Banks, forced by competition from money market funds, got the memo.

By Wolf Richter for WOLF STREET.

Money market funds have been paying over 5% since about April 2023, up from near 0% in April 2022, and Americans are liking it. A lot. And that has forced banks to compete for deposits by offering attractive interest rates on CDs. And Americans have flocked to those too.

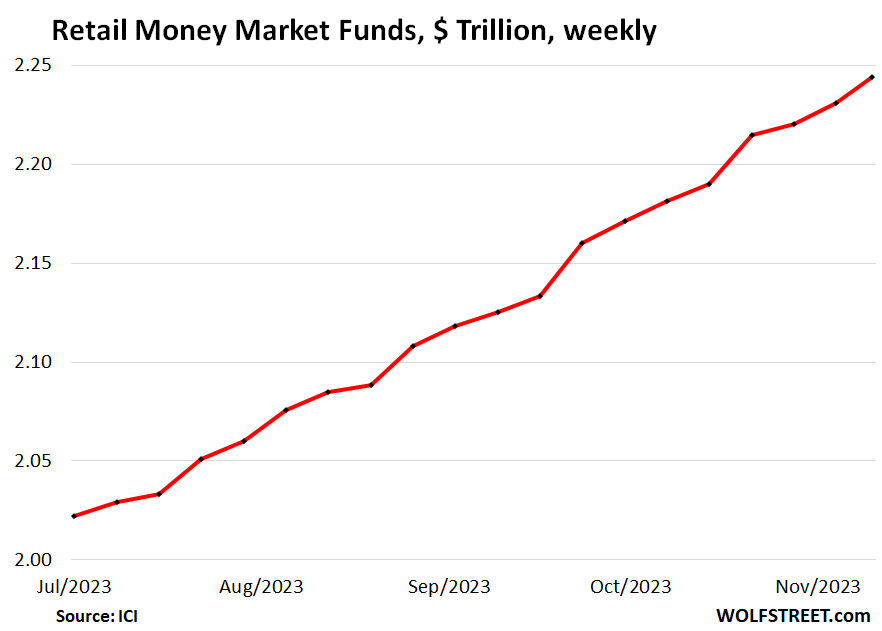

Money market funds for retail investors rose by 0.6% in the latest reporting week from the prior week, by 2.5% over the past four weeks, and by 8.9% over the past three months, to $2.24 trillion, ICI (Investment Company Institute) reported on November 22. This includes funds that invest in government instruments, such as T-bills; funds that invest in tax-exempt securities; and prime funds that invest in non-Treasury assets.

Those are just funds sold to retail investors. Money market funds (MMFs) are divided into two major categories in terms of who they’re targeted for, based on the language in their prospectus; and we look at them separately:

- Funds sold directly to retail investors (chart above)

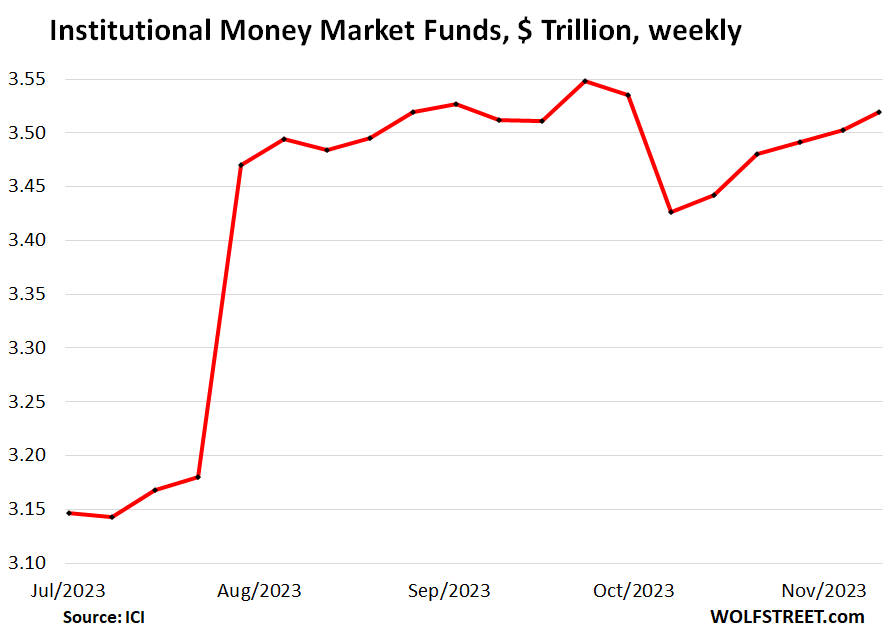

- Funds sold to institutions such as an employer, trustee, or fiduciary on behalf of its clients, employees, or owners (chart below)

MMFs are mutual funds that invest in relatively safe, short-term securities, such as Treasury bills, repos, including what the Fed offers and calls “Overnight Reverse Repos” (ON RRPs), high-grade commercial paper, and high-grade asset-backed commercial paper.

MMFs for institutions rose by 0.5% last week, by 2.2% over the past four weeks, but only by 1.4% over the past three months, after the dip in October, to $3.52 trillion.

Individuals are indirectly among the holders of these funds since the institutions include employers, trustees, or fiduciaries who buy those funds on behalf of their clients, employees, or owners.

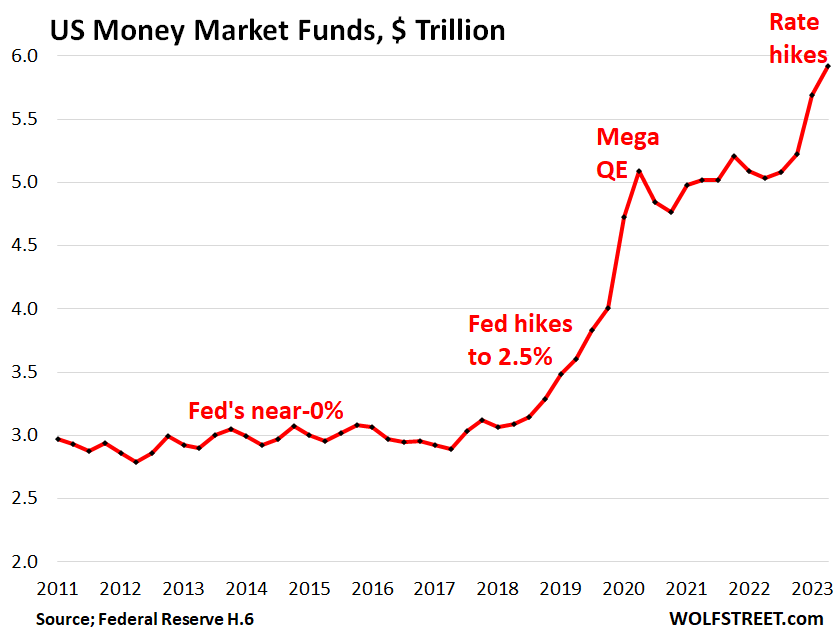

Total MMF balances rose by 2.3% over the past four weeks and by 4.2% over the past three months, to $5.76 trillion.

The ICI makes only the past 20 weeks of data available and excludes ETFs and funds that invest primarily in other mutual funds.

The Federal Reserve releases a slightly different metric on a quarterly basis as part of its money stock series, currently through Q2, and it has been the same song. You can see how the balances swell when the Fed hikes rates, first in the 2017-2019 period, and then again big time this year (data only through Q2).

Money-printing and money market funds. But note in the chart above how the mega-money-printing binge that started in March 2020 created so much liquidity that it went also into money market funds, even when they returned near 0%, which triggered its own set of problems as these funds had to buy T-bills, and their demand for T-bills pushed down the T-bill yield to 0% and even below 0%.

This caused all kinds of fears that some of the MMFs could “break the buck” because their 0% income or even negative income didn’t cover the fees and expenses and could cause the NAV of the fund to drop below $1, which could trigger a run on the fund, which would then trigger forced selling by those funds, panic, contagion, and the whole schmear.

Which is why the Fed offered overnight repurchase agreements (ON RRPs) to the MMFs. The ON RRPs did pay interest, and the Fed lifted that RRP interest rate with each rate hike. We have discussed RRPs and their now plunging balances here.

Banks now have to compete with MMFs.

Deposits are loans from bank customers to the banks and form the backbone of bank funding. When those deposits flee, as depositors yank their money out because they don’t like what they see or the interest they get, banks can collapse, as we have seen in ample detail with Silvergate Capital, Silicon Valley Bank, Signature Bank, and First Republic.

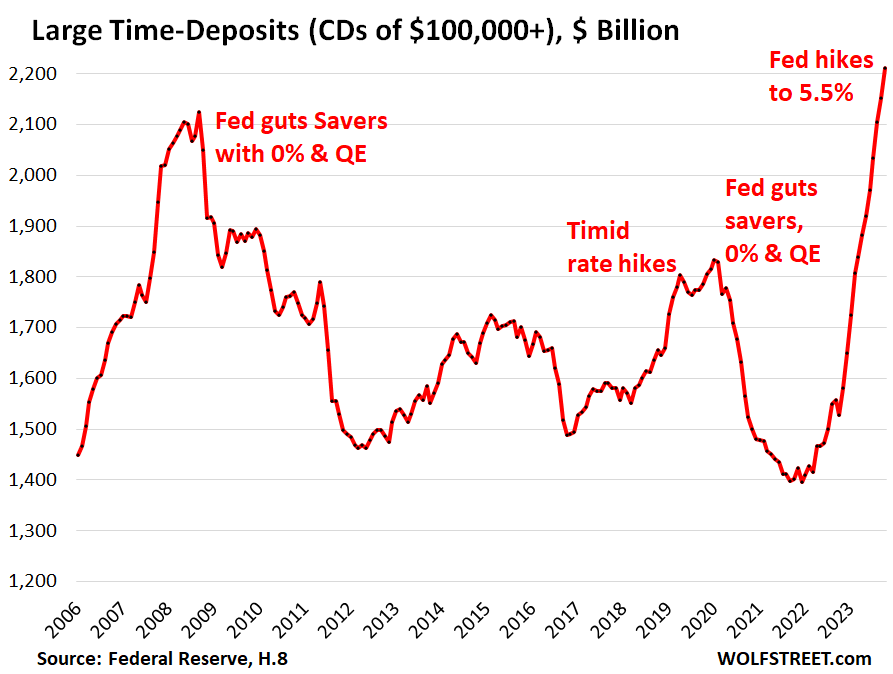

And so banks have gotten the memo, and they’re offering CDs that yield 5% and more, and savers have flocked to them. CDs, which have a maturity date, provide funding that is more stable than savings or checking accounts whose cash can be yanked out instantly via electronic funds transfer.

Large Time-Deposits – CDs of $100,000 or more – surged by 60% since the Fed began its rate hikes, to $2.1 trillion at the end of October, from about $1.4 trillion in March 2022, according to Federal Reserve data.

The Fed’s interest rate repression during the Financial Crisis – which sacrificed the cashflow of yield investors, such as savers, at the altar of asset-price inflation – caused banks to cut the interest rates they were paying on CDs to near-0%, and CD balances plunged, as deposits mostly reverted to other types of bank accounts that paid nothing and whose balances continue to swell.

You can see the rhythm. The timid rate hikes from December 2015 through December 2018 caused these time deposits to rise. The Fed’s interest rate repression from March 2020 caused CD balances to plunge. Since the rate hikes began in March 2022, CDs have become attractive again, and investors flocked to them:

Banks offered “brokered CDs” via brokers to investors with brokerage accounts that weren’t necessarily the banks’ customers in order to attract new deposits as their existing deposits began to flee the 0.1% rates that the banks were still paying. And then very reluctantly they stopped trying to endlessly screw their existing customers and began to offer 5%+ CDs to their existing customers to retain the deposits they still had.

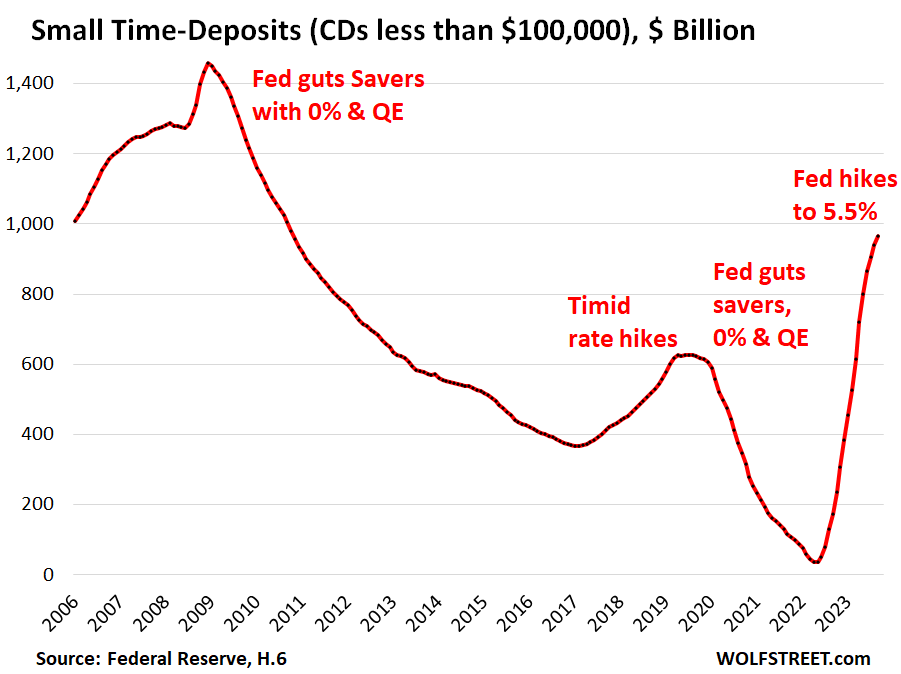

Small Time-Deposits – CDs of less than $100,000 – surged from just $36 billion in May 2022 to nearly $1 trillion by the end of September, the latest data available from the Fed’s H.6 money stock measures. It is likely that they continued to surge in October.

These small CDs reflect what regular folks are doing with their savings, and they too are now finally earning some income on their investments – which is encouraging people to save a little more:

CDs are not the only bank savings products that have become attractive by the force of competition with money market funds. Banks are also offering higher interest rates on savings accounts, some going to 5% and beyond, but the bank can change those rates without prior notice, and customers can yank their funds out, unlike CDs whose rates and funds are locked in until the maturity date.

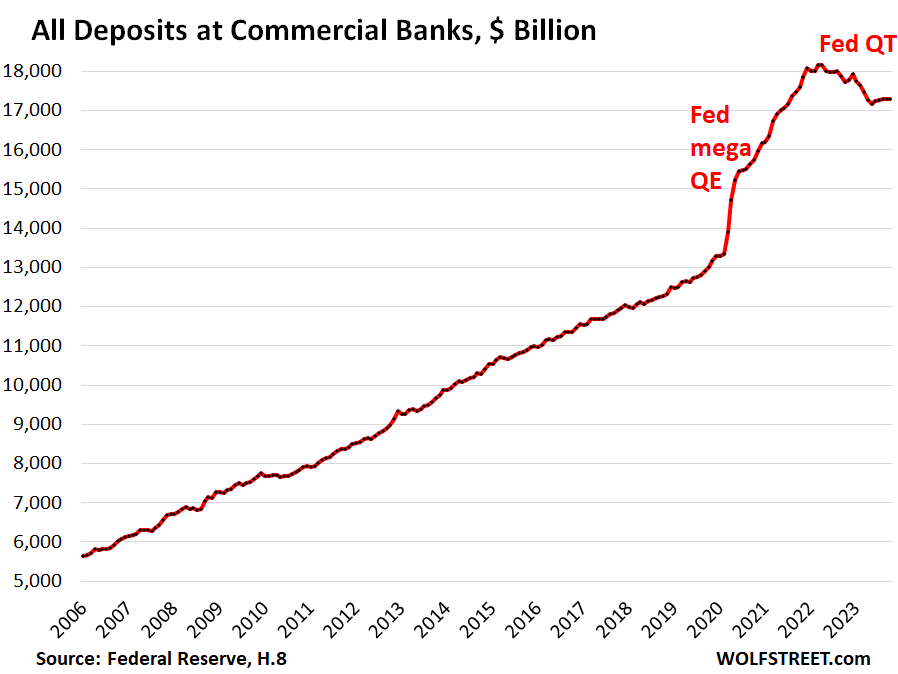

All deposits by all commercial banks – CDs, savings accounts, checking accounts, transaction accounts such as corporate payroll accounts, etc. – have dropped by $890 billion since the peak in March 2022, to $17.3 trillion, after the mega-money-printing binge starting in March 2020 had caused them to spike.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Yeah Baby Yeah!

Bank CDs are still a very bad deal compared to TBills because:

1. They are still paying lesser than treasuries for nearly all terms.

2. People who locked into 5 year CDs @ 4% are now regretting not buying the TBills @ >5%.

3. Bank CDs carry the same risks as bank deposits at a time when many banks are insolvent thanks to buying 0% yield bonds, issuing Jumbo mortgages at 3.5%, and are using accounting gimmicks to prove solvency.

4. The medium term CD rates rose above 5% only for a few days mimicking the 10 year treasuries and then collapse again.

Stick to the TBills. No, rates are not gonna fall anytime soon.

1. “Bank CDs carry the same risks as bank deposits at a time”

Which is Zero RISK if they’re FDIC insured CDs — limit is $250,000 per bank per account, and with brokered CDs from different banks you can hold $10 million in FDIC insured CDs. With the same ZERO risk as T-bills.

2. But money market funds have somewhat higher risks than FDIC-insured CDs and T-bills. That’s something to keep in mind if you want zero risk. I mentioned some of that in the article.

3. But, but, but… money market funds offer next-day liquidity, which CDs don’t (even brokered CDs are hard to sell), and you as small-scale investor might not get a good price if you sell T-Bills via your broker.

4. CD yields may or may not be higher than equivalent Treasury yields, depends on the offering. For example, Schwab is offering 2-year and 5-year “brokered CDs” with yields that are a little higher than today’s 2-year and 5-year Treasury yields. So it depends.

5. Treasuries of any kind offer big tax advantages for people in states with high income taxes, such as California. Treasuries offer no tax benefits in Texas and other states that don’t have state-income taxes.

6. Correct, that 4% 5-year CD bought last year that you mention, is not great now – you can get 5-year CDs at 4.55% at Schwab today and 4-year CDs at 4.7%, and we saw a 4-year 5%+ CD at Schwab a few weeks ago. But that 5-year 4% CD might be good in 2025-2027 if T-bill yields drop below 4%. That’s why you don’t put all your cash into one long-term CD, you get a mix of short-term and long-term, you can ladder a little. You will never time it perfectly, except through luck. All you can hope for is “good enough.”

I made the Nasdaq rally 35% for the year. Why are people still discussing CDs and TBills for 4% to 5% yield?

Sell all bonds and buy Nasdaq index funds powered by the big tech bubble that I inflated with trillions of dollars worth of QE. If you don’t invest now (FOMO), you will lose out forever to inflation :).

I locked into 4.9% 5 year brokered CDs at Fidelity in late March 2023

As for “Bank CDs carry the same risks as bank deposits at a time when many banks are insolvent” FDIC covers $250,000

My bad, I keep forgeting the 250K limit. You are free to guess why that is the case.

“No, rates are not gonna fall anytime soon.”

Where have you been the past two weeks? The market says otherwise. 10-year treasury yield has fallen significantly, and bonds are higher across the board. JPM says otherwise – they have begun calling their high yield brokered callable CDs….just issued in September.

TBill rates haven’t fallen.

Also, if you really believe that rates will fall again, you still won’t by CDs because Fed hasn’t managed to conquer inflation and any loosening will push real inflation above CD return. Also new QE will create a bigger stock bubble. So if you are really betting rate cuts, it’s best to hold FANGMAN stocks or Nasdaq index funds.

Have a look at the 4-week T-bill Mary.

In the past, some local bank CDs I bought had a fixed redemption penalty if you liquidated early. For example, on a 5 year CD you gave up 6 month’s interest for early redemption. If rates the CD rate was 4%, it cost you 2% in interest to redeem (at par) before maturity date. In a rising rate environment, this might have been better than selling a similar maturity treasury and taking a market-based discount.

Not saying CDs are better, just that it depends on all of the terms of the CD.

(Also, I’m not sure these types of CDs are available now…)

“In the past, some local bank CDs I bought had a fixed redemption penalty if you liquidated early.”

They still have that, only the penalties vary among banks. Also, some banks have no penalty CDs. They are lower rates, although not much, and they carry a fixed term at that rate, but you can redeem before the end of the term without penalty. So 11 months at 4.9, for example. You can ride out the entire term at that rate or cash in any time after 6 days from account opening.

The first thing to look at when buying a bank CD is the “early withdrawal penalty”. Some banks’ penalties are draconian, some only a few months. They vary a lot.

I wouldn’t buy CDs directly from a bank, simply because they make it difficult for you to move your money elsewhere. Many banks won’t allow you to wire more than $3k to $5k (varies by bank) out of the bank via electronic transfer or even wire transfer. They say its for your security, but we know better. As a result, you wind up writing a manual check to make the transfer, which takes a long time to clear and get credited to your new funds location. Lost time is lost interest. Also, many banks won’t allow you to close out a CD online. They make you get a hold of them by phone, which at some banks is quite a waiting game and hassle.

Better to by brokered CDs from your broker. Transferring funds out of a brokerage account is super quick and easy.

“Many banks won’t allow you to wire more than $3k to $5k (varies by bank) out of the bank via electronic transfer or even wire transfer.”

If you set up a permanent ACH fund transfer facility at your bank to your own accounts somewhere else, such as at your broker or at another bank, the limits are far higher, and you can set them, such as $100K per transfer. And transfers are free. But that applies only to transfers between your own accounts at these two institutions. Most people do that to connect their brokerage accounts and their bank accounts, and their account at TreasuryDirect. etc. If you move a lot of money around, you can set the top limit at $1 million or whatever.

T-bill rates will keep falling but may bump upwards for a short period of time in January and early February next year.

That is what I am thinking too. But I am amazed that there is still such a big appetite for US debt. Remember, according to the CBO, the US government is going to have to sell an extra 1.75 to 2 trillion of debt YOY going forward. It is predicted taht the US Gov will have 50 trillion in debt by 2030. That is 17 trillion more debt in 7 years,

Overall, foreign governments been selling treasuries lately.

If they are not buying then Wolf’s US MMF chart that has skyrocketed to 6 trillion needs to keep going up at this pace.

We need it to continue on a growth pace of 1 to 2 trillion a year for the next 7 years if Foreign governments do not step in So by 2030, the US MMF needs to be at least 10 trillion and maybe as much as 15 trillion. Is that possible?

Who will buy treasuries or MMFs if rates go down and stocks look more enticing? It looks like the FED can pause but a pivot may be difficult.

That being said, MarketWatch reported that more central banks are cutting rates than raising rates.

Again I ask, if we do cut rates then who will buy US treasuries. If rates start going down, then won’t people owning money market funds want to bail?

That is my 17 trillion question

The only reason rates have fallen in the last 60 years was economic weakness (stimulative). This time could eventually be a repeat of the late 40s though, where the unpayable 132% GDP debt burden will be monetized rapidly. We have wartime deficit and national debt.

Americans Figured it Out. — Not

Sorry Mr. Wolf 5% inflation and 5% interest on CDs does not make you going forward, just breaking even.

By a continuing process of inflation, governments can confiscate, secretly and unobserved, an important part of the wealth of their citizens. By this method, they not only confiscate, but they confiscate arbitrarily; and, while the process impoverishes many, it actually enriches some. The sight of this arbitrary rearrangement of riches strikes not only at security, but at confidence in the equity of the existing distribution of wealth. Those to whom the system brings windfalls . . . become ‘profiteers’, who are the object of the hatred of the bourgeoisie, whom the inflationism has impoverished not less than the proletariat. As the inflation proceeds . . . all permanent relations between debtors and creditors, which form the ultimate foundation of capitalism, become so utterly disordered as to be almost meaningless….

– John Maynard Keynes

all socialist believe in free lunches and zero risk

“Americans Figured it Out. — Not”

5% vs. 0.1%.

Americans who have not yet figured it out are still getting 0.1%. And they have the same inflation rate.

Again, a good article that documents the available data in a neutral presentation. Understanding that, in order for someone too be deemed normal, they have to conform to the idea that each graph should be viewed as normal when, in fact, they document an abnormal situation.

A Fed, out of control, imposed QE as the solution to the impending bankruptcy of all of the systemically banks.

At least the crazy bastards haven’t swung from party hardy and the cold light of redemption, a severe recession. What does mummy say ?

Is that u Austin

These sound like a simpler investments than rental properties.

Just rounding up the suckers before they print the next $19 Trillion.

Just rounding up the suckers before they get bailed in…or worse (yes there is worse)

Definitely!

Howdy Folks. Teaching the youngins with ZIRP was such a stupid thing to do. If THEY bring that nonsense back??? Inflation and Bubbles for forever…..

Seems like bubbles forever is their motto.

Well, Bubba, whose non de plume suggests a MAGA point of view, unaware that many of their privacy rights were being stripped away while cutting taxes for the wealthy.

Those of us “sacrificed on the altar of asset-prices”, butchered like pigs and offered up to the FED gods, expect full compensation for our contribution

We also expect justice from the “system” to punish these miscreants for their evil deeds.

Have a nice day!

🤣

Well, that is certainly one way to look at it.

If I were to disagree with you on a certain point it would be on your hang up expecting a justice system, as if it was a given. Unless your black.

And as the scripture suggests, many times, miscreants become nobel laurates or saints and the world would be less vibrant without them.

I guess this is why my “private client rep” is calling and urging me to look at CDs when she sees my (temporary) large cash balances

Those morons are trying to convince you that they are smarter than you, the one who actually made money to invest.

Odds are probably still high for a Santa Claus rally so plenty of money to go into everything it appears.

Odds are high you’re ALREADY SEEN the Santa Claus rally

How ridiculous are people. “Odds are probably still high for a Santa Claus rally”, after an already 15% run in a month. When did you allow Wall Street bros in here?

My bad. I thought this was a website to learn about smart investing and how things worked. It there an oath or something needed here?

Disclaimer: I have equity positions.

We will need allegiance to “Nothing goes to heck in a straight line” please. 😄

Alright, give me the odds.

Glen,

>It there an oath or something needed here?

Yup. The oath should be “I promise to let others express their opinions, which might differ from mine, in peace or reply with constructive discussion since different opinions is what makes a market and nobody has a lock on future events.”

Of course, someone will probably flame me for this. ;-)

The simplest odds are 66% chance of Santa Claus rally but obviously performance of prior years is not guarantee of current returns😉

Everyone was calling for a 30% drop at the end of October. Permabears lost back most of what they gained since July in 3 weeks.

If the permabear was shorting the market, sure.

I’m a bear in today’s economy, and my new money goes into 5.5% guaranteed instruments.

To each his own.

Thinking the normal Santa Clara rally will be the opposite this year

Jamie,

Cupertino rally? Menlo Park rally?

I ❤ autocorrect/autocomplete humor. My kind of bone-dry meaning-filled humor.

I love that kind of autocorrect humor! Keep it coming.

People forget that 2018 was a Christmas horror show. Anybody with money in the stock market got a huge lump of coal.

Yes indeed, and they forget that munchkin had to get on his red phone right around christmas to save the markets. They then forget the fed started lowering rates in spring of 2019 (which they won’t be able to do this time) and they also forget the banking system went into crisis again in late summer/fall of 2019. They also still think 2020 was something other then 2008 on crack! When they lose it all in the markets next time, they won’t forget ;)

I’m not sure if i want to laugh or cry with how they pat themselves on the back, thinking they’re so smart, when really they’re riding the feds tailwind right into a hurricane.

https://blogger.googleusercontent.com/img/b/R29vZ2xl/AVvXsEg_LxXkwMYJornftGr1cnkMQMUgqOotkUjtHdbay5gkzvirB9389aqqdvef1UaV9pNaBb3YFMCjlmGk1v06aCkcQDTcnIuSUmIS8T4ev9fagt0Nr4pmLeoPM1xDxEo_TFgnz9Cam3ZzE8-5idWqRwFlIASexQ36S-7W6eVXU4CyDq9pSLYjhYZsx7lGCMM/s1000/commodities.png

Who cares ?

Why is such a monumental status given too the financial losses of the marginal speculators, setting the current price. There are credible sources who see the S&P at 1600, a historically valuation.

There are those who suggest that there is no better way to lose money than the current stock market, flexing in the sun.

The revaluation of the financially indefensible stock asset price bubble is important from the aspect of moral hope and commitment.

We only go around once.

Glen

I am still riding the rally. I think the next inflation print will be important. It could cause another 5-10% gain or send us back into muddle-through. Tax selling will end the rally and probably cause a pull back but I will stay fully invested. Only a big rise in unemployment will cause me to turn defensive and I don’t expect that.

And yet it’s real easy to find plenty of people who believe the American consumer’s savings are totally depleted while at the same time up to their necks in CC debt.

I do however expect this holiday season to be kind of a dud retail wise …. not because people are out of money but due to a spending hangover from all the partying this year.

Online sales already look HOT.

Not sure why anyone still goes to the stores though.

As weird as it sounds some of us still like it Wolf, also Canadian winters are cold and I like indoor spaces this time of year 😂.

With so many people still working from home, the middle fingers given and received while navigating mall parking lots is the only form of social interaction some people will get all year.

Good one

True that!

I’m seeing this too. Record number of orders yesterday on the website I fill orders for. Looks like a hot shopping season so far in e-comm land.

I think Black Friday was a record this year for online sales (up 8% from last year). In-store sales up 2% from last year. I worked Friday and had no plans to buy anything this weekend, but ended up spending $1k yesterday on a resin 3D printer and handheld 3D scanner haha.

Christmas sales will be extraordinary, in a blow off top, followed by the obvious signs that a recession, undeclared, has begun.

We bought 2 new iphones and one Samsung and got $800 trade in for each phone. Ours were almost 5 years old.

The solution to high inflation is high inflation. America is great enough to be the first nation in history to inflate away all government funding issues; we are “on a roll.”

I like to refer to it as the golden glow of inflation. Pockets flush with the current units of exchange, lose their normal resistance to paying more for the same product.

Wolf,

I know it’s not the subject of this article but what is the money supply doing?

My brother and I were talking about this last night. Thanks.

First year I will pay property tax on credit cards. $200 sign up bonus plus 15 months 0% APR while keeping it invested I will beat the 2.29% I pay for putting on CC.

Glen-

Your comment reminds me of a discussion I have not seen for a while: brokerage firm margin rates and usage. Might be a good subject a future post. (Apologies if it was covered recently and I missed it…)

Here’s a quickie: comparison of Schwab vs Fidelity: Schwab is better on Treasuries, at least.

The Schwab ‘Value Advantage Money Fund’ has a 7 day yield @ 5.38% currently. Listed assets are close to $163B. Average maturity of what it holds is 39 days.

It has a quick turn-time. You can use those funds to buy other investments. Part of my portfolio is with Schwab, and it’s nice to earn a bit over 5% on my “dry powder.”

That’s a great idea I’ll find a card whose was yours for 200 bonus?

I use nerd wallet. For the first $3000 payment I will be using a Wells Fargo autograph card since $300 back after spending $1500 in three months. 0% for 12 months. They have $200 cash back for less but less rewards points. Plenty out there and my property tax also takes discover and AE. I’ll pick AE probably for April tax payment.

It’s not retirement money but nice to stick it to banks and put $1000 or do in my pocket.

Glen,

thank you for sharing. I just applied for WF Autograph card.

Recently got $260 from BMO, and $243 from Citi (so $503 cashback after $3500 spend – mostly groceries). Was on look out for new card. Perfect timing. Thanks.

GIC rates in Canada are going down these days. Maybe this is how the overleveraged hoomers with mortgages get bailed out; lower mortgage interest rates, which lower savings and GIC rates which affect savers.

Canada will do anything to prevent home prices from drastically falling.

A month ago, there used to be 6% GIC rates. Now the same banks lowered it to 5%.

You can still get 5.3 percent insured for a ten year GIC at Motive Financial without going to GIC brokers. The CDIC ceiling of $100,000 is a joke. The only place you can really put money is the credit unions in Manitoba. Achieva Financial is still paying 5.2 percent for 5 years on unlimited funds. Oaken will cut their 5 year GIC rate to 5 percent from 5.15 percent at the end of this month and the 5.2 percent rate at Achieva will fall to either 5 percent or 5.05 percent after Oaken cuts their rate. If you have at least a couple of hundred thousand dollars use a GIC broker.

Oaken Financial is still paying 6 percent for a 2 year term until the end of this month. They have $100,000 x 2 coverage for insured $200,000 coverage if you split the GIC evenly between Home Bank and Home Trust.

The brokerage firm Wealth Simple is giving away a free Iphone 15 for $100,000 minimum for a year or an Iphone pro 15 for minimum $200,000 to the end of this month. So insured up to a million you can snag 10 Iphone 15’s for Christmas gifts. As long as the total asset balance doesn’t fall below 100 thousand any time during the next 365 days. Commissions are free.

It’s truly inspiring to see how Americans have navigated the financial landscape with astuteness. The surge in money market funds, large CDs, and small CDs reflects a collective effort in financial literacy and strategic decision-making. This trend highlights a proactive approach to managing finances and making informed choices.

Money naturally flows to where it earns the most yield, just like water naturally flows downhill.

That was exactly the topic of the wolf’s previous article.

This battle of the markets against the central banks will lead to another increase in interest rates.

“This battle of the markets against the central banks will lead to another increase in interest rates.”

I really hope so, and that’s what I told the realtor who was inciting FOMO and cheering rates coming down on her Thanksgiving YouTube video. Damn realtors are coming out of the woodwork again.

Markets in Canada, Europe and the US are betting on an imminent rate cut. It was the same in Australia.

And look what happened in Australia. After a pause, the bank raised interest rates again.

When everyone bets on a certain event, the opposite usually happens.

I think that at the moment inflation is staying low because of the drop in oil prices. I read the ECB’s Legarde’s position in which she says that this is the reason why inflation is still low. But this is unlikely to last long.

Let’s take a look at the probability of that here https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html This doesn’t indicate that probability has much chance of occurring. As always subject to change based upon the interpretation of future data points.

I don’t take stock in probabilities based on wishful thinking. You are right though. We have no idea what the Fed will do.

I don’t think that is the probability of the interest rate as much as the distribution of the bets on the likely hood of a declining interest rate structure as expected by the speculators.

Remember, the free market has been in control these past 15 years or so. The bias seems to be skewed in the direction that the monetary politicians will revert to form of easy money.

What is the relationship between these kinds of instruments and the high interest savings ETFs which have become increasingly popular in Canada?

CashTO is based on prevailing bond yields which fluctuate. Oddly, the 5 year is being pressured downwards.

There are suspicions going around that those in power will not allow those renewing their mortgages in a few years to be paying higher interest rates (it was only in late 2020 that people were getting 1% mortgages for 5 years. They will be renewing next year and 2025).

This means that there is a concerted effort to push down the 5 year bond so that home owners will not be subjected to 5% mortgage rates upon renewal.

What does this mean in the future? Savers will be getting lower returns. All in the name of preventing the Canadian housing bubble from popping.

5 year GIC rates should rise as the banks try to sucker all the people with mortgages coming due into 5 year terms that being the lowest of all the mortgage rates. With so much demand for 5 year mortgages it will push the yield on 5 year GIC’s slightly higher than it would otherwise be. Yes the Bank of Canada only cares about the housing market to prevent any run on the banks. Likely rents will shoot to the moon in Canada and less and less immigrants will come to Canada. The cost of living will be astronomical in the future as the Bank of Canada and the governors of Canada are going to do everything to inflate home prices. Tiff at the Bank of Canada even came out and said no more interest rate increases.

It’s about C$2,200 a month for a one-bedroom apartment, C$2,700 for a two-bedroom apartment, and almost C$3,000 for a 3-bedroom apartment in the Greater Toronto Area.

Rooms are going for C$800 or more a month. A room.

Imagine a couple with a child: They need a two-bedroom apartment, so first and last is almost C$6,000. This was a lot of money a few years ago.

The housing bubble is unsustainable in Canada. I’ve spoken with newcomers who have a wife and a baby renting a master bedroom with its own bathroom for almost C$1,500 a month.

By the way, thanks for the GIC rates at the alternative lenders. I’ll look into them.

Tiff at the BoC did NOT say that: His words at last

announcement:

‘Governing Council is concerned that progress toward price stability is slow and inflationary risks have increased, and is prepared to raise the policy rate further if needed.”

BTW: it is silly to think that Canadian rates are determined by the BoC. If they were, isn’t it a hell of a coincidence that they have gone up in perfect lockstep 10 times since the Fed began its tightening? Correlation does not always mean causation but in this case it does. ‘Pause’ by the BoC means ‘wait to see what Fed does’.

Moving on, this run up in CD rates etc. is bad news for banks in both countries. They have spent the decade in ‘banking heaven’, paying next to nothing for deposits while getting up to 20 % on credit cards. The Can banks were even getting some profit on the 3 and sub 3% mortgages. They are now underwater on those and if they have to pay 5 % for money, they will be losing money for years on their mortgage book.

The Can Govt just came out with words intended to sooth, including ‘banks should extend amortization period’ for squeezed mortgagors.

Which suggests the gov doesn’t read the news papers. The banks are already doing that, with one being extended from 25 to 47 years making national news.

But this can’t go on for years. Some mortgagors are already having to turn to alternate lenders to stay afloat as the first mortgagee, the bank, reaches the end of accommodation.

The banks and CMC, the Federal govt insurer would all be happier if instead of going to foreclosure the mortgagor would sell while he still has some equity. Prediction: if we get a flood of foreclosures, there is going to be a lot of bickering between CMC and the banks re: latter’s diligence on these loans in the first place’

@GenZ,

“It’s about C$2,200 a month for a one-bedroom apartment….in the Greater Toronto Area….Rooms are going for C$800 or more a month. A room.”

Plenty of university students are paying $1000/mo for rooms. San Diego State, UCSD, USD, for example. And as for the $2.2k for a one bedroom, that’s still less than what San Francisco mediocre neighborhood one bedrooms went for in…the ’90s.

It’s all relative, man.

Toronto ain’t no California in terms of the quality and pay of jobs, weather and being a vacation home for billionaires and millionaires. San Diego pays way higher salaries than Toronto.

In Toronto, they pay university graduates starting C$35,000 a year, while in the USA they would get at least USD$50,000 on a visa.

Data compiled by Joseph Asheim for member banks, by size of bank, and by ratio of time to total deposits, revealed that: as the ratio of time deposits to total deposits rises:

(1) the ratio of total expenses to total earnings is higher;

(2) the ratio of net profits to capital accounts is lower;

(3) the ratio of net profits to total assets is lower;

(4) the ratio of dividends to capital accounts is lower; and

(5) the ratio of capital accounts to total assets is lower.

All these relationships ad up to one conclusion: “the higher the ratio of time to total deposits, the less profitable are banks of a given size group”.

Yes, banks and their stockholders HATE having to compete for deposits. It raises their cost of funding and squeezes their margin, which is how it should be. The freebies for the banks since 2008 were a horror show. Look at bank stocks. Most of them have fallen below their Feb 2020 high, some of them below their March 2020 lows. Even JPM, which hugely and uniquely benefited from the rate chaos, trades well below its Oct 2021 high.

The bigger banks in many cases, outside of marketing promos, don’t like to pay a lot of interest. Some will offer a bonus if you put money into a savings account but often the Internet is .1% or so. The bonus in that case is also taxable as interest income compared to credit card rewards which aren’t. Plenty of good options but the big bank marketing machines are in high gear. I tend to do treasuries mostly with Ally bank as a more liquid account and they have no penalty CDs which is really a savings account marketed as a CD but at least term guaranteed which means nothing until rates go down. Not the absolute best rates but was able to get it into a trust online with minimal paperwork. Dont want those to come after me to have to deal with probate.

Do “Money Market Funds” shown on the first chart include the FDIC-backed “Money Market Accounts” offered by my local bank, or are the latter counted as bank deposits?

I assume that FDIC guaranteed money market accounts generally off lower yields than non-FDIC-backed funds…?

Many banks also offer money market funds, and they’re included.

“And then very reluctantly they stopped trying to endlessly screw their existing customers and began to offer 5%+ CDs to their existing customers to retain the deposits they still had.”

Not my retarded bank. Only new money, they say, as I move my money out. What idiots.

I move around a bit but somewhat challenging as few online types of banks offer solid ways to easily setup as trust account. I take some chances but ensure it matures back to a trust account. I’m only mid 50s but no guarantees and single dad so all that planning necessary for me.

Care to share the names of the online banks you’ve found to make trust accts easy?

1) The 3M was a flatbed hugging zero rate between 2008 and 2015 and again between 2020 and 2021. A 3% CD was a bargain.

2) During the pandemic, when the economy was shut down the Fed raided banks accounts in repetitions to support shingle mums, small businesses, the elderly… transferring wealth to the poor and the middle class, creating a tsunami of money. No printing !

3) Commercial banks liability reached $18.2T. It’s down 900B. MMF are

up 900B to $6T. All that money in the gov roach motel.

4) Between 1981 and 2021 the long duration and the middle were above the 3M. Since 2021 rates have risen together, tangled with each other, until early 2022. Since 2022 the 3M minus 10Y flipped from (-)2.3% to +1.9%. The 3M minus 5Y also flipped to +1.9%. The 3M minus 2Y to +1.4%.

5) For the first the 3M is above the middle and the long duration. There is no reason for banks and MMF to pay 5.5%.

6) One day, even during a recession, the 10Y might rise above the 3M to please buyers.

see: https://www.stlouisfed.org/on-the-economy/2021/august/banks-navigate-surging-deposits-tepid-loan-activity

“Total deposits can be broken into transaction accounts and non-transaction accounts. Transaction accounts consist mostly of checking accounts. Non-transaction accounts consist mostly of money market deposit accounts but also include certificates of deposit (CDs) and other savings deposits.”

The composition of the money stock changed. It included a higher percentage of transaction accounts relative to gated deposits. This has fooled economists.

spencer-

I’m not seeing the change in money stock composition on the post you linked to.

From past readings, I thought they had used a terminology of “Time Deposits” v. “Demand Deposits.” Time deposits offered the depositor higher rates because you were more locked in, while demand deposits gave the depositor more liquidity, but were subject to rate limitations set by banking regulators. These rules, established in hopes of promoting a safer banking system, but were watered down over time. I’m foggy as to exactly when, but was intrigued by your post.

Maybe I’m way off base here. Is this the same subject you’re talking about?

The % change was 103.2.

Last month while visiting my credit uniom, I was giving the teller a hard time about their below-market yields (3-4% CDs, 1-2% savings accts). A week later I see a big ad on their webite: 5.5% 6-month special! Maybe they actually listened…

P.s. very minor typo Wolf: cause should be past tense here.

“This cause all kinds of fears that some of the MMFs could “break the buck”

I’m getting 6% on one of my 1 yr CDs at my local credit union. They have these promos every once in a while. Grab them while you can. Why take the risk in the casino (stock market) when you can get a guaranteed return like that. —-k the stock market.

Wow 6%, I’m jealous. The highest yield of any of my fixed income things is 5.55%

The federal deficit is a BLACK SWAN.

A black swan is something that is sudden and unexpected. The federal deficit is neither of those…

Reverse repo plunged to $865BN, down $65BN in one day, in one of the biggest liquidity injections in RRP history.

Also, fast approaching the $700BN reverse repo liquidity constraint level

*Overnight reverse repos

Helmut,

1. “in one of the biggest liquidity injections in RRP history.”

No, ON RRPs don’t “inject liquidity”. ON RRPs are cash that money market funds have in excess and store at the Fed to collect interest. When RRPs drop, it means money market funds are buying more of the flood of T-bills that the government sells every week, now that T-bills pay more than RRPs.

In terms of money flow, the MMF cash in ON RRPs (a liability at the Fed) moves via T-bill auctions to the Treasury Department’s TGA (also a liability at the Fed), which is the government’s checking account. Anyone, including MMFs, who buys T-bills (or any Treasury securities) at Treasury auctions moves that cash into the TGA, where it becomes part of the operating cash of the government, which then spends it on all the stuff it pays for. It doesn’t go into the market.

2. “Also, fast approaching the $700BN reverse repo liquidity constraint level”

This is TOTAL BS. I don’t know who the ignorant bloggers are on the internet that are still spreading this BS. I have shot this down a few days ago with an entire article, just for YOU. RTGDFA:

https://wolfstreet.com/2023/11/19/our-wall-street-crybabies-want-the-fed-to-stop-qt-and-they-wag-the-overnight-rrps-thatll-blow-up-the-banks-or-whatever/

The normal condition for ON RRPs = $0. It’s only QE excesses that caused the two big spikes in balances. RRPs will go back to $0 where they had been in March 2021. It’s “reserves” that you need to watch — they won’t and cannot go to $0, but they actually rose to $3.4 trillion.

Here is a 15-year chart of ON RRPs. Note the $0 levels during the more normal years:

Thanks Wolf, it was just a copy & paste from ZeroHedge@X.

It was supposed to be just a note to the audience that RRPs are going down fast.

Yes, they’re going down fast. They’re going back to normal. That’s a good thing. Money Market funds should buy T-bills — that’s what MMFs are for. And by golly, there are lots of T-bills to buy.

The TBAC: “In the past the Treasury did impact the money stock figure by allowing commercial banks to hold Treasury funds in Treasury Tax and Loan accounts, but since January 3, 2012, funds in these accounts must be transferred to the Fed by the close of business on the day they are received so the end-of-day balance is always zero”

The Wall Street free money junkies are constantly clammoring for another fix. They desperately want Powell to cave to their whims. Not mentioned thus far is how seniors have flocked to short-term CDs and Treasuries paying higher rates. TINA has left the scene. As long as they can keep their money in safe, short-term CDs and T-bills yielding 5% or more, seniors will reduce both their allocations to stocks and long-term bonds. This episode of rising rates has put a real dent in the 60-40 allocation. It’s being replaced with a hefty proportion to short-term safety. Just what seniors have wanted for 10+ years while the Fed suppressed rates. It’s high time for a rate structure aligned with historical norms. Let the 10-year Treasury yield 5%. And 30-year Treasuries even more. Cheap money destroys wealth and purchasing power. The dollar needs to be on a much more stable footing.

I put what I had into long term bonds before October 27th but I’ve got about 10 times that amount coming due at the very start of next year. I expect the bottom to fall out of interest rates between now and the first week of January next year.

Wolf, you didn’t mention I-Bonds. Thoughts please?

They don’t belong into this discussion. They’re 30-year variable-rate zero-coupon long-bonds indexed to CPI plus a base rate. They’re a long-term retirement investment. And you can only buy a small amount of them every year ($10k); you cannot move large amounts of money into them on a whim.

Canada Retail Sales Up led by new car sales +2.4% while Manufacturing down sharply. source gov of Canada.

Mexico GPD Growth increases for 10 Consecutive Quarters.

US Sharp drop in jobless claims 209K declined 24K they were forecasting 225K.

The US Government Debt to GDP 129% source: office of management and budget, the white house.

– Our US Banks and Brokers must buy US Gov Long Bonds from the Treasury and resell them at a profit.

I Do Not Make Any Money for disclosing.

This proves that banks COULD have been paying interest during the 14 years of ZIRP. If interest was an untenable expense, they wouldn’t be paying it now.

Seems ripe for a class action lawsuit.

But during ZIRP, banks were not earning very much interest on their loans, so there was no incentive for them to pay more to attract deposits to turn around and lend. Supply and demand.

polistra:

“Seems ripe for a class action lawsuit”.

On what basis? You agreed to the terms. You signed a document that claimed you read and agreed to said terms. Your “class action” is based on what?

That’s like saying that the bazillions of dollars that a multitude of people have in checkbook/passbook accounts paying .05% could “file a class action lawsuit” because they “shouldacouldawoulda” been paid more interest if THEY paid attention. Some are still holding out for the free toaster.

Making your money work for you isn’t easy. Takes time, planning, and action.

PS: The only people who win out in a class action lawsuit are the lawyers. Write it down.

I can see the year 2008 marking the year all my bank balances started going down the drain for the next 14 years straight. My net worth would have been infinitely higher if Ben had of just let the banks fail back then.

My mom was locked into a 5 year CD making .5% (from 2021).

I convinced her to call the bank and see what she could do. The bank charged her a small fee to switch to a short term CD with 5.5%.

She just didn’t realize it was an option until I explained it to her. And I knew because of this great site!

Everything is always negotiable. I just negotiated with a credit union on a share certificate that was charging a hefty early withdrawal. I guess they needed to keep my money badly enough to waive it entirely since I agreed to keep my money there in a cert with a much higher rate.

Elbowwilham-

Useful post!

I am not arguing against brokered CDs, but your story is a great example of why it pays to have a smattering of CDs from local institutions in one’s portfolio.

All of my Fidelity CD’s had an early term penalty, but you can dump them online overnight without having to communicate with anyone, nor write checks or make transfers. I think most online brokers have the same convenience.

I would like to see a graph over time of the banks’ “spread”. Also average size of loan along with number of loans made, broken down by small, regional, and large banks. This would tell us how screwed (or not) banks are. I suspect the small banks are eating it.

I’m on the 10 year plus plan where I’ll take my risks with the stock market in exchange for lower tax rates for long-term capital gains.

It’s not for everyone though.

And if you lose money in the stock market, you will never have to pay any taxes at all!!

The U.S. stock market if you don’t include Bitcoin is the last remaining ponzi. The Chinese real estate ponzi finally imploded really leaving just the U.S. stock market. The plunge protection team and all those circuit breakers won’t prevent a closure of all the major exchanges and a reopen at least fifty percent lower.

I have been doing just fine with the stock market over the last 40 years and also with Bitcoin over the last 8 years. I know most comments here are anti crypto but it was and will always be a great diversification tool for me.

Hey wolf,

Thanks again for your work and generosity of your knowledge. One cd I have has no call protection down about 15 points lower. I’m wondering about it being called or anyone else’s experience with a cd with no call protection.

If you have a callable CD, it can be called by the bank. So if rates drop a lot below the CD rate, the CD will probably be called. You’ll get all your money back, plus any and all accrued interest up to that point. You can buy another CD with the proceeds, but it will have a lower yield.

You got a higher yield to begin with because it was callable – which is why people buy them; they want that higher yield. But now there is a risk that you won’t get the lovely higher yield for the rest of the term of the CD. It’s not the end of the world.

Thanks Wolf,

We’ll see.

On GNMA mortgage backed securities they used to call that “repayment risk.” You got principle return early only at those times (after market rates had declined) when you didn’t want to be paid back.

Similar to your situation with the callable CD. Great that it’s only a part of a larger fixed income portfolio.

Thank you, interesting article.

Looking at Schwab’s bond trading page, 5 year Treasuries are yielding 4.51%. 5 year non-callable CDs yield 4.55%. There are 9 states with no income tax where it might make some sense to buy the CD, but maybe not even then as they are less liquid than the treasuries.

Also, poking around the ICI website, there is an interesting table that, on a weekly basis shows flow of funds into and out of the 3 types of MMFs. Institutional investors are going for government funds and individuals for prime and tax-free. Not sure what that is indicative of, but interesting anyway.

Most ‘money market funds’ are not FDIC insured.

Unrelated to this article except to the degree it could influence higher for longer decisions.

How much pressure exists both economically and politically to get housing market going in 2024?

Seems clear at this rates it won’t move as will be few buyers and sellers. Obviously this will be market by market but can’t see housing prices fall significantly, perhaps 10-15%, and feels like what gets it moving is lower interest rates, perhaps 3.50% or lower by Spring 2025. The combination of lower interest rates combined with decline in housing prices might jump start the market.

My only driving theory behind this is that affordable housing and mobility is not only an economic but political decision which as long as the Fed thinks inflation will stay in current range it might happen. Admittedly it will be difficult to separate the election ‘promises’ from what happens but young people not being able to buy a house hits a huge and important demographic. Of course the Fed will stay strong on the 2% inflation target but strong messaging is one thing and services inflation is a hard nut to crack.

Lower rates will only raise prices. Lower rates and you pull more buyers back. Those buyers will be clamoring to flee the sky high rent inflation. Its 12% in my state this year (NH) likely 8% nationally. Likely to maintain that rate of inflation for the rest of the decade. Maybe for the rest of all time. Its been +5% for a decade even before covid. Theres no fix here. System needs to collapse.

CNBC headline this morning:

“Stock futures fall slightly on Monday with Wall Street riding a four-week winning streak”

Somehow my mind did its own auto-correct and I read that as “four-week WHINING streak”

CDs MMFs and T Bills get taxed as ordinary income so that 5 percent becomes 3 percent real fast for anyone making wages now. When inflation is 5 percent those instruments aren’t really an ‘investment’. If you want to beat inflation you have to be in real estate, the markets, or other riskier investments.

They arent all equal unless you are in a state that has no state income taxes. I benefit from treasuries over CDs, all else being equal.

Sam,

1. Interest income from Treasury securities, including from T-bills, is exempt from state income taxes.

2. Taxes are also applied to income from equities, etc., just like CDs and money market funds.

5. Inflation eats the purchasing power of all assets, including risky assets. So you lose 20% on your stocks over two years (“risky assets”!), and inflation eats another 10% over those two years, you’re down about 30%. There is no escape from inflation.

I jumped onboard, MMF 5+%, bank 4.8% savings account. I did see a video of FDIC officials saying in a large banking crisis they wouldn`t have the money. I believe someone said they have enough to cover 1% of deposits!

“…someone said they have enough to cover 1% of deposits!”

That’s ignorant BS. And bloggers — such as those you heard this from — who say this are braindead and should be unplugged.

Banks have ASSETS, $23 trillion in ASSETS at commercial banks alone. When the FDIC takes over a bank, it gets ALL the assets, and it sells those assets, and the proceeds pay for most or all of the deposits it guarantees, with only a small portion if any coming out of the fund. Even in SVB’s case, where the FDIC unnecessarily made ALL account holders whole, not just the insured account holders, the assets covered all insured deposits and most of the uninsured deposits.

The loss to the fund would have been zero had the FDIC not decided to make uninsured account holders (the billionaires and their startups) whole, because the assets exceeded the insured deposits. But even covering the uninsured deposits, the loss was pretty small because SVB had a lot of assets that the FDIC sold.

The FDIC is backed by the US government and can borrow from the government. Even during the big bad Financial Crisis, the FDIC never failed to cover the deposits.

Spreading braindead BS about banks is one of the seven deadly sins of commenting here and gets you on the moderation list. Stop reading sites that tell you this BS. They’re lying to you. And if you do feel compelled to go to these sites to eat their BS, don’t crap it into here. Suck it up.