The Fed has shed 31% of the Treasury securities it had added during pandemic QE.

By Wolf Richter for WOLF STREET.

The Fed’s Quantitative Tightening (QT) hums along on autopilot. But the banks have figured out since one-year yields began to drop last November that they can earn risk-free interest income by borrowing from the Fed at the lower rate of the bank bailout facility, the BTFP, of around 4.85%, and then deposit that cash back at the Fed as reserves and earn 5.4%, risk free, hassle-free, thank you.

That cash stays at the Fed, it doesn’t go anywhere, it just makes the banks some risk-free moolah. And use of that trick has jumped, obviously. That facility is set to expire in March, so they’re trying to get in while they still can. And we’ll get to that in a moment.

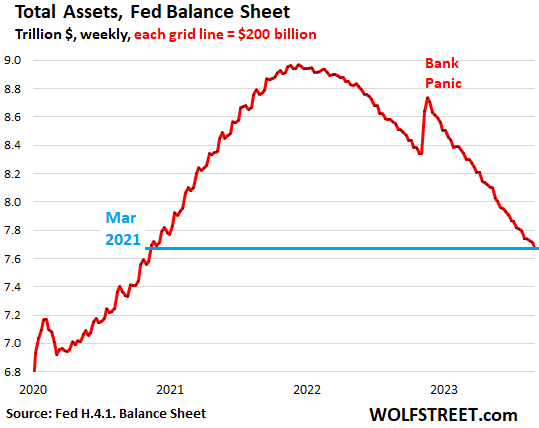

Total assets on the Fed’s balance sheet dropped by $56 billion in December, to $7.68 trillion, the lowest since March 2021, according to the Fed’s weekly balance sheet today. Since peak-QE in April 2022, the Fed has shed $1.284 trillion. The closeup view:

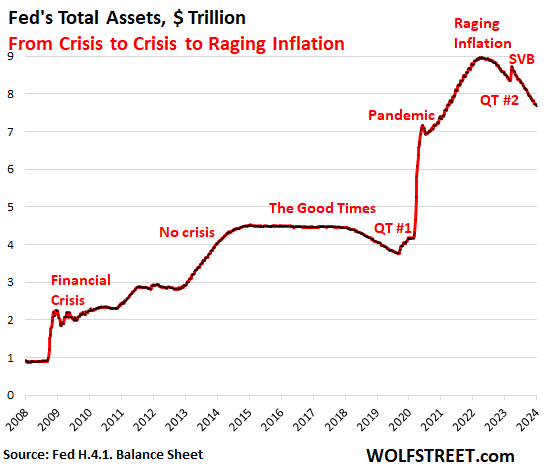

During QT #1 between November 2017 and August 2019, the Fed’s total assets dropped by $688 billion, while inflation was below or at the Fed’s target (1.8% core PCE in August 2019), and the Fed was just trying to “normalize” its balance sheet.

Now inflation is still ricocheting through services, with “core services CPI” running at an annualized rate of 5.8%, though overall inflation rates were brought down by plunging energy prices and dropping durable goods prices.

QT hums along on autopilot.

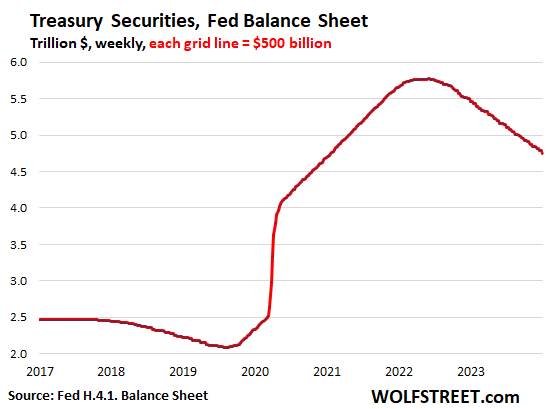

Treasury securities: -$59.5 billion in December, -$1.02 trillion from peak in June 2022, to $4.75 trillion, the lowest since January 2021.

The Fed has shed 31.1% of the $3.27 trillion in Treasury securities that it had added during its pandemic QE.

Treasury notes (2- to 10-year securities) and bonds (20- & 30-year securities) “roll off” the balance sheet mid-month and at the end of the month when they mature and the Fed gets paid face value. The roll-off is capped at $60 billion per month, and about that much has been rolling off, minus the inflation protection the Fed earns on Treasury Inflation Protected Securities (TIPS) which is added to the principal of the TIPS.

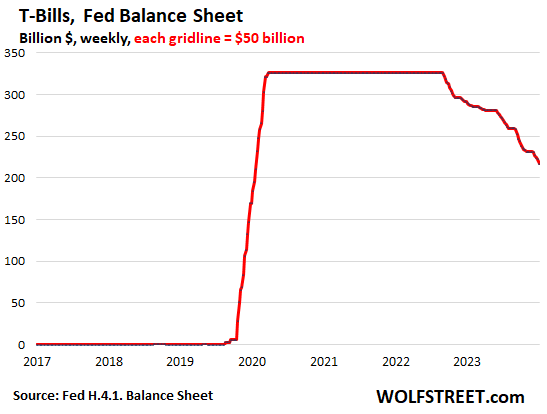

The special function of Treasury bills for the pace of QT. These short-term securities (1 month to 1 year) are included in the $4.75 trillion of Treasury securities on the Fed’s balance sheet. But they have an important function for the pace of QT.

The Fed lets them roll off (doesn’t replace them when they mature) if not enough longer-term Treasury securities mature and roll off to get to the $60-billion monthly cap. As long as the Fed has T-bills, the roll-off of Treasury securities will reach the cap of $60 billion every month.

When the Fed runs out of T-bills to fill in the gaps, the Treasury roll-off will start to fall below the $60 billion cap.

From March 2020 through the ramp-up of QT, the Fed held $326 billion in T-bills that it constantly replaced as they matured (the flat line in the chart). In September 2022, T-bills first started rolling off as needed to get the Treasury roll offs to $60 billion a month.

T-bills are now down to $217 billion, after $14 billion rolled off in December.

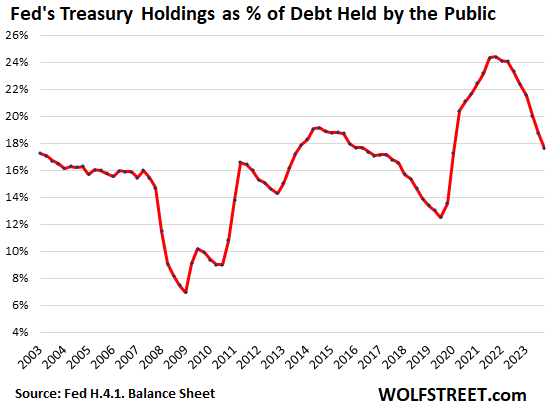

The Fed’s diminishing weight in the Treasury market: 17.6%

The incredibly ballooning US national debt, at $34 trillion, comes in two kinds of Treasury securities:

- $26.9 trillion of Treasury securities are traded and held by investors, including by the Fed. These “marketable securities” make up the Treasury bond market.

- $7.1 trillion of Treasury securities are held by entities of the US government, such as by government pension funds and the Social Security Trust Fund and are not in the bond market.

The Fed has now shed $1.02 trillion of Treasury securities, and its share of the “marketable” Treasury securities” — aka “Debt held by the public” — has fallen to 17.6%, from over 24% at the peak, as QT has reduced the Treasury securities on the Fed’s balance sheet, and as government debt ballooned (data points are quarterly).

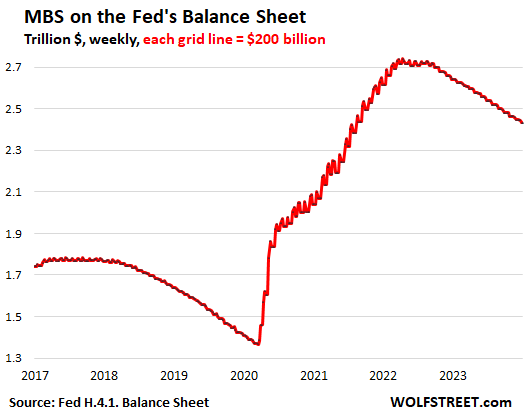

Mortgage-Backed Securities (MBS): -$15 billion in December, -$308 billion from the peak, to $2.43 trillion, the lowest since August 2021. The Fed has now shed 22% of the MBS it had added during pandemic QE.

The Fed only holds government-backed MBS, and taxpayers carry the credit risk. MBS come off the balance sheet primarily via pass-through principal payments that holders receive when mortgages are paid off (mortgaged homes are sold, mortgages are refinanced) and when mortgage payments are made.

The higher mortgage rates have caused home sales to plunge and mortgage refinancings to collapse, which slowed the mortgage payoffs, and therefore the pass-through principal payments. The MBS run-off has been between $15 billion and $21 billion a month, far below the $35-billion cap.

Banks got an arbitrage opportunity when yields dropped.

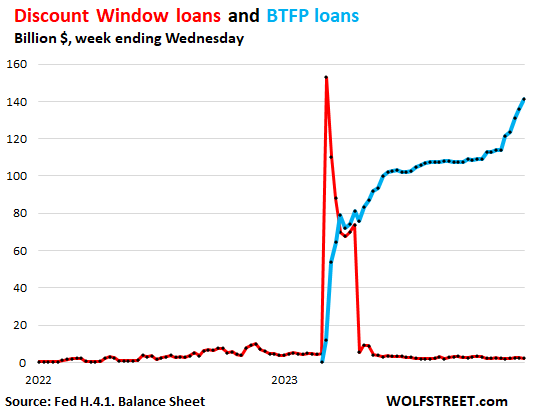

Discount Window: $2.2 billion. Roughly in this range for months, and down from $153 billion in bank-panic March (red line in the chart below). The Discount Window is the Fed’s classic liquidity supply to banks. The Fed currently charges banks 5.5%, and demands collateral at market value, and that’s expensive money for banks.

Bank Term Funding Program (BTFP): OK, now here comes the cheaper money. To borrow at the BTFP, banks have to pay the Fed a rate equal to the one-year overnight index swap rate plus 10 basis points, fixed for the term of the loan, up to one year. Back in March 2023, when the BTFP was invented, that rate worked out to be a little lower than the rate at the Discount Window, and collateral requirements were looser. So banks used it.

But starting in November, Treasury yields and related yields began to drop on rate-cut expectations. At the end of October, the 1-year Treasury yield was still at around 5.4%. The one-year overnight index swap rate was a little lower. By mid-December, the one-year yield had dropped to 4.9%, by the end of December, to 4.8%. The BTFP was charging banks around 4.85%, encouraging them to borrow at 4.85% from the Fed and deposit this cash back at the Fed in their reserve account to earn 5.4%, making them a risk-free spread of over 50 basis points.

It seems, however, that the Fed is looking askance at this trade, and only smaller banks are into it, not JP Morgan with $1 trillion.

The BTFP balance rose by $20 billion in December to $141 billion. This is the blue line in the chart below; note the surge starting in November. The BTFP is set to expire in March, so they’re trying to get in while they still can (the Discount Window is the red line):

The other bank bailout measures.

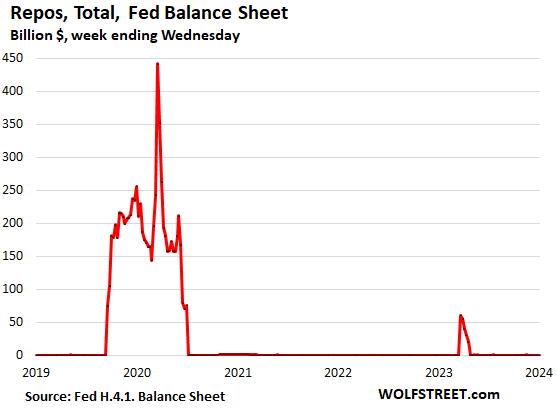

Repos: $0. Repos with “foreign official” counterparties (likely the Swiss National Bank which was backstopping the take-under of Credit Suisse by UBS) were paid off in April. The repos with US counterparties faded out in July 2020 and have remained at around zero. The Fed currently charges counterparties 5.5% on repos, as part of its five policy rates.

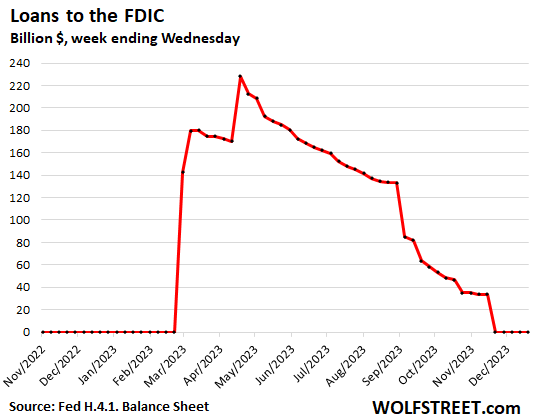

Loans to FDIC: $0. The FDIC paid off the remainder in November.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Is the reason BTFP risk free, is that the interest rate is fixed for the duration of the loan, but if the interest on reserve balances falls below the interest rate of BTFP (for example 7 rate cuts in 2024), the banks can just pay back the full amount of the loan with no prepayment penalties?

yes, if the Fed cuts its policy rates, and therefore the interest rate it pays on reserves, and it falls below or near the swap rate, the banks can just pay off the BTFP loans, and they will.

I think this is one of those unintended consequences that no one back then thought about. But it will almost guarantee that the Fed will let the BTFP expire in March (meaning no new money, but banks can hang on to the existing loans until they mature).

The arbitrage opportunity exists because the Fed’s administered rates, such as the interest it pays of reserves of 5.4%, have not changed, but the market rates have dropped.

I agree. Great analysis as well. Between the BTFP and repo/rrepo “market”, I think the Fed will have a difficult time getting the balance sheet below 7 trillion. Definitely no way they will get to the 5.5 trillion limit your analysis suggests.

Below 7 trillion some “unforeseen” event will result in more “emergency” measures…

Balanced budgets and sound money? One can dream….

They’ll be below $7 trillion by the end of 2024. There is still a HUGE amount of excess liquidity as you can see in the RRPs ($660 billion) from money market funds and $3.2 trillion in Reserves from banks. MM funds don’t need RRPs, that was an outlet to give them a place to put their excess cash. Banks need some reserves, but not $3.2 trillion. That can easily go down to $2 trillion or even lower without any kind of hiccup.

I am hearing fed might halt QT when RRP reserves drop to zero. Do we see QT ending soon?

You’re hearing ignorant BS. RRPs are NORMALLY zero, and they will go back to normal, namely zero or close to zero, no problem:

https://wolfstreet.com/2023/11/19/our-wall-street-crybabies-want-the-fed-to-stop-qt-and-they-wag-the-overnight-rrps-thatll-blow-up-the-banks-or-whatever/

I’m seeing the same, but I think it’s a lot of bull. Many of those I see pushing this narrative are Bitcoin evangelists, and most of the rest are tech bulls and RE speculators. The source of this “rumor” speaks volumes.

Let us see how QT progresses when and if the economy slows. Already some talking heads quoting some FED officials insist that QT is the next thing to be slowed or stopped citing how the overnight REPO market froze some five years ago when JP was doing baby QT and how he has to backtrack etc. No one can maker sober sailors out of drunkard sailors. The morning hangover is not an option for them :)

Your talking heads are spouting off ignorant BS and lies. No Fed official said that. RRPs are NORMALLY zero, and they will go back to normal, namely zero or close to zero, no problem.

These morons confuse reserves with RRPs. And reserves have RISEN in 2023.

https://wolfstreet.com/2023/11/19/our-wall-street-crybabies-want-the-fed-to-stop-qt-and-they-wag-the-overnight-rrps-thatll-blow-up-the-banks-or-whatever/

I’m still trying to understand the huge RRP balance that grew from essentially zero in 2020 to $2.4 trillion in 2022.

In the 11/19 article you said:

“Note how the RRP balances rose from near-$0 during the final stretches of both bouts of QE – first in late 2013 and then again in March 2021 when the financial system was creaking under excess liquidity. And now they’re heading back to this near-$0 level, which is the normal level for RRPs.”

Could you go into a little more detail on the part where you say “when the financial system was creaking under excess liquidity?”

How did excess liquidity cause the system to “creak?” I thought all that liquidity had saved (or bailed out) the system…

Thanks!

QE creates cash, and it needs to go some place, so institutional investors/banks were buying everything in sight, including T-bills, and T-bill yields started to go negative, a no-no for the Fed because it threatens money market funds that invest in T-bills with “breaking the buck,” which could again cause a panic. Too much liquidity is very bad. So the Fed started paying a little interest on RRPs and thereby provided an outlet for over $2 trillion.

It seems the more relevant figure to keep an eye on in this regard is the sum of reserves and RRP, is that fair to say, Wolf?

Really looking forward to March if the Fed let BTFP expire. That will shave off 140 billion off the balance sheet plus the 80 billion/month regular QT in Jan and Feb. 300 billion in two months will get the balance sheet down to 7.38 billion, a respectable number.

When the BTFP expires, banks can still hang on to the the existing BTFP loans until they mature. But after three rate cuts, those existing BTFP loans won’t be good deals anymore and banks will pay them off.

I see. That dashed some of my optimism. But thanks Woolf for the insight.

Wolf,

One way to interpret the BTFP chart is that roughly $80B was borrowed last March and therefore will be repaid in this coming March, quickly removing roughly half of the liquidity provided.

However, would there be any indication if banks were choosing to “reset” their one year clock now? If the banks were to repay their loans, and then turn around and immediately recycle those same securities back into BTFP, that would be a net $0 change and potentially (interest rates willing) extend their arbitrage opportunity a year beyond this March.

In other words, can we make any assumptions about when (until March 2025) the BTFP money will drain out of the system (other than when interest rates are no longer favorable to arbitrage)?

Yes, banks can repay those loans at any time and then get a new loan. So they could and likely did ratchet down their rates in November and December when rates dropped.

If the BTFP expires in March, in theory all existing loans at that time would run another 12 months. Since banks can pay off their old loans and get new loans just before the thing is set to expire, in theory, the maximum would be the March balance extended for 12 months, and then all of it would get paid off in March 2025. That would be the theoretical max.

Those loans have a fixed cost (the rate when the loan was taken out), but the earnings of that cash from the loan is not fixed.

If the Fed cuts twice, the interest rate on reserves that banks earn drops to 4.9% from 5.4% now. This would move most of those loans underwater, and the banks will likely start paying them off to get out of that arbitrage trade. With three rate cuts, the banks will rush to get out of that arbitrage trade entirely because it will be costing them. So if the Fed does 3 cuts in the second half, the BTFP arbitrage trade will end. There might still be a few banks that need the cash, so a remnant of the balance might stick around till March 2025.

So the plan is stop around 7 trillion?

There is no plan to stop at a particular point. They can go below $7 trillion. They can go a little below $6 trillion.

Assets can drop below $6 trillion, but not much further because the constraints of the liabilities, including the Treasury General Account, cash in circulation (paper dollars), and reserves. In September 2022, I calculated the floor below which the Fed cannot go; the numbers have changed, but that floor still holds. These are really important concepts:

https://wolfstreet.com/2022/09/05/by-how-much-can-the-fed-cut-its-assets-with-qt-feds-liabilities-set-a-floor/

Wolf, I understand the accounting of assets = liability (+ equity/capital), but since the Fed isn’t a normal bank and doesn’t need to attract deposits to make loans and prints out of thin air, why must they have these self-imposed accounting rules? Why can’t they accept liability (deposits from TGA and other banks) and just tell them we leave your “money” (digitally) here and they won’t be lost/stolen/bank-run’d ever since it’s backed by the money printer. Why must they have assets to match other than self-imposed accounting and then muddle into the bond market to have these assets? Even if some want to deposit their cash at the Fed in return for a bond (even if overnight) I think that should be left to regular bond markets…imo. That would allow Fed assets to go to $0 and then liabilities/deposits backed/insured by money printer (asset).

Z33-

Interesting question.

Double entry accounting seems like a sham when the Fed can conjure (or destroy) assets at will.

And no risk of insolvency…

(I inadvertently posted this further down in the comments… apologies for confusion.)

John H., I’m glad I’m not the only one. I understand the need for assets = liabilities when the Fed initiates a buy of an asset to expand money supply in the economy so they can then take that money out when they sell/mature the asset. What I’m not getting is why they need to have assets to back other liabilities (deposits) because someone else initiated a transaction to put their money there (MMF, banks, TGA). And the supposed soft limit of how low the Fed’s assets can go because of that…

I once tried to understand central bank accounting — and I have an MBA in finance and some accounting background and in 1985 did a thesis on an accounting issue (on an S&L that later blew up, LOL). Central bank accounting is different. It gives me a headache. You have to forget everything you ever learned about double-entry accounting (debits and credits). And I still don’t fully understand the basic principles. But here is what I do understand:

Central banks create and destroy money, instead of having a cash account. So there is no “cash” account on a central bank’s balance sheet. And it cannot do proper double-entry accounting (debits and credits) because the entry to the cash account doesn’t exist because the cash account doesn’t exist.

For example, if a normal bank buys $100 in securities, at the most basic level, it credits its asset account called “cash” with $100 (account goes down by $100) and debits its asset account called “securities” with $100 (account goes up by $100). Both are asset accounts, one goes down the other goes up, and overall, its assets don’t change.

If that bank borrows the $100 to later buy securities with, it credits a liability account (such as “deposits”), and it debits its asset account “cash,” and both assets and liabilities go up by $100. And to then buy the securities, it goes through the above accounting procedure. Borrowing causes a bank’s balance sheet to get bigger, not buying securities.

If the Fed buys $100 in securities, it cannot credit its cash account because it doesn’t have one. It just creates the cash. So there is no asset account that goes down. It debits its asset account “securities,” with $100, so that account goes up.

This absence of a cash account causes its assets to rise by $100 when it buys $100 in assets. Whereas a normal bank, assets overall don’t change, one goes down (cash), the other goes up (securities).

The way the Fed pays for the securities: it just credits $100 to the selling bank’s reserve account (a liability for the Fed, money that the Fed owes the bank). Crediting a liability account makes it go up. This actually creates the $100 of money. So that credit entry increases its liabilities (reserves) by $100. And its liabilities go up by $100.

This is why the Fed’s assets and liabilities both increase when it buys securities, and they decrease when it sheds securities.

This type of no-cash-account accounting is a specialty of all modern central banks, not just the Fed.

Since they create their own money, a modern central bank can never fail. But they can create a huge amount of inflation with this.

Z33-

The Fed, as currently constituted, grows in cycles, reaching new balance sheet heights, retreating some, then on to higher highs. IMHO.

You might appreciate this reminiscence from New York Fed president John Williams, comparing the methods of today’s Fed to when he started back in 1993 (Courtesy of Grant’s Interest Rate Observer, 11/24/23):

“From the perspective of monetary policy, ….1993 seems like a world away. Back then, the Fed’s balance sheet totaled about $400 billion. Now? It’s $8 trillion. So many things we take for granted weren’t even a “thing” back then. There were no FOMC statements…no press conferences…no dot plots…no long-run forecasts in the SEP [Summary Economic Projections]…no policy rule, optimal control or flexible inflation targeting. In fact, there was no inflation target at all!

There was no QE or QT, no LSAP [Large Scale Asset Purchases]…no ZLB [Zero Lower Bound], ELB [Effective Lower Bound] or shadow rates… no ample or abundant reserves… no IORB [Interest on Reserve Balances], ON RRP [Overnight Reverse Repurchase Agreement Facility] or SOFR [Secured Overnight Funding Rate]…no DSGE [Dynamic Stochastic General Equilibrium], EDO [Estimated Dynamic Optimization] or SIGMA” [a “new open economy model for policy annalysis]…no FRB/US model… and most shocking of all, no r-star.“

Progress or folly?

Might as well throw this one in, just to stir the pot (of Hayek detractors!)—

“There are definite limits to what we can expect science to achieve. This means that to entrust to science . . . . more than scientific method can achieve may have deplorable effects.

— F.A. Hayek, The Pretense of Knowledge (1974 Nobel Paper)

Z:

“There were no FOMC statements…no press conferences…no dot plots…no long-run forecasts in the SEP [Summary Economic Projections]…no policy rule, optimal control or flexible inflation targeting”

I so wish we could go back to that. Definitely folly.

Oops, meant to address above comment to John.

Yes! There’s a plan within the Fed to get down to a particular level on the balance sheet, but nobody at the Fed is going to talk about that number. We can all guess, but JPowell definitely has a target number he’d like to get down to before QE starts up again. To think otherwise is just ludicrous.

The whole point to QT is to destroy as much of this fake money as they reasonably can without causing a crisis. The $6T speculated by WR will soak up the rest of RRPs and about another $1T of the reserves banks have built up in ’23, leaving then close to the $2T figure outlined above by WR.

Remember, the great thing about QE is that it puts enormous amounts of liquidity into the market that helps the Treasury borrow massive amounts of money while QT is running. Without that liquidity, Treasury yields would zoom higher since demand for treasuries would dwindle.

Wolf

I thought BTFP was to keep the banks solvent, not line there pockets. What happened to paying it back quickly? Is this planned or unintended? The cynic in me says they don’t mind crises because they always come out on top eventually.

The BTFP is also expensive money, but not quite as expensive as the discount window, and they’ll pay that back as soon as they can, with funding from cheaper sources, such as deposits or asset sales of wherever they can get cash that’s less expensive.

I think we’re looking at unintended consequences. There are tons of smart people in finance who are trained to game the system. It didn’t take them long to figure this out.

Would announcing that the Fed will name the users of the BTFP cause a sudden repayment and end to the arbitrage?

I for one am shocked, absolutely shocked, that people in finance outsmarted the geniuses at the Fed.

“Unintended consequences” feels a bit generous to the Fed. Unless I misunderstand the arbitrage, the only requirement is an inverted yield curve in the 1 year timeframe, hardly an exotic happening in the current environment. Surely this scenario had to be obvious to the economists at the Fed when they came up with the program, and not something only divined by those wily Wall Street types?

“the only requirement is an inverted yield curve in the 1 year timeframe,”

That’s not the requirement. The requirement is that the overnight one-year index swap rate + 10 basis points is significantly below the rate the Fed pays on reserves (5.4%). That was not the case until November/December.

I don’t have access to the swap rates data to make charts with. But here is a stand-in that shows the principle. The chart shows the 1-year Treasury yield (which is a little higher than the one-year index swap rate) and the EFFR (5.33%) which is just a hair lower than the interest rate on reserves (5.40%). So this is not exact, but it shows the principle.

You can see when the arbitrage became profitable: when the red line (cost of funds) fell below the green line (income on funds), which happened in early November:

The BTFP loan balances went up about $32 billion or so since October, so a 0.5% spread between BTFP and one year yield would only be about $160 million yearly interest earnings arbitraged. Whittle that down to a 2-3 month timeframe From Oct-Nov to the present day, and the smaller banks have apparently gained only $40 million from this play so far.

This amount will certainly go higher heading into March expiry, but it seems pretty insignificant and might even be a small relief for banks saddled with a troubled CRE portfolios?

Thanks Wolf!

What do you think about the narrative that once reverse repo goes to zero, the credit conditions will get much tighter because banks would not have enough reserves? Can this cause problems for the banks?

The narrative is ignorant BS. RRPs are NORMALLY zero, and they will go back to normal, namely zero or close to zero, no problem:

https://wolfstreet.com/2023/11/19/our-wall-street-crybabies-want-the-fed-to-stop-qt-and-they-wag-the-overnight-rrps-thatll-blow-up-the-banks-or-whatever/

When the Fed offered BTFP the inflation rate was 9%.

In Oct 2008, when the Fed raided bank accounts for the first time, gov

debt was 10T. When the Fed started hiking in Mar 2022 gov debt was 30T.

For 13 years the gov paid negative rates, hollowing people’s money :

[10T + 30T/2 x 13 Y + (-)0.02 = (-) 5T.

RRP rate is 5.3%. RRP will not go to zero. RRP is Fed debt to the banks.

Fed balance sheet = Fed assets minus RRP. RRP deflated from 2.5T

to 1.086T. NO QT.

Add the gov Anti inflation act : 6T ==> QE.

1. “RRP will not go to zero.”

Nonsense.

2. “RRP is Fed debt to the banks.”

ignorant BS. 90%+ RRPs are the Fed’s debt to MONEY MARKETS. The rest is the Fed’s debt to GSEs, FHLBs, etc.

3. “Fed balance sheet = Fed assets minus RRP”

What kind of bullshit is this?

4. “RRP deflated from 2.5T to 1.086T.”

You’re behind, they’re already at $664 billion on their way to zero.

5. “NO QT.”

Stupid BS.

6. “Add the gov Anti inflation act : 6T ==> QE.”

More bullshit. nothing to do with QE, that’s an increase in the debt, and it provides inflationary pressures. The Fed has zero to do with it.

Where do you go to pollute your brain with this idiotic toxic BS?

Contrary to the FED, MMMFs are nonbanks. The accounting is different for banks.

Wow! The scoreboard reads

Wolf 100

ME 0

Somebody get the fire extinguisher! my monitor just caught fire.

Wolf,

Trying to understand the Math for my own understanding.

$59.5 billion Treasury Securities matured + $15 billion of MBS pass thorough payments. So FED Balance should have dropped $74.5 billion.

But BTFP $20 billion increase will make balance go higher.

So NET balance should be dropped by $54.5 billion. But at the top Article says $56 billion. Whats missing in my calculation?

Lots of other minor stuff changing on a balance sheet. I just cover the biggies. “Unamortized premiums” is one of those things I no longer show charts for because it’s always the same decline of about $2.5 to $3 billion a month, and the explanation is technical and not worth it. In December it was -$2.6 billion.

Thanks Wolf. Appreciate it for educating us on those misc details.

Thanks Wolf

Unintended consequences with BTFP. When btfp is over in March and services inflation is at 5.8% annually, could we see the one year drift back to where it was? I would think so with no rate cuts.

Indeed, funny how those “emergency measures” never really go away, especially when they make a relative few people, very, very wealthy…

same as it ever was.

BS. The BTFP is the only emergency measure left from the March 2023 bank crisis. All others went away already, see charts above. The BTFP will expire in March, and existing loans will mature and be paid off over the following 12 months, and then it’s gone.

During the pandemic, the Fed had a whole bunch of emergency measures, repos, the whole alphabet soup of SPVs, and all of them went away. It sold its corporate bonds and bond ETFs, and got rid of the TALF and all the other alphabet soup stuff. What’s left are Treasuries and MBS, and it’s shedding them now too.

Such the optimist. NO WAY the Fed’s Balance sheet gets “below 7 trillion by the end of 2024″…

Disclaimer: not without some “unforeseen” event requiring “emergency measures” being. YES, there is still plenty of liquidity, HOWEVER, Uncle SAM is going to run a 3+ trillion dollar deficit this year, and at higher interest. (yield solves all demand problems right?)

The 10-year yield at 4% shows that there is HUGE demand for Treasury debt. It should be 5%-6%.

Inflation in Europe is rising again.

From 2.4 to 2.9 percent.

I never doubted your prophecies Wolf!

“What’s left are Treasuries and MBS, and it’s shedding them now too”

And good luck with that, because, despite the available liquidity in the U.S. banking system (which you have covered extensively), global liquidity is a problem AND Uncle Sam has a boatload of new debt to issue at much higher rates! As you always say, “yield solves the demand problem”!!! Interest payments are going to be sucking up more than a trillion AND the government is already on track to deficit spend north of 3 trillion!

Right! We’ll have to wait and see if the “real market” picks up the proliferation of new treasury debt while the the Fed is reducing their holdings by not rolling them over.

MW: 10-year Treasury yield falls below 4% after weaker-than-expected ISM data outweighs hot U.S. jobs report

Yes, that was funny. The 10-year yield jumped from 4.03% to 4.08% on the jobs report, and then on the ISM services PMI, it fell to 3.95%, and then it bounced right back to 4.05%. It’s like whatever.

Is it even feasible to believe 10 years @ 6% in 2024 or did I miss the boat at 5%? I do not think inflation will be tamed in services or rents near term. T-bills and good relational MMA rates at small banks.

I am a patient man, but 3 bank managers recently told me that their folks are saying cuts by June, trying to push me into CDs, while they get to feast on the spread. One even quoted freaking Powell about rate cuts. I corrected him about iff inflation is tamed. He didn’t like that and challenged me that we should have a bet. I said like a dick, “Yeah, you win. I will just pull out my money from your bank”. Laughs all around, but deadly like snake bite.

Everybody is on edge. Thanks for your insight.

Much depends on inflation. If inflation goes back up, rather than heading straight to 2%, all this longer-term stuff will get repriced. If 4-6% CPI inflation looks like the future, the 10-year yield will move higher. If 2-3% inflation looks like the future, the 10-year yield may stay in this 4% range.

The Fed cuts its short-term rates to 4% this year and next year, then the yield curve uninverts with the 10-year going above 5%. And then the yield curve would be back to normal-ish.

Long-term yields are impacted by QT or QE much more than by short-term rates. The Fed is doing QT, so overall, longer-term rates are going to be higher. Sure, they’re volatile, they jump up and down a lot. Only if the Fed restarts QE will long-term rates go south seriously.

“If 4-6% CPI inflation looks like the future, the 10-year yield will move higher. If 2-3% inflation looks like the future, the 10-year yield may stay in this 4% range.”

I know you’re not recommending it as such, but that sounds almost like the elusive asymetric paired-trade opportunity!

This may be the futures traders making money on the spreads.

Great coverage, once again. I can tell by your replies to comments that you care about correcting the public narrative about this topic. You’re doing your part!

Hooray for continued QT. Happy to see the 10 year treasury FINALLY broke back above 4% today.

LOL! The 10 year was at 4.9% in October! Are you lending money to uncle sugar for ten years at anything less than the real inflation rate?

Good luck with that!

I’m not personally. I’m only buying bills and agency debt right now. My average yield is ~5.4%.

Good observation. The real inflation rate is the 2% formal floor plus all inflation overages during times of crisis. Unfortunately, with debt levels this high, just about any little hiccup qualifies as a crisis “requiring” money printing, interest rate repression, or other artificial support.

I wouldn’t touch a long bond paying less than 5%. Even at that rate, I would only dabble.

There is major systematic risk today that the Fed will try and control with all tools at its disposal, plus new tools it will invent.

Today I paid almost exactly par for some FFCB paper with a 5.98% coupon.

Real, positive yields are out there – you just have to know where to look. There’s more to the world of bonds than treasuries.

Z33-

Interesting question.

Double entry accounting seems like a sham when the Fed can conjure (or destroy) assets at will.

And no risk of insolvency…

Because of the large losses that the Fed has incurred in the last 12 months or so, one items that has changed quit a lot lately is Liabilities and Accrued Dividends. Although it currently sits on the liability side of the Fed’s balance sheet, it does so with a negative balance sheet (as a contra liability I suppose). Looks like this item will continue to grow until the Fed lowers it’s policy rates by at least 1 to 1.5%. It’s over -$100B in this release.

Just to shed a little extra light on this corner. It’s actually set up as a negative payable to the US Treasury department, when there used to be a positive payable when the Fed was still making money. The Fed remits its profits to the Treasury department, and the future remittances were carried in that payables account. Since it’s losing money, it no longer remits anything to the Treasury, and its losses go into the payables account where they’re accumulating. When the Fed starts making profits again, those profits will go against the negative amount in the payables account until it turns positive again, at which point the Fed will start remitting its profits again. As you suggested, this will take years. But it doesn’t impact its assets.

We will see what happens to interest rates when the Reverse Repo account is depleted in a few months.

RRPs don’t matter. They’re normally zero. See my 3 RRP charts in the comments above. It’s excess cash that money market funds had, and they these the RRPs to earn some interest on, and that they’re now shifting to T-bills and private repos that pay a little more. The Fed’s minutes explained that.

The thing you need to watch are reserves — that’s bank cash. But they have risen in 2023, and are just now dipping a little, and are very high, at $3.2 trillion. The problem the repo market ran into in 2019 was that reserves had dropped to $1.4 trillion, and banks stopped lending to the repo market. We’re $1.8 trillion in reserves above that. So there’s ways to go.

In the minutes, the Fed touched on the topic of reserves – it wants to be “somewhat above” what it considers “ample reserves.” In early 2020, when it formed that concept, “ample reserves” was about $1.5 to $1.6 trillion. Now reserves are at $3.2 trillion.

So you are saying the Fed does not use RRP to purchase Treasuries at auctions?

They’re completely unrelated.

The Fed pays for its securities purchases at auction by crediting the amount directly to the government’s checking account at the Fed, the TGA account.

How much of the portfolio of Treasury securities is available for use in RRP operations?

The FOMC directed the Desk to undertake overnight RRP (ON RRP) operations in amounts limited only by the value of Treasury securities held outright in the SOMA that are available for such operations.

I assume your quote from the FOMC’s Implementation Notes is related to your above question — “So you are saying the Fed does not use RRP to purchase Treasuries at auctions?”

Are you saying that this quote says that the Fed uses “RRPS to purchase Treasuries at auctions”? If that’s what you’re saying, you have no idea what you’re looking at, and you have no idea what RRPs even are.

1. ON RRPs are repos where the Fed posts collateral to borrow cash from counterparties. Read that sentence over and over again until you understand what it means.

2. RRPs have nothing to do with Treasury auctions. RRPs are repos conducted between the New York Fed and its counterparties in the morning of EVERY BUSINESS DAY.

3. The Federal government (Treasury Dept.) has zero to do with RRPs, is not involved, and there is no auction.

4. The COLLATERAL that the Fed posts as part of the RRPs are its Treasury securities that it already purchased during QE years ago and holds in its System Open Market Account (SOMA) at the New York Fed. This is the account that holds all the Fed’s Treasuries and MBS that are on the Fed’s balance sheet that I report here. There are $7.07 trillion as of this morning in the SOMA account.

I’m hoping short rates go back up a bit once the RRP isn’t competing with bills. I miss seeing the 26 week bill @ 5.6%.

Disregard the above comment…it was meant to be a response to Z33 above.

I still do not see enough mea culpas from the Fed and the insane risks they took from March 2020 to

Early 2022. They can’t keep taking crazy risks

Regarding the MBS rolloff, could it naturally start to accelerate over the next few years? I know that refi’s have pretty much stopped, but the Fed is no longer buying any new loans, so the average age of the mortgages in its portfolio is probably increasing (assuming there aren’t a bunch of older vintage loans maturing right now). The older a mortgage is, the more of its monthly payment is dedicated to principal repayment vs interest payment.

I wonder if anyone has modeled the Fed’s MBS portfolio to see if this effect might start accelerating the principal repayments even in the absence of refinancing activity?

If home sales pick and go back to normal, the MBS roll-off will accelerate a lot. And it will accelerate further and hit the cap if the Fed cuts rates by as much as markets expect because that will trigger refis. Right now the mortgage market is frozen.