Contributions jumped 11.8% (more people working, big pay increases). Outgo jumped 12.0% (more people at retirement age and the 8.7% COLA).

By Wolf Richter for WOLF STREET.

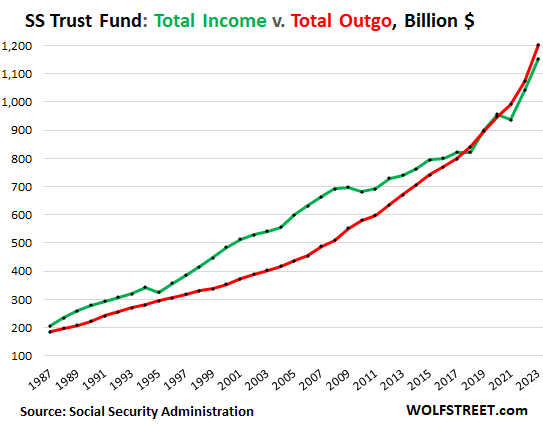

Total income from all sources jumped by $111 billion from the prior year, or by 10.7%, to a record $1.15 trillion in the US government fiscal year ended September 30, according to the Social Security Administration (SSA) today (green line in the chart below). By category of income:

- Contributions jumped by $110 billion, or by 11.8%, to $1.04 trillion due to employment growth and big pay increases in 2022 and 2023.

- Interest income from the securities in the Trust Fund dipped by $2 billion to $63 billion.

- Taxation of benefits rose by $3 billion to $50 billion.

Total outgo rose by $129 billion, or by 12.0%, to a record $1.20 trillion (red line), on the 8.7% Cost of Living Adjustment, the biggest since 1981, and more people at retirement age and drawing Social Security benefits. Benefits paid accounted for 99.2% of the outgo; the remaining 0.8% were made up of transfers to Railroad Retirement programs ($5.6 billion) and administrative costs ($4.3 billion).

When the green line (total income) was above the red line (total outgo), the Trust Fund accumulated assets. When the green line fell below the red line, the Trust Fund shrank.

The gap between income and outgo was $50 billion, up from a deficit of $32 billion in 2022, but down from the $55 billion deficit in 2021, after surpluses in 2020 and 2019.

The first deficit in the data going back to 1987 occurred in 2018 ($19 billion). Until then, the annual surpluses had produced the $2.8 trillion in the Trust Fund at the time.

The low 3.2% COLA for next year will slow the growth of the outgo. With the release of the CPI data two weeks ago, the CPI-W was also released. It’s the measure that the COLA calculations are based on, and they were pretty thin: In 2024, the COLA of 3.2% will be bad for retirees, but it will slow the deficit, or may even produce a surplus if employment and pay continue to grow at the current pace.

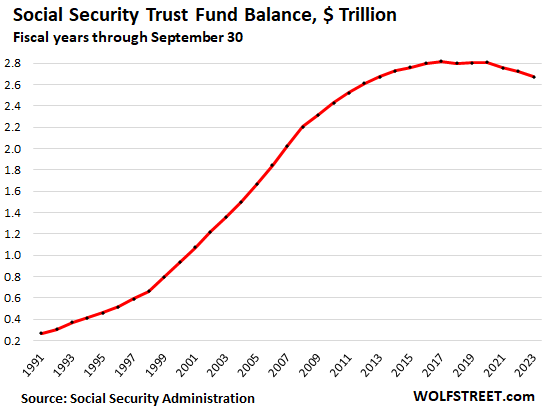

The Social Security Trust Fund.

Technically known as “Old-Age and Survivors Insurance (OASI) Trust Fund,” it declined by $50 billion, or by 1.8%, during the fiscal year, to $2.67 trillion, according to SSA data.

These figures to not include the Disability Insurance Trust Fund, which by law is a separate entity from the OASI Trust Fund, and is not part of this discussion here.

How the Trust Fund invests the $2.67 trillion.

The OASI Trust Fund invests in interest-bearing Treasury securities and short-term cash management securities. These securities are not traded in the secondary market, similar to the popular I-bonds that many people, including a number of WOLF STREET commenters here, are holding at TreasuryDirect.

It’s a good thing that the securities in the Trust Fund are not subject to the whims and occasional chaos of the secondary market: The value of these holdings – similar to the value of our accounts at TreasuryDirect – doesn’t fluctuate with the prices in the secondary market. The Trust Fund holds Treasury securities until they mature and then gets paid face value for them. Day-to-day price fluctuations are irrelevant for the Trust Fund.

At the end of the fiscal year, the Trust Fund held $2.47 trillion in interest-bearing special-issue Treasury securities and $202 billion in short-term cash-management securities (“certificates of indebtedness”).

Investing in Treasury securities when they’re issued and holding them until they mature is a low-risk conservative strategy that essentially eliminates credit risk.

This strategy allows the SSA to operate the system with ultra-low administrative expenses, amounting to just 0.16% of the assets under management.

The Fed’s interest rate repression created the deficit.

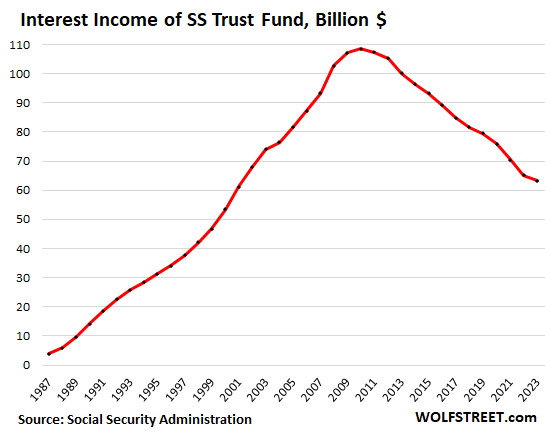

The Trust Fund earned $63 billion in interest on its Treasury holdings in the fiscal year, down by 42% from the peak in 2010, the year of peak interest, though the Trust Fund balance was smaller in 2010 than today.

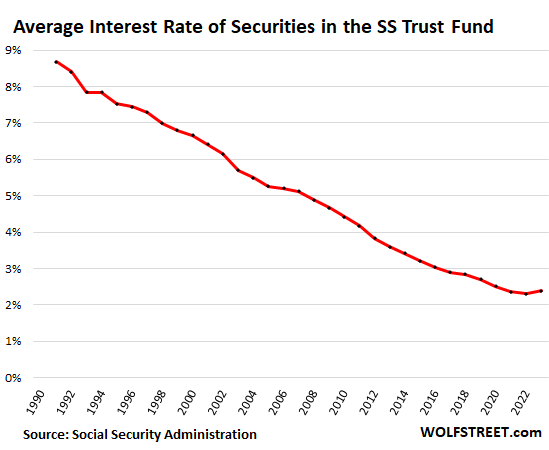

The average weighted interest rate that the Trust Fund earned ticked up to 2.4% this fiscal year, from 2.3% last year, as higher yielding securities began replacing some lower yielding securities in the Fund – but it’s still just a minuscule improvement.

As a result of the Fed’s interest rate repression starting in 2007, the interest rate that the Trust Fund earned was cut by more than half, from 5.1% in 2007, to 2.4% this year.

Because the Fund invests in long-term securities and because interest rates of securities don’t change until the securities mature and are replaced with new securities, there is a lag before changes in long-term yields filter into the “average interest rate” and into the interest-income stream.

The average number of years to maturity used to be around 7 to 7.5 years. But in 2020 it began to drop, and in the fiscal year through September, it declined to 5.67 years, the shortest on record. In other words, the current crop of higher-yielding securities is going to make their way into the Fund a little more quickly.

Today’s interest rates would eliminate the deficit.

If the Trust Fund had earned an average 5% on its balance of $2.67 trillion this year, it would have earned $133 billion in interest income, instead of $63 billion, and the Fund would have had a surplus of $20 billion!

Obviously, what the Trust Fund experienced – that the Fed wrecked its cash flow via interest rate repression between 2007 and 2022 – is precisely what all yield investors, including retirees, experienced on their fixed-income investments.

If longer-term Treasury yields normalize in the 4% to 8% range, as was the case between 1990 and 2007 (they were even higher in the prior 20 years), the Fund’s income and outgo would be back in balance. But it would take a few years before the low-yielding securities would be replaced by higher yielding securities.

Relatively small adjustments would eliminate the deficit.

The current gap is not large – $50 billion this year, or 4% of total income, despite the huge 8.7% COLA. The Trust Fund still has $2.67 trillion in accumulated surplus. It’s going to take many years before the fund runs out of money. At that out-of-money point, if no other adjustments are made, benefits would need to be cut by some percentage to match income, or Congress decides to fund the annual deficits then as part of its budget.

In addition to higher interest rates, a combination of relatively small adjustments to the plan would bring it back into balance for decades to come.

Several proposals have been floated in Congress over the years. And forbidding the Fed to engage in QE (repression of long-term interest rates) should be part of the solution, and would do some heavy lifting.

It’ll be there, but it won’t be enough.

Social Security was never intended to be the sole source of income in retirement. It was designed as a base layer of income to keep people out of abject poverty or worse when they can no longer work. Social Security will be there when people retire, the spousal benefits will be there, and the survivor benefits will be there. But they won’t be enough.

And the COLAs over the years will not be enough either to fully make up for the loss of the purchasing power of the retiree’s dollar.

Social Security was designed to be supplemented by other sources of income, such as from assets or savings that people put aside during their working lives.

In addition, working for as long as possible, even part-time, is hugely beneficial in all aspects. Our politicians have figured that out too. They’re working well past their full Social Security retirement age – some of them decades past their full retirement age – and they’re obviously having a blast doing it.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Reality will hit soon. Even though the COLAs are only to pretend to keep up with real inflation, for most Americans, the math will hurt. For example, if average home mortgages now charge 8% a year in interest, then only people who earn about $175,000 year, before taxes, etc., can buy the average home at $430,000 and pay normal living expenses, family gifts, trips, etc. There are lots of baby boomers hanging on to their main asset in life: their overpriced home.

Panic will set in as demand from fewer and fewer buyers causes house prices to crash, as more wealthier baby boomers retire each year, except at the high end of the market of mansions for those who do not really pay income taxes due to loopholes: e.g., the loopholes that SBF used to pay for a millionare lifestyle from his company are commonly used.

Yep. More people will become renters. I am also seeing more multigenerational families buying homes. This is a the current trend to afford a home.

Home ownership is still historically high at 65%. Prior to WW2 home ownership was at 49%. Who knows, maybe it will drop. Maybe more people will become renters.

We all rent. Even if you think you own your house debt free, you are renting it from the State in the form of property taxes.

“You will own nothing…” is closer to reality than you might think.

By that measure, you even just rent the beer you drink.

Another one of those “taxes are not in the Constitution fans?”

Boy do the Corps/old money dynasties love you!

Compared to them you have LESS than NOTHING at all, but you are talking their book. Another well spun savior hunter.

But at least you are a rugged individual and not a damn woke snowflake sissy commie like me. I doubt if I could even face you.

Now that the interest is starting to turn upward, the balance should do the same.

It’s good to hear that the Trust Fund knows the difference between a bond and a stock, and only buys bonds. (Contracts intended to be held to maturity, not entities to be sold at any time.)

Polistra-

“ It’s good to hear that the Trust Fund knows the difference between a bond and a stock, and only buys bonds. ”

Also good to see that the investment committee wisely shortened the average maturity during the rate suppression era.

The fact that politicians are working longer does not necessarily benefit the SS coffers since most if not all have big fat pensions, inexpensive medical, etc. Good for them, not so great for the rest of us.

McConnell is 81, how long you think he is going to get that fat pension when he retires?

McConnell could care less about money, what he does care about is his legacy. He single handedly is responsible for the most seismic shift in the judicial branch in 100 years.

I don’t think he’s all there at the moment. But still terribly powerful.

Those grifters make far more on the side than their constituents. Look at all the centimillionaires like Nancy Pelosi, raking in dough on their salaries and, uh, ‘other investments’. Putting them on the same footing as the rest of us can’t come soon enough.

Wolf,

Renting beer has been going on for many many years. Back when I was a young Marine in the Philippines we joked about this.

Off topic but still true!

Thanks for bringing old memories back.

The same will happen to cars, crypto-tulips, etc, qs capital tightens when baby boomers continue retiring each year.

Federal politicians work long past their Social Security retirement age for other reasons, including the pension they will receive under the Congressional Retirement System.

One term is enough to qualify for those pensions.

So they collect their salaries, and they get the per diems and other stuff. And they can do insider trading, collect “campaign contributions,” and they’re having a huge amount of fun being in the middle of the power center.

Yes, it’s very funny how the system was setup to benefit specific group.

How will history remember this people?

They will be remembered as corrupt as the Roman Senate was. A tale as old as time.

And how history remembers will bother them not one whit. They will long be dust.

It’s not too different from public employees unions, only congress gets to vote on their own benefits directly.

A huge amount of fun on the people’s wallet. They are corrupt to the core. All these benes need to be eliminated. It’s stealing on top of stealing. Truly a disgrace.

Bingo!!!!!

Related but unrelated. I was always under the impression one side of the aisle supported social security and one side attacked it. I did a bunch of research and much more complex than that, with most administrations trying to mess with it in unhealthy ways. Jacobin has some good articles on the aging population and the challenges it presents across mostly the developed economies of the world.

You stated: Social Security was never intended to be the sole source of income in retirement.

And it certainly isn’t. It barely meets the annual grocery, utility, MediCare Advantage, fuel and property tax needs of retirees.

So it is a pittance, especial for a single elder.

It is politicized as an entitlement, but most of old geezers, like me, have been paying in forever. And they are entitled to a small fraction of their money back.

This was a social contract. Not political. And a contract that should be honored.

So if it takes more funds to live up to the contract that should be done.

Or, screw the old farts and let them die and get off the books.

That is the economics of this decision.

Not very humane or honest.

We were workers who paid into a mandated Federal program.

Or were we your “Drunken Sailors”?

The word “entitlement” was coined for social security, you paid into it, your money was invested in interest bearing securities, so you are “entitled” to get it back. It is unlike welfare, for people or corporations, in that it is not just a transfer from one person to another.

It was designed in the 1930s to make it difficult for the wealthy to get rid of it. Roosevelt knew that the rich hated it because it allowed people to retire before death, which took people out of the labor force and drove up wages (as it is doing now). So they coined the term “entitlement” as a positive statement. Of course the big shareholder class has spent decades trying to repurpose the word entitlement to mean “welfare for the poor”. Which has become a meme in the imaginations of those on the far right.

Interesting. Thanks

I recommend you look carefully at your Social Security statement before complaining. I’m now retired, but not collecting yet. I took a look at my statement, and here’s the real numbers;

Lifetime contributions; approx. $125,000 for each myself and my employer match = $250,000 total paid in over 40 years of work.

Full retirement benefits at 66.5 years (I’m not quite there yet) = approx. $3000/month, or $36000/year.

Your statement that you only get a small fraction of your money back is wrong. In my illustration, I get all the contributions back in 7 years.

Naturally, someone with a lower income, or fewer years of work will be receiving less, but still will receive much more than was put in over the course of a normal length retirement.

So you deposited first dollar 40 years ago, and will get it back 7 years from now? Will they pay compounded interest on it over 47 years? Not an expert here, clearly. Thanks

Kenn was merely pointing out his benefits will likely comprise more than a small fraction of his contributions. If Kenn lives to 76.5 he’ll collect $360K+CPI adjustments. The longer he lives, the more he collects.

They do not pay compounded interest, they pay a lifetime inflation adjusted annuity. I think you know that though. If you didn’t, now you do.

Wasn’t a burger like 25 cents 40 years ago? Or is it apples to oranges?

You’re leaving out inflation.

Benefit payments are adjusted for inflation via COLAs. In 2023, benefit payments were increased by 8.7% from 2022. In 2024, benefits will increase by 3.2%. We don’t know what the future years of COLAs will be, but the payouts will increase each year based on those COLAs. And its cumulative.

Someone who collected $2,000 a month in 2021, given the known COLAs for 2022, 2023, and 2024, plus a guess of 5% COLA for 2025, and 4% COLAs for the remaining 6 years:

In this scenario, your monthly income from SS jumped by 58% in 10 years, from $2,000 to $3,156.

Spousal benefits and survivor benefits increase by the same 58%.

If you collect SS for 20 years, your benefits may double at the end from where they were at the beginning, depending on inflation, and if you add up on your last day of life all the benefits you received over those 20 years, it turns out to be a pretty good deal.

Regular monthly payments to retirees began in 1940, 5 years after the SSA was initiated. The first monthly retirement check was issued to Ida May Fuller of Ludlow, Vermont, for $22.54 in January 1940 and escalating over the years. She lived to be 100, so good score for her with only 5 years of contributions.

Final payment in say, 1975, would have been 157.70. Benefits have risen dramatically over the years concurrent with the election cycle; presently over $1600 a month.

I would challenge the use of the term ‘contributions’ though …

Many history buffs here today. Love it.

Don’t forget to look at your life expectancy chart!!

Instead of social security, what if you could have invested that money?

If we assume 10% average annual return from stock market/mutual fund investing since 1983 (a favorite benchmark of retirement planners), contributing $500 per month over 40 years, the balance could have theoretically grown to $2.6 million.

If the government would let you keep the FICA contributions, and your employer paid you his share in the form of a higher salary, you could have quite the nest egg to leave your grandchildren.

And the government would have a much higher interest payment enforcing stricter fiscal discipline. The world would be a better place.

This is exactly the kind of BS that wipes people out financially just as they get ready to retire. Think about why.

Theoretically it’s a great plan, and all such plans work out to megabucks. Also, I read William Nickerson’s book, and many other similar ones, as a teenager and didn’t do a thing about it.

SS was created because the greatest number of people don’t save in a disciplined way for retirement – there’s always plenty of time to do it later.

Sounds like you took your Social Security payments to early !

Really? I get $2219 a month after paying the Medicare premium and according to you, it barely covers groceries, utilities, property taxes, fuel and Medicare Advantage.

My property taxes are $31 a month. I spend about $20 a week on gas so that’s another $80. My utilities average about $150 a month. My grocery bill is about $750 a month. My Medicare Advantage costs me nothing extra as it just replaces regular Medicare for the same premium.

So all that adds up to a little over $1000 a month. Even throwing in my cell phone bill, internet and homeowners insurance only adds another $148.

Where do you live that your property tax is $31/month? Sounds like Zimbabwe.

Texas recently passed property tax relief that drastically reduced the property taxes for old codgers like myself. I got my annual property tax bill in the mail yesterday for my condo in the nicest neighborhood in San Antonio for $371. That’s about $31 a month. My condo is worth about $160k and valued for tax purposes at $131k. So, no, it’s not Zimbabwe.

That’s fantastic, you keep your fixed bills low 💵👍 You don’t have an HOA? Or car payment?

I don’t have a car payment. I do have an HOA payment of $336 a month but it includes a lot of services like trash pickup, water and hot water.

The low operating cost of 0.16% of AUM caught my eye.

I doubt turning over management to the private sector, as certain legislators have advocated over the years, will be able to beat that.

Hands off the SSA.

For a program this is under attack on a daily basis, it is surprisingly resilient

Thank you Wolf for reporting the facts.

George W wanted to privatize it.

A tad bit later the market crashed.

Let’s be glad they did not privatize it.

That’s only $11 Million per day in admin cost. I think they recount money in that fund manually each day. Trust is not cheap.

Makes me wonder why exactly was Obama demanding that government cut Social Security? This was while the fund had 2 trillion positive balance.

Your question is BS. Obama never demanded any such thing. What Congress did and Obama signed in Dec 2010 and extended through 2012 was a temporary payroll tax cut of 2 percentage points, where workers’ Social Security contributions were reduced from 6.2% of wages to 4.2% of wages, which effectively increased their take-home pay by 2 percentage points. It was a stimulus measure to stimulate consumption. The government then made up this shortfall in contributions to the Social Security Trust Fund with transfers from the General Fund.

It makes wonder why you continue to use sources of information that misinformation you regularly.

Why not use better sources?

what big pay increases?

These big pay increases https://wolfstreet.com/2022/11/02/wages-soar-by-7-7-but-job-hoppers-boost-their-pay-by-15-2-leveraging-this-historically-tight-labor-market/

Real wages are flat due to inflation though last I read.

Herpderp,

Real wages grew strongly in 2023 but declined during the inflation spike in 2021 and 2022.

Ill admit I haven’t checked recently. Thats good news.

working man,

If you didn’t get pay increases, you need to change jobs because you got screwed. Job changers increase their pay by a lot more than job stayers. Sitting lazily on your butt is not helpful in promoting your career.

“Sitting lazily on your butt” is a bit harsh.

“Foolishly staying loyal to an employer who doesn’t value you” is more like it.

Ruh Roh Raggy!

Does everyone realize that on one side of the accounting we are discussing the interest earned by the SS surplus, but just last week everyone was talking about the “net interest” paid on the US debt, which specifically EXCLUDES this interest amount since it is merely “intra-governmental” borrowing. I believe we are correct to count this $63 billion as real money, but that also means bumping up our national debt borrowing costs from $659 to $722 billion, a little closer to the actual cost of $879 billiion reported in the Treasury statements.

Everyone who holds Treasury Securities is costing the government money — interest expense! It doesn’t matter who holds it. The government borrowed $33.6 trillion because of decades of out-of-control deficit spending, put into hyperdrive since March 2020, and now comes the time to pay the piper(s). The government shouldn’t have borrowed that much!!!! Freaking Congress should have been more disciplined over the past 20 years. But each member of Congress has got to “bring home the bacon,” and so here we are. We elected corrupt goofballs to Congress, and that’s what we got.

Lol, corrupt goofballs, that definitively captures it.

I wonder if as the country’s finances have deteriorated less and less sane folks want to tackle this beautiful but listing ship. On the global balance our politicians are still pretty un-corrupt (especially given the $ numbers at play) but the trend isn’t pretty in my lifetime (53). I wonder if the India’s or even say Nigeria’s of the world will fare better politically as their fortunes flourish potentially will young populations (although more to it than that).

The SSI discussion reminds me of the joke about GM being a large pension fund with a car company attached. Not so different than the Feds these days. As we watch Fain & Co (UAW speaking of formerly corrupt!) slugging it out with the big 3, it’s amazing to think how profitable say GM was for decades to conceive of, promise, and deliver these rich benefits. I’m sure they have a few beneficiaries on the rolls for 50+ years. I’m also sure BYD doesn’t offer this to their workforce. Ergo what percentage of the modern global population has ever known benefit like SSI? It has to be tiny.

Deficits of $50-100B for SSI as a percentage of revs actually seem pretty manageable compared to the overall Federal budget which blows my hair back. Even if you raised taxes personal/corporate receipts by 50% (the

horror)!and whacked defense spending considerably unless the soon to be $1T net interest payments are suppressed by – you guessed it – QE not sure what the future holds?

Two comments;

First, it looks like the “total income” (first chart green line) declined in 1993, 2008, 2017, 2021, with gaps of 14 years, 11 years, and 4 years. I’m not a statistician, but this rising frequency seems concerning….

Second, how does the 90 year trend of ever longer life expectancies (at least pre-covid) effect the longevity of the trust fund. At its inception, I believe that the average life expectancy in US was 65 years old and the main intent was to provide a base income to those who lived beyond this life expectancy, AND the average household contributed to the trust fund through payroll taxes until just a few years before life expectancy. The ratio of years paying-in to years taking-out has decreased dramatically. (This was discussed admirably in “Social Insecurity” by former SS Commissioner Dorcas Hardy. It’s short, readable, slightly alarmist, and still available online.)

Meant to mention that the Dorcas Hardy book was written in mid 1990’s…

Spellcheck or fat finger error: “effect”

I believe life expectancy is trending downward now and baby boomer

bubble is being processed as we speak.

The real issue is the rate suppression that

the Fed imposed on the trust fund. One wonders if it was by design.

That life expectancy of 65 was from birth. Most of the gains have been from the reduction in child mortality.

If you look at the historical data on the social security website, in 1940, a 65 year old female had life expectancy of 13.4 years to age 78.4. Males had 11.9 years to age 76.9.

And even back in the 1700’s, Ben Franklin managed to live to the ripe old age of 85.

Ben Franklin?

Sì. Era un vecchio gatto intelligente. Ti sono piaciute le signore francesi, no? Grande uomo. Grazie Ben.

Viva la libertà!

Warren G. Harding-

Seems about right.

From Hardy book: “Of those who lived to 65, the increase in longevity was equally startling. A man who turned 65 in 1935 could expect to live another 11.9 years: a woman who turned 65 in the same year could expect to live another 13.2 years. By 1990, life expectancy at age 65 had jumped to 16 years for men, and 19.2% years for women.” (p.33)

The scope of SS “retirement” benefits has expanded in similar fashion over the succeeding decades. These retiree benefits are payed for directly by mandatory worker contributions of working stiffs, and indirectly by consumers who pay higher prices for domestic goods due to mandatory employer contributions.

The Center for Medicare and Medicaid Innovation was created by ACA in 2010 in HHS/CMS and funded by the SS trust fund, not the federal budget. I wonder how many other operations are also funded this way.

I have trouble nailing down who is funding the Center for Medicare and Medicaid Innovation. Can you cite a source for your claim that the Trust Fund is funding it?

I couldn’t find what funded it but not a significant amount, 10 billion a decade, however in the 2nd decade due to implementation it should save 34 billion.

From kfd.org

Kff.org!

Thanks.

I find it interesting with so many reported elderly people dying from Covid in 2020-21, that SS outlays didn’t decrease at least a little in the chart. Things that make you say hmmmm.

Not rocket science. Far more boomers are retiring (adding to SS outlays) than are dying.

Scott,

Stick your ZH BS where the sun doesn’t shine. RTGDFA. What does it say about COLAs and about a flood of boomers reaching SS retirement age? Adios.

I’d say that SS provides more than a base security for higher income folk. For example, married couples who’ve contributed up to the SS limit each year will get close to about $80k per year in current year dollars, which approximates median family income. Even so, it represents a poor return on their contributions.

SS demands a lot from high wage earners, who are subsidizing the lower income group.

That said, I’m glad we have a forced savings program. Given how many people spend beyond their means in the US, it’s clear many lower income people would not otherwise save anything for retirement and they’d be needing larger handouts when the tap runs dry.

All in all, I’d say SS represents a good compromise that recognizes the reality of poor cultural saving habits.

“All in all, I’d say SS represents a good compromise that recognizes the reality of poor cultural saving habits.”

I agree with you, it’s one of the best Government programs we have. It also benefits those with good savings habits because it functions, from the beneficiary perspective, like an annuity when markets are experiences losses. It also doesn’t have the lack of diversification risks of an annuity.

Better start building your mother-in-law ADU now. lol

I guess Peter forgot that the government collects taxes.

Alton Magson,

Peter Schiff is a lying moron. He’s lying because he is trying to scare people into buying gold from him so that he can get rich off of them. People who believe his shit are morons. He is the scum of the earth. He is Exhibit A of what’s wrong with the internet. People who abuse my site to spread his shit get blacklisted.

Wolf, are you ready for the stock market meltdown?

It has been melting down since late 2021. Just more or less slowly, haltingly, and very unevenly, interrupted by head fakes. This could go on for years like this. Until everyone gets tired of it and stops talking about it, and CNBC has to lay off a bunch of its anchors because viewers vanished because they got busy with life. That might be the bottom.

CNBC layoffs- the newest and most accurate recession indicator…I like it!

By that time you will be hiring into Wolf Media empire. Maybe get Melissa. And Joe Kernen. He always makes those insightful observations.

I should have said “are you ready for stock indexes meltdown”.

Wolf,

I know the Treasuries are supposed to be held to maturity, but at some point won’t the payouts so far exceed income, that in order to keep making full payments, the Trust will have to liquidate Treasuries before the maturity date? (This, of course, assumes Congress doesn’t do anything to modify the program to prevent the Trust fund from running out.)

No. Retirement age of the population is known. There are no surprises. With the average number of years to maturity below six years, and with $2.67 trillion in the fund, securities are maturing every month. If the Trust Fund needs a little extra cash, it can just not re-invest the cash from an issue of maturing securities.

In addition, I have some “nonmarketable” Treasury securities as have a lot of people here, namely I-bonds, and they can be redeemed by selling them back to the government at face value. So you never ever lose money on your I-bonds.

Same applies to the special issue nonmarketable Treasury securities in the Trust Fund: if somehow the Fund needs the cash more quickly than anticipated, it can redeem the securities by selling them back to the government at face value.

Wolf – what duration of securities is the SS fund purchasing? Do you have the breakdown as with the duration of treasuries that the gov sells to fund itself (mainly T-bills, if I’m not mistaken)?

I just looked up purchases in 2023. Many of them were short-term bills (“Special Issue Certificates”) maturing in 2023 and 2024. Others were Special Issue Bonds maturing over the next few years, 2031 being longest-dated one purchased (8 years). So this is now heavily weighted to the short end.

For the list, go to this link:

https://www.ssa.gov/cgi-bin/transactions.cgi

Choose #2 “Detailed monthly transactions…”

Choose OASI

Change year to 2023

and click Go

“Social security is broke, it will never be there for us by the time we retire. The sky is falling!”

Wolf is such a downer. Please stop ruining our pity parties with facts!

Howdy Folks. The Lone Wolf quote

Investing in Treasury securities when they’re issued and holding them until they mature is a low-risk conservative strategy that essentially eliminates credit risk.

The above is a bible verse in the life of a squirrel. ZIRP is dead and never should have been born. Squirrels feel the same about QE too…..

In the end, only pay as you go pension and social security will work as can be expected. Those working pay the pesnion and social security for those not working. Yes, the burden and the pay out have to match, but that is no worse than any kind of “saving” type of system.

Demographic shift may hit real assets that can be sold, corporate bonds, equities, real estate or gold as bad as a pay as you go system. You may look at these “savings” as pay as you go too. Those buying in now pay for those that now withdraw. Only the means of the transaction differ.

I think the demographic shifts you are talking about are slow enough they can be planned for and the trust fund just allows the bonds mature without renewing. If the trust fund begins running an unmanageable deficit, they just raise taxes or reduce benefits to compensate. As long as there are sufficient tax payers, they can pay the bills.

It may become an issue for the general fund if the SS trust fund stops purchasing bonds and the yield on government debt goes up to attract new buyers.

From the SSA site:

There has been a temptation throughout the program’s history for some people to suppose that their FICA payroll taxes entitle them to a benefit in a legal, contractual sense… This is the issue finally settled by Flemming v. Nestor.

…In its ruling, the Court rejected this argument and established the principle that entitlement to Social Security benefits is not contractual right.

So what? Did anyone here say it was a “contractual right?” Do you even know what a “contractual right” is? This is completely irrelevant and doesn’t make one iota of difference.

The Chief and one of his guests were talking about this in the first half hour of todays Stocks & Jocks show.

Excellent data and explanation, Wolf.

Wolf, others:

Ok so the simple calculation 2670 / 50

yields 53.4 years. SS should be solvent for 53 years with $2.67T in the SS trust fund and running an annual deficit of $50B.

Wolf says the 50B annual deficit will probably decrease… in the short term anyhow. If true and if that continues indefinitely then SS could be good for much longer than 53 years.

So the obvious question that I didn’t see anyone ask: Why do the politicians and media claim SS will become insolvent in something like

10 years ?

What are they not taking into account ? Alternatively what factors are they taking into account that Wolf is not considering ?

After all their math can’t be that bad….

If interest rates stay at around 5% for years to come, interest income to the fund will increase substantially, making up part of the shortfall from contributions, until there’s a recession with a big decline in employment, when contributions drop. And we’re going to get a recession someday, for sure, we always do sooner or later.

At the same time, the COLAs have gotten a lot bigger, and will stay bigger if inflation stays higher, so that increases the outgo, but by less than the interest income would increase.

The claims of “insolvency” by x date (that date has been moved out quite a bit) were based on near-0% Fed policy rates and low long-term yields forever. I don’t think the actuaries that work on these predictions over the past 10 years expected that we’d see 5% Treasury yields ever again. This is a massive change — especially if Treasury yields stay higher, and thereby revert to historically normal levels.

I agree that Congress needs to make some tweaks to the system to make it super-healthy for decades, so that it can weather recessions and declines in interest rates, to where the Trust Fund is growing again. That just makes sense. Brinkmanship with a retirement system is never good.

Removing the income cap on FICA taxes would go a long way to shoring up SS.

If the cap is raised faster than it currently is being raised, then they would also need to raise benefits in step, otherwise it would just be another tax increase on the upper middle class and that would do little to fix the wealth disparity, because the closer you get to the top, the less likely that their “income” is being generated by earned income, which is the only type that is subject to OASDI tax.

SS Solvency-

You could look at CBO view from year end 2022 by searching [ 2022 long-term projections for social security ]. They use a revenue/outlay analysis, revenue being the payroll taxes, and both revenues and outlay’s expressed as percent of GDP.

They conclude that give their assumptions of the ongoing gap, that the fund will be exhausted in 2033, and that the solution at that time will be to cut benefits or to increase payroll taxes by about 4% of then payroll.

Interestingly, you can drill down into the assumptions and find this chart on projected annual interest rate earned on the fund. One could argue that they are too low, especially on the short end, as Wolf pointed out.

https://www.cbo.gov/system/files/2022-12/58564-Additional-Info.xlsx

Wolf, John H.

Thank you for the timely responses.

I’ll have a look at your CBO link (not knowing what CBO stands for, but soon will).

Unfortunately, these bring late posts to Wolf’s article, few if any will see your responses.

All I read is stuff that has mellowed and commenters have thought about for a few days. I learn more that way. There are others like me, not to mention the non-commenters. They can wait months! Sometimes I read the top article, and see who “Won” the first comment contest.

Senile wealthy old babies. Too late to tell you to get a life, you all pissed it away long ago for……the first comment? Oh, and all your “stuff”, too.

Planet killers!

By all means look up CBO and re-read/scan the article and comments. This isn’t MSM…one shot stuff over and over.

Learning is fun!

NBay – my day is always better for seeing your handle…(taking some familial casualties at present).

may we all find a better day.

Sorry to hear that.

(just keep below the dike as best you can till the tracks show up)

Needless to say you are also appreciated…..it is hard to live in a world that has made so many unnecessary wrong turns, and be among people who just can’t wait to make another.

Best I can find to do is look for situational awareness……your “recon in the smoke” analogy.

Smoke just seems to be getting thicker, too, metaphorical and real.

NBay – thanks. (timely sitrep reminder, especially).

“…and I heard that the angel of mercy was gonna give us all break real soon, i just hope i can hang on ’til she do…”

– ‘Fair Play’, mike brewer (Brewer and Shipley).

Best, and-

may we all find a better day.