Roubini’s camp. Economics is called the “dismal science” for good reasons, although in fact it is not a “science”, but it is dismal.

I would be a strong buyer of homes at this point in time. I might buy some in Indiana this January.

Please do. I might buy a few from you pre-foreclosure.

I’m guessing he’s made much more selling books than he has in generated alpha based on his theories.

I was reading an article recently which was saying that the problem for the FED and .gov is that people view inflation differently than the actual definition. The FED and .gov will celebrate “inflation is gone” when the number gets back to their precious 2%, but the people don’t care if it’s 0%, because the new inflated prices are still “inflation” to them, and until prices go back to where they were, there’s still “inflation.” People are angry and want the old prices back.

Dont disagree people are irrational but if inflation is 3% and you get a 3% annual pay increase then it is the same although if one gets a raise ideally it would be a purchasing power increase not holding steady.

But the 3% can often come with unintended consequences – like moving you out of qualifying for various government programs. Then there’s the tax creep. 3% raises rarely turn into a 3% increase in disposable income.

The Krugmanites and DC journalists are perfectly happy with housing and transportation being unaffordable for the unwashed. Just because necessities are unaffordable doesn’t mean that policy hasn’t succeeded. I read plenty of these obtuse thumbsucker “what’s your beef?” articles; so many that it seems like a coordinated campaign.

No wonder the youtube realtors are desperately crawling out of the woodwork. Lol. Time for them to find real jobs.

I like Wolf’s statement that nothing goes to heck in a straight line. Yes, every geographic area is different but nationwide the prices are trending downward. The builder stated they are competing with apartments for first time buyers. I am in Jacksonville FL and there are numerous new apartment projects under construction with 13,700 from 21-23 and almost half of those in 23. I don’t think that many people are migrating to Jacksonville to support the new construction. New apartments competing with new apartments, older apartments competing to keep their tenants, and new homes competing for those tenants hoping to buy. I think it is just beginning to break in Jacksonville.

I am a little baffled that home builder stocks are still trending upwards. I guess they know what they are doing.

FL has net, NET!!, in migration of approx. 800-1,000 people per day….

has done so, approximately, for many years

Given “smaller product footprints”, should we be comparing median price per square foot? New vs. used? The drop should fair bit less.

Median house price is rather a crude metric. Well, it tells how much people are paying for a median house, it is just hard to tell what median house is now vs. like year ago.

I disgree.

It doesn’t matter what the median house is, be it a 4000sqft 5/3 or a cardbard box. What matters is the housing stock that’s available.

Lets say you *want* a smaller (<1200sqft) house – what % of houses on the market are this size or smaller?

I said compare median price for sqft of houses sold over time, new and used.

We are talking sales here, not inventory, I don’t care what is available, but what has sold.

I wonder if the hedonic quality adjustments will account for the “smaller product footprints,” and “de-amenitizing.”

If the median new house is now smaller than the median new house was a year ago, and has less amenities than the median new house a year ago, and this is the primary mechanism by which builders are enticing sales to maintain affordability for buyers, then we would expect the price premium of median new houses above median used houses to erode in the short term since the physical components that make a “median used house” can’t change as fast as that of a “median new house.”

I’ve built three new houses. Not one of them did I go face down on the “upgrades”. I had circuits installed for pot lights, but not the fixtures. Left the dead wires in the ceilings and documented where they were with photographs.

Fancy moldings? Nope. Not paying for it. Installed them myself (actually found a use for HS geometry).

Granite? Nope. Took the formica and then tore it out later on. Appliance package? Took the credit. Ditto flooring. Took the cheapest plumbing package (toilets) and replaced them with Toto’s after closing.

In a nutshell, probably saved 10’s of thousands of dollars with a bit of sweat equity. Of course, you can do the same with a “used” house.

None of this is rocket surgery. In 6 more days I *might* be able to give you a report from the field on an actual real estate transaction (and it ain’t pretty).

Too bad. Formica is damn’d handsome — especially over Baltic birch ply.

Yep. Marble counter tops are b.s. But, I’d rather you tell my wife that, not me.

Smart way to get a far better house than direct from the Builder.

I tried doing the same thing back in early 2021 – declined most of fancy upgrades in a new build, went with the cheapest flooring and only paid for some major additions that would be too hard to replace/install later on. Everyone, including my family, all my friends and even my realtor (lol!) were supporting my choice.

Almost three years later I think I made a huge mistake. The assumptions I used back then in my napkin calculations have proven to be very inaccurate. I don’t remember exact numbers now, of course, but basically the conversation went like “How much would be to add hardwood floors throughout the house? – $16k! (again, random number, may have been 10 or 20) – Wow, that’s too expensive, I can get hardwood at Home Depot for $3k and do it myself!”. Well (in a narrator’s voice), “He couldn’t. Prices at Home Depot went up big time”.

I understand it was mostly a bad timing, but I soooo much wish I went with all upgrades possible, rolled them into my 3.5% mtg and just relaxed with a bottle of cold beer in my hand instead haha.

Where I live in Markham, Ontario Canada a new detached house is about 3.5 million but all of them are custom built out of fieldstone. The lot sizes are usually about 50×115. A huge premium is paid for anything with 8’s in the address or anything very close to an elementary school.