Last remaining bailout tool from the March bank panic goes away. Current arbitrage may have been a factor in shutting down this baby.

By Wolf Richter for WOLF STREET.

The Bank Term Funding Program (BTFP), the Fed’s infamous tool to nip the March 2023 bank-panic and liquidity crisis in the bud, will expire on March 11, at its original one-year time limit, Michael Barr, Fed Vice Chair for Supervision, said at a panel appearance in Washington, D.C., today.

“The program worked as intended,” he said. “It dramatically reduced stress in the system very quickly,” he said. “It was highly effective.”

Banks can continue to take out new loans under this program until March 11, and refinance existing loans for a year, he said (reported by MarketWatch).

And that would be it for the March-2023 generation of liquidity measures. The other liquidity measures of that generation have already been paid off. We discussed all of them in our regular Fed balance sheet discussions, including last week here.

The BTFP was a new program put in place on March 12, 2023, to deal with a panic among depositors that had led them to yank their cash out of a bunch of banks, in some cases essentially in days, leading to the collapse of three regional banks, Silicon Valley Bank, Signature Bank, and First Republic, where all depositors were made whole by the FDIC, but investors were wiped out. A fourth bank, Silvergate Capital, which had experienced the first run on the bank in this cycle was unwound under pressure but without FDIC funding.

The BTFP had two specific features that made it less costly for banks to borrow from the Fed than at the Fed’s long-existing Discount Window:

- Banks could post collateral at the purchase price, not market value, but the collateral had to be purchased before March 12, 2023, so that banks couldn’t game the system. The Discount Window requires collateral valued at market value.

- Interest charged is a fixed rate for the term of the loan (up to one year) equal to the one-year overnight index swap rate, plus 10 basis points. This made it a little less costly than the Discount Window, whose rate is set by the Fed as one of its five policy rates (currently 5.5%)

The arbitrage.

But this feature #2 became a hot item in early November, when Treasury yields of one year and longer began to plunge on the rate-cut mania, with the one-year yield eventually dropping to around 4.85% in December. And the BTFP’s one-year overnight index swap rate, plus 10 basis points, moved in the same range.

So banks could borrow at around 4.85% from the Fed, and then leave the cash in their reserve accounts at the Fed to earn 5.4% on it, for a nice risk-free spread. This arbitrage opportunity caused a surge in the BTFP balances starting in early November.

Given that balances are still relatively small compared to other items on the Fed’s balance sheet, and compared to big banks, it’s likely that larger banks weren’t allowed to pursue this trade.

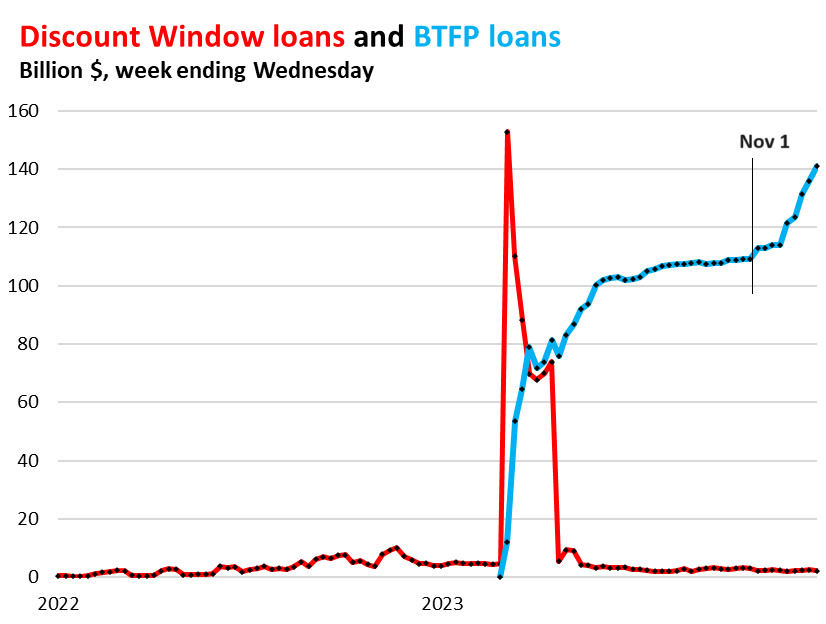

Since November 1, the BTFP balance (blue line) jumped by 30%, after having been essentially flat in the prior three months (the Discount Window is the red line):

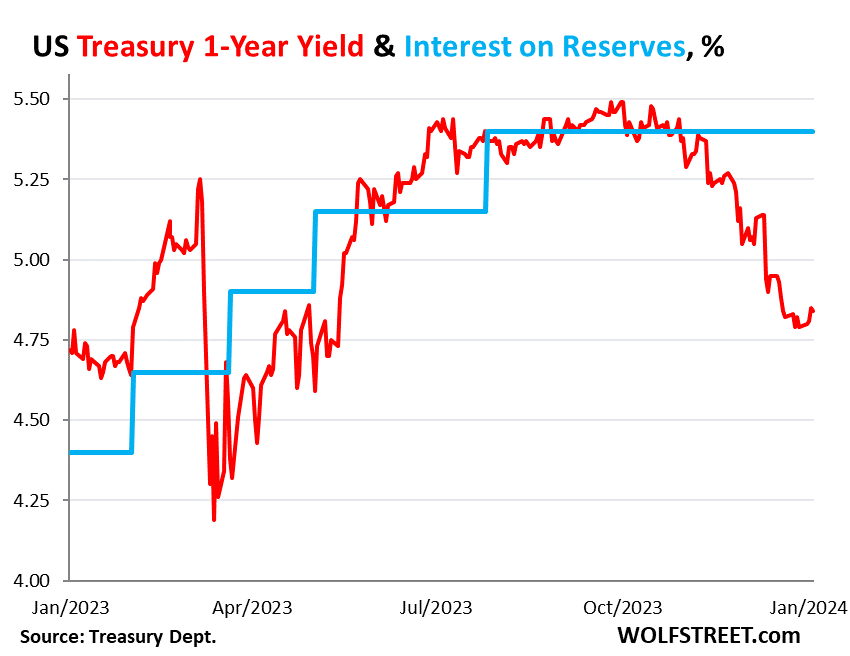

Since the BTFP’s rate (one-year overnight index swap rate, plus 10 basis points) runs close to the one-year Treasury yield, we use it as a stand-in for the chart below: It compares the one-year Treasury yield (red line) to the interest rate that the Fed pays banks on their reserve balances (blue line).

In early November, the red line (ca. BTFP cost of funds) dipped substantially below the blue line (income earned on those funds), and that’s where this risk-free arbitrage became profitable, and at least smaller banks jumped on it.

This arbitrage may have been another motivation for the Fed to shut down this baby.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

This is a cool angle, surprised that the Fed allowed this, but guess it’s not that huge in the grand scheme of things. Somebody wrote in on either one of my articles or yours to say that they thought the banks only made $100 million or so off the arbitrage, so it’s not a ton of money. They should let this expire.

Bloomberg article quoting Lorie Logan is interesting, they say the Fed may slow the pace of QT– I disagree and don’t think they should, but it seems like something they may do based on their past behavior. Of course, the cocktail party conversation is that they’re doing to try to help the Democrats.

Do you think the Fed will alter QT?

OK, I will post it again. #4. The Bloomberg headline twisted what Logan said. Here is what she actually said.

READ THE WHOLE THING ENTIRELY and don’t try to summarize it five words.

Also note that her refence to “when ON RRP balances approach zero” means that by that time, total assets must be at or below $7 trillion.

The last paragraph (bold) is crucial.

https://www.dallasfed.org/news/speeches/logan/2024/lkl240106

Turning to the Fed’s balance sheet and policy implementation, we have reduced our securities holdings since mid-2022 at a brisk pace consistent with the principles and plans that the FOMC announced earlier that year. While securities holdings have declined by $1.3 trillion, bank reserve balances have actually risen by $350 billion dollars to around $3.5 trillion. That’s because reduced balances in the Federal Reserve’s overnight reverse repurchase agreement (ON RRP) facility have more than offset the decline in securities holdings. Increased Treasury issuance and a less uncertain interest rate path have contributed to the rapid ON RRP runoff by motivating money market funds to invest more in Treasury bills.

Money markets and policy implementation are continuing to function smoothly. As we did in 2018 and early 2019, we are likely to see modest, temporary rate pressures as our balance sheet shrinks and our liabilities redistribute. These rate pressures can be a price signal that helps market participants redistribute liquidity to the places where it’s needed. Experience shows that these pressures tend to emerge first on dates when liquidity is unusually encumbered or is draining out of the system especially rapidly, like tax-payment dates, Treasury settlements and month-ends. And indeed, we saw small, temporary rises in the Secured Overnight Financing Rate (SOFR) over the November–December and year-end turns. But on nearly all days, broad money market rates have remained well below the interest rate on reserves.

The emergence of typical month-end pressures suggests we’re no longer in a regime where liquidity is super abundant and always in excess supply for everyone. In the aggregate, though, as rate conditions demonstrate, the financial system almost certainly still has more than ample bank reserves and more than ample liquidity overall. The most recent Senior Financial Officer Survey shows that most banks in the sample have reserves well in excess of their lowest comfortable levels and desired buffers. ON RRP balances remain around $700 billion. And the Federal Reserve’s Standing Repo Facility (SRF) provides a backstop against any unexpected pressures.

Still, individual banks can approach scarcity before the system as a whole. In this environment, the system needs to redistribute liquidity from the institutions that happen to have it to those that need it most. The faster our balance sheet shrinks, the faster that redistribution needs to happen. I’d note that the current pace of asset runoff is around twice what it was in the first half of 2019. And while the current level of ON RRP balances provides comfort that liquidity is ample in aggregate, there will be more uncertainty about aggregate liquidity conditions as ON RRP balances approach zero.

So, given the rapid decline of the ON RRP, I think it’s appropriate to consider the parameters that will guide a decision to slow the runoff of our assets. In my view, we should slow the pace of runoff as ON RRP balances approach a low level. Normalizing the balance sheet more slowly can actually help get to a more efficient balance sheet in the long run by smoothing redistribution and reducing the likelihood that we’d have to stop prematurely.

So what exactly is the correlation between bank reserves and the RRP facility? The RRP facility was not responsible for the 2019 repo problem. When the Fed now gets panic and start to slowdown their balance sheet run off, we will never see any large run off or a lower balance sheet in the future. Additionally, i predict we see relatively soon a new QE.

The “new normal” at the Fed since years: They do because the market wants, not because it is necessarily.

ON RRPs had nothing to do with the repo blowout in 2019. Money markets use ON RRPs to deal with excess cash. RRPs can go to zero, no problem, and they were at zero or near-zero for many years. They just spiked during the last phases of QE to absorb excess liquidity in the money markets. And money markets, whose assets are still growing, have been moving their cash from RRPs to regular repos and short T-bills whose yields are a little higher than the 5.3% the Fed pays on RRPs.

Note the years when RRPs were zero or near zero, and that’s where this is going to. That’s the normal condition for RRPs:

Banks use reserves to deposit some of their cash, and reserves are the thing to watch, not RRPs. When reserves dropped below $1.5 trillion in 2019, banks stopped lending to the repo market, and it ran into problems. Now reserves are at $3.4 trillion.

Liquidity shifts around, as Logan explained. So for example, in 2022, depositors pulled their money from banks and put it into money market funds because they paid more, which caused reserves (bank cash) to drop in 2022; but in 2023, banks hiked their interest rates on CDs to preserve their liquidity and they were successful and attracted deposits, and reserves rose.

The thing that the Fed watches is reserves – based on its 2020 doctrine of “ample reserves.” And reserves are still very high, with lots of room for QT, even after RRPs go to zero:

The Fed is great at coming up with all sorts of new ideas to inject liquidity in the banking system. It doesn’t matter what you call it: QE, RRP or BTFP. It’s all massive liquidity that’s just “lent” into existence.

The funny thing is that the banking system, in general, always comes out on top. Whether it’s $100B in annual RRP interest or whatever, there’s enormous, guaranteed money that goes into the pockets of all these entities that employ tons of people that receive the trickle down. And, it’s all lent out as guaranteed money.

Nobody really has to do anything but sit back and collect the gravy.

I agree with you Wolf. As you mentioned correctly, the bank reserves are high enough, and give the Fed a lot of room for further QT. Than i ask me the question, why a empty RRP facility requires a slower balance sheet runoff, in the view of Lorie Logan? Is she understanding the system?

@guesswhat – You nailed it. I lost track but I think since 2009, there have been over 20 special FED programs to save something (banks, hedge funds, etc) , inject liquidity, or some way to juice the economy.

The FED has our back. They seem to be doing a pretty good job. No big economic blow-ups. Economy seems to always be in a goldie-lock phase. There is no fear in the stock market. Every dip is bought.

All the Central Banks and Government money has to go somewhere. Geeze, even Bitcoin is doing well.

Buy America as Warren Buffet says. Buy American stocks and residential real estate. (not commercial) as the FED will have your back. Everyone else in the world is doing so. Live within your means and sock that extra money into the stock market. It has been a winning strategy since 1980. ???

I’m with GuessWhat. Arbitrage = more on-going bailouts for the banks. When will it stop? The answer is never, this is the whole system now.

Forget the american dream, we all have to support the speculator and banktocracy.

The nuttier the fabrications and conspiracy theories, the more people find them entertaining? That’s how fiction works.

I’m getting tired of seeing this BS on my site tho.

Wolf,

Thanks for adding the context– this is a more complete picture than I got from reading the Bloomberg piece.

If the Fed does start to taper QT at the point when it’s balance sheet hits $7T, there would be $3T of debt monetization still floating around just from 2020 forward, highly elevated M2, housing prices at all time unaffordability, stock prices at near record valuations, unemployment near all time lows, inflation likely still elevated, etc.

I have trouble understanding why it would be time to start tapering QT, unless the priority is asset price levitation. I think the “uncertainty” Logan wants to avoid is really just price discovery.

Bear in mind, the economy operated fine before 2009 with liquidity at a fraction of current levels, relative to GDP.

By 2026, the balance sheet cannot possibly go much below $6 trillion due to the Fed’s liabilities (TGA, currency in circulation, and reserves). We’ve covered this many times. So they slow down likely in ca. 2025 for the last mile, rather than sprinting all the way to the end?

Even if the balance sheet stays flat for a while, that’s a form of QT because the TGA and currency in circulation will grow (in part due to inflation), and so liquidity comes out of the financial system even if the balance sheet stays flat, but just very slowly. The Fed did that between 2014 and 2017, before it started QT proper.

Before 2008, the balance sheet always grew largely with currency in circulation. At that time, the TGA was with JPMorgan and other banks. The TGA was moved to the Fed in 2009, which caused another jump in the Fed’s balance sheet but had nothing to do with QE.

They could reduce assets much lower than $6T if they took excess bank reserves out of the system. It’s inflationary tinder that should be removed from the system. The historical chart of bank reserves is eye popping. The excess reserves influence banks to make loans they otherwise wouldn’t make. You combine that with lowered bank capital requirements and it’s a recipe for taxpayer bailouts.

If the Fed truly wants to normalize, it means getting liquidity levels back to levels before the housing bubble. We’ve been waiting for 15 years for market discipline to return, but the Fed keeps it’s foot in front of that door with its ample liquidity regime.

Wolf, why can’t the Fed reduce its currency in circulation (by requiring banks that get deposits to remove it) and make the banks reduce their reserves?

In other words, what caused the reserves to grow that much, and how can they be shrunk?

The amount of currency in circulation is demand-based through the banking system. If you walk up to a bank anywhere in the world and want to buy US paper dollars (such as ten $100-bills), the bank either has them in stock or gets them from correspondent banks in the US, and they get them from the Fed. The US banks cannot “buy” these paper dollars (“Federal Reserve Notes” is their official name). They have to exchange collateral, such as Treasury securities, with the Fed, which is why Treasuries (assets on the Fed’s balance sheet) rise when banks get more “Federal Reserve Notes” (liabilities on the Fed’s balance sheet).

Currency in circulation peaked in June 2023 and has since then dipped just a little. This is very unusual and likely related to inflation, with people moving their paper-dollars into interest-bearing accounts. So the banks get those paper-dollars back, and they then send them back to the Fed (and get their Treasury securities back) and the outstanding stock of paper dollars dips just a little.

But paper dollars are used in part overseas for nefarious purposes, tax dodging, or in countries like Zimbabwe or Argentina that trashed their own currency, or in countries that have officially dollarized (Ecuador, El Salvador, Panama, and a bunch of island groups).

Thanks Wolf, this is helpful. But instead of exchanging treasury securities for currency, why can’t banks just withdraw it from their reserve account at the Fed?

That would be like “buying” them — paying cash for Federal Reserve Notes. But they’re not for sale. They’re “notes,” meaning money that the Fed owes you. The Fed doesn’t sell them. So banks can borrow them for free, but they have to post collateral. And when they bring those FRNs back to the Fed, they get their collateral back.

That’s how it has been set up from the beginning for the major modern central banks. It was designed to let central banks fund themselves and help fund the government. They would issue the paper currency which doesn’t pay interest, in exchange for securities that DO pay interest, and the central banks put those securities on their balance sheet and earn the interest from them, which is their income to fund themselves. Before QE, that’s how modern central banks funded themselves.

For example – assuming a no-never-QE balance sheet – the $2.3 trillion in currency in circulation now put $2.3 trillion in interest-paying securities on the Fed’s balance sheet. In normal times, the Fed might make 4% on those securities, which would amount to $92 billion a year in interest income. The Fed would use $2 trillion to live on and remit the remaining $90 billion to the US Treasury. This way the currency in circulation gets turned into an income producing asset for the government and for the Fed. It’s a pretty nifty setup. But QE perverted the whole thing.

BTW, collateral can be other assets as well, such as MBS. There’s a list of what’s approved collateral.

Thank you. This is a lot to wrap my head around. I’m going to look at the break down of the balance sheet and try to understand how the currency in circulation increased, and what implication that had for the balance sheet, and how it could ever increase or decrease.

Also, I question whether the Fed should provide ample liquidity. In a free market, market participants are supposed to manage their own liquidity. They should maintain a strong balance sheet, or be in a position to take on debt or attract equity.

The ample liquidity provided by the Fed supplants market discipline that would ordinarily occur.

If parties want or need liquidity, let them go out to the market and get it. It’s not the Fed’s job to subsidize them with ample liquidity and higher equity prices. That’s distortion.

Too often, a “need” for liquidity is used as an excuse to avoid market discipline and price discovery.

Two comments:

1. Lorie Logan/Dallas Fed: “individual banks can approach scarcity before the system as a whole.”

Comment: Scarcity of reserves, that is. This what I have been saying for years. The FED “ample reserves” policy since 2008 is in part a “no bank left behind” policy to prevent ANY full Fed member bank from going under due to zero (or low) reserves left. It is a terrible policy, but it is what Fed does. Lots of reserves (the only real money) sloshing around tends to save the weak banks, because some of the reserves slosh into THEIR reserve accounts.

2. Lorie Logan/Dallas Fed != Logan Kane, wolfstreet poster. I was confused for a moment who “Logan” was.

25 bucks (to charity) says the Fed will introduce a new program/”tool” to bail out banks in some creative way before the year is up.

They’ll have to, the CRE and other junk loans they have on their books probably guarantees it.

Covid times was a (hopefully) once in many lifetimes illustration of collective madness.

Wolf, would like to see a chart or reference to a chart that shows how much the IRS takes in on a monthly or quarterly basis from tax withholding. Think this would give a better picture of the economy that these bizarre employment stats

“would like to see a chart or reference to a chart that shows how much the IRS takes in on a monthly or quarterly basis from tax withholding.”

In terms of income taxes, the source of variability is capital gains taxes. That plunge in capital gains tax receipts from the huge record in 2021 to much lower levels in 2022 (because markets tanked in 2022) caused overall tax receipts to drop in Q1 and Q2 2023. I report on that stuff quarterly (since estimated taxes are paid quarterly):

https://wolfstreet.com/2023/11/29/us-government-interest-payments-on-the-ballooning-debt-vs-tax-receipts-gdp-not-as-bad-as-in-1982-1997-but-getting-there/

In terms of just withholding taxes, the go-to source on a quarterly basis is Social Security contributions data, but that’s misleading because SS withholdings (included in estimated taxes) are capped at the top (at $160k in 2023), so the top end of the income trends don’t show up. I report on this annually as part of my Trust Fund report. These are fiscal years through Sep 30:

https://wolfstreet.com/2023/10/23/social-security-update-trust-fund-income-outgo-and-deficit-in-fiscal-2023/

Nyguy,

“They’ll have to, the CRE and other junk loans they have on their books probably guarantees it.”

Using BS to come up with Fed predictions leads to BS Fed predictions.

1. The SOLD all its corporate bonds and bond ETFs in the fall of 2021, and we covered this here.

2. The only “CRE” on the Fed’s balance sheet are $8 billion of government-guaranteed (Fannie Mae) CMBS, where the government takes the credit risk.

Sorry to pop your bubble.

I think he was referring to bad CRE loans on bank balance sheets.

Assuming there are some bad bank loans, I think the Fed should let the private market sort it out by forcing banks to attract debt or equity financing if necessary. Reducing bank stock buybacks and executive bonuses would be the best start, along with increased capital requirements.

The Fed must force banks to begin to deal with normalized liquidity. Bank executives have received poddy training for two decades by now.

I think Nyguy’s quote should be: “[The Fed will] have to, the CRE and other junk loans [the banks] have on their books probably guarantees it” as a response to Declan’s “the Fed will introduce a new program/”tool” to bail out banks in some creative way before the year is up.”

But, I think the commercial real estate loans aren’t so much on the banks’ books, but on REIT investors’ books, as I believe you’ve said elsewhere.

In any case, still BS.

Yes, only bubble is the one you’re in wolf, like that Seinfeld episode lol. I was referring to the banks, especially regional. Sure they offloaded some or maybe even most of the loans but I have a hunch not all. And maybe there are provisions in it forcing take backs in the case of fraud. Theres a woman on youtube named Melodie i think that talks about this. Seems like there could be plenty of issues for the banks, not to mention an inverted yield curve and very little loan activity.

The Fed will drop rates before they begin to consider new QE during the next recession.

No QT is tightening, I’m glad that was explained. Similar concept to holding rates steady is tightening, during times of disinflation.

Doing nothing has consequences. Yet I’m guessing the Fed attempts to front run the 2024 elections somewhat, in May/June. Fed has his hands full this year with the idiotic political system that doesn’t require members to understand basic economics and/or require useful real world experience.

Thanks, Wolf, for shining a light on this obscure corner of a Fed rescue project. For the ranters who cannot give the Fed a sliver of an even break, it’s clear to me that they were trying both to rescue numerous bank failures and do it with minimum moral hazard.

Somewhat off subject but a concern of many readers about whether the general market should be “risk on” right now, here are two general (traditional) measures of value of the S & P 500:

Price/Book Ratio (in order of the highest, historically):

1) Nov. ’99 = 5.05

2) Dec. ’21 = 4.73

3) Today = 4.45

Shiller’s P/E Ratio (highest three since 1890s)

1) Nov. ’99 = 40.4

2) Oct. ’21 = 38.6 (consider that earnings collapsed during the Covid lockdown pushing up the ratio)

3) Today = 32

4) July ’29 = 31.5

I think we can expect a sharp rise in the BTFP before the facility expire. Mainly due the reason existing loans can be refinanced for another year, and new applications for loans will be accepted until March 11th. The third and final reason is as you mentioned, the arbitrage option.

I hope Arbitrage is the reason. If it is not, watch for the reason.

Banks can use the Discount Window ANY time if they need cash (red line in the first chart). Once they can no longer borrow at the BTFP, banks presumably would shift their dire needs to the Discount Window. And so we’ll see.

The discount rate was made a penalty rate on Jan 9, 2003. Contrary to Bagehot’s’ dictum (and that Fed credit should not be used for profit), the BTFP became an exception.

So it sounds like all the treasuries they still have which are underwater they put up as collateral, and borrow at 4.85%. not priced at the yield in which they bought the bonds or the price of the original principle of the bonds when bought. Still seems desperate or just treading water with no real solution.

I’m not sure I follow this. There may be a misunderstanding. Posting collateral is like when you borrow money to buy a house and you post the house as collateral (=mortgage). You still own the house and get the benefits of the house. So banks continue to get the coupon interest on their Treasuries that they post as collateral, but now they have the cash they borrowed, and they can leave that in the reserves account at the Fed and earn 5.4% on it. What’s not to like? It’s just a smart move that takes advantage of the new spread between the overnight one-year swap rate and the interest on reserves. Nothing to do with desperation.

I don’t want to put words in John’s mouth, but I read it to mean that BTFP allows for banks to borrow against treasuries at par, not market value.

So 30 year bonds purchased at 2% with a face value of $10 million might only be worth $6 million today (or whatever it is). Ultimately, the banks have to pay back the loans, but it doesn’t change the fact that they have lost money on these bonds if they had to sell them today.

I will maintain that things will start getting interesting when the balance sheet gets below 7 trillion. A collateral crunch with much of the underlying collateral depreciating…

CONgress better get to work balancing that budget….

LMFAO!!!!

“Higher for longer”?!? Since when is 5% “higher”…?

Good work Wolf!

@WB: “Higher for longer”?!? Since when is 5% “higher”

Exactly. I don’t think the entire parade of recent Fed Chairs including Powell, Yellen, Bernanke, and Greenspan can answer this very legitimate question.

It’s a LOT higher than 0.25%

But Wolf, if 0.25% is extreme interest rate repression (as you yourself have said many times in the past), what is the “normal rate” that the Fed should not go below – 5%, 4.5%, 4%…?

3% seems to be too low with targeted inflation at 2%. Shouldn’t people expect a sensible return on their savings? Why can’t the Fed deliver that instead of forcing people to move their money into the stock or bond markets or other assets incurring higher risks?

The risk-free short-term highly-liquid rates should normally be a little above the rate of inflation, maybe 50 basis points above the rate of inflation. Inflation is not a steady thing, so that complicates this stuff. But if CPI inflation is 3%, then the risk-free highly-liquid short-term rates should be about 3.5%. If CPI inflation is 5%, then 5.5% would be appropriate. That kind of thing.

The purpose of interest is to compensate investors for credit risk, duration risk, inflation, and inconvenience/liquidity issues.

LOL, yes, yes…

While true, the cost of capital/money is probably one of the most important costs in a functioning market, hence true price discovery is key. Something that the Fed has utterly destroyed.

As you have mentioned multiple times, and as Greenspan pointed out a LONG time ago, the Fed can ensure that the Treasury always pays it’s bills. However, it cannot guarantee the purchasing power of the currency/money it issues…

Eventually, the producers realize they are being screwed and demand something real in return for the products of their labor. Full Faith and Credit… Hopefully we do slide into a hyperinflationary depression, which many see as the worst-case scenario. Being that it is in fact a global market, and central banks around the world have been monetizing their debt as well, it is possible that it would be a global event. In reality it is more likely that world war would start in earnest before that actually happened. History may not repeat, but it sure a heck rhymes.

The Fed has NO credibility, period. It’s actually much much worse too, unless you actually believe that inflation will remain under 5% for THIRTY years (last 30 year bond auctioned at 4.75%)…

There is still a lot of liquidity looking for something to do. I have hypothesized that bitcoin was always design to be a pressure release valve…

>unless you actually believe that inflation will remain under 5% for THIRTY years (last 30 year bond auctioned at 4.75%)…

You only need to believe that inflation will AVERAGE under 5%. Remember that in 15 years, the millenials (largest generation in US history) will be in their peak earning years; and the boomers will have mostly shuffled off leaving the much-smaller Generation X as old-age dependents. If this current baby bust persists there will also be very few child-dependents, which will be economically great (until it isn’t).

Also remember that if you’re frustrated by the state of US politics, it’s extremely likely that both major party candidates (and like half the Senate) will have died in the same time-frame, so we’ll have a fresh start there with people who maybe understand that we’re not in ZIRP-land anymore and the budget needs to be balanced.

So tons of reasons for optimism on a 30-year timeline. I’m also annoyed by the yield on the 30-year because it’d be cool to lock in some fixed income at 6%+, but I’m not gonna bet against the market on this one.

“Remember that in 15 years, the millennials (largest generation in US history) will be in their peak earning years”

Just to quibble with that time line a little bit:

The older Millennials (now in their early 40s) are already in their peak earning years. In 15 years they’ll be in their mid-late 50s and they’ll worry about age discrimination and about retirement.

In 15 years, the younger Millennials, now in their late 20s will be in their mid-40s, in the mid-to-late peak earning years, depending on the job.

Andrew, it is mathematically highly unlikely that the price increases on essentials will average less than 5% for 30 years. The physics/thermodynamics of life are what they are. In order to keep inflation under 5% without a significant decrease in the average standard of living or a significant decrease in the human population, we need a significant innovation in how we obtain energy (i.e. fusion reactors coming online). Even then, the input resources may still be a problem.

Why doesn’t the Fed simply announce accelerated expirations of these facilities like BTFP, which no more applications after the (unanticipated) announcements allowed. They have already declared a policy victory, so why leave it going? It’s just free arbitrage.

It seems to me to inspire some confidence to just do what you say you are going to do.

Because the Fed seems to always refuse to make changes that tighten conditions, even if the status quoa is harmful.

When it comes to tightening, even the hawks at the Fed walk carefully, and the doves tiptoe on eggshells. But of course, when the time comes to loosen, they all strap on their stomping boots.

The Fed put out a term sheet on March 12, 2023, that set forth the terms of this facility, including its expiration date. So the Fed would surely not violate the terms of its own term sheet by accelerating the expiration date.

Wolf,

As you point out in the article, it seems clear the larger banks are not participating in this arbitrage opportunity but by what mechanism are they “not allowed”? Can the Fed simply ask nicely for them to ignore the juicy term sheet provided?

What will ‘crash’?

MW: Hewlett Packard Enterprises to buy Juniper Networks in $14 billion deal

There is no crash coming.

What is happening for last 2 decades and would keep on happening is: devaluation of dollar, monetization of debts of all kind by cheaper money and lower quality of life for working people.

If the fed shuts that there tool box of theirs, I’m trying to figure out who makes good on all those cmbs and cdo’s that haven’t seen a payment in many tranches for ever? Prey tell.

This responsible decision out of the Fed is reassuring. If only the government could make similar good decisions, the USA could get back to something other than a dumpster fire.

Bank Term Funding Program (BTFP). I thought you meant BUY THE F***ing Dip. WOLF did you have that in Mind when you created the title? Or is it just a coincidence? lol

I thought this was a “Buy the Fcking Pivot” article…LOL

All the “BTF” mottos really should be “BTFL” with “L” being liquidity, global fed injected liquidity to be exact.

Global economic cycles mutated into liquidity cycles with he advent of QE. Japan started the game, and the USA is simply late but quickly passing everyone else as I seen today that 2024 deficit to GDP percentage for the USA is twice that of any other first world country. USA burn rate is astonishing to say the least, good luck getting back to ZIRP running such insane deficits and weaponizing central bank holdings so half the world won’t buy much more due to the risks involved. A lot of feel good policy without any understanding of logical unintended consequences. Politicians life in Barbie land…LOL

“Economic cycles mutated into liquidity cycles with the Advent of QE.”

Great way to describe what we’ve seen. You could also say market discipline has been overrun by moral hazards. Price discovery has been replaced by modern monetary theory. Taxes have been replaced by inflation.

It’s a clearly a bad road the Fed is driving down. When will they turn around? They never should have gone off map with QE.

The math is pretty clear that they can never “turn around”. Wolf has covered that.

Regardless, you are correct, and I hear eCONomists argue that inflation will take care of itself because people will simple stop purchasing whatever it is that has inflated in price. Unfortunately that doesn’t work with essentials like food, energy, and housing. Eventually the people that produce these real essentials will demand that they are paid with something other than the “fiat du jour”…

This has happened over and over throughout history, usually leads to war.

My point is that it is our own responsibility to be prepared for such things, so getting good information on what’s really happening is key.

Yes, that’s basically what it’s become now with this fake liquidity-directed economy. I don’t see them turning around…it will go until it can’t anymore and people stop participating.

ZR..not BTFP = “Buy the F***ing Dip” but..

“Buy the F****ing PUT”

that = BTFP

not BTPD!

lol

I wonder if this arbritage artificially increased demand for some treasuries by smaller entities? Although since btfp is still relatively small it might not have been enough to drastically alter yields. I also wonder if big banks knew but could not participate have they been holding back treasury purchases a bit until the program ends?

Wolf, can a bank re-post the same collateral from March ’23 to effectively get two years of BTFP loan against the same collateral? Or would different collateral need to be posted to get another year?

The question is not right? If you post your house as collateral for a 1-year mortgage, and a year later, you renew the mortgage, you obviously post the same house as collateral for the renewed mortgage for another year.

Wolf, to maybe clarify, do the terms of the BTFP allow me to renew at the 1 year mark? In other words, after 1 year could I renew with the BTFP or is bank out of luck. In essence, wondering if we don’t see a sharp drop in the BTFP balance until March ’25 vs March ’24.

The loans can be paid back at any time. And then the bank can take out another loans until March 11. After that no more new loans. This also means we have no idea about the maturity of the existing loans in the balance. They could all be refinanced on March 10, though I doubt it.

But on March 11, 2025, the last ones should be paid off and the balance should go to zero, that’s my understanding of the scant things he said about it.

Does this mean that in March the Fed will pull $140B of cash out of the economy and replace that cash with low value, over valued assets? This is in addition to the $75-90B they are taking out with QT?

My guess is that the Fed thought BTFP would wind down for a gradual absorbing of low value, over valued assets. My guess is that the Fed was wrong. My guess is it won’t be as smooth as they envisioned it.

It means that over the 12 months following March 11, 2024, the BTFP balance will go to zero. This means that banks pay off these loans with cash. If the BTFP contains $140 billion on March 11, the banks will pay $140 billion in cash to the Fed over those 12 months, and the Fed will destroy that money as a matter of routine. So that $140 billion in liquidity will come out of the banks.

Throughout, the banks keep their collateral, overvalued or not, doesn’t matter. After the banks pay off their BTFP loans they’re free to do with their collateral whatever they want.

“So banks could borrow at around 4.85% from the Fed, and then leave the cash in their reserve accounts at the Fed to earn 5.4% on it, for a nice risk-free spread. ”

Isnt there a “as needed” basis for dipping into the BTFP?

For example, to deal with REQUIRED reserves vs EXCESS reserves?

To just take money from the BTPF and load up a bank’s excess reserves to scalp the arbitrage seems like gifting to the banks.

And to consider collateral at cost vs market value is to create a false reality, IMO. Who else get this deal.

1. There are no more “required reserves” — the reserve requirement was reduced to 0% in March 2020. And so there are no more “excess reserves” either. There are now ONLY “reserves.” And the Fed pays banks 5.4% on their reserves.

2. There was no such “need” limit for the BTFP. Banks were encouraged to use it. This new arbitrage seems to have pissed off the Fed — bankers gaming the Fed’s bailout system. The Fed came up with the BTFP in like no time to calm the banking crisis, and they didn’t think about what would happen if longer-term yields began to drop before the Fed cuts its policy rates.

“The Fed came up with the BTFP in like no time to calm the banking crisis, and they didn’t think about what would happen if longer-term yields began to drop before the Fed cuts its policy rates.”

That’s frightening. Has the feel of desperate adolescents, after their buddies leave the party, trying to clean the beer and chips out of the living room carpet before the parents get home. (Never ended well for me…)

A bad look for policy makers at the Eccles Building.

They did this over the weekend. SVB collapsed on Friday, March 10, and was shut down that morning by state regulators and handed to the FDIC as receiver. A relatively small number of high-level people at the Fed, the FDIC, and the Treasury hashed out these multiple programs from Friday morning through Sunday morning, and on Sunday, March 12, announced them jointly.

I gave them lots of credit for not bailing out investors in those banks. Bailing out uninsured depositors was unnecessary in my opinion; 30% haircuts for uninsured depositors, as had been expected, would have been OK, and would have shown that the system works, and would not have led to contagion, but they were really spooked. Runs on banks are scary when they happen this fast.

The bank BTFD facility has been around for almost a year now. How many banks have gone out to raise equity or market-based debt to replace the BTFD and/or secure additional funds for prudent risk management?

Instead, I already hear calls for the Fed to reduce interest rates sooner to alleviate bank “liquidity issues.” Are banks again trying to avoid market discipline via Fed Reserve liquidity support and continued intervention? Why should the public be forced to pay for lifetime boarding of lame banking horses?

Bank CEOs should be trained to manage, not to cry for help.

“How many banks have gone out to raise equity or market-based debt to replace the BTFD and/or secure additional funds for prudent risk management?”

Quite a few banks have raised capital in 2023 by issuing preferred stock. This includes Wells Fargo, which raised $1.7 billion that way. And more are planning to do so in 2024.

Thanks for the info, but Wells Fargo’s dividends and buybacks were over $11B last year. I’d classify a $1.7B preferred capital raise as a token move, relatively speaking. I’d like to see banks be much more reliant on markets and less reliant on taxpayer bailouts, if it’s not too late already.

Bobber,

After-tax net income in 2022 was $13 billion, and in 2021, it was $21 billion. over the past five years, WFC made nearly $80 billion in after-tax net income. Those big banks are hugely profitable.

But raising capital via preferred stock is a good thing: preferred stock gets bailed in right after common stock, and we have seen that principle with SVB: equity and preferred equity got bailed in and lost everything. That reduced the cost to the FDIC. So banks are under pressure to increase their issuance of preferred debt as a cushion, and they’re doing it.

MW: Federal Reserve’s Williams says interest rates need to stay high ‘for some time’

This perhaps is the equivalent of injecting goo into your flat tire so that you can safely drive home.